Embed Size (px)

Citation preview

Retail Clinics Retail Clinics ––The Current Environment with a The Current Environment with a California UpdateCalifornia UpdateCalifornia UpdateCalifornia Update

bFebruary 2009Mary Kate Scott

© Scott & Company, Inc. 2009

CHCF commissioned two independent reports on clinics CHCF commissioned two independent reports on clinics to determine the opportunity to increase access to the to determine the opportunity to increase access to the underserved and a toolkit for CCHCs to develop underserved and a toolkit for CCHCs to develop strategies based on clinic principlesstrategies based on clinic principles

© Scott & Company, Inc. 2009 2

The first law of technology says…The first law of technology says…

“With every change in technology that affects consumer behavior we always ff y

overestimate the impact in the short term but then underestimate the full impact over f p

the long term.”

© Scott & Company, Inc. 2009 3

TraditionallyTraditionally retail clinics are retail clinics are inside a store, inside a store, operated by a clinic provideroperated by a clinic provider

• Inside a retail store • Offer routine medical care on an

ongoing basis• Staffed with NPs who can write

prescriptionsprescriptions

Clinic

© Scott & Company, Inc. 2009 4

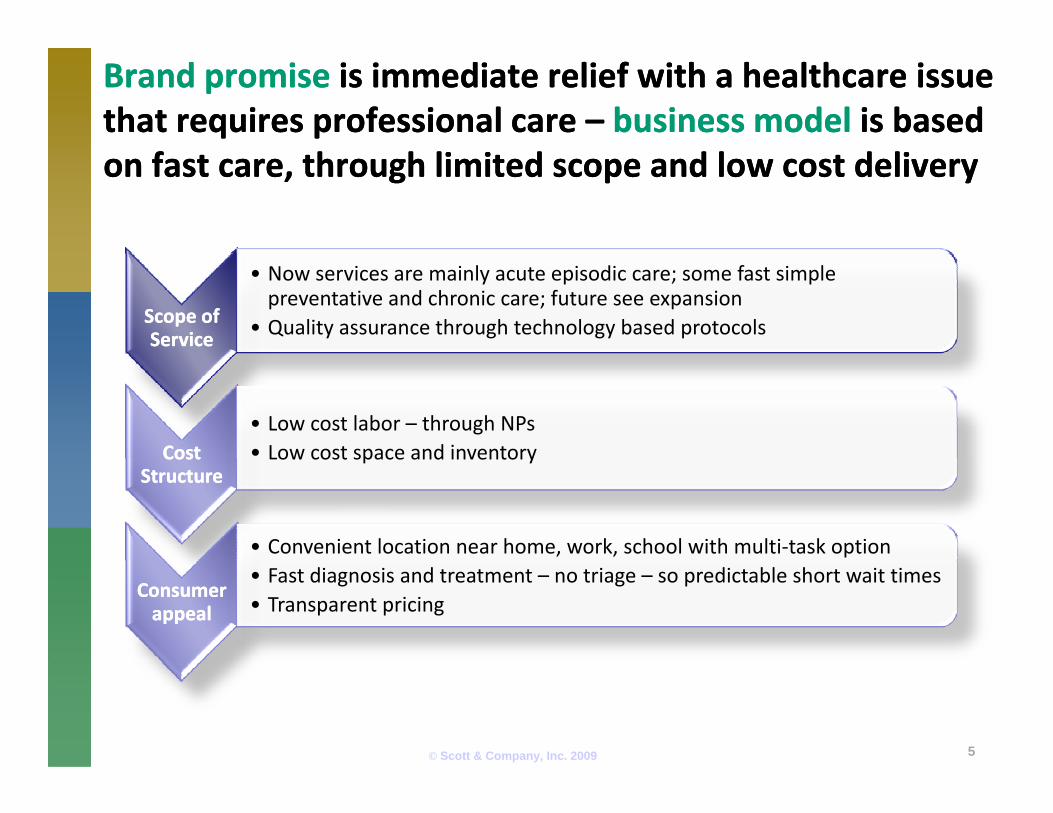

Brand promise Brand promise is immediate relief with a healthcare issue is immediate relief with a healthcare issue that requires professional care that requires professional care –– business model business model is based is based on fast care, through limited scope and low cost deliveryon fast care, through limited scope and low cost delivery

Scope of Scope of ServiceService

• Now services are mainly acute episodic care; some fast simple preventative and chronic care; future see expansion

• Quality assurance through technology based protocols

CostCost• Low cost labor – through NPs• Low cost space and inventoryCost Cost

StructureStructureLow cost space and inventory

• Convenient location near home, work, school with multi‐task option

Consumer Consumer appealappeal

• Fast diagnosis and treatment – no triage – so predictable short wait times• Transparent pricing

© Scott & Company, Inc. 2009 5

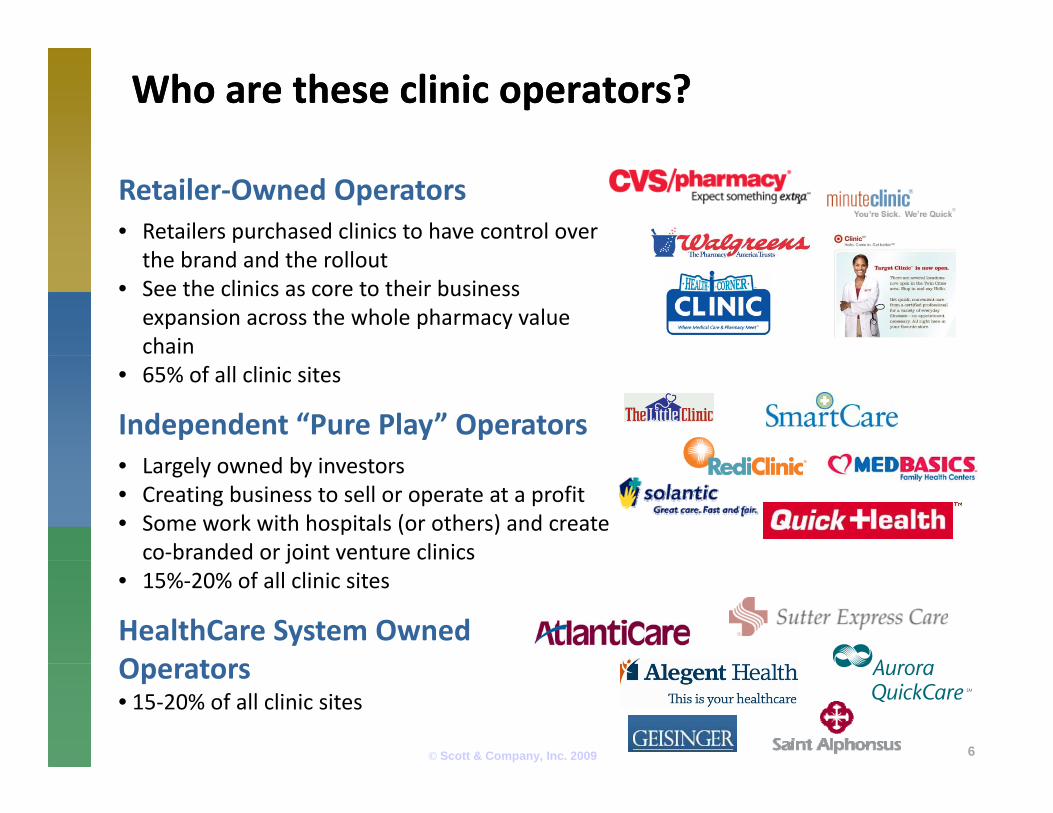

Who are these clinic operators?Who are these clinic operators?

Retailer‐Owned Operators• Retailers purchased clinics to have control over

h b d d h llthe brand and the rollout• See the clinics as core to their business expansion across the whole pharmacy value chain

• 65% of all clinic sites

Independent “Pure Play” OperatorsL l d b i• Largely owned by investors

• Creating business to sell or operate at a profit• Some work with hospitals (or others) and create co‐branded or joint venture clinicsj

• 15%‐20% of all clinic sites

HealthCare System Owned O t

© Scott & Company, Inc. 2009

Operators• 15‐20% of all clinic sites

6

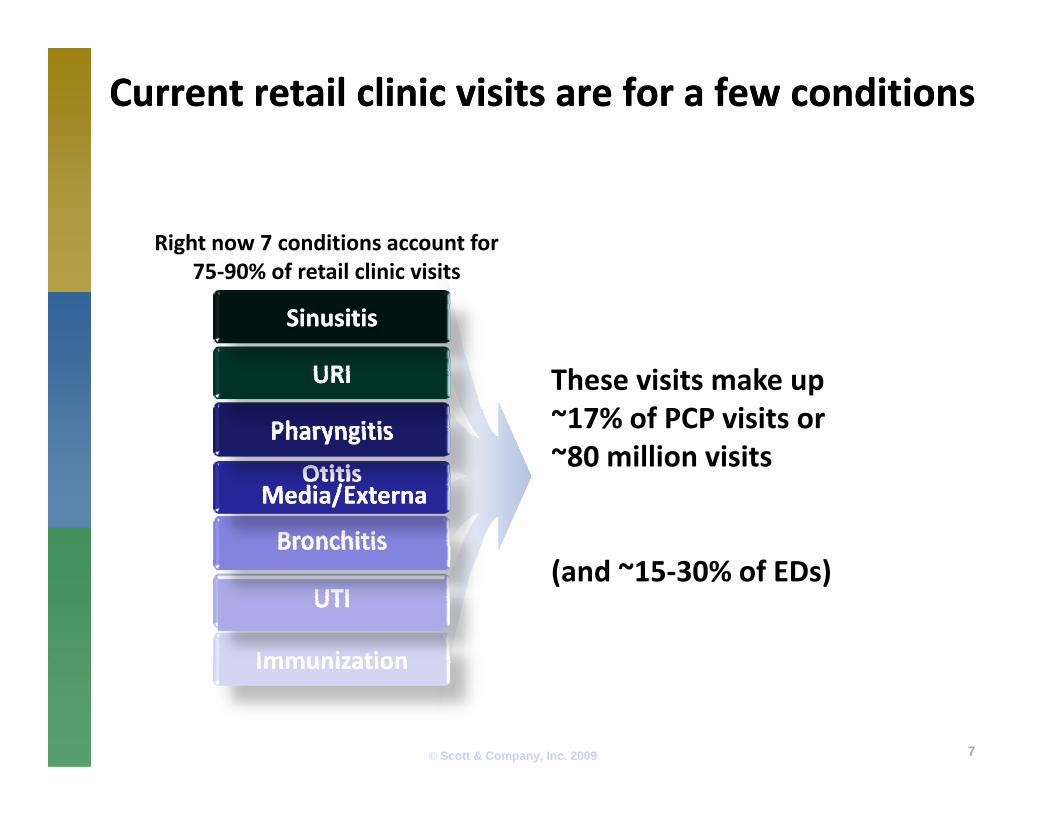

Current retail clinic visits are for a few conditionsCurrent retail clinic visits are for a few conditions

Right now 7 conditions account for g75‐90% of retail clinic visits

SinusitisSinusitis

PharyngitisPharyngitis

URIURI These visits make up ~17% of PCP visits or ~80 million visits

BronchitisBronchitis

Otitis Otitis Media/ExternaMedia/Externa

80 million visits

( d f )

ImmunizationImmunization

UTIUTI(and ~15‐30% of EDs)

© Scott & Company, Inc. 2009

ImmunizationImmunization

7

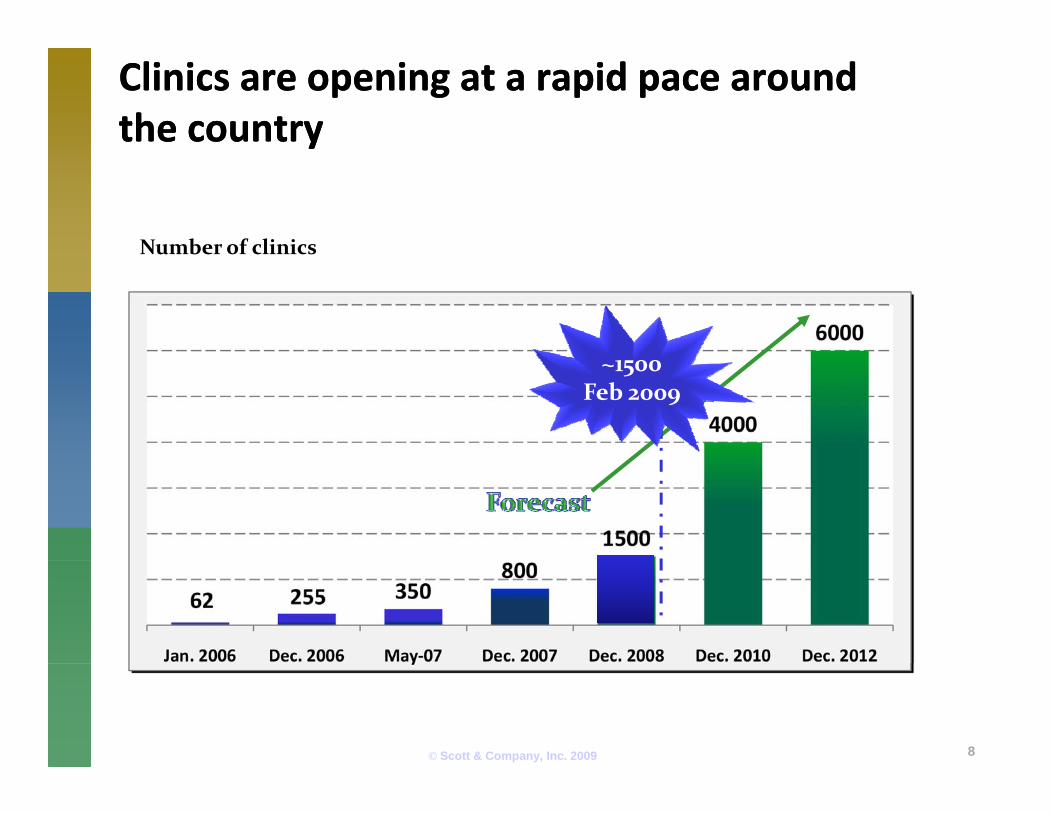

Clinics are opening at a rapid pace around Clinics are opening at a rapid pace around the countrythe country

Number of clinicsNumber of clinics

~1500Feb 2009

© Scott & Company, Inc. 2009 8

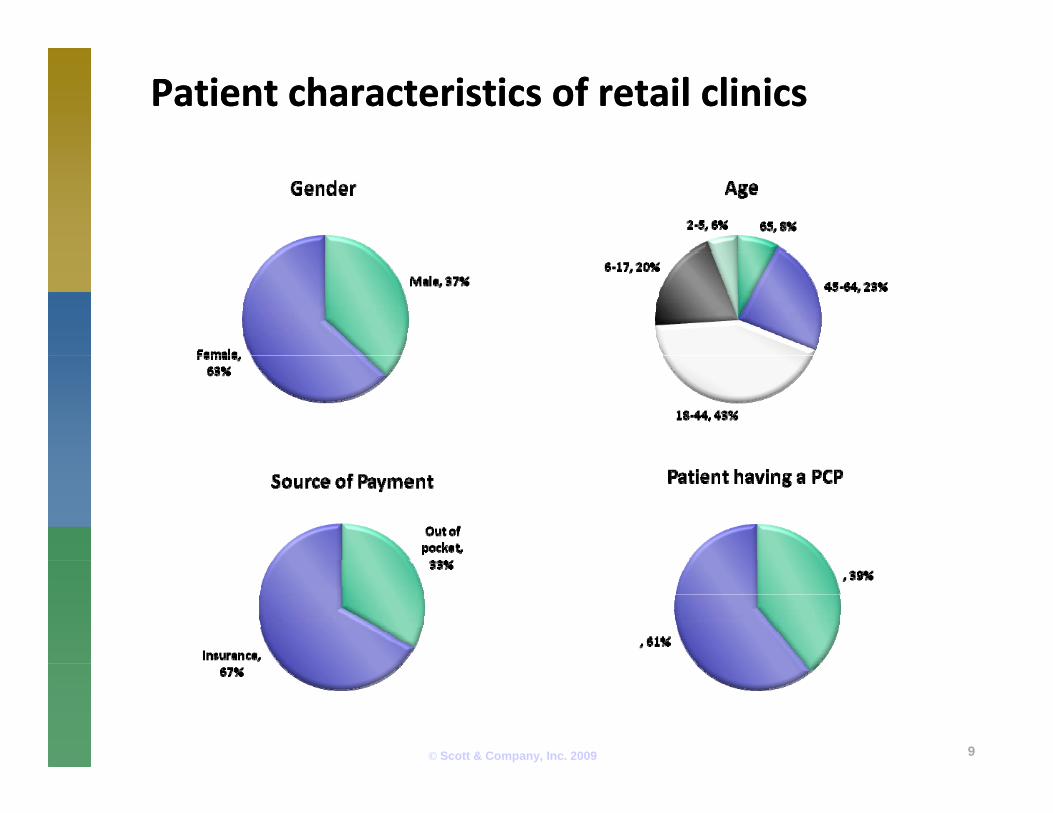

Patient characteristics of retail clinicsPatient characteristics of retail clinics

© Scott & Company, Inc. 2009 9

Consumer Satisfaction Remains HighConsumer Satisfaction Remains High

“Overall, how satisfied were you with your or your family member’s experience using an onsite health clinic in a pharmacy or retail chain on the following items?"

‐ Harris Interactive Survey, April 2007

“Very” or “Somewhat” Satisfied

© Scott & Company, Inc. 2009 10

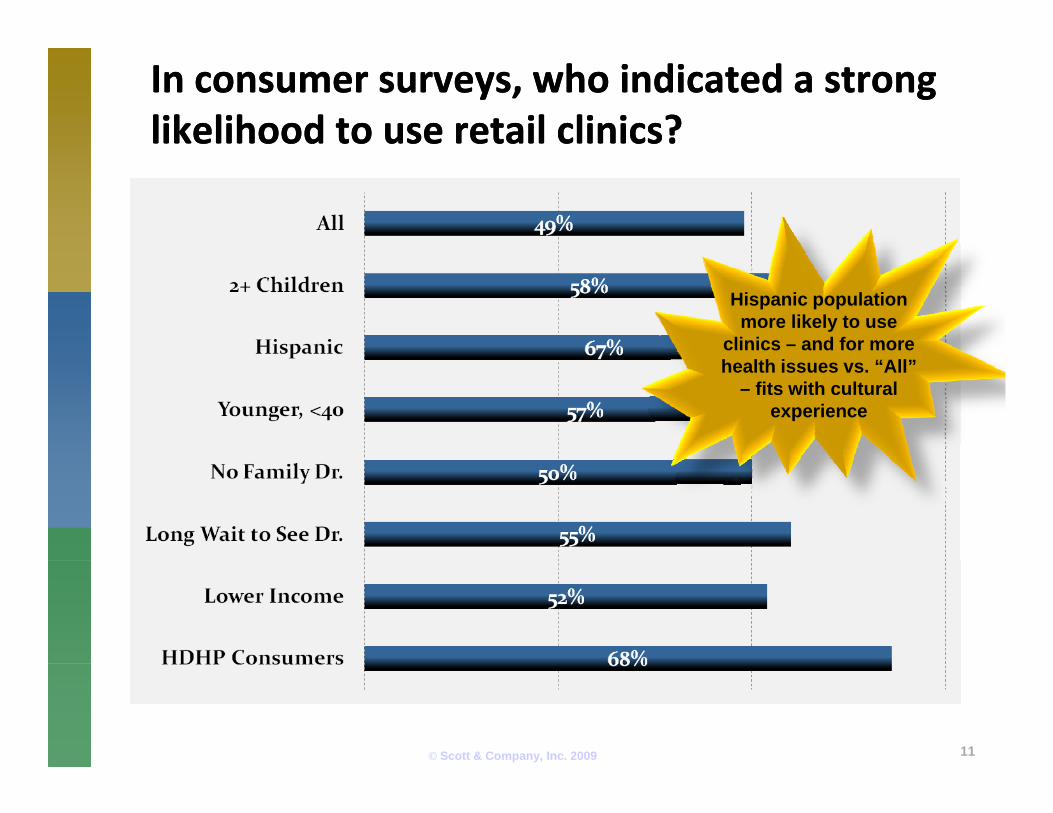

In consumer surveys, who indicated a strong In consumer surveys, who indicated a strong likelihood to use retail clinics?likelihood to use retail clinics?

Hispanic population more likely to use

clinics – and for more health issues vs. “All”

– fits with cultural experience

© Scott & Company, Inc. 2009 11

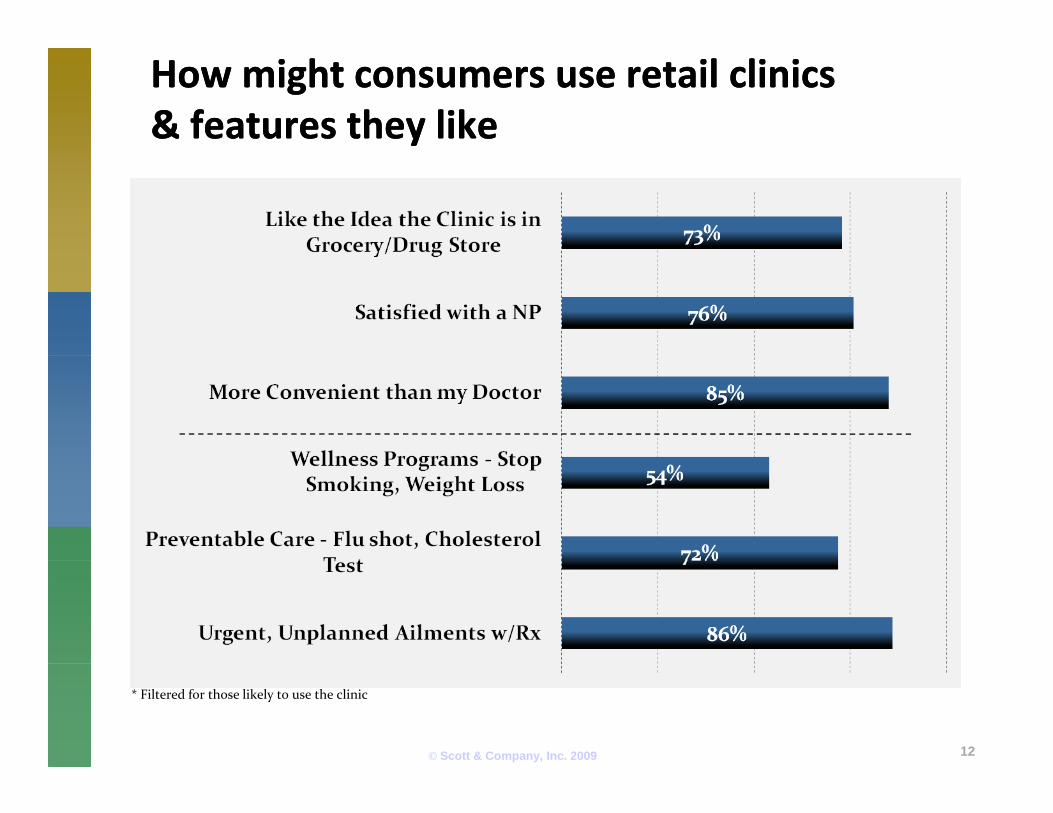

How might consumers use retail clinics How might consumers use retail clinics & features they like& features they like

© Scott & Company, Inc. 2009

* Filtered for those likely to use the clinic

12

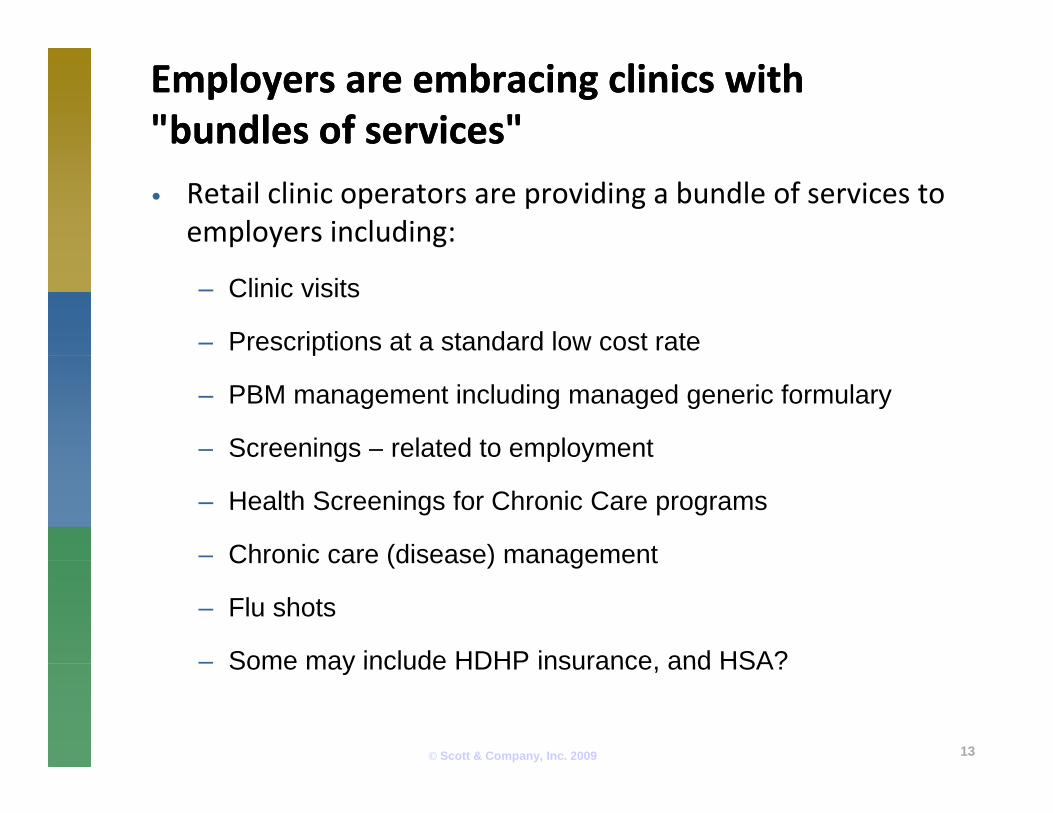

Employers are embracing clinics with Employers are embracing clinics with "bundles of services""bundles of services"• Retail clinic operators are providing a bundle of services to

employers including:

– Clinic visits

– Prescriptions at a standard low cost ratep

– PBM management including managed generic formulary

– Screenings – related to employmentg p y

– Health Screenings for Chronic Care programs

– Chronic care (disease) managementChronic care (disease) management

– Flu shots

– Some may include HDHP insurance and HSA?

© Scott & Company, Inc. 2009

– Some may include HDHP insurance, and HSA?

13

Clinics are part of "mainstream" healthcareClinics are part of "mainstream" healthcare

• Broad target market ‐ not just wealthy seeking convenience or uninsured seeking access – 62% of patients don't have a physician relationship

• 63% of clinic patients have insurance – and 95% of clinics accept63% of clinic patients have insurance and 95% of clinics accept insurance – halo effect but also it fits with consumer expectations

• High deductible plans are (finally) shifting the consumer into an active healthcare shopper and seeking affordable alternativeshealthcare shopper and seeking affordable alternatives

• Employers are pushing for retail clinic adoption

Clinics are expanding services and marketing the clinics• Clinics are expanding services and marketing the clinics

• Clinic operators are part of corporate America

Biggest growth in operators are coming from healthcare systems with• Biggest growth in operators are coming from healthcare systems – with strong interest from FQHC/CHCs

© Scott & Company, Inc. 2009 14

Clinics now certified under Jefferson CollegeClinics now certified under Jefferson College

© Scott & Company, Inc. 2009 15

What about quality of care?What about quality of care?

• Several studies on quality care:

• Health Affairs/RAND

• American Journal of Medical Quality

• Overprescribing: preliminary data suggests there are fewer Rx ibl d t ti ht t l th ibi th it f thpossibly due to tighter controls on the prescribing authority of the

NP

• Appropriate use of clinics: 2.3% triaged to an ED or PCP; consumers appear to understand how and when to use clinics

• No malpractice suit

• Disruption of PCP relationship: 62% don’t have a PCP relationships – there isn’t a medical home to disrupt – and it’s not a lack of insurance

© Scott & Company, Inc. 2009 16

• Limited number of clinical issues – decision making is supported by electronic protocols

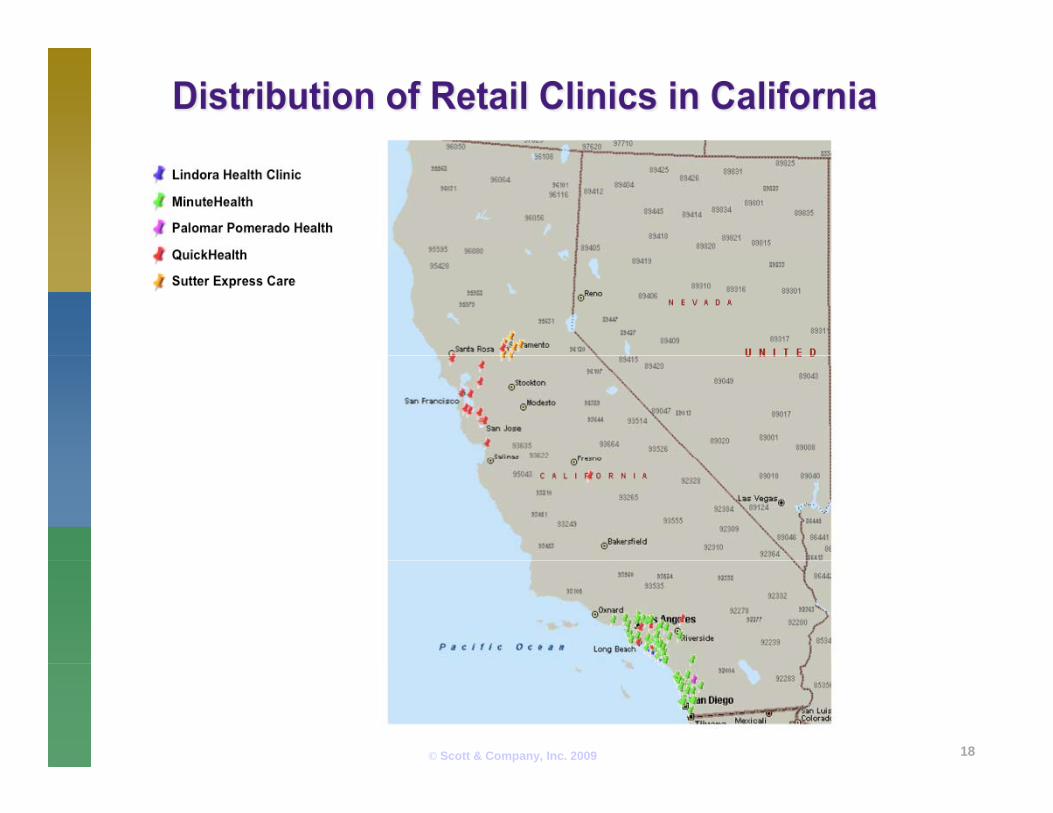

The California retail clinic marketplaceThe California retail clinic marketplace

• Large market with consumers familiar with the model – Highest number of uninsured in the country and most undocumented people

• MinuteClinic largest player with 80+ clinics – and a marketing campaign g p y g p gincluding full page color LA Times, in‐store signage, radio

– CVS only in Southern California (where CVS is located)

• Other players: QuickHealth, Sutter, Lindora, Palomar

• Blue Shield/Blue Cross strongly supportive – in all plans, low/same co‐pay; Nurse lines recommend Retail Clinics

• Wal‐Mart seeking to expand retail clinic locations – interested in CA

• Biggest challenges for operators: Expensive complex market– Corporate Practice of Medicine restricts ownership and would require a

separate physician owned model – higher administrative costs, less margin

– High cost labor (NPs); higher cost space, and marketing expensive• Strong penetration of Kaiser HMO model that excludes retail clinic

© Scott & Company, Inc. 2009

• Strong penetration of Kaiser HMO model that excludes retail clinic visits

17

© Scott & Company, Inc. 2009 18

Contact detailsContact details

Mary Kate ScottMary Kate ScottScott & Company, Inc.Scott & Company, [email protected]@MaryKateScott.com310310‐‐822822‐‐6130 office6130 office

© Scott & Company, Inc. 2009 19