Embed Size (px)

Citation preview

ANNUAL REPORT 2009

Centre for Actuarial Studies

Contents

2 mascos annual report 2008

The Year in Review .......................................................................... 3

Teaching............................................................................................ 5

Student Prize Winners ..................................................................... 6

PhD Students and Research Topics ................................................. 6

Publications and Other Research Activities in 2009 ..................... 7

Research Paper Series ...................................................................... 9

Staff and Advisory Board .............................................................. 13

The main activities of the Centre for Actuarial Studies areteaching future actuaries, research and knowledge transfer.The Centre is proud of the high achieving students it attractsand strives to give them the best preparation for actuarialand other quantitative work. Because it is fully accredited bythe Institute of Actuaries of Australia, the Centre forActuarial Studies allows its students to obtain exemptionsfrom the whole of Parts I and II of the actuarialexaminations. With regard to research, the members of theCentre are experts in their fields and are internationallyrecognised for their work in actuarial science, financialmathematics and related disciplines. The Centre has sevenfull-time academic staff and a number of part-time lecturersfrom the actuarial profession (the complete list is at the endof this report).

The new degree of Master of Actuarial Science was createdin 2009, and will come into existence in 2011. In 2009 theCentre saw an increase in the number of students, whileresearch output remained at a good level.

Staff NewsDaniel Dufresne became Director of the Centre in 2009,after David Dickson stepped down at the end of 2008.

Ping Chen joined the Centre for Actuarial Studies as Lecturerin September, having just completed her PhD in ActuarialScience at the University of Hong Kong.

Shuanming Li was promoted from Senior Lecturer toAssociate Professor, effective at the beginning of 2010.

David Dickson was appointed as an editor of the ASTINBulletin, having previously served on its Editorial Board.David was on long service leave for nine weeks in the middleof the year.

David Pitt was appointed as an associate editor of theAustralian Actuarial Journal.

Student RecruitmentOverall enrolments were up slightly from their 2008 level.Enrolments at the 3rd year level were very good, and 37students completed the Honours year. Details of enrolmentsare shown on page 5.

David Pitt and Richard Fitzherbert ran three classes in theMelbourne Schools Partnership International Program forhigh achieving Year 11 students. These were very wellattended with over 100 students learning about theActuarial Studies Program at Melbourne.

The Centre’s promotional activities included other schoolvisits by David Dickson and David Pitt.

TeachingDavid Dickson and Mr Mike Pottenger, Department ofEconomics, were awarded a Faculty Teaching Innovation,Application and Staff Development Grant of just over$25,000 for a project entitled “E-learning and collaborativelearning in business statistics”. David is teaching the subjectQuantitative Methods for Business, which is a core subjectin the Faculty’s Master of Management degree.

David Pitt and Xueyuan Wu were awarded a teaching grantof $10,000 for a project entitled “Development of acapstone subject in Actuarial Studies“.

Teaching was supported by a number of external lecturersincluding Mr Richard Fitzherbert (for Financial MathematicsI and II), Mr Donald Campbell, Dr Jules Gribble, Mr DavidHeath, Mr Cary Helenius and Dr Allen Truslove (for ActuarialPractice and Control I and II).

New Master in Actuarial ScienceThe Master of Actuarial Science degree will commence in2011. This two-year program will consist of 16 subjects (8core plus 8 elective subjects) and will provide actuarialeducation for graduates who have mathematical orstatistical specialisations (e.g. in commerce, mathematics,physics or engineering). The course enables students whoobtain a sufficiently high pass to receive exemptions fromthe professional actuarial examinations conducted by theInstitute of Actuaries of Australia and the Institute ofActuaries (UK), as is already the case for our undergraduateprogram. The program director is Professor David Dickson.Further information about this new degree is availableonline at http://www.melbournegsm.unimelb.edu.au/programs/actuarial-studies/master-of-actuarial-science.html.

University of Melbourne Actuarial AlumniDavid Dickson hosted an actuarial alumni evening inSingapore in May that was attended by 15 graduates from1999 to 2008.

Research Areas and PublicationsResearch continued in a variety of areas including appliedprobability, disability income insurance, financialmathematics, investments, market models and risk theory.Staff continue to publish in top journals and to present theirwork at seminars and conferences around the world. TheCentre holds the Joint Seminar Series on StochasticProcesses and Financial Mathematics, in collaboration withthe Department of Mathematics and Statistics.

Details of publications and additions to the Centre’sResearch Paper Series can be found at the end this report.

The Year in Review

centre for actuarial studies | annual report 2009 3

Research GrantsSeveral members of the Centre have ongoing grants fromthe Australian Research Council. Staff who obtained newgrants in 2009 are: David Pitt and Yan Wang (RMIT),Australian Actuarial Research Grant of $13,588 for theirproject “Claim termination for income protection insuranceand data mining”; Xueyuan Wu and Shuanming Li,Australian Actuarial Research Grant of $7,000 for theirproject “On the recursive evaluation of aggregate claims fora large family of claim number distributions”. Both grantsare funded by the Institute of Actuaries of Australia.

VisitorsProfessor David Stanford, from the Department of Statisticsand Actuarial Science at the University of Western Ontario,visited the Centre in February. David gave a talk entitled“Perturbed Risk Processes Analysed as Fluid Flows”.

Professor Peter Cerone from Victoria University visited theCentre from February to July.

A group of academics from the Central University of Financeand Economics, China, visited the Centre in August,including Professor Cunwen Tao, Associate Professors LijunGuo and Jingfeng Xu, and Dr. Sujin Zheng, all from theDepartment of Actuarial Science, School of Insurance.

Professor Jiadong Tong and Professor Junyi Guo fromNankai University, China, visited the Faculty and the Centrefor Actuarial Studies in December for discussions about ajoint Masters degree in Actuarial Science, to be taught inTianjin and in Melbourne.

Student exchange again took place with the Department ofActuarial Mathematics and Statistics at Heriot-WattUniversity, with two Melbourne students returning in Julyand two departing in September to spend a year inEdinburgh.

Knowledge TransferDavid Dickson co-authored a textbook with Mary Hardy(University of Waterloo, Canada) and Howard Waters(Heriot-Watt University, Edinburgh) entitled “ActuarialMathematics for Life Contingent Risks”, published byCambridge University Press.

Mark Joshi is an administrator of the xlw open-sourceproject, which released version 4.0 in 2009. This projectprovides a mechanism for the automatic integration of newfunctions into EXCEL, and is widely used in the bankingindustry to provide a user-friendly front-end for pricingmodels. The 4.0 release achieves new levels of user-friendliness by providing template projects that make it evenfaster for a new user to get started. Its functionality is alsoextended to encompass C# and VB.net as well as C++.

Mark Joshi continued to contribute to the QuantLib opensource derivatives pricing library and gave a training courseon it and the LIBOR market model with MoneyScience at theInstitute of Physics in London in February.

During the year the members of the Centre acted as refereesfor a wide variety of academic and professional journals(listed later in this report).

Professional ActivitiesDavid Dickson is an external examiner for the actuarialprogram at Nanyang Business School, Singapore, and alsoindependent examiner for the UK actuarial profession.

AwardsPing Chen was awarded the Best Demonstrator Award bythe Department of Statistics and Actuarial Science, TheUniversity of Hong Kong.

David Dickson and Shuanming Li were each awarded aDean’s Certificate for Research Excellence for 2009.

Shuanming Li was awarded a Dean’s Certificate for TeachingExcellence for 2009.

David Pitt was awarded an ALTC Citation by the AustralianLearning and Teaching Council. This is an outstandingachievement at the national level. He was also awarded aDean’s Certificate for Teaching Excellence for 2009.

The Year in Review

4 centre for actuarial studies | annual report 2009

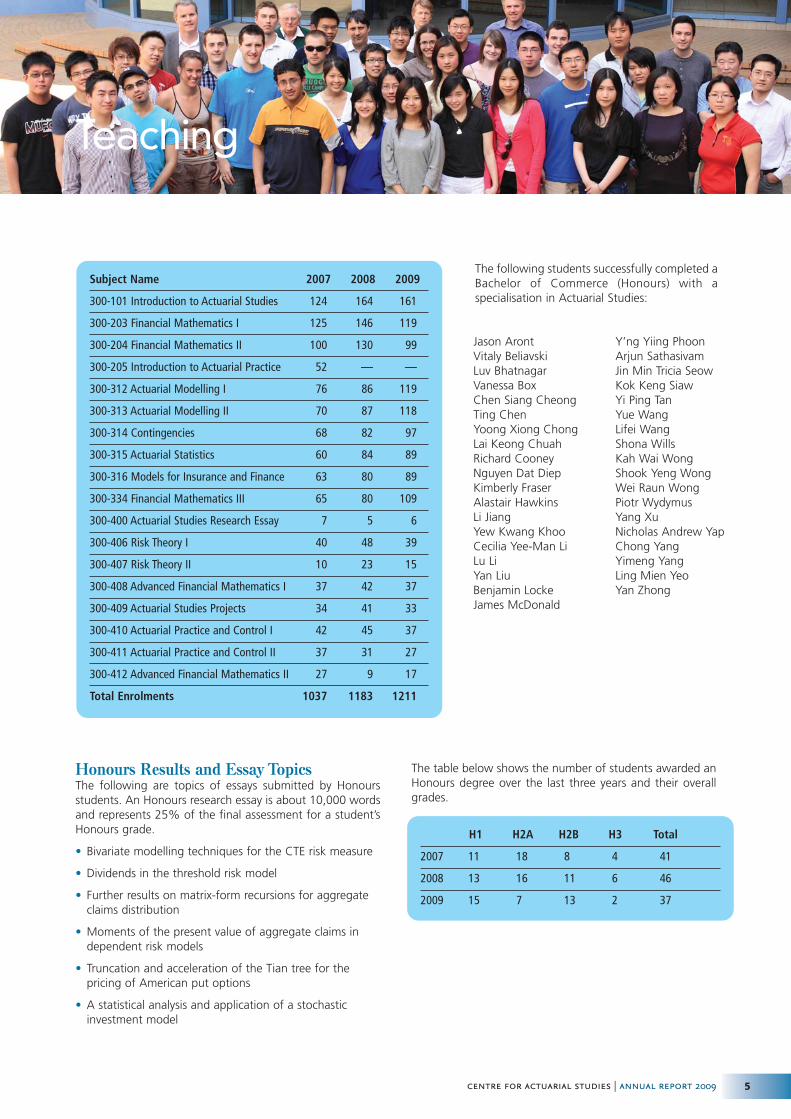

Honours Results and Essay TopicsThe following are topics of essays submitted by Honoursstudents. An Honours research essay is about 10,000 wordsand represents 25% of the final assessment for a student’sHonours grade.

• Bivariate modelling techniques for the CTE risk measure

• Dividends in the threshold risk model

• Further results on matrix-form recursions for aggregateclaims distribution

• Moments of the present value of aggregate claims independent risk models

• Truncation and acceleration of the Tian tree for thepricing of American put options

• A statistical analysis and application of a stochasticinvestment model

The table below shows the number of students awarded anHonours degree over the last three years and their overallgrades.

Teaching

centre for actuarial studies | annual report 2009 5

Subject Name 2007 2008 2009

300-101 Introduction to Actuarial Studies 124 164 161

300-203 Financial Mathematics I 125 146 119

300-204 Financial Mathematics II 100 130 99

300-205 Introduction to Actuarial Practice 52 — —

300-312 Actuarial Modelling I 76 86 119

300-313 Actuarial Modelling II 70 87 118

300-314 Contingencies 68 82 97

300-315 Actuarial Statistics 60 84 89

300-316 Models for Insurance and Finance 63 80 89

300-334 Financial Mathematics III 65 80 109

300-400 Actuarial Studies Research Essay 7 5 6

300-406 Risk Theory I 40 48 39

300-407 Risk Theory II 10 23 15

300-408 Advanced Financial Mathematics I 37 42 37

300-409 Actuarial Studies Projects 34 41 33

300-410 Actuarial Practice and Control I 42 45 37

300-411 Actuarial Practice and Control II 37 31 27

300-412 Advanced Financial Mathematics II 27 9 17

Total Enrolments 1037 1183 1211

H1 H2A H2B H3 Total

2007 11 18 8 4 41

2008 13 16 11 6 46

2009 15 7 13 2 37

The following students successfully completed aBachelor of Commerce (Honours) with aspecialisation in Actuarial Studies:

Jason ArontVitaly BeliavskiLuv BhatnagarVanessa BoxChen Siang CheongTing ChenYoong Xiong ChongLai Keong ChuahRichard CooneyNguyen Dat DiepKimberly FraserAlastair HawkinsLi JiangYew Kwang KhooCecilia Yee-Man LiLu LiYan LiuBenjamin LockeJames McDonald

Y’ng Yiing PhoonArjun SathasivamJin Min Tricia SeowKok Keng SiawYi Ping TanYue WangLifei WangShona WillsKah Wai WongShook Yeng WongWei Raun WongPiotr WydymusYang XuNicholas Andrew YapChong YangYimeng YangLing Mien YeoYan Zhong

Centre AwardsHonours Medal in Actuarial StudiesShona Wills

ANZ Prize For Financial MathematicsShona Wills

Aviva Prize For Contingencies Alexander Wiguna

Comminsure PrizeFor Introduction to Actuarial StudiesJeremiah Cheung and William Zheng

Deloitte Actuaries and Consultants PrizeFor Actuarial Practice and Control I and IIAlastair John Hawkins

Institute of Actuaries of Australia PrizeFor Research Essays and Projects (Honours year)Ting Chen

Taylor Fry Prize For Actuarial Statistics Navin Ranasinghe

Towers Perrin PrizeFor Risk Theory I and IIShona Wills and Lai Keong Chuah

Faculty of Business and Economics AwardsJ.F. Major Memorial PrizeFor the best student in the third year of the Bachelor ofCommerce degreeAlexander Wiguna

Kinsman Studentship Award and KinsmanHonours Research Essay PrizeFor the best publishable article, and for the best Honoursessay in the Department of Economics Wang Chun Wei

Student Prize Winners

PhD Students and Research Topics

6 centre for actuarial studies | annual report 2009

Christopher Beveridge Pricing long-dated exotic interest rate contracts in thedisplaced diffusion LIBOR market model

Jiun Hong ChanMethodologies for computation in the stochastic volatilityLMM

Stephen ChinOption pricing under stochastic volatility

Nicholas DensonVariance reduction using a Markov LIBOR market model

Evan HariyantoPricing and risk management of reverse mortgages in theAustralian market

Jingchao LiFinite time ruin problems

Qing LiuBivariate claim modelling for general insurance

Ciyu NieA lower barrier alerting system for risk processes

Robert TangThe accurate estimation of Greeks in multi-factor creditinterest-rate hybrid models

Chao YangPricing and hedging models

BookDickson D, Hardy M and Waters H. ActuarialMathematics for Life Contingent Risks. CambridgeUniversity Press, xvii+493 pages.

Refereed Journal ArticlesBeveridge C, Denson N and Joshi M. Comparingdiscretisations of the LIBOR market model in the spotmeasure. Australian Actuarial Journal. 15 (2): 231-253.

Chan J, Joshi M, Tang R and Yang C. Trinomial orbinomial: Accelerating American put option price on trees.Journal of Futures Markets. 29 (9): 826-839.

Dufresne D, Garrido J and Morales M. Fourier inversionformulas in option pricing and insurance. Methodology andComputing in Applied Probability. 3 (11): 359-383.

Denson NA and Joshi M. Flaming logs. Wilmott Journal.1 (5-6): 259-262.

Joshi M. Achieving smooth asymptotics for the prices ofEuropean options in binomial trees. Quantitative Finance.9 (2): 171-176.

Joshi M. The convergence of binomial trees for pricing theAmerican put. Journal of Risk. 11 (4): 87-108.

Li S and Lu Y. The distribution of total dividend paymentsin a Sparre Andersen model. Statistics and ProbabilityLetters. 79 (9): 1246-1251.

Li S, Lu Y and Garrido J. A review of discrete-time riskmodels. Real Academia de Ciencias Exactas, Fisicas yNaturales. Revista. Serie A, Matematicas. 103 (2): 321-337.

Lu Y and Li S. The Markovian regime-switching risk modelwith a threshold dividend strategy. Insurance: Mathematicsand Economics. 44 (2): 296-303.

Tanthanongsakkun S, Pitt D and Treepongkaruna S. Acomparison of corporate bankruptcy models in Australia:The Merton vs accounting based models. Asia-PacificJournal of Risk and Insurance, 3 (2): 93-112.

Taylor G. The chain ladder and Tweedie distributed claimsdata. Variance. 3: 96-104.

Taylor G and McGuire G. Adaptive reserving usingBayesian revision for the exponential dispersion family.Variance. 3:105-130.

Wu X and Li S. On the discounted penalty function in adiscrete time renewal risk model with general interclaimtimes. Scandinavian Actuarial Journal. 4 (109): 281-294.

Zhang Z, Li S and Yang H. The Gerber-Shiu discountedpenalty functions for a risk model with two classes of claims.Journal of Computational and Applied Mathematics. 230(2): 643-655.

Other PublicationsDickson D. Discussion of “On the joint distributions of thetime to ruin, the surplus prior to ruin, and the deficit at ruinin the classical risk model” by D. Landriault and G. Willmot.North American Actuarial Journal. 13 (2): 271-272.

McKenzie G, Gribble J, Pilger J. Developing theframework – industry efficiencies. Superfunds, No. 335.

Conference and Seminar PresentationsBeveridge, ChrisGeneric methods for obtaining rapid and tight bounds forBermudan derivatives using Monte Carlo simulations,Stochastic Processes and Financial Mathematics Seminar,The University of Melbourne, April.

Generic methods for obtaining rapid and tight bounds forBermudan derivatives using Monte Carlo simulations,Actuarial Science Seminar, The University of Amsterdam,September.

Generic methods for obtaining rapid and tight bounds forBermudan derivatives using Monte Carlo simulations,Quantitative Methods in Finance conference, The Universityof Technology Sydney, December.

Chen, PingExplicit solutions of optimal investment-consumptionstrategies under uncontrollable liabilities in a regime-switchmarket. Istanbul, Turkey, May.

Dickson, DavidOn the ruin time distributions for a Sparre Andersen processwith exponential claim sizes. Poster at Institute of Actuariesof Australia Biennial Convention, Sydney, April.

The probability and severity of ruin in finite time, NanyangBusiness School, Singapore, May.

Finite time ruin problems in Erlang risk models, AustralasianActuarial Education and Research Symposium, University ofNew South Wales, December.

Dufresne, DanielBeta-gamma algebra and Barnes’ integrals, AustralianMathematical Society Conference, University of SouthAustralia, January.

Beta-gamma algebra, discounted cash-flows and Barnes’Lemmas, Concordia University, Montreal, July.

Formule de Parseval pour options dans un modèle avec volatilitéstochastique, Université du Québec à Montréal, August.

Option pricing with stochastic volatility: Applying Parseval’sTheorem, Australasian Actuarial Education and ResearchSymposium, University of New South Wales, December.

Publications and Other Research Activities in 2009

centre for actuarial studies | annual report 2009 7

Education in Australian universities: Fooled byMeasurement, Australasian Actuarial Education andResearch Symposium, University of New South Wales,December.

Gribble, JulesQuantifying and Managing a Risk Culture, Institute ofActuaries of Australia Biennial Convention, Sydney, April.

Joshi, MarkMarket model vegas in the displaced diffusion LMM,Sydney, December.

Li, ShuanmingSome results for a Sparre Andersen model with phase-typeinter-claim times. Poster at Institute of Australia BiennialConvention, Sydney, April.

Pitt, DavidModel selection and claim frequency for workers’compensation insurance, Melbourne, May.

Model selection and claim frequency for workers’compensation insurance, London, U.K., December.

Model selection and claim frequency for workers’compensation insurance, Barcelona, Spain, December.

Taylor, Greg The chain ladder and Tweedie distributed claims data,Casualty Actuarial Society Spring Meeting, New Orleans,May.

Treatment of large claims in pricing and reserving. Instituteof Actuaries GIRO Seminar, Edinburgh, October.

A few reflections of a research-aware practitioner, Instituteof Actuaries of Australia Biennial Convention, Sydney, April.

Valuation assumptions, Institute of Actuaries of Australiaseminar on “GI in a GFC world”, Sydney, June.

Wu, XueyuanMatrix-form recursions for a family of compounddistributions, Australasian Actuarial Education and ResearchSymposium, UNSW, December.

Involvement as Editors and Reviewers David Dickson is an editor of ASTIN Bulletin, an associateeditor of Insurance: Mathematics and Economics, the BritishActuarial Journal, and Annals of Actuarial Science. David isalso a member of the editorial board of North AmericanActuarial Journal.

Shuanming Li is a reviewer for American MathematicalReviews.

David Pitt is an associate editor of Australian ActuarialJournal.

Greg Taylor is an associate editor of Insurance:Mathematics and Economics.

Members of the Centre acted as reviewers for thefollowing journals and publishers:

Acta Mathematica Applicatae Sinica

Annals of Actuarial Science

Annals of Applied Probability

ANZIAM

Applied Mathematics—A Journal of Chinese Universities

Applied Mathematics and Computation

Applied Stochastic Models in Business and Industry

Asian Journal of Control

ASTIN Bulletin

Australian Actuarial Journal

Blätter der DGVFM

Cambridge University Press

IMA Journal of Management Mathematics

Insurance: Mathematics and Economics

International Journal of Theoretical and Applied Finance

Journal of Computational and Applied Mathematics

Journal of Optimization Theory and Applications

Journal of Inequalities and Applications

Journal of Quantitative Finance

Journal of Systems Science and Complexity

Methodology and Computing in Applied Probability

North American Actuarial Journal

Revista de la Real Academia de Ciencias Exactas, Físicas yNaturales

Scandinavian Actuarial Journal

Statistics and Probability Letters

8 centre for actuarial studies | annual report 2009

Publications and Other Research Activities in 2009

No 180: A hierarchical Kalman filter By Greg Taylor Sundt’s hierarchical credibility model is generalised to a dynamicform, i.e. a form in which parameters are assumed to evolve overtime. This is done by superimposing a Kalman filter on Sundt’smodel. In the process it is shown that both Sundt’s model andthe Kalman filter may be derived as direct consequences ofHachemeister’s credibility regression model. A numerical exam-ple in Section 7 illustrates the application of the hierarchicalKalman filter to a hierarchy of occupational groups. The exam-ple shows how parameter estimates produced by the filter trackthe true values of parameters better than the estimates from astatic model when those parameters evolve over time.

No 181: G distributions and the beta-gamma algebraBy Daniel DufresneThis paper has four interrelated themes: (1) express Laplace andMellin transforms of sums of positive random variables in termsof the Mellin transform of the summands; (2) show the equiva-lence of the two Barnes’ lemmas with known properties ofgamma distributions; (3) establish properties of the sum of tworeciprocal gamma variables, and related results; (4) study the Gdistributions (whose Mellin transforms are ratios of products ofgamma functions).

No 182: A general formula for option pricesin a stochastic volatility modelBy Stephen Chin and Daniel DufresneWe consider the pricing of European derivatives in a Black-Scholes model with stochastic volatility. We show how Parseval’stheorem may be used to express those prices as Fourier integrals.This is a significant improvement over Monte Carlo simulation inmany cases. The main ingredient in our method is the Laplacetransform of the ordinary (constant volatility) price of a put or callin the Black-Scholes model, where the transform is taken withrespect to maturity (T); this does not appear to have been usedbefore in pricing options under stochastic volatility. We derivethese formulas and then apply them to the case where volatilityis modelled as a continuous-time Markov chain, the so-called“Markov regime switching model”. This model has been usedpreviously in stochastic volatility modelling, but mostly with onlyN = 2 states. We show how to use N = 3 states without difficul-ty, and how larger number of states can be handled. Numericalillustrations are given, including the implied volatility curve intwo and three-state models. The curves have the “smile” shapeobserved in practice.

No 183: Chain ladder forecast efficiencyBy Greg TaylorThe paper considers two models of a claim triangle, for both ofwhich the chain ladder algorithm for loss reserving is maximumlikelihood. Section 4 examines the relation between them interms of fitted values and forecasts. Later sections consider theprediction efficiency of the CL algorithm. For one model, thealgorithm is found to be minimum variance unbiased; for theother, it is biased but, if corrected for bias, is also minimum vari-ance unbiased (Section 5). The minimum variance unbiased esti-mators are also minimum prediction error unbiased forecasts(Section 6).

No 184: A review of the methodology offorecasting long-term equity returnsBy Richard FitzherbertThere are two main approaches to forecasting the long-termreturn from equities as an asset class. The first is to assume a pre-mium over interest rates or bond returns, justified by the risk-averse behaviour of portfolio investors. The second approach isto project dividend income assuming a link with inflation and/orparity with gross domestic profit. Except for GDP parity, thesemethods are all supported, superficially, by historical data.However the causal justifications for either the risk premium orthe inflation link are dubious – which reduces the status of theseassumptions from laws of nature to historical regularities uponwhose future we can only speculate. In a business environmentin which historical cost accounting prevails, return-on-sharehold-ers’ equity is the key variable which determines the underlyinglong-term return from equity portfolio investment which is mon-etary and not real in nature. Adjustments are required when his-torical cost accounting is not strictly applied.

No 185: Stochastic volatility and option pricingBy Daniel DufresneStochastic volatility models are now routinely used in invest-ments and option pricing. A brief introduction to those mod-els is first given, and then a method for pricing options isdescribed. The stochastic process that later became known as“Brownian motion” first appeared in Bachelier (1900), as amodel for security prices. Bachelier imagined the security priceas an arithmetic Brownian motion; this has the shortcoming ofallowing negative security prices. Osborne (1959), apparentlyunaware of Bachelier’s work, proposed geometric Brownianmotion (GBM) as a model for stock prices, in part becauseGBM cannot be negative. That model was used in economicsfrom the 1960s, notably to value options. Black and Scholes(1973) also used GBM for their risky asset, and since thenOsborne’s GBM model for stock prices has often been calledthe “Black-Scholes model”.

Research Paper Series

centre for actuarial studies | annual report 2009 9

Abstracts of the papers added in 2009 to the Centre’s Research Paper Series are given below. All these papers may be found athttp://www.economics.unimelb.edu.au/actwww/wps2009.shtml

No 186: Matrix-form recursions for afamily of compound distributionsBy Xueyuan Wu and Shuanming LiIn this paper, we aim to evaluate the distribution of the aggre-gate claims in the collective risk model. The number of claims isfirstly assumed to belong to a generalised (a, b, 0) family. Amatrix form recursive formula is then derived to evaluate therelated compound distribution when individual claim amountsfollow a discrete distribution on the non-negative integers. Thecorresponding formula is also given for continuous individualclaim amounts. Secondly, we pay particular attention to therecursive formula for compound phase-type distributions, sinceonly certain types of discrete phase-type distributions belong tothe generalised (a; b; 0) family. Similar recursive formulae areobtained for discrete and continuous individual claim amountdistributions. Finally, numerical examples are presented for threecounting distributions in this family.

No 187: The analysis of perturbed riskprocesses with markovian arrivalsBy Jiandong Ren and Shuanming Li In this paper, we study the perturbed risk processes withMarkovian arrivals. We present explicit formulas for the Laplacetransform of the time to cross a certain level before ruin, theLaplace transform of the time of recovery and the distributionof the maximum severity of ruin, as well as the expected dis-counted dividends and the distribution of the total dividendsprior to ruin for the risk model in the presence of a constant div-idend barrier.

No 188: The perturbed compound Poissonrisk model with two-sided jumpsBy Zhimin Zhang, Hu Yang, and Shuanming Li In this paper, we consider a perturbed compound Poisson riskmodel with two-sided jumps. The downward jumps representthe claims following an arbitrary distribution, while the upwardjumps are also allowed to represent the random gains. Assumingthat the density function of the upward jumps has a rationalLaplace transform, the Laplace transforms and defective renew-al equations for the discounted penalty functions are derived,and the asymptotic estimate for the probability of ruin is alsostudied for heavy-tailed downward jumps. Finally, some explicitexpressions for the discounted penalty functions, as well asnumerical examples, are given.

No 189: Fast sensitivity computations forMonte Carlo valuation of pension fundsBy Mark Joshi and David PittSensitivity analysis, or so-called ‘stress-testing’, has long beenpart of the actuarial contribution to pricing, reserving and man-agement of capital levels in both life and non-life assurance.

Recent developments in the area of derivatives pricing have seenthe application of adjoint methods to the calculation of optionprice sensitivities including the well-known ‘Greeks’ or partialderivatives of option prices with respect to model parameters.These methods have been the foundation for efficient and sim-ple calculations of a vast number of sensitivities to model param-eters in financial mathematics. This methodology has yet to beapplied to actuarial problems in insurance or in pensions. In thispaper we consider a model for a defined benefit pensionscheme and use adjoint methods to illustrate the sensitivity offund valuation results to key inputs such as mortality rates, inter-est rates and levels of salary rate inflation. The method ofadjoints is illustrated in the paper and numerical results are pre-sented. Efficient calculation of the sensitivity of key valuationresults to model inputs is useful information for practising actu-aries as it provides guidance as to the relative ultimate impor-tance of various judgments made in the formation of a liabilityvaluation basis.

No 190: Fast and accurate pricing andhedging of long-dated CMS spread optionsBy Mark Joshi and Chao YangWe present a fast method to price and hedge CMS spreadoptions in the displaced-diffusion co-initial swap market model.Numerical tests demonstrate that we are able to obtain suffi-ciently accurate prices and Greeks with computational timesmeasured in milliseconds. Further, we find that CMS spreadoptions are eakly dependent on the at-the-money Black impliedvolatility skews.

No 191: Efficient greek estimation in generic market modelsBy Mark Joshi and Chao YangAbstract: We first develop an efficient algorithm to computeDeltas of interest rate derivatives for a number of standard mar-ket models. The computational complexity of the algorithms isshown to be proportional to the number of rates times the num-ber of factors per step. We then show how to extend themethod to efficiently compute Vegas in those market models.

No 192: Fast delta computations in the swap market modelBy Mark Joshi and Chao YangWe develop an efficient algorithm to implement the adjoint

method that computes sensitivities of an interest rate derivative(IRD) with respect to different underlying rates in the co-terminalswap market model. The order of computation per step of thenew method is shown to be proportional to the number of ratestimes the number of factors, which is the same as the order inthe LIBOR market model.

Research Paper Series

10 centre for actuarial studies | annual report 2009

No 193: Model selection and claim frequency for workers’ compensation insuranceBy Jisheng Cui, David Pitt and Guoqi QianWe consider a set of workers’ compensation insurance claim

data where the aggregate number of losses (claims) reported toinsurers are classified by year of occurrence of the event causingloss, the US state in which the loss event occurred and the occu-pation class of the insured workers to which the loss countrelates. An exposure measure, equal to the total payroll ofobserved workers in each three-way classification, is also includ-ed in the dataset. Data are analysed across ten different states,24 different occupation classes and seven separate observationyears. A multiple linear regression model, with only predictors formain effects, could be estimated in 223+9+1+1 = 234 ways,theoretically more than 17 billion different possible models! Inaddition, one might expect that the number of claims recordedin each year in the same state and relating to the same occupa-tion class, are positively correlated. Different modelling assump-tions as to the nature of this correlation should also be consid-ered. On the other hand it may reasonably be assumed that thenumber of losses reported from different states and from differ-ent occupation classes are independent. Our data can thereforebe modelled using the statistical techniques applicable to paneldata and we work with generalised estimating equations (GEE)in the paper. For model selection, Pan (2001) suggested the useof an alternative to the AIC, namely the quasi-likelihood underindependence model criterion (QIC), for model comparison. Thispaper develops and applies a Gibbs sampling algorithm for effi-ciently locating, out of the more than 17 billion possible modelsthat could be considered for the analysis, that model with theoptimal (least) QIC value. The technique is illustrated using botha simulation study and using workers’ compensation insuranceclaim data.

No 194: Assessing the impact of suicideexclusion periods on life insuranceBy Paul Yip, David Pitt, Yan Wang, Xueyuan Wuand Tina XuWe study the impact of suicide exclusion periods, which arecommon in life insurance, on the rates of suicide and of acciden-tal death among life-insured individuals. The suicide exclusionperiod implies that if the life-insured individual were to die,where the cause of death is reported as suicide, during the exclu-sion period immediately after entering the policy of insurance,then the life insurance company would not be required to paythe sum insured to the deceased life’s estate. Suicide exclusionperiods are commonly thirteen months. Our first researchhypothesis is that the imposition of a suicide exclusion periodaffects the timing of suicides of life-insured individuals. Our sec-ond research hypothesis relates to the rates of accidental deathsreported to insurers. Given that insurers will not pay sum insured

benefits during the suicide exclusion period to individuals thatdie by suicide, it may be that there exists an increased desire toreport deaths as accidental rather than as suicide during the sui-cide exclusion period. A third research hypothesis is that lifeinsured individuals with higher sums insured have higher rates ofsuicide than other life-insured individuals. Crude and age-stan-dardized rates of suicide, accidental death and overall death,split by duration since the insured first bought their insurancepolicy, were computed. There were significantly fewer suicidesand no significant spike in the number of accidental deaths inthe exclusion period for Australian life insurance data. Anincreased number of suicides were detected for the first twoyears after the exclusion period. Also, life-insured individualswith higher sums insured have higher rates of suicide than otherlife-insured individuals. These provide evidence suggesting theexistence of adverse selection as a result of the exclusion periodadopted in the life insurance industry in Australia. We suggestthat by extending the exclusion period to three years, we mightprevent some “insurance induced” suicides. The rationale forpreventing suicide deaths by lengthening the suicide exclusionperiod is given.

No 195: Interpolation schemes in thedisplaced-diffusion LIBOR market modeland the efficient computation of prices and greeks for callable range accrualsBy Christopher Beveridge and Mark JoshiWe introduce a new arbitrage-free interpolation scheme for thedisplaced-diffusion LIBOR market model. Using this new exten-sion, and the Piterbarg interpolation scheme, we study the sim-ulation of range accrual coupons when valuing callable rangeaccruals in the displaced diffusion LIBOR market model. Weintroduce a number of new improvements that lead to signifi-cant efficiency improvements, and explain how to apply theadjoint-improved pathwise method to calculate deltas and vegasunder the new improvements, which was not previously possi-ble for callable range accruals. One new improvement is basedon using a Brownian-bridge-type approach to simulating therange accrual coupons. We consider a variety of examples,including when the reference rate is a LIBOR rate, when it is aspread between swap rates, and when the multiplier for therange accrual coupon is stochastic.

No 196: Graphical Asian optionsBy Mark JoshiWe discuss the problem of pricing Asian options inBlack–Scholes model using CUDA on a graphics processing unit.We survey some of the issues with GPU programming and dis-cuss code design and memory usage. We show that by using aQuasi Monte Carlo simulation with a geometric Asian option asa control variate, it is possible to get prices that are accurate to2E-4 within a fiftieth of a second.

Research Paper Series

centre for actuarial studies | annual report 2009 11

No 197: Pricing and deltas of discretely-monitored barrier options using stratifiedsampling on the hitting-times to the barrierBy Mark Joshi and Robert TangWe develop new Monte Carlo techniques based on stratifyingthe stock’s hitting-times to the barrier for the pricing and Deltacalculations of discretely-monitored barrier options using theBlack-Scholes model. We include a new algorithm for samplingan Inverse Gaussian random variable such that the sampling isrestricted to a subset of the sample space. We compare our newmethods to existing Monte Carlo methods and find that theycan substantially improve convergence speeds.

No 198: Fast Monte-Carlo greeks for financial products with discontinuous pay-offsBy Jiun Hong Chan and Mark JoshiWe introduce a new class of numerical schemes for discretizingprocesses driven by Brownian motions. These allow the rapidcomputation of sensitivities of discontinuous integrals usingpathwise methods even when the underlying densities post-dis-cretization are singular. The two new methods presented in thispaper allow Greeks for financial products with trigger features tobe computed in the LIBOR market model with similar speed tothat obtained by using the adjoint method for continuous pay-offs. The methods are generic with the main constraint beingthat the discontinuities at each step must be determined by aone-dimensional function: the proxy constraint. They are alsogeneric with the sole interaction between the integrand and thescheme being the specification of this constraint.

No 199: Minimal partial proxy simulation schemes for generic and robust Monte Carlo greeksBy Jiun Hong Chan and Mark JoshiIn this paper, we present a generic framework known as theminimal partial proxy simulation scheme. This framework allowsstable computation of the Monte-Carlo Greeks for financialproducts with trigger features via finite difference approxima-tion. The minimal partial proxy simulation scheme can be con-sidered as a special case of the partial proxy simulation scheme(Fries and Joshi, 2008b) as a measure change (weighted MonteCarlo) is performed to prevent path-wise discontinuities.However, our approach differs in term of how the measurechange is performed. Specifically, we select the measure changeoptimally such that it minimises the variance of the Monte-Carlo weight. Our method can be applied to popular classes of

trigger products including digital caplets, autocaps and targetredemption notes. While the Monte-Carlo Greeks obtainedusing the partial proxy simulation scheme can blow up in cer-tain cases, these Monte-Carlo Greeks remain stable under theminimal partial proxy simulation scheme. Standard errors forVega are also significantly lower under the minimal partial proxysimulation scheme.

No 200: Practical policy iteration: genericmethods for obtaining rapid and tightbounds for Bermudan exotic derivativesusing Monte Carlo simulationBy Christopher Beveridge and Mark JoshiWe introduce a set of improvements which allow the calculationof very tight lower bounds for Bermudan derivatives usingMonte Carlo simulation. These tight lower bounds can be com-puted quickly, and with minimal hand-crafting. Our focus is onaccelerating policy iteration to the point where it can be used insimilar computation times to the basic least-squares approach,but in doing so introduce a number of improvements which canbe applied to both the least-squares approach and the calcula-tion of upper bounds using the Andersen Broadie method. Theenhancements to the least-squares method improve both accu-racy and efficiency. Results are provided for the displaced-diffu-sion LIBOR market model, demonstrating that our practical pol-icy iteration algorithm can be used to obtain tight lower boundsfor cancellable CMS steepener, snowball and vanilla swaps insimilar times to the basic least-squares method.

No 201: Vega controlBy Nick Denson and Mark JoshiThe calculation of prices and sensitivities of exotic interest ratederivatives in the LIBOR market model is often very time consum-ing. One approach that has been previously suggested is to usea Markov-functional model as a control variate for prices anddeltas but not vegas. We present a new approach that is effec-tive for prices, deltas and vegas. It achieves a standard errorreduction by a factor of 10 for the price of five-factor, twenty-year Bermudan swaption, and of 5 for its vega.Advisory Board

Research Paper Series

12 centre for actuarial studies | annual report 2009

Staff and Advisory Board

centre for actuarial studies | annual report 2009 13

StaffProfessor in Actuarial StudiesDAVID C M DICKSON: BSc (Hons), PhD Heriot-Watt, FFAFIAAResearch interests: Aggregate claims distributions, renewalrisk processes, recursive methods in risk theory.

Professor in Actuarial Studies and DirectorDANIEL DUFRESNE: BSc Montreal, PhD The City University,FSAResearch interests: Financial mathematics, actuarialscience, probability.

Associate Professors in Actuarial StudiesMARK JOSHI: BA (Hons) Oxford, PhD MITResearch interests: Financial mathematicsSHUANMING LI: BSc Tianjin, MEc Renmin, PhD ConcordiaResearch interests: Risk and ruin theory, stochasticmodelling in insurance and finance, actuarial science.

Senior Lecturer in Actuarial StudiesDAVID PITT: BEc, BSc Macquarie, PhD ANU, FIAAResearch Interests: Analysis of disability income insuranceportfolios, stochastic modelling in actuarial science.

Lecturers in Actuarial StudiesPING CHEN: BAM (Qufu), MSc (CAS), PhD Hong KongResearch interests: Actuarial science, financial mathematics statistics and information XUEYUAN WU: BS, MS Nankai University, PhD Hong KongResearch interests: Risk and ruin theory, discrete-time riskmodels

Professorial AssociateGREG TAYLOR: BA, PhD, FIA, FIAA, FIMA, CMath, AOResearch interests: Modelling in general insurance.

Honorary Senior FellowsRICHARD FITZHERBERT: BSc, FIA, FIAA, F FinJULES GRIBBLE: BSc (Hons), PhD St Andrews, FIAA, FCIA,FSAGRANT HARSLETT: BSc (Hons) Adelaide, FIA, FIAA, ASA ALLEN TRUSLOVE: BSc (Hons), PhD Monash, MBA Deakin,FIA, FIAA

External Lecturers (if not listed above)DONALD CAMPBELL: BCom Melbourne, FIAADAVID HEATH: BEc (Hons) Monash, FIAA, CPA, F FinCARY HELENIUS: BSc (Hons), Dip Ed Melbourne, FIAA

Tutors Christopher Beveridge, BCom (Hons)Luv BhatnagarBen LockeStephen Chin, BSc, MFinMath Nguyen DiepEvan Hariyanto, BCom (Hons)Jingchao Li, BCom (Hons)Qing Liu, BCom (Hons)Ciyu (Jade) Nie, BCom (Hons)Abhimannyu Narenthiran, BCom (Hons)Robert Tang, BCom (Hons)Lifei WangShona WillsPiotr Wydymus Chao Yang, BCom (Hons), MCom

Advisory BoardThe membership of the Advisory Board is as follows:

External MembersMrs Helen McLeod AIGMr David McNiece Watson WyattProfessor Greg Taylor Taylor-Fry Consulting

ActuariesMr Chris White

University MembersProfessor Margaret Abernethy Dean, Faculty of

Economics andCommerce

Professor Nilss Olekalns Head of Department(Economics)

Professor Paul Kofman Department of FinanceProfessor David Dickson Centre for Actuarial

StudiesProfessor Daniel Dufresne Centre for Actuarial

StudiesProfessor Vance Martin Department of

Economics

Members

14 centre for actuarial studies | annual report 2009

Dr. Ping Chen Professor David Dickson

Professor Daniel Dufresne Associate Professor Mark Joshi

Members

centre for actuarial studies | annual report 2009 15

Associate Professor Shuanming Li Dr. David Pitt

Dr. Xueyuan Wu

http://www.economics.unimelb.edu.au/actwww/ActHome.shtml

Publication Disclaimer: The University has used its best endeav-ours to ensure the material contained in this publication wascorrect at the time of printing. The University gives no warran-ty and accepts no responsibility for the accuracy or complete-ness of information and the University reserves the right tomake changes without notice at any time in its absolute discre-tion. Users of this publication are advised to reconcile the accu-racy and currency of the information provided with the relevantfaculty or department of the University before acting upon or inconsideration of the information. Copyright in this publicationis owned by the University and no part of it may be reproducedwithout the permission of the University.

Authorised by the Director, Centre for Actuarial StudiesDepartment of EconomicsPublished by the Faculty of Business and Economics, July 2010© The University of Melbourne