Embed Size (px)

Citation preview

SIERRA RUTILE LIMITEDWorking for a better Sierra Leone

Company PresentationJune 2011

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

DisclaimerForward-Looking InformationThis document may contain forward-looking statements. These forward-looking statements are made as of the date of this document and Sierra Rutile Limited (the “Company”) does not intend, and does not assume any obligation, to update these forward-looking statements, except as requiredunder applicable securities legislation.

Forward-looking statements relate to future events or future performance and reflect Company management’s expectations or beliefs regarding future events and include, but are not limited to, statements with respect to the estimation of mineral reserves and resources, the realization of mineral reserve estimates, the timing and amount of estimated future production, costs of production, capital expenditures, success of mining operations, environmental risks, unanticipated reclamation expenses, title disputes or claims and limitations on insurance coverage. In certain cases, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved” or the negative of these terms or comparable terminology. By their very nature forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward lookingstatements. Such factors include, among others, risks related to actual results of current exploration activities; changes in project parameters as plans continue to be refined; future prices of mineral resources; possible variations in ore reserves, grade or recovery rates; accidents, labour disputes and other risks of the mining industry; delays in obtaining governmental approvals or financing or in the completion of development or construction activities; as well as those factors detailed from time to time in the Company's interim and annual reports.

Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

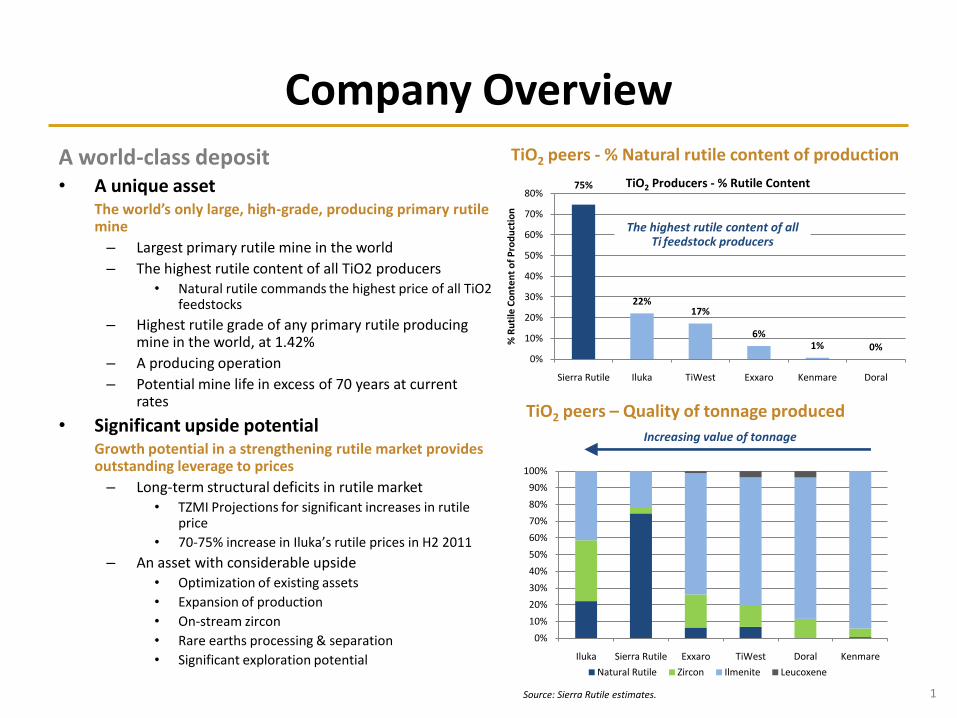

75%

22%17%

6%1% 0%

0%

10%

20%

30%

40%

50%

60%

70%

80%

Sierra Rutile Iluka TiWest Exxaro Kenmare Doral

% R

uti

le C

on

ten

t o

f P

rod

uct

ion

TiO2 Producers - % Rutile Content

Company Overview

TiO2 peers – Quality of tonnage produced

TiO2 peers - % Natural rutile content of production

Source: Sierra Rutile estimates.

A world-class deposit• A unique asset

The world’s only large, high-grade, producing primary rutilemine

– Largest primary rutile mine in the world

– The highest rutile content of all TiO2 producers• Natural rutile commands the highest price of all TiO2

feedstocks

– Highest rutile grade of any primary rutile producing mine in the world, at 1.42%

– A producing operation

– Potential mine life in excess of 70 years at current rates

• Significant upside potentialGrowth potential in a strengthening rutile market provides outstanding leverage to prices

– Long-term structural deficits in rutile market• TZMI Projections for significant increases in rutile

price

• 70-75% increase in Iluka’s rutile prices in H2 2011

– An asset with considerable upside• Optimization of existing assets

• Expansion of production

• On-stream zircon

• Rare earths processing & separation

• Significant exploration potential

1

Increasing value of tonnage

The highest rutile content of all Ti feedstock producers

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Iluka Sierra Rutile Exxaro TiWest Doral Kenmare

Natural Rutile Zircon Ilmenite Leucoxene

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

149 151 144

74 83 79 64 68

60.3 64.353.5

1416 17

15 1868

0

50

100

150

200

250

1992 1993 1994 2006 2007 2008 2009 2010

Pro

du

ctio

n (

'00

0 t

pa)

Rutile Ilmenite Zircon Average

Company Overview

SRL’s production history

Source: Sierra Rutile

An established mineral sands producer• Commenced mining in 1979

– Built and initially operated by global metals group, Bethlehem Steel

– Highly successful operations until civil war in 1995• Produced 30% of the world’s rutile before civil

war• Contributed 60% to Sierra Leone’s GDP

• Operations re-started in 2006– IPO on AIM in 2005– Under management at the time, growth strategy failed

• Target to increase production capacity to 200,000tpa

• D2– Ca. 100,000tpa of additional capacity– Commissioning and ramp-up delays– Eventual capsize

• D3– Construction plans shelved following D2 incident

• A wealth of experience in Sierra Leone– Sierra Leone well on the road to recovery

• A stable democracy• EU funding• Tony Blair “sponsorship”

– Long-standing relationships in government– Established mining law

• Deep mineral sands expertise– Decades of experience

• Many staff from pre-war times– Highly skilled workforce– >95% Sierra Leone nationals

Average pre-war production 208ktpa

Asset under-performance post-’06

D1 and floating wet plant working at Lanti

2

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

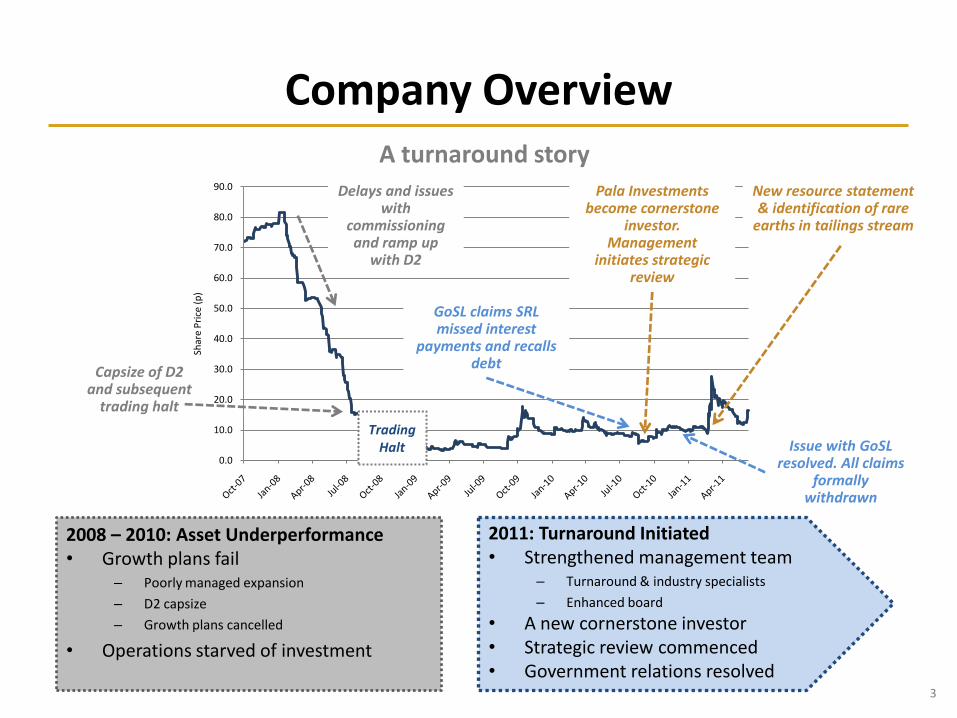

Capsize of D2 and subsequent

trading halt

0.0

10.0

20.0

30.0

40.0

50.0

60.0

70.0

80.0

90.0Sh

are

Pri

ce (

p)

GoSL claims SRL missed interest

payments and recalls debt

Company Overview

Pala Investments become cornerstone

investor. Management

initiates strategic review

New resource statement & identification of rare

earths in tailings stream

A turnaround story

Delays and issues with

commissioning and ramp up

with D2

2011: Turnaround Initiated• Strengthened management team

– Turnaround & industry specialists

– Enhanced board

• A new cornerstone investor• Strategic review commenced• Government relations resolved

2008 – 2010: Asset Underperformance• Growth plans fail

– Poorly managed expansion

– D2 capsize

– Growth plans cancelled

• Operations starved of investment

3

Issue with GoSLresolved. All claims

formally withdrawn

Trading Halt

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

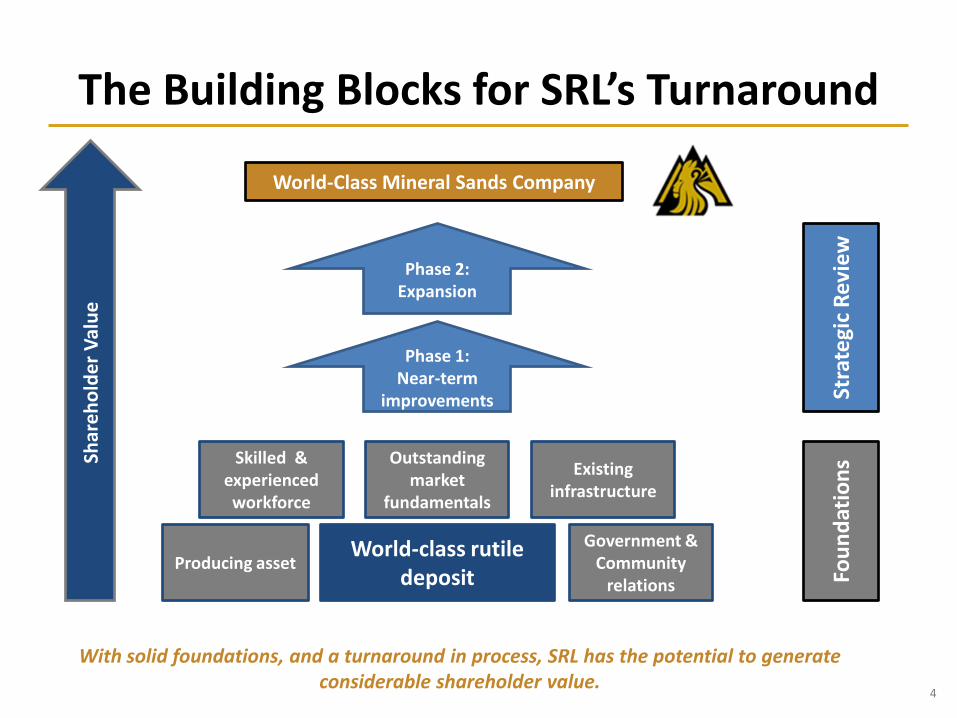

The Building Blocks for SRL’s Turnaround

Producing asset

Shar

eh

old

er

Val

ue

Skilled & experienced workforce

Phase 1:Near-term

improvements

With solid foundations, and a turnaround in process, SRL has the potential to generate considerable shareholder value.

Outstanding market

fundamentals

World-class rutiledeposit

Government & Community

relations

Existing infrastructure

Phase 2:Expansion

Stra

tegi

c R

evi

ew

Fou

nd

atio

ns

World-Class Mineral Sands Company

4

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

A World-Class Deposit

The largest primary rutile mine in the world

• JORC Mineral Resource in excess of 600 million tonnes at 0.8% rutile cut-off grade*

• Measured and indicated resource of 441 million tonnes

– High grade of natural rutile at 1.42%

• A potential mine life of over 70 years at current digging rates

• Fully licensed and permitted

*Mineral Resources include those resources which have been modified to produce the Ore Reserves. The figures reported represent 100% of the Mineral Resources and Ore Reserves attributable to Sierra Rutile Limited.

**Insufficient historical data was available to provide a JORC-compliant inferred heavy mineral, ilmenite and zircon grade estimate

Significant opportunity to expand resource

• 60,000 ha of land licensed for mining

– Only 10,000 ha has been explored

– Further exploration campaign commenced

SRL’s deposit is large, long life, and its assemblage dominated by high-value, high-grade rutile.

63% of payable heavy mineral is high-value rutile,

ca. 88% by value

Tonnes Grade (%) Contained Tonnes (kt)

Classification Millions HM Rut Ilm Zir HM Rut Ilm Zir

Measured 4.4 2.30 1.13 0.42 0.18 102 50 19 8

Indicated 436.6 6.18 1.42 0.74 0.32 26,992 6,204 3,242 1,377

Measured & Indicated 441.0 6.14 1.42 0.74 0.31 27,094 6,254 3,261 1,385

Inferred** 163.9 - 0.96 - - 1,575 - -

Total Measured, Indicated

& Inferred604.9 27,094 7,829 3,261 1,385

5

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

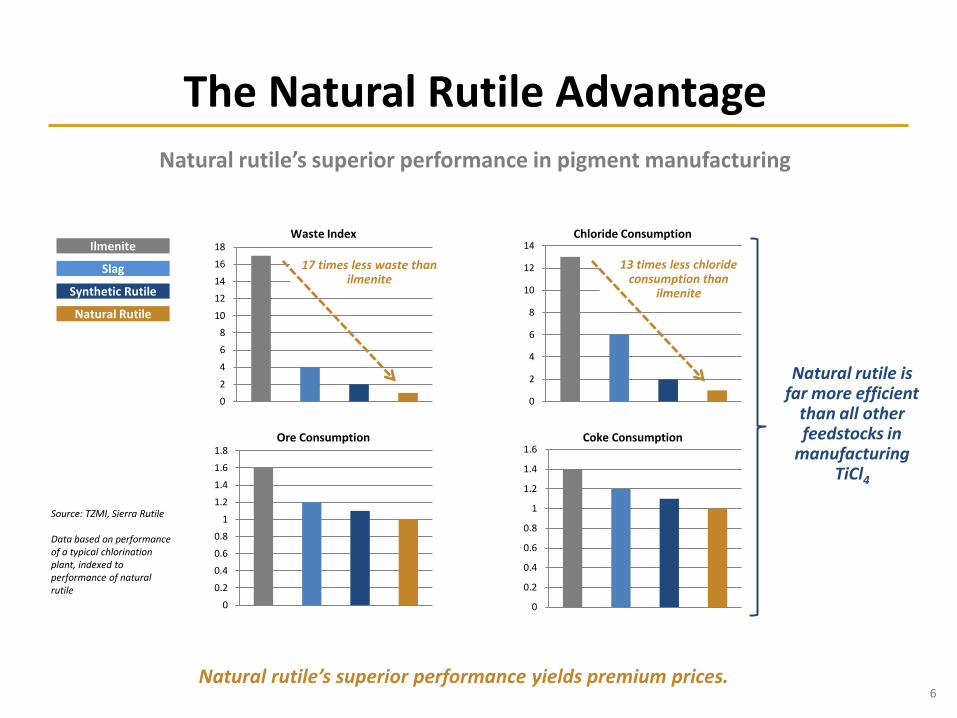

The Natural Rutile Advantage

Source: TZMI, Sierra Rutile

Data based on performance of a typical chlorination plant, indexed to performance of natural rutile

Natural rutile’s superior performance in pigment manufacturing

Natural rutile’s superior performance yields premium prices.

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8Ore Consumption

0

2

4

6

8

10

12

14Chloride Consumption

0

2

4

6

8

10

12

14

16

18Waste Index

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6Coke Consumption

Synthetic Rutile

Ilmenite

Slag

Natural Rutile

17 times less waste than ilmenite

13 times less chloride consumption than

ilmenite

Natural rutile is far more efficient

than all other feedstocks in

manufacturing TiCl4

6

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

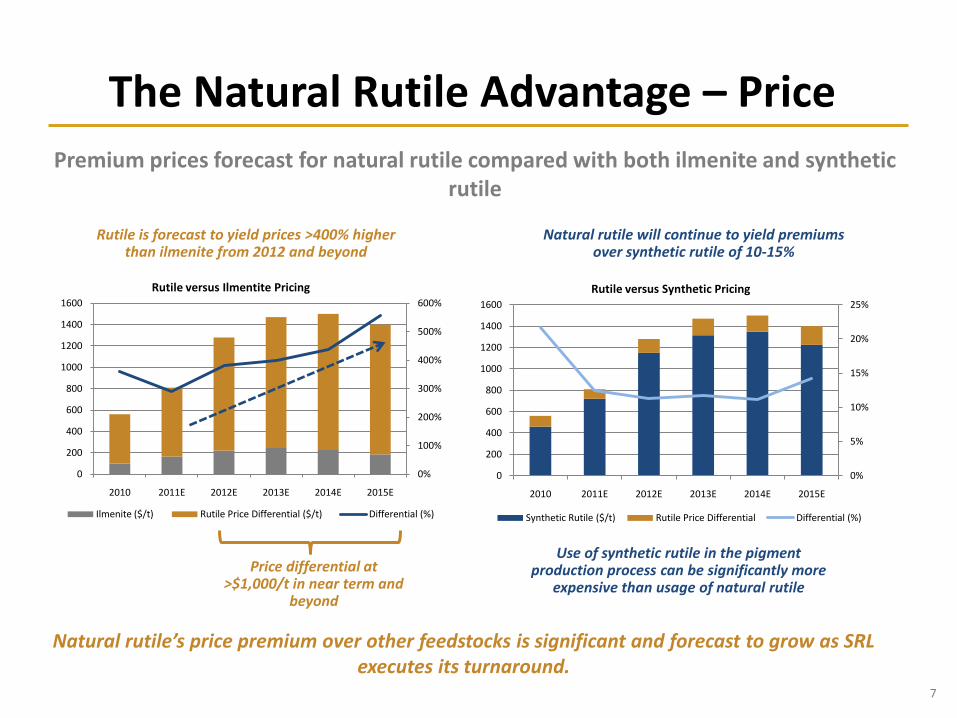

The Natural Rutile Advantage – Price

Price differential at >$1,000/t in near term and

beyond

0%

100%

200%

300%

400%

500%

600%

0

200

400

600

800

1000

1200

1400

1600

2010 2011E 2012E 2013E 2014E 2015E

Rutile versus Ilmentite Pricing

Ilmenite ($/t) Rutile Price Differential ($/t) Differential (%)

Rutile is forecast to yield prices >400% higher than ilmenite from 2012 and beyond

Premium prices forecast for natural rutile compared with both ilmenite and synthetic rutile

Natural rutile’s price premium over other feedstocks is significant and forecast to grow as SRL executes its turnaround.

Natural rutile will continue to yield premiums over synthetic rutile of 10-15%

0%

5%

10%

15%

20%

25%

0

200

400

600

800

1000

1200

1400

1600

2010 2011E 2012E 2013E 2014E 2015E

Rutile versus Synthetic Pricing

Synthetic Rutile ($/t) Rutile Price Differential Differential (%)

7

Use of synthetic rutile in the pigment production process can be significantly more

expensive than usage of natural rutile

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

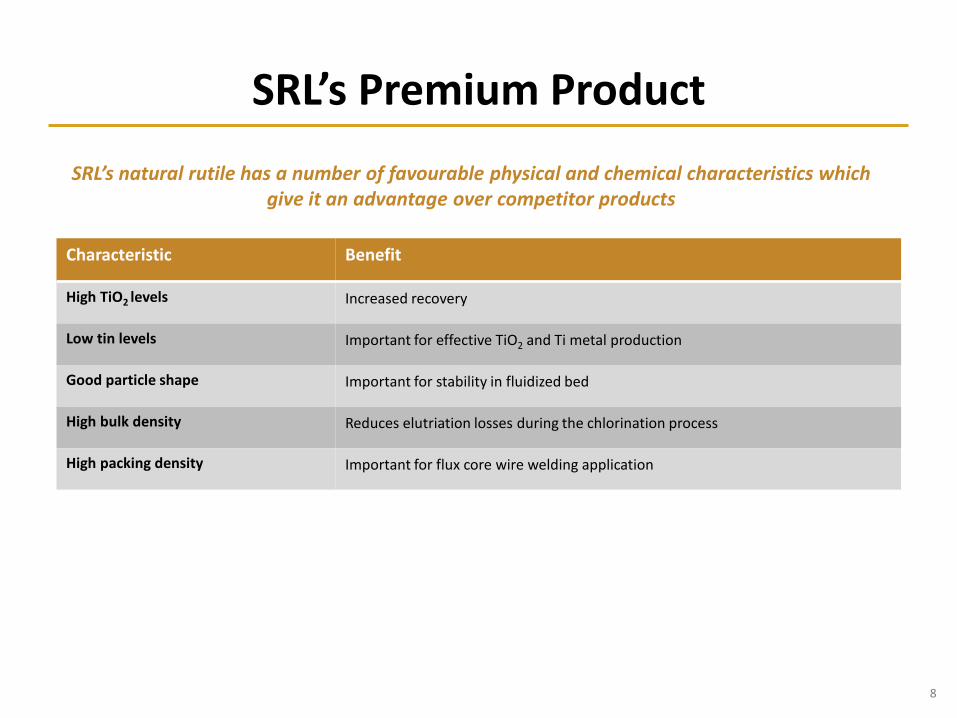

SRL’s Premium Product

Characteristic Benefit

High TiO2 levels Increased recovery

Low tin levels Important for effective TiO2 and Ti metal production

Good particle shape Important for stability in fluidized bed

High bulk density Reduces elutriation losses during the chlorination process

High packing density Important for flux core wire welding application

SRL’s natural rutile has a number of favourable physical and chemical characteristics which give it an advantage over competitor products

8

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Freetown

Sierra Leone

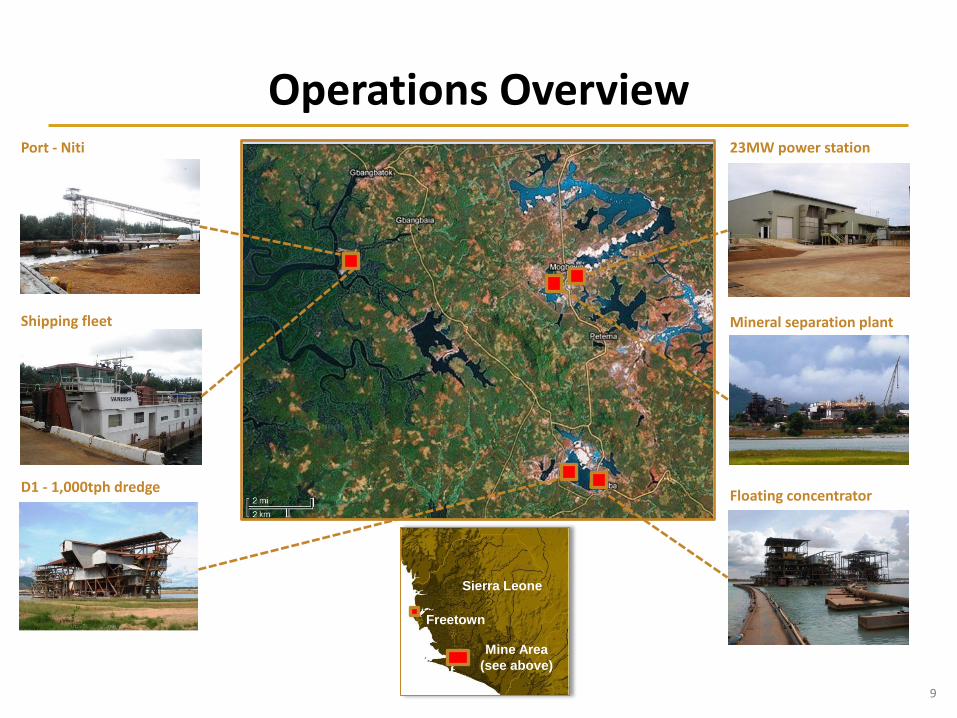

Operations OverviewPort - Niti

Shipping fleet

D1 - 1,000tph dredge Floating concentrator

Mineral separation plant

23MW power station

Mine Area

(see above)

9

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

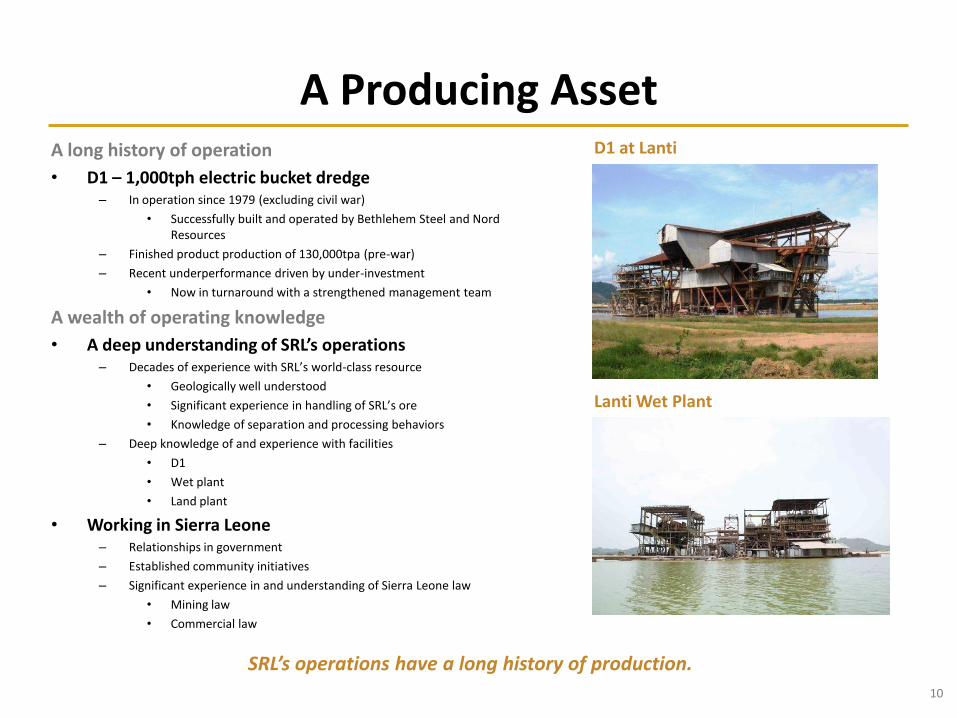

A Producing AssetA long history of operation

• D1 – 1,000tph electric bucket dredge– In operation since 1979 (excluding civil war)

• Successfully built and operated by Bethlehem Steel and Nord Resources

– Finished product production of 130,000tpa (pre-war)

– Recent underperformance driven by under-investment

• Now in turnaround with a strengthened management team

A wealth of operating knowledge

• A deep understanding of SRL’s operations– Decades of experience with SRL’s world-class resource

• Geologically well understood

• Significant experience in handling of SRL’s ore

• Knowledge of separation and processing behaviors

– Deep knowledge of and experience with facilities

• D1

• Wet plant

• Land plant

• Working in Sierra Leone– Relationships in government

– Established community initiatives

– Significant experience in and understanding of Sierra Leone law

• Mining law

• Commercial law

– Delays

D1 at Lanti

SRL’s operations have a long history of production.

10

Lanti Wet Plant

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

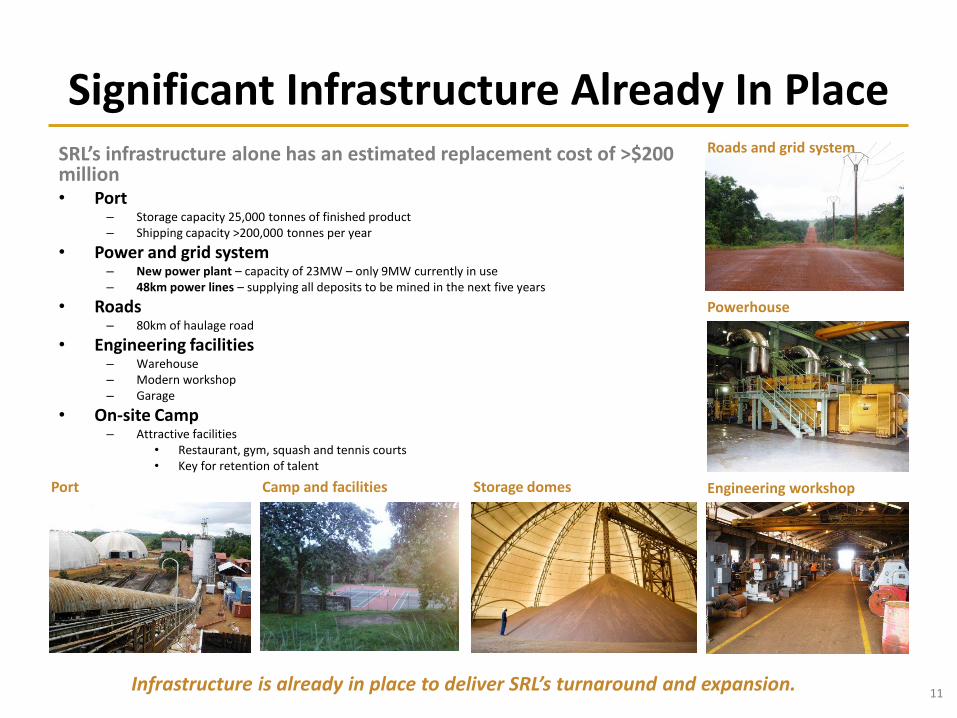

Significant Infrastructure Already In PlaceSRL’s infrastructure alone has an estimated replacement cost of >$200 million• Port

– Storage capacity 25,000 tonnes of finished product – Shipping capacity >200,000 tonnes per year

• Power and grid system– New power plant – capacity of 23MW – only 9MW currently in use– 48km power lines – supplying all deposits to be mined in the next five years

• Roads– 80km of haulage road

• Engineering facilities– Warehouse– Modern workshop– Garage

• On-site Camp – Attractive facilities

• Restaurant, gym, squash and tennis courts• Key for retention of talent

Engineering workshop

Powerhouse

Port

Roads and grid system

Camp and facilities

Infrastructure is already in place to deliver SRL’s turnaround and expansion.

Storage domes

11

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Focus on retaining and growing talent

• >95% Sierra Leonean nationals– Excellent retention rates

– A champion for Sierra Leone

• Regular training

• Programs– Fast track

– Apprenticeship

• Technical Institute

• Attractive facilities – Expats and senior management can live on-site

Highly-skilled workforce

• Decades of experience in mineral sands– Many employees from pre-war times

• Highly educated– >100 staff with university education

– Significant recruitment from premier universities of Sierra Leone, Fourah and Njala

• Focused management team– Strengthened management

– Specialists recruited for turnaround:

• Operations

• Strategy

• Risk management

Skilled & Experienced Workforce

Mining MetallurgyProcessing Lab

An existing workforce with deep mineral sands industry expertise.

12

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

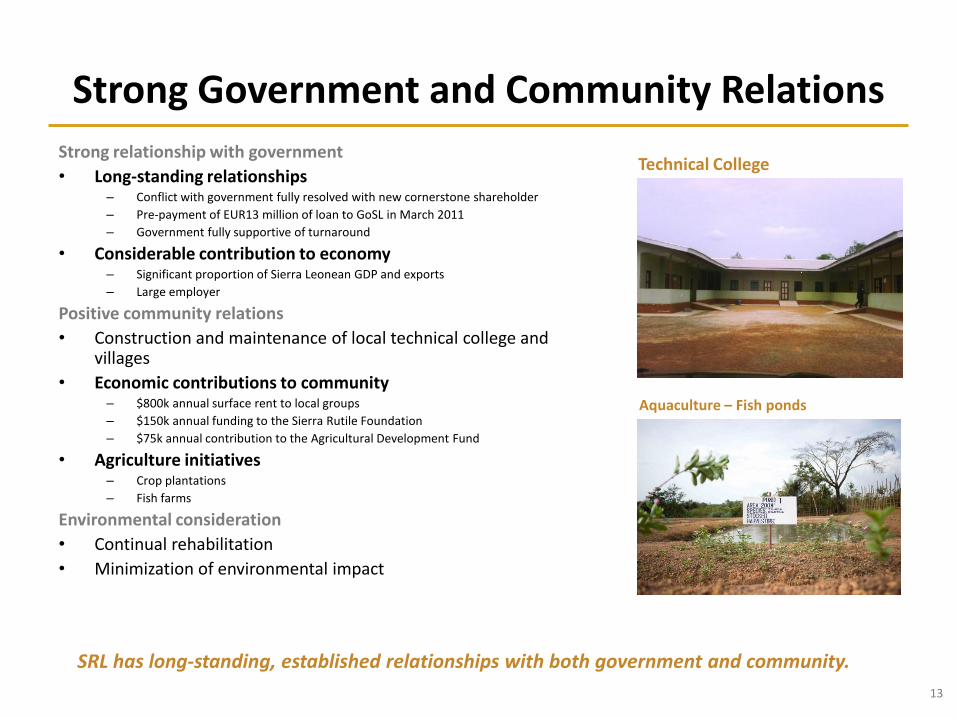

Strong Government and Community Relations

Technical College

Aquaculture – Fish ponds

Strong relationship with government

• Long-standing relationships– Conflict with government fully resolved with new cornerstone shareholder

– Pre-payment of EUR13 million of loan to GoSL in March 2011

– Government fully supportive of turnaround

• Considerable contribution to economy– Significant proportion of Sierra Leonean GDP and exports

– Large employer

Positive community relations

• Construction and maintenance of local technical college and villages

• Economic contributions to community– $800k annual surface rent to local groups

– $150k annual funding to the Sierra Rutile Foundation

– $75k annual contribution to the Agricultural Development Fund

• Agriculture initiatives– Crop plantations

– Fish farms

Environmental consideration

• Continual rehabilitation

• Minimization of environmental impact

SRL has long-standing, established relationships with both government and community.

13

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

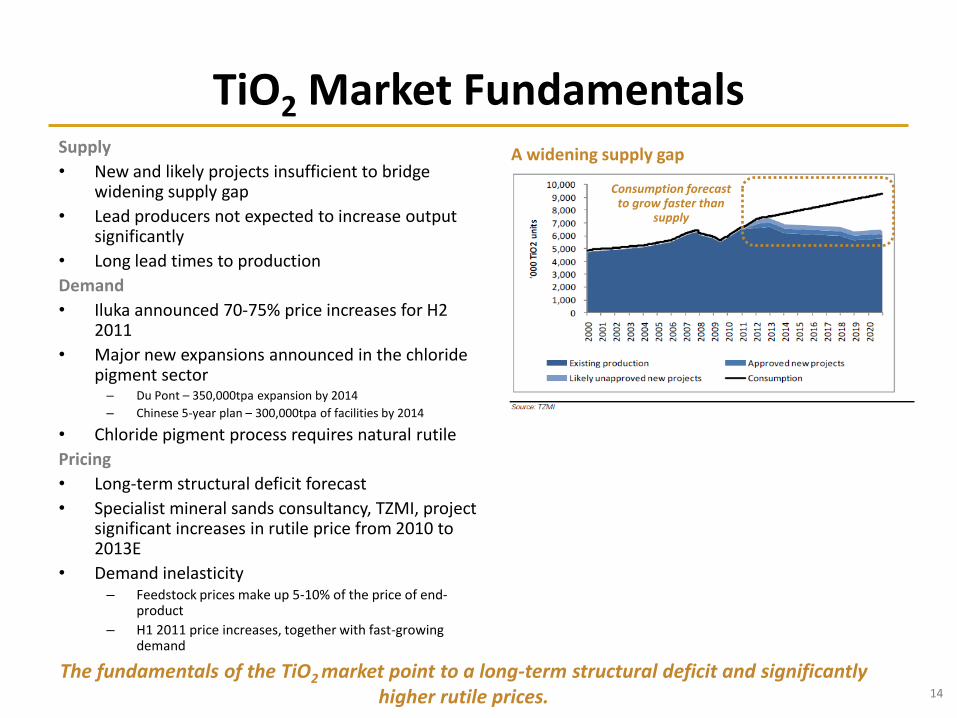

TiO2 Market FundamentalsA widening supply gap

Consumption forecast to grow faster than

supply

Supply

• New and likely projects insufficient to bridge widening supply gap

• Lead producers not expected to increase output significantly

• Long lead times to production

Demand

• Iluka announced 70-75% price increases for H2 2011

• Major new expansions announced in the chloride pigment sector

– Du Pont – 350,000tpa expansion by 2014

– Chinese 5-year plan – 300,000tpa of facilities by 2014

• Chloride pigment process requires natural rutile

Pricing

• Long-term structural deficit forecast

• Specialist mineral sands consultancy, TZMI, project significant increases in rutile price from 2010 to 2013E

• Demand inelasticity– Feedstock prices make up 5-10% of the price of end-

product

– H1 2011 price increases, together with fast-growing demand

The fundamentals of the TiO2 market point to a long-term structural deficit and significantly higher rutile prices. 14

SIERRA RUTILE LIMITED

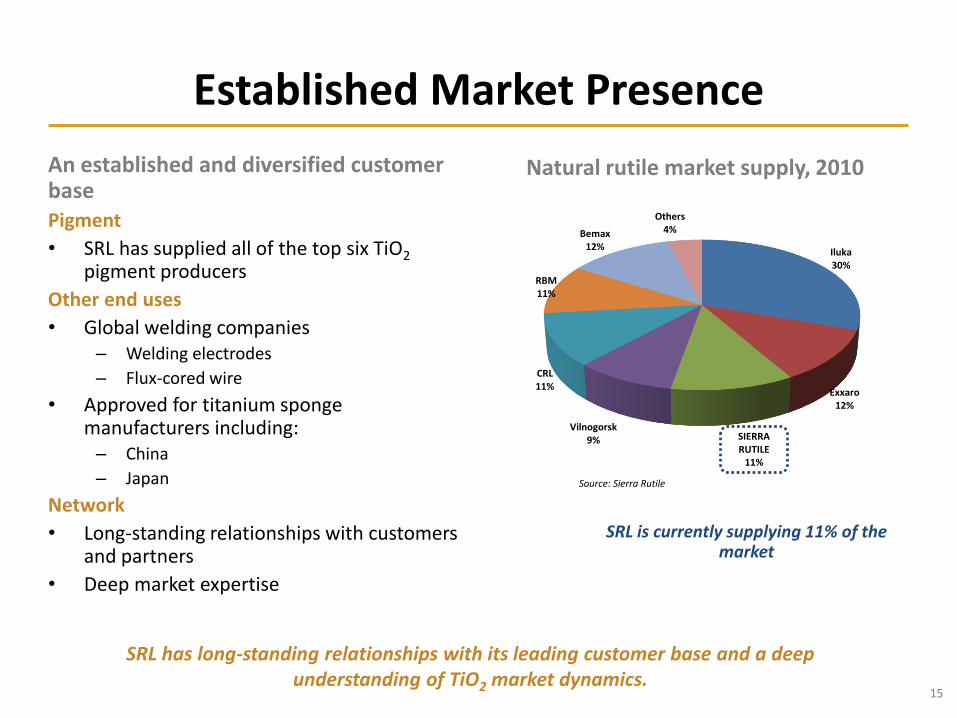

Working for a better Sierra Leone

Established Market Presence

Iluka30%

Exxaro12%

SIERRA RUTILE

11%

Vilnogorsk9%

CRL11%

RBM11%

Bemax12%

Others4%

Natural rutile market supply, 2010

Source: Sierra Rutile

An established and diversified customer basePigment

• SRL has supplied all of the top six TiO2

pigment producers

Other end uses

• Global welding companies – Welding electrodes

– Flux-cored wire

• Approved for titanium sponge manufacturers including:– China

– Japan

Network

• Long-standing relationships with customers and partners

• Deep market expertise

SRL has long-standing relationships with its leading customer base and a deep understanding of TiO2 market dynamics.

SRL is currently supplying 11% of the market

15

SIERRA RUTILE LIMITEDWorking for a better Sierra Leone

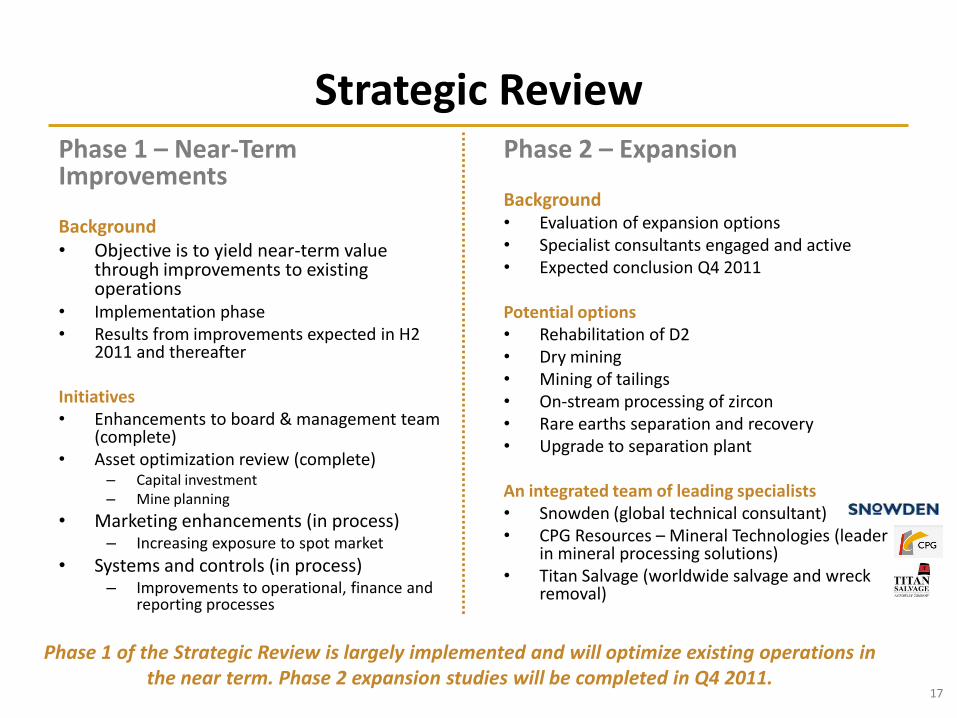

Strategic Review

The Turnaround of Sierra Rutile

16

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Strategic ReviewPhase 1 – Near-Term Improvements

Background• Objective is to yield near-term value

through improvements to existing operations

• Implementation phase• Results from improvements expected in H2

2011 and thereafter

Initiatives• Enhancements to board & management team

(complete)• Asset optimization review (complete)

– Capital investment– Mine planning

• Marketing enhancements (in process)– Increasing exposure to spot market

• Systems and controls (in process)– Improvements to operational, finance and

reporting processes

Phase 2 – Expansion

Background• Evaluation of expansion options• Specialist consultants engaged and active• Expected conclusion Q4 2011

Potential options• Rehabilitation of D2• Dry mining• Mining of tailings• On-stream processing of zircon• Rare earths separation and recovery• Upgrade to separation plant

An integrated team of leading specialists • Snowden (global technical consultant)• CPG Resources – Mineral Technologies (leader

in mineral processing solutions)• Titan Salvage (worldwide salvage and wreck

removal)

Phase 1 of the Strategic Review is largely implemented and will optimize existing operations in the near term. Phase 2 expansion studies will be completed in Q4 2011.

17

SIERRA RUTILE LIMITEDWorking for a better Sierra Leone

Phase 1

Near-Term Improvements

18

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Phase 1: Leadership & Management

A Strengthened BoardAdditions:

• Jan Castro, Non-Executive Chairman– Chief Executive, Pala Investments AG, an investment company

focused on the mining sector, and SRL’s cornerstone shareholder

– Significant strategic advisory, management and investment experience

– Serves on the boards of a number of mining and metals companies

• Charles Entrekin, Non-Executive– 35 years of experience in the mining sector– As former President of Titanium Metals Corporation, brings

significant industry specialism– Turnaround expertise

• Michael Brown, Non-Executive– Former Chief Operating Officer of South African mining

operation of the De Beers Group– Deep industry expertise in strategy, operations, construction– Led restructuring of De Beers during GFC– Now Senior Vice President at Pala Investments AG

• Michael Barton, Non-Executive– Senior Vice President at Pala Investments AG– Significant strategy and transaction advisory experience

Retentions:

• John Bonoh Sisay, CEO – Considerable experience in African mining sector, having worked in

10 African countries– Formerly De Beers, America Mineral Fields (now First Quantum)– Previously President of Chamber of Mines, Sierra Leone– Sierra Leone national

• Alex Kamara, Non-Executive– Head of Engineering at SRL from 1982-1995– Deep understanding of SRL’s operations– Chairman of Standard Chartered, Sierra Leone– Sierra Leone national

• Francois Colette, Non-Executive– 25 years of African mining experience– Formerly of Gécamines and AMFI-Adastra– Led copper, cobalt and zinc projects, including Kolwezi Tailings

Board on site

SRL’s board has been strengthened in order to deliver SRL’s turnaround.

19

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Phase 1: Leadership & Management

A New Focus on Turnaround & GrowthA New, Supportive Cornerstone Shareholder

• Pala Investments (38.2%) brings deep industry expertise

• A partner focused on value generation

Incentives

• Board and senior management share option plan closely aligns interests with shareholders

• New KPI-based bonus plan for staff

An Enhanced Senior Management Team

• Andrew Taylor, COO– 20 years of mining and processing expertise– Significant experience of operating in Africa with De Beers and

Anglo American– Managed the construction and commissioning of the Voorspoed

Mine in South Africa from 2005 to 2010

• Desmond Williams, Operations Manager– 10 years experience with SNC Lavelin and Worley Parsons– 10 years with pre-war Sierra Rutile– Senior management positions on numerous international projects,

including Bald Mountain Gold (Barrick) and Kabanga Nickel

• Joseph Connolly, CFO– Previously Director, Business Development at Clipper WindPower– Brings significant expertise in financial management, strategy,

business risk and corporate governance

• Sahr Wonday, Director of Strategic Projects– 32 years at SRL– Significant experience in operational enhancement

• Mark Button, Director of Resource Development– 22 years experience of working in Africa in a variety of mining and

geological roles– Formerly of Anglo American and Gold Fields

• Jean Lindberg Charles, Director of Corporate Controls– Formerly Ernst & Young and financial controller of Le Meridien– SRL Group Financial Controller 2005-2008

• Neil Gawthorpe, Marketing Director– 15 years experience in international industrial minerals marketing – Previous technical and marketing positions at Redland PLC, Frank &

Schulte GmbH and Minelco Group

A senior management team with the right experience, knowledge and skills to execute the turnaround of SRL.

20

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

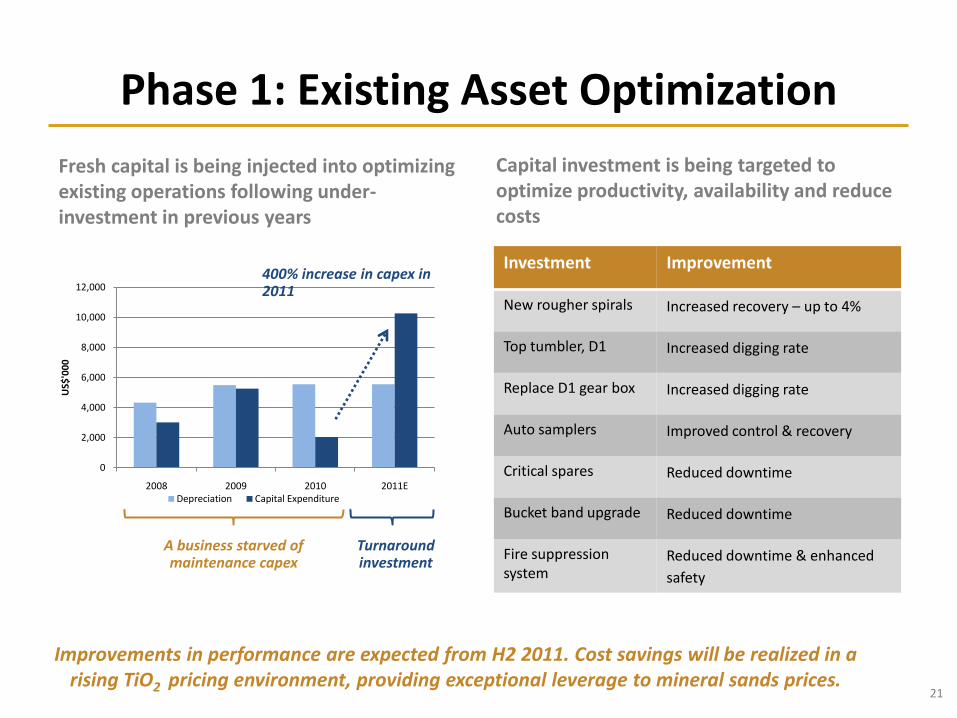

Phase 1: Existing Asset Optimization

Investment Improvement

New rougher spirals Increased recovery – up to 4%

Top tumbler, D1 Increased digging rate

Replace D1 gear box Increased digging rate

Auto samplers Improved control & recovery

Critical spares Reduced downtime

Bucket band upgrade Reduced downtime

Fire suppression system

Reduced downtime & enhanced

safety

Capital investment is being targeted to optimize productivity, availability and reduce costs

0

2,000

4,000

6,000

8,000

10,000

12,000

2008 2009 2010 2011E

US$

'00

0

Depreciation Capital Expenditure

Fresh capital is being injected into optimizing existing operations following under-investment in previous years

A business starved of maintenance capex

400% increase in capex in 2011

Improvements in performance are expected from H2 2011. Cost savings will be realized in a rising TiO2 pricing environment, providing exceptional leverage to mineral sands prices.

Turnaround investment

21

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

98%92%

84%

38%

2%8%

16%

46%

16%

100%

0

200

400

600

800

1000

1200

1400

1600

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

2008 2009 2010 2011 2012

Spo

t R

uti

le P

rice

(TZ

MI)

($

/t)

% o

f P

rod

uct

ion

Cap and Collar Fixed Uncontracted Rutile Price

Phase 1: Price Strategy

2012 production is currently un-contracted, providing full leverage to increasing prices

SRL has ceased trading under cap and collar arrangements to maximize exposure to rising prices

Sales contracts are being optimized to enhance leverage to increasing mineral sands prices and capitalize on SRL’s premium product.

With its premium product, SRL is aiming to become a price leader in the rutile market

• No more long term contracts

• No more cap and collar arrangements

• End of 2010 carryover in 2011

• Full leverage to spot market

22

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

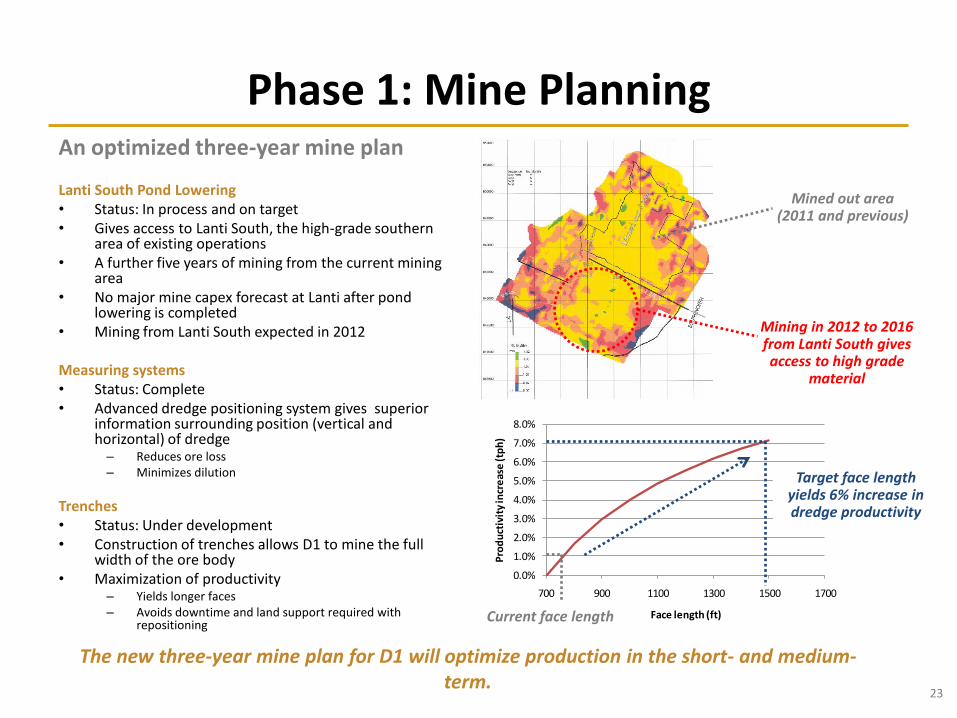

Phase 1: Mine Planning

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

700 900 1100 1300 1500 1700

Pro

du

ctiv

ity

incr

eas

e (t

ph

)

Face length (ft)

Mining in 2012 to 2016 from Lanti South gives access to high grade

material

Current face length

Target face length yields 6% increase in dredge productivity

An optimized three-year mine plan

Lanti South Pond Lowering• Status: In process and on target• Gives access to Lanti South, the high-grade southern

area of existing operations• A further five years of mining from the current mining

area• No major mine capex forecast at Lanti after pond

lowering is completed• Mining from Lanti South expected in 2012

Measuring systems• Status: Complete• Advanced dredge positioning system gives superior

information surrounding position (vertical and horizontal) of dredge

– Reduces ore loss– Minimizes dilution

Trenches• Status: Under development• Construction of trenches allows D1 to mine the full

width of the ore body• Maximization of productivity

– Yields longer faces – Avoids downtime and land support required with

repositioning

The new three-year mine plan for D1 will optimize production in the short- and medium-term.

Mined out area (2011 and previous)

23

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Phase 1: Systems & ControlsKey systems & controls improvements

ERP system• System upgrade

Mine planning• Enhanced planning process• New dredge positioning system (DPS)

Procurement process• Reduction in lead time• Consolidation in suppliers• Improved customs clearance & frequency of shipping

Inventory systems• Implementation of max/min ordering system• Strengthening of warehouse security

Fuel control• Installation of new flow meters• Leakage reduction program

Lines of responsibility strengthened• Performance owned by heads of department• Capital approval controls enhanced

Fuel flow meters installation

DPS calibration

Enhancements made to SRL’s systems & controls have been designed to optimize operational efficiency and to effectively manage risk.

24

SIERRA RUTILE LIMITEDWorking for a better Sierra Leone

Phase 2Expansion

25

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

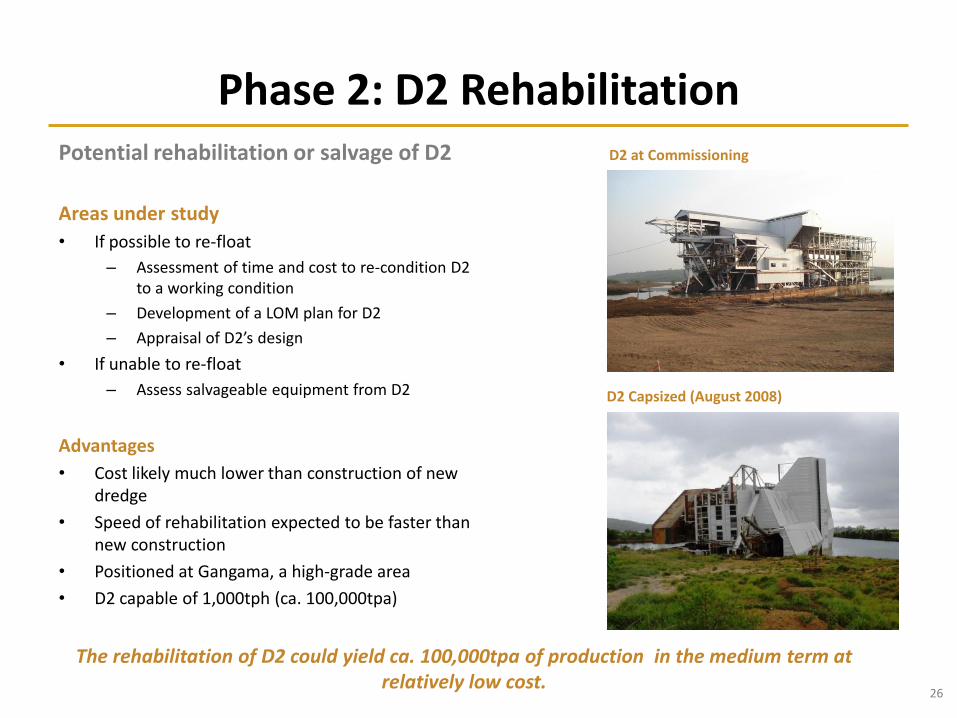

Potential rehabilitation or salvage of D2

Areas under study

• If possible to re-float

– Assessment of time and cost to re-condition D2 to a working condition

– Development of a LOM plan for D2

– Appraisal of D2’s design

• If unable to re-float

– Assess salvageable equipment from D2

Advantages

• Cost likely much lower than construction of new dredge

• Speed of rehabilitation expected to be faster than new construction

• Positioned at Gangama, a high-grade area

• D2 capable of 1,000tph (ca. 100,000tpa)

Phase 2: D2 Rehabilitation

D2 Capsized (August 2008)

D2 at Commissioning

The rehabilitation of D2 could yield ca. 100,000tpa of production in the medium term at relatively low cost.

26

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

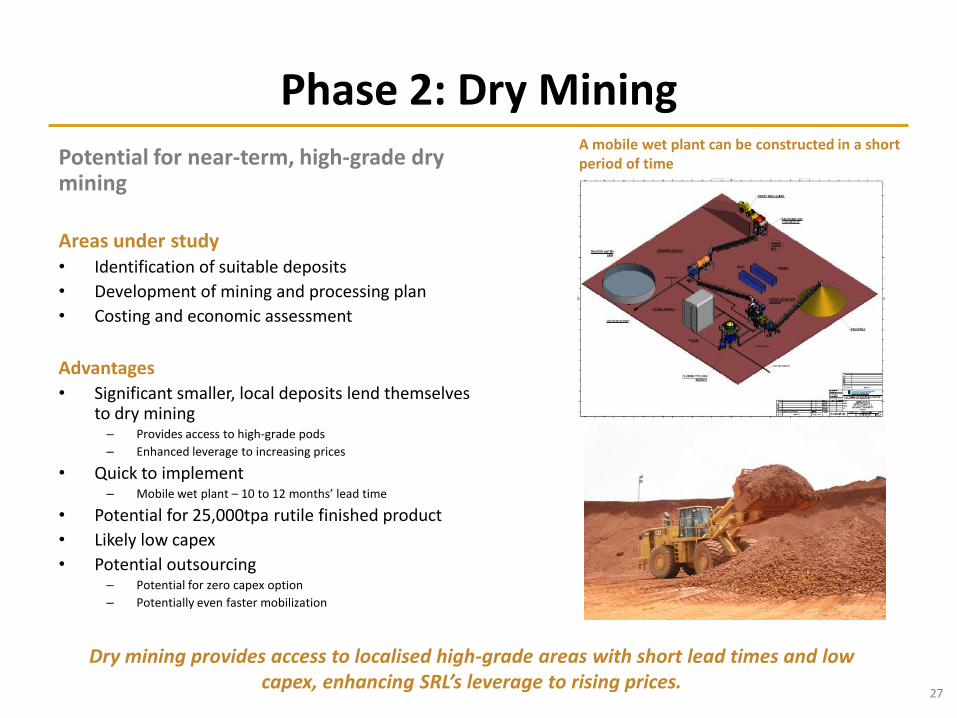

Potential for near-term, high-grade dry mining

Areas under study• Identification of suitable deposits

• Development of mining and processing plan

• Costing and economic assessment

Advantages• Significant smaller, local deposits lend themselves

to dry mining– Provides access to high-grade pods

– Enhanced leverage to increasing prices

• Quick to implement– Mobile wet plant – 10 to 12 months’ lead time

• Potential for 25,000tpa rutile finished product

• Likely low capex

• Potential outsourcing– Potential for zero capex option

– Potentially even faster mobilization

Phase 2: Dry MiningA mobile wet plant can be constructed in a short period of time

Dry mining provides access to localised high-grade areas with short lead times and low capex, enhancing SRL’s leverage to rising prices.

27

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

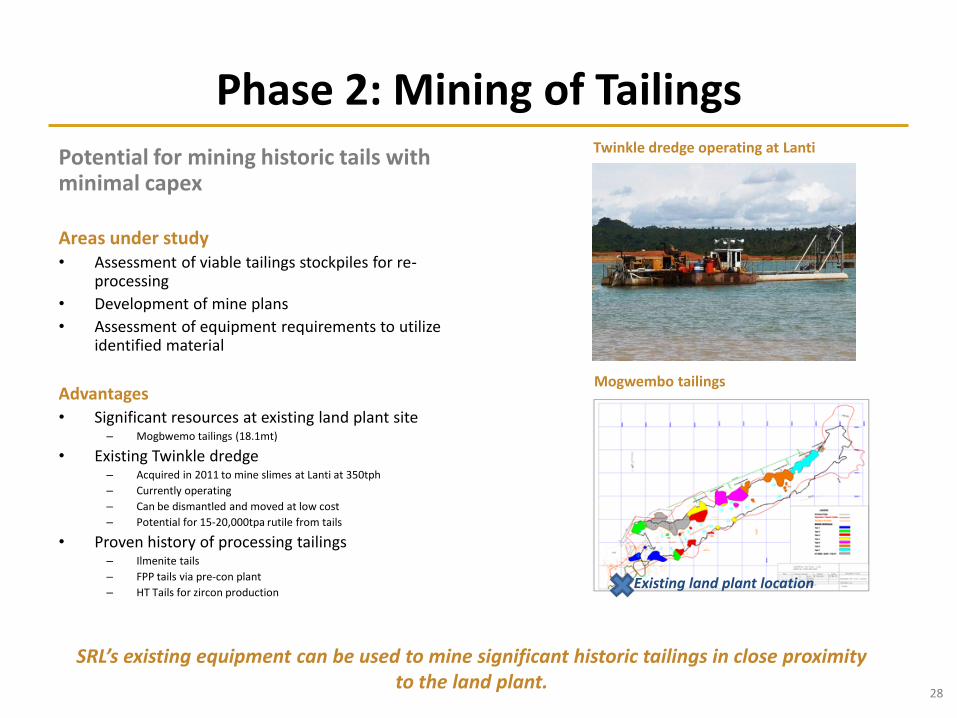

Phase 2: Mining of TailingsTwinkle dredge operating at Lanti

Mogwembo tailings

Potential for mining historic tails with minimal capex

Areas under study• Assessment of viable tailings stockpiles for re-

processing

• Development of mine plans

• Assessment of equipment requirements to utilize identified material

Advantages• Significant resources at existing land plant site

– Mogbwemo tailings (18.1mt)

• Existing Twinkle dredge– Acquired in 2011 to mine slimes at Lanti at 350tph

– Currently operating

– Can be dismantled and moved at low cost

– Potential for 15-20,000tpa rutile from tails

• Proven history of processing tailings– Ilmenite tails

– FPP tails via pre-con plant

– HT Tails for zircon productionExisting land plant location

SRL’s existing equipment can be used to mine significant historic tailings in close proximity to the land plant.

28

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

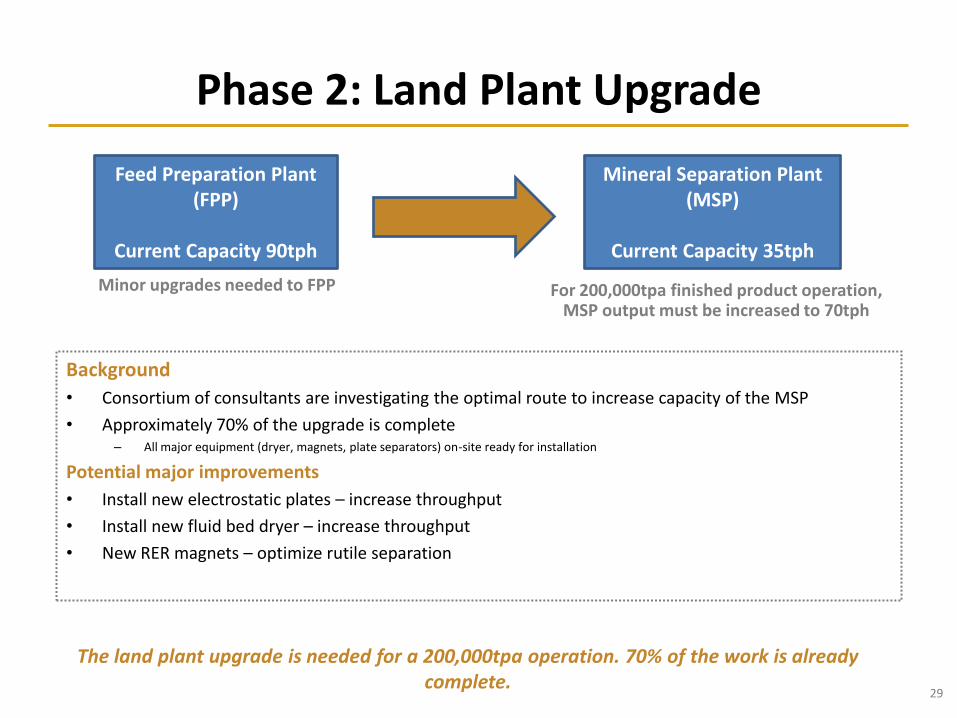

Phase 2: Land Plant Upgrade

Feed Preparation Plant (FPP)

Current Capacity 90tph

Mineral Separation Plant (MSP)

Current Capacity 35tph

Minor upgrades needed to FPP For 200,000tpa finished product operation, MSP output must be increased to 70tph

Background

• Consortium of consultants are investigating the optimal route to increase capacity of the MSP

• Approximately 70% of the upgrade is complete– All major equipment (dryer, magnets, plate separators) on-site ready for installation

Potential major improvements

• Install new electrostatic plates – increase throughput

• Install new fluid bed dryer – increase throughput

• New RER magnets – optimize rutile separation

The land plant upgrade is needed for a 200,000tpa operation. 70% of the work is already complete.

29

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

Phase 2: On-Stream Zircon Processing

Zircon in SRL high tension tailingsPotential for on-stream zircon processing and premium concentrate product

Background• Zircon currently produced in a batch process

– Re-processing of high-tension tails

• As land plant production ramps up, batch processing will no longer be possible

• Construction of a zircon upgrade circuit adjacent to the mineral separation plant

Advantages• On-stream processing with new equipment is likely to yield

a higher grade of zircon product– Current batch process yields product 43% ZrO2 (60% Zr eq.)

• At current production rates, on-stream zircon processing would yield ca. 9,000tpa product at 43% ZrO2

– With growth in mining rates, this could be considerably higher

• Potential to sell a premium 66% ZrO2 product– Assessment being made by CPG

• SRL will sell its zircon at spot, less treatment charges– Providing leverage to rising zircon prices

• Rare earths benefit– On-stream processing of zircon should provide a further-refined rare

earths concentrate

On-stream zircon processing will allow SRL to enhance its exposure to the attractive zircon market.

30

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

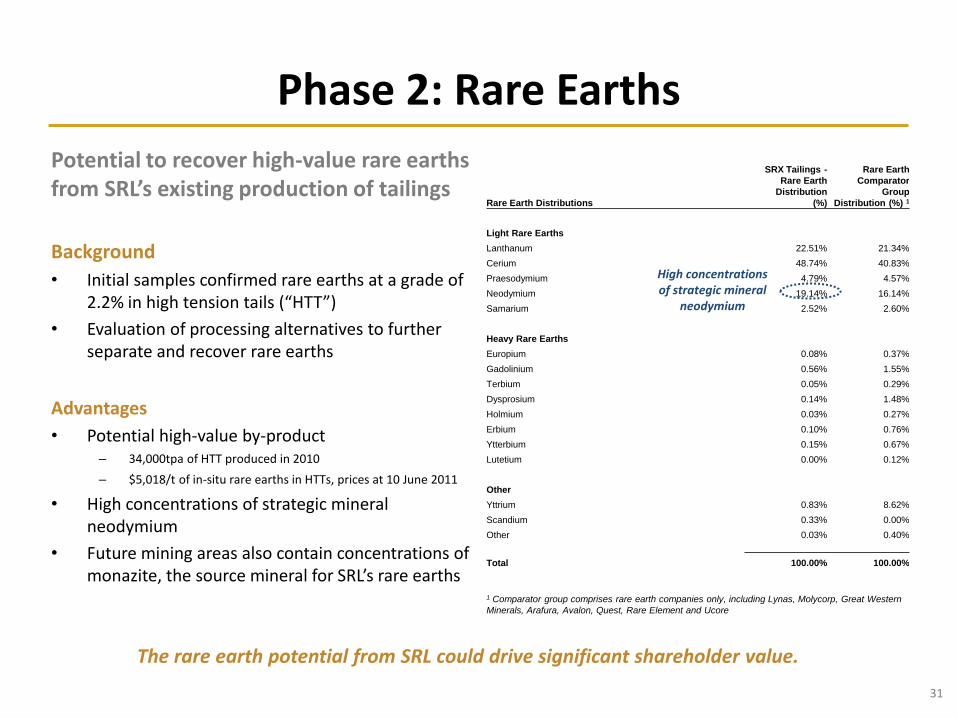

Phase 2: Rare Earths

Potential to recover high-value rare earths from SRL’s existing production of tailings

Background

• Initial samples confirmed rare earths at a grade of 2.2% in high tension tails (“HTT”)

• Evaluation of processing alternatives to further separate and recover rare earths

Advantages

• Potential high-value by-product– 34,000tpa of HTT produced in 2010

– $5,018/t of in-situ rare earths in HTTs, prices at 10 June 2011

• High concentrations of strategic mineralneodymium

• Future mining areas also contain concentrations of monazite, the source mineral for SRL’s rare earths

High concentrations of strategic mineral

neodymium

The rare earth potential from SRL could drive significant shareholder value.

Rare Earth Distributions

SRX Tailings -

Rare Earth

Distribution

(%)

Rare Earth

Comparator

Group

Distribution (%) 1

Light Rare Earths

Lanthanum 22.51% 21.34%

Cerium 48.74% 40.83%

Praesodymium 4.79% 4.57%

Neodymium 19.14% 16.14%

Samarium 2.52% 2.60%

Heavy Rare Earths

Europium 0.08% 0.37%

Gadolinium 0.56% 1.55%

Terbium 0.05% 0.29%

Dysprosium 0.14% 1.48%

Holmium 0.03% 0.27%

Erbium 0.10% 0.76%

Ytterbium 0.15% 0.67%

Lutetium 0.00% 0.12%

Other

Yttrium 0.83% 8.62%

Scandium 0.33% 0.00%

Other 0.03% 0.40%

Total 100.00% 100.00%

1 Comparator group comprises rare earth companies only, including Lynas, Molycorp, Great Western

Minerals, Arafura, Avalon, Quest, Rare Element and Ucore

31

SIERRA RUTILE LIMITEDWorking for a better Sierra Leone

Appendix

Financial Information

32

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

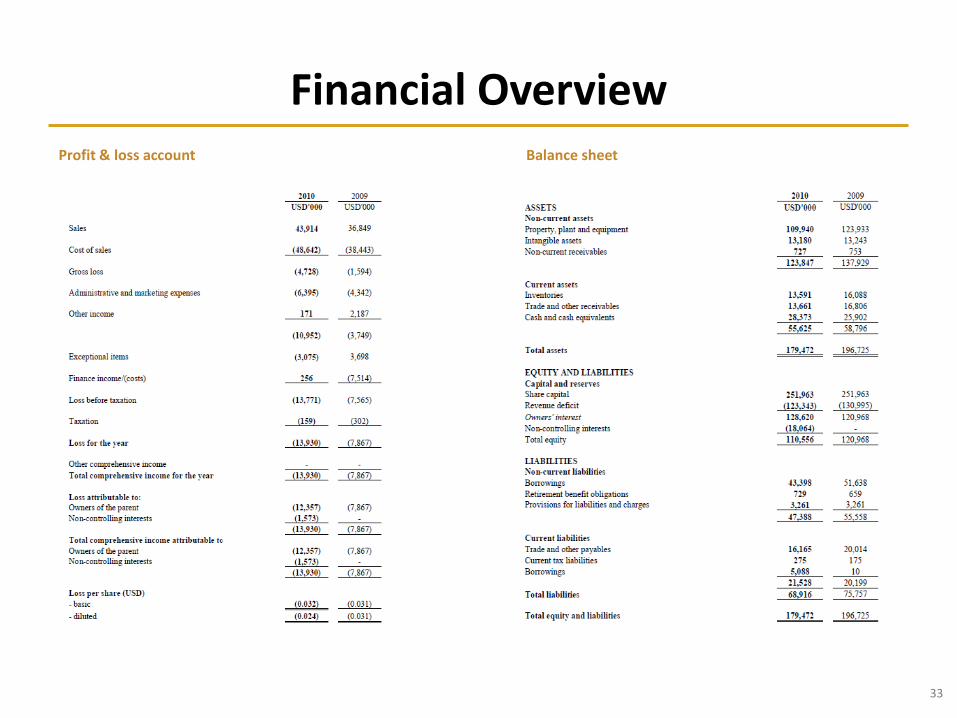

Financial OverviewProfit & loss account Balance sheet

33

SIERRA RUTILE LIMITED

Working for a better Sierra Leone

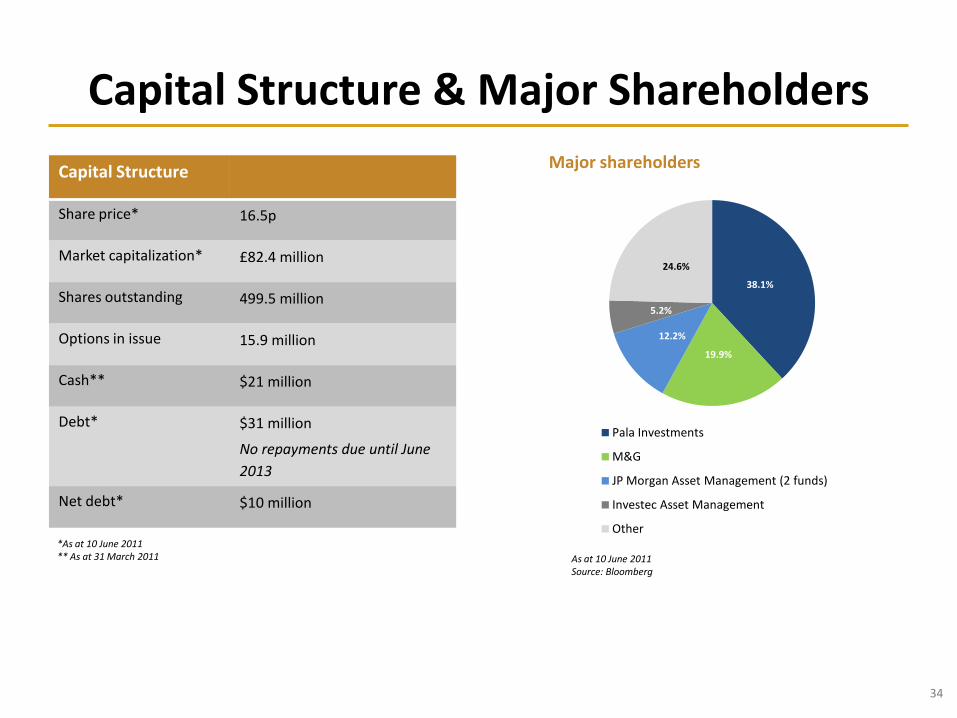

Capital Structure & Major Shareholders

Major shareholdersCapital Structure

Share price* 16.5p

Market capitalization* £82.4 million

Shares outstanding 499.5 million

Options in issue 15.9 million

Cash** $21 million

Debt* $31 million

No repayments due until June

2013

Net debt* $10 million

*As at 10 June 2011** As at 31 March 2011

34

38.1%

19.9%

12.2%

5.2%

24.6%

Pala Investments

M&G

JP Morgan Asset Management (2 funds)

Investec Asset Management

Other

As at 10 June 2011Source: Bloomberg

![Presentation May 2014 - Sierra Rutile · 2017. 11. 16. · > Chairman of Asian Mineral Resources [TSX-V: ASN] and Nevada Copper [TSX: NCU], also serves on the board of Alacer Gold](https://img.pdfslide.us/doc/110x75/6118643dcdb18d7613366170/presentation-may-2014-sierra-2017-11-16-chairman-of-asian-mineral-resources.jpg)