Embed Size (px)

Citation preview

Analysts: Sajid Huq

[email protected] Farjad Siddiqui

Moderate Profit Growth Expected amid Banking Sector Downturn We forecast BRAC Bank Limited (BBL) Loan & Advance (L&A) will grow

18% YoY and deposits will grow 21% YoY in 2011. We further expect

2011-LDR of 86%, lower than 2010-level of 98%. LDR is expected to fall

owing to 2011E multi-year high deposits growth rate (GR) driven by a

slowing stock market as well as significant M2 GR contraction. We

anticipate 2011 net interest margin (NIM) of 4.86% and interest rate

spread (IRS) of 5.07%.

BBL has the largest SME operation in the industry and thus basic

business model is SME oriented. BBL is continually searching for

diversifying its business to protect profitability in future competition–

bKash and ELDORADO are such initiatives.

As a non-PD, BBL is not expected to be substantially affected by 2011

government borrowing. However, increased Statutory Liquidity Reserve

(SLR) requirements since December 2010 are expected to raise BBL’s

treasury investments by 20%. BBL’s aggregate yield from treasuries

(including capital gains) is 18%. We expect investment income from

treasury securities GR of 56.47% YoY in 2011 on booking of trading

profit from ‘held-for-trade’ (HFT) and ‘available-for-sale’ treasury bonds.

BBL secured 4th position in total inward remittance market share among

all the domestic private commercial banks (PCBs) and 7th position

among all the domestic banks in 2011. We estimate 2011 commission &

fees income GR of 15% YoY, decline from 2010 GR of 22% YoY

considering significant fall in income from merchant bank-brokerage

subsidiaries.

On set of high inflation and decline in IRS income whereas a 44% market

correction eroded portfolio gains from 2010 DGEN appreciation of nearly

83%. We estimate 2011 EPS to be BDT 6.95, against BDT 6.28 in 2010,

10.7% higher YoY, but lower than 4-Year average GR of 58.61%.

Last but not least, worth noting that BBL has lower P/E ratio and higher

ROE than most leading banks in other frontier markets (e.g., Sri Lanka,

and Oman). Comparative price multiples and trading liquidity are

illustrated in enclosed report for select frontier market banks via scatter

plot.

Rating: We estimate EPS of BDT 8.70 and BVPS of BDT 31.00 for the

year ending December 2012, and set a target price of BDT 52.00 per

share with an OUTPERFORM rating. This implies a 35.50% price return

on current share price of BDT 38.20 (as on 14h February 2012).

BRAC Bank Ltd DSE: BRACBANK Bloomberg: BRAC:BD

Rating: Outperform Dec-2012 Fair Value Estimate: BDT 52 per share

February 14, 2012

Sources: Company Annual Report, BRAC EPL Research

Price performance of BBL in last 12 months

Sources: Dhaka Stock Exchange

Revenue BDT MM 2010 2011E 2012E

Net Interest Income 5,141.6 4,772.4 6,582.6

Investment Income 2,259.3 2,530.8 2,369.5

Commissions Income 2,771.3 3,187.0 3,760.6

Other income 227.3 262.3 346.2

Total revenue 10,399.5 10,752.4 13,058.9

Other Key Indica-

tors (%) 2010 2011E 2012E

Int. Rate Spread % 6.94% 5.75% 6.75%

NIM % 6.36% 4.86% 5.61%

Cost-to-Income 46.93% 53.00% 49.00% NPL 5.85% 5.60%

Margin and effi-

ciency (%) 2010 2011E 2012E

Operating efficiency 46.93% 53.00% 49.00%

Loan/Deposit 98.21% 85.73% 83.67%

ROE 21.39% 22.99% 29.38%

ROA 1.91% 1.72% 1.78%

Company Summary

Ticker BRACBANK Sector Bank Date of Operation Inception 4-Jul-01 Date of Listing 28-Jan-07 Financial Year End December Number of Shares (mn) 321.13 Current Market Capitalization (BDT bn) 12.23 DSE Market Capitalization (BDT bn) 2,235.80 % of DSE Market Capitalization 0.55% 52 Week High (BDT) 650 52 Week Low (BDT) 30.2 YTD Return (%) -17.00% 52 Week Average Volume Traded (BDT mn) 28.5 Trailing EPS (BDT) 6.28 Trailing P/E ratio (x) 6.71

.0

70.0

140.0

210.0

280.0

350.0

420.0

20

30

40

50

60

70

80

Tu

rno

ve

r, B

DT

MM

Pri

ce,

BD

T

Turnover Price

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

2

Growth in Loans and Advances (L&A) We estimate BRAC Bank Ltd (BBL) 2011 L&A growth rate (GR) of 18% YoY,

lower than 2010 L&A GR of 35% YoY, and 4-year L&A CAGR of 42%, on 2H11

M2 GR of -5.2% (21.3% to 19.6% June-Nov11) driven by inflationary pressures

and FX depreciation. Bangladesh Bank (BB) raised repo rates multiple times,

restricted loan-deposit ratio (LDR) to 90% and allowed large loans very

selectively. Mandate by BB to domestic private banks is to enable large loans to

agriculture, SME, and export-oriented sectors, but restrict them in case of

capital markets, real estate, and retail sectors.

M2 GR fell in March-Sep11 nearing BB’s FY12 year-end target of 18%. We

anticipate an M2 GR lower than BB-target, as BB tries to mitigate the

inflationary effect of a BoP deficit and FX depreciation. Government borrowing

is likely to drop in 1H12 with its impact becoming clearer in 2H12—on upward

revision of energy prices.

BBL ensures diversified geographical reach in SME loan disbursement via wide distribution channel. Network of 81 branches are complemented by 22 SME Service Centers, 48 SME/Krishi Branches, and 405 SME Unit offices across the country.

Figure 1: BBL L&A Growth

Figure 2: BBL L&A Composition

Sources: Company Annual Report, BRAC EPL Research

Sources: Company Annual Report (As on 4Q10)

66%62%

22%

35%

18%

0%

10%

20%

30%

40%

50%

60%

70%

0

20,000

40,000

60,000

80,000

100,000

120,000

2007 2008 2009 2010 2011E

GR

(Y

oY

)

L&

A (B

DT

MM

)

L&A (BDT MM) GR (YoY)

Overdraft2%

Demand loan

20%

Term loans24%

Lease Receivable

1%

SME50%

Credit Cards

2%

Staff Loan1%

Bills0.3%

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

3

SME is expected to be the key future growth driver of the bank (BBL) and

domestic economy as well. SME has been ignored for years but domestic

banks have started to add more focus. It can give a thrust to the banks at the

moment when there is a declining demand from big clients. BBL’s years long

SME focused business tactics, strategically located SME centers and employee

expertise to serve SME clients are expected to shape the bank’s future

success.

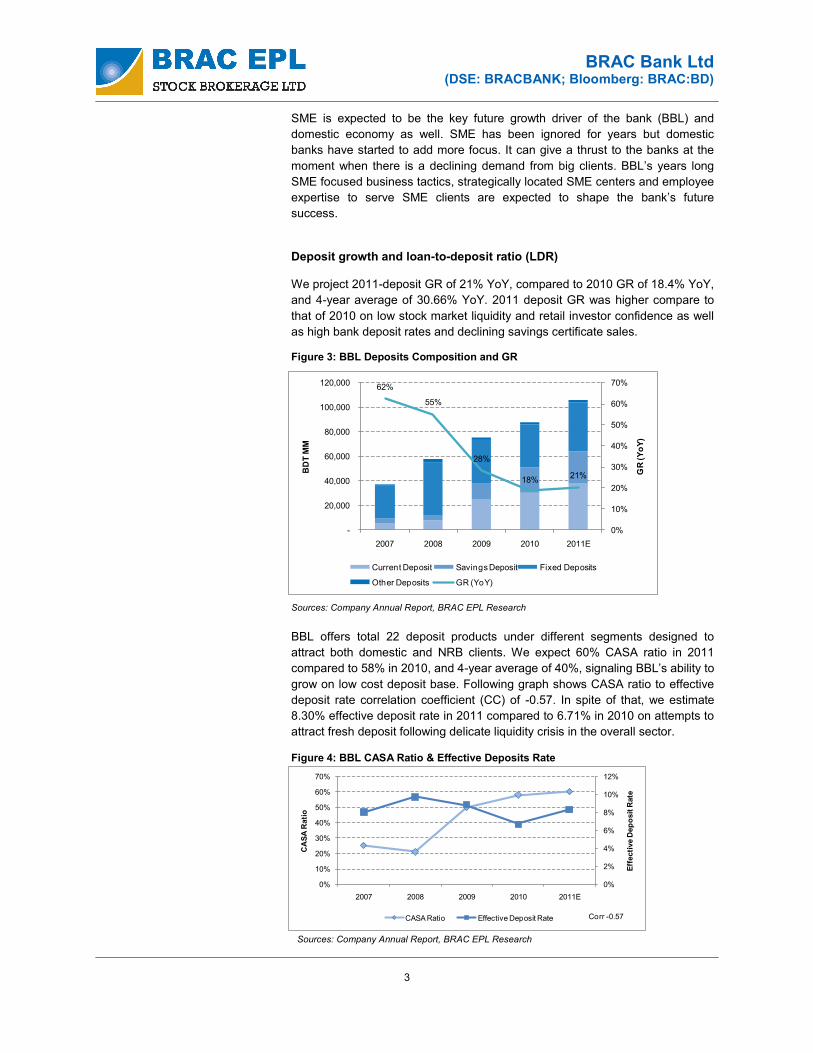

Deposit growth and loan-to-deposit ratio (LDR) We project 2011-deposit GR of 21% YoY, compared to 2010 GR of 18.4% YoY,

and 4-year average of 30.66% YoY. 2011 deposit GR was higher compare to

that of 2010 on low stock market liquidity and retail investor confidence as well

as high bank deposit rates and declining savings certificate sales.

BBL offers total 22 deposit products under different segments designed to

attract both domestic and NRB clients. We expect 60% CASA ratio in 2011

compared to 58% in 2010, and 4-year average of 40%, signaling BBL’s ability to

grow on low cost deposit base. Following graph shows CASA ratio to effective

deposit rate correlation coefficient (CC) of -0.57. In spite of that, we estimate

8.30% effective deposit rate in 2011 compared to 6.71% in 2010 on attempts to

attract fresh deposit following delicate liquidity crisis in the overall sector.

Figure 3: BBL Deposits Composition and GR

Sources: Company Annual Report, BRAC EPL Research

Figure 4: BBL CASA Ratio & Effective Deposits Rate

Sources: Company Annual Report, BRAC EPL Research

62%

55%

28%

18%21%

0%

10%

20%

30%

40%

50%

60%

70%

-

20,000

40,000

60,000

80,000

100,000

120,000

2007 2008 2009 2010 2011E

GR

(Y

oY

)

BD

T M

M

Current Deposit Savings Deposit Fixed Deposits

Other Deposits GR (YoY)

0%

2%

4%

6%

8%

10%

12%

0%

10%

20%

30%

40%

50%

60%

70%

2007 2008 2009 2010 2011E

Eff

ecti

ve D

ep

osit

Rate

CA

SA

Rati

o

CASA Ratio Effective Deposit Rate Corr -0.57

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

4

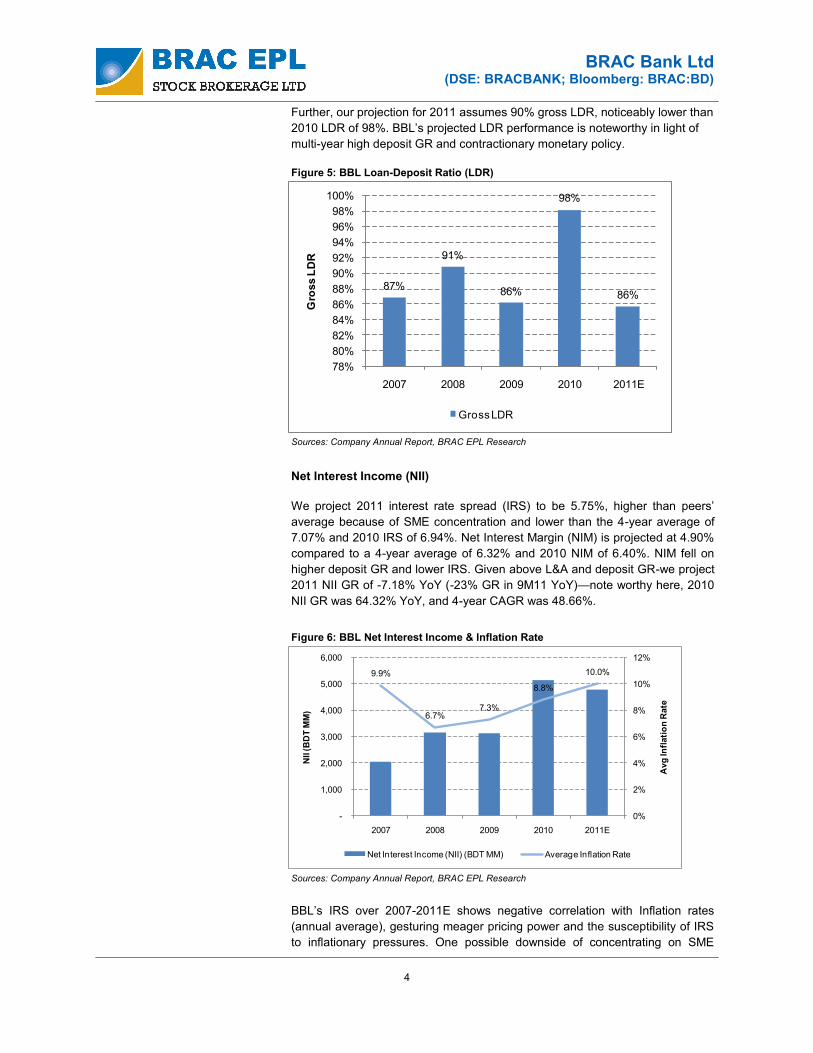

Further, our projection for 2011 assumes 90% gross LDR, noticeably lower than

2010 LDR of 98%. BBL’s projected LDR performance is noteworthy in light of

multi-year high deposit GR and contractionary monetary policy.

Net Interest Income (NII)

We project 2011 interest rate spread (IRS) to be 5.75%, higher than peers’

average because of SME concentration and lower than the 4-year average of

7.07% and 2010 IRS of 6.94%. Net Interest Margin (NIM) is projected at 4.90%

compared to a 4-year average of 6.32% and 2010 NIM of 6.40%. NIM fell on

higher deposit GR and lower IRS. Given above L&A and deposit GR-we project

2011 NII GR of -7.18% YoY (-23% GR in 9M11 YoY)—note worthy here, 2010

NII GR was 64.32% YoY, and 4-year CAGR was 48.66%.

BBL’s IRS over 2007-2011E shows negative correlation with Inflation rates

(annual average), gesturing meager pricing power and the susceptibility of IRS

to inflationary pressures. One possible downside of concentrating on SME

Figure 6: BBL Net Interest Income & Inflation Rate

Sources: Company Annual Report, BRAC EPL Research

Sources: Company Annual Report, BRAC EPL Research

Figure 5: BBL Loan-Deposit Ratio (LDR)

87%

91%

86%

98%

86%

78%

80%

82%

84%

86%

88%

90%

92%

94%

96%

98%

100%

2007 2008 2009 2010 2011E

Gro

ss L

DR

Gross LDR

9.9%

6.7%7.3%

8.8%

10.0%

0%

2%

4%

6%

8%

10%

12%

-

1,000

2,000

3,000

4,000

5,000

6,000

2007 2008 2009 2010 2011E

Avg

Infl

ati

on

Rate

NII (B

DT

MM

)

Net Interest Income (NII) (BDT MM) Average Inflation Rate

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

5

sector is the relatively less flexibility of loan re-pricing, as most of the clients are

not worthy that much. So, linear adjustment of loan rate with incremental

deposit rate is quite difficult.

In spite of NIM shock in a particularly difficult year for banks—BBL’s core

earnings driver is expected to be its IRS and deposit GR in 2011. IRS income

contributed 49% to 2010 total operating income and 44% in 2011 is expected.

However, we anticipate NIMs to be condensed for conventional commercial

banks over time amid increasing competition.

BBL’s new avenues in business Bangladesh bank sector has been enjoying higher IRS than that of other frontier

market banks. In the longer run, competition would drive domestic banks’ NII

down, and eventually profitability. Bangladesh Bank (BB) has recently issued a

directive to bring the IRS to 5%, lower than historical level.

Figure 8: Operating Income Composition

Figure 7: BBL Interest Rate Spread, NIM & Average Inflation Rate

Sources: Company Annual Report, BRAC EPL Research

-10%

-6%

-2%

2%

6%

10%

14%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2007 2008 2009 2010 2011E

Avg

Infl

ati

on

Rate

Inte

rest R

ate

Sp

read

& N

IM

Interest Rate Spread NIM Average Inflation Rate

58%52%

42%49% 44%

22% 32%

31%27%

30%

20% 15%26% 22% 24%

0.5% 0.3% 1% 2% 2%

0%

20%

40%

60%

80%

100%

120%

2007 2008 2009 2010 2011E

Co

mp

osit

ion o

f O

pera

ting

Incom

e

Net Interest Income Commission Income Invetsment Income Other Income

Sources: Company Annual Report, BRAC EPL Research

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

6

In this reality, BBL has concentrated on searching for alternative avenues of revenue generation that is linked to mobile technology- possible growth driver of domestic banking sector. bKash bKash is a joint venture between BBL and US-based ‘Money in Motion’ that

aims to serve the 83% of the population living on less than $2 a day. bKash‟s

one of the distribution partners is BRAC, an NGO with a large geographic

footprint and more than 8 million microfinance group members in Bangladesh,

enabling bKash to offer services where they are most needed.

While only 9% of Bangladeshis are banked, more than 44% of population owns

a mobile phone, making Bangladesh an ideal market for the introduction of

mobile financial services.

EL DORADO EL DORADO is a web based remittance and payment processing system for

BDT payments. A key issue facing the Bangladesh remittance delivery network

is the lack of electronic interconnectivity between banks, which is an important

factor if one bank has the obligation to deliver remittance proceeds to a

customer of another bank.

Non-Interest Income Non-interest income constitutes 55.62% of BBL’s 2011E total operating income.

As per 4-year average, its proportion was 49.45% of total operating income,

with investment income at 20.58% and commissions & fees income at 27.84%.

Commission income and Exchange gains are expected to have GR at 52% and

40% respectively in 2011. Foreign currency comes from export

and remittances. After meeting the internal needs like financing import clients,

excess currency are sold in the local market to the other banks. Profit

from foreign exchange dealings comes from the rate spread between position

taken and position sold. Over last 1 year, when BDT depreciated around 16%

against US$, that is expected to be the basic driver behind 40% GR in 2011

exchange gain.

Sources: World Bank Database

Table 1: Interest Rate Spread Comparative Analysis

2006 2007 2008 2009 2010

Bangladesh 7.66% 6.20% 6.80% 6.70% 6.40% 5.90%

Indonesia 7.84% 4.60% 5.90% 5.10% 5.20% 6.20%

Kuwait 5.44% 3.70% 3.10% 2.80% 3.30% 2.60%

Malaysia 2.66% 3.30% 3.20% 3.00% 3.00% 2.50%

Oman 5.68% 3.40% 3.10% 2.60% 3.30% 3.50%

Pakistan 12.66% 6.80% 6.50% 6.00% 5.90% 5.90%

Philippines 5.06% 4.50% 5.00% 4.30% 5.80% 4.50%

Qatar 6.68% 2.90% 3.00% 3.90% 2.80% 4.40%

Sri Lanka 11.54% 6.00% 8.00% 8.00% 5.10% 3.30%

Vietnam 10.96% 3.50% 3.70% 3.10% 2.20% 1.90%

Interest Rate Spread over Time5 Yr Avg

InflationCountr ies

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

7

from foreign exchange dealings comes from the rate spread between position

taken and position sold. Over last 1 year, when BDT depreciated around 16%

against US$, that is expected to be the basic driver behind 40% GR in 2011

exchange gain.

Investment Income As a non-PD, BBL is not expected to be substantially affected by 2011

government borrowing. Higher government borrowing (BDT 69.3 billion in Jul-

Sept11, a 23x rise YoY) is not expected to directly affect BBL’s 2011 treasury

investment portfolio. However, increased Statutory Liquidity Reserve (SLR)

requirements since December 2010 are expected to raise BBL’s treasury

investments by 20% in 2011 compared to 4-year average GR of 31%.

Figure 9: Comparative Analysis of Operating Income Composition (As on 9M 2011)

Sources: Company Annual Report, BRAC EPL Research

Figure 10: BBL Non-Interest Income Composition

Sources: Company Annual Report, BRAC EPL Research

36% 40%29%

43%35%

68%

37%

32% 24% 42%24% 38%

1%

30%

26%

18%

23% 28%22% 28% 30%

6%18%

6% 6% 5% 3% 3%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Prime Bank National Bank

Southeast Bank

Eastern Bank

NCC Bank Islami Bank Bangladesh

BRAC Bank

Co

mp

osit

ion o

f O

pera

ting

Incom

e

Net interest Income Investment Income Fee Income Other Income

120 259 426 1,026 923 654

1,693 1,840

1,745 2,241

693

909

1,924

2,259

2,531

16

20

85

227

262

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

2007 2008 2009 2010 2011E

BD

T M

M

Commission Income Fees Income Investment Income Other Income

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

8

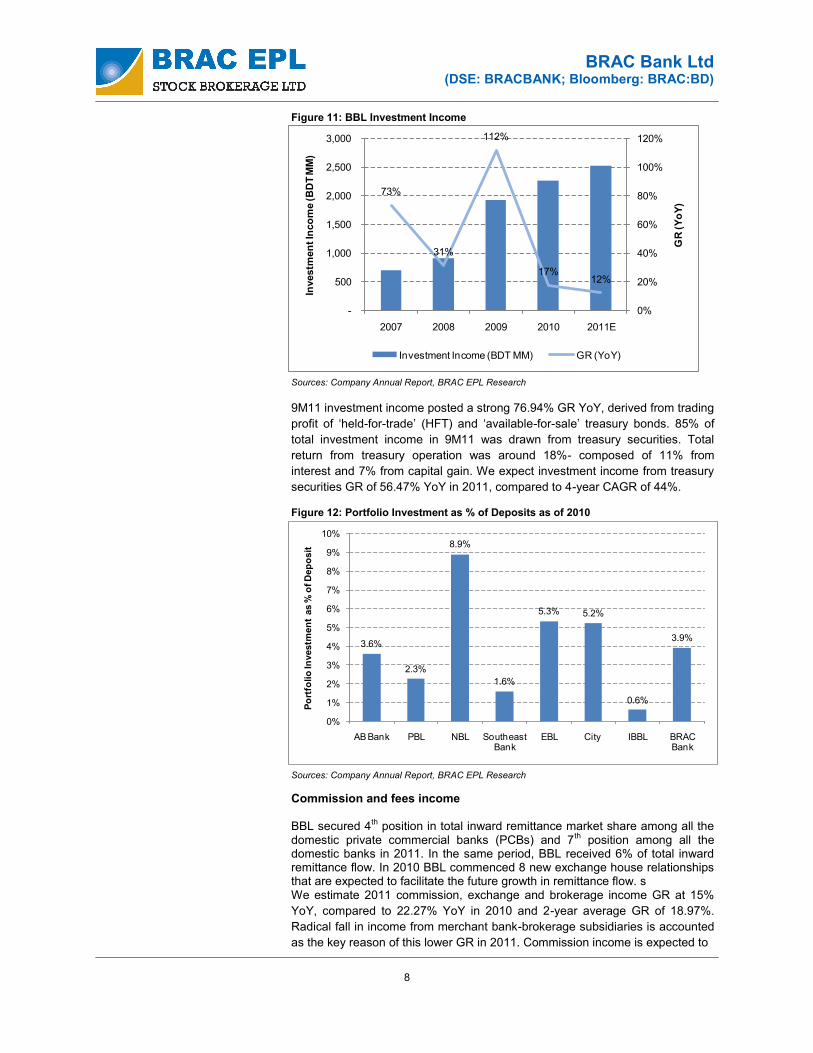

9M11 investment income posted a strong 76.94% GR YoY, derived from trading

profit of ‘held-for-trade’ (HFT) and ‘available-for-sale’ treasury bonds. 85% of

total investment income in 9M11 was drawn from treasury securities. Total

return from treasury operation was around 18%- composed of 11% from

interest and 7% from capital gain. We expect investment income from treasury

securities GR of 56.47% YoY in 2011, compared to 4-year CAGR of 44%.

Commission and fees income BBL secured 4th position in total inward remittance market share among all the domestic private commercial banks (PCBs) and 7th position among all the domestic banks in 2011. In the same period, BBL received 6% of total inward remittance flow. In 2010 BBL commenced 8 new exchange house relationships that are expected to facilitate the future growth in remittance flow. s We estimate 2011 commission, exchange and brokerage income GR at 15%

YoY, compared to 22.27% YoY in 2010 and 2-year average GR of 18.97%.

Radical fall in income from merchant bank-brokerage subsidiaries is accounted

as the key reason of this lower GR in 2011. Commission income is expected to

Figure 11: BBL Investment Income

Sources: Company Annual Report, BRAC EPL Research

Figure 12: Portfolio Investment as % of Deposits as of 2010

Sources: Company Annual Report, BRAC EPL Research

73%

31%

112%

17%12%

0%

20%

40%

60%

80%

100%

120%

-

500

1,000

1,500

2,000

2,500

3,000

2007 2008 2009 2010 2011E

GR

(Y

oY

)

Investm

en

t In

co

me (B

DT M

M)

Investment Income (BDT MM) GR (YoY)

3.6%

2.3%

8.9%

1.6%

5.3% 5.2%

0.6%

3.9%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

AB Bank PBL NBL Southeast Bank

EBL City IBBL BRAC Bank

Po

rtfo

lio

Investm

en

t as %

of D

ep

osit

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

9

grow 52% YoY, fees income 26%, YoY, exchange gain 40% YoY, and

merchant bank-brokerage subsidiaries operation by -40% YoY. However, the

bank’s remittance flow grew at a compound rate of 29.28% over the last 4

years. We estimate 10% growth in remittance flow YoY in 2011.

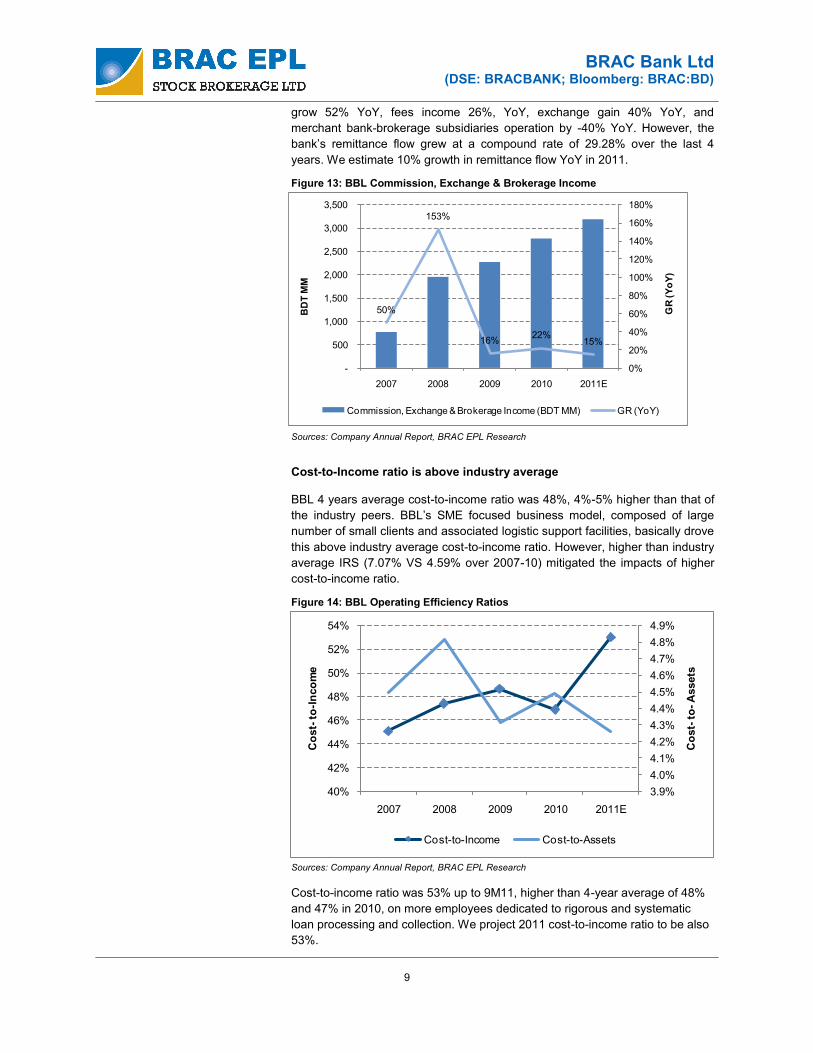

Cost-to-Income ratio is above industry average BBL 4 years average cost-to-income ratio was 48%, 4%-5% higher than that of

the industry peers. BBL’s SME focused business model, composed of large

number of small clients and associated logistic support facilities, basically drove

this above industry average cost-to-income ratio. However, higher than industry

average IRS (7.07% VS 4.59% over 2007-10) mitigated the impacts of higher

cost-to-income ratio.

Cost-to-income ratio was 53% up to 9M11, higher than 4-year average of 48%

and 47% in 2010, on more employees dedicated to rigorous and systematic

loan processing and collection. We project 2011 cost-to-income ratio to be also

53%.

Figure 13: BBL Commission, Exchange & Brokerage Income

Sources: Company Annual Report, BRAC EPL Research

50%

153%

16%22%

15%

0%

20%

40%

60%

80%

100%

120%

140%

160%

180%

-

500

1,000

1,500

2,000

2,500

3,000

3,500

2007 2008 2009 2010 2011E

GR

(Y

oY

)

BD

T M

M

Commission, Exchange & Brokerage Income (BDT MM) GR (YoY)

Figure 14: BBL Operating Efficiency Ratios

3.9%

4.0%

4.1%

4.2%

4.3%

4.4%

4.5%

4.6%

4.7%

4.8%

4.9%

40%

42%

44%

46%

48%

50%

52%

54%

2007 2008 2009 2010 2011E

Co

st-

to-A

ssets

Co

st-

to-I

nco

me

Cost-to-Income Cost-to-Assets

Sources: Company Annual Report, BRAC EPL Research

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

10

Moderate growth in EPS in spite of macro shocks The year 2011 has been severe on the bank sector. High inflation and

government borrowing cut IRS income whereas a 44%-market correction

eroded portfolio gains from 2010 DGEN appreciation of near 83%. We expect

BBL EPS stream and GR to be as follows.

BBL lower but positive income GR in 2011 is owing to combined outcome of macro shocks, lower IRS and lower income from non banking operation, moderate commission and fees income GR, profit booking from treasury operation and higher costs. We project 2011 EPS to be BDT 6.95, against BDT 6.28 in 2010, 10.7% higher YoY. EPS 4-Year average GR is 58.61% as of Dec10. EPS grew -10.84% YoY in 9M11. Inflation and BBL’s profit growth EPS GR YoY averaged 58.61% over 2007-2010. Inflation and net profit GR

exhibit negative correlation coefficient (CC) of -0.20. Below graph depicts higher

net profit YoY GR despite rising average inflation rate. Below graphs also depict

CC of non interest income YoY GR to average inflation rate of -0.64 and NII GR

to average inflation rate CC of 0.07. This is unexpected since negative

Figure 15: BBL EPS Trend

Sources: Company Annual Report, BRAC EPL Research

1.87

2.95

4.16

6.28

6.95

85.0%

57.4%

41.1%

50.9%

10.7%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

-

1

2

3

4

5

6

7

8

2007 2008 2009 2010 2011E

GR

Dilu

ted

EP

S

Diluted EPS GR

Figure 16: Correlation between Inflation & BBL Income Components

-20%

0%

20%

40%

60%

80%

100%

-20%

-16%

-12%

-8%

-4%

0%

4%

8%

12%

2007 2008 2009 2010 2011E

GR

in In

com

es (%

)

Ave

rag

e In

flat

ion

Rat

e

Average Inflation Rate GR in Net Interest Income

GR in Non Interest Income

Sources: BRAC EPL Research

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

11

Comfortable capital adequacy ratio (CAR)

Given that BBL has been maintaining CAR above regulatory requirement since

2003, we expect the trend to continue. The minimum CAR prescribed by the

Bangladesh Bank is 5% for Tier-I and 10% for total capital. BBL exceeded

these minimum ratio thresholds with a Tier-I capital ratio of 8.2% and total

capital ratio of 13.3% in 2010. Note worthy here, low risk grading for SME loan

facilitates attaining Basel II requirement. We expect that total CAR will remain

around 13.00% in 2011 with Tier-I capital ratio of 8.00%.

Improvement in asset quality

We expect 2011 NPL ratio to improve to 5.60% in 2011 from 5.90% in 2010.

Higher than comparable banks’ NPL ratio is an outcome of SME concentration.

Impressive improvement is less likely in a setup of infrastructural bottlenecks

and power shortage. 2007-10 average provision adequacy ratio was 1.20.

However, operation of Regional Credit Risk Management Centers has already

been started to maintain quality underwriting and bring the NPL ratio down.

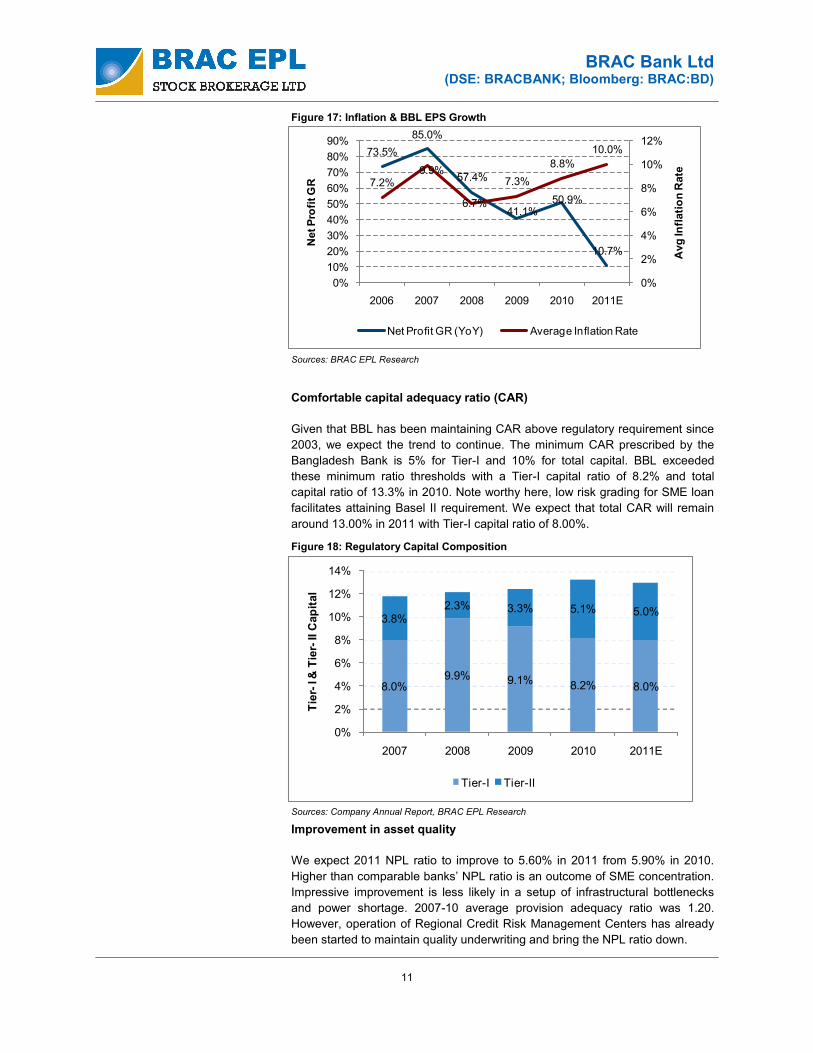

Figure 17: Inflation & BBL EPS Growth

73.5%

85.0%

57.4%

41.1%50.9%

10.7%

7.2%9.9%

6.7%

7.3%

8.8%

10.0%

0%

2%

4%

6%

8%

10%

12%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

2006 2007 2008 2009 2010 2011E

Avg

Infl

ati

on

Rate

Net P

rofi

t G

R

Net Profit GR (YoY) Average Inflation Rate

Sources: BRAC EPL Research

Figure 18: Regulatory Capital Composition

8.0%9.9% 9.1% 8.2% 8.0%

3.8%2.3% 3.3% 5.1% 5.0%

0%

2%

4%

6%

8%

10%

12%

14%

2007 2008 2009 2010 2011E

Tie

r-I &

Tie

r-II C

ap

ital

Tier-I Tier-II

Sources: Company Annual Report, BRAC EPL Research

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

12

However, operation of Regional Credit Risk Management Centers has already

been started to maintain quality underwriting and bring the NPL ratio down.

Increasing return-ROE is increasing We project ROE and ROA for 2011 to be 23.0% and 1.7%, respectively, up

from 21.4% and down from 1.9% in 2010. Higher ROE is driven by moderate

earnings growth and gradual paying off of preference share.

Table 2: BBL Asset Quality

Figure 19: BBL Gross NPL Ratio

Sources: Company Annual Report

Asset Quality 2009 2010

NPLs to total loans and advances 6.04% 5.85%

Provision for classified loans,MM 2,587 2,996

4.5%4.7%

6.0% 5.9%5.6%

0%

1%

2%

3%

4%

5%

6%

7%

2007 2008 2009 2010 2011E

Gro

ss N

PL

Rati

o

Gross NPL Ratio

Sources: Company Annual Report, BRAC EPL Research

Figure 20: BBL ROE & ROA Trend

31.6%

22.9%

19.2%21.4%

23.0%

1.9% 1.6% 1.6% 1.9% 1.7%

0%

5%

10%

15%

20%

25%

30%

35%

2007 2008 2009 2010 2011E

RO

E &

RO

A

ROE ROA

Sources: Company Annual Report, BRAC EPL Research

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

13

BBL in comparison to leading frontier market banks

A quick look at the some of the largest listed banks in frontier markets such as

Pakistan, Sri Lanka, Nigeria and Oman indicates how BBL fares in relation to its

frontier market peers.

With regards to profitability ratios BBL outperforms most of the leading banks in

Pakistan, Sri Lanka, Oman and Romania. Among the 7 tabulated above, BBL

is carrying below median P/E ratio and slightly above median P/B ratio.

Considering its ROE (highest among the above banks) and ROA, undoubtedly

BBL has further scope to appreciate in market.

Sources: BRAC EPL Research, Capital IQ (As on Dec 31, 2011)

Table 3: BBL in Comparison to other Frontier Market Banks (as on Dec 31, 2011)

MCAP

(USD mn)

BRAC Bank

Habib Bank (HB) Pakistan 1,317.10 7.1x 1.3x 19.20% 1.90%

National Bank of Pakistan (NBP) Pakistan 822.6 4.1x 0.6x 14.60% 1.90%

Commercial Bank of Ceylon PLC (CBC) Sri Lanka 711.7 14.1x 2.2x 18.00% 2.00%

Banca Transilvania (BT) Romania 465.4 10.9x 0.8x 13.10% 1.20%

Bank Muscat (BM) Oman 3,037.20 10.1x 1.4x 12.60% 1.60%

Access Bank (AB) Nigeria 536.3 7.9x 0.5x 7.30% 1.60%

1.72%Bangladesh 144.74 5.6x 1.4x 22.99%

Frontier Market Banks Country P/E P/B ROE ROA

Figure 21: BBL in Comparison to other Frontier Market Banks (as on Dec 31, 2011)

BRAC Bank

HB

NBP

CBC

BT BM

AB

0%

5%

10%

15%

20%

25%

0.8% 1.0% 1.2% 1.4% 1.6% 1.8% 2.0% 2.2%

RO

E (%

)

ROA (%)

Sources: BRAC EPL Research, Capital IQ (As on Dec 31, 2011)

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

14

Rating Our rating considered 2012E EPS and BVPS, 2012-outlook for the banking sector and other related factors. Considering the estimated EPS of BDT 8.70 and BVPS of BDT 31.00 for 2012, we estimate a fair value of BDT 52.00 per share with an OUTPERFORM rating. This fair value implies an 8.4x potential P/E and 1.45x potential P/B of the company’s Stock and 35.50% price gain over next 10 months investment horizons.

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

15

Balance Sheet, MM BDT 2008 2009 2010 2011E 2012E 2013E

Property & Assets:

Cash 4,315.9 6,619.1 9,853.0 13,382.6 19,793.8 26,138.0

Balance with Other Banks & F.I 3,195.0 5,649.1 3,887.3 3,906.7 3,984.8 4,383.3

Money at call .0 1,300.0 .0 .0 .0 .0

Investment 8,245.4 10,383.3 13,125.5 14,309.2 17,283.7 20,587.1

Loan & Advance 52,676.7 64,150.8 86,573.9 102,157.2 124,631.8 155,789.8

Fixed Assets 1,472.0 1,666.6 1,854.2 2,781.4 3,476.7 4,172.1

Other Assets 2,536.9 4,846.4 7,507.2 8,257.9 9,083.7 10,173.8

Total Assets 72,441.9 94,615.3 122,801.2 144,795.0 178,254.6 221,244.0

Liabilities & Equities:

Liabilities:

Borrowing from other banks, F.I 2,280.0 2,450.0 10,352.5 12,940.7 16,175.8 19,411.0

Deposits 58,006.9 74,455.7 88,154.9 106,226.6 132,783.3 165,979.1

Other Liability 6,717.5 8,878.4 13,742.4 16,216.1 19,135.0 22,579.3

Total Liabilities 67,004.4 85,784.1 112,249.8 135,383.3 168,094.1 207,969.3

Shareholder's Equity: 5,437.5 8,831.2 10,551.3 9,411.7 10,160.5 13,274.6

Total Liabilities & Equities 72,441.9 94,615.3 122,801.2 144,795.0 178,254.6 221,244.0

Income Statement, MM BDT 2008 2009 2010 2011E 2012E 2013E

Interest/Investment Income 8,021.1 9,202.3 11,028.5 13,805.9 17,307.7 21,659.2

Interest/profit paid on deposit 4,865.1 6,073.2 5,886.8 9,033.5 10,725.1 13,374.0

Net Interest Income 3,156.0 3,129.1 5,141.6 4,772.4 6,582.6 8,285.3

Income from investments 909.1 1,923.8 2,259.3 2,530.8 2,369.5 2,194.4

Commission, Excng & Brok 1,951.2 2,266.5 2,771.3 3,187.0 3,760.6 4,437.5

Other Income 19.9 85.1 227.3 262.3 346.2 541.5

Total Operating Income 6,036.2 7,404.6 10,399.5 10,752.4 13,058.9 15,458.7

Operating Expense 2,862.3 3,603.6 4,880.4 5,698.8 6,398.8 6,956.4

Profit Before Provision 3,173.9 3,801.1 5,519.1 5,053.6 6,660.0 8,502.3

Provision 1,150.5 1,574.0 2,053.0 1,228.9 1,658.9 2,003.5

Pre-Tax Profit 2,023.5 2,227.1 3,466.1 3,824.8 5,001.1 6,498.7

Tax 1,050.0 853.7 1,393.0 1,529.9 2,125.5 2,794.5

Profit After Tax 973.5 1,373.4 2,073.1 2,294.9 2,875.6 3,704.3

2008 2009 2010 2011E 2012E 2013E

Total Assets Growth 56.18% 30.61% 29.79% 17.91% 23.11% 24.12%

L & A Growth 62.28% 21.78% 34.95% 18.00% 22.00% 25.00%

Deposit Growth 55.23% 28.36% 18.40% 20.50% 25.00% 25.00%

EPS GR 57.43% 41.08% 50.95% 10.70% 25.31% 28.82%

IMPORTANT DISCLOSURES

Analyst Certification: Each research analyst and research associate who authored this document and whose name appears herein certifies that the recommendations and opinions expressed in the research report accurately reflect their personal views about any and all of the securities or issuers discussed therein that are within the coverage universe. Disclaimer: Estimates and projections herein are our own and are based on assumptions that we believe to be reasonable. Information presented herein, while obtained from sources we believe to be reliable, is not guaranteed either as to accuracy or completeness. Neither the information nor any opinion expressed herein constitutes a solicitation of the purchase or sale of any security. As it acts for public companies from time to time, BRAC-EPL may have a relationship with the above mentioned company(s). This report is intended for distribution in only those jurisdictions in which BRAC-EPL is registered and any distribution outside those jurisdictions is strictly prohibited. Compensation of Analysts: The compensation of research analysts is intended to reflect the value of the services they provide to the clients of BRAC-EPL. As with most other employees, the compensation of research analysts is impacted by the overall profitability of the firm, which may include revenues from corporate finance activities of the firm's Corporate Finance department. However, Research analysts' compensation is not directly related to specific corporate finance transaction. General Risk Factors: BRAC-EPL will conduct a comprehensive risk assessment for each company under coverage at the time of initiating research coverage and also revisit this assessment when subsequent update reports are published or material company events occur. Following are some general risks that can impact future operational and financial performance: (1) Industry fundamentals with respect to customer demand or product / service pricing could change expected revenues and earnings; (2) Issues relating to major competitors or market shares or new product expectations could change investor attitudes; (3) Unforeseen developments with respect to the management, financial condition or accounting policies alter the prospective valuation; or (4) Interest rates, currency or major segments of the economy could alter investor confidence and investment prospects.

BRAC EPL Stock Brokerage Capital Markets Group

Sajid Huq Amit Senior Research Analyst [email protected] 01755 541 254

Parvez Morshed Chowdhury Research Analyst [email protected] 01730 357 154

Ali Imam Investment Analyst [email protected] 01730 357 153

Khandakar Safwan Saad Research Associate [email protected] 01730 357 779

Aasim Tajwaar Matin Research Associate [email protected] 01730 727 913

M M Shahnewaz Kabir Shawon Research Associate [email protected] 01730 727 918

Farjad Siddiqui Research Associate [email protected] 01730 727 924

BRAC EPL Research www.bracepl.com 121/B Gulshan Avenue Gulshan-2, Dhaka-1212 Tel: +88 02 881 9421-5 Fax: +88 02 881 9426 E-Mail: [email protected]

BRAC Bank Ltd (DSE: BRACBANK; Bloomberg: BRAC:BD)

Institutional Sales and Trading

Delwar Hussain (Del) Head of Institutional Sales and Trading

[email protected] 01755 541 252