Embed Size (px)

Citation preview

1

Business Accelerators: Evidence from Start-Up Chile1

Juanita Gonzalez-Uribe2 and Michael Leatherbee

3

April 2015

An increasingly important institutional form in the entrepreneurial ecosystem is business

accelerators: fixed-term, cohort-based, financial intermediaries that offer cash, shared office

space, and mentorship to start-ups. We investigate whether they add value by focusing on the

case of Start-Up Chile (SUP), an accelerator sponsored by the Chilean government. This

focus is useful for two reasons. Selection into the programme follows a rules-based approach,

which can be exploited to provide clean causal estimates that deal with potential selection

biases from heterogeneity in growth opportunities across start-ups. In addition, we can

distinguish the effect of mentorship from other accelerator services, because only 20% of

applicants are mentored, and selection process into the mentor arm is also rules-based. We

find that mentoring (bundled with cash) has a causal positive effect on performance, while

basic services apparently not—for borderline applicants. Additional results suggest that

rejected applicants, including borderline ones, are unable to secure financing and that

alternative sources of mentorship are scarce. We thus conclude that SUP adds value to the

entrepreneurial community. These results provide new insights about the selection skills of

accelerators, the causal effect of mentoring on start-up performance, and the value added role

of government-sponsored accelerators.

1We thank Start-up Chile for generous access to the data. We also thanks Ulf Axelson, Taylor Bengley, Shai

Bernstein, Vicente Cunat, Joan Farre-Mensa, Thomas Hellman, Stefan Lewellen, Ramanan Nanda, Daniel

Paravisini, Rui Silva, Moqi Xu, and the seminar participants at the Department of Finance at LSE, the NBER

Entrepreneurship Meeting 2014, the Adam Smith Conference and the UNC Junior Roundtable 2015. Su Wang

provided excellent research assistance. Financial support from Abraaj Group is gratefully acknowledged.

PRELIMINARY VERSION, DO NOT CITE WITHOUT PERMISSION. Corresponding author: Juanita

Gonzalez-Uribe: [email protected]. 2 London School of Economics, [email protected]

3 Pontificia Universidad Católica de Chile, [email protected]

2

Business accelerators have emerged as a new institutional form in the entrepreneurial

ecosystem. From only one in 2005—Y Combinator in Silicon Valley—there are now

potentially thousands worldwide, including Techstars which operates in several cities in the

U.S., and Seedcamp, originally London-based and currently pan-European (e.g., Cohen and

Hochberg, 2014). Accelerators are structured as fixed-term and cohort-based programmes,

which offer cash infusion, shared-office space and business education to participants, often in

the form of mentorship. To date, we know very little about the effectiveness of accelerators in

selecting and adding value, but according to practitioners, mentorship is the biggest source of

the latter.45

Recently, the model of business accelerators has been also adopted by

governments as an attempt to foster entrepreneurship: by 2007 16% of accelerators

worldwide were estimated to be sponsored by public funds (NBIA, 2007). The emergence of

this institutional form in the private and public sector is intriguing, and raises several

questions: do accelerators affect start-up performance, can governments implement them

effectively, and if so, do these programmes add value?

In this paper we explore these questions by focusing on the case of Start-up Chile

(SUP), a business accelerator promoted by the Chilean government since late 2010. The

policy objective of Start-up Chile is to instigate a cultural revolution in Chile towards start-up

creation by temporarily attracting foreign entrepreneurs to Chile. The program offers

participants a cash infusion of U$40,000 (equity free), a one year work visa (i.e., the

programme is open to Chilean and non-Chilean teams), shared office space for six months in

Santiago de Chile, and the option to be selected into the Highway: the mentoring arm of the

programme where participants are given additional access to top mentors.

4 Two recent papers have helped fill this gap: Fehder and Hochberg (2014) and Yu (2015). The first estimates

the effect of business accelerators in regional development and the second, focuses on the case of a privately

sponsored accelerator in the US. 5 See for example this opinion piece (http://avc.com/2011/06/financing-options-contestsprizesaccelerator-

programs/ of Fred Wilson, venture capital partner at Venture Square Ventures in NY and a revered blogger in

the start-up space.

3

Focusing on the case of Start-up Chile is useful because selection into the programme

follows a rules-based approach, which can be exploited to provide clean causal estimates that

deal with potential selection biases from heterogeneity in growth opportunities across start-

ups. In addition, the programme also allows us with the unique opportunity to distinguish the

effect of mentorship from other accelerator services, as only 20% of applicants are mentored,

and selection process into the mentor arm is also rules-based.

In detail, selection into the programme is based on an external ranking of applicants,

and a fixed size of 100 spots per cohort, as ex-ante determined based on the programme’s

budget. Each round, applications are scored and subsequently ranked by external judges using

three criteria: the quality of the founding team, the merits of the project, and the expected

impact of the project on Chile’s entrepreneurial environment. Based on this external ranking,

Chilean government officials then select from the pool of applicants (circa 650 every four

months) the final 100 participants: roughly the first 100 ranking start-ups.6 We estimate the

causal effect of the basic services of the accelerator on start-up performance using a fuzzy

regression discontinuity design (RDD) that compares performance of start-ups that rank

marginally above and marginally below the 100th

company threshold. For these close-call

applicants, selection is akin to an independent random event (it is “locally” exogenous) and

therefore uncorrelated to start-up growth opportunities. Intuitively, the average growth

opportunities of start-ups that rank 97 are similar to those that rank 103. However, this small

difference in rank leads to a discrete change in the probability that the start-up is accelerated:

start-ups ranking below 100th

are 14.5% more likely to participate in the accelerator.

Our estimate captures the effect of the discrete change in the probability of selection

at the 100th

ranked company threshold, and this estimate does not incorporate any observed or

6 Except in generation 2 were the SUP decided before the application round was opened to accept 150

participants.

4

unobserved confounding factors as long as their effects are continuous around the threshold.

We show that indeed, for start-ups that ranked closed to the 100th

company threshold,

selection is uncorrelated with observed start-up and founder characteristics. Hence, by

focusing on these start-ups, we can plausibly estimate a casual effect.

Our analysis exploits hand-collected data at the applicant level for start-ups that

applied to the accelerator during the 2010-2013 period. The accelerator provided us access to

confidential records of the companies that applied to the programme, the evaluation scores

from the panel of judges, and the selection decisions made. Based on these records, we

looked for several sources of information regarding start-up performance. We remark, that

most applicants are missing from standard business data sources as they are seldom legally

incorporated, and if they are, they rarely incorporate in Chile. In addition, the probability that

these early stage start-ups “pivot” is so large, that is challenging to even define, let alone

adequately measure, post-application performance. We overcome this challenge using two

different data collection methodologies: a web survey to all applicants, and extensive web-

searches on the businesses and the teams’ leaders in fund raising sites such as AngeList,

Techcrunch, social media sites like Facebook, Linkedin, and in web-page tracking sites like

Google Insights.

We find little evidence that the basic accelerator services (i.e., cash and desk) offered

by the government-sponsored accelerator have a causal effect on start-up performance.

However, the effect that we identify pertains, by definition, only to participants that have

observations around the discontinuity, which affects the degree to which one can extrapolate

the results of our analysis to others.

We then exploit the rules-based selection process into the mentor arm to estimate the

casual effect of mentoring on performance. In detail, selection into the mentor arm is based

5

on scores from a pitch competition. Two months into the accelerator, participants have the

choice to apply for participation into the Highway through a “pitch-day” during which they

formally present their businesses to judges, both external (i.e., staff at other private

accelerators in Chile such as Telefonica’s Wayra) and internal (i.e. staff at SUP). The judges

independently score the start-ups, and then based on that score the staff at the accelerator

selects roughly 20% of the participants into the mentoring arm. While there is no restriction

on the fixed number of participants accepted to the mentor arm in each round, we show that

probability of acceptance increases by 40% for participants scoring more than 3.6 (over 5).

Using a RDD that compares start-up performance across participants scoring closely above

and below the 3.6 pitch score threshold, we show that mentorship—bundled with the basic

services—casually increases performance.

We then explore whether taken together our findings suggest that government-funded

accelerators add value to the entrepreneurial ecosystem. We present an analytical framework

that shows how one can recover the added-value of basic accelerator services to participants

using our RDD estimates, as long as there is underinvestment in entrepreneurship and

rejected applicants cannot secure alternative sources of financing. These assumptions make

sure that government intervention does not create potential crowding-out of the public sector.

We then explore whether these assumptions appear to be true in practice by investigating in

detail whether rejected applicants, specially borderline applicants, are able to raise financing,

and we find that on average they do not.. We conclude that the selection skills of accelerators

appear to add value, while their treatment effect on performance of closely rejected applicants

apparently does not. We repeat the same analysis for mentoring. Based on reported mentor

scarcity by participants, we argue that our RDD estimates suggest that the accelerator also

adds value through mentorship; both, by selecting good participants into the mentor arm, and

by causally increasing performance of mentored start-ups.

6

Finally, we explore evidence that the programme also affects non-participants, by

analysing business creation inside Santiago de Chile and changes in the perception of Chile

as an entrepreneurial hub. Since the policy objective was to instigate a cultural revolution in

Chile, it would be incomplete to judge the success of the policy based only on the effects to

participants. We find preliminary evidence of higher business incorporation rates after the

creation of the programme in 2010 in neighbourhoods closely located around the

headquarters of Start-up Chile. There are also significant changes in the ranking of Chile as

an entrepreneurial hot-spot in the same period. We conclude that taken together, the results

suggest that Start-up Chile adds value to the entrepreneurial community (participants and

non-participants).

In future versions of the paper we plan to: 1. explore the real effects of acceleration

beyond start-up performance, by focusing on the potential effects on founders, 2. include

results from a detailed survey on applicants regarding their experience in SUP, and their

opinion on the most useful aspects of the programme. Finally, we will also present more

suggestive evidence of the more general impact of SUP on the Chilean entrepreneurial

ecosystem, by comparing registering rates of start-ups in Chile across industries targeted and

not targeted by SUP.

Our paper contributes to the general literature assessing the impact of early stage

financiers on firms (e.g., Hellman and Puri (2000); Sorensen (2007) Kortum and Lerner

(2000); Schoar, Kerr and Lerner (2010)) in two ways. First, we focus on a neglected type of

investor: business accelerators. Second, our methodology allows us to uncover casual

estimates. Our paper also contributes to our understanding on what types of services to start-

ups appear to add more value, especially when imparted by government-sponsored

programmes. Our results point to an important role of mentorship which complements studies

7

in other fields such as subsistence businesses in developed economies (McKenzie and

Woodruff (2008), De Mel et al. (2014)).

Our paper has policy implications, in particular regarding design of policies to

sponsor entrepreneurship. Our results suggest that if the policy objective is to accelerate

participants, then more resources should be allocated towards mentorship, perhaps by

reducing the size of the programme but making sure that all start-ups are mentored. This is

the standard structure of private accelerators which have 30 participants on average, all of

which are mentored. However, the policy objective may not be to accelerate. Indeed, the

founder of Start-up Chile, Nicolas Shea, argued in our interview “...To accelerate was never

the objective. What we wanted was a cultural change in Chile. To reach that goal all you need

is a group of highly qualified entrepreneurs. Making sure they came to Chile was our job,

making sure they succeeded was, and will always be, theirs … ” In that case conclusions may

differ. For example, if the policy objective is to instigate a cultural change, as was the

objective in Start-up Chile, then size may matter, and funding larger programmes, even at the

expense of providing mentorship to participants, may be more effective.

The rest of this paper is as follows. In Section 1 we describe the accelerator programme

and the data provided, and detail the selection process. In Section 2 we explain the analytical

framework and in Section 3 the identification strategy. In Section 3 we also present results,

which we interpret in Section 4. We discuss the effect of the program on the local

entrepreneurial ecosystem in Section 5, and we conclude in Section 6.

8

1. INSTITUTIONAL SETTING: START-UP CHILE

SUP is a government-sponsored program launched in August 2010 to attract early-stage,

high-potential entrepreneurs to bootstrap their ventures in Chile.7 The programme is run by

the Ministry of Economy and is executed by the Chilean Economic Development Agency

(CORFO), the leading organization for promoting innovation and entrepreneurship in the

country. Its main long-term goal is to convert Chile into an innovation and entrepreneurial

hub in Latin America not only by bringing in more entrepreneurs, but also by creating a much

better-developed ecosystem of supporting institutions—including venture capital firms and

angel investors.

SUP offers four main benefits to participants. First, SUP provides selected start-ups

with $40,000 equity-free seed capital. The capital is staged: 50% is delivered at the beginning

of the programme, and the remaining 50%, 3 months after. The second instalment is

conditional on pre-determined performance milestones.8 The staging of capital provides

incentives to entrepreneurs to provide effort, and accountability of participants’ expenditures.

Second, SUP sponsors a temporary one-year work visa for accepted participants in

order to attract foreign entrepreneurs. The programme also helps participants settle in Chile

through a “buddy system”. The buddy-system pairs entrepreneurs with local members of the

Santiago business community based on background interests and language. Local buddies

advice participants on opening Chilean bank accounts, registering with the police, obtaining a

local ID, and securing housing and mobile phones, in addition to checking in with

participants once or twice a month throughout the entrepreneurs’ stay in the country.

7 For more details on SUP see Applegate et al., (2012) and Gonzalez-Uribe (2014).

8 In the inception of the programme, capital disbursements were neither pre-expense nor staged. This system

was implemented in the first semester of 2013.

9

Third, SUP provides free, shared office space in downtown Santiago, equipped with

WiFi, for all start-ups. Workshops on think-tanking and pitch-training based on peer to- peer

teaching are held on-site. Start-ups also have access to SUP’s network of mentors.

Starting in 2012, SUP expanded its programme to include more accelerator-type

activities such as national and international pitch competitions. It created a mentoring arm

within the accelerator known as the Highway, which provides additional resources to

participants including access to the most renowned mentors and frequent monitoring by the

SUP staff. Participants are carefully selected into the Highway after a pitch competition, in

which external and internal judges rank participants. Roughly 20% of participants in each

generation have classified into the Highway since SUP’s fourth generation.

The SUP program, in turn, requires accepted entrepreneurs to stay in Chile for the

six-month duration of the program, and contribute to the building of an entrepreneurial

culture in Chile. During their stay, entrepreneurs have to accumulate 4,000 in “Return Value

Agenda” (RVA) points, a system to measure the social contribution of participants in the

Chilean entrepreneurial ecosystem. Participants have the option to attend, organize or

innovate in social-related activities. Attendance refers to participation in local events, such as

meetings and conferences at which entrepreneurs make themselves available to share

knowledge and to network with locals. Organization can include giving a talk at a school,

presenting a pitch to a local investor, or mentoring a local entrepreneur or student. Innovation

refers to initiatives that actively engage the Chilean business community, such as starting a

new business with a Chilean partner or patenting a product in Chile.

1.1. DATA

We were given access to applicant records for seven generations of SUP. In total we have

information on 3,258 applicants, 616 and 2,642 participants and non-participants,

10

respectively. Panel A of Table 1 displays the number of applications judged per generation

(i.e., not all applications are judged by YouNoodle as some are incomplete), the number of

applications selected (e.g., and offer is extended by the accelerator to the start-up) and the

number of applications that are formalized (e.g., the start-up accepts offer and reallocates to

Chile for the 6 month duration of the programme).9 Panels B through D, and E through G,

describe the composition of the sample by start-up and lead founder characteristics,

respectively. For the empirical analysis, we bundle together all generations. While the

average quality of start-ups on the accelerator is likely to change over time (e.g., as the

accelerator gains recognition better start-ups may apply), we are unable to analyse

generations separately due to power considerations. We address this concern in our empirical

strategy including generation fixed effects throughout.

[INSERT TABLE 1 HERE]

For the 3,258 start-ups that constitute our sample we hand-collect performance measures

using extensive web-searches during the second semester of 2013. Table A1. in the Appendix

has a list of the performance measures and their sources. Table 2 displays the summary

statistics of these web-based performance measures.

[INSERT TABLE 2 HERE]

9 Results from the Global Entrepreneurship Monitor (GEM) report provide a basis for comparison between the

entrepreneurs that apply to SUP, and the average Chilean entrepreneur. According to the latest GEM (2012), the

average Chilean entrepreneur is 37.5 years old, is twice as likely to be male than female, has studies beyond

those that are compulsory, and has a business that serves the consumer sector. The survey on micro

entrepreneurship (EME) also provides a basis of comparison for the composition of Chilean SUP entrepreneurs.

According to the EME of 2012 the average Chilean micro entrepreneur is male (69%), has between 45 and 59

years of age (39%), is responsible for a home (74%), has basic to mid-level education (67%) and its business

belongs to the sectors: retail, restaurant and hotel (34%), agriculture and fishing (24%) and manufacturing

(13%).

11

1.2. SELECTION INTO THE ACCELERATOR

Selection into SUP is a two-part process that takes place every four months. First,

entrepreneurs apply to the programme and their applications are ranked by external judges.

SUP outsources this first part to YouNoodle, a consulting start-up in California, which

provides and objective evaluation of the merit of the start-ups outside the particular context of

the Chilean economy.

Entrepreneurs fill in their applications through an open survey, and then YouNoodle

resorts to Silicon Valley experts (3-4 judges per application) who evaluate applications using

three criteria: the quality of the founding team, the merits of the project, and the impact that it

is likely to have on Chile’s entrepreneurial environment. Using the experts’ judging sheets,

applicants are ranked. No ties are permitted; if companies tie in their judges’ score they are

randomly ranked.

The second part of the selection process is handled by CORFO, which makes the final

decision based on YouNoodle’s ranking. A threshold is pre-specified each round (normally

100), and only companies that rank above the threshold are meant to be selected.10

The

threshold corresponds to the pre-determined size of the program and is decided on by the

government before the application process begins as a function of its budget.

The start-ups cannot precisely manipulate their ranking. Because start-ups do not

know the judges’ scoring rules, and are unlikely to learn about these rules from past SUP

participants, it is improbable that start-ups have room for manipulating their scores around

the 100-th company cut-off. In addition, the judges are unlikely to manipulate the scores, as

no judge evaluates all applications and only observe the very few he/she is asked to score.

10

The threshold has been 100 in every generation, except the second generation where the threshold was set at

150.

12

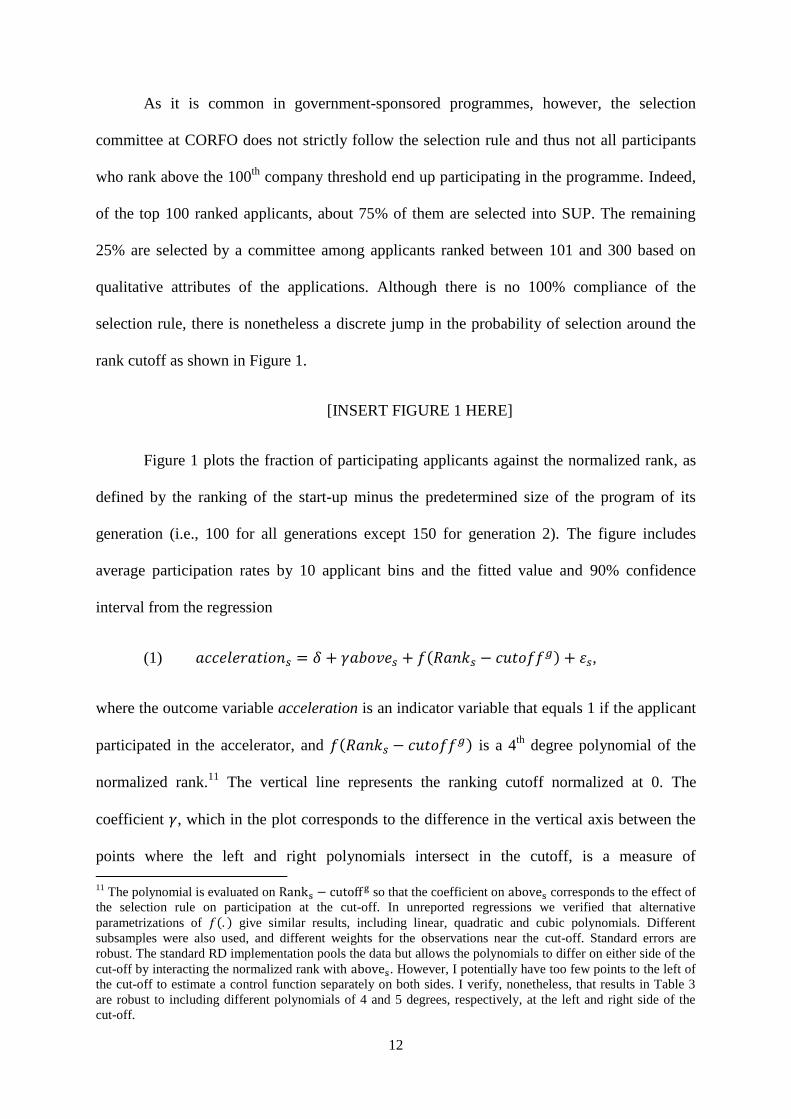

As it is common in government-sponsored programmes, however, the selection

committee at CORFO does not strictly follow the selection rule and thus not all participants

who rank above the 100th

company threshold end up participating in the programme. Indeed,

of the top 100 ranked applicants, about 75% of them are selected into SUP. The remaining

25% are selected by a committee among applicants ranked between 101 and 300 based on

qualitative attributes of the applications. Although there is no 100% compliance of the

selection rule, there is nonetheless a discrete jump in the probability of selection around the

rank cutoff as shown in Figure 1.

[INSERT FIGURE 1 HERE]

Figure 1 plots the fraction of participating applicants against the normalized rank, as

defined by the ranking of the start-up minus the predetermined size of the program of its

generation (i.e., 100 for all generations except 150 for generation 2). The figure includes

average participation rates by 10 applicant bins and the fitted value and 90% confidence

interval from the regression

(1) 𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠 = 𝛿 + 𝛾𝑎𝑏𝑜𝑣𝑒𝑠 + 𝑓(𝑅𝑎𝑛𝑘𝑠 − 𝑐𝑢𝑡𝑜𝑓𝑓𝑔) + 휀𝑠,

where the outcome variable acceleration is an indicator variable that equals 1 if the applicant

participated in the accelerator, and 𝑓(𝑅𝑎𝑛𝑘𝑠 − 𝑐𝑢𝑡𝑜𝑓𝑓𝑔) is a 4th

degree polynomial of the

normalized rank.11

The vertical line represents the ranking cutoff normalized at 0. The

coefficient 𝛾, which in the plot corresponds to the difference in the vertical axis between the

points where the left and right polynomials intersect in the cutoff, is a measure of

11

The polynomial is evaluated on Ranks − cutoff g so that the coefficient on aboves corresponds to the effect of

the selection rule on participation at the cut-off. In unreported regressions we verified that alternative

parametrizations of 𝑓(. ) give similar results, including linear, quadratic and cubic polynomials. Different

subsamples were also used, and different weights for the observations near the cut-off. Standard errors are

robust. The standard RD implementation pools the data but allows the polynomials to differ on either side of the

cut-off by interacting the normalized rank with aboves. However, I potentially have too few points to the left of

the cut-off to estimate a control function separately on both sides. I verify, nonetheless, that results in Table 3

are robust to including different polynomials of 4 and 5 degrees, respectively, at the left and right side of the

cut-off.

13

discontinuity. As per visual inspection, there is a discontinuity in the probability of

participation around the cutoff, which is sizable and significant.

[INSERT TABLE 3 HERE]

Table 3 presents the coefficient on the constant, 𝛿, and the coefficient on 𝑎𝑏𝑜𝑣𝑒𝑠, 𝛾,

using different specifications of equation (1): including generation fixed effects (column (2)),

covariates (column (3)), and restricting the sample to a window of 48 observations around the

cutoff (as calculated using the optimal bandwidth procedure of Calonico et al., 2014) and

differentially weighting observations using a triangular kernel (column (4)). Across all

specifications there is a significant jump in the probability of participation around the 100th

company threshold. The estimate in column (3) implies that ranking above the cutoff

increases probability of acceleration by 19%. The coefficient 𝛾 is significant at the 1% level

and is stable across the first three columns. The estimate in column (4) implies that ranking

above the cutoff increases the probability of acceleration by 30%. The coefficient is much

larger as the observations included only correspond to those in a window of 48 ranks around

the cutoff, which excludes start-ups ranking between 150-160 which were abnormally likely

to participate as can been seen in the plot (i.e., the fit of the polynomial around the

normalized rank of 50 is relatively poor).12

This selection rule based on a “size-of-the-program” cutoff is useful in evaluating the

causal effect of acceleration on start-up performance, because this cutoff dramatically

changes the probability of acceleration but is likely continuously related to performance. For

government-based programs this alternative evaluation method is important as these agencies

are often unwilling to randomize based on ethical considerations. In the next section we

present a simple analytical framework that shows how to recover the value of acceleration by

12

One potential explanation is that judges check start-ups ranking between 150 and 160 as a final check on the

sample. Interviews CORFO officials mentioned that their perceived “checking threshold” was closer to 200.

14

focusing on applicants close to the cutoff. In section 3 we explain in detail how we exploit

this selection rule in practice to identify the causal effect of SUP.

2. ANALYTICAL FRAMEWORK

In this section, we present an analytical framework that shows how to recover the value of

acceleration by focusing on applicants ranking close to the cutoff. We show that a

discontinuity analysis is a simple way to deal with heterogeneity in unobserved growth

opportunities across applicants.

Denote as 𝑟 the ranking of the applicant and 𝑉(𝑟) the added-value of government-

funded accelerator services. For simplicity, we assume throughout that the outcome of the

selection process is binding, that the threshold for selection is 𝑟 ≤ 100, and that the value of

acceleration to the start-up is fixed (i.e. is independent of 𝑟), such that 𝑉(𝑟) = �̅� if 𝑟 ≤ 100

and 0 otherwise. The objective of the empirical analysis is to estimate �̅�, the value of

acceleration, which is not directly observable. Further assume that the underlying growth

opportunities of the applicants can be represented by a function of the ranking 𝑟, 𝐺(𝑟), that is

continuous around the 100th

company threshold. For highly ranked applicants, growth

opportunities are likely very high. Around the threshold, growth opportunities may not be as

high, but most importantly, are comparable across participants in either side of the threshold.

Since 𝐺(𝑟) is a continuous function of 𝑟, but 𝑉(𝑟) is discontinuous at the 100th

company threshold, the performance of the applicant that one observes after acceleration is

also discontinuous at the 100th

company threshold. This implies that the difference in the

performance at the 100th

company threshold, VA, between a start-up that barely ranks above

the 100th

company and one that barely ranks below is exactly the value added of acceleration.

Under the assumptions outlined before, 𝑉𝐴 = (�̅� − 𝐺(𝑟)) − (0 − 𝐺(𝑟)) = �̅�. Therefore, one

15

can recover the value of acceleration form the difference in performance across start-ups that

rank close to the discontinuity. The only two crucial identification assumptions are that the

distribution of start-up characteristics and growth opportunities is similar on both sides of the

discontinuity, and that the probability of selection changes discretely when the company

ranks below 100.

We made a number of additional assumptions in our example, some of which do not

necessarily hold in reality but are not crucial for identification. For example, as explained, the

government committee sometimes decides to accept start-ups that fail to rank below 100.

Hence, in this case one should expect 𝑉(𝑟) to be slightly positive to the right of the threshold

and thus, the average performance to the right of the threshold will be less negative than if the

selection rule were strictly binding. At the same time, start-ups may decide last minute to

reject the offer; thus, 𝑉(𝑟) will be below the effective value of acceleration to the left of the

threshold, and the average performance of start-ups in the left will be less positive than if

selection were binding. Still, provided that 𝐺(𝑟) is continuous and the probability of selection

is discontinuous around the threshold, 𝑉𝐴 can be used as a measure of the value of

acceleration to the start-up. In this case, the value estimated at the discontinuity, 𝑉𝐴, is not

equal to �̅�, as in the previous example. However, as Lee and Lemieux (2010) discuss the

identification strategy is still valid as long as there is a discrete jump in the probability of

selection at the 100th

company threshold (this is the fuzzy regression discontinuity setting).

The estimate recovered is the average effect of acceleration for start-ups ranking close to the

threshold. An important issue, thus, is that the degree to which we can make generalizations

based on our results, will depend on how different are the applicants ranking close to the

threshold from other applicants. We return to this point in the next section when we discuss

the results.

16

Other important questions that arise when trying to infer the value of government-

funded acceleration from differences in performance at the discontinuity are whether we

should expect any effect of acceleration on start-ups that barely rank below or above the

threshold, and whether these differences appropriately evaluate the policy performance. The

issues here are (i) alternative sources of funding for rejected applicants (ii) objective function

of the government-funded accelerator.

On the one hand, if we take at face value the assumption behind government

intervention that there is underinvestment in entrepreneurship, then we can assume that

rejected applicants will most likely not have access to alternative sources of finance. In that

case, differences in performance across start-ups ranking barely below and above the

threshold will reflect the effects of alleviating financial constraints, as well as the potential

value of additional services provided by the accelerators (e.g., knowledge spillovers from

other accelerated projects).

However, no differences may necessarily be detected if the policy objective is not to

fund positive private NPV projects. The government-funded accelerator may pick negative

private NPV projects if their social return is positive, e.g., these investments can spark a

cultural change that will help address future underinvestment in entrepreneurship. Sizable

differences in performance across similar participants in either side of the threshold may thus

constitute only a partial metric of welfare consequences.

Finally, if the assumption of underinvestment in entrepreneurship is not valid and the

objective function of the accelerator is to fund positive NPV projects, then rejected applicants

ranking barely below the cut-off will likely find funding elsewhere (as we have assumed that

start-ups in either side of the threshold have the same distribution of growth opportunities).

Thus, we should expect to see differences in performance across start-ups closely ranking in

17

either side of the cut-off, only if added value from early stage investors is not constant across

investors. Under these assumptions welfare analysis is also nuanced due to potential

crowding-out of private investment by the government funded-accelerator (e.g., Wallsten,

2000). If absent the government-funded accelerator accepted applicants would have been

funded by the private sector, and there is heterogeneity in growth opportunities of start-ups

such that those ranking far above the cut-off are on average better than those below, then

private equity investors are negatively affected by the public programme (i.e., the better start-

ups are funded with public funds). Sizable differences in performance across closely ranked

start-ups in either side of the cut-off, do not necessarily imply then that the public accelerator

is welfare improving.

We come back to this discussion in Section 4 where we focus on interpretation of

results.

3. METHODOLOGY AND IDENTIFICATION STRATEGY

We now describe the empirical approach to measure the causal effect of acceleration on start-

up performance. Suppose start-up 𝑠 applies to the accelerator and is ranked at 𝑟𝑠 relative to all

other start-ups in its generation. We code the indicator for participation in the accelerator as

𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠 =1.

We are interested in the effect of acceleration on the performance of start-up 𝑠,

𝑜𝑢𝑡𝑐𝑜𝑚𝑒𝑠. We can write

(2) 𝑜𝑢𝑡𝑐𝑜𝑚𝑒𝑠 = 𝜋 + 𝛽𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠 + 휀𝑠,

where the coefficient 𝛽 that we are interested in is the effect of acceleration on the

performance measure, for example, survival, and 휀𝑠 represents all other determinants of

performance (𝐸(휀𝑠) = 0). The problem with estimating a regression such as (2) directly is

that acceptance into the accelerator is a highly endogenous outcome, and 𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠 is

18

unlikely to be independent of the error term (𝐸(𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠 , 휀𝑠) ≠ 0), in which case the

estimate of 𝛽 will be biased.

To get a consistent estimate, we would ideally want participation in the accelerator to

be a randomly assigned variable. The regression discontinuity framework that exploits the

ranking by external judges helps us approximate this ideal setup because ranking in an

arbitrarily small interval around the cut-off, is random, however, the probability of

acceptance is dramatically different in either side of the cut-off in that small window.

Intuitively, the idea is to compare the outcome of start-ups that almost participated in the

accelerator as they barely ranked below the cut-off, with those that barely ranked above and

almost didn’t participate. We implement this comparison using a fuzzy RD design (Imbens

and Lenieux, 2007; Roberts and Whited, 2013). In order to conclude that any difference

between start-ups ranking closely in either side of the cut-off is caused by participation in the

accelerator, we assume that these two groups are statistically indistinguishable during the

application stage. In the fuzzy RD setting, this assumption is equivalent to a continuous

distribution of the unobserved residual at the ranking cut-off.

Following Lee and Lemieux (2010), we test whether the data rejects the identification

assumption by inspecting the cross-sectional distribution of predetermined variables at the

cutoff. We remark first that the distribution of applicants is by construction smooth at the

cutoff because the selection mechanism is based on ranking. A visual test as suggested by

McCrary (2008) is not very informative in this case. Moreover, as we argued, the start-ups

are unlikely to precisely manipulate their ranking, because they do not know the judges’

scoring rules, and are unlikely to learn about these rules from past SUP participants. Judges

are also unlikely to manipulate the scores, as no judge evaluates all applications and only

observe the very few he/she is asked to score.

19

We focus instead in testing whether at the time of application there were any

systematic differences in characteristics of start-ups of founders in either side of the cut-off.

In figure 2 we plot the averages for applicant’s characteristics at the time of application

grouped in bins of 10 applicants. Five plots are shown for the variables Age, Chilean (i.e., a

variable that equals one if the applicant leader is Chilean), Gender (i.e., a variable that equals

one if the applicant is a man), Money Raised (i.e., an indicator variable that equals one if the

start-up has raised external finance application), and Prototype (i.e., a variable that equals one

if the project already has a prototype). The plots also show the fitted values form the

applicant level regression of each of these variables on the polynomial 𝑓(. ) and the 𝑎𝑏𝑜𝑣𝑒𝑠

variable. Visual inspection suggests that there are no statistical discontinuities in the cross-

sectional distributions of any of these variables around the cut-off. This result provides

support for the identification assumption.

[INSERT FIGURE 2 HERE]

By substituting equation (1) into the regression model (2) and relabeling coefficients

and the functional form 𝑓(. ), we obtain the fuzzy RD reduced form:

(3) 𝑜𝑢𝑡𝑐𝑜𝑚𝑒𝑠 = 𝛼 + 𝛾 × 𝛽𝑎𝑏𝑜𝑣𝑒𝑠 + 𝑓(𝑅𝑎𝑛𝑘𝑠 − 𝑐𝑢𝑡𝑜𝑓𝑓𝑔) + 휀

As noted by Hahn et al., 2001, in its simplest form, the fuzzy RD setting implements a

Wald estimator for 𝛽. This estimator is equal to the coefficient of 𝑎𝑏𝑜𝑣𝑒𝑠 on regression (3),

𝛾 × 𝛽, divided by the coefficient of 𝑎𝑏𝑜𝑣𝑒𝑠 on regression (1), 𝛾. Thus the fuzzy RD

procedure is akin to a setting where, conditional on 𝑓(𝑅𝑎𝑛𝑘𝑠 − 𝑐𝑢𝑡𝑜𝑓𝑓𝑔), 𝑎𝑏𝑜𝑣𝑒𝑠 is an

instrumental variable for 𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛𝑠. We estimate this regression using a two-stage least

squares (2SLS) procedure where (1) is the first stage and (2) (including an additional term for

the polynomial) is the second stage.13

13

To clarify the excluded instrument is only 𝑎𝑏𝑜𝑣𝑒𝑠, the polynomial on the normalized cut-off is a control in the

second stage.

20

An applicant ranking above the cut-off is more likely to participate in the accelerator,

but applicants are still endogenously chosen by the accelerator, and also endogenously self-

select into accepting an invitation to participate. Our main assumption is that crossing the cut-

off does not affect performance other tan through the change in the probability of

acceleration, and that all applicants ranking below the cut-off that are chosen by the

accelerator, would also be selected if they ranked above the cut-off (monotonicity). Then 𝛽

estimates the causal effect of acceleration on “compliers” of this instrument, that is, those

applicants that end up accelerated because they ranked above the cut-off, and thus the

estimate corresponds to a local average treatment effect (LATE). We remark that 𝛽 is

precisely the estimate of VA from section 2.

3.1. IMPLEMENTATION OF THE FUZZY RD

Implementations of RD inference vary considerably in the literature. Many researchers

control for high-degree polynomials of the underlying continuous forcing variable, where the

shape of the polynomial is often allowed to vary across the threshold, provided there are

enough observations in either side (e.g., Lee and Lemieux 2010). This method borrows

strength from observations far from the cut-off to estimate the average outcome for

observations near it. In practice, cubic or higher order polynomials are used, often based on

statistical information criteria or cross-validation to determine the degree of the polynomial.

Lee and Card (008) suggest a goodness-of-fit test to choose the polynomial degree. The

polynomial function is estimated including a full set of bin dummies. Additional polynomial

terms are added until the null hypothesis that the bin dummies are zero can no longer be

rejected. The drawback in using this first approach is the potential bias introduced by using

observations far from the cut-off.

Others prefer a local analysis, which discards observations above some bandwidth h

away from the cut-off, and estimates low-degree polynomial regressions on the remaining

21

observations (e.g., Gelman and Imbens, 2014). Several methods to choose the bandwidth

exist (e.g., Calonico et al., 2014). The drawback in using this second approach is the loss of

efficiency due to discarding observations. In this paper we do not take a stand on this

methodological discussion. Instead, we present results using both approaches.

3.2. RESULTS: ACCELERATION AND START-UP PERFORMANCE

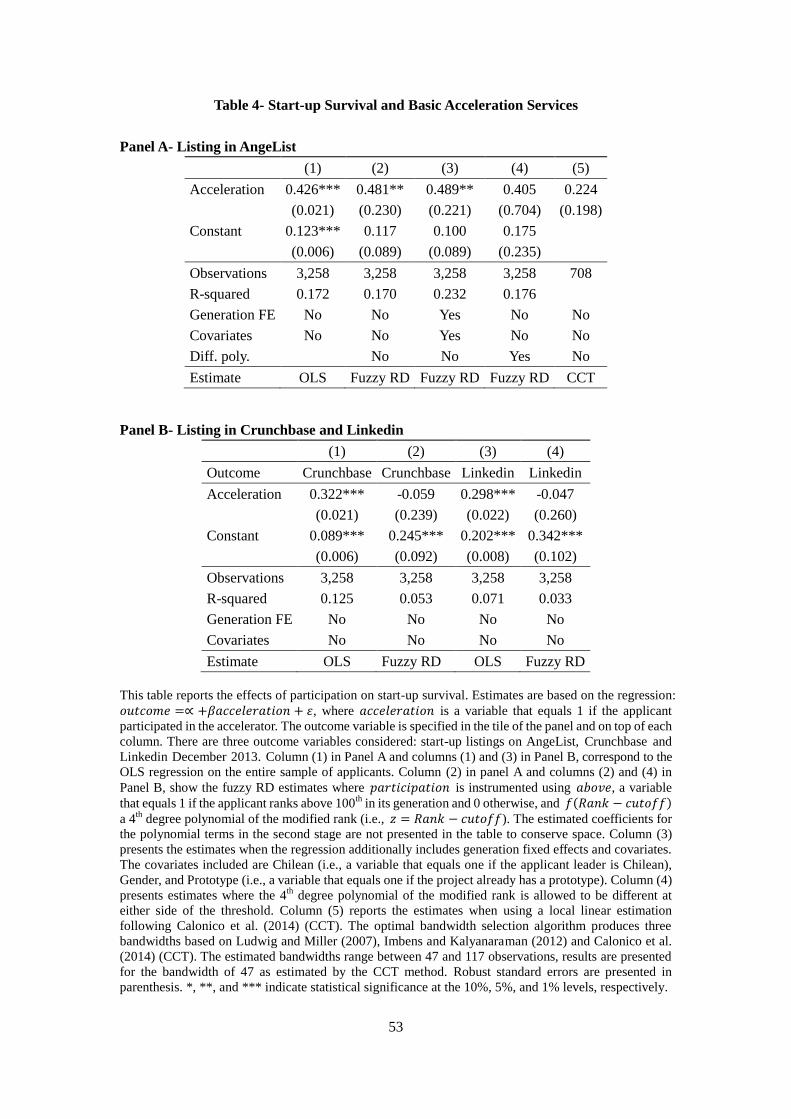

Figure 3 shows the average start-up survival as measured by a listing in AngeList by 2013 in

bins of 10 applicants, and the fitted values of the reduced form regression (3). Visual

inspection reveals a discontinuity in survival: an AngeList listing is more likely for applicants

ranking above the cut-off relative to those ranking below. Given the identification

assumption, the discontinuity in this survival metric is attributed to acceleration.

[INSERT FIGURE 3 HERE]

We formalize the intuition conveyed by the figure with regression tests as

summarized in panel A of Table 4. Reported standard errors are heterosedasticity robust.14

Column (1) reports estimates from a simple OLS estimation of regression (2). The coefficient

is positive and statistically significant at the 1% level: applicants that are accelerated are 43%

more likely to survive.

Column (2) in Table 4 reports results from the fuzzy RD regression (3), the estimates

for the polynomial terms are not included in the table to conserve space. The coefficient

equals 0.49% and is statistically significant at the 1% level. The RD design does not require

conditioning on baseline covariates, but doing so can reduce sampling variability. In Column

(3) we present results after conditioning for selected covariates and generation fixed effects.

Results continue to hold. Column (4) presents estimates allowing the polynomials to differ on

either side of the threshold. The point estimate remains similar but is no longer significant,

likely because we have too few data points to the left of the cut-off to estimate a control

14

In unreported regressions we repeat the analysis clustering standard errors by generation and results continue

to hold. Consistent with potential small cluster bias (there are only 7 generations) we find that standard errors

are most conservative without clustering.

22

function separately on both sides. Finally, column (5) presents estimates using a local linear

regression approach using a bandwidth of 47, which was optimally estimated following the

procedure suggested by Calonico et al., (2014) (CCT). The coefficient remains positive, but

more than halves in magnitude and is no longer significant, likely because 708 observations

do not provide enough statistical power to distinguish an effect of size 0.12 (i.e., a power

estimation indicates that at least 750 observations are needed to distinguish an effect of that

magnitude if the mean is 0.2, the standard deviation 0.4, and the ratio between treated and

control observations is 0.2).

[INSERT TABLE 4 HERE]

We repeat the analysis to check the robustness of the results using other survival

metrics: listing in Crunchbase and listing in Linkedin, two other well-known platforms

recording fundraising activities and employee recruiting, respectively. Panel B in Table 4

shows that results are dramatically different when using these alternative survival measures.

In particular, while the OLS estimates continue to be positive and significant at the 1% level,

the Fuzzy RD estimates are not significant, and the point estimates are very small and

negative. In unreported regressions, we find similar results when using other RD

implementation methods including lower degree polynomials and local linear regressions,

and other web-based performance proxies start-up growth, employment and fundraising.

Results are similar across the different specifications, i.e., OLS estimates are positive and

significant and fuzzy RD estimates are not significant, quantitatively smaller than the OLS

estimates, and often negative.

3.3. INTERPRETATION OF RESULTS

One interpretation of the differences in the RDD results when using performance metrics is

that having a listing in AngeList is not a good measure of performance, in particular because

23

Start-up Chile uses AngeList as a platform of communication with alumni (see: Gonzalez-

Uribe, 2014). Hence, start-ups may be reluctant to close their profiles in AngeList, even in

the case of failure, if they think this will decrease their access to the Start-up Chile’s network.

Results thus suggest that Start-up Chile is successful at establishing a network of participants,

but not at having a positive causal effect on their performance—at least not for closely

rejected participants.

An alternative interpretation is that we don’t have enough power to reject the null

hypothesis. Using a simple power calculation, we estimate that to have a power of 80% in

ruling out an effect of -0.059% (-0.047%) in the probability of having a listing in

Crunchbase (Linkedin), we would need a sample of 3,457 (6,671) observations, assuming a

1/3 proportion of participants to rejected applicants. Because our sample size is 3,258 we may

then not have enough power. If we had a larger sample then we may find a causal effect on

performance, but one that albeit small, is negative. One potential interpretation is that the

accelerator helps entrepreneurs determine faster which ventures will not be successful and

accelerates exit. This alternative interpretation is actually consistent with other work in the

area (see Yu, 2015).

A final interpretation of the findings is that our measures of performance are not

capturing real effects. This should not be such a crucial concern as these web-based metrics

are the metrics used by investors in start-ups, so they are relevant for this type of company.

One natural argument would be that because the program is Chilean perhaps we should focus

on local networks. However, SUP has an international focus. As we have already argued an

important of participants is foreign (see table 2) and the vast majority do not end up in Chile.

The official language in SUP is English and the focus is international: this means that the

relevant networks are likely the foreign ones. Indeed, in one of the interviews the executives

24

mentioned than an internal exit via a local accelerator such as Wayra was considered a

failure. Another idea would be to use data form Chilean registry but this is not feasible: most

projects are registered abroad. However, we explore this alternative interpretation in more

detail by conducting a survey to collect non-web-based measures of performance. An

explanation of the surveys and results are presented next.

3.4. ANALYSIS OF SURVEY-BASED PERFORMANCE MEASURES

Choosing and measuring performance indicators for early stage startups is

challenging. Conventional measures used for established companies—such as profits,

achieving an IPO, or market capitalization—are not quite useful for fledgling organizations

(Delmar & Shane, 2003). For example, profits in early stage companies are highly dependent

on the company’s business model, industry and strategy. Many highly successful and visible

companies purposely postpone organizational profitability for several years, by reinvesting

revenues to fuel growth.

Measures of online activity (LinkedIn, Facebook and AngeList listings) are useful for

exploring entrepreneurial liveliness for companies whose strategies rely on internet exposure.

However, they are not perfect measures of performance. In order to construct a

complementary measure of entrepreneurial performance we conducted a survey aimed at

gathering data on aspects such as employee and revenue growth. These measures are widely

used in the strategy and entrepreneurship literatures (e.g., Eisenhardt & Schoonhoven, 1990;

Baum, Locke and Smith, 2001; Maurer and Ebers, 2006).

In October of 2014 we sent an email invitation to participate in the survey to all

applicants to Start-Up Chile from the first generation through the seventh. A total of 3,798

invitations were sent out, of which 184 bounced due to email addresses that no longer

existed. This is reasonable given that many individuals who applied to the program did so

25

using their startup’s internet domain name, which may cease to exist when the startup no

longer is pursued. We received responses from 448 participants, giving us an effective

response rate of 12.4%. Generation 1 applicants applied to the program in March of 2011 and

those from generation 7 did so in March of 2013. Generation 7 graduated from the program

in January of 2014. Therefore, all the surveyed population of startups had a considerable

amount of time since inception and graduation from Start-Up Chile.

Table 5 shows the distribution of participants that were contacted and those who

responded to the survey. With the exception of generation 7, the proportion of respondents

per generation mirrors the proportion of applicants per generation. This is reasonable given a

greater sense of commitment with Start-Up Chile for those more recently involved in it.

[INSERT TABLE 5 HERE]

One of the challenges of surveying startups is potential selection bias. Not only should

we be interested in the statistics of those startups that are still alive, but also learn about those

that no longer exist. Therefore, we first asked respondents to tell us about the fate of the

startup they applied with to Start-Up Chile. We categorized responses into four groups.

Namely, whether the startup was sold to- or merged with- another company; it was still

operational and the entrepreneur was currently working there; the entrepreneur had pivoted

into a new startup (either based on the same idea or a new idea); or the startup was shutdown.

The specific questions are listed in Table AII in the Appendix.

Table 6 shows the distribution by category for each generation. Of the total sample,

11% of startups exited, 50% are still alive, 30% pivoted and 10% were closed. Consistent

with the liability of senescence, there is a larger proportion of closed startups among the older

generations in our sample. Furthermore, Figure 4 reflects the distribution of the fate of the

startups that applied to the program contingent on their participation. A Kolmogorov-

26

Smirnov test indicates a significant difference in distribution of outcomes (p<0.001), whereas

non-participating applicants changed their business idea (aka pivoted) significantly more than

participants. This might be suggestive of the path-dependent effects that accelerators have on

an entrepreneur’s given business idea.

[INSERT TABLE 6 HERE]

[INSERT FIGURE 4 HERE]

To gauge startup performance, we asked respondents to answer a number of different

measures. That is, the level of implementation of the business idea (from “I have only a

vague idea” to “I have made sales with the idea”), the phase of development of the business

(from “I want to start a business but I have only an idea regarding the product or service” to

“My startup is already profitable”), jobs created, company growth in the last 6 months, pre-

money valuation, market share, how successful the respondent believed others considered

him or her to be as an entrepreneur (from “not at all successful” to “very successful”), the

extent to which the respondent had achieved his or her most important goals for the startup

(from “not at all” to “completely”), the capital raised, the accumulated sales during the last 6

months, the profit achieved in the last six months, and the key entrepreneurial milestones

achieved.

Table 7 shows the average performance responses to each of the aforementioned

questions contingent on participation in Start-Up Chile. Results are shown for the full sample,

regardless of the distance of the applicants to the cutoff score. From this birds-eye view, there

are clear differences in the performance outcomes of both groups. For all performance

measures short of market share, third party perceived success, sales, and profits, Start-Up

Chile participants have significantly higher levels of performance.

27

[INSERT TABLE 7 HERE]

However, there are limitations to this group-level comparison, because both groups

are hardly comparable for the purposes of inferring a performance-enhancing causal effect to

participation in the program. Figure 5 shows the distribution of applicants across the ranking

score for participants and non-participants. As expected, roughly half of non-participants

ranked higher than 375, which is likely to indicate high levels of heterogeneity in the quality

of the compared groups and limit their comparability. However, a relevant proportion of non-

participants ranked below 100. Likewise, a relevant proportion of participants ranked above

100.

[INSERT FIGURE 5 HERE]

We try to take advantage of this overlap, to the extent that participants who are

roughly 150 points away from the cutoff may be comparable to some degree. Evidence from

Leatherbee and del Sol (2015), who study the predictive capacity of the judging process of

Start-Up Chile on the subsequent performance of entrepreneurs, suggests that the ability of

the ranking score to discriminate between higher- and lower-potential startups is surprisingly

limited. Therefore, it may well be the case that—within a reasonably large ranking variable

bandwidth—startups are in fact comparable. In Figure 5 we can see that of all participants

who responded to our survey, the lowest ranked fall within 150 points from the cutoff. Hence

our choice.

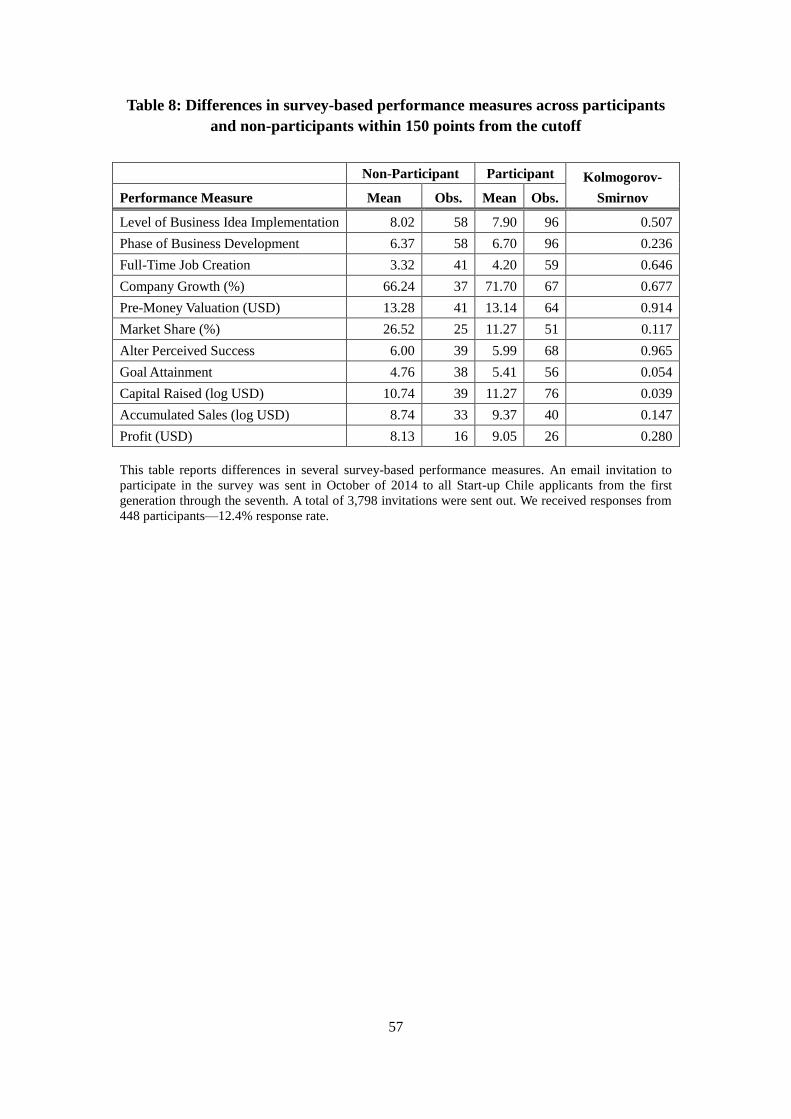

Table 8 shows the average performance measures comparing non-participants and

participants. While participants score higher on most of the measures, they score significantly

higher on the level of key goals achieved, capital raised, sales, and profits (at a lower level of

confidence).

28

[INSERT TABLE 8 HERE]

We conducted the same analysis for a window of 75 points from the cutoff (not reported) and

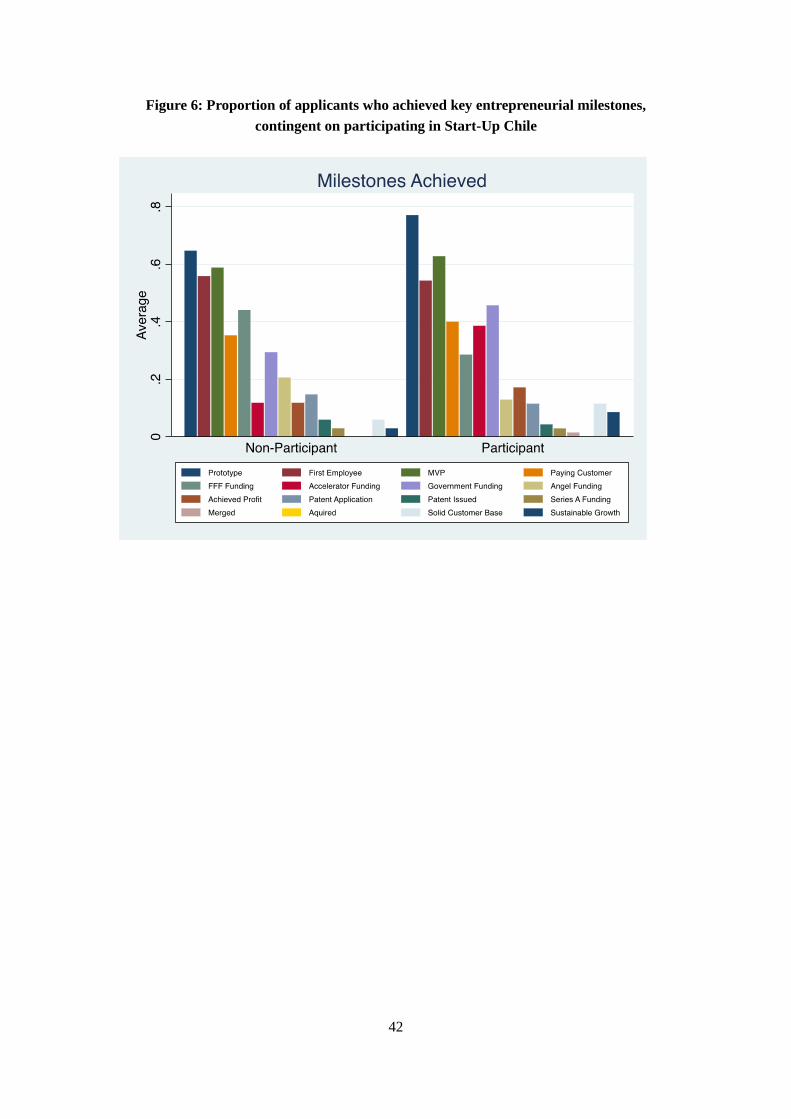

had consistent results. To illustrate, Figure 6 shows the proportion of participants who

achieved key entrepreneurial milestones for non-participants and participants within the 75-

points window. Consistent with what we may expect, a higher proportion of participants

appear to have achieved key milestones vis-à-vis non-participants.

[INSERT FIGURE 6 HERE]

4. CAUSAL EFFECT OF MENTORING ON START-UP PERFORMANCE

We exploit the unique opportunity of assessing the value of mentorship. Provision of this

service varies based on a selection rule that can be exploited to identify the causal effect, and

because mentorship is often an important part—usually not as easily scalable as monetary

resources—of these programmes. Understanding whether it adds value is important for policy

design, and possibly for our understanding of how accelerators affect performance more

generally.

4.1.1. SELECTION INTO THE MENTOR ARM

Participants in SUP have the option to join the Highway, the mentoring arm of the

programme, which provides access to top mentors. Two months into the accelerator the

application process for the mentor arm begins. It consists of a “pitch-day” in which start-ups

do a formal presentation of their businesses to judges, both external (i.e., staff at other private

accelerators in Chile such as Telefonica’s Wayra) and internal (i.e. staff at SUP) and a final

decision by staff at the accelerator in the days following the pitch competition. The judges

independently score the start-ups, and then based on that score the staff at the accelerator

selects roughly 20% of the participants. While in each generation the number of accepted

29

participants into the mentor arm is not strictly capped (in contrast to participation in the

accelerator), an implicit selection rule is evident in the data: there is a discrete jump in the

probability of selection into the mentoring arm of 34% if the start-up scores at least 3.6/5

during the pitch-day. Figure 7 shows the fraction of applicants participating in the pitch-day

that are selected into the mentor arm. Visual inspection reveals this fraction is

discontinuously higher for those participants that scored above 3.6 in the pitch-day. The

figure also shows the ordinary least squares (OLS) fitted values and 90% confidence interval

of the regression

(4) 𝑚𝑒𝑛𝑡𝑜𝑟 = 𝜏 + 𝜇𝐴𝑏𝑜𝑣𝑒3.6 + 𝑔(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) + 휀

where the outcome variable mentor is an indicator variable that equals 1 if the participant was

mentored, 𝐴𝑏𝑜𝑣𝑒3.6 is an indicator variable that equals one if the participant scored above 3.6

during the pitch-day, and 𝑔(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) is a 4th degree polynomial of the pitch-day

score. The polynomial 𝑔(. ) depicted graphically as the smooth line on both sides of the cut-

off controls for any underlying relationship between the fraction of participants that are

mentored and the score of pitch-day. The coefficient 𝜇, which in the plot corresponds to the

difference in the vertical axis between the points where the left and right polynomials

intersect in the cut-off, is a measure of the size of the discontinuity. As per visual inspection,

and as confirmed in the regressions of Table 9, the discontinuity is large—34%—and

significant—1% level.

[INSERT FIGURE 7 HERE]

[INSERT TABLE 9 HERE]

We implement a fuzzy RD design to identify the value added of mentoring by first

confirming that the identification assumption of balanced covariates around the 3.6 score is

30

satisfied. Figure 8 shows that participants in either side of the 3.6 score threshold are

indistinguishable. The only significant difference is for the covariate Money Raised, i.e.,

selected participants into the mentor arm, which scored close to 3.6 in the pitch-day, are

significantly more likely to have secured external financing prior to joining the accelerator.

We deal with this issue by controlling for this covariate in the fuzzy RD regressions.

[INSERT FIGURE 8 HERE]

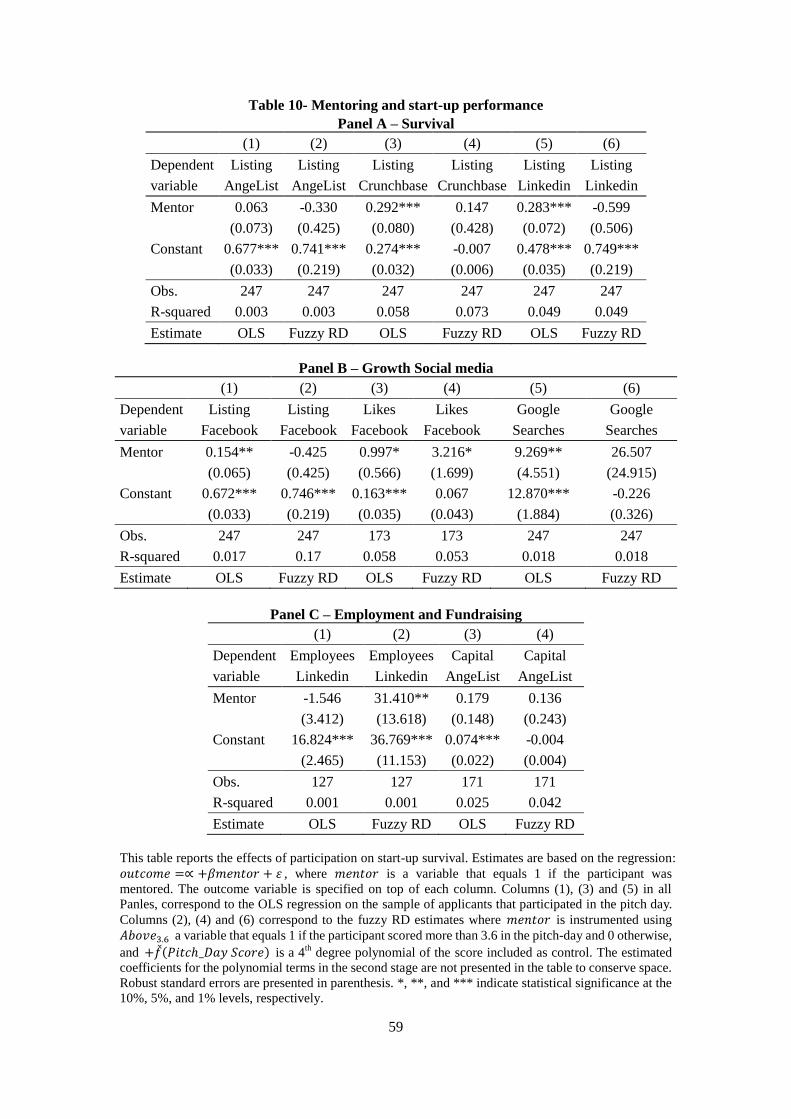

Table 10 documents differences in performance across start-ups in and out the mentor

arm using the OLS and the fuzzy RD approach based on the 3.6 score cut-off of the pitch-

day. The results in the table provide evidence, albeit weak, that mentoring has a positive

causal impact of start-up performance. There are no significant differences in survival as

measured by having a listing in AngeList, which is expected, as both, participants that are

mentored and those that are not, are encouraged to list their companies in AngeList by the

accelerator. However, there is evidence of impact on growth as measured by number of

Facebook likes and employment as measured by company size in Linkedin.

[INSERT TABLE 10 HERE]

One interpretation of these additional findings is that there is heterogeneity in impact

across services offered by the accelerator. While basic services such as cash infusion and

shared office space appear not to add value, mentoring appears to contribute more to start-up

growth.

5. DOES START-UP CHILE ADD VALUE TO THE ENTREPRENEURIAL

COMMUNITY?

We now explore whether taken together our findings suggest that government-funded

accelerators add value to the entrepreneurial ecosystem. In Section 3 we presented an

31

analytical framework that shows how one can recover the added-value of basic accelerator

services to participants using our RDD estimates, as long as there is underinvestment in

entrepreneurship and rejected applicants cannot secure alternative sources of financing. These

assumptions make sure that government intervention does not create potential crowding-out

of the public sector. We now explore whether these assumptions appear to be true in practice

by investigating in detail whether rejected applicants, specially borderline applicants, are able

to raise financing, and we find that on average they do not. We conclude that the selection

skills of accelerators appear to add value, while their treatment effect on performance of

closely rejected applicants apparently does not. We repeat the same analysis for mentoring.

Based on reported mentor scarcity by participants, we argue that our RDD estimates suggest

that the accelerator also adds value through mentorship; both, by selecting good participants

into the mentor arm, and by causally increasing performance of mentored start-ups.

5.1. FOUNDER AS THE UNIT OF ANALYSIS

Perhaps the correct unit of analysis should instead be the entrepreneur (founder) and not the

firm. Start-ups pivot a lot and failing is part of growing. What matters most is that

entrepreneur learns, tries again and is likely more to succeed after he is schooled in the

accelerator. The main challenge here is measuring outcomes at individual level. We

overcome this challenge by collecting information at the founder level from LinkedIn. In

future work we will summarize the results from analysis at the founder level.

5.2. REGIONAL EFFECTS

The policy objective was not to help accelerated start-ups. In fact, the founder of the

programme Nicolas Shea argued that the objective was to attract talent (not to be retained)

but instead to inspire Chileans to become entrepreneurs and start an internal mentality

revolution.

32

We explore evidence that the programme also affects non-participants, by analysing

business creation inside Santiago de Chile and changes in the perception of Chile as an

entrepreneurial hub. Since the policy objective was to instigate a cultural revolution in Chile,

it would be incomplete to judge the success of the policy based only on the effects to

participants. We find preliminary evidence of higher business incorporation rates after the

creation of the programme in 2010 in neighbourhoods closely located around the

headquarters of Start-up Chile. There are also significant changes in the ranking of Chile as

an entrepreneurial hot-spot in the same period. We conclude that taken together, the results

suggest that Start-up Chile adds value to the entrepreneurial community (participants and

non-participants). These results are consistent with Fehder and Hochberg (2014), who find

that there are subsequent local developments after accelerator programs. In future versions of

the paper we will summarize these additional results.

5.3. GOOD AT SELECTION

The differences in performance calculated using the OLS methodology indicate that the

accelerator is good at selecting. We explore this point further by investigating the correlation

between success and subsequent start-up performance. In future versions we will summarize

results from this analysis.

6. CONCLUSIONS

In this paper we provide new evidence performance of government sponsored programmes

that sponsor entrepreneurship. We focus on business accelerates a neglected yet increasingly

popular type of early stage financiers both in the public and the private sectors. We quantify

the causal impact of a government-funded accelerator in Chile, SUP, by simultaneously

exploiting novel, rich micro-data and addressing concerns about unobserved heterogeneity.

We find that mentoring (bundled with cash) has a causal positive effect on performance,

33

while basic services apparently not—for borderline applicants. Additional results suggest that

rejected applicants, including borderline ones, are unable to secure financing and that

alternative sources of mentorship are scarce. We thus conclude that SUP adds value to the

entrepreneurial community. These results provide new insights about the selection skills of

accelerators, the causal effect of mentoring on start-up performance, and the value added role

of government-sponsored accelerators.

34

References

Applegate, Lynda, William Kerr, Joshua Lerner, Dina D. Pomeranz, Gustavo herrero and

Cintra Scott. Start-up Chile. Harvard Business Review.

Baum, J.R., Locke, E.A., Smith, K.G., 2001. A Multidimensional Model of Venture Growth.

Acad. Manag. J.44, 292–303. doi:10.2307/3069456

Cohen, Susan and Yael Hochberg, 2014, Accelerating Startups: The Seed Accelerator

Phenomenon, available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2418000

Delmar F, Shane SA. 2003. Does business planning facilitate the development of new

ventures? Strategic Management Journal 24(April): 1165–1185.

Eisenhardt, K.M., Schoonhoven, C.B., 1990. Organizational Growth: Linking Founding

Team, Strategy, Environment, and Growth Among U.S. Semiconductor Ventures, 1978-1988.

Adm. Sci. Q. 35, 504–529.

Fehder, Daniel and Yael Hochberg, 2014, Accelerators and the Regional Supply of Venture

Capital Investment, available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2518668

Gonzalez-Uribe, Juanita, 2014, El caso de Start-up Chile. Programa de atracción de talento

para fomentar el emprendimiento, CAF, Development Bank of Latin America.

http://scioteca.caf.com/handle/123456789/685#sthash.3uyjaDPp.dpuf

Hahn, J., Todd, P., Van Der Klaauw, W., 2001. Identification and estimation of treatment

effects with a regression discontinuity design. Econometrica 69, 201–209

Hellmann, Thomas and Manju Puri, 2002, Venture Capital and the professionalization of

Start-Up Firms: Empirical Evidence, The Journal of Finance, pp. 169-198.

Kerr, William, Joshua Lerner and Antoinette Schoar, 2014, The Consequences of

Entrepreneurial Finance: Evidence from Angel Financings, Review of Financial Studies,

27(1) pp. 20-55.

Kortum, Samuel and Joshua Lerner, 2000, Assessing the Contribution of Venture Capital to

Innovation, RAND Journal of Economics 31(4), 674-692.

Lelarge, Claire, David Sraer and David Thesmar, 2013, Entrepreneurship and Credit

Constraints: Evidence from a French Loan Guarantee Program in NBER volume on

"International Differences in Entrepreneurship" edited by Joshua Lerner and Antoinette

Schoar, University of Chicago Press.

Maurer, I., Ebers, M., 2006. Dynamics of Social Capital and Their Performance Implications:

Lessons from Biotechnology Start-ups. Adm. Sci. Q. 51, 262–292. doi:10.2189/asqu.51.2.262

Lee, David and Thomas Lemieux, 2010. Regression Discontinuity Designs in

Economics, Journal of Economic Literature, vol. 48(2), pages 281-355, June.

35

Van Der Klaauw, W., 2002. Estimating the effect of financial aid offers on college

enrollment: a regression-discontinuity approach. International Economic Review 43, 1249–

1287.

Van Der Klaauw, W., 2008. Regression-Discontinuity Analysis: A Survey of Recent

Developments in Economics, Labour: Review of Labour Economics and Industrial Relations,

Vol. 22 (2), 2008, p.219-245.

36

Figure 1 – Fraction of accelerated applicants

The figure shows the average fraction of accelerated applicants in bins of 10 transformed ranks (i.e., 𝑧)

and the fitted values and 90% confidence interval from the regression mode: 𝑎𝑐𝑐𝑒𝑙𝑒𝑟𝑎𝑡𝑖𝑜𝑛 = 𝛿 +

𝛾𝑎𝑏𝑜𝑣𝑒 + 𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) + 휀, where the outcome variable acceleration is an indicator variable

that equals 1 if the applicant participated in the accelerator, and 𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) is a 4th

degree

polynomial of the transformed rank. The vertical line represents the ranking cutoff normalized at 0 for

the modified ranking.

0.2

.4.6

.8

-100 0 100 200z=Rank-cutoff

37

Figure 2 – Cross-sectional Covariates

The figure shows that predetermined variables are continuous at the cutoff for applicants. Five plots are

shown for the variables Age, Chilean (i.e., a variable that equals one if the applicant leader is Chilean),

Gender, Money Raised (pre application), and Prototype (i.e., a variable that equals one if the project

already has a prototype). All variables as of the application date. Plots show averages grouped in bins of

10 applicants. The plots also show the fitted values and 90% confidence interval of a modified versions

of the regression in equation (1), 𝑜𝑢𝑡𝑐𝑜𝑚𝑒 = 𝛼 + 𝛽𝑎𝑏𝑜𝑣𝑒 + 𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) + 휀, with each of

these variables as outcomes, on 𝑎𝑏𝑜𝑣𝑒, a variable that equals 1 if the applicant ranks above 100th in its

generation and 0 otherwise, and 𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) a 4th

degree polynomial of the modified rank (i.e.,

𝑧 = 𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓). The vertical line represents the ranking cutoff normalized at 0 for the modified

ranking.

28

30

32

34

36

-100 0 100 200z=Rank-cutoff

Age

.1.1

5.2

.25

.3.3

5

-100 0 100 200z=Rank-cutoff

Chilean

.2.3

.4.5

.6

-100 0 100 200z=Rank-cutoff

Gender

.15

.2.2

5.3

.35

.4

-100 0 100 200z=Rank-cutoff

Money_Raised.3

.4.5

.6.7

-100 0 100 200z=Rank-cutoff

Prototype

38

Figure 3 – Effect of participation in accelerator on listing in AngeList

The figure examines the effect of participation in the accelerator on having a listing in AngeList for all

applicants irrespective of whether they participated or not (i.e., the reduced form estimates). The plot

shows the average value of AngeList (i.e., a variable that equals 1 if the project has a listing on AngeList

by December 2013) in bins of 10 applicants. The plots also show the fitted values and 90% confidence

interval of a modified version of the regression in equation (1), 𝑜𝑢𝑡𝑐𝑜𝑚𝑒 = 𝛼 + 𝛽𝑎𝑏𝑜𝑣𝑒 + 𝑓(𝑅𝑎𝑛𝑘 −

𝑐𝑢𝑡𝑜𝑓𝑓) + 휀, with AngeList as outcome, on 𝑎𝑏𝑜𝑣𝑒, a variable that equals 1 if the applicant ranks above

100th

in its generation and 0 otherwise, and𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) a 4th

degree polynomial of the modified

rank (i.e., 𝑧 = 𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓). The vertical line represents the ranking cutoff normalized at 0 for the

modified ranking.

.1.2

.3.4

.5

-100 0 100 200z=Rank-cutoff

39

Figure 4 – Effect of participation in accelerator on alternative measures of performance

The figure examines the effect of participation in the accelerator on performance as measured by having

a listing in Crunchbase for all applicants irrespective of whether they participated or not (i.e., the reduced

form estimates). The plot shows the average value of Crunchbase (i.e., a variable that equals 1 if the

project has a listing on Crunchbase by December 2013) in bins of 10 applicants. The plots also show the

fitted values and 90% confidence interval of a modified version of the regression in equation (1),

𝑜𝑢𝑡𝑐𝑜𝑚𝑒 = 𝛼 + 𝛽𝑎𝑏𝑜𝑣𝑒 + 𝑓(𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓) + 휀 , with Crunchbase as outcome, on 𝑎𝑏𝑜𝑣𝑒 , a

variable that equals 1 if the applicant ranks above 100th in its generation and 0 otherwise, and𝑓(𝑅𝑎𝑛𝑘 −

𝑐𝑢𝑡𝑜𝑓𝑓) a 4th

degree polynomial of the modified rank (i.e., 𝑧 = 𝑅𝑎𝑛𝑘 − 𝑐𝑢𝑡𝑜𝑓𝑓). The vertical line

represents the ranking cutoff normalized at 0 for the modified ranking.

0.1

.2.3

.4

-100 0 100 200z=Rank-cutoff

40

Figure 4: Distribution of startup outcome among applicants

Kolmogorov-Smirnov exact test p< 0.001

41

Figure 5: Histogram of applicants across the ranking score contingent on

participation in Start-Up Chile

42

Figure 6: Proportion of applicants who achieved key entrepreneurial milestones,

contingent on participating in Start-Up Chile

43

Figure 7 – Fraction of mentored applicants

The figure shows the average fraction of mentored participants in bins of 0.2 scores by judges’

pitch-day scores, and the fitted values and 90% confidence interval from the regression: 𝑚𝑒𝑛𝑡𝑜𝑟 =

𝜏 + 𝜇𝐴𝑏𝑜𝑣𝑒3.6 + 𝑓(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) + 휀 , where the outcome variable mentor is an indicator

variable that equals 1 if the participant was mentored, 𝐴𝑏𝑜𝑣𝑒3.6 is an indicator variable that equals

one if the participant scored above 3.6 during the pitch-day, and 𝑓(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) is a 4th

degree

polynomial of the pitch-day score. The vertical line represents the implicit score cut-off of 3.6.

01

02

03

04

0

Num

ber

of p

art

icip

atio

ns in

0.2

score

bin

s

0.5

11

.5

0 1 2 3 4 5Pitch-Day Score

44

Figure 8- Cross-sectional covariates mentor arm

The figure shows that predetermined variables are continuous at the cutoff for applicants. Five plots are

shown for the variables Age, Chilean (i.e., a variable that equals one if the applicant leader is Chilean),

Gender, Money Raised (pre application), and Prototype (i.e., a variable that equals one if the project

already has a prototype). All variables as of the application date. Plots show averages grouped in bins of

10 applicants. The plots also show the fitted values and 90% confidence interval of a modified versions

of the regression in equation (1), 𝑚𝑒𝑛𝑡𝑜𝑟 = 𝜎 + 𝜔𝐴𝑏𝑜𝑣𝑒3.6 + 𝑓(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) + 𝜖, with each of

these variables as outcomes, , 𝐴𝑏𝑜𝑣𝑒3.6 is an indicator variable that equals one if the participant scored

above 3.6 during the pitch-day, and 𝑓(𝑃𝑖𝑡𝑐ℎ_𝐷𝑎𝑦 𝑆𝑐𝑜𝑟𝑒) is a 4th

degree polynomial of the pitch-day

score. The vertical line represents the implicit score cut-off of 3.6.

20

30

40

50

0 1 2 3 4 5Pitch-Day Score

Age

0.2

.4.6

.81

0 1 2 3 4 5Pitch-Day Score

Chilean

0.5

1

0 1 2 3 4 5Pitch-Day Score