Embed Size (px)

Citation preview

117

Chapter 4

RESEARCH METHODOLOGY &

DATA ANALYSIS

118

4.1 Research Methodology

This chapter explains the methods used in carrying out the study, giving

special emphasis to the measurement of variables. It should be noted at the

outset that the Methodology was to a certain extent an evolving one that took

definite shape as the study progressed. The content of this chapter is being

organized in logical order i.e., in terms of the relationships of the concepts.

But in the case of organization of procedures, chronological order is followed

i.e. discussing the steps in the order in which they were taken.

General Perspective

The research reported here embodied a quantitative perspective. Even

though this study touches different areas of diagnosis, description and even

exploration in the selection and linking of variables, the type of research is

designated as diagnostic research. The research method used to collect data

was sample survey method. Other methods of data collection were found

unsuitable in this context, especially considering the sample size and hence

ignored.

Variables

This study was designed to explore the impact of Business Communication

strategy on consumers in the service sector especially banking and insurance

sector.

The independent variable in this study is business communication. One factor

of this independent variable is formulation of communication strategy. Two

dependent variables are Communication-Effect and Consumer Purchase

Behavior of any services. Communication-Effect was measured both in terms

of Advertising Effectiveness and Communication Objectives. Each of these

119

variables is elaborated upon the coming section of this chapter.

Sample for the study

Sample for the study was taken from different cities of Gujarat; these cities

are the big cities of Gujarat State. Some of them are being the industrial hub

of Gujarat, have a cosmopolitan environment where people from every nook

and comer of the state reside. Moreover, these areas are centrally located

when compared to other corporation areas. In fact, whole Gujarat state can be

considered as a 'big city' due to its peculiar features like high density of

population and higher consumer orientation. The primary concern of research

was with the behavior of people in response to the communication by the

service sector.

Objectives of the study

To study customer’s perceptions and expectations towards the

communication from companies and to measure the overall

communication pattern in service sector in India.

To study the importance of business communication strategies

influencing viewers.

To compare the communication strategies across the major players in

service sector.

To segment customers into several perceived quality segments on the

basis of demographic, psychographic and other profiles.

To study awareness of the customers with regard to the

communication provided by the companies and consumer buying

behavior in service sector

120

Research Design: Descriptive Research

Sampling Design

Target population: Adults ( 18 years) who have used the particular services

as applicable) for at least last 1 year

Sampling unit: Individual / Group / banking & Insurance customers

Sampling Universe: all customers of public & private banking & insurance

sector

Estimated Sample Size: 250 respondents each form different service users

of Banking & insurance sector.

Sampling Technique: Quota sampling: As the population in Gujarat State

does not constitute a homogeneous group, quota sampling has been used so

as to obtain a representative sample. In this technique, the population is

classified into a number of non-overlapping subpopulations and sample items

are selected using convenience or judgmental sampling. The classification

variable used for purpose of this study will be geographical region, where

leading cities of Gujarat will be included. Further, to obtain a better

representation of the population, sample will consists of respondents from

different age groups, income levels and education levels.

Extend: This study was limited to the leading cities of Gujarat state

Sources of data: primary and secondary sources

121

Collection of data:

Secondary data: For conceptual clarity, earlier studies relevant to the

research have been referred from various journals, magazines and websites.

Primary data: Primary data has been collected using Structured

Questionnaires as the survey instrument. Separate set of questionnaires were

administered to the respondents of service sectors.

Tools and techniques: Statistical tools required for the purpose of study

applied.

Research instrument: structured questionnaires

122

4.2 Data Analysis

Introduction

The data, after collection, has to be processed and analyzed in accordance

with the outline laid down for the purpose at the time of developing the

research plan. This is essential for a scientific study and for ensuring that we

have all relevant data for making contemplated comparison and analysis. The

term “analysis” means the separation of a substance into its constituent

elements to determine either their nature (qualitative analysis) or their

proportions. It is computation of certain measures along with searching for

patterns of relationship that exist among data groups. Thus, “in the process of

analysis, relationships or differences, supporting or conflicting with original or

new hypotheses should be subjected to statistical tests of significance to

determine with what validity data have some indication or any conclusions.”

(Kothari, C.R. “Research Methodology”, Wishwa Prakashan pp . 151.) Taking

this statement as guiding torch, the primary data have been analyzed and

conclusions are drawn.

In Today’s era one of the most important things in the world of business is to

trigger off great relationships with Customers & other enterprises so that a

company can earn a name in the market. In order to establish a reputation in

the business world, sellers need to have a great business communication

strategy. Business communication can essentially be divided into internal and

external communication.

Today people are getting communicated for nearly all kinds of services,

products & ideas from different kinds of companies. From education to finance

& retailing to recreation each & every span of the market is full of

123

advertisements, which are the biggest platform providers to introduce the

company to the real customer.

Things like establishing a brand, marketing of products and services,

advertising, working on things like public relations, media management and

even business dealings with customers or other business firms fall in the

category of external business communication. Moreover technological

advances have made it possible for India to compete on a global basis in

areas of communication.

4.3 Demographic Factor-Wise Profile of Investor’s investing in

Banking Sector

The present study is conducted with the objective of identifying the

association between demographics of individual investors and effect of

business communication on their investment behaviors in bank. This chapter

presents the results of the primary survey of investors conducted to achieve

the above mention objective. It examines the null hypothesis that the business

communication has no effect on investment preferences of individual

investor’s demographic characteristics such as age, sex, income, occupation,

employment status and family size. It gives clear idea about the different

types of respondent’s demographic status. The table shows different

demographic factors like Gender, Total Annual Family Income, Education,

Age, and occupation. The respondents from different age group & income

group can be considered important for analyzing the impact of business

communication strategies on consumers. To begin with we shall present a

brief profile of the sample respondents. The rest of the chapter is talk about

the analysis of the data pertaining to investors preferences due to business

communication across their demographics.

124

The research was an attempt to know the investment pattern of investors in

banking sector because of business communication and its impact on

consumers of Gujarat.

Socio-Economic Status of the investors

Table 4.1 Gender, Total Annual Family Income, Education, Age, and occupation

Sl. No. Status Number of Respondents

Percentage to Total

Gender

1. Male 183 77.87

2. Female 52 22.13

Total 235 100

Total Annual Family Income 1 Under 250000 107 45.53

2 250000-500000 80 34.04

3 500000-750000 44 18.73

4 More than 750000 4 1.70

Total 235 100

Education

1 Below Metric 10 4.26

2 Higher Secondary 32 13.62

3 Graduation 139 59.15

4 Post-Graduation 54 22.98

Total 235 100.00

Age

1 Less than 25 48 20.43

2 26-35 81 34.47

3 36-45 66 28.09

4 46-55 27 11.49

5 Above 55 13 5.53

Total 235 100.00

Occupation

1 Government Service 27 11.49

2 Professional 49 20.85

3 Businessman 64 27.23

4 Private employee 63 26.81

5 Retired Personnel 6 2.55

6 Homemaker 26 11.06

Total 235 100.00

125

Table 4.1 exhibits the socio-economic status of the investors investing in

banking sector. It is clear from Table 4.1 that out of 235 investors investing in

banking sector, 77.87% were male and the remaining 22.13% investors were

female. From figure 5.1 it can be easily seen that there are very less female

who are investing in bank sector.

Fig. 4.1 Gender wise profile

Income play important role in investing. Figure 4.2 gives Total

Annual Income of the respondents. From figure it can be seen that maximum

investors have income less than 250000. Number of the respondents having

Income more than 7500000 is very low. With the income of 250000 to 500000

are also having important role in investing.

0

20

40

60

80

100

120

140

160

180

200

Male Female

126

Fig 4.2 Total Annual Income of Investors

Education Qualification is also one of the most influencing factors in financial

market. Out to 235 investors 4.26 investors education is below metric, 13.62

investors have taken education up to Higher Secondary, 59.15 are graduates

and 22.98% investors are post graduates. The Educational Qualification of

respondents is shown in figure 5.3. Chart shows that most of the respondents

are highly educated.

Fig. 4.3 Educational Qualification of investors

107

80

44

4

Below Metric

Higher Secondary

Graduation

Post Graduation

10.00

32.00

139.00

54.00

127

Age is considered to be the most important demographic factor that plays very

important role in determining the communication strategy especially in sector

like banking. Age has its impact on investment. Figure 4.4 represents

respondent’s age profile. From figure it can be easily seen that most of the

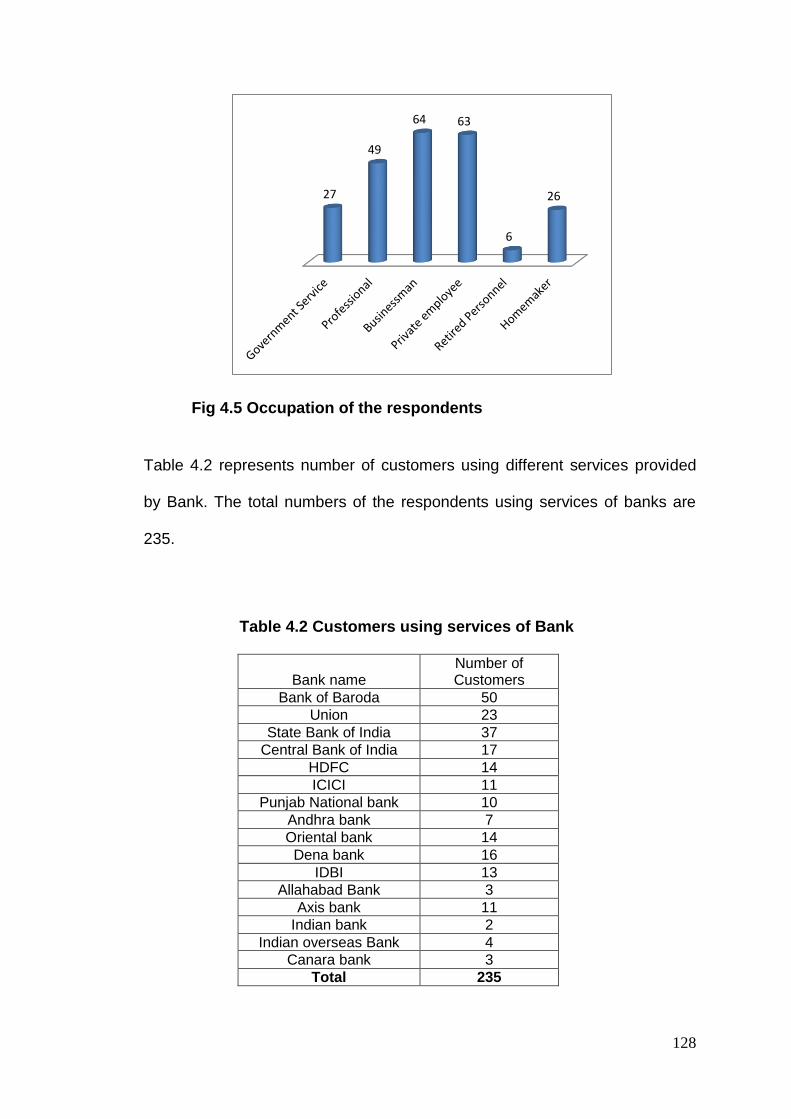

respondent are from 26-35. Figure 4.5 represents occupation of respondents.

In comparison of retired person businessman, private employee and

professionals are investing more in banking. While the number of government

employee and homemaker is also quite significant.

.

Fig 4.4 Age Profile of Respondents

Less than 25

26-35

36-45

46-55

Above 55

128

.

Fig 4.5 Occupation of the respondents

Table 4.2 represents number of customers using different services provided

by Bank. The total numbers of the respondents using services of banks are

235.

Table 4.2 Customers using services of Bank

Bank name Number of Customers

Bank of Baroda 50

Union 23

State Bank of India 37

Central Bank of India 17

HDFC 14

ICICI 11

Punjab National bank 10

Andhra bank 7

Oriental bank 14

Dena bank 16

IDBI 13

Allahabad Bank 3

Axis bank 11

Indian bank 2

Indian overseas Bank 4

Canara bank 3

Total 235

27

49

64 63

6

26

129

According to the table 4.2 number of customer of bank of baroda, union bank

& state bank of India are higher from the total number of respondents. In the

region surveyed the people using the service of allhabad bank are very low in

numbers.

Figure 4.6 represent percentage of customers using different services

provided by bank. From figure it can be easily seen that 21% of customers are

using services of Bank of Baroda, while 16% uses services provided by State

bank of India, it says that still customer have more reliability in government

bank compare to other. It also shows that the percentages of customer in the

surveyed region using the private bank facility are very low.

Fig 4.6 Customers using services of Bank

Bank of Baroda 21%

Union 10%

State Bank of India 16%

Central Bank of

India 7%

HDFC 6%

ICICI 5%

Punjab National bank 4%

Andhara bank 3%

Oriental bank 6%

Dena bank 7%

JOBI 6%

Allahabad Bank 1%

Axis bank 5%

Indian bank 1%

Indian overseas

Bank 2%

Canara bank 1%

130

Table 4.7 represents the reason why customer utilize the services provided by

bank. In order to study the relationship between services and reason of

selecting a particular bank Chi-Square Test has been used.

H0: There is no association between services and reason of selecting a particular bank. H1: : There is significant association between services and reason of selecting a particular bank .

Chi-Square Tests

Value df

Asymp. Sig. (2-sided)

Pearson Chi-Square 135.799(a) 135 .465

Likelihood Ratio 137.903 135 .415

N of Valid Cases 563

Here the value of 799.1352 .with P-value 0.465 which indicates no

relationship between services and reason of selecting a particular bank.

Researcher want to know what are services provided by bank due to which

consumers wants to be a customer of particular bank. Table 4.7 represent the

services utilize by the customer and reason to select particular bank.

131

Table 4.7, Customers utilizing the services provided by bank with reasons.

Bank Name Bank

reputation Convenient

service Regular

customer Excellent Service

Security Accessibility Returns Sales

product

Variety of

products Others

Bank of Baroda

35 17 34 25 13 18 7 10 6 35

Union 10 7 14 10 3 8 3 1 0 0 State

Bank of India

22 14 13 14 12 7 8 5 4 2

Central Bank of

India 8 6 7 6 1 2 3 2 0 0

HDFC 8 3 6 3 0 7 3 1 3 0 Punjab

National bank

3 0 3 3 0 1 1 0 1 0

ICICI 9 6 4 5 2 5 0 0 1 0 Andhra

bank 0 1 3 0 1 1 0 0 0 0

Oriental bank

3 2 7 0 1 3 1 1 1 0

Dena bank

7 5 6 3 3 4 3 0 3 0

IDBI 2 3 1 2 5 1 0 0 0 0 Allahabad

Bank 1 1 1 0 0 1 0 0 1 0

Axis bank 4 5 6 4 1 5 2 2 1 0 Indian bank

2 1 0 1 0 0 0 1 0 0

Indian overseas

Bank 3 1 3 0 0 0 0 0 1 1

Canara bank

3 0 3 0 0 0 0 0 0 0

From table it can be seen that customer gives highest priority to Bank

reputation for selecting a particular bank. To make picture clear researcher

are representing few graphs to show the importance for different services.

Figure 4.7 clear says that Bank reputation, Regular Customers and Excellent

service are the three main reasons for customer to utilize service of bank of

baroda.

132

h

Fig 4.7 Customers using services of Bank of Baroda For bank of baroda, the major factors that contribute most in selecting the

services of bank is the bank reputation and the familiarity with the bank

because 17% are the regular customers of the bank services. Excellent and

convenient services of the bank are also other important factors.

Fig 4.8 Customers using services of State Bank of India

Bank reputation 17%

Convenient service

8%

Regular customer 17%

Excellent Service

12% Security 7%

Accessibility 9%

Returns 4%

Sales product 5%

Variety of products

3%

Others 18%

Bank reputation 21%

Convenient service

14%

Regular customer

13% Excellent Service

14%

Security 12%

Accessibility 7%

Returns 8%

Sales product 5%

Variety of products

4%

Others 2%

133

Figure 4.8 clearly says that customers have given highest priority to Bank

Reputation while selecting State Bank of India. They have also given

approximately same priority to Convenient Service, Regular Customer,

Excellent Service and Security.

Fig 4.8 Customers using services of HDFC Bank

f

Fig 4.9 Customers using services of ICICI Bank

Bank reputation 23%

Convenient service

9%

Regular customer

18%

Excellent Service 9%

Security 0%

Accessibility 20%

Returns 9%

Sales product 3%

Variety of products

9%

Others 0%

Bank reputation 28%

Convenient service

19% Regular customer

12%

Excellent Service 16%

Security 6%

Accessibility 16%

Returns 0%

Sales product 0%

Variety of products

3%

Others 0%

134

Fig 4.8 and fig. 4.9 shows that even in private bank like HDFC and ICICI

customers are using services of bank due to its reputation, convenient

service, regular customer and excellent service.

There are few factors which influenced people’s decision for selecting a

service of a particular bank. Table 4.8 represents what are the influenced

factors which effect customer decision for choosing a particular bank. From fig

4.10 it can be seen that 38% customer’s take their decision on the basis of

Friends/Relative Recommendation, while 21% take decision to use bank

service after meeting the bank officer directly, 15% takes decision on the

basis of sales promotion, 13% takes decision due to sales person and 12%

take decision on the basis of advertisement given by the bank. Research has

also done ONE WAY ANOVA to check whether all the factors have same

effect or not. Results are reported in Table 4.9

Table 4.8 Influenced factors for choosing the services of a bank

Influenced Factor Number of Customers

Friends/Relative recommendation

144

Sales Promotion 57

Contacting bank officer directly

79

Advertisement 46

Sales person 49

Other 6

Table 4.9 ANOVA

Sum of Squares df

Mean Square F Sig.

Between Groups

28.162 4 7.040 36.263 .000

Within Groups

227.157 1170 .194

Total 255.319 1174

135

The value of F-statistic is 36.263 with significance value 0.000, indicating

significant impact of various influenced factors but since Levene’s test of

Homogeneity of variance is 29.401 with significance value p<0.00001, the

assumption of Homogeneity of variance for performing ANOVA is violated. So

one cannot reliable on the result of ANOVA and has to go for Welch and

Brown-Forsythe test. Table 4.10 gives the result of the Welch and Brown-

Forsythe robust test for equality of means. Since Welch and Brown-Forsythe

both of the test has significance value p<0.0001, which indicate significant

effect of various influenced factors. Research also done post hoc test for pair

comparison.

Table 4.10 Robust Tests of Equality of Means

Statistic

(a) df1 df2 Sig.

Welch 32.401 4 584.080 .000 Brown-Forsythe

36.263 4 1139.48

9 .000

a Asymptotically F distributed.

Fig 4.10 Influenced factors for choosing the services of a bank

Friends/Relative recommendatio

n 38%

Sales Promotion 15%

Contacting bank officer directly

21%

Advertisement 12%

Sales person 13%

Other 1%

136

From Table 4.11 it can be easily say that Friends/Relatives recommendation

has maximum effect on customer’s decision. The prompt services by the bank

officers also play a very vital role to influence people to contact the bank

officers directly for choosing the services of the bank. Now-a-days sales

promotion in banking sector is also considered to be important factor for

influencing customers.

Table 4.11 Multiple Comparisons

(I) VAR00001 (J) VAR00001 Mean

Difference (I-J) Std. Error Sig. 95% Confidence Interval

Lower Bound Upper Bound

Tamhane Friends/Relative salespromotion .37021277(*) .04241658 .000 .2508900 .4895356 bankofficer .27659574(*) .04435885 .000 .1518181 .4013734

advertisement .41702128(*) .04107074 .000 .3014709 .5325716

salesperson .40425532(*) .04146452 .000 .2876019 .5209087

salespromotion friends -.37021277(*) .04241658 .000 -.4895356 -.2508900

bankofficer -.09361702 .04169901 .226 -.2109174 .0236834

advertisement .04680851 .03818253 .918 -.0605982 .1542152 salesperson .03404255 .03860578 .991 -.0745532 .1426383

bankofficer friends -.27659574(*) .04435885 .000 -.4013734 -.1518181

salespromotion .09361702 .04169901 .226 -.0236834 .2109174

advertisement .14042553(*) .04032923 .005 .0269674 .2538837

salesperson .12765957(*) .04073018 .018 .0130774 .2422417

advertisement friends -.41702128(*) .04107074 .000 -.5325716 -.3014709 salespromotion -.04680851 .03818253 .918 -.1542152 .0605982

bankofficer -.14042553(*) .04032923 .005 -.2538837 -.0269674

salesperson -.01276596 .03712204 1.000 -.1171868 .0916549

salesperson friends -.40425532(*) .04146452 .000 -.5209087 -.2876019

salespromotion -.03404255 .03860578 .991 -.1426383 .0745532

bankofficer -.12765957(*) .04073018 .018 -.2422417 -.0130774 advertisement .01276596 .03712204 1.000 -.0916549 .1171868

Dunnett T3 Friends/Relative salespromotion .37021277(*) .04241658 .000 .2509168 .4895087

bankofficer .27659574(*) .04435885 .000 .1518458 .4013457

advertisement .41702128(*) .04107074 .000 .3014976 .5325449

salesperson .40425532(*) .04146452 .000 .2876286 .5208821

salespromotion friends -.37021277(*) .04241658 .000 -.4895087 -.2509168 bankofficer -.09361702 .04169901 .225 -.2108912 .0236572 advertisement .04680851 .03818253 .916 -.0605742 .1541913

salesperson .03404255 .03860578 .991 -.0745290 .1426141

bankofficer friends -.27659574(*) .04435885 .000 -.4013457 -.1518458

salespromotion .09361702 .04169901 .225 -.0236572 .2108912

advertisement .14042553(*) .04032923 .005 .0269933 .2538578

salesperson .12765957(*) .04073018 .018 .0131034 .2422157 advertisement friends -.41702128(*) .04107074 .000 -.5325449 -.3014976

salespromotion -.04680851 .03818253 .916 -.1541913 .0605742

137

bankofficer -.14042553(*) .04032923 .005 -.2538578 -.0269933

salesperson -.01276596 .03712204 1.000 -.1171637 .0916318

salesperson friends -.40425532(*) .04146452 .000 -.5208821 -.2876286

salespromotion -.03404255 .03860578 .991 -.1426141 .0745290 bankofficer -.12765957(*) .04073018 .018 -.2422157 -.0131034

advertisement .01276596 .03712204 1.000 -.0916318 .1171637

Games-Howell Friends/Relative salespromotion .37021277(*) .04241658 .000 .2540500 .4863755

bankofficer .27659574(*) .04435885 .000 .1551211 .3980704

advertisement .41702128(*) .04107074 .000 .3045334 .5295091

salesperson .40425532(*) .04146452 .000 .2906928 .5178179 salespromotion friends -.37021277(*) .04241658 .000 -.4863755 -.2540500

bankofficer -.09361702 .04169901 .165 -.2078116 .0205775

advertisement .04680851 .03818253 .736 -.0577546 .1513716

salesperson .03404255 .03860578 .904 -.0716784 .1397635

bankofficer friends -.27659574(*) .04435885 .000 -.3980704 -.1551211

salespromotion .09361702 .04169901 .165 -.0205775 .2078116 advertisement .14042553(*) .04032923 .005 .0299734 .2508777 salesperson .12765957(*) .04073018 .016 .0161125 .2392066

advertisement friends -.41702128(*) .04107074 .000 -.5295091 -.3045334

salespromotion -.04680851 .03818253 .736 -.1513716 .0577546

bankofficer -.14042553(*) .04032923 .005 -.2508777 -.0299734

salesperson -.01276596 .03712204 .997 -.1144228 .0888908

salesperson friends -.40425532(*) .04146452 .000 -.5178179 -.2906928 salespromotion -.03404255 .03860578 .904 -.1397635 .0716784

bankofficer -.12765957(*) .04073018 .016 -.2392066 -.0161125

advertisement .01276596 .03712204 .997 -.0888908 .1144228

* The mean difference is significant at the .05 level.

Table 4.12 and Figure 4.11 represent different banking services used by the

customers. 53% of the customers are using saving account service of a bank,

21% customers are using Fixed Deposits scheme of the bank, 13% are using

loans facilities while 12% are current account service. Researcher has drawn

table which shows service used by customer of a particular bank.

Table 4.12 Services used by the customer

Different banking services

No. of customers

Saving Account 209

Overdrafts 4

Loans 50

Current Account 47

Fixed Deposits 82

Others 0

138

.

Fig 4.11 Services used by the customers

Table 4.13 Banking Services used by customers

Bank Name Saving Account

Overdrafts Loans Current Account

Fixed Deposits

Bank of Baroda 46 1 14 15 24

Union 21 0 4 0 8

State Bank of India 32 1 7 10 13

Central Bank of India

15 0 5 4 5

HDFC 12 0 3 2 4

ICICI 10 0 2 1 3

Punjab National bank

9 0 1 0 6

Andhra bank 7 0 3 0 1

Oriental bank 12 0 1 3 5

Dena bank 15 1 2 3 5

IDBI 11 0 3 3 4

Allahabad Bank 2 0 0 1 0

Axis bank 8 0 4 3 2

Indian bank 2 0 0 0 0

Indian overseas Bank

4 0 1 0 1

Canara bank 3 0 0 2 0

Table 4.13 gives detailed analysis of the services used by the customers.

From table it can be seen that maximum number of customers are using

saving account service. It can be also seen that Customer preferred

Government Bank for Current Account, Fixed Deposit and Loan compare to

private bank.

Saving Account 53%

Overdrafts 1%

Loans 13%

Current Account

12%

Fixed Deposits 21%

139

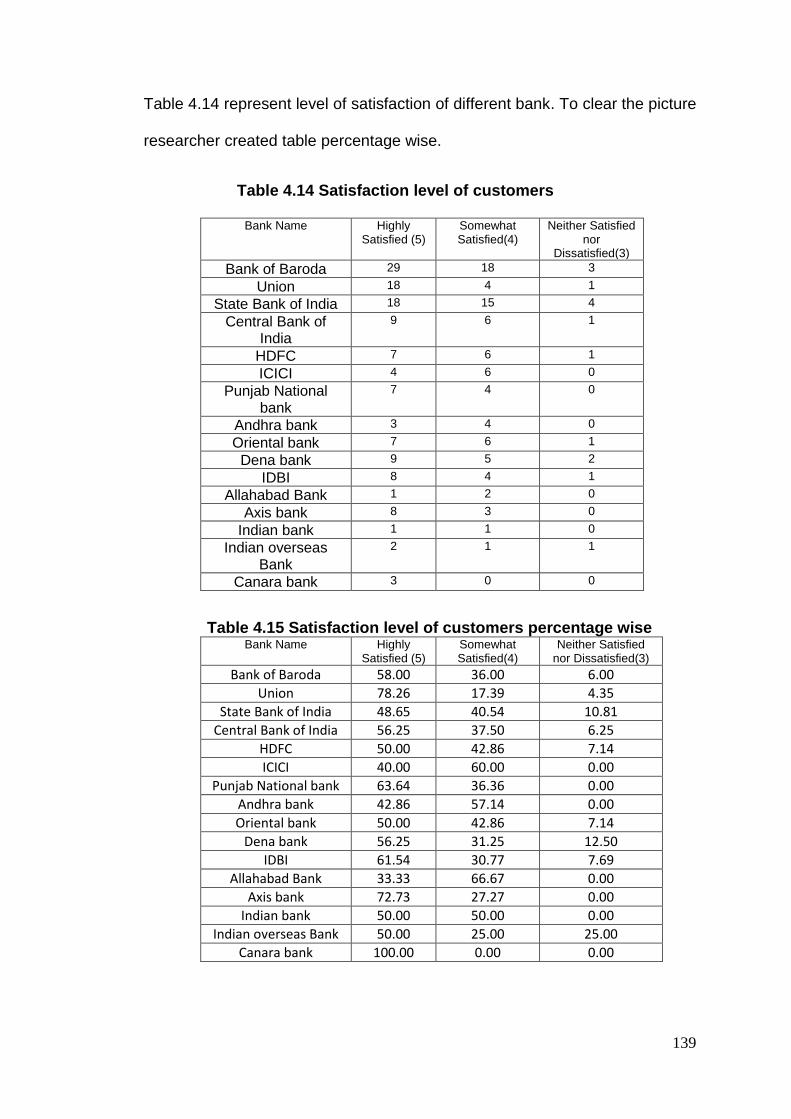

Table 4.14 represent level of satisfaction of different bank. To clear the picture

researcher created table percentage wise.

Table 4.14 Satisfaction level of customers

Bank Name Highly Satisfied (5)

Somewhat Satisfied(4)

Neither Satisfied nor

Dissatisfied(3)

Bank of Baroda 29 18 3

Union 18 4 1

State Bank of India 18 15 4

Central Bank of India

9 6 1

HDFC 7 6 1

ICICI 4 6 0

Punjab National bank

7 4 0

Andhra bank 3 4 0

Oriental bank 7 6 1

Dena bank 9 5 2

IDBI 8 4 1

Allahabad Bank 1 2 0

Axis bank 8 3 0

Indian bank 1 1 0

Indian overseas Bank

2 1 1

Canara bank 3 0 0

Table 4.15 Satisfaction level of customers percentage wise Bank Name Highly

Satisfied (5) Somewhat Satisfied(4)

Neither Satisfied nor Dissatisfied(3)

Bank of Baroda 58.00 36.00 6.00

Union 78.26 17.39 4.35

State Bank of India 48.65 40.54 10.81

Central Bank of India 56.25 37.50 6.25

HDFC 50.00 42.86 7.14

ICICI 40.00 60.00 0.00

Punjab National bank 63.64 36.36 0.00

Andhra bank 42.86 57.14 0.00

Oriental bank 50.00 42.86 7.14

Dena bank 56.25 31.25 12.50

IDBI 61.54 30.77 7.69

Allahabad Bank 33.33 66.67 0.00

Axis bank 72.73 27.27 0.00

Indian bank 50.00 50.00 0.00

Indian overseas Bank 50.00 25.00 25.00

Canara bank 100.00 0.00 0.00

140

Table 4.15 represents the satisfaction level of customer percentage wise.

Some of the points which can be say from table are Customers of Union Bank

of India and Axis bank are highly satisfied with his bank, it can be noted here

Canara bank is not considered because of less customer. Percentages of

Highly Satisfied Customer for ICICI, Andhra Bank, Allahabad bank are very

low, which means customer are not satisfied with bank. Researcher has also

drawn graph to make picture clearer.

Fig 4.12 Satisfaction level of customers

0

20

40

60

80

100

120

Ban

k o

f B

aro

da

Un

ion

Stat

e B

ank

of

Ind

ia

Ce

ntr

al B

ank

of

Ind

ia

HD

FC

ICIC

I

Pu

nja

b N

atio

nal

ban

k

An

dh

ra b

ank

Ori

en

tal b

ank

De

na

ban

k

IDB

I

Alla

hab

ad B

ank

Axi

s b

ank

Ind

ian

ban

k

Ind

ian

ove

rsea

s B

ank

Can

ara

ban

k

Highly Satisfied (5)

Somewhat Satisfied(4)

Neither Satisfied norDissatisfied(3)

141

Table 4.16 Number of Customers who recommend bank to others

Bank Name Definitely(5) Probably(4) May be(3) Probably not (2)

Bank of Baroda 28 15 6 0

Union 16 4 3 0

State Bank of India 19 12 5 1

Central Bank of India 9 6 1 0

HDFC 5 8 0 1

ICICI 5 5 1 0

Punjab National bank 4 6 0 0

Andhra bank 5 1 1 0

Oriental bank 5 9 0 0

Dena bank 7 8 1 0

IDBI 8 4 1 0

Allahabad Bank 2 1 0 0

Axis bank 9 2 0 0

Indian bank 0 2 0 0

Indian overseas Bank 2 0 2 0

Canara bank 3 0 0 0

Table 4.16 gives customer recommendation for particular bank to other. From

table we can say that customer recommends Bank of Baroda, Union Bank

and State Bank of India, i.e. government bank compare to private.

Fig 4.13 Customer Recommendation for Bank

To study the promotion strategy in banking, researcher has framed 5-point

Likert’s Scale which included 12 statements regarding promotion tools. To test

0

5

10

15

20

25

30

Definitely(5) Probably(4) May be(3) Probably not (2)

142

the reliability of scale Cronbach’s Alpha Reliability Test has applied. Result of

these test are as follows:

Reliability Statistics

Cronbach's Alpha

Cronbach's Alpha Based on

Standardized Items N of Items

.841 .842 12

Cronbach’s Alpha value is 0.841, which give support to Reliability of

Questionnaire. It also indicates one can definitely go for further analysis.

Table 4.17 represents the rank given by customers. Figure 4.14 represent the

highest rank given by customers for promotion tool.

Table 4.17 Ranking of Different Promotional Tool given by number of Customers

Promotion Tool Very

Effective(5) 4 3 2

Least

Effective (1)

Advertising on Television 43 92 48 34 10

Advertising in Newspapers 71 71 56 30 6

Personal Selling/Personal Contact 72 70 55 32 5

In Journals and Magazines 15 49 91 61 11

Tele Calling by Salespersons 16 67 76 53 18

Outdoor Advertising Hoardings etc 36 72 78 35 11

Schemes/Gifts/Prizefor customers 52 45 62 45 28

Public Relations/ Events/ Program. 25 58 85 37 28

Online Marketing/E-mail 16 57 81 44 32

Pamphlets/Propaganda 9 32 75 78 40

Letter/Mail/with Relevant Material 16 35 51 67 68

Publishing News in Newspapers 9 38 52 50 88

143

From fig 4.14, it can be easily seen that 19% of the customers have rank

Advertising on Newspaper and Personal Selling/Personal Contact as most

effective tool for promotion, 14% of the customers give priority to

Schemes/Gifts/Prize promotional tool, 11% customers believe on

advertisement on Television as very effective tool while 10% believe Outdoor

Advertising Hoardings etc as most effective tool for promotion.

Fig 4.14 Customers who assign “very effective” to different Promotional

Tool

To study Importance of Advertisement, Sales Promotion and Services

strategy in selecting services of banking, researcher has framed 5-point

Liker’s Scale which included 15 statements. To test the reliability of scale,

11%

19%

19%

4% 4%

10%

14%

7%

4%

2% 4% 2%

Advertising on Television

Advertising in Newspapers

Personal Selling/PersonalContact

In Journals and Magazines

Tele Calling by Salespersons

Outdoor AdvertisingHoardings etc

Schemes/Gifts/Prizeforcustomers

Public Relations/ Events/Program.

Online Marketing/E-mail

Pamphlets/Propaganda

144

KMO and Bartlett's Test and Cronbach’s Alpha Reliability Test has applied.

Result of these test are as follows:

KMO and Bartlett's Test

Kaiser-Meyer-Olkin Measure of Sampling Adequacy. .659

Bartlett's Test of Sphericity

Approx. Chi-Square 490.364

df 105

Sig. .000

Reliability Statistics

Cronbach's Alpha

Cronbach's Alpha Based on

Standardized Items N of Items

.778 .775 15

From the above tables, it can be said that Kaiser-Meyer-Olkin Measure of

Sampling Adequacy found 0.659; it indicates that the sample is adequate for

Factor analysis. The value of Bartlett’s Test of Sphericity is 490.364 with

significance value 0.000, while Cronbach’s Alpha value is 0.778 which give

support to Reliability of Questionnaire. Table 4.17 represents the customer

preference regarding advertisement, sales promotion and service strategy.

145

Fig 4.15 customer’s ranking towards advertisement strategy.

Fig 4.15 Ranking of Advertisement strategy in terms of importance given by number of Customers (Here 1 -means Highest, 2- means High, 3- means Average, 4-low and 5-lowest)

From fig 4.15 it can be said that maximum customers believe that the

contents in the advertisement through public document must be clear and

informative.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5

89

98 36 12

2

49

97

59 26

7

24

80

81 38

15

15 75

84 32

28

7 14 42 15

58

Advertising through other media

Advertising banner posting content is easily understandable and appealing to readers.

Advertising through internet is prominent and can be clicked to see the details easily.

Advertising signage is unique, attractive and understood easily.

The contents in the advertisement through the public document is clear and informative

146

Table 4.17 Ranking of Advertisement, Sales Promotion and Services strategy

in terms of importance given by number of Customers

Strategy

Level of Choosing service

Highest High Average Low Lowest

5 4 3 2 1

Advertisement

The contents in the advertisement through

the public document is clear and informative

89 98 36 12 2

Advertising signage is unique, attractive and

understood easily.

49 97 59 26 7

Advertising through internet is prominent

and can be clicked to see the details easily.

24 80 81 38 15

Advertising banner posting content is easily

understandable and appealing to readers.

15 75 84 32 28

Advertising through other media 7 14 42 15 58

Sales Promotion

Giving a special rate to customers, for

example senior citizens.

98 103 24 5 5

Waving commission charge 41 63 58 36 36

Distributing free gift 21 39 70 38 64

Other marketing support 17 11 30 18 48

Services

Bank Officers provide prompt service. 91 86 40 11 6

Officers provide the correct information

about service, product and financial

transaction.

80 91 45 12 8

Service officers are polite and courteous. 63 95 53 13 12

Financial Forms are easily accessible. 60 87 54 21 14

A convenient one-stop service point. 57 87 45 19 27

Other comments 2 7 19 13 33

147

.

Fig 4.16 Ranking of Sales Promotion strategy in terms of importance given by number of Customers (Here 1 -means Highest, 2- means High, 3- means Average, 4-low and 5-lowest).

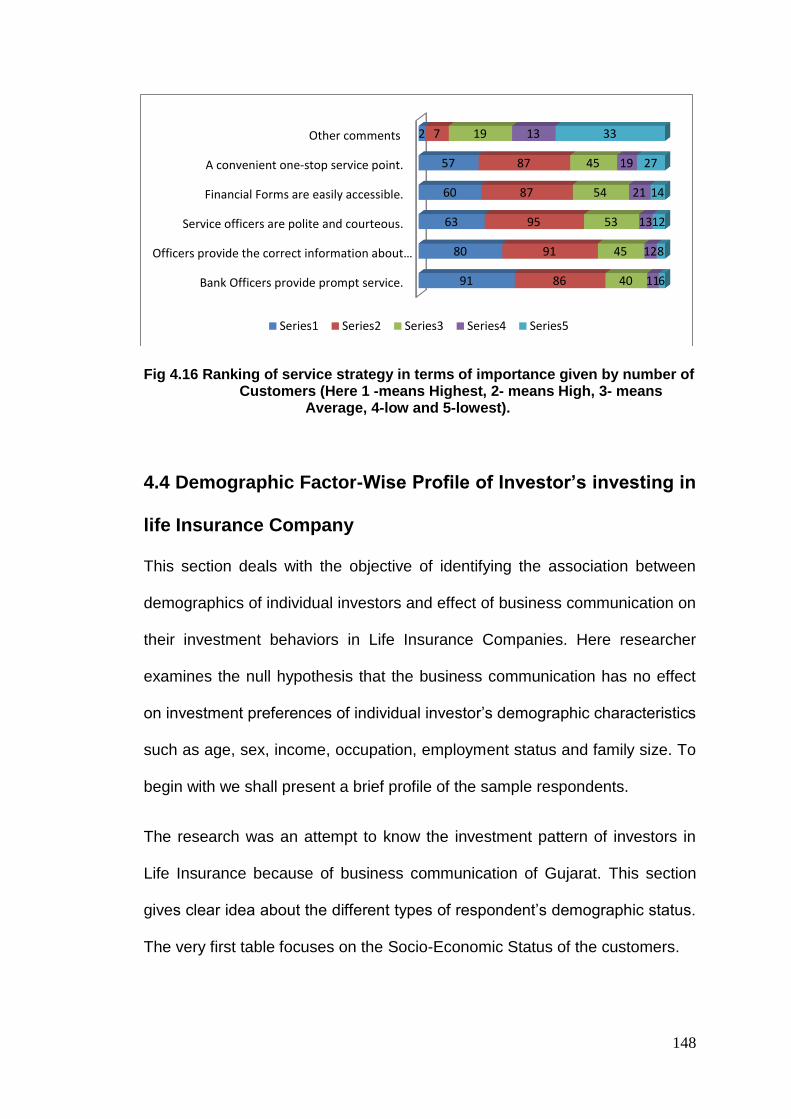

Fig 4.16 shows that customers give maximum importance to “Giving a special

rate to customers, for Example senior citizens. Fig 4.17 represents customer’s

importance regarding Services provided by bank. 91 customers give

importance to prompt service provided by Bank Officers.

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1 2 3 4 5

98 103

24 5 5

41 63

58 36

36

21 39

70 38

64

17 11 30 18

48

Other marketing support

Distributing free gift

Waving commission charge

Giving a special rate to customers, for example senior citizens.

148

Fig 4.16 Ranking of service strategy in terms of importance given by number of

Customers (Here 1 -means Highest, 2- means High, 3- means Average, 4-low and 5-lowest).

4.4 Demographic Factor-Wise Profile of Investor’s investing in

life Insurance Company

This section deals with the objective of identifying the association between

demographics of individual investors and effect of business communication on

their investment behaviors in Life Insurance Companies. Here researcher

examines the null hypothesis that the business communication has no effect

on investment preferences of individual investor’s demographic characteristics

such as age, sex, income, occupation, employment status and family size. To

begin with we shall present a brief profile of the sample respondents.

The research was an attempt to know the investment pattern of investors in

Life Insurance because of business communication of Gujarat. This section

gives clear idea about the different types of respondent’s demographic status.

The very first table focuses on the Socio-Economic Status of the customers.

Bank Officers provide prompt service.

Officers provide the correct information about…

Service officers are polite and courteous.

Financial Forms are easily accessible.

A convenient one-stop service point.

Other comments

91

80

63

60

57

2

86

91

95

87

87

7

40

45

53

54

45

19

11

12

13

21

19

13

6

8

12

14

27

33

Series1 Series2 Series3 Series4 Series5

149

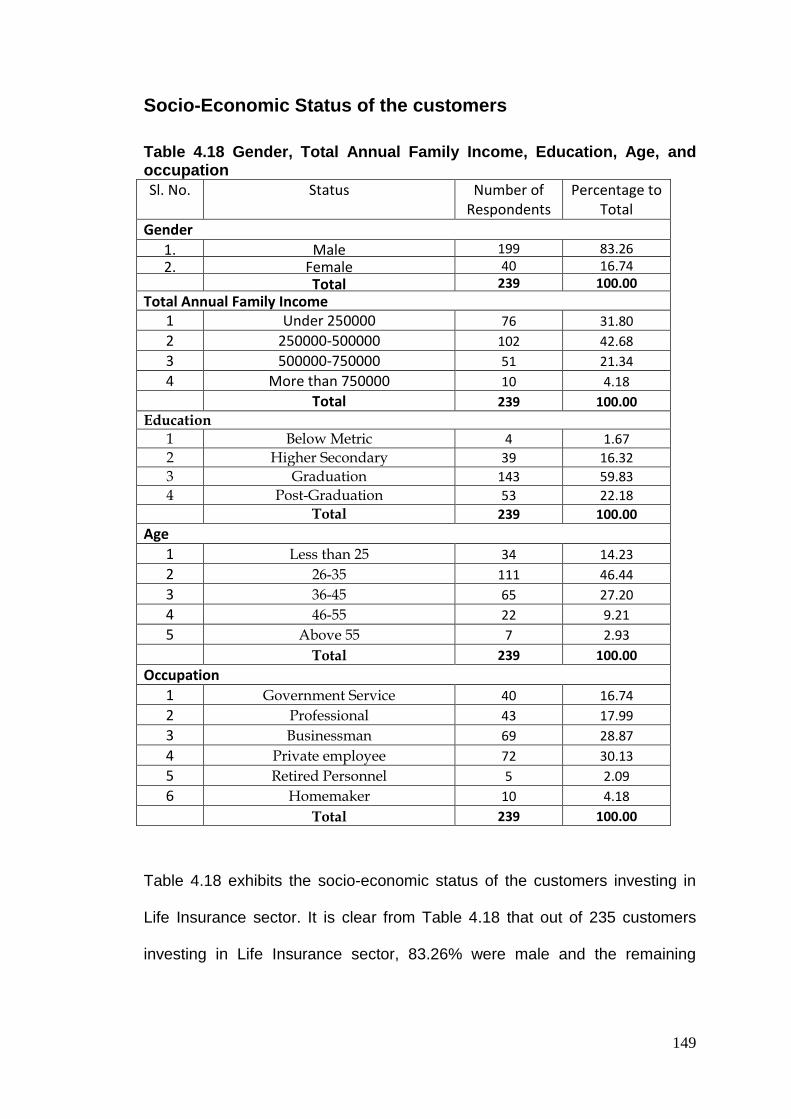

Socio-Economic Status of the customers

Table 4.18 Gender, Total Annual Family Income, Education, Age, and occupation

Sl. No. Status Number of Respondents

Percentage to Total

Gender

1. Male 199 83.26

2. Female 40 16.74

Total 239 100.00

Total Annual Family Income 1 Under 250000 76 31.80

2 250000-500000 102 42.68

3 500000-750000 51 21.34

4 More than 750000 10 4.18

Total 239 100.00

Education

1 Below Metric 4 1.67

2 Higher Secondary 39 16.32

3 Graduation 143 59.83

4 Post-Graduation 53 22.18

Total 239 100.00

Age

1 Less than 25 34 14.23

2 26-35 111 46.44

3 36-45 65 27.20

4 46-55 22 9.21

5 Above 55 7 2.93

Total 239 100.00

Occupation

1 Government Service 40 16.74

2 Professional 43 17.99

3 Businessman 69 28.87

4 Private employee 72 30.13

5 Retired Personnel 5 2.09

6 Homemaker 10 4.18

Total 239 100.00

Table 4.18 exhibits the socio-economic status of the customers investing in

Life Insurance sector. It is clear from Table 4.18 that out of 235 customers

investing in Life Insurance sector, 83.26% were male and the remaining

150

16.74% investors were female. From figure 4.17 it can be easily seen that

there are very less female who are investing in Insurance sector.

..

Fig. 4.17 Gender wise profile

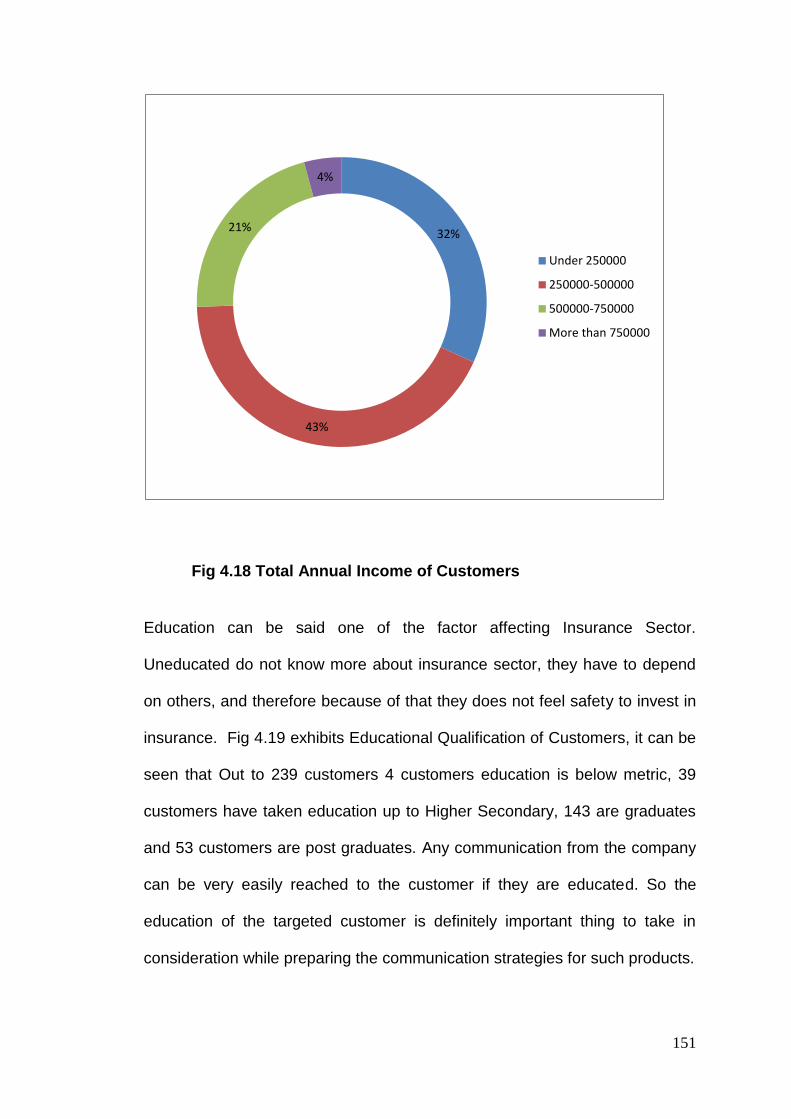

Investing in Insurance Policy lot depend on Income. Figure 4.18 gives Total

Annual Income of the respondents. From figure it can be seen that every

person in different income group are investing due to insecurity in today’s

environment. People from annual income of 500000 are showing higher

interest in investing the insurance policies. Simultaneously persons with

income more than 700000 are less likely to get interest in investing in

insurance policy due to insecurity.

83%

17%

Male Female

151

Fig 4.18 Total Annual Income of Customers

Education can be said one of the factor affecting Insurance Sector.

Uneducated do not know more about insurance sector, they have to depend

on others, and therefore because of that they does not feel safety to invest in

insurance. Fig 4.19 exhibits Educational Qualification of Customers, it can be

seen that Out to 239 customers 4 customers education is below metric, 39

customers have taken education up to Higher Secondary, 143 are graduates

and 53 customers are post graduates. Any communication from the company

can be very easily reached to the customer if they are educated. So the

education of the targeted customer is definitely important thing to take in

consideration while preparing the communication strategies for such products.

32%

43%

21%

4%

Under 250000

250000-500000

500000-750000

More than 750000

152

Fig. 4.19 Educational Qualification of customers

Figure 4.20 represents respondent’s age profile. From figure it can be easily

seen that most of the respondent are from 26-45. Figure 4.21 represents

occupation of respondents.

.

Fig 4.20 Age Profile of Respondents

4

39

143

53

0

20

40

60

80

100

120

140

160

Below Metric HigherSecondary

Graduation PostGraduation

Series1 Series2

Less than 25 14%

26-35 47%

36-45 27%

46-55 9%

Above 55 3%

153

Fig 4.21 Occupation of the respondents

From Fig 4.21 it can be seen that there are 40 respondents whom are

government employee, while remain most of the respondents are from private

sector, as we know private sector can also be said as insecurity sector, so to

make their future secure they will maximum invest in Life Insurance.

Table 4.19 represents number of Life Insurance Policy taken by the

customers and Fig 4.22 represents graphical presentation of the table data. It

can be seen that half of persons have taken life insurance policy for self,

spouse and children who give stamp of proof to our previous statement

regarding employee working in private sector invest more in Life Insurance

Policy.

Table 4.19 Respondents having total Life Insurance Policy

No. of life insurance policy

No. of Respondents

1 71

2 77

3 92

40

43

69

72

5

10

0 10 20 30 40 50 60 70 80

Government Service

Professional

Businessman

Private employee

Retired Personnel

Homemaker

154

Table 4.20 Respondents having Life Insurance Policy for family

Family Members Life Insurance Policy

Self 196

Spouse 173

Children 132

Fig 4.22 Number of Life Insurance Policy

.

Fig 4.23 Respondents having Life Insurance Policy for family

1 17%

2 33%

3 50%

Self Spouse Children

196 173 132

155

Table 4.20 represents respondents having Life Insurance Policy for Self,

Spouse and Children. Fig 4.23 shows that most of respondents have taken

Life Insurance Policy for each family member. Table 4.21 represents reason

for purchasing life insurance policy. Fig 4.24 shows the graphical presentation

of reason for purchasing life insurance data in percentage.

Table 4.21 Reasons for purchasing Life Insurance Policy

Reasons Number of

Respondents

Security Cover 172

Return 84

Saving 114

Income tax Return 100

Other 2

.

Fig 4.24 Reason for purchasing Life Insurance Policy

From Fig 4.24 it can be said that 37% purchase Life Insurance Policy for

Security Cover as most of the respondents are coming from Private Sector.

24% are taking Life Insurance for saving, 21% take Life Insurance Policy take

Security Cover 37%

Return 18%

Saving 24%

Income tax Return

21%

Other 0%

156

for Income tax return as 17% respondents are coming from government

sector, while 18% take for return.

Table 4.22 Total sum assured by Life Insurance for self

Insurance Policy (in lacs) No. of Respondents

Less than 1.5 44

1.5 - 3.0 90

3--5 38

5--10 34

10--20 31

More than 20 2

Table 4.22 show how much person has assured for self in Life Insurance. Fig

4.25 represents that out of total 38% of respondents have invested 1.5 – 3

lacs in Life Insurance for self, while 18% have invested less than 1.5 lacs,

16% invested 3-5 lacs for himself, 14% of respondents have invested 5-10

lacs, 13% invested in between 10-20 lacs in Life Insurance for himself, while

there are 1% respondents who have invested more than 20 lacs for himself in

Life Insurance.

.

Fig 4.25 Total sum in percentage assured by Life Insurance for self

Less than 1.5

18%

1.5 - 3.0 38%

3--5 16%

5--10 14%

10--20 13%

More than 20 1%

157

Table 4.23 Respondents most preferred Insurance Company

Life Insurance Company Number of Customers

LIC 125

RELIGARE 1

KOTAK 13

RELIANCE 17

AVIVA 11

ORIENTAL 1

TATA AIG 13

HDFC STANDARD 14

BAJAJ 20

MAX NEW YORK 4

POSTAL LIFE INSURANCE 1

MPT LIFE 2

BIRLA SUN LIFE 9

NATIONAL INSURANCE 3

ING 5

Total 239

Fig 4.26 Respondents most preferred Insurance Company

LIC 52%

RELIGARE 0%

KOTAK 6%

RELIANCE 7%

AVIVA 5%

ORIENTAL 0%

TATA AIG 6%

HDFC STANDARD 6%

BAJAJ 8%

MAX NEW YORK 2% POSTAL LIFE

INSURANCE 0%

MPT LIFE 1%

BIRLA SUN LIFE 4%

NATIONAL INSURANCE

1% ING 2%

158

Table 4.23 represents the list of Insurance Company preferred by

respondents. 52% respondents have named Life Corporation of India in his

most preferred list, which indicate that respondents have more trust in

Government Insurance Policy compare to Private Insurance Company. Table

4.24 shows different types of policy taken by respondents. From Table 4.24 it

can be seen that respondents mostly invest in Money Back Policy and in

Whole Life Insurance, after that they invest in Term Policy and Child Benefit

plan. There are some respondents who have invested in other insurance

policy also.

Table 4.24 Respondents having different type of Insurance Policy

Insurance Company

Name

Term Policy

Money Back

Policy

Whole Life

Insurance

ULIP Plan

Endowment Policy

Pension Plan

Child Benefit

Plan Other

LIC 20 65 65 10 8 21 38 3

RELIGARE 1 0 0 1 0 0 0 0

KOTAK 3 6 8 3 2 2 4 0

RELIANCE 3 9 9 0 0 3 1 2

AVIVA 5 1 7 1 1 1 5 0

ORIENTAL 0 0 0 0 0 1 0 1

TATA AIG 4 2 2 0 0 1 1 0 HDFC

STANDARD 4 0 2 2 0 1 1 0

BAJAJ 9 3 12 9 0 3 4 0 MAX NEW

YORK 2 3 3 0 0 0 1 0

POSTAL LIFE

INSURANCE 0 1 1 0 1 1 0 0

MPT LIFE 0 0 2 0 0 1 0 0 BIRLA SUN

LIFE 0 3 7 2 1 0 3 0

NATIONAL INSURANCE

1 1 2 0 1 2 1 0

ING 1 2 4 0 1 0 0 1

159

Table 4.25 Respondent’s Premium Paying Mode

Premium payment mode No. of Respondents

Through Agent 169

Online Payment 47

Company Branch office 64

Mobile Payment 8

Electronic Bill payment process 11

ECS 3

Credit card 28

Others 1

Table 4.25 indicates the respondent’s premium paying mode. From table we

can say that still most of the respondents i.e. 169 are paying premium through

agent, which means due to hectic schedule they prefer agent for premium

payment. 47 Respondents are doing payment through online which indicate

that people’s now are becoming familiar with internet. 64 respondents directly

go to branch office, 28 respondents do payment through Credit Card. There

are very less respondents who are doing payment using Mobile, Electronic Bill

Payment Process and ECS. Figure 4.27 represents the graphical presentation

of Premium paying mode.

Fig 4.27 Respondent’s Premium Paying Mode

169

47

64

8 11 3

28

1

ThroughAgent

OnlinePayment

CompanyBranchoffice

MobilePayment

ElectronicBill

paymentprocess

ECS Creditcard

Others

160

To verify which attribute respondents like most to invest in Insurance

Company, researcher has designed question regarding that. Table 4.26

represents the reason for selecting particular Insurance Company. In this

table researcher has consider those respondents who has given 5, 6 and 7

rate scale for attributes. To get clear picture researcher has represent value in

percentages in Table 4.27.

Table 4.26 Attribute which respondents value most

Insurance Company Name

Quality of

Service Returns

Premium Payment Facility

Service features/ attributes

Type of company

(private/Public Sector)

Claim Settlement

Policy/history others

LIC 43 60 67 44 55 30 2

RELIGARE 0 0 0 1 0 0 0

KOTAK 5 9 8 5 6 4 1

RELIANCE 4 7 6 6 4 5 2

AVIVA 4 7 8 7 6 4 1

ORIENTAL 0 1 1 0 0 0 0

TATA AIG 5 3 5 5 9 5 1

HDFC STANDARD 3 4 6 7 7 10 3

BAJAJ 12 10 7 7 10 6 0

MAX NEW YORK 1 3 3 3 2 2 0

POSTAL LIFE I 1 1 1 1 1 1 0

MPT LIFE 1 2 1 1 1 0 0

BIRLA SUN LIFE 1 5 4 1 6 2 1

NATIONAL 1 1 2 1 0 0 0

ING 2 1 4 1 4 2 0

*Here figure in table represents no. of respondents who has given rate scale 5,6 and 7.

161

Table 4.27 Attribute which respondents value most (Values indicate percentage)

Insurance Company

Name

Quality of

Service Returns

Premium Payment Facility

Service features/

Type of company

Claim Settlement

Policy/history others attributes (private/Public

Sector)

LIC 34.4 48 53.6 35.2 44 24 1.6

RELIGARE 0.00 0.00 0.00 100.00 0.00 0.00 0.00

KOTAK 38.46 69.23 61.54 38.46 46.15 30.77 7.69

RELIANCE 23.53 41.18 35.29 35.29 23.53 29.41 11.76

AVIVA 36.36 63.64 72.73 63.64 54.55 36.36 9.09

ORIENTAL 0.00 100.00 100.00 0.00 0.00 0.00 0.00

TATA AIG 38.46 23.08 38.46 38.46 69.23 38.46 7.69

HDFC STANDARD 21.43 28.57 42.86 50.00 50.00 71.43 21.43

BAJAJ 60.00 50.00 35.00 35.00 50.00 30.00 0.00

MAX NEW YORK 25.00 75.00 75.00 75.00 50.00 50.00 0.00

POSTAL LIFE 100.00 100.00 100.00 100.00 100.00 100.00 0.00

MPT LIFE 50.00 100.00 50.00 50.00 50.00 0.00 0.00

BIRLA SUN LIFE 11.11 55.56 44.44 11.11 66.67 22.22 11.11

NATIONAL 33.33 33.33 66.67 33.33 0.00 0.00 0.00

ING 40.00 20.00 80.00 20.00 80.00 40.00 0.00

Research has also done two way ANOVA to check whether the entire

attribute have same effect or not.

Table 4.28 Tests of Between-Subjects Effects

Dependent Variable: VAR00003

Source Type III Sum of Squares df Mean Square F Sig.

Corrected Model 10646.961(a) 16 665.435 16.411 .000

Intercept 4490.182 1 4490.182 110.738 .000

VAR00002 740.000 6 123.333 3.042 .012

VAR00001 9906.961 10 990.696 24.433 .000

Error 2432.857 60 40.548

Total 17570.000 77

Corrected Total 13079.818 76

a R Squared = .814 (Adjusted R Squared = .764)

162

Table 4.28 represents the results of Two-Way ANOVA. Here VAR00001

indicate Insurance Companies and VAR00002 indicate various attributes.

VAR00001 (Insurance Companies) p-value is 0.0000, which indicate that

Insurance Companies differs significantly according to attributes of a

company. Similarly, VAR00002(Attributes) p-value is 0.012, which indicate

that Attributes differs significantly. To know the which Insurance Company is

significant compare to other, POST HOC tests are carried out. Here

researcher has done Least Significant Difference (LSD), Bonferroni and

SIDAK POST HOC test. From Multi Comparison table 4.29 it can be seen that

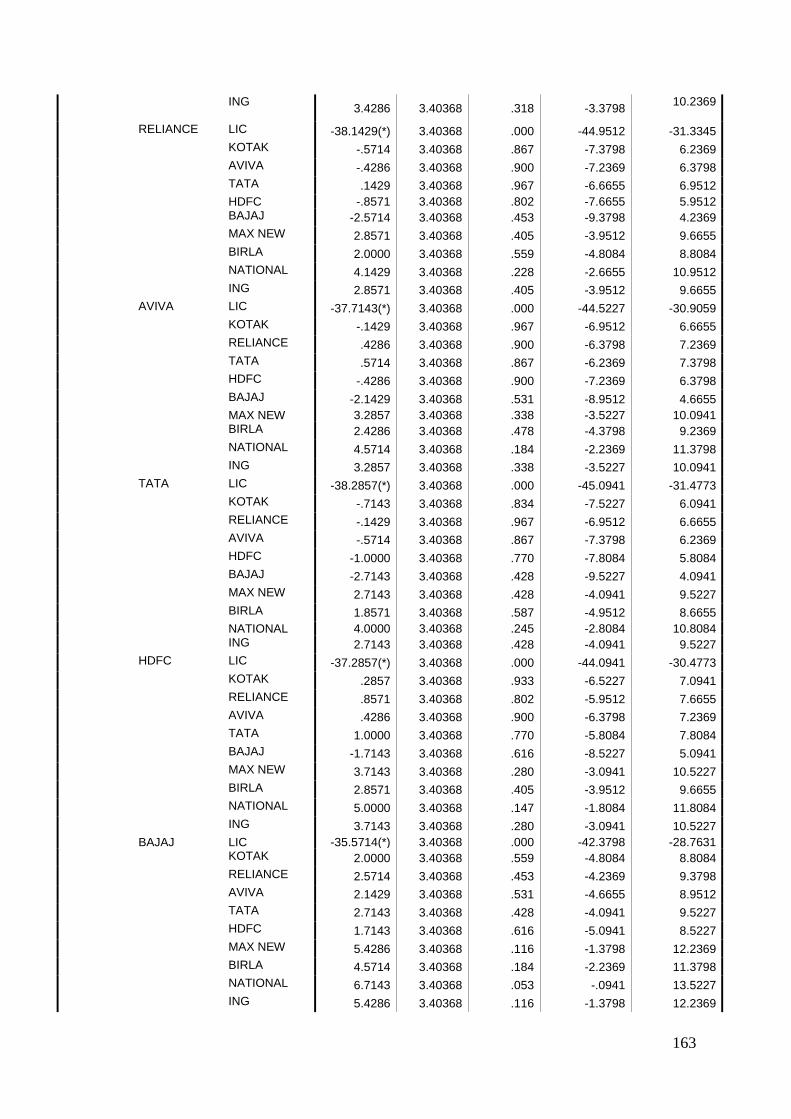

LIC differ significantly with other’s Insurance Company in all the POST HOC

tests, which indicate that LIC attribute are far better than other’s Insurance

Companies.

Table 4.29 Multiple Comparisons Dependent Variable: VAR00003

(I) VAR00001 (J) VAR00001

Mean Difference

(I-J) Std. Error Sig.

95% Confidence Interval

Lower Bound Upper Bound

LSD LIC KOTAK 37.5714(*) 3.40368 .000 30.7631 44.3798 RELIANCE 38.1429(*) 3.40368 .000 31.3345 44.9512

AVIVA 37.7143(*) 3.40368 .000 30.9059 44.5227

TATA 38.2857(*) 3.40368 .000 31.4773 45.0941

HDFC 37.2857(*) 3.40368 .000 30.4773 44.0941

BAJAJ 35.5714(*) 3.40368 .000 28.7631 42.3798

MAX NEW 41.0000(*) 3.40368 .000 34.1916 47.8084

BIRLA 40.1429(*) 3.40368 .000 33.3345 46.9512

NATIONAL 42.2857(*) 3.40368 .000 35.4773 49.0941

ING 41.0000(*) 3.40368 .000 34.1916 47.8084

KOTAK LIC -37.5714(*) 3.40368 .000 -44.3798 -30.7631

RELIANCE .5714 3.40368 .867 -6.2369 7.3798

AVIVA .1429 3.40368 .967 -6.6655 6.9512 TATA .7143 3.40368 .834 -6.0941 7.5227

HDFC -.2857 3.40368 .933 -7.0941 6.5227

BAJAJ -2.0000 3.40368 .559 -8.8084 4.8084

MAX NEW 3.4286 3.40368 .318 -3.3798 10.2369

BIRLA 2.5714 3.40368 .453 -4.2369 9.3798

NATIONAL 4.7143 3.40368 .171 -2.0941 11.5227

163

ING 3.4286 3.40368 .318 -3.3798

10.2369

RELIANCE LIC -38.1429(*) 3.40368 .000 -44.9512 -31.3345

KOTAK -.5714 3.40368 .867 -7.3798 6.2369

AVIVA -.4286 3.40368 .900 -7.2369 6.3798

TATA .1429 3.40368 .967 -6.6655 6.9512

HDFC -.8571 3.40368 .802 -7.6655 5.9512 BAJAJ -2.5714 3.40368 .453 -9.3798 4.2369

MAX NEW 2.8571 3.40368 .405 -3.9512 9.6655

BIRLA 2.0000 3.40368 .559 -4.8084 8.8084

NATIONAL 4.1429 3.40368 .228 -2.6655 10.9512

ING 2.8571 3.40368 .405 -3.9512 9.6655

AVIVA LIC -37.7143(*) 3.40368 .000 -44.5227 -30.9059

KOTAK -.1429 3.40368 .967 -6.9512 6.6655

RELIANCE .4286 3.40368 .900 -6.3798 7.2369

TATA .5714 3.40368 .867 -6.2369 7.3798

HDFC -.4286 3.40368 .900 -7.2369 6.3798

BAJAJ -2.1429 3.40368 .531 -8.9512 4.6655

MAX NEW 3.2857 3.40368 .338 -3.5227 10.0941 BIRLA 2.4286 3.40368 .478 -4.3798 9.2369

NATIONAL 4.5714 3.40368 .184 -2.2369 11.3798

ING 3.2857 3.40368 .338 -3.5227 10.0941

TATA LIC -38.2857(*) 3.40368 .000 -45.0941 -31.4773

KOTAK -.7143 3.40368 .834 -7.5227 6.0941

RELIANCE -.1429 3.40368 .967 -6.9512 6.6655

AVIVA -.5714 3.40368 .867 -7.3798 6.2369

HDFC -1.0000 3.40368 .770 -7.8084 5.8084

BAJAJ -2.7143 3.40368 .428 -9.5227 4.0941

MAX NEW 2.7143 3.40368 .428 -4.0941 9.5227

BIRLA 1.8571 3.40368 .587 -4.9512 8.6655

NATIONAL 4.0000 3.40368 .245 -2.8084 10.8084 ING 2.7143 3.40368 .428 -4.0941 9.5227

HDFC LIC -37.2857(*) 3.40368 .000 -44.0941 -30.4773

KOTAK .2857 3.40368 .933 -6.5227 7.0941

RELIANCE .8571 3.40368 .802 -5.9512 7.6655

AVIVA .4286 3.40368 .900 -6.3798 7.2369

TATA 1.0000 3.40368 .770 -5.8084 7.8084

BAJAJ -1.7143 3.40368 .616 -8.5227 5.0941

MAX NEW 3.7143 3.40368 .280 -3.0941 10.5227

BIRLA 2.8571 3.40368 .405 -3.9512 9.6655

NATIONAL 5.0000 3.40368 .147 -1.8084 11.8084

ING 3.7143 3.40368 .280 -3.0941 10.5227

BAJAJ LIC -35.5714(*) 3.40368 .000 -42.3798 -28.7631 KOTAK 2.0000 3.40368 .559 -4.8084 8.8084

RELIANCE 2.5714 3.40368 .453 -4.2369 9.3798

AVIVA 2.1429 3.40368 .531 -4.6655 8.9512

TATA 2.7143 3.40368 .428 -4.0941 9.5227

HDFC 1.7143 3.40368 .616 -5.0941 8.5227

MAX NEW 5.4286 3.40368 .116 -1.3798 12.2369

BIRLA 4.5714 3.40368 .184 -2.2369 11.3798

NATIONAL 6.7143 3.40368 .053 -.0941 13.5227

ING 5.4286 3.40368 .116 -1.3798 12.2369

164

MAX NEW LIC -41.0000(*) 3.40368 .000 -47.8084 -34.1916

KOTAK -3.4286 3.40368 .318 -10.2369 3.3798

RELIANCE -2.8571 3.40368 .405 -9.6655 3.9512 AVIVA -3.2857 3.40368 .338 -10.0941 3.5227

TATA -2.7143 3.40368 .428 -9.5227 4.0941

HDFC -3.7143 3.40368 .280 -10.5227 3.0941

BAJAJ -5.4286 3.40368 .116 -12.2369 1.3798

BIRLA -.8571 3.40368 .802 -7.6655 5.9512

NATIONAL 1.2857 3.40368 .707 -5.5227 8.0941

ING .0000 3.40368 1.000 -6.8084 6.8084

BIRLA LIC -40.1429(*) 3.40368 .000 -46.9512 -33.3345

KOTAK -2.5714 3.40368 .453 -9.3798 4.2369

RELIANCE -2.0000 3.40368 .559 -8.8084 4.8084

AVIVA -2.4286 3.40368 .478 -9.2369 4.3798

TATA -1.8571 3.40368 .587 -8.6655 4.9512 HDFC -2.8571 3.40368 .405 -9.6655 3.9512

BAJAJ -4.5714 3.40368 .184 -11.3798 2.2369

MAX NEW .8571 3.40368 .802 -5.9512 7.6655

NATIONAL 2.1429 3.40368 .531 -4.6655 8.9512

ING .8571 3.40368 .802 -5.9512 7.6655

NATIONAL LIC -42.2857(*) 3.40368 .000 -49.0941 -35.4773

KOTAK -4.7143 3.40368 .171 -11.5227 2.0941

RELIANCE -4.1429 3.40368 .228 -10.9512 2.6655

AVIVA -4.5714 3.40368 .184 -11.3798 2.2369

TATA -4.0000 3.40368 .245 -10.8084 2.8084

HDFC -5.0000 3.40368 .147 -11.8084 1.8084

BAJAJ -6.7143 3.40368 .053 -13.5227 .0941 MAX NEW -1.2857 3.40368 .707 -8.0941 5.5227

BIRLA -2.1429 3.40368 .531 -8.9512 4.6655

ING -1.2857 3.40368 .707 -8.0941 5.5227

ING LIC -41.0000(*) 3.40368 .000 -47.8084 -34.1916

KOTAK -3.4286 3.40368 .318 -10.2369 3.3798

RELIANCE -2.8571 3.40368 .405 -9.6655 3.9512

AVIVA -3.2857 3.40368 .338 -10.0941 3.5227

TATA -2.7143 3.40368 .428 -9.5227 4.0941

HDFC -3.7143 3.40368 .280 -10.5227 3.0941

BAJAJ -5.4286 3.40368 .116 -12.2369 1.3798

MAX NEW .0000 3.40368 1.000 -6.8084 6.8084

BIRLA -.8571 3.40368 .802 -7.6655 5.9512 NATIONAL 1.2857 3.40368 .707 -5.5227 8.0941

Bonferroni LIC KOTAK 37.5714(*) 3.40368 .000 25.6893 49.4535

RELIANCE 38.1429(*) 3.40368 .000 26.2607 50.0250

AVIVA 37.7143(*) 3.40368 .000 25.8322 49.5964

TATA 38.2857(*) 3.40368 .000 26.4036 50.1678

HDFC 37.2857(*) 3.40368 .000 25.4036 49.1678

BAJAJ 35.5714(*) 3.40368 .000 23.6893 47.4535

MAX NEW 41.0000(*) 3.40368 .000 29.1179 52.8821

BIRLA 40.1429(*) 3.40368 .000 28.2607 52.0250

NATIONAL 42.2857(*) 3.40368 .000 30.4036 54.1678

ING 41.0000(*) 3.40368 .000 29.1179 52.8821

KOTAK LIC -37.5714(*) 3.40368 .000 -49.4535 -25.6893 RELIANCE .5714 3.40368 1.000 -11.3107 12.4535

165

AVIVA .1429 3.40368 1.000 -11.7393 12.0250

TATA .7143 3.40368 1.000 -11.1678 12.5964

HDFC -.2857 3.40368 1.000 -12.1678 11.5964

BAJAJ -2.0000 3.40368 1.000 -13.8821 9.8821

MAX NEW 3.4286 3.40368 1.000 -8.4535 15.3107

BIRLA 2.5714 3.40368 1.000 -9.3107 14.4535

NATIONAL 4.7143 3.40368 1.000 -7.1678 16.5964

ING 3.4286 3.40368 1.000 -8.4535 15.3107

RELIANCE LIC -38.1429(*) 3.40368 .000 -50.0250 -26.2607

KOTAK -.5714 3.40368 1.000 -12.4535 11.3107

AVIVA -.4286 3.40368 1.000 -12.3107 11.4535

TATA .1429 3.40368 1.000 -11.7393 12.0250 HDFC -.8571 3.40368 1.000 -12.7393 11.0250

BAJAJ -2.5714 3.40368 1.000 -14.4535 9.3107

MAX NEW 2.8571 3.40368 1.000 -9.0250 14.7393

BIRLA 2.0000 3.40368 1.000 -9.8821 13.8821

NATIONAL 4.1429 3.40368 1.000 -7.7393 16.0250

ING 2.8571 3.40368 1.000 -9.0250 14.7393

AVIVA LIC -37.7143(*) 3.40368 .000 -49.5964 -25.8322

KOTAK -.1429 3.40368 1.000 -12.0250 11.7393

RELIANCE .4286 3.40368 1.000 -11.4535 12.3107

TATA .5714 3.40368 1.000 -11.3107 12.4535

HDFC -.4286 3.40368 1.000 -12.3107 11.4535

BAJAJ -2.1429 3.40368 1.000 -14.0250 9.7393 MAX NEW 3.2857 3.40368 1.000 -8.5964 15.1678

BIRLA 2.4286 3.40368 1.000 -9.4535 14.3107

NATIONAL 4.5714 3.40368 1.000 -7.3107 16.4535

ING 3.2857 3.40368 1.000 -8.5964 15.1678

TATA LIC -38.2857(*) 3.40368 .000 -50.1678 -26.4036

KOTAK -.7143 3.40368 1.000 -12.5964 11.1678

RELIANCE -.1429 3.40368 1.000 -12.0250 11.7393

AVIVA -.5714 3.40368 1.000 -12.4535 11.3107

HDFC -1.0000 3.40368 1.000 -12.8821 10.8821

BAJAJ -2.7143 3.40368 1.000 -14.5964 9.1678

MAX NEW 2.7143 3.40368 1.000 -9.1678 14.5964

BIRLA 1.8571 3.40368 1.000 -10.0250 13.7393 NATIONAL 4.0000 3.40368 1.000 -7.8821 15.8821

ING 2.7143 3.40368 1.000 -9.1678 14.5964

HDFC LIC -37.2857(*) 3.40368 .000 -49.1678 -25.4036

KOTAK .2857 3.40368 1.000 -11.5964 12.1678

RELIANCE .8571 3.40368 1.000 -11.0250 12.7393

AVIVA .4286 3.40368 1.000 -11.4535 12.3107

TATA 1.0000 3.40368 1.000 -10.8821 12.8821

BAJAJ -1.7143 3.40368 1.000 -13.5964 10.1678

MAX NEW 3.7143 3.40368 1.000 -8.1678 15.5964

BIRLA 2.8571 3.40368 1.000 -9.0250 14.7393

NATIONAL 5.0000 3.40368 1.000 -6.8821 16.8821

ING 3.7143 3.40368 1.000 -8.1678 15.5964 BAJAJ LIC -35.5714(*) 3.40368 .000 -47.4535 -23.6893

KOTAK 2.0000 3.40368 1.000 -9.8821 13.8821

RELIANCE 2.5714 3.40368 1.000 -9.3107 14.4535

AVIVA 2.1429 3.40368 1.000 -9.7393 14.0250

166

TATA 2.7143 3.40368 1.000 -9.1678 14.5964

HDFC 1.7143 3.40368 1.000 -10.1678 13.5964

MAX NEW 5.4286 3.40368 1.000 -6.4535 17.3107

BIRLA 4.5714 3.40368 1.000 -7.3107 16.4535

NATIONAL 6.7143 3.40368 1.000 -5.1678 18.5964

ING 5.4286 3.40368 1.000 -6.4535 17.3107

MAX NEW LIC -41.0000(*) 3.40368 .000 -52.8821 -29.1179

KOTAK -3.4286 3.40368 1.000 -15.3107 8.4535 RELIANCE -2.8571 3.40368 1.000 -14.7393 9.0250

AVIVA -3.2857 3.40368 1.000 -15.1678 8.5964

TATA -2.7143 3.40368 1.000 -14.5964 9.1678

HDFC -3.7143 3.40368 1.000 -15.5964 8.1678

BAJAJ -5.4286 3.40368 1.000 -17.3107 6.4535

BIRLA -.8571 3.40368 1.000 -12.7393 11.0250

NATIONAL 1.2857 3.40368 1.000 -10.5964 13.1678

ING .0000 3.40368 1.000 -11.8821 11.8821

BIRLA LIC -40.1429(*) 3.40368 .000 -52.0250 -28.2607

KOTAK -2.5714 3.40368 1.000 -14.4535 9.3107

RELIANCE -2.0000 3.40368 1.000 -13.8821 9.8821

AVIVA -2.4286 3.40368 1.000 -14.3107 9.4535 TATA -1.8571 3.40368 1.000 -13.7393 10.0250

HDFC -2.8571 3.40368 1.000 -14.7393 9.0250

BAJAJ -4.5714 3.40368 1.000 -16.4535 7.3107

MAX NEW .8571 3.40368 1.000 -11.0250 12.7393

NATIONAL 2.1429 3.40368 1.000 -9.7393 14.0250

ING .8571 3.40368 1.000 -11.0250 12.7393

NATIONAL LIC -42.2857(*) 3.40368 .000 -54.1678 -30.4036

KOTAK -4.7143 3.40368 1.000 -16.5964 7.1678

RELIANCE -4.1429 3.40368 1.000 -16.0250 7.7393

AVIVA -4.5714 3.40368 1.000 -16.4535 7.3107

TATA -4.0000 3.40368 1.000 -15.8821 7.8821

HDFC -5.0000 3.40368 1.000 -16.8821 6.8821 BAJAJ -6.7143 3.40368 1.000 -18.5964 5.1678

MAX NEW -1.2857 3.40368 1.000 -13.1678 10.5964

BIRLA -2.1429 3.40368 1.000 -14.0250 9.7393

ING -1.2857 3.40368 1.000 -13.1678 10.5964

ING LIC -41.0000(*) 3.40368 .000 -52.8821 -29.1179

KOTAK -3.4286 3.40368 1.000 -15.3107 8.4535

RELIANCE -2.8571 3.40368 1.000 -14.7393 9.0250

AVIVA -3.2857 3.40368 1.000 -15.1678 8.5964

TATA -2.7143 3.40368 1.000 -14.5964 9.1678

HDFC -3.7143 3.40368 1.000 -15.5964 8.1678

BAJAJ -5.4286 3.40368 1.000 -17.3107 6.4535

MAX NEW .0000 3.40368 1.000 -11.8821 11.8821 BIRLA -.8571 3.40368 1.000 -12.7393 11.0250

NATIONAL 1.2857 3.40368 1.000 -10.5964 13.1678

Sidak LIC KOTAK 37.5714(*) 3.40368 .000 25.7168 49.4261

RELIANCE 38.1429(*) 3.40368 .000 26.2882 49.9975

AVIVA 37.7143(*) 3.40368 .000 25.8597 49.5689

TATA 38.2857(*) 3.40368 .000 26.4311 50.1403

HDFC 37.2857(*) 3.40368 .000 25.4311 49.1403

BAJAJ 35.5714(*) 3.40368 .000 23.7168 47.4261

167

MAX NEW 41.0000(*) 3.40368 .000 29.1454 52.8546

BIRLA 40.1429(*) 3.40368 .000 28.2882 51.9975

NATIONAL 42.2857(*) 3.40368 .000 30.4311 54.1403

ING 41.0000(*) 3.40368 .000 29.1454 52.8546 KOTAK LIC -37.5714(*) 3.40368 .000 -49.4261 -25.7168

RELIANCE .5714 3.40368 1.000 -11.2832 12.4261

AVIVA .1429 3.40368 1.000 -11.7118 11.9975

TATA .7143 3.40368 1.000 -11.1403 12.5689

HDFC -.2857 3.40368 1.000 -12.1403 11.5689

BAJAJ -2.0000 3.40368 1.000 -13.8546 9.8546

MAX NEW 3.4286 3.40368 1.000 -8.4261 15.2832

BIRLA 2.5714 3.40368 1.000 -9.2832 14.4261

NATIONAL 4.7143 3.40368 1.000 -7.1403 16.5689

ING 3.4286 3.40368 1.000 -8.4261 15.2832

RELIANCE LIC -38.1429(*) 3.40368 .000 -49.9975 -26.2882

KOTAK -.5714 3.40368 1.000 -12.4261 11.2832 AVIVA -.4286 3.40368 1.000 -12.2832 11.4261 TATA .1429 3.40368 1.000 -11.7118 11.9975

HDFC -.8571 3.40368 1.000 -12.7118 10.9975

BAJAJ -2.5714 3.40368 1.000 -14.4261 9.2832

MAX NEW 2.8571 3.40368 1.000 -8.9975 14.7118

BIRLA 2.0000 3.40368 1.000 -9.8546 13.8546

NATIONAL 4.1429 3.40368 1.000 -7.7118 15.9975

ING 2.8571 3.40368 1.000 -8.9975 14.7118

AVIVA LIC -37.7143(*) 3.40368 .000 -49.5689 -25.8597

KOTAK -.1429 3.40368 1.000 -11.9975 11.7118

RELIANCE .4286 3.40368 1.000 -11.4261 12.2832

TATA .5714 3.40368 1.000 -11.2832 12.4261

HDFC -.4286 3.40368 1.000 -12.2832 11.4261 BAJAJ -2.1429 3.40368 1.000 -13.9975 9.7118

MAX NEW 3.2857 3.40368 1.000 -8.5689 15.1403

BIRLA 2.4286 3.40368 1.000 -9.4261 14.2832

NATIONAL 4.5714 3.40368 1.000 -7.2832 16.4261

ING 3.2857 3.40368 1.000 -8.5689 15.1403

TATA LIC -38.2857(*) 3.40368 .000 -50.1403 -26.4311

KOTAK -.7143 3.40368 1.000 -12.5689 11.1403

RELIANCE -.1429 3.40368 1.000 -11.9975 11.7118

AVIVA -.5714 3.40368 1.000 -12.4261 11.2832

HDFC -1.0000 3.40368 1.000 -12.8546 10.8546

BAJAJ -2.7143 3.40368 1.000 -14.5689 9.1403

MAX NEW 2.7143 3.40368 1.000 -9.1403 14.5689 BIRLA 1.8571 3.40368 1.000 -9.9975 13.7118

NATIONAL 4.0000 3.40368 1.000 -7.8546 15.8546

ING 2.7143 3.40368 1.000 -9.1403 14.5689

HDFC LIC -37.2857(*) 3.40368 .000 -49.1403 -25.4311

KOTAK .2857 3.40368 1.000 -11.5689 12.1403

RELIANCE .8571 3.40368 1.000 -10.9975 12.7118

AVIVA .4286 3.40368 1.000 -11.4261 12.2832

TATA 1.0000 3.40368 1.000 -10.8546 12.8546

BAJAJ -1.7143 3.40368 1.000 -13.5689 10.1403

MAX NEW 3.7143 3.40368 1.000 -8.1403 15.5689

BIRLA 2.8571 3.40368 1.000 -8.9975 14.7118

168

NATIONAL 5.0000 3.40368 1.000 -6.8546 16.8546 ING 3.7143 3.40368 1.000 -8.1403 15.5689

BAJAJ LIC -35.5714(*) 3.40368 .000 -47.4261 -23.7168

KOTAK 2.0000 3.40368 1.000 -9.8546 13.8546

RELIANCE 2.5714 3.40368 1.000 -9.2832 14.4261

AVIVA 2.1429 3.40368 1.000 -9.7118 13.9975

TATA 2.7143 3.40368 1.000 -9.1403 14.5689

HDFC 1.7143 3.40368 1.000 -10.1403 13.5689

MAX NEW 5.4286 3.40368 .999 -6.4261 17.2832

BIRLA 4.5714 3.40368 1.000 -7.2832 16.4261

NATIONAL 6.7143 3.40368 .950 -5.1403 18.5689

ING 5.4286 3.40368 .999 -6.4261 17.2832

MAX NEW LIC -41.0000(*) 3.40368 .000 -52.8546 -29.1454 KOTAK -3.4286 3.40368 1.000 -15.2832 8.4261

RELIANCE -2.8571 3.40368 1.000 -14.7118 8.9975

AVIVA -3.2857 3.40368 1.000 -15.1403 8.5689

TATA -2.7143 3.40368 1.000 -14.5689 9.1403

HDFC -3.7143 3.40368 1.000 -15.5689 8.1403

BAJAJ -5.4286 3.40368 .999 -17.2832 6.4261

BIRLA -.8571 3.40368 1.000 -12.7118 10.9975

NATIONAL 1.2857 3.40368 1.000 -10.5689 13.1403

ING .0000 3.40368 1.000 -11.8546 11.8546

BIRLA LIC -40.1429(*) 3.40368 .000 -51.9975 -28.2882

KOTAK -2.5714 3.40368 1.000 -14.4261 9.2832

RELIANCE -2.0000 3.40368 1.000 -13.8546 9.8546 AVIVA -2.4286 3.40368 1.000 -14.2832 9.4261

TATA -1.8571 3.40368 1.000 -13.7118 9.9975

HDFC -2.8571 3.40368 1.000 -14.7118 8.9975

BAJAJ -4.5714 3.40368 1.000 -16.4261 7.2832

MAX NEW .8571 3.40368 1.000 -10.9975 12.7118

NATIONAL 2.1429 3.40368 1.000 -9.7118 13.9975

ING .8571 3.40368 1.000 -10.9975 12.7118

NATIONAL LIC -42.2857(*) 3.40368 .000 -54.1403 -30.4311

KOTAK -4.7143 3.40368 1.000 -16.5689 7.1403

RELIANCE -4.1429 3.40368 1.000 -15.9975 7.7118

AVIVA -4.5714 3.40368 1.000 -16.4261 7.2832

TATA -4.0000 3.40368 1.000 -15.8546 7.8546 HDFC -5.0000 3.40368 1.000 -16.8546 6.8546

BAJAJ -6.7143 3.40368 .950 -18.5689 5.1403

MAX NEW -1.2857 3.40368 1.000 -13.1403 10.5689

BIRLA -2.1429 3.40368 1.000 -13.9975 9.7118

ING -1.2857 3.40368 1.000 -13.1403 10.5689

ING LIC -41.0000(*) 3.40368 .000 -52.8546 -29.1454

KOTAK -3.4286 3.40368 1.000 -15.2832 8.4261

RELIANCE -2.8571 3.40368 1.000 -14.7118 8.9975

AVIVA -3.2857 3.40368 1.000 -15.1403 8.5689

TATA -2.7143 3.40368 1.000 -14.5689 9.1403

HDFC -3.7143 3.40368 1.000 -15.5689 8.1403

BAJAJ -5.4286 3.40368 .999 -17.2832 6.4261 MAX NEW .0000 3.40368 1.000 -11.8546 11.8546

BIRLA -.8571 3.40368 1.000 -12.7118 10.9975

NATIONAL 1.2857 3.40368 1.000 -10.5689 13.1403

169

Based on observed means. * The mean difference is significant at the .05 level.

There are few factors which influenced people’s decision for selecting a

service of a particular Insurance Company. Table 4.30 represents what are

the influenced factors which effect customer decision for choosing a particular

Insurance Company. From fig 4.28 it can be seen that 36% customer’s take

their decision on the basis of Friends/Relative Recommendation, while 21%

take decision on the basis of advertisement. 31% takes decision on the basis

of sales person, 8% takes decision on the basis of companies sales

promotion and 4% take decision to use insurance service after meeting the

officer directly, Research has also done ONE WAY ANOVA to check whether

all the factors have same effect or not. Results are reported in Table 4.31

Table 4.30 Influenced factors for choosing the services of a bank

Influenced Factor Number of Customers

Friends/Relative recommendation

124

Advertisement 74

Sales Promotion 29

Sales Person 106

Contacting Officer Directly 14

Other 1

Table 4.31 ANOVA

Sum of Squares df Mean Square F Sig.

Between Groups 602.880 4 150.720 1.421 .236 Within Groups 7424.667 70 106.067 Total 8027.547 74

Table 4.32 Test of Homogeneity of Variances

Levene Statistic df1 df2 Sig.

2.135 4 70 .086

170

The value of F-statistic is 1.421 with significance value 0.236, indicating no

significant impact of various influenced factors, also Levene’s test of

Homogeneity of variance is 2.135 with significance value 0.086, the

assumption of Homogeneity of variance for performing ANOVA is satisfied.

Fig 4.28 Influenced factors for choosing the services of a Insurance Company

Table 4.33 represents level of satisfaction of different Insurance Company. To

clear the picture researcher created table percentage wise.

Table 4.34 represents the satisfaction level of customer percentage wise.

Some of the points which can be say from table are more than 70% of the

respondents of AVIVA and Birla Life Insurance are highly satisfied , it can be

noted here Religare, Oriental, Postal and MPT Insurance Company is not

considered because of less customer. Percentage of Highly Satisfied

Customer for National, ING, and HDFC Insurance Company are 60-70%,

Friends/Relative recommendatio

n 36%

Advertisement 21% Sales Promotion

8%

Sales Person 31%

Contacting Officer Directly

4%

Other 0%

171

while 50-60% of customers are highly satisfied with KOTAK, Reliance, TATA

and Max New York and 48% of the customers are highly satisfied with LIC

and BAJAJ which means LIC and BAJAJ are not taking care of customer.

Researcher has also drawn graph to make picture clearer.

Table 4.33 Satisfaction level of customers

Bank Name Highly Satisfied

(5)

Somewhat Satisfied(4)

Neither Satisfied nor

Dissatisfied(3)

Not Satisfied

LIC 61 48 16 0

RELIGARE 1 0 0 0

KOTAK 7 5 1 0

RELIANCE 10 6 1 0

AVIVA 8 3 0 0

ORIENTAL 0 1 0 0

TATA AIG 7 3 3 0

HDFC STANDARD

9 1 4 0

BAJAJ 12 6 1 6

MAX NEW YORK

1 2 1 0

POSTAL LIFE 1 0 0 0

MPT LIFE 2 0 0 0

BIRLA SUN LIFE

7 0 2 0

NATIONAL

2 0 1 0

ING 2 0 1 0

LIC 1 2 2 0

172

Table 4.34 Satisfaction levels of customer’s percentage wise

Bank Name Highly Satisfied

(5)

Somewhat Satisfied(4)

Neither Satisfied nor

Dissatisfied(3)

Not Satisfied

LIC 48.80 38.40 12.80 0.00

RELIGARE 100.00 0.00 0.00 0.00

KOTAK 53.85 38.46 7.69 0.00

RELIANCE 58.82 35.29 5.88 0.00

AVIVA 72.73 27.27 0.00 0.00

ORIENTAL 0.00 100.00 0.00 0.00

TATA AIG 53.85 23.08 23.08 0.00

HDFC STANDARD 64.29 7.14 28.57 0.00

BAJAJ 48.00 24.00 4.00 24.00

MAX NEW YORK 25.00 50.00 25.00 0.00

POSTAL LIFE 100.00 0.00 0.00 0.00

MPT LIFE 100.00 0.00 0.00 0.00

BIRLA SUN LIFE 77.78 0.00 22.22 0.00

NATIONAL 66.67 0.00 33.33 0.00

ING 66.67 0.00 33.33 0.00

LIC 20.00 40.00 40.00 0.00

Fig 4.29 Satisfaction level of customers

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

Series1

Series2

Series3

Series4

173

Table 4.35 Number of Customers who recommend Insurance Company to others

Bank Name Definitely(5) Probably(4) May be(3) Probably not (2)

LIC 57 39 25 3

RELIGARE 1 0 0 0

KOTAK 6 5 1 0

RELIANCE 6 8 3 0

AVIVA 6 4 3 0

ORIENTAL 0 1 0 0

TATA AIG 6 2 4 1

HDFC STANDARD 7 3 4 0

BAJAJ 12 3 5 0

MAX NEW YORK 0 3 1 0

POSTAL LIFE 1 0 0 0

MPT LIFE 2 0 0 0

BIRLA SUN LIFE 6 1 2 0

NATIONAL 2 0 1 0

ING 1 2 3 0

Table 4.35 gives customer recommendation for particular Insurance to other.

Fig 4.30 Customer Recommendation for Insurance Company

To study the promotion strategy in Insurance, researcher has framed 12

statements on a 5-point Likert’s Scale, where Scale-5 indicates very effective

0

10

20

30

40

50

60

LIC

REL

IGA

RE

KO

TAK

REL

IAN

CE

AV

IVA

OR

IEN

TAL

TATA

AIG

HD

FC S

TAN

DA

RD

BA

JAJ

MA

X N

EW Y

OR

K

PO

STA

L LI

FE

MP

T LI

FE

BIR

LA S

UN

LIF

E

N

ATI

ON

AL

Definitely(5)

Probably(4)

May be(3)

Probably not (2)

174

and Scale-1 indicate least effective. To test the reliability of scale Cronbach’s

Alpha Reliability Test has applied. Result of these test are as follows:

Table 4.36 Reliability Statistics

Cronbach's Alpha

Cronbach's Alpha Based on Standardized Items N of Items

0.838 0.834 12

Cronbach’s Alpha value is 0.838, which give support to Reliability of

Questionnaire. It also indicates one can definitely go for further analysis.

Researcher has also done ANOVA TEST to test effect of 12 statements.

Table 4.37 ANOVA with Friedman's Test

Sum of

Squares df Mean Square Friedman's Chi-Square Sig

Between People 964.074 238 4.051

Within People Between Items 362.238(a) 11 32.931 457.683 .000

Residual 1718.512 2618 .656

Total 2080.750 2629 .791

Total 3044.824 2867 1.062

Grand Mean = 3.6942 a Kendall's coefficient of concordance W = .119.

The value of F-statistic is 457.683 with significance value 0.000, indicating

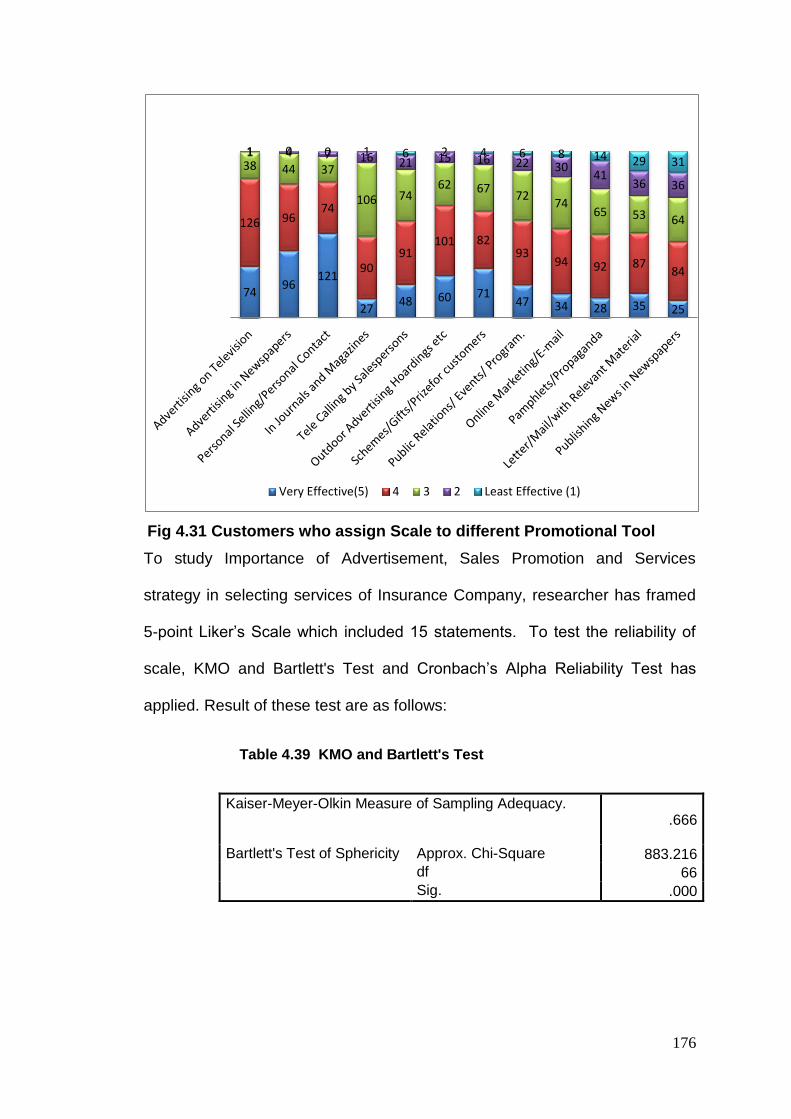

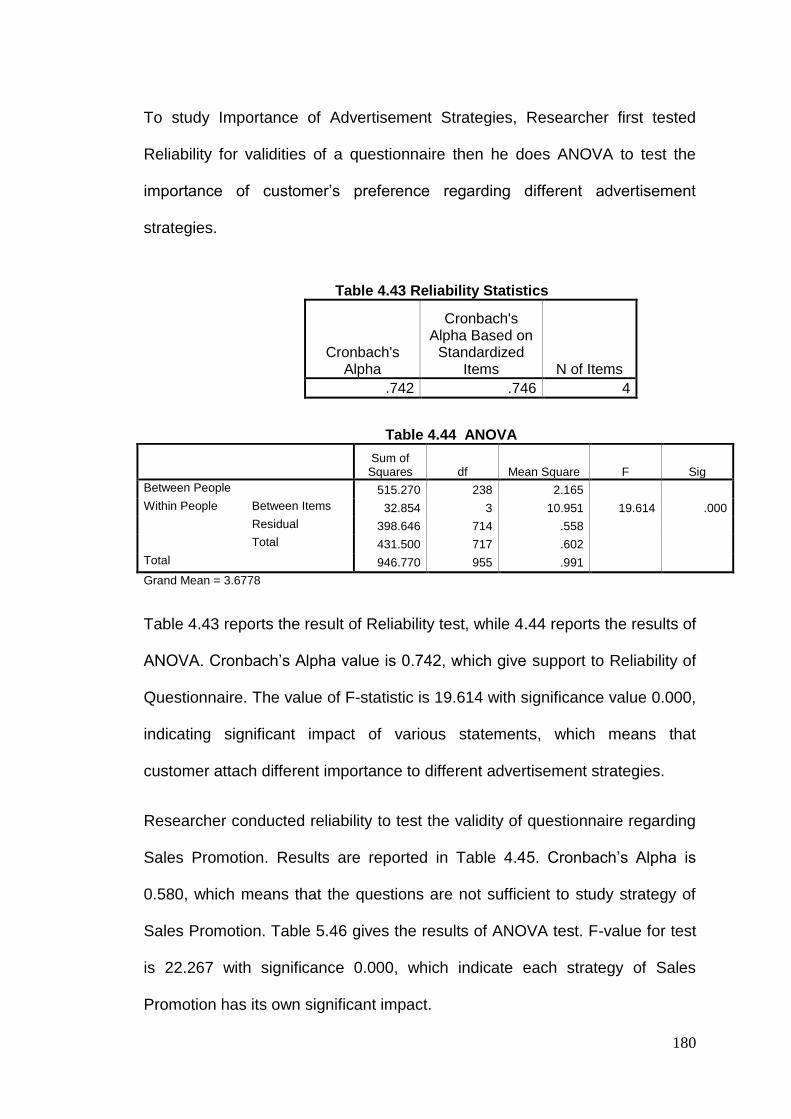

significant impact of various statements. Table 4.38 represents the rank given

by customers. Figure 4.14 represent the rank given by customers for

promotion tool.

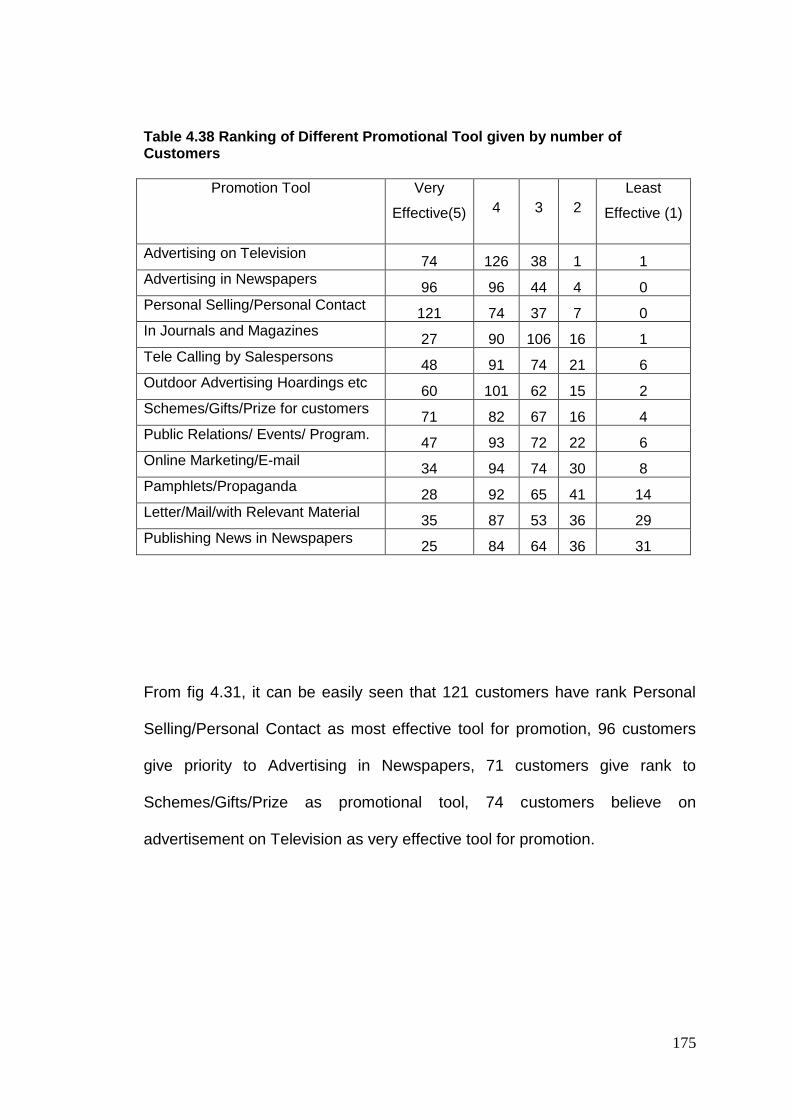

175

Table 4.38 Ranking of Different Promotional Tool given by number of Customers