Embed Size (px)

Citation preview

Business Overview and Opportunities

1

Philip J. Hawk, Chairman and CEO

Ted W. Owen, EVP and CFO

November 2010

Updated November 2, 2010

2

Safe Harbor Statement

Statements and projections in this presentation that relate to future results and

events are forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995 and are based upon our current expectations. Such

forward-looking statements and projections involve estimates, assumptions,

judgments and uncertainties. We have made reasonable efforts to ensure that the

information, assumptions and beliefs upon which these forward-looking statements

and projections are based are current, reasonable and complete. However, there

are a variety of known and unknown factors that could cause our actual results or

outcomes to differ materially from the projections, anticipated results or other

expectations expressed in this release. Such known factors are detailed in our

Annual Report on Form 10-K for the year ended May 31, 2010 and in our other

filings with the Securities and Exchange Commission. Accordingly, there can be no

assurance that the forward-looking statements and projections contained will occur

or that our objectives will be achieved. We assume no obligation to publicly update

or revise any forward-looking statements made today or any other forward-looking

statements made by the company, whether as a result of new information, future

events or otherwise.

3

Discussion Topics

Review Team’s business focus, strategy and recent

performance

Discuss Team’s recent purchase of Quest Integrity Group

Provide Team’s financial information and guidance

4

Overview of BusinessSpecialty Industrial Services

• Leading provider of specialty industrial services related to maintenance and installation of pressurized piping systems and processes and inspection

• Offers array of eight complementary services

• Organized into 2 divisions– TCM – Inspection/field heat treat– TMS – Mechanical service lines

• Largest North American service network with more than 100 locations

• Largest industry market share

• 3000+ employees

• Strong record of profitable growth

5

Inspection Services – NDT– Electro-Magnetic Testing – Magnetic Particle Testing– Radiographic Testing– Ultrasonic Testing– Liquid Penetrates Testing– Visual Inspection– Engineering– Metallurgical– Advanced Testing Methods

Heat Treating Services– Electric Resistance– Combustion– Equipment Sales / Rental / Repair

Service Offerings - TCM Division

6

Service Offerings - TMS Division

Mechanical On-Stream Services

– Leak Repair Services

– Hot Tapping Services

Leak Detection & Repair Services (LDAR)

Turnaround / Outage Services

– Field Machining Services

– Technical Bolting Services

– Valve Repair Services

– Pipe Isolation Services

7

US Service Locations

Mobile

BeaumontCorpus Christi

Houston

Texas City

Lake Charles

Lafayette

Baton Rouge

New Orleans

Los Angeles

San Francisco

Seattle

Billings

Salt Lake City

Denver

Minneapolis

Borger

Tulsa

St. Louis

ChicagoToledo

CincinnatiCharleston

Pittsburgh

Richmond

Syracuse

Philadelphia

New York City

Manchester

Odessa

Chattanooga

DecaturAugusta

Wilmington

Tampa

Columbus

Phoenix

Jacksonville

Cleveland

Detroit

Hammond

Hartford

Milwaukee

Branch Office

Branch Office and Equipment Center

Rumford

Longview

Kansas City

CharlotteMemphis

Missoula

Crown Point

8

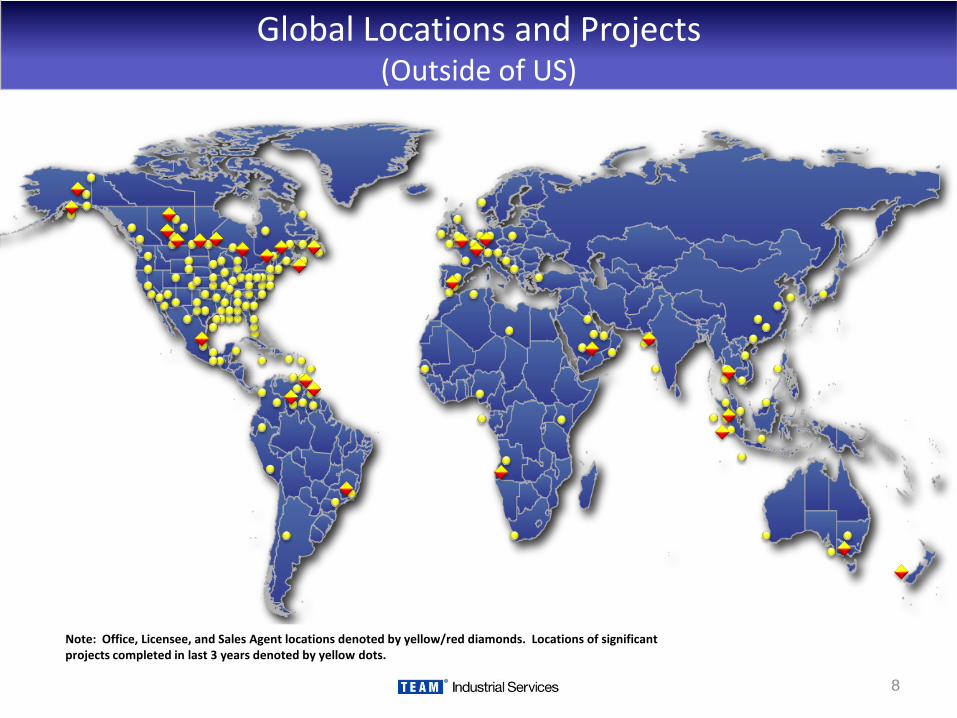

Global Locations and Projects (Outside of US)

Note: Office, Licensee, and Sales Agent locations denoted by yellow/red diamonds. Locations of significant projects completed in last 3 years denoted by yellow dots.

9

Industries Served

Petrochemical RefineriesPower

(Nuclear / Fossil / Hydro)

Pipeline Pulp & Paper Steel

Aerospace Hospitals Contractors

10

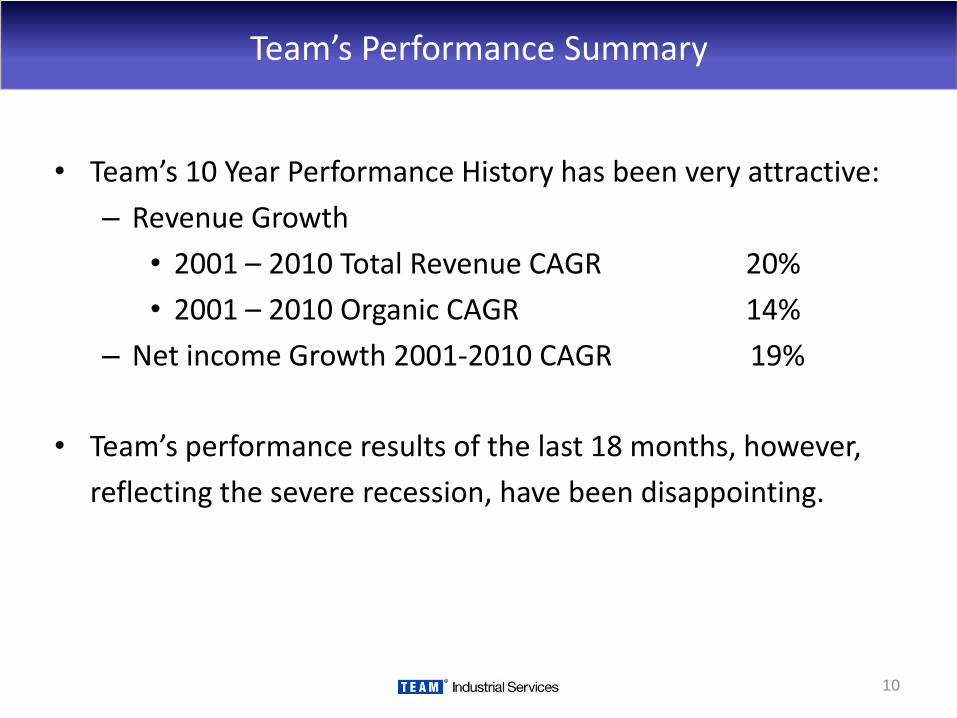

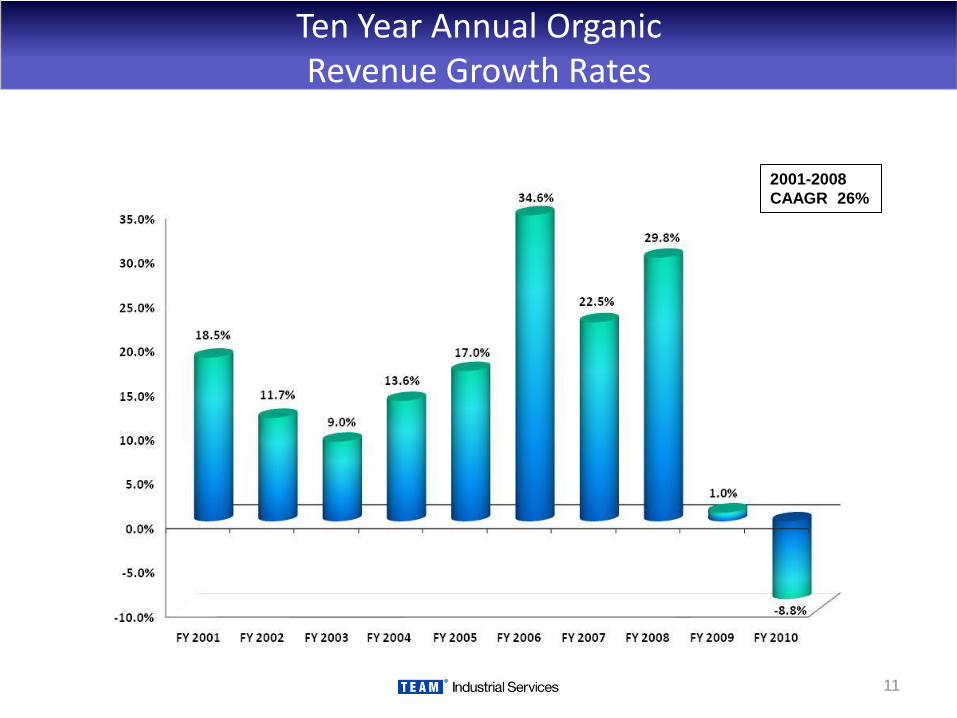

Team’s Performance Summary

• Team’s 10 Year Performance History has been very attractive:

– Revenue Growth

• 2001 – 2010 Total Revenue CAGR 20%

• 2001 – 2010 Organic CAGR 14%

– Net income Growth 2001-2010 CAGR 19%

• Team’s performance results of the last 18 months, however,

reflecting the severe recession, have been disappointing.

11

Ten Year Annual Organic Revenue Growth Rates

2001-2008

CAAGR 26%

12

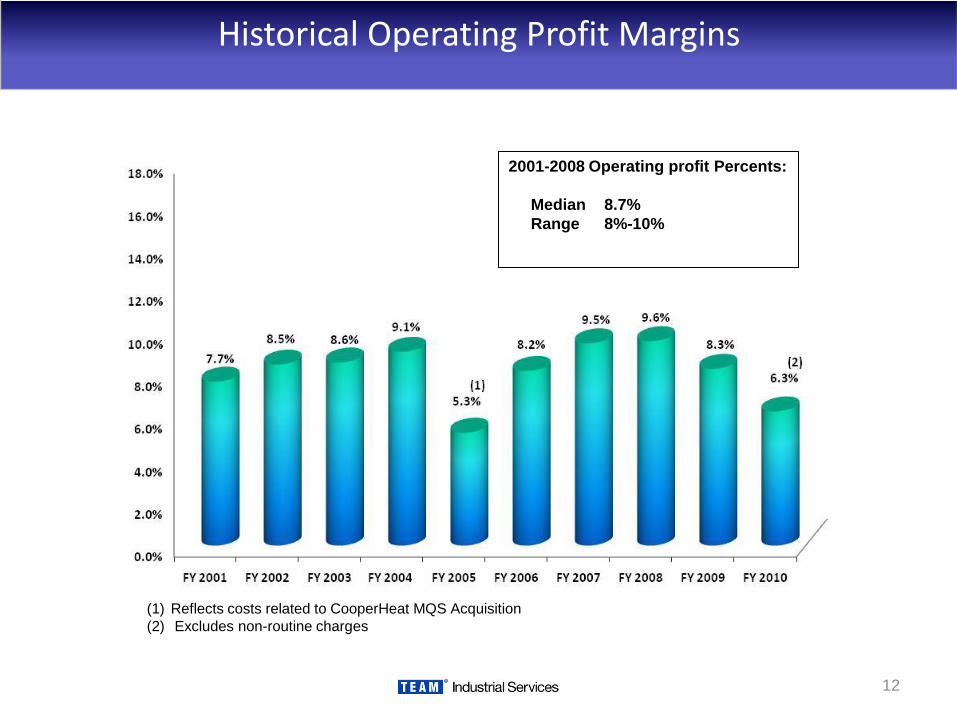

Historical Operating Profit Margins

(1) Reflects costs related to CooperHeat MQS Acquisition

(2) Excludes non-routine charges

2001-2008 Operating profit Percents:

Median 8.7%

Range 8%-10%

13

Key Investor Questions

• Can Team become a growth business again? How? When?

• Can Team’s historical profit margins be achieved and maintained in current market environment?

14

Team’s Answers

• Despite continuing difficult market conditions, Team expects revenue growth in the current fiscal year

• Team expects to achieve significant operating leverage from its near term growth and continued strong cash flow from operations

• Team’s longer term growth and performance prospects remain excellent

15

Our Perspective on Growth

• Despite continuing difficult market conditions, Team expects revenue growth in the current fiscal year– Demand for services has stabilized (but at a lower level)

– Team’s fundamental structural advantages are as relevant as ever

– Team has adapted its business development approach to reflect current market conditions and procurement processes

– New capabilities are creating supplemental growth opportunities

– We believe our growth began in last year’s fourth quarter

16

End Market Fundamentals

• Large, broad based market

– All plants/pipelines with pressurized piping systems require services – 10,000+ plants

– Overall market size - $2.5 billion in North America

• Stable demand – 85%+ of Business Related to Maintenance Activities

– Our services are required for uptime and safe operations – not discretionary over long-term

– Hydraulic, thermal, and corrosive stresses degrade piping systems

• No customer more than 5% of revenues

• Large number of competitors—still highly fragmented

17

Market and Competitive Overview

• Highly fragmented competitive landscape – Limited capital intensity, limited entry barriers historically – a

“service business”

– Business evolved locally as plants used local service personnel they knew

– Only a few service providers with multi-service and national presence

• Only one other national, multi-service line competitor

• More than 100 “Mom & Pop” competitors

18

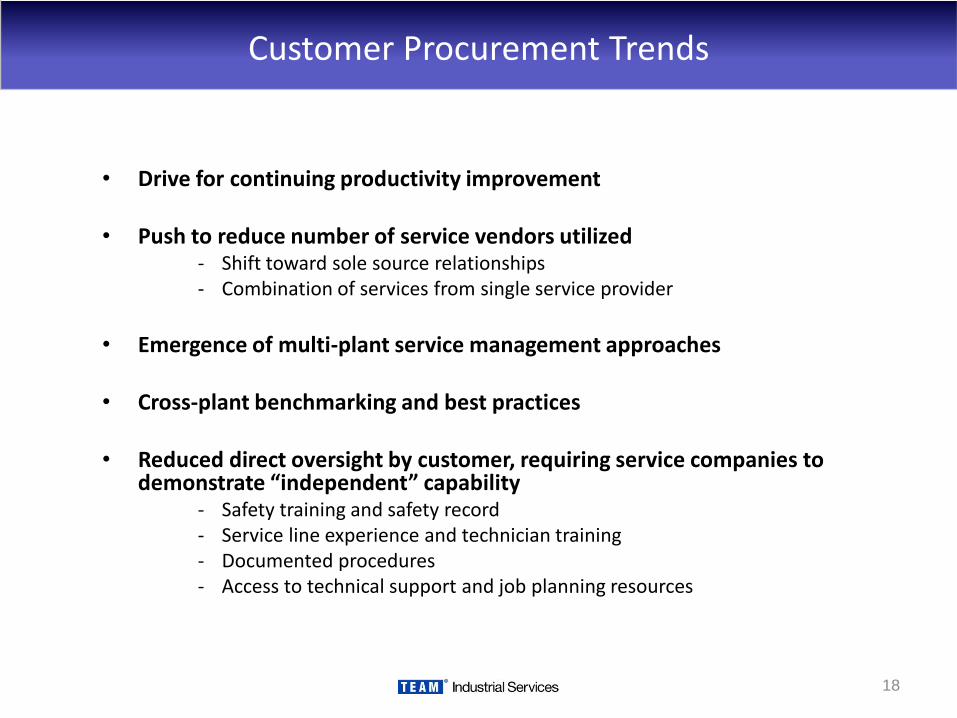

Customer Procurement Trends

• Drive for continuing productivity improvement

• Push to reduce number of service vendors utilized- Shift toward sole source relationships- Combination of services from single service provider

• Emergence of multi-plant service management approaches

• Cross-plant benchmarking and best practices

• Reduced direct oversight by customer, requiring service companies to demonstrate “independent” capability

- Safety training and safety record- Service line experience and technician training - Documented procedures- Access to technical support and job planning resources

19

Recent Customer/Industry Trends

• Global Economic Recession

• New Project Activity Significantly Reduced

• Oil and Refining Beginning to Stabilize

• Increased Focus on Price/Rates

• Interest in New Pricing Arrangements

• Safety and Quality Expectations are Higher

20

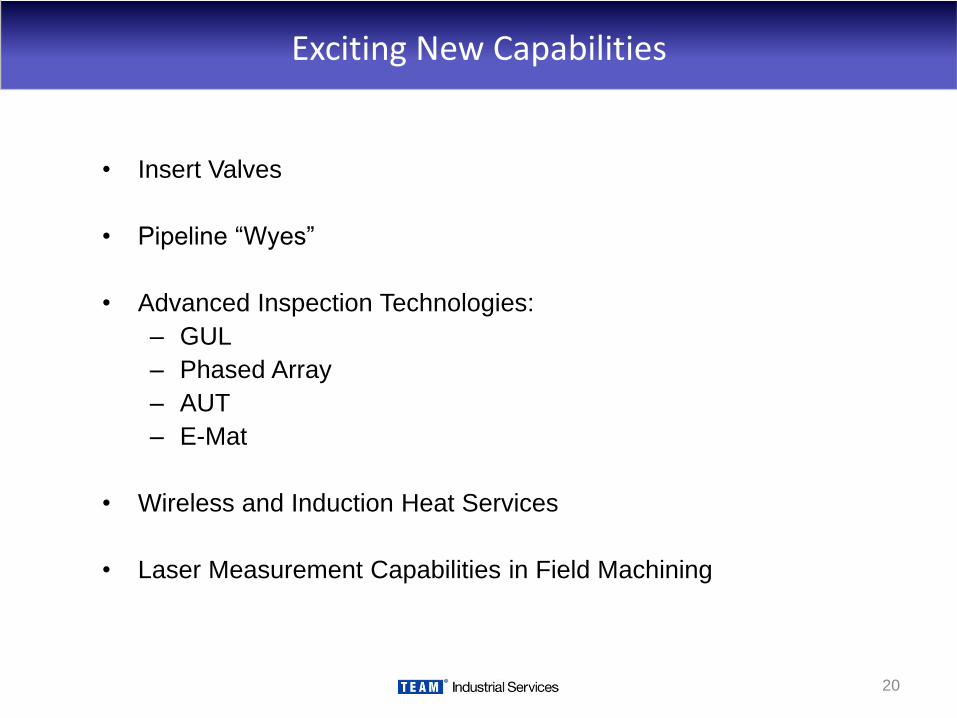

Exciting New Capabilities

• Insert Valves

• Pipeline “Wyes”

• Advanced Inspection Technologies:

– GUL

– Phased Array

– AUT

– E-Mat

• Wireless and Induction Heat Services

• Laser Measurement Capabilities in Field Machining

21

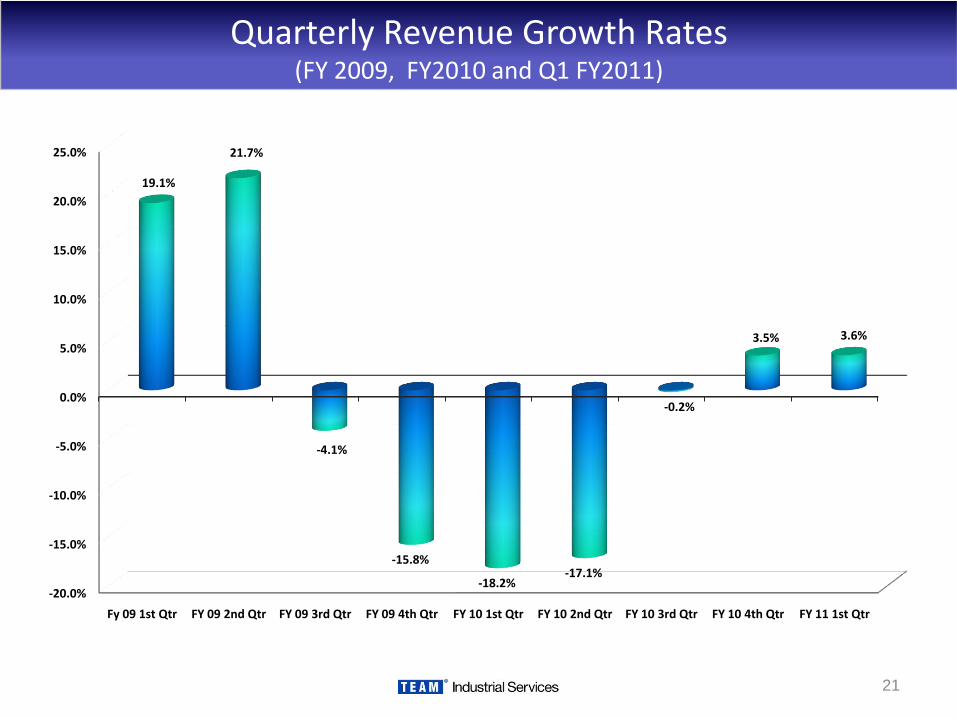

Quarterly Revenue Growth Rates(FY 2009, FY2010 and Q1 FY2011)

-20.0%

-15.0%

-10.0%

-5.0%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

Fy 09 1st Qtr FY 09 2nd Qtr FY 09 3rd Qtr FY 09 4th Qtr FY 10 1st Qtr FY 10 2nd Qtr FY 10 3rd Qtr FY 10 4th Qtr FY 11 1st Qtr

19.1%

21.7%

-4.1%

-15.8%

-18.2%-17.1%

-0.2%

3.5% 3.6%

22

Our Perspective on Operating Leverage

• Despite continuing difficult market conditions, Team expects revenue growth in the current fiscal year

• Team expects to achieve significant operating leverage from its near term growth and continued strong cash flow from operations– Team has substantially reduced its cost base over the past couple of years

– Working Capital performance improvements have lowered the investment requirements of future growth

23

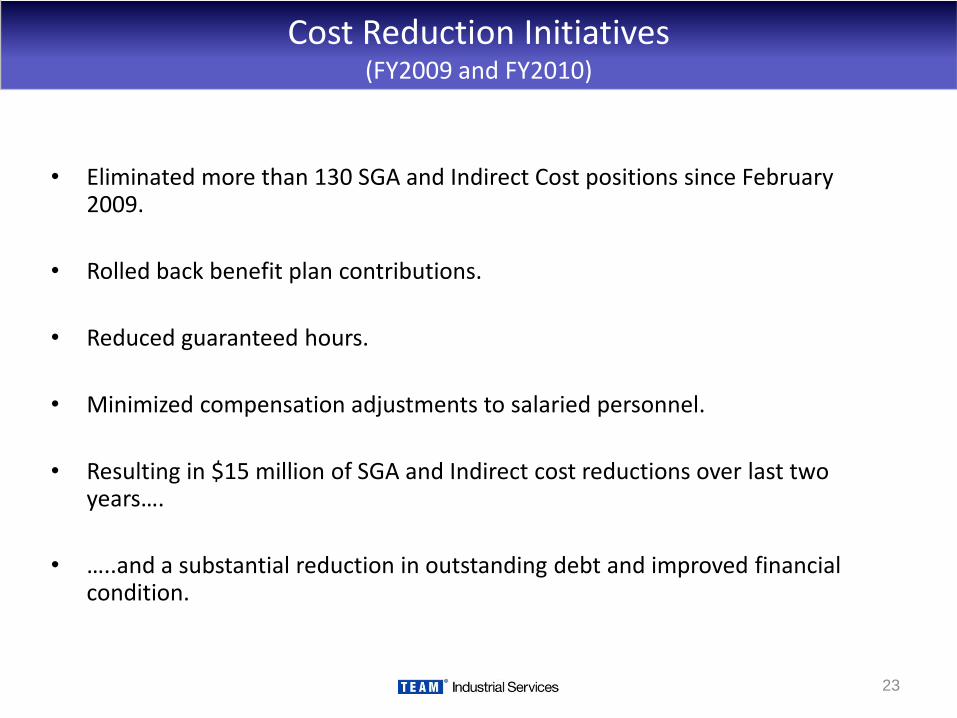

Cost Reduction Initiatives(FY2009 and FY2010)

• Eliminated more than 130 SGA and Indirect Cost positions since February 2009.

• Rolled back benefit plan contributions.

• Reduced guaranteed hours.

• Minimized compensation adjustments to salaried personnel.

• Resulting in $15 million of SGA and Indirect cost reductions over last two years….

• …..and a substantial reduction in outstanding debt and improved financial condition.

24

Our Perspective on Long Term Growth

• Despite continuing difficult market conditions, Team expects revenue growth in the current fiscal year

• Team expects to achieve significant operating leverage from its near term growth and continued strong cash flow from operations

• Team’s longer term growth and performance prospects remain excellent

– Current market share is less than 20%

– Potential growth in a number of exciting areas

– Corresponding profit growth/growth in business is highly leveraged.

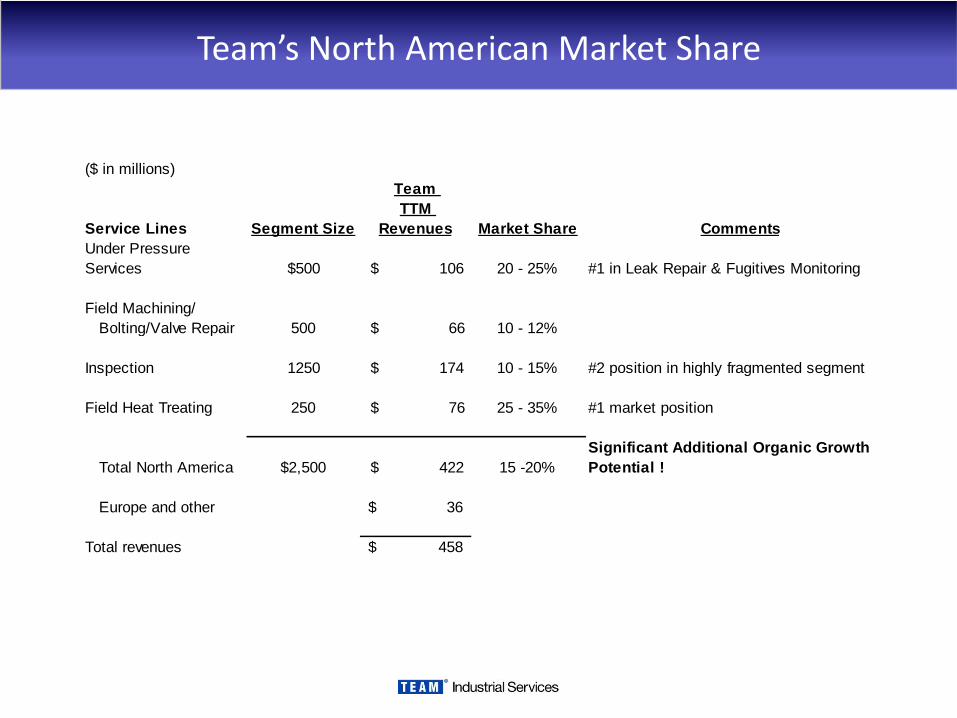

Team’s North American Market Share

($ in millions)

Team

TTM

Revenues

Under Pressure

Services $500 $ 106 20 - 25% #1 in Leak Repair & Fugitives Monitoring

Field Machining/

Bolting/Valve Repair

Inspection 1250 $ 174 10 - 15% #2 position in highly fragmented segment

Field Heat Treating 250 $ 76 25 - 35% #1 market position

Total North America $2,500 $ 422 15 -20%

Significant Additional Organic Growth

Potential !

Europe and other 36$

Total revenues 458$

Service Lines Segment Size Market Share Comments

500 $ 66 10 - 12%

26

Our Growth Strategy

• Continue to expand business by capitalizing on large, broad-based service network

– Extend service offering to complementary services– Continue pursuit of multi-service/multi-plant agreements in response to

procurement trends

• Supplement organic growth with opportunistic acquisitions– Complementary services– Geographic extensions

• Europe/Asia

• New markets for current services

• Bring revenue growth to the bottom-line– Manage job margins and supporting costs– Capture inherent operating leverage in business growth

• “Stay a great service company!”

27

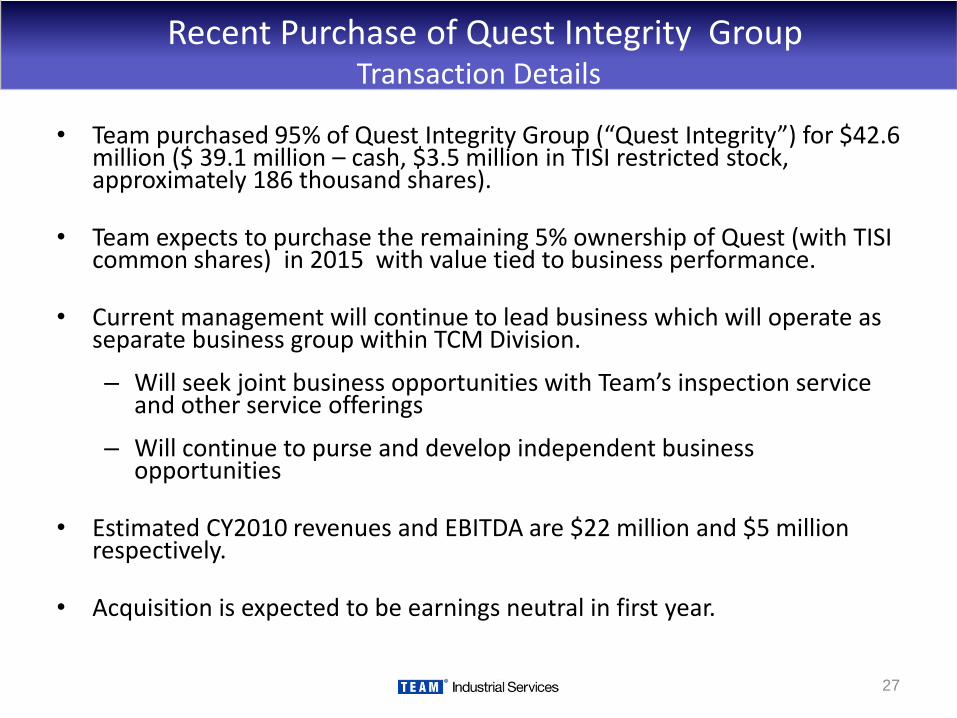

Recent Purchase of Quest Integrity GroupTransaction Details

• Team purchased 95% of Quest Integrity Group (“Quest Integrity”) for $42.6 million ($ 39.1 million – cash, $3.5 million in TISI restricted stock, approximately 186 thousand shares).

• Team expects to purchase the remaining 5% ownership of Quest (with TISI common shares) in 2015 with value tied to business performance.

• Current management will continue to lead business which will operate as separate business group within TCM Division.

– Will seek joint business opportunities with Team’s inspection service and other service offerings

– Will continue to purse and develop independent business opportunities

• Estimated CY2010 revenues and EBITDA are $22 million and $5 million respectively.

• Acquisition is expected to be earnings neutral in first year.

28

Strategic Goals for Quest Integrity Acquisition

• Expand the revenues and margins of Team’s inspection services business

– Enhance reputation to provide state-of-the-art, value-based solutions to customers

– Create growth opportunities in several new market segments and possibly accelerate growth opportunities in existing market segments

– Sustain strategic leadership in service segment via access to new and emerging technologies over time

• Capitalize on and accelerate, where appropriate, the future growth and performance of Quest Integrity Group

– Collaborate on North American market opportunities and increase market access/penetration for Quest Integrity Group services

– Provide appropriate corporate support and oversight for the high growth technology-enabled inspection services and capabilities

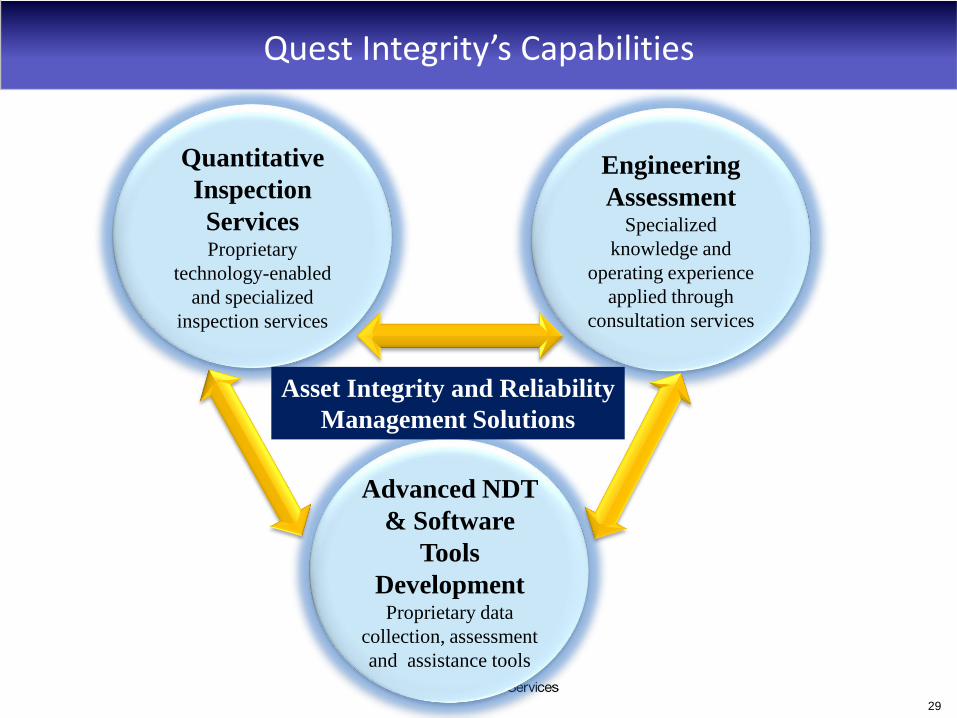

Quest Integrity’s Capabilities

29

Quantitative

Inspection

ServicesProprietary

technology-enabled

and specialized

inspection services

Engineering

AssessmentSpecialized

knowledge and

operating experience

applied through

consultation services

Advanced NDT

& Software

Tools

DevelopmentProprietary data

collection, assessment

and assistance tools

Asset Integrity and Reliability

Management Solutions

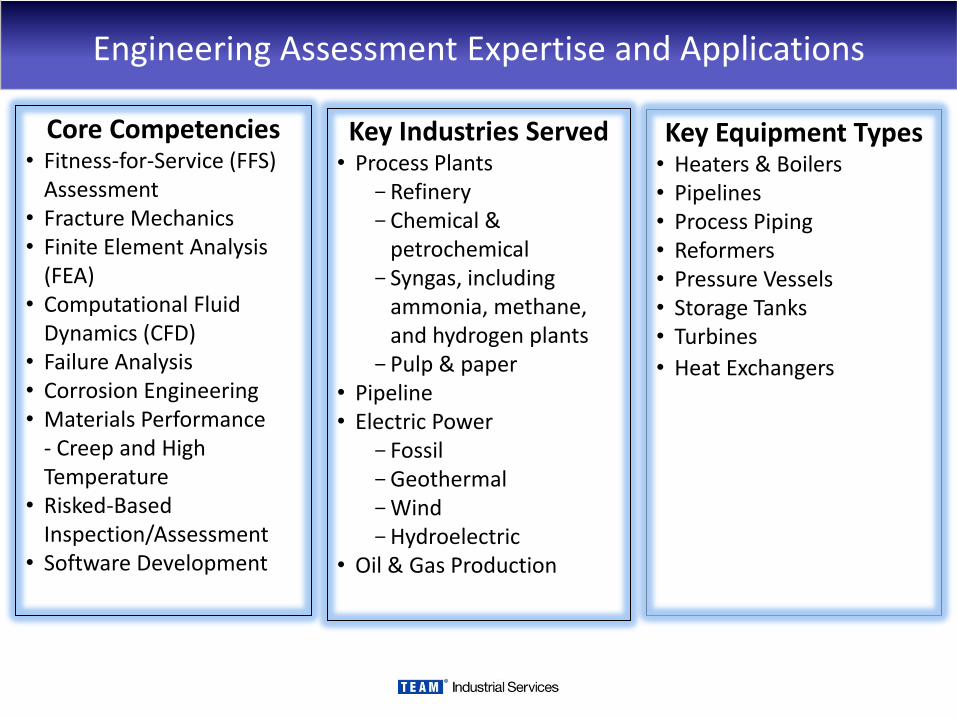

Engineering Assessment Expertise and Applications

Core Competencies • Fitness-for-Service (FFS)

Assessment• Fracture Mechanics• Finite Element Analysis

(FEA)• Computational Fluid

Dynamics (CFD)• Failure Analysis• Corrosion Engineering• Materials Performance

- Creep and High Temperature

• Risked-Based Inspection/Assessment

• Software Development

Key Industries Served• Process Plants

RefineryChemical &

petrochemicalSyngas, including

ammonia, methane, and hydrogen plants

Pulp & paper• Pipeline• Electric Power

FossilGeothermalWindHydroelectric

• Oil & Gas Production

Key Equipment Types• Heaters & Boilers• Pipelines• Process Piping• Reformers• Pressure Vessels• Storage Tanks• Turbines

• Heat Exchangers

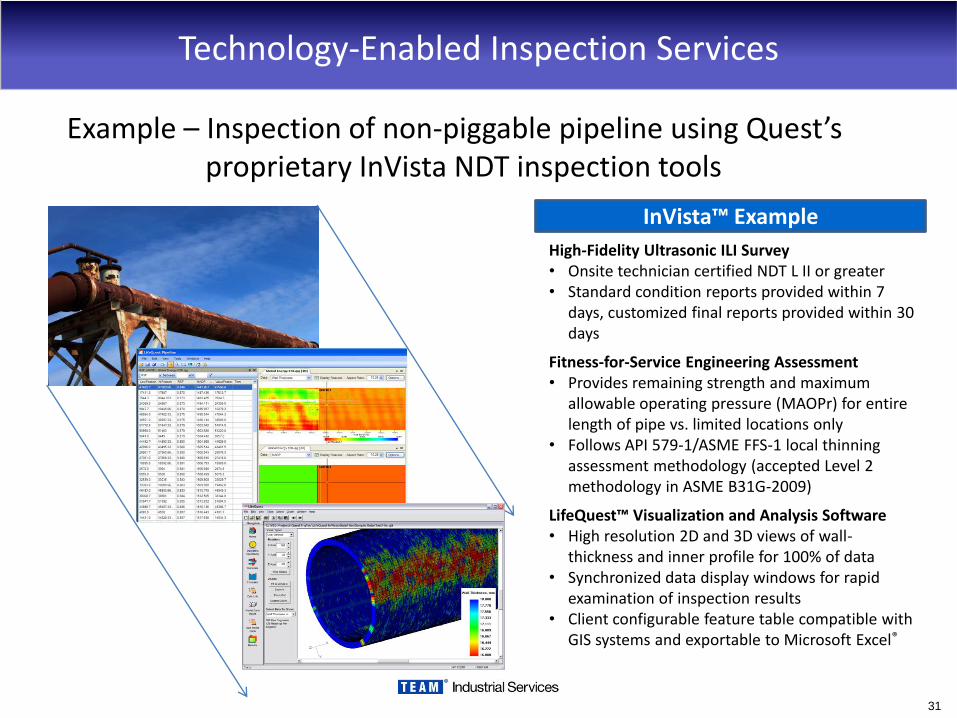

Technology-Enabled Inspection Services

Example – Inspection of non-piggable pipeline using Quest’s proprietary InVista NDT inspection tools

31

High-Fidelity Ultrasonic ILI Survey• Onsite technician certified NDT L II or greater• Standard condition reports provided within 7

days, customized final reports provided within 30 days

Fitness-for-Service Engineering Assessment• Provides remaining strength and maximum

allowable operating pressure (MAOPr) for entire length of pipe vs. limited locations only

• Follows API 579-1/ASME FFS-1 local thinning assessment methodology (accepted Level 2 methodology in ASME B31G-2009)

LifeQuest™ Visualization and Analysis Software• High resolution 2D and 3D views of wall-

thickness and inner profile for 100% of data• Synchronized data display windows for rapid

examination of inspection results• Client configurable feature table compatible with

GIS systems and exportable to Microsoft Excel®

InVista™ Example

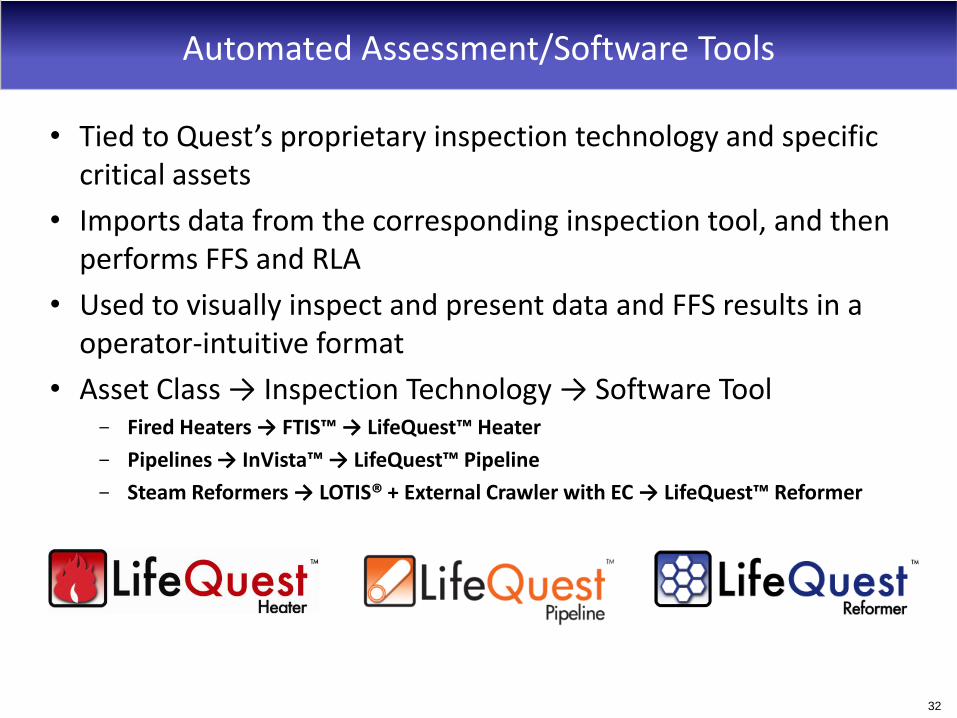

Automated Assessment/Software Tools

• Tied to Quest’s proprietary inspection technology and specific critical assets

• Imports data from the corresponding inspection tool, and then performs FFS and RLA

• Used to visually inspect and present data and FFS results in a operator-intuitive format

• Asset Class → Inspection Technology → Software Tool Fired Heaters → FTIS™ → LifeQuest™ Heater

Pipelines → InVista™ → LifeQuest™ Pipeline

Steam Reformers → LOTIS® + External Crawler with EC → LifeQuest™ Reformer

32

Quest Integrity Group Business Mix

2010YTD Revenue by Office 2010YTD Revenue by Division

USA 49.4%

New Zealand 18.9%

Canada 17.6%

Europe6.1%

Australia 6.0%

M. East 2.1%

Inspection 56.4%

Engineering Assessment

43.6%

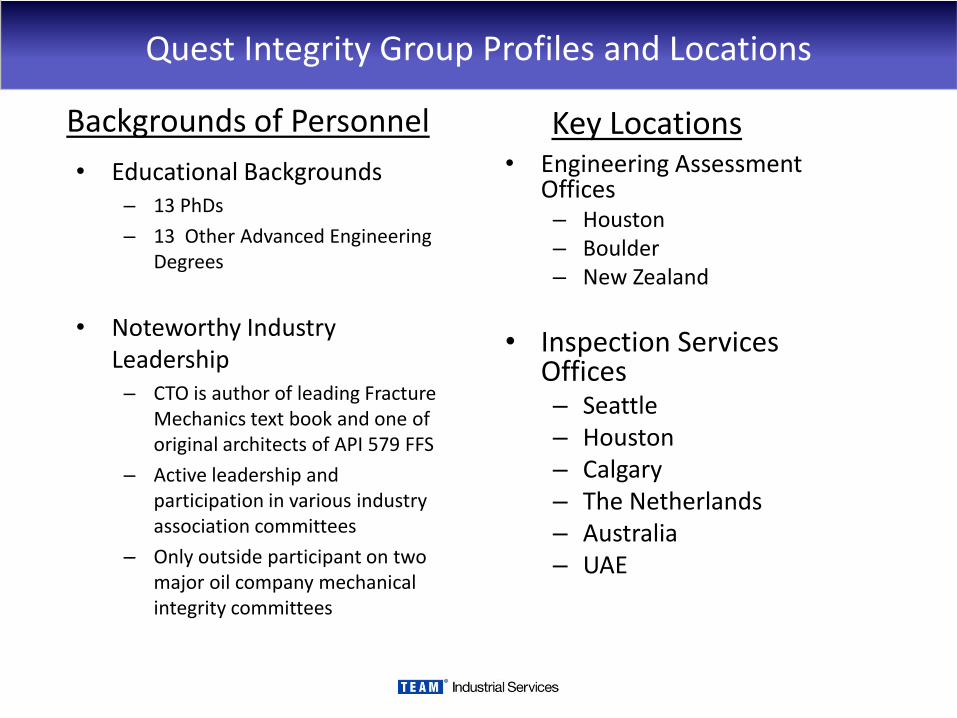

Quest Integrity Group Profiles and Locations

• Engineering Assessment Offices– Houston– Boulder– New Zealand

• Inspection Services Offices– Seattle– Houston– Calgary– The Netherlands– Australia– UAE

Key LocationsBackgrounds of Personnel

• Educational Backgrounds– 13 PhDs

– 13 Other Advanced Engineering Degrees

• Noteworthy Industry Leadership

– CTO is author of leading Fracture Mechanics text book and one of original architects of API 579 FFS

– Active leadership and participation in various industry association committees

– Only outside participant on two major oil company mechanical integrity committees

35

Wrap-Up

• Financial Summary

• FY2011 Guidance

• Our Values

36

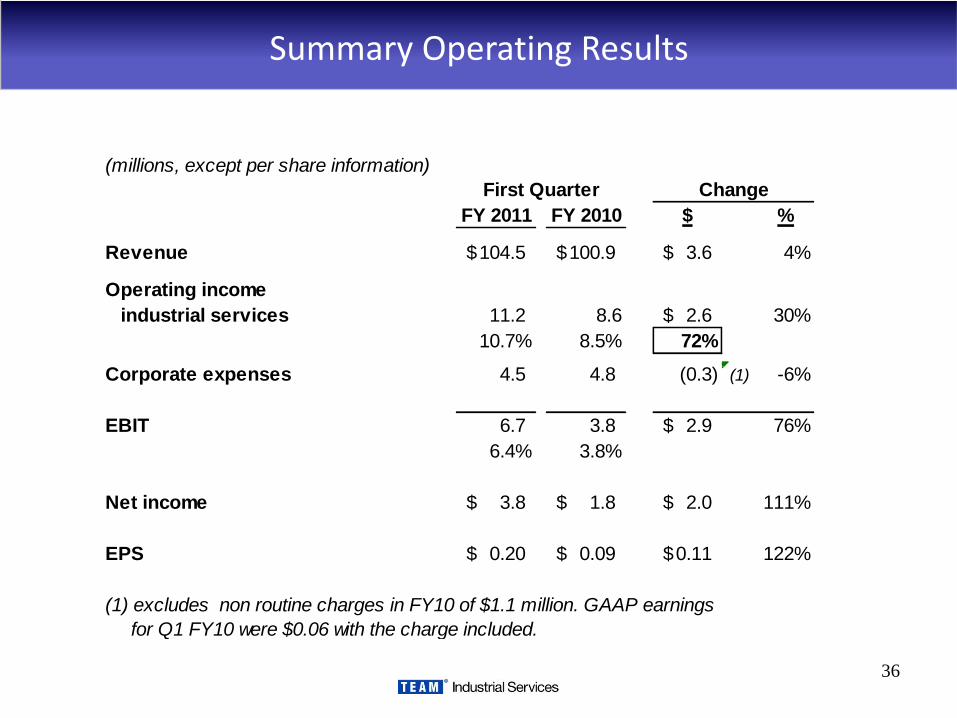

Summary Operating Results

(millions, except per share information)

FY 2011 FY 2010 $ %

Revenue 104.5$ 100.9$ 3.6$ 4%

Operating income

industrial services 11.2 8.6 2.6$ 30%

10.7% 8.5% 72%

Corporate expenses 4.5 4.8 (0.3) (1) -6%

EBIT 6.7 3.8 2.9$ 76%

6.4% 3.8%

Net income 3.8$ 1.8$ 2.0$ 111%

EPS 0.20$ 0.09$ 0.11$ 122%

(1) excludes non routine charges in FY10 of $1.1 million. GAAP earnings

for Q1 FY10 were $0.06 with the charge included.

First Quarter Change

37

Summary of Cash Flows

(in millions) Q1 F11 2010 2009

Net income 3.8$ 12.2$ 22.9$

Depreciation and amortization 3.1 12.5 12.1

Non-cash compensation 1.1 5.0 4.8

Other working capital changes and non cash charges 10.0 14.1 (0.9)

Cash flow from operating activities 18.0$ 43.8$ 38.9$

Capital expenditures and other investments (2.3) (8.0) (14.7)

Free cash flow 15.7 35.8 24.2

Debt repayments and other financing activities (10.1) (33.7) (16.2)

Stock repurchases (1.3)

Foreign exchange rate change effects 0.1 (2.1) (1.9)

Change in cash 4.4$ -$ 6.1$

FYE May 31,

38

Summary Balance Sheets

(in millions) Quest Team May 31,

Team Pro-forma Pro-Forma 2010

Cash 17.1$ 1.2$ 18.3$ 12.6$

Accounts Receivable 93.2 4.0 97.2 109.4

Other current assets 27.4 0.6 28.0 28.3

Tota current assets 137.7 5.8 143.5 150.3 -

Non-current assets 114.1 45.1 159.2 114.7

Total assets 251.8$ 50.9$ 302.7$ 265.0$

Current debt 0.3 0.3 0.3

Other current liabilities 36.5$ 2.4$ 38.9$ 42.8$

Long-Term Debt 38.3 42.6 80.9 47.8

Other 8.5 8.5 8.9 -

Stockholders' equity 168.2 5.9 174.1 165.2

Total liabilities and equity 251.8$ 50.9$ 302.7$ 265.0$

Net debt 21.5$ 41.4$ 62.9$ 35.5$

Net debt to TTM EBITDA (1) 0.4 1.2 0.8

(1) excludes non routine charges

Aug. 31, 2010 unaudited, proforma

39

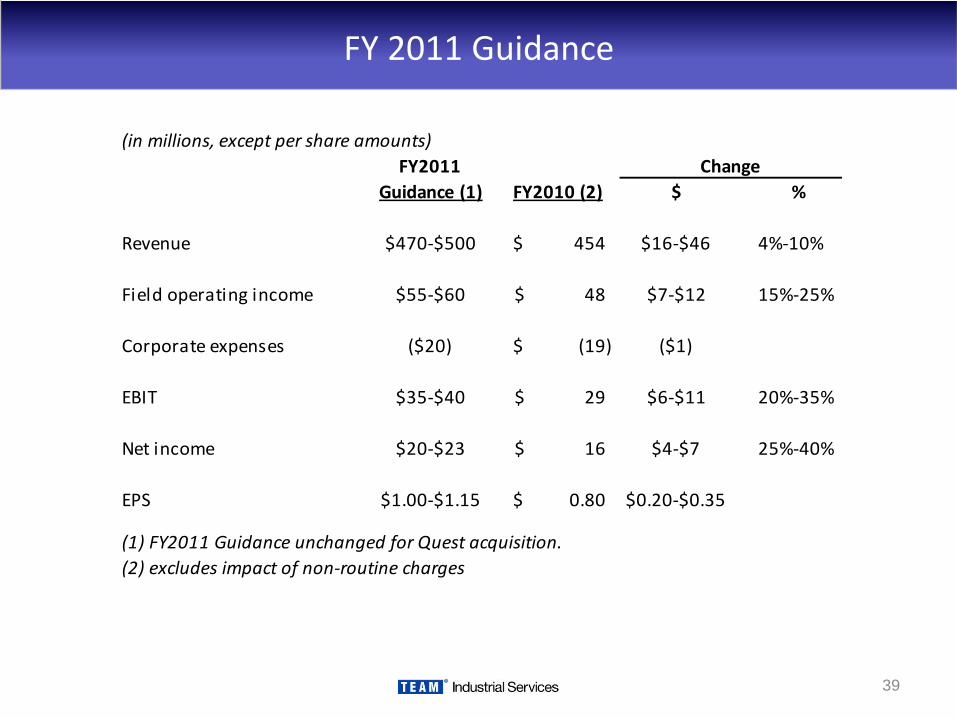

FY 2011 Guidance

(in millions, except per share amounts)

FY2011

Guidance (1) FY2010 (2) $ %

Revenue $470-$500 454$ $16-$46 4%-10%

Field operating income $55-$60 48$ $7-$12 15%-25%

Corporate expenses ($20) (19)$ ($1)

EBIT $35-$40 29$ $6-$11 20%-35%

Net income $20-$23 16$ $4-$7 25%-40%

EPS $1.00-$1.15 0.80$ $0.20-$0.35

(1) FY2011 Guidance unchanged for Quest acquisition.

(2) excludes impact of non-routine charges

Change

40

Maintaining Focus(keys to our success)

• Focus on our Customers – Maintaining a Service Mentality

• A Great Employee Team - Maintaining and Developing the Industry’s Best Organization

• Focus on Execution – More than 130,000+ Service Opportunities. Sweat the Details!

• “Walk the Talk” on Values – Integrity, Respect, and High Expectations

41

Team’s Values

• Safety First in everything we do

• Integrity means doing the right thing

• Service Leadership throughout the company

• Innovation supports continuous growth and improvement

• Pride and Respect for ourselves and our company.

42

Contact Information

Phil Hawk

281-388-5503

Ted Owen

281-388-5525