Embed Size (px)

Citation preview

The Financial Wellbeing of the Birmingham Community

Brenda Spencer, Community Banking Manager,

Adrian Oldman, Head of Partnership Development

Citysave Credit Union

31st July 2013

About Citysave Credit UnionBirmingham-based, established for 25 yearsRun by members for the benefit of our 10,000

members and here to support them and our communities

Promote responsible borrowing and financial wellbeing

No sales culture & no penal charges High volunteer presence – workplace and

community Fully regulated by FCA & PRALiquidity of 50% and capital of 15% Deposits covered by the FSCS

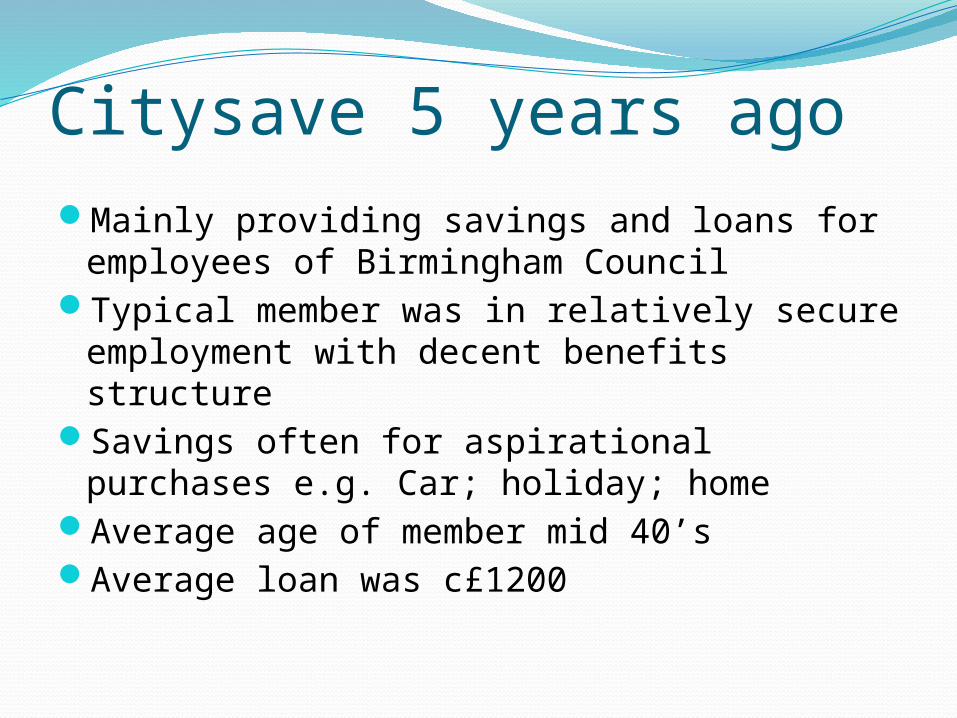

Citysave 5 years agoMainly providing savings and loans for

employees of Birmingham CouncilTypical member was in relatively secure

employment with decent benefits structureSavings often for aspirational purchases e.g.

Car; holiday; homeAverage age of member mid 40’sAverage loan was c£1200

A changing world Citysave now provide payroll deduction

schemes in c50 organisations – mainly public sector & NHS

50% of members save through payroll deduction

30% save through benefits – including DLA; Child benefit; pension; income support;

All members expected to have a savings plan from £2 per month

Average age of member has fallen to mid/late 30’s

Average loan size has fallen to <£700We have active outreach programme across

the cityOffice is open 6 days a week and 44.5 hours a

week

Citysave todaySegmented our loan book for better member

serviceMax turnaround on loans 24 hours (full

assessment)Most loans are instant (profiled for members)Same number of staff issue >2x loans issued

5yrs agoWe survey all loans to monitor service and

feedback: 96% of members rate us as excellent98% would recommend us to family / friends

Loan book is growing (not as fast as our savings!)

Bad debts reduced (net cost currently c2.7%)Loan income is c80% up in 4 years – and is

the basis for our sustainable organisation

The need to do more:9m adults without fit for purpose banking

solutionHome credit & mail order £3bn & growingArrears on utilities - £637m risen 33% in 12

months100k on prepayment meters in BirminghamArrears on rent and mortgages common High cost, highly promoted and easy access

payday lending sector now worth est £2bnGrowth in Payment cards such as Paypal &

Paypoint JRF report 2013 on Poverty Premium is that it is rising and now 10% of household income

Birmingham 2013Birmingham has 187 identified communities – Super

DiverseHighest %age of under 25’s in EU Significant numbers working part time or flexible

hours, and zero hours contract commonSubstantial need for financial services that overcome

barriers to including language, literacy, confidence, trust

Need to reach into different communities through different media efficiently

Different levels of vulnerability means a need to deliver a wider range of products to a wider range of membership

Need for supportive products – solutions must be high impact as well as low cost

Predators in our midstHigh cost lenders widely established9 Money Shops alone in the cityEasy access, attractively packaged and highly

promotedCost is high in both interest and feesEasy rollover and debt grows rapidly Low visibility & barriers to redemptionOften don’t show on credit searches Responsible lenders working harder to assess

loansRapid growth in debt interventions, debt

management plans and debt relief orders showing clear adverse impact on those we seek to support

Welfare Reform Local Housing allowance 28,600 £32mUnder Occupation 15,000 £10.1mNon dependent deductions7,100

£8mHousehold benefit cap 1,350

£6.5mCouncil Tax Benefit 88,000 £13mDisability Living Allowance 10,100

£30mIncapacity Benefits 26,200 £92mChild Benefit 143,100 £51mTax Credits 113,300 £92m1% uprating £85mTotal impact for Birmingham

£419m

Citysave’s CommitmentCommitted stakeholder in the FairBrum

campaign with our specialism being financial inclusion

Our mission is to: Inform on the issues of the day in a

responsible and coherent mannerTo provide constructive and joined up

solutions As part of this we are holding a series of events

entitledThe Financial Wellbeing of the Birmingham

Community

Focused and informative events Event 1: understanding and removal of the poverty

premium; Event 2: Identifying and tackling financial stress;

Birmingham Fair MoneyWe are partnering widely with CU’s and

CDFI’s promoting an alternative We are delighted to welcome Moneyline

moving in from September to offer loans from £50 - £300 in a responsible manner

Working with local authority to be disruptive to payday lending in the autumn period

[email protected] campaign www.citysavehome.org.uk info blog

Help needed to support our workRegulation of high cost lending sector Easier redemption of this lendingMore visibility to other lenders ie we would

ask for the same easy access register of higher cost lending that is in US – to allow us to quickly analyse small, instant loans for non members

Transparency of lending & financial services in our city

We need a more even playing field

Local supportBirmingham Council are being hugely

supportive of our workLooking at how we can tackle the impact

on individual households because of predatory & high cost lending

Assisting promotion to overcome the imbalance in marketing budgets

The council has also committed to using all available information from banking disclosure to inform and develop a better response in the city

& to campaign for all the information we need to allow us to do better with the resources we have

Cllr John Cotton – #FairBrum

Community Banking ServiceRange of accounts from 50p per weekNo hidden /penal costsHigh quality visa card High visibility – New integrated web site with

access; monthly statements & text balancesFrom 16+No credit check required24/7 Emergency Advice Service – legal,

medical and debt

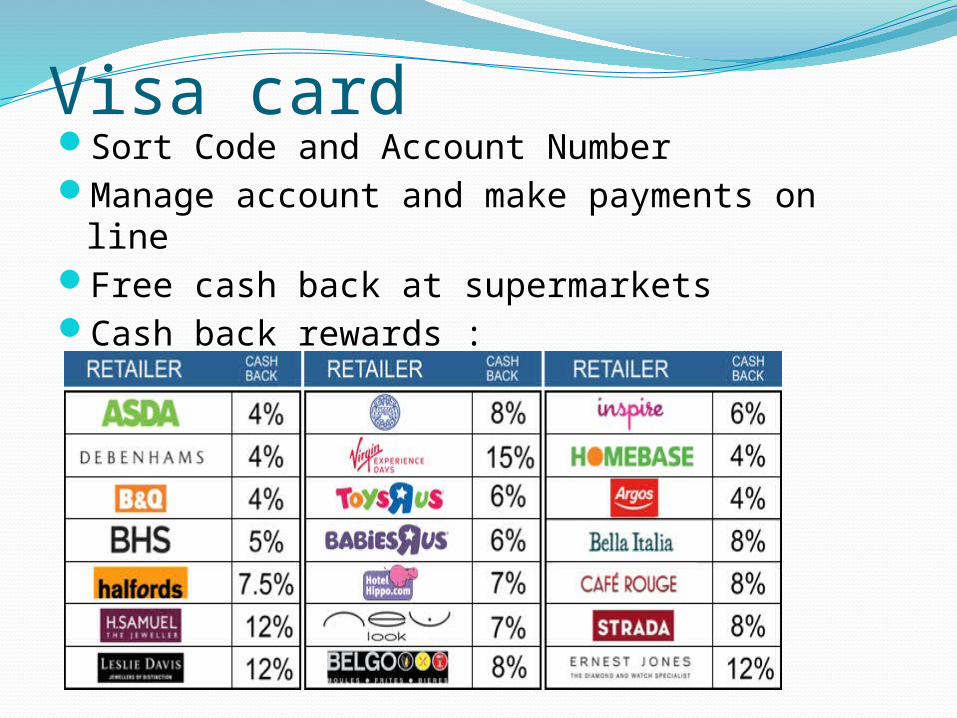

Visa cardSort Code and Account NumberManage account and make payments on lineFree cash back at supermarketsCash back rewards :

Partnering to drive out cost and increase accessibility: Care Sector, support and intervention

agenciesHousing providersEmployers and welfare to workCouncilsUtilities

Trusted PartnersPermission for another trusted organisation

to open accounts for their employees, tenants, customers, clients

Account opening is done at partner locationsBy authorised and trained staffID is taken and verified Overcomes all barriers to account

opening

A Trusted Partner App has been developed to simplify this

Service Centre On BoardingAccounts come into the centre from kiosk,

web site or Trusted Partner appA call is made from service centre within 24

hours Explain our service & T&C’sSet up payments in and out if requiredSet up savings planOrder cardSend welcome packDiary for next contact Relationship management – ie regular,

proactive and multi media information – texting, email, blog, in writing and phone

Invested in Kiosk networkTouch screen, and easy to navigateHigh functionality provides access to Citysave account/services& other key partners for financial inclusion and

literacyDiscreet source of help, advice and supportconfidential and free to use

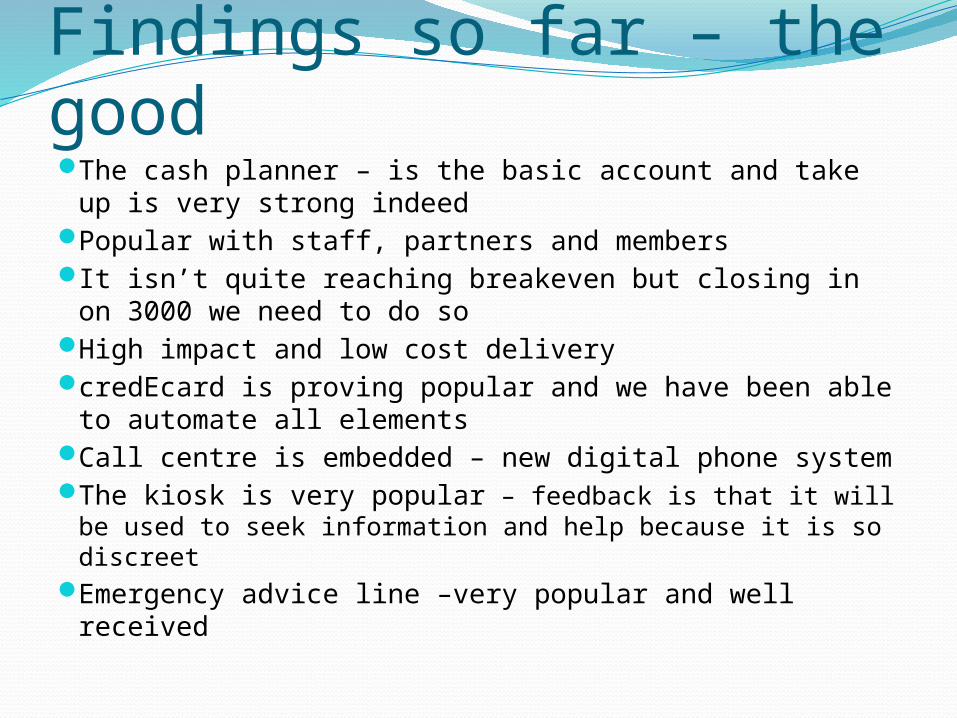

Findings so far – the goodThe cash planner – is the basic account and take up is

very strong indeed Popular with staff, partners and membersIt isn’t quite reaching breakeven but closing in on

3000 we need to do soHigh impact and low cost deliverycredEcard is proving popular and we have been able

to automate all elementsCall centre is embedded – new digital phone system The kiosk is very popular – feedback is that it will be

used to seek information and help because it is so discreetEmergency advice line –very popular and well

received

But we have just reached the starting line....much more to doBudget account is too complex for those that

need itTakes time for us or our partners to explain

productFinancial literacy is very low The scale required is hugeLayering impact of Welfare Reform is starting

alreadyChanges in time scales Not easy to engage with utility providersIntervention agencies and local authorities

have funding cuts and other priorities

Creating real solutions...Cash planner is popular & so we move to that

being sole product ....with ‘bolt ons’ ie bill payment to council tax, rent or utility

Common concept allowing a simple base product solution with valuable added benefits

Commissioned an Action Research project with Centre for Responsible Credit to evaluate products, delivery, cost and its benefit to the users and other stakeholders

The output will inform and guide product development and scaling to meet the needs of a modern generation

Funding and support is provided by RBS Group

There are many ways to climb a mountain...Lots of options being trialledWe continue to evolve our solutions to best

meet the needs in our cityHappy to share our learning & learn from

othersWill be fed in through Damon & the Centre

for Responsible Credit

Thank you