Embed Size (px)

Citation preview

Cost of Capital

=AssetValue

CF1

(1 + r)1

^+

CF2

(1 + r)2

^+ … +

CFn

(1 + r)n

^

r = firm’s required rate of return, which represents the return investors receive for providing funds to the firm

=AssetValue

CF1

(1 + r)1

^+

CF2

(1 + r)2

^+ … +

CFn

(1 + r)n

^

1

Chapter Essentials—The Questions

What types of capital do firms use to finance investments?

What is the cost of capital? How is the cost of capital used to make

financial decisions? Why do funds generated through

retained earnings have a cost? Who determines a firm’s cost of

capital?

2

Cost of Capital

Introduction

Cost of Debt, rdT

Cost of Equity, rps and (rs or re)

Marginal Cost of Capital (MCC)

MCC and Investment Opportunity (IOS) Schedules

3

Basic Definitions Capital—refers to the long-term funds used by a firm to

finance its assets. Capital components—the types of capital used by a firm—

long-term debt and equity Cost of capital—the cost associated with the various types

of capital used by the firm, which is based on the rate of return required by the investors who provide the funds to the firm.

Weighted average cost of capital, WACC—the average percentage cost, based on the proportion of each type of capital, of all the funds used by the firm to finance its assets.

Capital structure—the mix of the types of capital used by the firm to finance its assets.

Optimal capital structure—the mix of capital that minimizes the firm’s WACC, thus maximizes its value.

4

Weighted Average Cost of Capital (WACC)—Logic

A firm generally uses different types of funds to finance its assets—that is, debt and equity.

Costs associated with different types of capital (funds) usually are not the same—e.g., debt generally is cheaper than equity.

The overall cost, or average, should be weighted based on the proportion of each type of funds used by the firm.

Example: A firm is financed with debt and equity with the following characteristics:

Cost Proportion Debt rdebt =8% 10%

Equity rstock =12% 90%

The average cost of each dollar of financing is:

Weighted average = 8%(0.1) + 12%(0.9) = 11.6% 5

Cost of Capital

Investors who are the participants in the financial markets determine the firm’s costs of funds.

The firm’s costs of funds change when conditions in the financial markets change investors’ general risk aversion changes firm’s risk changes

6

Cost of Debt, rdT

rd—the before-tax cost of debt is simply the yield to maturity (YTM) of the debt

YTM—bondholders’ required rate of return = rd

rdT—the after-tax cost of debt

T)(1r Tr r

debt with associated

savingsTax

return of rate

required s'Bondholderr

ddd

dT

T = marginal tax rate

7

Cost of Debt, rdT—Example

A firm has debt with the following characteristics:Maturity value, M$1,000.00Coupon rate, C 8.0% (paid semiannually)Years to maturity 6 yrsMarket price $1,099.50Marginal tax rate 40.0%

Based on this information, we know that the following relationship exists:

12d

2d

1d

d)(1

$1,040

)(1

$40

)(1

$40$1,099.50 V

r

r

r

Solving for rd gives us the YTM for this bond

8

Cost of Debt, rdT—Example

Solve using: Trial-and-error process (numerical

solution) approximation equation

Financial calculator Spreadsheet

9

Cost of Debt, rdT—Example

rd approximation

2.97%0.0297$1,066.33

$31.71 $40

INT

maturity to yieldeApproximat

3$1,000 0)2($1,099.5

12$1,099.50 $1,000

3

M )2(V

N

V M

d

d

rd/2 = 2.97% per six-month period (interest payment)

rd = 2.97% x 2 = 5.94% ≈ 6%

10

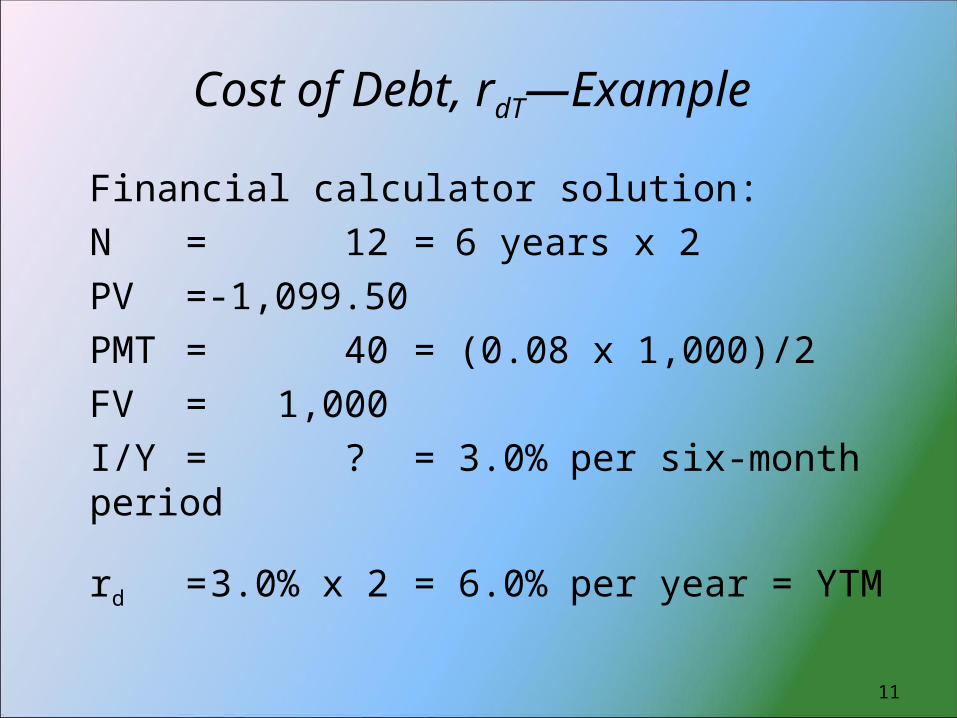

Cost of Debt, rdT—Example

Financial calculator solution:N = 12 = 6 years x 2 PV =-1,099.50PMT = 40 = (0.08 x 1,000)/2FV = 1,000I/Y = ? = 3.0% per six-month period

rd = 3.0% x 2 = 6.0% per year = YTM

11

Cost of Debt, rdT—Example

Bondholders/investors demand a 6 percent rate of return to invest in this firm’s long-term debt.

rd = YTM = 6% is the rate of return paid to bondholders.

The firm pays $80 interest per year, which is a tax deductible expense.

rd is a before-tax amount that needs to be adjusted so as to represent the actual after-tax cost to the firm—that is, the cost of the bond to the firm isn’t really 6 percent.

12

Cost of Debt, rT

Tax Deductibility of InterestExample: The firm issues a new $1,000 face value bond with a 6 percent coupon rate, thus interest equal to $60 is paid each year. If the firm’s taxable income before considering the interest payment is $500 and its marginal tax rate is 40 percent, then the tax liability with and without the interest expense is:

Tax without interest = $500(0.40) = $200Tax with interest = ($500 - $60)( 0.40) = $176

Savings = $24 = $60(0.4)

Net interest after tax savings = $60 - $24 = $36After-tax cost of the new bond = $36/$1,000 = 3.6%rdT = rd x (1 – T) = 6% x (1 – 0.4) = 3.6%

13

Cost of Debt, rdT

rdT = rd x (1 – T)rdT = rd x (1 – T)

= YTM x (1 – T)

rd = before-tax cost of debtT = marginal tax rate

14

Cost of Equity

The cost of equity is based on the rate of return required by the firm’s stockholders. Cost of preferred stock—dividends received by

preferred stockholders represent an annuity Cost of retained earnings (internal equity)—return

that common stockholders require the firm to earn on the funds that have been retained, thus reinvested in the firm, rather than paid out as dividends

Cost of new (external) equity—rate of return required by common stockholders after considering the cost associated with issuing new stock (flotation costs)

15

Cost of Equity—Preferred Stock

Most preferred stocks pay constant dividends, thus the dividend stream represents a perpetuity.

Valuing preferred stock as a perpetuity gives:

ps

ps0 r

D P

Solving for the required rate of return, rps, gives:

0

psps P

D r

Because flotation (issuing) costs have to be paid when preferred stock is issued, the cost of preferred stock is:

F) - (1P

D

NP

D r

0

ps

0

psps NP0= net proceeds from issue

F = flotation costs (percent)

16

Cost of Preferred Stock, rps—Example

A firm has preferred stock with the following characteristics:

Market price, P0 $75.00

Dividend, Dps $5.76

Flotation cost, F 4.0%

0.04) - $75.00(1

$5.76 rps

$72.00$5.76

= 0.08 = 8.0%

No tax adjustment, because dividends are not a tax-deductible expense.

17

Cost of Equity—Retained Earnings, rs

The firm must earn a return on reinvested earnings that is sufficient to satisfy existing common stockholders’ investment demands.

If the firm does not earn a sufficient return using retained earnings, then the earnings should be paid out as dividends so that stockholders can invest the funds outside the firm to earn an appropriate rate.

18

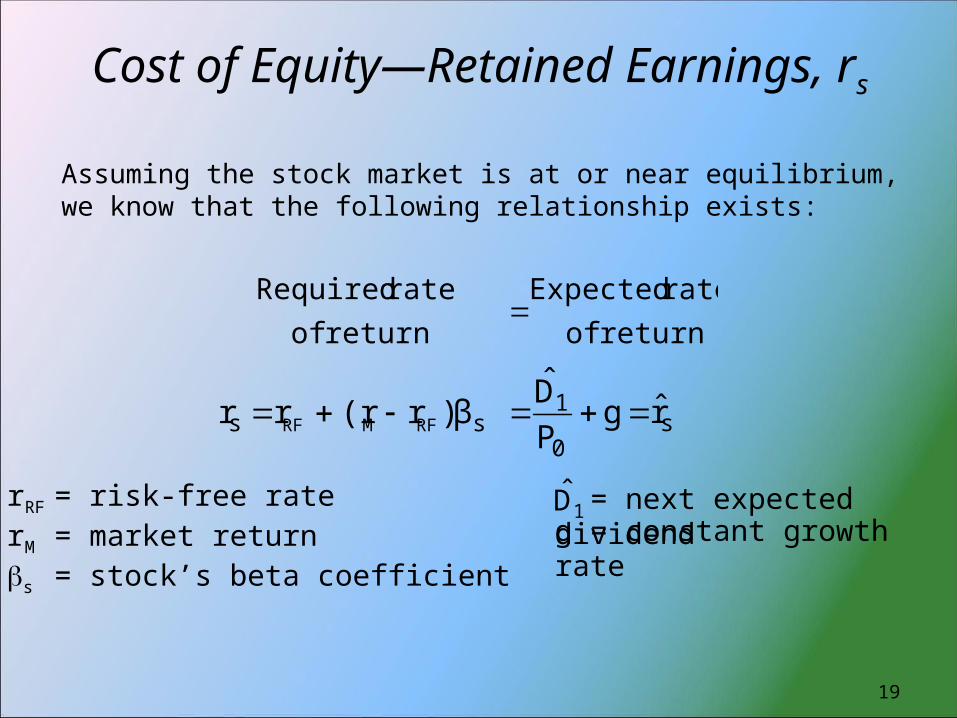

Cost of Equity—Retained Earnings, rs

Assuming the stock market is at or near equilibrium, we know that the following relationship exists:

return of

rate Expected

return of

rate Required

ss )β(r r RFMRF rr s0

1 rgPD ˆˆ

rRF = risk-free raterM = market returns = stock’s beta coefficient

= next expected dividend

1D̂g = constant growth rate

19

Cost of Retained Earnings, rs

CAPM Approach

Assumes the firm’s stockholders are very well diversified; if not, then beta probably is not the appropriate measure of risk for determining the firm’s cost of retained earnings.

rRF generally is associated with with Treasury securities; there are many different rates for Treasuries that have different terms to maturity.

ss )βr(r rr RFMRF

If rRF = 4%, rM = 9%, and s = 1.4

rs = 4% + (9% - 4%)1.4 = 11.0%

20

Cost of Retained Earnings, rs

Bond-Yield-Plus-Risk-Premium Approach

Studies have shown that the return on equity for a particular firm is approximately 3 to 5 percentage points higher than the return on its debt.

As a general rule of thumb, firms often compute the YTM, or rd, for their bonds and then add 3 to 5 percent.

In the current example, rd = 6.0%. As a rough estimate, then, we might say the cost of retained earnings is rs ≈ rd + 4% = 6% + 4% = 10.0%

21

Cost of Retained Earnings, rs

Discounted Cash Flow (DCF) Approach

If the firm is expected to grow at a constant rate, then we have the following relationship:

gain

Capital

yield

Dividendg

PD

rr0

1ss

ˆˆ

Example: The firm, which is growing at a constant rate of 5 percent, just paid a dividend equal to $1.20; its stock currently sells for $18.

0.05 $18.00

)$1.20(1.05 rs 0.05

$18.00$1.26

rs = 0.07 + 0.05 = 0.12 = 12.0%

22

Cost of Retained Earnings, rs

The three approaches we used to determine the cost of retained earnings give three different results.

The three approaches are based on different assumptions: CAPM approach assumes investors are extremely well

diversified DCF approach assumes the firms grows at a constant rate Bond-yield-plus-risk-premium approach assumes that the

return on equity is related to the return on the firm’s debt

Ideally all three approaches should give the same result; if not, however, we might average the results:

rs = (11% + 10% + 12%)/3 = 11%

23

Cost of EquityNewly Issued Common Stock, re

Rate of return required by common stockholders after considering the costs associated with issuing new stock, which are called flotation costs.

Because the firm has to provide the same gross return to new stockholders as existing stockholders, when the flotation costs associated with a common stock issue are considered, the cost of new common stock always must be greater than the cost of existing stock—that is, the cost of retained earnings.

Modify the DCF approach for computing the cost of retained earnings to include flotation costs

24

Cost of Newly Issued Common Stock (External Equity), re

NP0 = net proceeds from the sale of the stock

If flotation costs equal 6 percent, then re in our example is

gNPD

gF)(1P

Dr

0

1

0

1e

ˆˆ

0.05 0.06) $18(1

$1.26re

0.05

$16.92$1.26

12.45% 0.1245

25

Cost of Newly Issued Common Stock, re

Rationale

Assume a firm (different than in our example) has: total assets equal to $50,000 is financed with common stock only (5,000 shares) pays all earnings as dividends, thus g = 0 cost of retained earnings, rs = 10% = ROE

$1.00 5,000$5,000

D dividendCurrent

0

$5,000 10)$50,000(0. incomeCurrent

$10.00 0.10$1.00

P price,

stockCurrent

0

26

The firm sells new common stock: 800 shares, so that 5,800 shares are outstanding

after the sale market price, P0 = $10.00

net proceeds received by the firm, NP0 = $9.50

total amount received by the firm = $9.50 x 800 = $7,600

total assets after stock sale = $50,000 + $7,600 = $57,600

Cost of new equity, re

10.53% 0.1053 0 $9.50$1.00

re

Cost of Newly Issued Common Stock, re

Rationale

27

Total assets after stock sale = $57,600

If the firm earns rs = 10% on all investments

$0.9931 5,800$5,760

D dividend

New

$5,760 10)$57,600(0. incomeNew

$9.93 0.10

$0.9931

P price,stock New

0

Cost of Newly Issued Common Stock, re

Rationale

28

Total assets after stock sale = $57,600 If the firm earns re = 10.53% on new investments

$1.00 5,800$5,800

D dividend

New

sinvesmtent new

from Income

sinvestment existing

from Income Income

$5,800 053)$7,600(0.1 10)$50,000(0.

Stock price would remain at $10, because investors require a 10 percent return; but, the firm must earn 10.53 on new investments to generate 10 percent to investor (due to flotation costs)

Cost of Newly Issued Common Stock, re

Rationale

29

Weighted Average Cost of Capital, WACC

To make decisions about capital budgeting projects, we need to combine the various costs of capital—debt, preferred stock, and common stock—into a single required rate of return.

Weighted average cost of capital, or WACC—the weighted average of the component costs of capital using as the weights the proportion each type of financing makes up of the total financing of the firm.

)eror s(rsw psrpsw dTrdw

stock

preferred %

debt

%WACC

equity common

ofCost

equity

common %

stock preferred

ofCost

debt ofcost

tax-After

30

Weighted Average Cost of Capital, WACC

Suppose our illustrative firm has the following capital structure:

Debt, d 40.0Preferred stock, ps 10.0Common equity, s 50.0

100.0

3.6%8.0

11.0 or 12.45

PercentType of Financing of total

Percent After-TaxType of Financing of total Cost, r

If the firm can use retained earnings to finance new projects

WACC = 0.4(3.6%) + 0.1(8.0%) + 0.5(11.0%) = 7.74%

If the firm has to issue new common stock to finance new projects

WACC = 0.4(3.6%) + 0.1(8.0%) + 0.5(12.45%) = 8.47%

31

Marginal Cost of Capital, MCC

Weighted average cost of raising additional funds.

Generally, MCC often is greater than the existing WACC—that is, the cost of new funding increases—because the firm’s risk increases, which causes investors to

require a higher rate of return

costs of issuing new funds increase

MCC schedule—a graph that shows the average cost of funds at various levels of new financing

32

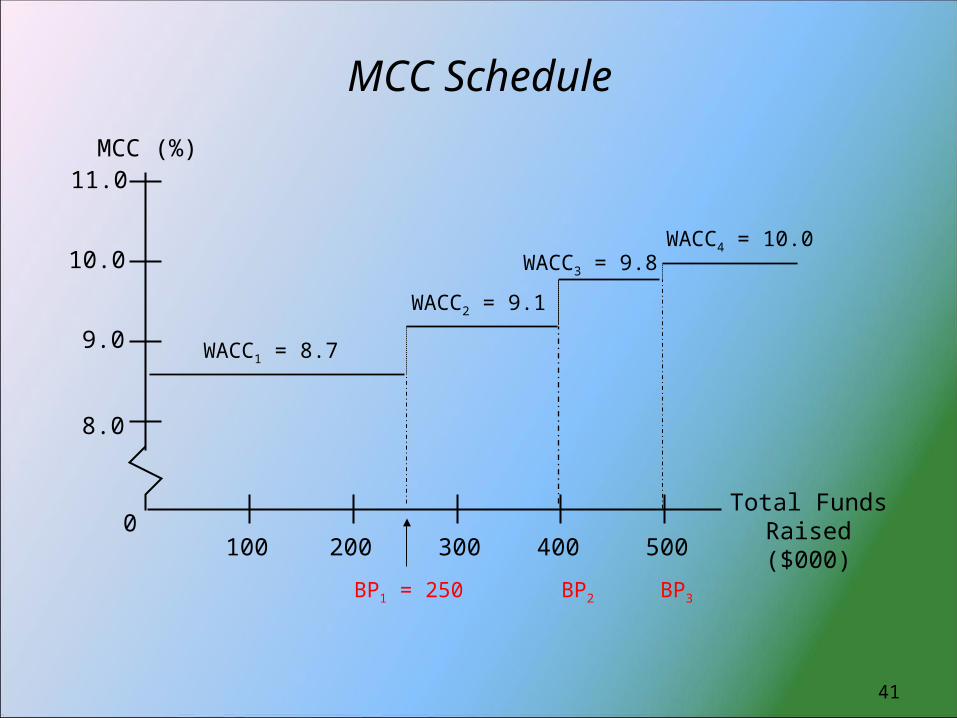

MCC Schedule

If the firm expects to retain $200,000 this year

400,000

7.7

Total of New Funds Raised ($)0

New WACC =MCC (%)

WACC1

CE = 400,000 x 0.5 = 200,000

8.5WACC2

BreakPoint

33

MCC Schedule—Break Points

Break points occur when WACC increases, which is caused by an increase in any of the component costs of capital

debt—when rd1 < rd2 < … < rdn

preferred stock—when rps1 < rps2 < … < rpsn

common equity—retained earnings or new common stock There is a break point when retained earnings generated in

the current period is exhausted.

Once the current addition to retained earnings is exhausted, then the firm must issue new common stock to satisfy additional common equity financing requirements.

Costs of funds often increase as the firm uses significantly higher amounts—risk increases.

34

MCC Schedule—Break Points

structure capital the in capital of type this of Proportioncostlower theat capital of type given a ofamount Total

pointBreak

$400,000 0.50

$200,000

equity common of Proportionearnings Retained

35

MCC Schedule Break Points—Example

Assume the firm faces the following situation this year: Debt (40%):

Amount of Funds Cost of Debt, rdT

$ 0 - $100,000 6.0%

100,001 - 200,000 6.5

200,001 - 7.0 Preferred Stock (10%): rps = 8.0%, no matter the amount

needed Common Equity (50%):

Retained earnings generated during the year = $200,000 Cost of retained earnings (internal equity), rs = 11.0%

Cost of new common stock (external equity), re = 12.4%, no

matter how much is needed

36

MCC Schedule Break Points—Example

Debt (40%): Amount of Funds Cost of Debt, rdT

$ 0 -$100,000 6.0%100,001 - 200,000 7.0200,001 - 7.5

$250,000 0.40

$100,000

PointBreak

debt1

$500,000 0.40

$200,000

PointBreak

debt2

If the firm needs total funds equal to $250,000, 40%, or $100,000 would be debt.

If the firm needs total funds equal to $500,000, 40%, or $200,000 would be debt.

37

MCC Schedule Break Points—Example

Preferred Stock (10%): rps = 8.0%, no matter the amount

needed

Constant cost—no break due to preferred stock Common Equity (50%):

Retained earnings generated during the year = $200,000 Cost of retained earnings (internal equity), rs = 11.0%

Cost of new common stock (external equity), re = 12.4%, no

matter how much is needed

$400,000 0.50

$200,000

PointBreak

RE

If the firm needs total funds equal to $400,000, 50%, or $200,000 would be RE.

38

MCC Schedule—Example

Funds = $0 - $250,000Amount at After-Tax $250,000 Weight x Cost, k = WACC

DebtPreferred StockCommon Equity

Funds = $250,001 - $400,000Amount at After-Tax $400,000 Weight x Cost, r = WACC

DebtPreferred StockCommon Equity

$100,00025,000

125,000250,000

0.4

0.1

0.5

1.0

2.40.85.58.7%= WACC1

$160,00040,000

200,000400,000

0.4

0.1

0.5

1.0

6.0

8.0

11.0

7.0

8.0

11.0

2.80.85.59.1%= WACC2

Funds = $0 - $250,000Amount at After-Tax $250,000 Weight x Cost, r = WACC

DebtPreferred StockCommon Equity

39

Funds = $400,001 - $500,000Amount at After-Tax $500,000 Weight x Cost, k = WACC

DebtPreferred StockCommon Equity

Funds = above $500,000Amount at After-Tax $600,000 Weight x Cost, r = WACC

DebtPreferred StockCommon Equity

$200,00050,000

250,000500,000

0.4

0.1

0.5

1.0

2.80.86.29.8%= WACC3

$240,00060,000

300,000600,000

0.4

0.1

0.5

1.0

7.0

8.0

12.4

7.5

8.0

12.4

3.00.86.2

10.0%= WACC4

Funds = $400,001 - $500,000Amount at After-Tax $500,000 Weight x Cost, r = WACC

DebtPreferred StockCommon Equity

MCC Schedule—Example

40

MCC Schedule

BP1 = 250

400

Total Funds Raised ($000)0

MCC (%)

300200100 500

8.0

9.0

10.0

11.0

WACC1 = 8.7

WACC2 = 9.1

WACC3 = 9.8WACC4 = 10.0

BP2 BP3

41

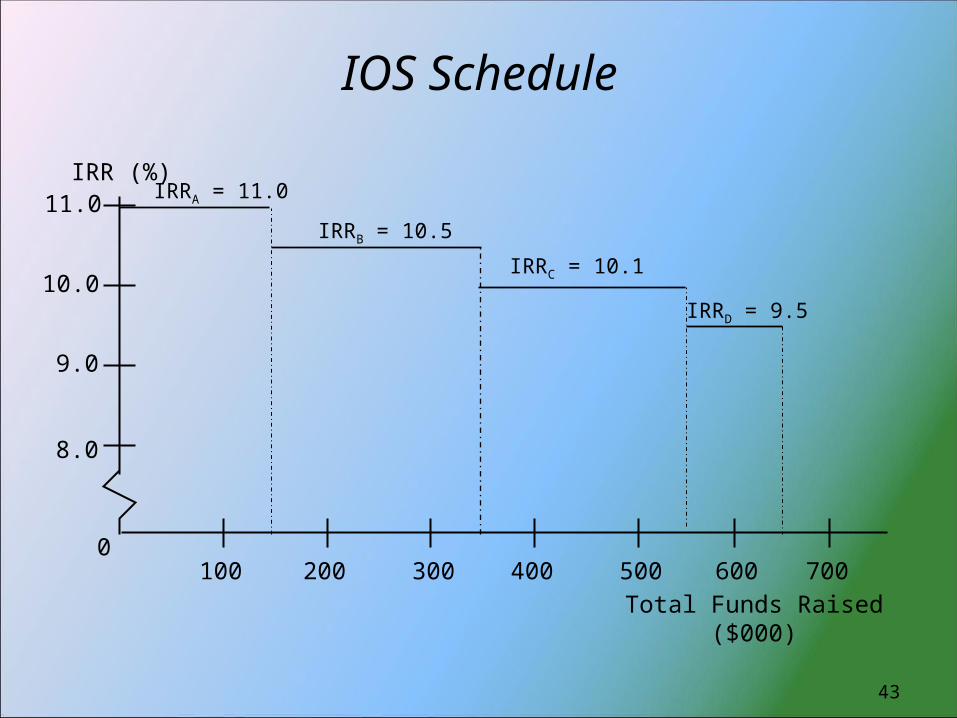

MCC Schedule and Investment Opportunity (IOS) Schedule

The firm’s capital budgeting analysis results are:

Project Cost IRR A $150,000 11.0%B 200,000 10.5C 200,000 10.1D 100,000 9.5

42

IOS Schedule

400Total Funds Raised

($000)

0

IRR (%)

300200100 500

8.0

9.0

10.0

11.0

600 700

IRRA = 11.0

IRRB = 10.5

IRRC = 10.1

IRRD = 9.5

43

MCC Schedule

400

Total Funds Raised ($000)0

MCC (%)

300200100 500

8.0

9.0

10.0

11.0

WACC1 = 8.7

WACC2 = 9.1

WACC3 = 9.8WACC4 = 10.0

44

MCC & IOS Schedules

400Total Funds Raised

($000)

0

IRR

/MC

C (

%)

300200100 500

8.0

9.0

10.0

11.0

600 700

IRRA = 11.0

IRRB = 10.5

IRRC = 10.1

IRRD = 9.5

Optimal CapitalBudget = 550

WACC1 = 8.7

WACC2 = 9.1

WACC3 = 9.8

WACC4 = 10.0

45

What types of capital do firms use to finance investments? Either debt (bond issues) or equity

(preferred stock and common equity)

What is the cost of capital? The average price a firm pays for the funds

it uses to purchase assets

How is the cost of capital used to make financial decisions? A firm should invest in projects that are

expected to provide returns greater than its WACC

Chapter Essentials—The Answers

46

Why do funds generated through retained earnings have a cost? Firms may retain earnings only as long as

it can reinvest the earnings at a higher rate than stockholders can earn elsewhere

Who determines a firm’s cost of capital? Investors

Chapter Essentials—The Answers

47

![Flag Control instructions CLC clear carry flag CF = 0 STC set carry flag CF= 1 CMC complement carry flag [CF] CF](https://img.pdfslide.us/doc/110x75/56649e925503460f94b97808/flag-control-instructions-clc-clear-carry-flag-cf-0-stc-set-carry-flag-cf.jpg)