Embed Size (px)

Citation preview

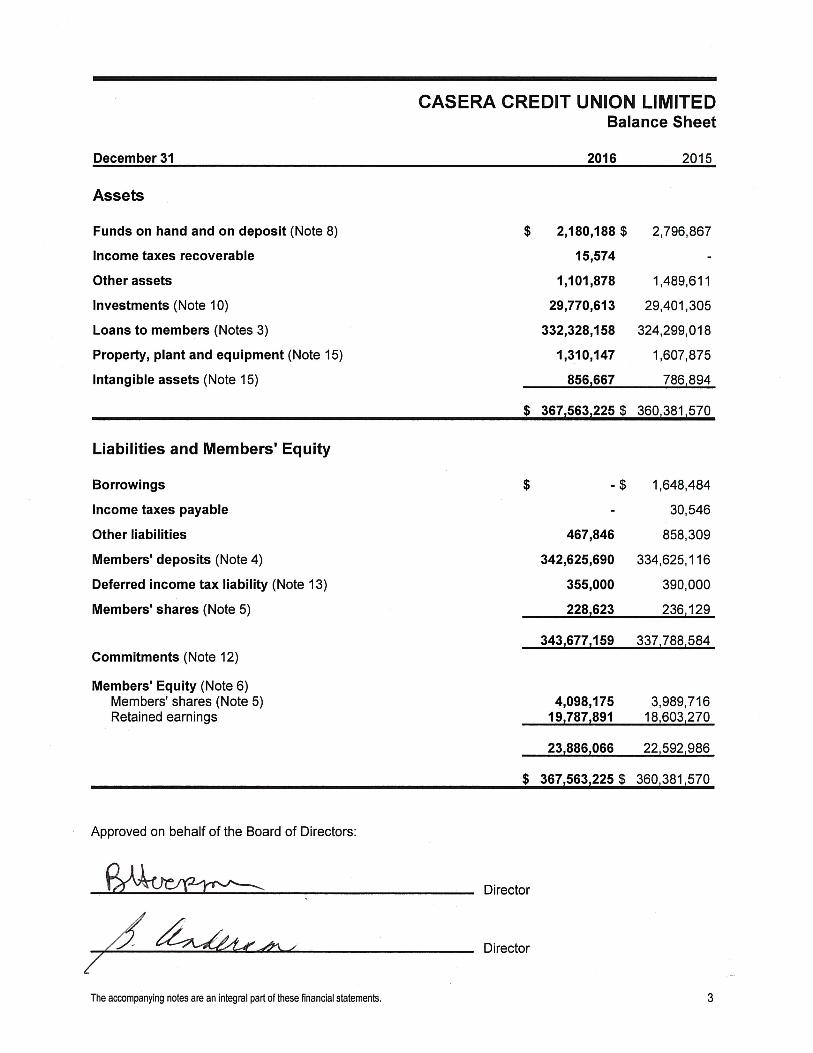

CASERA CREDIT UNION LIMITED

Financial StatementsFor the year ended December 31, 2016

CASERA CREDIT UNION LIMITED

Financial StatementsFor the year ended December 31, 2016

Contents

Independent Auditor's Report 2

Financial Statements

Balance Sheet 3

Statement of Comprehensive Income 4

Statement of Changes in Members' Equity 5

Statement of Cash Flows 6

Notes to Financial Statements

1. Corporate Information 7

2. Basis of Presentation 7

3. Loans to Members 8

4. Members' Deposits 14

5. Members' Shares 16

6. Capital Management 17

7. Cash and Cash Equivalents 18

8. Funds on Hand and on Deposit 18

9. Financial Margin and Interest 19

10. Investments 20

11. Foreign Exchange Risk 22

12. Commitments 22

13. Income Taxes 23

14. Pension Plan 24

15. Property, Plant and Equipment and Intangible Assets 25

16. Related Party Transactions 26

17. Personnel Expenses 27

18. Standards, Amendments and Interpretations Not Yet Effective 27

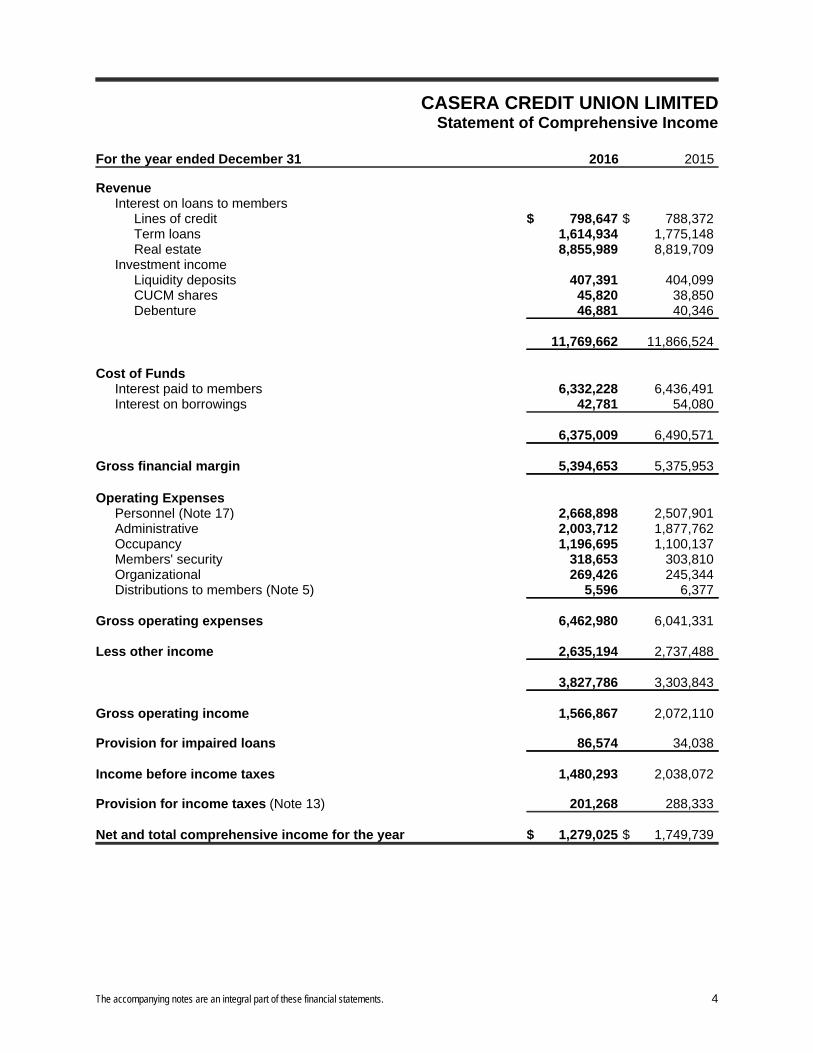

CASERA CREDIT UNION LIMITEDStatement of Comprehensive Income

For the year ended December 31 2016 2015

RevenueInterest on loans to members

Lines of credit $ 798,647 $ 788,372Term loans 1,614,934 1,775,148Real estate 8,855,989 8,819,709

Investment incomeLiquidity deposits 407,391 404,099CUCM shares 45,820 38,850Debenture 46,881 40,346

11,769,662 11,866,524

Cost of FundsInterest paid to members 6,332,228 6,436,491Interest on borrowings 42,781 54,080

6,375,009 6,490,571

Gross financial margin 5,394,653 5,375,953

Operating ExpensesPersonnel (Note 17) 2,668,898 2,507,901Administrative 2,003,712 1,877,762Occupancy 1,196,695 1,100,137Members' security 318,653 303,810Organizational 269,426 245,344Distributions to members (Note 5) 5,596 6,377

Gross operating expenses 6,462,980 6,041,331

Less other income 2,635,194 2,737,488

3,827,786 3,303,843

Gross operating income 1,566,867 2,072,110

Provision for impaired loans 86,574 34,038

Income before income taxes 1,480,293 2,038,072

Provision for income taxes (Note 13) 201,268 288,333

Net and total comprehensive income for the year $ 1,279,025 $ 1,749,739

The accompanying notes are an integral part of these financial statements. 4

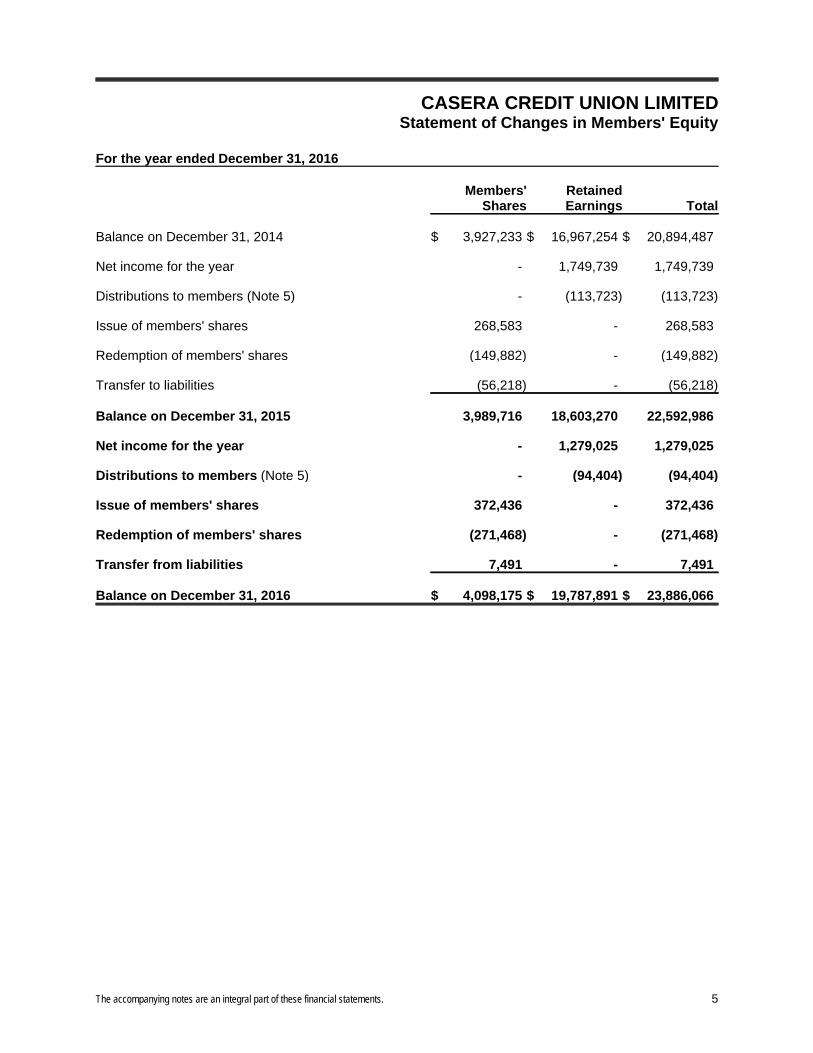

CASERA CREDIT UNION LIMITEDStatement of Changes in Members' Equity

For the year ended December 31, 2016

Members'Shares

RetainedEarnings Total

Balance on December 31, 2014 $ 3,927,233 $ 16,967,254 $ 20,894,487

Net income for the year - 1,749,739 1,749,739

Distributions to members (Note 5) - (113,723) (113,723)

Issue of members' shares 268,583 - 268,583

Redemption of members' shares (149,882) - (149,882)

Transfer to liabilities (56,218) - (56,218)

Balance on December 31, 2015 3,989,716 18,603,270 22,592,986

Net income for the year - 1,279,025 1,279,025

Distributions to members (Note 5) - (94,404) (94,404)

Issue of members' shares 372,436 - 372,436

Redemption of members' shares (271,468) - (271,468)

Transfer from liabilities 7,491 - 7,491

Balance on December 31, 2016 $ 4,098,175 $ 19,787,891 $ 23,886,066

The accompanying notes are an integral part of these financial statements. 5

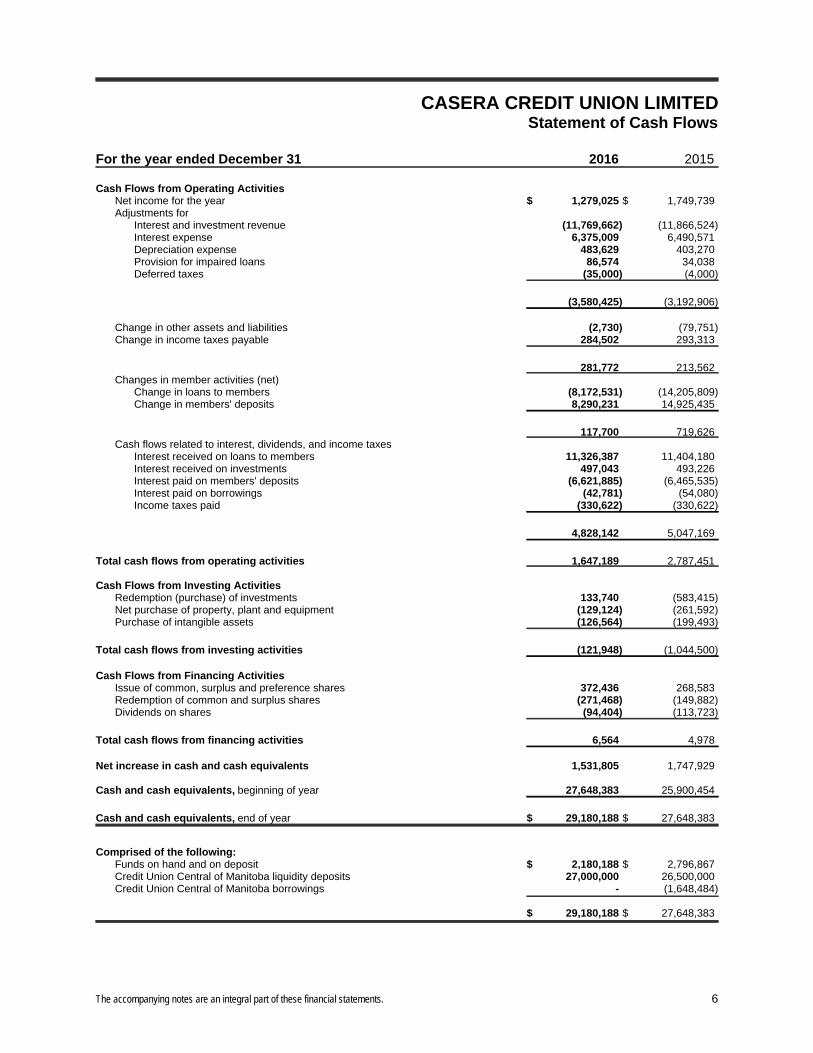

CASERA CREDIT UNION LIMITED Statement of Cash Flows

For the year ended December 31 2016 2015

Cash Flows from Operating ActivitiesNet income for the year $ 1,279,025 $ 1,749,739Adjustments for

Interest and investment revenue (11,769,662) (11,866,524)Interest expense 6,375,009 6,490,571Depreciation expense 483,629 403,270Provision for impaired loans 86,574 34,038Deferred taxes (35,000) (4,000)

(3,580,425) (3,192,906)

Change in other assets and liabilities (2,730) (79,751)Change in income taxes payable 284,502 293,313

281,772 213,562Changes in member activities (net)

Change in loans to members (8,172,531) (14,205,809)Change in members' deposits 8,290,231 14,925,435

117,700 719,626Cash flows related to interest, dividends, and income taxes

Interest received on loans to members 11,326,387 11,404,180Interest received on investments 497,043 493,226Interest paid on members' deposits (6,621,885) (6,465,535)Interest paid on borrowings (42,781) (54,080)Income taxes paid (330,622) (330,622)

4,828,142 5,047,169

Total cash flows from operating activities 1,647,189 2,787,451

Cash Flows from Investing ActivitiesRedemption (purchase) of investments 133,740 (583,415)Net purchase of property, plant and equipment (129,124) (261,592)Purchase of intangible assets (126,564) (199,493)

Total cash flows from investing activities (121,948) (1,044,500)

Cash Flows from Financing ActivitiesIssue of common, surplus and preference shares 372,436 268,583Redemption of common and surplus shares (271,468) (149,882)Dividends on shares (94,404) (113,723)

Total cash flows from financing activities 6,564 4,978

Net increase in cash and cash equivalents 1,531,805 1,747,929

Cash and cash equivalents, beginning of year 27,648,383 25,900,454

Cash and cash equivalents, end of year $ 29,180,188 $ 27,648,383

Comprised of the following:Funds on hand and on deposit $ 2,180,188 $ 2,796,867Credit Union Central of Manitoba liquidity deposits 27,000,000 26,500,000Credit Union Central of Manitoba borrowings - (1,648,484)

$ 29,180,188 $ 27,648,383

The accompanying notes are an integral part of these financial statements. 6

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

1. Corporate Information

Reporting Entity

Casera Credit Union Limited (the "Credit Union") is incorporated under The Credit Unions andCaisses Populaires Act of the Province of Manitoba ("The Act") and is a member of Credit UnionCentral of Manitoba ("CUCM"). The Credit Union operates as one operating segment in the loansand deposit taking industry in Manitoba. Products and services offered to its members includeconsumer and commercial loans and mortgages, chequing and savings accounts, term deposits,registered deposits, automated teller machines ("ATMs"), debit and credit cards, Internet bankingand the sale of mutual funds. The Credit Union has three branches located in Winnipeg. The CreditUnion's head office is located at 1300 Plessis Road, Winnipeg, Manitoba.

These financial statements have been authorized for issue by the Board of Directors on March 27,2017.

2. Basis of Presentation

(a) Statement of Compliance

These financial statements have been prepared in accordance with International FinancialReporting Standards ("IFRS") as issued by the International Accounting Standards Board (the"IASB").

(b) Basis of Measurement

These financial statements were prepared under the historical cost convention, as modified bythe revaluation of available-for-sale financial assets and derivative financial instrumentsmeasured at fair value.

The Credit Union’s functional and presentation currency is the Canadian dollar.

(c) Judgements and Estimates

The preparation of financial statements in compliance with IFRS requires management to makecertain critical accounting estimates. It also requires management to exercise judgment inapplying the Credit Union’s accounting policies. The areas involving critical judgements andestimates in applying accounting policies that have the most significant risk of causing materialadjustment to the carrying amounts of assets and liabilities recognized in the financialstatements with the next financial year are:

• In determining whether an impairment loss should be recorded relating to loans tomembers in the statement of comprehensive income (Note 3).

• The Credit Union determines the fair value of certain financial instruments using valuationtechniques. Those techniques are significantly affected by the assumptions used, includingdiscount rates and estimates of future cash flows (Notes 3, 4 and 10).

In addition, in preparing the financial statements, the notes to the financial statements wereordered such that the most relevant information was presented earlier in the notes and thedisclosures that management deemed to be immaterial were excluded from the notes to thefinancial statements. The determination of the relevance and materiality of disclosures involvedsignificant judgement.

7

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

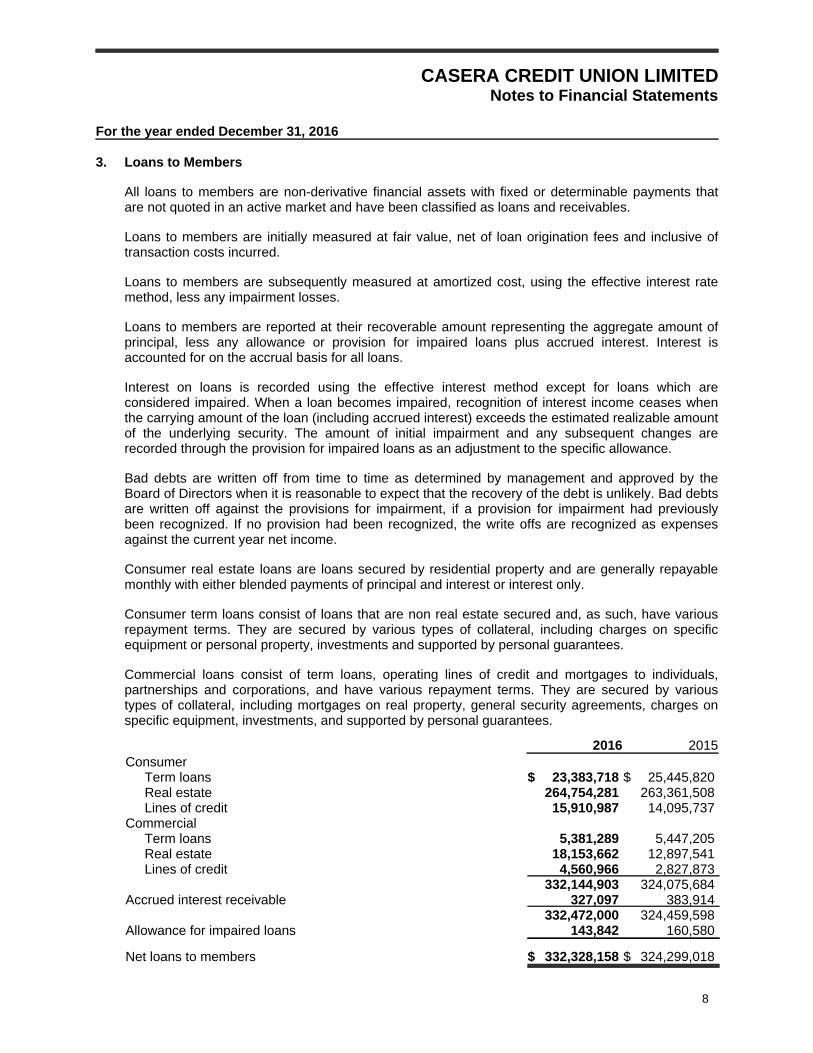

3. Loans to Members

All loans to members are non-derivative financial assets with fixed or determinable payments thatare not quoted in an active market and have been classified as loans and receivables.

Loans to members are initially measured at fair value, net of loan origination fees and inclusive oftransaction costs incurred.

Loans to members are subsequently measured at amortized cost, using the effective interest ratemethod, less any impairment losses.

Loans to members are reported at their recoverable amount representing the aggregate amount ofprincipal, less any allowance or provision for impaired loans plus accrued interest. Interest isaccounted for on the accrual basis for all loans.

Interest on loans is recorded using the effective interest method except for loans which areconsidered impaired. When a loan becomes impaired, recognition of interest income ceases whenthe carrying amount of the loan (including accrued interest) exceeds the estimated realizable amountof the underlying security. The amount of initial impairment and any subsequent changes arerecorded through the provision for impaired loans as an adjustment to the specific allowance.

Bad debts are written off from time to time as determined by management and approved by theBoard of Directors when it is reasonable to expect that the recovery of the debt is unlikely. Bad debtsare written off against the provisions for impairment, if a provision for impairment had previouslybeen recognized. If no provision had been recognized, the write offs are recognized as expensesagainst the current year net income.

Consumer real estate loans are loans secured by residential property and are generally repayablemonthly with either blended payments of principal and interest or interest only.

Consumer term loans consist of loans that are non real estate secured and, as such, have variousrepayment terms. They are secured by various types of collateral, including charges on specificequipment or personal property, investments and supported by personal guarantees.

Commercial loans consist of term loans, operating lines of credit and mortgages to individuals,partnerships and corporations, and have various repayment terms. They are secured by varioustypes of collateral, including mortgages on real property, general security agreements, charges onspecific equipment, investments, and supported by personal guarantees.

2016 2015Consumer

Term loans $ 23,383,718 $ 25,445,820Real estate 264,754,281 263,361,508Lines of credit 15,910,987 14,095,737

CommercialTerm loans 5,381,289 5,447,205Real estate 18,153,662 12,897,541Lines of credit 4,560,966 2,827,873

332,144,903 324,075,684Accrued interest receivable 327,097 383,914

332,472,000 324,459,598Allowance for impaired loans 143,842 160,580

Net loans to members $ 332,328,158 $ 324,299,018

8

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

3. Loans to Members (continued)

Credit Risk Management

Credit risk rating systems are designed to assess and quantify the risk inherent in credit activities inan accurate and consistent manner. To assess credit risk, the Credit Union takes into considerationthe member's character, ability to pay, and value of collateral available to secure the loan.

The Credit Union's credit risk management principles are guided by its overall risk managementprinciples. The Board of Directors ensures that management has a framework, and policies,processes and procedures in place to manage credit risks and that the overall credit risk policies arecomplied with at the business and transaction level.

The Credit Union's credit risk policies set out the minimum requirements for management of creditrisk in a variety of transactional and portfolio management contexts. Its credit risk policies comprisethe following:

• General loan policy statements including approval of lending policies, eligibility for loans,exceptions to policy, policy violations, liquidity, loan administration, credit concentration limits,and risk rating;

• Loan lending limits including Board of Directors limits, schedule of assigned limits andexemptions from aggregate indebtedness;

• Loan collateral security classifications which set loan classifications, advance ratios anddepreciation periods;

• Procedures outlining loan overdrafts, release or substitution of collateral, temporary suspensionof payments and loan renegotiations;

• Loan delinquency controls regarding procedures followed for loans in arrears; and

• Audit procedures and processes are in existence for the Credit Union's lending activities.

With respect to credit risk, the Board of Directors receives monthly reports summarizing new loans,delinquent loans and overdraft utilization. The Board of Directors also receives an analysis of baddebts and allowance for impaired loans quarterly.

For the current year, the amount of financial assets that would otherwise be past due or impairedwhose terms have been renegotiated is $NIL.

There have been no significant changes from the previous year in the exposure to risk or policies,procedures and methods used to measure the risk.

Concentration of Risk

The Credit Union has an exposure to groupings of individual loans which concentrate risk and createexposure to particular segments as noted below.

9

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

3. Loans to Members (continued)

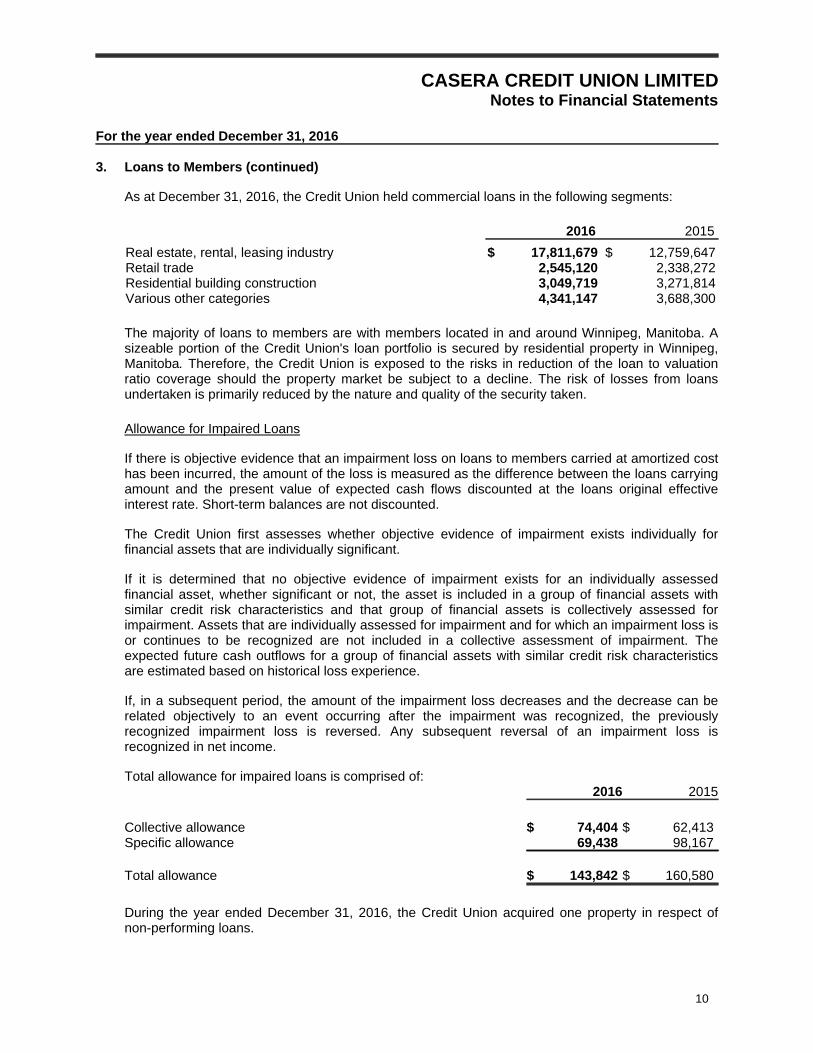

As at December 31, 2016, the Credit Union held commercial loans in the following segments:

2016 2015

Real estate, rental, leasing industry $ 17,811,679 $ 12,759,647Retail trade 2,545,120 2,338,272Residential building construction 3,049,719 3,271,814Various other categories 4,341,147 3,688,300

The majority of loans to members are with members located in and around Winnipeg, Manitoba. Asizeable portion of the Credit Union's loan portfolio is secured by residential property in Winnipeg,Manitoba. Therefore, the Credit Union is exposed to the risks in reduction of the loan to valuationratio coverage should the property market be subject to a decline. The risk of losses from loansundertaken is primarily reduced by the nature and quality of the security taken.

Allowance for Impaired Loans

If there is objective evidence that an impairment loss on loans to members carried at amortized costhas been incurred, the amount of the loss is measured as the difference between the loans carryingamount and the present value of expected cash flows discounted at the loans original effectiveinterest rate. Short-term balances are not discounted.

The Credit Union first assesses whether objective evidence of impairment exists individually forfinancial assets that are individually significant.

If it is determined that no objective evidence of impairment exists for an individually assessedfinancial asset, whether significant or not, the asset is included in a group of financial assets withsimilar credit risk characteristics and that group of financial assets is collectively assessed forimpairment. Assets that are individually assessed for impairment and for which an impairment loss isor continues to be recognized are not included in a collective assessment of impairment. Theexpected future cash outflows for a group of financial assets with similar credit risk characteristicsare estimated based on historical loss experience.

If, in a subsequent period, the amount of the impairment loss decreases and the decrease can berelated objectively to an event occurring after the impairment was recognized, the previouslyrecognized impairment loss is reversed. Any subsequent reversal of an impairment loss isrecognized in net income.

Total allowance for impaired loans is comprised of:2016 2015

Collective allowance $ 74,404 $ 62,413Specific allowance 69,438 98,167

Total allowance $ 143,842 $ 160,580

During the year ended December 31, 2016, the Credit Union acquired one property in respect ofnon-performing loans.

10

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

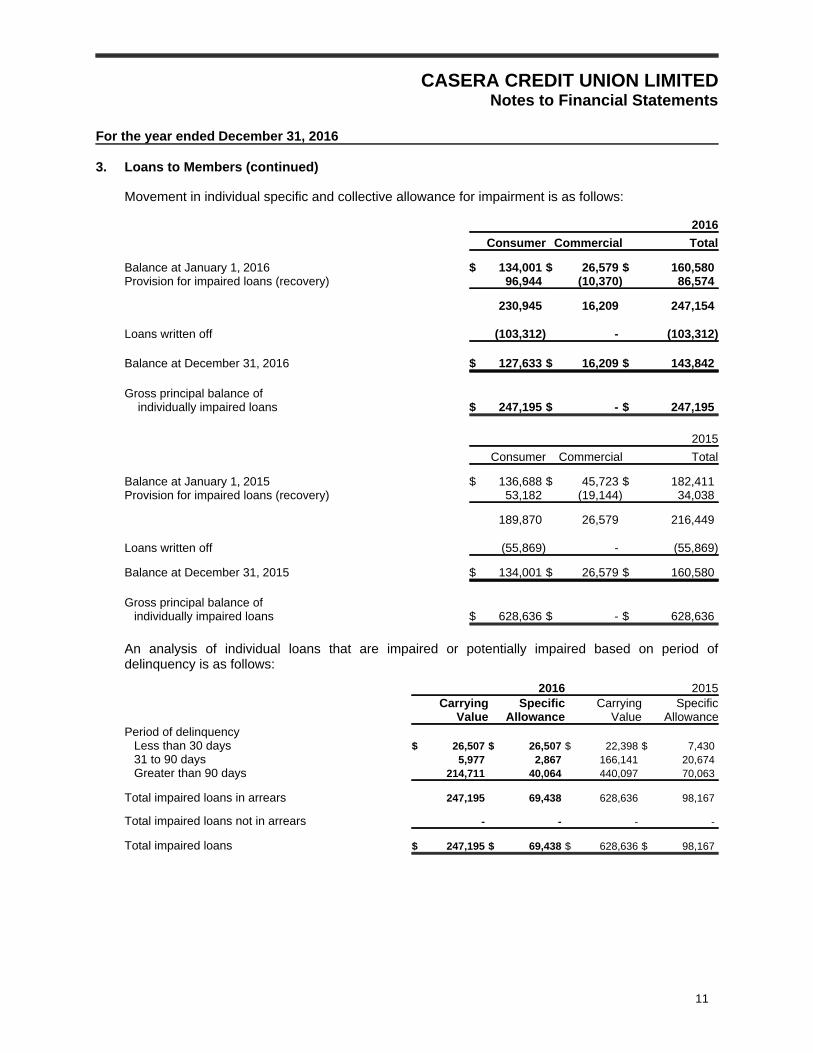

3. Loans to Members (continued)

Movement in individual specific and collective allowance for impairment is as follows:

2016

Consumer Commercial Total

Balance at January 1, 2016 $ 134,001 $ 26,579 $ 160,580Provision for impaired loans (recovery) 96,944 (10,370) 86,574

230,945 16,209 247,154

Loans written off (103,312) - (103,312)

Balance at December 31, 2016 $ 127,633 $ 16,209 $ 143,842

Gross principal balance of individually impaired loans $ 247,195 $ - $ 247,195

2015

Consumer Commercial Total

Balance at January 1, 2015 $ 136,688 $ 45,723 $ 182,411Provision for impaired loans (recovery) 53,182 (19,144) 34,038

189,870 26,579 216,449

Loans written off (55,869) - (55,869)

Balance at December 31, 2015 $ 134,001 $ 26,579 $ 160,580

Gross principal balance of individually impaired loans $ 628,636 $ - $ 628,636

An analysis of individual loans that are impaired or potentially impaired based on period ofdelinquency is as follows:

2016 2015Carrying

ValueSpecific

AllowanceCarrying

ValueSpecific

AllowancePeriod of delinquency

Less than 30 days $ 26,507 $ 26,507 $ 22,398 $ 7,43031 to 90 days 5,977 2,867 166,141 20,674Greater than 90 days 214,711 40,064 440,097 70,063

Total impaired loans in arrears 247,195 69,438 628,636 98,167

Total impaired loans not in arrears - - - -

Total impaired loans $ 247,195 $ 69,438 $ 628,636 $ 98,167

11

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

3. Loans to Members (continued)

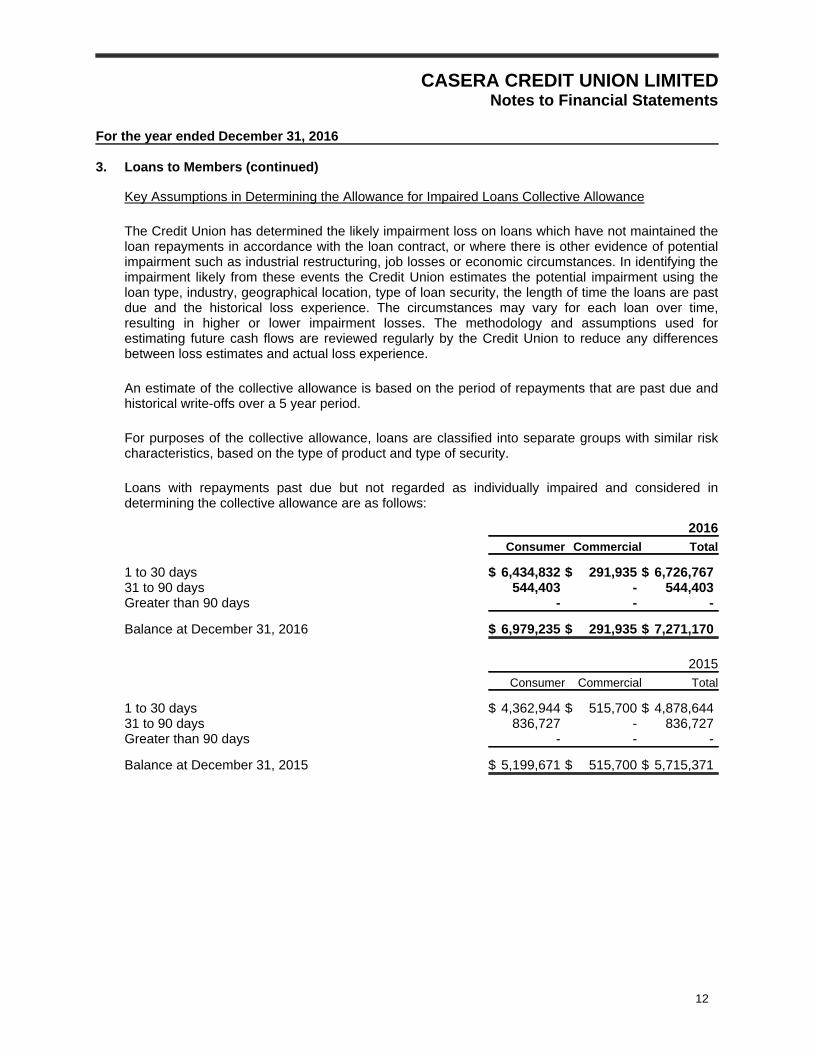

Key Assumptions in Determining the Allowance for Impaired Loans Collective Allowance

The Credit Union has determined the likely impairment loss on loans which have not maintained theloan repayments in accordance with the loan contract, or where there is other evidence of potentialimpairment such as industrial restructuring, job losses or economic circumstances. In identifying theimpairment likely from these events the Credit Union estimates the potential impairment using theloan type, industry, geographical location, type of loan security, the length of time the loans are pastdue and the historical loss experience. The circumstances may vary for each loan over time,resulting in higher or lower impairment losses. The methodology and assumptions used forestimating future cash flows are reviewed regularly by the Credit Union to reduce any differencesbetween loss estimates and actual loss experience.

An estimate of the collective allowance is based on the period of repayments that are past due andhistorical write-offs over a 5 year period.

For purposes of the collective allowance, loans are classified into separate groups with similar riskcharacteristics, based on the type of product and type of security.

Loans with repayments past due but not regarded as individually impaired and considered indetermining the collective allowance are as follows:

2016Consumer Commercial Total

1 to 30 days $ 6,434,832 $ 291,935 $ 6,726,76731 to 90 days 544,403 - 544,403Greater than 90 days - - -

Balance at December 31, 2016 $ 6,979,235 $ 291,935 $ 7,271,170

2015Consumer Commercial Total

1 to 30 days $ 4,362,944 $ 515,700 $ 4,878,64431 to 90 days 836,727 - 836,727Greater than 90 days - - -

Balance at December 31, 2015 $ 5,199,671 $ 515,700 $ 5,715,371

12

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

3. Loans to Members (continued)

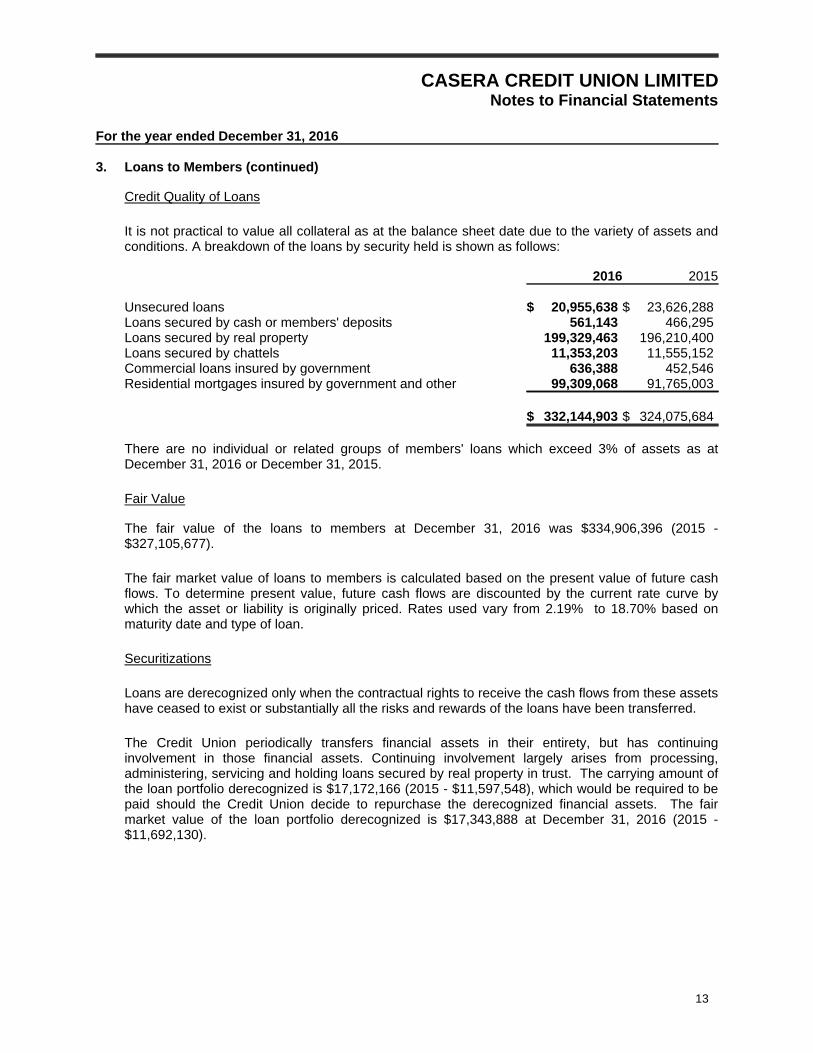

Credit Quality of Loans

It is not practical to value all collateral as at the balance sheet date due to the variety of assets andconditions. A breakdown of the loans by security held is shown as follows:

2016 2015

Unsecured loans $ 20,955,638 $ 23,626,288Loans secured by cash or members' deposits 561,143 466,295Loans secured by real property 199,329,463 196,210,400Loans secured by chattels 11,353,203 11,555,152Commercial loans insured by government 636,388 452,546Residential mortgages insured by government and other 99,309,068 91,765,003

$ 332,144,903 $ 324,075,684

There are no individual or related groups of members' loans which exceed 3% of assets as atDecember 31, 2016 or December 31, 2015.

Fair Value

The fair value of the loans to members at December 31, 2016 was $334,906,396 (2015 -$327,105,677).

The fair market value of loans to members is calculated based on the present value of future cashflows. To determine present value, future cash flows are discounted by the current rate curve bywhich the asset or liability is originally priced. Rates used vary from 2.19% to 18.70% based onmaturity date and type of loan.

Securitizations

Loans are derecognized only when the contractual rights to receive the cash flows from these assetshave ceased to exist or substantially all the risks and rewards of the loans have been transferred.

The Credit Union periodically transfers financial assets in their entirety, but has continuinginvolvement in those financial assets. Continuing involvement largely arises from processing,administering, servicing and holding loans secured by real property in trust. The carrying amount ofthe loan portfolio derecognized is $17,172,166 (2015 - $11,597,548), which would be required to bepaid should the Credit Union decide to repurchase the derecognized financial assets. The fairmarket value of the loan portfolio derecognized is $17,343,888 at December 31, 2016 (2015 -$11,692,130).

13

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

3. Loans to Members (continued)

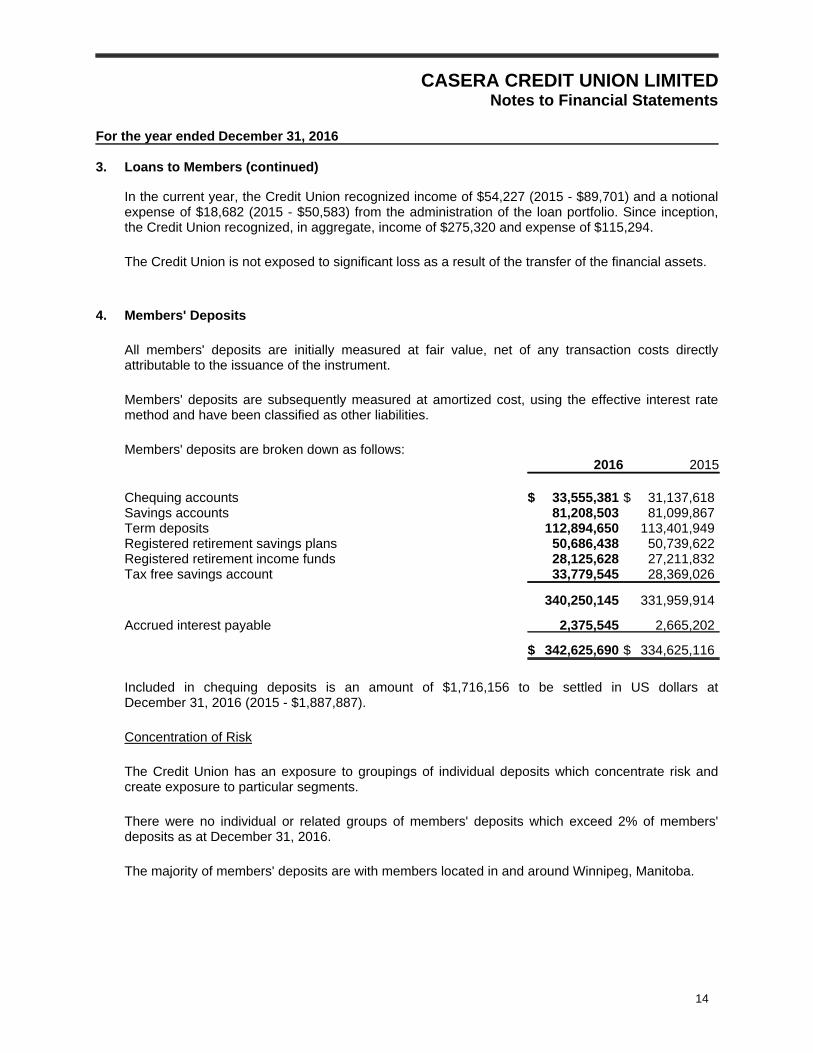

In the current year, the Credit Union recognized income of $54,227 (2015 - $89,701) and a notionalexpense of $18,682 (2015 - $50,583) from the administration of the loan portfolio. Since inception,the Credit Union recognized, in aggregate, income of $275,320 and expense of $115,294.

The Credit Union is not exposed to significant loss as a result of the transfer of the financial assets.

4. Members' Deposits

All members' deposits are initially measured at fair value, net of any transaction costs directlyattributable to the issuance of the instrument.

Members' deposits are subsequently measured at amortized cost, using the effective interest ratemethod and have been classified as other liabilities.

Members' deposits are broken down as follows:2016 2015

Chequing accounts $ 33,555,381 $ 31,137,618Savings accounts 81,208,503 81,099,867Term deposits 112,894,650 113,401,949Registered retirement savings plans 50,686,438 50,739,622Registered retirement income funds 28,125,628 27,211,832Tax free savings account 33,779,545 28,369,026

340,250,145 331,959,914

Accrued interest payable 2,375,545 2,665,202

$ 342,625,690 $ 334,625,116

Included in chequing deposits is an amount of $1,716,156 to be settled in US dollars atDecember 31, 2016 (2015 - $1,887,887).

Concentration of Risk

The Credit Union has an exposure to groupings of individual deposits which concentrate risk andcreate exposure to particular segments.

There were no individual or related groups of members' deposits which exceed 2% of members'deposits as at December 31, 2016.

The majority of members' deposits are with members located in and around Winnipeg, Manitoba.

14

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

4. Members' Deposits (continued)

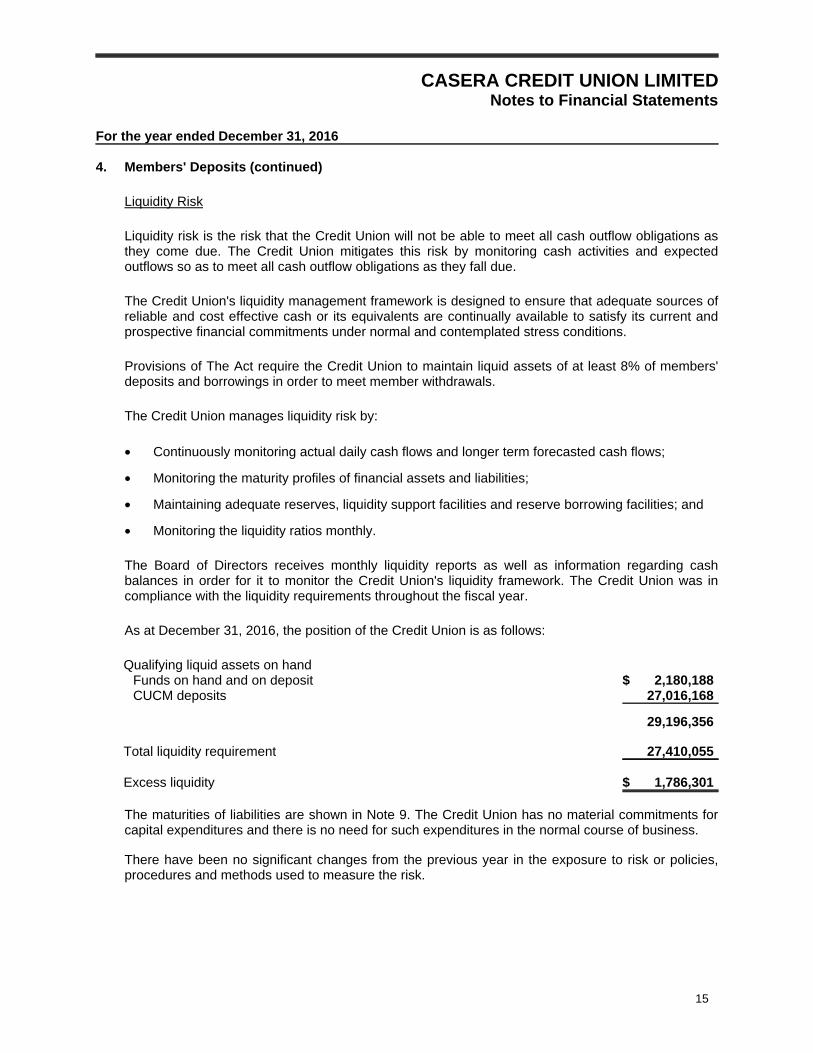

Liquidity Risk

Liquidity risk is the risk that the Credit Union will not be able to meet all cash outflow obligations asthey come due. The Credit Union mitigates this risk by monitoring cash activities and expectedoutflows so as to meet all cash outflow obligations as they fall due.

The Credit Union's liquidity management framework is designed to ensure that adequate sources ofreliable and cost effective cash or its equivalents are continually available to satisfy its current andprospective financial commitments under normal and contemplated stress conditions.

Provisions of The Act require the Credit Union to maintain liquid assets of at least 8% of members'deposits and borrowings in order to meet member withdrawals.

The Credit Union manages liquidity risk by:

• Continuously monitoring actual daily cash flows and longer term forecasted cash flows;

• Monitoring the maturity profiles of financial assets and liabilities;

• Maintaining adequate reserves, liquidity support facilities and reserve borrowing facilities; and

• Monitoring the liquidity ratios monthly.

The Board of Directors receives monthly liquidity reports as well as information regarding cashbalances in order for it to monitor the Credit Union's liquidity framework. The Credit Union was incompliance with the liquidity requirements throughout the fiscal year.

As at December 31, 2016, the position of the Credit Union is as follows:

Qualifying liquid assets on handFunds on hand and on deposit $ 2,180,188CUCM deposits 27,016,168

29,196,356

Total liquidity requirement 27,410,055

Excess liquidity $ 1,786,301

The maturities of liabilities are shown in Note 9. The Credit Union has no material commitments forcapital expenditures and there is no need for such expenditures in the normal course of business.

There have been no significant changes from the previous year in the exposure to risk or policies,procedures and methods used to measure the risk.

15

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

4. Members' Deposits (continued)

Fair Value

The fair value of members' deposits at December 31, 2016 was $343,257,847 (2015 -$335,362,279).

The fair market value of members' deposits is calculated based on the present value of future cashflows. To determine present value, future cash flows are discounted by the current rate curve bywhich the asset or liability is originally priced. Rates used vary from 0.10% to 2.30% based onrenewal date of the deposit.

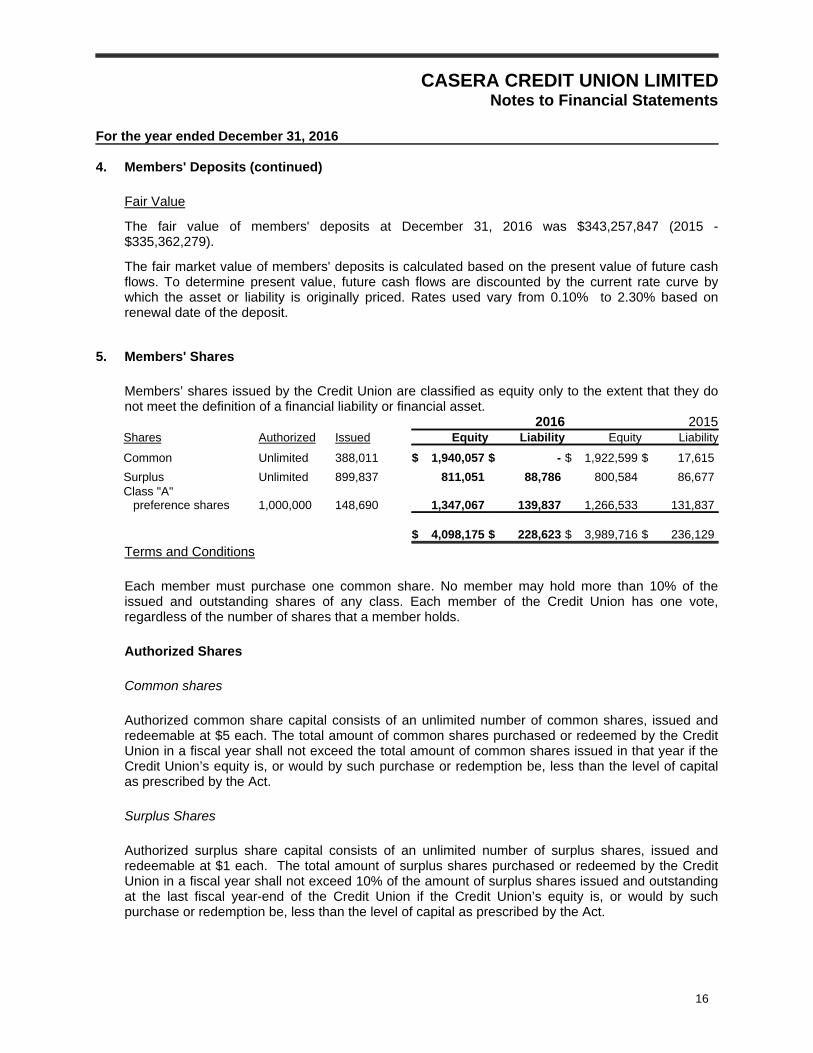

5. Members' Shares

Members’ shares issued by the Credit Union are classified as equity only to the extent that they donot meet the definition of a financial liability or financial asset.

2016 2015Shares Authorized Issued Equity Liability Equity Liability

Common Unlimited 388,011 $ 1,940,057 $ - $ 1,922,599 $ 17,615

Surplus Unlimited 899,837 811,051 88,786 800,584 86,677Class "A"

preference shares 1,000,000 148,690 1,347,067 139,837 1,266,533 131,837

$ 4,098,175 $ 228,623 $ 3,989,716 $ 236,129

Terms and Conditions

Each member must purchase one common share. No member may hold more than 10% of theissued and outstanding shares of any class. Each member of the Credit Union has one vote,regardless of the number of shares that a member holds.

Authorized Shares

Common shares

Authorized common share capital consists of an unlimited number of common shares, issued andredeemable at $5 each. The total amount of common shares purchased or redeemed by the CreditUnion in a fiscal year shall not exceed the total amount of common shares issued in that year if theCredit Union’s equity is, or would by such purchase or redemption be, less than the level of capitalas prescribed by the Act.

Surplus Shares

Authorized surplus share capital consists of an unlimited number of surplus shares, issued andredeemable at $1 each. The total amount of surplus shares purchased or redeemed by the CreditUnion in a fiscal year shall not exceed 10% of the amount of surplus shares issued and outstandingat the last fiscal year-end of the Credit Union if the Credit Union’s equity is, or would by suchpurchase or redemption be, less than the level of capital as prescribed by the Act.

16

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

5. Members' Shares (continued)

Class "A" Preference Shares

Authorized Class “A” preference share capital consists of 1,000,000 non-voting Class “A” preferenceshares, having a non-cumulative dividend rate, when declared, of not less than the first year rate ofthe latest issue of Canada Savings Bonds, issued and redeemable at $10 each.

Dividends are payable at the discretion of the Board. The total amount of Class “A” preferenceshares purchased or redeemed by the Credit Union in a fiscal year shall not exceed 10% of theamount of Class “A” preference shares issued and outstanding at the last fiscal year-end of theCredit Union if the Credit Union’s equity is, or by such purchase or redemption would be, less thanthe level of capital as prescribed by the Act. Class “A” preference shares are redeemable at thediscretion of the Board.

Distributions to Members

The Board of Directors have declared dividends on common and Class "A" preference shares of$100,000 (2015 - $121,100) of which $5,596 (2015 - $6,377) has been presented as operatingexpenses on the statement of comprehensive income and $94,404 (2015 - $113,723) has beenpresented as a reduction of equity on the statement of changes in members' equity. Tax savings of$14,842 (2015 - $16,397) have been applied to reduce current income tax expense on the statementof comprehensive income.

6. Capital Management

The Credit Union’s objectives with respect to capital management are to maintain a capital base thatis structured to exceed regulatory requirements and to best utilize capital allocations.

Regulations under The Act require that the Credit Union establish and maintain a level of capital thatmeets or exceeds the following:

• Total members' equity as shown on the balance sheet shall not be less than 5% of the bookvalue of all assets;

• Retained earnings shall not be less than 3% of the book value of assets; and

• Capital calculated in accordance with The Act shall not be less than 8% of the risk weightedvalue of its assets.

The Credit Union considers its capital to include members' shares (common shares and surplusshares), and retained earnings. There have been no changes in what the Credit Union considers tobe its capital since the previous period.

The Credit Union establishes the risk weighted value of its assets in accordance with Regulations toThe Act which establishes the applicable percentage for each class of assets. The Credit Union'srisk weighted value of its assets as at December 31, 2016 was $131,393,375 (2015 - $128,471,022).

17

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

6. Capital Management (continued)

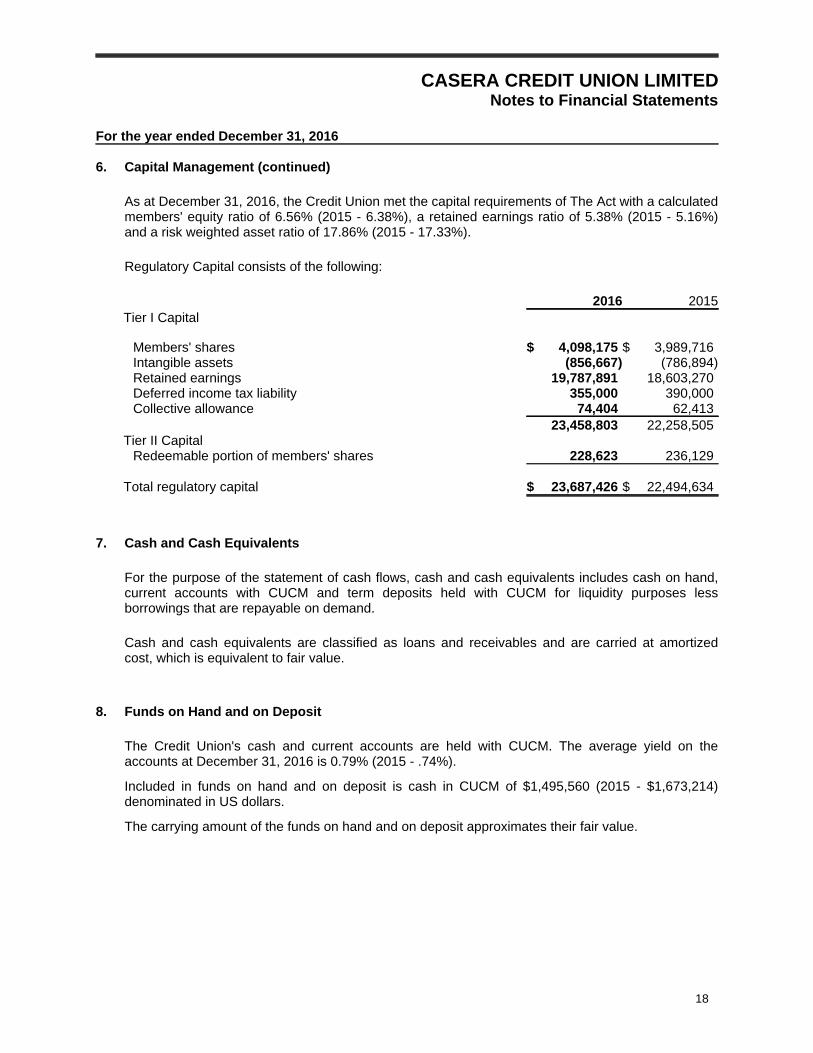

As at December 31, 2016, the Credit Union met the capital requirements of The Act with a calculatedmembers' equity ratio of 6.56% (2015 - 6.38%), a retained earnings ratio of 5.38% (2015 - 5.16%)and a risk weighted asset ratio of 17.86% (2015 - 17.33%).

Regulatory Capital consists of the following:

2016 2015Tier I Capital

Members' shares $ 4,098,175 $ 3,989,716Intangible assets (856,667) (786,894)Retained earnings 19,787,891 18,603,270Deferred income tax liability 355,000 390,000Collective allowance 74,404 62,413

23,458,803 22,258,505Tier II Capital

Redeemable portion of members' shares 228,623 236,129

Total regulatory capital $ 23,687,426 $ 22,494,634

7. Cash and Cash Equivalents

For the purpose of the statement of cash flows, cash and cash equivalents includes cash on hand,current accounts with CUCM and term deposits held with CUCM for liquidity purposes lessborrowings that are repayable on demand.

Cash and cash equivalents are classified as loans and receivables and are carried at amortizedcost, which is equivalent to fair value.

8. Funds on Hand and on Deposit

The Credit Union's cash and current accounts are held with CUCM. The average yield on theaccounts at December 31, 2016 is 0.79% (2015 - .74%).

Included in funds on hand and on deposit is cash in CUCM of $1,495,560 (2015 - $1,673,214)denominated in US dollars.

The carrying amount of the funds on hand and on deposit approximates their fair value.

18

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

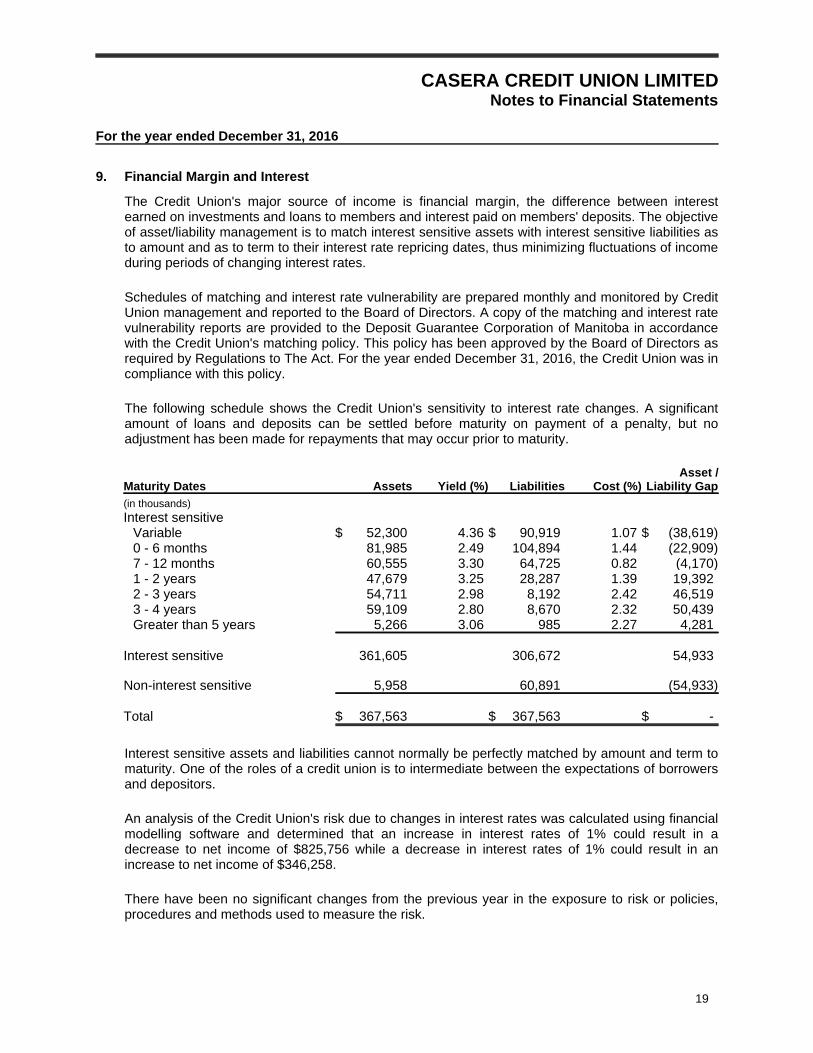

9. Financial Margin and Interest

The Credit Union's major source of income is financial margin, the difference between interestearned on investments and loans to members and interest paid on members' deposits. The objectiveof asset/liability management is to match interest sensitive assets with interest sensitive liabilities asto amount and as to term to their interest rate repricing dates, thus minimizing fluctuations of incomeduring periods of changing interest rates.

Schedules of matching and interest rate vulnerability are prepared monthly and monitored by CreditUnion management and reported to the Board of Directors. A copy of the matching and interest ratevulnerability reports are provided to the Deposit Guarantee Corporation of Manitoba in accordancewith the Credit Union's matching policy. This policy has been approved by the Board of Directors asrequired by Regulations to The Act. For the year ended December 31, 2016, the Credit Union was incompliance with this policy.

The following schedule shows the Credit Union's sensitivity to interest rate changes. A significantamount of loans and deposits can be settled before maturity on payment of a penalty, but noadjustment has been made for repayments that may occur prior to maturity.

Maturity Dates Assets Yield (%) Liabilities Cost (%)Asset /

Liability Gap

(in thousands)Interest sensitive

Variable $ 52,300 4.36 $ 90,919 1.07 $ (38,619)0 - 6 months 81,985 2.49 104,894 1.44 (22,909)7 - 12 months 60,555 3.30 64,725 0.82 (4,170)1 - 2 years 47,679 3.25 28,287 1.39 19,3922 - 3 years 54,711 2.98 8,192 2.42 46,5193 - 4 years 59,109 2.80 8,670 2.32 50,439Greater than 5 years 5,266 3.06 985 2.27 4,281

Interest sensitive 361,605 306,672 54,933

Non-interest sensitive 5,958 60,891 (54,933)

Total $ 367,563 $ 367,563 $ -

Interest sensitive assets and liabilities cannot normally be perfectly matched by amount and term tomaturity. One of the roles of a credit union is to intermediate between the expectations of borrowersand depositors.

An analysis of the Credit Union's risk due to changes in interest rates was calculated using financialmodelling software and determined that an increase in interest rates of 1% could result in adecrease to net income of $825,756 while a decrease in interest rates of 1% could result in anincrease to net income of $346,258.

There have been no significant changes from the previous year in the exposure to risk or policies,procedures and methods used to measure the risk.

19

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

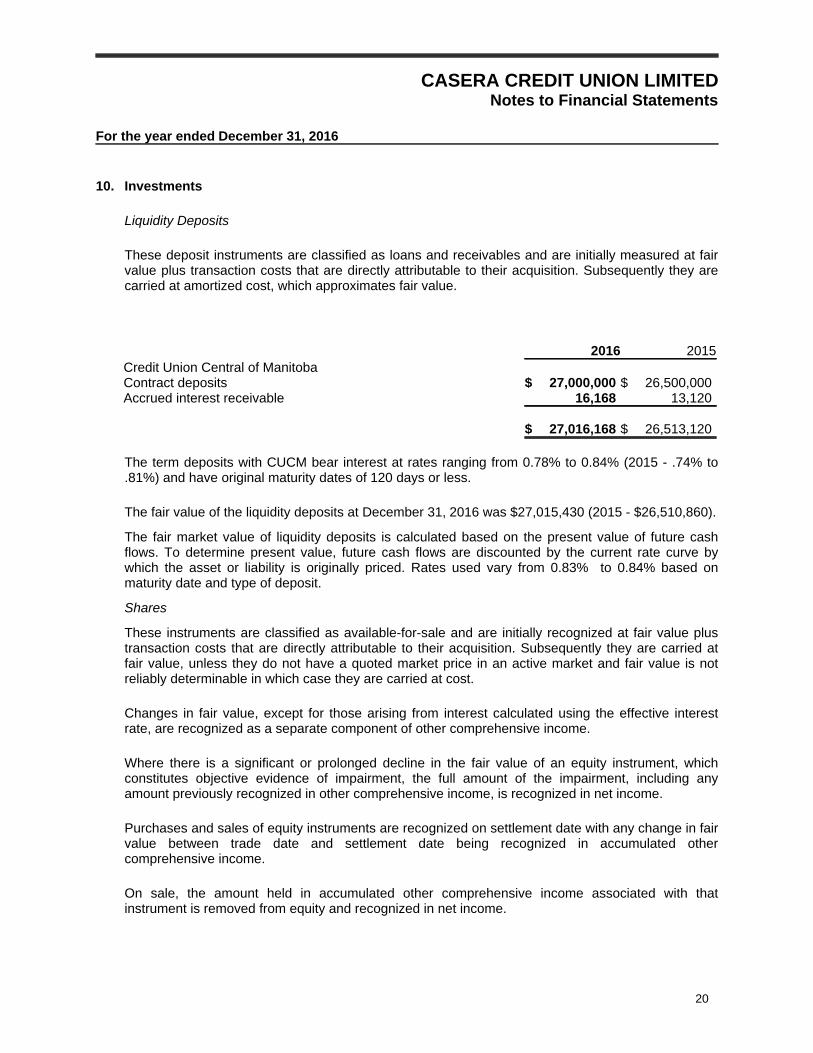

10. Investments

Liquidity Deposits

These deposit instruments are classified as loans and receivables and are initially measured at fairvalue plus transaction costs that are directly attributable to their acquisition. Subsequently they arecarried at amortized cost, which approximates fair value.

2016 2015Credit Union Central of ManitobaContract deposits $ 27,000,000 $ 26,500,000Accrued interest receivable 16,168 13,120

$ 27,016,168 $ 26,513,120

The term deposits with CUCM bear interest at rates ranging from 0.78% to 0.84% (2015 - .74% to.81%) and have original maturity dates of 120 days or less.

The fair value of the liquidity deposits at December 31, 2016 was $27,015,430 (2015 - $26,510,860).

The fair market value of liquidity deposits is calculated based on the present value of future cashflows. To determine present value, future cash flows are discounted by the current rate curve bywhich the asset or liability is originally priced. Rates used vary from 0.83% to 0.84% based onmaturity date and type of deposit.

Shares

These instruments are classified as available-for-sale and are initially recognized at fair value plustransaction costs that are directly attributable to their acquisition. Subsequently they are carried atfair value, unless they do not have a quoted market price in an active market and fair value is notreliably determinable in which case they are carried at cost.

Changes in fair value, except for those arising from interest calculated using the effective interestrate, are recognized as a separate component of other comprehensive income.

Where there is a significant or prolonged decline in the fair value of an equity instrument, whichconstitutes objective evidence of impairment, the full amount of the impairment, including anyamount previously recognized in other comprehensive income, is recognized in net income.

Purchases and sales of equity instruments are recognized on settlement date with any change in fairvalue between trade date and settlement date being recognized in accumulated othercomprehensive income.

On sale, the amount held in accumulated other comprehensive income associated with thatinstrument is removed from equity and recognized in net income.

20

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

10. Investments (continued)

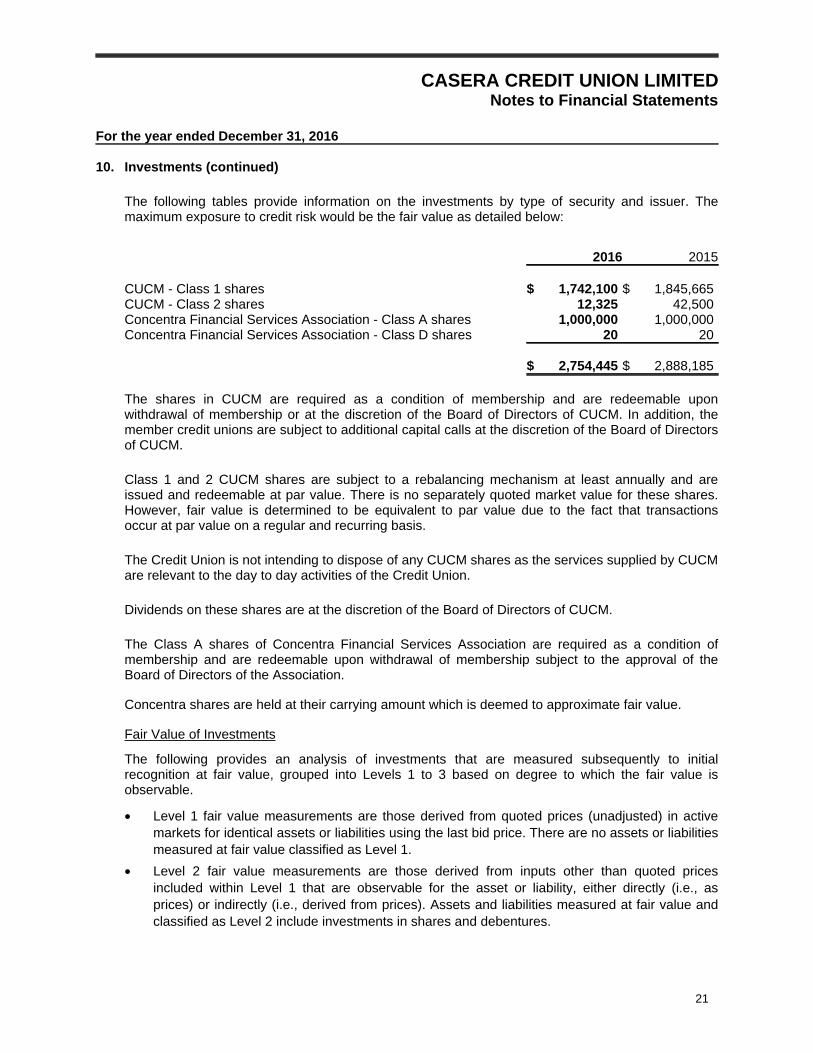

The following tables provide information on the investments by type of security and issuer. Themaximum exposure to credit risk would be the fair value as detailed below:

2016 2015

CUCM - Class 1 shares $ 1,742,100 $ 1,845,665CUCM - Class 2 shares 12,325 42,500Concentra Financial Services Association - Class A shares 1,000,000 1,000,000Concentra Financial Services Association - Class D shares 20 20

$ 2,754,445 $ 2,888,185

The shares in CUCM are required as a condition of membership and are redeemable uponwithdrawal of membership or at the discretion of the Board of Directors of CUCM. In addition, themember credit unions are subject to additional capital calls at the discretion of the Board of Directorsof CUCM.

Class 1 and 2 CUCM shares are subject to a rebalancing mechanism at least annually and areissued and redeemable at par value. There is no separately quoted market value for these shares.However, fair value is determined to be equivalent to par value due to the fact that transactionsoccur at par value on a regular and recurring basis.

The Credit Union is not intending to dispose of any CUCM shares as the services supplied by CUCMare relevant to the day to day activities of the Credit Union.

Dividends on these shares are at the discretion of the Board of Directors of CUCM.

The Class A shares of Concentra Financial Services Association are required as a condition ofmembership and are redeemable upon withdrawal of membership subject to the approval of theBoard of Directors of the Association.

Concentra shares are held at their carrying amount which is deemed to approximate fair value.

Fair Value of Investments

The following provides an analysis of investments that are measured subsequently to initialrecognition at fair value, grouped into Levels 1 to 3 based on degree to which the fair value isobservable.

• Level 1 fair value measurements are those derived from quoted prices (unadjusted) in activemarkets for identical assets or liabilities using the last bid price. There are no assets or liabilitiesmeasured at fair value classified as Level 1.

• Level 2 fair value measurements are those derived from inputs other than quoted pricesincluded within Level 1 that are observable for the asset or liability, either directly (i.e., asprices) or indirectly (i.e., derived from prices). Assets and liabilities measured at fair value andclassified as Level 2 include investments in shares and debentures.

21

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

10. Investments (continued)

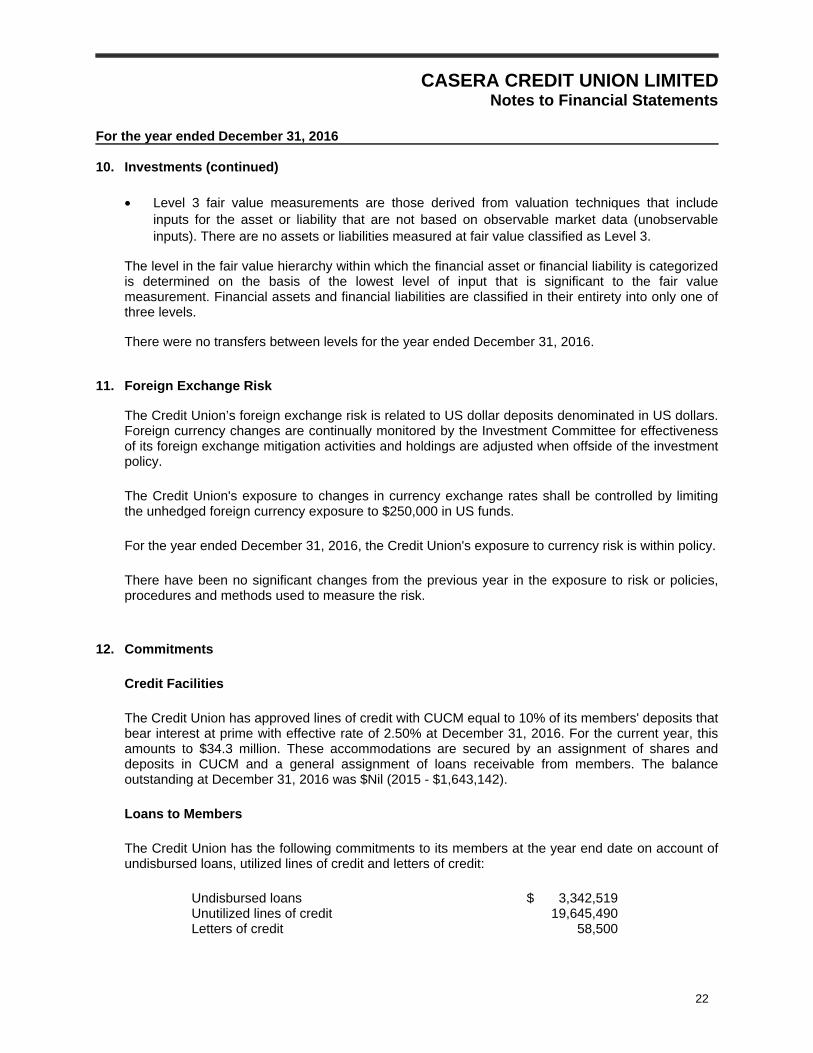

• Level 3 fair value measurements are those derived from valuation techniques that includeinputs for the asset or liability that are not based on observable market data (unobservableinputs). There are no assets or liabilities measured at fair value classified as Level 3.

The level in the fair value hierarchy within which the financial asset or financial liability is categorizedis determined on the basis of the lowest level of input that is significant to the fair valuemeasurement. Financial assets and financial liabilities are classified in their entirety into only one ofthree levels.

There were no transfers between levels for the year ended December 31, 2016.

11. Foreign Exchange Risk

The Credit Union’s foreign exchange risk is related to US dollar deposits denominated in US dollars.Foreign currency changes are continually monitored by the Investment Committee for effectivenessof its foreign exchange mitigation activities and holdings are adjusted when offside of the investmentpolicy.

The Credit Union's exposure to changes in currency exchange rates shall be controlled by limitingthe unhedged foreign currency exposure to $250,000 in US funds.

For the year ended December 31, 2016, the Credit Union's exposure to currency risk is within policy.

There have been no significant changes from the previous year in the exposure to risk or policies,procedures and methods used to measure the risk.

12. Commitments

Credit Facilities

The Credit Union has approved lines of credit with CUCM equal to 10% of its members' deposits thatbear interest at prime with effective rate of 2.50% at December 31, 2016. For the current year, thisamounts to $34.3 million. These accommodations are secured by an assignment of shares anddeposits in CUCM and a general assignment of loans receivable from members. The balanceoutstanding at December 31, 2016 was $Nil (2015 - $1,643,142).

Loans to Members

The Credit Union has the following commitments to its members at the year end date on account ofundisbursed loans, utilized lines of credit and letters of credit:

Undisbursed loans $ 3,342,519Unutilized lines of credit 19,645,490Letters of credit 58,500

22

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

12. Commitments (continued)

Contractual Obligations

Premises

The Credit Union has entered into operating leases for its premises. The following are the minimumlease payments for the next five years:

2017 $ 336,5032018 324,6562019 318,2052020 318,2052021 316,266

Other

Credit Union Central of Manitoba

The Credit Union is a member of CUCM, which provides banking and other services to CreditUnions in Manitoba. By nature of membership in CUCM, the Credit Union is obligated to payaffiliation dues which are based on membership and assets.

Deposit Guarantee Corporation of Manitoba

The Deposit Guarantee Corporation of Manitoba ("DGCM") is a deposit insurance corporation. Bylegal obligation under the Act, DGCM guarantees the deposits of all members of Manitoba CreditUnions/Caisse. By legislation, the Credit Union/Caisse pays a quarterly levy to DGCM based on apercentage of members' deposits.

Celero Solutions

The Credit Union has entered into an agreement with Celero Solutions to provide the delivery ofsome banking system services and the maintenance of the infrastructure needed to ensureuninterrupted delivery of such services. Celero Solutions is a company formed as a joint venture bythe Credit Union Centrals of Alberta, Saskatchewan and Manitoba along with Concentra Financialand Credit Union Electronic Transaction Services. The agreement expires in 2022.

13. Income Taxes

Income tax expense comprises current and deferred income tax. Current and deferred income taxesare recognized in net income except to the extent that it relates to a business combination, or itemsrecognized directly in equity or in other comprehensive income.

23

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

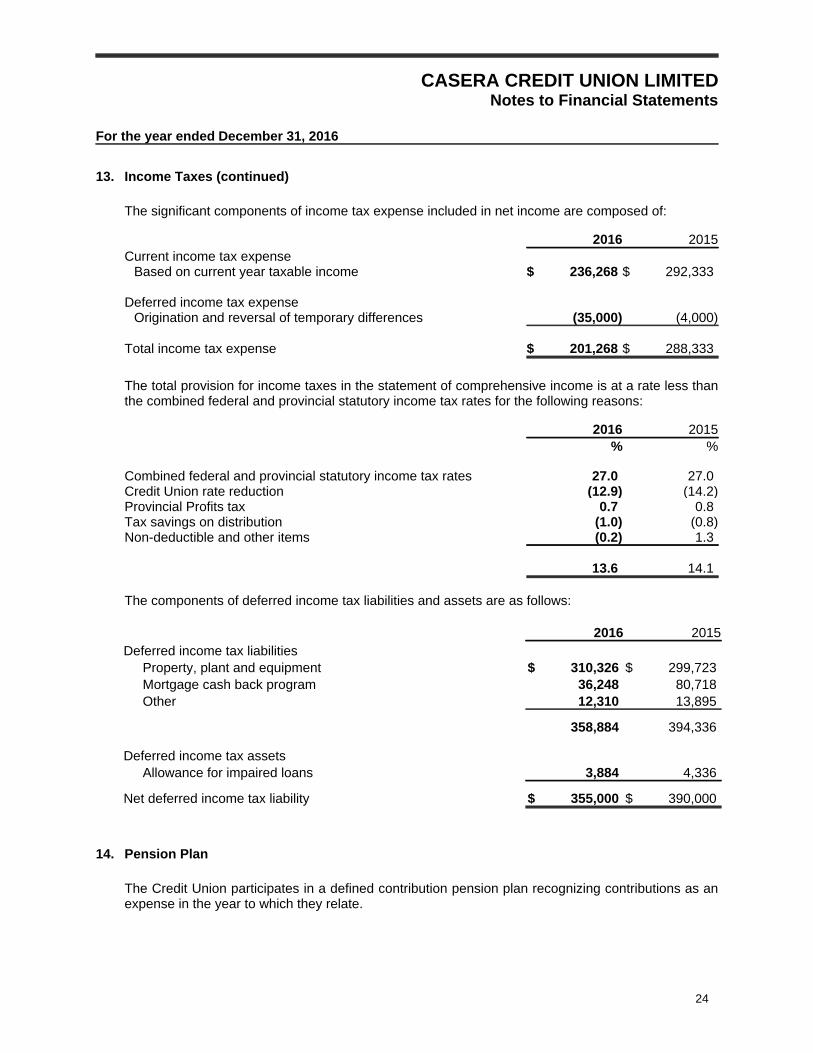

13. Income Taxes (continued)

The significant components of income tax expense included in net income are composed of:

2016 2015Current income tax expense

Based on current year taxable income $ 236,268 $ 292,333

Deferred income tax expenseOrigination and reversal of temporary differences (35,000) (4,000)

Total income tax expense $ 201,268 $ 288,333

The total provision for income taxes in the statement of comprehensive income is at a rate less thanthe combined federal and provincial statutory income tax rates for the following reasons:

2016 2015% %

Combined federal and provincial statutory income tax rates 27.0 27.0Credit Union rate reduction (12.9) (14.2)Provincial Profits tax 0.7 0.8Tax savings on distribution (1.0) (0.8)Non-deductible and other items (0.2) 1.3

13.6 14.1

The components of deferred income tax liabilities and assets are as follows:

2016 2015Deferred income tax liabilities

Property, plant and equipment $ 310,326 $ 299,723Mortgage cash back program 36,248 80,718Other 12,310 13,895

358,884 394,336

Deferred income tax assetsAllowance for impaired loans 3,884 4,336

Net deferred income tax liability $ 355,000 $ 390,000

14. Pension Plan

The Credit Union participates in a defined contribution pension plan recognizing contributions as anexpense in the year to which they relate.

24

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

14. Pension Plan (continued)

The Credit Union has a defined contribution pension plan for full-time employees. The contributionsare held in trust by the Cooperative Superannuation Society Limited and are not recorded in thesefinancial statements. The Credit Union matches employee contributions at a rate of 6% of theemployee salary. The expense for the year ended December 31, 2016 was $102,686 (2015 -$102,761). As a defined contribution pension plan, the Credit Union has no further liability orobligation for future contributions to fund benefits earned in 2016 for plan members.

15. Property, Plant and Equipment and Intangible Assets

Property, Plant and Equipment

Property, plant and equipment is initially recorded at cost and subsequently measured at cost lessaccumulated depreciation and any accumulated impairment losses, with the exception of land whichis not depreciated. Depreciation is recognized in net income and is provided on a straight-line basisover the estimated useful life of the assets as follows:

Buildings 40 yearsFurniture and equipment Up to 10 yearsComputer equipment 5 yearsSecurity equipment Up to 40 yearsSignage 10 yearsLeasehold improvements 15 years

Leasehold improvements are amortized over the remaining life of the lease.

Depreciation methods, useful lives and residual values are reviewed annually and adjusted ifnecessary.

Where it is not possible to estimate the recoverable amount of an individual asset, the impairmenttest is carried out on the asset's cash-generating unit, which is the lowest group of assets in whichthe asset belongs for which there are separately identifiable cash flows.

Impairment charges are included in net income, except to the extent they reverse gains previouslyrecognized in other comprehensive income.

2016 2015

Accumulated Net Book Net Book Cost Depreciation Value Value

Land $ 40,724 $ - $ 40,724 $ 40,724Buildings 1,655,318 1,389,616 265,702 320,232Furniture and equipment 1,051,130 732,769 318,361 376,372Computer equipment 398,956 210,355 188,601 188,408Security equipment 353,548 222,593 130,955 124,884Projects in process 75,125 - 75,125 231,820Leasehold improvements 1,034,981 792,311 242,670 299,561Signage 348,277 300,268 48,009 25,874

$ 4,958,059 $ 3,647,912 $ 1,310,147 $ 1,607,875

25

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

15. Property, Plant and Equipment and Intangible Assets (continued)

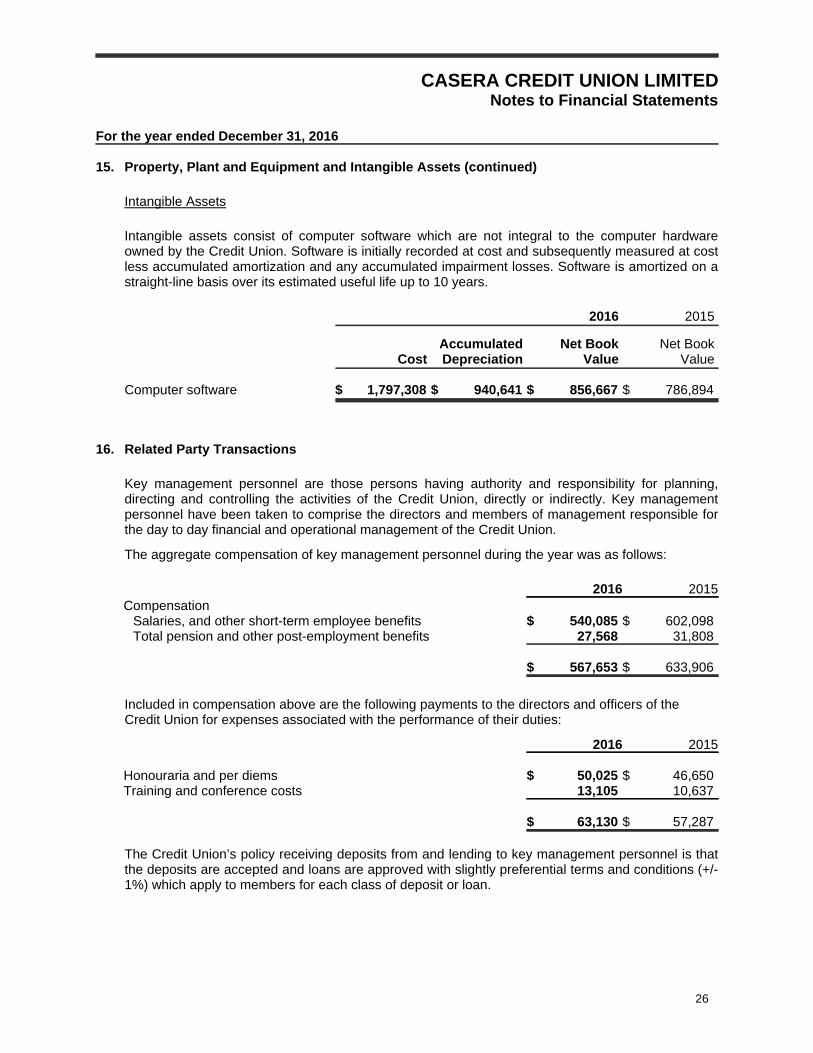

Intangible Assets

Intangible assets consist of computer software which are not integral to the computer hardwareowned by the Credit Union. Software is initially recorded at cost and subsequently measured at costless accumulated amortization and any accumulated impairment losses. Software is amortized on astraight-line basis over its estimated useful life up to 10 years.

2016 2015

Accumulated Net Book Net Book Cost Depreciation Value Value

Computer software $ 1,797,308 $ 940,641 $ 856,667 $ 786,894

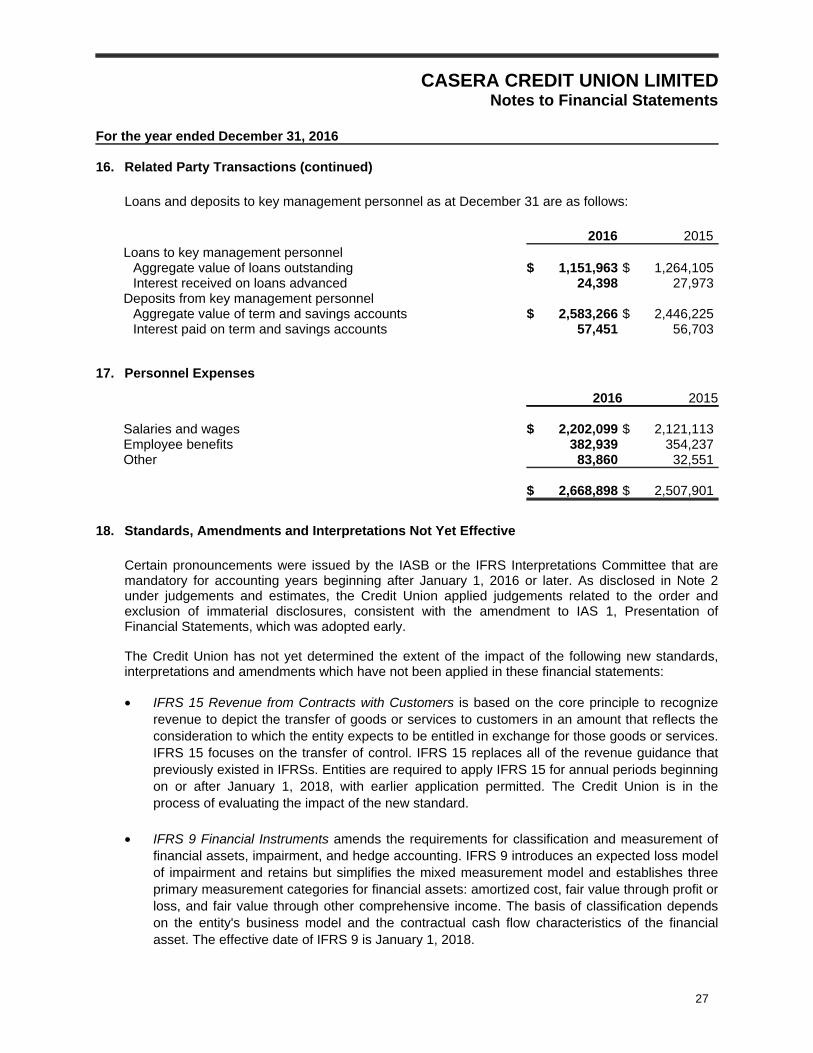

16. Related Party Transactions

Key management personnel are those persons having authority and responsibility for planning,directing and controlling the activities of the Credit Union, directly or indirectly. Key managementpersonnel have been taken to comprise the directors and members of management responsible forthe day to day financial and operational management of the Credit Union.

The aggregate compensation of key management personnel during the year was as follows:

2016 2015Compensation

Salaries, and other short-term employee benefits $ 540,085 $ 602,098Total pension and other post-employment benefits 27,568 31,808

$ 567,653 $ 633,906

Included in compensation above are the following payments to the directors and officers of theCredit Union for expenses associated with the performance of their duties:

2016 2015

Honouraria and per diems $ 50,025 $ 46,650Training and conference costs 13,105 10,637

$ 63,130 $ 57,287

The Credit Union’s policy receiving deposits from and lending to key management personnel is thatthe deposits are accepted and loans are approved with slightly preferential terms and conditions (+/-1%) which apply to members for each class of deposit or loan.

26

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

16. Related Party Transactions (continued)

Loans and deposits to key management personnel as at December 31 are as follows:

2016 2015Loans to key management personnel

Aggregate value of loans outstanding $ 1,151,963 $ 1,264,105Interest received on loans advanced 24,398 27,973

Deposits from key management personnelAggregate value of term and savings accounts $ 2,583,266 $ 2,446,225Interest paid on term and savings accounts 57,451 56,703

17. Personnel Expenses

2016 2015

Salaries and wages $ 2,202,099 $ 2,121,113Employee benefits 382,939 354,237Other 83,860 32,551

$ 2,668,898 $ 2,507,901

18. Standards, Amendments and Interpretations Not Yet Effective

Certain pronouncements were issued by the IASB or the IFRS Interpretations Committee that aremandatory for accounting years beginning after January 1, 2016 or later. As disclosed in Note 2under judgements and estimates, the Credit Union applied judgements related to the order andexclusion of immaterial disclosures, consistent with the amendment to IAS 1, Presentation ofFinancial Statements, which was adopted early.

The Credit Union has not yet determined the extent of the impact of the following new standards,interpretations and amendments which have not been applied in these financial statements:

• IFRS 15 Revenue from Contracts with Customers is based on the core principle to recognizerevenue to depict the transfer of goods or services to customers in an amount that reflects theconsideration to which the entity expects to be entitled in exchange for those goods or services.IFRS 15 focuses on the transfer of control. IFRS 15 replaces all of the revenue guidance thatpreviously existed in IFRSs. Entities are required to apply IFRS 15 for annual periods beginningon or after January 1, 2018, with earlier application permitted. The Credit Union is in theprocess of evaluating the impact of the new standard.

• IFRS 9 Financial Instruments amends the requirements for classification and measurement offinancial assets, impairment, and hedge accounting. IFRS 9 introduces an expected loss modelof impairment and retains but simplifies the mixed measurement model and establishes threeprimary measurement categories for financial assets: amortized cost, fair value through profit orloss, and fair value through other comprehensive income. The basis of classification dependson the entity's business model and the contractual cash flow characteristics of the financialasset. The effective date of IFRS 9 is January 1, 2018.

27

CASERA CREDIT UNION LIMITEDNotes to Financial Statements

For the year ended December 31, 2016

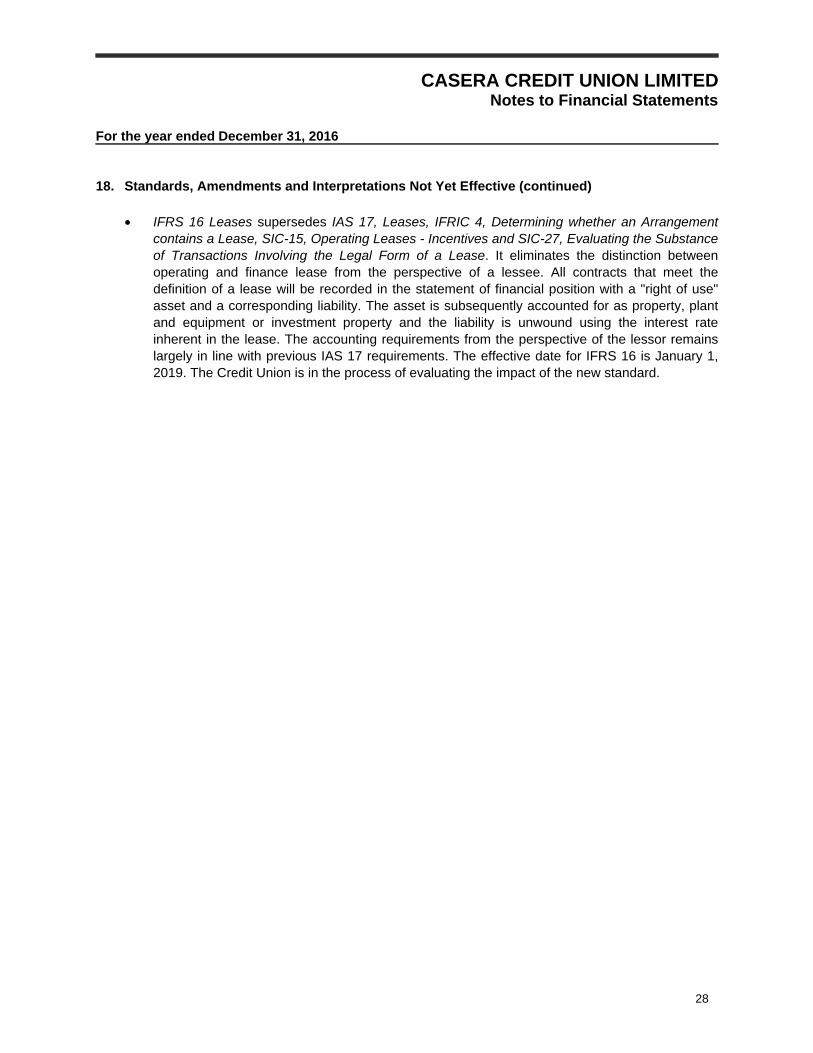

18. Standards, Amendments and Interpretations Not Yet Effective (continued)

• IFRS 16 Leases supersedes IAS 17, Leases, IFRIC 4, Determining whether an Arrangementcontains a Lease, SIC-15, Operating Leases - Incentives and SIC-27, Evaluating the Substanceof Transactions Involving the Legal Form of a Lease. It eliminates the distinction betweenoperating and finance lease from the perspective of a lessee. All contracts that meet thedefinition of a lease will be recorded in the statement of financial position with a "right of use"asset and a corresponding liability. The asset is subsequently accounted for as property, plantand equipment or investment property and the liability is unwound using the interest rateinherent in the lease. The accounting requirements from the perspective of the lessor remainslargely in line with previous IAS 17 requirements. The effective date for IFRS 16 is January 1,2019. The Credit Union is in the process of evaluating the impact of the new standard.

28