Embed Size (px)

Citation preview

October 2, 2013

Global and U.S. Coal Outlook

2013 American Waterways Symposium

Jacob Williams

Vice President Global Energy Analytics

Global and U.S. Coal Outlook

● Coal is the fastest-growing fuel in the world and

expected to surpass oil as the world‟s largest energy

source in coming years

● Near-term coal demand is rebounding in the United

States due to coal‟s competitive advantage over higher

priced natural gas

● Greater deployment of advanced technologies drives our

energy, economic and environmental “3E” goals

Key Discussion Points

2

0

1,000

2,000

3,000

4,000

5,000

Coal Oil Natural Gas

Nuclear Hydro Bio- energy

Wind/ Solar

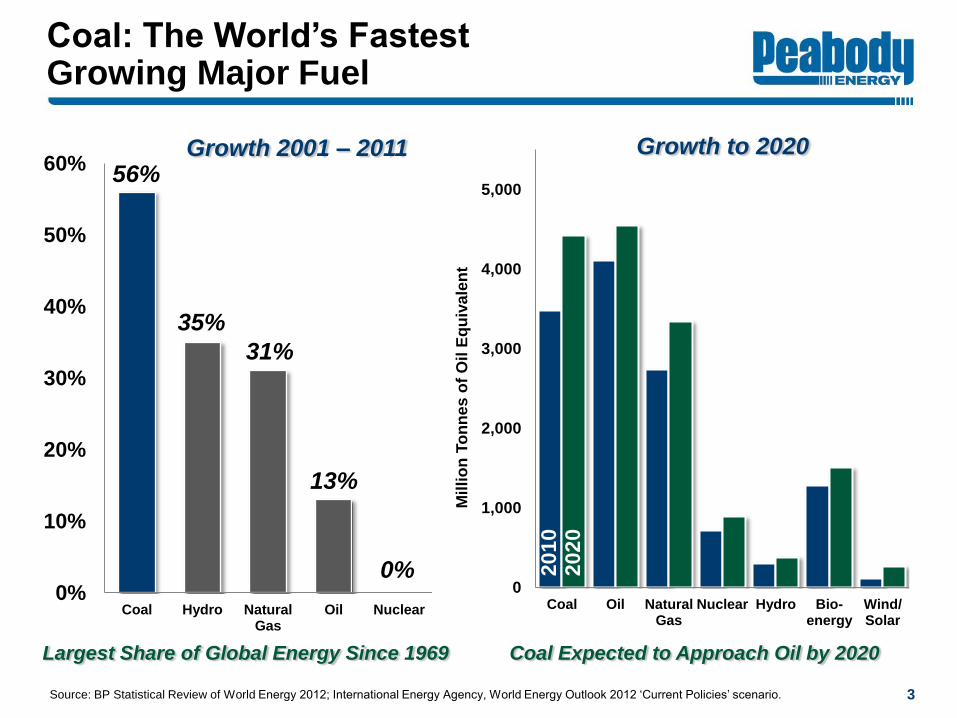

Coal: The World’s Fastest Growing Major Fuel

0%

10%

20%

30%

40%

50%

60%

Coal Hydro Natural Gas

Oil Nuclear

56%

35%

13%

31%

0%

Source: BP Statistical Review of World Energy 2012; International Energy Agency, World Energy Outlook 2012 „Current Policies‟ scenario. 3

Largest Share of Global Energy Since 1969

Growth 2001 – 2011 Growth to 2020

20

10

2

02

0

Mil

lio

n T

on

ne

s o

f O

il E

qu

iva

len

t

Coal Expected to Approach Oil by 2020

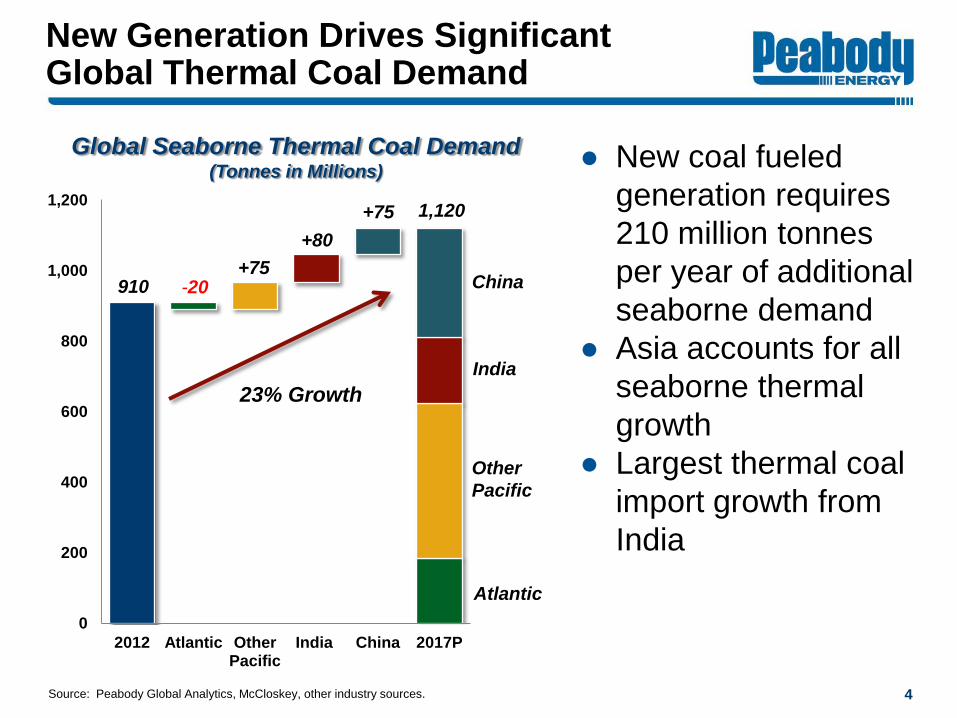

0

200

400

600

800

1,000

1,200

2012 Atlantic Other Pacific

India China 2017P

New Generation Drives Significant Global Thermal Coal Demand

● New coal fueled

generation requires

210 million tonnes

per year of additional

seaborne demand

● Asia accounts for all

seaborne thermal

growth

● Largest thermal coal

import growth from

India

910

1,120

+75

+80

+75

Global Seaborne Thermal Coal Demand (Tonnes in Millions)

23% Growth

China

Other

Pacific

India

-20

Atlantic 190

440

Source: Peabody Global Analytics, McCloskey, other industry sources. 4

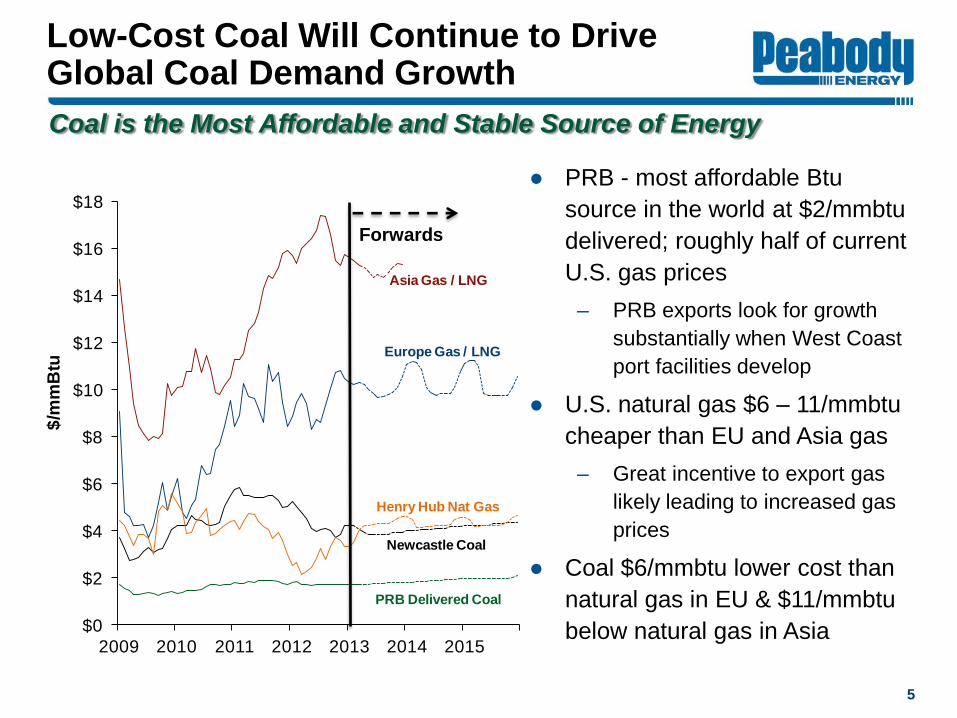

Low-Cost Coal Will Continue to Drive Global Coal Demand Growth

Coal is the Most Affordable and Stable Source of Energy

5

● PRB - most affordable Btu

source in the world at $2/mmbtu

delivered; roughly half of current

U.S. gas prices

‒ PRB exports look for growth

substantially when West Coast

port facilities develop

● U.S. natural gas $6 – 11/mmbtu

cheaper than EU and Asia gas

‒ Great incentive to export gas

likely leading to increased gas

prices

● Coal $6/mmbtu lower cost than

natural gas in EU & $11/mmbtu

below natural gas in Asia

$0

$2

$4

$6

$8

$10

$12

$14

$16

$18

2009 2010 2011 2012 2013 2014 2015

$/m

mB

tu

Europe Gas / LNG

Newcastle Coal

Henry Hub Nat Gas

PRB Delivered Coal

Asia Gas / LNG

Forwards

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

$90,000

$100,000

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

1970 1980 1990 2000 2010 2020 2030

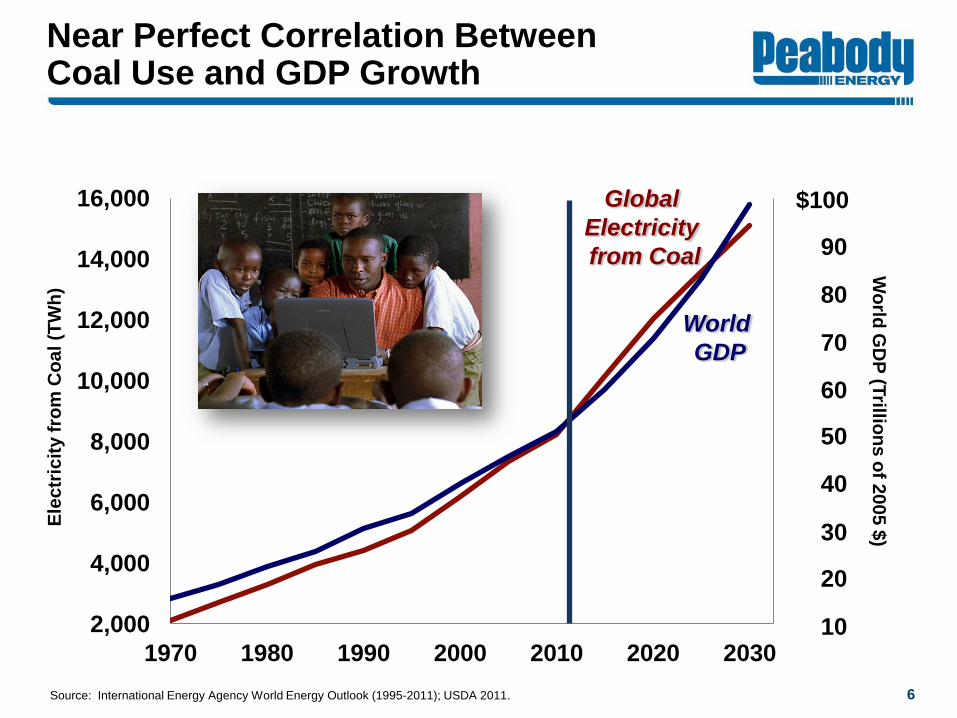

Near Perfect Correlation Between Coal Use and GDP Growth

Ele

ctr

icit

y f

rom

Co

al

(TW

h)

Global

Electricity

from Coal

World

GDP

Source: International Energy Agency World Energy Outlook (1995-2011); USDA 2011.

$100

90

80

70

60

50

40

30

20

10

Wo

rld G

DP

(Trillio

ns

of 2

00

5 $

)

6

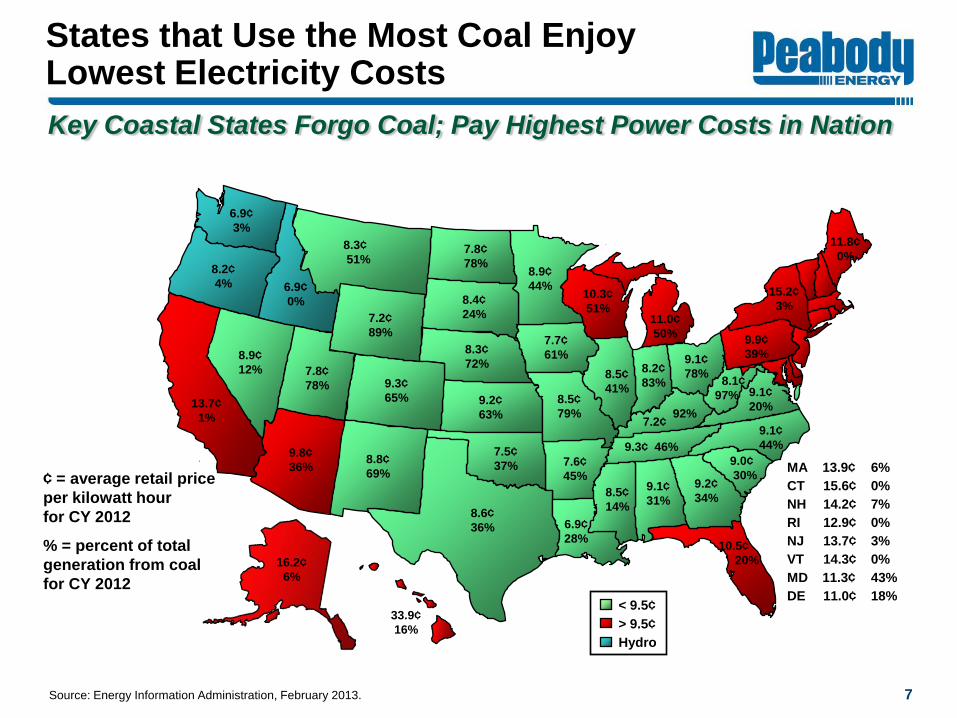

States that Use the Most Coal Enjoy Lowest Electricity Costs

7 Source: Energy Information Administration, February 2013.

10.5¢

20%

8.3¢

51% 7.8¢

78%

6.9¢

3%

8.3¢

72%

7.2¢

89%

9.3¢

65%

8.2¢

4%

9.2¢

63%

8.8¢

69%

8.9¢

12%

13.7¢

1%

7.8¢

78%

8.4¢

24%

8.6¢

36%

7.7¢

61%

8.9¢

44%

7.5¢

37%

8.5¢

79%

8.5¢

41%

9.8¢

36%

10.3¢

51%

7.6¢

45%

6.9¢

28%

11.0¢

50%

8.2¢

83%

9.1¢

78%

11.8¢

0%

8.5¢

14%

9.1¢

31%

9.2¢

34%

9.0¢

30%

7.2¢

9.1¢

20%

9.9¢

39%

8.1¢

97%

9.1¢

44% 9.3¢ 46%

6.9¢

0%

16.2¢

6%

33.9¢

16%

MA 13.9¢ 6%

CT 15.6¢ 0%

NH 14.2¢ 7%

RI 12.9¢ 0%

NJ 13.7¢ 3%

VT 14.3¢ 0%

MD 11.3¢ 43%

DE 11.0¢ 18%

¢ = average retail price

per kilowatt hour

for CY 2012

% = percent of total

generation from coal

for CY 2012

< 9.5¢

> 9.5¢

Hydro

15.2¢

3%

92%

Key Coastal States Forgo Coal; Pay Highest Power Costs in Nation

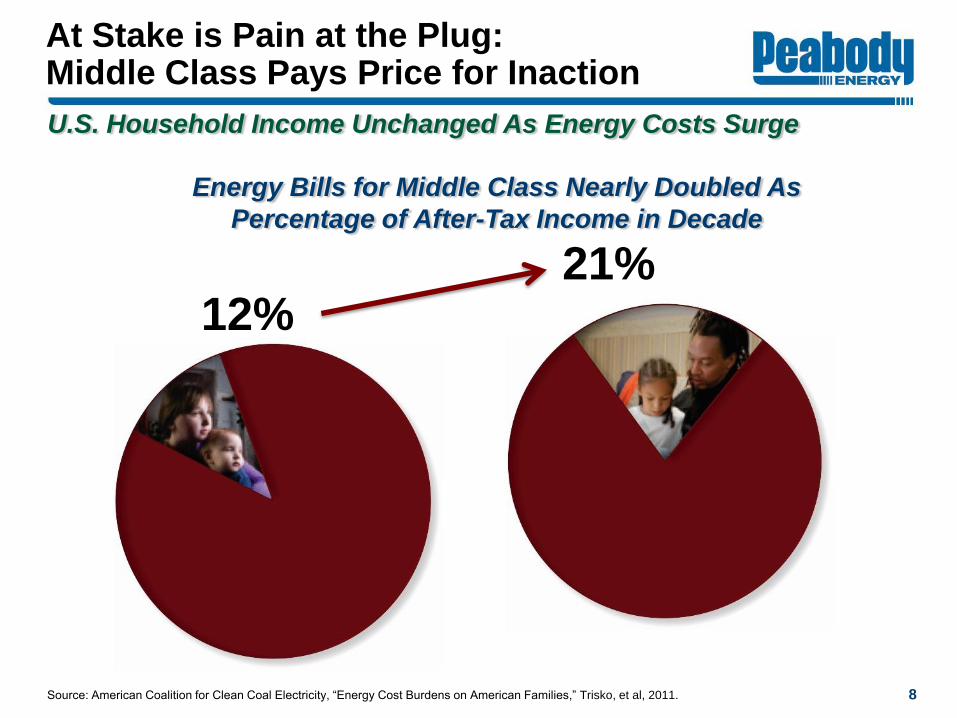

12% 21%

U.S. Household Income Unchanged As Energy Costs Surge

Source: American Coalition for Clean Coal Electricity, “Energy Cost Burdens on American Families,” Trisko, et al, 2011.

Energy Bills for Middle Class Nearly Doubled As

Percentage of After-Tax Income in Decade

8

At Stake is Pain at the Plug: Middle Class Pays Price for Inaction

0

200

400

600

Source: Peabody Global Analytics.

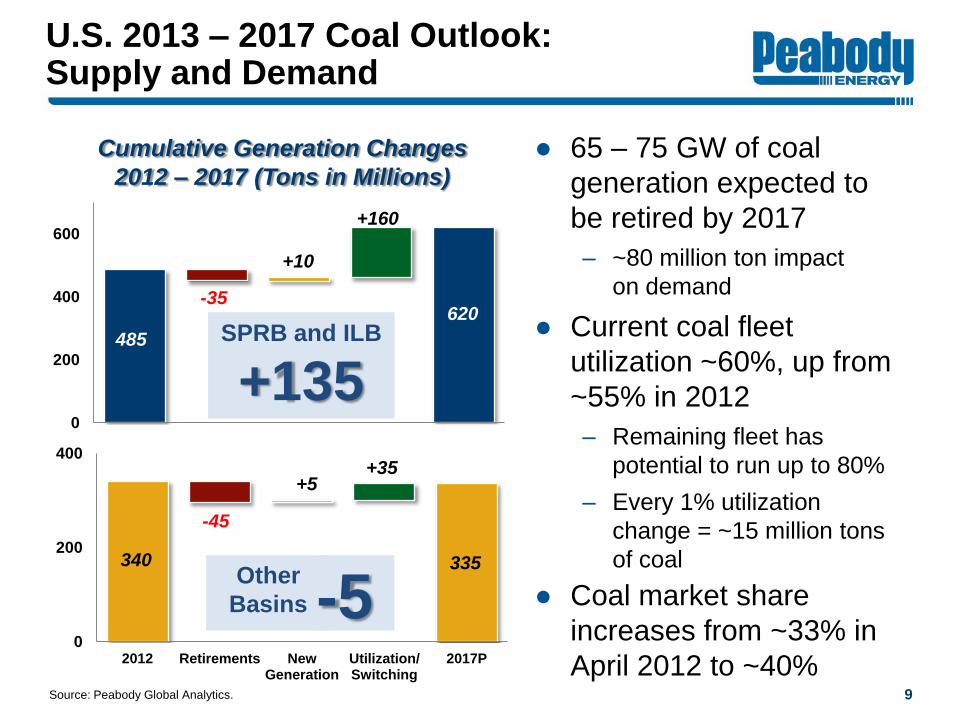

U.S. 2013 – 2017 Coal Outlook: Supply and Demand

● 65 – 75 GW of coal

generation expected to

be retired by 2017

– ~80 million ton impact

on demand

● Current coal fleet

utilization ~60%, up from

~55% in 2012

– Remaining fleet has

potential to run up to 80%

– Every 1% utilization

change = ~15 million tons

of coal

● Coal market share

increases from ~33% in

April 2012 to ~40%

Cumulative Generation Changes

2012 – 2017 (Tons in Millions)

(35)

+35

+160

+135

0

200

400

2012 Retirements New Generation

Utilization/ Switching

2017P

-35

-45

+10

+5

+160

+35

SPRB and ILB

+135

Other

Basins

485

620

340 335

9

-5

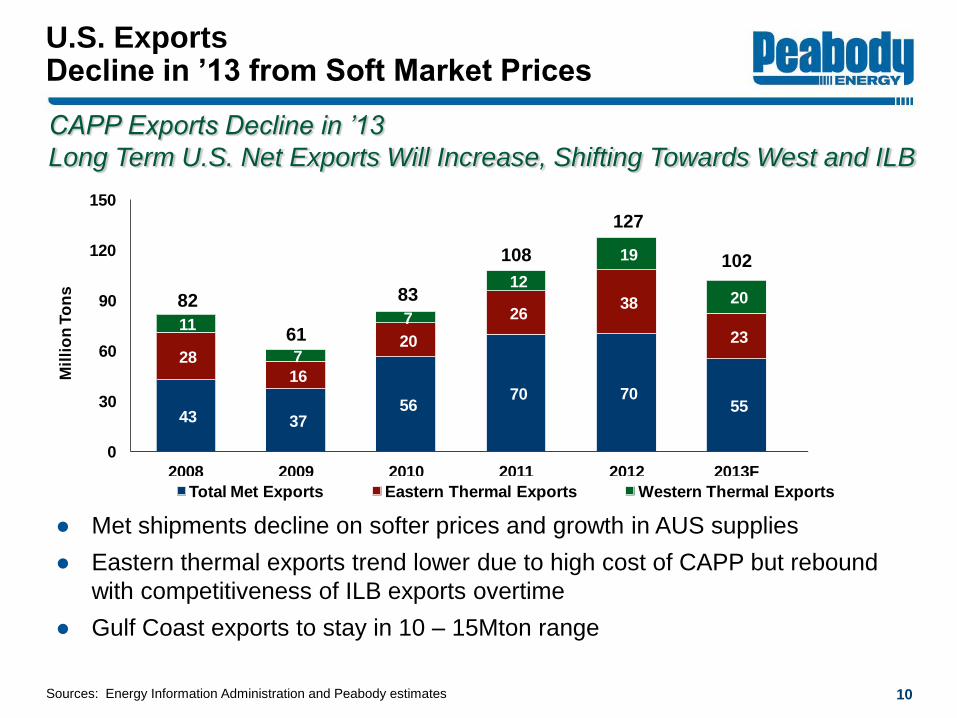

10 Sources: Energy Information Administration and Peabody estimates

● Met shipments decline on softer prices and growth in AUS supplies

● Eastern thermal exports trend lower due to high cost of CAPP but rebound

with competitiveness of ILB exports overtime

● Gulf Coast exports to stay in 10 – 15Mton range

CAPP Exports Decline in ’13

Long Term U.S. Net Exports Will Increase, Shifting Towards West and ILB

U.S. Exports Decline in ’13 from Soft Market Prices

43 37 56

70 70 55

44

28 16

20

26 38

23 32

11

7

7

12

19

20 23 82

61

83

108

127

102 99

0

30

60

90

120

150

2008 2009 2010 2011 2012 2013F 2017F

Mil

lio

n T

on

s

Total Met Exports Eastern Thermal Exports Western Thermal Exports

● PRB, CO and ILB able to serve rising exports

● Major port capacity being pursued in the Pacific

Northwest and Canada

● Global encompassing permitting stance threat to

all U.S. commodity exports

West and Gulf Expansion Opportunities with Improved Infrastructure

Asian Growth Creates Opportunity to Grow U.S. Exports

Site of Planned Gateway Pacific Terminal 11

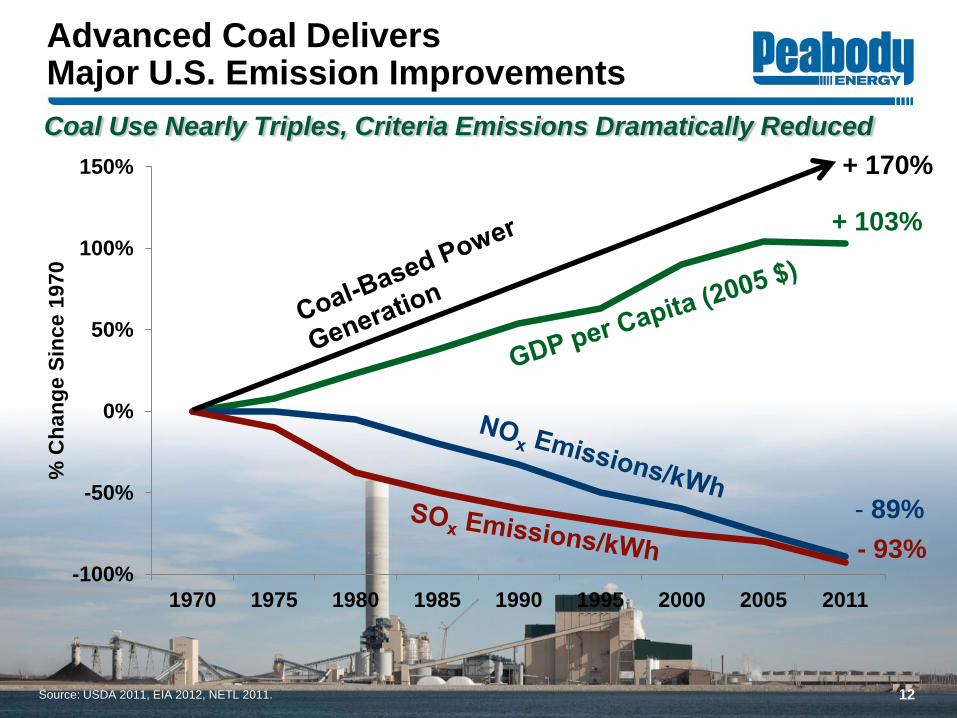

Advanced Coal Delivers Major U.S. Emission Improvements

12

-100%

-50%

0%

50%

100%

150%

1970 1975 1980 1985 1990 1995 2000 2005 2011

% C

han

ge S

ince 1

970

+ 103%

- 89%

- 93%

Source: USDA 2011, EIA 2012, NETL 2011.

+ 170%

Coal Use Nearly Triples, Criteria Emissions Dramatically Reduced

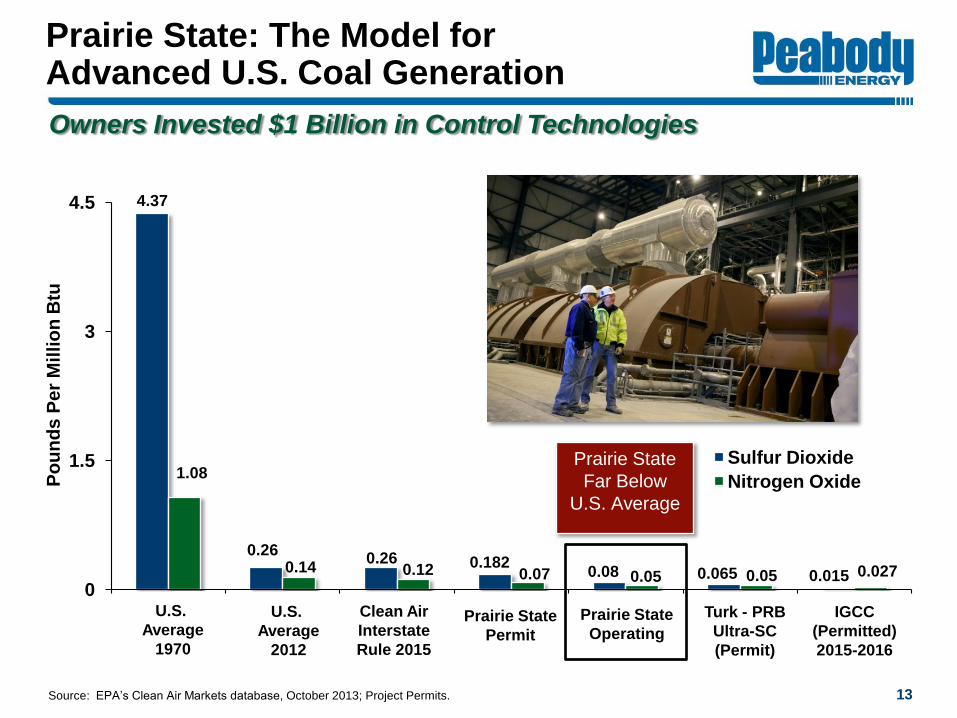

0

1.5

3

4.5

Po

un

ds

Pe

r M

illio

n B

tu

Sulfur Dioxide

Nitrogen Oxide

Prairie State

Far Below

U.S. Average

Source: EPA‟s Clean Air Markets database, October 2013; Project Permits.

U.S.

Average

2012

Prairie State

Permit

Clean Air

Interstate

Rule 2015

4.37

0.14

0.26 0.12 0.182

0.07

1.08

0.26

U.S.

Average

1970

0.015 0.027

IGCC

(Permitted)

2015-2016

Turk - PRB

Ultra-SC

(Permit)

0.065 0.05

Owners Invested $1 Billion in Control Technologies

Prairie State

Operating

0.08 0.05

Prairie State: The Model for Advanced U.S. Coal Generation

13

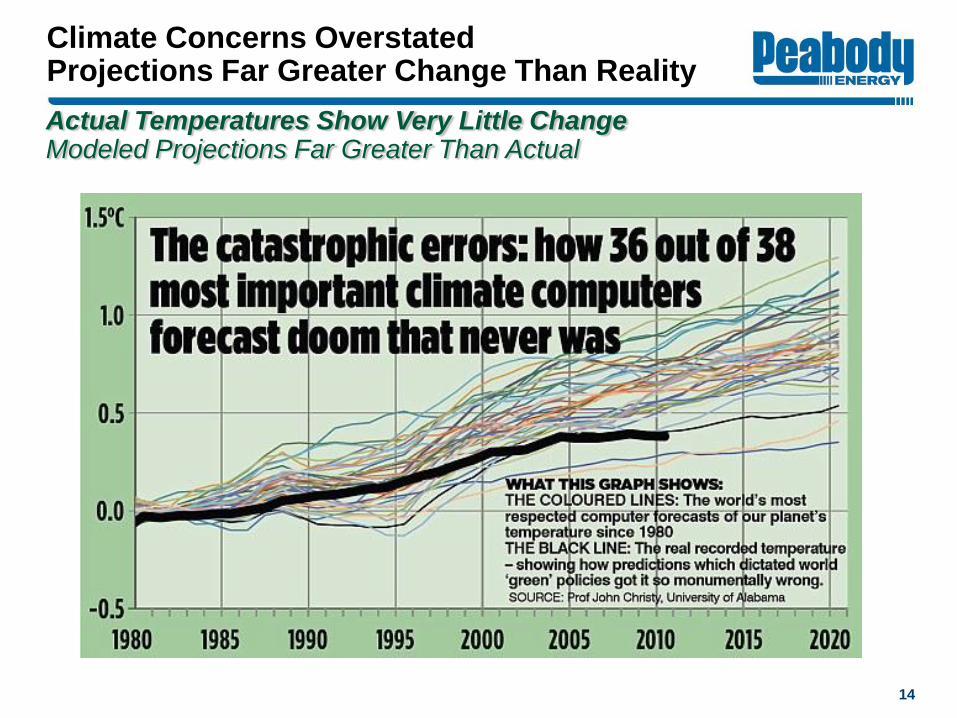

Actual Temperatures Show Very Little Change Modeled Projections Far Greater Than Actual

Climate Concerns Overstated Projections Far Greater Change Than Reality

14

www.PeabodyEnergy.com