Embed Size (px)

Citation preview

Financial Restructuring11

CHAPTER INDEX

1. Need for Financial Restructuring.

2. Reorganisation of Capital.

3. Reduction of Share Capital.

4. Buyback of Shares – Concept and Objects.

5. Provisions of Buy Back under Companies Act, 2013.

6. SEBI (Buy Back of Securities) Regulations, 1998.

7. Private Limited Company and Unlisted Public Limited Company (Buy Back of Securities) Rules, 1999.

ALLOCATION OF MARKS TO THIS CHAPTER IN THE LAST 11 EXAMS.

LEVEL CS Professional Programme

EXAM D08 J09 D09 J10 D10 J11 D11 J12 D12 J13 D13

THEORY 6 17 – 5 7 17 – – – – 9

PRACTICAL – – 8 8 4 3 – 15 – – –

TOTAL 6 17 8 13 11 20 – 15 – – 9

11.2 Reliance’s Corporate Restructuring, Valuations and Insolvency

I PMPORTANT ROVISIONS AT A GLANCE

1. KEY NOTES.

1. Financial restructuring of a company involves a rearrangement of its financial structure to make the company’s finances more balanced.

2. A company may reorganize its capital in different ways, such as reduction of paid up share capital; conversion of one type of shares into another; conversion of shares into debentures or other securities.

3. Section 66 of the Companies Act deals with reduction of capital which means reduction of issued, subscribed and paid up capital of the company.

4. Section 68 of the Companies Act is an exception to the prohibition under Section 67 as it allows companies to buy-back their own shares as well as ‘other specified securities’, subject to the conditions specified therein.

5. Under Section 68, any company limited by shares or company Ltd. by guarantee and having a share capital can buy-back its own securities, whether it is a private, public, listed or unlisted company.

6. The buy back of securities of listed companies are guided by SEBI (Buy-back of Securities) Regulations, 1998.

7. The buy-back in respect of securities which are not listed on any recognized stock exchange must be in accordance with Private Limited Company and Unlisted Public Limited Company (Buy-back of Securities) Rules, 1999.

2. FINANCIAL STRUCTURE OF A COMPANY.

Broadly speaking, the financial structure of a company comprises its

(i) paid up equity and preference share capital;

(ii) various reserves;

(iii) all borrowings in the form of –

(a) long-term loans from financial institutions;

(b) working capital from banks including loans through commercial papers;

(c) debentures;

(d) bonds;

(e) credits from suppliers;

(f) trade deposits;

(g) public deposits;

(h) deposits/loans from directors, their relatives and business associates;

Financial Restructuring 11.3

(i) deposits from shareholders;

(j) Global Depository Receipts, American Depository Receipts and Foreign Currency Convertible Bonds;

(k) funds raised through any other loan instrument.

A company may require any one or more of the above keeping in view its financial requirements at a particular point of time. A dynamic Board should constantly review the financial structure of the company and effect financial restructuring and reorganisation whenever the need arises.

3. NEED FOR FINANCIAL RESTRUCTURING.

A company is required to balance between its debt and equity in its capital structure and the funding of the resulting deficit. The targets a company sets in striking this balance are influenced by business conditions, which seldom remain constant.

When, during the life time of a company, any of the following situations arise, the Board of Directors of a company is compelled to think and decide on the company’s restructuring:

(i) necessity for injecting more working capital to meet the market demand for the company’s products or services;

(ii) when the company is unable to meet its current commitments;

(iii) when the company is unable to obtain further credit from suppliers of raw materials, consumable stores, bought-out components etc. and from other parties like those doing job work for the company.

(iv) when the company is unable to utilise its full production capacity for lack of liquid funds.

Financial restructuring of a company involves rearrangement of its financial structure so as to make the company’s finances more balanced.

4. OVER CAPITALISATION AND UNDER CAPITALISATION.

A company is said to be over-capitalized, if its earnings are not sufficient to justify a fair return on the amount of share capital and debentures that have been issued. Otherwise, it is said to be over capitalized when total of owned and borrowed capital exceeds its fixed and current assets i.e. when it shows accumulated losses on the assets side of the balance sheet.

If the owned capital of the business is much less than the total borrowed capital than it is said to be under capitalization. We may say that the owned capital of the company is disproportionate to the scale of its operation and the business is dependent more upon borrowed capital.

Key Notes: Under capitalization may be the result of excess volume of trading and over capitalization may be due to insufficient volume of trading.

11.4 Reliance’s Corporate Restructuring, Valuations and Insolvency

5. RESTRUCTURING OF UNDER CAPITALISED COMPANY.

An under-capitalized company may restructure its capital by taking one or more of the following corrective steps:

(i) injecting more capital whenever required either by resorting to rights issue/preferential issue or additional public issue.

(ii) resorting to additional borrowings from financial institutions, banks, other companies etc.

(iii) issuing debentures, bonds, etc. or

(iv) inviting and accepting fixed deposits from directors, their relatives, business associates and public.

6. RESTRUCTURING OF OVER CAPITALISED COMPANY.

If a company is over-capitalized, its capital also requires restructuring by taking following corrective measures:

(i) Buy-back of own shares.

(ii) Paying back surplus share capital to shareholders.

(iii) Repaying loans to financial institutions, banks, etc.

(iv) Repaying fixed deposits to public, etc.

(v) Redeeming its debentures, bonds, etc.

State whether the following statement is true or false.

A over capitalized company can resort to buy- back of shares.

Ans: True

Financial Restructuring 11.5

7. PROCEDURE FOR REDUCTION OF CAPITAL.

Pass special resolution and �le MGT-14 with Registrarof Companies

File Form No. INC-28 with registrar ofcompanies with respect to court ordersanctioning the reduction

11.6 Reliance’s Corporate Restructuring, Valuations and Insolvency

8. BUY BACK OF SHARES.

The Concept: The Companies Amendment Act, 1999 introduced the concept of buy-back of shares.

Buy-back of shares means the purchase by the company of its own shares. Buy-back of equity shares is an important mode of capital restructuring. It is a corporate financial strategy which involves capital restructuring and is prevalent globally with the underlying objectives of increasing earnings per share, averting hostile takeovers, improving returns to the stakeholders and realigning the capital structure.

In India, while buy-back of securities is not permitted as a treasury option under which the securities may be reissued later, a company can resort to buy-back to reduce the number of shares issued and return surplus cash to the shareholders.

Legal Framework:

(a) The Companies Act, 2013 - Sections 68, 39 and 70 (applies to listed and unlisted companies).

(b) Securities and Exchange Board of India (Buyback of Securities) Regulations, 1998(applies to a listed company).

(c) Private Limited Company and Unlisted Public Limited Company (Buy-back of Securities) Rules, 1999(applies to an unlisted company).

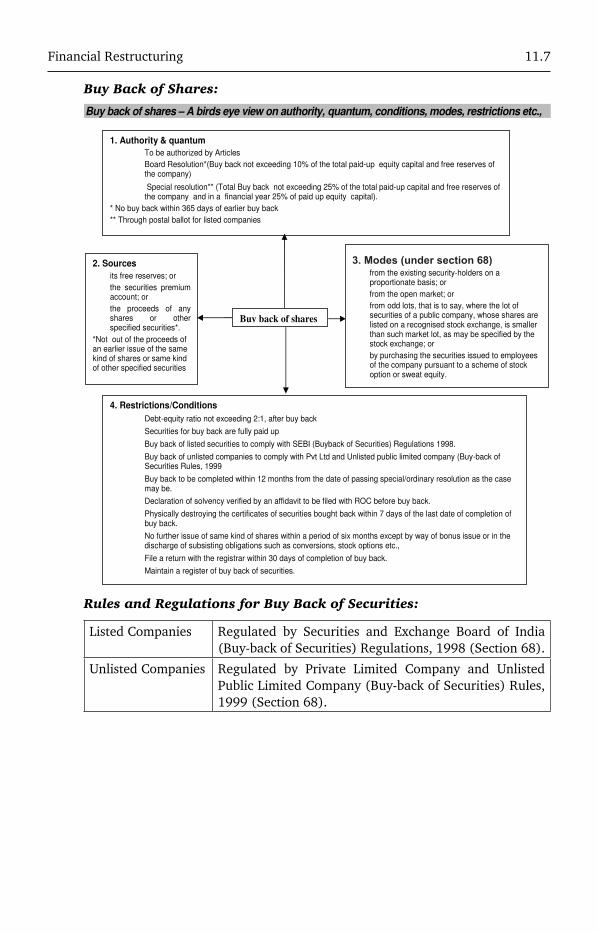

Financial Restructuring 11.7

Buy Back of Shares:

3. Modes (under section 68)

Rules and Regulations for Buy Back of Securities:

Listed Companies Regulated by Securities and Exchange Board of India (Buy-back of Securities) Regulations, 1998 (Section 68).

Unlisted Companies Regulated by Private Limited Company and Unlisted Public Limited Company (Buy-back of Securities) Rules, 1999 (Section 68).

11.8 Reliance’s Corporate Restructuring, Valuations and Insolvency

QUESTIONS FROM PAST CS EXAMINATIONS

S NHORT OTES

2004, June CS Final, 3 Marks SN 1: Write short notes on the following:

Buy-back through book building.

Answer: Buy-back through book-building route: A company can buy-back its securities through the book building route under Regulation 17 of (SEBI (Buy-back of Securities) Regulations, 1998) by the following procedures:

(i) The maximum price at which the buy-back will be made is to be specified in the resolution.

(ii) The company should appoint a merchant banker.

(iii) Public announcement regarding buy-back should be made at least 7 days prior to commencement of buy-back.

(iv) Escrow account as per Regulation 10 to be opened and deposit therein shall be’ made before the date of public announcement.

(v) The copy of public announcement has to be filed with SEBI within 2 days of announcement along with stipulated fees.

(vi) Book building process should be made through an electronically linked transparent facility.

(vii) Bidding centres to be opened which shall not be less than 30 in number and at least one electronically linked terminal should be there at all bidding centres.

(viii) Offer of buy back should remain open for a period of not less than 15 days and not exceeding 30 days.

(ix) The buy-back price shall be based on the acceptances received and the highest price accepted in the bidding process should be paid to all holders whose securities have been accepted for buy-back.

2004, December, CS Final, 4 Marks SN 2: Write short notes on the following:

Declaration of solvency in case of buy-back of securities.

Answer: Declaration of Solvency in case of buy-back of securities: In case of buy-back of shares by a company, before making buy-back, the company must file with the ROC and SEBI, a declaration of solvency in the prescribed Form No. SH-9 and verified by an affidavit to the effect that the Board of Directors has made full inquiry into the affairs of the company and as a result of that has formed opinion that the company is capable of meeting its liabilities and will not be rendered insolvent within

Financial Restructuring 11.9

a period of one year from the date of declaration adopted by the Board, and signed by at least two directors of the company, one of whom should be managing director, if any.

No declaration of solvency shall be filed with the Securities and Exchange Board of India by a company whose shares are not listed on any recognized stock exchange.

D BISTINGUISH ETWEEN

2010, December Professional Programme - 3 Marks DB 1: Distinguish the following;

‘Reduction of capital’ and ‘diminution of capital’.

Answer: Reduction of capital’ and ‘diminution of capital’: Reduction of Capital means reduction of issued, subscribed and paid up capital of the Company. Section 66 provides for reduction of share capital, if there is an enabling provision in the Articles of Association of the company. A company may resort to reduction of capital to restructure its capital to clean balance sheet by reducing business losses, heavy capital expenditures etc. The company need to seek confirmation of the Court to reduce its capital. There are following ways to reduce capital of the company, namely:

1. By reducing or extinguishing the liability of members in respect of uncalled or unpaid capital;

2. By paying off or returning paid up capital not wanted for the company;

3. By conditional pay off of un paid capital;

4. By combination of any of the above methods;

5. By writing off or cancelling the capital lost or unrepresented by assets of the company.

In following cases diminution of Capital shall not mean reduction of capital such as

1. Cancellation of shares which have not been taken or agreed to be taken by any person under section 61 of the Companies Act, 2013;

2. Redemption of redeemable preference shares u/s 80 of the Companies Act, 2013;

3. Buy Pack of shares u/s 77A of the of the Companies Act, 2013.

11.10 Reliance’s Corporate Restructuring, Valuations and Insolvency

D QESCRIPTIVE UESTIONS

2004, June, CS Final, 4 Marks DQ 1: Describe the needs for financial restructuring and what steps may be taken in case of under-capitalisation and over-capitalisation.

Answer: Need for financial restructuring: When during the life time of a company, any of the following situations arise,.the Board of Directors of a company is compelled to think and decide on the company’s restructuring:

(i) necessity for injecting more working capital to meet the market demand for the company’s products or services;

(ii) when, the company is unable to meet its current commitments;

(iii) when the company is unable to obtain further credit from suppliers of raw materials, consumable stores, bought out components etc. and from other parties like those doing job work for the company.

(iv) when the company is unable to utilize its full production capacity for lack of liquid funds.

An under-capitalized company may consider restructuring its capital by taking one or more of the following corrective steps :

(a) injecting more capital whenever required either by resorting to rights issue or additional public issue.

(b) resorting to additional borrowings from financial institutions, banks, other companies, etc.

(c) issuing debentures, bonds, etc. or

(d) inviting and accepting fixed deposits from directors, their relatives, business associates and public.

If a company is over capitalized, it can consider restructuring its capital by taking following corrective measures :

(a) Buy-back of own shares;

(b) Paying back surplus share capital to shareholders;

(c) Repaying loans to financial institutions, banks, etc.

(d) Repaying fixed deposits to public; etc.

(e) Redeeming its debentures, bonds/etc

2004, June, CS Final, 8 Marks DQ 2: What is the offer procedure under the buy-back regulations for buy-back from existing shareholders.

Financial Restructuring 11.11

Answer: As per Regulation 9 of Securities & Exchange Board of India (Buy-back of Securities) Regulations, 1998 the procedure for offer for buy-back from existing shareholders is as follows:

1. The offer must remain open for a period of not less than 15 days and not exceeding 30 days.

2. The date of opening of the offer must not be earlier than 7 days or later than 30 days after the specified date.

3. The letter of offer should be sent so as to reach the security holders before the opening of the offer.

4. If number of specified securities offered by security holders is more than total No. of specified securities to be bought back, then the following formula should be applied to decide the eligibility.:

AS =

ATSTA

NSB×

where, AS = Acceptance per security holder

ATS = Acceptance tendered by security holder

TA = Total acceptance received.

NSB = Total Number of securities to be bought back.

5. The company is required to complete the verification of the offer within 15 days, of the closure of the offer and the specified securities lodged shall be deemed to be accepted unless a communication of rejection is made within fifteen days from the closure of the offer.

2004, December, CS Final, 4 Marks DQ 3: What are the provisions for extinguishment of bought back securities under the Companies Act, 2013 as well as the SEBI Regulations?

Answer: Section 68 of the Companies Act, 2013 lays down that where a company buys back its own securities, it should, within seven days of the last date of completion of the buy-back, extinguish and physically destroy the securities so bought back. Regulation 12 of the SEBI Regulations provides that -

1. The company should extinguish and physically destroy the securities certificates so bought back, in the presence of a Registrar or the Merchant Banker, and the Statutory Auditor within seven days from the date of acceptance of the securities.

2. In case of dematerialized securities, these should be extinguished and destroyed in the manner specified under the SEBI (Depositories and Participants) Regulations, 1996 and the bye-laws made thereunder.

3. The company is required to furnish a certificate to SEBI by :

(a) the Registrar and where there is no Registrar, through the Merchant banker,

(b) two whole-time directors, including the managing director;

11.12 Reliance’s Corporate Restructuring, Valuations and Insolvency

(c) the statutory auditor of the company; and (d) certifying compliance as specified by sub-regulation (1) within seven days of the extinguishments and destruction of the certificates.

4. The particulars of the security certificates extinguished and destroyed under sub-regulation (1) should be furnished to the stock exchange where the securities of the company are listed within seven days of extinguishments and destruction of the certificates.

2004, December, CS Final, 6 Marks DQ 4: What is “buy-back of securities’ ? Discuss the sources and methods of buy-back of securities by a listed company.

Answer: ‘Buy-back of securities’ is a prominent mode of restructuring the capital of the company. It is a financial strategy that allows a company to buy back its equity shares and other specified securities, including securities issued of employees of the company pursuant to a scheme of stock option or sweat equity.

Buy back of securities is regulated by Sections 68, 69 and 70 of the Companies Act, 2013. In case of Listed companies, SEBI (Buy Back of Securities) Regulations 1998 are also applicable and are to be complied with.

According to Section 68 of the Companies Act, 2013, a company may purchase its own shares or other specified securities out of three sources :

(i) its free reserves; or

(ii) the securities premium account; or

(iii) the proceeds of any shares or other specified securities.

Provided that no buy back of any kind of shares or other specified securities shall be made out of the proceeds of an earlier issue of the same kind of shares or the same kind of other specified securities.

As per Section 68, the permissible methods of buy-back of securities include the following:

(a) Buy back from the existing security-holders on a proportionate basis; or

(b) Buy back form open market; or

(c) Buy back from odd lots; and

(d) Buy back by purchasing the securities issued pursuant to a scheme of stock option or sweat equity,

As per regulation 4 of the SEBI (Buy Back of Securities) Regulations, 1998, a listed company may buy back its own securities by any one of the following methods:.

(a) Buy back from the existing security-holders on a proportionate basis through the tender offer; or

(b) Buy back from open market through :

– Book building process

Financial Restructuring 11.13

– Stock exchange

(c) Buy back from odd lot-holders.

2005, June, CS Final, 4 Marks DQ 5: Comment on the following proposals citing case laws, wherever applicable:

A company proposes to compulsorily acquire shares held by small shareholders under a scheme of arrangement.

Answer: Section 391 (2) of the Companies Act, 1956 provides that if a majority in number representing three-fourths in value of the creditors, or class of creditors, or members, or class of members, as the case may be, present and voting either in person or by proxy at the meeting, agree to any compromise or arrangement, the compromise or arrangement shall, if sanctioned by the Court, be binding on all the creditors, all the creditors of the class, all the members, or all the members of the class as the case may be, and also on the company.

Also, Section 395(1) provides that where a scheme or contract involving the transfer of shares of the transferor company to transferee company, has, within four months after the making of the offer been approved by the holders of not less than nine-tenths (9/10th) in value of the shares whose transfer is involved, the transferee company may, at any time within two months after the expiry of the said four months, give notice in the prescribed manner to any dissenting shareholder, that it desires to acquire his shares.

The transferee company shall, unless, on an application made by the dissenting shareholder within one month from the date on which the notice was given the Court thinks fit to order otherwise, be entitled and bound to acquire those shares on the terms on which, under the scheme or contract, the shares of the approving shareholders are to be transferred to the transferee company.

It has been held in SEBI v. Sterlite Industries (India) Ltd. (2003) 53 CLA 41 (Bom) that under Section 391 of the Companies Act, the court is vested with very wide powers to approve or sanction any scheme of amalgamation; arrangement, compromise or reconstruction. The Court has the power to sanction all matters which for their effectuation require a special procedure to be followed under the Companies Act. The only exception to this is special procedure to be followed under Section 101 for reduction of capital since Rule 85 of the Companies (Court) Rules, 1959 specifically enjoins the following of special procedure prescribed for reduction of share capital.

Note: The provision relating to this section has not yet been notified.

2005, June, CS Final, 6 Marks DQ 6: List out the communications to be made with various authorities in a buy-back process. Draft one such communication.

Answer: List of Communications to be made with various authorities in a Buy-back process:

11.14 Reliance’s Corporate Restructuring, Valuations and Insolvency

(i) Registrar of Companies (ROC)

(a) File Form MGT-14 within 30 days from the date of passing the special resolution in the general meeting.

(b) File declaration of solvency in Form SH-9 before the buy-back.

(c) File Form SH-11 within 30 days of completion of Buy back.

(ii) Securities and Exchange Board of India (SEBI)

(a) File a copy of the special resolution within 7 days from the date of passing of the resolution.

(b) File a copy of the public announcement within 2 days of the announcement.

(c) File draft letter of offer within 7 days of the public announcement, if the shares are to be bought back from the existing shareholders.

(d) File Declaration of Solvency in Form 4A before the Buy back.

(e) File certificate of compliance regarding extinguishment and physical destruction of securities within 7 days.

(f) File Form SH-11 within 30 days of completion of Buy back.

(iii) Stock Exchanges where securities are listed

(a) Intimate about Board meeting convened to decide buy back.

(b) File a copy of the special resolution within 7 days,.

(c) Furnish particulars of the security certificates extinguished and destroyed within 7 days of the extinguishments and destruction of the share certificates.

(d) File a copy of the letter of offer before opening date of the offer.

(e) File share holding pattern after the buy back of shares.

Specimen of one such communication

Draft of Form SH-9 to be filed with SEBI & ROC is

FORM NO. SH-9Declaration of solvency

(See Rule 5C)

Name of Company : .........................................

Address (Regd. Office) : .........................................

Presented by :.........................................(Name)

......................................... (Designation)

We,...................................of.................................. and...............................being all the directors of M/s.................................. do solemnly affirm and declare that we have formed the opinion that the company is capable of meeting its total liabilities and that the company will not be rendered insolvent within a period of one year from the date of making this declaration.

Financial Restructuring 11.15

We append a statement of company’s assets and liabilities as at ...........................being the latest date before making of this declaration.

We further declare that the company’s audited annual accounts including the Balance Sheet have been filed upto date with the Registrar of Companies............................

Signature ....................

Name .........................

Managing Director

Signature ....................

Name : .......................

Directors

Signature ....................

Name .........................

Directors

Verification

And we make this solemn declaration believing the same to be true.

We solemnly declare that we have made a full enquiry into the affairs of the company including assets and liabilities of this company and that having done so and having noted that the shareholders by a special resolution have approved the buy-back of................... (...................)(in words) number of shares/securities as per the provisions of Section 68 of the Companies Act, 2013, as inserted by the Companies (Amendment) Ordinance, 1999.

Verified this...................day the...................day of...................20......

Signature ....................

Name .........................

Managing Director

Signature ....................

Name : .......................

Directors

Signature ....................

Name .........................

Directors

Solemnly affirmed and declared at................the................ day of................ 20…… before me.

Commissioner for Oaths and Notary Public or Justice of the Peace

[NOTE: Students may give a draft of any other such communication].

11.16 Reliance’s Corporate Restructuring, Valuations and Insolvency

2005, December, CS Final, 6 Marks DQ 7: Explain the concepts of ‘financial restructuring’ in the cases of under-capitalised and over-capitalised companies.

Or

Describe ‘financial restructuring’. What steps may be taken in case of under-capitalisation and over-capitalisation? [2007, December, CS Final, 6 Marks]

Or

A company is overcapitalized due to rights issue, bonus issue and allotment of shares to the shareholder of transferor companies. Its share prices have plunged due to floating shares and do not represent its fair value in the market. The management is now thinking to take some corrective measures. The company has sufficient liquid cash at its disposal. State briefly the corrective measures. [2010, December Professional Programme - 4 Marks]

Answer: Financial restructuring deals with the restructuring of capital base and raising finance for new projects. This involves decisions relating to acquisitions, mergers, joint ventures and strategic alliances. Financial restructuring of a company involves a rearrangement of its financial structure to make the company’s finances more balanced.

Restructuring of under capitalized company: An under capitalized company may consider restructuring its capital by taking one or more of the following corrective step:

(a) Injecting more capital whenever required either through right issue/preferential Issue or additional public issue;

(b) Resorting to additional borrowings from financial institutions, banks, etc.

(c) Issuing debentures, bonds, etc.; or

(d) Inviting and accepting fixed deposits from directors, their relatives, business associates and public.

Restructuring of over capitalized company: If a company is over capitalized, its capital also requires restructuring by taking following corrective measures :

(a) Buy back of own shares;

(b) Paying back surplus capital to shareholders;

(c) Repaying loans to financial institutions, banks, etc.;

(d) Repaying fixed deposits to public etc.;

(e) Redeeming its preference shares, debentures, bonds, etc.

A dynamic Board should constantly review the financial structure of the company and effect financial restructuring and recoganization whenever the need arises.

Financial Restructuring 11.17

2005, December, CS Final, 2 Marks DQ 8: State whether the following statements are true or false and mention briefly the relevant provisions of law:

A company can buy-back more than 25% of its paid-up capital in a single year.

Answer: The statement is partly true. In terms of Section 68, a company cannot buy-back more than 25% of its total paid-up capital and free reserves. Further, buy-back of equity shares in any financial year should not exceed 25% of the total paid-up equity capital of the company.

However, in the case of SEBI v. Sterlite Industries (India) Ltd. (2003) 53 CLA 41 (2002) 113 Comp Cas 273 (Bom), the Bombay High Court has held that, the submission that the non-obstinate clause in Section 68 gives precedence to that section over the provisions of Sections 66, and Section 391 is misconceived. Section 68 is merely an enabling provision and the court’s powers under Sections 66 and Section 391 are not in any way affected.

Therefore, if so directed by the court, the company can buy back more than 25% of its paid up capital in a single year.

2006, June, CS Final, 4 Marks DQ 9: What are the obligations’ of a company after the announcement of buy-back of securities?

Answer: According to Regulation 19 of the SEBI (Buyback of Securities) Regulations, 1998, the following are the obligations of a company after the announcement of Buyback of securities:

(i) all material connected with buyback must contain true and factual information only and must also state that the directors of the company accept the responsibility for information provided in such material.

(ii) the company shall not issue any shares or other specified securities including by way of bonus till the date of closure of the offer.

(iii) the company shall pay consideration in cash only;

(iv) the offer letter once filed with SEBI or the public announcement of the offer to buy-back will not be withdrawn.

(v) the promoter shall not deal in the shares or specified securities of the company during the period of buy back.

(vi) no public announcement of buy back shall be made during the pendency of any scheme of amalgamation/compromise/arrangement.

(vii) nominate a compliance officer and investors’ service centre for compliance and redressal of investor grievances in this connection;

(viii) particulars of security certificates extinguished and destroyed to be furnished to stock exchange where the shares or other specified securities are listed within 7 days of extinguishment and destruction of certificates;

11.18 Reliance’s Corporate Restructuring, Valuations and Insolvency

(ix) locked in securities not to be bought back;

(x) publication of post buy back advertisement within 2 days of completion in a national daily with complete details of number of securities bought back, amount invested etc.

2006, December, CS Final, 6 Marks DQ 10: What are the disclosures to be made in the letter of offer for buy-back?

Answer: The letter of offer shall inter, alia contain the following:

(i) Details of the offer to be effected.

(ii) Proposed time table of the offer till extinguishment of certificates.

(iii) Authority for offer of buyback

(iv) Full and complete disclosure of all material facts

(v) Necessity for buy back

(vi) Process to be adopted for buy-back.

(vii) Minimum and maximum number of securities that the company proposes to buy back; sources of funds and cost of financing.

(viii) Brief information about the company.

(ix) Audited financial information for the last three years and the particulars shall not be more than six months old from the date of offer documents, together with financial ratios.

(x) Present capital structure

(xi) Aggregate shareholding of promoter group and of persons who are in control of the company;

(xii) Management discussion and analysis on the likely impact of buyback on company’s earnings, public holidays, holdings of NRIs, change in management, structure.

(xiii) Details of statutory approvals obtained.

(xiv) Aggregate number of equity shares purchased or sold by the promoter/s during the twelve month preceding the date of the offer with the maximum and minimum price at which purchase and sales were made.

(xv) Certain declarations.

(xvi) Such other disclosures as may be specified by Central Government.

(xvii) The offer letter must be dated and signed by the Board of Directors.

2008, December, CS Final, 6 Marks DQ 11: Can a private or an unlisted public company buy-back its own shares? Answer citing relevant provisions of the law.

Financial Restructuring 11.19

Answer: The procedure to be adopted for buy-back of securities by private limited companies and by unlisted public limited companies is laid down in Sections 68, 69 and 70 of the Companies Act, 2013 and the Private Limited Company and Unlisted Public Limited company (Buy-back of Securities) Rules, 1999.

According to Rule 3, an unlisted company can buy-back its shares from the existing shareholders on a proportionate basis through private offers or by purchasing the securities issued to employees of the company pursuant to a scheme of stock option or sweat equity. The process of buy-back of shares begins with the approval of the Board of Directors of the Company. The Board will pass the necessary resolutions approving the proposal for buy-back.

When buy-back is subsequently to be approved by a special resolution passed in a general meeting of the company, the notice of the general meeting at which the special resolution is proposed to be passed should be accompanied by an explanatory statement.

Rule 5 lays down that before buy-back, the company should file with the concerned Registrar of Companies a draft letter of .offer containing the prescribed particulars as specified in Schedule II of the Rules.

The procedure is as under :

(a) According to the Rule 6, the letter of offer should be despatched immediately after filing with the Registrar of Companies but not later than 21 days from such filing.

(b) The offer should remain open to the members for a period of not less than fifteen days and not exceeding thirty days from the date of despatch of the letter of offer.

(c) In case the number of shares offered by the shareholders is more than the total number of shares to be bought back by the company, the acceptance per shareholder should be on proportionate basis.

(d) The company should complete the verification of the offers received within 15 days of the closure of the offer and the shares lodged will be deemed to be accepted unless a communication of rejection is made within 21 days from the closure of the offer.

The rules with regard to payment to shareholders :

(a) Rule 7 provides that the company should immediately after the date of closure of the offer open a special bank account and deposit therein, such sum, as would make up the entire sum due and payable as consideration for the buy-back in terms of the Rules.

(b) The company should within 7 days of the specified period make the payment of consideration in cash or bank draft/pay order to those shareholders whose offer has been accepted or return the share certificates to the shareholders forthwith.

2009, June, CS Final, 5 Marks DQ 12: Explain the provisions relating to buy-back of shares through book-building, route.

11.20 Reliance’s Corporate Restructuring, Valuations and Insolvency

Answer: Buy Back through Book Building Route: A company can buy back its securities through the book building process as provided under Securities and Exchange Board of India (Buy Back of Securities) Regulations, 1998 which is as under:

1. (a) The special resolution as in Regulation 5 or 5A, should specify the maximum price at which the buy back will be made.

(b) The company should appoint a merchant banker.

(c) A public announcement as referred to in Regulation 8 shall be made atleast 7 days prior to the commencement of the buy back.

(d) Subject to the provisions of Sub- clauses (i) and (ii), the provisions of Regulation 10 regarding escrow account are applicable –

(i) The deposit in the escrow account should be made before the date of the public announcement.

(ii) The amount to be deposited in the escrow account should be determined with reference to the maximum price as specified in the public announcement.

(e) A copy of the public announcement must be filed with SEBI within two days of the announcement along with the fees specified in Schedule IV to the Regulations. The public announcement shall also contain the detailed methodology of the book building process, manner of acceptance, format of acceptance to be sent by the security holders pursuant to public announcement and details of bidding centers.

(f) The book building process should be made through an electronically linked transparent facility.

(g) The number of bidding centers should not be less than thirty and there should be atleast one electronically linked computer terminal at all the bidding centers;

(h) The offer for buy back should be kept open to the security holders for a period of not less than fifteen days and not exceeding thirty days.

(i) The merchant banker and the company should determine the buy back price based on the acceptances received and the final buy back price which should be the highest price accepted should be paid to all the holders whose securities have been accepted for the buy back.

2. The provisions of Regulation 9(5) pertaining to verification of acceptances and the provisions of Regulation 11 pertaining to opening of special account and payment of consideration are applicable mutatis mutandis.

2009, June, CS Final, 7 Marks DQ 13: Reduction of capital is one of the modes of re-organisation of capital structure of the company and to a certain extent it can be done without the sanction of the court. Explain with relevant provisions of the law.

Financial Restructuring 11.21

Answer: A company may reorganize its capital in different ways which may include the following:

(a) reduction of paid-up capital;

(b) conversion of one type of shares into another;

(c) conversion of shares into debentures.

There may be many other ways and manner of reorganization of capital. Re-organization of share capital may be proposed between the company and its creditors or class of creditors or members or class of members and requires confirmation of CLB under Section 391 (new section not yet notified). Reduction of capital means reduction of issued, subscribed and paid up capital of the company. Section 100 provides for the reduction of share capital, if the articles of the company so authorize with the confirmation of the Court.

However in following cases, reduction of share capital can be made without sanction of court

(a) Surrender of Shares: This means the surrender of shares already issued to the company by the registered holder of shares. Where shares are surrendered to the company, whether by way of settlement of a dispute or for any other reason, it will have the same effect as a transfer in favour of the company and amount to reduction of capital. But if, under any arrangement such shares instead of being surrendered to the company, are transferred to a nominee of the company then there will be no reduction of capital [Collector of Moradabad v. Equity Insurance Company Limited (1948) 18 Com Cases 309: AIR 1948 Oudh 197]. Surrender may be accepted by the company under the same circumstances where forfeiture is justified. It has the effect of releasing the shareholder whose surrender is accepted for further liability on shares.

The Companies Act contains no provisions for surrender of shares. Thus surrender of shares is valid only when Articles of Association provide for the same and;

(i) Where forfeiture of such shares is justified; or

(ii) When shares are surrendered in exchange for new shares of same nominal value.

Both forfeiture and surrender lead to termination of membership. However, in the case of forfeiture it is at the initiative of the company and in the case of surrender it is at the initiative of member or shareholder.

(b) Forfeiture of Shares: A company may if authorized by its articles, forfeit shares for non-payment of calls and the same will not require confirmation of the court.

Where the power is given in the articles, it must be exercised strictly in accordance with the regulations regarding notice, procedure and manner stated therein, otherwise the forfeiture will be void. Forfeiture will be effected by means of Board resolution.

The power of forfeiture must be exercised bona fide and in the interest of the company.

11.22 Reliance’s Corporate Restructuring, Valuations and Insolvency

(c) Diminution of Capital: Where the company cancels shares which have not been taken or agreed to be taken by any person. [Section 61]

(d) Redemption of redeemable preference shares.

(e) Purchase of shares of a member by the company under Section 242.

(f) Buy back of its own shares under Section 68.

(g) Reduction of capital when company is defunct.

2009, June, CS Final, 5 Marks DQ 14: In a buy-back of securities, a company-has to pay stamp duty under the Indian Stamp Act, 1899 for physical shares. Do you agree? Explain.

Answer: Any transfer of shares is liable for stamp duty under the Indian Stamp Act, 1899 vide entry No. 62 in the Schedule I. For completion of transfer of shares, a company is required to register the shares in the name of the transferee. But purchase of own shares by a company cannot be registered in the name of the company. These shares are supposed to be mandatorily extinguished and the capital stands reduced to that extent. They cannot keep the bought back shares as ‘Treasury Stock” for reissue though such things are permissible in some western countries.

As per provisions of the Companies Act, 2013 and relevant rules, the bought back shares must be extinguished within 7 days from the closure date of said buy back and it should not be” treated as “Release” under Article 55 of the Indian Stamp Act. Hence, no registration of such shares takes place in the name of the company.

The names of the members/shareholders from whom the shares are bought back, have to be struck off from the register of members of the company. Therefore, buy back cannot be considered as transfer and stamp duty would not be payable in a case where buy-back of shares takes place in physical form even if the shares are accompanied by an application form for transfer of shares in favour of the company.

2010, June Professional Programme – 5 marks DQ 15: Though the terms ‘diminution of share capital’ and ‘reduction of capital’ look synonymous, but sometimes diminution of share capital does not amount to reduction of capital Briefly explain the circumstances when such exercises do not fall within the purview of ‘reduction of capital’ and procedure of reduction of capital under section 66 is not to be followed.

Answer: Though the terms ‘diminution of share capital’ and ‘reduction of capital look synonymous, but sometimes diminution of share capital does not amount to reduction of capital. In the following cases, the diminution of share capital is not to be treated as reduction of the capital:

(i) Where the company cancels shares which have not been taken or agreed to be taken by any person [Section 61];

(ii) Where redeemable preference shares are redeemed in accordance with the provisions of Section 55;

Financial Restructuring 11.23

(iii) Where the company buys-back its own shares under Section Ilk of the Act.

In the above mentioned situations, the procedure for reduction of capital as laid down in Section 66 of the Companies Act, 2013 is not attracted.

2011, June Professional Programme - 5 Marks DQ 16: Explain the circumstances where reduction of share capital is done without confirmation by the court.

Answer: Reduction of share capital without sanction of the Court: The following are cases which amount to reduction of share capital but where no confirmation by the Court is necessary:

(a) Surrender of shares - “Surrender of shares” means the surrender of shares already issued to the company by the registered holder of shares. Where shares are surrendered to the company, whether by way of settlement of a dispute or for any other reason, it will have the same effect as a transfer in favour of the company and amount to a reduction of capital.

(b) Forfeiture of shares - A company may If authorised by its articles, forfeit shares for non-payment of calls and the same will not require confirmation of the Court, when it is re-issued.

(c) Diminution of capital - Where the company cancels shares which have not been taken or agreed to be taken by any person [Section 61].

(d) Redemption of redeemable preference shares.

(e) Purchase of shares of a member by the company under Section 242.

(f) Buy-back of its own shares under Section 68.

2011, June Professional Programme - 4 Marks DQ 17: A company has passed a special resolution for ‘reduction of capital’ and effected the same and applied before die Registrar of Companies (ROC) for issuance of certificate confirming the reduction.

The ROC issued certificate confirming the reduction. Subsequently, it was found that:

(i) the company had no authority under its articles to reduce capital; and

(ii) the special resolution was invalid one.

State with brief reasons separately in both the above circumstances, whether the reduction of capital would be allowed.

Answer: Conclusiveness of certificate for reduction of capital: Where the Registrar had issued his certificate confirming the reduction, the same was held to be conclusive although it was discovered later that the company had no authority under its articles to reduce capital [Re Walkar & Smith Ltd., (1903) 88 LT 792 (Ch D)]. Similarly, in a case where the special resolution for reduction was an invalid one, but

11.24 Reliance’s Corporate Restructuring, Valuations and Insolvency

the company had gone through with the reduction, the reduction was not allowed to be upset [Ladies’s Dress Assn. v. Pulbrook, (1900) 2 QB 376].

2011, June Professional Programme - 5 Marks DQ 18: It is a well known fact that to maximise the shareholders value, a company having surplus funds often induced to buy-back its own shares. What arc common reasons which usually induces a company to resort to buy-back?

Answer: Good corporate governance calls for maximizing the shareholder value. When a company has surplus, funds for which it does not have good avenues for deployment assuring an average return on capital employed and earnings per share, the company’s financial structure requires balancing.

The reasons for buy-back may be one or more of the following:

(i) to improve earnings per share;

(ii) to improve return on capital, return on net worth and to enhance the long-term shareholder value;

(iii) to provide an additional exit route to shareholders when shares are under valued or are thinly traded;

(iv) to enhance consolidation of stake in the company;

(v) to prevent unwelcome takeover bids;

(vi) to return surplus cash to shareholders;

(vii) to achieve optimum capital structure;

(viii) to support share price during periods of sluggish market conditions;

(ix) to service the equity more efficiently.

The decision to buy-back is also influenced by various other factors relating to the company, such as growth opportunities, capital structure, sourcing of funds, cost of capital and optimum allocation of funds generated.

2011, June Professional Programme - 1 Mark each DQ 19: A company whether listed or not is required to make a ‘declaration of solvency’ and has to submit to the appropriate authorities before making a buy-back of shares. In view of the statement, you are required to answer where the declaration of solvency is to be submitted in case of—

(i) A listed company.

(ii) An unlisted company.

(iii) A private limited company.

Answer:

(i) In the case of buy-back of listed securities, before making a buy-back, the company must file with the Registrar of Companies and SEBI. a declaration of solvency in the prescribed form.

Financial Restructuring 11.25

(ii) In the case of unlisted companies, a declaration of solvency has to be filed with Registrar of Companies before buy-back of shares.

(iii) In the case of private Limited Companies, the Declaration of Solvency is to be filed with Registrar of Companies before buy-back of shares.

2013, December, Professional Programme - 9 marks DQ 20: Explain the provisions of buy-back under the Companies Act, 2013 with reference to Board resolution and shareholders resolution. What is the maximum quantum of buy-back allowed under the Act?

Answer: Board resolution and quantum of buy-back: By passing a resolution, the Board can authorize the buy-back of securities not exceeding 10% of the total paid-up equity capital and free reserves of the company. [Proviso to Section 68 of Companies Act, 2013]. The aforesaid limit is to be applied not to the number of securities to be bought back but to the amount required for buy-back of such securities.

The resolution authorizing buy-back should be passed at a meeting of the Board [Section 179]. Such a resolution should not be passed by circulation or at a meeting of a committee of the Board. However, the methodology, mode of buy-back and other procedural requirements for buy-back may be delegated by the Board.

Shareholders resolution and quantum of buy-back: By passing a special resolution, the shareholders can authorize the buy-back of securities not exceeding 25% of the total paid-up capital and free reserves of the company in that financial year. [Section 68].

Paid-up capital includes both equity and preference share capital.

11.26 Reliance’s Corporate Restructuring, Valuations and Insolvency

P QRACTICAL UESTIONS

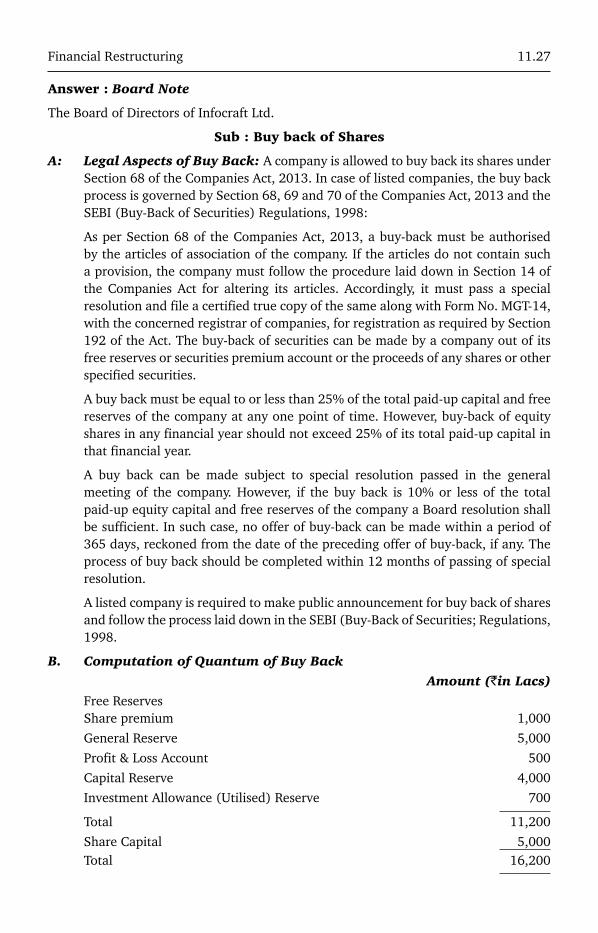

2005, June, CS Final, 10 Marks PQ 1: Infocraft Ltd., a listed company, has the following balance-sheet as at 31st March, 2004:

Source of Funds ` in LakhsShare capital 5,000Reserves and surplus Share premium 1,000 General reserve 5,000 Profit and loss account 500 Capital reserve 4,000 Revaluation reserve . 1,000 Subsidy reserve 1,000 Debenture redemption reserve 2,000 Foreign project reserve 300 Investment allowance reserve 1,000 Investment allowance (utilised) reserve 700 Capital redemption reserve 800 17,300

Total shareholders fund (A) 22,300

14.5% Debentures . 8,00015% Term loans 4,000

Total loan fund (B) 12,000

Total funds (A+B) 34,300

Application of Funds Net fixed block. 22,000Investments 3,000Net current assets 9,000Miscellaneous expenditure 300

Total applications 34,300

The Board of directors of the company proposes to buy-back the company’s shares from its shareholders at a price of ` 50 per share. You are required to prepare a note for consideration of the Board of directors indicating–

(i) the applicable legal provisions; and

(ii) the computation of the quantum of share capital which can be bought back.

Financial Restructuring 11.27

Answer : Board Note

The Board of Directors of Infocraft Ltd.

Sub : Buy back of Shares

A: Legal Aspects of Buy Back: A company is allowed to buy back its shares under Section 68 of the Companies Act, 2013. In case of listed companies, the buy back process is governed by Section 68, 69 and 70 of the Companies Act, 2013 and the SEBI (Buy-Back of Securities) Regulations, 1998:

As per Section 68 of the Companies Act, 2013, a buy-back must be authorised by the articles of association of the company. If the articles do not contain such a provision, the company must follow the procedure laid down in Section 14 of the Companies Act for altering its articles. Accordingly, it must pass a special resolution and file a certified true copy of the same along with Form No. MGT-14, with the concerned registrar of companies, for registration as required by Section 192 of the Act. The buy-back of securities can be made by a company out of its free reserves or securities premium account or the proceeds of any shares or other specified securities.

A buy back must be equal to or less than 25% of the total paid-up capital and free reserves of the company at any one point of time. However, buy-back of equity shares in any financial year should not exceed 25% of its total paid-up capital in that financial year.

A buy back can be made subject to special resolution passed in the general meeting of the company. However, if the buy back is 10% or less of the total paid-up equity capital and free reserves of the company a Board resolution shall be sufficient. In such case, no offer of buy-back can be made within a period of 365 days, reckoned from the date of the preceding offer of buy-back, if any. The process of buy back should be completed within 12 months of passing of special resolution.

A listed company is required to make public announcement for buy back of shares and follow the process laid down in the SEBI (Buy-Back of Securities; Regulations, 1998.

B. Computation of Quantum of Buy Back Amount (`in Lacs)

Free Reserves Share premium 1,000General Reserve 5,000Profit & Loss Account 500Capital Reserve 4,000Investment Allowance (Utilised) Reserve 700

Total 11,200Share Capital 5,000

Total 16,200

11.28 Reliance’s Corporate Restructuring, Valuations and Insolvency

25% of Free Reserve and paid-up capital 4,05025% of Equity Share Capital 1,250

Therefore the buy-back during the year 2004-05 should not exceed ` 4050 lacs. However the buy-back of equity shares(assuming the share capital given, comprises of equity only) should not exceed ` 1250 lacs.

2005, December, CS Final, 8 Marks PQ 2: Amar Ltd. proposed a scheme of arrangement with its shareholders for the purpose of buying-back the small lot of shares held in physical form. The scheme was approved by majority of shareholders.

However, the Registrar of Companies, representing the Central Government, raised an objection that the purpose of the scheme is to buy-back the shares and as such the company ought to have followed the provisions of Section 68.

Discuss in the light of judicial pronouncements (new section of yet notified).

Answer: The objection of Registrar is not tenable as Sections 391 and 68 are independent of each other. The Legislative intention behind the introduction of Section 68 is to provide an alternative method by which a company may buyback its own shares upto a certain percentage.

There is nothing in the provisions of Section 68 to indicate that the jurisdiction of the Court under Section 391 or 394 has been taken away or substituted. Section 68 is an enabling provision and the Court’s power under Sections 66 and 391 (new section not yet notified) are not in any way affected. [TCI Industries Ltd., (2004) 118 Comp. Cas. 373 (AP) N.V. Ramana J.].

In the case of Union of India v. Sterlite Industries (India) Ltd. (2003)-(113)-Comp Cas 0273, (Bom), the Court observed that the non obstante clause in Section 68, namely “Notwithstanding anything contained in this Act means that not withstanding the provisions of Section 67 and Sections 66, the company can buy-back its shares subject to compliance with the conditions mentioned in Section 68 without approaching the Court under Sections 100 to 104 or Section 391 .Therefore, Section 68 is an enabling provision and the Court’s powers under Sections 66 and Sections 391 are not in any way curtailed or affected. The provisions of Section 68 are applicable only to buy-back of securities under Section 68 and the conditions applicable to Sections 66 and Section 391 cannot be imported into or made applicable to buy-back of securities under Section 68. Similarly, the conditions for buy-back of securities under Section 68 cannot be applied to a scheme under Sections 66 and Section 391 (not yet notified), as the two operate in independent fields.

In the case of Himachal Telematics Ltd. v. Himachal Futuristic Communications Ltd. (1996) 86 Comp Cas 325 (Del) a scheme of amalgamation was to be undertaken. However, the transferee company had a subsidiary which was holding shares of the transferor company. An objection was raised that the sanction of the scheme of amalgamation would result in the buying back by the transferee company of shares of its subsidiary and would thereby violate the provisions of Sections 42 and 67 of the

Financial Restructuring 11.29

Act. Dealing with the argument regarding violation of Section 67, it was held that no violation would result as a consequence of sanctioning the scheme of amalgamation as the transferee company was not buying any of its own shares.

In Gurmit Singh v. Polymer Papers Ltd. (2003) 45 SCL 251. (CLB - N. Delhi), petitions were filed under Sections 397 and 398 (new sections not yet notified). The issue considered in this case was whether the power of CLB is subject to compliance with the provisions of Section 68 in view of its non obstante clause. It was observed that the object of Section 68 is to put some checks and balances when a company, on its own, desires to buy-back its own shares and as such Section 68 has no application in a case where the CLB exercises its powers under Section 242. The contention that no court can bypass the provisions of Section 68 would only mean that the provisions of those Sections empowering the Court to pass an order on a company to purchase its own shares would be nugatory. When the Legislature had intended that the CLB should have the power to order purchase of its own shares by a company with the purpose of putting an end to the matters complained of, it would never have intended that such a power was subject to the provisions of other Sections. Thus, the powers of the CLB to pass an order directing a company to purchase its own shares in terms of Section 242 are not curtailed by the provisions of Section 68. Moreover, Section 242 empowers the CLB to direct purchase of shares of a member not only by the company but even by other members.

It was also held that even assuming that Section 68 is a bar to give a direction to a company to purchase its shares, directions can be given to other members to purchase the shares of any member as long as the direction is with a view to put an end to the matters against which complaints were raised. The ultimate aim in such a direction is to safeguard the interest of the company and its members.

2006, June, CS Final, 8 Marks PQ 3: Gem Ltd., a listed company of which you are the Company Secretary, is planning to buy-back its shares through book building process.

You are required to prepare an activity chart for carrying out the whole process with time to be involved in the process.

Answer: Activity Chart of Gem Ltd. for buy back of shares through Book Building process with minimum time involved in the process:

ActivityCompletion

dates

Intimate the Stock Exchanges where the company’s securities are listed regarding Board Meeting at which the matter of Buyback of securities through Book Building process is to be considered by the Board.

Prepare a schedule of all activities relating to the buy-back through Book Building.

Hold Board meeting to consider the matter of buy-back through Book Building and appointment of Merchant Banker.

7 days before the date of Board meeting

11.30 Reliance’s Corporate Restructuring, Valuations and Insolvency

ActivityCompletion

dates

Approve the notice of general meeting along with explanatory statement for passing special resolution with the approval of members.

The explanatory statement shall consist of the following additional disclosures since the buy-back is made through Book Building:

(i) the maximum price at which the buy-back of securities shall be made;

(ii) whether the Board is being authorized at the general meeting to determine subsequently the specific prices at which the buy-back may be made at the appropriate time;

(iii) in case the promoters intend to offer their securities, the following additional disclosures shall also be made

(a) the quantum of securities proposed to be tendered by pro-moters; and

(b) the details of their transactions and their holdings for the last 6 months prior to the passing of the special resolution for buy-back including information of number of securities acquired, the price and the date of acquisition.

Hold general meeting and take approval of members by way of special resolution giving consent to buy-back through Book Building. The resolution passed for buy- back through book building should specify the maximum price at which the buy-back should be made.

Day 0

File special resolution with Form MGT-14 with Registrar of companies, SEBI and Stock Exchanges where shares of a company are listed.

Day 0 (For filing at RoC, 30 days time is available).

Hold Board meeting to approve the public announcement. Day 1

Open escrow, account and deposit the amount as specified in Regulation 10 of SEBI (Buyback of Securities) Regulations 1998. The amount should be deposited before the public, announcement and the amount should be in relation to the maximum price specified in the announcement.

Day 2

Make a public announcement in at least one English National Daily, one Hindi National Daily and a Regional language daily all with wide circulation at the place where the Registered office of the company is situated and shall contain all the material information as specified in Schedule II at least 7 days prior to opening.

Besides the disclosures mentioned in tender offer, the public announcement should also contain disclosures relating to the detailed methodology of the book building process, the manner of acceptance to be sent by the security holders pursuant to the public announcement and the details of bidding centers.

Day 3

Financial Restructuring 11.31

ActivityCompletion

dates

The book building process should be conducted through an electronically linked transparent facility and all bidding centers, the number of which should not be less than 30, should have atleast one electronically linked computer terminal.

File public announcement with SEBI along with fees. Day 4

File solvency declaration with SEBI & Registrar of Companies. Day 4

Offer opens Day 9

Offers closes (remain open for atleast 15 days and not exceeding 30 days)

Day 24

Open special bank account Day 25

Transfer money out of escrow account to special bank account Day 25

Verify securities and finalize list of applicants Day 39

Remit consideration Day 46

Extinguish/Destroy Share Certificates Day 46

Advertisement in national daily newspaper within 2 days of completion of extinguishment/destruction of share certificate.

Day 48

Reporting to SEBI and Stock Exchanges Day 51

File return with Registrar of Companies Day 76

2007, December, CS Final, 4+3+3 = 10 Marks PQ 4: In October, 2006, OCL, a listed company, made a rights issue of 18 lakh zero coupon convertible debentures (ZCCD) to the shareholders of the company. As per the terms of offer, each ZCCD was automatically and compulsorily converted into one equity share of ` 10 on 1st January, 2007. Further, each ZCCD had one detachable warrant attached thereto which entitles the holder thereof to apply for and seek allotment of one equity share of the company. The company now proposed that an offer be made to the warrantholders for buy-back of the entire 18,00,000 warrants. In light of above case, answer the following questions confined to Section 68 and the SEBI (Buy-back of Securities) Regulations, 1998:

(i) Whether the provisions of Section 68 will be applicable to buy-back of warrants

(ii) Whether the provisions of the SEBI (Buy-back of Securities) Regulations, 1998 will be applicable to the proposed buy-back of warrants?

(iii) Are partly paid-up securities eligible for buy-back?

Answer:

(i) Section 68 of the Act applies to buy-back of company’s own shares or “other specified securities”. Section 68 does not define “securities” nor is it defined

11.32 Reliance’s Corporate Restructuring, Valuations and Insolvency

elsewhere in the Act. However, under Section 68, a company is allowed to buy its securities (other than shares) only if they are “specified securities”. Explanation (a) at the end of the Section provides that “specified securities” includes Employees Stock Option or other securities as may be notified by Central Government from time to time. Since no securities have been notified by the Central Government so far, buy-backs of warrants are not covered by Section 68.

(ii) In the case of listed companies, a buyback of the shares or other specified securities listed on any recognised stock exchange shall be in accordance with the SEBI (Buy Back of Securities) Regulations, 1998.The Regulations will not apply to buy back of the warrants. In this case, since Section 68 itself is not applicable as clarified above. It may be noted that the regulations, which are made under Section 68 of the Companies Act do not apply to transactions not covered under Section 68.

(iii) According to Section 68 of the Companies Act, 2013, all the shares or other specified securities to be bought-back must be fully-paid at the time of buyback. If any of the securities which are proposed to be bought back are partly paid, steps must be taken to make them fully paid before a buyback of such securities.

2009, December Professional Programme – 4 marks PQ 5: A company whose shares were listed on a stock exchange for 3 months as on the relevant date made preferential allotment at ` 100 per share. On completing the period of 6 months of being listed on the stock exchange, the company recomputed the share price based on the guidelines issued by SEBI in this respect and price of share so recomputed came to ` 150 per share. The company demanded additional amount of ` 50 per share from the allottees of shares. Is the action of the company justified ? Give reasons.

Answer: The action of the company is justified. Chapter XIII Of SEBI (Issue of Capital & Disclosure Requirements) Regulations, 2009 clearly provided the rules regarding the price at which shares be Issued on a preferential basis.

The action of the company is in tune with those regulations and hence correct as Chapter XIII, specially provides that where the equity shares are listed for less than six months, on completing a period of six months of being listed on a stock exchange, the company shall recompute the price of the shares in accordance with the provisions mentioned above and if the price at which shares were allotted on a preferential basis under clause was lower than the price so recomputed, the difference shall be paid by the allottees to the company.

2009, December Professional Programme – 4 marks PQ 6: The capital structure of Joharitd. is as follows :

— 5 lakh equity shares of ` 10 each fully paid-up.

— 10 lakh equity shares of ` 10 each on which `5 is paid-up.

— Free reserves of ` 3 crore.

Financial Restructuring 11.33

The Board of directors of the company has passed a resolution authorising the buy-back of shares worth `40 lakh for the financial year 2009-10. Is the Board of directors empowered to do so ? Give reasons.

Answer: Board by passing a resolution can authorize the buy-back of securities not exceeding 10% of the total paid-up equity capital and free reserves of the company [Proviso to section 68].

But the buy-back of equity shares in any financial year should not exceed 25% of the total paid-up equity capital of the company [Proviso to section 68].

In this case

10% of paid-up equity share capital and (fee reserves = `40,00,000 i.e-10% of (50 lac + 50 lac + 300 lac).

25% of paid-up equity capital + `25,00,000 i.e. 25% of (`50,00,000 + `50,00,000),

So the Board is not empowered to buy-back shares worth `40,00,000.

2010, June Professional Programme – 2 marks each PQ 7: The position of capital and reserves as on 31st March. 2009 of Matrix Ltd. are given below:

` Equity shares (Fully paid-up of face value ` 10 each) 1,00,00,000Equity shares (` 5 is paid-up on face value of ` 10 each) 1,00,00,000Equity shares with differential voting rights (Fully paid-up of face value of ` 10 each) 1,00,00,000Preference shares (Fully paid-up of`100 each) 1,00,00,000Free reserves 7,50,00,000

The managing director of Matrix Ltd. wanted to place proposal before the Board for buy-back of its 100% preference share capital. You as a Company Secretary, advise your managing director on the following issues:

(i) Maximum limit upto which Board can approve buy-back of shares,

(ii) Maximum limit upto which shareholders can approve buy-back of shares.

(iii) Maximum limit upto which company can buy-back its own shares.

(iv) The situation in which further offer of buy-back can be given by the company within a period of 365 days.

Answer:

(i) According to the proviso to Section 68 of the Companies Act, 2013, the Board can authorize buy back of securities not exceeding 10% of total paid up equity capital and free reserves of the Company. The above limit states the quantum of fund required to be bought back with the approval of the Board.

The total paid up equity capital of the company excluding the preference shares is `3,00,00,000

11.34 Reliance’s Corporate Restructuring, Valuations and Insolvency

The maximum amount upto which board can approve buy back is 10% of total paid up equity capital and free reserve which is 10% of (`3,00,00,000 + `7.50,00,000) = ` 1,05,00,000.

(ii) According to Section 68 of the Companies Act, 2013, shareholders by passing Special resolution can approve buy back upto 25% of paid up capital and free reserves. The paid up capital shall include preference capital, if any.

In the given question, shareholders can approve 25% of the paid up capital and free reserves i.e. 25% of `11.50,00,000/- (` 3,00,00,000 + ` 1.00,00.000+ `7,50.00,000} = ` 2,87,50,000.

(iii) A company can buy back upto 25% of the total paid up capital and free reserves (Section 68), Further, buy back of equity shares in any financial year should not exceed 25% of the total paid up equity capital of the Company. However, company is free to buy back its entire preference capital during the financial year subject to overall limit of 25% of the total paid up capital and free reserves

Hence, in the given question maximum buy back of equity shares should be limited to 25% of the total paid up equity capital of ` 3, 00, 00,000 which is ` 75,00,000.

(iv) Once the buyback has been made with the authorization of the Board and not that of the shareholders , no further, offer for buy back of any securities can be made without the consent of shareholders accorded by Special Resolution with in 365 days reckoned from the date of the offer [Section 68 - second proviso).

However, shareholders can make further offer of buy back within a period of 365 days provided the aggregate of authorization does not exceed the limit prescribed in 68.

2010, December Professional Programme - 4 Marks PQ 8: By analysing a balance sheet of Aadarsh Ltd., it was found that there are plethora of reserves in the balance sheet for the year ended 31st March, 2009, and the reserves are summarised below:

(i) Investment fluctuation reserve

(ii) Statutory reserve

(iii) Securities premium account

(iv) General reserve

(v) Foreign currency fluctuation reserve

(vi) Dividend equalisation reserve

(vii) Dividend redemption reserve (preference shares)

(viii) Capital, redemption reserve.

Now, the Chairman of Aadarsh Ltd. asks you as a Company Secretary to know which of the above reserves can be utilised for the proposed buy-back of shares of the company. Advise.

Financial Restructuring 11.35

Answer: Aadarsh Ltd., can utilize the following reserves for the proposed buy-back of shares:

(i) Investment fluctuation reserve

(ii) Securities premium account

(iii) General reserve

(iv) Foreign currency fluctuation reserve (provided it is not in the nature of provision)

(v) Dividend equalization reserve.

2011, June Professional Programme - 3 Marks PQ 9: A listed company had drafted a special resolution to be passed through postal ballot to buy-back 25% of its paid-up equity share capital. As a Company Secretary, you are required to draft the explanatory statement to the proposed resolution. What factors will you consider to prepare the explanatory statement?

Answer: Whereas unlisted companies should obtain shareholders’ approval by passing the special resolution only at a duly convened general meeting, listed companies should obtain such approval by postal ballot.

The notice containing the special resolution proposed to be passed should be accompanied by an explanatory statement stating:

(a) all material facts, fully and completely disclosed;

(b) the necessity for buy-back;

(c) the class of security intended to be purchased under the buy-back;

(d) the amount to be invested under buy-back; and

(e) the time limit for completion of buy-back [Section 68].

2012, June Professional Programme - 15 Marks PQ 10: BM (India) Ltd. (BMIL) is a company registered in India. 99% of shareholding of BMIL is controlled by three companies namely, Van India Ltd, (VAN) (45%), Man India Ltd. (MAN) (45%) and Ran India Ltd. (RAN) (9%) which are the promoters of BMIL. The remaining 1 % shareholding is in the control of 10 individual shareholders.

BMIL has filed a petition before the court for reduction of its share capital under sections 100 to 105 and stated that “only the shares of minority shareholding which at present is 1% of the total paid capital will be extinguished and reduced.” The articles of association of BMIL contain provisions for the reduction of capital. 99.99% shareholders have approved the special resolution except one shareholder Gaurav who has 0.01% of shares of the company. Gaurav has raised objection on the proposed scheme of reduction of capital on the following grounds:

— Proposed reduction of share capital by BMIL amounts to ‘forcible acquisition’ of shares of public shareholders as only their shares are

11.36 Reliance’s Corporate Restructuring, Valuations and Insolvency

being extinguished, whereas the shares of promoter group, i.e., VAN, MAN and RAN remain unaffected. According to Gaurav, the actual intent and reason for reduction of share capital is only to eliminate the minority shareholders as members of the company and is thus wholly unfair, discriminatory and malafide. Gaurav submits that reduction, if any, should be spread equally over all the different classes of shareholders of BMIL.

— Gaurav submits that the reduction of share capital proposed by BMIL is in fact a buy-back of the shares under section 68 and accordingly reduction of share capital has - to be done on proportionate basis as mentioned in section 68.

Keeping in view the provisions of section 68, sections 100 to 105 and also the objections of Gaurav, you, being the Company Secretary and Legal Advisor of BMIL, are asked to give your opinion on the following:

(i) Reduction of capital under section 66 gives liberty to the company to reduce its capital in ‘any manner’ other than what is illustrated in clause (a), (b) and (c) of section 66.

(ii) Section 68 should not be applicable in case where petition for reduction of capital is moved to the court pursuant to sections 100 to 66.

Cite relevant case law in support of your answer.

Answer: Section 66 of the Companies Act, 2013 expressly permits a company, if so authorised by its Article of Association, to reduce its share capital provided it has passed a Special Resolution for that purpose and the said resolution has been sanctioned by the Court. Clauses (a) (b) and (c) of Section 66 are mere illustrations and are not the only manner in which share capital of a company can be reduced. In fact, the power of reduction of capital is general and extend to any possible method of reduction subject to compliance of the applicable provisions. In Bhimbhai v. Ishwar Das (1984) ILR 18 Bom 152, the court has held that any arrangement concerning the company’s capital which has the effect of reducing it is within the purview of this Section.

Hence the given statement is correct that reduction of capital can be done in any manner other than what is illustrated in clause (a) (b) and (c) of Section 66 of the Companies Act, 2013.

Section 68 of the Companies Act, 2013 is a facilitating provision which enables a company to buy back its shares without approaching to the Court under Section 66 of the Act. In fact, the provisions of Section 68 and 66 of the Act operate in different field. The Bombay High Court in the Sterlite Industries (India) Limited (2003) 113 Com cas 273/45 SCL 475 (Bom) has held that “Section 77A is merely an enabling provision and Court’s power under Section 66 are not in any way affected. The conditions provided in Section 68 are applicable only to buy back of shares under Section 68. The conditions applicable to Section 66 cannot be imported into or made applicable to a buy back under Section 68. Similarly, the conditions for buy back under Section 68 cannot be applied to a Scheme under Section 66. The two operates in independent filed.

Financial Restructuring 11.37