Embed Size (px)

Citation preview

1

BOUSTEAD HOLDINGS BERHAD (“BHB” OR “COMPANY”)

PROPOSED CONVERSION OF AL-HADHARAH BOUSTEAD REIT TO A PRIVATE PROPERTY TRUST BY WAY OF AMENDMENT TO THE TRUST DEED, PROPOSED SELECTIVE UNIT REDEMPTION EXERCISE AND SPECIAL DIVIDEND

1. INTRODUCTION

On behalf of the board of directors (“Board”) of BHB, AFFIN Investment Bank Berhad (“AFFIN Investment”) wishes to announce that BHB’s wholly-owned subsidiary, Boustead Plantations Berhad (“BPB”), had on 16 July 2013, issued a letter (“SUR Proposal Letter”) to the Board of Boustead REIT Managers Sdn Bhd (“Manager”), as the manager of Al-Hadharah Boustead REIT (“BREIT” or “Fund”) and to CIMB Islamic Trustee Berhad (“Trustee”), being the trustee for the Fund, to notify that BPB intends to convert the Fund from being a collective investment scheme to a private property trust. In this regard, BPB has requested the Manager to undertake the following corporate exercises: (i) proposed amendment to the relevant clauses in the trust deed dated 11 December

2006, and amended and restated on 3 September 2009 (“Trust Deed”), executed between the Trustee and the Manager, constituting the Fund to allow the following: the implementation of the Proposed SUR (as defined below); and

the conversion of the Fund to a private property trust which sole beneficiary

shall be BPB. (collectively referred to as the “Proposed Amendment”);

(ii) proposed selective unit redemption exercise, involving the redemption of all undivided

interest in the Fund as constituted by the Trust Deed (“Units”) held by the Fund’s unitholders (save and except for the Units held by BPB) and the corresponding cash repayment of RM1.90 per Unit to the Fund’s unitholders (excluding BPB) (“Proposed SUR”); and

(iii) proposed special dividend of RM0.20 per Unit to all unitholders (including BPB) of the

Fund (“Special Dividend”). (the Proposed Amendment, Proposed SUR and Special Dividend are collectively referred to as the “Proposals”).

The cash payment under the Proposed SUR and the Special Dividend will collectively amount to RM2.10 per Unit (“Deemed Consideration Price”). For information purposes, the Proposals are deemed to be a related party transaction under Chapter 10 of the Main Market Listing Requirements of Bursa Malaysia Securities Berhad (“Bursa Securities”) (“Listing Requirements”) as BHB will be transacting with Lembaga Tabung Angkatan Tentera (“LTAT”), its major shareholder (as defined in the Listing Requirements) which is also a major unitholder in the Fund. Pursuant to the percentage threshold set out in Section 14 of this announcement and Chapter 10 of the Listing Requirements, the Proposals will require the appointment of an independent adviser to advise the non-interested directors and shareholders of BHB. In this regard, Public Investment Bank Berhad (“PIBB”) has been appointed by BHB to act as the independent adviser to advise the non-interested directors and shareholders of BHB on the Proposals.

Further details of the Proposals are set out in the ensuing sections of this announcement.

2

2. DETAILS OF THE PROPOSALS 2.1 Proposed Amendment

The Proposed Amendment is envisaged to encapsulate the following areas to enable the corporate integration of the Fund under BPB: (i) Implementation of the Proposed SUR

The amendments to the Trust Deed will enable the Fund to implement the Proposed SUR and undertake the de-listing procedures under Chapter 16.07(b) of the Listing Requirements.

(i) Conversion of the Fund to a private property trust

The Fund was established as a real estate investment trust and constituted pursuant to the execution of the Trust Deed and regulated by the Capital Markets and Services Act 2007 (“CMSA”) and the Securities Commission Malaysia (“SC”) Guidelines on Real Estate Investment Trusts (“REIT Guidelines”). The Fund is a unit trust scheme that invests primarily in income generating real estate assets with the main objective of providing its investors with stable returns and/or distributions of income/yield primarily from the leasing of plantation assets to BHB and its subsidiaries (“BHB Group”). Upon the successful completion of the Proposed SUR and payment of the Special Dividend, the Fund will be converted to a private property trust with BPB being its sole beneficiary. As a private property trust, the Fund will no longer be a collective investment scheme for the purposes of the REIT Guidelines and hence will not be regulated under the CMSA and the REIT Guidelines.

2.2 Proposed SUR

2.2.1 Background information on the Proposed SUR

The Proposed SUR shall involve the redemption of all Units held by the Fund’s unitholders, save and except for the Units held by BPB, which involves a redemption payment of RM1.90 per Unit being made to all unitholders of the Fund (excluding BPB) (“Entitled Unitholders”) whose names appear in the Record of Depositors on an entitlement date to be determined later by the Board of the Manager (“Entitlement Date”). As at 30 June 2013 (“LPD”), the Fund had 626,904,500 Units in circulation. The Units in the Fund shall be redeemed by way of cancellation of 290,990,000 Units held by the Entitled Unitholders. Upon completion of the Proposed SUR, BPB will hold 335,914,500 Units which will represent the entire interest in the Units in the Fund. The Board of BPB have indicated that it does not intend to maintain the listing status of the Fund on the Main Market of Bursa Securities upon completion of the Proposed SUR. Following the above, BPB will request the Manager to make the application to Bursa Securities to delist the Fund and withdraw its listing status from the Official List upon completion of the Proposals.

3

2.2.2 Special Dividend

As a condition to the Proposed SUR, BPB also proposes that the Fund in turn proposes the Special Dividend of RM0.20 per Unit to the Entitled Unitholders and BPB. The final amount of the Special Dividend to be proposed by the Manager on behalf of the Fund shall depend on, inter alia, the investment securities held by the Fund to be liquidated, the expected lease rental and any performance based profit sharing to be received by the Fund up to the Entitlement Date, after deducting all the expected and relevant expenses incurred by the Fund.

2.2.3 Mode of settlement The Entitled Unitholders will receive cash as consideration for the cancellation for their Units pursuant to the Proposed SUR and for the Special Dividend. The Proposals are expected to be funded by way of internally generated funds of the Fund, and /or advances to the Fund through external borrowings to be raised by the BHB Group.

2.2.4 Salient terms of the SUR Proposal Letter The salient terms of the Proposed SUR are as follows: (i) If the Fund declares, makes and/or pays a dividend or other

distribution of any nature whatsoever ( “Distribution”) after the date of the SUR Proposal Letter up to completion of the Proposals, the Deemed Consideration Price shall be reduced by an amount equivalent to the Distribution made per Unit. However, the Special Dividend and the interim dividend for the financial year ending 31 December 2013 shall be excluded for the purposes of ascertaining any Distribution.

(ii) From the date of the SUR Proposal Letter until the completion of the

Proposals, the Manager/Trustee shall undertake that they will not:

(a) conduct any form of capital raising exercise, whether in the form of debt or equity and will not grant any options over the Units or issue any new Units in the Fund;

(b) cause the Fund to enter into any material commitment or

material contract or undertake any obligation or acquire or dispose of any of its assets or create a security interest over any of its assets outside the ordinary course of business;

(c) pass any resolution in a meeting (other than in respect of any ordinary business tabled in an annual general meeting or pursuant to the Proposals) or make any alteration to the provisions of the Trust Deed save for the Proposed Amendment;

(d) do or cause, or allow to be done or omitted, any act or thing

which would result (or be likely to result) in a breach of any lawful obligation of the Fund;

4

(e) dilute the interest, holdings or economic interest of the Fund which the Fund holds shares, other than investments in quoted Shariah-compliant securities and for the purposes of the dividend payment pursuant to the Special Dividend; and

(f) not enter into any discussion, negotiation or agreement, with any other party with respect to the sale of the assets and liabilities of the Fund which amount exceeds RM5.0 million,

without BPB’s prior written consent.

(iii) In addition, the Manager/Trustee shall not enter into any discussion, negotiation or agreement, with any other party with respect to any privatisation proposal involving the Fund or any other matters specified under paragraph 2.2.4(ii)(b) above at any time until completion of the Proposals; and

(iv) The Manager/Trustee shall also agree with and undertake to BPB that, as from the date of acceptance of the Proposals (in accordance with the SUR Proposal Letter) until the completion of the Proposals, the Manager/Trustee (and the Manager/Trustee shall use reasonable endeavours to cause and procure that the Fund) shall carry on the business of the Fund only in the usual, regular and ordinary course in substantially the same manner as the same is carried on as of the date hereof so as to preserve the Fund’s relationship with all parties in ensuring that the Fund’s goodwill and going concern shall not be materially impaired at the completion date, save as otherwise agreed in writing by BPB.

2.2.5 Liabilities to be assumed by BHB Save for the borrowings to be raised by the BHB Group to be advanced to the Fund and/or external borrowings by the Fund pursuant to the Proposals, there are no other liabilities including contingent liabilities and guarantees to be assumed by the BHB Group arising from the Proposals.

2.2.6 Listing status of the Fund As indicated in the SUR Proposal Letter, BPB does not intend to maintain the listing status of the Fund on the Main Market of Bursa Securities. In this respect (subject to the approval from the relevant authorities, shareholders of BHB and the Entitled Unitholders to be obtained at a later date) upon completion of the Proposals, the Fund will be converted to a private property trust with BPB being the sole beneficiary to the trust and removed from the Official List of Bursa Securities.

5

2.2.7 Original cost of investment The original cost and date of investment of the Fund by BPB is set out below:

Date of acquisition No. of Units acquired Unit price

Cost of investment

RM RM

8 February 2007 179,164,500 1.00 179,164,500

21 July 2007 71,750,000 1.00 71,750,000

15 December 2008 85,000,000 1.10 93,500,000

Total 335,914,500 344,414,500

2.3 Deemed Consideration Price

The Deemed Consideration Price of RM2.10 per Unit comprises the following: (i) RM1.90 per Unit, for the consideration for the Proposed SUR (“SUR Offer

Price”); and

(ii) RM0.20 per Unit, for the cash payment of the Special Dividend.

The Entitled Unitholders whose names appear on the Entitlement Date shall receive a total cash payment from the Fund of RM611,079,000 which represents cash amount of RM2.10 per Unit. BPB shall only receive the Special Dividend under the Proposals. The final Special Dividend to be proposed by the Manager may be varied compared to the RM0.20 per Unit which is being proposed by BPB and if such situation takes place, the SUR Offer Price will also be adjusted accordingly to ensure that the Deemed Consideration Price remains at RM2.10 per Unit. For avoidance of doubt, regardless of the amount of Special Dividend proposed by the Manager, the Entitled Unitholders shall receive a total cash payment of RM2.10 per Unit being the SUR Offer Price and Special Dividend.

3. BACKGROUND INFORMATION ON BPB AND THE FUND

3.1 Background information on BPB

3.1.1 Information on BPB and its principal activities

BPB was incorporated in Malaysia as a public limited company under the Companies Ordinance 1910 under the name Kuala Sidim Rubber Co. Ltd on 4 July 1946. On 15 April 1966, the company changed its name to Kuala Sidim Rubber Company Berhad and subsequently to Kuala Sidim Berhad on 12 December 1994. Kuala Sidim was officially listed on Bursa Securities (formerly known as the Kuala Lumpur Stock Exchange) and the Singapore Stock Exchange on 1 August 1973 respectively. In line with the national policy of promoting the listing of Malaysian public listed companies on Bursa Securities, Kuala Sidim was de-listed from the Singapore Stock Exchange effective from 1 January 1990. On 29 August 2003, Kuala Sidim Berhad was de-listed from Bursa Securities following a take-over offer by BHB for the remaining ordinary shares in Kuala Sidim Berhad not already owned by BHB. On 10 April 2004, Kuala Sidim Berhad changed its name to BPB.

6

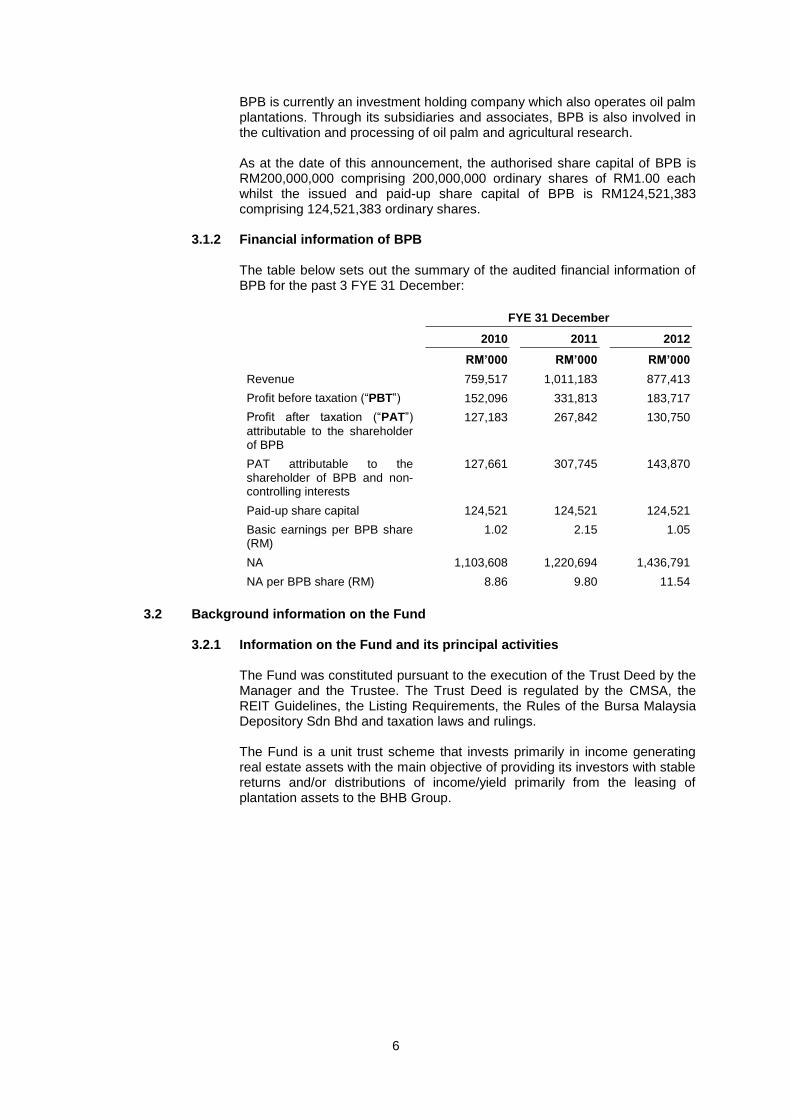

BPB is currently an investment holding company which also operates oil palm plantations. Through its subsidiaries and associates, BPB is also involved in the cultivation and processing of oil palm and agricultural research. As at the date of this announcement, the authorised share capital of BPB is RM200,000,000 comprising 200,000,000 ordinary shares of RM1.00 each whilst the issued and paid-up share capital of BPB is RM124,521,383 comprising 124,521,383 ordinary shares.

3.1.2 Financial information of BPB The table below sets out the summary of the audited financial information of BPB for the past 3 FYE 31 December:

FYE 31 December

2010 2011 2012

RM’000 RM’000 RM’000

Revenue 759,517 1,011,183 877,413

Profit before taxation (“PBT”) 152,096 331,813 183,717

Profit after taxation (“PAT”)

attributable to the shareholder of BPB

127,183 267,842 130,750

PAT attributable to the shareholder of BPB and non-controlling interests

127,661 307,745 143,870

Paid-up share capital 124,521 124,521 124,521

Basic earnings per BPB share (RM)

1.02 2.15 1.05

NA 1,103,608 1,220,694 1,436,791

NA per BPB share (RM) 8.86 9.80 11.54

3.2 Background information on the Fund

3.2.1 Information on the Fund and its principal activities The Fund was constituted pursuant to the execution of the Trust Deed by the Manager and the Trustee. The Trust Deed is regulated by the CMSA, the REIT Guidelines, the Listing Requirements, the Rules of the Bursa Malaysia Depository Sdn Bhd and taxation laws and rulings. The Fund is a unit trust scheme that invests primarily in income generating real estate assets with the main objective of providing its investors with stable returns and/or distributions of income/yield primarily from the leasing of plantation assets to the BHB Group.

7

3.2.2 Financial information on the Fund The table below sets out the summary of the audited financial information of the Fund for the past 3 FYE 31 December:

FYE 31 December

2010 2011 2012

RM’000 RM’000 RM’000

Revenue 75,022 99,556 90,500

PBT 82,075 305,799 91,620

PAT 82,075 305,799 91,620

Paid-up Unitholders’ capital 565,681 658,635 658,635

Earnings per Unit (RM)

- Realised 0.1217 0.1529 0.1207

- Unrealised 0.0257 0.3487 0.0254

NA (RM’000) 793,273 1,132,416 1,145,673

NA per Unit (RM) 1.4242 1.8064 1.8275

4. BASIS AND JUSTIFICATION OF THE DEEMED CONSIDERATION PRICE 4.1 For illustrative purposes only, a comparison of the Deemed Consideration Price

against the historical market prices of the Units in the Fund up to 12 July 2013, being the last trading date prior to the date of this announcement (“LTD”), is set out below:

Price per Unit

Deemed Consideration

Price

Premium of the Deemed

Consideration Price

RM RM RM %

Last transacted price on Bursa Securities as at the LTD

1.87 2.10 0.23 12.30

5-day volume weighted average market price (“VWAMP”) of the Units

in the Fund on Bursa Securities up to the LTD

1.85 2.10 0.25 13.51

1-month VWAMP of the Units in the Fund on Bursa Securities up to the LTD

1.84 2.10 0.26 14.13

3-month VWAMP of the Units in the Fund on Bursa Securities up to the LTD

1.88 2.10 0.22 11.70

6-month VWAMP of the Units in the Fund on Bursa Securities up to the LTD

1.88 2.10 0.22 11.70

4.2 For illustrative purposes only, the price-to-book multiple (“PB Multiple”) based on the Deemed Consideration Price over the Fund’s audited net assets (“NA”) per Unit as at 31 December 2012 is as follows:

NA per Unit

PB Multiple

RM times

Based on the audited NA of the Fund as at 31 December 2012 1.83 1.15

8

5. RATIONALE AND PROSPECTS 5.1 Proposed Amendment

The Proposed Amendment is undertaken to enable the implementation of the Proposed SUR subject to the exemption under and in accordance with Practice Note 44 of the Malaysian Code on Take-Overs and Mergers, 2010 (“Code”) and the conversion of the Fund to a private property trust upon completion of the Proposed SUR.

5.2 Proposed SUR and Special Dividend

The Fund was formed with the objectives of providing: (i) unitholders with an investment asset which provides a stable distribution of

income derived from the lease of the Fund’s plantation assets; and

(ii) long-term growth in the net asset value (“NAV”) per Unit of the Fund.

Since the listing of the Fund on the Official List of Bursa Securities on 8 February 2007, the Trustee, on behalf of the Fund, had undertaken the following acquisitions of plantation assets: (i) Malakoff Estate and Bebar Estate; and

(ii) Sutera Estate and Taiping Rubber Plantation (including Trong Oil Mill). The abovementioned acquisitions were made from the BHB Group. The Fund’s NAV had increased from RM1.00 per Unit on its listing date to RM1.83 per Unit as at 31 December 2012. The sustainability of the Fund’s objectives is dependent upon its ability to maintain its dividend yield, finance capital expenditure requirements in relation to its existing plantation assets, as well as financing plantation asset acquisitions in the future. The ability of the Fund to grow its mature plantation assets vis-à-vis yield sustainability, and hence deliver capital growth and stable distribution income to the unitholders in accordance with the objectives of the Fund, appears limited due to the following factors: (i) in pursuing growth through acquisitions, the Fund is currently facing the

challenge of maintaining its dividend yield to the unitholders in view of the scarcity and high market prices of mature plantation assets with prime yielding trees. Conversely, whilst plantation assets with younger tree profile may be acquired at lower prices, the high cost of maintenance and capital expenditure required to maintain the plantation assets, and the low yield from such plantation assets may have a dilutive effect on the Fund’s per Unit earnings. Moreover, as a real estate investment trust, the Fund is limited with regard to its ability to acquire non-yielding plantation assets;

(ii) the existing lease agreements between the lessors and the Fund are subject to, inter alia, automatic renewals over a 12-year period, comprising 4 tenancy terms of not exceeding 3 years each. Going forward, there is no assurance that the lease agreements will be renewed on comparable or more favourable terms. This may compromise the Fund’s ability to sustain its yield levels in the future; and

9

(iii) the Fund as a collective investment scheme distributes at least 90% of its distributable earnings to unitholders to qualify for tax exemption of its earnings. As such, the Fund is unable to retain sufficient internally generated funds to engage in growth strategies via acquisitions of mature plantation assets.

In view of the above, the Fund may be constrained from meeting its objectives in the future. The Proposed SUR and the subsequent conversion of the Fund to a private property trust will provide an avenue for BPB to merge and streamline the plantation assets of the BPB Group and the Fund under one entity, namely BPB, and as a preparatory step for the proposed listing of the enlarged BPB to be undertaken within the next 12 months, subject to, inter alia, the necessary approvals being obtained. In addition, the corporate integration of the Fund under BPB and the proposed listing of BPB will enable BPB to raise funds and access the equity capital market as well as provide the financial flexibility to pursue further growth opportunities. The Deemed Consideration Price of RM2.10 per Unit is close to the record high of the Units’ transacted price of RM2.16 per Unit on 24 August 2012 since the listing of the Fund in 2007 and as such, provides an attractive exit point for the unitholders of the Fund to realise capital gain on their investment in the Fund. In addition, the Units have experienced a relatively thin level of trading in the past whereby the average monthly trading volume of the Units on Bursa Securities over the past one (1)-year up to the LPD amounted to 4.2 million Units, representing approximately 1.43% of the Fund’s total free float shares (based on 290,990,000 Units, being the number of Units not held by BPB). Therefore, the Proposals would provide an opportunity to the Entitled Unitholders to realise their investments in the Fund in an efficient and expeditious manner at a premium to the market price of the Units.

6. INDUSTRY OVERVIEW AND OUTLOOK 6.1 Overview on the Malaysian economy

Amid the challenging global economic conditions, the Malaysian economy recorded a growth of 5.2% (compared to the second quarter of 2012 of 5.6%) during the third quarter of 2012. Growth was affected by slower external demand, which resulted in a further decline in net real exports of goods and services.

Domestic demand however, continued to sustain growth, supported by the favourable performance of private consumption and investment activity by both the private and public sectors. Domestic demand expanded by 11.4% in the third quarter of 2012 (compared to the second quarter of 2012 of 14.0%) supported by the favourable performance of private consumption and investment activity by both the private and public sectors. Private investment grew by 22.9% (compared to the second quarter of 2012 of 24.6%), supported by capital spending in the services sector, such as the transportation, real estate and utilities sub-sectors and the on-going implementation of projects in the oil and gas sector. Public investment expanded by 22.4% (compared to the second quarter of 2012 of 28.9%), driven by capital spending by the public enterprises (mostly, the non-financial public enterprises in the transportation, oil and gas, and utilities sectors). Private consumption grew at a continued strong pace of 8.5% in the third quarter (compared to the second quarter of 2012 of 8.8%) while public consumption moderated to 2.3% (2Q 2012: 10.9%), attributable to lower spending in supplies and services.

10

On the supply side, activities in most economic sectors moderated in the third quarter of 2012. Growth in the manufacturing sector slowed, weighed down by the weaker external environment while the mining sector contracted due to a sharp decline in natural gas production following a prolonged planned shutdown of several gas facilities for maintenance purposes. In the agriculture sector, growth turned positive in line with the recovery in crude palm oil production and strong output of food crops. The construction sector continued to record robust growth, while growth in the services sector expanded further, driven by firm domestic demand. Moving forward, recent economic indicators suggest some stabilisation in global growth. Nevertheless, risks remain arising from continued policy uncertainties in several key economies. In particular, policymakers in these economies face a challenging task of weighing crucial decisions on issues related to fiscal consolidation and key reforms to address the underlying structural weaknesses that impede economic recovery. (Source: Economic and Financial Developments in Malaysia in the Third Quarter of 2012, Bank Negara Malaysia)

In relation to the Malaysian economy, while the weakness in global economic conditions has affected growth in the third quarter, domestic demand continued to provide support to growth. The more challenging international environment would present risks to Malaysia’s growth prospects. Nevertheless, domestic demand is expected to continue to be the anchor of growth, supported by the expansion in private consumption and investment. Public spending and investment activity are also expected to lend support towards growth. The Malaysian economy is expected to strengthen further and projected to grow at a faster rate of 4.5% to 5.5% in 2013. This will be supported by improved exports and strong domestic demand on the assumption that global economic growth will pick up, especially during the second half of 2013. (Source: Economic Performance and Prospects, Economic Report 2012/2013, Ministry of Finance)

6.2 Overview on the oil plantation sector

Value-added of the oil palm sub-sector contracted to 8.6% during the first half of 2012 (January – June 2011: 6.5%), due to less favourable weather conditions and a natural production down cycle that constrained the output of Fresh Fruit Bunch (“FFB”). Despite higher oil extraction rates, the lower average FFB yield at 11.19 tonnes per hectare (January – August 2011: 12.52 tonnes per hectare) led to a lower output of Crude Palm Oil (“CPO”) by 7% to 11.2 million tonnes (January – August 2011: 8.2%, 12.million tonnes). However, the yield is expected to improve in the later part of the year, with the sub-sector registering a smaller contraction of 2.8% in 2012 (2011: 10.8%). (Source: Economic Performance and Prospects, Economic Report 2012/2013, Ministry of Finance)

The year 2012 was a challenging year for the Malaysian oil palm industry. During the first half of the year, the industry was faced with lower CPO production compared to the corresponding period of 2011 as FFB yielded low due to the stress on the trees after experiencing high FFB production in 2011, as well as high imports of palm oil. In the second half of the year, palm oil prices declined due to palm oil stock build-up arising from high carry-over stocks in the beginning of the year, increased CPO production as well as weaker export demand. Palm oil stocks reached 2.63 million tonnes at the end of December 2012, CPO production declined marginally to 18.79 million tonnes and imports increased to 1.39 million tonnes. Total exports of palm products was 24.56 million tonnes, an increase of 1.2% with palm kernel cake and oleochemical products registered an increase in exports, while palm oil recorded a

11

decline of 2.4% to 17.56 million tonnes. The average price of CPO for the year was RM2,764 per tonne, lower by 14.1% compared to RM3,219 in 2011, while export revenue of palm products declined by 11.2% to RM71.40 billion against RM80.41 billion recorded in 2011 due to lower export prices. The oil palm planted area in 2012 reached 5.08 million hectares, an increase of 1.5% against 5.00 million hectares recorded in 2011. This was mainly due to the increase in planted area in Sarawak, which recorded an increase of 5.3% or 54,651 hectares. Sabah is still the largest oil palm planted state, with 1.44 million hectares or 28.4% of total oil palm planted area, followed by Sarawak with 1.08 million hectares with 21.2%. Production of CPO in 2012 declined marginally by 0.7% to 18.79 million tonnes, with Peninsular Malaysia’s production declined marginally by 0.5% to 10.32 million tonnes, while Sabah declined by 5.1% to 5.54 million tonnes. Sarawak, on the other hand registered an increase of 8.4% to 2.92 million tonnes due to new areas coming into production. Palm oil stocks in 2012 was higher by 27.7% to close at 2.63 million tonnes as compared to 2.06 million tonnes recorded in 2011. The high closing stock was attributed to the high palm oil opening stocks, increased in palm oil imports by 6.5% and decline in palm oil exports by 2.4%. Palm oil imports rose due to the need to supplement the decline in palm oil production (0.7%) to 18.79 million tonnes compared to 18.91 million tonnes in 2011 as well as to cater demand for further processing (local and export). Total exports of oil palm products, consisting of palm oil, palm kernel oil, palm kernel cake, oleochemicals, biodiesel and finished products increased marginally by 1.2% or 0.29 million tonnes to 24.56 million tonnes in 2012 from 24.27 million tonnes recorded in 2011. Total export revenue, however declined by 11.2% or RM9.02 billion to RM71.40 billion compared to the RM80.41 billion achieved in 2011 due to lower export prices. (Source: Overview of the Malaysian Oil Palm Industry 2012, Malaysian Palm Oil Board)

7. RISK FACTORS Save as disclosed below, the Proposals are not expected to materially change the risk profile of the BHB Group’s business as the BHB Group owns the majority of the Units in the Fund and is exposed to similar business risks of one of the key business segments of the BHB Group. The Proposals are subject to, amongst others, the approval from the shareholders of BHB, the unitholders of the Fund, the SC and Bursa Securities as set out in Section 9 of this announcement. In the event that these approvals are not obtained, the Fund will not be able to implement the Proposals. Nevertheless, the Boards of BHB and BPB will take reasonable steps to procure the aforesaid approvals in order to implement the Proposals.

8. EFFECTS OF THE PROPOSALS 8.1 Share capital and substantial shareholders’ shareholdings

The Proposals does not involve to any issuance of new BHB shares, and correspondingly, will not have any effect on the issued and paid-up share capital and the shareholdings of substantial shareholders of BHB.

12

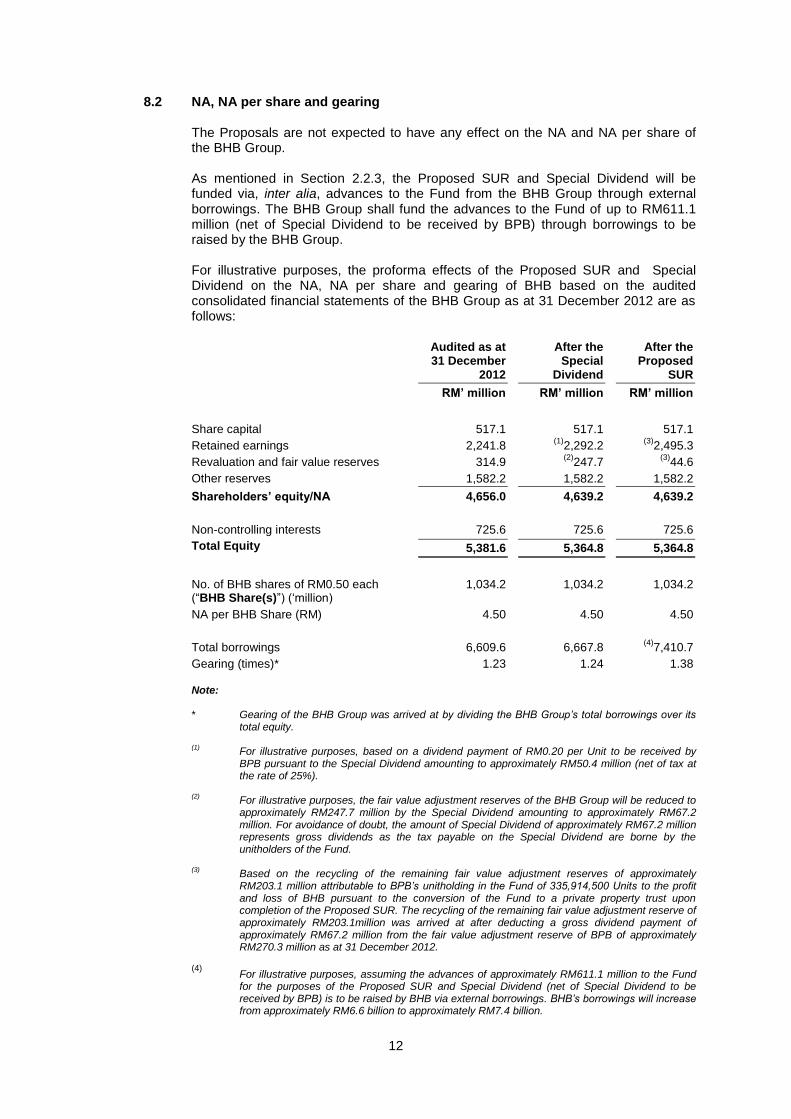

8.2 NA, NA per share and gearing

The Proposals are not expected to have any effect on the NA and NA per share of the BHB Group. As mentioned in Section 2.2.3, the Proposed SUR and Special Dividend will be funded via, inter alia, advances to the Fund from the BHB Group through external borrowings. The BHB Group shall fund the advances to the Fund of up to RM611.1 million (net of Special Dividend to be received by BPB) through borrowings to be raised by the BHB Group. For illustrative purposes, the proforma effects of the Proposed SUR and Special Dividend on the NA, NA per share and gearing of BHB based on the audited consolidated financial statements of the BHB Group as at 31 December 2012 are as follows:

Audited as at 31 December

2012

After the Special

Dividend

After the Proposed

SUR

RM’ million RM’ million RM’ million

Share capital 517.1 517.1 517.1

Retained earnings 2,241.8 (1)

2,292.2 (3)

2,495.3

Revaluation and fair value reserves 314.9 (2)

247.7 (3)

44.6

Other reserves 1,582.2 1,582.2 1,582.2

Shareholders’ equity/NA 4,656.0 4,639.2 4,639.2

Non-controlling interests 725.6 725.6 725.6

Total Equity 5,381.6 5,364.8 5,364.8

No. of BHB shares of RM0.50 each (“BHB Share(s)”) (‘million)

1,034.2 1,034.2 1,034.2

NA per BHB Share (RM) 4.50 4.50 4.50

Total borrowings 6,609.6 6,667.8 (4)

7,410.7

Gearing (times)* 1.23 1.24 1.38 Note: * Gearing of the BHB Group was arrived at by dividing the BHB Group’s total borrowings over its

total equity. (1)

For illustrative purposes, based on a dividend payment of RM0.20 per Unit to be received by BPB pursuant to the Special Dividend amounting to approximately RM50.4 million (net of tax at the rate of 25%).

(2) For illustrative purposes, the fair value adjustment reserves of the BHB Group will be reduced to

approximately RM247.7 million by the Special Dividend amounting to approximately RM67.2 million. For avoidance of doubt, the amount of Special Dividend of approximately RM67.2 million represents gross dividends as the tax payable on the Special Dividend are borne by the unitholders of the Fund.

(3) Based on the recycling of the remaining fair value adjustment reserves of approximately

RM203.1 million attributable to BPB’s unitholding in the Fund of 335,914,500 Units to the profit and loss of BHB pursuant to the conversion of the Fund to a private property trust upon completion of the Proposed SUR. The recycling of the remaining fair value adjustment reserve of approximately RM203.1million was arrived at after deducting a gross dividend payment of approximately RM67.2 million from the fair value adjustment reserve of BPB of approximately RM270.3 million as at 31 December 2012.

(4) For illustrative purposes, assuming the advances of approximately RM611.1 million to the Fund

for the purposes of the Proposed SUR and Special Dividend (net of Special Dividend to be received by BPB) is to be raised by BHB via external borrowings. BHB’s borrowings will increase from approximately RM6.6 billion to approximately RM7.4 billion.

13

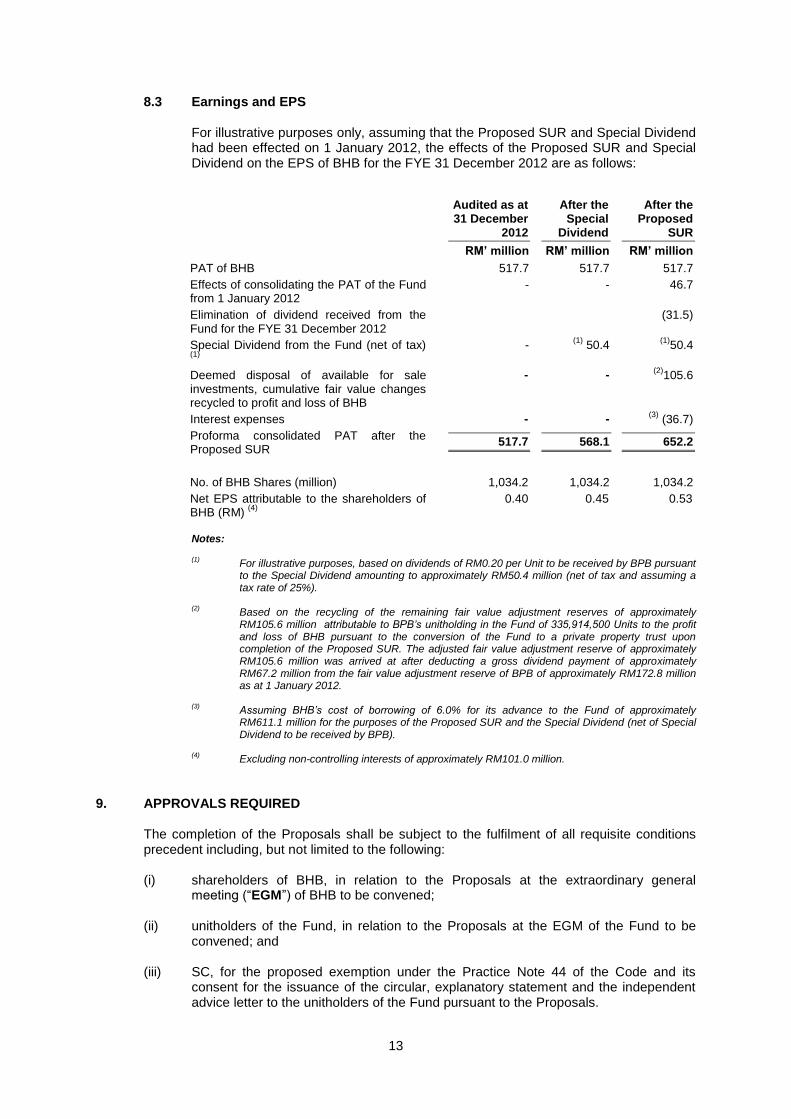

8.3 Earnings and EPS For illustrative purposes only, assuming that the Proposed SUR and Special Dividend had been effected on 1 January 2012, the effects of the Proposed SUR and Special Dividend on the EPS of BHB for the FYE 31 December 2012 are as follows:

Audited as at 31 December

2012

After the Special

Dividend

After the Proposed

SUR

RM’ million RM’ million RM’ million

PAT of BHB 517.7 517.7 517.7

Effects of consolidating the PAT of the Fund from 1 January 2012

- - 46.7

Elimination of dividend received from the Fund for the FYE 31 December 2012

(31.5)

Special Dividend from the Fund (net of tax) (1)

-

(1) 50.4

(1)50.4

Deemed disposal of available for sale investments, cumulative fair value changes recycled to profit and loss of BHB

- - (2)

105.6

Interest expenses - - (3)

(36.7)

Proforma consolidated PAT after the Proposed SUR

517.7 568.1 652.2

No. of BHB Shares (million) 1,034.2 1,034.2 1,034.2

Net EPS attributable to the shareholders of BHB (RM)

(4)

0.40 0.45 0.53

Notes: (1)

For illustrative purposes, based on dividends of RM0.20 per Unit to be received by BPB pursuant to the Special Dividend amounting to approximately RM50.4 million (net of tax and assuming a tax rate of 25%).

(2) Based on the recycling of the remaining fair value adjustment reserves of approximately

RM105.6 million attributable to BPB’s unitholding in the Fund of 335,914,500 Units to the profit and loss of BHB pursuant to the conversion of the Fund to a private property trust upon completion of the Proposed SUR. The adjusted fair value adjustment reserve of approximately RM105.6 million was arrived at after deducting a gross dividend payment of approximately RM67.2 million from the fair value adjustment reserve of BPB of approximately RM172.8 million as at 1 January 2012.

(3)

Assuming BHB’s cost of borrowing of 6.0% for its advance to the Fund of approximately RM611.1 million for the purposes of the Proposed SUR and the Special Dividend (net of Special Dividend to be received by BPB).

(4)

Excluding non-controlling interests of approximately RM101.0 million.

9. APPROVALS REQUIRED The completion of the Proposals shall be subject to the fulfilment of all requisite conditions precedent including, but not limited to the following: (i) shareholders of BHB, in relation to the Proposals at the extraordinary general

meeting (“EGM”) of BHB to be convened;

(ii) unitholders of the Fund, in relation to the Proposals at the EGM of the Fund to be convened; and

(iii) SC, for the proposed exemption under the Practice Note 44 of the Code and its consent for the issuance of the circular, explanatory statement and the independent advice letter to the unitholders of the Fund pursuant to the Proposals.

14

The Proposed Amendment, Proposed SUR and the Special Dividend are inter-conditional with each other. In terms of the implementation of the Proposals, the Special Dividend will be implemented prior to the Proposed SUR.

The Proposals will become effective upon registration of the amended Trust Deed with the SC. The payment of the Deemed Consideration Price to the unitholders will be made as soon as practicable following the registration of the amended Trust Deed. The applications to be made to the relevant authorities are expected to be made within 4 months from the date of this announcement.

10. ESTIMATED TIMEFRAME FOR COMPLETION OF THE PROPOSALS Barring any unforeseen circumstances, the Proposals are expected to be completed by end of 2013.

11. DIRECTORS’ AND MAJOR SHAREHOLDERS’ INTERESTS Save as disclosed below, to the best knowledge of BHB, there are no other directors of BHB, major shareholders of BHB and/or persons connected to them who are interested in the Proposals. Tan Sri Dato’ Seri Lodin bin Wok Kamaruddin (“TSLWK”), is the Chief Executive of LTAT, the Deputy Chairman and Group Managing Director of BHB, and the Chairman of the Board of the Manager. As at the LPD, he holds 28,192,758 BHB Shares or approximately 2.73% equity interest in BHB and is also a unitholder in the Fund with direct holdings of 250,000 Units or approximately 0.04% interest in the Fund. In view of this, TSLWK is an interested Director in the Proposals. As such, TSLWK has abstained from all deliberations and voting on the Proposals at the relevant Board meeting of BHB. TSLWK will also abstain from voting in respect of his shareholdings in BHB on the resolutions for the Proposals to be tabled at the EGM of BHB to be convened. In addition, TSLWK will ensure that all persons connected to him will abstain from voting in respect of their direct and indirect shareholdings in BHB pertaining to the Proposals at the EGM of BHB to be convened. As at the LPD, LTAT is a major shareholder of BHB with 61.47% equity interest in BHB and is also a unitholder in the Fund. As at the LPD, LTAT holds 635,739,809 BHB shares and 79,620,200 Units in the Fund respectively. In this regard, LTAT is an interested major shareholder pursuant to the Proposals. LTAT will abstain from voting in respect of its shareholdings in BHB on the resolutions for the Proposals to be tabled at the EGM of BHB to be convened. In addition, LTAT will ensure that all persons connected to it will abstain from voting in respect of their direct and indirect shareholdings in BHB pertaining to the Proposals at the EGM of BHB to be convened.

15

12. STATEMENT OF THE AUDIT COMMITTEE The Audit Committee of BHB, having considered all aspects of the Proposals is of the opinion that the Proposals are: (i) in the best interest of BHB; (ii) fair and reasonable and based on normal commercial terms; and (iii) not detrimental to the interest of the non-interested shareholders of BHB. In arriving at its views above, the Audit Committee had taken into consideration, among others, the following: (i) the basis of arriving at the Deemed Consideration Price of the Proposals as set out in

Section 4 above;

(ii) the financial effects of the Proposals; (iii) the rationale and prospects for the Proposals as set out in Sections 5 and 6

respectively above; and

(iv) the evaluation of the Proposals by PIBB. In forming its view, the Audit Committee has sought the independent advice of PIBB.

13. DIRECTORS’ STATEMENT

The Board (save for TSLWK being the interested Director), having considered all aspects of the Proposals is of the opinion that the Proposals are in the best interest of BHB.

14. HIGHEST PERCENTAGE RATIO The highest percentage ratio as set out in Paragraph 10.02(g) of the Listing Requirements in relation to the Proposals is approximately 24.61%.

15. TOTAL AMOUNT TRANSACTED WITH RELATED PARTIES FOR THE PRECEDING 12 MONTHS The total amount transacted between LTAT and its subsidiaries and the BHB Group and/or persons connected to them for the preceding 12 months was approximately RM200.6 million.

16. ADVISERS AFFIN Investment has been appointed as the Principal Adviser to BHB for the Proposals. PIBB has been appointed by BHB to act as the independent adviser to advise the non-interested directors and shareholders of BHB on the Proposals.

16

17. RELATED PARTY TRANSACTIONS In view of the interest of TSLWK and LTAT as set out in Section 11 above, the Proposals are a related party transaction under Chapter 10 of the Listing Requirements. Pursuant to Paragraph 10.08(2) of the Listing Requirements, PIBB has been appointed by BHB as the independent adviser to advise the non-interested directors and shareholders of BHB on whether the terms of the Proposals are fair and reasonable, and whether the Proposals are detrimental to the non-interested shareholders of BHB.

18. DOCUMENT FOR INSPECTION

The SUR Proposal Letter dated 16 July 2013 is available for inspection during normal office hours at the registered office of BHB located on 28th Floor, Menara Boustead 69, Jalan Raja Chulan, 50200 Kuala Lumpur, Malaysia from Mondays to Fridays (except for public holidays) for a period of three (3) months from the date of this announcement.

This announcement is dated 16 July 2013.