Embed Size (px)

Citation preview

Business Financial Crime: Issues in Fighting Financial Crime

2

Impact of financial crime

Most recent report on fraud in UK by NERA (National Economic Research Associates) 2002 put the annual cost of financial crime at £14 billion

3

Impact of financial crime

Financial crime is low risk high reward for the criminalFor example armed robbery and drug crime

usually attract greater penalties A £500,000 robbery offender will net 15 yearsFraud of the same value may not result in a

custodial sentence

4

To regulate or control?

When applied to business the term regulation refers to

“use of the law to constrain and organise the activities of business and industry”

(Hutter, 1997)

4

5

To regulate or control? Financial regulation is

Directed at the control of fraud , and At the regulation of standards in the market and

in business and financial services Can be distinguished from social regulation

which incorporates such areas as health and safety, food safety and quality, environmental health, pollution and consumer protection

5

6

To regulate or control? Regulatory approach associated with form of

law and enforcement developed in the 19th and early 20th centuries.

Criminal laws considered necessary to protect the public from dangers they could not protect themselves from

Criminal sanctions were justified as deterrents.

6

7

To regulate or control? Difficulties in proving intent led to

development of strict liability with regulatory offences being considered mala prohibita (wrong as prohibited) rather than mala in se (wrong in itself)

Or not really crime but technical offences This developed into a discretionary

enforcement style where criminal prosecution is used as a last resort

7

8

To regulate or control? A regulatory approach is therefore associated

with a minimal use of criminal sanctions The debate hinges on which regulatory or

criminal law can and should be used to control the activities of business

Involves a range of theoretical and political positions Summarised as conservative, liberal and radical

8

9

To regulate or control? Conservative is based on laissez faire and free

market principles Minimal regulation as market forces provide sufficient

protection

Liberal views accept that regulation is necessary Seeks a balance between regulatory and criminal

sanctions

Radical takes the view that law and regulation are limited by the influence of business interests Therefore criminalisation is necessary

9

10

To regulate or control? Advocates of each, place differing emphasis on

the aims of legislation To regulatory approaches the main aim is to

secure and maintain high standards of business and commerce Enforcement therefore should be a balance between

industry interests and public protection

Crime control approaches emphasise prosecution and punishment To deter or incapacitate offenders To secure justice and show society’s disapproval

10

11

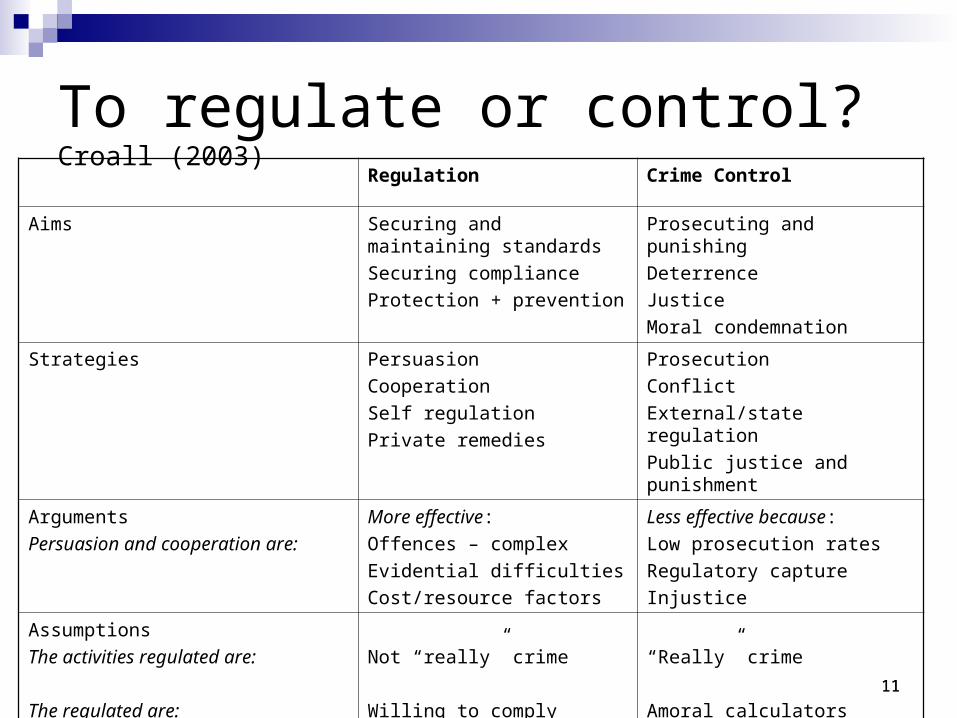

To regulate or control? Croall (2003)

11

Regulation Crime Control

Aims Securing and maintaining standards

Securing compliance

Protection + prevention

Prosecuting and punishing

Deterrence

Justice

Moral condemnation

Strategies Persuasion

Cooperation

Self regulation

Private remedies

Prosecution

Conflict

External/state regulation

Public justice and punishment

Arguments

Persuasion and cooperation are:

More effective:

Offences – complex

Evidential difficulties

Cost/resource factors

Less effective because:

Low prosecution rates

Regulatory capture

Injustice

Assumptions

The activities regulated are:

The regulated are:

Not “really” crime

Willing to comply

“Really” crime

Amoral calculators

12

To regulate or control? Regulation incorporates self regulation Crime control stresses state regulation Regulation includes compensation, negotiation

and out of court settlements Criminal justice deals with “punishment” and

“justice” which is seen to be done.

In practice regulators adopt a range of styles more a continuum

12

13

To regulate or control? Arguments

Persuasive and cooperative strategies are said to promote good relationships based on mutual respect between business and regulators

Critics would say that such styles can lead to sympathy between the parties and “regulatory capture” (ie domination by vested interest who “capture” decision makers)

Approach of compliance rather than crime may undermine the symbolic role of criminal law

Leads to a class of offenders being treated more favourably

13

14

To regulate or control? Arguments

Cooperative approaches assume that the majority of businesses are willing to comply and can be persuaded

Whereas others suggest that businesses are rational “amoral” calculators in the pursuit of profit

14

15

Financial regulation and crime control Incorporates elements of both crime control and

regulatory approaches Many areas of financial regulation have shifted

from self regulation to state regulation Financial Services Act 1986 Creation of Serious Fraud Office in 1988 Creation of Financial Services Authority in 2000

Seen as necessary to encourage investors and to protect them from the risks of a more open market

16

Aims of regulation

Laws covering serious fraud emphasise crime control but also reflect a wider concern with standards

“provide a regulatory framework within which commerce can function” Levi (1987)

Aims of the SFO are defined as “investigate and prosecute serious and complex fraud and maintain confidence in the probity of business and financial services in the UK”

This is similarly reflected in the objectives of the FSA ie “market confidence”

17

Strategies of regulation Agency strategies reflect elements of regulation

and crime control SFO and the police in fraud cases stress

detection and prosecution In general however, most financial crime control

is compliance based with arrest and imprisonment as subordinate For example HM Revenue and Customs rarely

prosecutes and uses out of court settlement and fines The FSA also follows a similar approach

18

Respective merits

The government established the Fraud Trials Committee, an independent committee of inquiry, in 1983.

Chaired by Lord Roskill, it considered the introduction of more effective means of fighting fraud through changes to the law and to criminal proceedings.

It was the impetus for introducing the Criminal Justice Act 1987 and creating the SFO

Known as 'the Roskill Report' published in 1986.

19

Respective merits

Following this, discussions on the regulatory and crime control approaches stress high expertise needed in fraud detection and the evidential difficulties.

Consequent high cost of “risky” prosecutions

Makes regulatory sanctions attractive

20

Respective merits

Contrast situations:Where evidence of serious dishonesty and

high level of public concern for punishment. The nature of the offence requires strong criminal

deterrence

Regulatory action is more appropriate where the offence is seen as technical or in a “grey area”

21

Respective merits Rosalind Wright (ex head of SFO)

underlined the significance of criminal sanctions along with their moral and symbolic dimensions “… can provoke fundamental changes in attitudes and practices amongst businessmen and their advisers”.

Especially so of accountants and solicitors

22

Respective merits Use of regulatory strategies in some areas

has attracted widespread criticism Low rates of prosecution and “scandals”

such as pensions mis-selling This undermines the moral and symbolic

role of law Suggests class bias along with a tolerance

of activities such as lying cheating or stealing

23

Contested moral status of activities

While many forms of fraud are unambiguously criminalOffences involving market regulation are often

regarded as “technical”However, what distinguishes “mis-selling” or

“mis-description” of goods in fraud What degree of deception is criminal?Do regulatory offences not involve morality?

24

Contested moral status of activities

Moral ambiguity gives offenders a justification for resisting regulation

Insider dealing is an example where in court defendants argue “technical” nature and that they are following normal business practice

25

Effective regulation

Regulation is generally agreed to work better where:

There is agreement between regulators and those regulated over the objectives of regulation Where regulated are morally committed to compliance Contentious legislation creates resistance and leads

to unacceptable compliance ie letter and not spirit complied with

26

Effective regulation

A mixture of strategies and sanctions is available and used Range of formal and informal sanctions

Regulators avoid “capture” Pension mis-selling industry persistently denied

wrongdoing

There is a single regulator with power over one industry The US Federal Drugs Agency is regarded as very

effective for this reason

27

Effective regulation

Within corporations, objectives are clearly communicated and structures support compliance If compliance officers or internal audit are

below status of sales department then profits are priority rather than standards

Paying commissions can also be problematic eg insurance mis-selling

“Incentivises lying as well as selling”

28

Does deterrence work?

The deterrent effect of criminal law is assumed to be greater in financial corporate and white collar crime

Potential offenders are assumed to be rational, making decisions by calculating costs of compliance or offending against costs of prosecution and sanction

ie Amoral calculators

29

Sources of consensus

Generally a broad agreement that control of crime in business requires a combination of approaches incorporating instrumental and moral dimensions

Suggests utility of Braithwaite’s Enforcement Pyramid

30

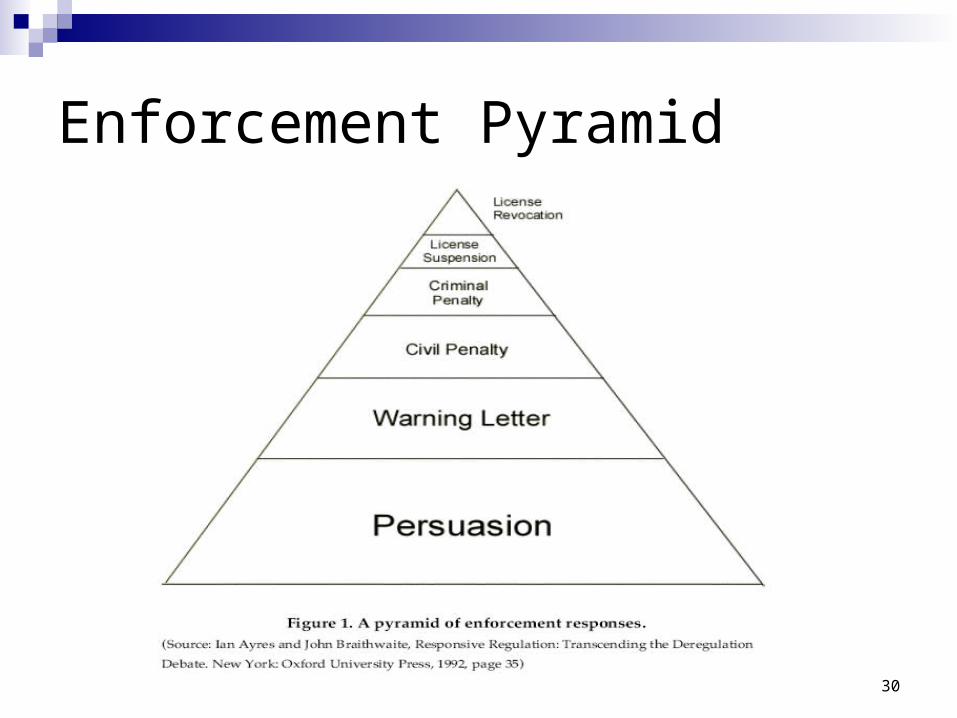

Enforcement Pyramid

31

Enforcement Pyramid Defection from cooperation is likely to be a less attractive

proposition for business when it faces a regulator with an enforcement pyramid than when confronted with a regulator having only one deterrence option.

This is true even where the deterrence option available to the regulator is a powerful, even cataclysmic, one.

It is not uncommon for regulatory agencies to have the power to withdraw or suspend licenses as the only effective power at their disposal.

The problem is that the sanction is such a drastic one that it is politically impossible and morally unacceptable to use it with any but the most extraordinary offences.

32

Different offences different approaches Different levels of complexity and visibility Different kinds of offenders

Those with “respectability” may be more deterred by public exposure

Others by threats to profits Those attracted to the “thrill” are less amenable to

deterrence Amoral offenders

Stress moral unacceptability

33

Different offences different approaches Large corporations present problems as

they may be able to impede the work of external regulators and influence regulatory agendas by exercising influence over the law making process

“regulatory capture”

34

Moral or Amoral Calculators Research has shown high standards of ethics

amongst intending business persons However, moral standards can be subverted within

the corporate environment Managers not “bad people” they can become “amoral

chameleons” (Punch, 1996) As employees they may face dilemmas in prioritising

business interests over professional ethics in situations where they are expected to “find ways around the law”

Business may have differing moral codes and cultures of compliance

35

A range of sanctions?

The arguments suggest effective regulation requires a wide range of strategies and sanctions

Incorporating regulatory and crime control strategies

Takes account of instrumental and moral dimension

Some self regulation effective but must be backed by full range of sanctions which must be used

36

A range of sanctions?

Certainty of detection is a major feature of deterrence

Law is undermined if detection rates are low Suggested (eg Rosalind Wright ex SFO) more

resources for policing of fraud required Need for central fraud agency Lack of public stigma could be addressed by

more publicity Contrast with the developing US approach

37

Current Issues

Financial crime does not figure in government crime objectives

The formation of the Assets recovery Agency and the Proceeds of Crime Act 2002 have started to redress the balance

Creation of the Serious Organised Crime Agency in April 2006 will have a positive impact on reducing financial offences

38

Current Issues

Investigating financial crime has also been impeded by the absence in the UK of a statutory offence of fraud

The Fraud Act 2006 introduced in January 2007

39

Current Issues

The Act repeals all the deception offences in the Theft Acts of 1968 and 1978 and replaces them with a single offence of fraud (Section 1) which can be committed in three different ways by: false representation (Section 2); failure to disclose information when there is a legal

duty to do so (Section 3); abuse of position (Section 4).

40

Current Issues

The Act also creates new offences of possession (Section 6) and making or supplying articles for use in frauds (Section7).

The offence of fraudulent trading (Section 458 of the Companies Act 1985) will apply to sole traders (Section 9).

Obtaining services by deception is replaced by a new offence of obtaining services dishonestly (Section 11).

41

Current Issues

UK Fraud Review recommendationsNational Fraud Reporting Centre Increases in fraud related sentencesFormal system of plea management

Avoiding lengthy trials and resource expenditure

42

Global Approach

Financial Times December 12 2007 “UK First for Price Fixing Charges” There oil industry executives face first ever UK

criminal prosecution for price fixing under a US deal.

Will plead guilty in Texas before travelling to UK to arrested and charged under the 2002 Enterprise Act

Global crackdown on cartels and price fixing

43

References Bowron, M. and Shaw, O. (2007) Fighting Financial

Crime: A UK Perspective, IEA Economic Affairs, March. Croall, H. (2003) Combating Financial Crime: Regulatory

Versus Crime Control Approaches, Journal of Financial Crime, 11(1).

Hutter, B. (1997) Compliance: Regulation and the Environment, Clarendon Press, Oxford.

Nakajima, C. (2007) Issues in Fighting Financial Crime, IEA Economic Affairs, March

Punch, M. (1996) Dirty Business: Exploring Corporate Misconduct, Sage, London.

43