Embed Size (px)

Citation preview

© 2016 Chevron Corporation

Chevron 2016 Investor presentation

August 2016

2

light blue 0/157/217

mid blue 0-102-178

dark blue 11-45-113

teal 0-178-189

mid teal 0-112-140

dark teal 0-54-83

light green 178-204-52

mid green 118-146-49

dark green 68-75-13

red 226-24-54

mid red 151-0-46

dark red 88-0-28

light orange 250-171-24

mid orange 229-96-31

dark orange 113-27-0

light purple 186-48-147

mid purple 117-18-105

dark purple 58-13-54

light gray 219-220-221

mid gray 140-143-147

dark gray 107-109-111

warm color family R-G-B

cool color family R-G-B

use the color picker or

type in the RGB values to

select color

do not use tints from the

color palette

© 2016 Chevron Corporation

Cautionary statement CAUTIONARY STATEMENTS RELEVANT TO FORWARD-LOOKING INFORMATION

FOR THE PURPOSE OF “SAFE HARBOR” PROVISIONS OF THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

This presentation of Chevron Corporation contains forward-looking statements relating to Chevron’s operations that are based on management’s current expectations, estimates and

projections about the petroleum, chemicals and other energy-related industries. Words or phrases such as “anticipates,” “expects,” “intends,” “plans,” “targets,” “forecasts,” “projects,”

“believes,” “seeks,” “schedules,” “estimates,” “positions,” “may,” “could,” “should,” “budgets,” “outlook,” “on schedule,” “on track,” “goals,” “objectives” and similar expressions are intended to

identify such forward-looking statements. These statements are not guarantees of future performance and are subject to certain risks, uncertainties and other factors, many of which are

beyond the company’s control and are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or forecasted in such forward-looking

statements. The reader should not place undue reliance on these forward-looking statements, which speak only as of the date of this presentation. Unless legally required, Chevron

undertakes no obligation to update publicly any forward-looking statements, whether as a result of new information, future events or otherwise.

Among the important factors that could cause actual results to differ materially from those in the forward-looking statements are: changing crude oil and natural gas prices; changing refining,

marketing and chemicals margins; the company’s ability to realize anticipated cost savings and expenditure reductions; actions of competitors or regulators; timing of exploration expenses;

timing of crude oil liftings; the competitiveness of alternate-energy sources or product substitutes; technological developments; the results of operations and financial condition of the

company’s suppliers, vendors, partners and equity affiliates, particularly during extended periods of low prices for crude oil and natural gas; the inability or failure of the company’s joint-

venture partners to fund their share of operations and development activities; the potential failure to achieve expected net production from existing and future crude oil and natural gas

development projects; potential delays in the development, construction or start-up of planned projects; the potential disruption or interruption of the company’s operations due to war,

accidents, political events, civil unrest, severe weather, cyber threats and terrorist acts, crude oil production quotas or other actions that might be imposed by the Organization of Petroleum

Exporting Countries or other natural or human causes beyond its control; changing economic, regulatory and political environments in the various countries in which the company operates;

general domestic and international economic and political conditions; the potential liability for remedial actions or assessments under existing or future environmental regulations and

litigation; significant operational, investment or product changes required by existing or future environmental statutes and regulations, including international agreements and national or

regional legislation and regulatory measures to limit or reduce greenhouse gas emissions; the potential liability resulting from other pending or future litigation; the company’s future

acquisition or disposition of assets and gains and losses from asset dispositions or impairments; government-mandated sales, divestitures, recapitalizations, industry-specific taxes, changes

in fiscal terms or restrictions on scope of company operations; foreign currency movements compared with the U.S. dollar; material reductions in corporate liquidity and access to debt

markets; the effects of changed accounting rules under generally accepted accounting principles promulgated by rule-setting bodies; the company’s ability to identify and mitigate the risks

and hazards inherent in operating in the global energy industry; and the factors set forth under the heading “Risk Factors” on pages 21 through 23 of the company’s 2015 Annual Report on

Form 10-K. Other unpredictable or unknown factors not discussed in this presentation could also have material adverse effects on forward-looking statements.

Certain terms, such as “unrisked resources,” “unrisked resource base,” “recoverable resources,” and “oil in place,” among others, may be used in this presentation to describe certain

aspects of the company’s portfolio and oil and gas properties beyond the proved reserves. For definitions of, and further information regarding, these and other terms, see the “Glossary of

Energy and Financial Terms” on pages 50 and 51 of the company’s 2015 Supplement to the Annual Report and available at Chevron.com. As used in this presentation, the term “project”

may describe new upstream development activity, including phases in a multiphase development, maintenance activities, certain existing assets, new investments in downstream and

chemicals capacity, investment in emerging and sustainable energy activities, and certain other activities. All of these terms are used for convenience only and are not intended as a precise

description of the term “project” as it relates to any specific government law or regulation.

3 © 2016 Chevron

Key messages

• Maintain and grow dividend is the priority

• Improve free cash flow by:

− Reducing capital and operating spend

− Growing volume and margin

• Use strong balance sheet to complete

projects under construction

• Positioned to improve returns and

selectively grow in lower price environment

4 © 2016 Chevron

CVX ranking relative to competitors, 1 being the lowest rate

Leading operational excellence performance

Days away from work rate Oil spills to land or water Thousands of barrels

Competitor range: BP, RDS, XOM

Source: Annual company sustainability reports. DAFWR – XOM is lost time incident rates; RDS is lost time

incident rates for injuries only. Oil spills to land or water – when needed, units converted to thousand bbl based

on the following assumptions 1 ton = 7.3 bbl 1 bbl = 0.16 cubic meters 1 bbl = 159 liters

0.05

0.10

2011 2012 2013 2014 2015

1

1 1 1

30

60

2011 2012 2013 2014 2015

CVX ranking relative to competitors, 1 being the lowest rate

Competitor range: BP, RDS, XOM

1 1 2

2 1

1

5 © 2016 Chevron

Competitor average:

BP, RDS, TOT, XOM

100

200

300

2005 2015

S&P 500

Financial priorities

Indexed dividend growth Basis: 2005 = 100

Source: Public information

Chevron Competitor range:

BP, RDS, TOT, XOM

~9% compound annual

growth rate

Maintain and

grow dividend

Fund

capital program

for future earnings

Maintain

strong balance sheet

Return

surplus cash

to stockholders

6 © 2016 Chevron

Financial performance

2Q16 YTD

Earnings $(2.2) billion

Cash flow from operations $ 3.7 billion

C&E spending $ 12.0 billion

Debt ratio ~23%

Dividends paid $4.0 billion

Low price environment

Responding to market

• Completing projects underway

• Capital and operating spend reduction

• Asset sales for value

• Prudently using balance sheet

7 © 2016 Chevron Corporation

Light blue 0-157-217

Mid blue 0-102-178

Dark blue 11-45-113

Light teal 0-178-189

Mid teal 0-112-140

Dark teal 0-54-83

Light green 178-204-52

Mid green 118-146-49

Dark green 68-75-13

Light red 226-24-54

Mid red 151-0-46

Dark red 88-0-28

Light orange 250-171-24

Mid orange 229-96-31

Dark orange 113-27-0

Light purple 186-48-147

Mid purple 117-18-105

Dark purple 58-13-54

Light gray 219-220-221

Mid gray 140-143-147

Dark gray 107-109-111

Warm color family R-G-B

Cool color family R-G-B

Use the color picker or type in the

RGB values to select color.

Do not use tints from the color

palette.

Background gray 237-237-238

(15)

(10)

(5)

0

5

10

Improving free cash flow

Cash flow after dividends* (including asset sales)

$ billions

2015 Actual* $52/bbl

2017* $52/bbl

Reduced

cash C&E

spend

Upstream

TCO

financing/

asset sales DS&C/ Other

Price

recovery

Cash flow from operations

*Cash flow after dividends = estimated cash flow from operations plus asset sales, less cash C&E, less dividends. 2015

includes asset sales proceeds of $5.7B. 2017 at $52/bbl Brent is for illustration purposes only and not indicative of

Chevron’s forecast

Reduced spend

Further flexibility

depending on market

Volume and margin

growth

8 © 2016 Chevron

8.0 5.9 4.4

2013 2014 2015

Chevron Southeast Asia competitor average

Thailand drilling efficiency Average days per 10,000 feet drilled – Rushmore benchmarking

Examples of efficiency gains

Cost and procurement activities

2,622

Sustainable actions

• Organizational activities

‒ ~4,000 through 1Q 2016

– On target to reach ~8,000

• Efficiency gains

– Logistics

– Drilling

• Strategic supplier engagement

2014 2015 2016 Estimate

Number of vessels

Africa logistics efficiency

~40%

- - - - -

- - - - -

- - - - -

~45%

- -

9 © 2016 Chevron

4

6

8

2014avg

2015avg

1Q 2Q 3Q 4Q

4

6

8

10

12

2014avg

2015avg

1Q 2Q 3Q 4Q

Spend momentum

Total capital & exploratory Quarterly

$ billions

Total C&E includes affiliate spend

OPEX and SG&A Quarterly

$ billions

OPEX and SG&A = operating, selling, general and administrative expenses as

reported on income statement (excludes affiliate spend)

Quarterly average

2016 C&E is trending

to lower end of

guidance range

YTD 2016 vs. YTD 2015: -31%

OPEX reductions

continue to be realized

YTD 2016 vs. YTD 2015: -8%

2016 Quarterly average 2016

10 © 2016 Chevron

Total capital & exploratory $ billions

TCO FGP / WPMP

Reducing spend

Total C&E includes affiliate spend. TCO FGP / WPMP = Tengiz Future Growth Project and Wellhead

Pressure Management Project

15

30

2014 2015 2016 2017 2018

OPEX / SG&A $ billions

OPEX / SG&A = operating, selling, general and administrative expenses as reported on income statement

(excludes affiliate spend)

Projects under

construction in 2015 Base & other

20

40

2014 2015 2016 2017 2018

$25-28

guidance

$17-22

guidance

11 © 2016 Chevron

40% 45% 60% 65%

2015 2016 2017 2018

Spend profile

• Increase in shale and tight

• More brownfield opportunities

• Fewer major capital projects

Reduced execution risk

Base and short-cycle

Shorter-cycle, higher return investments

Total capital & exploratory Percentage of capital program

TCO FGP / WPMP Growth MCPs and exploration

Total C&E includes affiliate spend. TCO FGP / WPMP = Tengiz Future Growth Project and Wellhead Pressure

Management Project

12 © 2016 Chevron

Growth

• Major capital projects online

• Shale and tight

Uncertainties / timing

• Divestments

• Price effects

• Spend levels

2015 2016 2017 2018 2019 2020

Growing upstream volume

Projected net production MMBOED

2.62

0-4%

growth*

*Includes estimated impact of divestments

13 © 2016 Chevron

$52/bbl

$60/bbl

$52/bbl

$70/bbl

10

20

30

2015 2017

Growing upstream margin

Projected cash margin* $ per BOE

*Estimated after-tax cash margin based on Chevron’s internal analysis

New barrels accretive

Divestment of

lower margin barrels

Expansion strongly linked

to oil prices

14 © 2016 Chevron

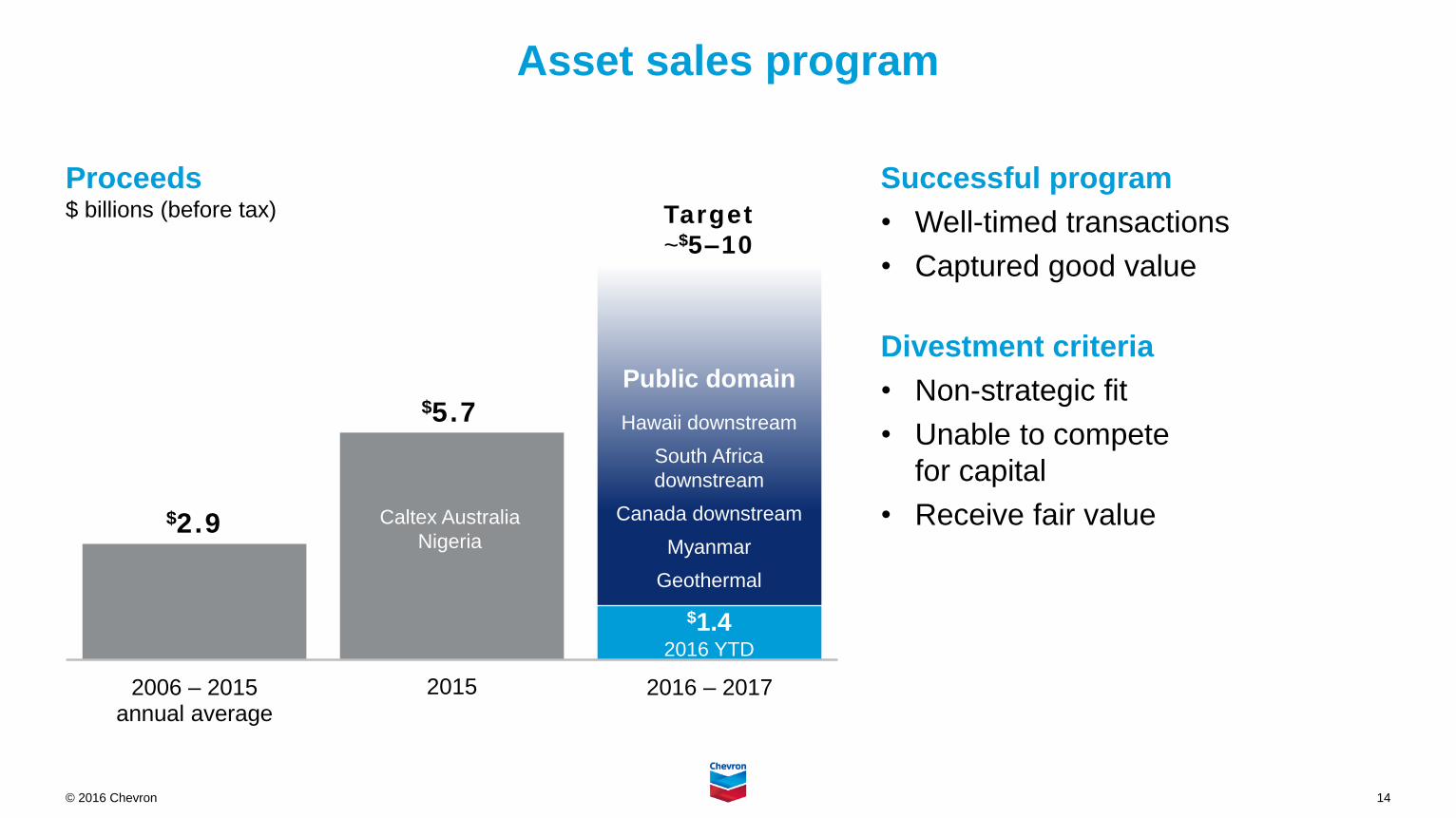

5

10

2006 – 2015 annual average

2015 2016 – 2017

Axis

Tit

le

Asset sales program

Proceeds $ billions (before tax)

Successful program

• Well-timed transactions

• Captured good value

Divestment criteria

• Non-strategic fit

• Unable to compete

for capital

• Receive fair value

Target

~$5–10

Public domain

Hawaii downstream

South Africa

downstream

Canada downstream

Myanmar

Geothermal

$1.4 2016 YTD

$2.9 Caltex Australia

Nigeria

$5.7

15 © 2016 Chevron

BP

XOM

RDS (Post-BG)

TOT

10%

30%

50%

70%

-20 -10 10 20 30 40

Debt capacity: incremental debt capacity to 30% debt ratio ($ billions)

Others: APC, COP, DVN, ENI, EOG, HES, MRO, OXY, STO

Strong balance sheet

Reported annual debt ratio and debt capacity

Source: Public information as of 4Q 2015. ENI based on 3Q 2015 data;

RDS/BG post-deal based on average of analyst estimates

Debt ratio

16 © 2016 Chevron

• Lower pre-productive capital from long-

cycle projects

• More high return, short-cycle and

brownfield spend

• Project execution improvements

• Lower unit operating expense

• Oil-price exposure 5

10

15

5-year 1-year

Source: Adjusted ROCE analysis as of 4Q15 based on Chevron estimates and public information treated on a

consistent basis. Excludes special items. S&P on non-adjusted reported basis.

Pathway to improve returns

Adjusted ROCE Percent

Competitors: BP, RDS, TOT, XOM S&P 500

17 © 2016 Chevron © 2016 Chevron Corporation

Upstream

18 © 2016 Chevron

Source: Wood Mackenzie. Estimate of remaining reserves (on a reported basis) as of 1/1/2016; does not include

sub-commercial resources defined as an estimate of discovered resources not expected to be developed in the

near-term

Upstream portfolio

Strategically positioned geography Percent of total commercial reserve portfolio

Strong, flexible portfolio

• World class legacy assets

• Premier shale positions

• Outstanding mature assets

• Strong deepwater holdings

Competitors: BP, RDS, TOT, XOM CVX

39% 23%

US

7% 12%

Canada

15% 15%

Africa /Latin America

27%

12%

Asia / Oceania

0% 12%

Russia2% 8%

Europe 8% 5%

Caspian

2% 13%

Middle East

19 © 2016 Chevron

Strong reserves performance

Reserve

replacement ratio

107%

1 year

113%

5 year

5 year reserve replacement BBOE

Additions Production

(4.8) 5.6

Asset

sales

10.5 11.2

2010 2015

(0.2)

Numbers do not add due to rounding

20 © 2016 Chevron

2015

Resource

additions

Leading exploration performance

1

2

3

4

$1.22

11.3 BBOE

Resource* adds

10 year total

2006–2015

Unit finding cost

in 2015

62%

Success rate

10 year average

2006–2015

1.8

$1.73

BBOE

Resource* adds

in 2015

57%

Success rate

in 2015

Unit finding cost

10 year average

2006–2015

Source: Wood Mackenzie Company Exploration Benchmarking October 2015 * Recoverable resources as defined in the Supplement to the Annual Report

Competitor range: BP, RDS, TOT, XOM

Discovery costs 2005–2014

$/BOE

21 © 2016 Chevron

Improving efficiency

Deepwater Gulf of Mexico

• Intelligent well completions

enhance economic recovery

• Basin experience and

standardization improving

performance

Technology

• 30% production increase from

artificial intelligence

techniques in California

• 2,000+ critical rotating

machines centrally monitored

Tengiz

• New well stimulation method

reduced costs ~70%

• Debottlenecking increased

production capacity ~16 MBOPD

Average days per 10,000 feet drilled

2013 2014 20152014 2013 2015

Transportation cost reduction

~25%

83 77 59 41

2014 competitor

average 2015

competitor average

2012 2014 2013 2015

22 © 2016 Chevron

Gorgon / Wheatstone

Gorgon

• Train 1

– Current rate ~90 MBOED

– Producing at 70% capacity

– Full capacity expected by 4Q16

• Train 2 first LNG early 4Q16

• Train 3 first LNG 2Q17

Wheatstone

• All 9 wells flow tested and ready for production

• Plant structural, piping and cabling work

currently ahead of plan

• Train 1 first LNG expected mid-2017

• Train 2 first LNG expected 6-8 months after

Train 1

23 © 2016 Chevron

Other 2016 start-ups

Mafumeira Sul • All four platforms installed

• Hook-up & commissioning ongoing

• First production expected 2H 2016

Chuandongbei • All three trains online

Alder • First production

expected 2H 2016

Bangka • First production

expected 2H 2016

Angola LNG • Achieved 75% capacity

• Four LNG cargoes shipped post restart

• Planned shut-down for strainer maintenance is underway

• Sustained production expected 3Q16

24 © 2016 Chevron

Leveraging Permian performance to other shale & tight assets

Duvernay

• Appraisal program advancing

• Best-in-class drilling; days per

well reduced ~35%

• Unit development cost

decreased ~35%

Appalachia

• Pacing investment

• Well costs reduced ~35%

• Cycle time shortened ~45%

• EUR increased ~30%

• Unit development cost

decreased ~40%

Vaca Muerta

• Initiated horizontal factory mode

• Horizontal well costs reduced ~20%

• Improved well designs have

achieved IP rates ~800 BOED

• Unit development cost

decreased ~30%

Appalachia baseline 1Q 2014 Duvernay baseline 2H 2014 Vaca Muerta baseline 4Q 2014

25 © 2016 Chevron

Competitive Permian growth

Advantaged acreage

• ~2 MM acres

‒ 1 MM acres in Delaware Basin

‒ 0.5 MM acres in Midland Basin

• ~85% no or low royalty

• ~9 BBOE resource1

1 Potentially recoverable resources as defined in the Supplement to the Annual Report

2 Figures reflect cumulative well counts for ~30% of operated acreage

Breakevens per Wood Mackenzie definition: 10% rate of return at flat real oil price 3 Per Wood Mackenzie, top eight acreage holders in the Delaware and Midland Basins 4 Reflects CVX shale and tight production only

500 1000 1500 2000

Midland & Delaware net acres3 (1000 acres)

Chevron

Net production4 – Midland & Delaware MBOED

100

200

300

400

2014 2015 2016 2017 2018 2019 2020

Base decline Growth Growth range Actual production

Chevron

2015 2017 2016 2018 2020 2019

1,300

4,000

5,500

<$40 <$50 <$60

Breakevens2 $ WTI

26 © 2016 Chevron

$0

$5

$10

$15

$20

2Q15 3Q15 4Q15 1Q16 2Q16

Chevron operated Non-operated JV

Competitive Permian growth

Well information Total D&C ($MM)

Pad Lateral (ft.) Best Avg

Salado Draw 5,000 3.5 3.7

Bradford Ranch 7,500 5.5 5.6

Greater Bryant G 7,500 4.9 5.6

Greater Bryant G 10,000 6.7 7.2

Recent CVX cost performance2 (YTD 2016)

1 Includes drilling, completion, facilities, and G&A costs 2 Includes drilling and completion costs only

Competitive development costs

• Paced, efficient development of

prioritized queue

• JV and industry best practices have

allowed accelerated learning

• EUR performance on target

Improvements continue

• Cost reductions in both drilling and

completions

• Characterization of our acreage

• Future developments will benefit from

infrastructure investments made today

Average development cost1

$/BOE

27 © 2016 Chevron

Base projects

Well factories

• Gulf of Thailand

• San Joaquin Valley

• Indonesia

Asset enhancements

• Infill drilling

• Debottlenecking and

reliability upgrades

Base deepwater

• Focused on development of

existing assets

• Agbami, Tahiti, Jack / St. Malo,

Caesar Tonga, Mad Dog

Platong II Tahiti Tengizchevroil Second Generation Project

28 © 2016 Chevron

FGP / WPMP

Final investment decision (FID) in July

Wellhead Pressure Management Project

(WPMP)

• Lower back-pressure on wells to maintain

the existing plants at full capacity

Future Growth Project (FGP)

• Increasing capacity ~260 MBOED utilizing

proven technology

• Improves reservoir recovery

• Extends the production plateau by

increasing TCO gas handling capability

Expected incremental recovery ~2 BBOE

Production profile

All figures shown are TCO 100%

Original Plant

Second

Generation Plant WPMP

FGP

Start-up in 2022

29 © 2016 Chevron

FGP / WPMP financials

Project cost

• Total: $36.8 B

– Facilities: $27.1 B

– Wells: $3.5 B

– Contingency / Escalation: $6.2 B

• ~$18/BOE project development cost

Financing in place

Accommodation building construction All figures shown are TCO 100%

30 © 2016 Chevron

FGP / WPMP execution readiness

Project engineers assigned to equipment packages from design

through start-up; Quality Control personnel co-located at main factories

5,300 camp beds available now; dredging ~50% complete;

fabrication starts after 90% model review

Module fabricator involved in early design; integration of owner and

EPC teams; matching scope of work to contractor capabilities

Process design and specifications of major equipment verified;

facilities hazard & operability studies complete at FID

Strengthening design

assurance

Optimizing contracting

strategy

Verifying execution

readiness

Improving quality

management

Engineering > 50% at FID; underground piping, electrical and

foundations in 3D model; 85% of equipment on order at FID

Increasing engineering

maturity at FID

Critical lessons learned incorporated into FGP / WPMP design and planning

31 © 2016 Chevron

FGP / WPMP

Builds on previous successes

• Great partnership

• World class reservoir

• Proven technology

Now is the time

• Reservoir pressure decline

• Capture market opportunities

• Project synergies

Upside potential

• Future infill wells

• Debottlenecking opportunities

32 © 2016 Chevron

Future major

capital project

Shale & tight

Conventional

exploration &

appraisal wells

Liard Basin

Horn River Basin

Duvernay Marcellus

Utica

Bonga SW / Aparo

Captain EOR

TCO FGP / WPMP

Gendalo-Gehem

Midland &

Delaware Basins

Rosebank

Tahiti Vertical Expansion

Mad Dog 2 Wafra

Steamflood

Vaca Muerta

Kurdistan Region of Iraq

Deepwater

Gulf of Mexico Suriname

Republic of Congo

Nigeria

Western Australia

Bight Basin

Kitimat

LNG

Ubon

Tahiti Upper Sands Development

Future opportunity queue

Agbami Infill

33 © 2016 Chevron © 2016 Chevron Corporation

Downstream & Chemicals

34 © 2016 Chevron

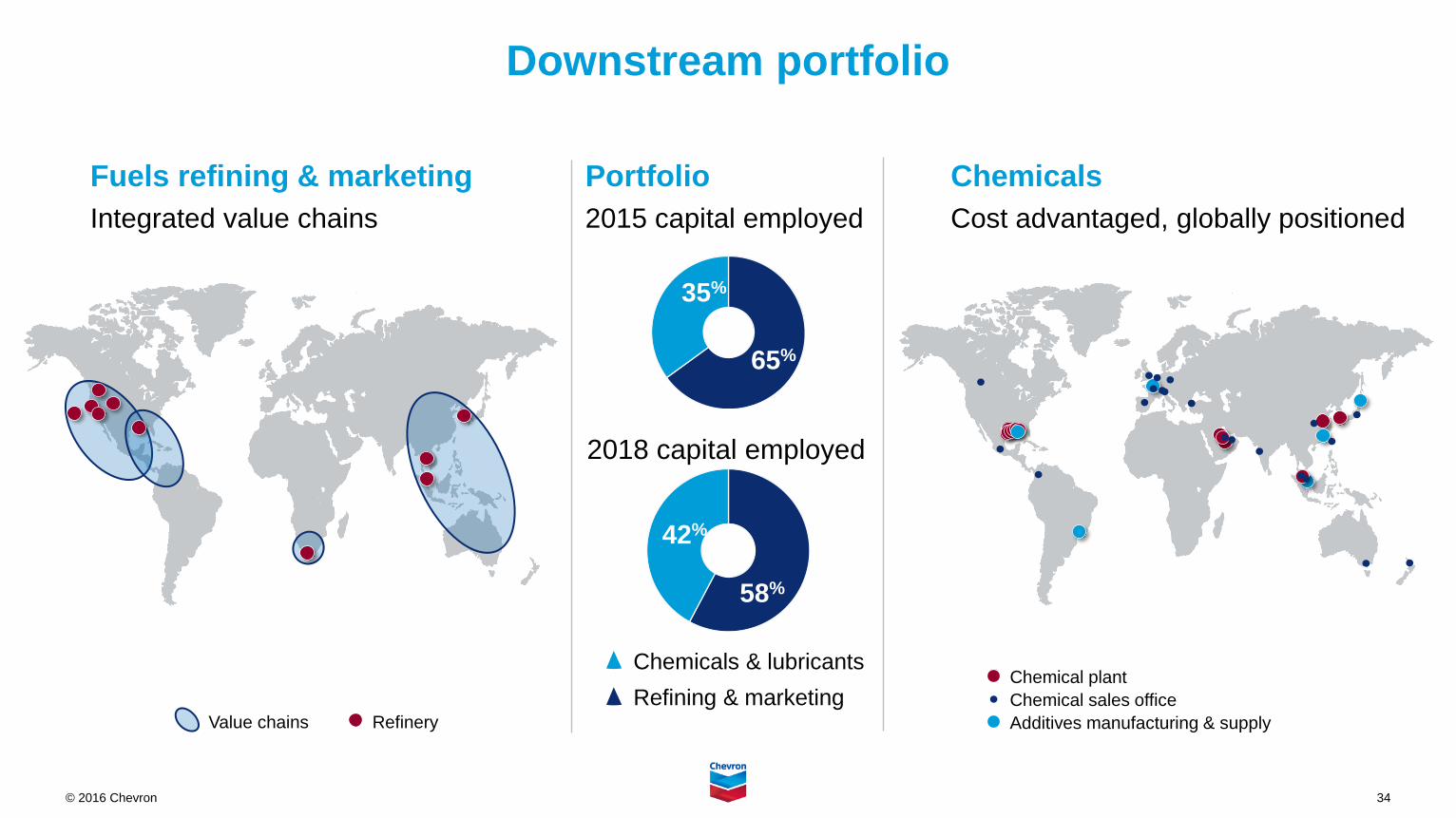

Downstream portfolio

Chemicals

Cost advantaged, globally positioned

Fuels refining & marketing

Integrated value chains

Portfolio

2015 capital employed

Chemicals & lubricants

Refining & marketing

35%

65%

2018 capital employed

42%

58%

Chemical plant

Chemical sales office

Additives manufacturing & supply Value chains Refinery

35 © 2016 Chevron

Strategy focused on competitive returns

Deliver competitive returns and grow

earnings across the value chain

• Improve operational excellence

• Grow higher return segments

– Petrochemicals

– Lubricants and additives

• Focused refining and marketing

• Integration with upstream

• Increase near-term cash

36 © 2016 Chevron

0% 5%

Gasoline

Distillate

Finished Lubricants

Additives

Petrochemicals*

Premium Base Oil

Demand growth points to attractive segments

2015–25 global product demand growth Compound annual growth rate

2015-25 global fuels demand growth MMBD

Distillate Gasoline

Source: NexantThinking™, Kline & Company, Wood Mackenzie and Chevron estimates *Ethylene, propylene, butadiene, benzene, and paraxylene

-2

0

2

4

6

NorthAmerica

Europe /Middle East

LatinAmerica

Asia Pacific

37 © 2016 Chevron

Levels the playing field

• U.S. light-sweet crude gets global

parity pricing

• U.S. heavy coking margins improve

relative to U.S. light cracking margins

• Minimal impact to California refiners

Impact of lifting the U.S. crude export ban

2015 U.S. crude capacity by region

Source: EIA as of November 2015

50%

100%

Chevron Industry

East coast West coast Gulf coast Mid-continent

38 © 2016 Chevron

Chevron Phillips Chemical USGC petrochemicals project

Overview

• 1,500 kMTA ethylene, Baytown, Texas

• 1,000 kMTA polyethylene, Old Ocean, Texas

– 500 kMTA HDPE

– 500 kMTA LDPE

• Advanced proprietary technology

Progress

• ~80% complete (>6,000 people onsite)

• Polyethylene reactors in-place

• Ethylene major compressors in place; furnace

erection in progress

• Projected start-up 2017