Embed Size (px)

Citation preview

COMPANY OVERVIEW

JUNE 2016

DISCLAIMER

2

Some of the statements made in this presentation are forward-looking statements and arebased on the current beliefs, assumptions, expectations, estimates, objectives and projectionsof the directors and management of Zee Entertainment Enterprises Limited (ZEE) about itsbusiness and the industry and markets in which it operates.

These forward-looking statements include, without limitation, statements relating to revenuesand earnings.

The words “believe”, “anticipate”, “expect”, “estimate”, “intend”, “project” and similarexpressions are also intended to identify forward looking statements.

These statements are not guarantees of future performance and are subject to risks,uncertainties and other factors, some of which are beyond the control of the Company and aredifficult to predict. Consequently, actual results could differ materially from those expressed orforecast in the forward-looking statements as a result of, among other factors, changes ineconomic and market conditions, changes in the regulatory environment and other businessand operational risks. ZEE does not undertake to update these forward-looking statements toreflect events or circumstances that may arise after publication.

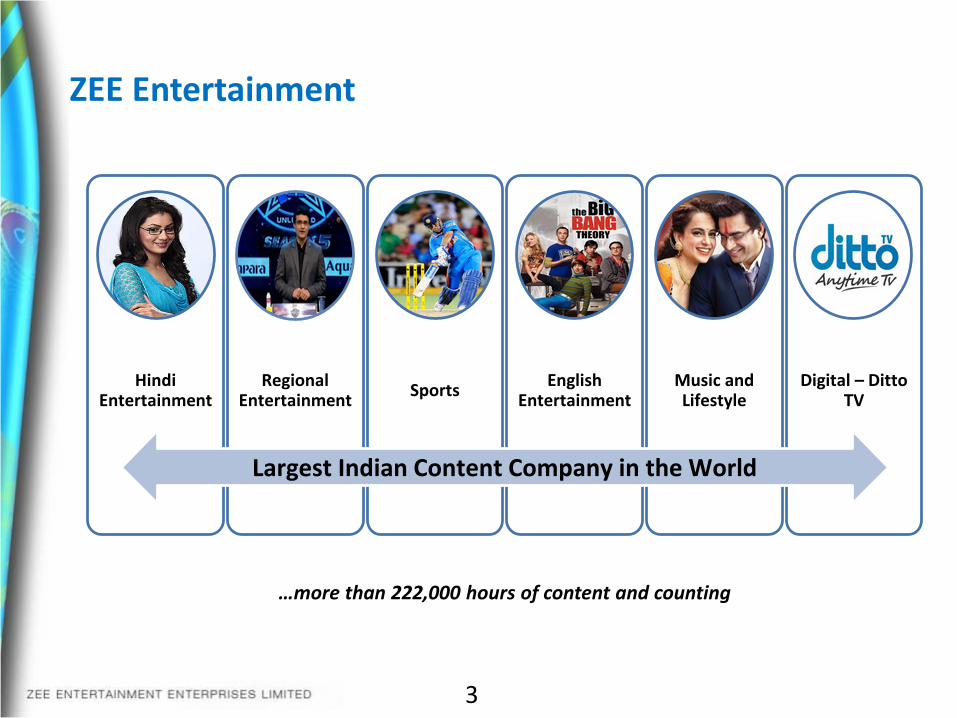

ZEE Entertainment

3

Hindi Entertainment

Regional Entertainment

SportsEnglish

EntertainmentMusic and Lifestyle

Digital – Ditto TV

Largest Indian Content Company in the World

…more than 222,000 hours of content and counting

Leading Hindi Entertainment Network

Consistently Innovating

Leading Sports Network

ZEE MARATHI

Leading Regional Entertainment Network

English Entertainment

9

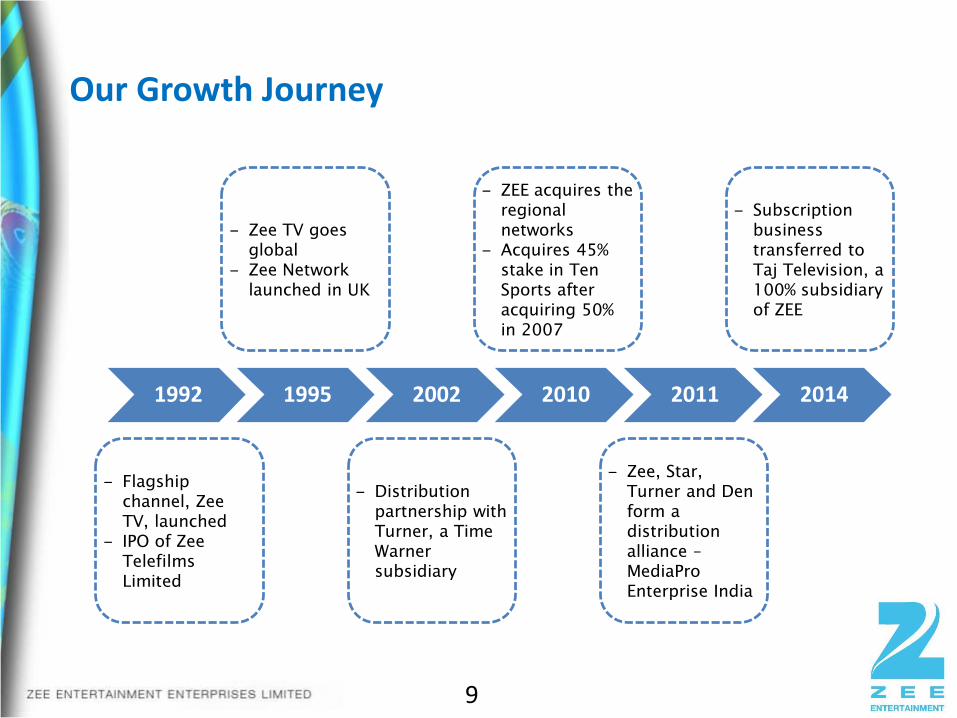

1992 1995 2002 2010 2011 2014

‒ Flagship

channel, Zee

TV, launched

‒ IPO of Zee

Telefilms

Limited

‒ Zee TV goes

global

‒ Zee Network

launched in UK

‒ Distribution

partnership with

Turner, a Time

Warner

subsidiary

‒ ZEE acquires the

regional

networks

‒ Acquires 45%

stake in Ten

Sports after

acquiring 50%

in 2007

‒ Zee, Star,

Turner and Den

form a

distribution

alliance –

MediaPro

Enterprise India

‒ Subscription

business

transferred to

Taj Television, a

100% subsidiary

of ZEE

Our Growth Journey

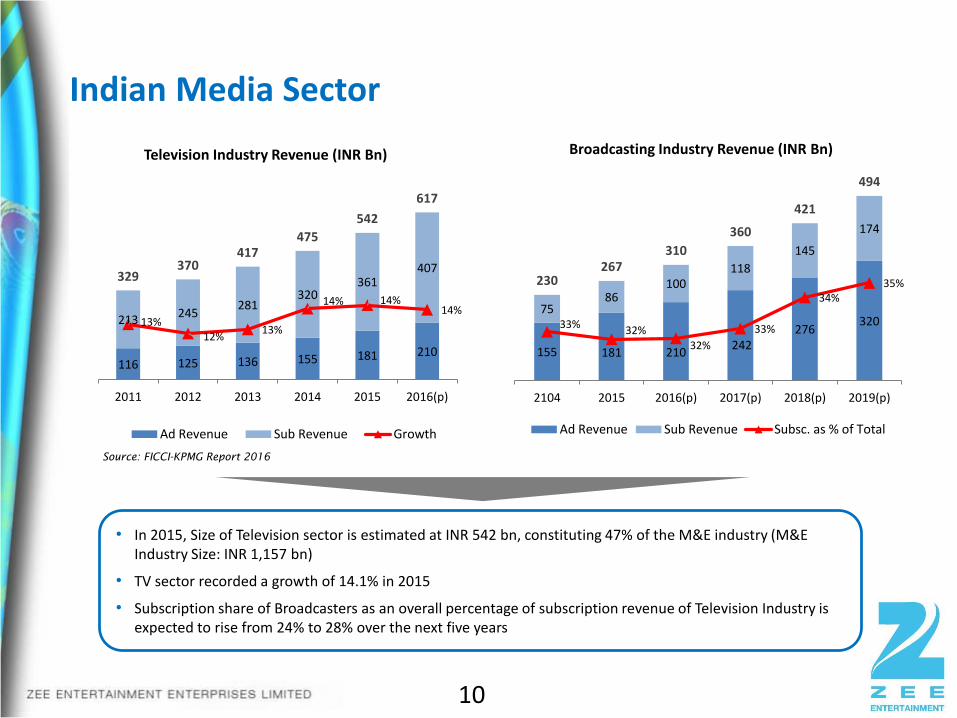

• In 2015, Size of Television sector is estimated at INR 542 bn, constituting 47% of the M&E industry (M&E Industry Size: INR 1,157 bn)

• TV sector recorded a growth of 14.1% in 2015

• Subscription share of Broadcasters as an overall percentage of subscription revenue of Television Industry is expected to rise from 24% to 28% over the next five years

Indian Media Sector

Source: FICCI-KPMG Report 2016

10

116 125 136 155 181 210

213245

281320

361407

329370

417475

542

617

13%12%

13%

14% 14%14%

9%

11%

13%

15%

17%

19%

-50

50

150

250

350

450

550

650

2011 2012 2013 2014 2015 2016(p)

Television Industry Revenue (INR Bn)

Ad Revenue Sub Revenue Growth

155 181 210242

276320

7586

100118

145

174

230267

310

360

421

494

33%32%

32%

33%

34%35%

30%

31%

32%

33%

34%

35%

36%

37%

38%

39%

40%

0

50

100

150

200

250

300

350

400

450

500

2104 2015 2016(p) 2017(p) 2018(p) 2019(p)

Broadcasting Industry Revenue (INR Bn)

Ad Revenue Sub Revenue Subsc. as % of Total

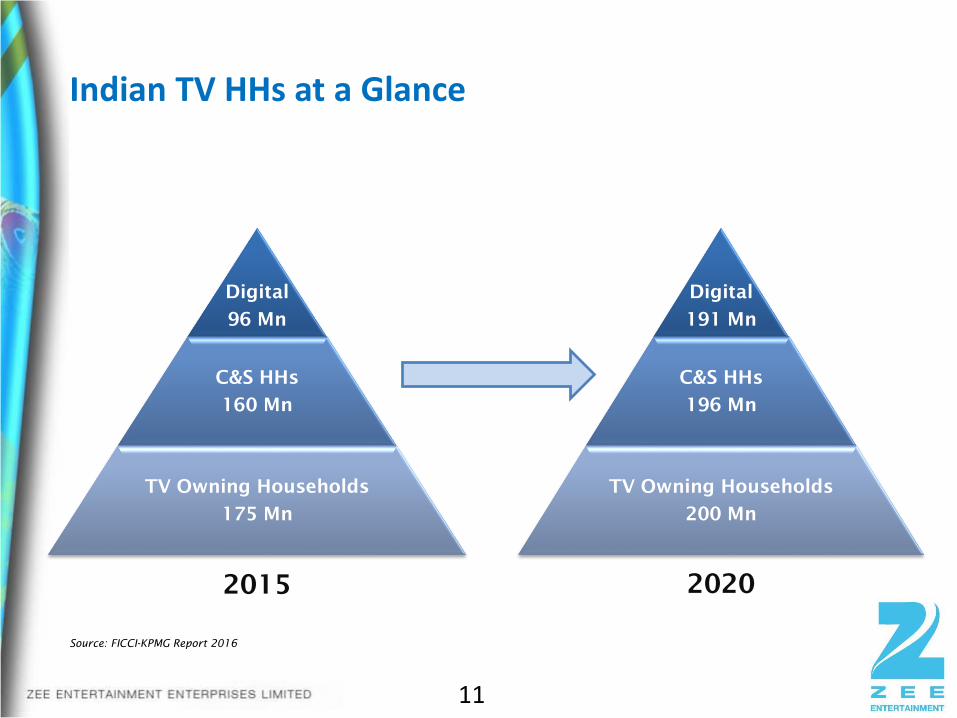

Indian TV HHs at a Glance

Digital

96 Mn

C&S HHs

160 Mn

TV Owning Households

175 Mn

2015

Source: FICCI-KPMG Report 2016

11

Digital

191 Mn

C&S HHs

196 Mn

TV Owning Households

200 Mn

2020

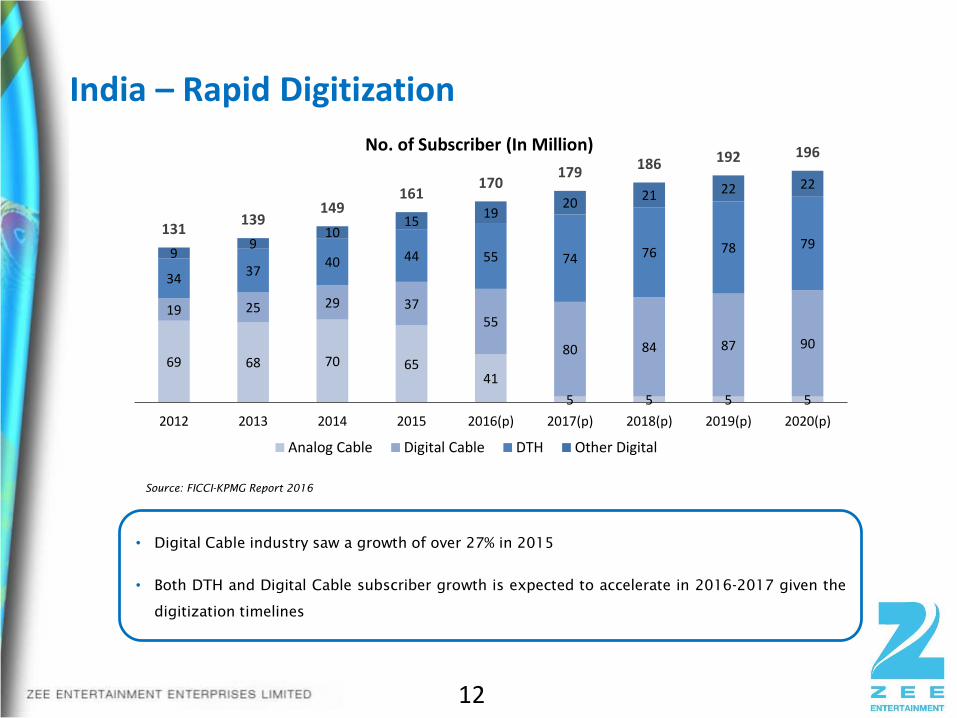

India – Rapid Digitization

Source: FICCI-KPMG Report 2016

12

• Digital Cable industry saw a growth of over 27% in 2015

• Both DTH and Digital Cable subscriber growth is expected to accelerate in 2016-2017 given the

digitization timelines

69 68 70 6541

5 5 5 5

19 25 29 3755

80 84 87 90

3437

40 44 55 74 76 78 799

910

1519

2021 22 22

131139

149161

170179

186 192 196

2012 2013 2014 2015 2016(p) 2017(p) 2018(p) 2019(p) 2020(p)

No. of Subscriber (In Million)

Analog Cable Digital Cable DTH Other Digital

13

ZEEL : A leading player in the Indian Television Market

Product Offering

14

Hindi Entertainment Hindi Cinema Regional Entertainment

English EntertainmentMusic, Lifestyle and NicheSports

HD Channels Select International Channels

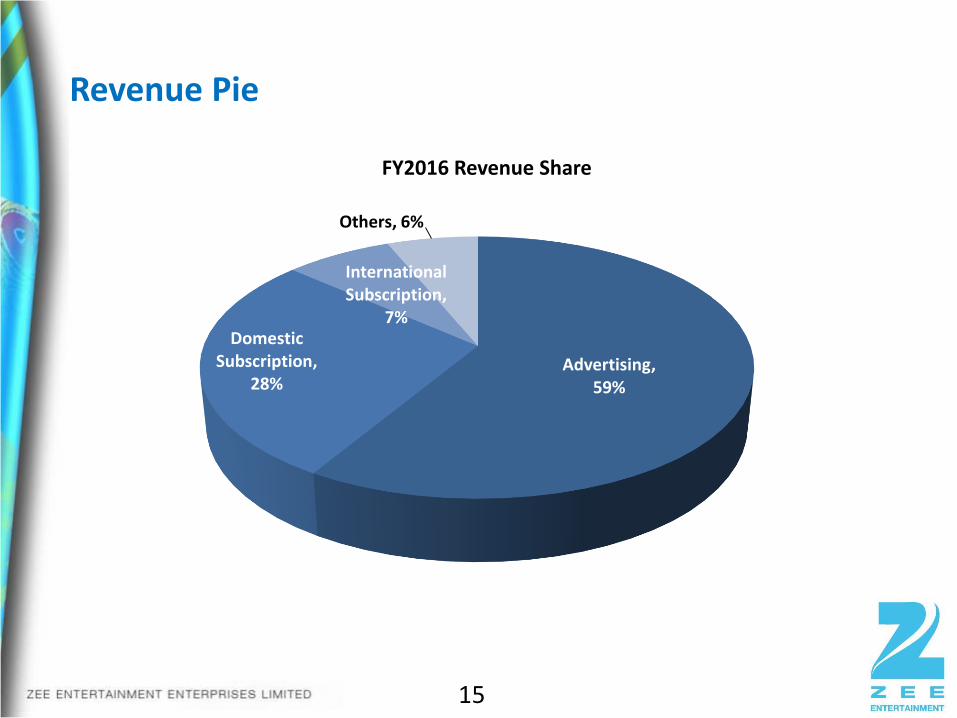

Revenue Pie

15

Advertising, 59%

Domestic Subscription,

28%

International Subscription,

7%

Others, 6%

FY2016 Revenue Share

BusinessPerformance

Hindi Entertainment Channels

• Zee TV is the largest Hindi entertainment channel of the world

17

Strong Movie Library

18

Largest Hindi Movie Library in the World

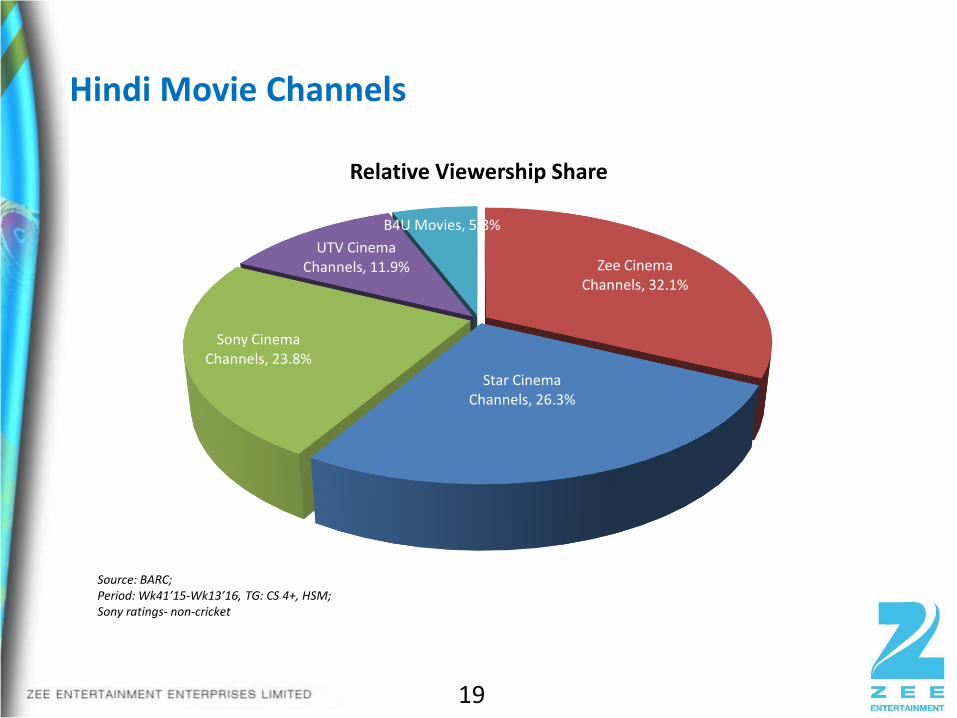

Hindi Movie Channels

19

Source: BARC; Period: Wk41’15-Wk13’16, TG: CS 4+, HSM; Sony ratings- non-cricket

Zee Cinema Channels, 32.1%

Star CinemaChannels, 26.3%

Sony Cinema Channels, 23.8%

UTV Cinema Channels, 11.9%

B4U Movies, 5.8%

Relative Viewership Share

20

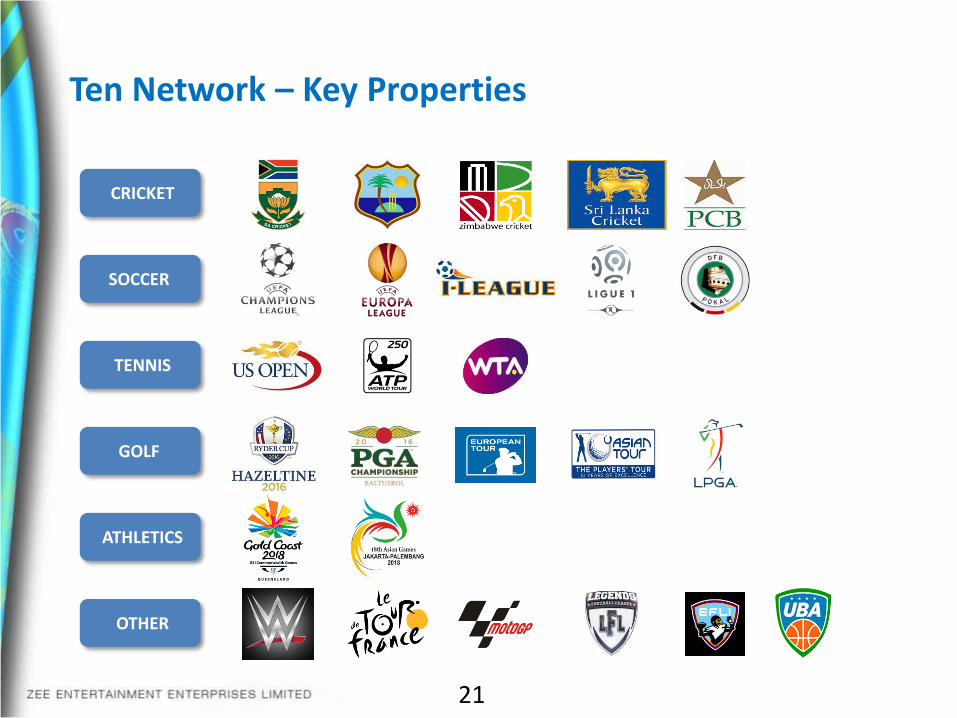

Ten Network – Key Properties

21

CRICKET

SOCCER

TENNIS

ATHLETICS

GOLF

OTHER

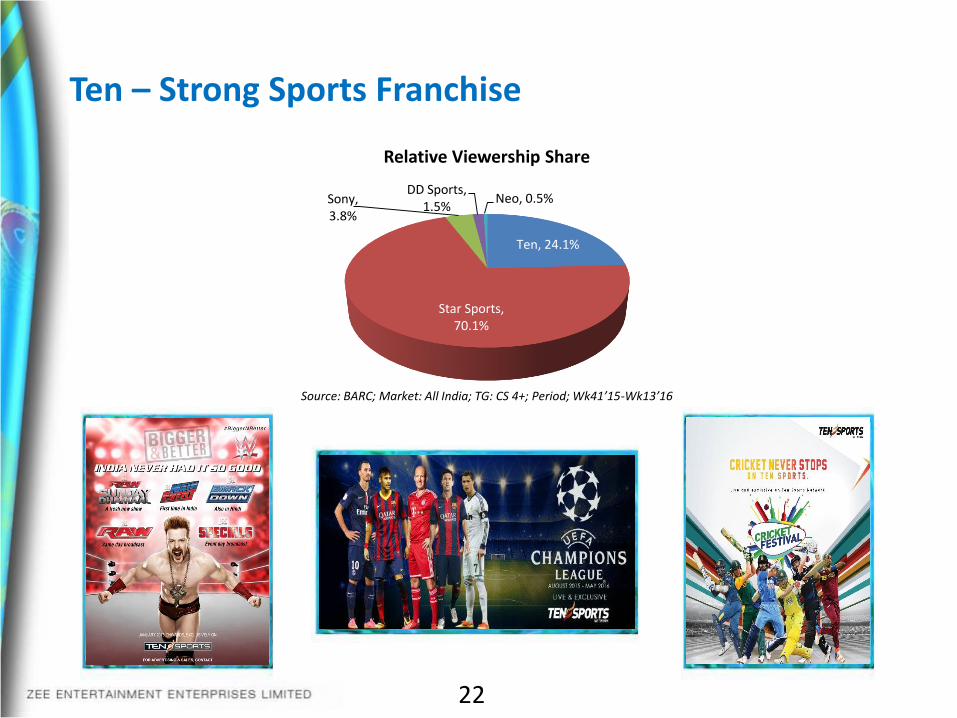

Ten – Strong Sports Franchise

22

Source: BARC; Market: All India; TG: CS 4+; Period; Wk41’15-Wk13’16

Ten, 24.1%

Star Sports, 70.1%

Sony, 3.8%

DD Sports, 1.5%

Neo, 0.5%

Relative Viewership Share

English and Niche Channels

• Tie-ups with leading studios across the world

23

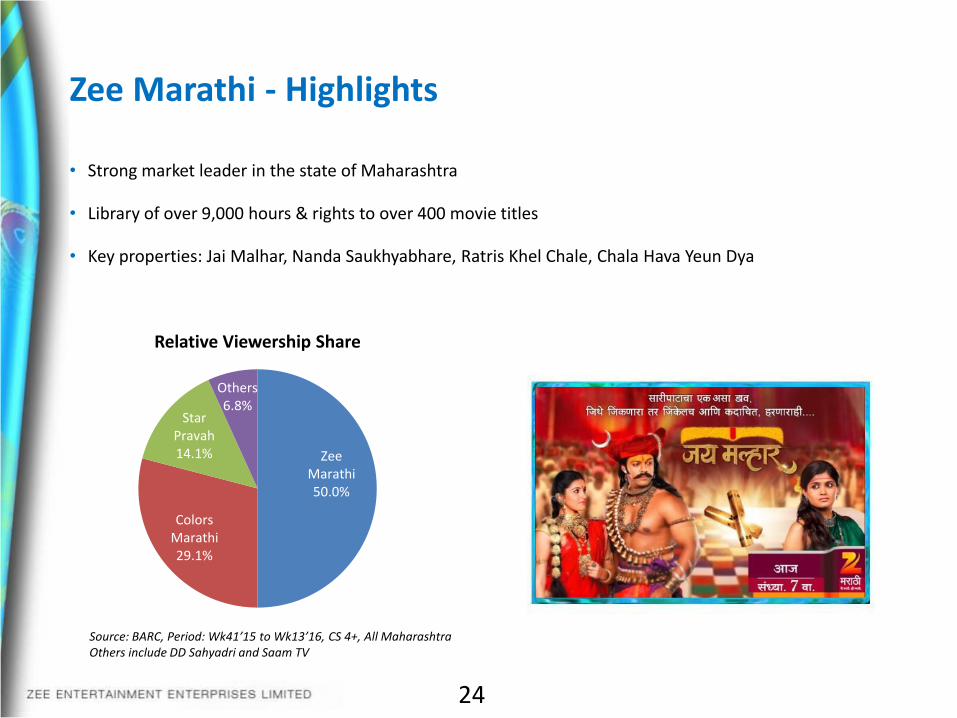

Zee Marathi - Highlights

• Strong market leader in the state of Maharashtra

• Library of over 9,000 hours & rights to over 400 movie titles

• Key properties: Jai Malhar, Nanda Saukhyabhare, Ratris Khel Chale, Chala Hava Yeun Dya

24

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All MaharashtraOthers include DD Sahyadri and Saam TV

Zee Marathi50.0%

Colors Marathi29.1%

Star Pravah14.1%

Others6.8%

Relative Viewership Share

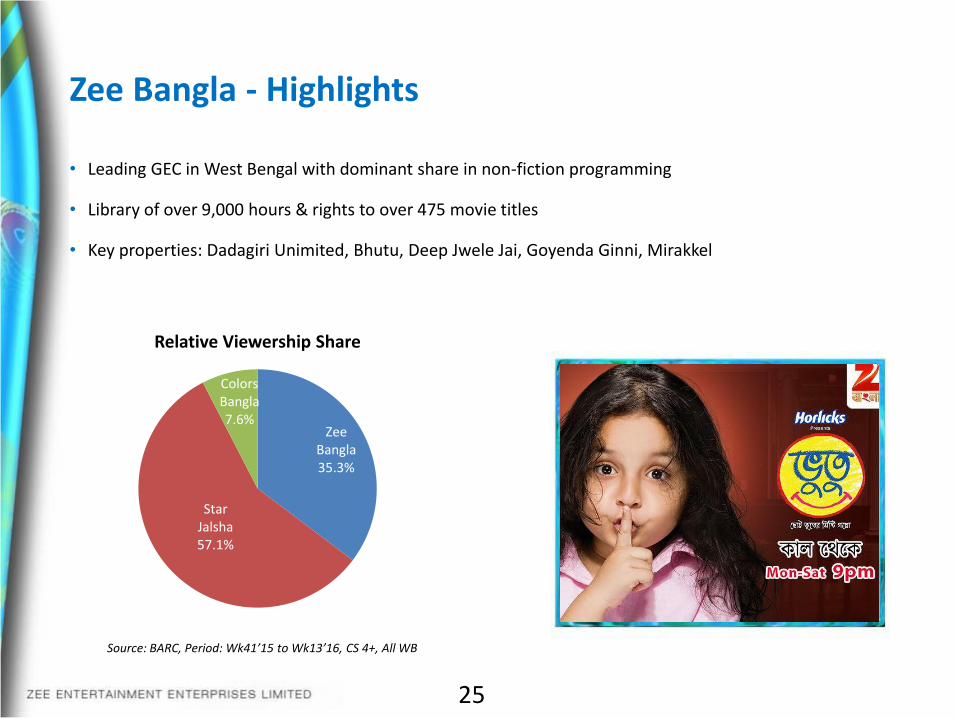

Zee Bangla - Highlights

• Leading GEC in West Bengal with dominant share in non-fiction programming

• Library of over 9,000 hours & rights to over 475 movie titles

• Key properties: Dadagiri Unimited, Bhutu, Deep Jwele Jai, Goyenda Ginni, Mirakkel

25

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All WB

Zee Bangla35.3%

Star Jalsha57.1%

Colors Bangla7.6%

Relative Viewership Share

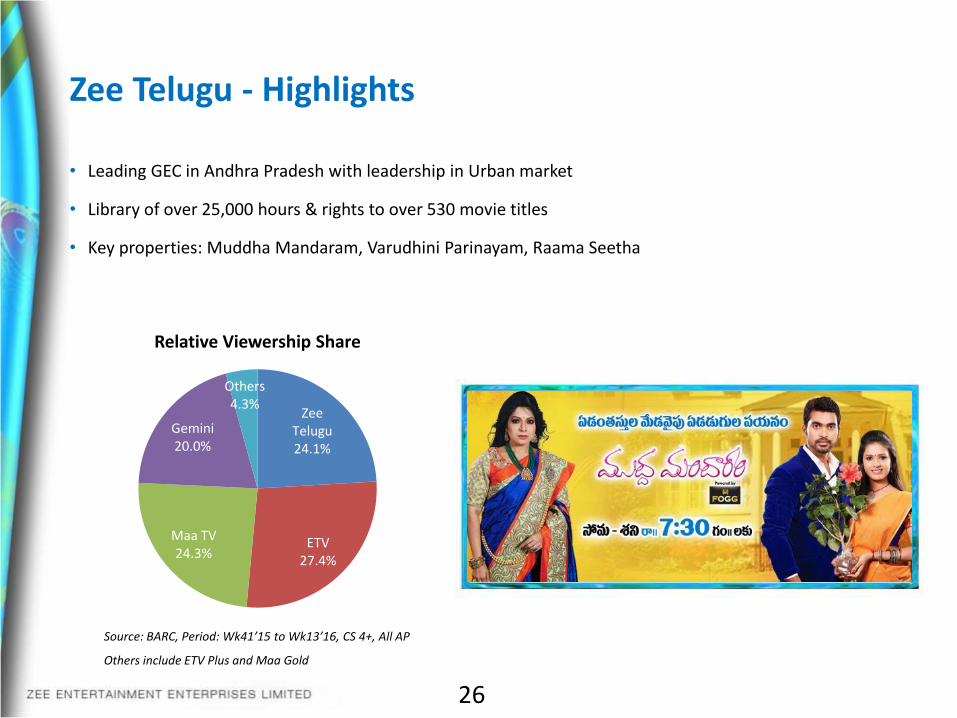

Zee Telugu - Highlights

• Leading GEC in Andhra Pradesh with leadership in Urban market

• Library of over 25,000 hours & rights to over 530 movie titles

• Key properties: Muddha Mandaram, Varudhini Parinayam, Raama Seetha

26

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All AP

Others include ETV Plus and Maa Gold

Zee Telugu24.1%

ETV27.4%

Maa TV24.3%

Gemini20.0%

Others4.3%

Relative Viewership Share

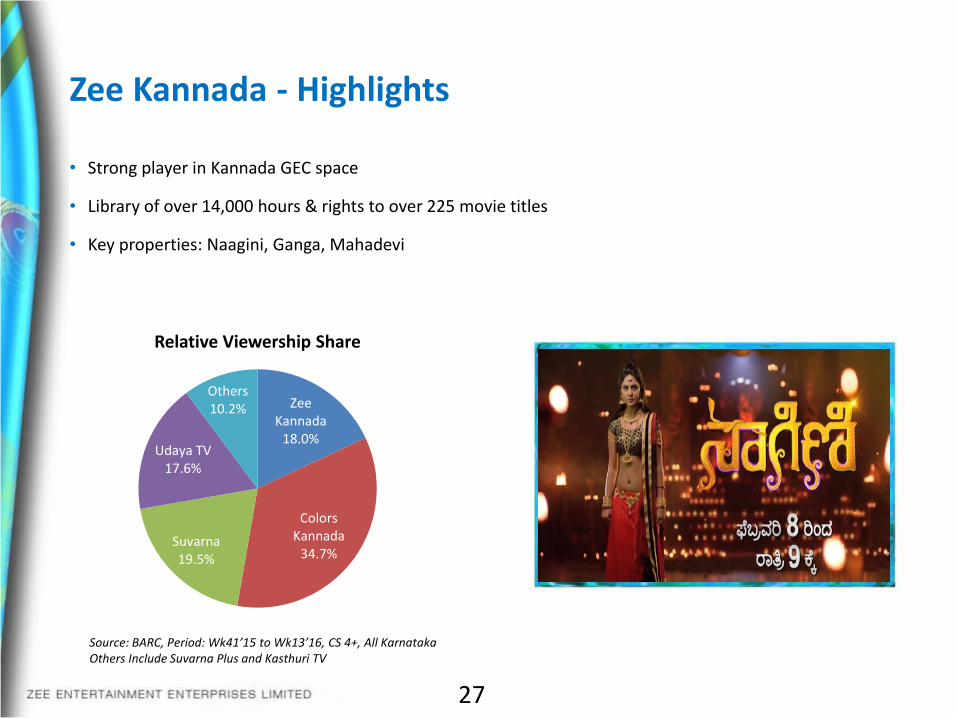

Zee Kannada - Highlights

• Strong player in Kannada GEC space

• Library of over 14,000 hours & rights to over 225 movie titles

• Key properties: Naagini, Ganga, Mahadevi

27

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All KarnatakaOthers Include Suvarna Plus and Kasthuri TV

Zee Kannada

18.0%

Colors Kannada

34.7%Suvarna19.5%

Udaya TV17.6%

Others10.2%

Relative Viewership Share

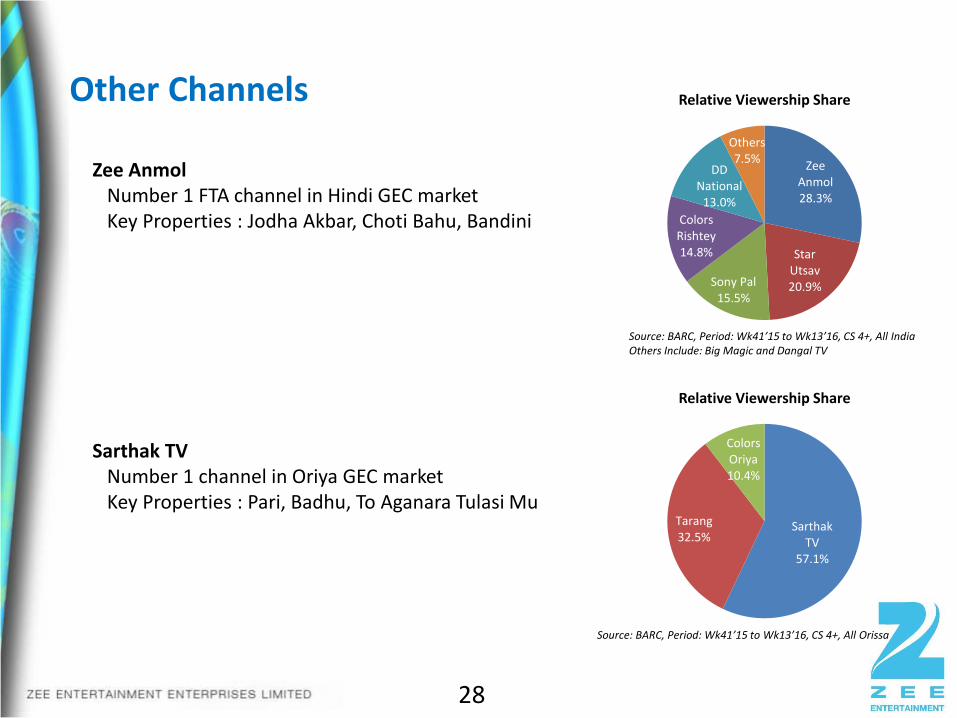

Other Channels

28

Zee Anmol Number 1 FTA channel in Hindi GEC marketKey Properties : Jodha Akbar, Choti Bahu, Bandini

Sarthak TV Number 1 channel in Oriya GEC marketKey Properties : Pari, Badhu, To Aganara Tulasi Mu

Zee Anmol28.3%

Star Utsav20.9%Sony Pal

15.5%

Colors Rishtey14.8%

DD National

13.0%

Others7.5%

Relative Viewership Share

Sarthak TV

57.1%

Tarang32.5%

Colors Oriya10.4%

Relative Viewership Share

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All IndiaOthers Include: Big Magic and Dangal TV

Source: BARC, Period: Wk41’15 to Wk13’16, CS 4+, All Orissa

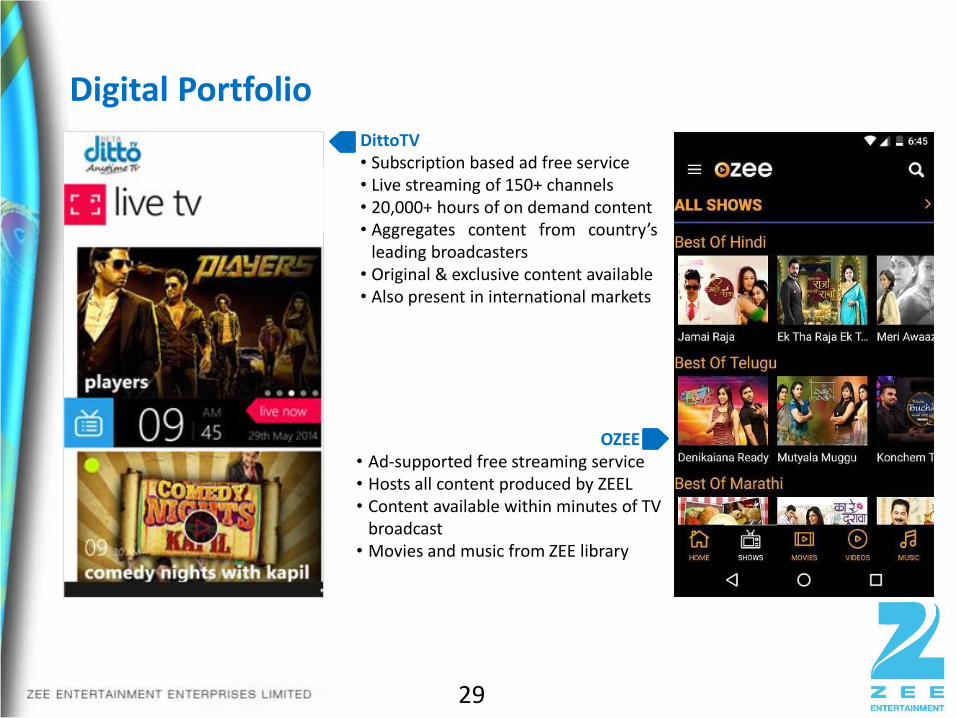

Digital Portfolio

29

DittoTV• Subscription based ad free service• Live streaming of 150+ channels• 20,000+ hours of on demand content• Aggregates content from country’s

leading broadcasters• Original & exclusive content available• Also present in international markets

OZEE• Ad-supported free streaming service• Hosts all content produced by ZEEL• Content available within minutes of TV

broadcast• Movies and music from ZEE library

• Presence across 5 continents through over

38 dedicated channels

• Catering to both South Asian as well as non

South Asian communities

• Increased reach through new distribution

deals in Caribbean, African & APAC markets

• International operations contributed 17% of

company top line in Q4FY2016

• Renewed focus on advertising as a source of

revenues

International Operations

30

Focused Investments

Digital InvestmentsRegional Channels

31

International ChannelsNational Channels

New Initiatives

32

Initiative to preserve and spread

centuries old Indian heritage and

taking its timeless stories to audiences

across the world

Key Financials

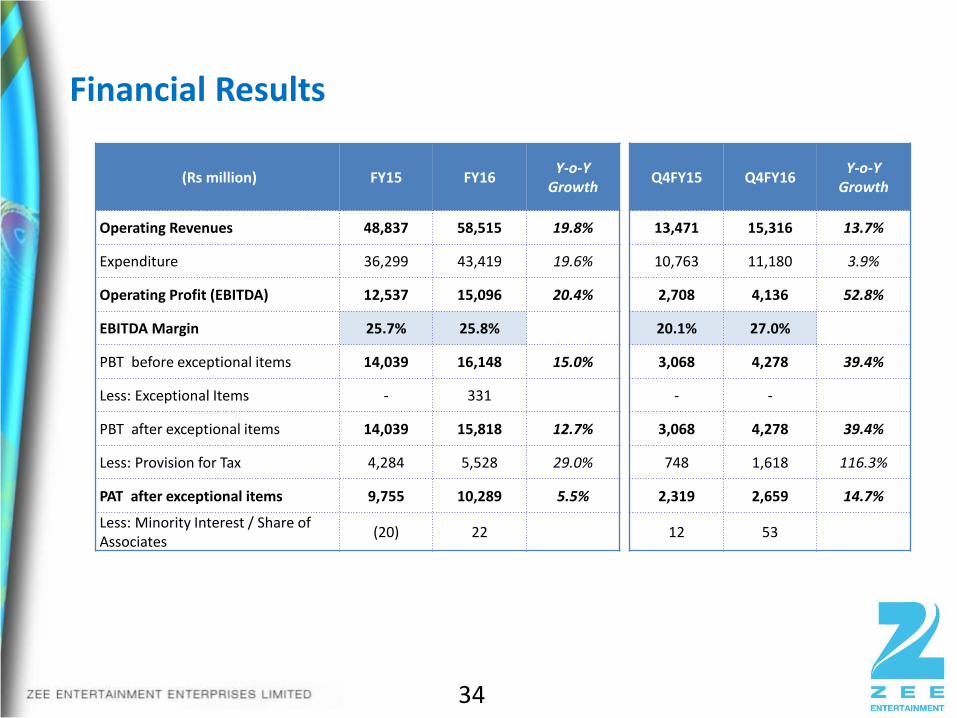

Financial Results

34

(Rs million) FY15 FY16Y-o-Y

Growth Q4FY15 Q4FY16

Y-o-Y Growth

Operating Revenues 48,837 58,515 19.8% 13,471 15,316 13.7%

Expenditure 36,299 43,419 19.6% 10,763 11,180 3.9%

Operating Profit (EBITDA) 12,537 15,096 20.4% 2,708 4,136 52.8%

EBITDA Margin 25.7% 25.8% 20.1% 27.0%

PBT before exceptional items 14,039 16,148 15.0% 3,068 4,278 39.4%

Less: Exceptional Items - 331 - -

PBT after exceptional items 14,039 15,818 12.7% 3,068 4,278 39.4%

Less: Provision for Tax 4,284 5,528 29.0% 748 1,618 116.3%

PAT after exceptional items 9,755 10,289 5.5% 2,319 2,659 14.7%

Less: Minority Interest / Share of Associates

(20) 22 12 53

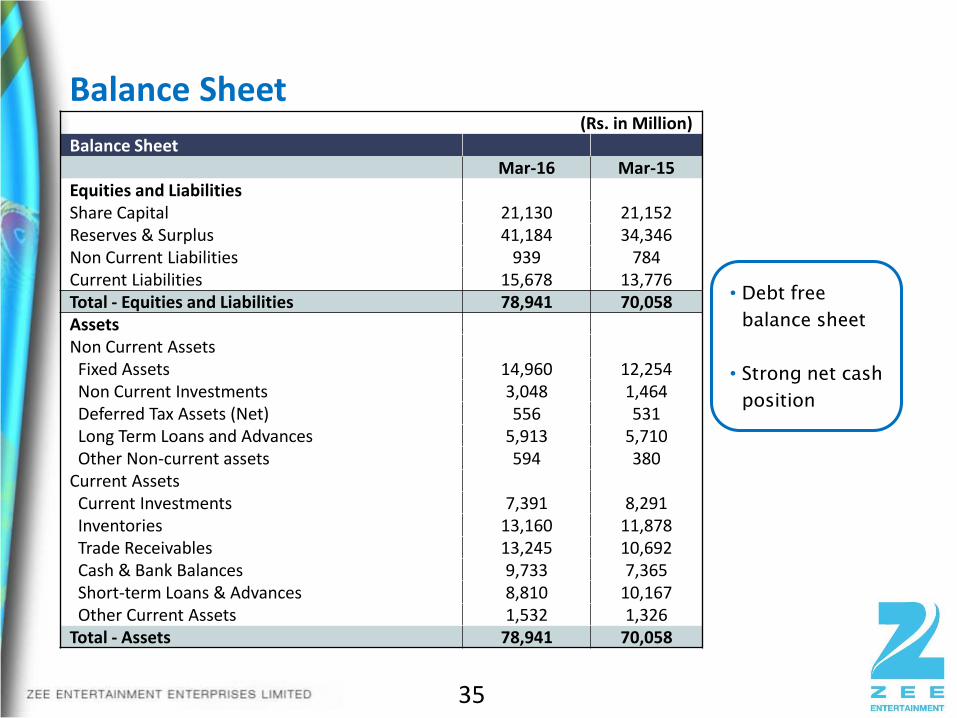

Balance Sheet

35

• Debt free

balance sheet

• Strong net cash

position

(Rs. in Million)Balance Sheet

Mar-16 Mar-15Equities and LiabilitiesShare Capital 21,130 21,152 Reserves & Surplus 41,184 34,346 Non Current Liabilities 939 784 Current Liabilities 15,678 13,776 Total - Equities and Liabilities 78,941 70,058 AssetsNon Current AssetsFixed Assets 14,960 12,254 Non Current Investments 3,048 1,464 Deferred Tax Assets (Net) 556 531 Long Term Loans and Advances 5,913 5,710 Other Non-current assets 594 380

Current AssetsCurrent Investments 7,391 8,291 Inventories 13,160 11,878 Trade Receivables 13,245 10,692 Cash & Bank Balances 9,733 7,365 Short-term Loans & Advances 8,810 10,167 Other Current Assets 1,532 1,326

Total - Assets 78,941 70,058

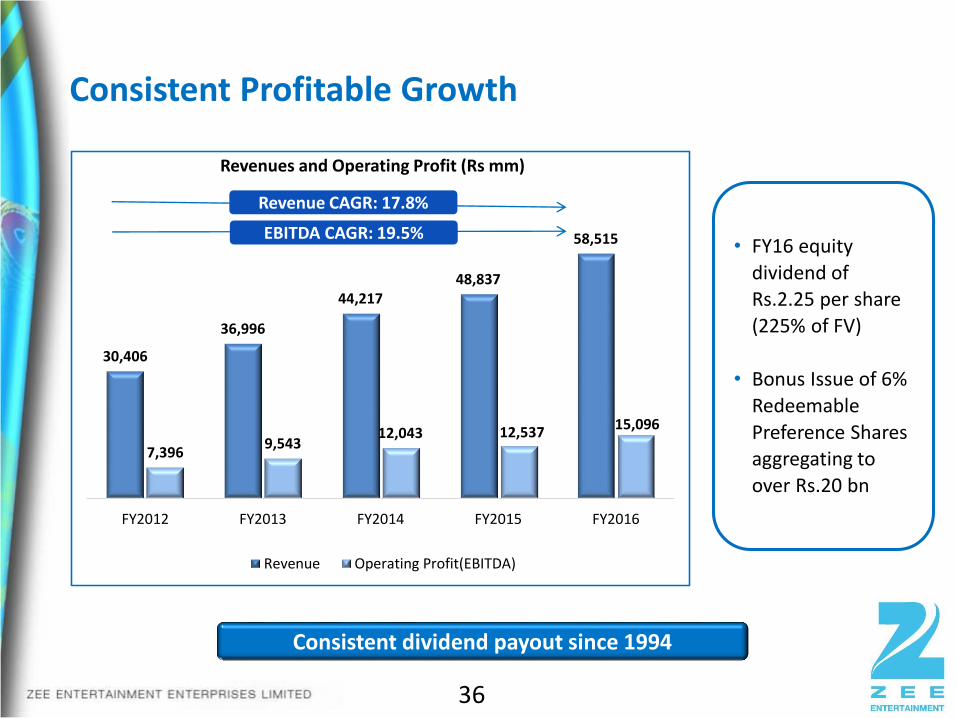

30,406

36,996

44,21748,837

58,515

7,3969,543

12,043 12,53715,096

FY2012 FY2013 FY2014 FY2015 FY2016

Revenues and Operating Profit (Rs mm)

Revenue Operating Profit(EBITDA)

Consistent Profitable Growth

36

Consistent dividend payout since 1994

Revenue CAGR: 17.8%

EBITDA CAGR: 19.5%• FY16 equity

dividend of Rs.2.25 per share

(225% of FV)

• Bonus Issue of 6%

Redeemable

Preference Shares aggregating to

over Rs.20 bn

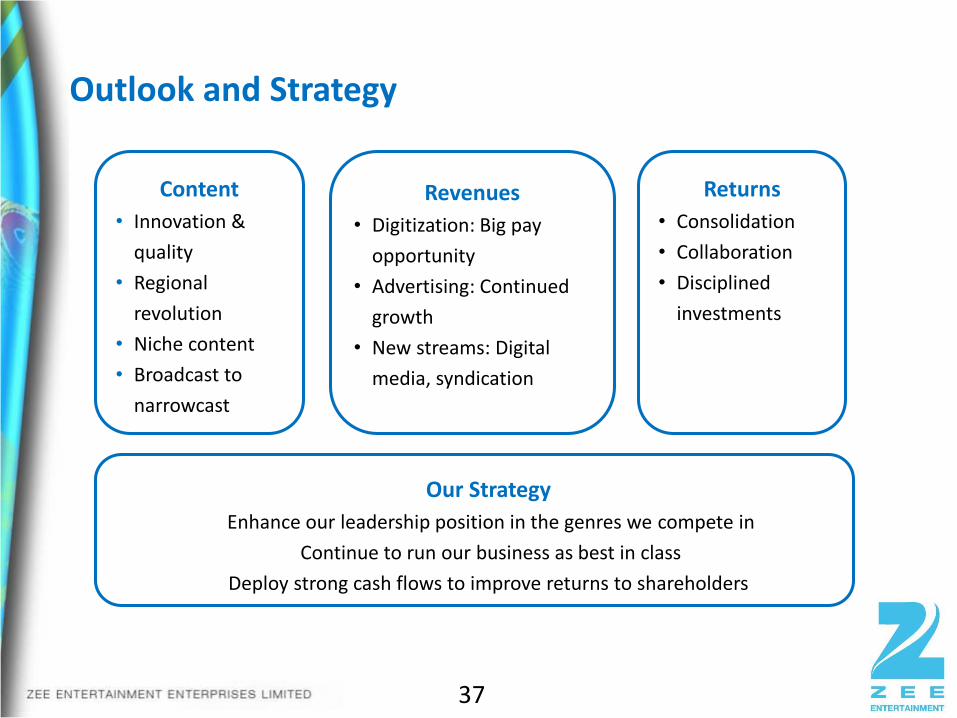

Outlook and Strategy

37

Revenues

• Digitization: Big pay

opportunity

• Advertising: Continued

growth

• New streams: Digital

media, syndication

Content

• Innovation &

quality

• Regional

revolution

• Niche content

• Broadcast to

narrowcast

Our Strategy

Enhance our leadership position in the genres we compete in

Continue to run our business as best in class

Deploy strong cash flows to improve returns to shareholders

Returns

• Consolidation

• Collaboration

• Disciplined

investments

38

Pioneer in several entertainment genres

World’s leading Indian TV network with 1 billion+ viewers in over 171 countries

Consistent performer since inception; Shareholder value CAGR of >30% since listing

The global force in entertainment