Embed Size (px)

Citation preview

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 1/13

Corporate Financial Policy:Risk, Return and the CAPM

Jide Wintoki

Fall 2013

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 1 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 2/13

Lecture Outline

The Relationship Between Risk and Return

The Security Market Line

Calculating Individual Stock Betas

Validity and the Role of the CAPM

Some Alternative Theories

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 2 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 3/13

Risk and Return

The return earned on investments represents the marginal benefit of investing.

Risk represents the marginal cost of investing.

For any project to create value, the marginal benefit must exceed themarginal cost of investing.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 3 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 4/13

Project or asset risk

In general, the risk of investing in any project or holding any asset consistsof two components:

Undiversifiable risk (systematic risk, market risk)

Only systematic risk is priced in the market.

This is the only type of risk that is relevant for capital budgeting orasset valuation.

Beta is one way to measure the systematic risk of an asset.

Diversifiable risk (unsystematic risk, idiosyncratic risk, or unique risk)

Investors do not care about unsystematic risk because it can bediversified away very cheaply.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 4 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 5/13

Capital Asset Pricing Model (CAPM)

E (R i ) = R f + β i [E (R m − R f )]

Only beta changes from one security to the next. For that reason, analystsclassify the CAPM as a single-factor model, meaning that just one variableexplains differences in returns across securities.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 5 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 6/13

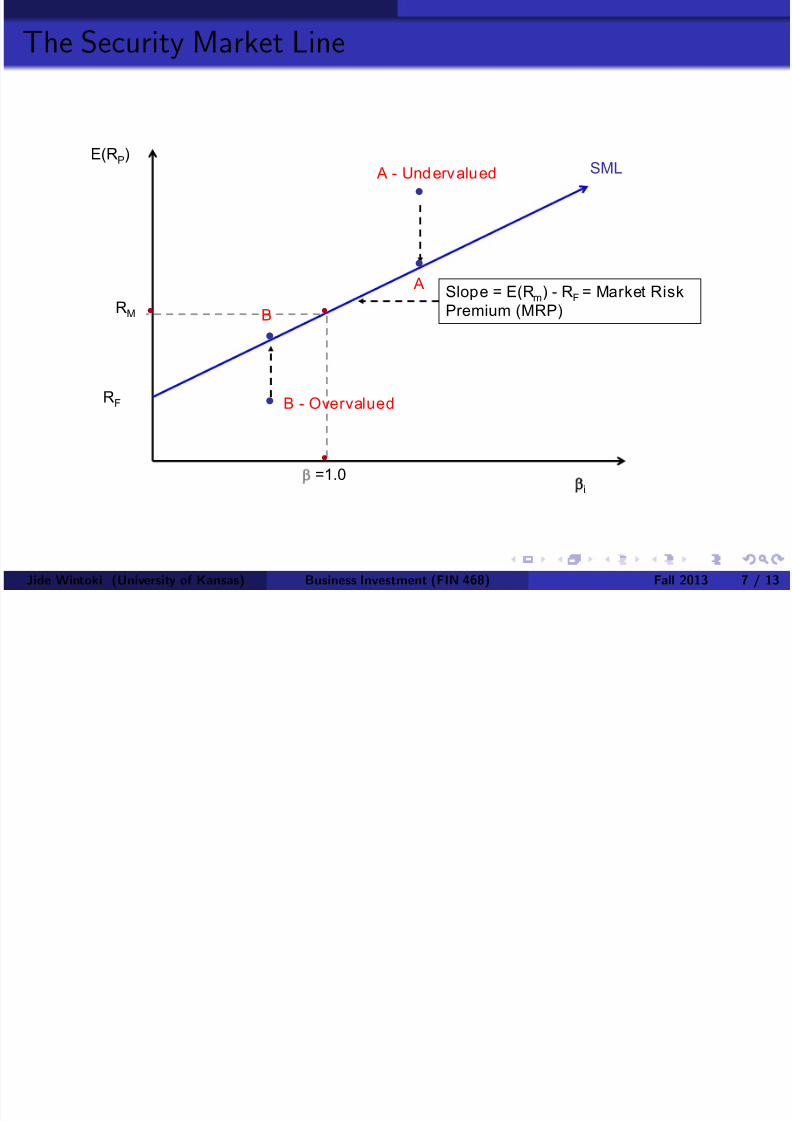

The Security Market Line

Plots the relationship between expected return and betas

In equilibrium, all assets lie on this line

If stock lies above the line:

Expected return is too high

Investors bid up price until expected return falls

If stock lies below the line:

Expected return is too low

Investors sell stock, driving down price until expected return rises

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 6 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 7/13

The Security Market Line

β i

E(RP)

RF

SML

Slope = E(Rm) - RF = Market Risk

Premium (MRP)

•

A - Undervalued

•

•

•RM

β =1.0

•

B

• A

• B - Overvalued

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 7 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 8/13

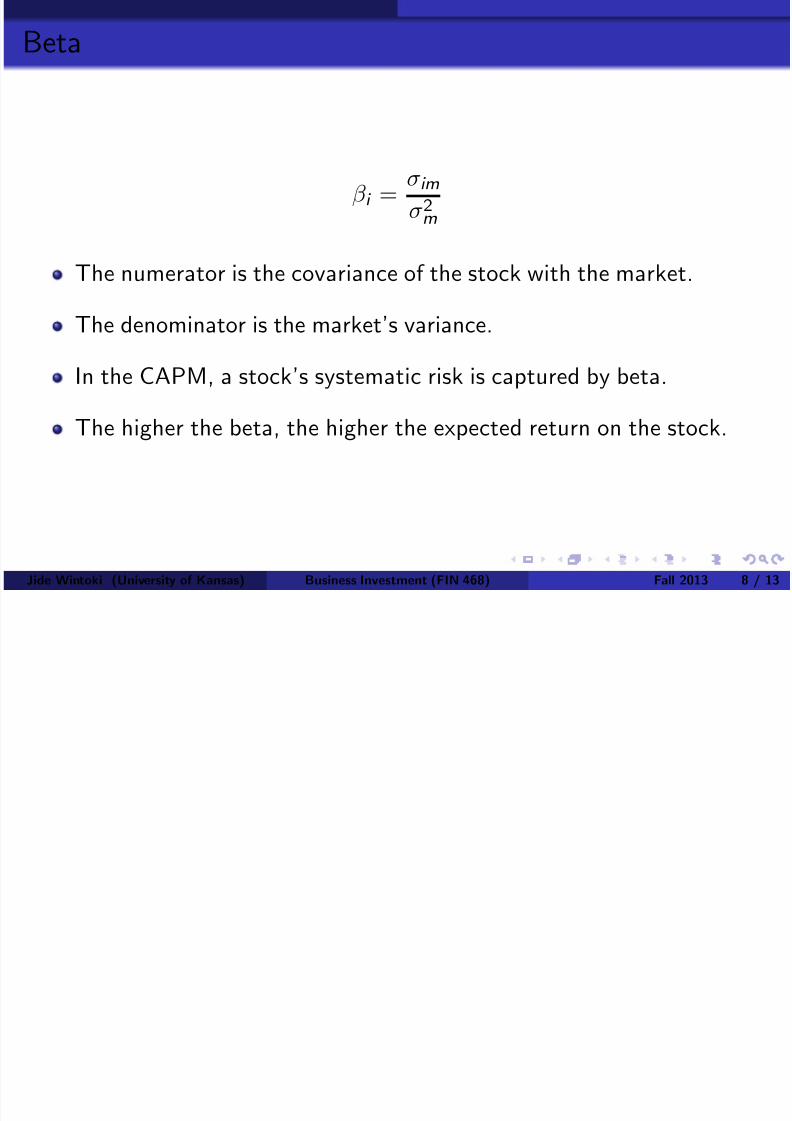

Beta

β i =σim

σ2m

The numerator is the covariance of the stock with the market.

The denominator is the market’s variance.

In the CAPM, a stock’s systematic risk is captured by beta.

The higher the beta, the higher the expected return on the stock.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 8 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 9/13

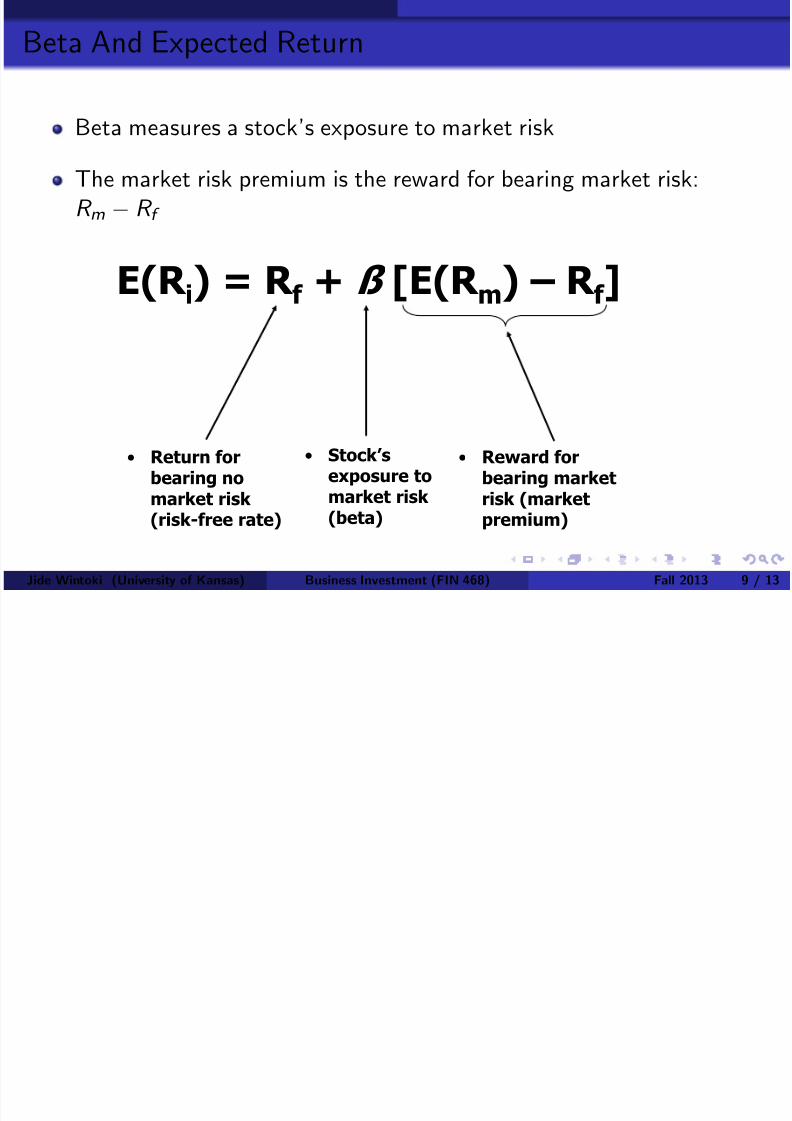

Beta And Expected Return

Beta measures a stock’s exposure to market riskThe market risk premium is the reward for bearing market risk:R m − R f

E(R i) = R f + ß [E(R m) – R f ]

• Return forbearing nomarket risk (risk-free rate)

• Stock’sexposure tomarket risk (beta)

• Reward forbearing marketrisk (marketpremium)

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 9 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 10/13

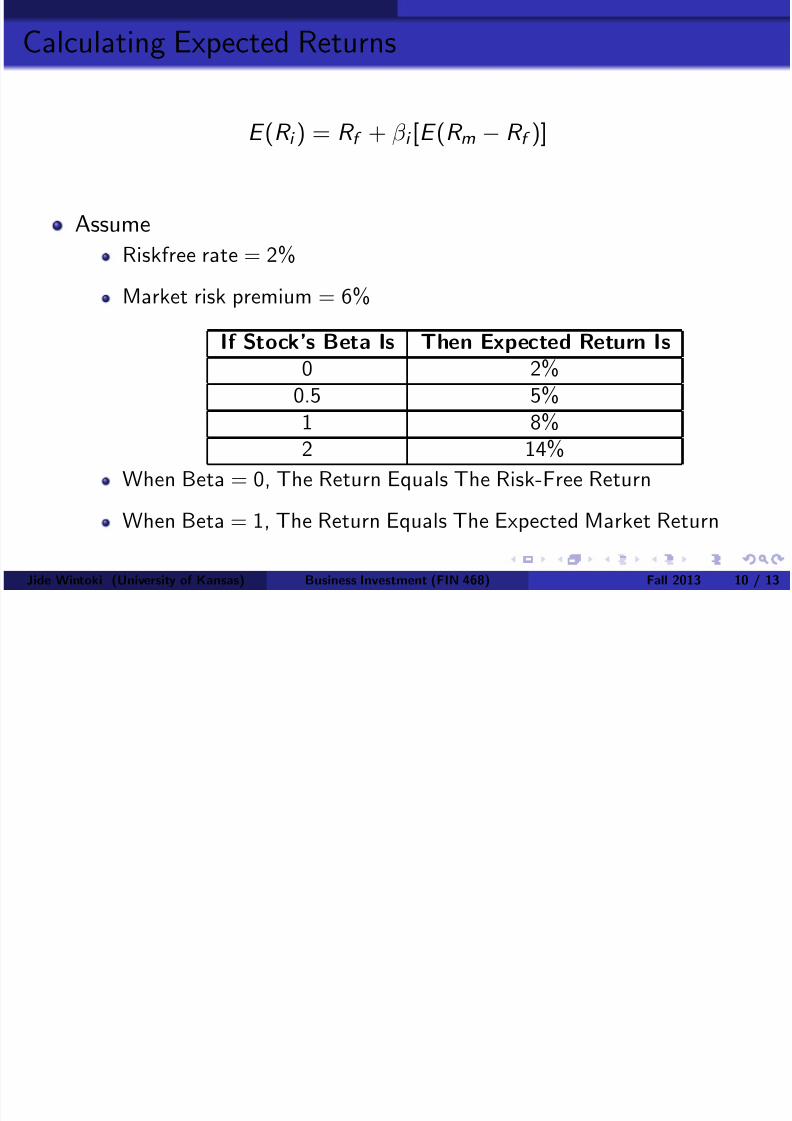

Calculating Expected Returns

E (R i ) =

R f + β i [

E (R m− R

f )]

Assume

Riskfree rate = 2%

Market risk premium = 6%

If Stock’s Beta Is Then Expected Return Is0 2%

0.5 5%

1 8%2 14%

When Beta = 0, The Return Equals The Risk-Free Return

When Beta = 1, The Return Equals The Expected Market Return

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 10 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 11/13

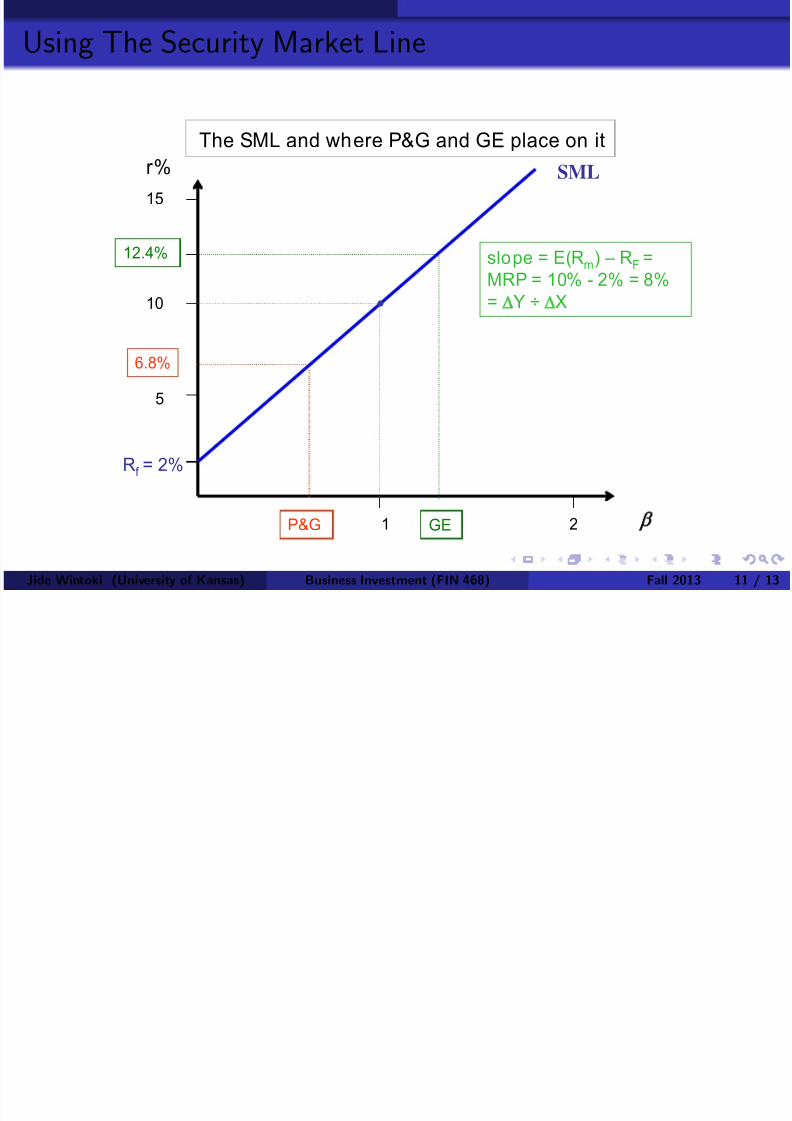

Using The Security Market Line

r%

β

12.4%

10

5

Rf = 2%

1 2GEP&G

SML

6.8%

15

•

slope = E(Rm) – RF =

MRP = 10% - 2% = 8%= ΔY ÷ ΔX

The SML and where P&G and GE place on it

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 11 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 12/13

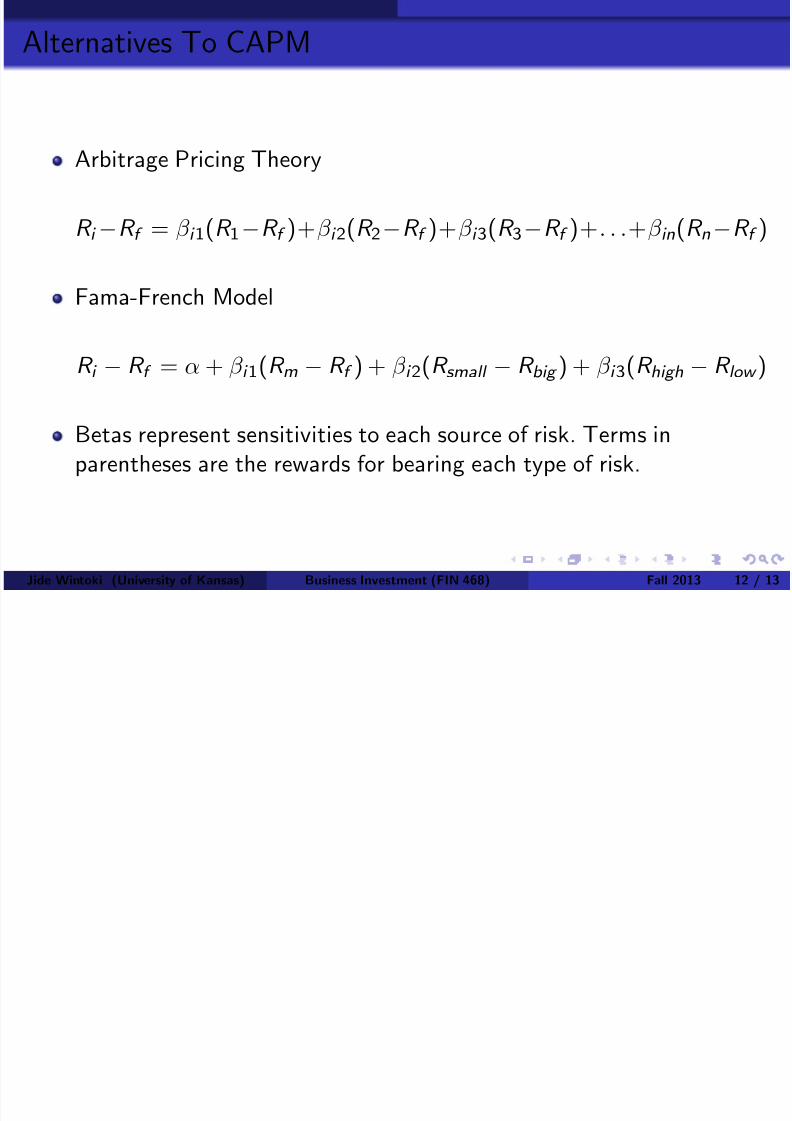

Alternatives To CAPM

Arbitrage Pricing Theory

R i −R f = β i 1(R 1−R f )+β i 2(R 2−R f )+β i 3(R 3−R f )+. . .+β in(R n−R f )

Fama-French Model

R i − R f = α + β i 1(R m − R f ) + β i 2(R small − R big ) + β i 3(R high − R low )

Betas represent sensitivities to each source of risk. Terms inparentheses are the rewards for bearing each type of risk.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 12 / 13

7/27/2019 CF Risk Return(2)

http://slidepdf.com/reader/full/cf-risk-return2 13/13

The Current State of APT

Investors demand compensation for taking risk because they are riskaverse.

There is widespread agreement that systematic risk drives returns.

You can measure systematic risk in several different ways dependingon the asset pricing model you choose.

The CAPM is still widely used in practice in both corporate finance

and investment-oriented professions.

Jide Wintoki (University of Kansas) Business Investment (FIN 468) Fall 2013 13 / 13