Embed Size (px)

Citation preview

1

Cans or CarsAluminium & the Automotive IndustryJLR Light Weight Vehicle (LWV) Strategy

Mark WhiteChief Technical SpecialistJaguar & Land Rover Cars Aluminium 200621st International Aluminium ConferenceMoscow 18/09/2006

2

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

3

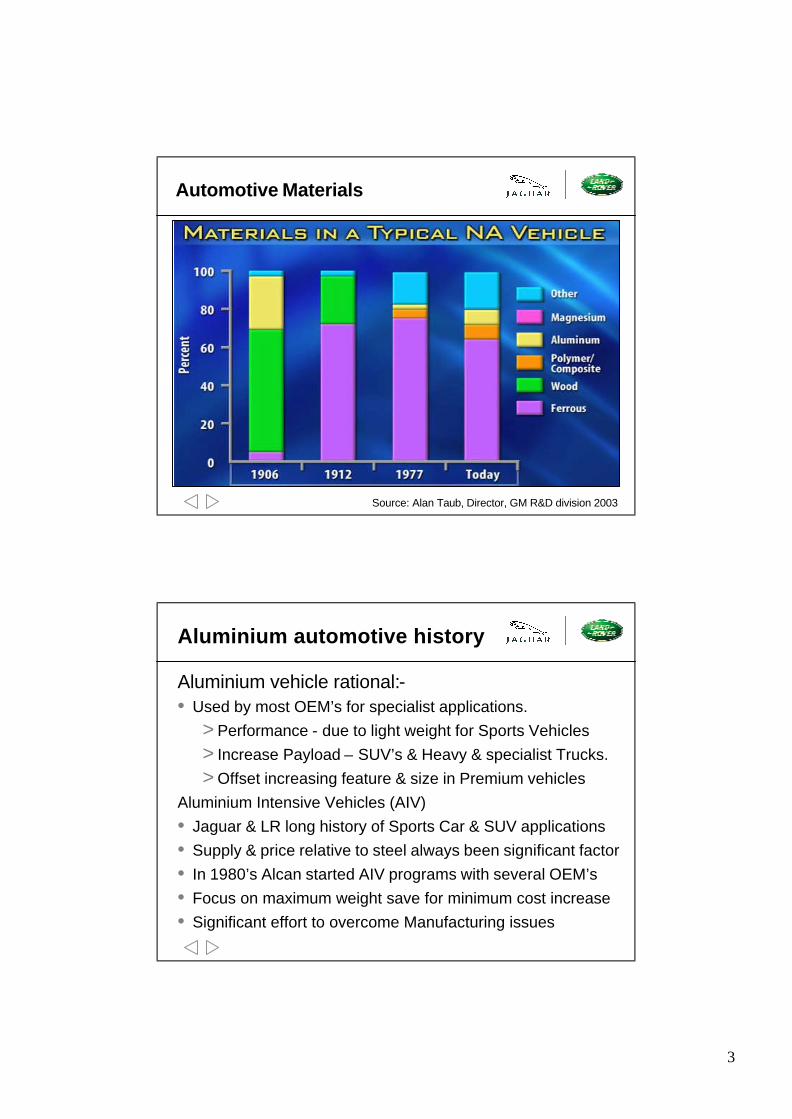

Automotive Materials

Source: Alan Taub, Director, GM R&D division 2003

Aluminium automotive history

Aluminium vehicle rational:-• Used by most OEM’s for specialist applications.

> Performance - due to light weight for Sports Vehicles> Increase Payload – SUV’s & Heavy & specialist Trucks.> Offset increasing feature & size in Premium vehicles

Aluminium Intensive Vehicles (AIV)• Jaguar & LR long history of Sports Car & SUV applications• Supply & price relative to steel always been significant factor• In 1980’s Alcan started AIV programs with several OEM’s• Focus on maximum weight save for minimum cost increase• Significant effort to overcome Manufacturing issues

4

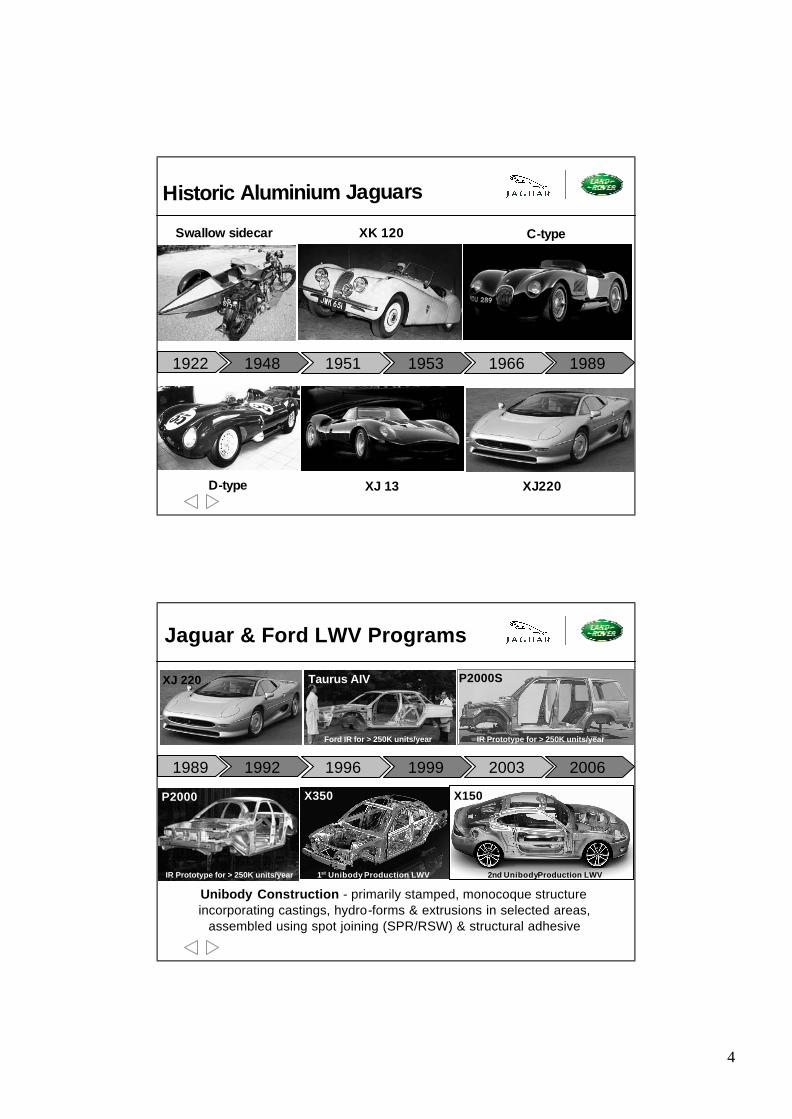

Historic Aluminium Jaguars

XK 120Swallow sidecar

XJ 13 XJ220

C-type

D-type

1922 1948 1951 1966 19891953

P2000 X350

Taurus AIV P2000S

Ford IR for > 250K units/year

1st Unibody Production LWVIR Prototype for > 250K units/year

IR Prototype for > 250K units/year

Unibody Construction - primarily stamped, monocoque structure incorporating castings, hydro-forms & extrusions in selected areas,

assembled using spot joining (SPR/RSW) & structural adhesive

Jaguar & Ford LWV Programs

X150

2nd UnibodyProduction LWV

1989 1992 1996 2003 20061999

XJ 220

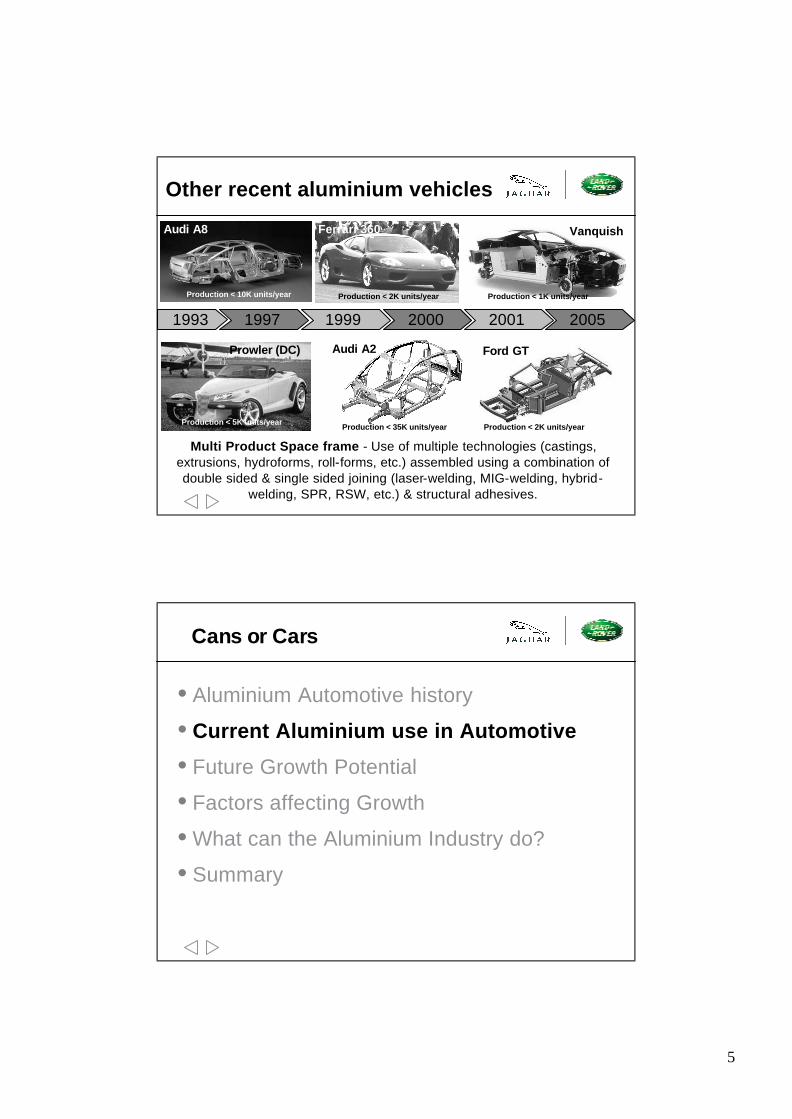

5

Multi Product Space frame - Use of multiple technologies (castings, extrusions, hydroforms, roll-forms, etc.) assembled using a combination of double sided & single sided joining (laser-welding, MIG-welding, hybrid-

welding, SPR, RSW, etc.) & structural adhesives.

Ford GT

VanquishAudi A8

Prowler (DC)

Production < 2K units/year

Production < 1K units/year

Production < 5K units/year

Audi A2

Other recent aluminium vehicles

Production < 35K units/year

Production < 10K units/year

1993 1997 1999 2001 20052000

Ferrari 360

Production < 2K units/year

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

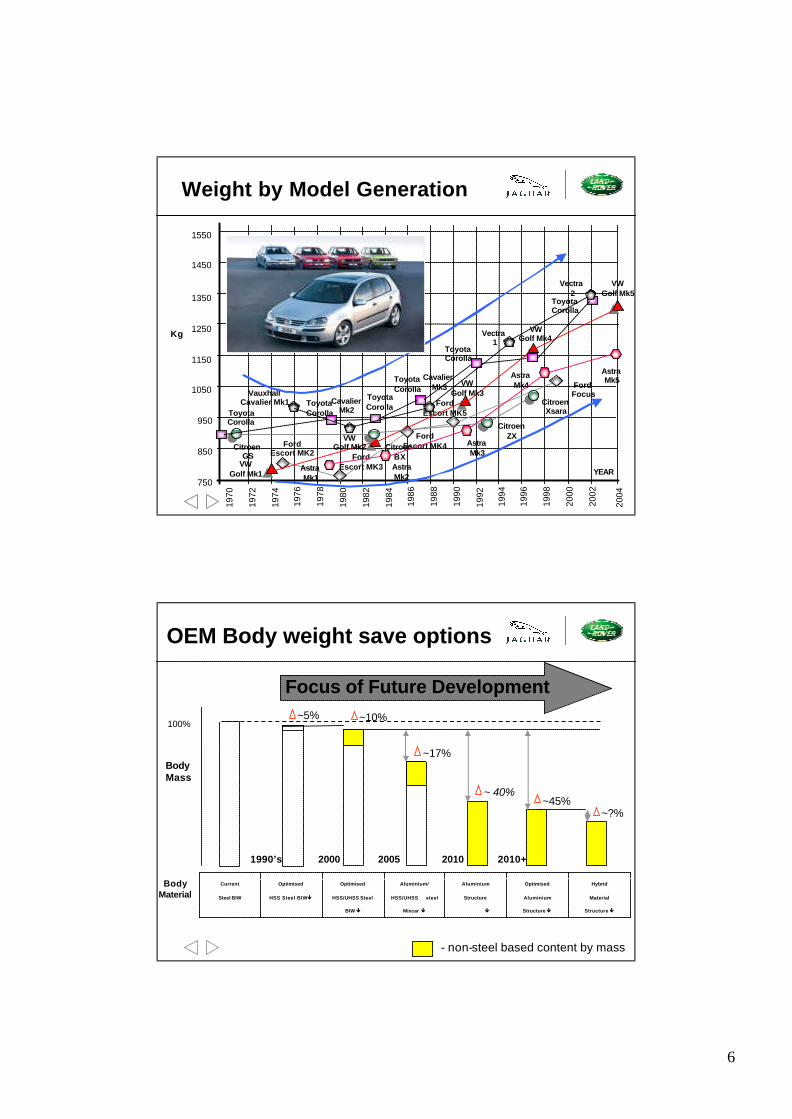

6

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

2000

1998

2002

750

950

1050

1150

1250

1350

850

1450

1550

FordEscort MK2 Ford

Escort MK3

FordEscort MK4

FordEscort MK5

FordFocus

VWGolf Mk1

VWGolf Mk4

2004

CitroenGS

CitroenBX

VWGolf Mk5

CitroenZX

CitroenXsaraToyota

Corolla

ToyotaCorolla

ToyotaCorolla

ToyotaCorolla

ToyotaCorolla

ToyotaCorolla

AstraMk1

AstraMk2

AstraMk3

AstraMk4

AstraMk5

VauxhallCavalier Mk1 Cavalier

Mk2

CavalierMk3

Vectra1

Vectra2

YEAR

Kg

Weight by Model Generation

VWGolf Mk3

VWGolf Mk2

OEM Body weight save options

BodyMaterial

Hybrid

Material

Structure ê

Optimised

Aluminium

Structure ê

Aluminium

Structure

ê

Aluminium/

HSS/UHSS steel

Mixcar ê

Optimised

HSS/UHSS Steel

BIW ê

Optimised

HSS Steel BIW ê

Current

Steel BIW

- non-steel based content by mass

Focus of Future Development

BodyMass

100%~5%

~45%

~17%

~10%

~?%

~ 40%

1990’s 2000 2005 2010 2010+

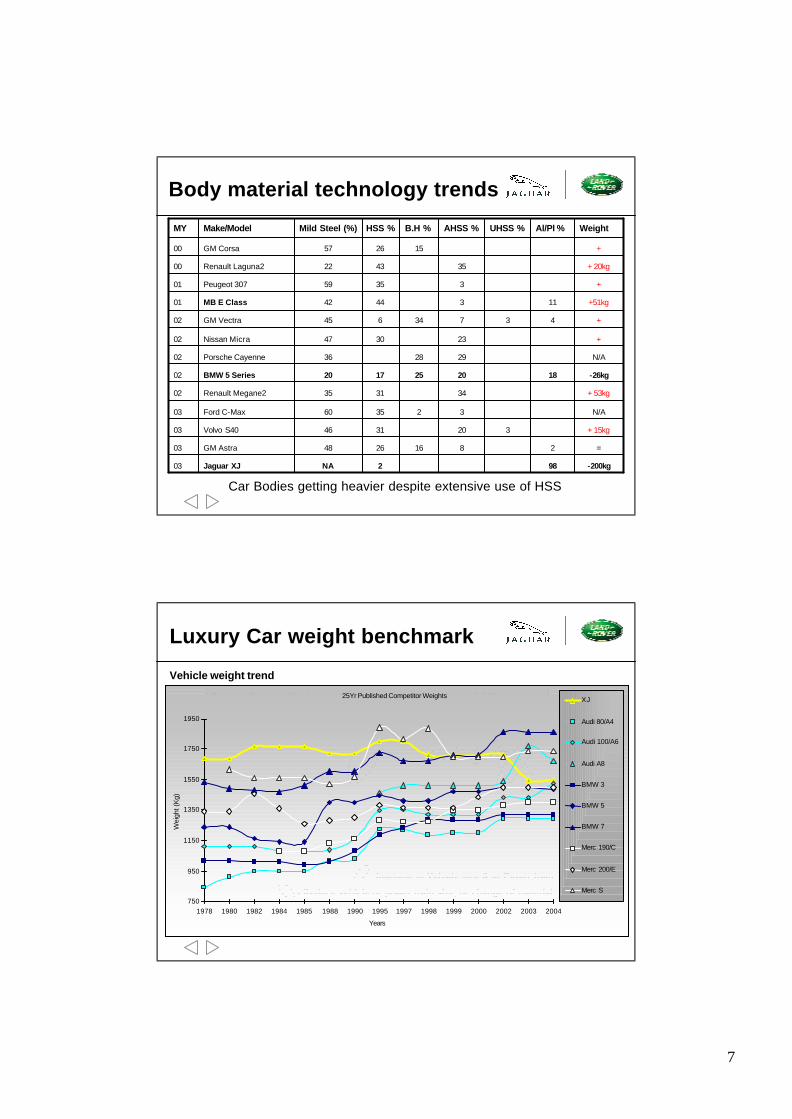

7

=28162648GM Astra03

98

18

4

11

Al/Pl %

3

3

UHSS %

N/A323560Ford C-Max03

+ 15kg203146Volvo S4003

N/A292836Porsche Cayenne02

-26kg20251720BMW 5 Series 02

+233047Nissan Micra02

+ 53kg343135Renault Megane202

-200kg2NAJaguar XJ03

+734645GM Vectra02

+51kg34442MB E Class01

+33559Peugeot 30701

+ 20kg354322Renault Laguna200

+152657GM Corsa00

Weight AHSS %B.H %HSS %Mild Steel (%)Make/ModelMY

Body material technology trends

Car Bodies getting heavier despite extensive use of HSS

Vehicle weight trend

Luxury Car weight benchmark

Data indicates all vehicle sectors increased in weight 10-20kg per year average despite use of new materials on new models

- Increase in Vehicle size & or Power train

- Reduce vehicle or power train size, or change of material

25Yr Published Competitor Weights

750

950

1150

1350

1550

1750

1950

1978 1980 1982 1984 1985 1988 1990 1995 1997 1998 1999 2000 2002 2003 2004

Years

Wei

ght (

Kg)

XJ

Audi 80/A4

Audi 100/A6

Audi A8

BMW 3

BMW 5

BMW 7

Merc 190/C

Merc 200/E

Merc S

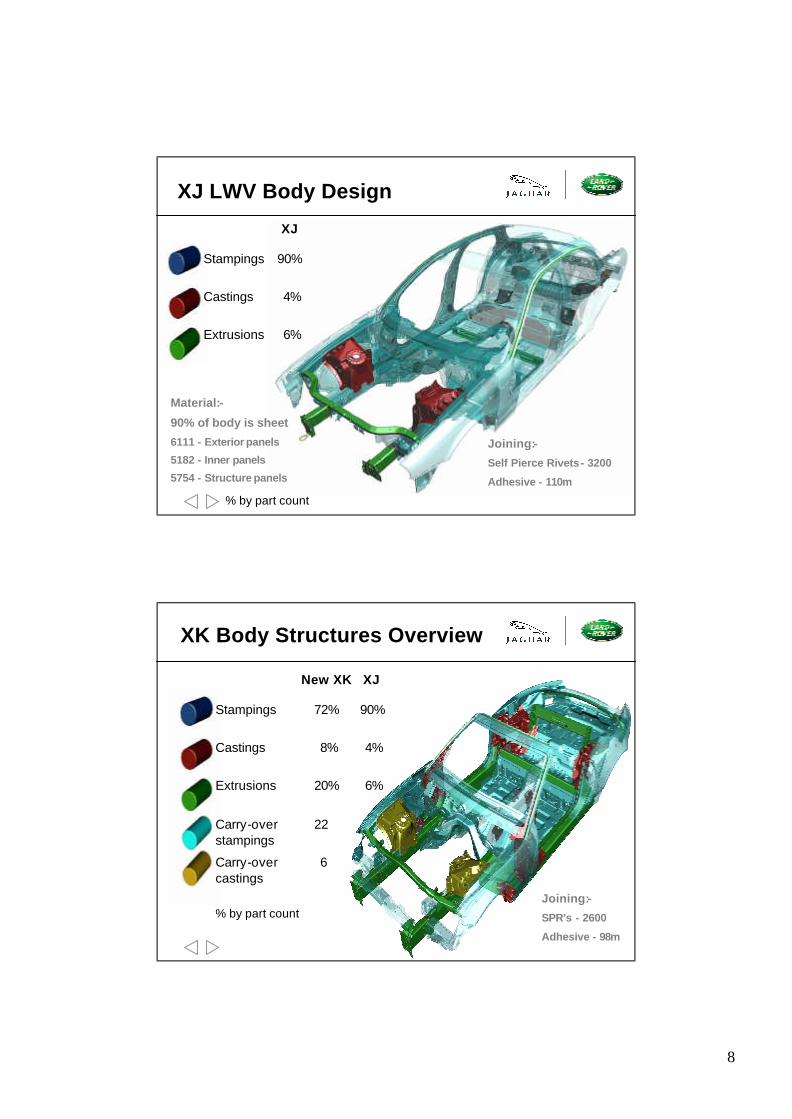

8

Stampings

Castings

Extrusions

XJ

90%

4%

6%

% by part count

XJ LWV Body Design

Material:-

90% of body is sheet

6111 - Exterior panels

5182 - Inner panels

5754 - Structure panels

Joining:-

Self Pierce Rivets - 3200

Adhesive - 110m

XK Body Structures Overview

Stampings

Castings

Extrusions

Carry-overstampings

Carry-overcastings

New XK XJ

72% 90%

8% 4%

20% 6%

22

6

% by part countJoining:-

SPR’s - 2600

Adhesive - 98m

9

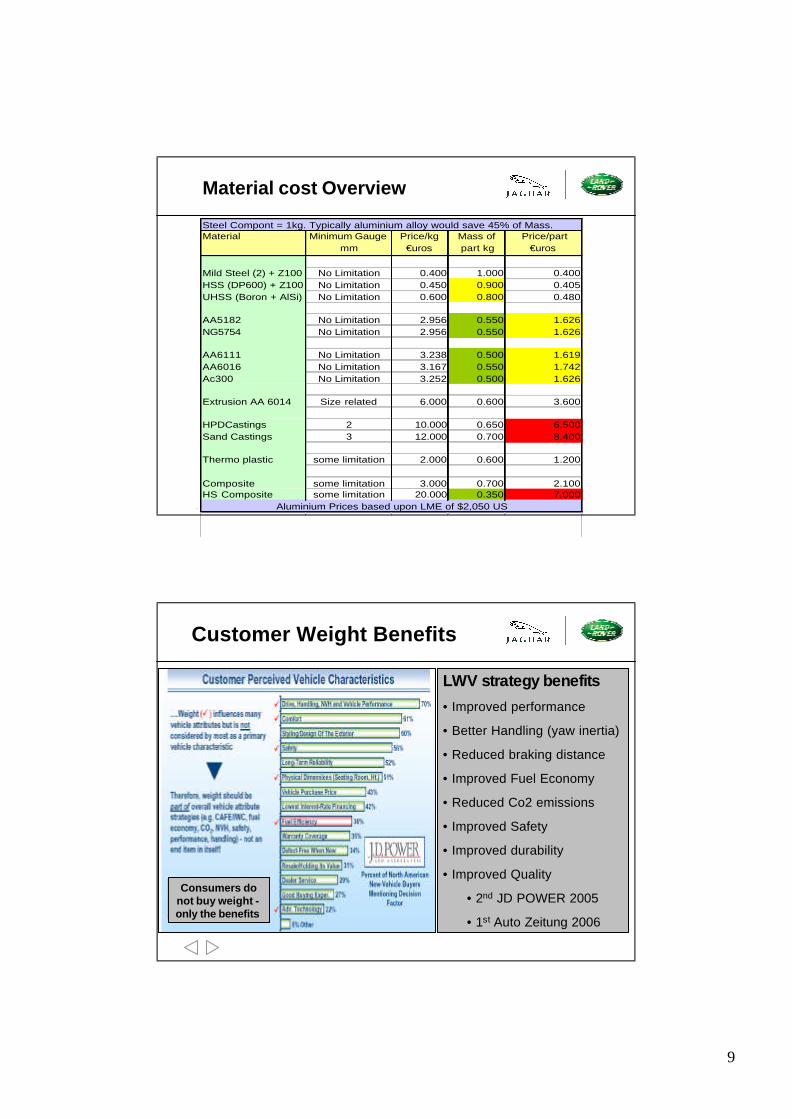

Material cost Overview

Steel Compont = 1kg. Typically aluminium alloy would save 45% of Mass.

Mild Steel (2) + Z100 No Limitation 0.400 1.000 0.400HSS (DP600) + Z100 No Limitation 0.450 0.900 0.405UHSS (Boron + AlSi) No Limitation 0.600 0.800 0.480

AA5182 No Limitation 2.956 0.550 1.626NG5754 No Limitation 2.956 0.550 1.626

AA6111 No Limitation 3.238 0.500 1.619AA6016 No Limitation 3.167 0.550 1.742Ac300 No Limitation 3.252 0.500 1.626

Extrusion AA 6014 Size related 6.000 0.600 3.600

HPDCastings 2 10.000 0.650 6.500Sand Castings 3 12.000 0.700 8.400

Thermo plastic some limitation 2.000 0.600 1.200

Composite some limitation 3.000 0.700 2.100HS Composite some limitation 20.000 0.350 7.000

Aluminium Prices based upon LME of $2,050 US

Price/part €uros

Material Minimum Gauge mm

Price/kg €uros

Mass of part kg

Customer Weight Benefits

Consumers do not buy weight -only the benefits

LWV strategy benefits• Improved performance

• Better Handling (yaw inertia)

• Reduced braking distance

• Improved Fuel Economy

• Reduced Co2 emissions

• Improved Safety

• Improved durability

• Improved Quality

• 2nd JD POWER 2005

• 1st Auto Zeitung 2006

10

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

Automotive Industry overview

• The Automotive industry is the Biggest in the world> Cars £900bn> Commercial Vehicles £225bn> Parts £150bn

• Predicted Continued future growth

> More cars made in next 20 years than the last 110

• World wide production expected to top 60m by 2020

• Significant increase from Only 40m in 2000

11

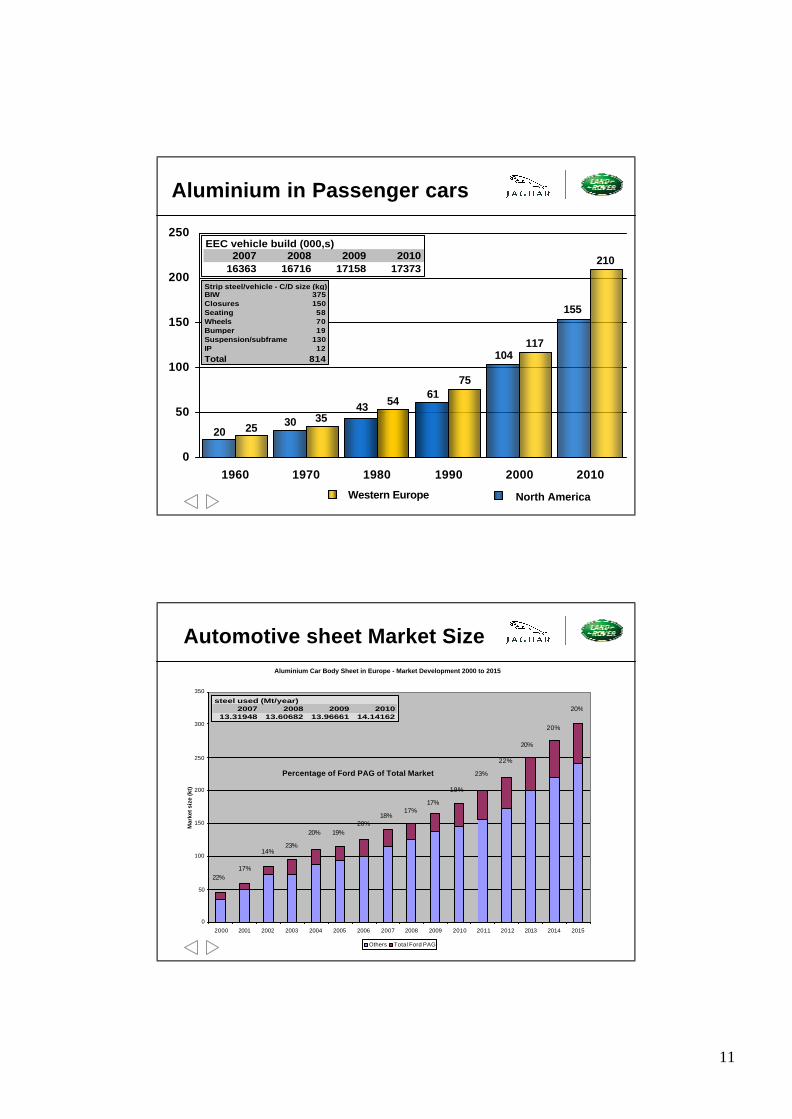

Western Europe North America

Aluminium in Passenger cars

155

104

6143

3020 25

35

54

75

117

210

0

50

100

150

200

250

1960 1970 1980 1990 2000 2010

EEC vehicle build (000,s)2007 2008 2009 2010

16363 16716 17158 17373

Strip steel/vehicle - C/D size (kg)BIW 375Closures 150Seating 58Wheels 70Bumper 19Suspension/subframe 130IP 12

Total 814

Aluminium Car Body Sheet in Europe - Market Development 2000 to 2015

0

50

100

150

200

250

300

350

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Mar

ket s

ize

(kt)

Others Total Ford PAG

Percentage of Ford PAG of Total Market

22%17%

14%23%

20% 19%20%

18%17%

17%

19%

23%

22%

20%

20%

20%steel used (Mt/year)

2007 2008 2009 201013.31948 13.60682 13.96661 14.14162

Automotive sheet Market Size

12

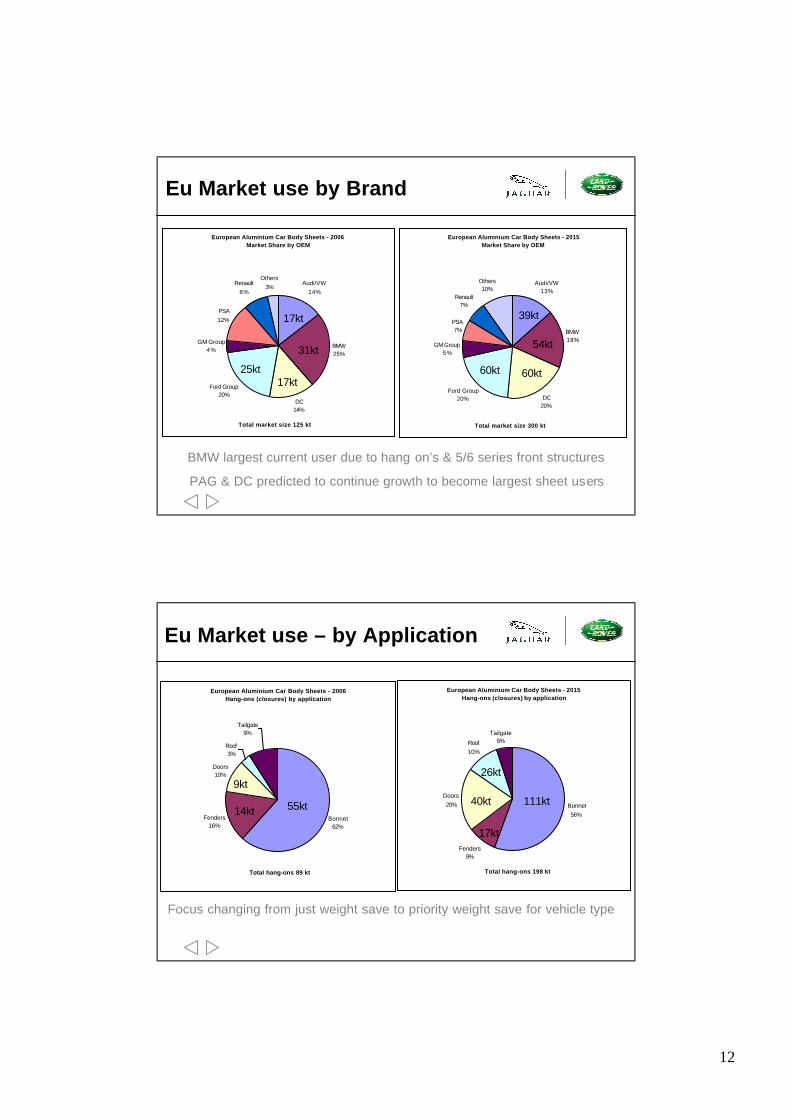

Eu Market use by Brand

European Aluminium Car Body Sheets - 2006Market Share by OEM

Audi/VW14%

BMW25%

DC14%

Ford Group20%

GM Group4%

PSA12%

Renault8%

Others3%

Total market size 125 kt

European Aluminium Car Body Sheets - 2015Market Share by OEM

Audi/VW13%

BMW18%

DC20%

Ford Group20%

GM Group5%

PSA7%

Renault7%

Others10%

Total market size 300 kt

31kt

17kt

17kt25kt 60kt 60kt

54kt

39kt

BMW largest current user due to hang on’s & 5/6 series front structures

PAG & DC predicted to continue growth to become largest sheet users

Eu Market use – by Application

European Aluminium Car Body Sheets - 2015Hang-ons (closures) by application

Bonnet56%

Fenders9%

Doors20%

Roof10%

Tailgate5%

Total hang-ons 198 kt

European Aluminium Car Body Sheets - 2006Hang-ons (closures) by application

Bonnet62%

Fenders16%

Doors10%

Roof3%

Tailgate9%

Total hang-ons 89 kt

55kt14kt

9kt

40kt 111kt

26kt

17kt

Focus changing from just weight save to priority weight save for vehicle type

13

Eu Market use – BIW Structure

European Aluminium Car Body Sheets - 2015BIW structure

Front module80%

behind A-pillar20%

Total BIW structure 102 kt

82kt

20kt

European Aluminium Car Body Sheets - 2006BIW structure

Front module72%

behind A-pillar

Total BIW structure 36 kt

26kt

10kt

28%

Cast Al.

Ext. Al.

Sheet Al.

Sheet Steel31%

31%

22%

16%

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

14

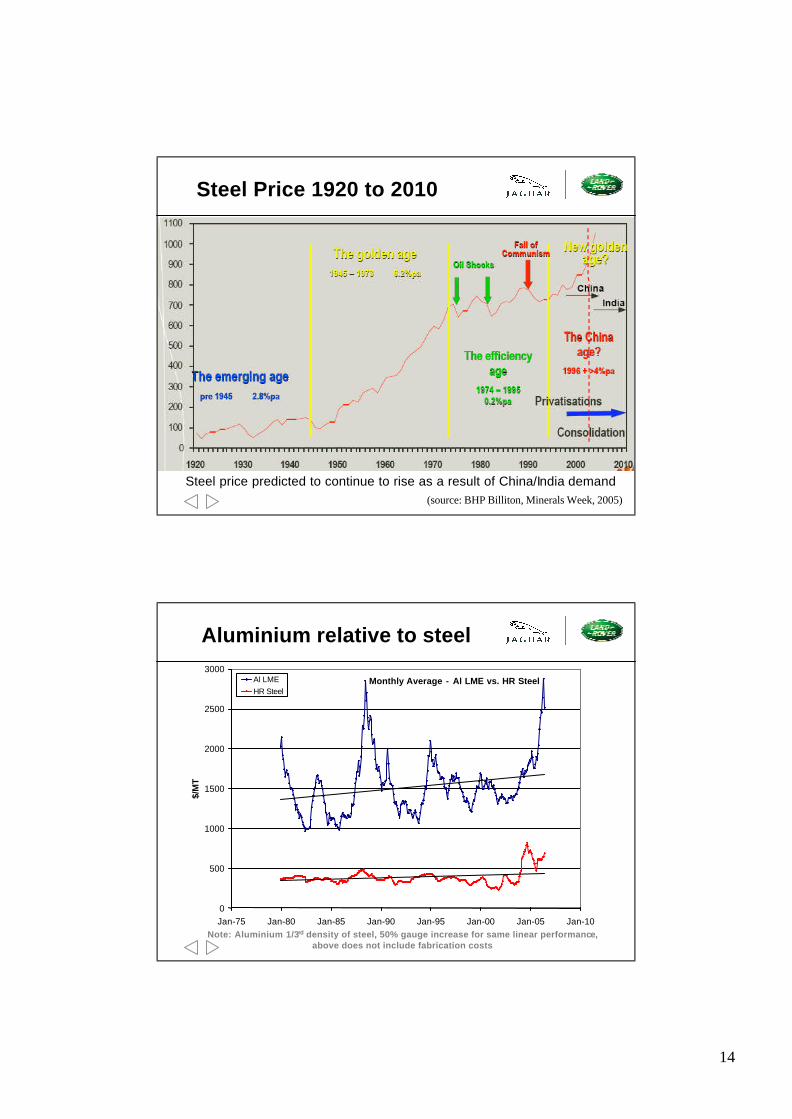

Steel Price 1920 to 2010

(source: BHP Billiton, Minerals Week, 2005)

Steel price predicted to continue to rise as a result of China/India demand

Monthly Average - Al LME vs. HR Steel

0

500

1000

1500

2000

2500

3000

Jan-75 Jan-80 Jan-85 Jan-90 Jan-95 Jan-00 Jan-05 Jan-10

$/M

T

Al LMEHR Steel

Aluminium relative to steel

Note: Aluminium 1/3rd density of steel, 50% gauge increase for same linear performance, above does not include fabrication costs

15

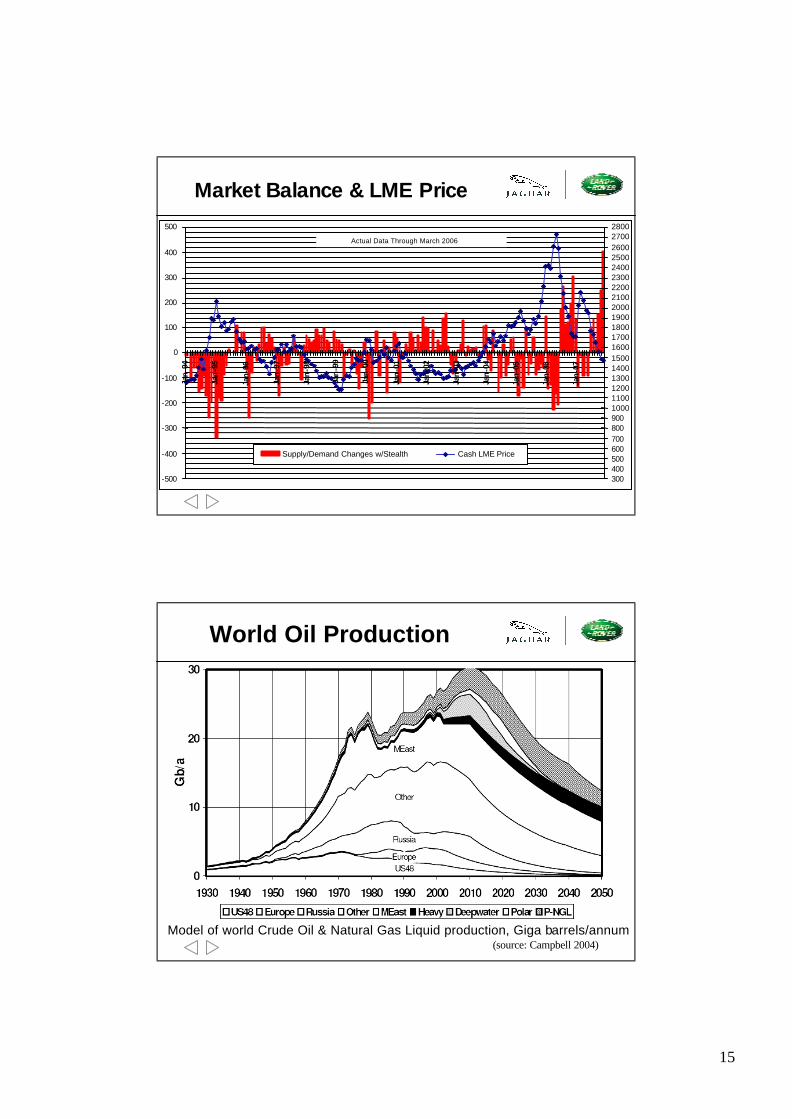

Market Balance & LME Price

-500

-400

-300

-200

-100

0

100

200

300

400

500

Jan

-94

Jan

-95

Jan

-96

Jan

-97

Jan

-98

Jan

-99

Jan

-00

Jan

-01

Jan

-02

Jan

-03

Jan

-04

Jan

-05

Jan

-06

Jan

-07

3004005006007008009001000110012001300140015001600170018001900200021002200230024002500260027002800

Supply/Demand Changes w/Stealth Cash LME Price

Actual Data Through March 2006

World Oil Production

Model of world Crude Oil & Natural Gas Liquid production, Giga barrels/annum(source: Campbell 2004)

16

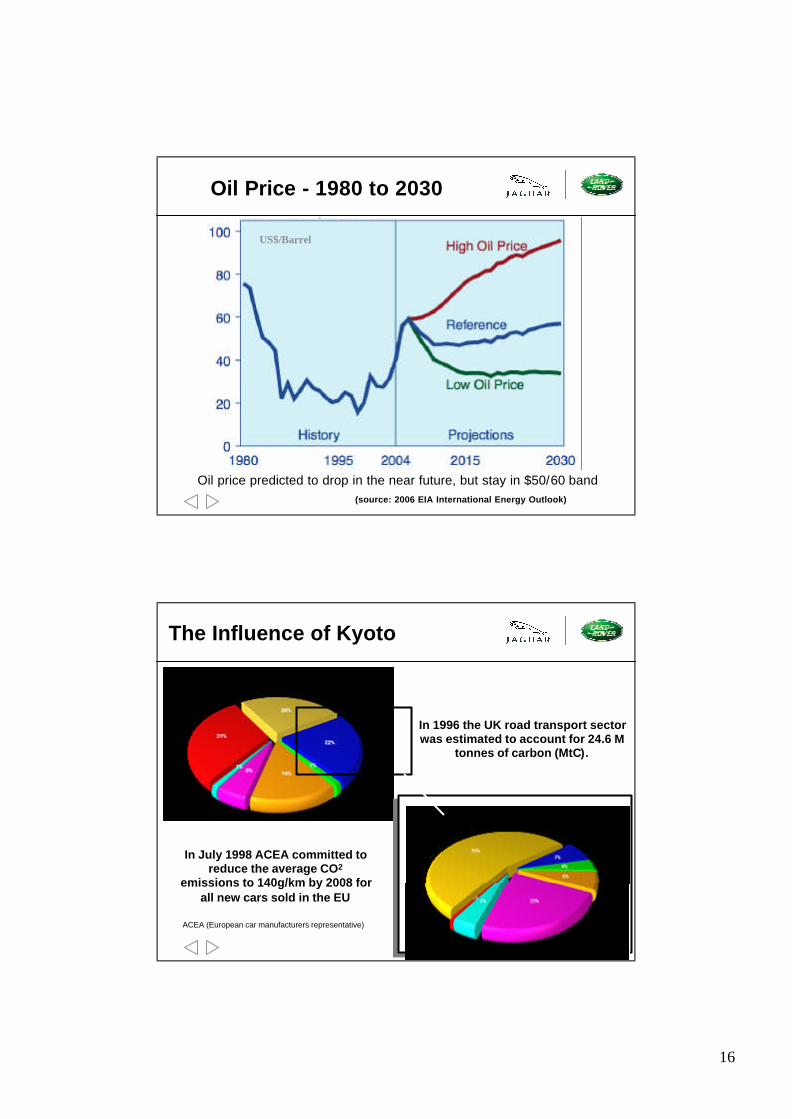

Oil Price - 1980 to 2030

Oil price predicted to drop in the near future, but stay in $50/60 band (source: 2006 EIA International Energy Outlook)

US$/Barrel

The Influence of Kyoto

In 1996 the UK road transport sector was estimated to account for 24.6 M

tonnes of carbon (MtC).

In July 1998 ACEA committed to reduce the average CO2

emissions to 140g/km by 2008 for all new cars sold in the EU

ACEA (European car manufacturers representative)

17

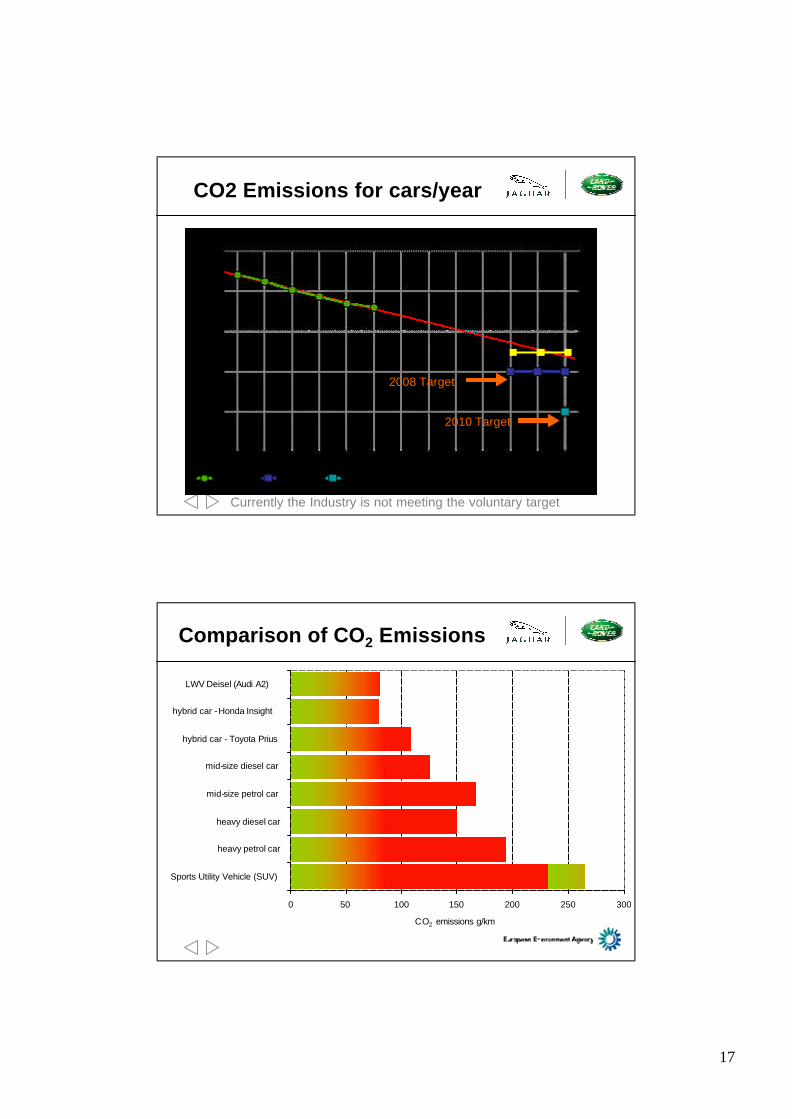

CO2 Emissions for cars/year

2008 Target

2010 Target

Currently the Industry is not meeting the voluntary target

Comparison of CO2 Emissions

0 50 100 150 200 250 300

Sports Utility Vehicle (SUV)

heavy petrol car

heavy diesel car

mid-size petrol car

mid-size diesel car

hybrid car - Toyota Prius

hybrid car -Honda Insight

LWV Deisel (Audi A2)

CO2 emissions g/km

18

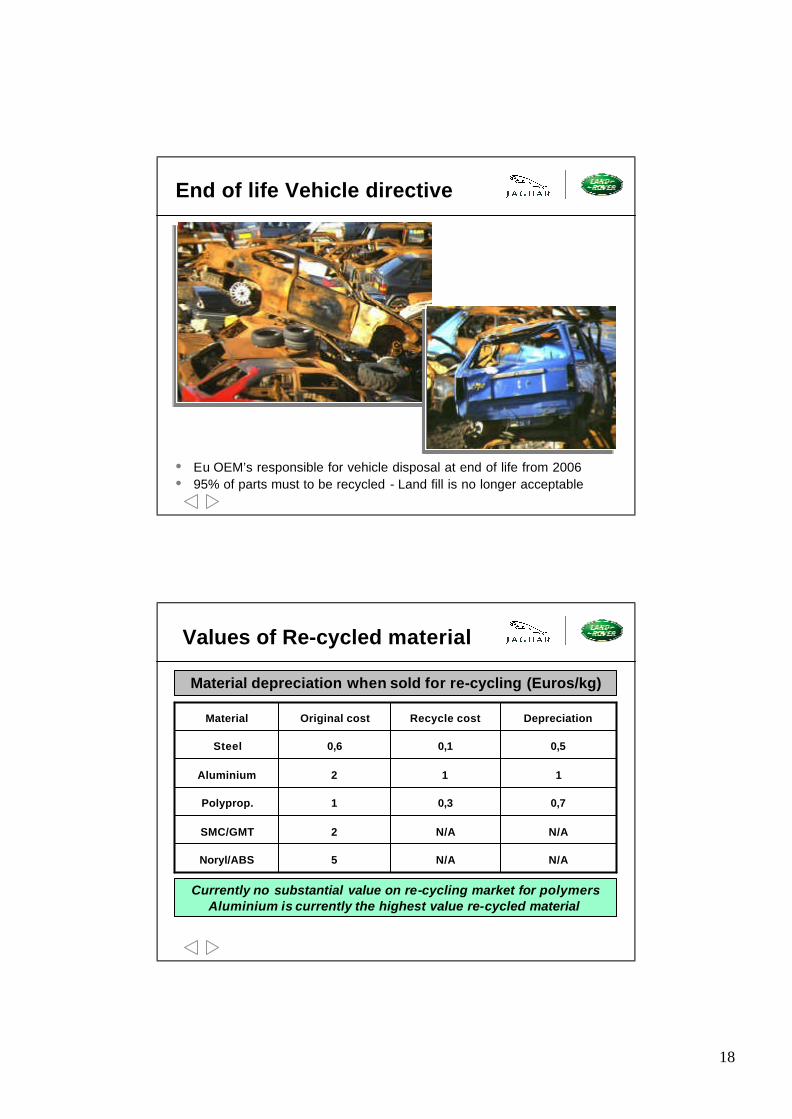

End of life Vehicle directive

• Eu OEM’s responsible for vehicle disposal at end of life from 2006• 95% of parts must to be recycled - Land fill is no longer acceptable

Values of Re-cycled material

Currently no substantial value on re-cycling market for polymersAluminium is currently the highest value re-cycled material

Material depreciation when sold for re-cycling (Euros/kg)

N/AN/A5Noryl/ABS

N/AN/A2SMC/GMT

0,70,31Polyprop.

112Aluminium

0,50,10,6Steel

DepreciationRecycle costOriginal costMaterial

19

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What Can the Aluminium Industry do?

• Summary

Cans or Cars

$395.00

$290.00

$280.00

$311.00

$135.00

Alumina

Energy

Labour

Overhead

Capital Recovery

0

$200

$400

$600

$800

$1000

$1200

$1400

$1600

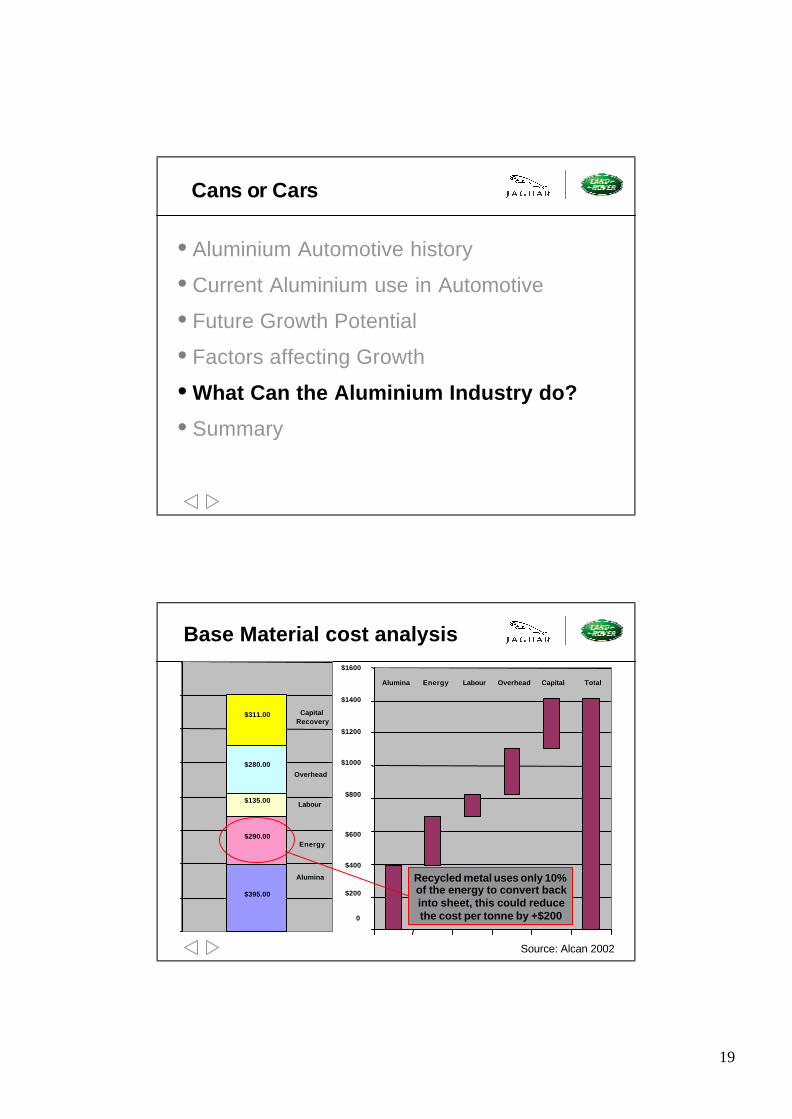

Alumina Energy Labour Overhead Capital Total

Base Material cost analysis

Recycled metal uses only 10% of the energy to convert back into sheet, this could reduce the cost per tonne by +$200

Source: Alcan 2002

20

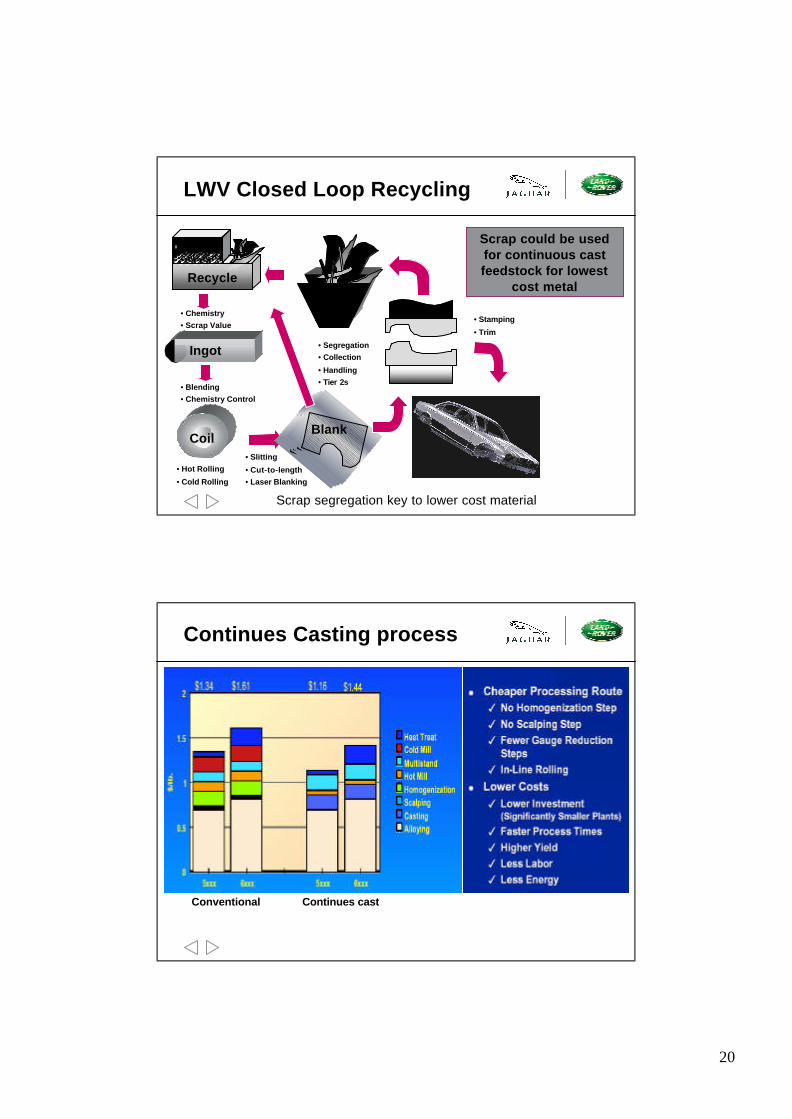

Ingot

Coil

• Chemistry • Scrap Value

• Blending• Chemistry Control

• Hot Rolling

• Cold Rolling

Recycle

Scrap

Blank

• Segregation• Collection

• Handling• Tier 2s

• Slitting

• Cut-to-length• Laser Blanking

Stamping• Stamping

• Trim

LWV Closed Loop Recycling

Scrap segregation key to lower cost material

Scrap could be used for continuous cast feedstock for lowest

cost metal

Continues Casting process

Conventional Continues cast

21

Continuous Cast Growth

Continuous Casting Capacity 1960-1999

Source: Monitor analysis, CRU, Press, Light Metal Age

Cumulative Capacity

(ktpa)

North America

Latin America

Western Europe

Eastern Europe

Asia-Pacific

Middle East & Africa

0

1000

2000

3000

4000

5000

6000

7000

60 62 64 66 68 70 72 74 76 78 80 82 84 86 88 90 92 94 96 98

• Aluminium Automotive history

• Current Aluminium use in Automotive

• Future Growth Potential

• Factors affecting Growth

• What can the Aluminium Industry do?

• Summary

Cans or Cars

22

• Cost/kg still dominant factor in restricting growth

• Industry needs to close the gap relative to steel

• Stable pricing required for future business planning

• External Pressures likely to drive Growth rate

• Review short term profits relative to future growth

Summary

Finally it is down to the aluminium Industry to choice

Cans or Cars?

Cans or Cars?

Thank you for Listening