Embed Size (px)

Citation preview

Chapter 6The Stock Market

•Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Take stock in yourself. Make sure you have a good understanding of:

1. The difference between private and public equity and primary and secondary stock markets.

2. The workings of the New York Stock Exchange.

3. The workings of the Toronto Stock Exchange.

4. How NASDAQ operates.

5. How to calculate index returns.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Our goal in this chapter is to provide a “big picture” overview of:

Who owns stocks,How a stock exchange works, andHow to read and understand the stock market

information reported in the financial press.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

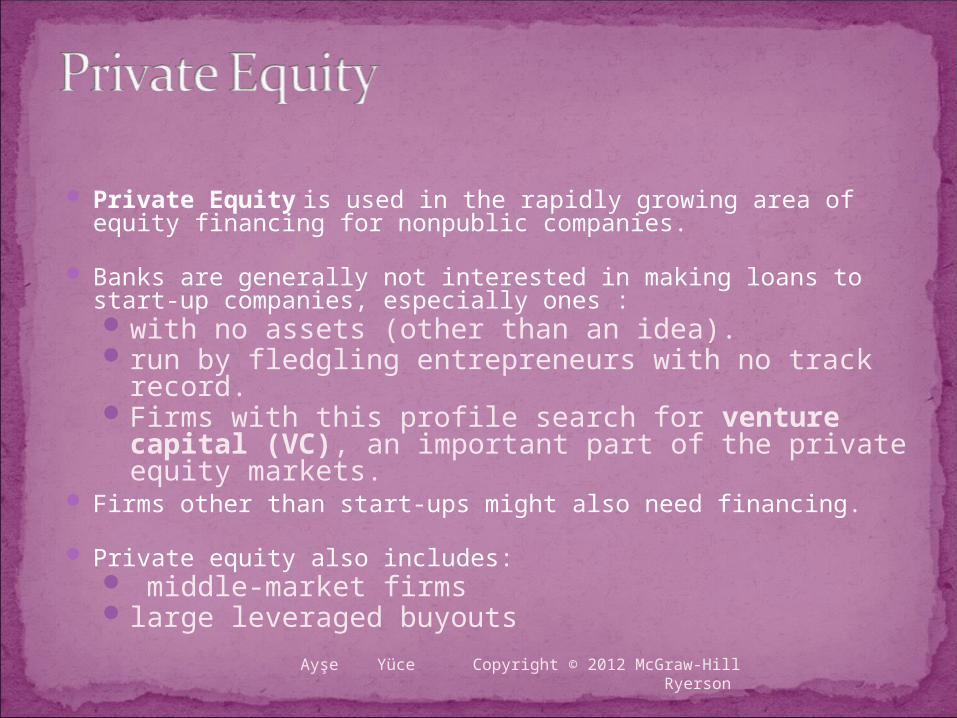

Private Equity is used in the rapidly growing area of equity financing for nonpublic companies.

Banks are generally not interested in making loans to start-up companies, especially ones :with no assets (other than an idea).run by fledgling entrepreneurs with no track record.Firms with this profile search for venture capital

(VC), an important part of the private equity markets.

Firms other than start-ups might also need financing.

Private equity also includes: middle-market firms large leveraged buyouts

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Private equity funds and hedge funds are two types of investment companies. Both are set up as limited partnerships. pool money from investors. invest this money on behalf of these investors.use, typically, a 2/20 fee structure (i.e., a 2 percent

annual management fee and 20 percent of profits).have built-in constraints to prevent managers from

taking excessive compensation.

Private equity funds generally have:a high-water-mark provisiona “clawback” provision

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Venture Capital refers to financing new, often high-risk, start-ups.

Individual venture capitalists invest their own money.

Venture capital firms pool funds from various sources, likeIndividualsPension fundsInsurance companiesLarge corporationsUniversity endowments

Venture capitalists know that many new companies will fail.

The companies that succeed can provide enormous profits.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

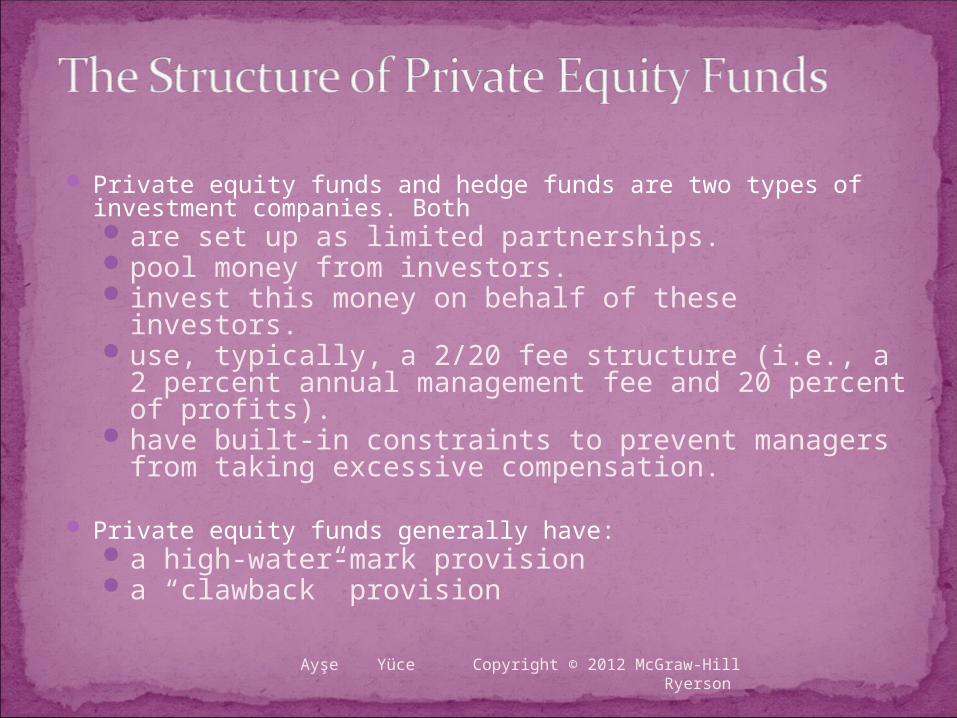

To limit their risk:Venture capitalists generally provide financing in

stages.Venture capitalists actively help run the company.

At each stage, enough money is invested to reach the next stage. Ground-floor financing Mezzanine Level financing

At each stage of financing, the value of the founder’s stake grows and the probability of success rises.

If goals are not met, the venture capitalists withhold further financing.

If a start-up succeeds: The big payoff frequently comes when the company is sold to

another company or goes public. Either way, investment bankers are often involved in the

process.Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Many small, regional private equity funds concentrate their investments in “middle market” companies. ongoing concerns (i.e., not start-ups) known performance historytypically, small and family owned and operated.

Reasons middle market companies seek more capitalExpansion beyond their existing regionFounder wants to “cash out”

A private equity fund might purchase a portion of the business so that others can now manage the company.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Suppose a company (or someone else) purchases all the shares of the company held by the public at large?

This process is called “taking the company private.”

The cost of going private is often high. A manager or investor who wants to take a company

private probably needs to borrow a significant amount of money.

Taking a company private is called a leveraged buyout (LBO).

LBO market activity levels depend on credit markets. Around 2005, the LBO market was quite active. Activity in the LBO market came to a standstill after the

crash of 2008.Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The primary market is the market where investors purchase newly issued securities. Initial public offering (IPO): An IPO occurs when a company

offers stock for sale to the public for the first time. Seasoned equity offering (SEO): If a company already has

public shares, an SEO occurs when a company raises more equity.

The secondary market is the market where investors trade previously issued securities. An investor can trade: Directly with other investors. Indirectly through a broker who arranges transactions for others. Directly with a dealer who buys and sells securities from

inventory.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

An IPO (and an SEO) involves several steps.

Company appoints an investment banking firm to arrange financing.

Investment banker designs the stock issue and arranges for fixed commitment or best effort underwriting.

Company prepares a prospectus (usually with outside help) and submits it to the Securities and Exchange Commission (SEC) for approval. Investment banker circulates preliminary prospectus (red herring).

Upon obtaining SEC approval, company finalizes prospectus.

Underwriters place announcements (tombstones) in newspapers and begin selling shares.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The goal of a secondary market is to match investors wishing to buy stocks with investors wishing to sell stocks.

Common stock trading typically occurs on either an organized stock exchange or a trading network.

Important concepts: The bid price:

The price dealers pay investors. The price investors receive from dealers.

The ask price: The price dealers receive from investors. The price investors pay dealers.

The difference between the bid and ask prices is called the

bid-ask spread, or simply the spread.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The New York Stock Exchange (NYSE), popularly known as the Big Board, celebrated its bicentennial in 1992.

The NYSE has occupied its current building on Wall Street since the early 1900’s.

For 200 years, the NYSE was a not-for-profit New York State corporation.

The NYSE went public in 2006 NYSE Group, Inc., ticker: NYXNaturally, NYX stock is listed on the NYSE

In 2007, NYSE Group merged with Euronext to form NYSE Euronext, the world’s largest exchange.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Historically, the NYSE had 1,366 exchange members. These members: Were said to own “seats” on the exchange. Collectively owned the exchange, although professionals

managed the exchange. Regularly bought and sold seats (Record seat price: $3

million in 2005) Seat holders could buy and sell securities on the exchange

floor without paying commissions.

In 2006, all of this changed when the NYSE went public. Instead of purchasing seats, exchange members purchase

trading licenses: number limited to 1,500 In 2010, a license would set you back a cool $40,000—per year.

Having a license entitles the holder to buy and sell securities on the floor of the exchange.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

For a long time, most securities listed at the NYSE were divided among specialists—an exclusive dealer, or intermediary, for a set of securities.

Specialists: posted bid prices and ask prices for each security assigned to

them. were obligated to make and maintain a fair, orderly market Specialists stood ready to buy at bid prices and sell at ask prices

when outside sell and buy order flows were unequal

Specialists had an exclusive, advance look at incoming orders flowing to the display book. Because of this advance look, specialists had an information

advantage when they were making quotes and matching orders. Under this system, specialists, however, could “work” orders, that

is, try to improve trading prices for customers.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

In 2009, aiming to stay competitive, the NYSE replaced the role of specialists with two classes of market makers: designated market makers (DMMs) and supplemental liquidity providers (SLPs).

What were specialists are now the DMMs. The DMMs are assigned a set of securities and are obligated to maintain a fair and orderly market in these stocks

Differences between the Specialist Role and the DMM Role DDMs can compete against other exchange members for trades. Specialists had to step back from a trade if a floor broker order

had the same price. Unlike the former specialist system, however, DMMs do not

receive an advance look at incoming orders.

DMMs do not have an exclusive right to make markets in their assigned securities.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The largest number of NYSE members are registered as commission brokers.

Commission brokers execute customer orders to buy and sell stocks.

When commission brokers are too busy, they may delegate some orders to floor brokers, or two-dollar brokers, for execution.

A small number of NYSE members are floor traders, who independently trade for their own accounts.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

In 2008, the total number of companies listed on the NYSE represented a total global market value of about $16.7 trillion.

Initial and annual listing fees are charged based on the number of shares.

To apply for listing, companies have to meet certain minimum requirements with respect to:The number of shareholdersTrading activityThe number and value of shares held in public

handsAnnual earnings

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The Toronto Stock Exchange (TSX), unlike the NYSE, is a computerized exchange.

In 2002, the Toronto Stock Exchange celebrated its 150th birthday having started its operations in 1861 with 18 securities and 14 member firms.

In 1861, approximately twenty-five businessmen decided to form a stock exchange in Toronto in their meeting at Toronto’s Masonic Temple. At that time, members paid $250 to purchase a seat.

In 1901, the price of membership had risen to $12,000 and trading volume became approximately 1 million shares per year.

The Toronto Stock Exchange experienced solid growth and became the third largest North American exchange in the 1940s.

By 1955 a membership seat cost $100,000 and trading volume reached 1 billion shares.

In 1977, the Toronto Stock Exchange introduced the world’s first Computer Assisted Trading System (CATS) and closed its trading floor to become the largest electronic North American Exchange.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The Toronto Stock Exchange, with Canadian exchange restructuring in 1999, became the major stock exchange for trading senior equities.

Canadian derivatives trading were transferred to the Montreal Exchange.

The Vancouver and Alberta Exchanges merged to become the Canadian Venture Exchange (CDNX).

Later the TSX purchased the CDNX and called it the TSX Venture Exchange.

In 2008, the shareholders of the TSX group decided to change the name of the company from TSX Group to TMX Group. According to market capitalization, the TSX group is the third largest exchange in North America and the seventh largest exchange in the world.

As of 2009, there are 3,640 listed issuers in TSX and TSXV(Toronto Venture Exchange), and the TMX group is second in the world for number of listed issuers. There are 281 international issuers and 302new listings.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Currently the TMX Group is the leader exchange in oil and gas sector.

The TMX group is the global leader in mining industry as well. The highest number of mining companies are listed at the TSX and TSXV. The total number of the listed companies is 1531. In 2010, the trading volume related to mining industry exceeded 91 billion Canadian Dollar.

In February 2011, the TMX announced that they are evaluating a merger with the London Stock Exchange. If the merger would have been approved by the authorities the new exchange would have become the third largest exchange in the world. However, later in the year the group rejected the offer and began negotiating an offer by the Maple Group( a group of Canadian banks and the firms.

Today the TSX has over 100 participating organizations and member

firms. These organizations help companies in underwriting their new issues, in listing and in providing corporate financial services. Different customer orders (market, limit or stop orders) are entered into the system by these organizations.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The name “NASDAQ” is derived from the acronym NASDAQ, which stands for National Association of Securities Dealers Automated Quotations system.

NASDAQ is now a proper name in its own right.

Introduced in 1971, the NASDAQ market is a computer network of securities dealers who disseminate timely security price quotes to NASDAQ subscribers.

The NASDAQ has more companies listed than the NYSE.

On most days, volume on the NASDAQ exceeds the NYSE volume.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The third market is an off-exchange market for securities listed on an organized exchange.

The fourth market is for exchange-listed securities in which investors trade directly with one another, usually through a computer network.

For dually listed stocks, regional exchanges also attract substantial trading volume.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

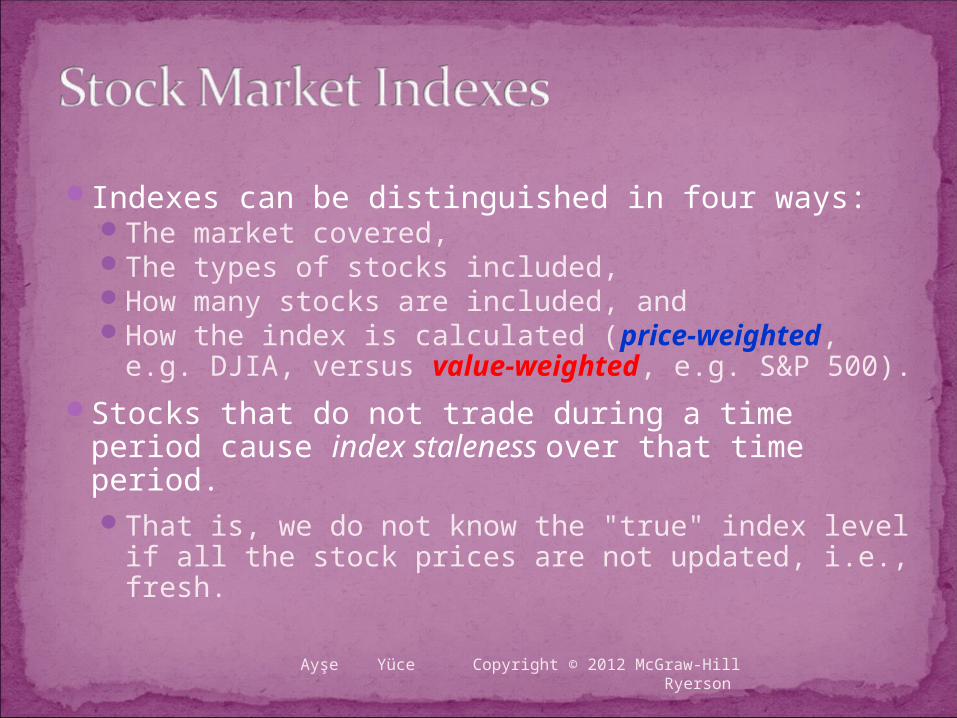

There are essentially four differences between the stock indexes them: (1) the market covered; (2) the types of stocks included; (3) how many stocks are included; and (4) how the index is calculated.

The first three differences are straightforward. Some indexes such as the S&P/TSX Energy Index, focus on specific industries.

Others, such as the S&P/TSX Composite , focus on particular markets. Some have a small number of stocks, like the S&P/TSX 60 which contains only 60 stocks. Some indexes contain small companies, like the S&P/TSX Cdn Small Cap.

How stock market indexes are computed is not quite so straightforward, but it is important to understand. There are two major types of stock market index: price-weighted and value-weighted.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

The most widely followed barometer of day-to-day stock market activity is the Dow Jones Industrial Average (DJIA), or “Dow” for short.

The DJIA is an index of the stock prices of 30 large companies representative of American industry.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Indexes can be distinguished in four ways:The market covered,The types of stocks included,How many stocks are included, andHow the index is calculated (price-weighted,

e.g. DJIA, versus value-weighted, e.g. S&P 500).

Stocks that do not trade during a time period cause index staleness over that time period.That is, we do not know the "true" index level if

all the stock prices are not updated, i.e., fresh.

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

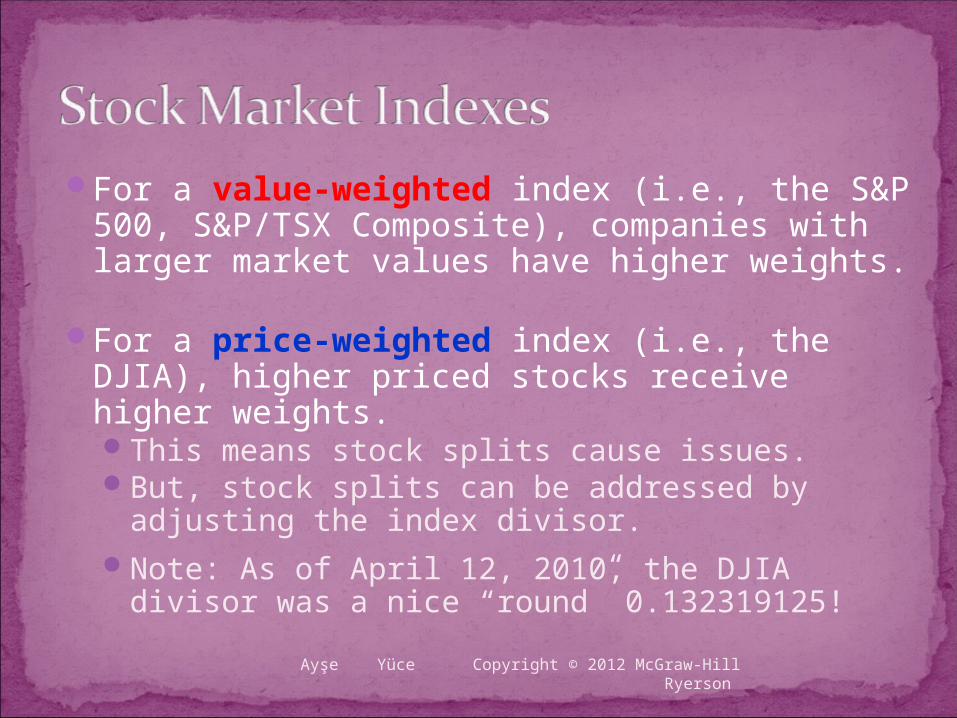

For a value-weighted index (i.e., the S&P 500, S&P/TSX Composite), companies with larger market values have higher weights.

For a price-weighted index (i.e., the DJIA), higher priced stocks receive higher weights.This means stock splits cause issues.But, stock splits can be addressed by adjusting

the index divisor. Note: As of April 12, 2010, the DJIA divisor was

a nice “round” 0.132319125!

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Price Shares

Company Price Weight to Buy

Boeing 67.50 0.5148 7,626

Nordstrom 41.93 0.3198 7,626

Lowe's 21.70 0.1655 7,626

131.130 1.000 7,626

Note: Shares = $1,000,000 / 131.130 = 7,626

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Day 1 of Index: Company Price

Boeing 67.50Nordstrom 41.93Lowe's 21.70Sum: 131.13

Index: 43.71 (Divisor = 3)

Before Day 2 starts, you want to replace Lowe's with Home Depot, selling at $32.90.

To keep the value of the Index the same, i.e., 43.71:

Boeing 67.50Nordstrom 41.93Home Depot 32.90Sum: 142.33

142.33 / Divisor = 43.71, if Divisor is: 3.256234271

What would have happened to the divisor if Home Depot shares were selling at $65.72 per share instead

of $32.90?Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Shares Capitalization Value SharesCompany Price (millions) (millions) Weight to Buy

Boeing 67.50 732.74 49,460.0 0.5550 8,223

Nordstrom 41.93 219.65 9,210.0 0.1034 2,465

Lowe's 21.70 1,402.76 30,440.0 0.3416 15,742

Total: 131.130 Total: 89,110.0 1.0000 26,430

Note: Shares to Buy = $1,000,000*Weight / Price

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Lowe's 21.70 1402.76 30,440

Total MV(1): 89,110

Divisor (Set by Vendor): 89.11

Day 1 Index Level: 1,000.00

Total Shares Market CapitalizationDay 2: Company Price (millions) (millions)

Boeing 69.00 732.74 50,559Nordstrom 41.93 219.65 9,210Lowe's 21.70 1402.76 30,440

Total MV(2): 90,209

Day 2 Index Level: 1,012.33

Using the Portfolio from Example III:

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Total Shares Market Capitalization

Day 3: Company Price (millions) (millions)

Boeing 71.10 732.740 52,098Nordstrom 41.93 219.650 9,210Lowe's 21.70 1,402.760 30,440

Total MV(3): 91,748

Total MV(2): 90,209

Day 2 Index Level: 1,012.33

Day 3 Index Level: 1,029.60

Total MV(1): 89,110

Day 3 Index Level: 1,029.60

1Day LevelIndex 1Day ValueMarket

3Day ValueMarketIndex 3Day

or

2Day LevelIndex 2Day ValueMarket

3Day ValueMarketIndex 3Day

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

www.hoovers.com (information on Initial Public Offerings, or IPOs)

www.nyse.com (website for the New York Stock Exchange) www.tmx.com (website for the Toronto Stock Exchange) www.nasdaq.com (website for the NASDAQ) averages.dowjones.com (The Dow Jones Industrial Average) www.russell.com (the Russell Indexes) www.barra.com (reference for “value” and “growth” indexes) www.djindexes.com (reference for current divisor for the

DIJA) www.standardandpoors.com (website for S&P 500) www.nni.nikkei.co.jp (website for Japan’s Nikkei 225 index)

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Private and Public EquityPrivate Equity Funds

The Primary and Secondary Stock MarketsThe Primary Market for Common StockThe Secondary Market for Common StockDealers and Brokers

The New York Stock ExchangeNYSE-Listed Stocks

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson

Toronto and Toronto Venture Exchange

NYSE and NASDAQ CompetitorsStock Market Information

Stock Market IndexesMore on Price-Weighted IndexesValue-Weighted Indexes

Ayşe Yüce Copyright © 2012 McGraw-Hill Ryerson