Embed Size (px)

Citation preview

www.woodmac.com

Comparative Energy Framework in Malaysia, Indonesia and ThailandWood Mackenzie paper prepared for the 4th National Energy Forum

S t b 2012September 2012

Strategy with substance

www.woodmac.com

Disclaimer

This presentation has been prepared for presentation at the 4th National Energy Forum in Malaysia. The presentation is intended solely for the benefit of forum participants and its contents and conclusions maypresentation is intended solely for the benefit of forum participants, and its contents and conclusions may not be disclosed to any other persons or companies without Wood Mackenzie’s prior written permission.

The information upon which this presentation is based comes from our own experience, knowledge, and d t b Th i i d i thi t ti th f W d M k i Th h bdatabases. The opinions expressed in this presentation are those of Wood Mackenzie. They have been arrived at following careful consideration and enquiry but, as of this date, are subject to change. We do not accept any liability for your reliance on them.

September 2012

Strategy with substance© Wood Mackenzie 2

www.woodmac.com

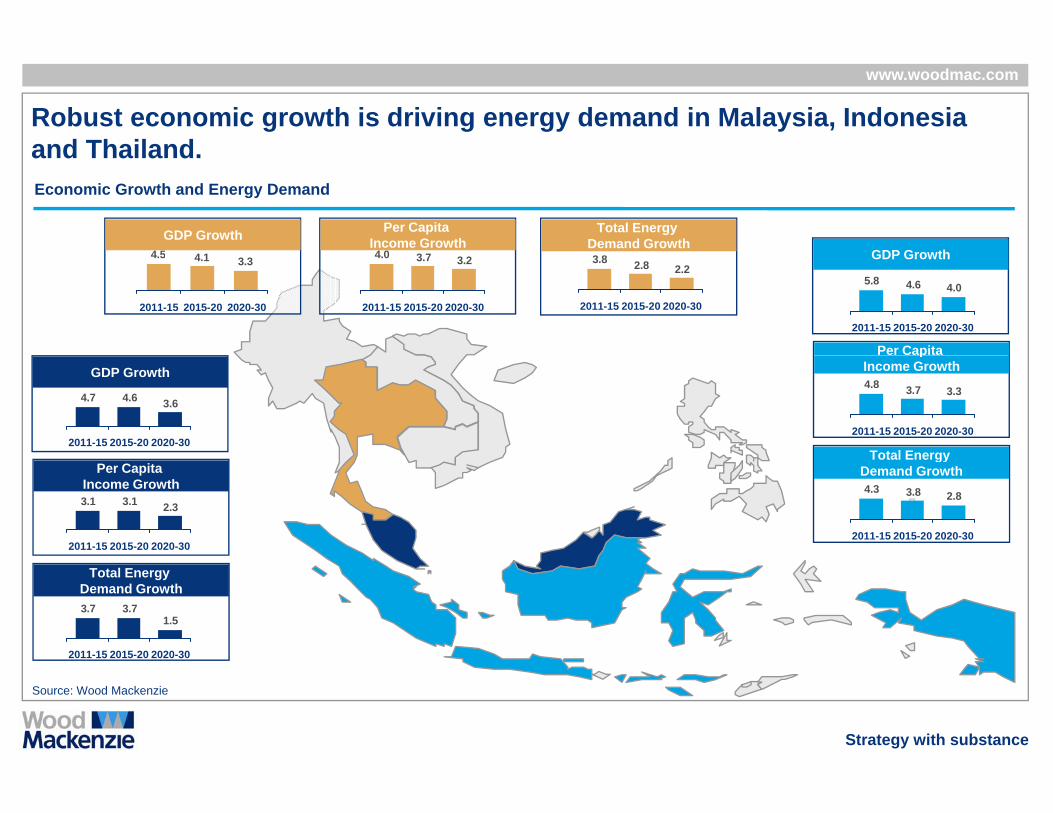

Robust economic growth is driving energy demand in Malaysia, Indonesia and Thailandand Thailand.Economic Growth and Energy Demand

4 04 5GDP Growth Per Capita

Income GrowthTotal Energy

Demand GrowthGDP Growth

4.04.65.8

2011-15 2020-302015-20

2.22.83.8

2020-302015-202011-15

3.23.74.0

2020-302015-202011-15

3.34.14.5

2020-302015-202011-15

Per Capita

GDP Growth

3.64.64.7

2020-302015-202011-15

GDP Growth3.33.74.8

2015-20 2020-302011-15

pIncome Growth

Total Energy

2.33.13.1

2020-302015-202011-15

Per Capita Income Growth

2.83.84.3

2020-302015-202011-15

Total Energy Demand Growth

Total Energy Demand Growth

1.53.73.7

2015-202011-15 2020-30

Strategy with substance

Source: Wood Mackenzie

www.woodmac.com

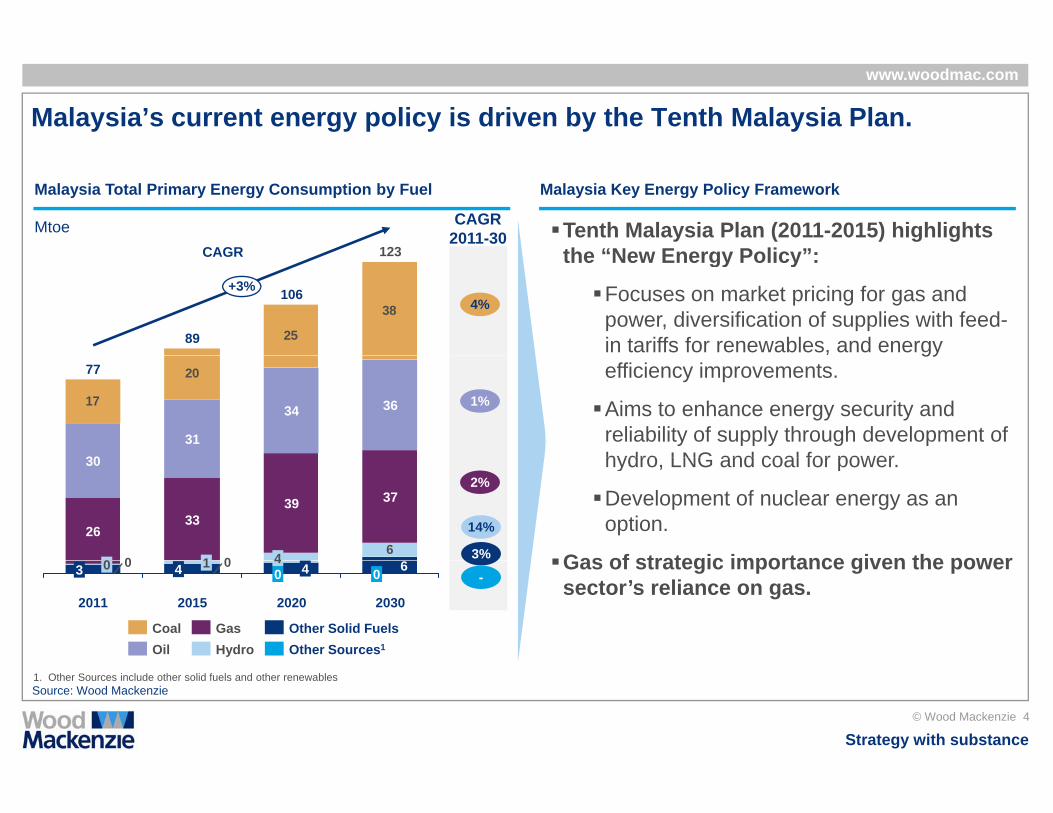

Malaysia’s current energy policy is driven by the Tenth Malaysia Plan.

Malaysia Total Primary Energy Consumption by Fuel Malaysia Key Energy Policy Framework

Mtoe123CAGR

CAGR 2011-30 Tenth Malaysia Plan (2011-2015) highlights

the “New Energy Policy”:

25

38

89

106

123

+3%

CAGR

4%

the “New Energy Policy”:

Focuses on market pricing for gas and power, diversification of supplies with feed-in tariffs for renewables, and energy

17

20

31

77

3634

30

1%

gyefficiency improvements.

Aims to enhance energy security and reliability of supply through development of hydro LNG and coal for power

006

1

33

0

26

4

39 37

30

3%

14%

2%hydro, LNG and coal for power.

Development of nuclear energy as an option.

Gas of strategic importance given the power00 4 1

2011

3 0

2020

0 44

2015 2030

0 6 Gas of strategic importance given the power sector’s reliance on gas.

Other Sources1

Other Solid FuelsHydroGas

OilCoal

-

Strategy with substance© Wood Mackenzie 4

Source: Wood Mackenzie1. Other Sources include other solid fuels and other renewables

www.woodmac.com

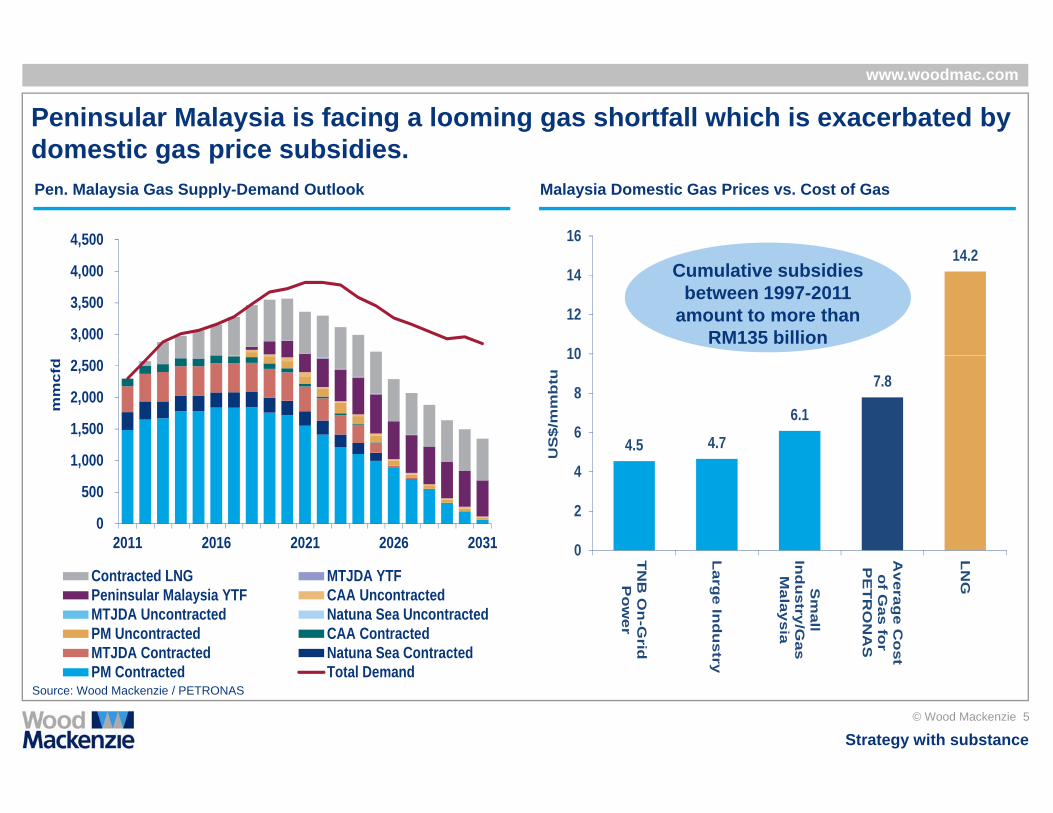

Peninsular Malaysia is facing a looming gas shortfall which is exacerbated by domestic gas price subsidiesdomestic gas price subsidies. Pen. Malaysia Gas Supply-Demand Outlook Malaysia Domestic Gas Prices vs. Cost of Gas

4,50014 2

16

3,000

3,500

4,00014.2

10

12

14 Cumulative subsidies between 1997-2011

amount to more than RM135 billion

1 000

1,500

2,000

2,500

mm

cfd

4.5 4.76.1

7.8

6

8

10

US

$/m

mb

tu

0

500

1,000

2011 2016 2021 2026 2031 0

2

4

A

Contracted LNG MTJDA YTFPeninsular Malaysia YTF CAA UncontractedMTJDA Uncontracted Natuna Sea UncontractedPM Uncontracted CAA ContractedMTJDA Contracted Natuna Sea Contracted

TN

B O

n-G

ridP

ow

er

Larg

e Ind

ustr

Sm

allIn

du

stry/Gas

Malaysia

Averag

e Co

sto

f Gas fo

rP

ET

RO

NA

S

LN

G

Strategy with substance© Wood Mackenzie 5

Source: Wood Mackenzie / PETRONASPM Contracted Total Demand

ry t

www.woodmac.com

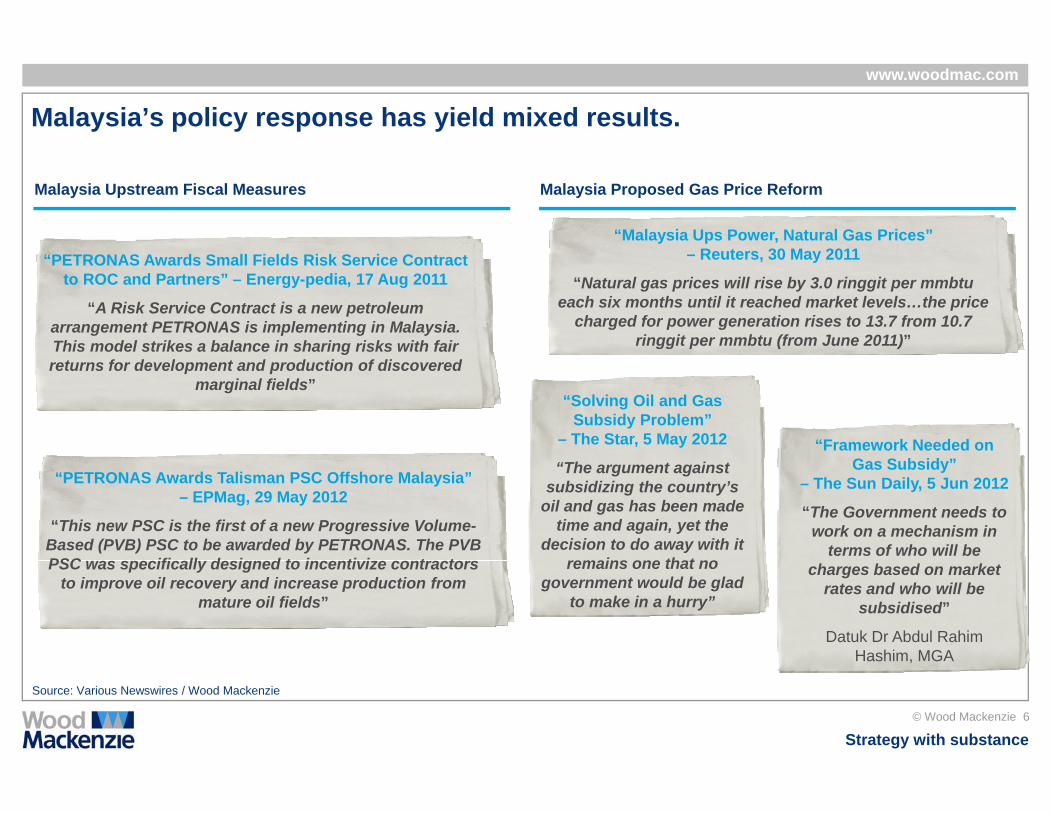

Malaysia’s policy response has yield mixed results.

Malaysia Upstream Fiscal Measures Malaysia Proposed Gas Price Reform

“Malaysia Ups Power, Natural Gas Prices” Reuters 30 May 2011– Reuters, 30 May 2011

“Natural gas prices will rise by 3.0 ringgit per mmbtu each six months until it reached market levels…the price

charged for power generation rises to 13.7 from 10.7 ringgit per mmbtu (from June 2011)”

“PETRONAS Awards Small Fields Risk Service Contract to ROC and Partners” – Energy-pedia, 17 Aug 2011

“A Risk Service Contract is a new petroleum arrangement PETRONAS is implementing in Malaysia. This model strikes a balance in sharing risks with fair

“Solving Oil and Gas Subsidy Problem”

– The Star, 5 May 2012 “Framework Needed on G S

returns for development and production of discovered marginal fields”

“The argument against subsidizing the country’s

oil and gas has been made time and again, yet the

decision to do away with it remains one that no

Gas Subsidy” – The Sun Daily, 5 Jun 2012

“The Government needs to work on a mechanism in

terms of who will be

“PETRONAS Awards Talisman PSC Offshore Malaysia” – EPMag, 29 May 2012

“This new PSC is the first of a new Progressive Volume-Based (PVB) PSC to be awarded by PETRONAS. The PVB PSC ifi ll d i d t i ti i t t remains one that no

government would be glad to make in a hurry”

charges based on market rates and who will be

subsidised”

Datuk Dr Abdul Rahim Hashim, MGA

PSC was specifically designed to incentivize contractors to improve oil recovery and increase production from

mature oil fields”

Strategy with substance© Wood Mackenzie 6

Source: Various Newswires / Wood Mackenzie

,

www.woodmac.com

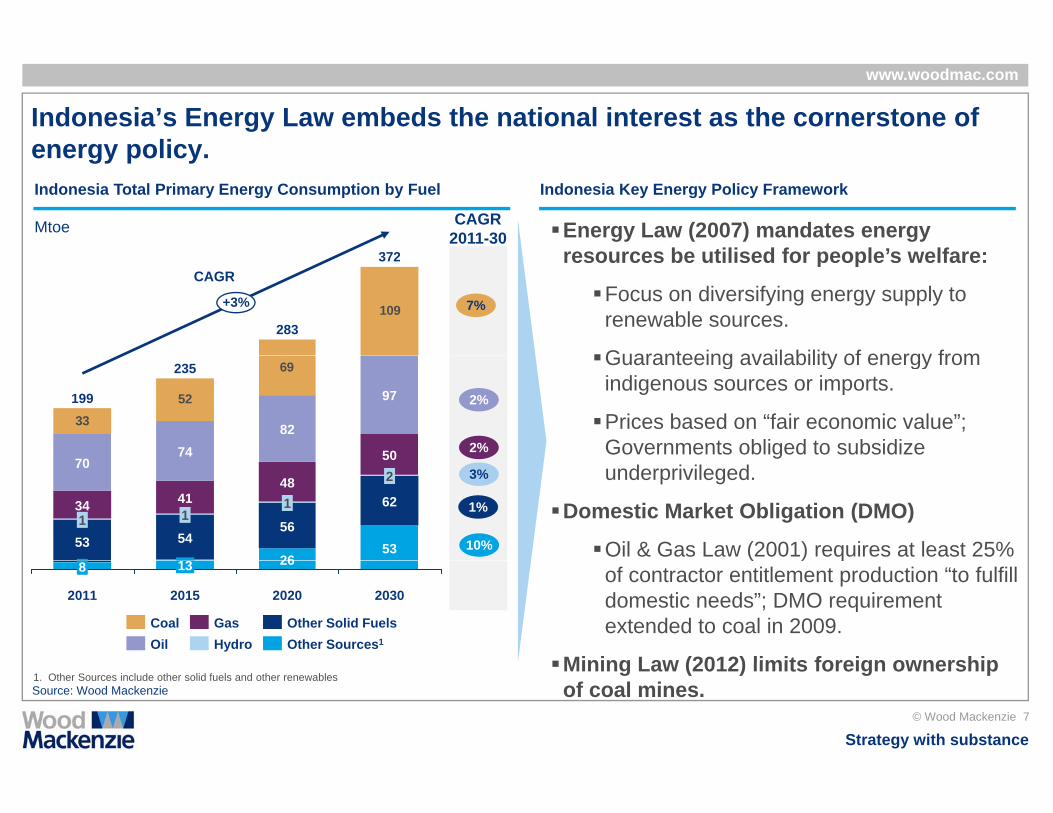

Indonesia’s Energy Law embeds the national interest as the cornerstone of energy policyenergy policy.Indonesia Total Primary Energy Consumption by Fuel Indonesia Key Energy Policy Framework

Mtoe

372

Energy Law (2007) mandates energy resources be utilised for people’s welfare:

CAGR 2011-30

109+3%

372

283

CAGR

7%

resources be utilised for people’s welfare:

Focus on diversifying energy supply to renewable sources.

Guaranteeing availability of energy from

3352

69

82

235

74

199

50

97 2%

2%

Guaranteeing availability of energy from indigenous sources or imports.

Prices based on “fair economic value”; Governments obliged to subsidize

531

34

70

53

62

2

13

541

4148

50

26

56

1 1%

3%

gunderprivileged.

Domestic Market Obligation (DMO)

Oil & Gas Law (2001) requires at least 25% 10%

20302015

13

2011

8

2020

26 ( ) qof contractor entitlement production “to fulfill domestic needs”; DMO requirement extended to coal in 2009.

Mining Law (2012) limits foreign ownership

GasOilCoal

Other Sources1

Other Solid FuelsHydro

Strategy with substance© Wood Mackenzie 7

Source: Wood Mackenzie1. Other Sources include other solid fuels and other renewables

Mining Law (2012) limits foreign ownership of coal mines.

www.woodmac.com

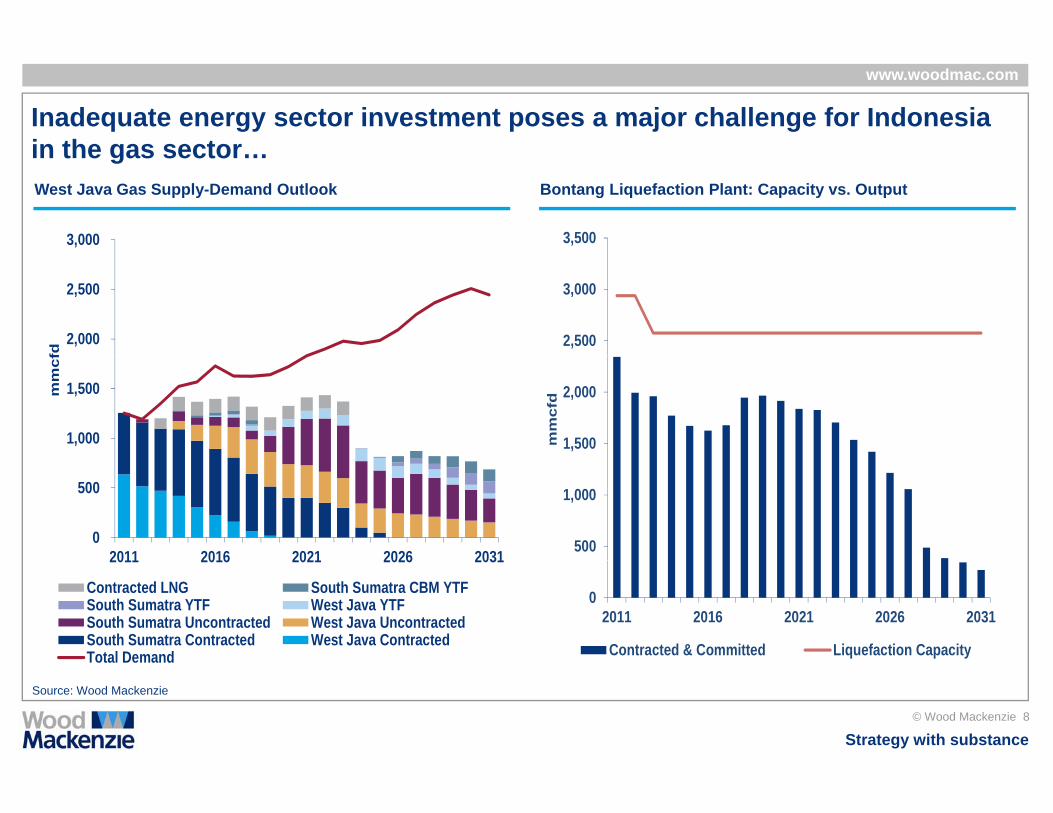

Inadequate energy sector investment poses a major challenge for Indonesia in the gas sectorin the gas sector…West Java Gas Supply-Demand Outlook Bontang Liquefaction Plant: Capacity vs. Output

3,000 3,500

2,000

2,500

fd

2,500

3,000

1,000

1,500mm

cf

1,500

2,000

mm

cfd

0

500

2011 2016 2021 2026 2031 500

1,000

2011 2016 2021 2026 2031

Contracted LNG South Sumatra CBM YTFSouth Sumatra YTF West Java YTFSouth Sumatra Uncontracted West Java UncontractedSouth Sumatra Contracted West Java ContractedTotal Demand

02011 2016 2021 2026 2031

Contracted & Committed Liquefaction Capacity

Strategy with substance© Wood Mackenzie 8

Source: Wood Mackenzie

www.woodmac.com

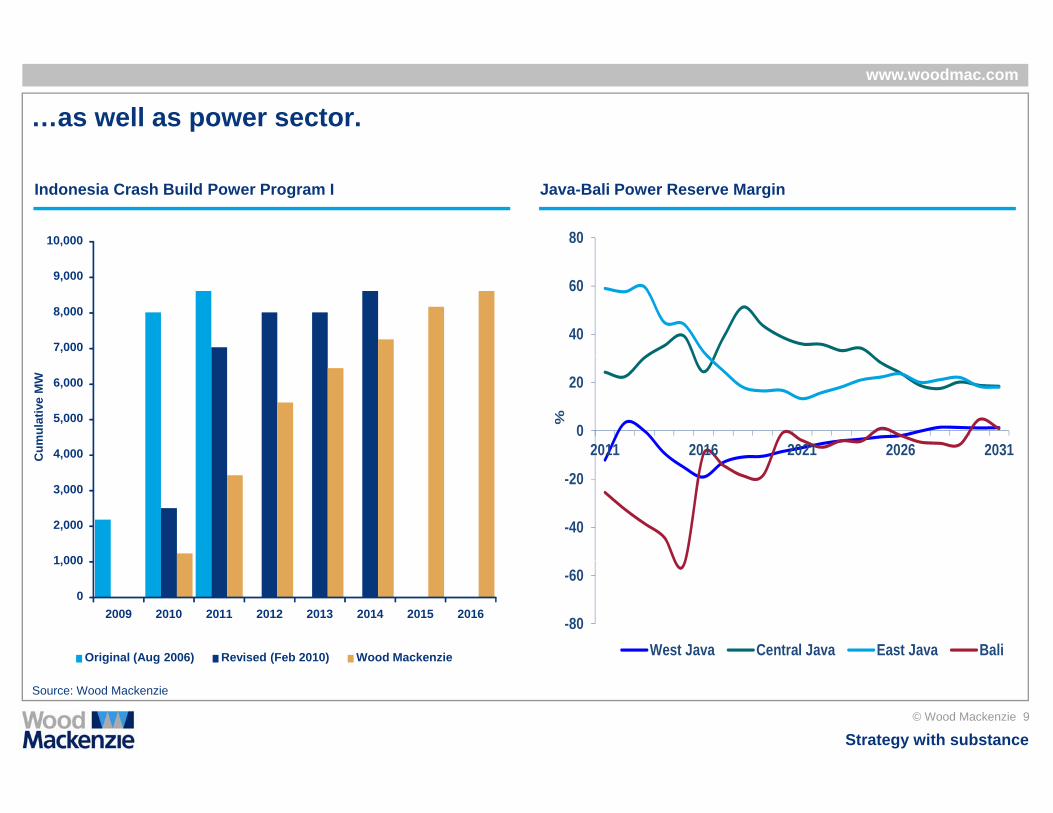

…as well as power sector.

Java-Bali Power Reserve MarginIndonesia Crash Build Power Program I

8010,000

40

60

7,000

8,000

9,000

0

20

2011 2016 2021 2026 2031

%

4,000

5,000

6,000

Cum

ulat

ive

MW

-40

-20

1 000

2,000

3,000

,C

-80

-60

West Java Central Java East Java Bali

0

1,000

2009 2010 2011 2012 2013 2014 2015 2016

Original (Aug 2006) Revised (Feb 2010) Wood Mackenzie

Strategy with substance© Wood Mackenzie 9

Source: Wood Mackenzie

g ( g ) ( )

www.woodmac.com

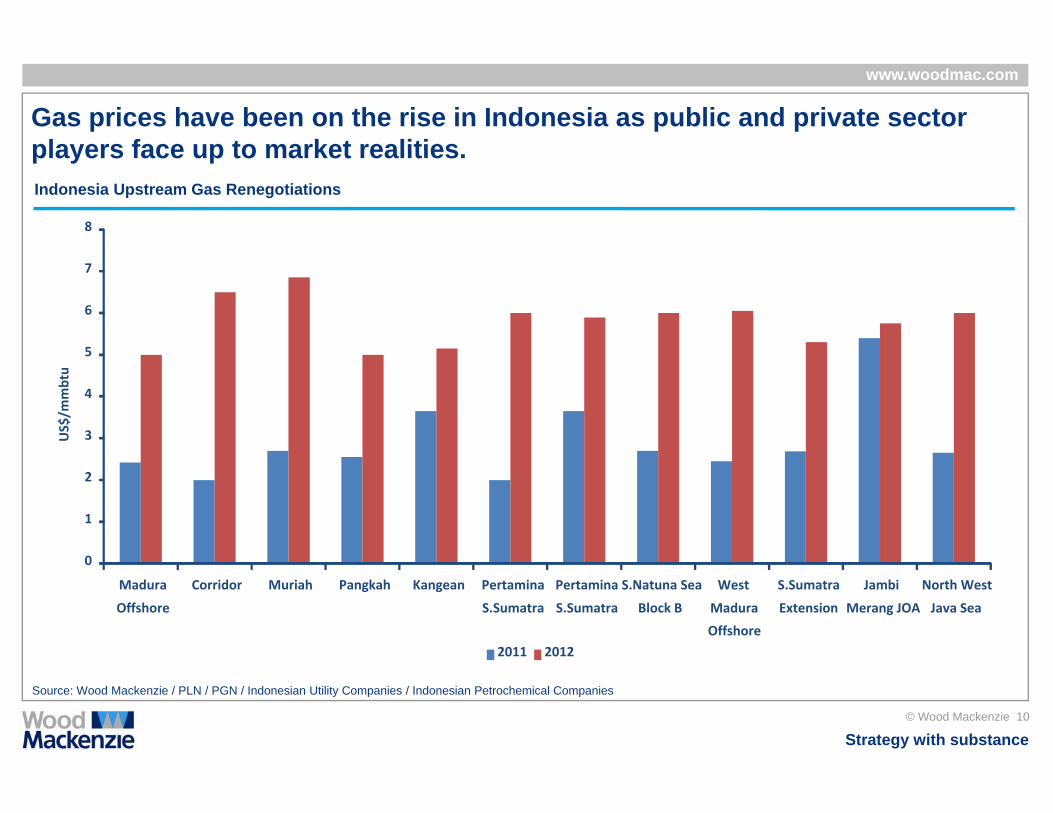

Gas prices have been on the rise in Indonesia as public and private sector players face up to market realitiesplayers face up to market realities.Indonesia Upstream Gas Renegotiations

8

5

6

7

3

4

5

US$/m

mbtu

0

1

2

0

Madura

Offshore

Corridor Muriah Pangkah Kangean Pertamina

S.Sumatra

Pertamina

S.Sumatra

S.Natuna Sea

Block B

West

Madura

Offshore

S.Sumatra

Extension

Jambi

Merang JOA

North West

Java Sea

2011 2012

Strategy with substance© Wood Mackenzie 10

Source: Wood Mackenzie / PLN / PGN / Indonesian Utility Companies / Indonesian Petrochemical Companies

www.woodmac.com

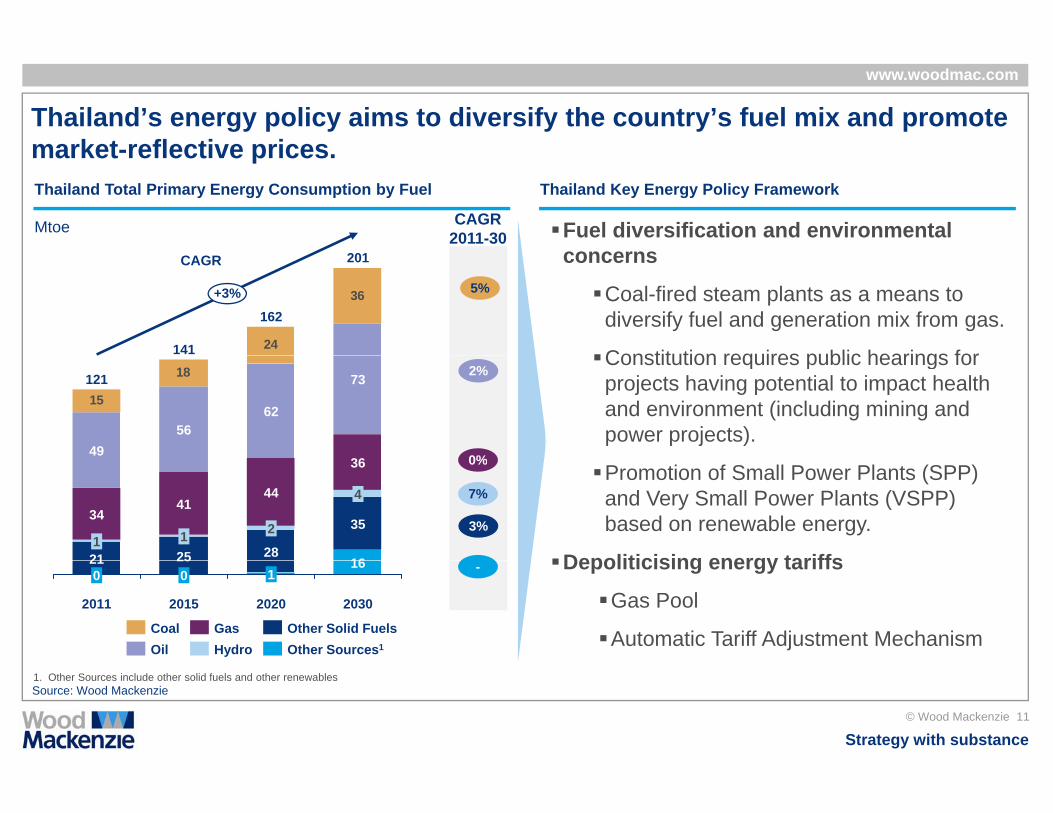

Thailand’s energy policy aims to diversify the country’s fuel mix and promote market-reflective pricesmarket-reflective prices. Thailand Total Primary Energy Consumption by Fuel Thailand Key Energy Policy Framework

Mtoe

201

Fuel diversification and environmental concerns

CAGR 2011-30

24

36162

141

+3%

201CAGR

5%

concerns

Coal-fired steam plants as a means to diversify fuel and generation mix from gas.

Constitution requires public hearings for

15

18

36

73

6256

121

49

2%

0%

Constitution requires public hearings for projects having potential to impact health and environment (including mining and power projects).

4

36

28

2

44

251

41

211

3435

16

3%

7%

0%Promotion of Small Power Plants (SPP) and Very Small Power Plants (VSPP) based on renewable energy.

Depoliticising energy tariffs

2020

1

2015

025

2011

021 16

2030

Depoliticising energy tariffs

Gas Pool

Automatic Tariff Adjustment Mechanism Oil Other Sources1

Other Solid FuelsHydroGasCoal

-

Strategy with substance© Wood Mackenzie 11

Source: Wood Mackenzie1. Other Sources include other solid fuels and other renewables

www.woodmac.com

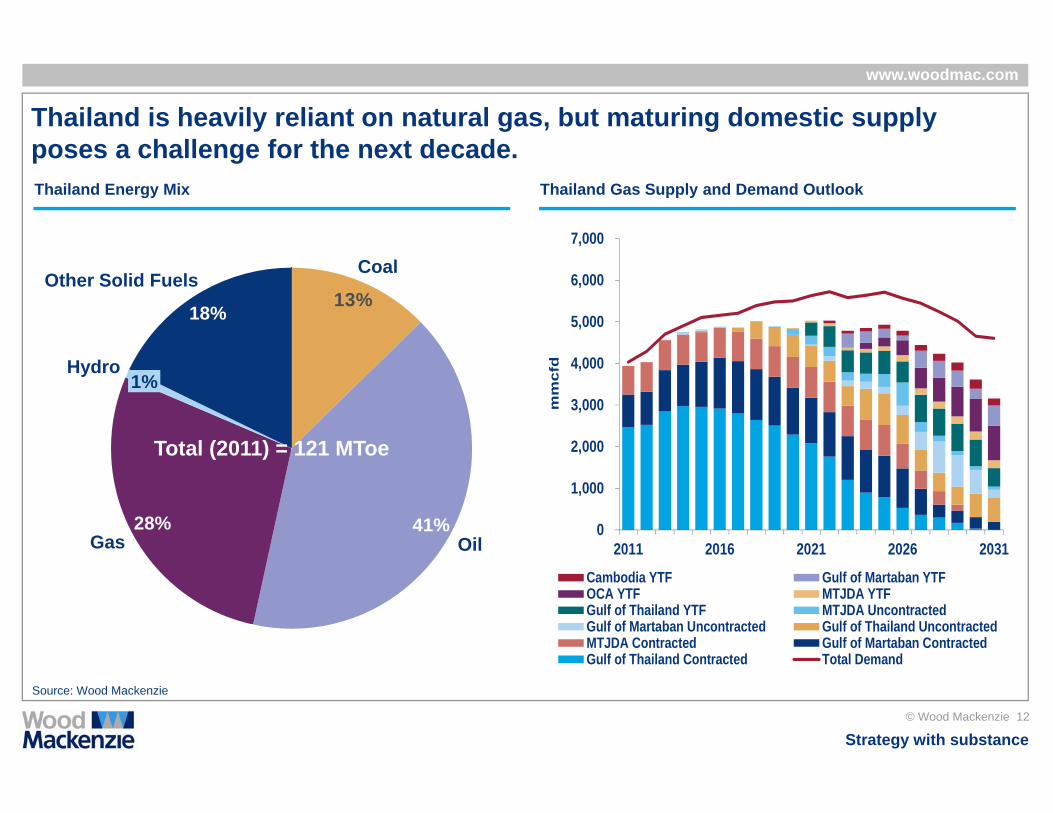

Thailand is heavily reliant on natural gas, but maturing domestic supply poses a challenge for the next decadeposes a challenge for the next decade.Thailand Energy Mix Thailand Gas Supply and Demand Outlook

7,000

5,000

6,00013%

CoalOther Solid Fuels

18%

2,000

3,000

4,000

mm

cfdHydro

1%

Total (2011) = 121 MToe

0

1,000

2011 2016 2021 2026 2031Gas41%

Oil28%

( )

Cambodia YTF Gulf of Martaban YTFOCA YTF MTJDA YTFGulf of Thailand YTF MTJDA UncontractedGulf of Martaban Uncontracted Gulf of Thailand UncontractedMTJDA Contracted Gulf of Martaban ContractedGulf of Thailand Contracted Total Demand

Strategy with substance© Wood Mackenzie 12

Source: Wood Mackenzie

Gulf of Thailand Contracted Total Demand

www.woodmac.com

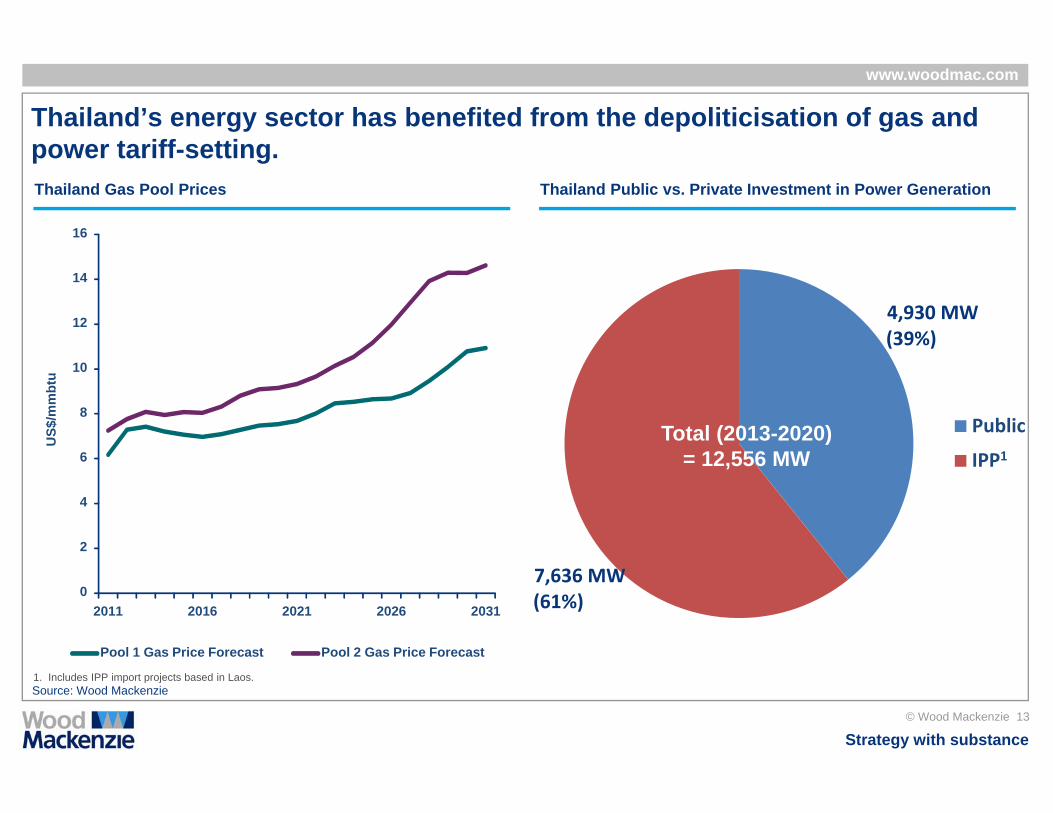

Thailand’s energy sector has benefited from the depoliticisation of gas and power tariff-settingpower tariff-setting. Thailand Gas Pool Prices Thailand Public vs. Private Investment in Power Generation

16

12

14

4,930 MW (39%)

6

8

10

US$

/mm

btu

Public

IPP1Total (2013-2020)

= 12 556 MW

2

4

6 IPP1= 12,556 MW

02011 2016 2021 2026 2031

Pool 1 Gas Price Forecast Pool 2 Gas Price Forecast

7,636 MW (61%)

Strategy with substance© Wood Mackenzie 13

Source: Wood Mackenzie1. Includes IPP import projects based in Laos.

www.woodmac.com

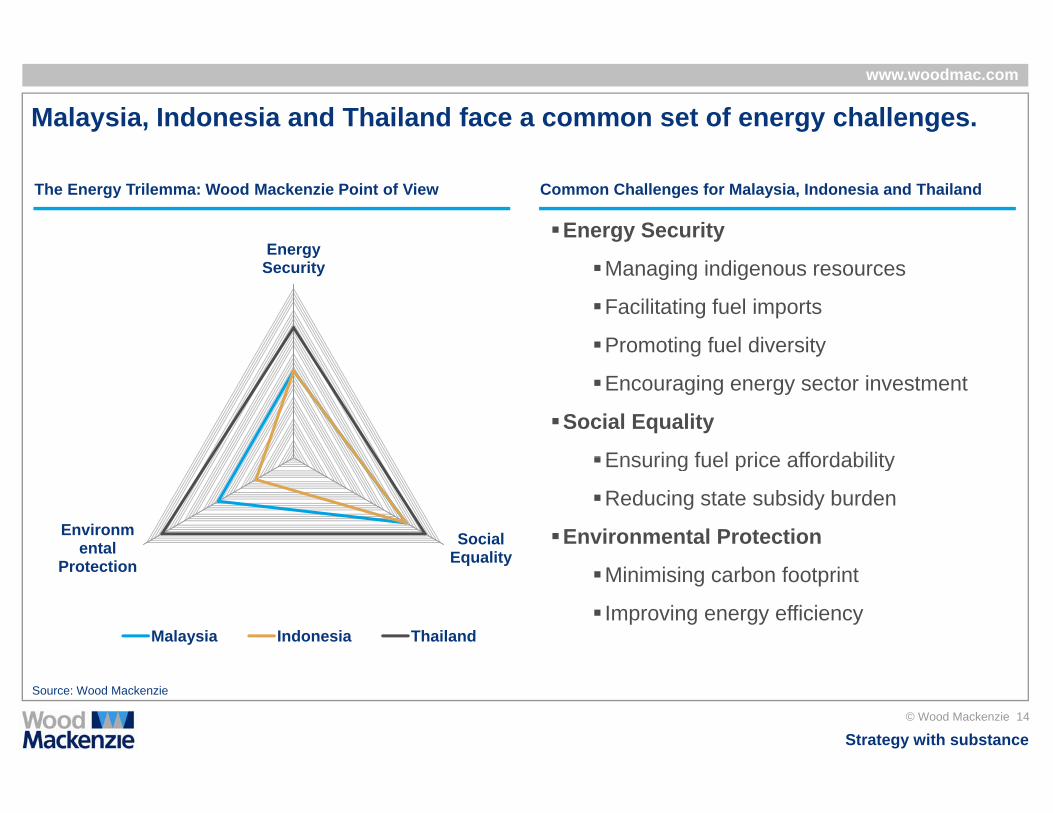

Malaysia, Indonesia and Thailand face a common set of energy challenges.

The Energy Trilemma: Wood Mackenzie Point of View

Energy

Common Challenges for Malaysia, Indonesia and Thailand

Energy SecurityEnergy

Security Managing indigenous resources

Facilitating fuel imports

Promoting fuel diversityg y

Encouraging energy sector investment

Social Equality

Ensuring fuel price affordability

Social Equality

Environmental

P i

Ensuring fuel price affordability

Reducing state subsidy burden

Environmental ProtectionEqualityProtection

Malaysia Indonesia Thailand

Minimising carbon footprint

Improving energy efficiency

Strategy with substance© Wood Mackenzie 14

Source: Wood Mackenzie

www.woodmac.com

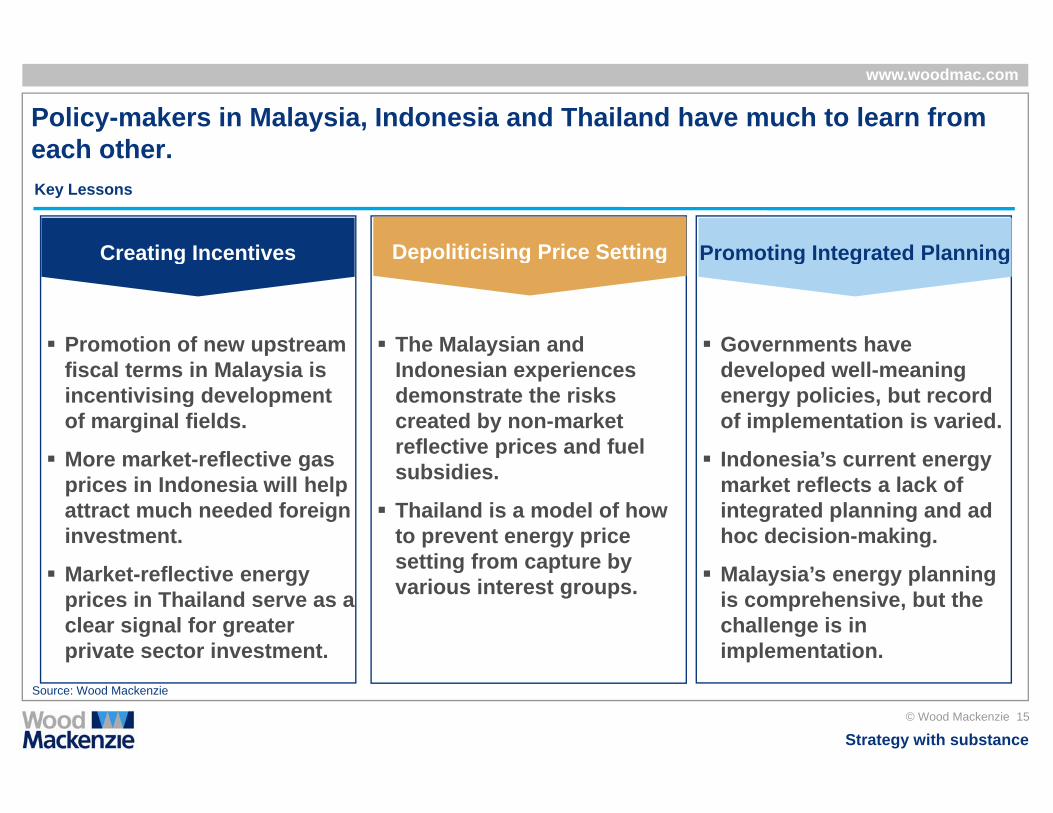

Policy-makers in Malaysia, Indonesia and Thailand have much to learn from each othereach other.Key Lessons

Creating Incentives Depoliticising Price Setting Promoting Integrated Planning

Promotion of new upstream The Malaysian and Governments have

Creating Incentives Depoliticising Price Setting Promoting Integrated Planning

pfiscal terms in Malaysia is incentivising development of marginal fields.

More market reflective gas

yIndonesian experiences demonstrate the risks created by non-market reflective prices and fuel

developed well-meaning energy policies, but record of implementation is varied.

Indonesia’s current energyMore market-reflective gas prices in Indonesia will help attract much needed foreign investment.

subsidies.

Thailand is a model of how to prevent energy price setting from capture by

Indonesia s current energy market reflects a lack of integrated planning and ad hoc decision-making.

Market-reflective energy prices in Thailand serve as a clear signal for greater private sector investment.

setting from capture by various interest groups. Malaysia’s energy planning

is comprehensive, but the challenge is in implementation.

Strategy with substance© Wood Mackenzie 15

Source: Wood Mackenzie

www.woodmac.com

Contacts

G CRajnish GoswamiHead of Gas & Power Consulting - Asia & Middle EastT: +65 6518 0829 E: rajnish goswami@woodmac com

Valery Chow Vice President - Gas & Power Consulting T: +65 6518 0854E: valery chow@woodmac com

Strategy with substance© Wood Mackenzie 16

www.woodmac.com

Global OfficesAustraliaBrazilCanadaChinaIndia

Global Contact DetailsEurope +44 (0)131 243 4400Americas +1 713 470 1600Asia Pacific +65 6518 0800Email [email protected] www woodmac com

IndonesiaJapanMalaysiaRussiaSingapore

South KoreaUnited Arab EmiratesUnited KingdomUnited States

IndiaWebsite www.woodmac.com Singapore

Wood Mackenzie is the most comprehensive source of knowledge about the world’s energy and metals industries. We analyse and advise on every stage along the value chain - from discovery to delivery, and beyond - to provide

Strategy with substance© Wood Mackenzie 17

y y g g y y yclients with the commercial insight that makes them stronger. For more information visit: www.woodmac.com