Embed Size (px)

Citation preview

Name: Kazi Rasel

ID: 12302199

Program: BBA

BRAC Bank Limited, the youngest commercial bank in Bangladesh banking industry was founded in July 04, 2001, by Bangladesh Rural Advance committee (BRAC), one of the biggest development finance institutions founded by Sir Fazle Hasan Abed

Vision:

“ Building profitable and socially responsible financial institution focused on Market and Business with Growth potential, thereby assisting BRAC and stakeholders to build a just, enlightened, healthy democratic and poverty free Bangladesh”.

Mission :

Value the fact that one is a member of the BRAC family

Creating an honest, open and enabling environment

Have a strong customer focus and build relationships based on superior service and mutual benefit

BRAC Bank is governed by board members. The board members are elected from among distinguished individuals with sound reputations in social development, business or the professions who have demonstrated their personal commitment.

Top management and policy-making body of BRAC Bank limited. Presently the Board consists of a chairman and four directors. The Directors are appointed from amongst those who have had experience and shown capacity in the field of finance and banking, trade, commerce, industry agriculture. The Chief Operations Officer executes all the activities under the direction of the Board.

SME is defined as, “A firm managed in a personalized way by its owners or partners, which has only a small share of its market and is not sufficiently large to have access to the stock exchange for raising capital”.

The report will work on some specific objectives. Those are as follows-

To provide a brief overview of BRAC Bank Ltd-

• Background of BRAC Bank Ltd

• Different divisions and subsidiaries of BRAC Bank Ltd.

• SWOT analysis of BRAC Bank Ltd.

To present an overview of SME division of BRAC Bank Ltd-

• Detail description of SME division of BRAC Bank Ltd

• Operation Process of SME Loan Disbursement of BBL.

• Risk management process and collection process of BRAC Bank Ltd.

SAMPLING PROCEDURE

a. Probability sampling

b. Simple random sampling.

SAMPLING FRAME

The customer who are take SME loan from Bank. I have selected them as our sampling frame.

SAMPLE SIZE

I have take 40 sample for our research.

RESEARCH INSTRUMENT

I have use Yes No and 5 liker scale using close ended question.

As an independent researcher, I have conducted quantitative research on Customer satisfaction of SME department in BRAC Bank Ltd. Survey question close ended questions that is Yeas No questions and 5 liker scale questions .

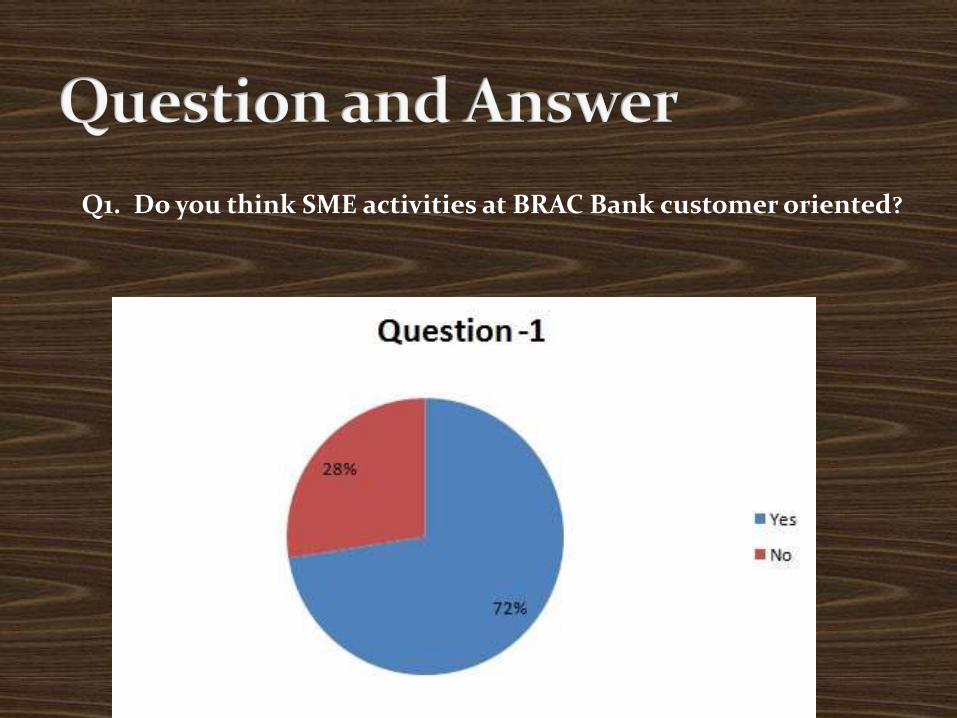

Q1. Do you think SME activities at BRAC Bank customer oriented?

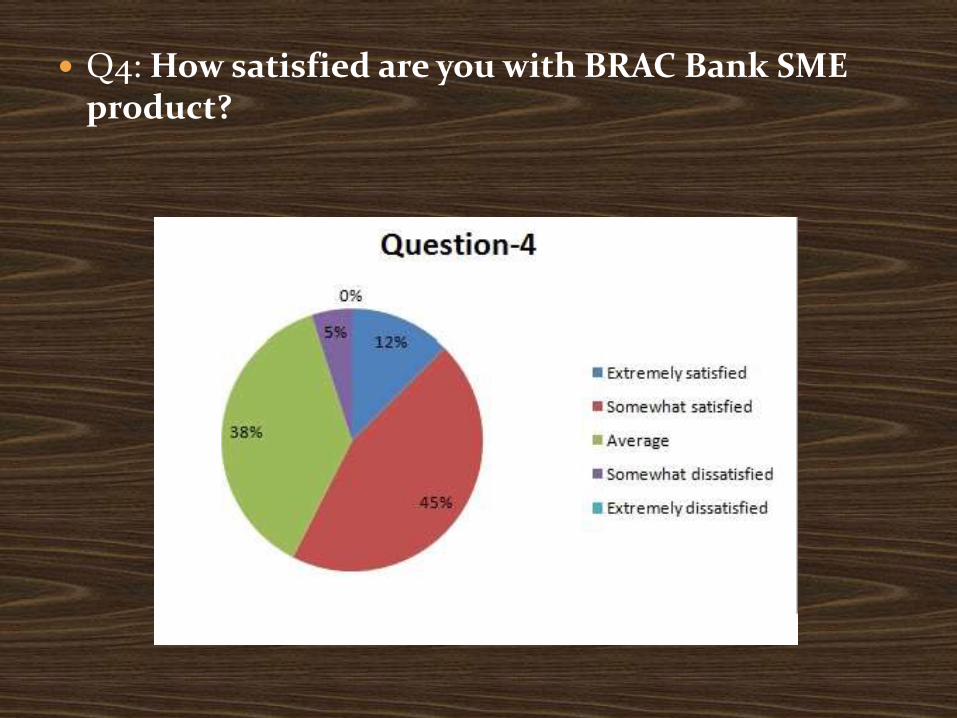

Q4: How satisfied are you with BRAC Bank SME product?

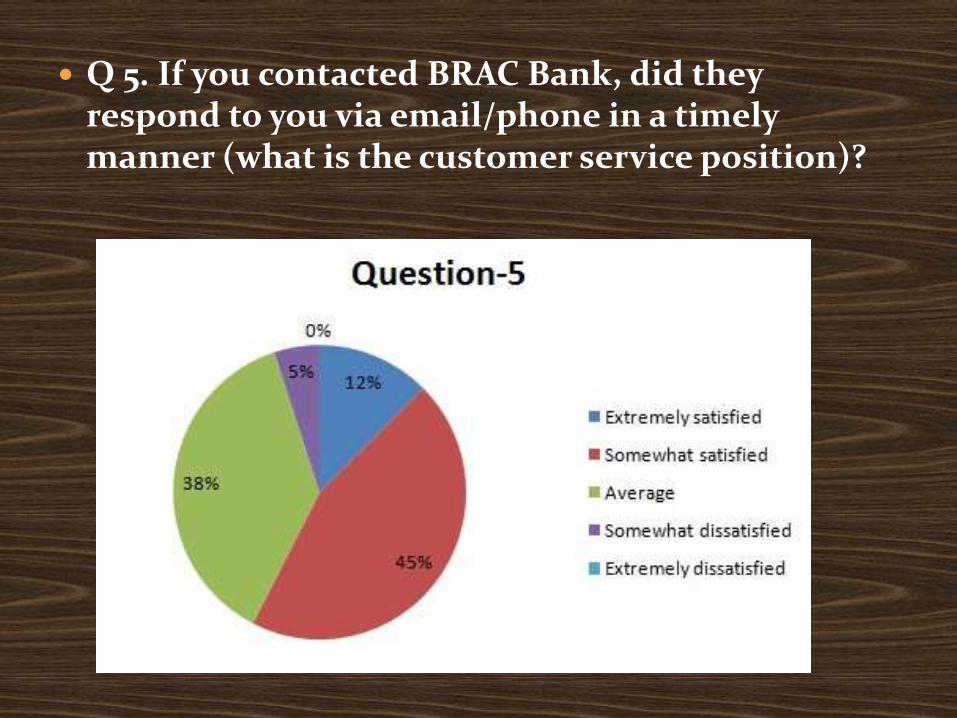

Q 5. If you contacted BRAC Bank, did they respond to you via email/phone in a timely manner (what is the customer service position)?

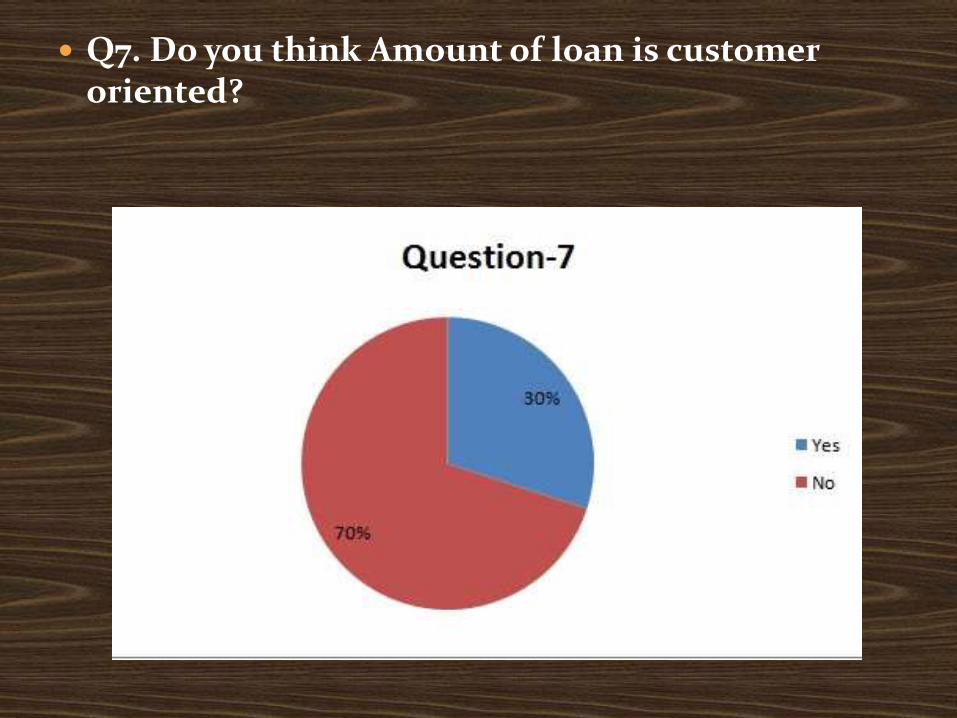

Q7. Do you think Amount of loan is customer oriented?

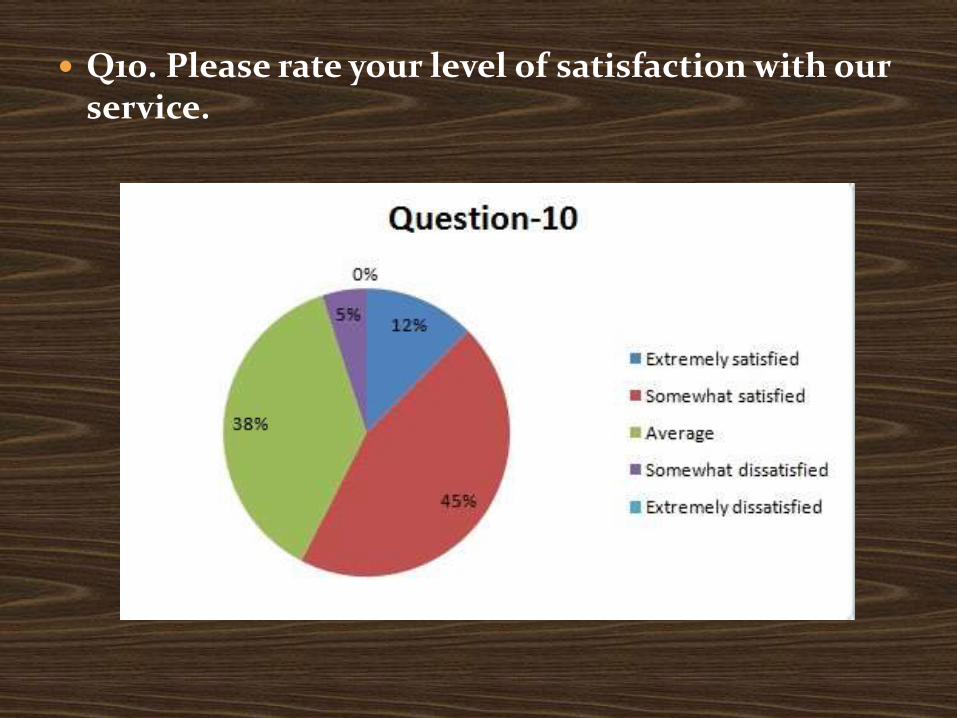

Q10. Please rate your level of satisfaction with our service.

Regarding SME activities of BRAC Bank 72% people says it is customer oriented and other 28% people says it is not customer oriented need to improve.

For reasons of selecting BRAC Bank easy to get loan(38%), interest rate(10%), customer service(20%), reputation(22) and influence by marketing(10%),

Security documentation process at BRAC Bank 63% says is difficult and 27% says it is not difficult to get loan

Customer service 25% says somewhat satisfied and 83% says it is average 12%extemele satisfied 5% dissatisfied and 0%extremely dissatisfied.

Selection criteria 45% satisfied and 38% are average so it is almost average position.

Amount of loan are not enough for the customer 70% says it is not good.

Customer satisfaction rate 45% somewhat satisfied, 38% average satisfied, 12% extremely satisfied, 5%somewhat dissatisfied and 0% extremely dissatisfied.

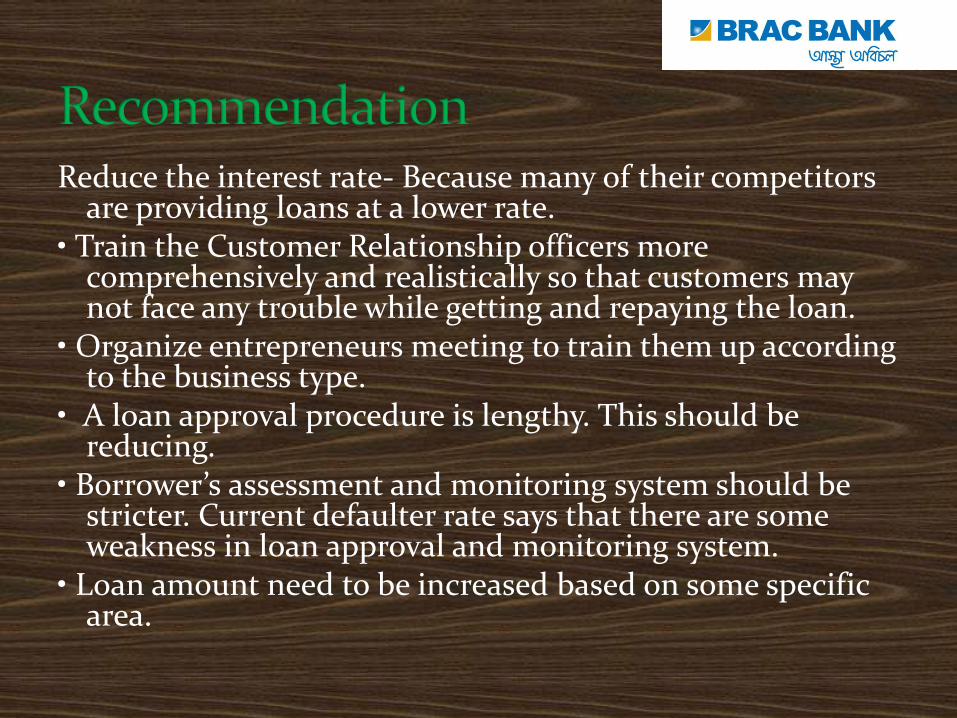

Reduce the interest rate- Because many of their competitors are providing loans at a lower rate.

• Train the Customer Relationship officers more comprehensively and realistically so that customers may not face any trouble while getting and repaying the loan.

• Organize entrepreneurs meeting to train them up according to the business type.

• A loan approval procedure is lengthy. This should be reducing.

• Borrower’s assessment and monitoring system should be stricter. Current defaulter rate says that there are some weakness in loan approval and monitoring system.

• Loan amount need to be increased based on some specific area.

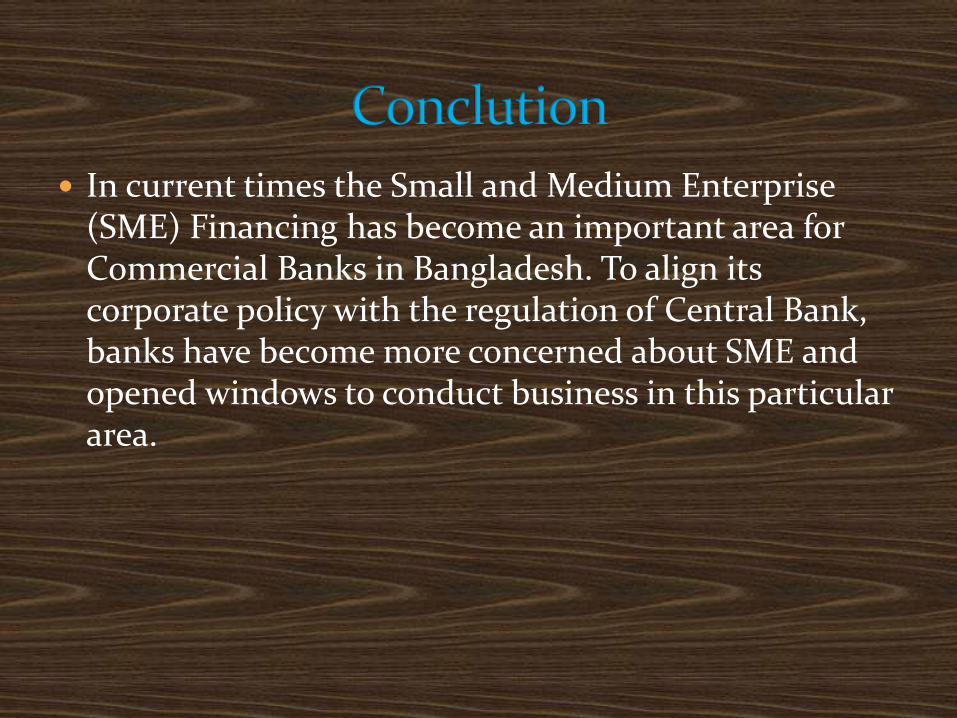

In current times the Small and Medium Enterprise (SME) Financing has become an important area for Commercial Banks in Bangladesh. To align its corporate policy with the regulation of Central Bank, banks have become more concerned about SME and opened windows to conduct business in this particular area.