Embed Size (px)

Citation preview

SEQ 0001 JOB B09-001-006 PAGE-0003 COVER REVISED 28MAY96 AT 11:25 BY LR DEPTH: 66.04 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-001

3

Bulletin No. 1996–8February 27, 1996

HIGHLIGHTSOF THIS ISSUE

These synopses are intended only as aids to the reader inidentifying the subject matter covered. They may not berelied upon as authoritative interpretations.

INCOME TAX

PS–7–89, page 24.Proposed regulations under section 1254 of the Coderelating to the treatment of gain from the disposition ofinterest in certain natural resource recapture propertyby S corporations and their shareholders.

T.D. 8645, page 4.Final regulations under section 469 of the Codeproviding rules for rental real estate activities oftaxpayers engaged in certain real property trades orbusinesses.

T.D. 8646, page 10.Final regulations under section 861 of the Codeprovides guidance concerning the allocation and appor-tionment of research and experimental expenditures forpurposes of determining taxable income from sourcesinside and outside the U.S.

EMPLOYEE PLANS

Notice 96–11, page 19.Guidelines are set forth for determining for February1996, the weighted average interest rate and theresulting permissible range of interest rates used tocalculate current liability for purposes of the full fundinglimitation of section 412(c)(7) of the Code as amendedby the Omnibus Budget Reconciliation Act of 1987 andby the Uruguay Round Agreements Act (GATT).

EXEMPT ORGANIZATIONS

Announcement 96–10, page 30.A list is provided of organizations that no longer qualifyas organizations to which contributions are deductibleunder section 170 of the Code.

EXCISE TAXES

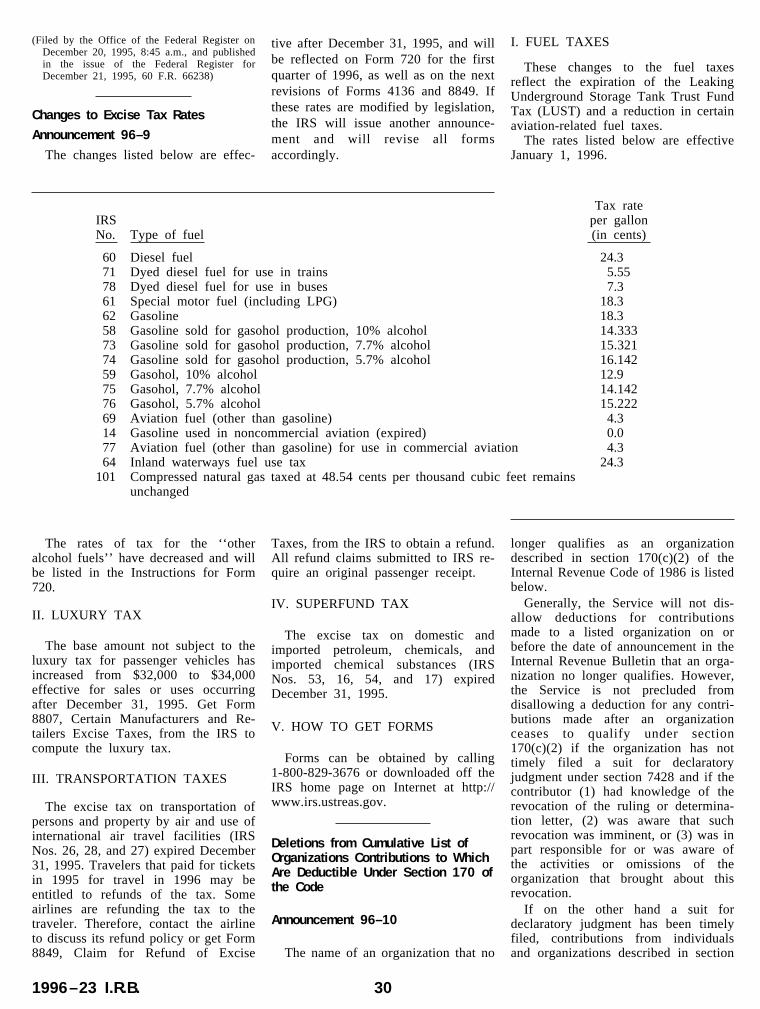

Announcement 96–9, page 30.Effective after December 31, 1995, the rates for fueltaxes and the base amount not subject to the luxury taxhave changed. Also, excise taxes on transportation andon the superfund expired December 31, 1995.

ADMINISTRATIVE

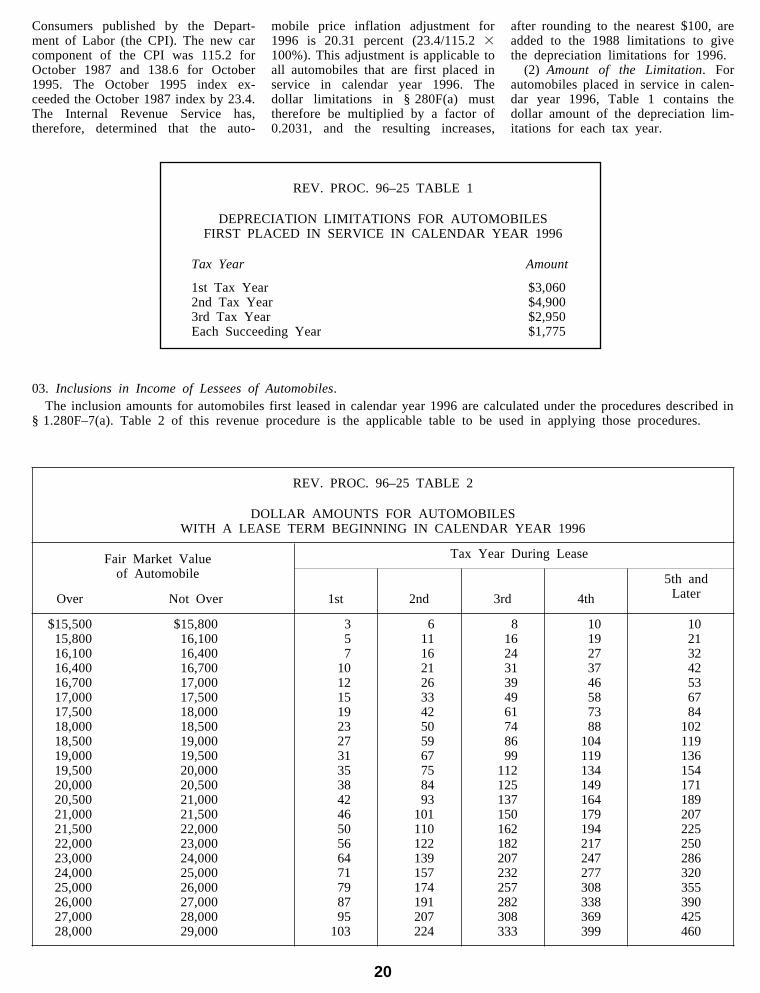

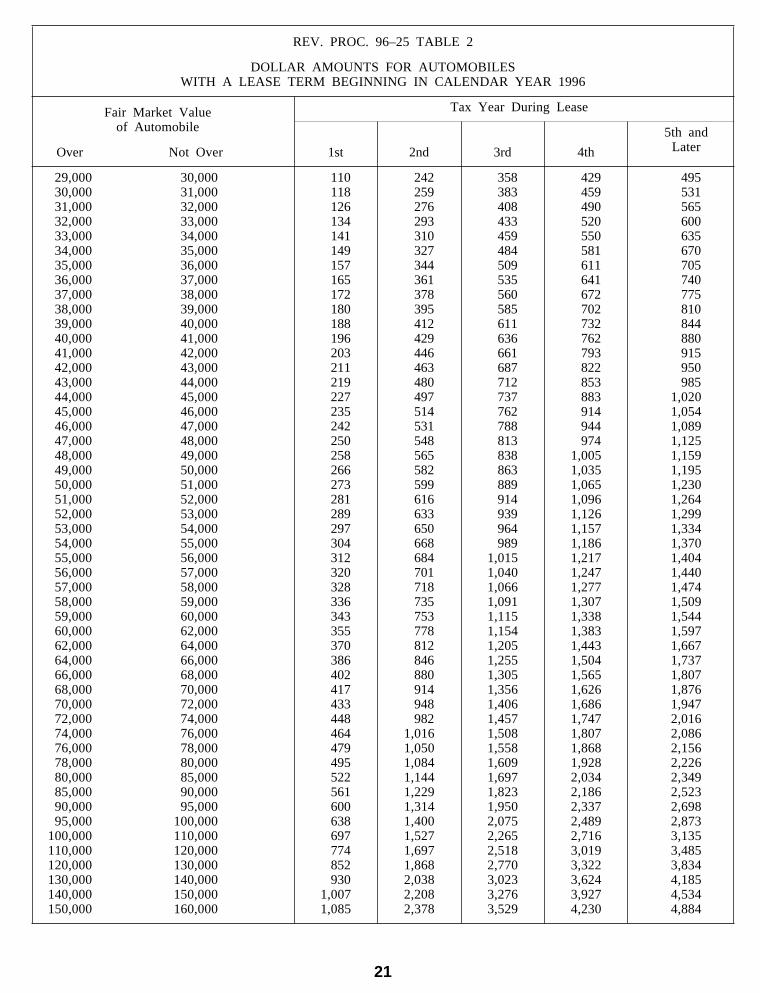

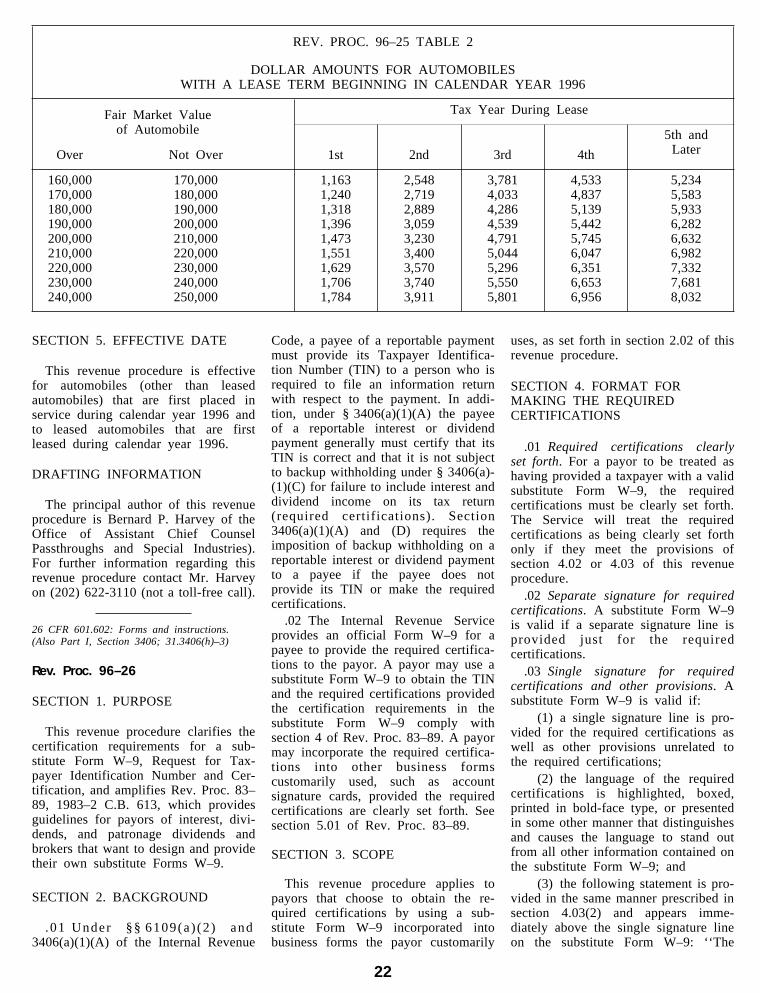

Rev. Proc. 96–25, page 19.Automobile owners and lessees. This procedure providesowners and lessees of passenger automobiles withtables detailing the limitations on depreciation deduc-tions for automobiles first placed in service duringcalendar year 1996 and the amounts to be included inincome for automobiles first leased during calendaryear 1996.

Rev. Proc. 96–26, page 22.Backup withholding; substitute Form W–9. The require-ments for payors that want to use a substitute Form W–9, Request for Taxpayer Identification Number andCertification, are clarified.

Finding Lists begin on page 00.Announcement of Disbarments and Suspensions begin on page 00.Announcement of Declaratory Judgment Proceeding Under Section 7428 on page 00.

SEQ 0002 JOB B09-002-002 PAGE-0002 MISSION REVISED 28MAY96 AT 11:25 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-002

2

Mission of the ServiceThe purpose of the Internal Revenue Service is tocollect the proper amount of tax revenue at the leastcost; serve the public by continually improving the

quality of our products and services; and perform in amanner warranting the highest degree of publicconfidence in our integrity, efficiency and fairness.

Statement of Principlesof Internal RevenueTax AdministrationThe function of the Internal Revenue Service is toadminister the Internal Revenue Code. Tax policyfor raising revenue is determined by Congress.

With this in mind, it is the duty of the Service tocarry out that policy by correctly applying the lawsenacted by Congress; to determine the reasonablemeaning of various Code provisions in light of theCongressional purpose in enacting them; and toperform this work in a fair and impartial manner,with neither a government nor a taxpayer point ofview.

At the heart of administration is interpretation of theCode. It is the responsibility of each person in theService, charged with the duty of interpreting thelaw, to try to find the true meaning of the statutoryprovision and not to adopt a strained construction inthe belief that he or she is ‘‘protecting the revenue.’’The revenue is properly protected only when we as-certain and apply the true meaning of the statute.

The Service also has the responsibility of applyingand administering the law in a reasonable,practical manner. Issues should only be raised byexamining officers when they have merit, neverarbitrarily or for trading purposes. At the sametime, the examining officer should never hesitateto raise a meritorious issue. It is also importantthat care be exercised not to raise an issue or toask a court to adopt a position inconsistent withan established Service position.

Administration should be both reasonable andvigorous. It should be conducted with as littledelay as possible and with great courtesy andconsiderateness. It should never try to overreach,and should be reasonable within the bounds of lawand sound administration. It should, however, bevigorous in requiring compliance with law and itshould be relentless in its attack on unreal taxdevices and fraud.

SEQ 0003 JOB B09-002-002 PAGE-0003 MISSION REVISED 28MAY96 AT 11:25 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-002

3

IntroductionThe Internal Revenue Bulletin is the authoritativeinstrument of the Commissioner of Internal Revenue forannouncing official rulings and procedures of theInternal Revenue Service and for publishing TreasuryDecisions, Executive Orders, Tax Conventions, legisla-tion, court decisions, and other items of generalinterest. It is published weekly and may be obtainedfrom the Superintendent of Documents on a subscrip-tion basis. Bulletin contents of a permanent nature areconsolidated semiannually into Cumulative Bulletins,which are sold on a single-copy basis.

It is the policy of the Service to publish in the Bulletinall substantive rulings necessary to promote a uniformapplication of the tax laws, including all rulings thatsupersede, revoke, modify, or amend any of thosepreviously published in the Bulletin. All publishedrulings apply retroactively unless otherwise indicated.Procedures relating solely to matters of internalmanagement are not published; however, statements ofinternal practices and procedures that affect the rightsand duties of taxpayers are published.

Revenue rulings represent the conclusions of theService on the application of the law to the pivotal factsstated in the revenue ruling. In those based onpositions taken in rulings to taxpayers or technicaladvice to Service field offices, identifying details andinformation of a confidential nature are deleted toprevent unwarranted invasions of privacy and to complywith statutory requirements.

Rulings and procedures reported in the Bulletin do nothave the force and effect of Treasury DepartmentRegulations, but they may be used as precedents.Unpublished rulings will not be relied on, used, or citedas precedents by Service personnel in the disposition ofother cases. In applying published rulings and proce-dures, the effect of subsequent legislation, regulations,court decisions, rulings, and procedures must beconsidered, and Service personnel and others con-cerned are cautioned against reaching the sameconclusions in other cases unless the facts andcircumstances are substantially the same.

The Bulletin is divided into four parts as follows:

Part I.—1986 Code.This part includes rulings and decisions based onprovisions of the Internal Revenue Code of 1986.

Part II.—Treaties and Tax Legislation.This part is divided into two subparts as follows:Subpart A, Tax Conventions, and Subpart B, Legislationand Related Committee Reports.

Part III.—Administrative, Procedural, and Miscellanous.To the extent practicable, pertinent cross references tothese subjects are contained in the other Parts andSubparts. Also included in this part are Bank SecrecyAct Administrative Rulings. Bank Secrecy Act Admin-istrative Rulings are issued by the Department of theTreasury’s Office of the Assistant Secretary(Enforcement).

Part IV.—Items of General Interest.With the exception of the Notice of Proposed Rulemak-ing and the disbarment and suspension list included inthis part, none of these announcements are consoli-dated in the Cumulative Bulletins.

The first Bulletin for each month includes an index forthe matters published during the preceding month.These monthly indexes are cumulated on a quarterlyand semiannual basis, and are published in the firstBulletin of the succeeding quarterly and semi-annualperiod, respectively.

The Bulletin Index-Digest System, a research andreference service supplementing the Bulletin, may beobtained from the Superintendent of Documents on asubscription basis. It consists of four Services: ServiceNo. 1, Income Tax; Service No. 2, Estate and GiftTaxes; Service No. 3, Employment Taxes; Service No.4, Excise Taxes. Each Service consists of a basicvolume and a cumulative supplement that provides (1)finding lists of items published in the Bulletin, (2)digests of revenue rulings, revenue procedures, andother published items, and (3) indexes of Public Laws,Treasury Decisions, and Tax Conventions.

The contents of this publication are not copyrighted and may be reprinted freely. A citation of the Internal Revenue Bulletin as the source would be appropriate.

For sale by the Superintendent of Documents U.S. Government Printing Office, Washington, D.C. 20402.

SEQ 0004 JOB B09-003-004 PAGE-0004 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

4

Part I. Rulings and Decisions Under the Internal Revenue Code of 1986

Section 280F.—Limitation onDepreciation for Luxury Automobiles;Limitation where Certain PropertyUsed for Personal Purposes

26 CFR 280F–5T: Leased Property(temporary).

This procedure provides owners and lessees ofpassenger automobiles with tables detailing thelimitations on depreciation deductions for auto-mobiles first placed in service during calendaryear 1996 and the amounts to be included in in-come for automobiles first leased during calendaryear 1996. See Rev. Proc. 96–25, page 19.

26 CFR 280F–7: Property leased after December31, 1986.

This procedure provides owners and lessees ofpassenger automobiles with tables detailing thelimitations on depreciation deductions for auto-mobiles first placed in service during calendaryear 1996 and the amounts to be included in in-come for automobiles first leased during calendaryear 1996. See Rev. Proc. 96–25, page 19.

Section 469.—Passive ActivityLosses and Credits Limited

26 CFR 1.469–4: Definition of activity.

T.D. 8645

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Rules for Certain Rental Real EstateActivities

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document containsfinal regulations providing rules forrental real estate activities of taxpayersengaged in certain real property tradesor businesses. The regulations reflectchanges to the law made by the Omni-bus Budget Reconciliation Act of 1993,and affect taxpayers subject to thelimitations on passive activity lossesand passive activity credits.

DATES: These regulations are effectiveon January 1, 1995. See §1.469–11 forapplicability.

ADDRESSES: Send submissions to:CC:DOM:CORP:T:R (TD 8645), Room

5228, Internal Revenue Service, POB7604, Ben Franklin Station, Wash-ington, DC 20044. In the alternative,submissions may be hand deliveredbetween the hours of 8:00 a.m. and5:00 p.m. to: CC:DOM:CORP:T:R (TD8645), Courier’s Desk, Internal Reve-nue Service, 1111 Constitution AvenueNW, Washington, DC.

FOR FURTHER INFORMATIONCONTACT: William M. Kostak at(202) 622-3080 (not a toll-freenumber).

SUPPLEMENTARY INFORMATION:

Paperwork Reduction Act

The collection of information con-tained in these final regulations hasbeen reviewed and approved by theOffice of Management and Budget inaccordance with the Paperwork Reduc-tion Act (44 U.S.C. 3504(h)) undercontrol number 1545–AS38. The esti-mated annual burden per respondentvaries from 0.10 hours to 0.25 hours,depending on individual circumstances,with an estimated average of 0.15hours.

Comments concerning the accuracyof this burden estimate and suggestionsfor reducing this burden should be sentto the Internal Revenue Service, Attn:IRS Reports Clearance Officer, IT:FP,Washington, DC 20224, and to theOffice of Management and Budget,Attn: Desk Officer for the Departmentof the Treasury, Office of Informationand Regulatory Affairs, Washington,DC 20503.

Background

This document amends 26 CFR part1 to provide rules relating to thetreatment of rental real estate activitiesof certain taxpayers under the passiveactivity loss and credit limitations ofsection 469. Section 469 disallowslosses from passive activities to theextent they exceed income from pas-sive activities and similarly disallowscredits from passive activities to theextent they exceed tax liability alloca-ble to passive activities. In general,passive activities are activities in whichthe taxpayer does not materially partici-pate. In addition, until the enactment of

the Omnibus Budget Reconciliation Actof 1993 (OBRA 1993), all rentalactivities (including those in which ataxpayer materially participated) werepassive.

OBRA 1993 added section 469(c)(7),which provides that rental real estateactivities of qualifying taxpayers arenot subject to the rule that treats allrental activities as passive. Thus, arental real estate activity of a qualify-ing taxpayer is not passive if thetaxpayer materially participates in theactivity. Further, section 469(c)(7)provides that each of a qualifyingtaxpayer’s interests in rental real estateis treated as a separate activity unlessthe taxpayer elects to treat all interestsin rental real estate as a single activity.

On January 10, 1995, the IRS pub-lished in the Federal Register a noticeof proposed rulemaking (60 FR 2557[PS–80–93, 1995–1 C.B. 1015]) toprovide guidance regarding section469(c)(7). A number of public com-ments were received concerning theproposed regulations, and a publichearing was held on May 11, 1995.After consideration of the commentsreceived, the proposed regulations areadopted as revised by this Treasurydecision.

Explanation of provisions

I. General Background

The proposed regulations providerules for determining whether a tax-payer qualifies for treatment undersection 469(c)(7). The proposed regula-tions also provide rules for determiningthe rental real estate activities ofqualifying taxpayers for purposes ofsection 469. Except for modificationsin response to comments received onthe proposed regulations, the finalregulations generally adopt the rulescontained in the proposed regulations.

II. Public Comments

Several comments requested that theService reconsider the rule in theproposed regulations prohibitingqualifying taxpayers from groupingrental real estate activities with otheractivities in determining whether thetaxpayers materially participate in therental real estate activities. After care-

SEQ 0005 JOB B09-003-004 PAGE-0005 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

5

ful consideration, the final regulationsadopt the rule in the proposed regula-tions because that position is consistentwith the statutory language and thelegislative history.

Several comments suggested that therule in the proposed regulations pro-hibiting the grouping of rental realestate activities with other activities bemodified to allow qualifying taxpayersto group the activities of developmentor construction of rental real estatewith rental real estate activities. Thefinal regulations do not adopt thismodification because in most casesdevelopment and construction activitiesare separate and distinct from rentalactivities. In addition, this modificationwould introduce significant administra-tive difficulties in determining whichdevelopment activities or constructionactivities qualify. However, the IRSand Treasury Department invite com-ments concerning whether the materialparticipation tests in §1.469–5T(a)should be amended to include a look-back material participation test fortaxpayers significantly involved in thedevelopment or construction of theirrental real estate interests.

Several comments requested clar-ification regarding whether a qualifyingtaxpayer’s participation in a manage-ment activity may count towards mate-rial participation in a rental real estateactivity if the management activityincludes the management of rental realestate owned by the taxpayer. The finalregulations clarify that a qualifyingtaxpayer may participate in a rental realestate activity through participation in amanagement activity. In determiningwhether the taxpayer materially partici-pates in the rental real estate activity,however, work the taxpayer performsin the management activity is takeninto account only to the extent it isperformed in managing the taxpayer’sown rental real estate. The final regula-tions also clarify that a qualifyingtaxpayer who owns rental real estatethrough an entity, including a C corpo-ration that is subject to section 469,may count work performed by the tax-payer in managing the rental real estateof the entity in establishing materialparticipation in the taxpayer’s rentalreal estate activities. Thus, if a qualify-ing taxpayer owns some interests inrental real estate through a closely heldC corporation and makes the electionto treat all interests in rental real estateas a single activity, the aggregate rentalreal estate activity will include those

interests held through the closely heldC corporation for purposes of materialparticipation.

One comment requested that theregulations modify the definition oftrade or business to clarify that ataxpayer’s real property trades or busi-nesses are determined without regard tothe taxpayer’s grouping of activitiesunder §1.469–4. The final regulationsclarify that a taxpayer’s grouping ofactivities under §1.469–4 does notcontrol the determination of the tax-payer’s real property trades or busi-nesses for purposes of this section.

Several comments requested that theregulations provide a detailed definitionof real property trades or businessesbeyond the cross-reference to section469(c)(7)(C). However, to avoid com-plex and mechanical rules, the finalregulations do not adopt a detaileddefinition of real property trades orbusinesses. Instead, the regulationsprovide that taxpayers may use anyreasonable method for determiningtheir real property trades or businesses.

Several comments requested that thefinal regulations modify the rule in theproposed regulations providing thatonly employees who are five-percentowners of their employer at all timesduring the taxable year may treatpersonal services performed as anemployee as services performed in areal property trade or business. Thecomments suggested that the regula-tions should take into account personalservices performed by employees thatare five-percent owners for a signifi-cant portion of a taxable year. Inresponse to these comments, the finalregulations are modified to provide thatan employee may count services per-formed in a real property trade orbusiness during the portion of thetaxable year that the employee is afive-percent owner in the employer.

Several comments requested clar-ification concerning whether a qualify-ing taxpayer that makes an election totreat all interests in rental real estate asa single activity will be treated ashaving a single rental real estateactivity for purposes of the formerpassive activity rule under section469(f). In addition, comments requestedthat the regulations be modified toprovide that qualifying taxpayers thatmake the aggregation election will betreated as having separate activities forpurposes of the disposition rules undersection 469(g) and §1.469–4(g). In re-

sponse to these comments, the finalregulations clarify that a qualifyingtaxpayer that makes the election totreat all interests in rental real estate asa single rental real estate activity willbe treated as having a single activityfor all purposes of section 469, includ-ing sections 469(f) and (g). The statu-tory language and the legislative his-tory do not support a rule allowing aqualifying taxpayer to treat all interestsin rental real estate as a single activityfor purposes of material participationand section 469(f), but as separateactivities for purposes of section469(g).

In addition, in response to comments,the final regulations provide an exam-ple illustrating the operation of theformer passive activity rule for qualify-ing taxpayers that make the election totreat all interests in rental real estate asa single activity. This example illus-trates that qualifying taxpayers thatmake the aggregation election may usecurrent net income from the aggregaterental real estate activity to offset theprior-year disallowed passive losses ofthe aggregate rental real estate activity,regardless of which rental real estateinterests within that activity producedthe income or prior-year losses.

Some comments requested that theregulations permit qualifying taxpayersto make or revoke the aggregationelection on an amended income taxreturn. After careful consideration ofthis issue, the final regulations adoptthe rule in the proposed regulations thataggregation elections must be made orrevoked on an original return. The finalregulations provide, however, that theelection may be revoked in any year inwhich the facts are materially changedfrom those in the taxable year forwhich the election was made.

In addition, one comment requestedclarification as to what constitutes amaterial change in the facts and cir-cumstances that would allow a taxpayerto revoke an aggregation election.However, the final regulations do notprovide an example or bright-line rulefor determining when a material changein the facts and circumstances hasoccurred, because this determination isintended to be a broad factual inquiry.Providing an example or bright-linerule may inappropriately restrict thescope of that inquiry.

One comment requested the modi-fication of the rule in the proposed

SEQ 0006 JOB B09-003-004 PAGE-0006 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

6

regulations that the aggregation electionhas no effect in years the taxpayer isnot a qualifying taxpayer. Instead, thecomment suggested that, for ease ofadministration and compliance, the ag-gregation election should be bindingand irrevocable for all future years,including years in which the taxpayeris not a qualifying taxpayer. However,the final regulations adopt the rule inthe proposed regulations because theposition advocated by the commentwould be unfavorable to many tax-payers and would not significantlyimprove administration.

Several comments requested that theregulations modify the rule in theproposed regulations treating eachrental real estate interest of a pass-through entity as a separate interest ofa person owning a fifty-percent orgreater interest in the capital, gain,loss, income, deduction, or credit of theentity at any time during a taxableyear. A commentator stated that thisrule is burdensome on many pass-through entities and should be elimi-nated or modified. The final regulationsmodify this rule so that it applies onlywhen a qualifying taxpayer owns afifty-percent or greater interest in thecapital, profits, or losses of a pass-through entity for a taxable year.Accordingly, this rule will not apply ifa qualifying taxpayer owns a fifty-percent or greater interest in a singleitem of income or deduction but doesnot own a fifty-percent or greaterinterest in the overall capital, profits, orlosses of the passthrough entity.

In response to one comment, thefinal regulations also clarify the ap-plication of the fifty-percent ownershiprule to tiered passthrough entities. Thefinal regulations provide that if apassthrough entity owns a fifty-percentor greater interest in the capital, profits,or losses of another passthrough entityfor a taxable year, each interest inrental real estate of the lower-tier entitywill be a separate interest in rental realestate of the upper-tier entity.

In response to another comment, thefinal regulations clarify that section469(i) applies after the rules of section469(c)(7) are applied. Accordingly, the$25,000 offset will be applied onlyagainst passive losses from rental realestate activities, and not against lossesthat are allowable as a result of section469(c)(7). In addition, the final regula-tions clarify that adjusted gross incomefor purposes of section 469(i) is notreduced by any losses from rental real

estate that are allowable as a result ofsection 469(c)(7).

Several comments requested a modi-fication to the effective date provision,to provide that aggregation electionsmade for taxable years beginning be-fore January 1, 1995, are not bindingfor future years. Because taxpayers hadsufficient notice of the rules of section469(c)(7) and these regulations, thismodification is unnecessary and wouldadd administrative complexity. Accord-ingly, the final regulations adopt theeffective date provision of the proposedregulations.

Finally, in response to a comment,the activity regrouping rule of §1.469–4(e)(2) is clarified to provide that ataxpayer may not regroup activitiesunless the taxpayer’s original groupingwas clearly inappropriate or there hasbeen a material change in the facts andcircumstances that makes the originalgrouping clearly inappropriate.

III. Effective Dates

In general, section 469(c)(7) appliesfor taxable years beginning after De-cember 31, 1993. These regulations areeffective for taxable years beginning onor after January 1, 1995. These regula-tions are also effective for electionsunder section 469(c)(7)(A) and para-graph (g) of these regulations that aremade with returns filed on or afterJanuary 1, 1995.

Special Analyses

It has been determined that thisTreasury decision is not a significantregulatory action as defined in EO12866. Therefore, a regulatory assess-ment is not required. It also has beendetermined that section 553(b) of theAdministrative Procedure Act (5 U.S.C.chapter 5) and the Regulatory Flex-ibility Act (5 U.S.C. chapter 6) do notapply to these regulations, and, there-fore, a Regulatory Flexibility Analysisis not required. Pursuant to section7805(f) of the Internal Revenue Code,the notice of proposed rulemakingpreceding these regulations was submit-ted to the Small Business Administra-tion for comment on its impact onsmall business.

Drafting Information

The principal author of these regula-tions is William M. Kostak, Office of

Assistant Chief Counsel (Passthroughsand Special Industries), IRS. However,other personnel from the IRS andTreasury Department participated intheir development.

* * * * * *

Adoption of Amendments to theRegulations

Accordingly, 26 CFR part 1 isamended as follows:

PART I—INCOME TAXES

Paragraph 1. The authority citationfor part 1 is amended by adding anentry in numerical order to read asfollows:

Authority: 26 U.S.C. 7805. * * * Section 1.469–9 also issued under 26

U.S.C. 469(c)(6), (h)(2), and (l)(1). Par. 2. Section 1.469–0 is amended

by:1. Revising the entry for §1.469–

4(h).2. Revising the heading for §1.469–9

and adding entries for paragraphs (a)through (j) of §1.469–9.

3. Revising the entry for §1.469–11-(b)(2) and removing the entries for§1.469–11(b)(2)(i) and (ii).

4. Revising the entry for §1.469–11-(b)(3).

5. Adding an entry for §1.469–11-(b)(4).

6. The revisions and additions readas follows:

§1.469–0 Table of contents.

* * * * * *

§1.469–4 Definition of Activity.

* * * * * *

(h) Rules for grouping rental realestate activities for taxpayers qualifyingunder section 469(c)(7).

* * * * * *

§1.469–9 Rules for certain rentalreal estate activities.

(a) Scope and purpose. (b) Definitions.

(1) Trade or business. (2) Real property trade or

business.(3) Rental real estate.(4) Personal services.

SEQ 0007 JOB B09-003-004 PAGE-0007 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

7

(5) Material participation. (6) Qualifying taxpayer.

(c) Requirements for qualifyingtaxpayers.(1) In general.(2) Closely held C

corporations.(3) Requirement of material

participation in the realproperty trades or busi-nesses.

(4) Treatment of spouses. (5) Employees in real prop-

erty trades or businesses.(d) General rule for determining

real property trades orbusinesses.(1) Facts and circumstances. (2) Consistency requirement.

(e) Treatment of rental real estateactivities of a qualifyingtaxpayer.(1) In general.(2) Treatment as a former

passive activity. (3) Grouping rental real estate

activities with otheractivities.(i) In general.(ii) Special rule for certain

management activities.(4) Example.

(f) Limited partnership interests inrental real estate activities.(1) In general.(2) De minimis exception.

(g) Election to treat all interestsin rental real estate as a singlerental real estate activity.(1) In general.(2) Certain changes not mate-

rial. (3) Filing a statement to

make or revoke theelection.

(h) Interests in rental real estateheld by certain passthroughentities.(1) General rule.(2) Special rule if a qualify-

ing taxpayer holds a fifty-percent or greater interestin a passthrough entity.

(3) Special rule for interestsheld in tiered passthroughentities.

(i) [Reserved].(j) $25,000 offset for rental real

estate activities of qualifyingtaxpayers.(1) In general. (2) Example.

* * * * * *

§1.469–11 Effective date andtransition rules.

* * * * * *

(b) * * * (2) Additional transition rule for

1992 amendments.(3) Fresh starts under consistency

rules.(i) Regrouping when tax liability is

first determined under Project PS–1–89.

(ii) Regrouping when tax liability isfirst determined under §1.469–4.

(iii) Regrouping when taxpayer isfirst subject to section 469(c)(7).

(4) Certain investment creditproperty.

* * * * * *

Par. 3. Section 1.469–4 is amendedby revising paragraphs (e)(1) and (2)and (h). The revisions read as follows:

§1.469–4 Definition of Activity.

* * * * * *

(e) * * *(1) Original groupings. Except as

provided in paragraph (e)(2) of thissection and §1.469–11, once a taxpayerhas grouped activities under this sec-tion, the taxpayer may not regroupthose activities in subsequent taxableyears. Taxpayers must comply withdisclosure requirements that the Com-missioner may prescribe with respect toboth their original groupings and theaddition and disposition of specificactivities within those chosen groupingsin subsequent taxable years.

(2) Regroupings. If it is determinedthat a taxpayer’s original grouping wasclearly inappropriate or a materialchange in the facts and circumstanceshas occurred that makes the originalgrouping clearly inappropriate, the tax-payer must regroup the activities andmust comply with disclosure require-ments that the Commissioner mayprescribe.

* * * * * *

(h) Rules for grouping rental realestate activities for taxpayers qualify-ing under section 469(c)(7). See§1.469–9 for rules for certain rentalreal estate activities.

Par. 4. Section 1.469-9 is revised toread as follows:

§1.469–9 Rules for certain rentalreal estate activities.

(a) Scope and purpose. This sectionprovides guidance to taxpayers engagedin certain real property trades or busi-nesses on applying section 469(c)(7) totheir rental real estate activities.

(b) Definitions. The following defi-nitions apply for purposes of thissection:

(1) Trade or business. A trade orbusiness is any trade or businessdetermined by treating the types ofactivities in §1.469–4(b)(1) as if theyinvolved the conduct of a trade orbusiness, and any interest in rental realestate, including any interest in rentalreal estate that gives rise to deductionsunder section 212.

(2) Real property trade or business.Real property trade or business isdefined in section 469(c)(7)(C).

(3) Rental real estate. Rental realestate is any real property used bycustomers or held for use by customersin a rental activity within the meaningof §1.469–1T(e)(3). However, anyrental real estate that the taxpayergrouped with a trade or businessactivity under §1.469–4(d)(1)(i)(A) or(C) is not an interest in rental realestate for purposes of this section.

(4) Personal services. Personal serv-ices means any work performed by anindividual in connection with a trade orbusiness. However, personal servicesdo not include any work performed byan individual in the individual’s capac-ity as an investor as described in§1.469–5T(f)(2)(ii).

(5) Material participation. Materialparticipation has the same meaning asunder §1.469–5T. Paragraph (f) of thissection contains rules applicable tolimited partnership interests in rentalreal estate that a qualifying taxpayerelects to aggregate with other interestsin rental real estate of that taxpayer.

(6) Qualifying taxpayer. A qualify-ing taxpayer is a taxpayer that owns atleast one interest in rental real estateand meets the requirements of para-graph (c) of this section.

(c) Requirements for qualifying tax-payers—(1) In general. A qualifyingtaxpayer must meet the requirements ofsection 469(c)(7)(B).

(2) Closely held C corporations. Aclosely held C corporation meets therequirements of paragraph (c)(1) of thissection by satisfying the requirements

SEQ 0008 JOB B09-003-004 PAGE-0008 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

8

of section 469(c)(7)(D)(i). For purposesof section 469(c)(7)(D)(i), gross re-ceipts do not include items of portfolioincome within the meaning of §1.469–2T(c)(3).

(3) Requirement of material par-ticipation in the real property trades orbusinesses. A taxpayer must materiallyparticipate in a real property trade orbusiness in order for the personalservices provided by the taxpayer inthat real property trade or business tocount towards meeting the requirementsof paragraph (c)(1) of this section.

(4) Treatment of spouses. Spousesfiling a joint return are qualifyingtaxpayers only if one spouse separatelysatisfies both requirements of section469(c)(7)(B). In determining the realproperty trades or businesses in whicha married taxpayer materially partici-pates (but not for any other purposeunder this paragraph (c)), work per-formed by the taxpayer’s spouse in atrade or business is treated as workperformed by the taxpayer under§1.469–5T(f)(3), regardless of whetherthe spouses file a joint return for theyear.

(5) Employees in real propertytrades or businesses. For purposes ofparagraph (c)(1) of this section, per-sonal services performed during ataxable year as an employee generallywill be treated as performed in a tradeor business but will not be treated asperformed in a real property trade orbusiness, unless the taxpayer is a five-percent owner (within the meaning ofsection 416(i)(1)(B)) in the employer.If an employee is not a five-percentowner in the employer at all timesduring the taxable year, only thepersonal services performed by theemployee during the period theemployee is a five-percent owner in theemployer will be treated as performedin a real property trade or business.

(d) General rule for determiningreal property trades or businesses—(1)Facts and circumstances. The deter-mination of a taxpayer’s real propertytrades or businesses for purposes ofparagraph (c) of this section is basedon all of the relevant facts andcircumstances. A taxpayer may use anyreasonable method of applying the factsand circumstances in determining thereal property trades or businesses inwhich the taxpayer provides personalservices. Depending on the facts andcircumstances, a real property trade orbusiness consists either of one or more

than one trade or business specificallydescribed in section 469(c)(7)(C). Ataxpayer’s grouping of activities under§1.469–4 does not control the deter-mination of the taxpayer’s real propertytrades or businesses under this para-graph (d).

(2) Consistency requirement. Once ataxpayer determines the real propertytrades or businesses in which personalservices are provided for purposes ofparagraph (c) of this section, thetaxpayer may not redetermine thosereal property trades or businesses insubsequent taxable years unless theoriginal determination was clearly inap-propriate or there has been a materialchange in the facts and circumstancesthat makes the original determinationclearly inappropriate.

(e) Treatment of rental real estateactivities of a qualifying taxpayer—(1)In general. Section 469(c)(2) does notapply to any rental real estate activityof a taxpayer for a taxable year inwhich the taxpayer is a qualifyingtaxpayer under paragraph (c) of thissection. Instead, a rental real estateactivity of a qualifying taxpayer is apassive activity under section 469 forthe taxable year unless the taxpayermaterially participates in the activity.Each interest in rental real estate of aqualifying taxpayer will be treated as aseparate rental real estate activity,unless the taxpayer makes an electionunder paragraph (g) of this section totreat all interests in rental real estate asa single rental real estate activity. Eachseparate rental real estate activity, orthe single combined rental real estateactivity if the taxpayer makes anelection under paragraph (g), will be anactivity of the taxpayer for all purposesof section 469, including the formerpassive activity rules under section469(f) and the disposition rules undersection 469(g). However, section 469will continue to be applied separatelywith respect to each publicly tradedpartnership, as required under section469(k), notwithstanding the rules ofthis section.

(2) Treatment as a former passiveactivity. For any taxable year in whicha qualifying taxpayer materially partici-pates in a rental real estate activity,that rental real estate activity will betreated as a former passive activityunder section 469(f) if disalloweddeductions or credits are allocated tothe activity under §1.469–1(f)(4).

(3) Grouping rental real estate ac-tivities with other activities—(i) In

general. For purposes of this section, aqualifying taxpayer may not group arental real estate activity with any otheractivity of the taxpayer. For example, ifa qualifying taxpayer develops realproperty, constructs buildings, andowns an interest in rental real estate,the taxpayer’s interest in rental realestate may not be grouped with thetaxpayer’s development activity or con-struction activity. Thus, only the par-ticipation of the taxpayer with respectto the rental real estate may be used todetermine if the taxpayer materiallyparticipates in the rental real estateactivity under §1.469–5T.

(ii) Special rule for certain manage-ment activities. A qualifying taxpayermay participate in a rental real estateactivity through participation, withinthe meaning of §§1.469–5(f) and 5T(f),in an activity involving the manage-ment of rental real estate (even if thismanagement activity is conductedthrough a separate entity). In determin-ing whether the taxpayer materiallyparticipates in the rental real estateactivity, however, work the taxpayerperforms in the management activity istaken into account only to the extent itis performed in managing the tax-payer’s own rental real estate interests.

(4) Example. The following exampleillustrates the application of this para-graph (e).

Example. (i) Taxpayer B owns interests inthree rental buildings, U, V and W. In 1995, Bhas $30,000 of disallowed passive losses alloca-ble to Building U and $10,000 of disallowedpassive losses allocable to Building V under§1.469–1(f)(4). In 1996, B has $5,000 of netincome from building U, $5,000 of net lossesfrom building V, and $10,000 of net income frombuilding W. Also in 1996, B is a qualifyingtaxpayer within the meaning of paragraph (c) ofthis section. Each building is treated as aseparate activity of B under paragraph (e)(1) ofthis section, unless B makes the election underparagraph (g) to treat the three buildings as asingle rental real estate activity. If the buildingsare treated as separate activities, material par-ticipation is determined separately with respectto each building. If B makes the election underparagraph (g) to treat the buildings as a singleactivity, all participation relating to the buildingsis aggregated in determining whether B mate-rially participates in the combined activity.

(ii) Effective beginning in 1996, B makes theelection under paragraph (g) to treat the threebuildings as a single rental real estate activity. Bworks full-time managing the three buildings andthus materially participates in the combinedactivity in 1996 (even if B conducts thismanagement function through a separate entity,including a closely held C corporation). Accord-ingly, the combined activity is not a passiveactivity of B in 1996. Moreover, as a result ofthe election under paragraph (g), disallowed

SEQ 0009 JOB B09-003-004 PAGE-0009 PT 1 PGS 4- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-003

9

passive losses of $40,000 ($30,000 + $10,000)are allocated to the combined activity. B’s netincome from the activity for 1996 is $10,000($5,000 – $5,000 + $10,000). This net income isnonpassive income for purposes of section 469.However, under section 469(f), the net incomefrom a former passive activity may be offsetwith the disallowed passive losses from the sameactivity. Because Buildings U, V and W aretreated as one activity for all purposes of section469 due to the election under paragraph (g), andthis activity is a former passive activity undersection 469(f), B may offset the $10,000 of netincome from the buildings with an equal amountof disallowed passive losses allocable to thebuildings, regardless of which buildings pro-duced the income or losses. As a result, B has$30,000 ($40,000 – $10,000) of disallowed pas-sive losses remaining from the buildings after1996.

(f) Limited partnership interests inrental real estate activities—(1) Ingeneral. If a taxpayer elects underparagraph (g) of this section to treat allinterests in rental real estate as a singlerental real estate activity, and at leastone interest in rental real estate is heldby the taxpayer as a limited partnershipinterest (within the meaning of §1.469–5T(e)(3)), the combined rental realestate activity will be treated as alimited partnership interest of the tax-payer for purposes of determiningmaterial participation. Accordingly, thetaxpayer will not be treated under thissection as materially participating inthe combined rental real estate activityunless the taxpayer materially partici-pates in the activity under the testslisted in §1.469–5T(e)(2) (dealing withthe tests for determining the materialparticipation of a limited partner).

(2) De minimis exception. If aqualifying taxpayer elects under para-graph (g) of this section to treat allinterests in rental real estate as a singlerental real estate activity, and thetaxpayer’s share of gross rental incomefrom all of the taxpayer’s limitedpartnership interests in rental real estateis less than ten percent of the tax-payer’s share of gross rental incomefrom all of the taxpayer’s interests inrental real estate for the taxable year,paragraph (f)(1) of this section does notapply. Thus the taxpayer may deter-mine material participation under anyof the tests listed in §1.469–5T(a) thatapply to rental real estate activities.

(g) Election to treat all interests inrental real estate as a single rentalreal estate activity—(1) In general. Aqualifying taxpayer may make an elec-tion to treat all of the taxpayer’sinterests in rental real estate as a singlerental real estate activity. This election

is binding for the taxable year in whichit is made and for all future years inwhich the taxpayer is a qualifyingtaxpayer under paragraph (c) of thissection, even if there are interveningyears in which the taxpayer is not aqualifying taxpayer. The election maybe made in any year in which the tax-payer is a qualifying taxpayer, and thefailure to make the election in one yeardoes not preclude the taxpayer frommaking the election in a subsequentyear. In years in which the taxpayer isnot a qualifying taxpayer, the electionwill not have effect and the taxpayer’sactivities will be those determinedunder §1.469–4. If there is a materialchange in the taxpayer’s facts andcircumstances, the taxpayer may revokethe election using the procedure de-scribed in paragraph (g)(3) of thissection.

(2) Certain changes not material.The fact that an election is lessadvantageous to the taxpayer in aparticular taxable year is not, of itself,a material change in the taxpayer’sfacts and circumstances. Similarly, abreak in the taxpayer’s status as aqualifying taxpayer is not, of itself, amaterial change in the taxpayer’s factsand circumstances.

(3) Filing a statement to make orrevoke the election. A qualifying tax-payer makes the election to treat allinterests in rental real estate as a singlerental real estate activity by filing astatement with the taxpayer’s originalincome tax return for the taxable year.This statement must contain a declara-tion that the taxpayer is a qualifyingtaxpayer for the taxable year and ismaking the election pursuant to section469(c)(7)(A). The taxpayer may makethis election for any taxable year inwhich section 469(c)(7) is applicable.A taxpayer may revoke the electiononly in the taxable year in which amaterial change in the taxpayer’s factsand circumstances occurs or in asubsequent year in which the facts andcircumstances remain materiallychanged from those in the taxable yearfor which the election was made. Torevoke the election, the taxpayer mustfile a statement with the taxpayer’soriginal income tax return for the yearof revocation. This statement mustcontain a declaration that the taxpayeris revoking the election under section469(c)(7)(A) and an explanation of thenature of the material change.

(h) Interests in rental real estateheld by certain passthrough entities—

(1) General rule. Except as provided inparagraph (h)(2) of this section, aqualifying taxpayer’s interest in rentalreal estate held by a partnership or anS corporation (passthrough entity) istreated as a single interest in rental realestate if the passthrough entity groupedits rental real estate as one rentalactivity under §1.469–4(d)(5). If thepassthrough entity grouped its rentalreal estate into separate rental activitiesunder §1.469–4(d)(5), each rental realestate activity of the passthrough entitywill be treated as a separate interest inrental real estate of the qualifyingtaxpayer. However, the qualifying tax-payer may elect under paragraph (g) ofthis section to treat all interests inrental real estate, including the rentalreal estate interests held through pass-through entities, as a single rental realestate activity.

(2) Special rule if a qualifying tax-payer holds a fifty-percent or greaterinterest in a passthrough entity. If aqualifying taxpayer owns, directly orindirectly, a fifty-percent or greaterinterest in the capital, profits, or lossesof a passthrough entity for a taxableyear, each interest in rental real estateheld by the passthrough entity will betreated as a separate interest in rentalreal estate of the qualifying taxpayer,regardless of the passthrough entity’sgrouping of activities under §1.469–4(d)(5). However, the qualifying tax-payer may elect under paragraph (g) ofthis section to treat all interests inrental real estate, including the rentalreal estate interests held through pass-through entities, as a single rental realestate activity.

(3) Special rule for interests held intiered passthrough entities. If a pass-through entity owns a fifty-percent orgreater interest in the capital, profits, orlosses of another passthrough entity fora taxable year, each interest in rentalreal estate held by the lower-tier entitywill be treated as a separate interest inrental real estate of the upper-tierentity, regardless of the lower-tierentity’s grouping of activities under§1.469–4(d)(5).

(i) [Reserved].(j) $25,000 offset for rental real

estate activities of qualifying tax-payers—(1) In general. A qualifyingtaxpayer’s passive losses and creditsfrom rental real estate activities (in-cluding prior-year disallowed passiveactivity losses and credits from rentalreal estate activities in which the

SEQ 0010 JOB B09-004-003 PAGE-0010 PT 1 PGS 10- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-004

10

taxpayer materially participates) areallowed to the extent permitted undersection 469(i). The amount of losses orcredits allowable under section 469(i)is determined after the rules of thissection are applied. However, lossesallowable by reason of this section arenot taken into account in determiningadjusted gross income for purposes ofsection 469(i)(3).

(2) Example. The following exampleillustrates the application of this para-graph (j).

Example. (i) Taxpayer A owns building X andbuilding Y, both interests in rental real estate. In1995, A is a qualifying taxpayer within themeaning of paragraph (c) of this section. A doesnot elect to treat X and Y as one activity undersection 469(c)(7)(A) and paragraph (g) of thissection. As a result, X and Y are treated asseparate activities pursuant to section 469(c)(7)-(A)(ii). A materially participates in X which has$100,000 of passive losses disallowed from prioryears and produces $20,000 of losses in 1995. Adoes not materially participate in Y whichproduces $40,000 of income in 1995. A also has$50,000 of income from other nonpassivesources in 1995. A otherwise meets the require-ments of section 469(i).

(ii) Because X is not a passive activity in1995, the $20,000 of losses produced by X in1995 are nonpassive losses that may be used byA to offset part of the $50,000 of nonpassiveincome. Accordingly, A is left with $30,000($50,000 – $20,000) of nonpassive income. Inaddition, A may use the prior year disallowedpassive losses of X to offset any income from Xand passive income from other sources. There-fore, A may offset the $40,000 of passive incomefrom Y with $40,000 of passive losses from X.

(iii) Because A has $60,000 ($100,000 –$40,000) of passive losses remaining from X andmeets all of the requirements of section 469(i), Amay offset up to $25,000 of nonpassive incomewith passive losses from X pursuant to section469(i). As a result, A has $5,000 ($30,000 –$25,000) of nonpassive income remaining anddisallowed passive losses from X of $35,000($60,000 – $25,000) in 1995.

Par. 5. Section 1.469–11 is amendedas follows:

1. Paragraph (a)(2) is amended byremoving ‘‘; and’’ and adding ‘‘;’’ inits place.

2. Paragraph (a)(3) is redesignatedas paragraph (a)(4) and a new para-graph (a)(3) is added.

3. Paragraph (b)(1) is revised.4. The heading for paragraph (b)(2)

is revised; the headings for paragraphs(b)(2)(i) and (b)(2)(ii) are removed;paragraph (b)(2)(ii) is removed, andparagraph (b)(2)(i) is redesignated asparagraph (b)(2).

5. Paragraph (b)(3) is redesignatedas paragraph (b)(4).

6. A new paragraph (b)(3) is added.

The added and revised provisionsread as follows:

§1.469–11 Effective date andtransition rules.

(a) * * *(3) The rules contained in §1.469–9

apply for taxable years beginning on orafter January 1, 1995, and to electionsmade under §1.469–9(g) with returnsfiled on or after January 1, 1995; and

* * * * * *

(b) * * * (1) Application of 1992amendments for taxable years begin-ning before October 4, 1994. Except asprovided in paragraph (b)(2) of thissection, for taxable years that end afterMay 10, 1992, and begin beforeOctober 4, 1994, a taxpayer maydetermine tax liability in accordancewith Project PS–1–89 published at1992–1 C.B. 1219 (see §601.601(d)(2)-(ii)(b) of this chapter).

(2) Additional transition rule for1992 amendments. * * *

(3) Fresh starts under consistencyrules—(i) Regrouping when tax lia-bility is first determined under ProjectPS–1–89. For the first taxable year inwhich a taxpayer determines its taxliability under Project PS–1–89, thetaxpayer may regroup its activitieswithout regard to the manner in whichthe activities were grouped in thepreceding taxable year and must re-group its activities if the grouping inthe preceding taxable year is inconsist-ent with the rules of Project PS–1–89.

(ii) Regrouping when tax liability isfirst determined under §1.469–4. Forthe first taxable year in which ataxpayer determines its tax liabilityunder §1.469–4, rather than under therules of Project PS–1–89, the taxpayermay regroup its activities without re-gard to the manner in which theactivities were grouped in the preced-ing taxable year and must regroup itsactivities if the grouping in the preced-ing taxable year is inconsistent with therules of §1.469–4.

(iii) Regrouping when taxpayer isfirst subject to section 469(c)(7). Forthe first taxable year beginning afterDecember 31, 1993, a taxpayer may re-group its activities to the extent neces-sary or appropriate to avail itself of theprovisions of section 469(c)(7) andwithout regard to the manner in which

the activities were grouped in thepreceding taxable year.

* * * * * *

Margaret Milner Richardson,Commissioner of

Internal Revenue.

Approved December 12, 1995.

Leslie Samuels,Assistant Secretary of

the Treasury (Tax Policy).

(Filed by the Office of the Federal Register onDecember 21, 1995, 8:45 a.m., and publishedin the issue of the Federal Register forDecember 22, 1995, 60 F.R. 66496)

Section 861.—Income From SourcesWithin the United States

26 CFR 1.861–8: Computation of taxableincome from sources within the United Statesand from other sources and activities.

T.D. 8646

DEPARTMENT OF THE TREASURYInternal Revenue Service26 CFR Part 1

Allocation and Apportionment ofResearch and ExperimentalExpenditures

AGENCY: Internal Revenue Service(IRS), Treasury.

ACTION: Final regulations.

SUMMARY: This document providesguidance concerning the allocation andapportionment of research and experi-mental expenditures for purposes ofdetermining taxable income fromsources within and without the UnitedStates. This document affects taxpayersthat have income from United Statesand foreign sources and that have madeexpenditures for research and experi-mentation that the taxpayer deductsunder section 174 of the InternalRevenue Code of 1986.

EFFECTIVE DATE: January 1, 1996.

FOR FURTHER INFORMATIONCONTACT: Carl Cooper at (202)622-3840 (not a toll-free number).

SEQ 0011 JOB B09-004-003 PAGE-0011 PT 1 PGS 10- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-004

11

SUPPLEMENTARY INFORMATION:

Background and Explanation ofProvisions

On May 24, 1995, the IRS publisheda notice of proposed rulemaking andnotice of public hearing in the FederalRegister (60 FR 27453 [INTL–23–95,1995–1 C.B. 987]) proposing amend-ments to the Income Tax Regulations(26 CFR part 1) under section 861 ofthe Internal Revenue Code of 1986.Section 1.861–8(e)(3) of the IncomeTax Regulations provides rules regard-ing the allocation and apportionment ofresearch and experimental expendituresfor purposes of determining taxableincome from sources inside and outsidethe United States.

The notice of proposed rulemakingproposed three principal changes to theexisting regulations. First, allocation ofresearch and experimental expendituresto three digit SIC code product catego-ries of gross income would be permit-ted. Second, the percentage of researchand experimental expenditures that maybe exclusively apportioned to UnitedStates source income under the salesmethod of apportionment under§1.861–8(e)(3)(ii) would be increasedfrom 30 percent to 50 percent. Third,use of the optional gross incomemethods of apportionment would con-stitute a binding election to use suchmethods in subsequent years. Theelection would not be revocable with-out the prior consent of the Commis-sioner. The three changes were pro-posed in part on the basis of aneconomic study performed by theTreasury Department pursuant to Rev.Proc. 92–56 (1992–2 C.B. 409), ‘‘TheRelationship between U.S. Researchand Development and Foreign In-come,’’ which was published by theTreasury Department simultaneouslywith the proposed regulations.

Written comments responding to thenotice were received, and a publichearing was held on September 8,1995.

Regarding the determination of prod-uct categories under §1.861–8(e)-(3)(i)(B) of the proposed regulations,commenters suggested that the rulerequiring a taxpayer to determine rele-vant product categories by reference tothe three digit classification of theStandard Industrial Classification Man-ual should be modified to allow deter-minations by reference to the five digit

classifications of the Manual. Thissuggestion was not adopted, becausesuch a rule would too narrowly restrictthe necessarily broad scope of thededuction. The IRS continues to be-lieve that research and experimentationis an inherently speculative activity,that findings may contribute unex-pected benefits, and that gross incomederived from successful research andexperimentation must bear the cost ofunsuccessful research and experi-mentation.

Commenters suggested that the reg-ulations permit taxpayers to determineproduct categories by reference to twoor three digit categories at the annualelection of the taxpayer. This sugges-tion was not adopted. The regulationsprovide that a taxpayer may determineproduct categories by reference to twoor three digit categories. A taxpayermay aggregate, disaggregate or changea previously selected SIC code cate-gory if the taxpayer establishes to thesatisfaction of the Commissioner that,due to changes in the relevant facts, achange in product category is appropri-ate. This rule provides a simple andworkable format for balancing the needfor consistency with the desire forflexibility.

Referring to current §1.861–8(g) Ex-ample 6 (which has been redesignated§1.861–17(h) Example 4), commenterssuggested that the regulations allow theuse of the Wholesale Trade SIC codecategory with respect to sales from anyother category. The current §1.861–8(g)Example 6 was not correct on this pointand does not override the rule statedparenthetically in the list of two digitSIC code categories in present §1.861–8(e)(3)(i)(A) that wholesale trade maynot be combined with other productcategories. The final regulations in-clude this rule along with Example 6corrected to conform to the rule.

Regarding the exclusive place ofperformance apportionment rule under§1.861–8(e)(3)(ii)(A) of the proposedregulations, commenters suggestedadding a rule providing that if the ratioof foreign research and experimentalexpenditures in a three digit SIC codecategory of all foreign affiliates of aUnited States consolidated group overforeign affiliate sales in that SIC codecategory exceed fifty percent of theratio of United States consolidatedgroup research and experimental expen-ditures in that SIC code category overUnited States consolidated group salesin that SIC code category, then the

United States consolidated group re-search and experimental expendituresshould be exclusively apportioned toUnited States source gross income.This suggestion has not been adopted.Although a foreign affiliate may incursubstantial research and experimentalexpenditures in a given product cate-gory, the foreign affiliate may stillbenefit from the research and experi-mental expenditures of the UnitedStates consolidated group. See Perkin-Elmer Corporation v. Commissioner,103 T.C. 464 (1994).

Regarding the optional gross incomemethods of apportionment under§1.861–8(e)(3)(iii) of the proposed reg-ulations, commenters suggested that thefinal regulations include a fifty percentexclusive place of performance appor-tionment under the optional gross in-come methods to be parallel with§1.861–8(e)(3)(ii)(A). This suggestionhas been adopted in part. Section(b)(1)(ii) of the final regulations in-cludes a twenty-five percent exclusiveplace of performance apportionmentunder the optional gross incomemethods. This twenty-five percent ex-clusive apportionment ensures that tax-payers electing to use one of theoptional gross income methods alsoobtain results comparable to thoseobtained by taxpayers electing to usethe sales method, i.e., an overallallocation that is twenty-five percentlower on average than the allocation toforeign source income resulting fromthe current regulations. The TreasuryDepartment study does not support agreater exclusive apportionment.

Commenters suggested that the pro-posed regulations should be modifiedto reduce the floor on the amount ofresearch and experimental expendituresthat must be apportioned to foreignsource income under the optional grossincome methods from fifty percent tothirty percent of the amount that wouldhave been apportioned under the salesmethod. This suggestion has not beenadopted. The adoption of this suggestedrule in addition to the twenty-fivepercent exclusive apportionment rule isnot supported by the Treasury Depart-ment study.

Commenters suggested the elimina-tion of the binding election to use theoptional gross income methods under§1.861–8(e)(3)(iii)(C) of the proposedregulations. Commenters also suggestedthat the binding election rule should bemodified to provide for a change ofmethod without the prior consent of the

SEQ 0012 JOB B09-004-003 PAGE-0012 PT 1 PGS 10- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-004

12

Commissioner after five years’ use ofone method. This suggestion, whichrecognizes the need for consistencywhile reducing the administrative bur-den on taxpayers, has been adopted.

Commenters suggested that the effec-tive date election under §1.861–8(e)-(3)(vi) of the proposed regulationspermit election by fiscal year taxpayerswhose taxable years begin after August1, 1994, but before January 1, 1995.This suggestion has been adopted.

Finally, these provisions, which werepreviously published as §1.861–8(e)(3),have been renumbered and will now bepublished as §1.861–17. This changehas been made solely for the purposeof achieving greater clarity in format-ting and is not intended to result in anyadditional substantive changes.

Special Analyses

It has been determined that thesefinal regulations are not a significantregulatory action as defined in EO12866. Therefore, a regulatory assess-ment is not required. It also has beendetermined that section 553(b) of theAdministrative Procedure Act (5 U.S.C.chapter 5) and the Regulatory Flex-ibility Act (5 U.S.C. chapter 6) do notapply to these regulations, and there-fore a Regulatory Flexibility Analysisis not required. Pursuant to section7805(f) of the Internal Revenue Code,the notice of proposed rulemakingpreceding these final regulations hasbeen submitted to the Chief Counselfor Advocacy of the Small BusinessAdministration for comment on itsimpact on small business.

Drafting Information

The principal author of these regula-tions is Carl Cooper, Office of theAssociate Chief Counsel (Interna-tional). However, other personnel fromIRS and Treasury participated in theirdevelopment.

* * * * * *

Amendments to the Regulations

Accordingly, 26 CFR part 1 isamended as follows:

PART 1—INCOME TAXES

Paragraph 1. The authority citationcontinues to read as follows:

Authority: 26 U.S.C. 7805 * * *Par. 2. Section 1.861–8 is amended

by:1. Revising paragraph (e)(3) to

read as set forth below.2. Removing and reserving para-

graph (g), Examples 3 through 16 and23.

§1.861–8 Computation of taxableincome from sources within theUnited States and from other sourcesand activities.

* * * * * *

(e) * * *(3) Research and experimental ex-

penditures. For rules regarding theallocation and apportionment of re-search and experimental expenditures,see §1.861–17.

* * * * * *

Par. 3. Section 1.861–17 is added toread as follows:§1.861–17 Allocation and apportion-ment of research and experimentalexpenditures.

(a) Allocation—(1) In general. Themethods of allocation and apportion-ment of research and experimentalexpenditures set forth in this sectionrecognize that research and experimen-tation is an inherently speculative ac-tivity, that findings may contributeunexpected benefits, and that the grossincome derived from successful re-search and experimentation must bearthe cost of unsuccessful research andexperimentation. Expenditures for re-search and experimentation that a tax-payer deducts under section 174 or-dinarily shall be considered deductionsthat are definitely related to all incomereasonably connected with the relevantbroad product category (or categories)of the taxpayer and therefore allocableto all items of gross income as a class(including income from sales, royalties,and dividends) related to such productcategory (or categories). For purposesof this allocation, the product category(or categories) that a taxpayer may beconsidered to have shall be determinedin accordance with the provisions ofparagraph (a)(2) of this section.

(2) Product categories—(i) Alloca-tion based on product categories. Or-dinarily, a taxpayer’s research andexperimental expenditures may be di-vided between the relevant productcategories. Where research and experi-

mentation is conducted with respect tomore than one product category, thetaxpayer may aggregate the categoriesfor purposes of allocation and appor-tionment; however, the taxpayer maynot subdivide the categories. Whereresearch and experimentation is notclearly identified with any productcategory (or categories), it will beconsidered conducted with respect toall the taxpayer’s product categories.

(ii) Use of three digit standardindustrial classification codes. A tax-payer shall determine the relevantproduct categories by reference to thethree digit classification of the StandardIndustrial Classification Manual (SICcode). A copy may be purchased fromthe Superintendent of Documents,United States Government Printing Of-fice, Washington, DC 20402. Theindividual products included withineach category are enumerated in Ex-ecutive Office of the President, Officeof Management and Budget, StandardIndustrial Classification Manual, 1987(or later edition, as available).

(iii) Consistency. Once a taxpayerselects a product category for the firsttaxable year for which this section iseffective with respect to the taxpayer, itmust continue to use that productcategory in following years, unless thetaxpayer establishes to the satisfactionof the Commissioner that, due tochanges in the relevant facts, a changein the product category is appropriate.For this purpose, a change in thetaxpayer’s selection of a product cate-gory shall include a change from athree digit SIC code category to a twodigit SIC code category, a change froma two digit SIC code category to athree digit SIC code category, or anyother aggregation, disaggregation orchange of a previously selected SICcode category.

(iv) Wholesale trade category. Thetwo digit SIC code category ‘‘Whole-sale trade’’ is not applicable withrespect to sales by the taxpayer ofgoods and services from any other ofthe taxpayer’s product categories and isnot applicable with respect to a domes-tic international sales corporation(DISC) or foreign sales corporation(FSC) for which the taxpayer is arelated supplier of goods and servicesfrom any of the taxpayer’s productcategories.

(v) Retail trade category. The twodigit SIC code category ‘‘Retail trade’’is not applicable with respect to sales

SEQ 0013 JOB B09-004-003 PAGE-0013 PT 1 PGS 10- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-004

13

by the taxpayer of goods and servicesfrom any other of the taxpayer’sproduct categories, except wholesaletrade, and is not applicable with respectto a DISC or FSC for which the tax-payer is a related supplier of goods andservices from any other of the tax-payer’s product categories, exceptwholesale trade.

(3) Affiliated Groups—(i) In gen-eral. Except as provided in paragraph(a)(3)(ii) of this section, the allocationand apportionment required by thissection shall be determined as if allmembers of the affiliated group (asdefined in §1.861–14T(d)) were asingle corporation. See §1.861–14T.

(ii) Possessions corporations. (A)For purposes of the allocation andapportionment required by this section,sales and gross income from productsproduced in whole or in part in apossession by an electing corporation(within the meaning of section 936(h)-(5)(E)), and dividends from an electingcorporation, shall not be taken intoaccount, except that this paragraph(a)(3)(ii) shall not apply to sales of(and gross income and dividends at-tributable to sales of) products withrespect to which an election undersection 936(h)(5)(F) is not in effect.

(B) The research and experimentalexpenditures taken into account forpurposes of this section shall bereduced by the amount of such expen-ditures included in computing the cost-sharing amount (determined under sec-tion 936(h)(5)(C)(i)).

(4) Legally mandated research andexperimentation. Where research andexperimentation is undertaken solely tomeet legal requirements imposed by apolitical entity with respect to improve-ment or marketing of specific productsor processes, and the results cannotreasonably be expected to generateamounts of gross income (beyond deminimis amounts) outside a singlegeographic source, the deduction forsuch research and experimentation shallbe considered definitely related andtherefore allocable only to the grouping(or groupings) of gross income withinthat geographic source as a class (andapportioned, if necessary, between suchgroupings as set forth in paragraphs (c)and (d) of this section). For example,where a taxpayer performs tests on aproduct in response to a requirementimposed by the U.S. Food and DrugAdministration, and the test resultscannot reasonably be expected to gen-

erate amounts of gross income (beyondde minimis amounts) outside the UnitedStates, the costs of testing shall beallocated solely to gross income fromsources within the United States.

(b) Exclusive apportionment—(1) Ingeneral. An exclusive apportionmentshall be made under this paragraph (b),where an apportionment based upongeographic sources of income of adeduction for research and experimen-tation is necessary (after applying theexception in paragraph (a)(4) of thissection).

(i) Exclusive apportionment underthe sales method. If the taxpayerapportions on the sales method underparagraph (c) of this section, an amountequal to fifty percent of such deductionfor research and experimentation shallbe apportioned exclusively to the statu-tory grouping of gross income or theresidual grouping of gross income, asthe case may be, arising from thegeographic source where the researchand experimental activities which ac-count for more than fifty percent of theamount of such deduction wereperformed.

(ii) Exclusive apportionment underthe optional gross income methods. Ifthe taxpayer apportions on the optionalgross income methods under paragraph(d) of this section, an amount equal totwenty-five percent of such deductionfor research and experimentation shallbe apportioned exclusively to the statu-tory grouping or the residual groupingof gross income, as the case may be,arising from the geographic sourcewhere the research and experimentalactivities which account for more thanfifty percent of the amount of suchdeduction were performed.

(iii) Exception. If the applicable fiftypercent geographic source test of thepreceding paragraph (b)(1)(i) or (ii) isnot met, then no part of the deductionshall be apportioned under this para-graph (b)(1).

(2) Facts and circumstances sup-porting an increased exclusive ap-portionment—(i) In general. The exclu-sive apportionment provided for inparagraph (b)(1) of this section reflectsthe view that research and experimenta-tion is often most valuable in thecountry where it is performed, for tworeasons. First, research and experimen-tation often benefits a broad productcategory, consisting of many individualproducts, all of which may be sold inthe nearest market but only some of

which may be sold in foreign markets.Second, research and experimentationoften is utilized in the nearest marketbefore it is used in other markets, andin such cases, has a lower value perunit of sales when used in foreignmarkets. The taxpayer may establish tothe satisfaction of the Commissionerthat, in its case, one or both of theconditions mentioned in the precedingsentences warrant a significantlygreater exclusive allocation percentagethan allowed by paragraph (b)(1) ofthis section because the research andexperimentation is reasonably expectedto have very limited or long delayedapplication outside the geographicsource where it was performed. Pastexperience with research and experi-mentation may be considered in deter-mining reasonable expectations.

(ii) Not all products sold in foreignmarkets. For purposes of establishingthat only some products within theproduct category (or categories) aresold in foreign markets, the taxpayershall compare the commercial produc-tion of individual products in domesticand foreign markets made by itself, byuncontrolled parties (as defined underparagraph (c)(2)(i) of this section) ofproducts involving intangible propertywhich was licensed or sold by thetaxpayer, and by those controlled cor-porations (as defined under paragraph(c)(3)(ii) of this section) that canreasonably be expected to benefit di-rectly or indirectly from any of thetaxpayer’s research expense connectedwith the product category (or catego-ries). The individual products comparedfor this purpose shall be limited, fornonmanufactured categories, solely tothose enumerated in Executive Officeof the President, Office of Managementand Budget Standard Industrial Classi-fication Manual, 1987 (or later edition,as available), and, for manufacturedcategories, solely to those enumeratedat a 7-digit level in the U.S. Bureau ofthe Census, Census of Manufacturers:1992, Numerical List of ManufacturedProducts, 1993, (or later edition, asavailable). Copies of both of thesedocuments may be purchased from theSuperintendent of Documents, UnitedStates Government Printing Office,Washington, DC 20402.

(iii) Delayed application of researchfindings abroad. For purposes ofestablishing the delayed application ofresearch findings abroad, the taxpayershall compare the commercial introduc-tion of its own particular products and

SEQ 0014 JOB B09-004-003 PAGE-0014 PT 1 PGS 10- REVISED 28MAY96 AT 11:26 BY LR DEPTH: 65.01 PICAS WIDTH 46 PICAS COMPOSITE COLOR

778/20048/28MAY96/B09-004

14

processes (not limited by those listed inthe Standard Industrial ClassificationManual or the Numerical List of Manu-factured Products) in the United Statesand foreign markets, made by itself, byuncontrolled parties (as defined underparagraph (c)(2)(i) of this section) ofproducts involving intangible propertythat was licensed or sold by thetaxpayer, and by those controlled cor-porations (as defined under paragraph(c)(3)(i) of this section) that canreasonably be expected to benefit,directly or indirectly, from the tax-payer’s research expense. For purposesof evaluating the delay in the applica-tion of research findings in foreignmarkets, the taxpayer shall use a safehaven discount rate of 10 percent peryear of delay unless he is able toestablish to the satisfaction of theCommissioner, by reference to the costof money and the number of yearsduring which economic benefit can bedirectly attributable to the results of thetaxpayer’s research, that another dis-count rate is more appropriate.

(c) Sales method—(1) In general.The amount equal to the remainingportion of such deduction for researchand experimentation, not apportionedunder paragraph (a)(4) or (b)(1)(i) ofthis section, shall be apportioned be-tween the statutory grouping (or amongthe statutory groupings) within theclass of gross income and the residualgrouping within such class in the sameproportions that the amount of salesfrom the product category (or catego-ries) that resulted in such gross incomewithin the statutory grouping (or statu-tory groupings) and in the residualgrouping bear, respectively, to the totalamount of sales from the productcategory (or categories).

(i) Apportionment in excess of grossincome. Amounts apportioned underthis section may exceed the amount ofgross income related to the productcategory within the statutory grouping.In such case, the excess shall beapplied against other gross incomewithin the statutory grouping. See§1.861–8(d)(1) for instances where theapportionment leads to an excess ofdeductions over gross income withinthe statutory grouping.

(ii) Leased property. For purposes ofthis paragraph (c), amounts receivedfrom the lease of equipment during ataxable year shall be regarded as salesreceipts for such taxable year.

(2) Sales of uncontrolled parties. Forpurposes of the apportionment under

paragraph (c)(1) of this section, thesales from the product category (orcategories) by each party uncontrolledby the taxpayer, of particular productsinvolving intangible property that waslicensed or sold by the taxpayer to suchuncontrolled party shall be taken fullyinto account both for determining thetaxpayer’s apportionment and for deter-mining the apportionment of any othermember of a controlled group ofcorporations to which the taxpayerbelongs if the uncontrolled party canreasonably be expected to benefit di-rectly or indirectly (through any mem-ber of the controlled group of corpora-tions to which the taxpayer belongs)from the research expense connectedwith the product category (or catego-ries) of such other member. An uncon-trolled party can reasonably be ex-pected to benefit from the researchexpense of a member of a controlledgroup of corporations to which thetaxpayer belongs if such member canreasonably be expected to license, sell,or transfer intangible property to thatuncontrolled party or transfer secretprocesses to that uncontrolled party,directly or indirectly through a memberof the controlled group of corporationsto which the taxpayer belongs. Pastexperience with research and experi-mentation shall be considered in deter-mining reasonable expectations.