Embed Size (px)

Citation preview

All details given in good faith but without guarantee Deep Sea Tankers +44 (0)20 7535 2626 Dry Cargo Chartering +44 (0)20 7535 2666 Container Chartering +44 (0)20 7535 2867

W

ee

kly

Cha

rte

ring R

epo

rt

Braemar Seascope Thursday, 17 January 2013

Market Indicator Wet* 16-Jan-13 Dec Avg Avg YTD 2012 Avg

TCE ( US $ / Da y ) TCE ( US $ / Da y ) TCE ( US $ / Da y ) TCE ( US $ / Da y )

260,000 NHC AG/EAST TD3 7,500 16,000 7,500 11,000

130,000 NHC WAFR/USAC TD5 5,000 10,500 8,000 12,000

80,000 NHC NSEA/CONT TD7 4,500 10,500 6,000 7,500

55,000 CLN AG/JAPAN TC5 7,000 20,000 11,500 8,500

37,000 CLN CONT/USAC TC2 16,500 15,500 18,500 10,000

38,000 CLN CARIB/USAC TC3 11,000 13,000 10,000 9,500

* All rates based on benchmark Baltic Exchange speed and consumption f igures

Dry 16-Jan-13 Dec Avg Avg YTD 2012 Avg

BDI 781 856 744 920

BCI 1,431 1,584 1,362 1,573

BPI 754 858 722 963

BSI 738 749 740 904

Container 14-Jan-13 Dec Avg Avg YTD 2012 Avg

B O X i 53.55 53.91 53.65 55.76

Financial 16-Jan-13 Dec Avg Avg YTD 2012 Avg

BRENT CRUDE US$/bbl 111.20 109.09 111.63 111.81

IFO 380 ROTT US$/tonne 610.50 581.47 609.32 640.97

YEN/US$ 88.65 83.11 88.10 79.70

WON/US$ 1,059 1,077 1,060 1,123

US$/EURO 1.33 1.31 1.32 1.34

Braemar Seascope Weekly Chartering Report 2

17/01/2013

Cru

de C

hart

ering

VLCC The transition to the 2013 Worldscale rates has helped charterers reduce rates further. S-oil quoted their 2-4 Feb cargo from AG to S Korea basis asking for offers in the new flat rates. The result was around seven offers and a friendly neighbour owner who decided to take rates below the ws40.0 mark. The fixture, at 274kt x ws38.25, shows a TCE at around US$14,000/day, which is more than US$4,000/day less than others have fixed on the new flats. Nevertheless, the ship is over 15 years old now and in order to find employment, a discount is offered to seduce the charterers. Having said that, the view from many was soft and predicted the charterers to take a couple of points off the board down to ws40.0. Breaking it, however, was not predicted. Earlier in the week, there has been a great mix of old and new Worldscale fixing, with charterers benefiting from cargoes being drip-fed, leaving owners with a slim chance of improving rates, even with an increased volume of cargoes towards the end of this week. A few of the owners who fixed earlier this week did manage to cherry pick the cargoes of choice, especially a Scandinavian fleet that took out three Japanese cargoes at better numbers, thanks to the tougher restrictions at discharge ports and charterers having to take a more careful approach. With the last done now back down below an important physiological barrier, we can assume that a lot of the independent owners out there will try and maintain a firm stance on fixing, saying no thank you to sub-ws40.0 levels, leaving the eternal struggle between owners and charterers in such a poor market. It is always a hard task to follow this particular South Korean charterer as time after time they manage to find the bottom; very few find the strength to push it down further. It was a week of limited activity in West Africa. Unipec continue to be relatively quiet from the region and the tonnage list continues to face constant pressure from the ever present 'eastern ballasters'. As a result, sentiment in West Africa is softening slowly but steadily, as charterers drip-feed cargoes into the market. The established rate of ws46.5 was broken by Day Harvest, who fixed W Africa/China at ws44.0 (2012), which equates to approximately ws41.0 basis the 2013 flat rate. The number of cargoes for the first half of February has been on the lower side and we expect to see more activity in the region for the second half of the month. This limited activity in the first half was also reflected by the Indian charterers as IOC entered for their first West Africa cargo for 16-17 Feb dates. Charterers received up to seven offers for the cargo and fixed the business at US$3.425m for WC India discharge. It is interesting to note that this vessel has been spot in the Atlantic for approximately a month already, and has to wait another month for the IOC laycan. We are assessing W Africa/WC India at US$3.45m and W Africa/EC India at US$3.7m. In the Caribbean, Reliance are already fixing well into second decade of February, while Petrochina are still reported to be working their first decade barrels from the region. There is sufficient tonnage available in the Caribbean for the second decade of Feb for charterers to choose from. However, charterers still looking to cover their first decade cargoes may have to pay slightly above the established levels for Caribs/WC India and Caribs/East. On the Continent this week, the Mesdar fixed Unipec for a Skaw/Ningbo cargo at US$5.25m, however the subjects did not materialise. We expect the activity in this region to begin next week for February laycans as charterers will have a clearer picture on tonnage opening up on the Continent, once vessels fixed west have received their form discharge orders. The 30 day availability index shows 61 VLCCs arriving at Fujairah, of which six are over 15 years old, compared to 62 last week. With January pretty much covered and first decade of February well on the way, we probably have another ten to fifteen cargoes in the 1-10 window to go, a large number of the 20 fixed stems done on Chinese/Chinese contracts keeping the position lists unchanged. The pressure is surely on owners at this time to make sure they hold their heads above the water. The bunker price today is US$618.5/tonne, down US$8.5 from last week. The freight rate for 280,000mt AG/USG is ws23.75 (2012), same as last week, so owners' earnings are: Assuming one way, this equates to US$22,000/day (US$30,000/day last week)* Round Trip Cape Laden/Suez Ballast US$-15,800/day (US$-8,000/day last week)* The freight rate for 270,000mt is ws40.0, down ws6.0 from last week, so owners' earnings are: Round Trip Ras Tanura/Ulsan US$15,700/day (US$18,600/day last week)* *Obviously with slow steaming these daily earnings can be improved.

Route Size Load Discharge Today’s Assessment Last Week’s Average

TD1 280,000 Ras Tanura LOOP ws22.0 ws23.0

TD2 265,000 Ras Tanura Singapore ws40.0 ws42.0

TD3 265,000 Ras Tanura Chiba ws40.0 ws42.0

TD4 260,000 Bonny LOOP ws42.5 ws44.5

TD15 260,000 West Africa China ws41.0 ws42.0

China41%

Korea-Japan24%

India10%

Med/Red Sea11%

NW Europe7%

USA4%

Spore/Indo3%

VLCC AG Weekly Spot Fixtures by VolumeIntended Discharge (10 - 16 Jan 2013)

Long East74%

Short East19%

West7%

VLCC AG Monthly Spot Fixtures by VolumeFinal Destination (Dec 2012)

Cru

de C

hart

ering

Braemar Seascope Weekly Chartering Report 3

17/01/2013

This week saw the conversion from 2012 to 2013 Worldscale flat rates, which may have led to some confusion as to where rates stood. Rates in West Africa continued their depression this week, with market levels quite firmly centred around ws57.5 UKC-Med late on and the usual differentials. An early double fixture by one charterer was reported at ws57.5 for USAC, which set the tone for the week. Subsequently, ws58.75 and then ws57.0 fixed to UKC-Med, with a shorter voyage to Portugal at ws59.0 also featuring. In the end, the market settled on ws57.5 for UKC-Med. Rates to the Far East followed the trend, with a relatively cheap ws62.0 being fixed to Singapore and US$2.15m for W Africa/Mangalore. The dates have firmly moved into the middle of February, with most of January being covered. There were a couple of late cargoes that met some resistance but off natural fixing dates the list looks ample. With ws57.5 UKC-Med being the established rate, it looks a safe bet to suggest that rates are bottoming slightly. The levels of activity for the rest of this week and early next week will determine the future direction of this market. It was a relatively quiet start to this week as charterers took stock in the Mediterranean after the first full week of fixing. By the time that fixing started, cross-Med was being done at ws70.0 with ws65.0 to UKC. The trans-Atlantic rates followed West Africa very closely, with ws50.0 USG being done a couple of times. Eastbound we saw US$2.75m to Singapore and US$3.2m to China. The Black Sea dates moved from end January firmly into February, and there was a decent level of fixing done in the first decade. The delays in the straits dropped from five days northbound to three days, although they were closed at the time or writing. This did nothing to help the sentiment, and charterers managed to drive rates down to 135kt x ws60.0 for UKC-Med of the pro rate of that. The North Sea and Baltic has been reasonably busy, with ws62.5 USAC and ws60.0 USG, and represents the one market that was busier than usual this week. There was good level of enquiry from Tallinn, which has attracted the interest of Continent ships. Whether this will take away tonnage from the West African or Med markets remains to be seen. With foreboding forecasts for European weather, perhaps owners will gain some respite from the frostbite this week, though position lists do remain healthy. Meanwhile, the AG continued its downward trajectory regarding westbound cargoes, falling another 2.5 points off to ws32.5 Med. Life was not so dire headed east, with ws65.0 fixed to the Philippines, not far off last week's levels, with 125kt x ws80.0 WC India and 131 EC India equally reasonably. But EC India dropped off to 123kt x ws74.0 later in the week, and ws72.5 to Thailand on 2012 rates represented levels consistent with the earlier Philippines fixture. A large list at first glance can be shortened by eliminating ballasters, but there is still plenty of choice for charterers who wish to shop around. Impending weather delays in the Med may push rates up there, which is likely influencing the low market levels for westbound cargoes as owners try to move their ships into the stronger markets

Suezmax

NW Europe46%

USA27%

W Africa18%

India East9%

Suezmax WAFR Weekly Spot Fixtures by VolumeIntended Discharge (10 - 16 Jan 2013)

Route Size Load Discharge Today’s Assessment Last Week’s Average

TD5 130,000 Bonny Philadelphia ws57.5 ws59.5

TD6 135,000 Novorossiysk Augusta ws60.0 ws61.5

135,000 Mediterranean UK Cont ws65.0 ws65.0

135,000 North Sea US Gulf ws60.0 ws60.0

135,000 Ras Tanura South East Asia ws65.0 ws65.0

W Africa27%

Med/Red Sea20%

AG15%

Black Sea11%

NW Europe10%

Carib/EC Mex8%

USA5%

Korea-Japan2% India

2%

Suezmax Weekly Spot Fixtures by VolumeLoad Area (10 - 16 Jan 2013)

Braemar Seascope Weekly Chartering Report 4

17/01/2013

Cru

de C

hart

ering

Aframax

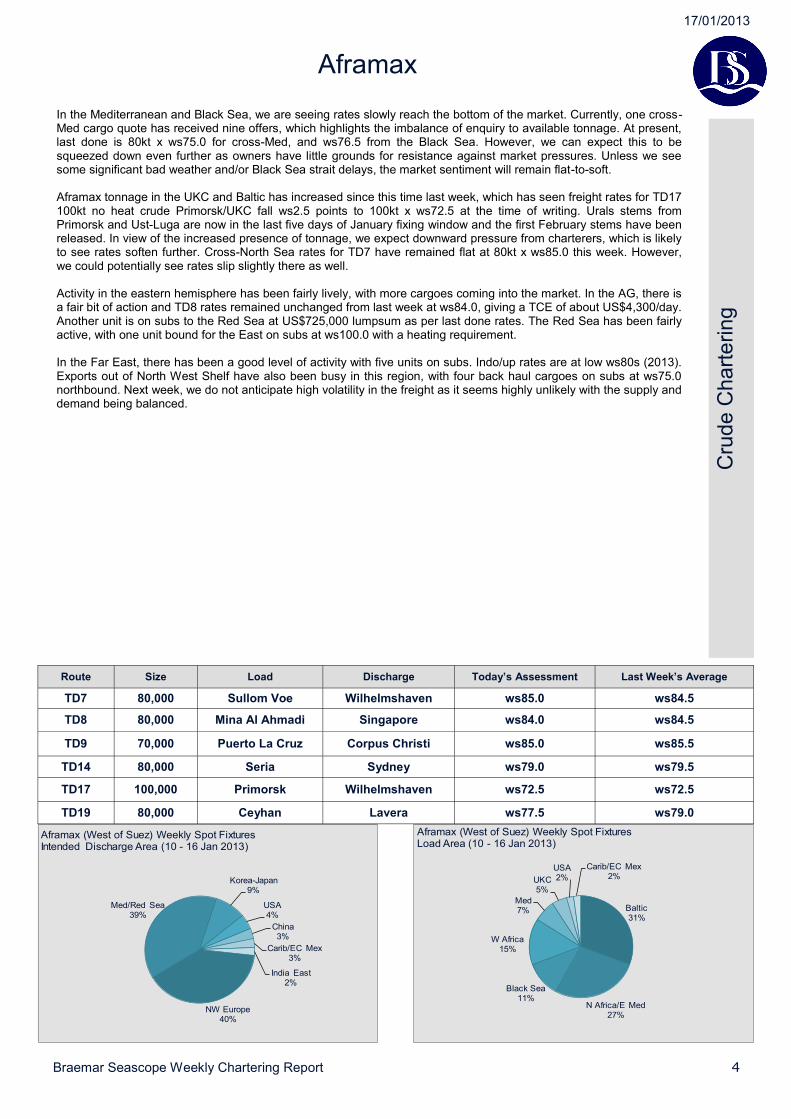

In the Mediterranean and Black Sea, we are seeing rates slowly reach the bottom of the market. Currently, one cross-Med cargo quote has received nine offers, which highlights the imbalance of enquiry to available tonnage. At present, last done is 80kt x ws75.0 for cross-Med, and ws76.5 from the Black Sea. However, we can expect this to be squeezed down even further as owners have little grounds for resistance against market pressures. Unless we see some significant bad weather and/or Black Sea strait delays, the market sentiment will remain flat-to-soft. Aframax tonnage in the UKC and Baltic has increased since this time last week, which has seen freight rates for TD17 100kt no heat crude Primorsk/UKC fall ws2.5 points to 100kt x ws72.5 at the time of writing. Urals stems from Primorsk and Ust-Luga are now in the last five days of January fixing window and the first February stems have been released. In view of the increased presence of tonnage, we expect downward pressure from charterers, which is likely to see rates soften further. Cross-North Sea rates for TD7 have remained flat at 80kt x ws85.0 this week. However, we could potentially see rates slip slightly there as well. Activity in the eastern hemisphere has been fairly lively, with more cargoes coming into the market. In the AG, there is a fair bit of action and TD8 rates remained unchanged from last week at ws84.0, giving a TCE of about US$4,300/day. Another unit is on subs to the Red Sea at US$725,000 lumpsum as per last done rates. The Red Sea has been fairly active, with one unit bound for the East on subs at ws100.0 with a heating requirement. In the Far East, there has been a good level of activity with five units on subs. Indo/up rates are at low ws80s (2013). Exports out of North West Shelf have also been busy in this region, with four back haul cargoes on subs at ws75.0 northbound. Next week, we do not anticipate high volatility in the freight as it seems highly unlikely with the supply and demand being balanced.

NW Europe40%

Med/Red Sea39%

Korea-Japan9%

USA4%

China3%

Carib/EC Mex3%

India East2%

Aframax (West of Suez) Weekly Spot FixturesIntended Discharge Area (10 - 16 Jan 2013)

Baltic31%

N Africa/E Med27%

Black Sea11%

W Africa15%

Med7%

UKC5%

USA2%

Carib/EC Mex2%

Aframax (West of Suez) Weekly Spot FixturesLoad Area (10 - 16 Jan 2013)

Route Size Load Discharge Today’s Assessment Last Week’s Average

TD7 80,000 Sullom Voe Wilhelmshaven ws85.0 ws84.5

TD8 80,000 Mina Al Ahmadi Singapore ws84.0 ws84.5

TD9 70,000 Puerto La Cruz Corpus Christi ws85.0 ws85.5

TD14 80,000 Seria Sydney ws79.0 ws79.5

TD17 100,000 Primorsk Wilhelmshaven ws72.5 ws72.5

TD19 80,000 Ceyhan Lavera ws77.5 ws79.0

Braemar Seascope Weekly Chartering Report 5

17/01/2013

Cru

de T

anker

Su

mm

ary

-20,000

-10,000

0

10,000

20,000

30,000

40,000

50,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TD3 - 260 - Ras Tanura - Chiba TCE

2011

2012

2013

0

10,000

20,000

30,000

40,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TD5 - 130 - Bonny - Philadelphia TCE

2011

2012

2013

0

10,000

20,000

30,000

40,000

50,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TD7 - 80 - Sullom Voe - Wilhelmshaven TCE

2011

2012

2013

-5,000

5,000

15,000

25,000

35,000

45,000

55,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TD9 - 70 Puerto La Cruz- Corpus Christi TCE

2011

2012

2013

Braemar Seascope Weekly Chartering Report 6

17/01/2013

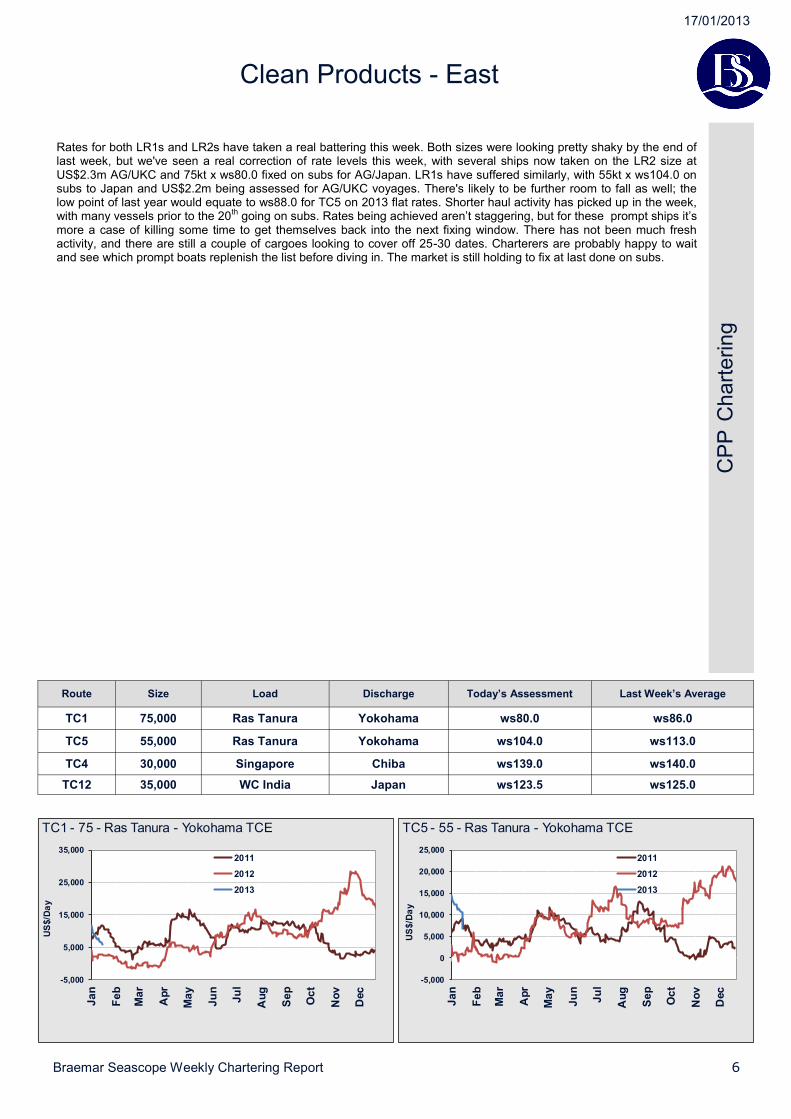

Rates for both LR1s and LR2s have taken a real battering this week. Both sizes were looking pretty shaky by the end of last week, but we've seen a real correction of rate levels this week, with several ships now taken on the LR2 size at US$2.3m AG/UKC and 75kt x ws80.0 fixed on subs for AG/Japan. LR1s have suffered similarly, with 55kt x ws104.0 on subs to Japan and US$2.2m being assessed for AG/UKC voyages. There's likely to be further room to fall as well; the low point of last year would equate to ws88.0 for TC5 on 2013 flat rates. Shorter haul activity has picked up in the week, with many vessels prior to the 20th going on subs. Rates being achieved aren’t staggering, but for these prompt ships it’s more a case of killing some time to get themselves back into the next fixing window. There has not been much fresh activity, and there are still a couple of cargoes looking to cover off 25-30 dates. Charterers are probably happy to wait and see which prompt boats replenish the list before diving in. The market is still holding to fix at last done on subs.

CP

P C

hart

ering

Clean Products - East

-5,000

5,000

15,000

25,000

35,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TC1 - 75 - Ras Tanura - Yokohama TCE

2011

2012

2013

-5,000

0

5,000

10,000

15,000

20,000

25,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TC5 - 55 - Ras Tanura - Yokohama TCE

2011

2012

2013

Route Size Load Discharge Today’s Assessment Last Week’s Average

TC1 75,000 Ras Tanura Yokohama ws80.0 ws86.0

TC5 55,000 Ras Tanura Yokohama ws104.0 ws113.0

TC4 30,000 Singapore Chiba ws139.0 ws140.0

TC12 35,000 WC India Japan ws123.5 ws125.0

Braemar Seascope Weekly Chartering Report 7

17/01/2013

CP

P C

hart

ering

Clean Products - West

0

10,000

20,000

30,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TC2 - 37 - Rotterdam - New York TCE

2011

2012

2013

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

Ja

n

Fe

b

Ma

r

Ap

r

Ma

y

Ju

n

Ju

l

Au

g

Se

p

Oc

t

No

v

Dec

US

$/D

ay

TC3 - 38 - Aruba - New York TCE

2011

2012

2013

Route Size Load Discharge Today’s Assessment Last Week’s Average

TC2 37,000 Rotterdam New York ws160.0 ws167.5

TC3 38,000 Aruba New York ws130.0 ws131.5

TC6 30,000 Skikda Lavera ws170.0 ws171.0

The UKC/USAC 37kt (TC2) market last Friday faltered as rates dipped below ws180.0 to ws177.5. This sentiment continued over the weekend into Monday, with rates quickly dropping through the ws160s as the week progressed, with ws160.0 on subs today. The overall outlook (or hope) is that this would be bottoming out. However, with the lack of confidence in the futures that we've seen, we now expect this – coupled with further tonnage ballasting into the area, and last palm ships looking a little uncomfortable – to result in a continued softening of rates. With cargo dates currently out till the end of the month, owners will certainly be hoping for more enquiry next week. Handy and Flexi tonnage has continued to be gainfully employed, with little drop off to speak of. Ice tonnage remains at 22kt x ws235.0-ws245.0 (slightly soft) and 30kt x ws185.0 (steady). Non-ice is only slightly below these levels. The outlook still good as ice continues through the Baltic. The Mediterranean market has been relatively steady at 30kt x ws170.0 for this week, and expectations are that this will continue into next week. Stateside, the market peaked around ws115.0, with vessels being replaced by charterers as delays in Mexico, Venezuela and Puerto Moin tied up discharging vessels. Tonnage remains tight up to 23 rd-24th January, but more vessels are available afterwards. Rates are now around 38kt x ws105.0 USG/trans-Atlantic. There is also interest in naphtha cargoes USG/East as the arbitrage looks open for now, which may keep the market tight for the balance of January. At the time of writing, TC14 FFAs for February traded down at ws87.0 before be bought back to ws89.0 level.

17/01/2013

Dry

Carg

o C

ha

rtering

Braemar Seascope Weekly Chartering Report 8

Another roller coaster week in the Capesize market as the sentiment bottoms and recovers in the Pacific, but activity in the Atlantic keeps sentiment positive. In the Pacific, poor weather off West Australia caused a significant slowdown in the market. As a result of a lack of cargo from the majors, rates dropped down to US$6.70/tonne. Patience paid off for some owners as the return of the majors saw the market rise up to mid-US$7s/tonne just as quickly as it dropped; with a constant flow of cargo the market could continue to push considerably. The Atlantic market has been more consistent than the Pacific as the sentiment has not changed, but the rate has pushed a lot higher. The lack of ballasters sailing prior to Christmas due to a lack of cargo seems to be causing a slight squeeze now for those charterers with January cancelling cargo. Rates now being talked of are in excess US$19.00/tonne for Tubarao/Qingdao and could improve further. With trans-Atlantic trading around US$10,000/day, not many owners will be too keen to leave the Atlantic basin. A few vessels have been reported for short period fixing this week, but little details have emerged. With the potential of more cyclones in the coming months, we believe re-letting for a few months may not be such a bad idea.

Capesize

0

2,000

4,000

6,000

8,000

10,000

-25,000

0

25,000

50,000

75,000

100,000

125,000

Jan

-09

Ap

r-09

Ju

l-0

9

Oc

t-0

9

Jan

-10

Ap

r-10

Ju

l-1

0

Oc

t-1

0

Jan

-11

Ap

r-11

Ju

l-1

1

Oc

t-1

1

Jan

-12

Ap

r-12

Ju

l-1

2

Oc

t-1

2

Jan

-13

BC

I

US

$/d

ay

The Baltic Capesize Index vs Atlantic & Pacific Earnings

Atlantic Pacific BCI

Dry

Carg

o C

ha

rtering

17/01/2013

The positive sentiment of last week in the Pacific has evaporated this week as new tonnage kept entering the market, with very little business showing. Furthermore, Indonesian mines are flooded, with some places under three metres of water, and stockpiles at the ports are now running low. A modern Kamsarmax fixed two years period at US$9,000/day, whilst there has been plenty of activity in the short period market, with index types fixing around US$7,000/day. Prior to Chinese New Year, we traditionally see the market pick up but it's unlikely to happen now. With most of January front-haul requirements having been covered and few fresh cargo requirements entering the market, the Atlantic is continuing its subdued trend from last week. Much of the business focus is on the EC S America grain market, and a number of forward freights for March and April dates have already been booked in by head grain shippers in the past week as operators re-adjusted their freight ideas in the face of weakening market prospects. With Chinese New Year holidays in early February and the number of ballasters from the Pacific on the increase, the outlook for next week remains weak.

Braemar Seascope Weekly Chartering Report 9

Panamax

0

1,000

2,000

3,000

4,000

5,000

6,000

0

10,000

20,000

30,000

40,000

50,000

60,000

Jan

-09

Ap

r-09

Ju

l-0

9

Oc

t-0

9

Jan

-10

Ap

r-10

Ju

l-1

0

Oc

t-1

0

Jan

-11

Ap

r-11

Ju

l-1

1

Oc

t-1

1

Jan

-12

Ap

r-12

Ju

l-1

2

Oc

t-1

2

Jan

-13

BP

I

US

$/d

ay

The Baltic Panamax Index vs Atlantic & Pacific Earnings

Atlantic Pacific BPI

Dry

Carg

o C

ha

rtering

17/01/2013

Braemar Seascope Weekly Chartering Report 10

Supramax tonnage remains tight in the US Gulf as owners continue to build confidence for January. Don’t expect it to turn the other way anytime soon, but sentiment suggests the market is likely to stabilize. Some grains have been fixed to the Far East on eco tonnages at low US$18,000/day levels. A few Dolphin 57k Dwt type ships have been discussed at low US$14,000/day levels for a petcoke trip to the East Med. The market has gone from strength to strength this week in the South Atlantic as tonnage remains tight for mid/end January dates. Owners’ expectations have climbed accordingly, with Supramax levels for ships open West Africa having been quoted around US$15,000/day DOP for straight trips to Singapore/Japan range, with longer duration trips via EC S America and out around US$13,000-US$13,500/day DOP. Charterers with prompt requirements have been forced to pay up in order to secure tonnage from an active market. Owners have quoted short period levels for Atlantic redelivery a tick under US$14,000/day for EC S America delivery and around US$13,000/day for WW redelivery with WAF delivery. Handymax owners have also seen some impressive numbers, with rumours that an end January 48k Dwt vessel had seen US$13,000/day DOP for a straight trip to China. With tonnage looking to loosen as we move into early February and the Chinese New Year looming, it seems likely that market conditions will soon start to cool. Enquiries in the East Med remain few and far between this week, with a continued oversupply of tonnage being quoted in relation to available cargoes, maintaining the Med as an unappealing destination for many owners. We hear charterers talking on Supramaxes for short period delivery East Med at around US$9,500/day levels with WW redelivery and around US$8,500/day levels with Atlantic redelivery. Owners are aiming numbers starting with a ‘10’ in front. Trips out on the Japanese type Supramax are paying to AG around US$10,500/day levels, India US$10,000/day and CJK US$9,000/day. It was rumoured that a nice Japanese built 50k Dwt 2001 vessel spot East Med fixed a trip to Tema at US$6,500 daily; the ship is open and loading in Canakkale. Looking ahead, it seems likely that the Med market will remain difficult for owners throughout January. Supramax mineral cargoes ex-WC India to China have been concluded at upper US$7,000/day levels while iron ore trips to China on vessels coming open in Haldia/Paradip were traded/concluded at US$5,000-US$5,500/day levels. Supramax units basis delivery South Africa have been fixed around mid-US$8,000s/day plus US$280,000 BB for trips back to India, while South Africa/Far East trades have been concluded at low US$9,000s/day plus US$325,000 BB. No period fixtures have been reported for the area.

Handy/Handymax/Supramax

0

1,000

2,000

3,000

4,000

5,000

0

10,000

20,000

30,000

40,000

50,000

Jan

-09

Ap

r-09

Ju

l-0

9

Oc

t-0

9

Jan

-10

Ap

r-10

Ju

l-1

0

Oc

t-1

0

Jan

-11

Ap

r-11

Ju

l-1

1

Oc

t-1

1

Jan

-12

Ap

r-12

Ju

l-1

2

Oc

t-1

2

Jan

-13

BS

I

US

$/d

ay

The Baltic Supramax Index vs Atlantic & Pacific Earnings

Atlantic Pacific BSI

Braemar Seascope Weekly Chartering Report 11

17/01/2013

Rio Tinto iron ore output tops 2012 target Global miner Rio Tinto aims to boost iron ore output by 15% this year after production in 2012 climbed to 253m tonnes, beating its own guidance, as resurgent Chinese demand drives a price recovery. Rio Tinto, the world's second-biggest producer behind Brazil's Vale, has stuck to an aggressive expansion plan in iron ore driven by the hope of top buyer China underpinning prices. "Markets remain volatile, but our business continues to perform well," Rio Tinto Chief Executive Tom Albanese said in the company's fourth-quarter production report. Iron ore prices have soared more than 80% since September as Chinese steel mills -- the single biggest buyers of seaborne-traded ore -- returned to the market on signs of a recovery in the Chinese economy. Benchmark prices hit a 15-month high of US$158.50/tonne last week, as China's iron ore imports topped 70m tonnes for the first time in December helped by a resurgent economy and a cold snap that cut local production. Iron ore prices have started to retract, however, suggesting a peak in the recent cycle, though analysts are not expecting a return to sub-US$100/tonne levels that could threaten production from more marginal producers. India's NTPC sees up to 20m tonnes per annum coal imports in 2-3 years NTPC, India's largest power producer, expects to import up to 20m tonnes of coal annually in the next three fiscal years, a 25% rise from its 2012/13 purchases at the upper range, a senior company official said on Thursday. "What we see in the next two-three years is that we will be remaining at around 16-20m tonnes per annum," said N.N. Misra, director of operations at NPTC. The state utility has contracted to import 16.4m tonnes of coal in 2012/13, a third more than the previous year. Last year, NTPC had floated import tenders for 9.4m tonnes and 7m tonnes of coal to fuel its plants as local supplies trailed demand. "Deliveries are still going on," Misra said. In a clear sign of domestic supply lagging galloping demand, the country's thermal and coking coal imports jumped 73.6% in November from a year earlier. China’s grain surge neared 300% Larger price gaps between international and domestic markets drove a surge of nearly 300% in China’s grain imports during last year’s first 11 months, Beijing said. According to commerce ministry spokesman Danyang Shen, the widening price differences made Chinese groups more willing than in the past to place import orders. Over January-November 2012, imports of wheat, rice and corn rose 294.5% y-o-y to 10.775m tonnes, customs data indicated. “The prices in the international markets began to fall since March and April last year,” Shen said. “So the Chinese firms imported grains in large amount, while import prices stayed relatively lower.” For wheat, the average import price fell 9.4% y-o-y to US$299.3/tonne, with corn prices decreasing 3.2% on average, Shen added. Prices of imported rice posted the steepest fall, 26.5% y-o-y. Meanwhile, Chinese companies turned to the international market to restock corn, with the domestic supply tight and stock limited. Russia grain lobby says winter crop conditions tough Weather conditions have been difficult for Russia's winter grain crop due to dry conditions during sowing and to cold snaps in some regions in December, the head of Russia's Grain Union said on Wednesday. The conditions described by Grain Union head Arkady Zlochevsky are broadly similar to those of last winter, which preceded a fall in Russia's gross grain harvest to just over 70m tonnes in 2012 from 94m tonnes in 2011, though Zlochevsky cautioned it was too early to estimate the damage. "Of over 15m hectares sown (to winter grains), about 1.2m can be written off because of dry weather conditions. They just did not sprout," he told a news conference. "They will be re-sown to spring grain." India reaps reward of bumper wheat crops as world exports shrink India is poised to triple wheat exports this year to a higher-than-expected, record 6m tonnes, helping plug a shortfall in lower-quality grain supplies and keep a lid on global prices. Five years of bumper harvests have created unruly, large stockpiles of wheat in India at a time when Australia and Russia, the world's second and third largest exporters, face shrinking production due to adverse weather. The amount India is set to export is paltry in a global trade of nearly 140m tonnes, but it will fulfil the needs of the biggest buyers of lower-quality wheat in the Middle East and Africa as global supplies ease.

Asia

/ A

ustr

alia

Mark

et N

ew

s

Asia / Australia News

Conta

iner

Chart

ering

17/01/2013

Braemar Seascope Weekly Chartering Report 12

As expected, there was a notable pick up in business this week with a number of fresh fixtures concluded, in addition to numerous enquiries from lines starting to implement their chartering strategies for 1Q 2013 and beyond. In spite of this resumption of activity, there is a noticeable deviation in fortunes between regions and across the size brackets, and whilst many sectors have simply moved sideways, the significant exposure in the mid sizes and in the Far East continues to squeeze rates further, hence the slight decrease to our index. For the Post-Panamax sector, the year has started where 2012 left off, and whilst there is certainly still an element of demand from a handful of large liner companies, rates are still failing to ignite in spite of the increasingly short supply. This is being further compounded by the withdrawal and reintegration of numerous short-term relets. Rumours therefore, that two major lines have entered a vessel sharing agreement to satisfy one line's long standing requirement for 6500teu tonnage does not come as a surprise, given the lack of alternatives available. The Panamax sector has been muted since the turn of the year, and whilst there is an element of forward enquiry, albeit preferably for modern, economical tonnage, the general oversupply in this sector is a cause for concern and it is difficult to see how and where the market can absorb this supply overhang in the coming weeks. Although there has been some activity in the mid sizes, rates have certainly taken a hit, with rumours circulating at the time of writing that one gearless 2800teu vessel has significantly broken below the US$6,000/day barrier, a level which had represented what seemed to be a natural floor for this sector in recent weeks. The highly resilient 1700teu sector appears to have slightly bowed to pressure after a relatively strong showing in recent months, and although there have been numerous fixtures concluded, rates are starting to show signs of weakening. Further down the spectrum, rates are predominantly static. As the new year kick-starts, there are obviously several challenges at hand and the sentiment is far from positive, yet there are pockets of encouragement to be taken from regions such as the Mediterranean, where it is hoped a shortage of readily available tonnage and a notable resumption of demand will spark a rare rate revival that could well have a positive yet limited knock on effect elsewhere.

Containers

Vessel (Teu/Hmg) Gear Speed Knots Index + / -510/285 Gearless 15.5 3.61 ► 0.00

700/440 Gearless 17.5 4.00 ► 0.00

750/415 Geared 16.0 4.71 ► 0.00

1000/650 Geared 17.5 5.00 ► 0.00

1100/715 Geared 20.0 5.94 ► 0.00

1350/925 Geared 20.0 4.19 ► 0.00

1600/1150 Gearless 18.0 5.15 ► 0.00

1700/1125 Geared 19.5 4.69 ▼ 0.04

1740/1300 Geared 20.5 4.84 ▼ 0.08

2000/1600 Geared 21.0 1.81 ▼ 0.01

2500/1900 Geared 22.0 3.16 ▼ 0.07

2800/2000 Gearless 22.0 2.70 ► 0.00

3500/2500 Gearless 23.0 2.23 ► 0.00

4250/2800 Gearless 24.0 1.72 ► 0.00

Index Total 53.55 ▼ 0.20

0

40

80

120

160

200

Jan-0

8

Apr-

08

Jul-

08

Oct-

08

Jan-0

9

Apr-

09

Jul-

09

Oct-

09

Jan-1

0

Apr-

10

Jul-

10

Oct-

10

Jan-1

1

Apr-

11

Jul-

11

Oct-

11

Jan-1

2

Apr-

12

Jul-

12

Oct-

12

Jan-1

3

The Box Index B O X i