Embed Size (px)

Citation preview

CHAPTER 6CHAPTER 6

THE SALES/COLLECTION BUSINESS PROCESS

The sales collection process is a series of operating events that collectively serve to attract customers, help customers select goods and services., deliver the goods and services requested and collect payments for the goods and services.

If the sales/collection process does not function well, it is unlikely the organization will the generate sufficient revenue to sustain itself. Generating revenue is the key to achieving growth and profitability

Planned production this planning impacts financial resources the organizations must secure and manage through the financing process.

In not-for-profit instructions, the revenue/collection and acquisition/payment processes are highly integrated because of the use of fixed budgets.

• The Following explanation of the flowchart is organized by operating events :– Take Order – Approve Credit – Fill Order – Ship Product – Bill Customer– Receive Payment – Information Processes

• An Overview of The Traditional Automated Sales/ Collection Process– Information technology has been applied to the

traditional sales/collection process. – Typical IT applications automated the business and

information process rules f the manual system

From Customer or salesperson

Customer’s order

Performedby sales

order clerk

Customer’s order

Edit order, perform

credit check, and check inventory

Open sales

order file file

Picking slipAcknowledge

To warehouse To customer Orders

1Sales order

Enter order via terminal

Print order document

Error and exception

display

Customer master

file

Merchandise inventory master file

Orders

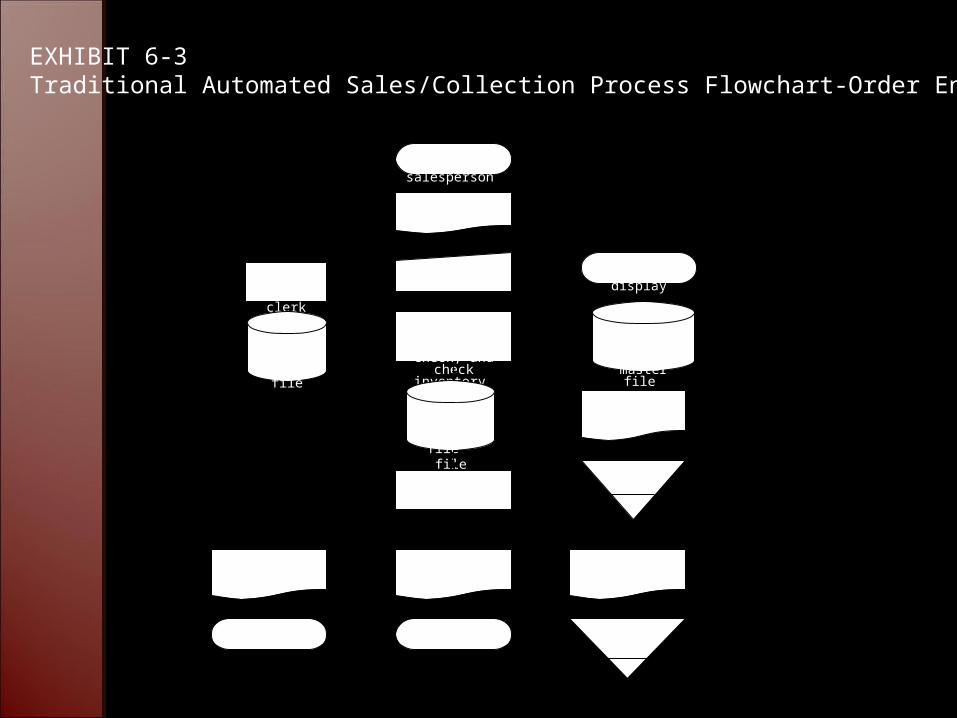

EXHIBIT 6-3Traditional Automated Sales/Collection Process Flowchart-Order Entry

To refer to these flowcharts as you read the following narrative◦Order Entry ◦Warehousing/Shipping◦Billing ◦Remittance ◦Account Receivable

Receive Customer Payments ◦The information risk of lapping. Lapping occurs

when a employee steals cash from a customer payment and delays posting a payment to the customer’s account.

◦Other information risk associated with receiving cash include failing to record a customer payment, accepting duplicate payments for the same invoice, crediting a payment to the wrong customers account and depositing a payment in the wrong cash account.

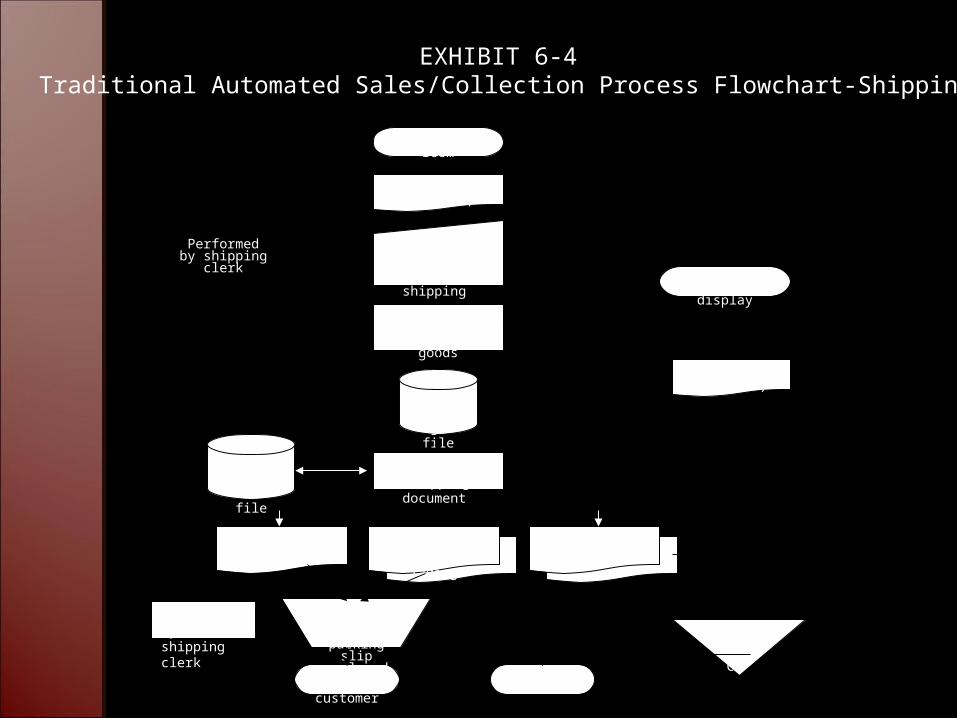

EXHIBIT 6-4 Traditional Automated Sales/Collection Process Flowchart-Shipping

From mail room

Picking list (amended)

Performedby shipping

clerk

Packing list(amended)

Edit dataconcerning picked

goods

Shipping file

Packing slip 21Bill of lading

To carrier and customer

To billing

Shipping

File

2 1

shipping notice

Enter data concerning

goods delivered to shipping

Print shipping document

Pack goods with

packing slip

enclosed and ship

Performed by shipping clerk

Error and exception display

Shipping Reference

file

C

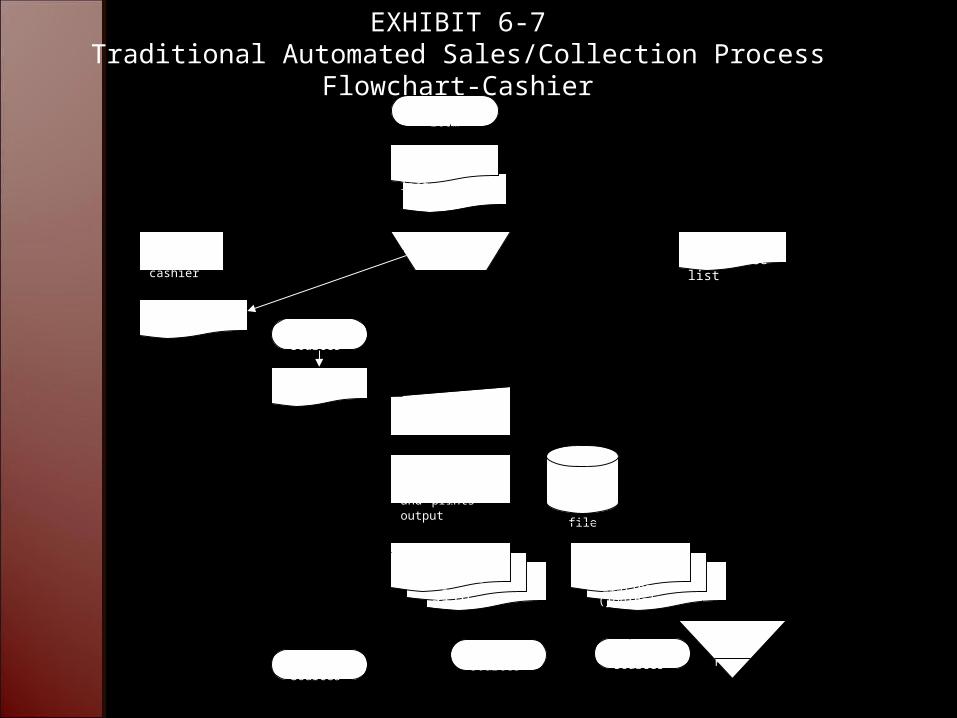

EXHIBIT 6-7Traditional Automated Sales/Collection Process Flowchart-

CashierFrom mail

room

Checks

1Remittance list

Compare Performed by cashier

1Remittance list

Check From otherSources

CheckEnter data from

checks

Add new check

data to file and prints output

Cash receipts

file

321

Deposit slip 32

Cash receipts 1

Listing (journal)

From otherSources

From otherSources From other

Sources

C/R File C

Organizations can significantly improve processes by following just one simple principle

Embedding IT into the business process allows business and information processes to be improved simultaneously.

The sales/collection process contributes several important numbers for external reporting, including gross sales, sales returns, sales allowances, sales discounts, bad debt expense and the accounts receivable balance.

Accounting uses information from this process to prepare management reports and financial statements

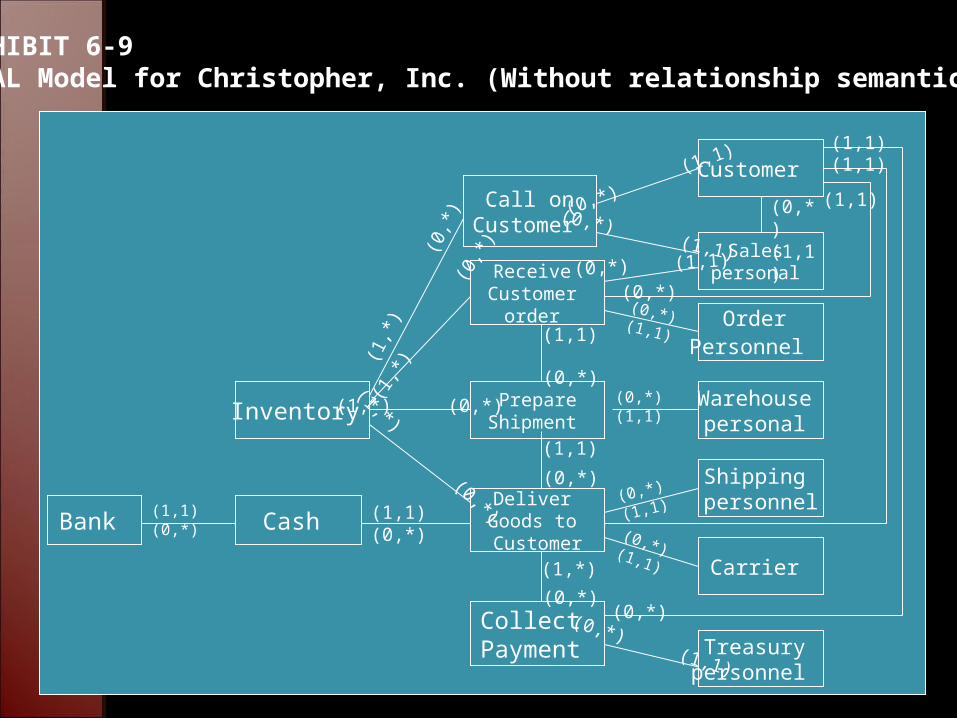

Customer

Sales personal

Order Personnel

Warehouse personal

Shipping personnel

Call onCustomer

PrepareShipment

Collect Payment

Inventory

Cash Bank (1,1) (0,*)

(1,1) (0,*)

(1,*

)

(0,*) (1

,1)

Receive Customer

order

Deliver Goods to Customer

(0,*

) (0,*) (1,1)

Carrier

Treasury personnel

(1,1)

(1,1)

(1,1)

(1,1)

(1,1)

(0,*) (1,1)

(0,*)(0,*) (1,1)

(1,*)

(0,*)

(0,*)

(0,*)

(0,*)

(1,1) (0,*) (1,1)

(0,*) (1,1)

(0,*)(0,*) (1,1)

(0,*) (1,1)

(1,*

)

(0

,*)

(1,*) (0,*)(1,*) (0,*)

EXHIBIT 6-9REAL Model for Christopher, Inc. (Without relationship semantics)

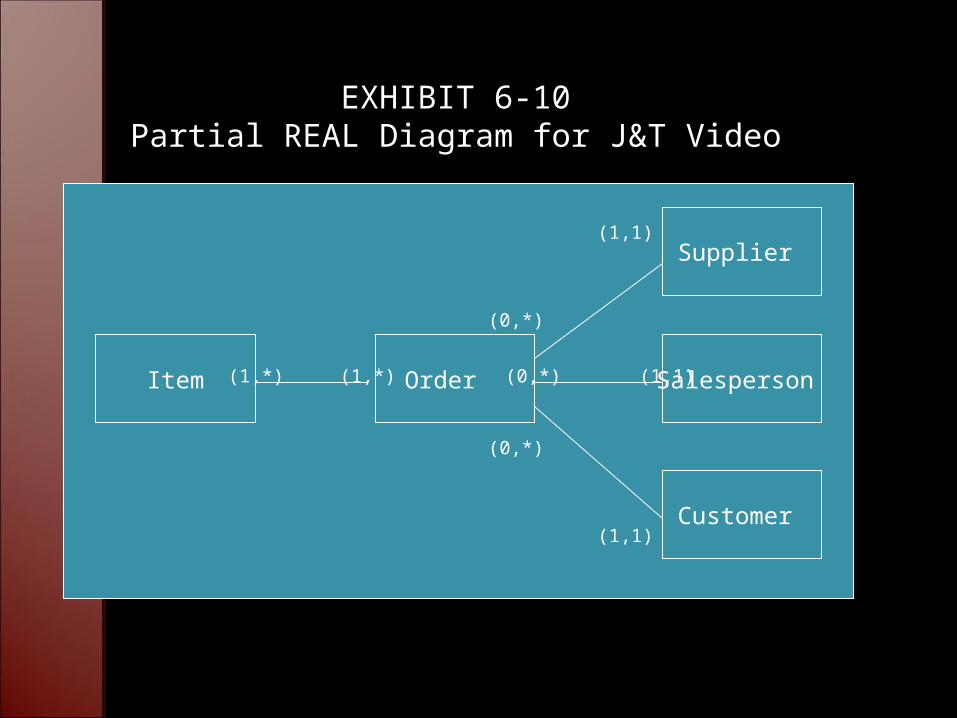

Customer

Order Item Salesperson

Supplier

(1,1)

(1,*) (1,*) (0,*) (1,1)

(1,1)

(0,*)

(0,*)

EXHIBIT 6-10Partial REAL Diagram for J&T Video

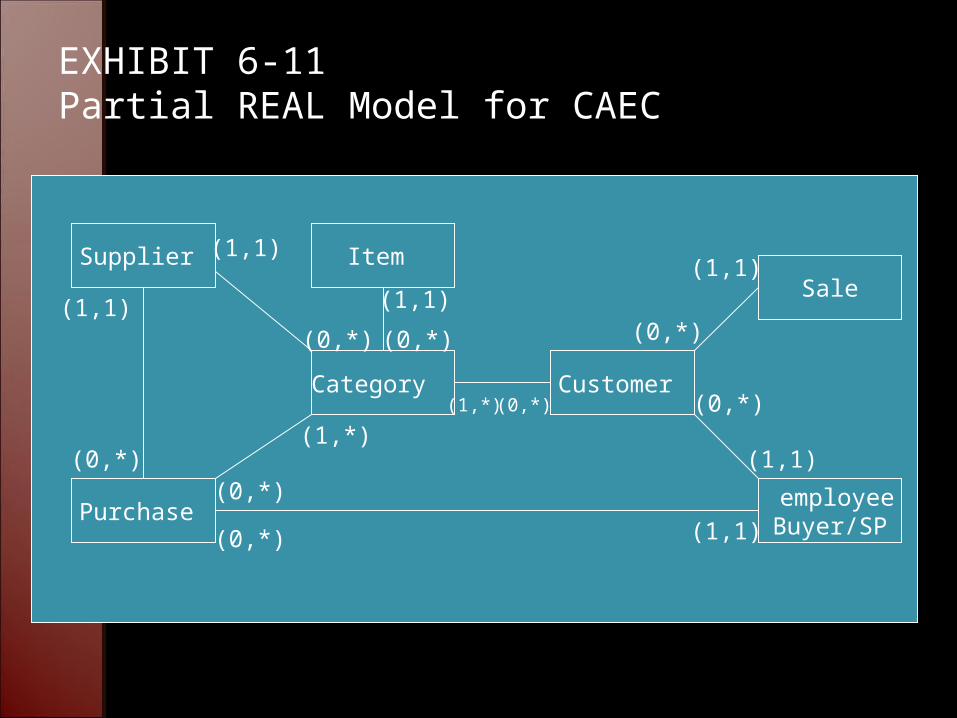

Supplier Item

Category

employeeBuyer/SP

Purchase

Customer

Sale

(1,1)

(1,1)

(1,1)

(1,1)(1,1)

(1,1)(0,*)(0,*)

(0,*)

(0,*)

(0,*)

(0,*)

(0,*) (0,*)

(1,*)(1,*)

EXHIBIT 6-11Partial REAL Model for CAEC