Embed Size (px)

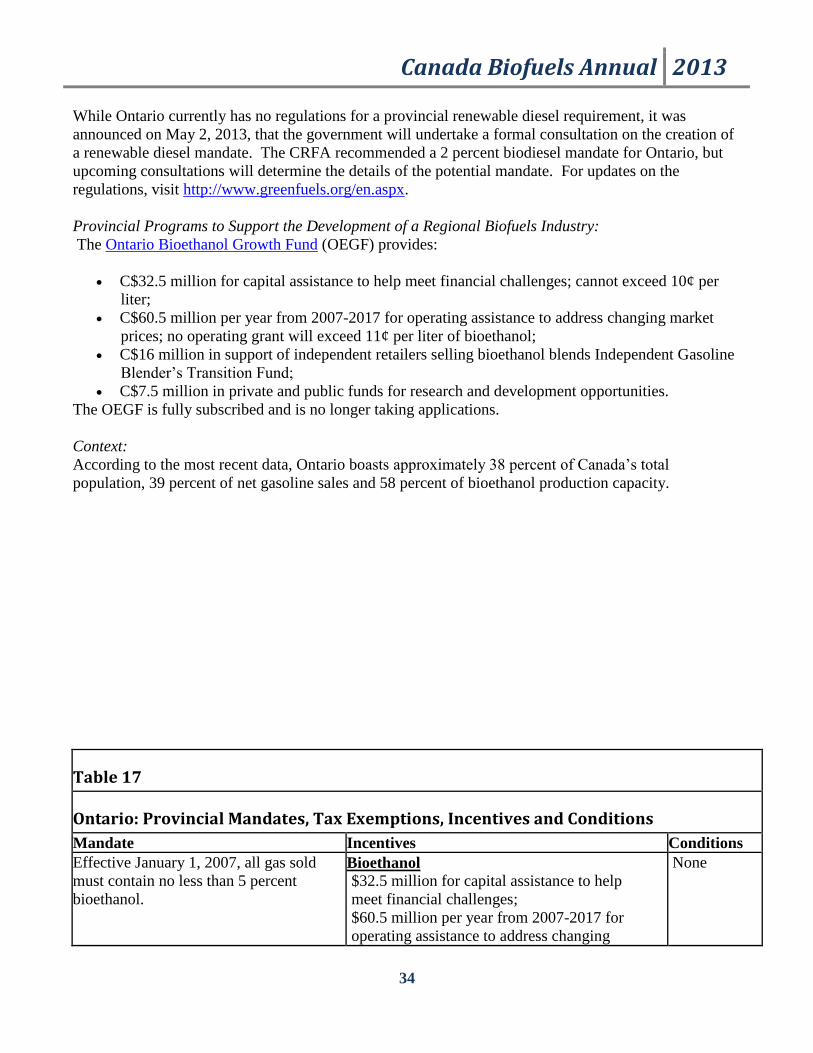

Citation preview

THIS REPORT CONTAINS ASSESSMENTS OF COMMODITY AND TRADE ISSUES MADE BY

USDA STAFF AND NOT NECESSARILY STATEMENTS OF OFFICIAL U.S. GOVERNMENT

POLICY

Date:

GAIN Report Number:

Approved By:

Prepared By:

Report Highlights:

On July 1, 2011, Canada implemented a federal mandate of 2 percent renewable content in the national

distillate pool. Proposed regulations, published in the Canada Gazette on May 18, 2013, will extend the

Atlantic exemption period until June 30, 2013, and permanently exempt diesel heating oil from the 2

percent renewable content requirement. These regulations are in addition to the mandate of 5 percent

renewable content in the national gasoline pool. As the Canadian biofuels industry is continuing

compliance preparation, ethanol and biodiesel production has grown in recent years. Ethanol

production in 2013 is estimated to increase about 4 percent from 2012 levels, and biodiesel production

is estimated to more than double due to new production facilities. At this time, the Canadian biofuels

industry remains below Post’s estimates to meet the federal standards, and limited production suggests

that Canada will not soon become a major player in the global ethanol market.

Brent Evans

Robin Gray

2013

Biofuels Annual

Canada

CA13034

6/28/2013

Required Report - public distribution

Canada Biofuels Annual 2013

2

Contents I. Executive Summary ................................................................................................................... 3

II. Policy and Programs.................................................................................................................. 4

Context: Canada’s Overall Energy Situation ........................................................................ 4

A. National Biofuels Mandate ................................................................................................ 6

B. Federal Programs to Encourage the Development of a Canadian Renewable Fuels Industry

................................................................................................................................................. 7

C. Provincial Mandates and Programs to Encourage Renewable Fuels Industry Development............................................................................................................................................... 10

Cap-And-Trade Research ..................................................................................................... 11

D. Factors Affecting the Long-term Viability of a Canadian Biofuel Industry ................ 11

III. Ethanol .................................................................................................................................... 13

A. Production ...................................................................................................................... 14

B. Impacts of Ethanol Production on Feedstock Markets .................................................. 15

i. Ethanol Produced from Corn.......................................................................................... 15

ii. Ethanol Produced from Wheat ....................................................................................... 15

C. Consumption................................................................................................................... 16

D. Trade .............................................................................................................................. 16

E. Ending Stocks ................................................................................................................. 17

IV. Biodiesel ................................................................................................................................. 17

A. Biodiesel Production ...................................................................................................... 19

B. Impacts of Biodiesel Production on Feedstock Markets ................................................ 20

C. Consumption................................................................................................................... 20

D. Biodiesel Trade .............................................................................................................. 21

E. Ending Stocks ................................................................................................................. 22

V. Advanced Biofuels ................................................................................................................. 22

VI. Biomass for Heat and Power .................................................................................................. 22

A. Wood Pellets .................................................................................................................... 23

B. Fuels Produced from Other Biomass .............................................................................. 24

Appendix I: Transport Fuel and Energy Consumption ................................................................. 26

Appendix II: Provincial Mandates, Policies, Tax Exemptions, Incentives, and Conditions ........ 28

A. Alberta Biofuel Policies ................................................................................................. 28

B. British Columbia Biofuel Policies .................................................................................. 30

C. Manitoba Biofuel Policies .............................................................................................. 32

D. Ontario Biofuel Policies ................................................................................................. 33

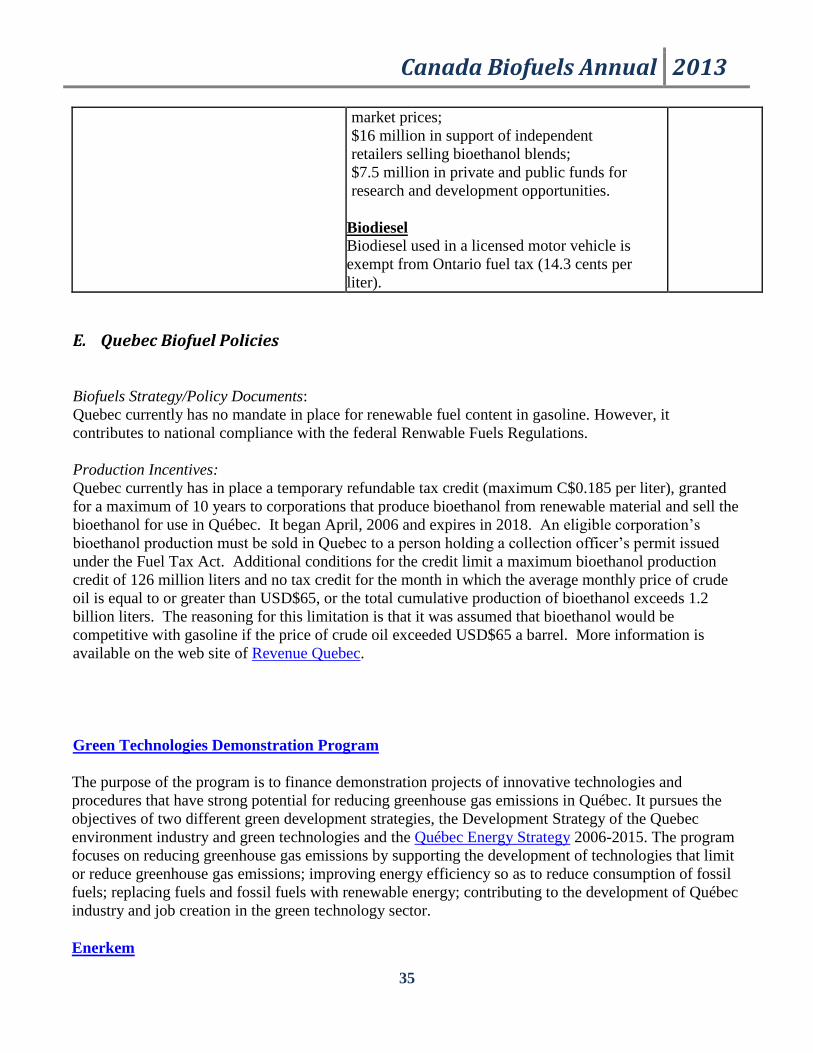

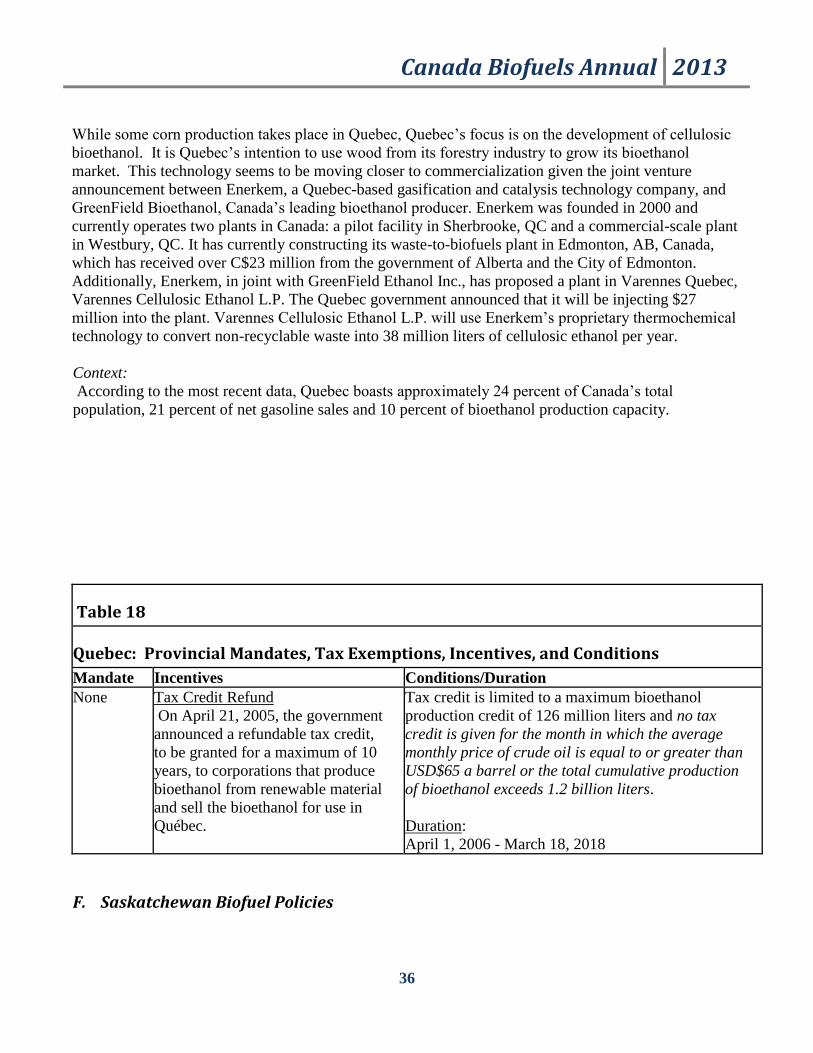

E. Quebec Biofuel Policies ................................................................................................. 35

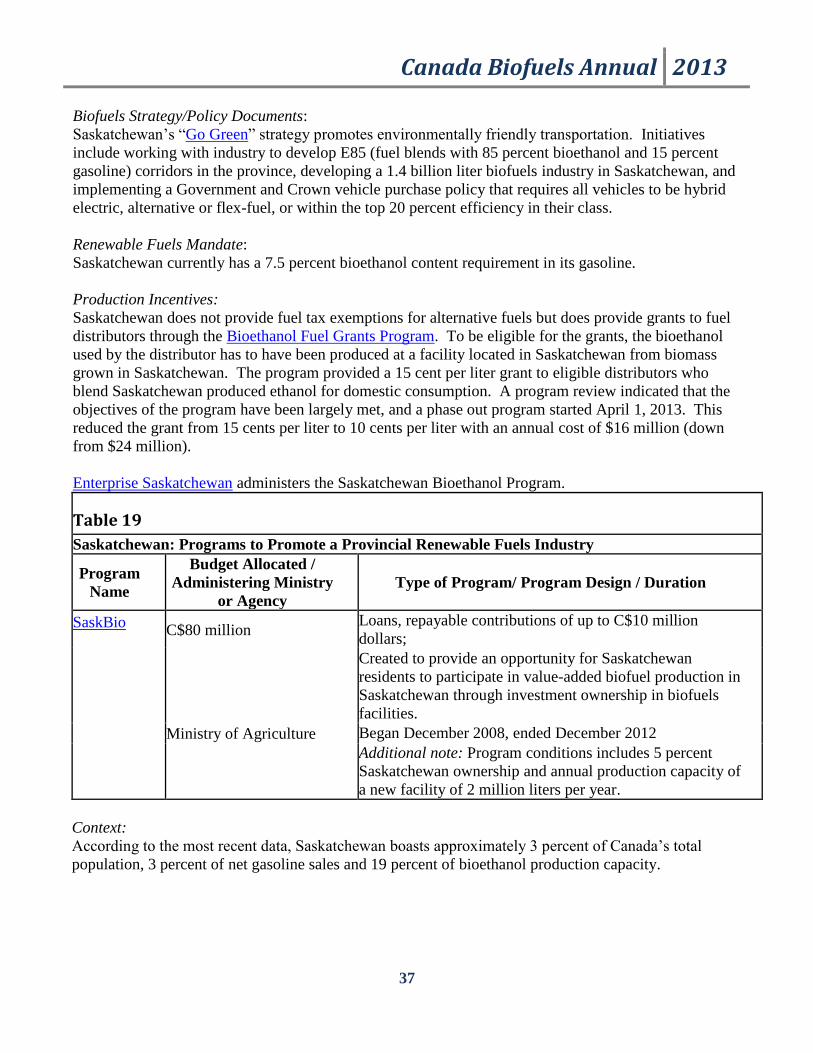

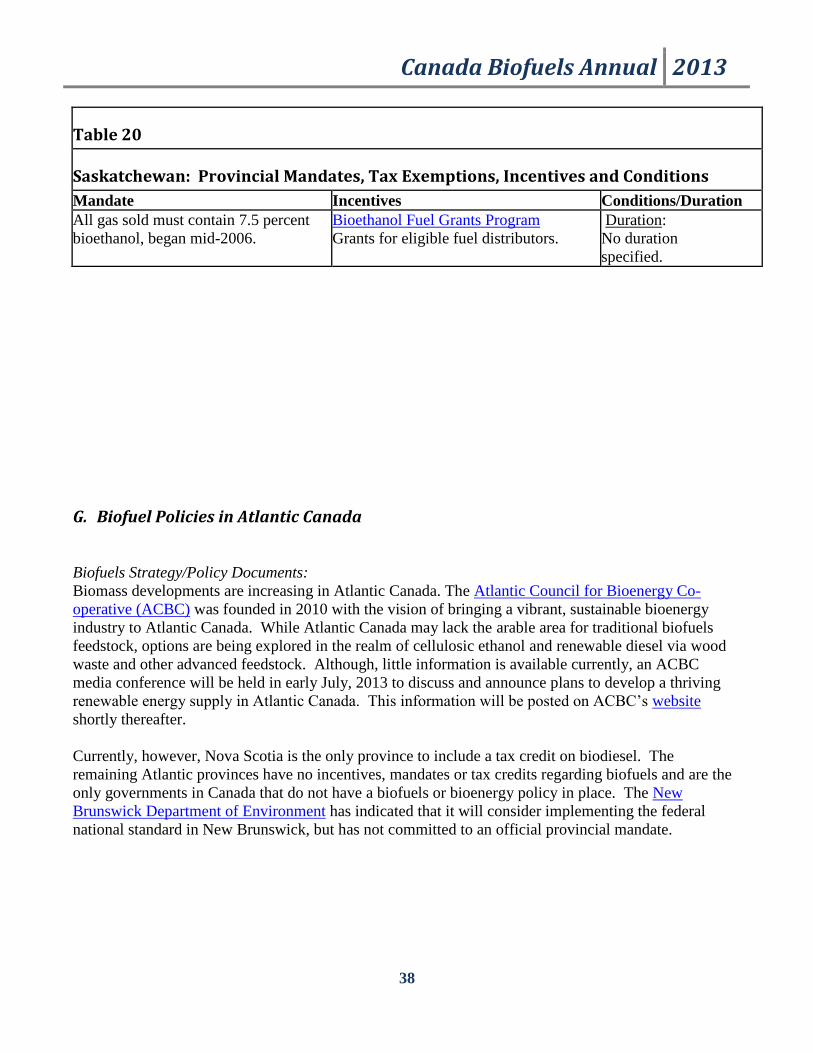

F. Saskatchewan Biofuel Policies ....................................................................................... 36

G. Biofuel Policies in Atlantic Canada ............................................................................... 38

Appendix III: Biofuel Plants: Existing, Expanding, Under Construction .................................... 40

Ethanol Production Plants .................................................................................................... 40

Biodiesel Production Plants ................................................................................................. 41

Canada Biofuels Annual 2013

3

I. Executive Summary

Since December 15, 2010, Canada has had a federal mandate requiring 5 percent of the national

gasoline pool to be renewable (ethanol). In addition, many provinces have equivalent or higher

provincial mandates, including a 5 percent renewable content mandate in Ontario, 7.5 percent in

Saskatchewan, and 8.5 percent in Manitoba. In 2013, these provinces alone are expected to make up

about 86 percent of Canada’s overall ethanol production. British Columbia and Alberta account for

approximately a quarter of net national gasoline sales, but are expected to make up only 4 percent of

Canada’s overall ethanol production in 2013.

Ethanol production in Canada will increase in 2013 to an expected 1,979 million liters, slightly up from

2012, and is forecast to grow further to 2,006 million liters in 2014. Due to the fact that this does not

surpass the federal content requirement, which Post estimates as 2,269 million liters for 2013 and 2014,

imports are expected to continue to increase to fulfill federal and provincial renewable content

requirements. The national fuel ethanol production capacity for 2013 and 2014 is estimated at 1,802

million liters, and national capacity use is estimated at 99 percent in 2013, up from 96 percent in 2012

and only 75 percent in 2011. Primary feedstocks remain corn and wheat. However, small production

levels of cellulosic ethanol from wood waste and municipal solid waste exist and are being developed

by Enerkem. Atlantic Canada is also looking into future possibilities of cellulosic ethanol production,

details of which will be announced in the near future.

Canada’s limited biofuels production, both in the short and medium term, suggests that Canada will not

soon become a major player in the global ethanol market. While domestic supply in Canada limits the

amount of trade, there is an increasing amount of trade in the co-products of ethanol production. Cross-

border trade between Canada and the United States in biofuels reflects the most economical trade

corridors.

On July 1, 2011, the federal government implemented a federal mandate of two percent renewable

content in diesel fuel and heating oil. The eastern part of Canada was initially given an implementation

exemption until December 31, 2012, but on May 18, 2013, regulations Amending the Renewable Fuels

Regulations were released, extending the exemption until June 30, 2013, as well as providing a

permanent exemption from the mandate for heating oils. Some provincial mandates for renewable

content are also in place, including a 4 percent requirement in British Columbia and 2 percent

requirements in Alberta, Saskatchewan, and Manitoba. Ontario will soon be undertaking consultations

regarding the creation of a mandate. At this time, Canada’s biodiesel production, at an estimated 471

million liters in 2013, remains below Post’s estimation of approximately 568 million liters needed to

meet the federal standard (excluding heating oil) if it was in full effect in 2013. However, biodiesel

production, due to the completion of new facilities, is expected to reach 646 million liters in 2014,

surpassing production needed to supply the federal requirement. While production from soybean as a

feedstock is expected to take place, primary feedstocks remain canola, animal fat, and recycled oils.

Canola feedstock is expected to account for nearly 40 percent of Canadian biodiesel production by the

end of 2014.

Canada Biofuels Annual 2013

4

II. Policy and Programs

Context: Canada’s Overall Energy Situation

Unlike the United States, energy security is not a factor behind the recent and projected growth in

Canada’s renewable fuel industry. According to the U.S. Energy Information Administration (EIA),

Canada has the world’s third largest proven oil reserves (estimated at 180 billion barrels), behind

Venezuela and Saudi Arabia. Canada is one of the world’s top ten oil exporters, and is one of the

world’s five largest energy producers.

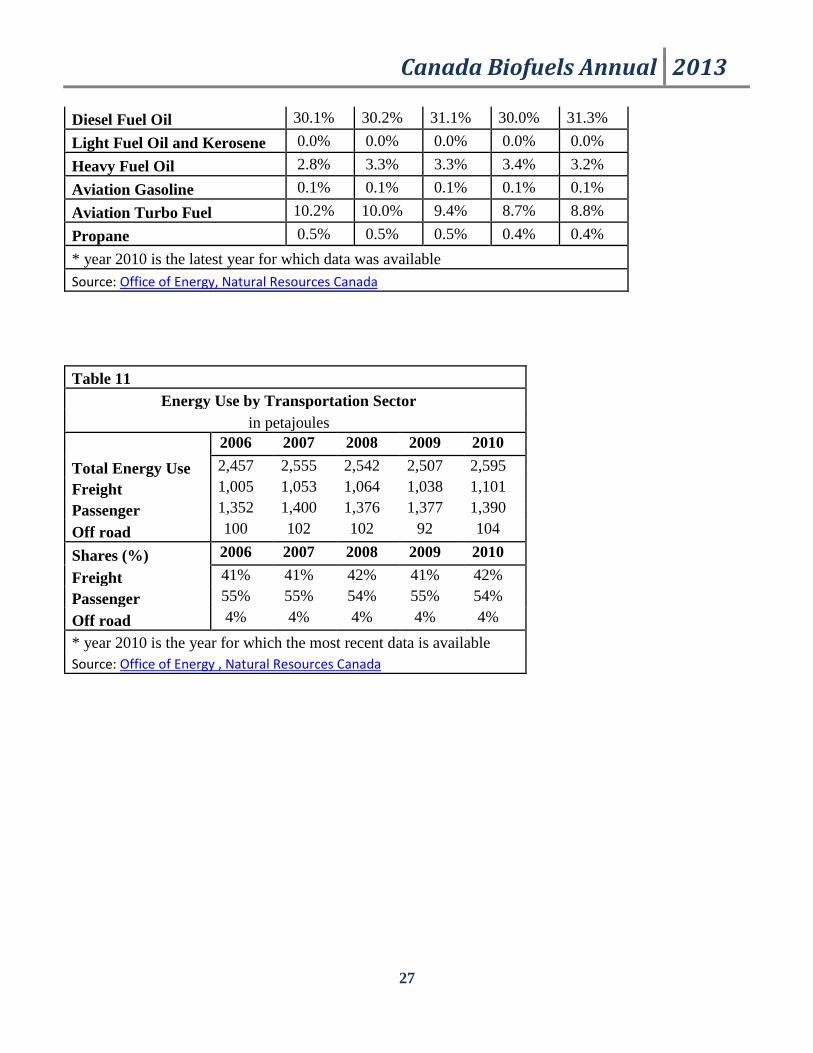

While Canada is a significant producer of oil, it also ranks among the world’s top ten consumers of

petroleum. Between the years of 2006-2011 transportation accounted for about one-third of energy

consumption (see Appendix I, Table 9), and motor gasoline and diesel fuel oil accounted for

approximately 85 percent of the energy used (see Appendix I, Table 10). A closer look at the use of

energy within the transportation industry shows that on average between the years 2006-2010 (most

recent available data), the share of energy used for freight averaged a little more than 41 percent per

year and the share of energy used for passenger transportation averaged a little under 55 percent (see

Appendix I, Table 11).

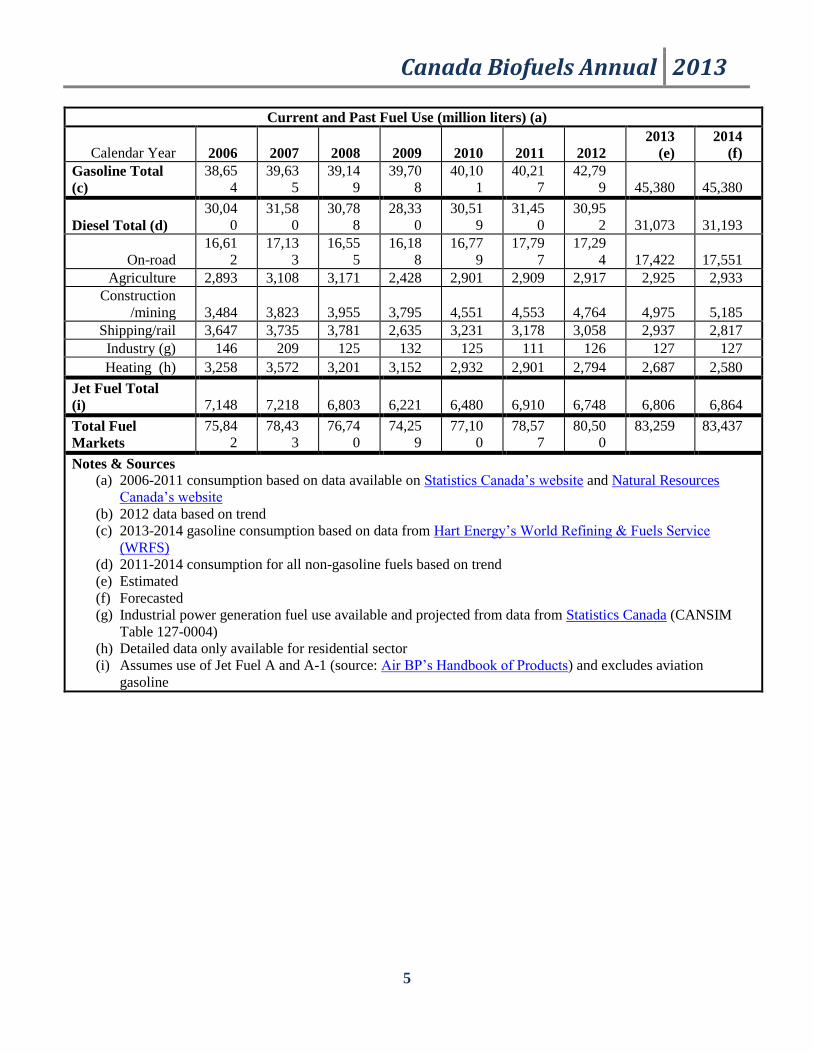

A breakdown of energy use by fuel type reveals that gasoline and diesel fuel account for an average of

52 percent and 40 percent, respectively, of the fuel type used in the period 2006-2011 and now dominate

as the transportation sector’s main energy sources. Table 1 below illustrates current and past fuel

consumption for 2006 through a forecasted 2014. Note that this excludes industrial power generation

fuel use due to lack of availability. Table 2 illustrates Post’s projections through 2023.

Table 1

Canada Biofuels Annual 2013

5

Current and Past Fuel Use (million liters) (a)

Calendar Year 2006 2007 2008 2009 2010 2011 2012

2013

(e)

2014

(f)

Gasoline Total

(c)

38,65

4

39,63

5

39,14

9

39,70

8

40,10

1

40,21

7

42,79

9 45,380 45,380

Diesel Total (d)

30,04

0

31,58

0

30,78

8

28,33

0

30,51

9

31,45

0

30,95

2 31,073 31,193

On-road

16,61

2

17,13

3

16,55

5

16,18

8

16,77

9

17,79

7

17,29

4 17,422 17,551

Agriculture 2,893 3,108 3,171 2,428 2,901 2,909 2,917 2,925 2,933

Construction

/mining 3,484 3,823 3,955 3,795 4,551 4,553 4,764 4,975 5,185

Shipping/rail 3,647 3,735 3,781 2,635 3,231 3,178 3,058 2,937 2,817

Industry (g) 146 209 125 132 125 111 126 127 127

Heating (h) 3,258 3,572 3,201 3,152 2,932 2,901 2,794 2,687 2,580

Jet Fuel Total

(i) 7,148 7,218 6,803 6,221 6,480 6,910 6,748 6,806 6,864

Total Fuel

Markets

75,84

2

78,43

3

76,74

0

74,25

9

77,10

0

78,57

7

80,50

0

83,259 83,437

Notes & Sources

(a) 2006-2011 consumption based on data available on Statistics Canada’s website and Natural Resources

Canada’s website

(b) 2012 data based on trend

(c) 2013-2014 gasoline consumption based on data from Hart Energy’s World Refining & Fuels Service

(WRFS)

(d) 2011-2014 consumption for all non-gasoline fuels based on trend

(e) Estimated

(f) Forecasted

(g) Industrial power generation fuel use available and projected from data from Statistics Canada (CANSIM

Table 127-0004)

(h) Detailed data only available for residential sector

(i) Assumes use of Jet Fuel A and A-1 (source: Air BP’s Handbook of Products) and excludes aviation

gasoline

Canada Biofuels Annual 2013

6

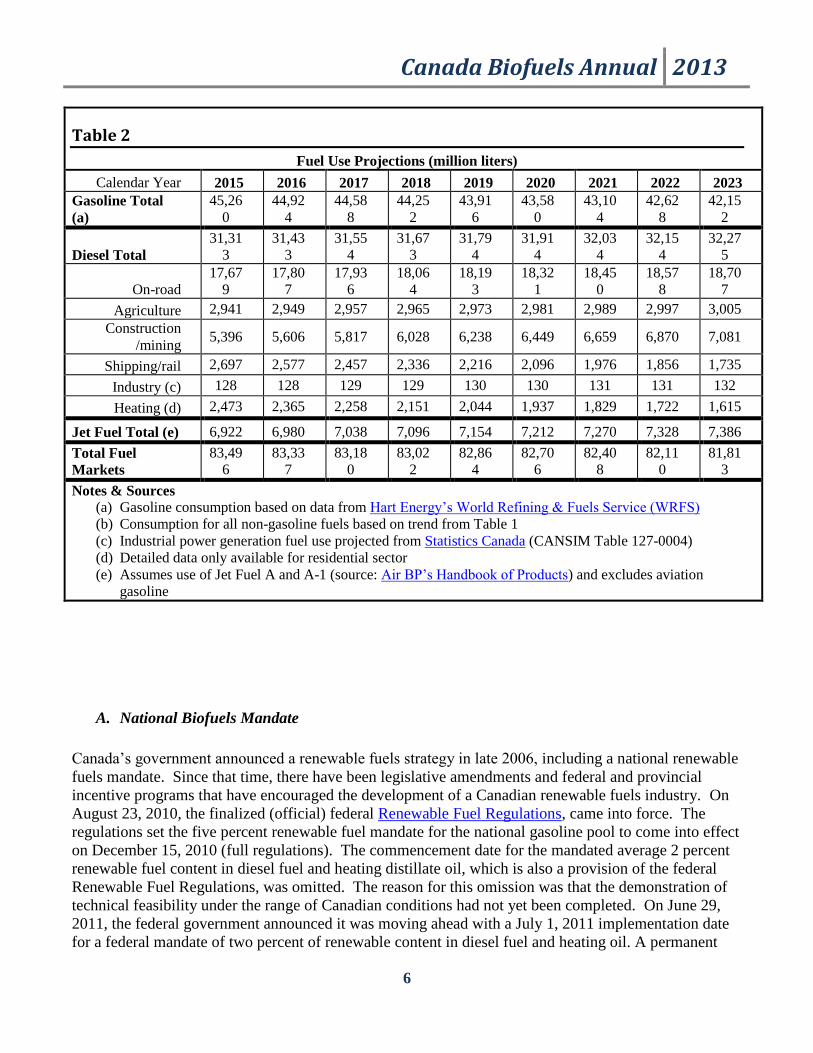

Table 2

Fuel Use Projections (million liters)

Calendar Year 2015 2016 2017 2018 2019 2020 2021 2022 2023

Gasoline Total

(a)

45,26

0

44,92

4

44,58

8

44,25

2

43,91

6

43,58

0

43,10

4

42,62

8

42,15

2

Diesel Total

31,31

3

31,43

3

31,55

4

31,67

3

31,79

4

31,91

4

32,03

4

32,15

4

32,27

5

On-road

17,67

9

17,80

7

17,93

6

18,06

4

18,19

3

18,32

1

18,45

0

18,57

8

18,70

7

Agriculture 2,941 2,949 2,957 2,965 2,973 2,981 2,989 2,997 3,005

Construction

/mining 5,396 5,606 5,817 6,028 6,238 6,449 6,659 6,870 7,081

Shipping/rail 2,697 2,577 2,457 2,336 2,216 2,096 1,976 1,856 1,735

Industry (c) 128 128 129 129 130 130 131 131 132

Heating (d) 2,473 2,365 2,258 2,151 2,044 1,937 1,829 1,722 1,615

Jet Fuel Total (e) 6,922 6,980 7,038 7,096 7,154 7,212 7,270 7,328 7,386

Total Fuel

Markets

83,49

6

83,33

7

83,18

0

83,02

2

82,86

4

82,70

6

82,40

8

82,11

0

81,81

3

Notes & Sources

(a) Gasoline consumption based on data from Hart Energy’s World Refining & Fuels Service (WRFS)

(b) Consumption for all non-gasoline fuels based on trend from Table 1

(c) Industrial power generation fuel use projected from Statistics Canada (CANSIM Table 127-0004)

(d) Detailed data only available for residential sector

(e) Assumes use of Jet Fuel A and A-1 (source: Air BP’s Handbook of Products) and excludes aviation

gasoline

A. National Biofuels Mandate

Canada’s government announced a renewable fuels strategy in late 2006, including a national renewable

fuels mandate. Since that time, there have been legislative amendments and federal and provincial

incentive programs that have encouraged the development of a Canadian renewable fuels industry. On

August 23, 2010, the finalized (official) federal Renewable Fuel Regulations, came into force. The

regulations set the five percent renewable fuel mandate for the national gasoline pool to come into effect

on December 15, 2010 (full regulations). The commencement date for the mandated average 2 percent

renewable fuel content in diesel fuel and heating distillate oil, which is also a provision of the federal

Renewable Fuel Regulations, was omitted. The reason for this omission was that the demonstration of

technical feasibility under the range of Canadian conditions had not yet been completed. On June 29,

2011, the federal government announced it was moving ahead with a July 1, 2011 implementation date

for a federal mandate of two percent of renewable content in diesel fuel and heating oil. A permanent

Canada Biofuels Annual 2013

7

exemption has been provided for renewable content in diesel fuel and heating distillate oil sold in

Newfoundland and Labrador to address the logistic challenges of blending biodiesel in this region.

Temporary exemptions for renewable content in diesel fuel and heating distillate oil sold in Quebec and

all Atlantic provinces were provided until December, 31, 2012, to give eastern Canada time to install

biodiesel blending infrastructure. On May 18, 2013, the Regulations Amending the Renewable Fuels

Regulations, were published in the Canada Gazette. The amendments extended the Maritime provincial

exemption from the 2 percent renewable diesel requirement, increasing it to end on June 30, 2013. The

amendments also created a permanent national exemption for the 2 percent renewable content

requirement for heating oil. The Renewable Fuels Regulations are annexed to the Canadian

Environmental Protection Act, 1999.

The overall structure is similar to the Renewable Fuel Standard in the United States, with the point of

compliance at the point of production or importation. The objective of the regulations is to reduce green

house gas (GHG) emissions by mandating renewable fuel content based on the gasoline volume, as well

as diesel fuel and heating distillate oil volumes, and fighting climate change. The regulations are

estimated to result in an incremental reduction of GHG emissions of about one ton of carbon dioxide

equivalent (1 MT CO2) per year over and above the reductions attributable to existing provincial

requirements already in place. The regulations fulfill the commitments under the federal government`s

Renewable Fuels Strategy of reducing GHG emissions from liquid petroleum fuels and creating a

demand for renewable fuels in Canada.

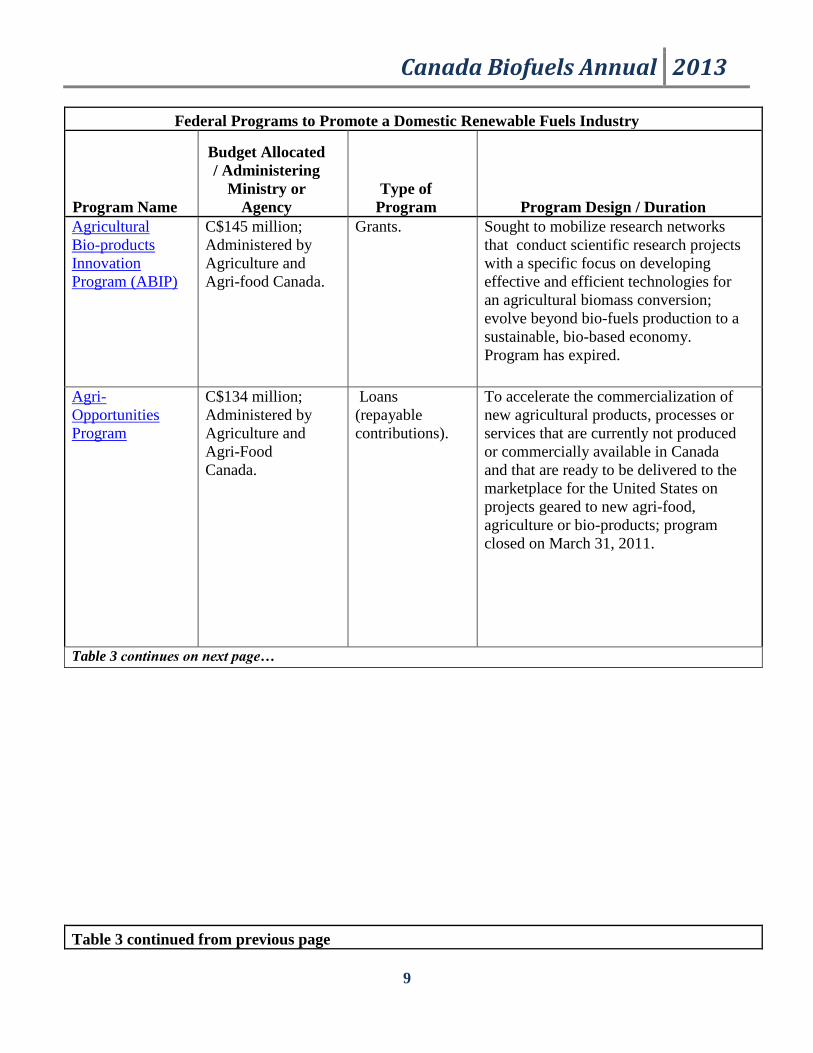

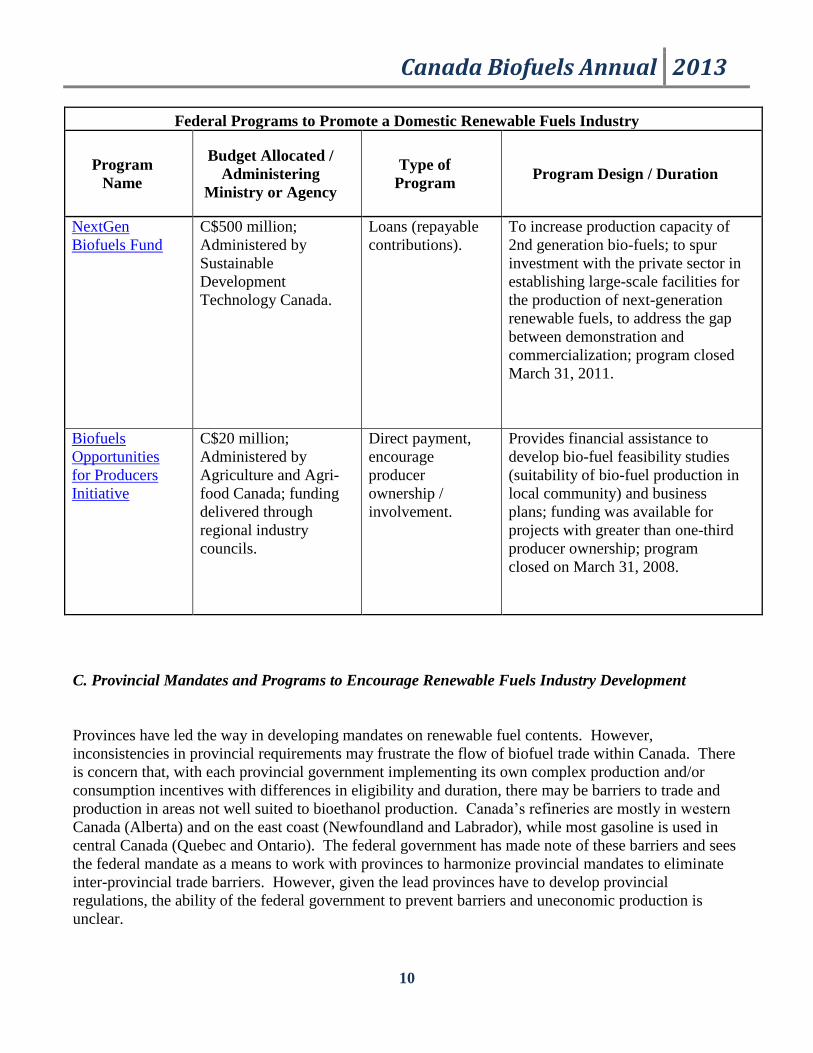

B. Federal Programs to Encourage the Development of a Canadian Renewable Fuels Industry

With its announcement of a renewable fuels strategy, the Canadian government launched several

programs designed to promote the development of a domestic renewable fuels industry. Several of the

programs are designed to encourage agricultural producer involvement in renewable fuels and the usage

of agricultural biomass to produce bioethanol. Many federal programs which were announced as part of

the renewable fuel strategy expired at the end of March 31, 2011. The federal government has not, as of

yet, announced any future measures to replace the programs which have expired.

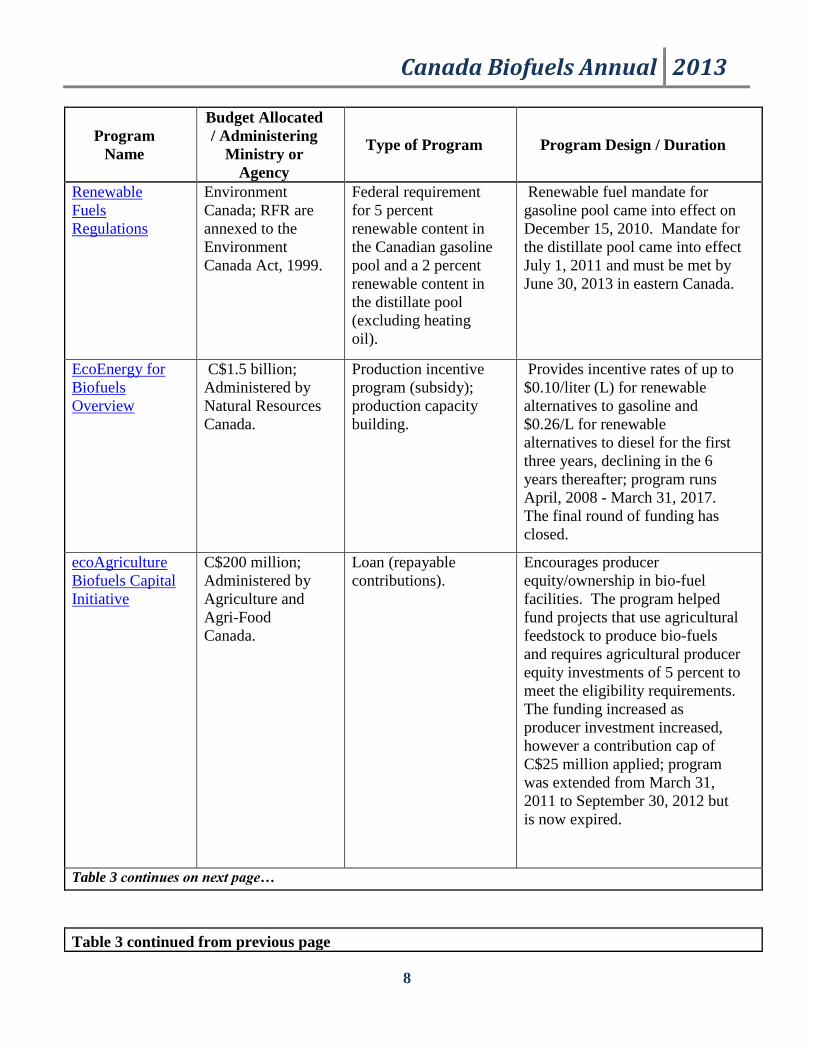

Table 3

Federal Programs to Promote a Domestic Renewable Fuels Industry

Canada Biofuels Annual 2013

8

Program

Name

Budget Allocated

/ Administering

Ministry or

Agency

Type of Program Program Design / Duration

Renewable

Fuels

Regulations

Environment

Canada; RFR are

annexed to the

Environment

Canada Act, 1999.

Federal requirement

for 5 percent

renewable content in

the Canadian gasoline

pool and a 2 percent

renewable content in

the distillate pool

(excluding heating

oil).

Renewable fuel mandate for

gasoline pool came into effect on

December 15, 2010. Mandate for

the distillate pool came into effect

July 1, 2011 and must be met by

June 30, 2013 in eastern Canada.

EcoEnergy for

Biofuels

Overview

C$1.5 billion;

Administered by

Natural Resources

Canada.

Production incentive

program (subsidy);

production capacity

building.

Provides incentive rates of up to

$0.10/liter (L) for renewable

alternatives to gasoline and

$0.26/L for renewable

alternatives to diesel for the first

three years, declining in the 6

years thereafter; program runs

April, 2008 - March 31, 2017.

The final round of funding has

closed.

ecoAgriculture

Biofuels Capital

Initiative

C$200 million;

Administered by

Agriculture and

Agri-Food

Canada.

Loan (repayable

contributions).

Encourages producer

equity/ownership in bio-fuel

facilities. The program helped

fund projects that use agricultural

feedstock to produce bio-fuels

and requires agricultural producer

equity investments of 5 percent to

meet the eligibility requirements.

The funding increased as

producer investment increased,

however a contribution cap of

C$25 million applied; program

was extended from March 31,

2011 to September 30, 2012 but

is now expired.

Table 3 continues on next page…

Table 3 continued from previous page

Canada Biofuels Annual 2013

9

Federal Programs to Promote a Domestic Renewable Fuels Industry

Program Name

Budget Allocated

/ Administering

Ministry or

Agency

Type of

Program Program Design / Duration

Agricultural

Bio-products

Innovation

Program (ABIP)

C$145 million;

Administered by

Agriculture and

Agri-food Canada.

Grants. Sought to mobilize research networks

that conduct scientific research projects

with a specific focus on developing

effective and efficient technologies for

an agricultural biomass conversion;

evolve beyond bio-fuels production to a

sustainable, bio-based economy.

Program has expired.

Agri-

Opportunities

Program

C$134 million;

Administered by

Agriculture and

Agri-Food

Canada.

Loans

(repayable

contributions).

To accelerate the commercialization of

new agricultural products, processes or

services that are currently not produced

or commercially available in Canada

and that are ready to be delivered to the

marketplace for the United States on

projects geared to new agri-food,

agriculture or bio-products; program

closed on March 31, 2011.

Table 3 continues on next page…

Table 3 continued from previous page

Canada Biofuels Annual 2013

10

Federal Programs to Promote a Domestic Renewable Fuels Industry

Program

Name

Budget Allocated /

Administering

Ministry or Agency

Type of

Program Program Design / Duration

NextGen

Biofuels Fund

C$500 million;

Administered by

Sustainable

Development

Technology Canada.

Loans (repayable

contributions).

To increase production capacity of

2nd generation bio-fuels; to spur

investment with the private sector in

establishing large-scale facilities for

the production of next-generation

renewable fuels, to address the gap

between demonstration and

commercialization; program closed

March 31, 2011.

Biofuels

Opportunities

for Producers

Initiative

C$20 million;

Administered by

Agriculture and Agri-

food Canada; funding

delivered through

regional industry

councils.

Direct payment,

encourage

producer

ownership /

involvement.

Provides financial assistance to

develop bio-fuel feasibility studies

(suitability of bio-fuel production in

local community) and business

plans; funding was available for

projects with greater than one-third

producer ownership; program

closed on March 31, 2008.

C. Provincial Mandates and Programs to Encourage Renewable Fuels Industry Development

Provinces have led the way in developing mandates on renewable fuel contents. However,

inconsistencies in provincial requirements may frustrate the flow of biofuel trade within Canada. There

is concern that, with each provincial government implementing its own complex production and/or

consumption incentives with differences in eligibility and duration, there may be barriers to trade and

production in areas not well suited to bioethanol production. Canada’s refineries are mostly in western

Canada (Alberta) and on the east coast (Newfoundland and Labrador), while most gasoline is used in

central Canada (Quebec and Ontario). The federal government has made note of these barriers and sees

the federal mandate as a means to work with provinces to harmonize provincial mandates to eliminate

inter-provincial trade barriers. However, given the lead provinces have to develop provincial

regulations, the ability of the federal government to prevent barriers and uneconomic production is

unclear.

Canada Biofuels Annual 2013

11

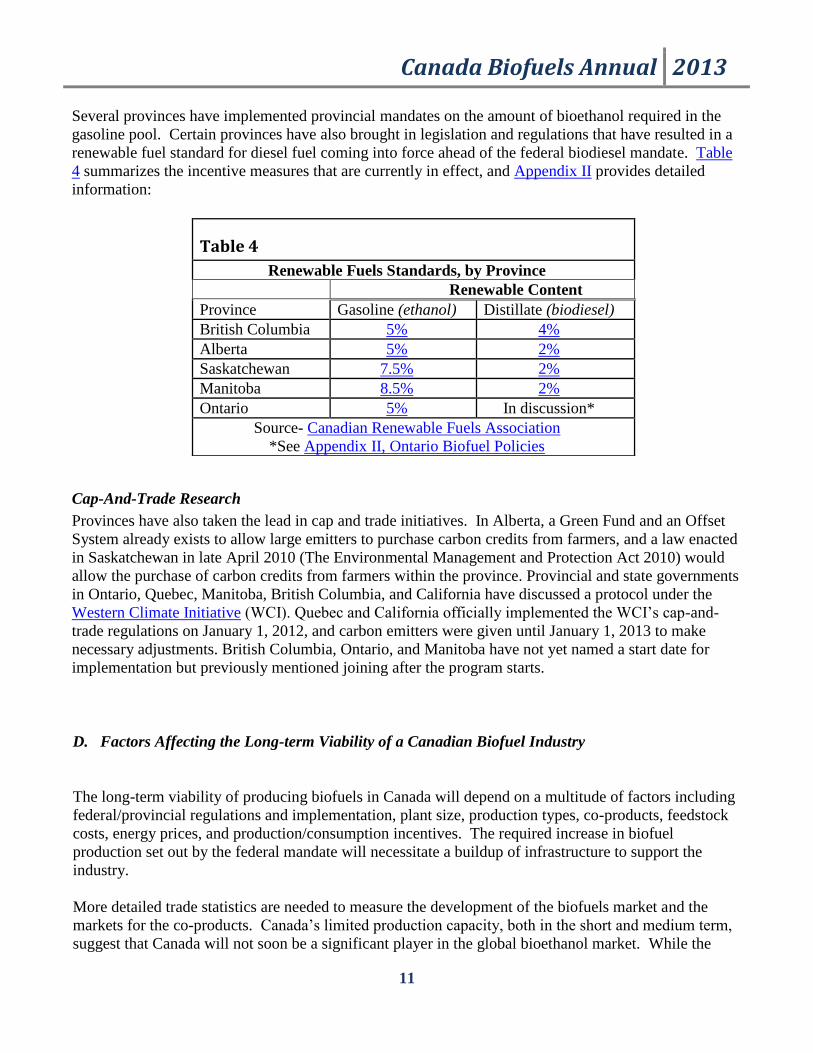

Several provinces have implemented provincial mandates on the amount of bioethanol required in the

gasoline pool. Certain provinces have also brought in legislation and regulations that have resulted in a

renewable fuel standard for diesel fuel coming into force ahead of the federal biodiesel mandate. Table

4 summarizes the incentive measures that are currently in effect, and Appendix II provides detailed

information:

Cap-And-Trade Research

Provinces have also taken the lead in cap and trade initiatives. In Alberta, a Green Fund and an Offset

System already exists to allow large emitters to purchase carbon credits from farmers, and a law enacted

in Saskatchewan in late April 2010 (The Environmental Management and Protection Act 2010) would

allow the purchase of carbon credits from farmers within the province. Provincial and state governments

in Ontario, Quebec, Manitoba, British Columbia, and California have discussed a protocol under the

Western Climate Initiative (WCI). Quebec and California officially implemented the WCI’s cap-and-

trade regulations on January 1, 2012, and carbon emitters were given until January 1, 2013 to make

necessary adjustments. British Columbia, Ontario, and Manitoba have not yet named a start date for

implementation but previously mentioned joining after the program starts.

D. Factors Affecting the Long-term Viability of a Canadian Biofuel Industry

The long-term viability of producing biofuels in Canada will depend on a multitude of factors including

federal/provincial regulations and implementation, plant size, production types, co-products, feedstock

costs, energy prices, and production/consumption incentives. The required increase in biofuel

production set out by the federal mandate will necessitate a buildup of infrastructure to support the

industry.

More detailed trade statistics are needed to measure the development of the biofuels market and the

markets for the co-products. Canada’s limited production capacity, both in the short and medium term,

suggest that Canada will not soon be a significant player in the global bioethanol market. While the

Table 4

Renewable Fuels Standards, by Province

Renewable Content

Province Gasoline (ethanol) Distillate (biodiesel)

British Columbia 5% 4%

Alberta 5% 2%

Saskatchewan 7.5% 2%

Manitoba 8.5% 2%

Ontario 5% In discussion*

Source- Canadian Renewable Fuels Association

*See Appendix II, Ontario Biofuel Policies

Canada Biofuels Annual 2013

12

possibility of increased bioethanol trade, especially between the northwest United States and Western

Canada (wheat-bioethanol to the United States and corn-based bioethanol to Canada), is unlikely to

develop quickly, there is an increasing amount of trade in the co-products of bioethanol production,

such as distiller’s dried grains (DDGs).

Canada Biofuels Annual 2013

13

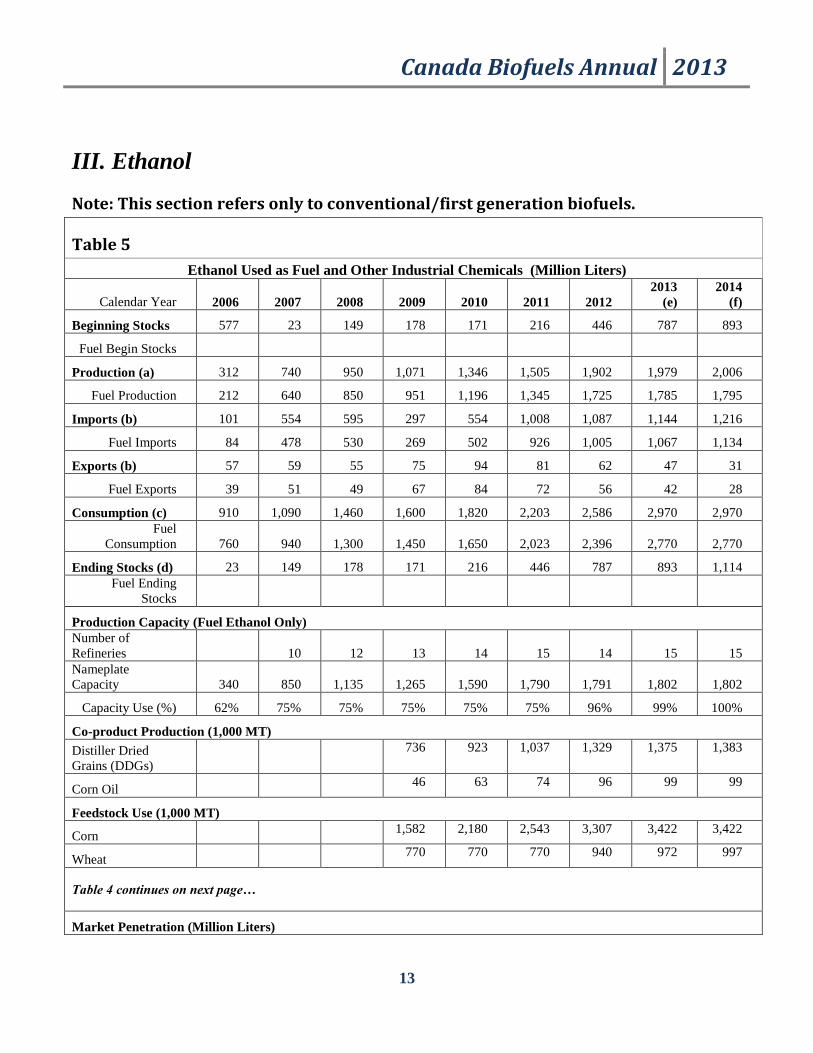

III. Ethanol

Note: This section refers only to conventional/first generation biofuels.

Table 5

Ethanol Used as Fuel and Other Industrial Chemicals (Million Liters)

Calendar Year 2006 2007 2008 2009 2010 2011 2012

2013

(e)

2014

(f)

Beginning Stocks 577 23 149 178 171 216 446 787 893

Fuel Begin Stocks

Production (a) 312 740 950 1,071 1,346 1,505 1,902 1,979 2,006

Fuel Production 212 640 850 951 1,196 1,345 1,725 1,785 1,795

Imports (b) 101 554 595 297 554 1,008 1,087 1,144 1,216

Fuel Imports 84 478 530 269 502 926 1,005 1,067 1,134

Exports (b) 57 59 55 75 94 81 62 47 31

Fuel Exports 39 51 49 67 84 72 56 42 28

Consumption (c) 910 1,090 1,460 1,600 1,820 2,203 2,586 2,970 2,970

Fuel

Consumption 760 940 1,300 1,450 1,650 2,023 2,396 2,770 2,770

Ending Stocks (d) 23 149 178 171 216 446 787 893 1,114

Fuel Ending

Stocks

Production Capacity (Fuel Ethanol Only)

Number of

Refineries 10 12 13 14 15 14 15 15

Nameplate

Capacity 340 850 1,135 1,265 1,590 1,790 1,791 1,802 1,802

Capacity Use (%) 62% 75% 75% 75% 75% 75% 96% 99% 100%

Co-product Production (1,000 MT)

Distiller Dried

Grains (DDGs)

736 923 1,037 1,329 1,375 1,383

Corn Oil 46 63 74 96 99 99

Feedstock Use (1,000 MT)

Corn 1,582 2,180 2,543 3,307 3,422 3,422

Wheat 770 770 770 940 972 997

Table 4 continues on next page…

Market Penetration (Million Liters)

Canada Biofuels Annual 2013

14

Fuel Ethanol 760 940 1,300 1,450 1,650 2,023 2,396 2,770 2,770

Gasoline

38,65

4

39,63

5

39,14

9

39,70

8

40,10

1

40,21

7

42,79

9 45,380 45,380

Blend Rate (%) 2.0% 2.4% 3.3% 3.7% 4.1% 5.0% 5.6% 6.1% 6.1%

(a) 2006-2010 Production data based on information from F.O.Licht. 2011-2014 Fuel ethanol production based on data from Canadian Renewable Fuels Association along with industry discussion, and overall ethanol production based on fuel ethanol:all ethanol ratio from 2006-2010.

(b) Trade data based on information from F.O.Licht and the Global Trade Atlas. Ethanol is harmonized under HS code 2207.10 and 2207.20. GTA reports Canadian ethanol trade as LPA, and no official statistics are available in liters. Fuel ethanol proportion of trade based on proportions of fuel ethanol in consumption and production.

(c) Consumption data based on information from F.O.Licht, Statistics Canada, and federal/provincial Renewable Fuel Standards.

(d) Ending stocks only available for 2006-2010 from F.O.Licht. Stocks for all other years are based on calculations of Canadian trade balances.

(e) Estimated (f) Forecasted

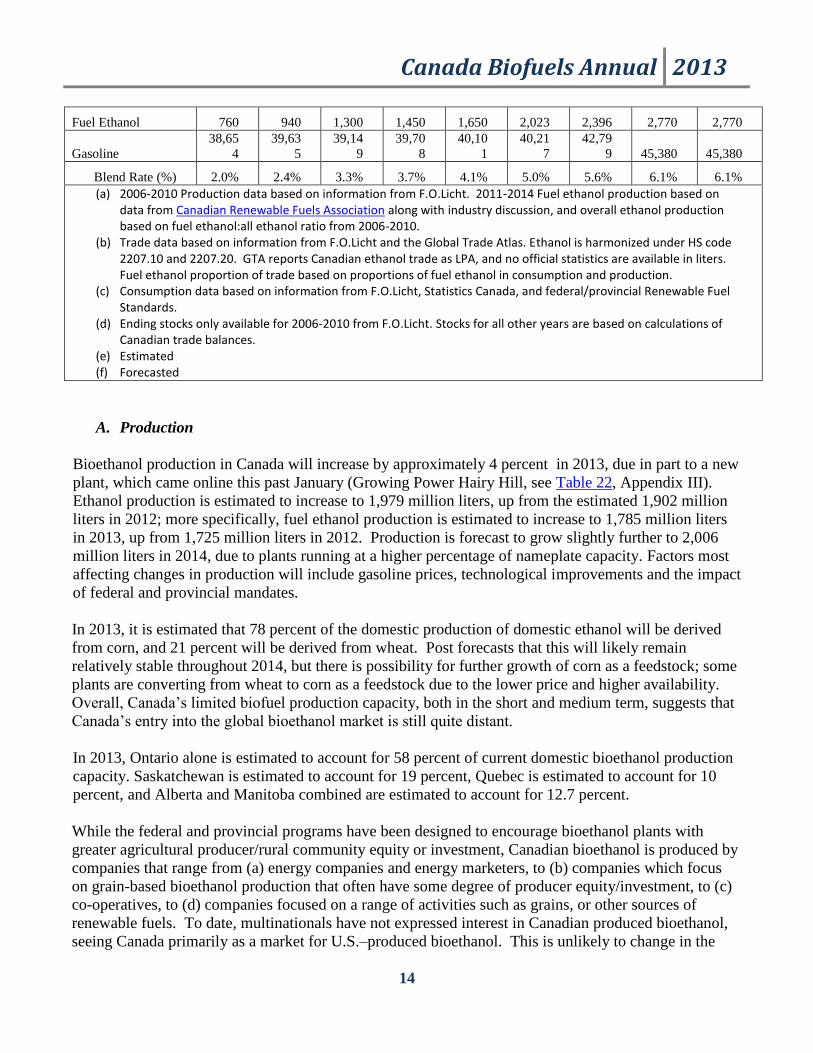

A. Production

Bioethanol production in Canada will increase by approximately 4 percent in 2013, due in part to a new

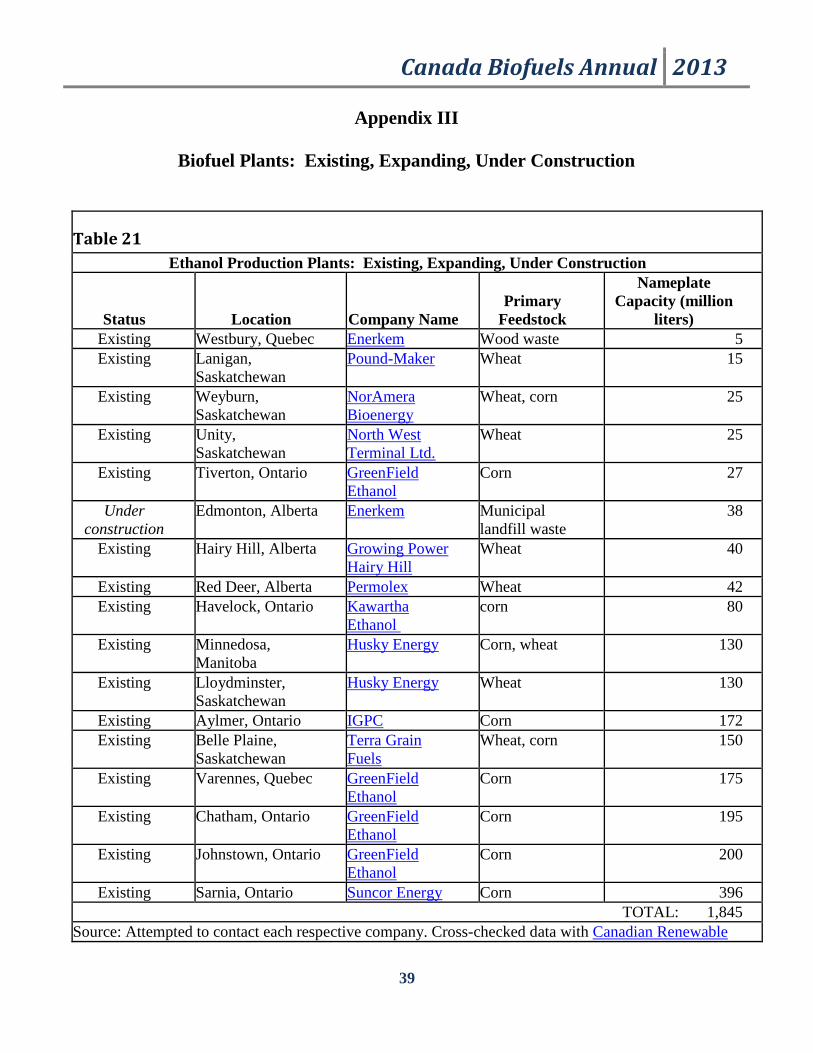

plant, which came online this past January (Growing Power Hairy Hill, see Table 22, Appendix III).

Ethanol production is estimated to increase to 1,979 million liters, up from the estimated 1,902 million

liters in 2012; more specifically, fuel ethanol production is estimated to increase to 1,785 million liters

in 2013, up from 1,725 million liters in 2012. Production is forecast to grow slightly further to 2,006

million liters in 2014, due to plants running at a higher percentage of nameplate capacity. Factors most

affecting changes in production will include gasoline prices, technological improvements and the impact

of federal and provincial mandates.

In 2013, it is estimated that 78 percent of the domestic production of domestic ethanol will be derived

from corn, and 21 percent will be derived from wheat. Post forecasts that this will likely remain

relatively stable throughout 2014, but there is possibility for further growth of corn as a feedstock; some

plants are converting from wheat to corn as a feedstock due to the lower price and higher availability.

Overall, Canada’s limited biofuel production capacity, both in the short and medium term, suggests that

Canada’s entry into the global bioethanol market is still quite distant.

In 2013, Ontario alone is estimated to account for 58 percent of current domestic bioethanol production

capacity. Saskatchewan is estimated to account for 19 percent, Quebec is estimated to account for 10

percent, and Alberta and Manitoba combined are estimated to account for 12.7 percent.

While the federal and provincial programs have been designed to encourage bioethanol plants with

greater agricultural producer/rural community equity or investment, Canadian bioethanol is produced by

companies that range from (a) energy companies and energy marketers, to (b) companies which focus

on grain-based bioethanol production that often have some degree of producer equity/investment, to (c)

co-operatives, to (d) companies focused on a range of activities such as grains, or other sources of

renewable fuels. To date, multinationals have not expressed interest in Canadian produced bioethanol,

seeing Canada primarily as a market for U.S.–produced bioethanol. This is unlikely to change in the

Canada Biofuels Annual 2013

15

short to medium term as Canada is still working towards building enough production capacity to meet

its own domestic mandates.

B. Impacts of Ethanol Production on Feedstock Markets

Corn and wheat are the main feedstock for bioethanol production in Canada and the introduction of the

mandatory renewable fuel content by the Canadian government undoubtedly have had and will have an

impact on production patterns. At this time, there are no official statistics for the amount of corn and

wheat directed into bioethanol production.

i. Ethanol Produced from Corn

Corn remains the main feedstock for Canadian bioethanol production, and Ontario remains the largest

corn-producing province in Canada. In 2013 and 2014, corn is expected to account for about 78 percent

of bioethanol feedstock, respectively.

ii. Ethanol Produced from Wheat

Wheat is the feedstock for most of the balance of Canada’s bioethanol production. It is forecast to

account for about 22 percent of bioethanol feedstock for years 2013 and 2014. The newer wheat

bioethanol plants have more flexibility. Pipes are larger and allow the use of other feedstock, such as

corn, when wheat feedstock may be too expensive. For example, the Husky Energy wheat-based

bioethanol plant in Minnedosa, Manitoba uses corn when wheat feedstock is unavailable or too

expensive. However, Husky Energy has agreed that 80 percent of the feedstock used to produce

bioethanol will come from Manitoba producers. The agreement is with the Manitoba government and

expires in 2017.

As the bioethanol industry grows, demand for different wheat varieties is also expected to grow,

resulting in increased competition between wheat end-users, such as the Canadian bioethanol producers,

livestock producers and the milling industry. The need for high-yielding, low-protein wheat by the

livestock industry and the bioethanol plants are in direct conflict with the needs of the flour industry.

Increases in bioethanol efficient wheat is expected to affect production patterns and result in more

Canadian wheat farmers seeding area to lower protein/high starch wheat such as Winter Wheat and

Canadian Prairie Spring Wheat, rather than higher protein/lower starch wheat varieties used by the

milling industry. The livestock sector, especially the hog sector, competes for the same wheat varieties

as the bioethanol sector.

Additional layers of complication were removed with the December 15, 2011 decision by Canadian

legislators to pass into law the divisive Marketing Freedom for Grain Farmers Act. This Act has

transitioned the Canadian Wheat Board (CWB) from a state trading enterprise into a commercial

enterprise. Prior to the August 1, 2012 enactment date, the CWB had the exclusive right to purchase

Canada Biofuels Annual 2013

16

and sell western wheat (and barley) for domestic food use or export for the 70 years. However, since

the CWB was never very involved in bioethanol production, it is unlikely that this change will have an

effect on wheat-based bioethanol production.

C. Consumption

Based on the trend of net national sales of gasoline used for road motor vehicles between 2006 and

2011, and the projected trend for 2011-2014 (see Table 6, below), the federal mandate of 5 percent

renewable fuel content requires an estimated minimum of 2,269 million liters for 2013 and 2014 of

ethanol production — not just capacity. Production capacity of bioethanol is not expected to surpass

1,802 million liters in 2013 and 2014 (see Table 21, Appendix III).

Table 6

Canada: Sales of Gasoline Used for Road Motor Vehicles

in million liters

2006 2007 2008 2009 2010 2011 2012

2013

(e)

2014

(f)

Net sales

of

gasoline

38,65

4

39,63

5

39,14

9

39,70

8

40,10

1

40,21

7

42,79

9 45,380 45,380

Notes & Sources

(a) 2006-2011 consumption based on data available on Statistics Canada’s website and Natural Resources

Canada’s website

(b) 2012 data based on trend

(c) 2013-2014 gasoline consumption based on data from Hart Energy’s World Refining & Fuels Service

(WRFS)

(e) Estimated (f) Forecasted

D. Trade

While there are few reliable trade statistics for Canada’s fuel ethanol due to broad and changing HS

codes, Post forecasts that imports will rise to 1,144 and 1,216 million liters per year for 2013 and 2014,

respectively, up from an estimated 1,087 million liters in 2012. This increase is expected to be driven

by an increasing demand for ethanol because of mandates and industry’s inability to produce the

required amount of ethanol. Exports are expected to decrease between 2013 and 2014. This decrease

will most likely be due to the need for Canada to meet its own domestic mandates.

Due to the North American Free Trade Agreement (NAFTA), there is no tariff on renewable fuels

produced in the United States and imported into Canada. However, Canada does have a tariff on

bioethanol imported from other countries such as Brazil ($0.05 per liter).

Canada Biofuels Annual 2013

17

While the current differences in provincial tax exemptions for renewable fuels do not greatly affect

production decisions, the combination of lower oil prices (e.g. return to pre-2005 levels), and higher

grain prices could make certain provincial tax-exemption restrictions obstacles to expanding the

industry.

In recent years, nearly 100 percent bioethanol trade for Canada has been with the United States.

However, the possibility of significant increases in bioethanol trade, especially between the

northwestern United States and Western Canada (wheat-based bioethanol to the United States and corn-

based bioethanol to Canada), is unlikely to develop in the short to medium term. This is due mainly to

the fact that Canada does not have excess bioethanol production capacity, which would permit large

volumes of exports to the United States.

E. Ending Stocks

Due to a relative lack in data availability for stocks, stock data is mostly calculated based on estimated

trade balances. The high stocks listed for more recent years in Table 5 may, however, be put toward

consumption in order to meet mandated renewable content levels.

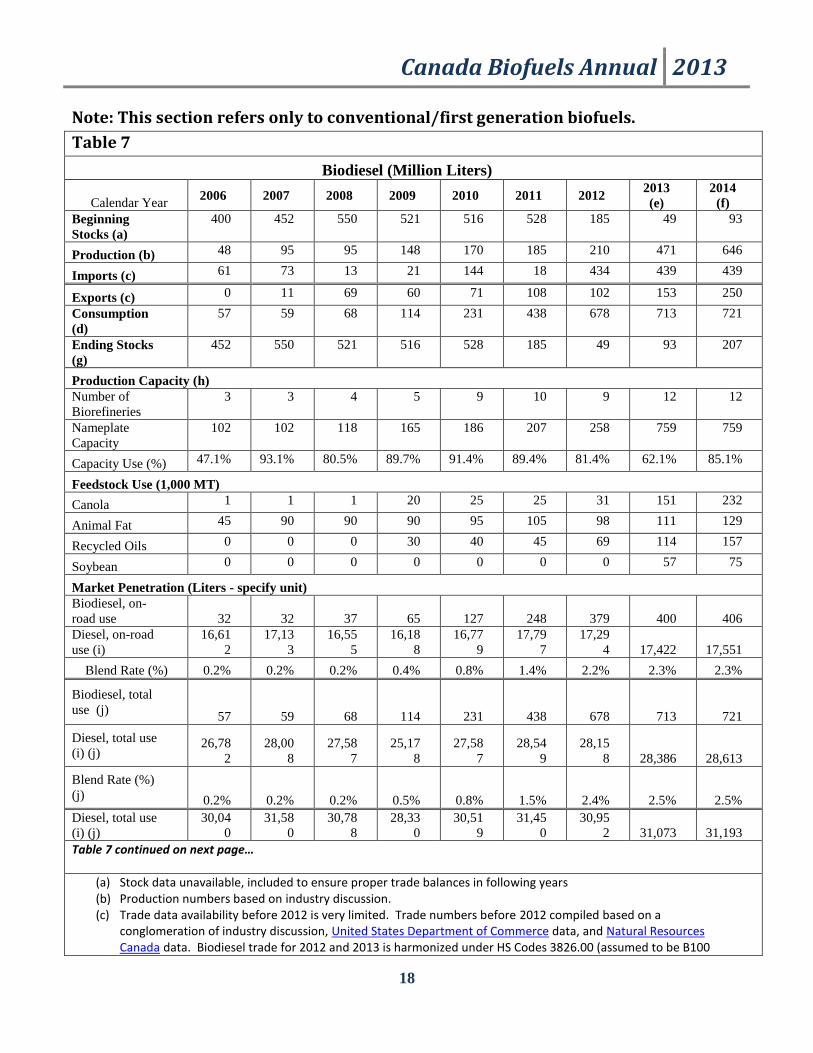

IV. Biodiesel

Canada Biofuels Annual 2013

18

Note: This section refers only to conventional/first generation biofuels.

Table 7

Biodiesel (Million Liters)

Calendar Year 2006 2007 2008 2009 2010 2011 2012

2013

(e)

2014

(f)

Beginning

Stocks (a)

400 452 550 521 516 528 185 49 93

Production (b) 48 95 95 148 170 185 210 471 646

Imports (c) 61 73 13 21 144 18 434 439 439

Exports (c) 0 11 69 60 71 108 102 153 250

Consumption

(d)

57 59 68 114 231 438 678 713 721

Ending Stocks

(g)

452 550 521 516 528 185 49 93 207

Production Capacity (h)

Number of

Biorefineries

3 3 4 5 9 10 9 12 12

Nameplate

Capacity

102 102 118 165 186 207 258 759 759

Capacity Use (%) 47.1% 93.1% 80.5% 89.7% 91.4% 89.4% 81.4% 62.1% 85.1%

Feedstock Use (1,000 MT)

Canola 1 1 1 20 25 25 31 151 232

Animal Fat 45 90 90 90 95 105 98 111 129

Recycled Oils 0 0 0 30 40 45 69 114 157

Soybean 0 0 0 0 0 0 0 57 75

Market Penetration (Liters - specify unit)

Biodiesel, on-

road use 32 32 37 65 127 248 379 400 406

Diesel, on-road

use (i)

16,61

2

17,13

3

16,55

5

16,18

8

16,77

9

17,79

7

17,29

4 17,422 17,551

Blend Rate (%) 0.2% 0.2% 0.2% 0.4% 0.8% 1.4% 2.2% 2.3% 2.3%

Biodiesel, total

use (j) 57 59 68 114 231 438 678 713 721

Diesel, total use

(i) (j) 26,78

2

28,00

8

27,58

7

25,17

8

27,58

7

28,54

9

28,15

8 28,386 28,613

Blend Rate (%)

(j) 0.2% 0.2% 0.2% 0.5% 0.8% 1.5% 2.4% 2.5% 2.5%

Diesel, total use

(i) (j)

30,04

0

31,58

0

30,78

8

28,33

0

30,51

9

31,45

0

30,95

2 31,073 31,193

Table 7 continued on next page…

(a) Stock data unavailable, included to ensure proper trade balances in following years (b) Production numbers based on industry discussion. (c) Trade data availability before 2012 is very limited. Trade numbers before 2012 compiled based on a

conglomeration of industry discussion, United States Department of Commerce data, and Natural Resources Canada data. Biodiesel trade for 2012 and 2013 is harmonized under HS Codes 3826.00 (assumed to be B100

Canada Biofuels Annual 2013

19

diesel fuel oil) and 2710.20 (assumed to be B5 diesel fuel oil). (d) Biodiesel consumption for each year based on provincial and federal renewable fuel mandates and data from

Statistics Canada. (e) Estimated (f) Forecasted (g) Data availability for diesel and biodiesel ending stocks is virtually nonexistent. Stock numbers estimated to ensure

correct trade balance for each year. (h) Production capacities and plant specifics based on industry discussion. (i) Diesel fuel comsuption data derived and projected from data from Statistics Canada. (j) Excluding consumption in heating sector. This is due to the recent development that heating oil will be exempted

from federal renewable content requirements.

A. Biodiesel Production

The federal biodiesel mandate of 2 percent in diesel fuel and distillate heating oil came into effect on

July 1, 2011. A permanent exemption has been provided for renewable content in diesel fuel and

heating distillate oil sold in Newfoundland and Labrador (to address the logistic challenges of blending

biodiesel in this region) as well as for renewable content in heating distillate oil. Temporary exemptions

for renewable content in diesel fuel and heating distillate oil sold in Quebec and all Atlantic provinces

have been extended, until June 30, 2013 to give Eastern Canada time to install biodiesel blending

infrastructure. This announcement, in combination with the extension of the ecoABC Initiative (a

program which assisted in the construction of biofuel facilities that have a minimum of five percent

producer investment) which was extended until September of 2012, is likely to help spur investment in

biodiesel production facilities. With the ecoABC Initiative and forecasted increased production, industry

is preparing to comply with the mandated requirements.

Biodiesel production is projected to more than double in 2013 to 471 million liters, up from an

estimated 210 million in 2012, due to new production capacity. In 2014, production is forecast to

increase even further to 646 million liters, partially due to the expected completion of a 265 million liter

plant. In the longer term, the European Union’s (EU) increased demands for renewable energy has

generated a potential and growing market for biodiesel exports from Canada, as has the RFS2 in the

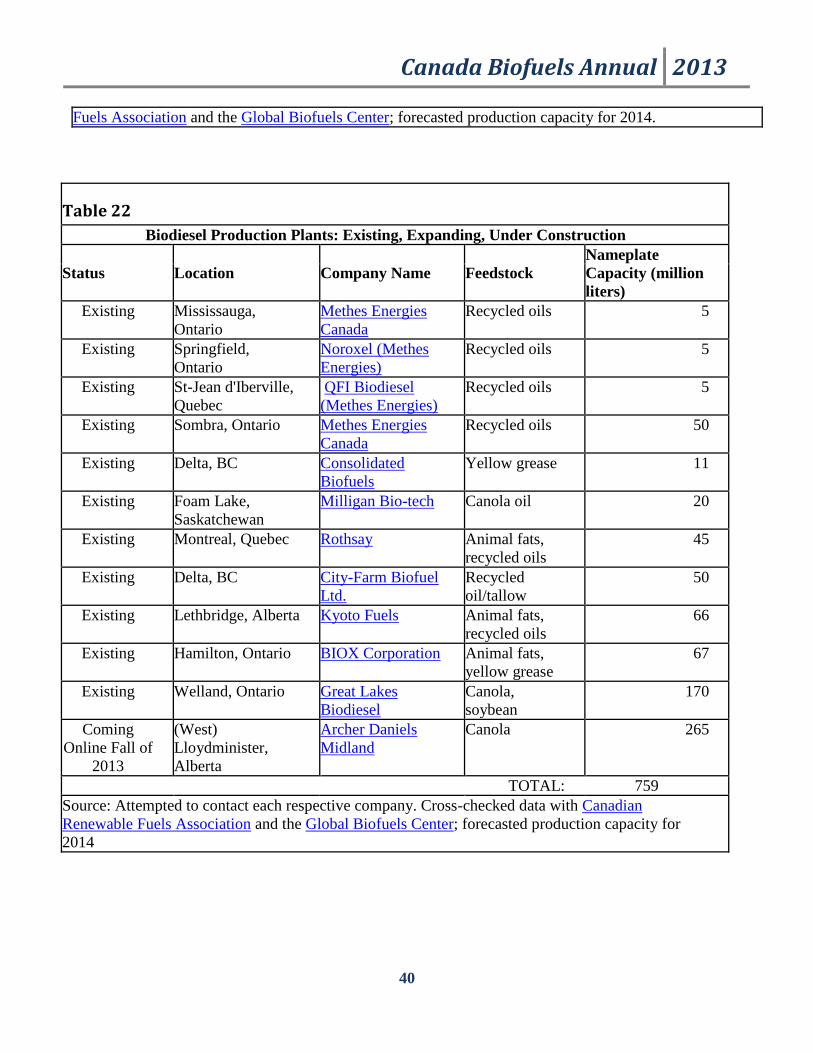

United States. With the current plants and four plants under construction, including a 265 million liter

Archer Daniels Midland (ADM) plant, the federal biodiesel mandate is likely to be met with domestic

production by the end of 2014. ADM, a large American company involved in over 75 countries, is the

first instance of multi-national interest in the Canadian biodiesel industry. Despite the current growth,

future growth of the Canadian biodiesel industry may be limited due to the industry’s inability to secure

cheap feedstock. Most of the current and forecasted increase in biodiesel comes from canola and strong

world demand for vegetable oils may hinder Canada’s ability to take advantage of the growing biodiesel

market opportunities.

The federal government’s biofuel strategy program is geared more towards bioethanol and is therefore

limited in their ability to address the limiting factors for biodiesel market growth. This has implications

when trying to determine the profitability for a biodiesel venture. For example, crushing plants can be

used to produce oil for both biodiesel production and human consumption, but the federal government

does not want to inadvertently subsidize crushing capacity for oils destined for human consumption.

Canada Biofuels Annual 2013

20

B. Impacts of Biodiesel Production on Feedstock Markets

While biodiesel can be made from a variety of different feedstocks, prices and availability are the

determining factors likely to be considered. Canola, largely due to the abundance of the Canadian

production, has proven to be the natural feedstock choice. Projected canola-based biodiesel production

shows increases from 151 million liters (35 percent production share) in 2013 to 232 million liters (39

percent share) in 2014. Key competitors facing canola oil for use in biodiesel are rendered animal fats

(tallow), rendered oils (yellow grease), palm oil (which would be imported as Canada does not produce

palm oil), and soybean oil. Canola and soybeans are high-priced feedstock for biodiesel since they are

priced as food oils in international markets. Palm oil and rendered fats are priced at feed and industrial

use levels.

In fall of 2011, the United States Environmental Protection Agency (EPA) signed the Canadian

Aggregate Approach Petition to approve Canadian feedstocks, including canola, for biodiesel

production in the United States. This decision provides secure access for Canadian canola as a

sustainable feedstock for U.S. biodiesel markets. As a result, it is likely that there will be more Canadian

exports of canola to the United States to meet RFS2, with some canola derived biodiesel returning to

Canada.

Most of the growth in biodiesel production capacity has occurred in Western Canada, where the

majority of the canola is grown, spurred on by provincial mandates in addition to the federal mandate.

Canola production has reached record high levels in recent years. Increased demand for canola oil from

the food retail industry has resulted in higher prices. In 2012, canola producers responded by planting

record acreage, up 13 percent from an already record 2011 year. In 2013, area seeded to canola is

estimated to have fallen 8 percent from the previous year, but remains at a historically high level.

Despite the supply response of recent years, some industry observers suggest that canola could remain

too expensive, and that a 2 percent biodiesel blend must be met with cheaper feedstock. As demand for

the feedstock increases, it is likely that canola prices will also increase.

While canola use for biodiesel by-itself may be expensive, the co-products from biodiesel production

may make economic sense. Co-products include meal to be used in animal feed. There are limits on the

profitability of using canola as a feedstock if by-products are part of the everyday production process.

For example, off-seed canola may not be a suitable feedstock since this meal may not meet quality

standards. Despite these limitations, co-products and the production capacity of the plants (these plants

could potentially supply the vast majority of the federal 2 percent biodiesel mandate), combined with

provincial biodiesel mandates may make the industry profitable, despite higher commodity prices.

In 2014, while the amount of tallow used for biodiesel is forecast to increase by 16 percent, the share of

biodiesel production from tallow (animal fats) is expected to decrease from estimated 2013 levels of 26

percent to 22 percent due to completion of new biodiesel plants using other feedstocks. The share of

biodiesel produced from yellow grease is forecast to fall to remain relatively steady at 26 percent of

production.

C. Consumption

Canada Biofuels Annual 2013

21

Based on the trend of net national sales of diesel used for road motor vehicles between 2006 and 2011

(see Table 1, above), and the federal mandate which includes renewable fuel content in both the diesel

oil sales for transportation as well other sectors, Post estimates that Canada will consume 713 million

liters of biodiesel in 2013 and forecasts consumption at 721 million liters of biodiesel production in

2014 (see Table 7, above). By the end of 2014, the temporary exemptions for eastern Canada and

Quebec will have been lifted, the compliance period will have ended, and the full federal mandate

should be in force.

D. Biodiesel Trade

Trade data for biodiesel is problematic since Canada did not have an established HS code for biodiesel

until 2012. Adding to the complication, a European Union anti-dumping trade investigation which

concluded in 2010, revealed inconsistencies between the European Union biodiesel import trade data

and the Canadian biodiesel production capacity, which is still in its infancy. The trade data from before

2012 used in this report is therefore based on a conglomeration of industry discussion, United States

Department of Commerce data, Natural Resources Canada data, and Global Trade Atlas data. Lack of

biodiesel production capacity in some provinces has meant that some provincial mandates have

necessitated the importation of biodiesel to ensure compliance, such as BC in 2010. Imports are

expected to become less necessary over the next few years as production capacity grows and fulfills

more of the federal and provincial mandates. Thus, import amounts are expected to level out in 2013 to

2014. However, this is subject to considerable variation depending on the amount of actual production,

which fluctuates due to changing capacity use. Exports are expected to increase in 2013-2014 as U.S.

demand for biodiesel increases.

Of note, the two Canadian companies that participated in the EU anti-dumping investigation have been

exempt from the anti-dumping duties placed on the Canadian biodiesel industry following the

investigation. Future Canadian biodiesel companies who wish to export biodiesel to the European

Union will be provided the opportunity to apply for exemptions as well.

More information on the EU investigation is available at:

Council implementing regulation no 443/2011 (anti-subsidy)

http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:122:0001:0011:EN:PDF

Council implementing regulation no 444/2011 (anti-dumping)

http://eur-lex.europa.eu/LexUriServ/LexUriServ.do?uri=OJ:L:2011:122:0012:0021:EN:PDF

Canada Biofuels Annual 2013

22

E. Ending Stocks

There are no official statistics kept on biodiesel stocks, so Post has estimated stocks based on trade

balance calculations. However the biodiesel forecast to be put toward stocks could instead be exported

or put toward domestic consumption, depending on Canadian need to meet the mandated renewable

content levels.

V. Advanced Biofuels

While Canada is still not a significant producer of advanced biofuels, over the past few years it has been

making progress toward beginning full-scale operation plants. In 2009, Enerkem opened a

demonstration biofuels and biochemicals facility; in spring of 2012, this plant began production of

cellulosic ethanol via treated wood as feedstock at a 5 million liter capacity. Although this may be the

only advanced biofuels plant in Canada at the current moment, Enerkem is undergoing construction of a

38 million liter, cellulosic ethanol plant in Edmonton, Alberta. Edmonton will provide 100,000 dry

metric tons of municipal solid waste to the plant as feedstock. The plant is expected to be operational in

early 2014. Further into the future, Varennes Cellulosic Ethanol L.P., a joint venture of Enerkem and

Greenfield Ethanol Inc., is also planning a full-scale, cellulosic ethanol plant in Varennes, Quebec. The

plant will use Enerkem’s proprietary thermochemical technology to convert non-recyclable waste into

38 million liters of cellulosic ethanol per year.

There is also Atlantic Canadian interest in producing cellulosic from wood waste or other advanced

feedstock. For more information, please see the below section regarding biofuels in Atlantic Canada.

According to the Canada Gazette, as of February 26, 2011, some biodiesel producers may be

considering the possibility of renovating existing refineries in order to produce hydrotreated vegetable

oil (HVO). These considerations are attributable to some substantial advantages that HVO has over

biodiesel, including higher energy content, no need for temperature regulation during transportation, and

significant convenience for blenders due to the chemical equivalence to diesel. However, HVO is

currently less economic than biodiesel, resulting in less Canadian demand. There are currently no

domestic HVO production facilities, and any intentions to start-up such facilities are not expected to be

fulfilled in the near future.

Although recent data from F.O.Licht has shown relatively little domestic consumption of HVO, there

has been some demand which has, in recent years, pushed imports of HVO to levels comparable to

imports of biodiesel.

VI. Biomass for Heat and Power

Canada Biofuels Annual 2013

23

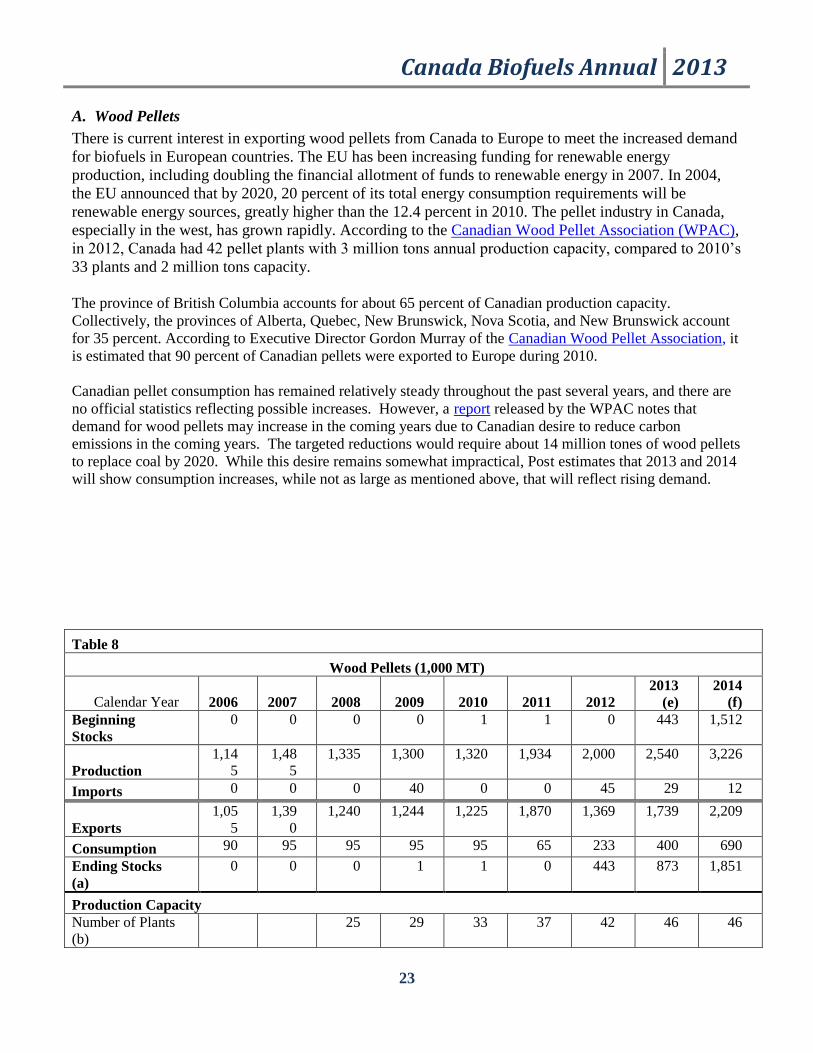

A. Wood Pellets

There is current interest in exporting wood pellets from Canada to Europe to meet the increased demand

for biofuels in European countries. The EU has been increasing funding for renewable energy

production, including doubling the financial allotment of funds to renewable energy in 2007. In 2004,

the EU announced that by 2020, 20 percent of its total energy consumption requirements will be

renewable energy sources, greatly higher than the 12.4 percent in 2010. The pellet industry in Canada,

especially in the west, has grown rapidly. According to the Canadian Wood Pellet Association (WPAC),

in 2012, Canada had 42 pellet plants with 3 million tons annual production capacity, compared to 2010’s

33 plants and 2 million tons capacity.

The province of British Columbia accounts for about 65 percent of Canadian production capacity.

Collectively, the provinces of Alberta, Quebec, New Brunswick, Nova Scotia, and New Brunswick account

for 35 percent. According to Executive Director Gordon Murray of the Canadian Wood Pellet Association, it

is estimated that 90 percent of Canadian pellets were exported to Europe during 2010.

Canadian pellet consumption has remained relatively steady throughout the past several years, and there are

no official statistics reflecting possible increases. However, a report released by the WPAC notes that

demand for wood pellets may increase in the coming years due to Canadian desire to reduce carbon

emissions in the coming years. The targeted reductions would require about 14 million tones of wood pellets

to replace coal by 2020. While this desire remains somewhat impractical, Post estimates that 2013 and 2014

will show consumption increases, while not as large as mentioned above, that will reflect rising demand.

Table 8

Wood Pellets (1,000 MT)

Calendar Year 2006 2007 2008 2009 2010 2011 2012

2013

(e)

2014

(f)

Beginning

Stocks

0 0 0 0 1 1 0 443 1,512

Production

1,14

5

1,48

5

1,335 1,300 1,320 1,934 2,000 2,540 3,226

Imports 0 0 0 40 0 0 45 29 12

Exports

1,05

5

1,39

0

1,240 1,244 1,225 1,870 1,369 1,739 2,209

Consumption 90 95 95 95 95 65 233 400 690

Ending Stocks

(a)

0 0 0 1 1 0 443 873 1,851

Production Capacity

Number of Plants

(b)

25 29 33 37 42 46 46

Canada Biofuels Annual 2013

24

Nameplate

Capacity

1,400 1,700 2,000 2,931 3,000 3,707 3,707

Capacity Use (%)

95.4

%

76.5

%

66.0

%

66.0

%

66.7

%

68.5

%

87.0

%

Data based on available information from the Canadian Wood Pellet Association and Statistics Canada. All other

data estimated based on trend.

(a) No official stock data available. Stocks assumed to reflect trade balance. Wood pellet stock in 2013 and 2014

may be put toward consumption or export depending on Canadian and European future demand.

(b)Plant information regarding number of plants and capacity unavailable before 2008.

B. Fuels Produced from Other Biomass

There has been growing interest and investment in producing bioenergy from sources other than corn

and wheat. Recently, there have been announcements of joint ventures to make cellulosic bioethanol

and biogas, including a joint cellulosic bioethanol venture announced by GreenField Bioethanol and

Enerkem. Enerkem, a Quebec-based gasification and catalysis technology company, has developed

technology to convert biomass such as municipal solid waste and wood residue into cellulosic

bioethanol. Its commercial-scale demonstration facility in Westbury, Quebec, which was completed in

2009, reached 1,000 hours of operation in 2010 and agreed to sell all ethanol produced to GreenField

Ethanol. Enerkem continues to grow, and is in the construction phase of its second plant, in partnership

with the City of Edmonton and Alberta Innovates. The commercial waste-to-biofuels production

facility is scheduled to begin ethanol production in the beginning of 2014. It is expected to have a

production capacity of 38 million liters of ethanol per year.

Biogas is also of increasing interest and investment. Two of the three bio-energy projects that received

funding under Alberta’s Biorefining Commercialization and Market Development Program and the Bio-

energy Infrastructure Development Program are for the development of biogas as an alternative source

of energy. Kingdom Farm Inc. received a significant grant to review the potential for bio-gas from large

scale Alberta hog operations. Highmark Renewables Research also received a significant grant from

AVAC Ltd. for a bio-gas feasibility study at a large scale dairy facility.

Most fuels derived from non-grain biomass remain at the research level. One company moving to

commercialize this technology is Lignol Energy Corporation, which specializes in cellulosic bioethanol

and biorefining. Lignol announced the completion of a fully integrated industrial-scale biorefinery pilot

plant in Burnaby, British Columbia in 2009. This plant is an end-to-end producer of cellulosic

bioethanol. On June 15, 2010, Lignol signed a research and development agreement with Novozymes,

the world’s leading producer of industrial enzymes, to make biofuel from wood chips and other forestry

residues. The partners aim to develop a process for making biofuel from forestry waste at a cost as low

as $2 per gallon, a price competitive with gasoline and corn bioethanol at the current United States’

market prices. On February 7, 2012, it was announced that Sustainable Development Technology

Canada (SDTC) awarded $2.06 million to Lignol, in addition to $4.2 million already contributed.

Ontario Power Generation (OPG) is looking to buy two to three million tons of biomass annually by

2015 – the date at which the Ontario government has mandated an end to burning coal for electricity

generation. Biomass is targeted to replace coal as soon as technical obstacles are overcome. OPG will

Canada Biofuels Annual 2013

25

phase out the use of coal at its thermal electricity stations by the end of 2014. However, for biomass to

completely replace coal, it must find a more efficient and condensed solution for transport and handling.

Canada Biofuels Annual 2013

26

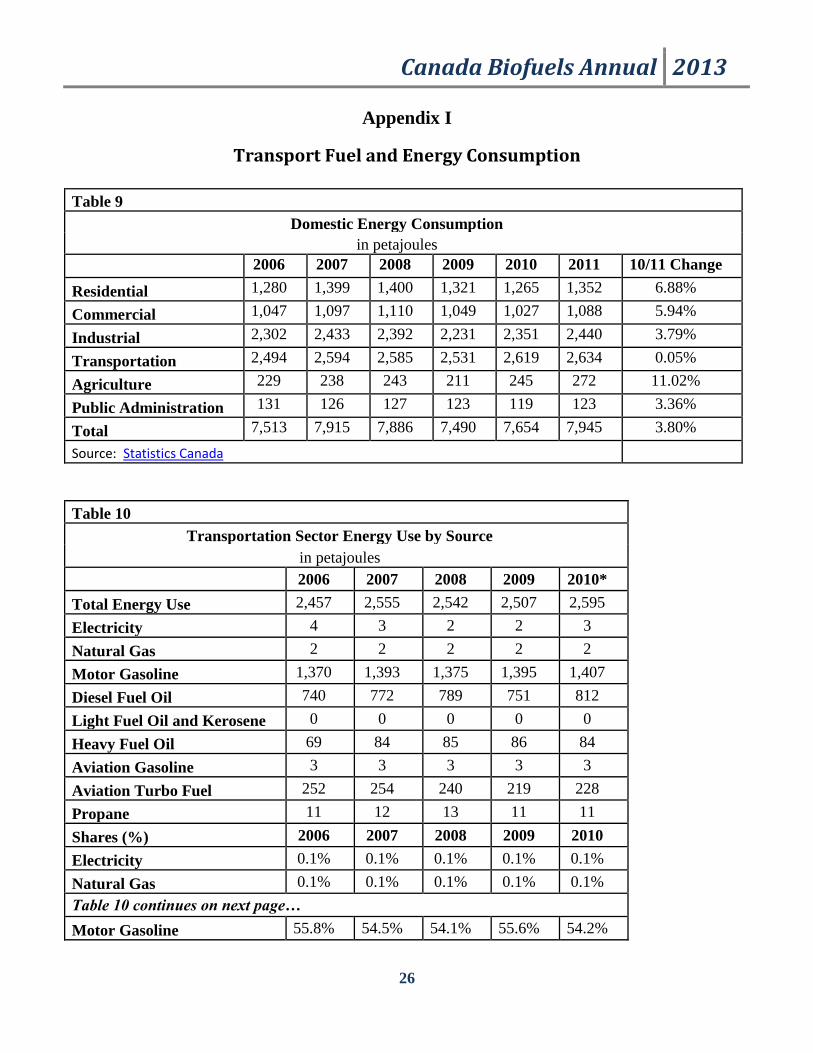

Appendix I

Transport Fuel and Energy Consumption

Table 9

Domestic Energy Consumption

in petajoules

2006 2007 2008 2009 2010 2011 10/11 Change

Residential 1,280 1,399 1,400 1,321 1,265 1,352 6.88%

Commercial 1,047 1,097 1,110 1,049 1,027 1,088 5.94%

Industrial 2,302 2,433 2,392 2,231 2,351 2,440 3.79%

Transportation 2,494 2,594 2,585 2,531 2,619 2,634 0.05%

Agriculture 229 238 243 211 245 272 11.02%

Public Administration 131 126 127 123 119 123 3.36%

Total 7,513 7,915 7,886 7,490 7,654 7,945 3.80%

Source: Statistics Canada

Table 10

Transportation Sector Energy Use by Source

in petajoules

2006 2007 2008 2009 2010*

Total Energy Use 2,457 2,555 2,542 2,507 2,595

Electricity 4 3 2 2 3

Natural Gas 2 2 2 2 2

Motor Gasoline 1,370 1,393 1,375 1,395 1,407

Diesel Fuel Oil 740 772 789 751 812

Light Fuel Oil and Kerosene 0 0 0 0 0

Heavy Fuel Oil 69 84 85 86 84

Aviation Gasoline 3 3 3 3 3

Aviation Turbo Fuel 252 254 240 219 228

Propane 11 12 13 11 11

Shares (%) 2006 2007 2008 2009 2010

Electricity 0.1% 0.1% 0.1% 0.1% 0.1%

Natural Gas 0.1% 0.1% 0.1% 0.1% 0.1%

Table 10 continues on next page…

Motor Gasoline 55.8% 54.5% 54.1% 55.6% 54.2%

Canada Biofuels Annual 2013

27

Diesel Fuel Oil 30.1% 30.2% 31.1% 30.0% 31.3%

Light Fuel Oil and Kerosene 0.0% 0.0% 0.0% 0.0% 0.0%

Heavy Fuel Oil 2.8% 3.3% 3.3% 3.4% 3.2%

Aviation Gasoline 0.1% 0.1% 0.1% 0.1% 0.1%

Aviation Turbo Fuel 10.2% 10.0% 9.4% 8.7% 8.8%

Propane 0.5% 0.5% 0.5% 0.4% 0.4%

* year 2010 is the latest year for which data was available

Source: Office of Energy, Natural Resources Canada

Table 11

Energy Use by Transportation Sector

in petajoules

2006 2007 2008 2009 2010

Total Energy Use 2,457 2,555 2,542 2,507 2,595

Freight 1,005 1,053 1,064 1,038 1,101

Passenger 1,352 1,400 1,376 1,377 1,390

Off road 100 102 102 92 104

Shares (%) 2006 2007 2008 2009 2010

Freight 41% 41% 42% 41% 42%

Passenger 55% 55% 54% 55% 54%

Off road 4% 4% 4% 4% 4%

* year 2010 is the year for which the most recent data is available

Source: Office of Energy , Natural Resources Canada

Canada Biofuels Annual 2013

28

Appendix II

Provincial Mandates, Policies, Tax Exemptions, Incentives and Conditions

A. Alberta Biofuel Policies

Biofuels Strategy/Policy Documents:

The buildup of biofuels production capacity in Alberta has largely been the result of its nine-point

bioenergy plan, first announced in October 2006. In December 2008, the government built on this plan

and announced its Provincial Energy Strategy.

Renewable Fuel Standard:

As part of the strategy, the government of Alberta announced its intention to implement a renewable

fuel standard of 5 percent bioethanol content in gasoline and 2 percent renewable content in diesel by

2010. The implementation was later pushed back to April 1, 2011. In addition, the production and

manufacturing life cycle of the renewable fuel must be at least 25 percent lower than emissions from

producing and manufacturing the same quantity of traditional fossil fuels.

Production Incentives:

As mentioned in Table 13, the province of Alberta offered a Bioenergy producer credit program (PCP).

It was, however, announced in Alberta’s Budget 2013 that future rounds of the PCP have been

discontinued.

Context:

According to the most recent data, Alberta boasts approximately 11 percent of Canada’s total

population, 14 percent of net gasoline sales and 6.5 percent of bioethanol production capacity.

Table 12

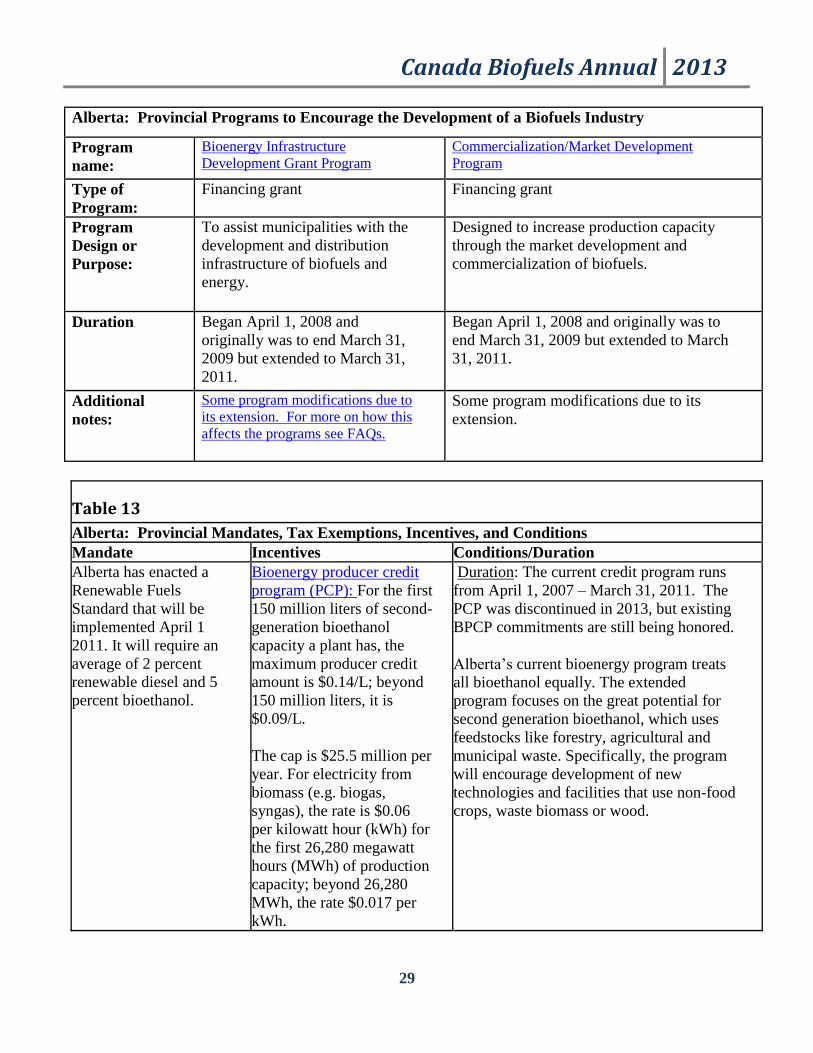

Alberta: Provincial Programs to Encourage the Development of a Biofuels Industry

Program name: Bioenergy Infrastructure

Development Grant Program

Commercialization/Market Development

Program

Budget

Allocation:

Alberta’s Biorefining Commercialization and Market Development Program and

Bioenergy Infrastructure Development Program have both been fully allocated and

expired on March 31, 2011. Together, the programs supported more than 70

bioenergy projects with grants totalling approximately $150 million.

These two programs are no longer accepting applications.

Administering

Ministry

Alberta Energy

Table 12 continued on following page…

Canada Biofuels Annual 2013

29

Alberta: Provincial Programs to Encourage the Development of a Biofuels Industry

Program

name:

Bioenergy Infrastructure

Development Grant Program

Commercialization/Market Development

Program

Type of

Program:

Financing grant Financing grant

Program

Design or

Purpose:

To assist municipalities with the

development and distribution

infrastructure of biofuels and

energy.

Designed to increase production capacity

through the market development and

commercialization of biofuels.

Duration Began April 1, 2008 and

originally was to end March 31,

2009 but extended to March 31,

2011.

Began April 1, 2008 and originally was to

end March 31, 2009 but extended to March

31, 2011.

Additional

notes:

Some program modifications due to

its extension. For more on how this

affects the programs see FAQs.

Some program modifications due to its

extension.

Table 13

Alberta: Provincial Mandates, Tax Exemptions, Incentives, and Conditions

Mandate Incentives Conditions/Duration

Alberta has enacted a

Renewable Fuels

Standard that will be

implemented April 1

2011. It will require an

average of 2 percent

renewable diesel and 5

percent bioethanol.

Bioenergy producer credit

program (PCP): For the first

150 million liters of second-

generation bioethanol

capacity a plant has, the

maximum producer credit

amount is $0.14/L; beyond

150 million liters, it is

$0.09/L.

The cap is $25.5 million per

year. For electricity from

biomass (e.g. biogas,

syngas), the rate is $0.06

per kilowatt hour (kWh) for

the first 26,280 megawatt

hours (MWh) of production

capacity; beyond 26,280

MWh, the rate $0.017 per

kWh.

Duration: The current credit program runs

from April 1, 2007 – March 31, 2011. The

PCP was discontinued in 2013, but existing

BPCP commitments are still being honored.

Alberta’s current bioenergy program treats

all bioethanol equally. The extended

program focuses on the great potential for

second generation bioethanol, which uses

feedstocks like forestry, agricultural and

municipal waste. Specifically, the program

will encourage development of new

technologies and facilities that use non-food

crops, waste biomass or wood.

Canada Biofuels Annual 2013

30

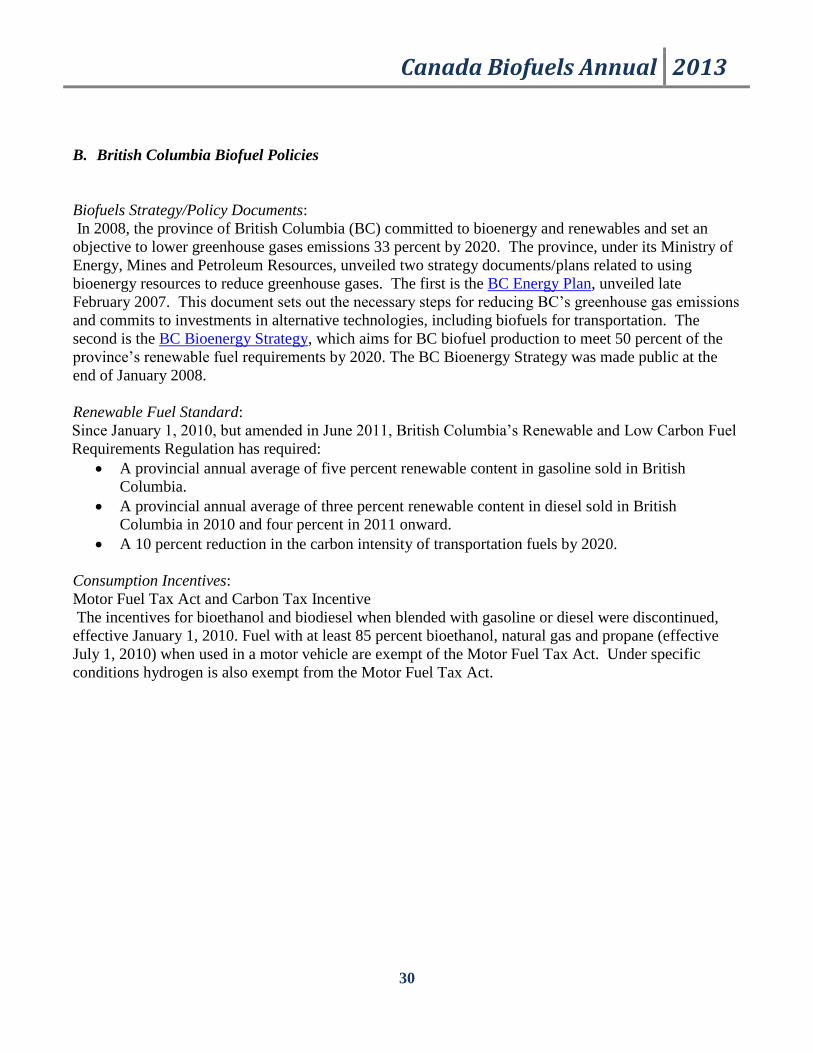

B. British Columbia Biofuel Policies

Biofuels Strategy/Policy Documents:

In 2008, the province of British Columbia (BC) committed to bioenergy and renewables and set an

objective to lower greenhouse gases emissions 33 percent by 2020. The province, under its Ministry of

Energy, Mines and Petroleum Resources, unveiled two strategy documents/plans related to using

bioenergy resources to reduce greenhouse gases. The first is the BC Energy Plan, unveiled late

February 2007. This document sets out the necessary steps for reducing BC’s greenhouse gas emissions

and commits to investments in alternative technologies, including biofuels for transportation. The

second is the BC Bioenergy Strategy, which aims for BC biofuel production to meet 50 percent of the

province’s renewable fuel requirements by 2020. The BC Bioenergy Strategy was made public at the

end of January 2008.

Renewable Fuel Standard:

Since January 1, 2010, but amended in June 2011, British Columbia’s Renewable and Low Carbon Fuel

Requirements Regulation has required:

A provincial annual average of five percent renewable content in gasoline sold in British

Columbia.

A provincial annual average of three percent renewable content in diesel sold in British

Columbia in 2010 and four percent in 2011 onward.

A 10 percent reduction in the carbon intensity of transportation fuels by 2020.

Consumption Incentives:

Motor Fuel Tax Act and Carbon Tax Incentive

The incentives for bioethanol and biodiesel when blended with gasoline or diesel were discontinued,

effective January 1, 2010. Fuel with at least 85 percent bioethanol, natural gas and propane (effective

July 1, 2010) when used in a motor vehicle are exempt of the Motor Fuel Tax Act. Under specific

conditions hydrogen is also exempt from the Motor Fuel Tax Act.

Canada Biofuels Annual 2013

31

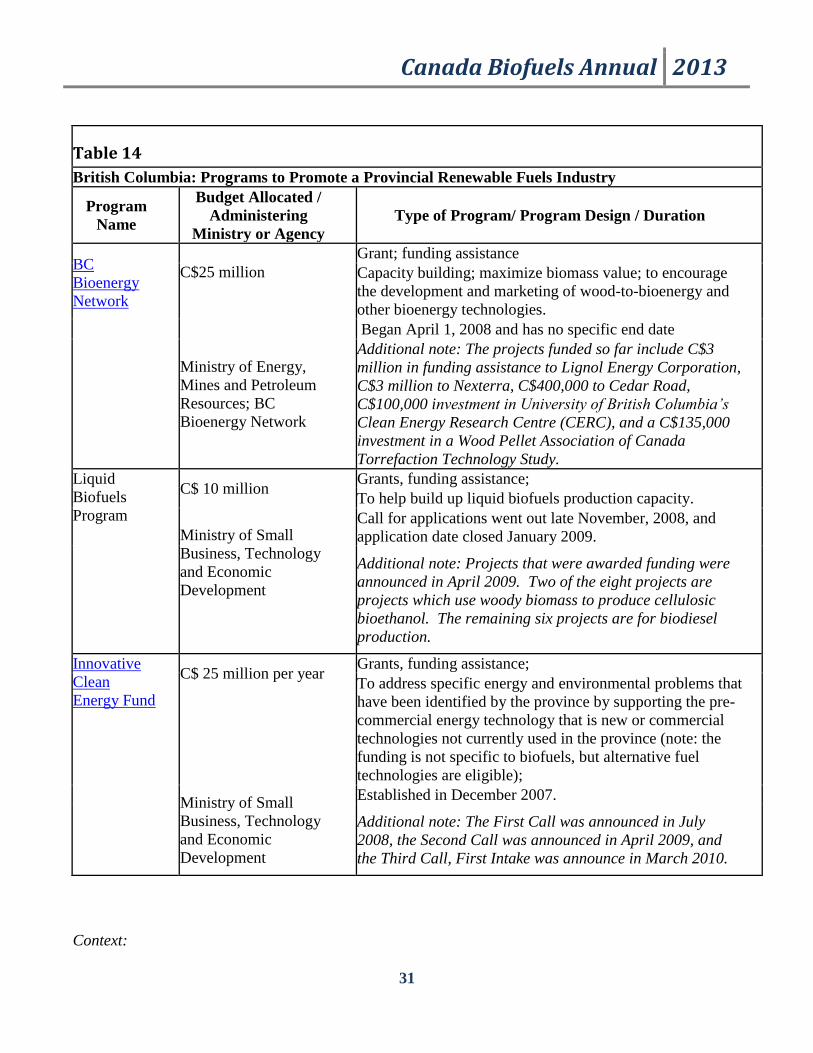

Table 14

British Columbia: Programs to Promote a Provincial Renewable Fuels Industry

Program

Name

Budget Allocated /

Administering

Ministry or Agency

Type of Program/ Program Design / Duration

BC

Bioenergy

Network

C$25 million

Grant; funding assistance

Capacity building; maximize biomass value; to encourage

the development and marketing of wood-to-bioenergy and

other bioenergy technologies.

Ministry of Energy,

Mines and Petroleum

Resources; BC

Bioenergy Network

Began April 1, 2008 and has no specific end date

Additional note: The projects funded so far include C$3

million in funding assistance to Lignol Energy Corporation,

C$3 million to Nexterra, C$400,000 to Cedar Road,

C$100,000 investment in University of British Columbia’s

Clean Energy Research Centre (CERC), and a C$135,000

investment in a Wood Pellet Association of Canada

Torrefaction Technology Study.

Liquid

Biofuels

Program

C$ 10 million Grants, funding assistance;

To help build up liquid biofuels production capacity.

Ministry of Small

Business, Technology

and Economic

Development

Call for applications went out late November, 2008, and

application date closed January 2009.

Additional note: Projects that were awarded funding were

announced in April 2009. Two of the eight projects are

projects which use woody biomass to produce cellulosic

bioethanol. The remaining six projects are for biodiesel

production.

Innovative

Clean

Energy Fund

C$ 25 million per year

Grants, funding assistance;

To address specific energy and environmental problems that

have been identified by the province by supporting the pre-

commercial energy technology that is new or commercial

technologies not currently used in the province (note: the

funding is not specific to biofuels, but alternative fuel

technologies are eligible);

Ministry of Small

Business, Technology

and Economic

Development

Established in December 2007.

Additional note: The First Call was announced in July

2008, the Second Call was announced in April 2009, and

the Third Call, First Intake was announce in March 2010.

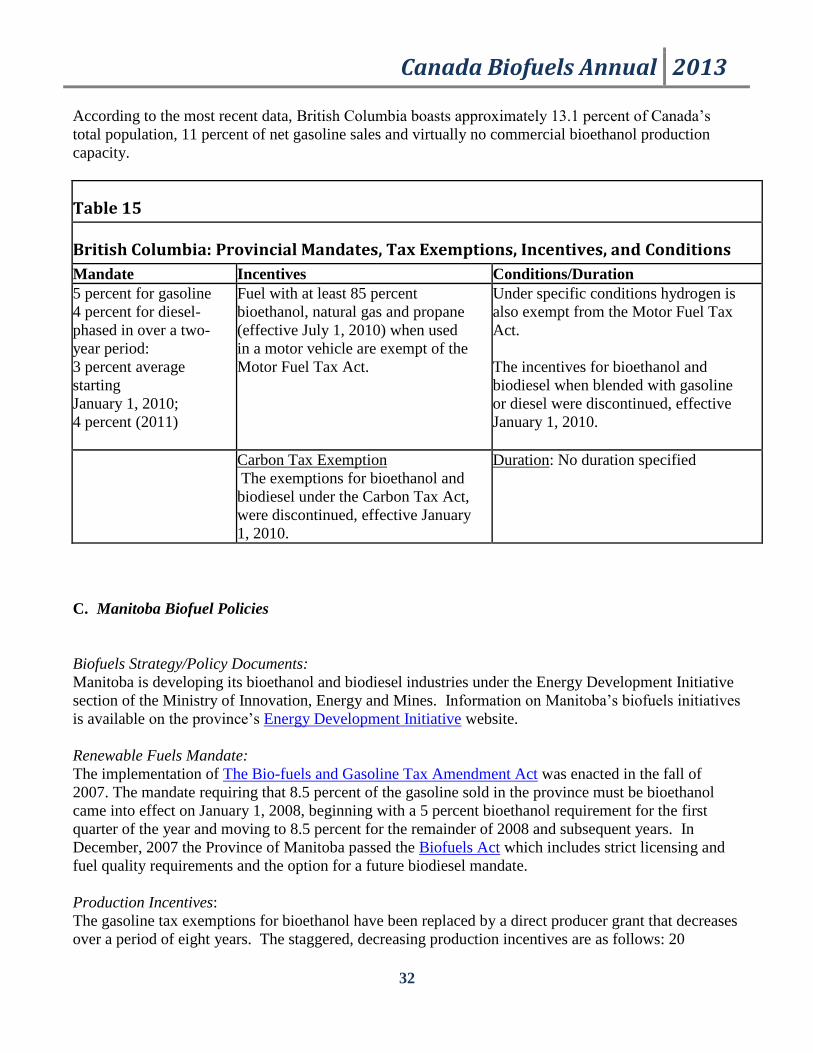

Context:

Canada Biofuels Annual 2013

32

According to the most recent data, British Columbia boasts approximately 13.1 percent of Canada’s

total population, 11 percent of net gasoline sales and virtually no commercial bioethanol production

capacity.

Table 15

British Columbia: Provincial Mandates, Tax Exemptions, Incentives, and Conditions

Mandate Incentives Conditions/Duration

5 percent for gasoline

4 percent for diesel-

phased in over a two-

year period:

3 percent average

starting

January 1, 2010;

4 percent (2011)

Fuel with at least 85 percent

bioethanol, natural gas and propane

(effective July 1, 2010) when used

in a motor vehicle are exempt of the

Motor Fuel Tax Act.

Under specific conditions hydrogen is

also exempt from the Motor Fuel Tax

Act.

The incentives for bioethanol and

biodiesel when blended with gasoline

or diesel were discontinued, effective

January 1, 2010.

Carbon Tax Exemption

The exemptions for bioethanol and

biodiesel under the Carbon Tax Act,

were discontinued, effective January

1, 2010.

Duration: No duration specified

C. Manitoba Biofuel Policies

Biofuels Strategy/Policy Documents:

Manitoba is developing its bioethanol and biodiesel industries under the Energy Development Initiative

section of the Ministry of Innovation, Energy and Mines. Information on Manitoba’s biofuels initiatives

is available on the province’s Energy Development Initiative website.

Renewable Fuels Mandate:

The implementation of The Bio-fuels and Gasoline Tax Amendment Act was enacted in the fall of

2007. The mandate requiring that 8.5 percent of the gasoline sold in the province must be bioethanol

came into effect on January 1, 2008, beginning with a 5 percent bioethanol requirement for the first

quarter of the year and moving to 8.5 percent for the remainder of 2008 and subsequent years. In

December, 2007 the Province of Manitoba passed the Biofuels Act which includes strict licensing and

fuel quality requirements and the option for a future biodiesel mandate.

Production Incentives:

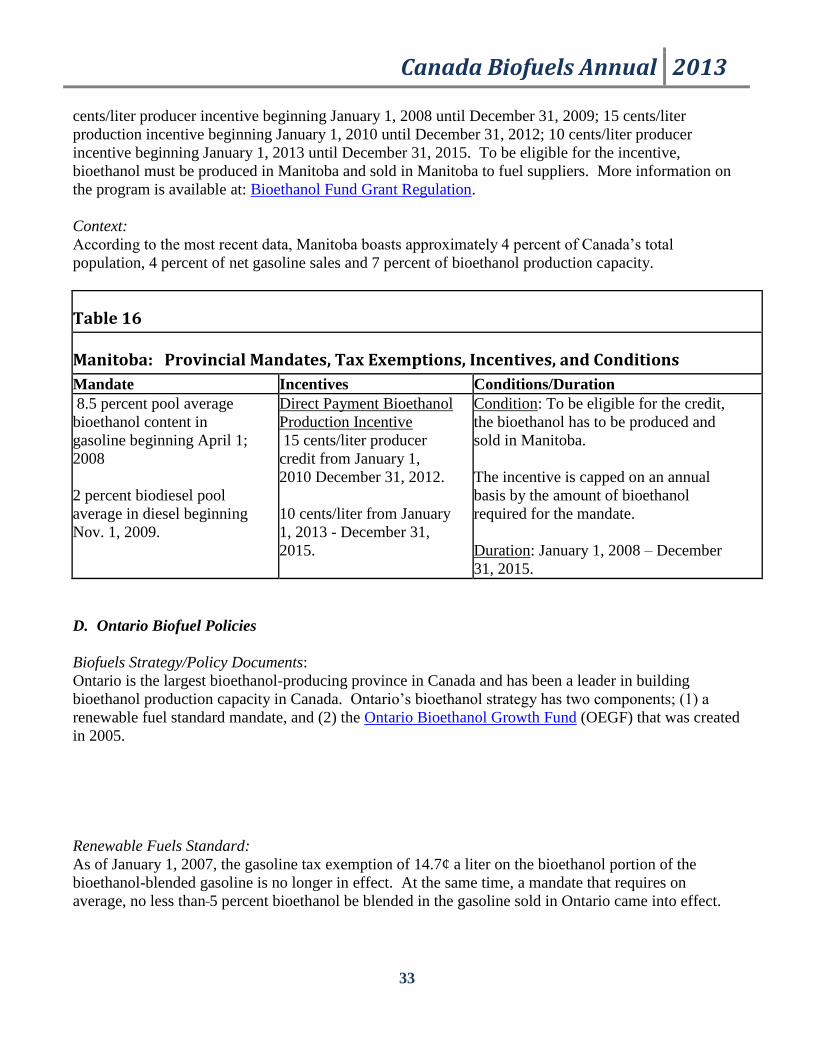

The gasoline tax exemptions for bioethanol have been replaced by a direct producer grant that decreases

over a period of eight years. The staggered, decreasing production incentives are as follows: 20

Canada Biofuels Annual 2013

33

cents/liter producer incentive beginning January 1, 2008 until December 31, 2009; 15 cents/liter

production incentive beginning January 1, 2010 until December 31, 2012; 10 cents/liter producer

incentive beginning January 1, 2013 until December 31, 2015. To be eligible for the incentive,

bioethanol must be produced in Manitoba and sold in Manitoba to fuel suppliers. More information on

the program is available at: Bioethanol Fund Grant Regulation.

Context:

According to the most recent data, Manitoba boasts approximately 4 percent of Canada’s total

population, 4 percent of net gasoline sales and 7 percent of bioethanol production capacity.

Table 16

Manitoba: Provincial Mandates, Tax Exemptions, Incentives, and Conditions

Mandate Incentives Conditions/Duration

8.5 percent pool average

bioethanol content in

gasoline beginning April 1;

2008

2 percent biodiesel pool

average in diesel beginning

Nov. 1, 2009.

Direct Payment Bioethanol

Production Incentive

15 cents/liter producer

credit from January 1,

2010 December 31, 2012.

10 cents/liter from January

1, 2013 - December 31,

2015.