Embed Size (px)

Citation preview

CHAPTER – IV

IMPACT OF PRIORITY SECTOR LENDING ON

URBAN CO-OPERATIVE BANKS

A) INTRODUCTION

B) BACKGROUND OF AURANGABAD AND

JALNA DISTRICTS

C) FINANCIAL POSITION AND

PERFORMANCE OF URBAN CO-

OPERATIVE BANKS IN AURANGABAD

AND JALNA DISTRICTS

D) ANALYSIS OF PRIORITY SECTOR

LENDING DATA OF SELECTED URBAN

CO-OPERATIVE BANKS.

E) ANALYSIS OF MAJOR FINANCIAL

INDICATORS OF SELECTED URBAN CO-

OPERATIVE BANKS.

F) STUDY OF RECENT PERFORMANCE OF

THE SELECTED URBAN CO-OPERATIVE

BANKS.

CHAPTER NO. IV

IMPACT OF PRIORITY SECTOR LENDING ON

URBAN CO-OPERATIVE BANKS

The Urban co-operative banks have passed through many phase since

the enactment of the agriculture credit co-operative Societies Act, 1904.

Presently the Urban co-operative banks are facing number of problems

mainly problem of overdue, increasing amount of NPA, competition with

foreign, private and public commercial banks, political interference, lack of

trained personnel, low profitability etc. These banks are required to lend

60% of their total lending to priority sector. 25% of the priority sector

lending shall be given to weaker section of the society. Some experts

believe that the priority sector lending is the one of the major cause of the

poor performance of the number of urban banks.

The present chapter is an attempt to study the impact of priority sector

lending by the urban banks in Aurangabad and Jalna district. Priority sector

lending reports and annual reports of the selected banks for the period from

1995-96 to 2004-05 have been reviewed on the basis of various aspects such

as sub-sector wise study of loans sanctioned, amount advanced, amount of

overdue, profitability, Net NPA, Net GPA etc.

Background of Aurangabad Districts

Aurangabad is a regional headquarter of the Marathwada region. The

district headquarters situated on kham river is a place of great attraction for

the tourists because of numerous ancient remains. Aurangabad district is

famous for Ajanta caves, Ellora caves, Daultabad (Deogiri) Fort, Paithan,

84

Pawan Chakki and Bibi ka maqbara. Aurangabad district is a great center of

culture activities and place of political activities. Aurangabad is also an

industrial city and a good center of education having number of excellent

educational institutes. Dr. Babasaheb Ambedkar Marathwada University is

situated in Aurangabad, imparting and monitoring higher education in

Aurangabad, Jalna, Beed and Osmanabad districts of the Marathwada

region.

The geographical area of Aurangabad district is nearly 8900 Sq. kms.

Aurangabad district includes Kannad, Sillod, Soygaon, Khultabad, Vaijapur,

Gangapur, Aurangabad, Paithan and Fulambri talukas. The major rivers

flowing through the district are Godavari, Dudhana, Kham, Purna, Vaghur,

Kelna, Anjana, Girja, Shivana, Yelganga etc. The average rainfall in the

district is 725 mm and the temperature ranges between 130 to 42

0C.

According to 2001 census report the population of Aurangabad district was

2920348 and the literacy rate was 73.63 %.

District of Aurangabad is continuously a place of draught and

inadequate rainfall, bad and rocky land, less proportion of fertile land and

lack of perennial water source. All these aspects always hampered the

agricultural prospects of the district. It was Jayakwadi Project which filled

the breath in the farming economy of the district.

Till Nizam’s time the district had only traditional village industry

which has direct contribution in the village or local economy but not in the

district as such and not in the state. It only provided needs of society and

inadequate subsistence to the village professionals. Fortunately the Constant

& efforts of Government for upliftment of society gave fruits, though with

very slow pace, and various aspects including economy and industry grew

85

to the betterment. The best policy of the Government was the foundation of

the Maharashtra Industrial Development Corporation (MIDC). Similarly,

various financing institutes like SICOM, MSFC, MSSIDC, Regional

Development corporations, District Industrial Centers, Khadi Village

Industrial Corporation, Women Economical Development Corporation and

various schemes floated for time to time have also contributed in the

development of Aurangabad district. Aurangabad district received first

Industrial Estate called Chikalthana. Now Aurangabad has 5 major

industrial estates. The industrial estates are located at Chikalthana, Waluj,

Railway Station, Paithan road area, and at Paithan.

Communication of all types is an important factor in the development

of the society. Aurangabad is well connected with distance area through

railway, road and air transport system. (1)

Background of Jalna Districts

Jalna become the district in 1981. Prior to May, 1981 Jalna district

was a part of Aurangabad district. The district headquarters is situated on

Kundlika river. Jamb Samrtha in Jalna district is well known as a birth place

of Swami Ramdas Samarth. Asai in Jafrabad taluka is a famous place

known for the battle of 1803 between British and Maratha. Bhokardan, a

taluka headquarters is famous for early historical habitation and caves of

vakataka period.

Jalna is known as the seed capital of India. There are nearly 35 seed

processing units. Mahico Seeds Co., Mahendra Seeds Co., Safal Seeds Co.,

86

Krishidhan Seeds Co. etc. are well-known seeds companies in national as

well as in international market.

Re-rolling mills and steel companies have been flourished during last

30 years and the steel market is well known in Maharashtra.

Jalna is a well-known trading center of Maharashtra. Jalna grain

market is famous for certain goods all over the country.

The geographical area of Jalna is nearly 7405 Sq. kms. Jalna district

includes Jalna, Ambad, Bhokardan, Jafrabad, Partur, Mantha, Badnapur and

Ghansawangi talukas. The major rivers flowing through the district are

Godavari, Dudhana, Kundalika, Purna, Girja, Khelana, Galhati, Kalyan,

Jiverkhi, Jui, Dhamana etc. The average rainfall in the district is 730 mm

and the temperature ranges between 70 to 42

0 C. According to 2001 census

report, the population of Jalna district was 1612357.

The district has inadequate water sources including rain. Major area is

irrigated under well and artificial irrigation system which is still

undeveloped and inadequate. The district does not have major irrigation

project. The project of Jayakwadi of Paithan in Aurangabad district has

some influence over this district. The small farmers are greater in number

and that has immense effect on the agricultural product. The production and

yield of the major crops is much less as compare to the other districts of

Maharashtra. According to 1991 census report, 46.63% of the district

population was farmers and 36.16% were agricultural labours. This shows

that major portion of the population is dependent upon farming.

87

Jalna is one of the industrially backward district of Maharashtra state.

Jalna has four major Industrial estates. The first Industrial estate came into

existence in the year 1962 on co-operative basis which is situated near the

Christian grave yard. The second Industrial estate came into existence after

1980 which is situated on Aurangabad road. Industrial estates have also

been established in Partur and Ambad. The industrial development in the

district has accelerated to some extent only after establishment of District

Industrial Center in 1982.

Jalna is a major railway station on Mumbai-Kacheguda railway line.

It is well connected with distance area through railway and road. However,

development of new railway routes is very important for the development of

trade, commerce and industry in the Jalna districts.

Among many other problems, irregular and inadequate supply of

water is the burning problem of Jalna district which is hampering the

development of the district. (2)

Financial Position and Performance of Urban Co-operative Banks in

Aurangabad District.

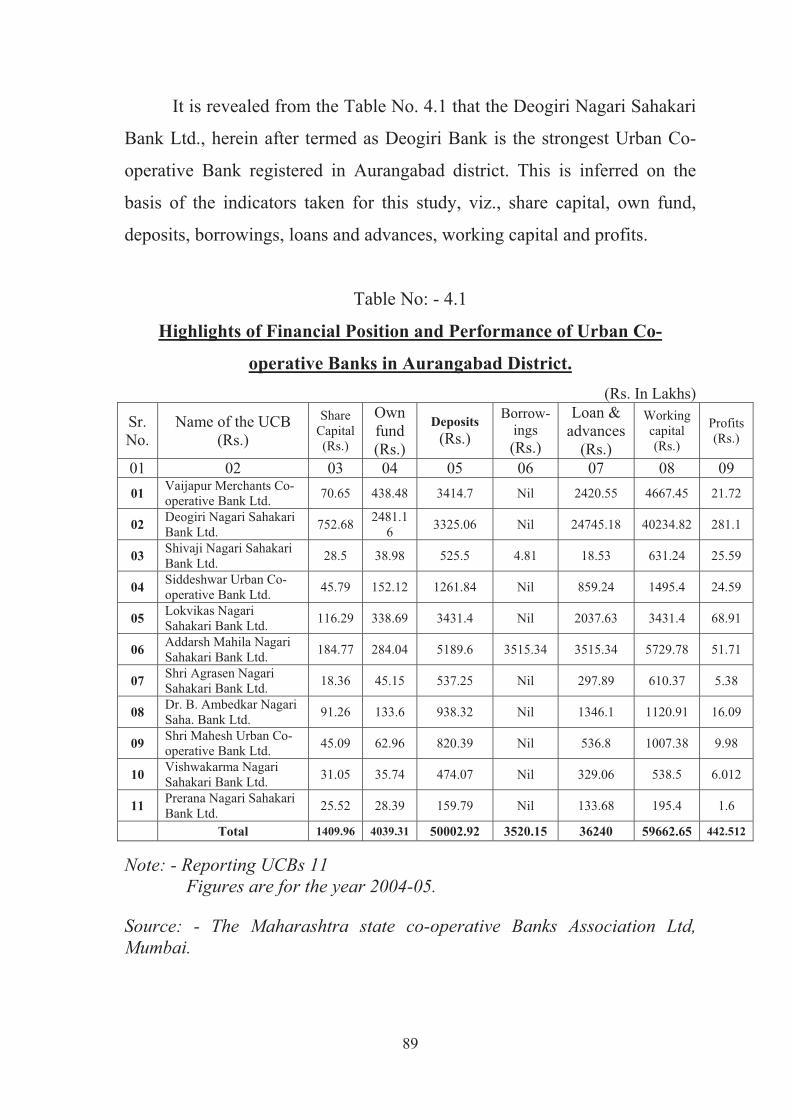

The researcher has used secondary data for this purpose. According

to the available data for the year 2004-2005, there were 16 UCBs registered

in Aurangabad district. Table No. 4.1 provides better insight of the financial

position and performance of UCBs registered and operating in Aurangabad

district.

88

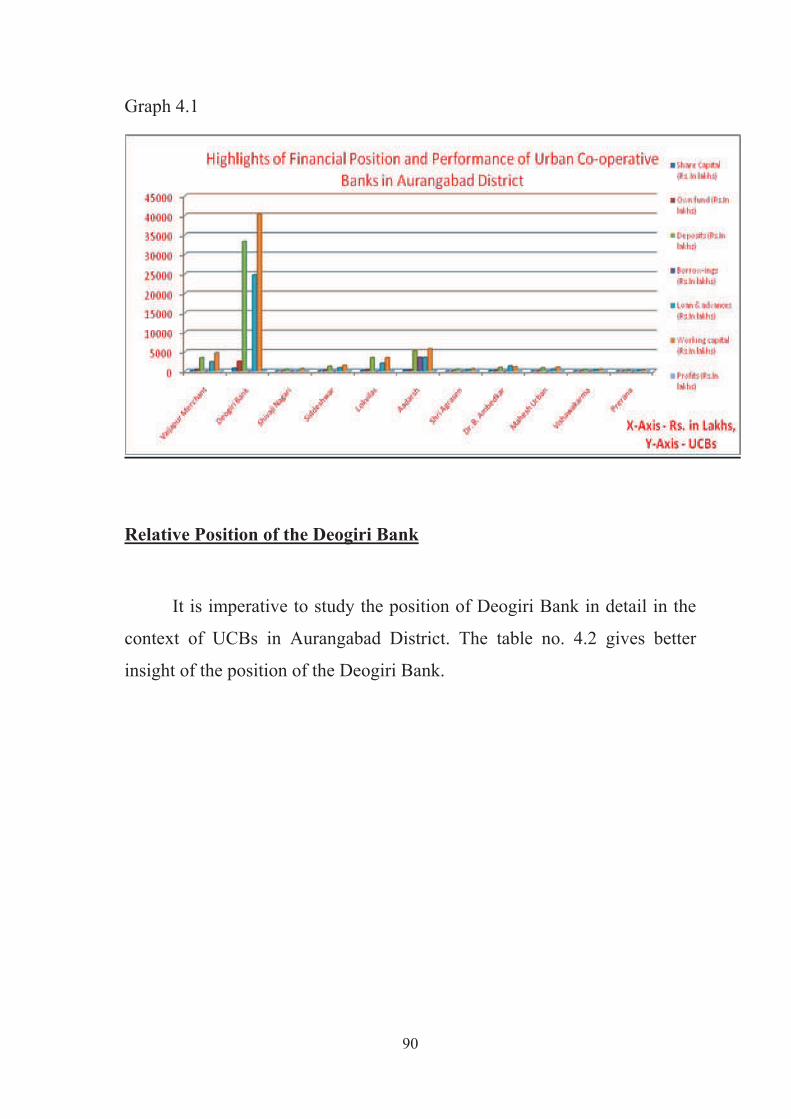

It is revealed from the Table No. 4.1 that the Deogiri Nagari Sahakari

Bank Ltd., herein after termed as Deogiri Bank is the strongest Urban Co-

operative Bank registered in Aurangabad district. This is inferred on the

basis of the indicators taken for this study, viz., share capital, own fund,

deposits, borrowings, loans and advances, working capital and profits.

Table No: - 4.1

Highlights of Financial Position and Performance of Urban Co-

operative Banks in Aurangabad District.

(Rs. In Lakhs)

Sr.

No.

Name of the UCB

(Rs.)

Share

Capital

(Rs.)

Own

fund

(Rs.)

Deposits

(Rs.)

Borrow-

ings

(Rs.)

Loan &

advances

(Rs.)

Working

capital

(Rs.)

Profits

(Rs.)

01 02 03 04 05 06 07 08 09

01Vaijapur Merchants Co-

operative Bank Ltd.70.65 438.48 3414.7 Nil 2420.55 4667.45 21.72

02Deogiri Nagari Sahakari

Bank Ltd.752.68

2481.1

63325.06 Nil 24745.18 40234.82 281.1

03Shivaji Nagari Sahakari

Bank Ltd.28.5 38.98 525.5 4.81 18.53 631.24 25.59

04Siddeshwar Urban Co-

operative Bank Ltd.45.79 152.12 1261.84 Nil 859.24 1495.4 24.59

05Lokvikas Nagari

Sahakari Bank Ltd.116.29 338.69 3431.4 Nil 2037.63 3431.4 68.91

06Addarsh Mahila Nagari

Sahakari Bank Ltd.184.77 284.04 5189.6 3515.34 3515.34 5729.78 51.71

07Shri Agrasen Nagari

Sahakari Bank Ltd.18.36 45.15 537.25 Nil 297.89 610.37 5.38

08Dr. B. Ambedkar Nagari

Saha. Bank Ltd.91.26 133.6 938.32 Nil 1346.1 1120.91 16.09

09Shri Mahesh Urban Co-

operative Bank Ltd.45.09 62.96 820.39 Nil 536.8 1007.38 9.98

10Vishwakarma Nagari

Sahakari Bank Ltd.31.05 35.74 474.07 Nil 329.06 538.5 6.012

11Prerana Nagari Sahakari

Bank Ltd.25.52 28.39 159.79 Nil 133.68 195.4 1.6

Total 1409.96 4039.31 50002.92 3520.15 36240 59662.65 442.512

Note: - Reporting UCBs 11

Figures are for the year 2004-05.

Source: - The Maharashtra state co-operative Banks Association Ltd,

Mumbai.

89

Graph 4.1

Relative Position of the Deogiri Bank

It is imperative to study the position of Deogiri Bank in detail in the

context of UCBs in Aurangabad District. The table no. 4.2 gives better

insight of the position of the Deogiri Bank.

90

Table No. 4.2

Relative Position of the Deogiri Bank in

Comparison to Total UCBs in Aurangabad District.(Rs. In Lakhs)

Sr.

No.Indicators

Position of all

UCBs in A. bad.

(Rs.)

Position of Deogiri

Bank (Rs.)

% Share of

Deogiri Bank.

01 02 03 04 05

01 Deposit 50,062.92 31248.70 66.42 %

02 Loans & Advance 36240.00 24745.18 68.28 %

03 Borrowing 3520.15 Nil Nil

04 Own fund 4039.31 2481.16 61.42 %

05 Profit 442.512 281.1 63.52 %

06 Share capital 1409.96 725.80 51.47 %

07 Working capital 59662.65 40234.82 67.43 %

Note: - 1) Figure relating to the year 2004-05 is being considered.

2) Reporting Banks 11

Source: - the Maharashtra state Co-operative Banks Association Ltd.

Mumbai.

Graph 4.2

91

It is revealed from the Table No. 4.2 that during 2004-05, the share

capital of Deogiri Bank in total Share capital of registered and operating

UCBs in Aurangabad district is more than 50%, where as in case of own

fund, deposits, loans & advances and working capital it is above 65 %. Its

profits is just below 65% of the total profits earned by reporting UCBs in

Aurangabad district.

It is also seen that the Deogiri bank is fully self-sufficient as there

were no borrowings during 2004-05.

The above fact shows that the financial position and profitability of

the Deogiri bank is very strong. It is seen that the Deogiri bank had

occupied the dominating position amongst the UCBs registered and

operating in Aurangabad district.

Financial Position and Performance of Urban Co-operative Banks in

Jalna District

According to the data available for the year 2004-05 there were seven

UCBs registered in Jalna district. Table No. 4.3 provides better insight of

the financial position and performance of UCBs registered and operating in

Jalna district.

92

Table No – 4.3

Highlights of Financial Position and Performance of

Urban Co-operative Banks in Jalna District.(Rs. In Lakhs)

Sr.

No

.

Name of the UCB

(Rs.)

ShareCapital

(Rs.)

Own

fund

(Rs.)

Deposits

(Rs.)Borrowin

gs (Rs.)

Loan &

advance

s (Rs.)

Working

capital

(Rs.)

Profits

(Rs.)

01 02 03 04 05 06 07 08 09

01

The Jalna Peoples

Co-operative Bank

Ltd.

124.58 638.7 6131.49 131.51 4482.5 7859.30 5.06

02

Shri Gajanan

Maharaj Urban Co-

operative Bank Ltd.

52.53 114.7 700.86 578.83 578.83 961.95 14.34

03

Priyadarshinai

Nagari Sahakari

Bank Ltd.

35.68 44.54 583.01 Nil 374.31 647.09 0.27

04

Jalna Merchants

Co-operative Bank

Ltd.

46.71 156.46 1616.14 Nil 1051.78 1940.56 43.34

05Mantha Urban Co-

operative Bank Ltd.28.97 54.19 809.8 Nil 535.97 930.84 6.64

Total 288.29 1008.59 9841.3 710.34 7023.39 12339.79 55.31

Note: - Reporting UCBs 05

Source: - The Maharashtra state Co-operative Banks’ Association Ltd.,

Mumbai.

Graph 4.3

93

It is revealed from table No. 4.3 that the position of Jalna peoples Co-

operative Bank Ltd., hereinafter termed as Peoples’ Bank, is stronger in

comparison to other UCBs registered in Jalna district on the basis of the

indicators, viz., share capital, own fund, deposits, loans and advances and

working capital. However, its profitability seems to be less than two other

UCBs, registered and operating in Jalna district. It is also seen that the

Peoples’ Bank has resorted to external borrowing where as there were three

other UCBs, which have not resorted to external borrowings for the year

2004-05. Hence on this parameter the position of Peoples’ bank is seems to

be weak.

The profitability of the Jalna Merchants Co-operative Bank Ltd was

highest as compared to other UCBs in Jalna district and it was not depend

upon external borrowings. However, merchants Bank came into existence in

1998 and the present study covers the period from 1995-96 to 2004-05. The

profitability of the Gajanan Maharaj Urban Co-operative Bank Ltd. was also

higher than the Peoples’ Bank. However, it came into existence in 1995 &

its dependence on external borrowing was also higher than the Peoples’

Bank.

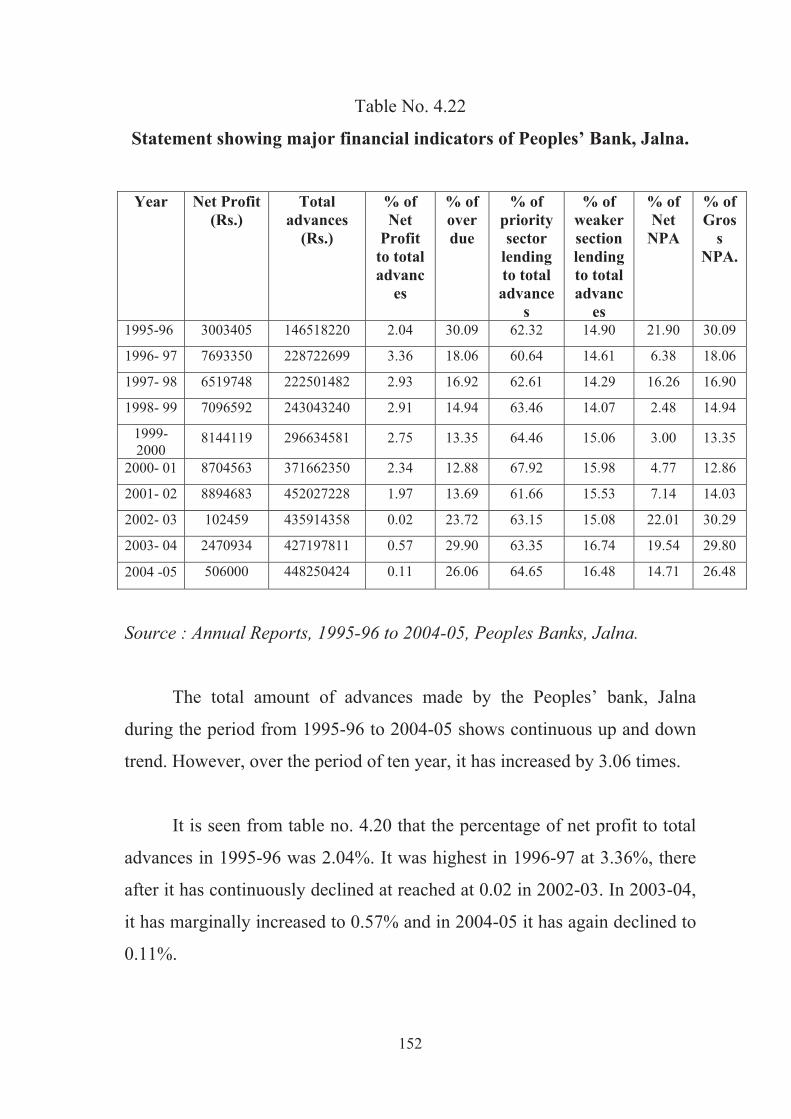

Relative Position of Peoples’ bank, Jalna

It is imperative to study the position of Peoples Bank in detail in the

context of UCBs in Jalna District. The table no. 4.3 gives better insight of

the position of the Peoples Bank.

94

It is reveled from the table No. 4.4 that the share of Jalna Peoples Co-

operative Bank in total share capital of operating registered UCBs in Jalna

district during 2004-05 was 43.21%, where as in case of own fund, deposits,

loans and advances and working capital it was around 63%. It is also seen

that its borrowing was moderate at 18.51% during the same period.

The above facts show that the Peoples’ Bank is the strongest UCB in

Jalna district. However, it is also revealed that its share of profit is just

9.14% of the profit earned by all the operating registered UCBs in Jalna

district during 2004-05. It is a cause of concern for the Peoples’ Bank.

The researcher had to select one UCB each from Aurangabad and

Jalna district. The selection was made on purposive and systematic

sampling basis after analyzing the relative positions of the UCBs registered

in Aurangabad and Jalna districts.

Table No : 4.4

Relative Position of Peoples’ bank, Jalna in Comparison to

Total Urban Co-operative Banks in Jalna District.

(Rs. In Lakhs)

Sr.

No.Indicators

Position of

all UCBs in

Jalna (Rs.)

Position of

Peoples’

Bank (Rs.)

% Share of

JPC in UCBs

in Jalna

01 02 03 04 05

01 Share capital 288.29 124.58 43.21%

02 Own fund 1008.59 638.7 63.32

03 Deposit 9841.3 6131.49 62.30%

04 Borrowing 710.34 131.51 18.51%

05 Loans & Advance 7023.39 4482.5 63.82%

06 Working capital 12339.79 7859.35 63.69

07 Profit 55.31 5.06 9.14%

95

Graph No. 4.4

Deogiri Bank being the strongest bank amongst the UCBs registered

in Aurangabad and Peoples’ bank being the dominating UCB in Jalna

districts have been selected for detail study of the impact of priority sector

lending on UCBs in Aurangabad and Jalna districts.

Deogiri Bank was established in 1985 & working through ten

branches, two extension counters, one training center & head office. There

were 11232 shareholders. Peoples’ Bank was established in 1958 &

working through Nine branches & head office. There were 19090

shareholders. The area of operation of both the banks is confined to

Aurangabad & Jalna districts.

96

Priority Sector lending by Deogiri bank Aurangabad

To get deep insight of priority sector lending by these two banks, it is

necessary to study the number of borrowing units limits sanctioned, amount

advanced balance outstanding and amount of overdue under the priority

sector lending for the period from 1995-96 to 2004-05.

Table no. 4.5 gives better insight of the number of borrowing units

limits sanctioned, amount advanced balance outstanding and amount of

overdue under the priority sector lending by Deogiri bank, Aurangabad for

the period from 1995-96 to 2004-05.

Table No 4.5

Priority Sector lending by Deogiri bank Aurangabad

(Rs. In thousands)

Sr.

NoYear

No. Of

borrowing

units

Limits

sanctioned

Amount

Advanc

ed

Balance

outstandi

ng

Amt.

Overdue

01 02 03 04 05 06 07

01 March End

1995-962881 184842 181687 145377 19552

02 1996-97 3656 288724 283817 217375 21467

03 1997-98 4533 429587 431303 364936 28407

04 1998-99 3727 472667 450255 357628 23044

05 1999-2000 N. A. N. A. N. A. N. A. N. A.

06 2000-01 8613 1127226 1113854 957968 75894

07 2001-02 9120 1419897 1419897 1125196 88167

08 2002-03 9795 1430315 1403294 1182491 109660

09 2003-04 10679 1664075 1664076 1351557 178818

10 2004-05 11131 1884039 1855425 1576484 190817

Note: N. A. (Not available)

Source: - Deogiri Bank, priority sector Reports from 1995-96 to 2004-05.

97

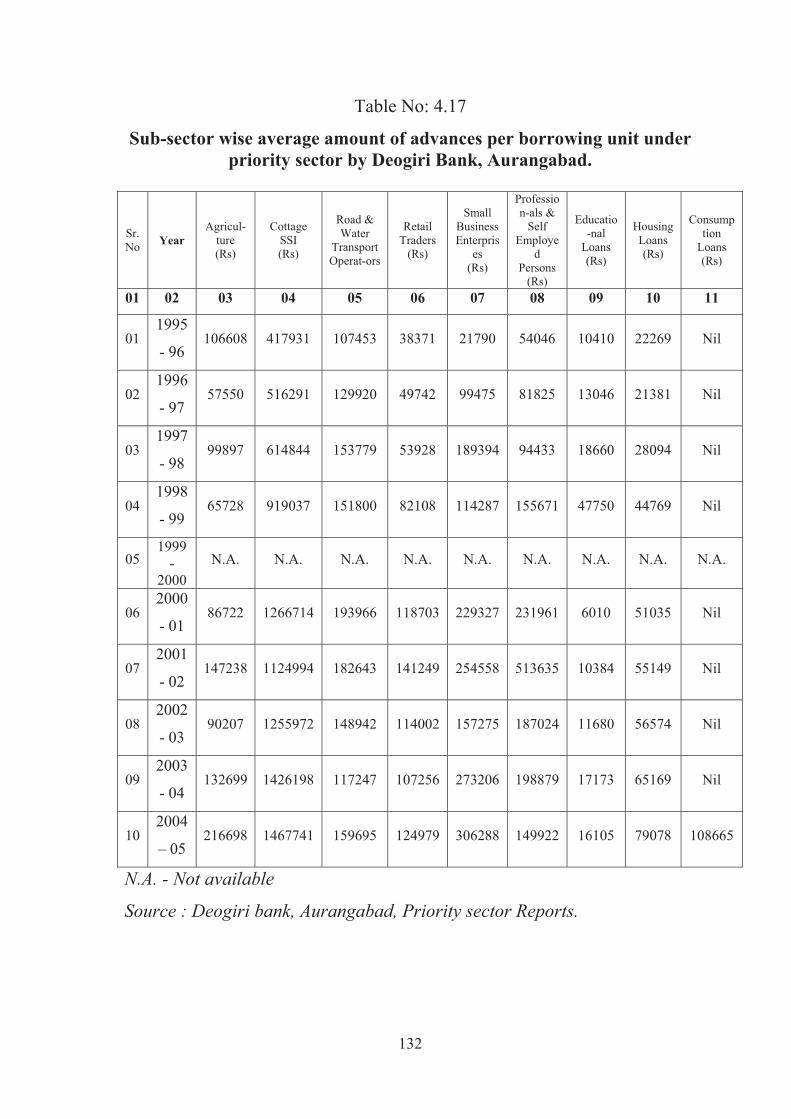

It is seen from the Table No. 4.5 that the number of borrowers under

priority sector lending by Deogiri Nagari Sahakari Bank Ltd, Aurangabad

has increased from 2881 during 1995-96 to 11131 during 2004-05. There

was an increase by 286.35% in the number of borrowers during the period

of 10 years. It is also seen that during the year 2000-01 number of borrowers

as compared to 1998-99 has increased at a very high rate & there after the

increase in the number of borrowers was only moderate.

It is also seen from the Table No. 4.5 that the limits sanctioned under

the priority sector lending has increased from Rs. 184842 thousands in

1995-96 to Rs. 1884039 thousands in 2004-05 indicating an increase of over

10 times during the period of 10 years. It is also seen that there were

constant increase in the amount sanctioned under priority sector by the

Deogiri bank. However, the increase in limits sanctioned during 2000-01

seems to be sharp as compared to the year 1998-99.

It is also evident that the amount advanced under the priority sector

lending by Deogiri Bank has increased from Rs. 181687 thousands in 1995-

96 to Rs. 1855425 thousands in 2004-05, indicating nearly 10 times increase

during the period of 10 years. Almost same trend is evident so far as year-

to-year increase in amount advance is concerned as seen for limits

sanctioned.

The Table No 4.5 also reveals that the amount outstanding at the end

of March 1996 was Rs. 145377 thousands. It was Rs. 1576484 thousand at

the end of March 2005 indicating an increase of more than 10 times during

the period 1995-96 to 2004-05.

98

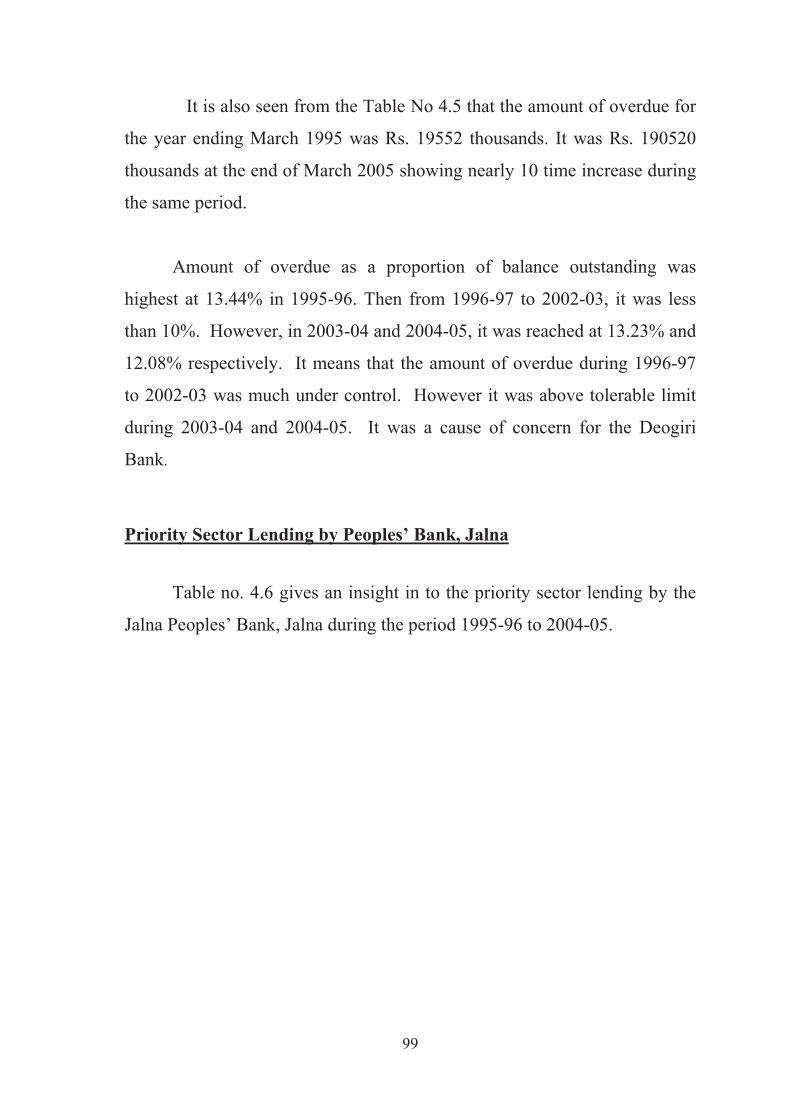

It is also seen from the Table No 4.5 that the amount of overdue for

the year ending March 1995 was Rs. 19552 thousands. It was Rs. 190520

thousands at the end of March 2005 showing nearly 10 time increase during

the same period.

Amount of overdue as a proportion of balance outstanding was

highest at 13.44% in 1995-96. Then from 1996-97 to 2002-03, it was less

than 10%. However, in 2003-04 and 2004-05, it was reached at 13.23% and

12.08% respectively. It means that the amount of overdue during 1996-97

to 2002-03 was much under control. However it was above tolerable limit

during 2003-04 and 2004-05. It was a cause of concern for the Deogiri

Bank.

Priority Sector Lending by Peoples’ Bank, Jalna

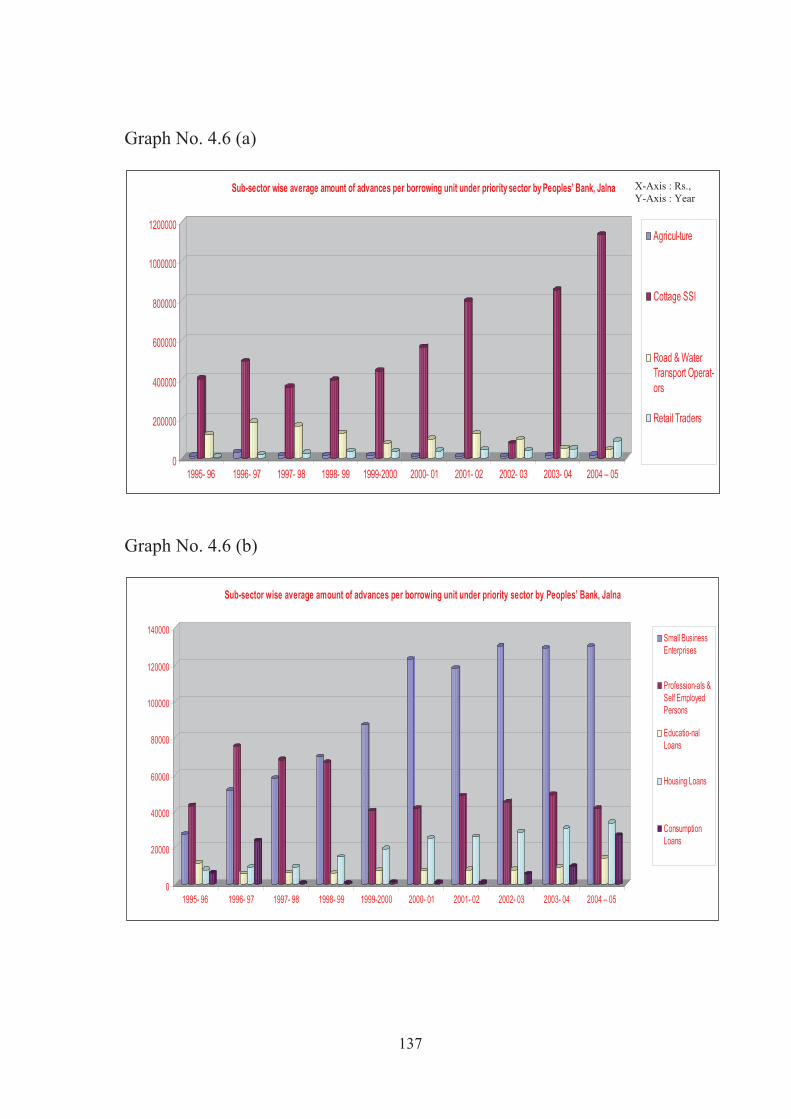

Table no. 4.6 gives an insight in to the priority sector lending by the

Jalna Peoples’ Bank, Jalna during the period 1995-96 to 2004-05.

99

Table No.: 4.6

Priority Sector Lending by Peoples’ Bank, Jalna(Rs. In thousands)

Sr.

No.Year

No of

borrowing

units

Limits

sanctioned

Amt.

Advanced

Balance

outstanding

Amt.

Overdue

01 02 03 04 05 06 07

01March

End

19963256 119273 99206 91265 29115

02 1997 3431 166744 150582 138705 27528

03 1998 3908 167339 145158 122364 23234

04 1999 4039 173589 160705 154229 20561

05 2000 4773 194185 195400 191160 20875

06 2001 5912 264848 266438 252433 23967

07 2002 5693 270468 291294 278737 37007

08 2003 5404 310369 301577 275292 45912

09 2004 4902 309065 296121 270626 53992

10 2005 3950 286114 278220 249052 48681

Source: - Peoples’ Bank Priority Sectors reports (1995-96 to 2004-05)

It is seen from the Table No. 4.6 that the number of borrowers under

priority sector lending by Jalna Peoples’ co-operative Bank Ltd. Jalna has

increased from 3256 at the end of March 1996 to 3950 at the end of March

2005. There was an increase of 21.31 % in the number of borrowers over a

period of 10 years. It is also seen that the number of borrower has increased

from 3256 in 1995-96 to 5912 in 2000-01 & there after there was a

declining trend till 2004-05.

It is also seen from the Table No 4.6 that the limits sanctioned under

the priority sector lending has increased from Rs. 119273 thousands in

1995-96 to Rs. 286114 thousands in 2004-05 indicating an increase of

139.88 % over the period of ten years. It is also revealed that there was

continuous increase in the limits sanctioned by peoples’ bank under priority

100

sector lending, except the year 2003-04, and 2004-05 in which it is seen that

limit sanctioned was slightly lower than the previous years.

A careful analysis of amount advanced under priority sector lending

by Peoples’ Bank, Jalna during 1995-96 to 2004-05 showed fluctuating

trends. In 1996-97, it has increased to Rs. 150582 thousands as compared

Rs. 99206 thousands in 1995-96, witnessing an increase of 51.78 %. In

1997-98, it has reduced to Rs. 145158 thousands witnessing a decline of

3.61 % as compared to 1996-97. There after there was a continuous

increase in amount advanced under priority sector till 2002-03. However, in

2003-04 it has declined to Rs. 296121 thousands as compared to Rs. 301577

thousands in 2002-03. In 2004-05, it has further reduced to Rs. 278220

thousands.

It is also seen that the amount of overdue was Rs. 29115 thousands in

1995-96. It has continuously decline till 1998-99 and reached the lowest

level of the period under study to Rs. 20561 thousands. There after, it has

shown a continued increasing trend till 2003-04 showing Rs. 53992

thousands in 2003-04. However, in 2004-05, it has declined to Rs. 48681

thousands. Over the period of 10 years, i.e. from 1995-96 to 2004-05, it has

increased by 67.20 %.

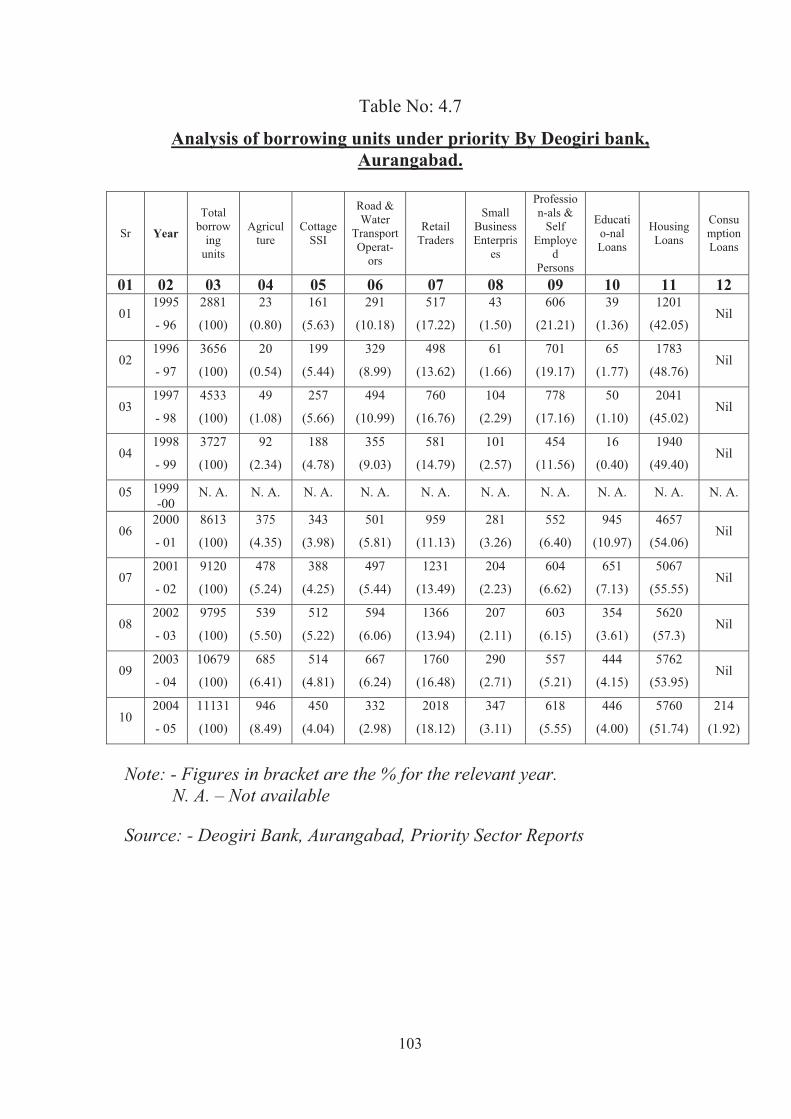

Analysis of borrowing units under priority sector lending.

It is imperative to study the total no. of beneficiaries and sub-sector

wise number of beneficiaries under the priority sector lending by Deogiri

Bank, Aurangabad and Peoples’ Bank, Jalna, for the period of 10 years from

1995-96 to 2004-05. It will reveal the relative significance of sub-sector

101

wise lending under the priority sector in the context of number of

beneficiaries.

Table no. 4.7 reveals the sub-sector wise increase or decrease in the

number of beneficiaries under the priority sector lending by Deogiri Bank,

Aurangabad, for the period from 1995-96 to 2004-05.

It is evident from table no. 4.7 that the total borrowing units under the

priority sector lending by Deogiri Bank, Aurangabad has continuously

increased from 2881 units in 1995-96 to 11131 units in 2004-05, except for

one year 1998-99. It was 2881 in 1995-96. It was increased to 11131 in

2004-05. It indicate that during the period of 10 years from 1995-96 to

2004-05, the total number of borrowing units under priority sector lending

by Deogiri bank has increased by 3.86 times. It means that this bank has

succeeded in attracting more and more borrowers over the period of time.

102

Table No: 4.7

Analysis of borrowing units under priority By Deogiri bank,

Aurangabad.

Sr Year

Total

borrow

ing

units

Agricul

ture

Cottage

SSI

Road &

Water

Transport

Operat-

ors

Retail

Traders

Small

Business

Enterpris

es

Professio

n-als &

Self

Employe

d

Persons

Educati

o-nal

Loans

Housing

Loans

Consu

mption

Loans

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

2881

(100)

23

(0.80)

161

(5.63)

291

(10.18)

517

(17.22)

43

(1.50)

606

(21.21)

39

(1.36)

1201

(42.05)Nil

021996

- 97

3656

(100)

20

(0.54)

199

(5.44)

329

(8.99)

498

(13.62)

61

(1.66)

701

(19.17)

65

(1.77)

1783

(48.76)Nil

031997

- 98

4533

(100)

49

(1.08)

257

(5.66)

494

(10.99)

760

(16.76)

104

(2.29)

778

(17.16)

50

(1.10)

2041

(45.02)Nil

041998

- 99

3727

(100)

92

(2.34)

188

(4.78)

355

(9.03)

581

(14.79)

101

(2.57)

454

(11.56)

16

(0.40)

1940

(49.40)Nil

05 1999

-00N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A.

062000

- 01

8613

(100)

375

(4.35)

343

(3.98)

501

(5.81)

959

(11.13)

281

(3.26)

552

(6.40)

945

(10.97)

4657

(54.06)Nil

072001

- 02

9120

(100)

478

(5.24)

388

(4.25)

497

(5.44)

1231

(13.49)

204

(2.23)

604

(6.62)

651

(7.13)

5067

(55.55)Nil

082002

- 03

9795

(100)

539

(5.50)

512

(5.22)

594

(6.06)

1366

(13.94)

207

(2.11)

603

(6.15)

354

(3.61)

5620

(57.3)Nil

092003

- 04

10679

(100)

685

(6.41)

514

(4.81)

667

(6.24)

1760

(16.48)

290

(2.71)

557

(5.21)

444

(4.15)

5762

(53.95)Nil

102004

- 05

11131

(100)

946

(8.49)

450

(4.04)

332

(2.98)

2018

(18.12)

347

(3.11)

618

(5.55)

446

(4.00)

5760

(51.74)

214

(1.92)

Note: - Figures in bracket are the % for the relevant year.

N. A. – Not available

Source: - Deogiri Bank, Aurangabad, Priority Sector Reports

103

Table no 4.7 also revealed that the total number of borrowing units

under all the sub sectors has increased over the period from 1995-96 to

2004-05. However, the increase in the number of borrowing units under

housing loan, agriculture, educational loan and consumption loan was very

impressive.

It is further revealed from table no. 4.7 that the number of borrowing

units under the sub-sector housing loan by Deogiri Bank, has continuously

increase from 1201 units in 1995-96 to 5760 units in 2004-05. The number

of borrowing units under the agriculture sector has increase from 23 units in

1995-96 to 946 units in 2004-05. The increase in the number of borrowing

units under the housing loan and agriculture loan is very impressive.

In 1995-96, the relative position of various sub-sectors of the priority

sector lending by Deogiri Bank in the context of borrowing units were

in the following order, namely, (i) housing loan, (ii) professional and self –

employed, (iii) retail traders, (iv) road and water transport operators, (v)

cottage and SSI, (vi) small business enterprises, (vii) educational loan, (viii)

agriculture. During 1995-96 to 2003-04, no consumption loan was granted

by Deogiri bank.

In 2004-05, the relative position of number of borrowing units under

various sub-sectors of the priority sector were in the following order,

namely, (i) housing loan, (ii) retail traders, (iii) agriculture, (iv)

professionals and self-employed persons, (v) cottage and small SSI, (vi)

educational loan, (vii) small business enterprises, (viii) Road and water

transport operator, (ix) consumption loan.

104

The relative position of these sub-sectors have undergone a sea

change over the period of 10 years from 1995-96 to 2004-05.

It is also seen from the table no. 4.25 that the proportionate share of

borrowing units under housing loan, professionals and self employed

persons and retail traders in 1995-96 were 42.05 %, 21.21% and 17.22%

respectively and the share of remaining sub-sectors of the priority sector

was only 19.52 %. In 2004-05 the proportionate share of borrowing units

under the housing loan, retail traders and agriculture were 51.74 %, 18.12 %

and 8.49 % respectively. The share of remaining sub-sector of the priority

sector lending was 21.65 %.

It is further evident from table no. 4.7 that the relative importance of

agriculture loan have been considerably increased over the period from

1995-96 to 2004-05.

Analysis Of Borrowing Units Under Priority Sector Lending By

Peoples’ Bank, Jalna.

The table no. 4.8 reveals the sub-sector wise increase or decrease in

the number of beneficiaries under the priority sector lending by the Peoples’

Bank, Jalna for the period of 10 years from 1995-96 to 2004-05.

It is evident from table no. 4.8 that the total borrowing units under the

priority sector lending by Peoples’ Bank, Jalna has continuously increased

during 1995-96 to 2000-01. It was 3256 in 1995-96. It was increased to

5912 in 2000-01. Thereafter it has declined continuously from 2001-02 and

reached to 3950 in 2004-05. It means that the large number of borrowing

105

units have been shifted to other financial institutions or repaid their entire

amount of loan.

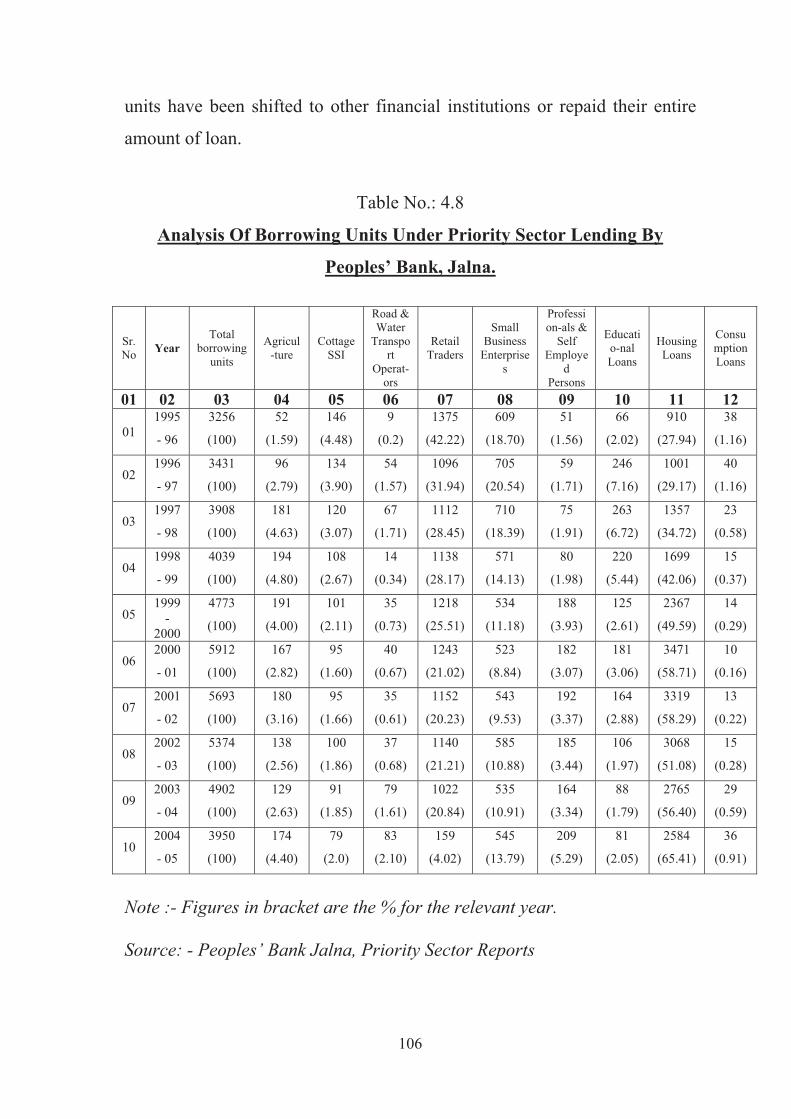

Table No.: 4.8

Analysis Of Borrowing Units Under Priority Sector Lending By

Peoples’ Bank, Jalna.

Sr.

NoYear

Total

borrowing

units

Agricul

-ture

Cottage

SSI

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

Small

Business

Enterprise

s

Professi

on-als &

Self

Employe

d

Persons

Educati

o-nal

Loans

Housing

Loans

Consu

mption

Loans

01 02 03 04 05 06 07 08 09 10 11 12

01

1995

- 96

3256

(100)

52

(1.59)

146

(4.48)

9

(0.2)

1375

(42.22)

609

(18.70)

51

(1.56)

66

(2.02)

910

(27.94)

38

(1.16)

021996

- 97

3431

(100)

96

(2.79)

134

(3.90)

54

(1.57)

1096

(31.94)

705

(20.54)

59

(1.71)

246

(7.16)

1001

(29.17)

40

(1.16)

031997

- 98

3908

(100)

181

(4.63)

120

(3.07)

67

(1.71)

1112

(28.45)

710

(18.39)

75

(1.91)

263

(6.72)

1357

(34.72)

23

(0.58)

041998

- 99

4039

(100)

194

(4.80)

108

(2.67)

14

(0.34)

1138

(28.17)

571

(14.13)

80

(1.98)

220

(5.44)

1699

(42.06)

15

(0.37)

051999

-

2000

4773

(100)

191

(4.00)

101

(2.11)

35

(0.73)

1218

(25.51)

534

(11.18)

188

(3.93)

125

(2.61)

2367

(49.59)

14

(0.29)

062000

- 01

5912

(100)

167

(2.82)

95

(1.60)

40

(0.67)

1243

(21.02)

523

(8.84)

182

(3.07)

181

(3.06)

3471

(58.71)

10

(0.16)

072001

- 02

5693

(100)

180

(3.16)

95

(1.66)

35

(0.61)

1152

(20.23)

543

(9.53)

192

(3.37)

164

(2.88)

3319

(58.29)

13

(0.22)

082002

- 03

5374

(100)

138

(2.56)

100

(1.86)

37

(0.68)

1140

(21.21)

585

(10.88)

185

(3.44)

106

(1.97)

3068

(51.08)

15

(0.28)

092003

- 04

4902

(100)

129

(2.63)

91

(1.85)

79

(1.61)

1022

(20.84)

535

(10.91)

164

(3.34)

88

(1.79)

2765

(56.40)

29

(0.59)

102004

- 05

3950

(100)

174

(4.40)

79

(2.0)

83

(2.10)

159

(4.02)

545

(13.79)

209

(5.29)

81

(2.05)

2584

(65.41)

36

(0.91)

Note :- Figures in bracket are the % for the relevant year.

Source: - Peoples’ Bank Jalna, Priority Sector Reports

106

Table no. 4.8 also revealed that the total number of borrowing units

under the sub-sector housing loan by peoples’ bank has increased from 910

units in 1995-96 to 2584 units in 2004-05. The number of borrowing units

has declined from 1375 in 1995-96 to 159 in 2004-05. However, the number

of borrowing units under loans to retail traders during the year 1995-96 and

1996-97 was higher than the number of borrowing units under housing loan.

In 1995-96, the relative position of various sub-sectors of the priority

sector lending by peoples’ bank, Jalna in the context of borrowing units

were in the following order, namely, (i) retail traders, (ii) housing loan, (iii)

small business enterprises (iv) cottage and SSI, (v) educational loan, (vii)

agriculture, (vii) professionals and self-employed persons (viii)

consumption loan, (ix) road and water transport operators.

In 2004-05 the relative position of the number of borrowing units

under various sub-sector of the priority sector were in the following order,

namely, (i) housing loan, (ii) small business enterprises, (iii) professionals

and self-employed persons, (iv) agriculture, (v) retail traders, (vi) road and

water transport operators (vii) educational loan, (viii) cottage and small

scale industries, (ix) consumption loan.

The relative position of these sub-sectors have undergone a sea

change over the period of 10 years from 1995-96 to 2004-05.

It also reveled from the table no. 4.8 that the proportionate share of

borrowing units under housing loan, loans to retail traders and small

business enterprises in 1995-96 were 27.94%, 42.22%, and 18.70%

respectively. The share of remaining sub-sectors of the priority sectors was

only 11.14%.

107

In 2004-05 the proportionate share of borrowing units under the

housing loan, small business enterprises and professionals and self-

employed persons were 65.41%, 13.79% and 5.29% respectively. The share

of remaining sub-sectors of the priority sector lending was only 15.51%.

It is also evident from the table no. 4.8 that the relative importance of

the housing loan has been considerably increased over the period of 10 year

1995-96 to 2004-05. During the same period, the relative importance of

retail traders of and small business enterprises has declined.

Analysis of Limits Sanctioned Under Priority Sector Lending

After studying the number of borrowing units under various sub-

sectors of the priority sector lending by Deogiri Bank, Aurangabad and

Peoples’ bank, Jalna, it is imperative to study the salient features of limit

sanctioned by both the banks to various sub-sectors of the priority sector.

The table no. 4.9 reveals the salient features of limit sanctioned by

Deogiri Bank, Aurangabad to various sub-sectors of the priority sector

lending during the period from 1995-96 to 2004-05.

It is evident from the table no. 4.9 that the total amount of limits

sanctioned by Deogiri bank, Aurangabad under the priority sector lending

during the period of 10 years from 1995-96 to 2004-05 has shown the

increasing trend. The total amount of limits sanctioned under priority sector

lending by Deogiri Bank, Aurangabad in 1995-96 was Rs. 184842

thousands. It has reached to Rs. 1884039 thousands in 2004-05. It indicates

an increase of 10.19 times over a period 10 years from 1995-96 to 2004-05.

108

It is revealed from the table no. 4.9 that the limits sanctioned to

various sub-sectors of priority sector by Deogiri bank has under gone a sea

change over the period from 1995-96 to 2004-05. In 1995-96, the

proportionate share of limits sanctioned to cottage & SSI professional and

self-employed persons, road and water transport operators, housing loans,

retail traders was 37.62%, 17.86%, 17.11%, 14.56% and 10.75%

respectively. The proportionate share of remaining priority sectors was

2.05% of the total priority sector lending by Deogiri Bank.

In 2004-05, the proportionate share of the limits sanctioned to cottage

and SSI, housing loan, retail traders agriculture small business enterprises

was 35.50%, 24.87%, 13.51%, 10.96% 5.68% and the proportionate share

of remaining priority sectors was only 15.48% of the total priority sector

lending.

It means that the cottage and SSI sector remained at the top in the

amount of limits sanctioned by the Deogiri bank over a period of 10 years

from 1995-96 to 2004-05. However, during the same period the

proportionate share of limits sanctioned to professionals and road and water

transport operators have declined. The proportionate share of limits

sanctioned to agriculture, housing and retail traders have increased. The

relative increase in the limits sanctioned to agriculture was very impressive.

109

Table No: 4.9

Analysis of Limits Sanctioned Under Priority Sector Lending by

Deogiri Bank, Aurangabad.

(Rs. In thousands)

Sr.

NoYear

Limit

sanctioned

(Rs)

Agricul

-ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Busines

s

Enterpri

ses

(Rs)

Professio

n-als &

Self

Employe

d

Persons

(Rs)

Educati

o-nal

Loans

(Rs)

Housing

Loans

(Rs)

Consu

mptio

n

Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

184842

(100)

2455

(1.32)

69542

(37.62)

31643

(17.11)

19873

(10.75)

964

(0.52)

33028

(17.86)

406

(0.21)

26931

(14.56)Nil

021996

- 97

288724

(100)

1159

(0.40)

103734

(35.92)

43025

(14.90)

24772

(8.57)

6168

(2.13)

60646

(21.00)

848

(0.29)

48372

(16.75)Nil

031997

- 98

429587

(100)

4960

(1.15)

157020

(36.55)

75011

(17.46)

40958

(9.53)

19034

(4.43)

74919

(17.43)

918

(0.21)

54767

(13.21)Nil

041998

- 99

472667

(100)

6441

(1.36)

190318

(40.26)

53906

(11.40)

47810

(10.11)

11775

(2.49)

73073

(15.45)

764

(0.16)

88580

(18.74)Nil

05 1999

- 00 N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N.A.

062000

- 01

1127226

(100)

33203

(2.94)

441594

(39.17)

97130

(8.61)

114565

(10.16)

64603

(5.73)

130476

(11.57)

5680

(0.50)

239975

(21.28)Nil

072001

- 02

1419897

(100)

70380

(4.95)

436498

(30.74)

90774

(6.39)

173878

(12.24)

51930

(3.65)

310236

(21.84)

6760

(0.47)

279441

(19.68)Nil

082002

- 03

1430315

(100)

51294

(3.58)

656415

(45.89)

88764

(6.20)

156240

(10.92)

33182

(2.13)

117051

(8.18)

4165

(0.29)

323204

(22.59)Nil

092003

- 04

1664075

(100)

90899

(5.46)

733066

(44.05)

78204

(4.69)

188771

(11.34)

79230

(4.76)

110776

(6.65)

7625

(0.45)

375504

(22.56)Nil

102004

- 05

1884039

(100)

206637

(10.96)

668894

(35.50)

53155

(2.82)

254544

(13.51)

107052

(5.68)

93890

(4.98)

7383

(0.39)

468640

(24.87)

23844

(1.26)

Note: - Figures in bracket are the % for the relevant year.

N. A. – Not available

Source: - Deogiri Bank, Aurangabad, Priority Sector Reports

110

It is also revealed that the limits sanctioned to housing loans by the

Deogiri bank, Aurangabad during 1995-96 to 2004-05 has shown increasing

trend. The amount of limits sanctioned to housing loans in 1995-96 was Rs.

26931 thousands. In 2004-05, it has increased to Rs. 468640 thousands. It

indicates an increase of 17.40 times over the period of 10 years from 1995-

96 to 2004-05. It means that the housing loan is gaining popularity among

the customers of Deogiri bank. Similarly, it is revealed that the limits

sanctioned to cottage and small-scale industries by the Deogiri bank,

Aurangabad during 1995-96 to 2004-05 has shown increasing trend except

the year 2001-02 in which it was slightly lower than the year 2000-01. The

amount of limits sanctioned to cottage and small-scale industries in 1995-96

was Rs. 69542 thousands. In 2004-05, it has increased to Rs. 668894

thousands an increase of 9.61 times over the period of 10 years from 1995-

96 to 2004-05. Further it is revealed that the limits sanctioned to retail

traders by Deogiri bank, Aurangabad during 1995-96 to 2004-05 has shown

increasing trend except the year 2002-03, in which it was approximately 10

% lower than the year 2001-02. The amount of limits sanctioned to retail

traders in 1995-96 was Rs. 19873 thousands. In 2004-05 it was Rs. 254544

thousands. It has increased by 12.80 times over the period of 10 years from

1995-96 to 2004-05.

It is also seen that the Deogiri bank has sanctioned the loans for

consumption purpose only in 2004-05. There were no consumption loans

during 1995-96 to 2003-04. The amount of limits sanctioned for

consumption in 2004-05 was negligible. The amount of limits sanctioned for

educational loan was also negligible throughout the period from 1995-96 to

2004-05.

111

It is also revealed that the limits sanctioned to agriculture, road and

water transport operators, small business enterprises, professionals and self–

employed persons, educational loans by Deogiri bank, Aurangabad during

1995-96 to 2004-05 has shown fluctuating trend. However, it is also seen

that there was sharp increase in the amount of limits sanctioned to

agriculture in 2004-05.

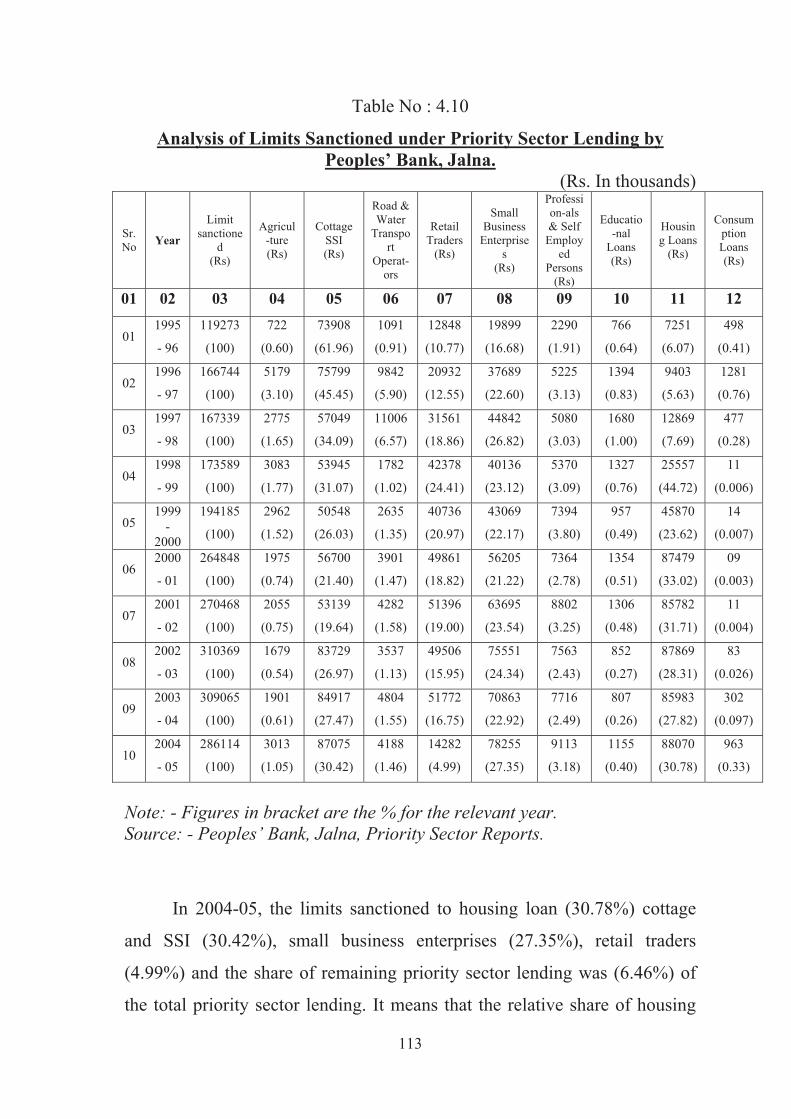

The table no. 4.10 reveals the salient features of limit sanctioned by

Peoples’ Bank, Jalna to various sub-sectors of the priority sector lending

during the period from 1995-96 to 2004-05.

It is evident from the table no. 4.10 that the total amount of limits

sanctioned by Peoples’ Bank, Jalna under the priority sector lending during

1995-96 to 2004-05, showed the increasing trend till the year 2002-03, there

after it has declined during the year 2003-04 and 2004-05.

The total amount of limits sanctioned under priority sector lending by

Peoples’ Bank in 1995-96 was Rs. 119273 thousands. It has reached to Rs.

286114 thousands in 2004-05. It indicate an increase of 2.39 times over a

period of 10 years from 1995-96 to 2004-05.

It is reveled from the table no. 4.10 that the limits sanctioned to

various sub-sectors of priority sector has undergone a sea change over the

period of 10 years from 1995-96 to 2004-05. In 1995-96 the limits

sanctioned to cottage and small scale industries (61.96%), small business

enterprises (16.68%), retail traders (10.77%), housing (6.07%) and the share

of remaining priority sector was (4.52%) of the total priority sector lending

by peoples’ bank.

112

Table No : 4.10

Analysis of Limits Sanctioned under Priority Sector Lending by

Peoples’ Bank, Jalna.

(Rs. In thousands)

Sr.

NoYear

Limit

sanctione

d

(Rs)

Agricul

-ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Business

Enterprise

s

(Rs)

Professi

on-als

& Self

Employ

ed

Persons

(Rs)

Educatio

-nal

Loans

(Rs)

Housin

g Loans

(Rs)

Consum

ption

Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

119273

(100)

722

(0.60)

73908

(61.96)

1091

(0.91)

12848

(10.77)

19899

(16.68)

2290

(1.91)

766

(0.64)

7251

(6.07)

498

(0.41)

021996

- 97

166744

(100)

5179

(3.10)

75799

(45.45)

9842

(5.90)

20932

(12.55)

37689

(22.60)

5225

(3.13)

1394

(0.83)

9403

(5.63)

1281

(0.76)

031997

- 98

167339

(100)

2775

(1.65)

57049

(34.09)

11006

(6.57)

31561

(18.86)

44842

(26.82)

5080

(3.03)

1680

(1.00)

12869

(7.69)

477

(0.28)

041998

- 99

173589

(100)

3083

(1.77)

53945

(31.07)

1782

(1.02)

42378

(24.41)

40136

(23.12)

5370

(3.09)

1327

(0.76)

25557

(44.72)

11

(0.006)

051999

-

2000

194185

(100)

2962

(1.52)

50548

(26.03)

2635

(1.35)

40736

(20.97)

43069

(22.17)

7394

(3.80)

957

(0.49)

45870

(23.62)

14

(0.007)

062000

- 01

264848

(100)

1975

(0.74)

56700

(21.40)

3901

(1.47)

49861

(18.82)

56205

(21.22)

7364

(2.78)

1354

(0.51)

87479

(33.02)

09

(0.003)

072001

- 02

270468

(100)

2055

(0.75)

53139

(19.64)

4282

(1.58)

51396

(19.00)

63695

(23.54)

8802

(3.25)

1306

(0.48)

85782

(31.71)

11

(0.004)

082002

- 03

310369

(100)

1679

(0.54)

83729

(26.97)

3537

(1.13)

49506

(15.95)

75551

(24.34)

7563

(2.43)

852

(0.27)

87869

(28.31)

83

(0.026)

092003

- 04

309065

(100)

1901

(0.61)

84917

(27.47)

4804

(1.55)

51772

(16.75)

70863

(22.92)

7716

(2.49)

807

(0.26)

85983

(27.82)

302

(0.097)

102004

- 05

286114

(100)

3013

(1.05)

87075

(30.42)

4188

(1.46)

14282

(4.99)

78255

(27.35)

9113

(3.18)

1155

(0.40)

88070

(30.78)

963

(0.33)

Note: - Figures in bracket are the % for the relevant year.

Source: - Peoples’ Bank, Jalna, Priority Sector Reports.

In 2004-05, the limits sanctioned to housing loan (30.78%) cottage

and SSI (30.42%), small business enterprises (27.35%), retail traders

(4.99%) and the share of remaining priority sector lending was (6.46%) of

the total priority sector lending. It means that the relative share of housing

113

loan and small business enterprises have increased over the period of 10

years from 1995-96 to 2004-05. Over the same period the relative share of

cottage and SSI and retail traders have declined. The relative increase in the

limits sanctioned to the housing was impressive.

It is also revealed that the amount of limits sanctioned to all the sub-

sectors of priority sector lending by the Peoples bank, Jalna during 1995-96

to 2004-05 has show fluctuating trend.

It is also seen that the amounts of limits sanctioned for consumption

loans during 1995-96 to 1997-98 and 2002-03 to 2004-05 were relatively

higher than the limit sanctioned during the year 1998-99 to 2001-02. It was

almost negligible during 1998-99 to 2001-02.

The relative share of limits sanctioned to cottage and small sector

industries in total limits sanctioned by Peoples’ bank, Jalna in 1995-96 was

61.92%. There after it has successively declined and reached lowest level of

19.64% in 2001-02. However, it has started to increase from 2002-03 at

reached at 30.42% in 2004-05.

The relative share of limits sanctioned to housing loans in total limits

sanctioned under priority sector lending by Peoples’ bank, Jalna in 1995-96

was only 6.07 %. It has successively increased and reached the highest level

of 33.02% in 2000-01. It was 30.78% in 2004-05. The relative share of

limits sanctioned by Peoples’ bank, Jalna to retail traders in 1995-96 was

10.77%. It reached the highest level of 24.41% in 1998-99. It was at its

lowest level of 4.99% in 2004-05.

114

The relative share of limits sanctioned by Peoples’ bank, Jalna to

small business enterprises in 1995-96 was at 16.68 %. In 2004-05, it was at

its highest level of 27.35%.

The table no. 4.10 Revealed that the relative importance of housing

loans and loans to small business enterprises have increased on the other

hand, the relative importance of cottage and small scale industries and retail

traders have declined.

Analysis of amount Advanced under Priority Sector lending

After studying the number of borrowing units and limits sanctioned

under priority sector lending by Deogiri bank, Aurangabad and Peoples’

bank, Jalna it is necessary to study the salient features of amount advanced

under priority sector lending to sub-sectors by both the banks.

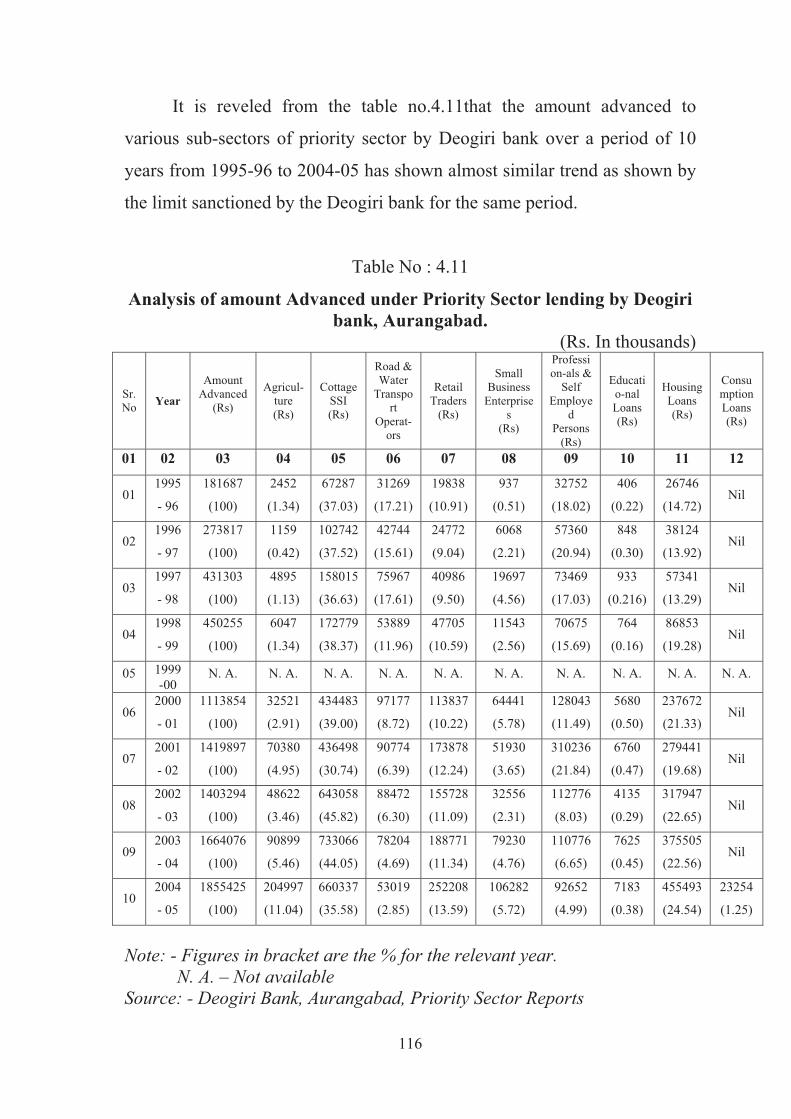

The table no. 4.11 reveals the salient features of amount advanced to

priority sector by Deogiri bank, Aurangabad during the period from 1995-96

to 2004-05.

It is seen from table no. 4.11 that the amount advanced under the

priority sector lending by Deogiri bank, Aurangabad during the period of 10

years from 1995-96 to 2004-05 has shown increasing trend except the year

2002-03, in which it was slightly lower than the earlier year 2001-02. The

total amount advanced under priority sector lending by Deogiri bank,

Aurangabad in 1995-96 was Rs. 181687 thousands. To It has reached to

1855425 thousands in 2004-05. It indicates an increase of 10.21 times over

a period of 10 years from 1995-96 to 2004-05.

115

It is reveled from the table no.4.11that the amount advanced to

various sub-sectors of priority sector by Deogiri bank over a period of 10

years from 1995-96 to 2004-05 has shown almost similar trend as shown by

the limit sanctioned by the Deogiri bank for the same period.

Table No : 4.11

Analysis of amount Advanced under Priority Sector lending by Deogiri

bank, Aurangabad.

(Rs. In thousands)

Sr.

NoYear

Amount

Advanced

(Rs)

Agricul-

ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Business

Enterprise

s

(Rs)

Professi

on-als &

Self

Employe

d

Persons

(Rs)

Educati

o-nal

Loans

(Rs)

Housing

Loans

(Rs)

Consu

mption

Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

181687

(100)

2452

(1.34)

67287

(37.03)

31269

(17.21)

19838

(10.91)

937

(0.51)

32752

(18.02)

406

(0.22)

26746

(14.72)Nil

021996

- 97

273817

(100)

1159

(0.42)

102742

(37.52)

42744

(15.61)

24772

(9.04)

6068

(2.21)

57360

(20.94)

848

(0.30)

38124

(13.92)Nil

031997

- 98

431303

(100)

4895

(1.13)

158015

(36.63)

75967

(17.61)

40986

(9.50)

19697

(4.56)

73469

(17.03)

933

(0.216)

57341

(13.29)Nil

041998

- 99

450255

(100)

6047

(1.34)

172779

(38.37)

53889

(11.96)

47705

(10.59)

11543

(2.56)

70675

(15.69)

764

(0.16)

86853

(19.28)Nil

05 1999

-00N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A.

062000

- 01

1113854

(100)

32521

(2.91)

434483

(39.00)

97177

(8.72)

113837

(10.22)

64441

(5.78)

128043

(11.49)

5680

(0.50)

237672

(21.33)Nil

072001

- 02

1419897

(100)

70380

(4.95)

436498

(30.74)

90774

(6.39)

173878

(12.24)

51930

(3.65)

310236

(21.84)

6760

(0.47)

279441

(19.68)Nil

082002

- 03

1403294

(100)

48622

(3.46)

643058

(45.82)

88472

(6.30)

155728

(11.09)

32556

(2.31)

112776

(8.03)

4135

(0.29)

317947

(22.65)Nil

092003

- 04

1664076

(100)

90899

(5.46)

733066

(44.05)

78204

(4.69)

188771

(11.34)

79230

(4.76)

110776

(6.65)

7625

(0.45)

375505

(22.56)Nil

102004

- 05

1855425

(100)

204997

(11.04)

660337

(35.58)

53019

(2.85)

252208

(13.59)

106282

(5.72)

92652

(4.99)

7183

(0.38)

455493

(24.54)

23254

(1.25)

Note: - Figures in bracket are the % for the relevant year.

N. A. – Not available

Source: - Deogiri Bank, Aurangabad, Priority Sector Reports

116

It is also revealed that the amount advanced to housing loans by

Deogiri bank during 1995-96 to 2004-05 has shown increasing trend. The

amount advanced to housing loans in 1995-96 was Rs. 26746 thousands. In

2004-05, it has increased to Rs. 455493 thousands. It indicates an increase

of 17.03 times over the period of 10 years from 1995-96 to 2004-05. It is

also seen that the amount advanced to cottage and small-scale industries by

Deogiri bank, Aurangabad has continuously increased from Rs. 67287

thousands in 1995-96 to Rs. 733066 thousands in 2003-04. However, it has

declined to Rs. 660337 thousands in 2004-05.

It is further revealed that the amount advanced to retail traders by

Deogiri bank, Aurangabad during 1995-96 to 2004-05 has shown increasing

trend except the year 2002-03 in which it was approximately 10% lower

than the year 2001-02. The amount advanced to retail traders in 1995-96

was Rs. 19838 thousands. In 2004-05, it was Rs. 252208 thousands. It has

increased by 12.71 times over the period of 10 years from 1995-96 to 2004-

05.

It is also seen that the amount advanced to agriculture by Deogiri

bank, Aurangabad during 1995-96 was Rs. 2452 thousands. It has increased

at a high rate from 2000-01 and reached the highest level of Rs. 204997

thousands in 2004-05. The amount advanced to agriculture has increased by

83.60 times during the period of 10 years from 1995-96 to 2004-05.

It is seen that the amount advanced to small business enterprises by

Deogiri bank, Aurangabad during 1995-96 was Rs. 937 thousands. It has

increased to the highest level of the period under study to Rs. 106282

thousands in 2004-05. It has increased by 113.42 times over a period of 10

years from 1995-96 to 2004-05.

117

This study revealed that the relative importance of agriculture, retail

traders, small business enterprises, and housing loan has increased over the

period of time.

It is also seen that during the period from 1995-96 to 2003-04 there

were no consumption loan granted by Deogiri bank. It has granted

consumption loans only during the terminal year of this study. Amount

advanced under this sub-sector was negligible.

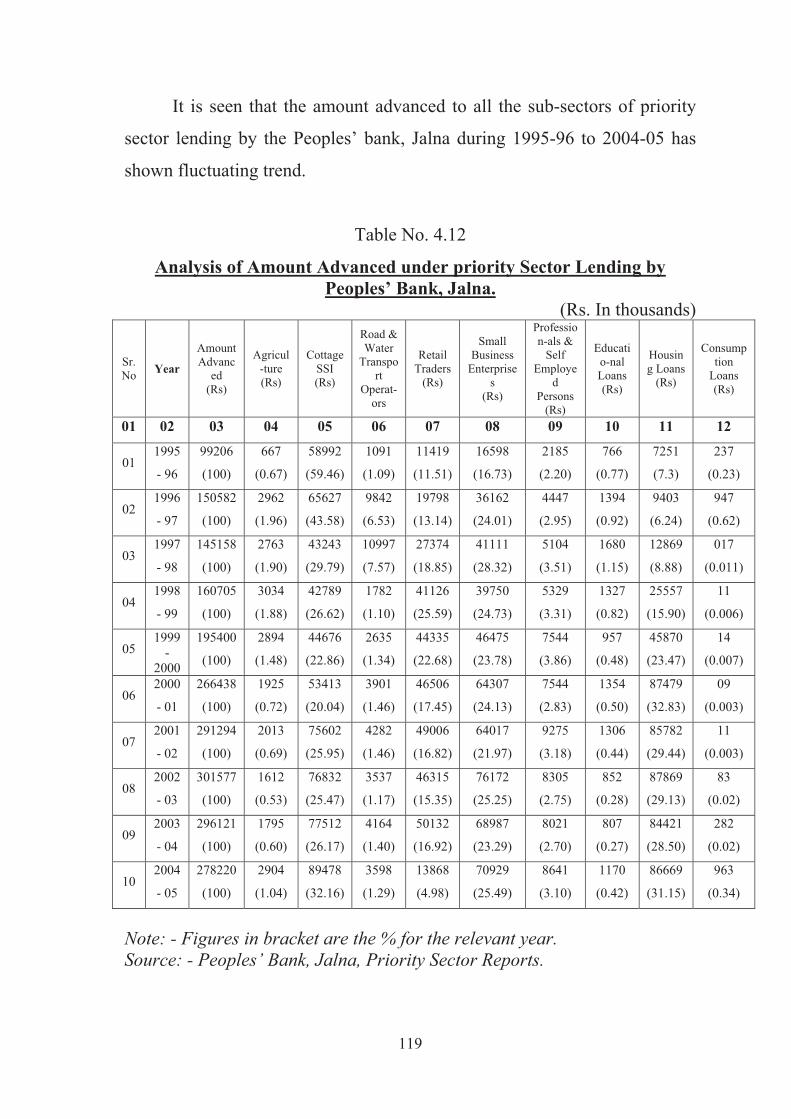

The table no. 4.12 reveals the salient features of amount advanced to

priority sector by Peoples’ bank, Jalna during the period from 1995-96 to

2004-05.

It is revealed from the table no. 4.12 that the amount of advanced

under priority sector lending by Peoples’ bank, Jalna during the period of 10

years from 1995-96 to 2004-05 has shown the increasing trend from 1995-

96 to 2002-03. There after it has declined in 2003-04 and 2004-05. The

total amount of advanced under priority sector lending by Peoples’ bank,

Jalna in 1995-96 was Rs. 99206 thousands. It reached the highest level of

Rs. 301577 thousands in 2002-03 then reduced to Rs. 278220 thousands in

2004-05. It indicates an increase of 2.80 times over a period of 10 years

from 1995-96 to 2004-05.

It is revealed from the table no. 4.12 that the amount of advanced to

various sub-sectors of priority sector by Peoples’ bank over a period of 10

years from 1995-96 to 2004-05 has also shown similar trend as shown by

the limits sanctioned by the Peoples’ bank for the same period.

118

It is seen that the amount advanced to all the sub-sectors of priority

sector lending by the Peoples’ bank, Jalna during 1995-96 to 2004-05 has

shown fluctuating trend.

Table No. 4.12

Analysis of Amount Advanced under priority Sector Lending by

Peoples’ Bank, Jalna.

(Rs. In thousands)

Sr.

NoYear

Amount

Advanc

ed

(Rs)

Agricul

-ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Business

Enterprise

s

(Rs)

Professio

n-als &

Self

Employe

d

Persons

(Rs)

Educati

o-nal

Loans

(Rs)

Housin

g Loans

(Rs)

Consump

tion

Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

99206

(100)

667

(0.67)

58992

(59.46)

1091

(1.09)

11419

(11.51)

16598

(16.73)

2185

(2.20)

766

(0.77)

7251

(7.3)

237

(0.23)

021996

- 97

150582

(100)

2962

(1.96)

65627

(43.58)

9842

(6.53)

19798

(13.14)

36162

(24.01)

4447

(2.95)

1394

(0.92)

9403

(6.24)

947

(0.62)

031997

- 98

145158

(100)

2763

(1.90)

43243

(29.79)

10997

(7.57)

27374

(18.85)

41111

(28.32)

5104

(3.51)

1680

(1.15)

12869

(8.88)

017

(0.011)

041998

- 99

160705

(100)

3034

(1.88)

42789

(26.62)

1782

(1.10)

41126

(25.59)

39750

(24.73)

5329

(3.31)

1327

(0.82)

25557

(15.90)

11

(0.006)

051999

-

2000

195400

(100)

2894

(1.48)

44676

(22.86)

2635

(1.34)

44335

(22.68)

46475

(23.78)

7544

(3.86)

957

(0.48)

45870

(23.47)

14

(0.007)

062000

- 01

266438

(100)

1925

(0.72)

53413

(20.04)

3901

(1.46)

46506

(17.45)

64307

(24.13)

7544

(2.83)

1354

(0.50)

87479

(32.83)

09

(0.003)

072001

- 02

291294

(100)

2013

(0.69)

75602

(25.95)

4282

(1.46)

49006

(16.82)

64017

(21.97)

9275

(3.18)

1306

(0.44)

85782

(29.44)

11

(0.003)

082002

- 03

301577

(100)

1612

(0.53)

76832

(25.47)

3537

(1.17)

46315

(15.35)

76172

(25.25)

8305

(2.75)

852

(0.28)

87869

(29.13)

83

(0.02)

092003

- 04

296121

(100)

1795

(0.60)

77512

(26.17)

4164

(1.40)

50132

(16.92)

68987

(23.29)

8021

(2.70)

807

(0.27)

84421

(28.50)

282

(0.02)

102004

- 05

278220

(100)

2904

(1.04)

89478

(32.16)

3598

(1.29)

13868

(4.98)

70929

(25.49)

8641

(3.10)

1170

(0.42)

86669

(31.15)

963

(0.34)

Note: - Figures in bracket are the % for the relevant year.

Source: - Peoples’ Bank, Jalna, Priority Sector Reports.

119

It is also seen that the amount advanced to consumption loans during

1995-96, 1996-97 and 2002-03 to 2004-05 were relatively higher than the

amount advanced during 1997-98 to 2001-02. It was almost negligible

during 1997-98 to 2001-02.

The relative share of amount advanced to cottage and small scale

industries in total amount advanced by Peoples’ bank, Jalna in 1995-96

were 59.46%. There after its share in amount advanced to priority sector

has continuously declined till 2000-01 and reached to the lowest level of

20.04%. In 2004-05, it reached at 32.16%. It means that the relative

importance of cottage and small-scale industries has declined during the

period 1995-96 to 2004-05. It is seen that the share of cottage and small-

scale industries during 1999-2000 to 2003-04 was lower than the share of

housing loans.

The relative share of amount advanced to housing loans in total

amount advanced under priority sector lending by Peoples’ bank, Jalna was

7.3% in 1995-96. It has successively increased and reached the highest

level of 32.83% in 2000-01. It was 31.15% in 2004-05.

The relative share of amount advanced to retail traders in total amount

advanced under priority sector lending in 1995-96 was 11.51%. It has

continuously increased and reached its highest level of 25.59% in 1998-99.

There after from 1999-00 to 2004-05 it has shown continuously declining

trend and reached its lowest level of 4.98% in 2004-05.

The relative share of amount advanced to small business enterprises

in total amount advanced under priority sector in 1995-96 was 16.73%. It

was at its highest level of 28.32% in 1997-98. In 2004-05, it was at 25.49%.

120

The table no. 4.12 revealed that the relative importance of housing

loans and small business enterprises have increased during the priority

under study. On the other hand, the relative importances of cottage and

small scale industries and retail traders have declined during the same

period.

Analysis of Balance Outstanding under Priority Sector Lending

The study of balance outstanding under priority sector lending by

urban banks is essential to reveal the effectiveness or otherwise of the

lending policy and the collection policy of the urban banks.

The table no. 4.13 reveals the salient features of balance outstanding

under priority sector lending by Deogiri bank, Aurangabad during the period

from 1995-96 to 2004-05.

It is revealed from table no. 4.13 that the amount of balance

outstanding under priority sector lending by Deogiri bank has shown

increasing trend during the period from 1995-96 to 2004-05 except the year

1998-99 in which it has declined marginally from the amount of balance

outstanding for the year 1997-98. The amount of total balance outstanding

under priority sector lending by Deogiri bank for the year 1995-96 was Rs.

145377 thousands. In 2004-05, it was Rs. 1576484 thousands. It indicates an

increase of 10.84 times over a period of 10 years from 1995-96 to 2004-05.

121

Table No: 4.13

Analysis of Balance Outstanding under Priority Sector Lending by

Deogiri Bank

(Rs. In thousands)

Sr.

N

oYear

Total

Balance

outstand-

ing

(Rs)

Agricul

-ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Business

Enterprise

s

(Rs)

Professi

on-als &

Self

Employe

d

Persons

(Rs)

Educati

o-nal

Loans

(Rs)

Housing

Loans

(Rs)

Consu

mption

Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

145377

(100)

2689

(1.84)

59156

(40.69)

20066

(13.08)

16179

(11.12)

708

(0.48)

24687

(16.98)

365

(0.25)

21527

(14.80)Nil

021996

- 97

217375

(100)

986

(0.45)

85370

(39.27)

31328

(14.41)

20368

(9.37)

5310

(2.44)

37904

(17.43)

733

(0.33)

35376

(16.27)Nil

031997

- 98

364936

(100)

4037

(1.10)

145983

(40.00)

59389

(16.27)

35724

(9.78)

18951

(5.18)

57032

(15.63)

717

(0.19)

43103

(11.80)Nil

041998

- 99

357628

(100)

5005

(1.39)

141897

(39.67)

36321

(10.15)

42273

(11.82)

10265

(2.87)

53301

(14.90)

734

(0.20)

67832

(18.96)Nil

05 1999

-00N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A. N. A.

062000

- 01

957968

(100)

24004

(2.50)

410100

(42.80)

71308

(7.44)

98636

(10.29)

52344

(5.46)

102163

(10.66)

4829

(0.50)

194584

(20.31)Nil

072001

- 02

1125196

(100)

50249

(4.46)

349341

(31.04)

60054

(5.33)

128825

(11.44)

33345

(2.96)

273909

(24.34)

4674

(0.41)

224799

(19.97)Nil

082002

- 03

1182491

(100)

39497

(3.34)

559134

(47.28)

66302

(5.60)

146158

(12.36)

25869

(2.18)

86575

(7.32)

3609

(0.30)

255347

(21.59)Nil

092003

- 04

1351557

(100)

76838

(5.68)

625037

(46.24)

48445

(3.58)

153486

(11.35)

64767

(4.79)

80907

(5.98)

6496

(0.48)

295581

(21.86)Nil

102004

– 05

1576484

(100)

174625

(11.07)

539732

(34.23)

31560

(2.00)

237782

(15.08)

90507

(5.74)

69883

(4.43)

6643

(0.42)

406590

(25.79)

19162

(1.21)

Note: - Figures in bracket are the % for the relevant year.

N. A. – Not available

Source: - Deogiri Bank, Aurangabad, Priority Sector Reports

The proportionate share of balance outstanding of Deogiri bank

against the loans granted to cottage and small-scale industries, housing

loans, retail traders and professionals and self-employed persons for the

122

period under consideration found to be much higher than the other segments

of priority sector.

The sub-sectors wise trend of the amount of balance outstanding

against the priority sector lending seems to be similar as seen in case of

limits sanctioned and amount advanced. It is seen that the amount of balance

outstanding is positively co-related with the limits sanctioned and amount of

advanced granted to various sub-sectors of priority sector lending by

Deogiri bank.

The table no. 4.14 reveals the salient features of balance outstanding

under priority sector lending by Peoples’ bank, Jalna during the period from

1995-96 to 2004-05.

123

Table No : 4.14

Analysis of Balance outstanding under priority Sector Lending by

Peoples Bank, Jalna.

(Rs. In thousands)

Sr.

NoYear

Total

Balance

outstan

d

(Rs)

Agricul

-ture

(Rs)

Cottage

SSI

(Rs)

Road &

Water

Transpo

rt

Operat-

ors

Retail

Traders

(Rs)

Small

Business

Enterpris

es

(Rs)

Professio

n-als &

Self

Employe

d

Persons

(Rs)

Educatio

-nal

Loans

(Rs)

Housin

g Loans

(Rs)

Consumpt

ion Loans

(Rs)

01 02 03 04 05 06 07 08 09 10 11 12

011995

- 96

91265

(100)

595

(0.65)

55407

(60.71)

670

(0.73)

10969

(12.01)

15533

(17.01)

1856

(2.03)

406

(0.44)

5596

(6.13)

233

(0.25)

021996

- 97

138705

(100)

2961

(2.13)

61363

(44.23)

8537

(6.15)

18584

(13.39)

34353

(24.76)

3947

(2.84)

1365

(0.98)

7567

(5.45)

28

(0.020)

031997

- 98

122364

(100)

2752

(2.24)

44446

(36.32)

8826

(7.27)

9743

(7.96)

39471

(32.25)

4896

(4.00)

1472

(1.20)

10758

(8.79)Nil

041998

- 99

154229

(100)

3059

(1.98)

42363

(27.46)

1420

(0.92)

39616

(25.68)

37196

(24.11)

4630

(3.00)

1324

(0.85)

24608

(15.95)

13

(0.008)

051999

-

2000

191160

(100)

3124

(1.63)

43963

(22.99)

1817

(0.95)

48336

(25.28)

41108

(21.50)

6551

(3.42)

806

(0.42)

45444

(23.77)

11

(0.005)

062000

- 01

252433

(100)

2279

(0.90)

54404

(21.55)

3123

(1.23)

46089

(18.25)

65068

(25.77)

6852

(2.71)

1241

(0.49)

73368

(29.06)

09

(0.003)

072001

- 02

278737

(100)

2689

(0.96)

78934

(28.31)

3014

(1.08)

47951

(17.20)

59723

(21.42)

7893

(2.83)

1566

(0.56)

76955

(27.60)

12

(0.004)

082002

- 03

275292

(100)

2202

(0.79)

75681

(27.49)

2346

(0.85)

45646

(16.58)

72919

(26.48)

7214

(2.62)

939

(0.34)

68261

(24.79)

84

(0.030)

092003

- 04

270626

(100)

1758

(0.64)

78187

(28.89)

3189

(1.17)

47027

(17.38)

66186

(24.45)

7211

(2.67)

826

(0.30)

65960

(24.37)

282

(0.10)

102004

- 05

249052

(100)

2957

(1.18)

88430

(35.50)

2670

(1.07)

13679