Embed Size (px)

Citation preview

Competing in the Digital Now:Competing in the Digital Now: Winning in the New Digital Era

Bob Black, Senior Advisor to BCG and former Group President Kimberly Clark & Annie's Board of DirectorsDan Cooke, General Manager, Global eCommerce, Kellogg Company

CONFIDENTIAL MATERIAL

August 15, 2015Gabrielle Novacek, Partner, Boston Consulting Group

GMA Steering Committee members

Rick Brindle Dan Cooke Evan Fernando Keith Aldredge David Wurmg

Sarah Wagoner Eric Ong Tim Madigan James Splinter Jeff Malat

1

Steve Savell Sara Mirelez Nigel Burton Gian-Carlo Peressutti Scott Cameron

CPG companies face a '1-5-10' market over next few yearsy

with multiple PENETRATIONWe are living in a HYBRID WORLD...

5%

10%

... with multiple PENETRATION LEVELS by market/category/ segment ...

1+% ... that will ACCELERATE at1 %an unknown pace

2Note: From BCG-GMA "The Digital Future: A Game Plan for Consumer Packaged Goods" (2014)

Potential market evolution

750

US grocery sales ($B)Online Offline

Contribution to Growth

36

725

700

+2%

718

28

Contribution to Growth

~50%

8

36700

675

52

666 24

+

8

0

3

2018E2013

Note: From BCG-GMA "The Digital Future: A Game Plan for Consumer Packaged Goods" (2014)Source: IRI Database L52 ending May 2014, Wells Fargo analyst report on online grocery, BCG analysis

Brick & mortar shelf Website shelf Mobile shelf

4Source: Store visit (Target), Amazon website and mobile app (accessed August 4, 2015)

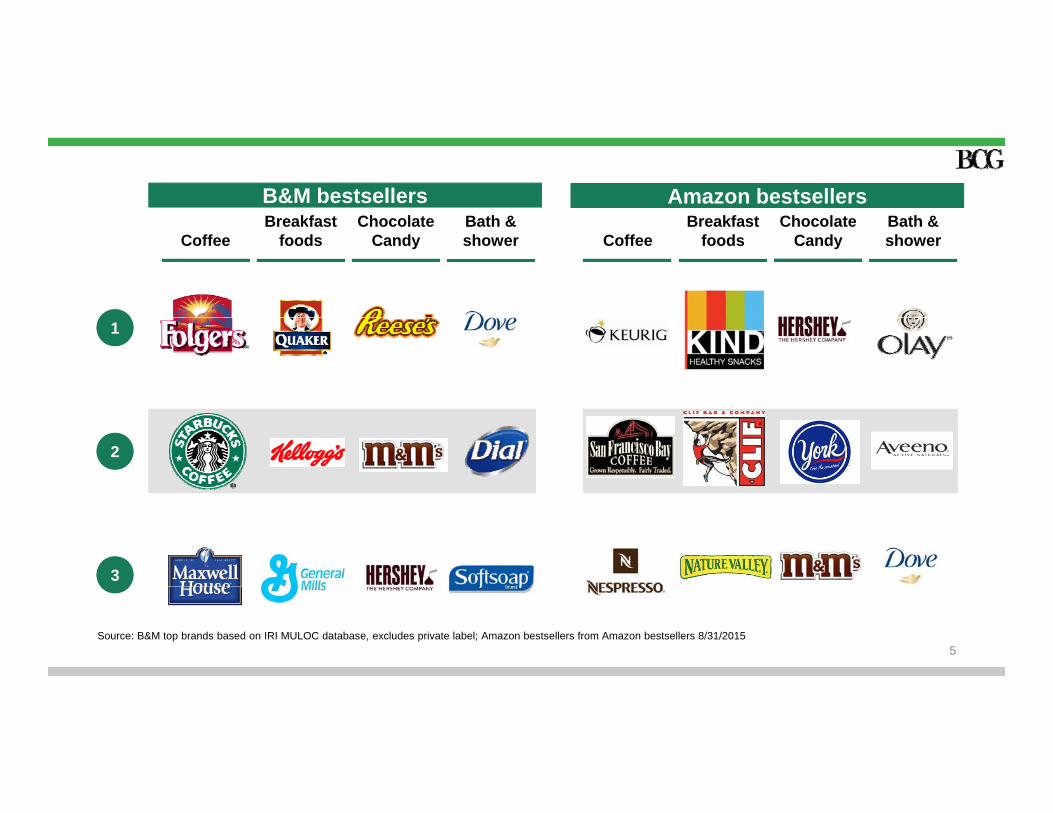

Breakfast Chocolate Bath & Breakfast Chocolate Bath & B&M bestsellers Amazon bestsellers

Coffee foods Candy shower Coffee foods Candy shower

1

2

3

5Source: B&M top brands based on IRI MULOC database, excludes private label; Amazon bestsellers from Amazon bestsellers 8/31/2015

FairFair shareshare

6

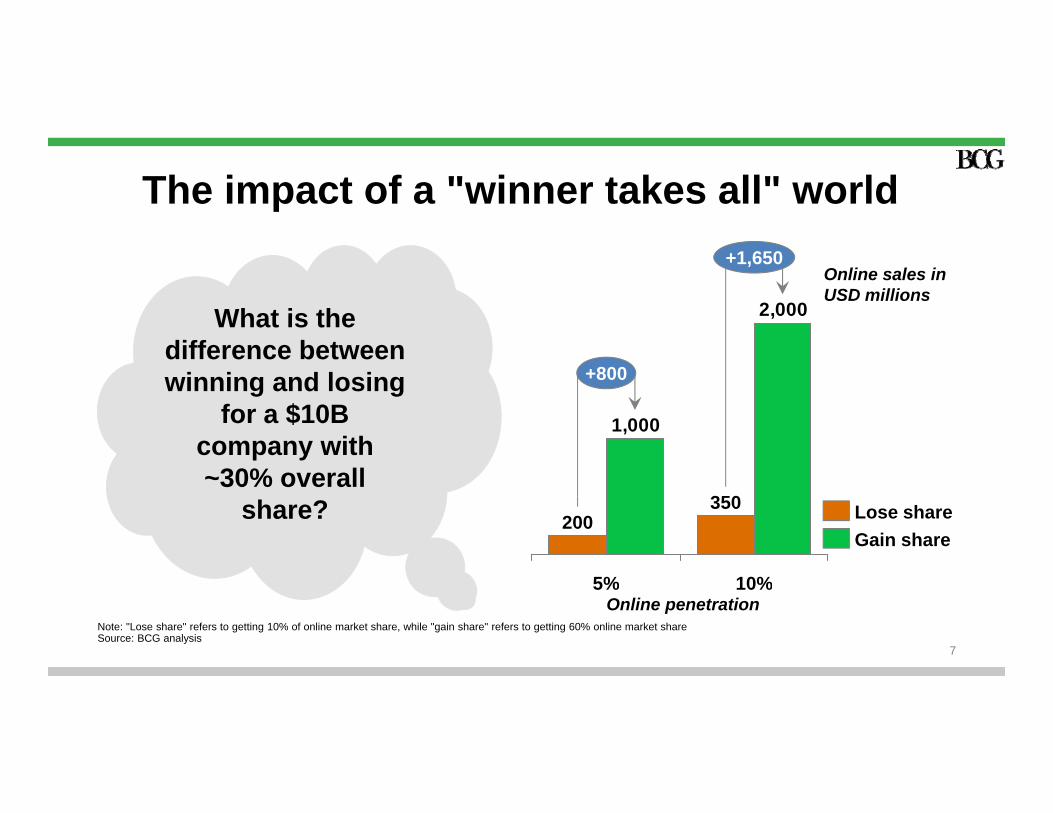

The impact of a "winner takes all" world

What is the 2,000

+1,650Online sales in USD millions

What is the difference between winning and losing

f $10B

,

+800

for a $10B company with ~30% overall

1,000

350share?

10%

350

5%

200 Lose shareGain share

7

Note: "Lose share" refers to getting 10% of online market share, while "gain share" refers to getting 60% online market shareSource: BCG analysis

10%5%Online penetration

8

Click & Collect in France

4,000

No. of C&C locations in France

Aggressive

Maturity

2,7213,000>3,000

Entrance of others

ggrollout

1,890

1 000

2,000

First mover

2nd entrant

750

0

1,000 First mover

9

201020082009 20142013201220112001 200520032000 2002 20062004 2007

Source: Leclerc website, Nielsen Research, BCG analysis

Pilots C&CPilots C&C Pilots C&C

2009 2010

Pilots C&C

Pilots C&C Announces plans for 1.2K C&C stores

Tests CurbsidePickup

Starts C&C atall stores

Opens storePlanning C&C in Pilots C&C Pilots C&CPilots C&C Pilots C&CExpands

10

pick-upSilicon Valley with Instacartin AKin AZ/AL in OHC&C in OH

Source: Press search

Picking options Collection optionsPicking options Collection options

11

Key actions to win in Click & Collect

1. Position yourself as a critical source of C&C knowledge and expertise for retailers

– Dedicate a cross-functional team

– "Go to school" on iterations in Europe – beyond your own categories

– Actively engage and lead in pilots across multiple retailers – your categories

2. Set standards for product content, shopping list optimization, and fundamentals

3 Aggressively experiment and innovate for unique consumer and logistical aspects of your3. Aggressively experiment and innovate for unique consumer and logistical aspects of your

categories, e.g.,

– Lane and locker sampling programs, e.g., small pack, impulse

12

– Unique point of pick-up promotional strategies, e.g, bulky, fresh, and impulse

– Shopping list population, basket auto repeats

13

Maximize total Support Amazon's goal to get greater share of household contribution dollars spending through optimal prices, selection and convenience

Master operational basics and become

top partner

Supply chain PackagingA+ product content

Strategic Vendor Services

14

Strategic Vendor Services SEO Vine program

SVS enables a more strategic, beneficial relationship with Amazon

Amazon not conducive for personalized account management

SVS provides opportunities to sell more strategically

Amazon culture - biased to minimize human contact

Dependence on algorithm limits need for

CPG companies can fund a single point of contact through SVS• Ensures success of promotional efforts,

helps address challengesDependence on algorithm limits need for suppliers relationships

No single point of contact for most vendors – scale not correlated with bargaining

helps address challenges• Provides an interpretive lens to

performance

But... SVS comes at cost and does notscale not correlated with bargaining power

But... SVS comes at cost and does not solve all Amazon challenges

15Source: Expert interviews, 3rd party data vendors, and GMA members, online research, BCG analysis

Developing A+ product content Optimizing for search

old

Min. 6 high quality images Direct link to

other SKUs

Brand name in title

p g p p g

Amazon ranks search results by: 1. Relevance2. Product sales performance

Abo

ve fo

Optimize keywords on a regular basis to achieve page 1 ranking

• Monitor related keywords that are

Expanded product description

Interactive/ inspirational contentd

Monitor related keywords that are popular/trending

• Infuse these keywords in product descriptions and page HTMLp

Bel

ow fo

ld

16

B

Digital marketing spend outpacing traditional media

CPG digital marketing spend reaching ~25% of media spend

Kraft Foods Group

CPG digital spending survey estimatesAd Age 2014

Kraft Foods Group

Clorox Co.

McCormick & Co.

Proctor & Gamble Co.

Unilver

Heineken USA

Mondelez International

0 10 20 30 40

General Mills

Campbell Soup Co.

17

% digital share of media mix

Source: BCG Digital Marketing COE; Advertising Age, eMarketer, Jeffries

C Fan sentimentHigh

Blogs

ForumsReviews

D Consumer engagement

Level of interaction

Blogs Social Media

E Controlled experience

A Digital shelf space

e-mail marketingO li d

MobileB Targeted impressions

Retail com

A Digital shelf space

Search engineti i ti

L l f t lL Hi h

marketingOnline adsRetail.com optimizationLow

18

Level of controlLow High

Source: BCG analysis

Driving brand onlineDriving sales online

Digital coupons

19

No "Fair" Share. Make your move – laggard, winner or disruptor?

Laggards Dabblers Winners Disruptors

Most traditional retailers and

consumer products companies

• Do nothing or are very late to react

• Very conservative investment stance playing catch-up

• Elevate consumer experience • Transformed consumer expectationsreact

• Don't capitalize on trend for fear of cannibalizing existing product sales

stance, playing catch-up

• Face flat or stagnating sales• Aggressive digital bets,

experiment heavily, move fast

expectations

• Disrupting the value chain

• Move from manufacturer to consumer company

ree

of

ange

20

Deg

rch

a

Source: BCG analysis

BE BOLDnot stupidnot stupid

21

Key Actions to Win

– Commit to action - today– Set bold objectives – winners not laggardsAlign as a

leadership team j gg– Invest ahead of volume - risk of inaction is too high

– Immerse as consumers – go on a digital diet

leadership team

Immerse as consumers go on a digital diet– Follow consumers 24/7- understand evolving behaviors– Make digital a core focus – discuss Walmart AND Walmart.com

Engage as a leadership team

– Identify key places to win – where and with who– Reallocate resources – prioritize across key levers– Integrate across functions - eliminate silos that are barriers

Focus as an organization

22

– Accelerate talent and capabilities – new needs for a new market

Contact information

Leslie Hinchcliffe (for publication details)[email protected]@ g

Gabrielle [email protected]

Dan CookeD i l C k @k ll

23