Embed Size (px)

DESCRIPTION

project is made in 2014 with a experience of internship in IDBI fedral life insurance pvt. ltd

Citation preview

CHAPTER 1-PROFILE

1

1.1 INTRODUCTION

IDBI Federal Life Insurance Co Ltd, is a joint venture between three leading

financial conglomerates – India’s premier development and commercial bank, IDBI,

India’s leading private sector bank, Federal Bank and Europe’s premier Bank

assurer, Ageas, each of which enjoys a significant status in their respective business

segments. In this venture, IDBI owns 48% equity while Federal Bank and Fortis

own 26% equity each.

Let us have a brief look over these three companies:

1.1.1 IDBI Bank Limited

Development Banking emerged after the Second World War and the Great

Depression in 1930s. The demand for reconstruction funds for the affected nations

compelled in setting up of national institutions for reconstruction. At the time of

Independence in 1947, India had a fairly developed banking system. The adoption of

bank dominated financial development strategy was aimed at meeting the sectoral

credit needs, particularly of agriculture and industry. Specialized development

financial institutions (DFIs) such as the IDBI, NABARD, NHB and SIDBI, etc.,

with majority ownership of the Reserve Bank were set up to meet the long-term

financing requirements of industry and agriculture.

The Industrial Development Bank of India (IDBI) was established in 1964 under an

Act of Parliament as a wholly owned subsidiary of the Reserve Bank of India. In

1976, the ownership of IDBI was transferred to the Government of India and it was

made the principal financial institution for , promoting and developing industry in

2

India. But after the public issue of IDBI in July 1995, the Government shareholding

in the Bank came down from 100% to 75%.

IDBI, formally entered the portals of banking business as IDBI Ltd. from 1 October 2004. In

2006, IDBI Bank acquired United Western Bank in a rescue. By acquiring UWB, IDBI Bank

more than doubled the number of its branches from 195 to 425.

1.1.2 Federal Bank

Federal Bank Limited is a major Indian commercial bank in the private sector,

headquartered at Aluva, Kochi, Kerala. It is the fourth largest bank in India in terms

of capital base. As of 2 June 2014, Federal Bank has 1174 branches spread across 24

states and 1371 ATMs across the country. Its balance-sheet stood at Rs 1.03 trillion

as of end March 2014 and its net profit stood at Rs 839 crore for the full fiscal .

In 1931, Travancore Federal Bank began operations at Pattamukkil Varattisseril

house near Nedumpuram, near Thiruvalla, Kerala. The home functioned as the bank

office for nearly 15 years. A lawyer from Perumbavoor named K.P.Hormis, and his

acquaintances, bought the bank and took over the management. In 1945 they moved

the bank's registered office to Aluva and Hormis became the Managing Director. In

1947, the bank's name was shortened from Travancore Federal Bank to Federal

Bank.

Between 1963 and 1970, Federal Bank took over Chalakudy Public Bank, Cochin

Union Bank (1963) in Trichur, Alleppey Bank (1964) in Alappuzha, St. George

Union Bank (1965) in Puthenpally, and Marthandam Commercial Bank (1968)

in Thiruvananthapuram. In 1970, it became a scheduled commercial bank and came

out with itsinitial public offering in 1994.

3

In January 2008 Federal Bank opened its first overseas representative office in Abu

Dhabi.

In August 2013 Federal Bank introduced FedBook, the first electronic passbook

launched by any bank in India. FedBook is a mobile app through which customers

can view their passbook details.

1.1.3 AGEAS

Ageas Insurance Company (Asia) Limited is an insurance company based

in Hong Kong. It was acquired by Fortis, the Belgium and Netherlands based public

finance group in 2007

Prior to then the company was called Pacific Century Insurance Holdings Limited

and was controlled by Pacific Century Regional Developments Limited.

Ageas Insurance Company (Asia) Limited ("Ageas") ranks one of the largest life

insurance companies in Hong Kong. it offers the Hong Kong market a diversity of

financial protection products and wealth management services. Ageas is an

international insurance group with a heritage spanning 190 years. Ranked among

the top 20 insurance companies in Europe

Ageas operates successful partnerships in Belgium, the UK, Luxembourg, Italy,

Portugal, Turkey, China, Malaysia, India and Thailand and has subsidiaries in

France, Hong Kong and the UK. Ageas is the market leader in Belgium for

individual life and employee benefits, as well as a leading non-life player through

AG Insurance. In the UK, Ageas is the second largest Motor insurer and has a

4

strong presence in the growing over 50’s market. and has annual inflows of more

than EUR 23 billion.

The literal meaning of AGEAS is:

AG - reflects roots-the creation of AG Leven in 1824

EA - two key markets-Europe and Asia

AS - Assurance, our single minded focus on our core insurance business

Having started in March 2008, in just five months of inception, IDBI Federal became one of the

fastest growing new insurance companies by garnering Rs.100 Cr in premiums. The company

offers its services through a vast nationwide network 2,308 partner bank branches of IDBI Bank

and Federal Bank in addition to a sizeable network of advisors and partners. As on 31st

December 2013, the company has issued nearly 5.5 lakh policies with a sum assured of over Rs.

32,110.48 crores.

1.2 Company’s vision:

To be the leading provider of wealth management, protection and retirement solutions that

meets the needs of our customers and adds value to their lives.

1.3 Company’s mission:

To continually strive to enhance customer experience through innovative product

offerings, dedicated relationship management and superior service delivery while

striving to interact with our customers in the most convenient and cost effective

manner.

To be transparent in the way we deal with our customers and to act with integrity.

5

To invest in and build quality human capital in order to achieve our mission.

To deliver world-class wealth management, protection and retirement solutions that

provides value and convenience to the Indian customer.

1.4 Companies values and believes:

Transparency: Crystal Clear communication to our partners and stakeholders

Value to Customers: A product and service offering in which customers perceive value

Rock Solid and Delivery on Promise: This translates into being financially strong,

operationally robust and having clarity in claims

Customer-friendly: Advice and support in working with customers and partners

Profit to Stakeholders: Balance the interests of customers, partners, employees,

shareholders and the community at large

1.5 Company Information

Full name: IDBI Federal Life Insurance Co Ltd.

Legal Address: 1st Floor, Trade view Building, Oasis Complex, Kamala City, Pandurang

Budhkar Marg, Lower Parel ( W ); Mumbai; Maharashtra; 400013 14

Legal Form: Other non-liability limited

Type Joint Venture

Industry Life insurance

Founded March 2008

Headquarters Headquaters in Mumbai India

6

1.6 Key peoples:

Board of directors:

Mr. R. M. Malla (Non-Executive Director)

Mr. Suresh Kumar (Non-Executive Director)

Mr. Bart De Smet (Non-Executive Director)

Mr. R. K. Bansal (Non-Executive Director)

Mr. Filip A. L. Coremans (Non-Executive Director)

Mr. S. Santhanakrishnan (Independent (Non-Executive) Director)

Mr. R. K. Thapliyal (Independent (Non-Executive) Director)

Mr. Davinder Rajpal (Independent (Non-Executive) Director)

Senior management committee:

Mr. Ajay Oberoi (Chief People Officer & Head – Administration)

Mr. Ashley Kennedy (National Head – Agency & Alliances)

Mr. Aneesh Khanna (Head – Marketing & Product Management)

Mr. Aneesh Srivastava (Chief Investment Officer)

Mr. Rajesh Ajgaonkar (Head – Legal, Compliance &Company Secretary)

Mr. Vignesh Shahane (CEO & Whole – Time Director)

Mr. George John (Corporate Controller)

7

1.7 Products

1.7.1 Childsurance

IDBI Federal Childsurance Savings Protection Plan is a endowment plan that

ensures your child’s future financial needs are fulfilled. Childsurance Savings, is

designed to give you guaranteed annual payouts and aid the important milestones in

your child’s life. What’s more, in the unfortunate event of you not being around, the

policy will continue exactly as you had planned it, without any further premiums

being paid. .In other words, this plan ensures that your child gets to live his/her

dream exactly as you have planned, whether or not you are around.

8

Figure 1. 1 childsurence

1.7.2 Group Microsurance Plan

The IDBI Federal Group Microsurance Plan provides affordable life insurance

cover to groupsThe plan is extremely useful to Micro Finance Institutions, Self

Help Groups and NGOs to insure the lives of their group members and thus provide

security to the group members’ families. The plan can also be used for providing

loan protection to the group members’ families

1.7.3 Incomesurence

DBI Federal Incomesuranc Guaranteed Money Back Insurance Plan is a non-

linked non-participating money back plan which gives you guaranteed* returns on

9

Figure 1. 2 Group Microsurance Plan

Figure 1. 3 Incomesurence

your investment, so that you stop worrying about the future. With Incomesurance,

you can guarantee a secure future for your family even when you are not around.

1.7.4 Lifesurence

IDBI Federal Lifesurance® Savings Insurance Plan (UIN:135N029V01) is a

fixed term non-linked participating plan that provides you the twin benefits of

long-term savings and life cover. With Lifesurance Savings, your small savings

will help you realise the big dreams that you have for yourself and your family.

This plan also offers you the benefit of life cover that will provide financial

security to your family in your absence.

10

Figure 1. 4 Lifesurence

1.7.5 Loansurance Group Insurance Plan

IDBI Federal Loansurance® Group Insurance Plan, hereafter referred to as

Loansurance®, is a group credit protection plan that helps protect your borrower’s

assets and savings. Through Loansurance® you extend peace of mind to your

clients, ensuring that their debt does not become a burden on their family in their

absence. In return, you are also protected from the risk of non-payment of the loan

dueatoadeathaofatheaborrower.

Loansurance® allows you to cover the persons who are directly liable for loan

repayment (and the partners, in case of a partnership) be it a loan taken by

individuals or by business. Thus, even a business entity will be protected against

loan default in case of death of the persons who are responsible for loan repayment.

Furthermore, with this product, you gain competitive edge while attracting new

customersdanddretainingdthedexistingdones..

11

Figure 1. 5 Loansurance Group Insurance Plan

1.7.6 Termsurance

IDBI Federal Termsurance Group Insurance Plan is a pure group term plan

designed to cater to a wide variety of formal and informal groups such as the

employer-employee groups/bank-depositor groups/ customer-supplier

groups/professionals/affinity groups. It is a Group Term Insurance plan that

provides basic life insurance protection to the members of the plan.

1.7.7 Wealthsurance

12

Figure 1. 6 Termsurance

IDBI Federal Wealthsurance® Suvidha Growth Insurance Plan (UIN:

135L033V01) is a simple unit linked plan that helps you take your first step towards

wealth creation and that too, with ease. What’s more, the life cover with this plan

provides financial protection to your loved ones.

1.7.8 Retiresurance

IDBI Federal Retiresurance Group Insurance Plan is a non-linked non-participating

variable insurance plan, designed for employer-employee groups only. It enables

employers with more than 10 employees to outsource the management of their

13

Figure 1. 7 Wealthsurance

Figure 1. 8 Retiresurance

employee’s gratuity, superannuation and leave encashment funds. It also provides

basic life insurance protection to the members of the plan.

1.8 Size of firm

It is this commitment that has helped us achieve break-even in just the 5 year of

operation and declare a maiden profit of ` 9.24 crore. We offer our services through a

nationwide network of 2,186 bank branches of IDBI Bank and Federal Bank in addition to

a sizeable network of our advisors. As on 31 March, 2013, IDBI Federal Life Insurance

issued over 5 lakh policies with a sum assured of more than ` 28,500 crore.

Moreover, IDBI Federal life insurance is a fast growing insurance company as achieving a

break-even in just 5 years is a great achievement for a insurance company. It also raised

100crores in just 6 mounts, and that’s something highlighting.

After declaring the maiden profit of RS.9.2 crores (approx.) (as on 31st march 2013), it took

a huge jump in reference to profits and declared 80 crores (8.6 times profit of the last year,

i.e., 2013), in 2014 as profit.

1.9 Market Share Of The Firm

14

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

100.00

63.47

5.885.66 4.4

3.142.73

2.46 2.31.27

1.271.05 1.02

0.990.99

0.5800000000000010.530.42

0.410.41

0.3900000000000010.3300000000000020.20.0900000000000001

Figure 1. 9 market share of the idbi Federal life insurance

15

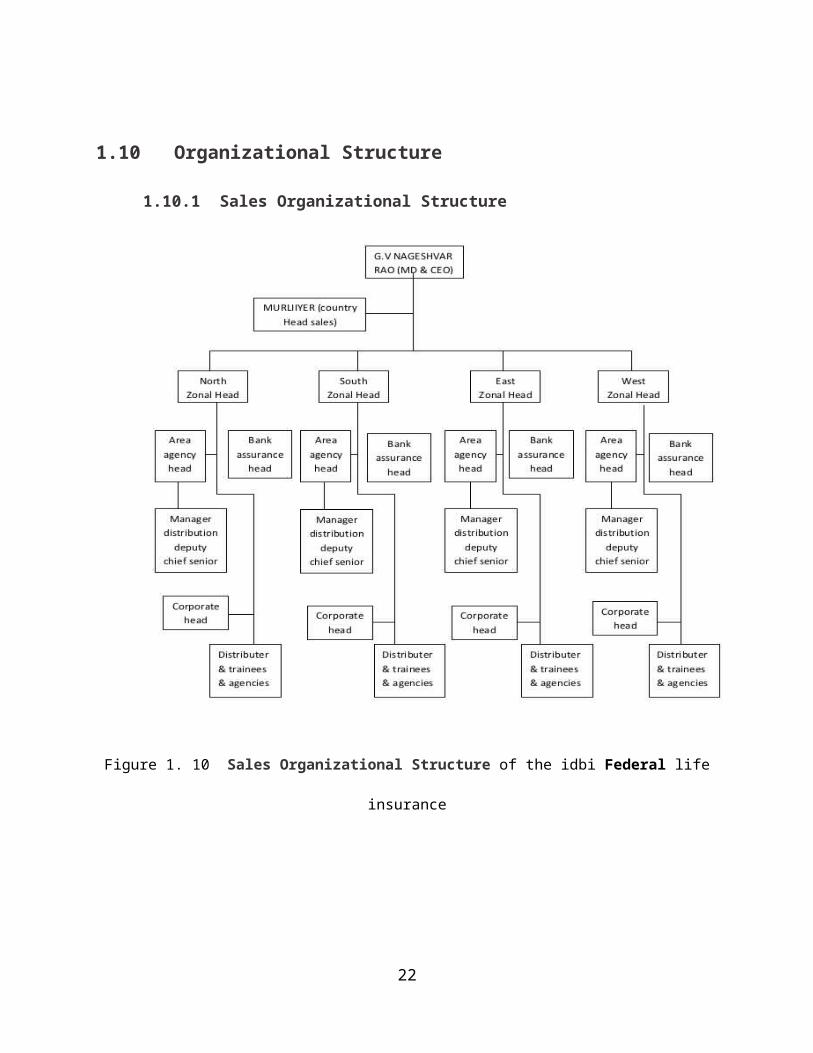

1.10 Organizational Structure

1.10.1 Sales Organizational Structure

Figure 1. 10 Sales Organizational Structure of the idbi Federal life insurance

16

1.10.2 Human Resource Organizational Structure

Figure 1. 11 Human Resource Organizational Structure of the idbi Federal life insurance

17

1.10.3 Operational Organizational Structure

Figure 1. 12 Operational Organizational Structure of the idbi Federal life insurance

18

1.11.1 Objective of study

To compare my skills and knowledge with the requirement of corporate world

To implement the concept studies in academics in real world

To learn about various types of investment tools

To compare the tools and find out the positives and negatives of every tool

1.11.2 Sources of data

Primary data

Primary data was collected by my colleagues, seniors, and by

distributing the questionnaires to the people of different backgrounds. The

questionnaires were carefully designed under the supervision of my supervisor, Mr.

Sanjeev Malik, taking every parameter of my study in my mind.

Secondary data

Data was collected from books, magazines, web sites, going through the

records of the organisation, etc. It is the data which has been collected

by individual or someone else forth purpose of other than those of our

particular research study.

19

CHAPTER 2SWOT Analysis of

IDBI FEDERAL LIFE INSURANCE

20

2.1 Strengths & Weaknesses

2.1.1 Strengths

skilled workforce

reduced labor costs

Superior customer service

High degree of customer satisfaction.

Dedicated workforce aiming at making a long-term career in the field.

Large pool of technically skilled manpower with in depth knowledge and

understanding of the market

2.1.2 Weakness

Management cover insufficient.

Sectoral growth is constrained by low unemployment levels and competition for

staff.

Low customer confidence on the private players

Low or negative growth rate

2.2 Opportunities & Threats

2.2.1 Opportunities

Insurable population : According to IRDA only 10% of the population is insured

which represent around 30% of the insurable population.

21

Due to new budget, FDI is possible due to which company can grow

Quick claim settlement (policy of claim settlement in 8 working days)

Efficient R&D team to launch new products

2.2.2 Threats

tax changes

FDI increased the completion

Threat from international players

2.3 Unique Selling Prepositions

the USP of IDBI FEDERAL LIFE INSURANCE PVT. Ltd is that it is a reliable

firm, as it constitute the combination of a government bank, a private but top most

(in south India) bank, and the second largest insurance firm, ageas. Moreover it has

a believe of ‘what we say, is what it is’ which is mostly missing in other insurance

firms.

And it also have highly R&D team which innovates its products to make it best.

The company has all unique products on which customers can relay. One such

product is INCOMESURENCE, Which gives GARUNTEED 138% cash back,

from 6th year, on the premium paid, first 5 years.

22

Moreover it has a policy of paid-up, in which, if the customer is unable to pay

premium after two years, his policy will be converted according to the amount

paid.

All such products are reliable due to everything mentioned in the policy in writing.

Maximum firms promises such things but do not give these thing in writing ans

they are making virtual promises, but IDBI FEDERAL gives surety about the

money of the customer.

23

CHAPTER 3 Comparative study on

various investment instruments-

INSURANCE and MUTUAL FUNDS

24

3.1 Introduction

Saving is income not spent, or deferred consumption. Methods of saving include putting

money aside in a bank or pension plan. Saving also includes reducing expenditures, such as

recurring costs. In terms of personal finance, saving specifies low-risk preservation of

money, as in a deposit account, versus investment, wherein risk is higher.

Saving is closely related to investment. By not using income to buy consumer goods and

services, it is possible for resources to instead be invested by being used to produce fixed,

such as factories and machinery. Saving can therefore be vital to increase the amount of

fixed capital available, which contributes to economic growth.

Investment is the purchase of an asset or item with the hope that it will generate income or

appreciate in the future and be sold at the higher price. The term investment is usually used

when referring to a long-term outlook. This is the opposite of trading or speculation, which

are short-term practices involving a much higher degree of risk.

the various types of investing tools are:

Bank (FD, RD,SA)

Shares

Bonds

Gold

Insurance

Post office

Mutual funds

25

All the instruments are good to be invested with some positives and negative factors. Let us

do a detailed study of insurance and mutual funds as the investment tools in current era

and compare both of them.

3.2 INSURANCE

Insurance is the equitable transfer of the risk of a loss, from one entity to another in

exchange for payment. It is a form of risk management. Insurance involves pooling funds

from many insured entities (known as exposures) to pay for the losses that some may incur.

The insured entities are therefore protected from risk for a fee, with the fee being

dependent upon the frequency and severity of the event occurring.

An insurer, or insurance carrier, is a company selling the insurance; the insured, or

policyholder, is the person or entity buying the insurance policy. The amount of money to

be charged for a certain amount of insurance coverage is called the premium.

Methods for transferring or distributing risk were practiced

by Chinese and Babylonian traders as long ago as the 3rd and 2nd millennia BC,

respectively. Chinese merchants travelling treacherous river rapids would redistribute their

wares across many vessels to limit the loss due to any single vessel's capsizing. The

Babylonians developed a system which was recorded in the famous Code of Hammurabi, c.

1750 BC, If a merchant received a loan to fund his shipment, he would pay the lender an

additional sum in exchange for the lender's guarantee to cancel the loan should the

shipment be stolen or lost at sea.

26

3.2.1 Types of insurance

Figure 3. 1 types of insurance

27

Types Of Insurence

life insurancenon- life

insurance

FireMiscellaneousMotor

Health

travell

Propert

y

Marine

re-insurance

3.2.1 Life Insurance

Life insurance is a contract between an insured and an insurer or assurer, where the

insurer promises to pay a designated beneficiary a sum of money in exchange for a

premium, upon the death of the insured person. Depending on the contract, other

events such as terminal illness or critical illness may also trigger payment. The

policy holder typically pays a premium, either regularly or as a lump sum. Other

expenses (such as funeral expenses) are also sometimes included in the benefits.

Life policies are legal contracts and the terms of the contract describe the limitations

of the insured events. Specific exclusions are often written into the contract to limit

the liability of the insurer; common examples are claims relating to suicide, fraud,

war, riot, and civil commotion.

Life insurance provides a monetary benefit to a decedent's family or other designated

beneficiary, and may specifically provide for income to an insured person's family,

burial, funeral and other final expenses. Basically, the insured person pay premiums

according to the policy, when he is alive, and gets the grantee of payback the total

premium amount with increment in amount in form of interest, bonuses etc, to his

family after his death. Life insurance policies often allow the option of having the

proceeds paid to the beneficiary either in a lump sum cash payment or an annuity.

3.2.2 Reinsurance

Reinsurance is insurance that is purchased by an insurance company from one or

more other insurance companies. The ceding company and the reinsurer enter into

a reinsurance agreement which details the conditions upon which

28

the reinsurer would pay a share of the claims incurred by the ceding company. The

reinsurer is paid a "reinsurance premium" by the ceding company, which issues

insurance policies to its own policyholders.

The reinsurer may be either a specialist reinsurance company, which only undertakes

reinsurance business, or another insurance company.

For an example of a reason for purchasing reinsurance, assume an insurer sells 1,000

policies, each with a $1 million policy limit. Theoretically, the insurer could lose $1

million on each policy – totaling up to $1 billion. It may be better to pass some risk

to a reinsurer as this will reduce the ceding company's exposure to risk.

A healthy reinsurance marketplace helps to ensure that insurance companies can

remain solvent (financially viable) because the risks and costs are spread,

particularly after a major disaster such as a major hurricane.

3.2.3 Non- Life Insurance

non life insurance include all other types of insurance other than life insurance. Let

us have a brief review of them. They are

1. Fire insurance

Insurance that is used to cover damage to a property caused by fire. Fire

insurance is a specialized form of insurance beyond property insurance, and is

designed to cover the cost of replacement, reconstruction or repair beyond

what is covered by the property insurance policy. Policies cover damage to the

29

building itself, and may also cover damage to nearby structures, personal

property and expenses associated with not being able to live in or use the

property if it is damaged.

2. Marine insurance

Marine insurance covers the loss or damage of ships, cargo, terminals, and

any transport or cargo by which property is transferred, acquired, or held

between the points of origin and final destination. Cargo insurance —

discussed here — is a sub-branch of marine insurance, though Marine also

includes Onshore and Offshore exposed property, Marine Casualty. and

Marine Liability. When goods are transported by mail or courier, shipping is

used instead.

3. Miscellaneous

It includes:

Automobile insurance

A policy purchased by vehicle owners to mitigate costs associated with

getting into an auto accident. Instead of paying out of pocket for auto

accidents, people pay annual premiums to an auto insurance company;

the company then pays all or most of the costs associated with an auto

accident or other vehicle damage.

Health insurance

Health insurance is insurance against the risk of incurring medical

expenses among individuals. According to the Health Insurance

Association of America, health insurance is defined as "coverage that

30

provides for the payments of benefits as a result of sickness or injury.

Includes insurance for losses from accident, medical expense,

disability, or accidental death and dismemberment"

Travel insurance

Travel Insurance is insurance that is intended to

cover medical expenses, financial default of travel suppliers, and other

losses incurred while traveling, either within one's own country, or

internationally.

Property insurance

Property insurance provides protection against most risks

to property, such as fire, theft and some weather damage.

3.3 MUTUAL FUNDS

A mutual fund is a type of professionally managed collective investment scheme that

pools money from many miscellaneous investors to purchase securities. While there is no

legal definition of the term mutual fund, it is most commonly applied only to those

collective investment vehicles that are regulated and sold to the general public. They are

sometimes referred to as "investment companies" or "registered investment

companies". Most mutual funds are open-ended, meaning stockholders can buy or sell

shares of the fund at any time by redeeming them from the fund itself, rather than on an

exchange. Hedge funds are not considered a type of mutual fund, primarily because they

are not sold publicly.

31

Mutual funds have both advantages and disadvantages compared to direct investing in individual

securities.

The fund manager, also known as the fund sponsor or fund management company, trades(buys and

sells) the fund's investments in accordance with the fund's investment objective. A fund manager

must be a registered investment advisor. Funds that are managed by the same fund manager and

that have the same brand name are known as a fund family orfund complex.

Advantages and disadvantages

Mutual funds have advantages compared to direct investing in individual securities. These

include:

Increased diversification: A fund must hold many securities. Diversifying reduces risks

compared to holding a single stock, bond, other available instruments.

Daily liquidity: This concept applies only to open-end funds. Shareholders may trade

their holdings with the fund manager at the close of a trading day based on the closing net

asset value of the fund's holdings. However, there may be fees and restrictions as stated

in the fund prospectus. For holders of individual stocks, bonds, closed-end funds, ETFs,

and other available instruments, there may not be a buyer/seller for that instrument every

day, making such investments less liquid.

Professional investment management: A highly variable aspect of a fund discussed in the

prospectus. Actively managed funds may have large staffs of analysts who actively trade

the fund holdings. Management of an index fund may just passively re-balance holdings

to match a market index like the Standard and Poors 500 Index.

Ability to participate in investments that may be available only to larger investors:

Foreign markets, in particular, are rarely open and affordable for individual investors.

32

Moreover, the research required to make sensible foreign investments may require

knowledge of another language and the rules of regulations of other markets.

Service and convenience: This is not a feature of a mutual fund, but rather a feature of the

fund management company. Increasingly in recent years, there are funds, notably

Exchange Traded Funds (ETFs) that are purely investment instruments without any

additional services from the fund management company.

Government oversight: Largely, the US government's role with mutual funds is to require

the publication of a prospectus describing the fund. No such document is required for

stock, bonds, currencies, and other investment instruments. There is no governmental

oversight of a fund's investment success/failure.

Ease of comparison: Since mutual funds are available from many providers, it is

generally easy to find similar funds and compare features such as expenses.

Mutual funds have disadvantages as well, which include

Fees

Less control over timing of recognition of gains

Less predictable income

No opportunity to customize

33

3.4 Comparison of insurance And Mutual Funds

Now after knowing a lot about both, insurance and mutual funds, let us compare both of

them and study the feasibility of investing the money them:

3.4.1 Investing by insurance

By investing in life insurance, almost anyone can transfer the financial risks of

dying early, guaranteeing to family members who might otherwise be left in

economic turmoil. Today's life insurance policies, however, often come with

features borrowed from the investment world, blending traditional insurance with

attributes of a mutual fund account. Those who haven't purchased a policy may be

familiar only with "term" life insurance, which covers the owner for a set period of

time. If the owner lives past that date, the plan expires and is worthless. But now,

life insurance policies are "cash value," which means the fees, or premium is then

invested in a "separate account," either by the insurer or in an account controlled

by the policy holder, building up cash value. Any investment gains can be used in

a few ways: to increase the death benefit, to borrow against for any use or to keep

the policy in effect if one stop paying monthly premiums. In this system, the cash

value and benefits may actually decrease or go away completely depending upon

the performance of the investments

Note: the investment of insurance premium is basically calles ULIP (Unit

Linked Insurance Plans)

34

ADVANTAGES:

The advantages of investing in insurance are:

1. Investment

The money given in premium is invested by some experts of the company,

therefore the chances of losses decreases

2.Tax Benefit:

the premium and the bash received back are wholly tax exempted.

3.Insurance benefits:

The thing insured is the basic advantage of the insurance as the risk is

transferred to the company.

3.4.2 Investing in mutual funds

The basics of investing money in Stocks, Bonds, Mutual funds, are simple and

easy as one proceeds step by step . Any successful stock market investor is familiar

with the basics of mutual fund investing. But mostly investors are not even aware

on their investments in mutual funds schemes, where their money have been

invested. Investing in equity, mutual funds, keeping an eye opportunities, watching

the trends is not easy but one can learn the steps for successful investing.

Both the long term and short term investors can benefit from such type investments

but there is a need of regular update on new investing schemes. Talking about

Indian market, Indian stock market is quite mature. In fact India has the largest

investor base in the world after the US and Japan. Investors can invest in shares,

debentures, mutual funds and securities among other investment tools. In addition

to above two main stock exchanges India have 21 recognised stock exchanges but

35

the most active ones are the NSE and the BSE. NSE set up has a model exchange

as a fully automated screen based system. BSE one of the oldest in the world

accounts for the largest number of listed companies has also started a screen based

trading system with the introduction of the Bombay online trading system.

Regulations on the capital markets and the protection of investors interest is

primarily the responsibility of the Securities and Exchange Board of India (SEBI)

Headquartered in Mumbai. Consider three parameters while selecting a company.

ADVANTAGES:

Mutual funds are relatively stables as the money is invested in many firms, the

drop in 1 can be compensated by other. The risk factor is low. And returns are

most of the times good.

3.4.3 INSURANCE VS. MUTUAL FUNDS

BASIS INSURANCE MUTUAL FUNDS

Description Insurance Plans refer to

plans, that allow investors to

direct part of their premiums

into different types of funds

(equity, debt, money market,

hybrid etc.).

A mutual fund pools the

money from investors and

uses it to invest in various

securities according to a pre-

specified investment

objective.

Objective They are long term plans

offering you a dual benefit of

insurance and investment.

Mutual funds are ideal

investment tool for the short

to medium term.

Tax Benefit All Plans offer tax benefits Only investments in tax

36

under section 80C. saving funds are eligible for

section 80C benefits.

Switching

options

allows you to switch your

investment between the

funds linked to the plan. This

enables you to change the

risk return.

No switching option is

available. If you are not

satisfied with the performance

of the fund you can exit

completely from the same by

paying exit charges, if

applicable.

Additional

Benefits

Some of the Plans give you

an additional benefit or

loyalty benefit by issuing

extra fund units.

There are no additional

benefits issued by mutual

funds

Liquidity Plans have limited liquidity.

One needs to stay invested

for a minimum period of

time as specified in the

policy before redeeming the

units.

You can easily sell mutual

fund units (except for ELSS

and funds that have a

minimum lock-in period).

Charges

structure

Charges in a plan include

mortality charges for the life

insurance provided. In

addition, premium allocation

Mutual fund charges include

an entry load, the annual fund

management charge and an

exit load, if applicable.

37

charge, fund management

charge and administration

charges are applicable.

Table 3. 1 comparison between insurance and mutual funds

38

Review of literature

1. Kumar (2001) investigated the effects of FII inflows on the Indian stock market

represented by the Sensex using monthly data from January 1993 to December 1997.

Kumar (2001) inferred that FII investments are more driven by Fundamentals and they do

not respond to short-term changes or technical position of the market. In testing whether

Net FII Investment (NFI) has any impact on Sensex, a regression of NFI was estimated

on lagged values of the first difference of NFI, first difference of Sensex and one lagged

value of the error correction term (the residual obtained by estimating the regression

between NFI and Sensex). The study concluded that Sensex causes NFI. Similarly,

regression with Sensex as dependent variable showed that one month lag of NFI is

significant, meaning that there iscausality from FII to Sensex.

2. Stanley Morgan (2002) has examined that FIIs have played a very important role in

building up India’s forex reserves, which have enabled a host of economic reforms.

Secondly, FIIs are now important investors in the country’s economic growth despite

sluggish domestic sentiment. The Morgan Stanley report notes that FII strongly influence

short-term market movements during bear markets. However, the correlation between

returns and flows reduces during bull markets as other market participants raise their

involvement reducing the influence of FIIs. Research by Morgan Stanley shows that the

correlation between foreign inflows and market returns is high during bear and weakens

with strengthening equity prices due to increased participation by other players.

39

3. Agarwal, Chakrabarti et al (2003) have found in their research that the equity return has a

significant and positive impact on the FII. But given the huge volume of investments,

foreign investors could play a role of market makers and book their profits, i.e., they can

buy financial assets when the prices are declining thereby jacking-up the asset prices and

sell when the asset prices are increasing. Hence, there is a possibility of bi-directional

relationship between FII and the equity returns.

4. P. Krishna Prasanna (2008) has examined the contribution of foreign institutional

investment particularly among companies included in sensitivity index (Sensex) of

Bombay Stock exchange. Also examined is the relationship between foreign institutional

investment and firm specific characteristics in terms of ownership structure, financial

performance and stock performance. It is observed that foreign investors invested more in

companies with a higher volume of shares owned by the general public. The promoters’

holdings and the foreign investments are inversely related. Foreign investors choose the

companies where family shareholding of promoters is not substantial. Among the

financial performance variables the share returns and earnings per share are significant

factors influencing their investment decision

5. Anand Bansal and J.S. Pasricha (2009) studied the impact of market opening to FIIs on

Indian stock market behavior. They empirically analyze the change of market return and

volatility after the entry of FIIs to Indian capital market and found that while there is no

significant change in the Indian stock market average returns; volatility is significantly

reduced after India unlocked its stock market to foreign investors. In the next section we

are discussing the data sources and methodology of the study.

40

Data AnalysisAnd

Interpretation

41

The Segmentation of sample as on the basis of gender, age, family status, annual income,

occupation etc. the demographic profile is as follows

Basis Particulars Frequency Percentage

gender

male 14 70

female 6 30

total 20 100

age

18-30 5 25

31-40 4 20

41-50 6 30

50+ 5 25

total 20 100

Marital

status

married 18 90

single 2 10

total 20 100

Income( in

lakhs)

1-2 1 5

2-3 13 65

3-4 5 25

More than 4 1 5

42

total 20 100

Occupation business 16 80

service 4 20

total 20 100

Table 3. 2 demografic profile

Q1. Do you know About ULIP Insurance?

Particulars Response Percentage

yes 17 85

no 3 15

total 20 100

Table 3. 3 awareness of ulip

85%

15%

AWARENESS

yesno

Figure 3. 2 awareness of ulip

Interpretation

As insurance sector is growing rapidly so most of the life insurance players are selling ULIP

plans. And the awareness about ULIP is growing most of the people knows the ULIP of life

43

insurance. Since last 4-5 years the returns provided by ULIP were very good so people tend more

to words ULIP.

Q2. Do you have taken any ULIP insurance policy? Can you name it?

particulars Company name responses percentage

yes Idbi federal life insurance 9 45

Reliance Life Insurance 2 10

SBI Life Insurance 5 25

no 4 20

total 20 100

Table 3. 4 preference of company

56%

13%

31%

PREFERENCE FOR COMPANY

Idbi fedral life insuranceReliance Life InsuranceSBI Life Insurance

Figure 3. 3 preference of company

INTERPRATION

While investing, people are most likely to invest in idbi federal life insurance followed by SBI

life insurance and at the end IDBI federal life insurance

44

Q3. If yes, which company’s ULIP you have taken and why?

Particulars Response Percentage

SECURTY 5 31.25

INVESTMENT 6 37.5

TAX RELIEF 5 31.25

Table 3. 5 reasons for investment

31%

38%

31%

REASON FOR INVESTMENT

securityinvestmenttax relief

Figure 3. 4 reasons for investment

INTERPRATION

Most of the people invest in ulip for investment.

45

Q4. Do you know about Mutual fund?

Particulars Response Percentage

yes 12 60

no 8 40

total 20 100

Table 3. 6 awareness for mutual funds

60%

40%

AWARENESS

yesno

Figure 3. 5 awareness for mutual funds

Interpretation

As now till date people in India did not to invest in share market because then were thinking that

it is a bad thing but as the awareness about Mutual fund is increasing as more and more private

players are entering in the market. So awareness about MF is Good and it can be improved.

Q5) If yes, what is the preference for choosing the mutual funds?

46

Particulars Response Percentage

GOOD

RETURNS

6 50

INVESTMENT 2 16.66

LIQUIDITY 4 33.33

Table 3. 7 reasons for investment in mutual funds

50%

17%

33%

REASON FOR INVESTMENT

good returnsinvestmentliquidity

Figure 3. 6 reasons for investment in mutual funds

INTERPRITATION

While investing in mutual fund 50% investors preferring more to the returns the mutual fund is

providing and 17% for the Investment and 33% for Liquidity reasons.

Q6) Which is the factor you consider the most while choosing any Investment Option?

47

Particulars Response Percentage

returns 6 36

security 11 64

total 17 100

Table 3. 8 Basis for preference of investment tool

returns security

36%

64%

BASIS FOR PREFERENCE OF IN-VESTMENT TOOL

Figure 3. 7 Basis for preference of investment tool

Interpretation

In future people will be more preferring to the security of their money means they want an

secured option which should provide good returns. As ULIP are the option in which you can

have the security also and good returns. The second choice of the investors is return of their

money.

Q7) Whom Do you prefer first for

investment?

48

Investment

Option

Response

(No. of

Persons)

percentage

Mutual Fund 7 41

ULIP 10 59

Total 17 100

mutual funds vs ulip

mutual funds ulip

41%59%

mutual funds vs ulip

Figure 3. 8 mutual funds vs ulip

Interpretation

As most of the people want the option which should provide security and good returns and there

is only option available with good liquidity is ULIP of IDBI federal Life Insurance. 59% people

had opted for ULIP as their future investment and 41% of people opted for Mutual Fund. So we

can find that there not so much difference in these option.

49

Table 3. 9

Q8) How would you rate IDBI federal life insurance?

Ratings Response

(No. of Persons)

Fair 3

Average 6

Good 5

Best 6

Table 3. 10 ratings for the company

Fair Average Good Best0

1

2

3

4

5

6

7 Ratings

Ratings

Figure 3. 9 ratings for the company

Interpretation

From this we can analyze that IDBI federal Life Insurance is doing good but it is having good

potential in Market. To improve its market share they should improve the awareness level of the

common people.

Conclusions and/or Recommendations

50

From above analysis and survey we can conclude as follows

Awareness of ULIP is increasing as more number of private players are entering in life

insurance industry.

Mutual Fund is also getting more and more famous in Indian market as many private

companies innovating new funds as the investors demand.

ULIP differentiate from Mutual fund in respect of Insurance cover.

Investors in IDBI federal Life ULIP will be getting the advantage of life insurance cover.

ULIP and Mutual fund are providing same type of investment funds like, equity funds,

debt funds, infrastructure fund, balanced fund etc.

In terms of expenses mutual funds are having low expenses as compared to ULIP of IDBI

federal life insurance.

People are turning to words the ULIP as a good investment option but as ULIP is in its

starting phase so customers are preferring only big brands.

Mutual fund is having good growth but many customers from rural areas don’t have any

knowledge about Mutual fund.

There is a need for insurers to undertake a demand audit in order to understand what the

policyholder wants and needs.

Deriving the right feedback from customers and bringing out innovative products which

cater to customer demands will go a long way in tapping the market potential of the

insurance and Mutual fund sector.

51

Mutual fund and ULIP insurance both are facing fierce competition; increasingly more

organizations are seeking to enhance their demand in the market place.

IDBI federal Life Insurance should go for innovating more and more products and

improving the distribution channels as per the area of sales.

52

Chapter-4Lessons Learnt

53

I join the IDBI federal life insurance with the theoretical knowledge gained in the academics,

with an objective to ascertain the practical knowledge. My basic objective was to experience

how the corporate world works in real life.

This internship was full of ups and downs which made me learnt many lessons and help me to

gain several experiences

Working environment was excellent. Great staff members were there. Well maintained office.

All facilities were provided to the employees. Flexibility was maintained. Employees doubt and

suggestions was always welcomed.

We were called on alternative days and trained and made learn about the company profile,

culture, its products and many more things.

Then we were told to contact our closed and dear ones in order to sell the product to the. This

activity gave me confidence as I was feeling as a professional and was dealing with the

customers on the behalf of such a large scale firm. That feeling was great.

Almost all the queries raised by customers was tackled by me, but in case, I got struck anywhere,

the managers act as a support system for me. This culture of firm helped me to fulfill my

deadlines and work well.

Personal Experience

I learned various things:

It helped me in improving my communication skills and presentation skills

My confidence level was increased

How to tackle different client base

54

Practical knowledge

Tackling the quarries

Handling the work loads

Difficulties faced during the internship

Overall it was a good experience while working in UAS International, but I faced little bit difficulties

during my internship period.

Handling customers quarries

Meeting with tough deadlines

Competitive working environment

Personally I would like to recommend my friends to be a part of this firm and also like to see

future in the same. IDBI federal life insurance co. ltd. Offers the interns ample of scope to

develop the persons personality, rather say professional personality.

55