Embed Size (px)

Citation preview

Centre for Administrative Science Faculty of Social and Political Science

University of Indonesia

a

Income Tax on Oil and Gas Industry in Indonesia

(Law No. 22/2001)

South- South Sharing of Successful Tax Practices

LAW No. 22/2001

Upstream Industry

Downstream Industry

Exploration

Exploitation

Processing

Trasportation

Storage

Retail

Exploration : Any activities aimed at obtaining information on geological data to find hydrocarbon deposit and estimation of its reserve.

Explotation Activities:o Drilling & Well Cementingo Construction of Transport Infrastructureso Processing (including refinery)

Upstream Industry; can only be carried out by:o A business entity; oro A permanent establishment

Provision in Indonesia Oil and Gas Law (art 10):o A business entity/Permanent Establishment

(PE) that is engaged in the upstream industry is prohobited to engage in downstream industry

oA business entity that is engaged in the downstream industry is not allowed to conduct business in the downstream industry

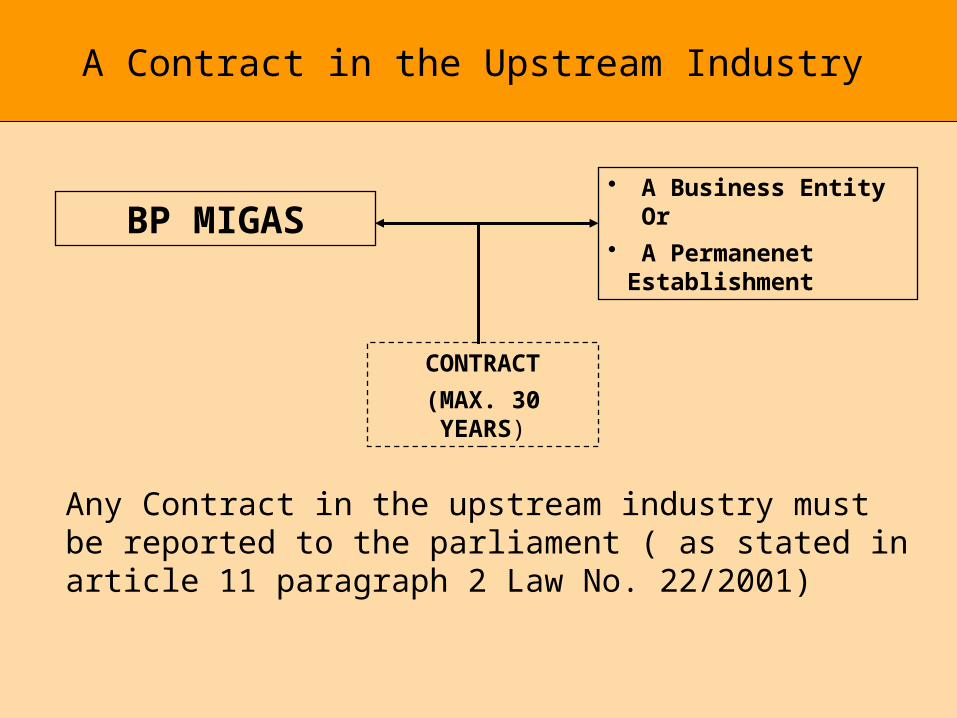

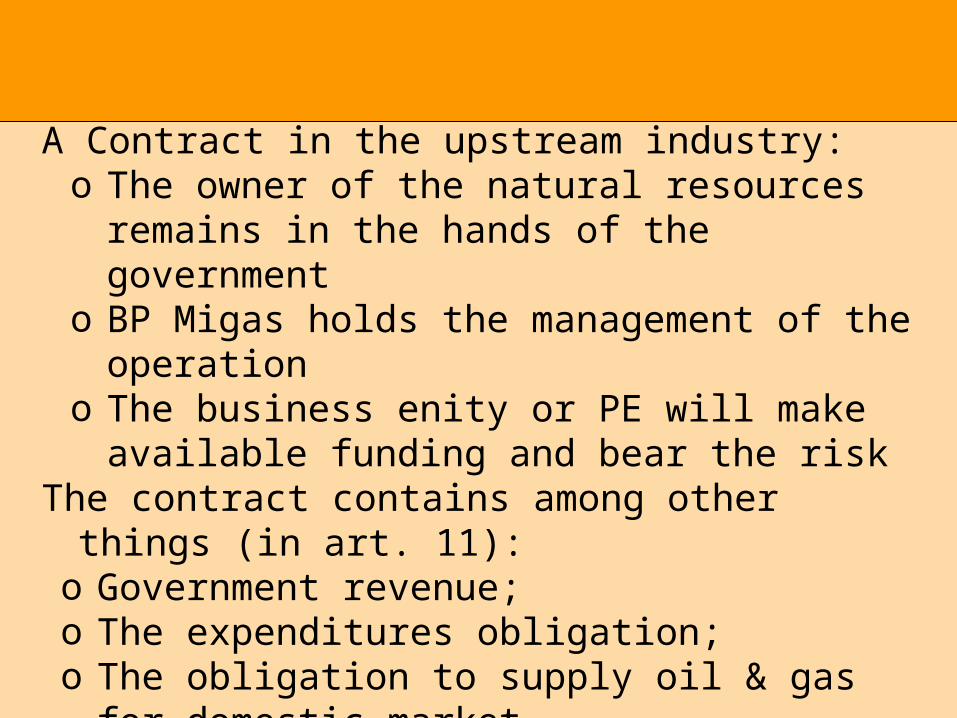

A Contract in the Upstream Industry

BP MIGAS• A Business Entity Or• A Permanenet

Establishment

CONTRACT

(MAX. 30 YEARS)

Any Contract in the upstream industry must be reported to the parliament ( as stated in article 11 paragraph 2 Law No. 22/2001)

A State Owned Legal Entity

BP MIGAS

The budget for its operation is based on fee

from the government

A Contract in the upstream industry:o The owner of the natural resources remains in the

hands of the governmento BP Migas holds the management of the operationo The business enity or PE will make available

funding and bear the riskThe contract contains among other things (in art. 11):o Government revenue;o The expenditures obligation;o The obligation to supply oil & gas for domestic

marketo The transfer of rights and obligationo Reporting requirements

The applicable tax laws and their implementing regulations go into effect at the time the contract was signed, OR, the laws and their implementing regulations currently in force.

Tax Revenue

Tax Revenue

TaxesCustoms and Excise on

ImportLocal Taxes and Retribution

Non Tax Revenue

State’s SharesDead Rent & Exploitation

and Exploration feesBonuses

Income Tax Treatment

Exploration Period

Lasts for 6 years, can be extended

for another 4 years

Exploration Cost (Pre-Production

Cost)

Income Tax Treatment

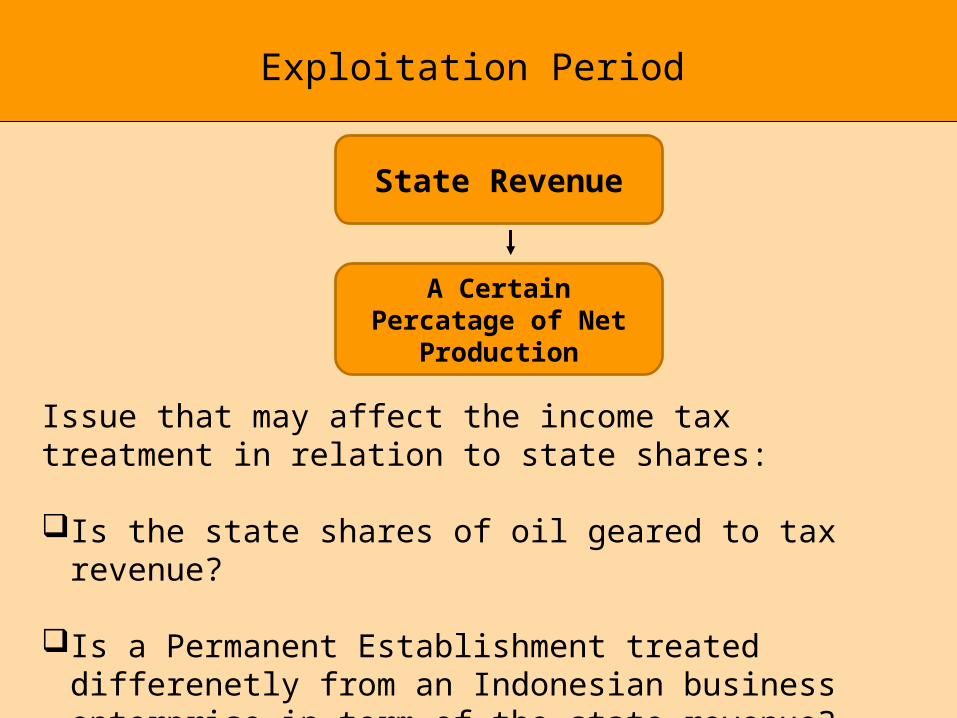

Exploitation Period

State Revenue

A Certain Percatage of Net Production

Issue that may affect the income tax treatment in relation to state shares:

Is the state shares of oil geared to tax revenue?

Is a Permanent Establishment treated differenetly from an Indonesian business enterprise in term of the state revenue?

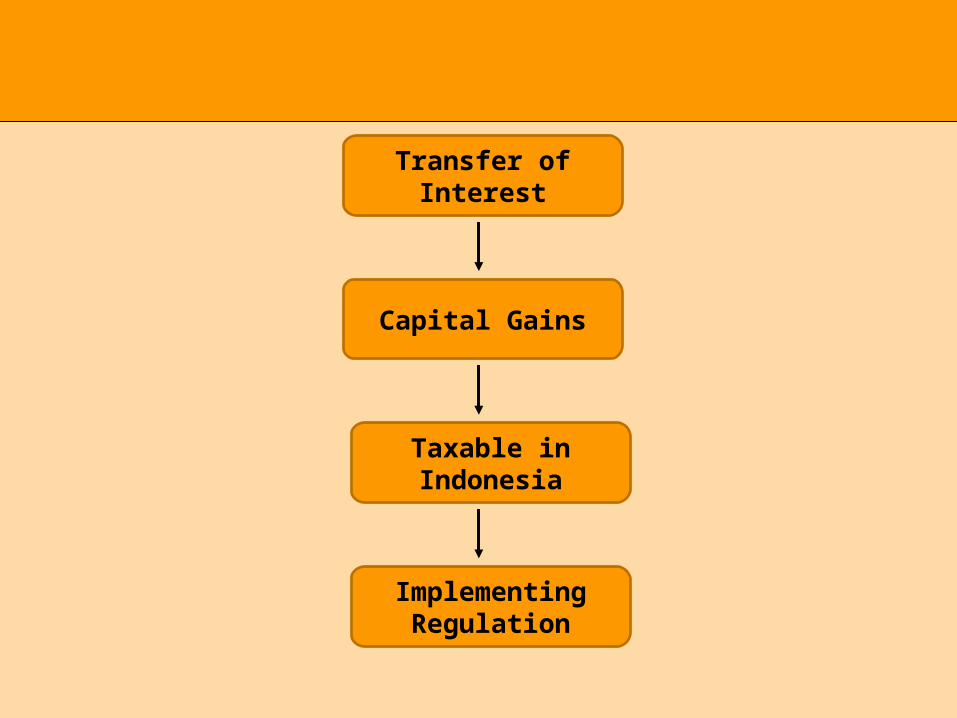

Transfer of Interest

Capital Gains

Taxable in Indonesia

Implementing Regulation

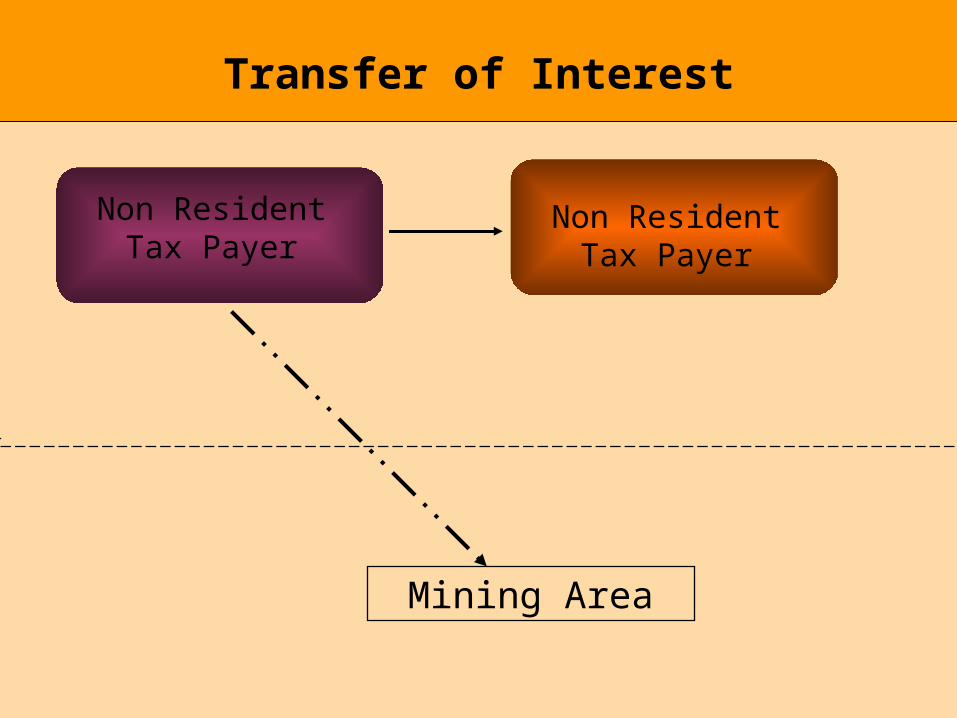

Transfer of Interest

Non Resident Tax Payer

Mining Area

Non Resident Tax Payer

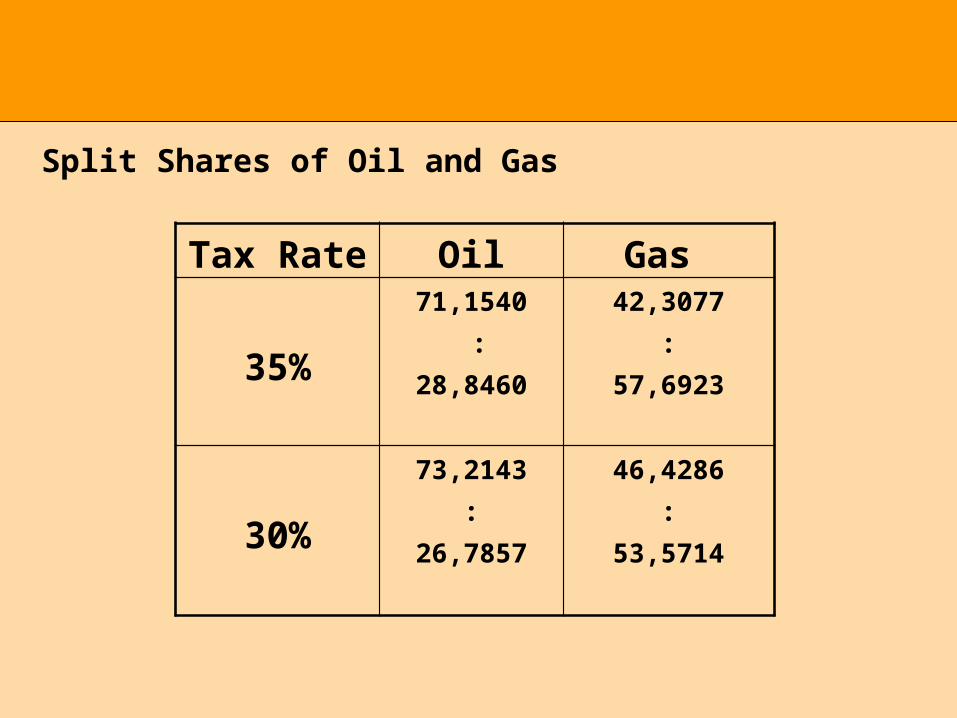

Split Shares of Oil and Gas

Tax Rate Oil Gas

35%

71,1540 :

28,8460

42,3077:

57,6923

30%

73,2143:

26,7857

46,4286:

53,5714

International Tax Aspects

Ring Fencing PolicyDeductibles Expenses of A Permanent

EstablishmentCapital GainsBranch Profit TaxExpatriate’s Income Tax

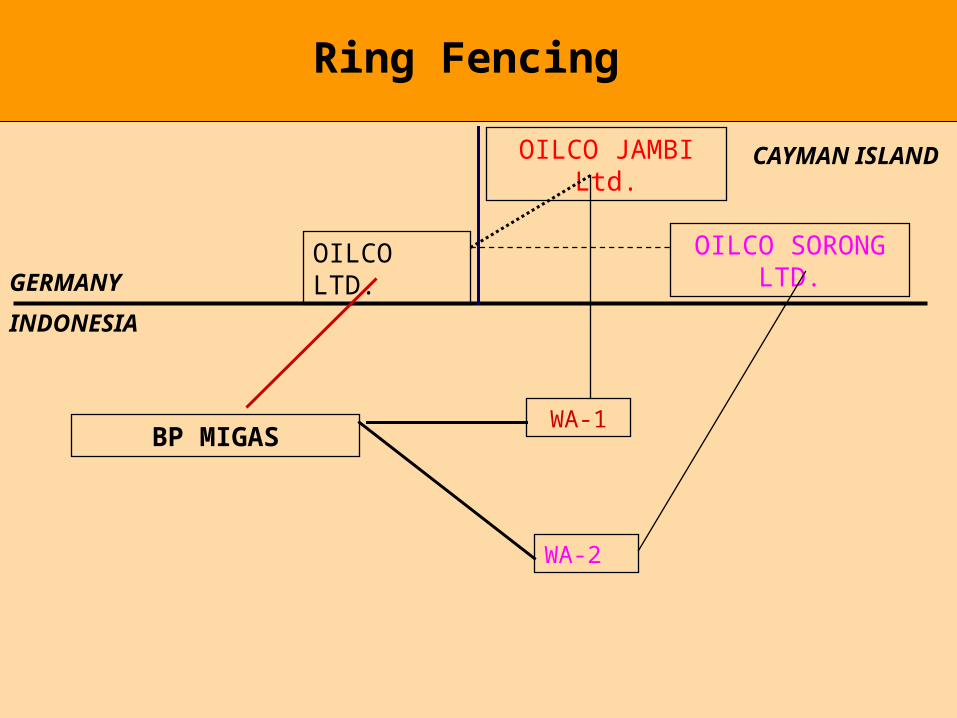

Ring Fencing

GERMANY

INDONESIA

OILCO LTD.

WA-1

WA-2

BP MIGAS

CAYMAN ISLANDOILCO JAMBI Ltd.

OILCO SORONG LTD.

Ring Fencing

GERMANY

CAYMAN ISLAND

OILCO LTD. OILCO JAMBI

WORKING AREA-1TAX ISSUES:

• PE OF OILCO LTD.

• WITHHOLDING BY OILCO JAMBI

• VAT

INDONESIA

DESPATCH OF PERSONNEL

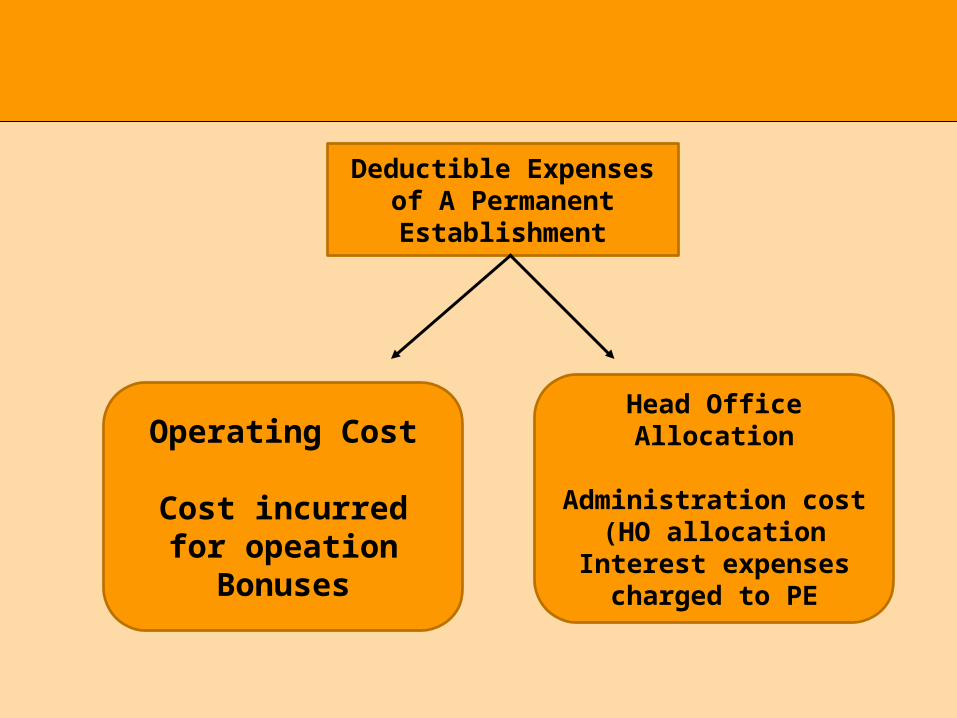

Deductible Expenses of A Permanent Establishment

Head Office Allocation

Administration cost (HO allocation

Interest expenses charged to PE

Operating Cost

Cost incurred for opeationBonuses

Operating Cost (OECD Model Article 7)

“ In Determining the profits of a Permanent Establishment, there shall be allowed as deduction expenses which are incurred for the purpose of the permanent establishment, including executive and general administrative expenses so incurred whether in the state in which the permanent establishment is situated

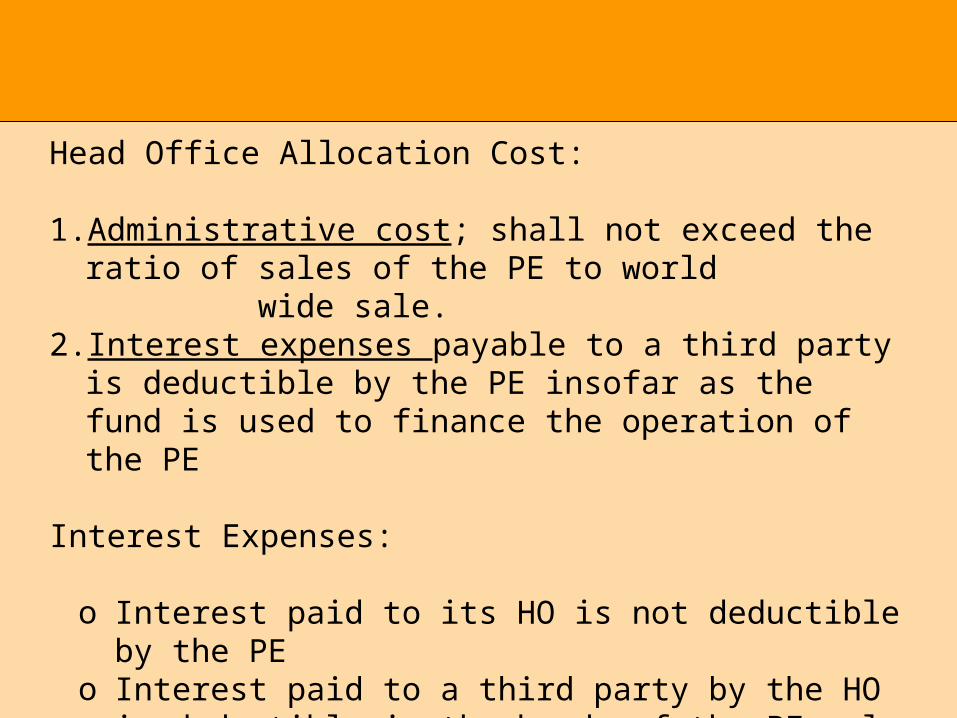

Head Office Allocation Cost:

1. Administrative cost; shall not exceed the ratio of sales of the PE to world wide sale.

2. Interest expenses payable to a third party is deductible by the PE insofar as the fund is used to finance the operation of the PE

Interest Expenses:

o Interest paid to its HO is not deductible by the PEo Interest paid to a third party by the HO is deductible in

the hands of the PE only if the fund is used for the purpose of the operation of the PE

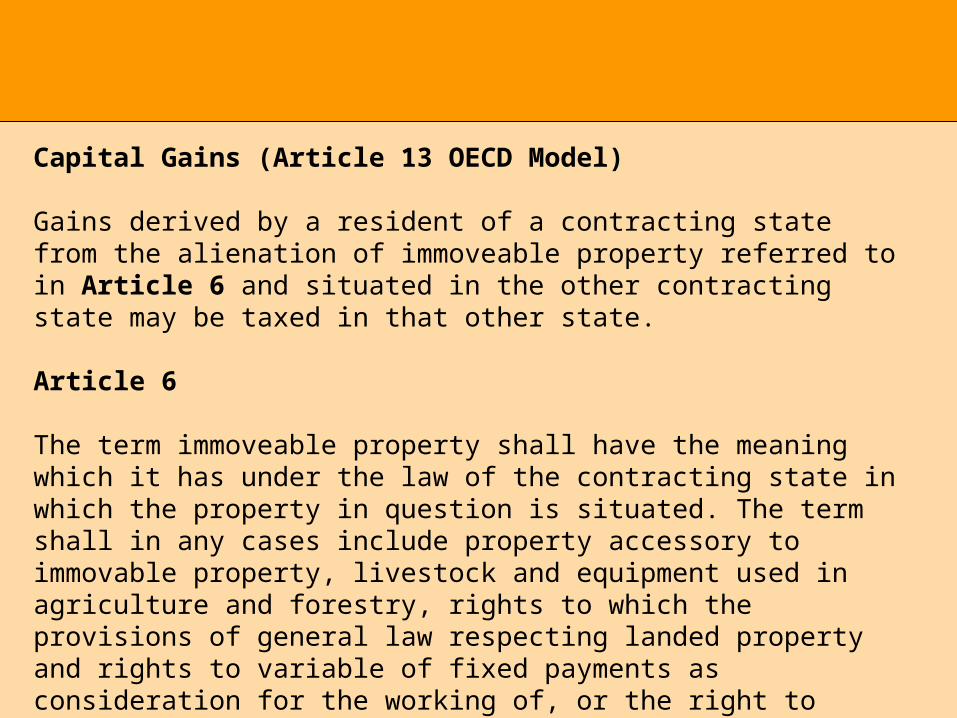

Capital Gains (Article 13 OECD Model)

Gains derived by a resident of a contracting state from the alienation of immoveable property referred to in Article 6 and situated in the other contracting state may be taxed in that other state.

Article 6

The term immoveable property shall have the meaning which it has under the law of the contracting state in which the property in question is situated. The term shall in any cases include property accessory to immovable property, livestock and equipment used in agriculture and forestry, rights to which the provisions of general law respecting landed property and rights to variable of fixed payments as consideration for the working of, or the right to work, mineral deposits, source and other natural resources, ships, boats and aircrafts shall bot be regarded as immoveable property

CAPITAL GAINS

USA

CAYMAN ISLANDOILCO LTD. OILCO JEPARA

WORKING AREA-1INDONESIA

OILCO JEPARA TRANSFERS OF ITS

INTEREST WORKING AREA-1 TO OTHER

PARTY

ISSUES:

• THE IMPLEMENTING REGULATIONS TO TAX

THE GAINS

• TAX BASE

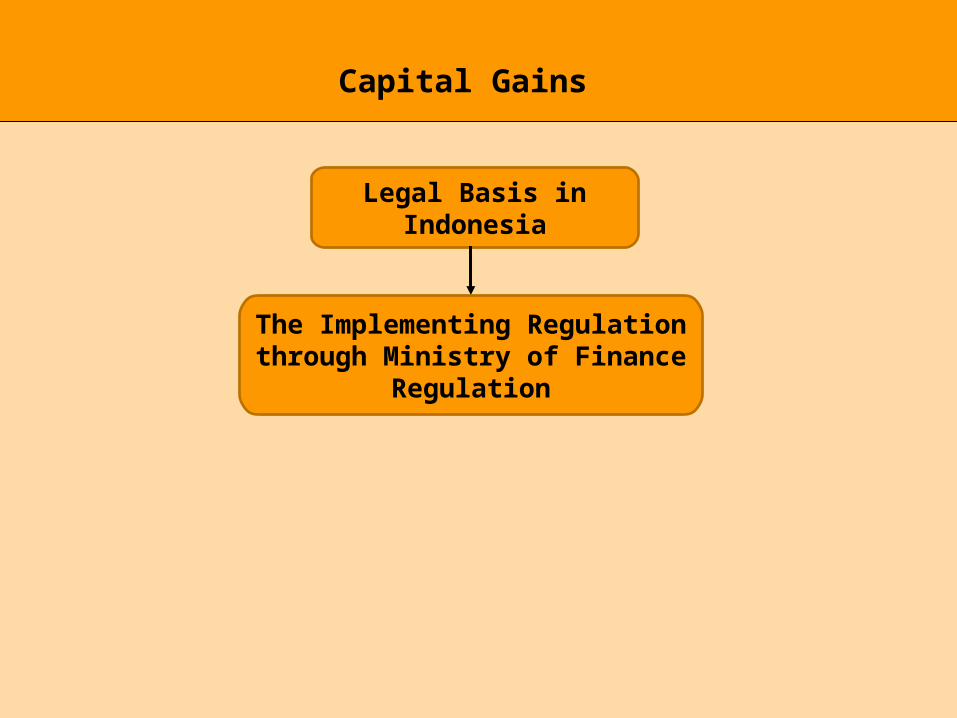

Capital Gains

Legal Basis in Indonesia

The Implementing Regulation through Ministry of Finance

Regulation

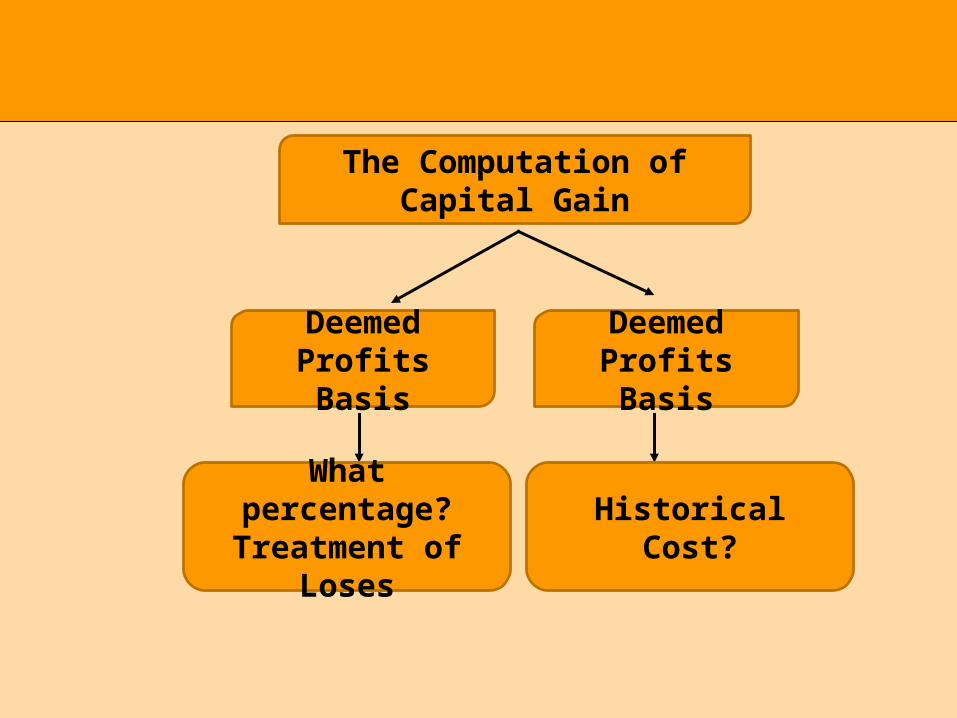

The Computation of Capital Gain

Deemed Profits Basis

Deemed Profits Basis

What percentage?Treatment of Loses

Historical Cost?

BRANCH PROFIT TAX

GENERAL POLICY UNDER LAW NO. 8/1971:

THE REDUCED RATE OF BPT IN THE TREATY DOES NOT APPLY TO

PSC IN OIL AND GAS

SOME OF THE DTA-s DO NOT PROTECT THE PSC FROM REDUCED RATE

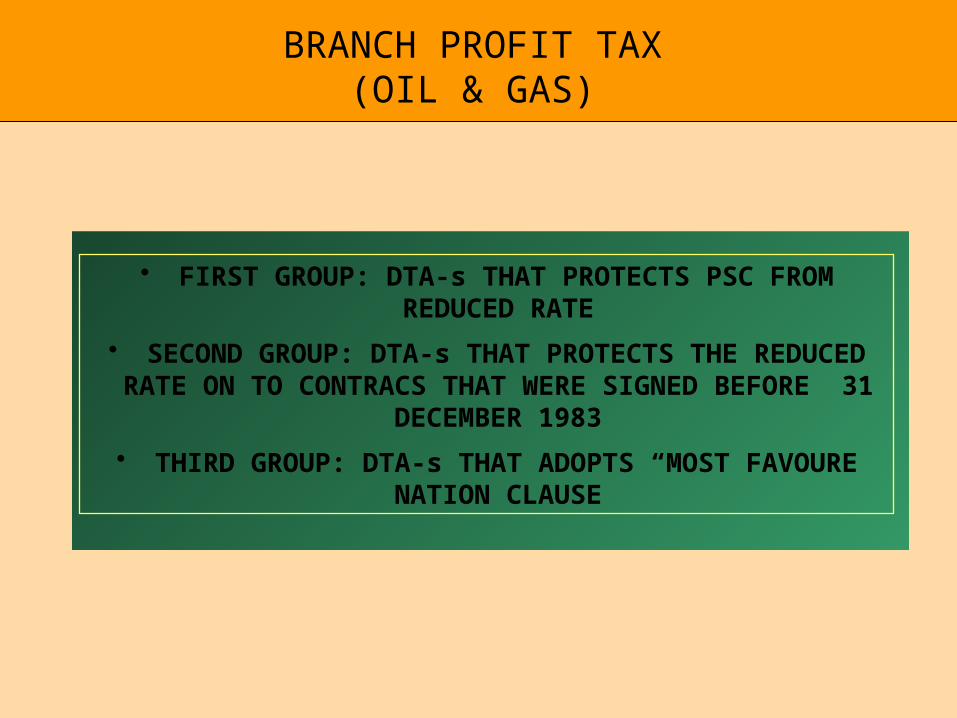

BRANCH PROFIT TAX(OIL & GAS)

• FIRST GROUP: DTA-s THAT PROTECTS PSC FROM REDUCED RATE

• SECOND GROUP: DTA-s THAT PROTECTS THE REDUCED RATE ON TO CONTRACS THAT WERE SIGNED BEFORE 31

DECEMBER 1983

• THIRD GROUP: DTA-s THAT ADOPTS “MOST FAVOURE NATION CLAUSE

Branch Profit Tax 1st Group

DTA-s• Australia, Austria,

Bulgaria, Czech Republic, Hungary, Luxemburg, Philipines, Poland, Rep of South Africa, Sudah, Syria, Taiwan, Tunisia, United Arab Emirates, Ukraine, USA, Uzbekistan, Venezuela, Vietnam

Branch Profit Tax 2nd Group

DTA-s

• Belgium, Canada, Denmark, Finlandia, India, Italy, Rep of Korea, Netherland, Norway, Pakistan, Romania, Spain, Sweden, Switzerland, UK, Germany, France

Branch Profit Tax 3rd Gup

DTA-s

• Japan• Malaysia• Singapore

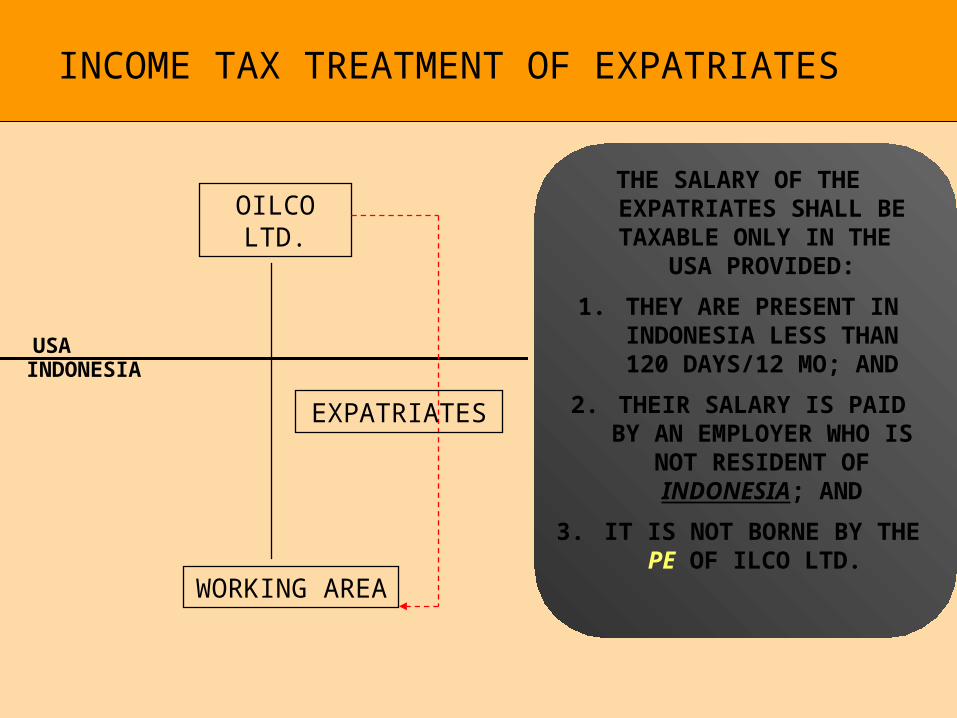

INCOME TAX TREATMENT OF EXPATRIATES

USAINDONESIA

OILCO LTD.

WORKING AREA

EXPATRIATES

THE SALARY OF THE EXPATRIATES SHALL BE TAXABLE ONLY IN THE

USA PROVIDED:

1. THEY ARE PRESENT IN INDONESIA LESS THAN 120

DAYS/12 MO; AND

2. THEIR SALARY IS PAID BY AN EMPLOYER WHO IS

NOT RESIDENT OF INDONESIA; AND

3. IT IS NOT BORNE BY THE PE OF ILCO LTD.