Embed Size (px)

DESCRIPTION

BCC's monthly economic review for 02/2014

Citation preview

05/02/2014 UK Economic Review PAGE 1 OF 4

UK Monthly Economic Review February 2014 (Based on January 2014 data releases)

Monthly headlines:

UK economic growth reaches six-year high, and the IMF raises its forecast for UK GDP

Although most sectors saw a rise in output in Q4, services remains the key driver of growth

UK employment reaches historic high, but an early interest rate rise is not expected

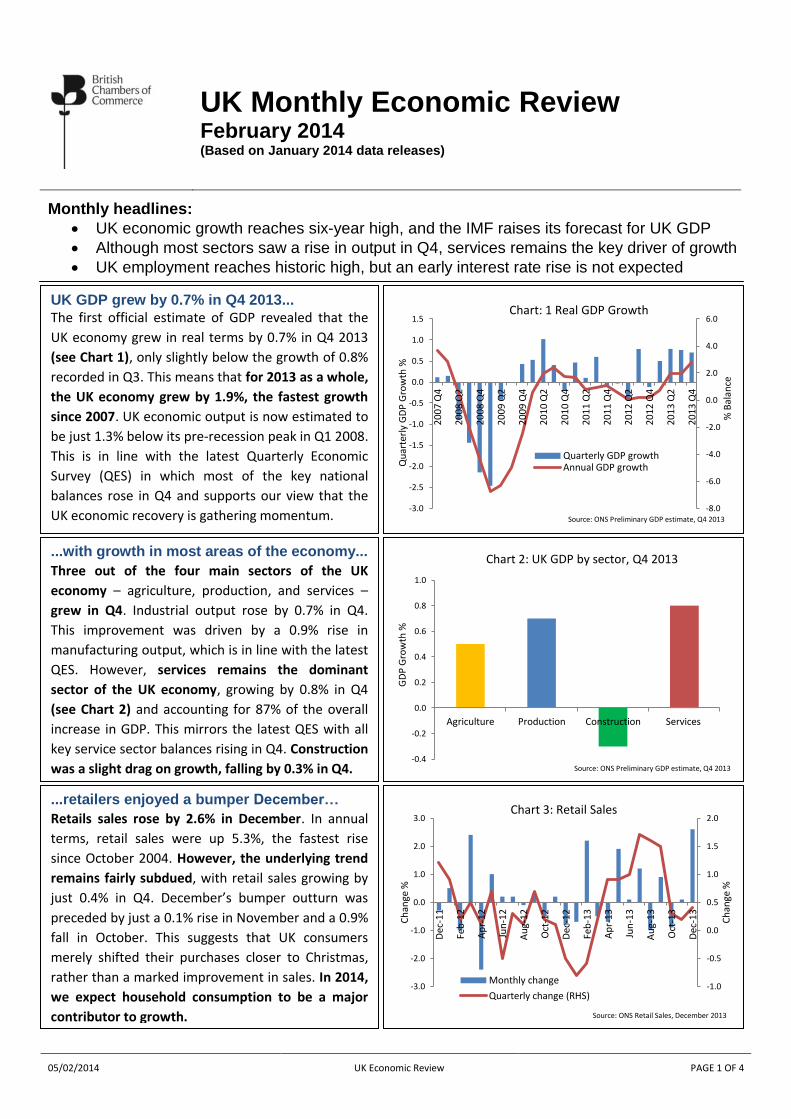

UK GDP grew by 0.7% in Q4 2013...

The first official estimate of GDP revealed that the

UK economy grew in real terms by 0.7% in Q4 2013

(see Chart 1), only slightly below the growth of 0.8%

recorded in Q3. This means that for 2013 as a whole,

the UK economy grew by 1.9%, the fastest growth

since 2007. UK economic output is now estimated to

be just 1.3% below its pre-recession peak in Q1 2008.

This is in line with the latest Quarterly Economic

Survey (QES) in which most of the key national

balances rose in Q4 and supports our view that the

UK economic recovery is gathering momentum.

-8.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

6.0

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

20

07

Q4

20

08

Q2

20

08

Q4

20

09

Q2

20

09

Q4

20

10

Q2

20

10

Q4

20

11

Q2

20

11

Q4

20

12

Q2

20

12

Q4

20

13

Q2

20

13

Q4

% B

alan

ce

Qu

arte

rly

GD

P G

row

th %

Chart: 1 Real GDP Growth

Quarterly GDP growth Annual GDP growth

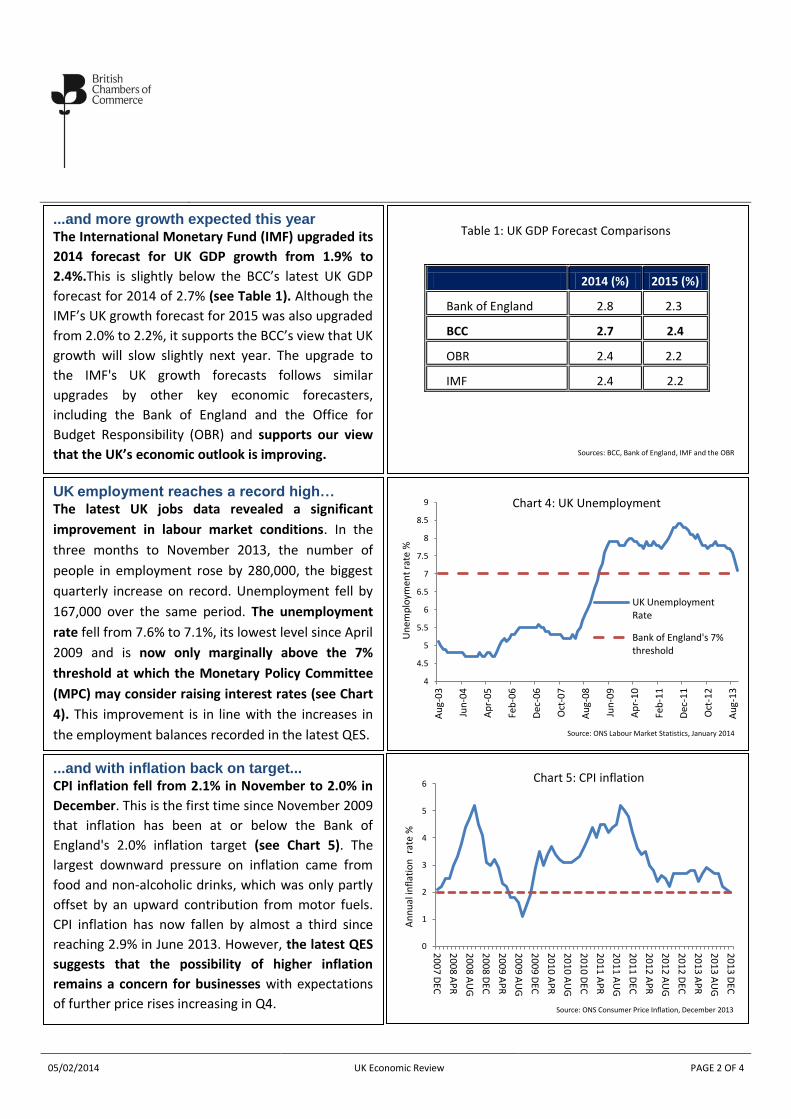

...with growth in most areas of the economy...

Three out of the four main sectors of the UK

economy – agriculture, production, and services –

grew in Q4. Industrial output rose by 0.7% in Q4.

This improvement was driven by a 0.9% rise in

manufacturing output, which is in line with the latest

QES. However, services remains the dominant

sector of the UK economy, growing by 0.8% in Q4

(see Chart 2) and accounting for 87% of the overall

increase in GDP. This mirrors the latest QES with all

key service sector balances rising in Q4. Construction

was a slight drag on growth, falling by 0.3% in Q4.

.

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

Agriculture Production Construction Services

GD

P G

row

th %

Chart 2: UK GDP by sector, Q4 2013

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

Dec

-11

Feb

-12

Ap

r-1

2

Jun

-12

Au

g-1

2

Oct

-12

Dec

-12

Feb

-13

Ap

r-1

3

Jun

-13

Au

g-1

3

Oct

-13

Dec

-13

Ch

ange

%

Ch

ange

%

Chart 3: Retail Sales

Monthly change

Quarterly change (RHS)

...retailers enjoyed a bumper December…

Retails sales rose by 2.6% in December. In annual

terms, retail sales were up 5.3%, the fastest rise

since October 2004. However, the underlying trend

remains fairly subdued, with retail sales growing by

just 0.4% in Q4. December’s bumper outturn was

preceded by just a 0.1% rise in November and a 0.9%

fall in October. This suggests that UK consumers

merely shifted their purchases closer to Christmas,

rather than a marked improvement in sales. In 2014,

we expect household consumption to be a major

contributor to growth.

Source: ONS Preliminary GDP estimate, Q4 2013

Source: ONS Preliminary GDP estimate, Q4 2013

Source: ONS Retail Sales, December 2013

05/02/2014 UK Economic Review PAGE 2 OF 4

+

some

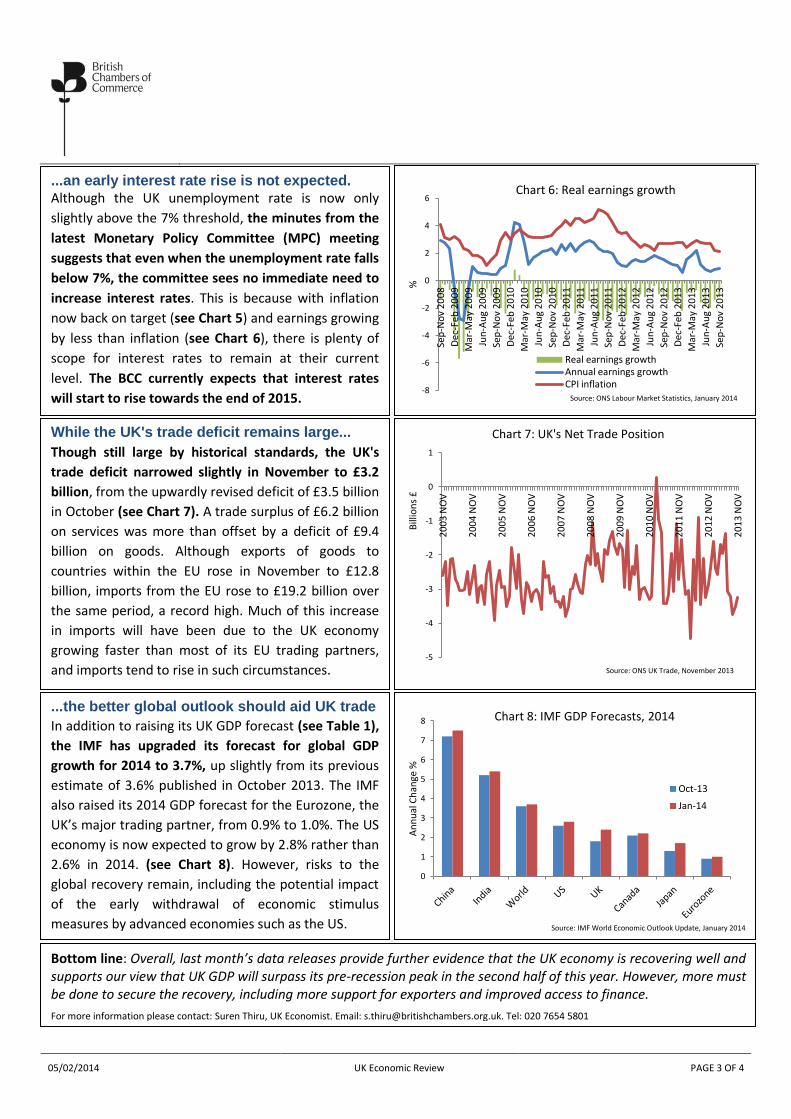

...and more growth expected this year

The International Monetary Fund (IMF) upgraded its

2014 forecast for UK GDP growth from 1.9% to

2.4%.This is slightly below the BCC’s latest UK GDP

forecast for 2014 of 2.7% (see Table 1). Although the

IMF’s UK growth forecast for 2015 was also upgraded

from 2.0% to 2.2%, it supports the BCC’s view that UK

growth will slow slightly next year. The upgrade to

the IMF's UK growth forecasts follows similar

upgrades by other key economic forecasters,

including the Bank of England and the Office for

Budget Responsibility (OBR) and supports our view

that the UK’s economic outlook is improving.

2014 (%) 2015 (%)

Bank of England 2.8 2.3

BCC 2.7 2.4

OBR 2.4 2.2

IMF 2.4 2.2

4

4.5

5

5.5

6

6.5

7

7.5

8

8.5

9

Au

g-0

3

Jun

-04

Ap

r-0

5

Feb

-06

Dec

-06

Oct

-07

Au

g-0

8

Jun

-09

Ap

r-1

0

Feb

-11

Dec

-11

Oct

-12

Au

g-1

3

Un

emp

loym

ent

rate

%

Chart 4: UK Unemployment

UK Unemployment Rate

Bank of England's 7% threshold

...and with inflation back on target...

CPI inflation fell from 2.1% in November to 2.0% in

December. This is the first time since November 2009

that inflation has been at or below the Bank of

England's 2.0% inflation target (see Chart 5). The

largest downward pressure on inflation came from

food and non-alcoholic drinks, which was only partly

offset by an upward contribution from motor fuels.

CPI inflation has now fallen by almost a third since

reaching 2.9% in June 2013. However, the latest QES

suggests that the possibility of higher inflation

remains a concern for businesses with expectations

of further price rises increasing in Q4.

0

1

2

3

4

5

6

20

07

DEC

20

08

AP

R

20

08

AU

G

20

08

DEC

20

09

AP

R

20

09

AU

G

20

09

DEC

20

10

AP

R

20

10

AU

G

20

10

DEC

20

11

AP

R

20

11

AU

G

20

11

DEC

20

12

AP

R

20

12

AU

G

20

12

DEC

20

13

AP

R

20

13

AU

G

20

13

DEC

An

nu

al in

flat

ion

rat

e %

Chart 5: CPI inflation

UK employment reaches a record high…

The latest UK jobs data revealed a significant

improvement in labour market conditions. In the

three months to November 2013, the number of

people in employment rose by 280,000, the biggest

quarterly increase on record. Unemployment fell by

167,000 over the same period. The unemployment

rate fell from 7.6% to 7.1%, its lowest level since April

2009 and is now only marginally above the 7%

threshold at which the Monetary Policy Committee

(MPC) may consider raising interest rates (see Chart

4). This improvement is in line with the increases in

the employment balances recorded in the latest QES.

Source: ONS Labour Market Statistics, January 2014

Source: ONS Consumer Price Inflation, December 2013

Table 1: UK GDP Forecast Comparisons

Sources: BCC, Bank of England, IMF and the OBR

05/02/2014 UK Economic Review PAGE 3 OF 4

Bottom line: Overall, last month’s data releases provide further evidence that the UK economy is recovering well and supports our view that UK GDP will surpass its pre-recession peak in the second half of this year. However, more must be done to secure the recovery, including more support for exporters and improved access to finance.

For more information please contact: Suren Thiru, UK Economist. Email: [email protected]. Tel: 020 7654 5801

For more information please contact: Suren Thiru, UK Economic Advisor. Email: [email protected]

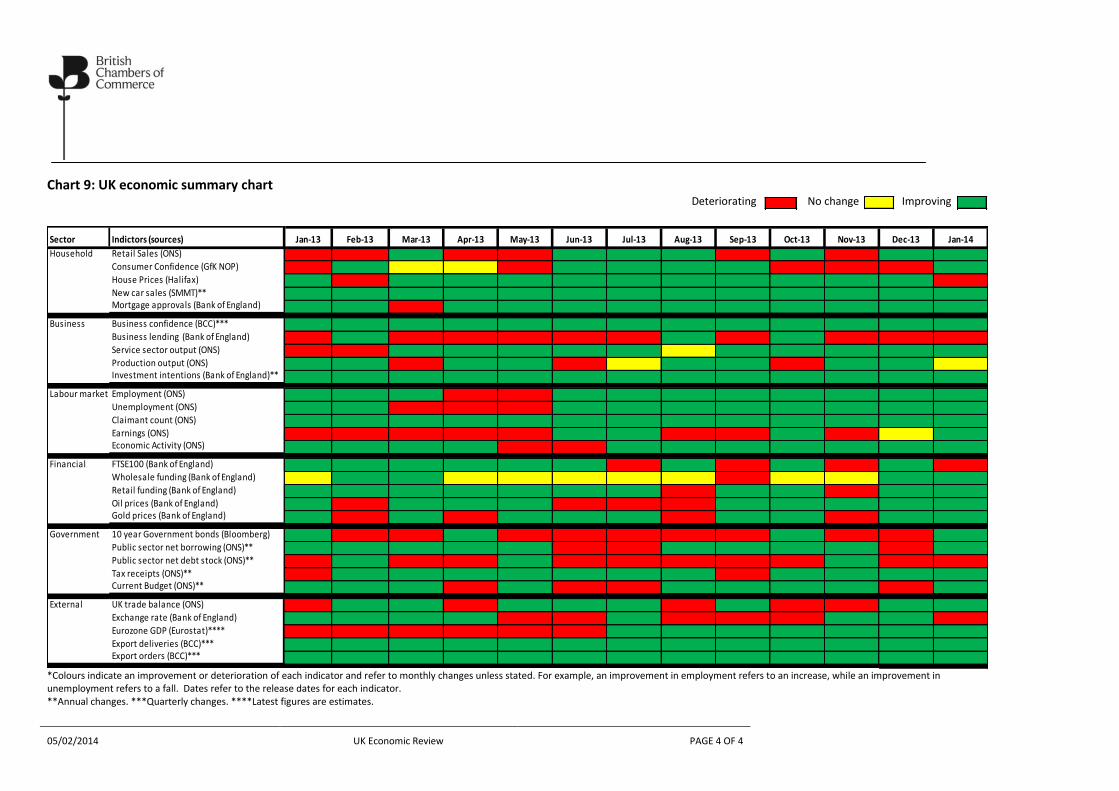

...an early interest rate rise is not expected.

Although the UK unemployment rate is now only

slightly above the 7% threshold, the minutes from the

latest Monetary Policy Committee (MPC) meeting

suggests that even when the unemployment rate falls

below 7%, the committee sees no immediate need to

increase interest rates. This is because with inflation

now back on target (see Chart 5) and earnings growing

by less than inflation (see Chart 6), there is plenty of

scope for interest rates to remain at their current

level. The BCC currently expects that interest rates

will start to rise towards the end of 2015.

While the UK's trade deficit remains large...

Though still large by historical standards, the UK's

trade deficit narrowed slightly in November to £3.2

billion, from the upwardly revised deficit of £3.5 billion

in October (see Chart 7). A trade surplus of £6.2 billion

on services was more than offset by a deficit of £9.4

billion on goods. Although exports of goods to

countries within the EU rose in November to £12.8

billion, imports from the EU rose to £19.2 billion over

the same period, a record high. Much of this increase

in imports will have been due to the UK economy

growing faster than most of its EU trading partners,

and imports tend to rise in such circumstances.

...the better global outlook should aid UK trade

In addition to raising its UK GDP forecast (see Table 1),

the IMF has upgraded its forecast for global GDP

growth for 2014 to 3.7%, up slightly from its previous

estimate of 3.6% published in October 2013. The IMF

also raised its 2014 GDP forecast for the Eurozone, the

UK’s major trading partner, from 0.9% to 1.0%. The US

economy is now expected to grow by 2.8% rather than

2.6% in 2014. (see Chart 8). However, risks to the

global recovery remain, including the potential impact

of the early withdrawal of economic stimulus

measures by advanced economies such as the US.

-8

-6

-4

-2

0

2

4

6

Sep

-No

v 2

00

8

Dec

-Feb

20

09

Mar

-May

20

09

Jun

-Au

g 2

00

9

Sep

-No

v 2

00

9

Dec

-Feb

20

10

Mar

-May

20

10

Jun

-Au

g 2

01

0

Sep

-No

v 2

01

0

Dec

-Feb

20

11

Mar

-May

20

11

Jun

-Au

g 2

01

1

Sep

-No

v 2

01

1

Dec

-Feb

20

12

Mar

-May

20

12

Jun

-Au

g 2

01

2

Sep

-No

v 2

01

2

Dec

-Feb

20

13

Mar

-May

20

13

Jun

-Au

g 2

01

3

Sep

-No

v 2

01

3 %

Chart 6: Real earnings growth

Real earnings growth Annual earnings growth CPI inflation

-5

-4

-3

-2

-1

0

1 2

00

3 N

OV

20

04

NO

V

20

05

NO

V

20

06

NO

V

20

07

NO

V

20

08

NO

V

20

09

NO

V

20

10

NO

V

20

11

NO

V

20

12

NO

V

20

13

NO

V

Bill

ion

s £

Chart 7: UK's Net Trade Position

0

1

2

3

4

5

6

7

8

An

nu

al C

han

ge %

Chart 8: IMF GDP Forecasts, 2014

Oct-13

Jan-14

Source: ONS Labour Market Statistics, January 2014

Source: IMF World Economic Outlook Update, January 2014

Source: ONS UK Trade, November 2013

05/02/2014 UK Economic Review PAGE 4 OF 4

Chart 9: UK economic summary chart Deteriorating No change Improving

*Colours indicate an improvement or deterioration of each indicator and refer to monthly changes unless stated. For example, an improvement in employment refers to an increase, while an improvement in unemployment refers to a fall. Dates refer to the release dates for each indicator. **Annual changes. ***Quarterly changes. ****Latest figures are estimates.

Sector Indictors (sources) Jan-13 Feb-13 Mar-13 Apr-13 May-13 Jun-13 Jul-13 Aug-13 Sep-13 Oct-13 Nov-13 Dec-13 Jan-14

Household Retail Sales (ONS)

Consumer Confidence (GfK NOP)

House Prices (Halifax)

New car sales (SMMT)**Mortgage approvals (Bank of England)

Business Business confidence (BCC)***

Business lending (Bank of England)

Service sector output (ONS)

Production output (ONS)Investment intentions (Bank of England)**

Labour market Employment (ONS)

Unemployment (ONS)

Claimant count (ONS)

Earnings (ONS)Economic Activity (ONS)

Financial FTSE100 (Bank of England)

Wholesale funding (Bank of England)

Retail funding (Bank of England)

Oil prices (Bank of England)Gold prices (Bank of England)

Government 10 year Government bonds (Bloomberg)

Public sector net borrowing (ONS)**

Public sector net debt stock (ONS)**

Tax receipts (ONS)**Current Budget (ONS)**

External UK trade balance (ONS)

Exchange rate (Bank of England)

Eurozone GDP (Eurostat)****

Export deliveries (BCC)***Export orders (BCC)***