Embed Size (px)

Citation preview

AFFIN BANK BERHAD (25046-T)

Annual Report 2012

Banking is

About...

Banking is About...At AffinBAnk, we remove the boundaries within the processes of banking and focus on customer centricity. We reach out to our customers, improve relationships with them and ensure that each one of them feels privileged and has the best of service from us. We set ourselves apart in this industry through a concerted effort to understanding our customers, listening to them, then delivering the most appropriate financial solutions. Simply put, banking is about you and your continued satisfied relationship with us.

Corporate informationCorporate Structure

Board of Directors & MD/CEOProfile of DirectorsManagement Team

Management Team ProfilesChairman’s Statement

Performance Reviewfinancial Highlights

Corporate DiaryStatement of Corporate Governance

Statement on internal ControlAudit & Examination Committee

network of Branchesnotice of Annual General Meeting

financial Statements

12131416202226303334364346485456

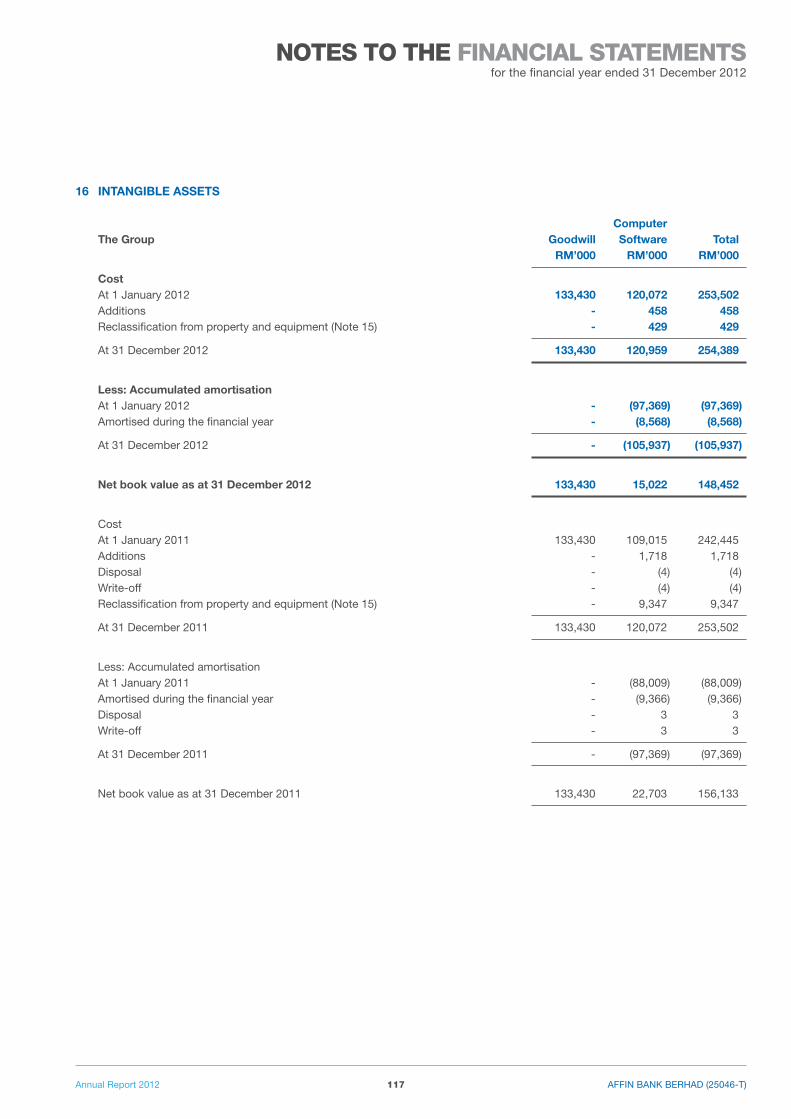

Contents

... Banking Without Barriers™

• Creativity

• Discip

line

• Integrity

• Hum

ility

• Carin

gOur Vision

Our Mission

A Premier Partner for financial Growth and innovative Services.

To provide innovative financial solutions and services to target customers in order to generate profits and create value for our shareholders and other stakeholders.

in so doing, we provide opportunities for employees to contribute and excel; and be competitive in providing our solutions and services to our valued customers.

We shall conduct our business with integrity and professionalism in compliance with good corporate governance principles and practices.

• Creativity

• Discip

line

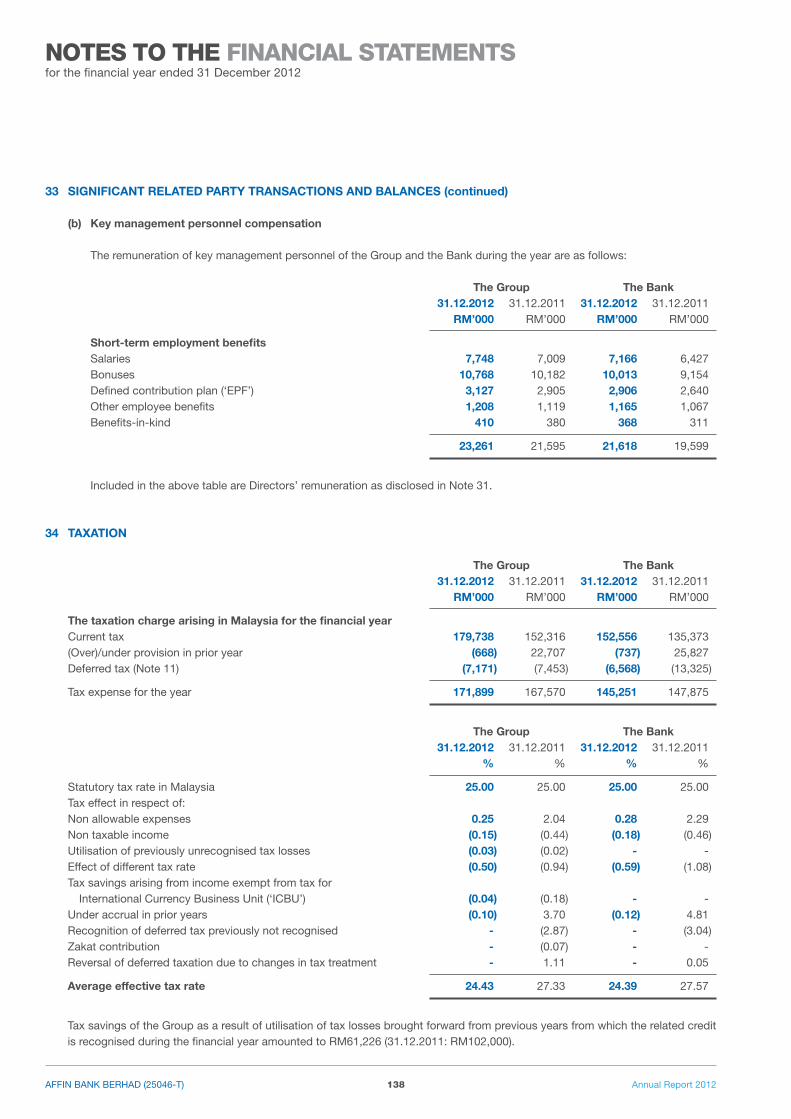

• Integrity

• Hum

ility

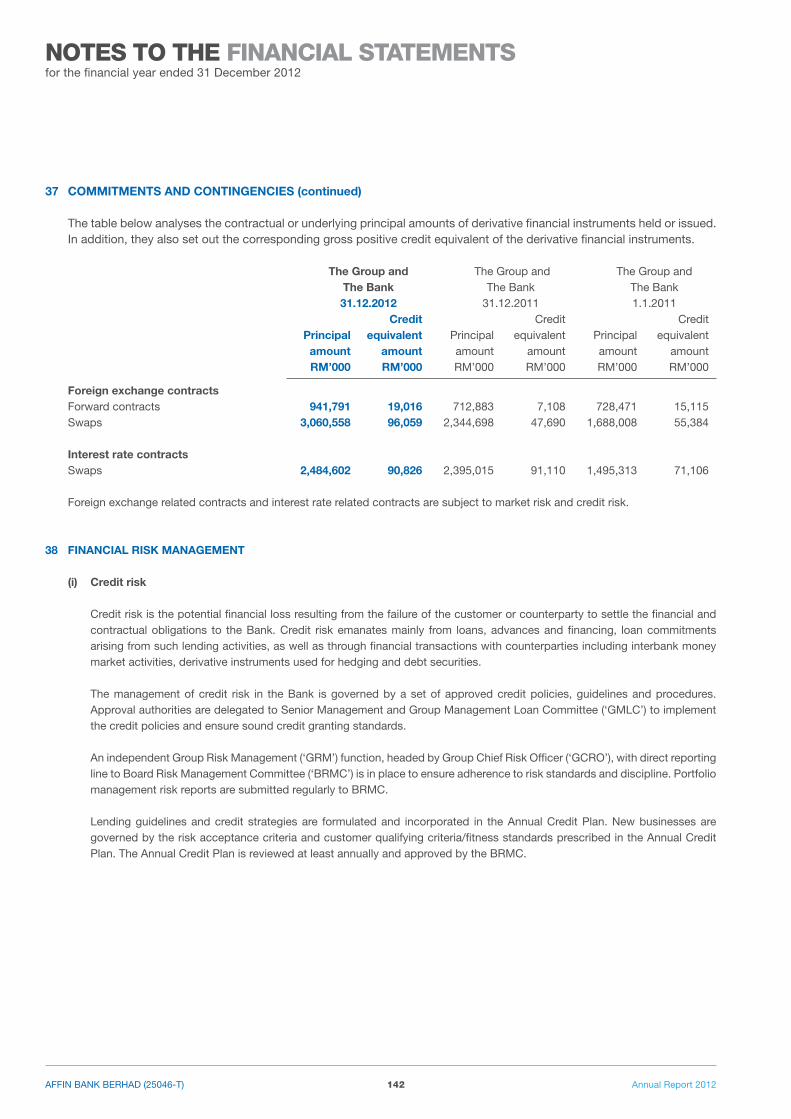

• Carin

g

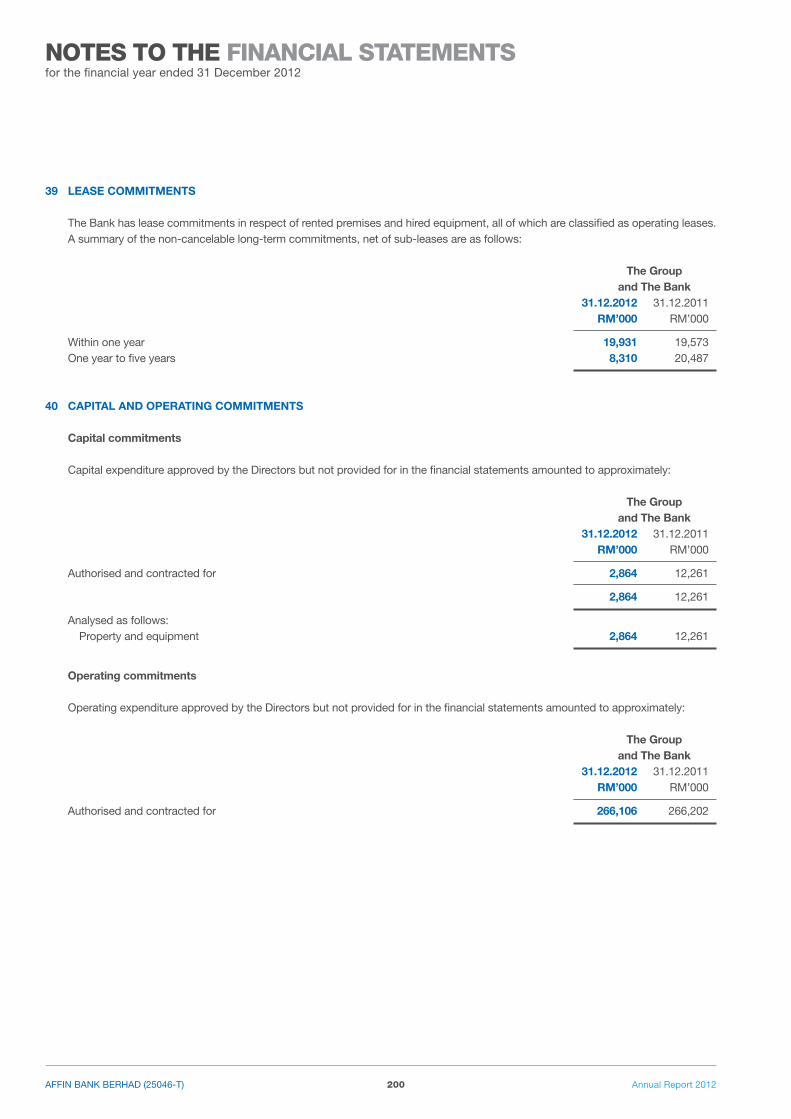

We are passionate in all that we do. A passion to achieve more, be better and to have that focused discipline to be able to carry forth a service that our customers deserve and require.

Banking is about being passionate

• Creativity

• Integrity

• Hum

ility

• Carin

g

Banking is about adding values

It’s not just about numbers, nor a focus on the bottom line only. Our belief is in delivering a trust that is self evident in the way we service each of our customers...a genuine courtesy and respect which comes from a desire to deliver more.

• Creativity

• Hum

ility

• Carin

g

Banking is about bringing smiles

We understand that when we are able to consistently provide financial solutions for our customers, when they know they can trust a bank that delivers more for them – that’s when we are truly satisfied that we have fulfilled our goals.

• Creativity

• Carin

g

Banking is about being thoughtful

It’s a genuine care for our customers that truly makes a difference – listening to them, understanding them and finally delivering our promises – now that’s a bank that goes beyond barriers.

• Creativity

Banking is about being imaginative

No two financial challenges are ever the same. It requires a deep understanding of the situation and innovative solutions. At AFFINBANK, we look beyond the standard to provide financial solutions to our many customers.

Affin BAnk BERHAD (25046-T) 12 Annual Report 2012

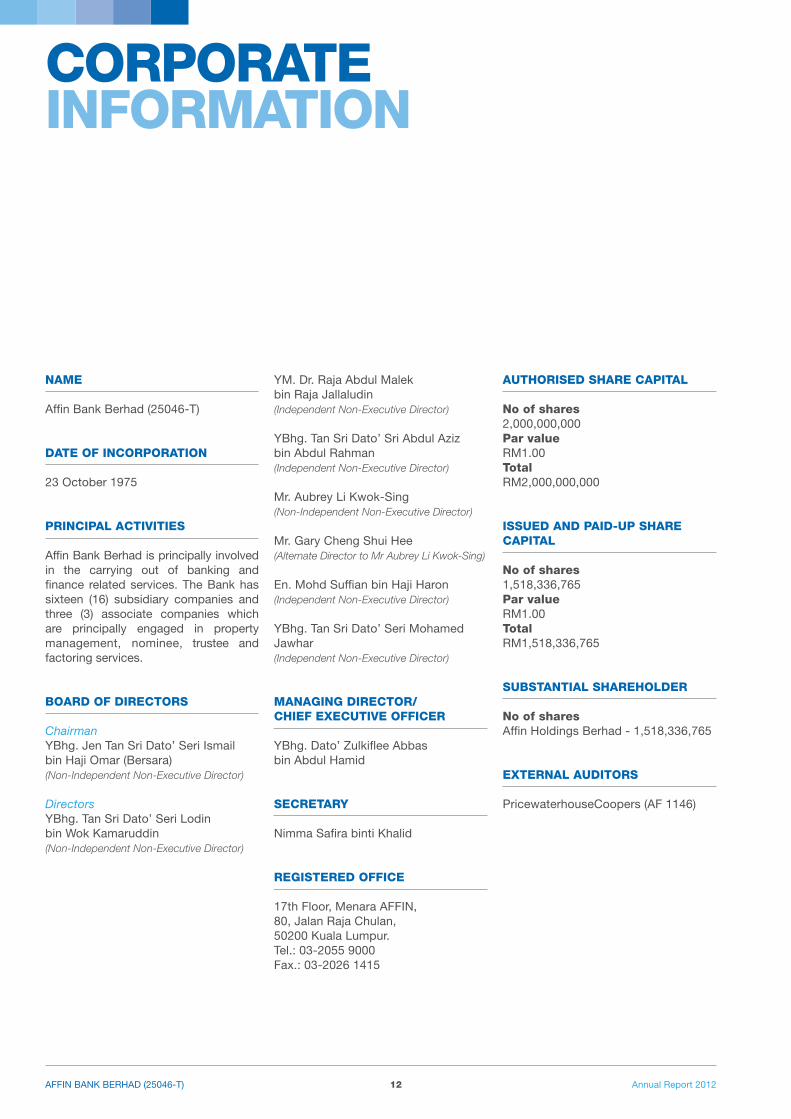

CORPORATE INFORMATION

NAME

Affin Bank Berhad (25046-T)

DATE OF INCORPORATION

23 October 1975

PRINCIPAL ACTIVITIES

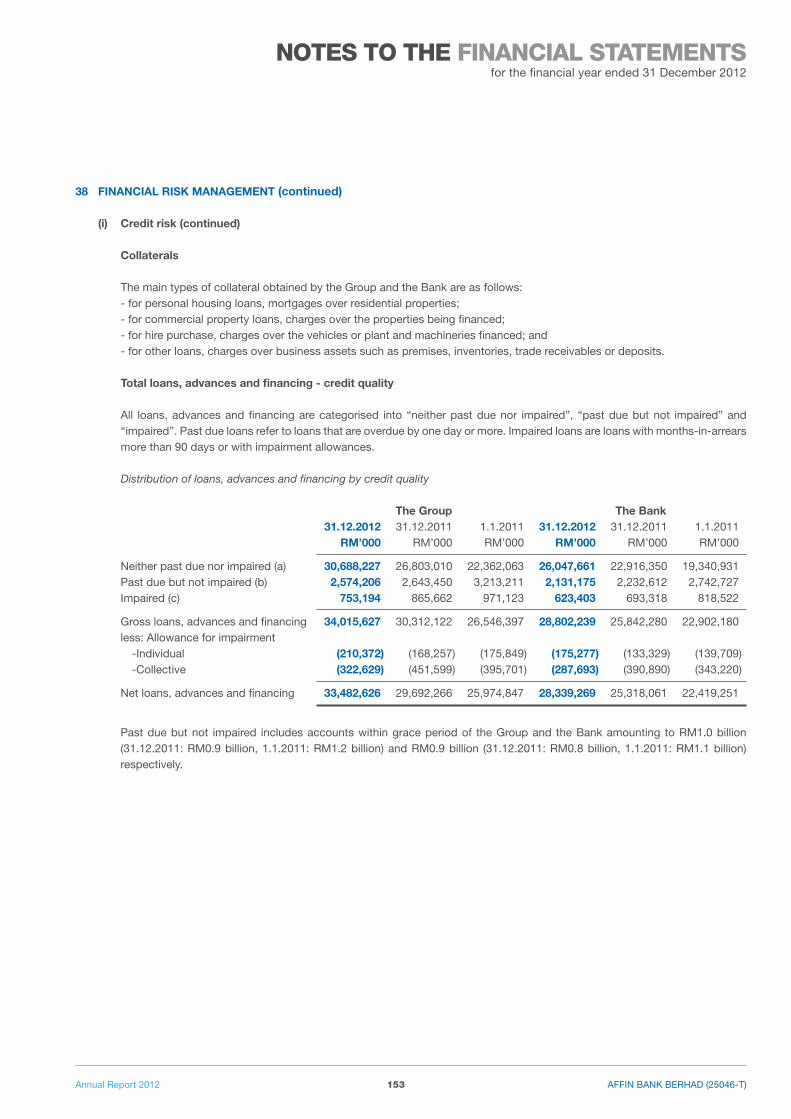

Affin Bank Berhad is principally involved in the carrying out of banking and finance related services. The Bank has sixteen (16) subsidiary companies and three (3) associate companies which are principally engaged in property management, nominee, trustee and factoring services.

BOARD OF DIRECTORS

ChairmanYBhg. Jen Tan Sri Dato’ Seri ismail bin Haji Omar (Bersara)(Non-Independent Non-Executive Director)

DirectorsYBhg. Tan Sri Dato’ Seri Lodin bin Wok kamaruddin(Non-Independent Non-Executive Director)

YM. Dr. Raja Abdul Malek bin Raja Jallaludin(Independent Non-Executive Director)

YBhg. Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman(Independent Non-Executive Director)

Mr. Aubrey Li kwok-Sing(Non-Independent Non-Executive Director)

Mr. Gary Cheng Shui Hee (Alternate Director to Mr Aubrey Li Kwok-Sing)

En. Mohd Suffian bin Haji Haron (Independent Non-Executive Director)

YBhg. Tan Sri Dato’ Seri Mohamed Jawhar(Independent Non-Executive Director)

MANAgINg DIRECTOR/CHIEF ExECuTIVE OFFICER

YBhg. Dato’ Zulkiflee Abbas bin Abdul Hamid

SECRETARY

nimma Safira binti khalid

REgISTERED OFFICE

17th floor, Menara Affin,80, Jalan Raja Chulan,50200 kuala Lumpur.Tel.: 03-2055 9000fax.: 03-2026 1415

AuTHORISED SHARE CAPITAL

No of shares2,000,000,000Par valueRM1.00TotalRM2,000,000,000

ISSuED AND PAID-uP SHARE CAPITAL

No of shares1,518,336,765Par valueRM1.00TotalRM1,518,336,765

SuBSTANTIAL SHAREHOLDER

No of sharesAffin Holdings Berhad - 1,518,336,765

ExTERNAL AuDITORS

PricewaterhouseCoopers (Af 1146)

Affin BAnk BERHAD (25046-T)13Annual Report 2012

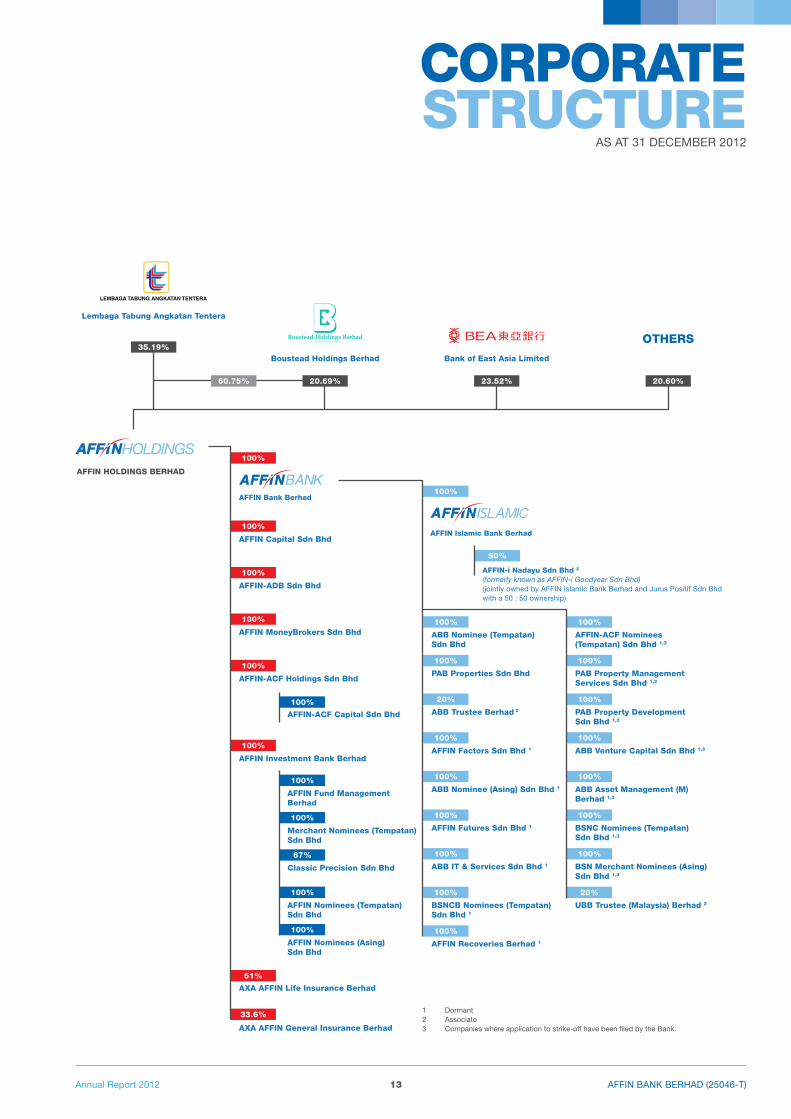

CORPORATE STRuCTuRE

AS AT 31 DECEMBER 2012

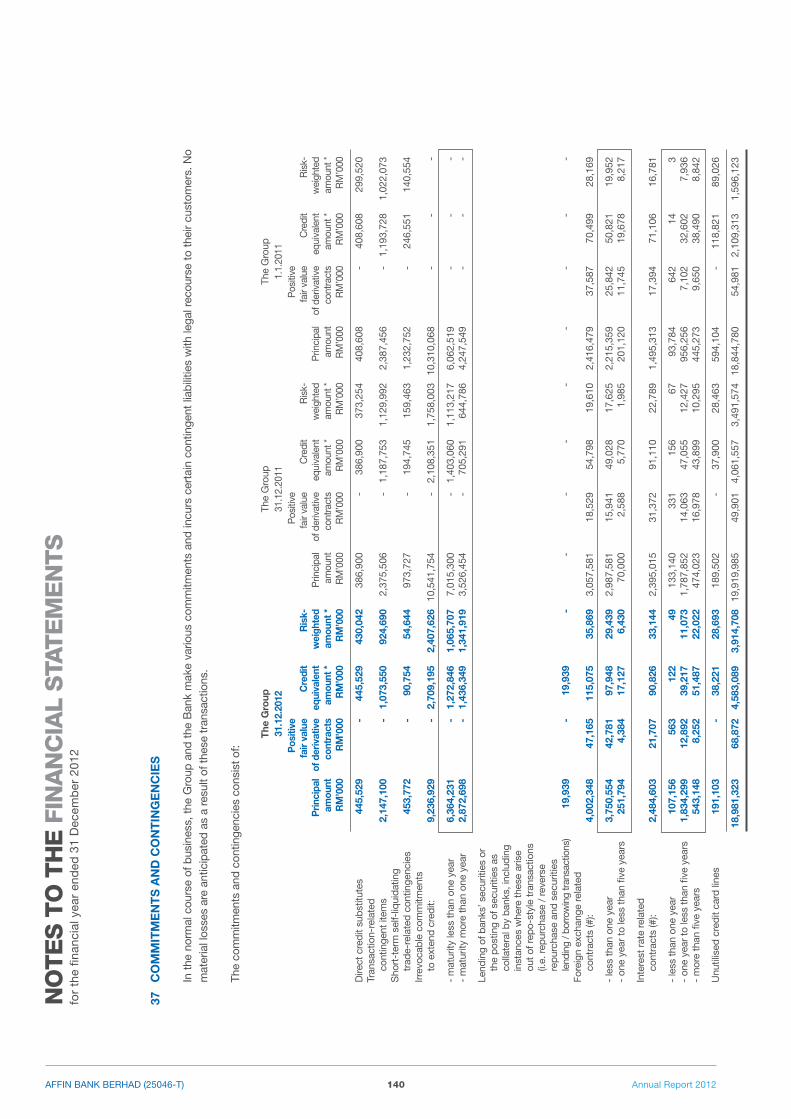

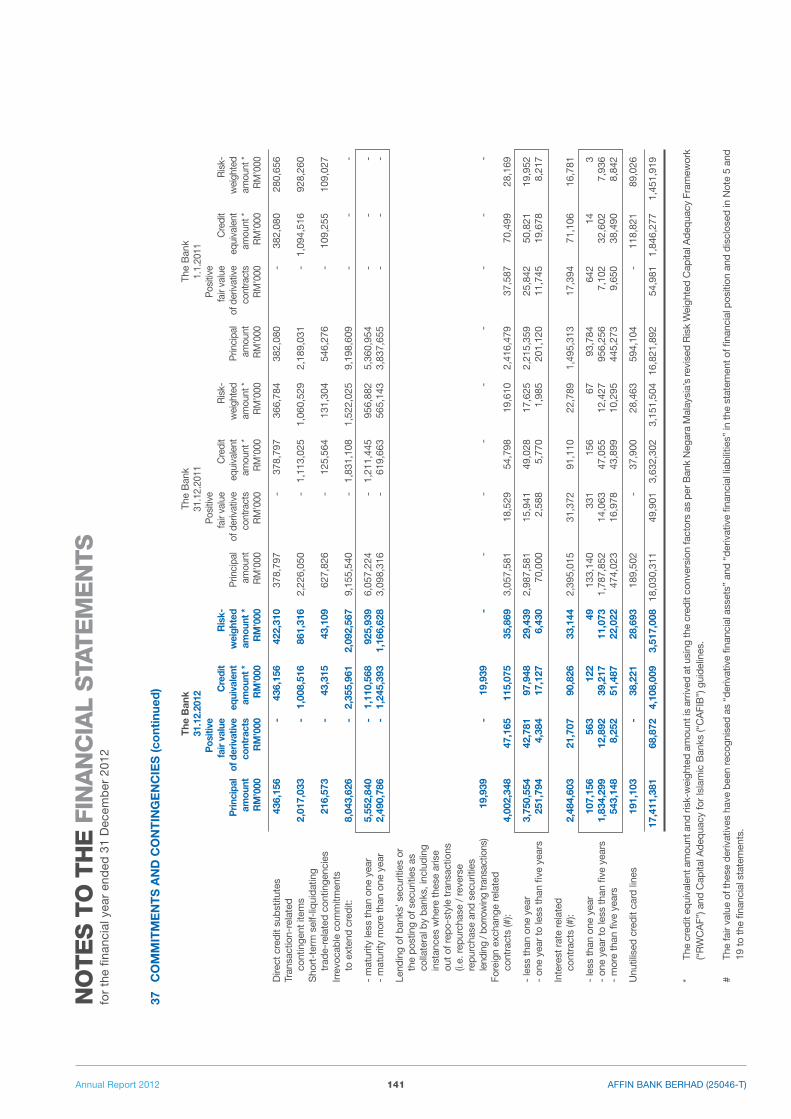

1 Dormant 2 Associate3 Companies where application to strike-off have been filed by the Bank.

OTHERS

AFFIN HOLDINgS BERHAD

AFFIN Bank Berhad

AFFIN Islamic Bank Berhad

Lembaga Tabung Angkatan Tentera

AFFIN Capital Sdn Bhd

AxA AFFIN Life Insurance Berhad

AxA AFFIN general Insurance Berhad

AFFIN-ADB Sdn Bhd

AFFIN MoneyBrokers Sdn Bhd

AFFIN-ACF Holdings Sdn Bhd

AFFIN Investment Bank Berhad

AFFIN-ACF Capital Sdn Bhd

AFFIN-i Nadayu Sdn Bhd 2

(formerly known as AFFIN-i Goodyear Sdn Bhd)(jointly owned by Affin islamic Bank Berhad and Jurus Positif Sdn Bhd with a 50 : 50 ownership)

AFFIN Fund Management Berhad

Merchant Nominees (Tempatan) Sdn Bhd

Classic Precision Sdn Bhd

AFFIN Nominees (Tempatan) Sdn Bhd

AFFIN Nominees (Asing)Sdn Bhd

Boustead Holdings Berhad Bank of East Asia Limited

100%

51%

33.6%

100%

100%

100%

PAB Properties Sdn Bhd

ABB Trustee Berhad 2

AFFIN Futures Sdn Bhd 1

ABB IT & Services Sdn Bhd 1

BSNCB Nominees (Tempatan)Sdn Bhd 1

AFFIN Recoveries Berhad 1

100%

100%

20%

100%

100%

100%

100%

100%

100%

ABB Nominee (Tempatan) Sdn Bhd

AFFIN-ACF Nominees (Tempatan) Sdn Bhd 1,3

AFFIN Factors Sdn Bhd 1

ABB Nominee (Asing) Sdn Bhd 1

PAB Property Management Services Sdn Bhd 1,3

PAB Property Development Sdn Bhd 1,3

ABB Venture Capital Sdn Bhd 1,3

ABB Asset Management (M) Berhad 1,3

BSNC Nominees (Tempatan) Sdn Bhd 1,3

BSN Merchant Nominees (Asing)Sdn Bhd 1,3

uBB Trustee (Malaysia) Berhad 2

100%

100%

100%

100%

100%

100%

100%

20%

100%

100%

100%

50%

100%

100%

67%

100%

100%

100%

35.19%

60.75% 20.69% 23.52% 20.60%

Affin BAnk BERHAD (25046-T) 14 Annual Report 2012

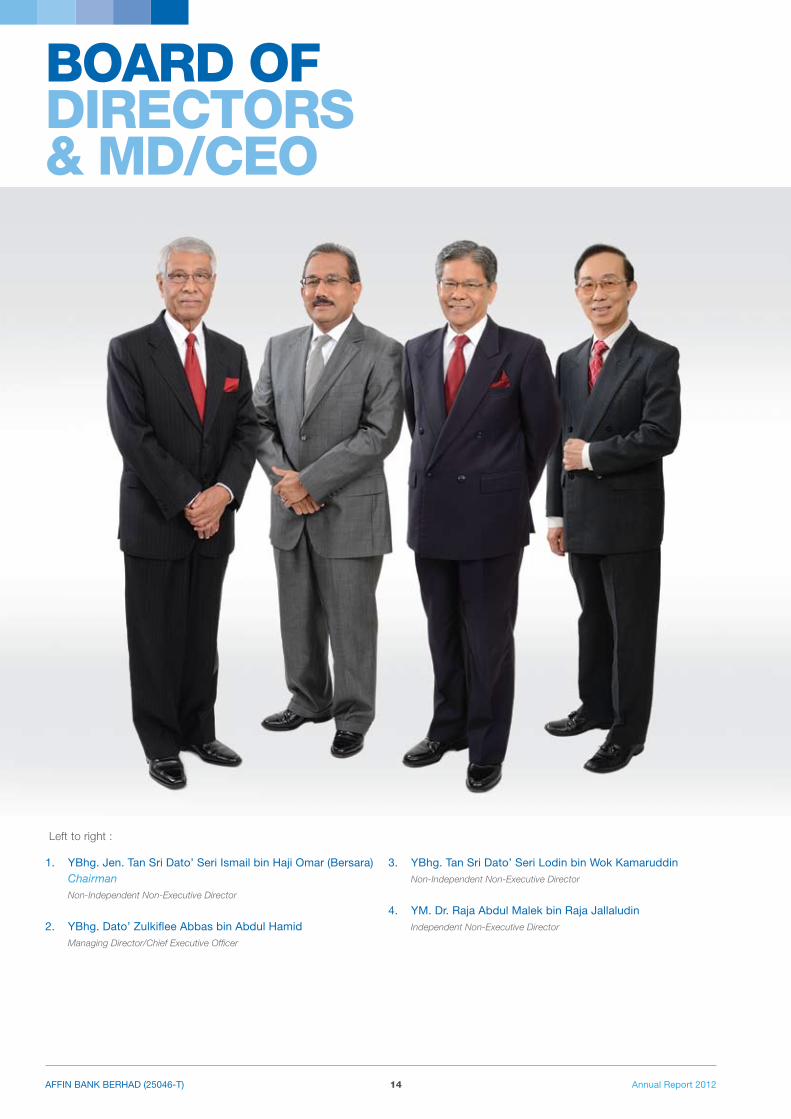

1. YBhg. Jen. Tan Sri Dato’ Seri ismail bin Haji Omar (Bersara) Chairman Non-Independent Non-Executive Director

2. YBhg. Dato’ Zulkiflee Abbas bin Abdul Hamid Managing Director/Chief Executive Officer

Left to right :

3. YBhg. Tan Sri Dato’ Seri Lodin bin Wok kamaruddin Non-Independent Non-Executive Director

4. YM. Dr. Raja Abdul Malek bin Raja Jallaludin Independent Non-Executive Director

BOARD OF DIRECTORS & MD/CEO

Affin BAnk BERHAD (25046-T)15Annual Report 2012

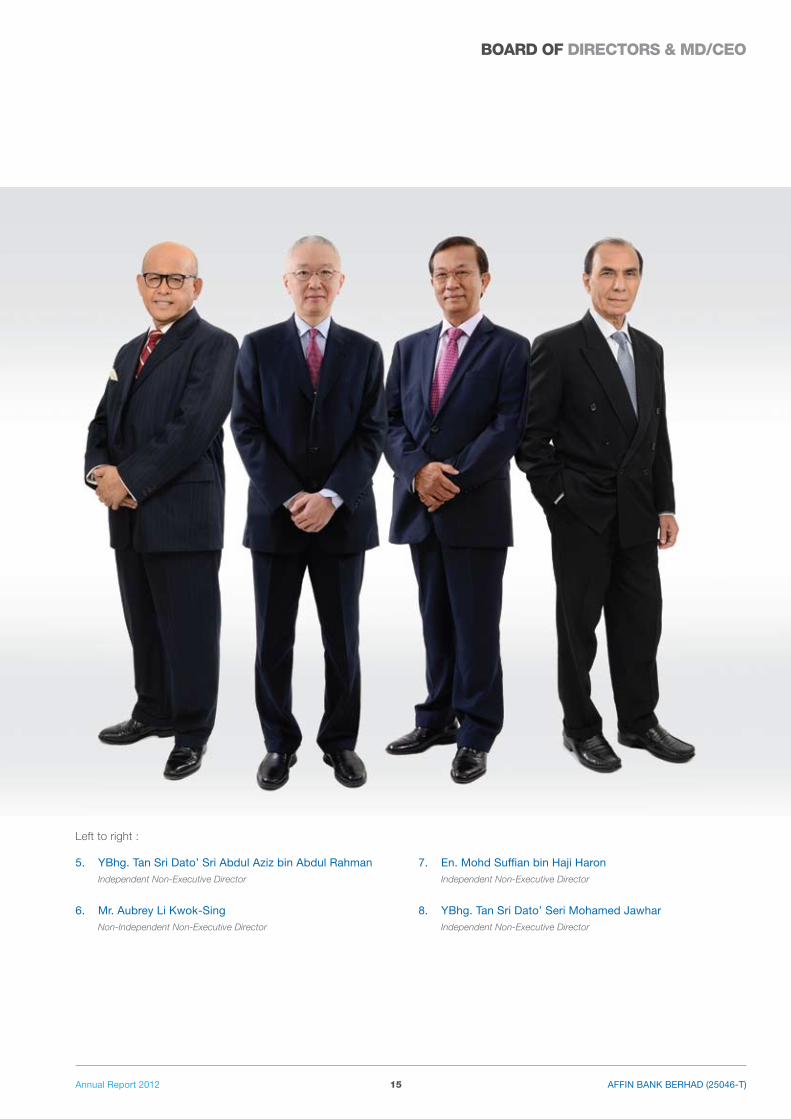

Left to right :

5. YBhg. Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman Independent Non-Executive Director

6. Mr. Aubrey Li kwok-Sing Non-Independent Non-Executive Director

7. En. Mohd Suffian bin Haji Haron Independent Non-Executive Director

8. YBhg. Tan Sri Dato’ Seri Mohamed Jawhar Independent Non-Executive Director

BOARD OF DIRECTORS & MD/CEO

Affin BAnk BERHAD (25046-T) 16 Annual Report 2012

PROFILE OF DIRECTORS

YBHg. JEN. TAN SRI DATO’ SERI ISMAIL BIN HAJI OMAR (BERSARA)

Chairman / Non-Independent Non-Executive Director

Jen. Tan Sri Dato’ Seri ismail bin Haji Omar (Bersara), aged 71, was appointed as a Director and Chairman of AffinBAnk on 21 May 2002.

He was formerly Chief Defence forces (CDf) Malaysia from 1995 until his retirement in 1998, after 38 years of military service. He graduated from Royal Military Academy, Sandhurst, United kingdom in 1961 and subsequently attended professional and management development courses at several institutions including The Land forces Command and Staff College, Canada; the United nation international Peace Academy, Vienna; the national Defence College, india and inTAn Malaysia.

His military service saw key Command and Staff appointments at all levels of the Armed forces. As CDf, his responsibilities included key roles in Malaysia’s Regional and international Defence Relations.

He was the Chairman of Affin Holdings Berhad and Affin-ACf finance Berhad from 1999 prior to joining AffinBAnk. He currently holds directorships in Affin islamic Bank Berhad, ABB Trustee Berhad, EP Engineering Sdn Bhd and Global Medical Alliance Sdn Bhd.

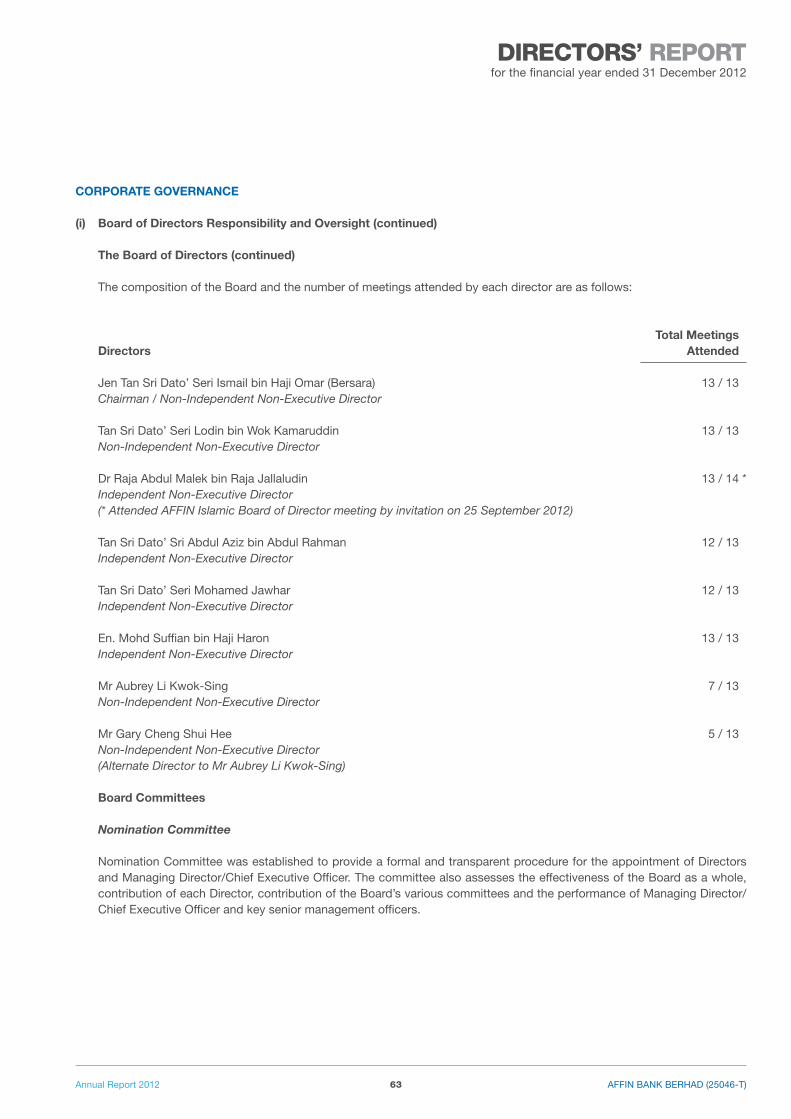

Jen. Tan Sri Dato’ Seri ismail bin Haji Omar (Bersara) attended all 13 Board Meetings held during the financial year ended 31 December 2012.

YBHg. TAN SRI DATO’ SERI LODIN BIN WOk kAMARuDDIN

Non-Independent Non-Executive Director

Tan Sri Dato’ Seri Lodin bin Wok kamaruddin, aged 63, was re-appointed to the Board of Directors of AffinBAnk on 4 October 2010. He was appointed as the Managing Director of Affin Holdings Berhad in february 1991 and redesignated as Deputy Chairman on 1 July 2008.

He has extensive experience in managing a provident fund and in the establishment, restructuring and management of various business interest ranging from plantation, trading, financial services, property development, oil and gas, pharmaceuticals to shipbuilding. He is the Chief Executive of LTAT and the Deputy Chairman / Group Managing Director of Boustead Holdings Berhad. Prior to joining LTAT, he was the General Manager of Perbadanan kemajuan Bukit fraser for 9 years.

He is also the Chairman of Boustead Heavy industries Corporation Berhad, Boustead naval Shipyard Sdn Bhd, Boustead Petroleum Marketing Sdn Bhd, Boustead REiT Managers Sdn Bhd, Johan Ceramics Berhad and 1Malaysia Development Berhad and also sits on the Board of UAC Berhad, The University of nottingham in Malaysia Sdn Bhd, Minority Shareholder Watchdog Group, Atlas Hall Sdn Bhd, Affin islamic Bank Berhad, Affin investment Bank Berhad and AXA Affin Life insurance Berhad.

He graduated from the University of Toledo, Ohio, USA with a Bachelor of Business Administration and a Master of Business Administration Degree. Among the many awards Tan Sri Dato’ Seri Lodin received to-date include the Chevalier De La Legion D’Honneur from the french Government, the Malaysian Outstanding Entrepreneurship Award, the Degree of Laws honoris causa from the University of nottingham, United kingdom, the UiTM Alumnus of the Year 2010 Award and The BrandLaureate Most Eminent Brand iCOn Leadership Award 2012 by Asia Pacific Brands foundation.

Tan Sri Dato’ Seri Lodin bin Wok kamaruddin attended all 13 Board Meetings held during the financial year ended 31 December 2012.

Affin BAnk BERHAD (25046-T)17Annual Report 2012

PROFILE OF DIRECTORS

YBHg. TAN SRI DATO’ SRI ABDuL AZIZ BIN ABDuL RAHMAN

Independent Non-Executive Director

Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman, aged 66, was appointed to the Board of Directors of AffinBAnk on 28 January 2003.

He graduated with a Bachelor of Commerce from University of new South Wales, Sydney, Australia. He is a member of the Malaysian institute of Certified Public Accountants (MiCPA) and the Malaysian institute of Accountants (MiA).

He has served as Chairman and Board member of several government institutions, agencies and public listed companies, both in Australia and Malaysia.

At the corporate level he was with Price Waterhouse & Co. Sydney, Malaysia Airlines and Managing Director of Bank Rakyat Bhd before venturing into politics and public service as the Pahang State Assemblyman, State Executive Councillor and Deputy Chief Minister of Pahang. He was a Senator of Malaysian Parliament for a maximum period of two (2) terms.

Presently he is the Board member of Affin islamic Bank Berhad, the international islamic University Malaysia and University Malaysia Pahang.

Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman attended 12 out of 13 Board Meetings held during the financial year ended 31 December 2012.

YM. DR. RAJA ABDuL MALEk BIN RAJA JALLALuDIN

Independent Non-Executive Director

Dr. Raja Abdul Malek bin Raja Jallaludin, aged 67, was appointed to the Board of Directors of AffinBAnk on 29 January 1991.

He graduated as a doctor from the University of Malaya in 1972 and, early in his career, worked at the General Hospital, kuala Lumpur and the faculty of Medicine, UkM. in late 1975, he went into private medical practice and became a senior partner of Drs. Catterall, khoo, Raja Malek & Partners until 2003 when he resigned from the firm. Professionally he is widely experienced and has served in various peer and academic activities. Amongst others, he had been a clinical tutor in the faculty of Medicine, UMMC; been a member of the Ethical Committee of the Malaysian Medical Council, MOH; was the Chairman of Council Academy of family Physicians, Malaysia.

He also has vast experience in the pharmaceutical world and had actively been involved since 1984. He had been the Medical Director (Malaysia-Singapore) for Parke Davis-Warner Lambert from 1984-2000, and had remained briefly so too with Pfizer Malaysia when these two incorporations merged in 2001. in 2003, Dr. Raja Abdul Malek joined HOE/Pharmaceuticals/HOEPharma Holdings Bhd as the Director of Medical and Scientific Affairs and holds this position to this day.

Presently he is the Board member of ABB Trustee Berhad and also a member of the Advisory Panel of StemLife Berhad.

Dr. Raja Abdul Malek bin Raja Jallaludin attended 12 out of 13 Board Meetings held during the financial year ended 31 December 2012.

Affin BAnk BERHAD (25046-T) 18 Annual Report 2012

PROFILE OF DIRECTORS

MR. AuBREY LI kWOk-SINg

Non-Independent Non-Executive Director

Mr. Aubrey Li kwok-Sing, aged 62, was appointed to the Board of Directors of AffinBAnk on 17 March 2008. He is a Director of The Bank of East Asia, Limited and Chairman of MCL Partners Limited.

He possesses extensive experience in investment banking, merchant banking and capital markets. Presently he is the Board member of Café de Coral Holdings Limited, China Everbright international Limited, kunlun Energy Limited, kowloon Development Co. Ltd, Pokfulam Development Company Limited, Tai Ping Carpets international Limited and Dalton Capital (Guernsey) Limited.

Mr. Aubrey Li kwok-Sing attended 7 out of the 13 Board Meetings held during the financial year ended 31 December 2012.

Mr. Aubrey Li kwok-Sing’s Alternate Director, Mr. Gary Cheng Shui Hee was appointed on 18 April 2011. He attended 5 out of the 13 Board Meetings held during the financial year ended 31 December 2012.

EN. MOHD SuFFIAN BIN HAJI HARON

Independent Non-Executive Director

En. Mohd Suffian bin Haji Haron, aged 67, was appointed to the Board of Directors of AffinBAnk on 15 August 2009.

He graduated with a Bachelor of Economics from University of Malaya (1970) and holds a Master of Business Administration from University of Oregon in the United States (1976).

Presently he is the Board member of Affin islamic Bank Berhad, L.k. & Associates Sdn Bhd and Pharmaniaga Berhad.

En. Mohd Suffian bin Haji Haron attended all 13 Board Meetings held in the financial year ended 31 December 2012.

Affin BAnk BERHAD (25046-T)19Annual Report 2012

PROFILE OF DIRECTORS

YBHg. TAN SRI DATO’ SERI MOHAMED JAWHAR

Independent Non-Executive Director

Tan Sri Dato’ Seri Mohamed Jawhar, aged 68, was appointed as a Director of AffinBAnk on 1 november 2011.

His other positions include: independent non-Executive Director, Affin islamic Bank Berhad; Chairman iSiS Malaysia, non-Executive Chairman, new Straits Times Press (Malaysia) Berhad; Member of Securities Commission Malaysia; Member, Advisory Board, Malaysian Anti-Corruption Commission; Distinguished fellow, institute of Diplomacy and foreign Relations (iDfR); Board Member, institute of Advanced islamic Studies (iAiS); Chairman, Malaysian national Committee of the Council for Security Cooperation in the Asia Pacific (CSCAP); and Member, international Advisory Board, East West Center, USA. He is also the Expert and Eminent Person for the ASEAn Regional forum (ARf).

He was also Co-Chair, network of East Asia Think-tanks (nEAT) 2005-2006; Chairman, Malaysian national Committee, Pacific Economic Cooperation Council (PECC) 2006-2010; and Co-Chair, Council for Security Cooperation in the Asia Pacific (CSCSP) 2007-2009.

He served with the government before he joined iSiS Malaysia as Deputy Director-General in 1990. He was appointed Director-General in March 1997 and was subsequently appointed Chairman and CEO in 2006. He was appointed Chairman iSiS Malaysia on 9 January 2010.

His positions while in government included Director-General, Department of national Unity; Under-Secretary, Ministry of Home Affairs; Director (Analysis) Research Division, Prime Minister’s Department; and Principal Assistant Secretary, national Security Council. He also served as Counselor in the Malaysian Embassies in indonesia and Thailand.

Tan Sri Dato’ Seri Mohamed Jawhar during his tenure attended 12 out of 13 Board Meetings held during the financial year ended 31 December 2012.

Affin BAnk BERHAD (25046-T) 20 Annual Report 2012

MANAgEMENT TEAM

YBhg. Dato’ Zulkiflee Abbas Bin Abdul HamidManaging Director / Chief Executive Officer

En. Amirudin Abdul HalimDirector, Business Banking

En. kamarul Ariffin Mohd Jamil Chief Executive Officer, Affin Islamic Bank

En. idris Abd. HamidDirector, Consumer Banking

En. Shariffudin Mohamad Executive Director, Operations

Mr. Tan kok ToonDirector, Treasury

Affin BAnk BERHAD (25046-T)21Annual Report 2012

MANAgEMENT TEAM

Mr. Ee kok SinChief Financial Officer

YBhg. Dato’ Mohammad Aslam khan Gulam HassanChief Recovery Specialist (Resigned w.e.f. 31.10.2012)

Mr. kasinathan T.kasipillai Group Chief Risk Officer

Pn. nor Rozita nordinChief Human Resource Officer

Pn. khatimah MahadiGroup Chief Internal Auditor

En. nazlee khalifahChief Corporate Strategist

Affin BAnk BERHAD (25046-T) 22 Annual Report 2012

YBHg. DATO’ ZuLkIFLEE ABBAS BIN ABDuL HAMID

Managing Director/ Chief Executive Officer

Dato’ Zulkiflee Abbas bin Abdul Hamid is currently Managing Director/ Chief Executive Officer of Affin Bank Berhad, a position held since April 2009. Dato’ Zulkiflee also holds the mandate to drive Affin Banking Group’s strategic and development agenda for all entities within the group.

Dato’ Zulkiflee joined AffinBAnk on 1 March 2005 as Director of Enterprise Banking. Subsequently in 2008, Dato’ Zulkiflee was appointed as Executive Director of Banking, which encompassed both Business and Consumer Banking.

Dato’ Zulkiflee carries with him more than 30 years of banking experience, both locally in Malaysia and internationally in London and new York. Dato’ Zulkiflee has assumed pivotal roles in banking, which include Regional Manager, Chief Credit Officer, and Global Head of Enterprise Banking, amongst others.

Dato’ Zulkiflee holds a Master in Business Administration (1981) and a Bachelor of Science degree in Marketing (1979), both from Southern illinois University.

EN. kAMARuL ARIFFIN MOHD JAMIL

Chief Executive Officer, Affin Islamic Bank

En. kamarul Ariffin Mohd Jamil joined Affin Bank Berhad in 2003 as Head, Corporate Strategy Division. in 2005, kamarul was appointed as Head, islamic Banking Division. With the establishment of Affin islamic Bank, kamarul was appointed as its Chief Executive Officer.

Prior to AffinBAnk, kamarul held various positions at Pengurusan Danaharta nasional Berhad, Trenergy Malaysia Berhad and Shell Malaysia Trading Sdn Bhd in various capacities including business development, and strategic planning.

kamarul graduated from the University of Cambridge in 1992 with a Bachelor of Arts in Economics.

EN. SHARIFFuDIN MOHAMAD

Executive Director, Operations

En. Shariffudin Mohamad joined Affin in 2007 as Director of Operations and was appointed as Executive Director, Operations in 2009.

Shariffudin has 25 years local and overseas experience in banking. His hands-on experience covers Branch Operations, Trade finance, Corporate Banking, Corporate Relationship Management, Credit Operations, Cash Management and Securities Services. His last position was Head, Project Management Services (Technology & Operations) in a leading foreign bank and its local outsourcing subsidiary.

Shariffudin graduated from Southern illinois University, with a Master in Business Administration (1981) and a Bachelor of Science degree in finance (1980).

MANAgEMENT TEAM PROFILES

Affin BAnk BERHAD (25046-T)23Annual Report 2012

EN. IDRIS ABD. HAMID

Director, Consumer Banking

En. idris Abd Hamid is currently Director of Consumer Banking, a position he has held since May 2009.

idris began his career with Affin Bank Berhad in 1994 as General Manager of Affin finance Berhad. He was appointed as Deputy Chief Executive Officer for Affin-ACf finance Berhad from 2000 to 2005.

idris has over 30 years of experience in the banking industry, which includes exposure as Branch Manager, and in Corporate and Consumer Loans management.

idris graduated with a Master in Business Administration from the University of northern Colorado in 1984.

MANAgEMENT TEAM PROFILES

EN. AMIRuDIN ABDuL HALIM

Director, Business Banking

En. Amirudin Abdul Halim joined Affin Bank Berhad as Director, Business Banking in July 2009.

Prior to AffinBAnk, Amirudin was at Malayan Banking Group (Maybank) for more than 21 years where he gained extensive banking experience in Branch Operations, Credit Control, Business Banking, Retail Marketing, Consumer Banking and Corporate Services.

He has served in several senior strategic roles at Maybank, including Deputy Head of Business Banking Division, Head of Mortgage & Automobile financing and as the Deputy Chief Executive Officer of Mayban fortis Berhad (a member of the Maybank Group of Companies).

Amirudin graduated with a Bachelor of Arts degree in finance from St. Louis University in 1986.

MR. TAN kOk TOON

Director, Treasury

Mr. Tan kok Toon joined Affin Bank Berhad as its Head of Treasury in October 2004 and is responsible for managing all aspects of Treasury Division. He is currently the Honorary Secretary of Persatuan Pasaran kewangan Malaysia (Association Cambiste internationale) and Chair to the Seminar and Education Committee.

Prior to AffinBAnk, Tan was with one of the largest banks in Malaysia. Tan has more than 20 years banking experience, particularly in Treasury operations. He has served as Treasury Manager with the new York branch, and was Treasury Business Advisor to turnaround a business project in the Philippines.

Tan graduated from University Malaya in 1987 with a Bachelor of Science degree (honours) in Mathematics.

Affin BAnk BERHAD (25046-T) 24 Annual Report 2012

PN. kHATIMAH MAHADI

Group Chief Internal Auditor

Pn. khatimah Mahadi joined Affin Bank Berhad as Chief internal Auditor in 2004. khatimah has more than 30 years of experience in internal Auditing.

She has led the Audit and Compliance function in a number of financial institutions which include Bank Simpanan nasional, Citibank Berhad, Malaysia Credit finance, UAB/Bank of Commerce.

khatimah graduated with a Diploma in Accountancy from UiTM in 1978.

MANAgEMENT TEAM PROFILES

MR. kASINATHAN T.kASIPILLAI

Group Chief Risk Officer

Mr. kasinathan T. kasipillai joined Affin Bank Berhad in 2005 as its Chief Risk Officer. kasinathan has more than 35 years of local and overseas banking experience particularly in the areas of Risk Management. He comes from a foreign bank background working in the risk function serving in a number of countries including London, Singapore, Hong kong, Mumbai and Jakarta.

kasinathan holds a Masters in Business Administration from the University of Bath, Uk and is a Certified Risk Professional awarded by Bank Administration institute, Chicago, USA.

kasinathan is also an Associate fellow of institute of Bankers Malaysia, and continues to serve as an active member of CCP Examination Committee.

MR. EE kOk SIN

Chief Financial Officer

Mr. Ee kok Sin joined Affin Bank Berhad in 2005 as the Chief financial Officer. Prior to his appointment at AffinBAnk, Ee was the General Manager of finance & Services at Pengurusan Danaharta nasional Berhad.

Ee began his career in 1982 as a Trainee Accountant with a firm of Chartered Accountants in London. He has extensive experience in auditing, treasury functions, financial accounting, financial management and information technology.

Ee is a fellow Member of the Association of the Chartered Certified Accountants (ACCA) and a member of The Malaysian institute of Certified Public Accountants (MiCPA) and Malaysian institute of Accountants (MiA).

Affin BAnk BERHAD (25046-T)25Annual Report 2012

PN. NOR ROZITA NORDIN

Chief Human Resource Officer

Pn. nor Rozita nordin was appointed as Chief Human Resource Officer of Affin Bank Berhad in May 2011. Prior to joining AffinBAnk, Rozita was Executive Vice-President and Head of Group Human Resources at EOn Bank Group.

Rozita has more than 30 years’ experience in Human Resource Development and Customer Relations Strategy, in various industries which include banking, oil and gas, manufacturing, retail, and shared services. Rozita has taken on strategic and operational roles, both locally and abroad.

Rozita graduated from Southern illinois University with a Master of Science degree in 1984, a Bachelor of Science in Education and a Bachelor of Arts degree in Linguistics, both in 1982.

EN. NAZLEE kHALIFAH

Chief Corporate Strategist

En. nazlee khalifah joined Affin Bank Berhad in february 2009 as Head of Business Strategy and Support, Business Banking Division. Subsequently, in April 2011, nazlee was appointed as Chief Corporate Strategist.

nazlee has more than 20 years’ experience in the banking industry. Prior to joining AffinBAnk, nazlee was with Maybank for 17 years in various capacities, mostly in Strategic Management positions.

nazlee graduated from Simon fraser University in Vancouver in 1991, with a Bachelor degree in Business Administration, majoring in Accounting and finance.

MANAgEMENT TEAM PROFILES

Affin BAnk BERHAD (25046-T) 26 Annual Report 2012

CHAIRMAN’S STATEMENT

Dear Shareholders,

On behalf of the Board of Directors, I am pleased to present the Annual Report and Financial Statements for Affin Bank Berhad for the financial year ended 31 December 2012.

Affin BAnk BERHAD (25046-T)27Annual Report 2012

CHAIRMAN’S STATEMENT

During the year under review, Affin Bank Berhad (“AffinBAnk” or “the Bank”) registered another year of strong growth in revenue and earnings. The Bank recorded a profit before zakat and taxation of RM703.2 million, which is a growth of 14.7% compared to the previous financial year. The Bank also registered robust growth in loans, advances and deposits.

Throughout 2012, we continued to diligently focus on growing the Bank’s business and market presence. We launched new marketing campaigns, expanded our branch network and further improved on customer service levels by enhancing operational efficiency and productivity. The Bank also increased its investment in operational capabilities to support long-term business growth, particularly in Talent Management and information Technology (iT).

in line with this improvement, the Board is recommending a final dividend of 6 sen per share, subject to shareholders’ approval at the Annual General Meeting (AGM). Together with the interim dividend of 9 sen per share paid, the total dividend payout will amount to 15 sen per share or RM227.8 million, representing a record payment.

Aside from financial performance, AffinBAnk also saw healthy organic growth in its business operations.

We successfully opened three new branches to bring our network strength to 100 nationwide. Expanding our network is vital for further building our market presence and to tap growing opportunities, particularly in serving the retail and SME segments in which we already have a strong positioning.

Our O.M.G marketing campaign, O.M.G The Trilogy, now in its third year, has proven to be most successful in growing our deposits portfolio. The campaign was one of the key success factors towards the significant growth in the Bank’s customers and deposits.

internally, we focused on comprehensive human capital development and talent recruitment strategies to attract top industry talent and to retain our high performing employees. We also emphasised on the improvement of our working and organisational culture.

+14.7%Profit Before

Zakat & Taxation

+12.2%Loan Growth

Affin BAnk BERHAD (25046-T) 28 Annual Report 2012

CHAIRMAN’S STATEMENT

+12.9%Customer

Deposits Growth

The Bank continued with its implementation of a structured talent and leadership development program aimed at effective succession planning and strengthening the performance of operational teams via further refinement of core functional competencies.

information Technology (iT) continues to be a key enabler for the Bank. iT is viewed as a key strategy in empowering the Bank to deliver its unique proposition and offerings faster, more conveniently and with greater customer satisfaction.

Besides ensuring sound financial achievements, the Bank also measures its success on other initiatives to reinforce the positive image of our brand. 2012 was also a year where AffinBAnk made a bigger contribution to Corporate Social Responsibility (CSR) initiatives.

for the second consecutive year, the Bank participated as the main sponsor for the Treat Every Environment Special (TrEES) programme. Rallying to the call to help protect the environment, over

500 students from 42 secondary schools came together to help reduce environmental problems. These students are all participants in “Young Voices for Conservation”, an environment education programme organised by TrEES in partnership with AffinBAnk. The TrEES programme is supported by the Ministry of Education and has been a successful CSR initiative in educating the community amongst the younger segment.

As a further support to schools, AffinBAnk sponsored the “Step Up” – niE Pullout for Primary Schools (organised by The Star Publications) to promote English amongst primary students. Under niE, The Star newspapers will be distributed to selected schools for students years four, five and Six. The objective of this program is to contribute to the community by helping students explore a more creative and innovative way of learning through the use of newspapers.

Reaching out to the poor, we supported BHPetrol’s initiative of the production and airing of a TV programme called ‘Di Celah-Celah kehidupan’ on

Affin BAnk BERHAD (25046-T)29Annual Report 2012

CHAIRMAN’S STATEMENT

RTM1. The programme depicts real life stories of people who face poverty, who are disabled and old age in need of care and attention. Besides donating cash to the recipients, the Bank became the channel where the public can send their donations.

As in previous years, the Bank’s Educ-Aid (Scholarship Programme) is in its 9th year, awarding The Examination Excellence Award to students of Bank employees who excelled in their PMR and SPM examinations. This year, AffinBAnk awarded the Examination Excellence Award to 70 PMR and SPM achievers. The Bank also continued to provide scholarships to the employees’ children for their tertiary education, with a value of up to RM15,000 per year for each scholarship, up to a maximum of RM75,000 per scholar.

Other CSR activities for the year include our annual partnership with the national Blood Centre. A blood donation drive was held in AffinBAnk’s headquarters, where the Bank’s employees took the time to donate blood in between their work schedules. We also sent a team of five runners to The Bursa Edge Rat Race and donated to a fund which will benefit 26 charitable organisations around Malaysia. As in previous years, we continued to support the annual “Hari Pahlawan” or Warriors Day.

Going forward, whilst we expect the upcoming financial year to present many challenges, we also see opportunities ahead. The global economy is expected to remain sluggish and the domestic environment is also expected to be impacted. further market liberalisation, new entrants and competing products will result in a more competitive environment.

However, we believe that AffinBAnk will continue to perform well in 2013.

Given the Bank’s sound fundamentals, our growing market presence and the continued improvement in efficiency and productivity, AffinBAnk is in a solid position to deliver another year of growth and progress.

in 2013, the Bank will be focusing on industries or sectors with high growth potentials. As we explore new collaboration and market opportunities, we will further tap the retail and SME segment, where we have already established our brand and solutions.

With more Entry Point Projects expected to be rolled out as part of the Economic Transformation Programme (ETP), we look forward to playing a role in the financing of these projects, particularly in key growth sectors such as healthcare, education and construction.

On behalf of the Board, i wish to express my sincere appreciation to our shareholders and business partners for their continued vote of confidence and support.

i wish to also take the opportunity to record our thanks to the senior management and our employees for their dedication, commitment and tireless effort during the year under review. Their contribution has been a key driver in our continued growth and success. Last but not least, i wish to say thank you to my fellow Board members for their counsel and stewardship in what has been a year of progress for AffinBAnk.

Jen. Tan Sri Dato’ Seri ismail bin Hj. Omar (Bersara)Chairman

Affin BAnk BERHAD (25046-T) 30 Annual Report 2012

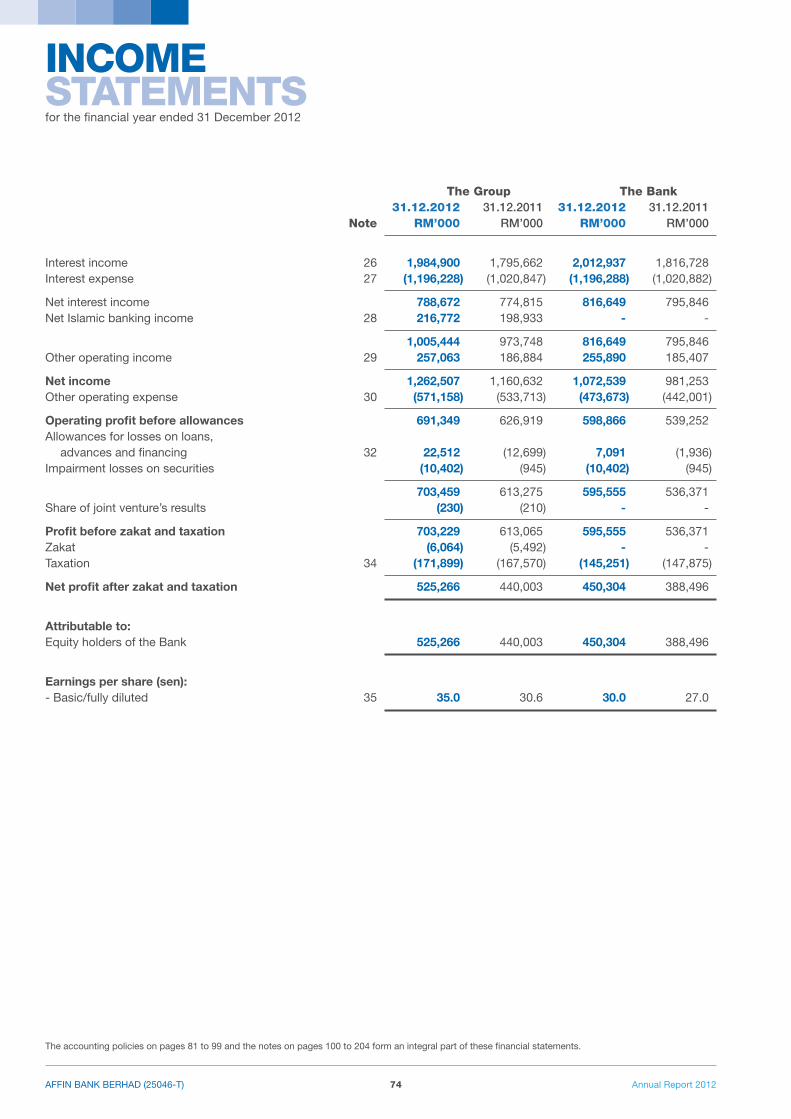

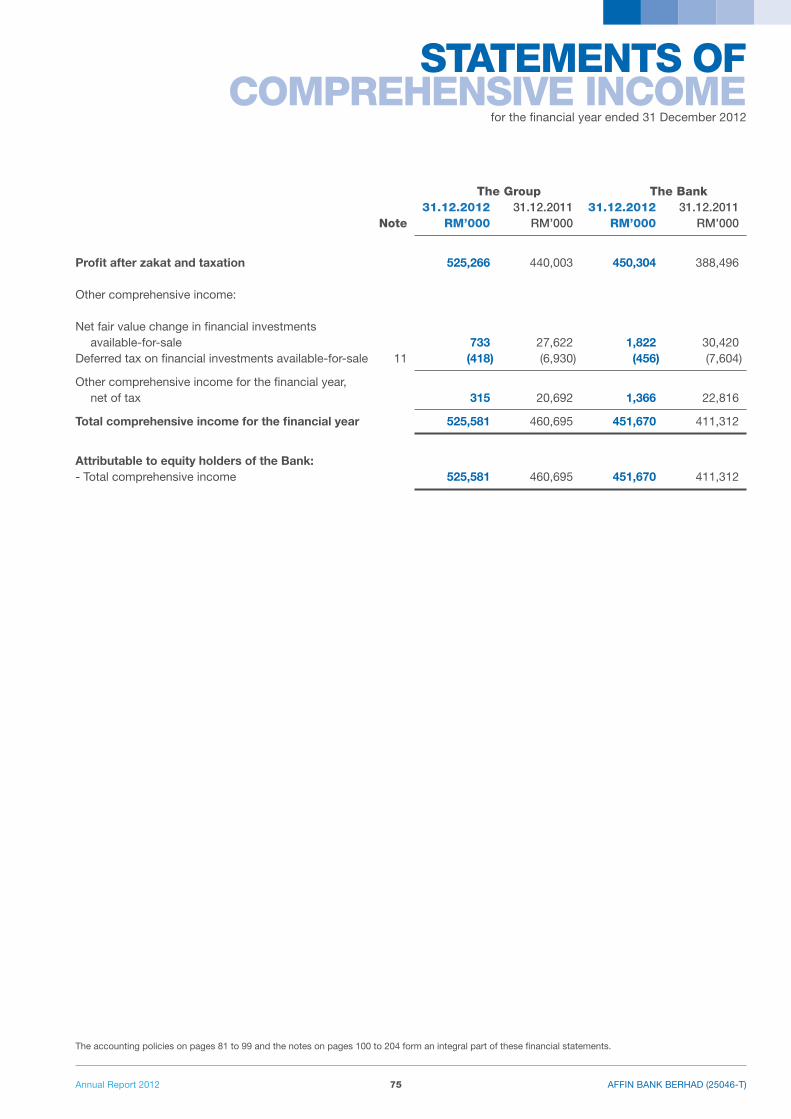

AffinBAnk’s profit after zakat and taxation grew by 19.4% from RM440.0 million in 2011 to RM525.3 million in 2012. Total Assets reached RM52.1 billion in 2012, which is a growth of 5.8% compared to RM49.2 billion in the previous financial year.

The Bank also successfully achieved its target of double digit loans growth for 2012. During the year, gross loans and advances grew by 12.2%. Return-on-Equity (ROE) after tax was 14.1% while Cost-to-income ratio was recorded at 45.2%. The Bank also continued to grow its total deposit portfolio by 12.9% in 2012 from RM36.5 billion in 2011 to RM41.3 billion in 2012.

PERFORMANCE REVIEW

+5.8%Total Assets

+19.4%Profit After

Zakat & Taxation

For the year under review, AFFINBANK recorded a profit before zakat and taxation of RM703.2 million, which is a growth of 14.7% compared to 2011. The Bank has been registering consistent growth in revenue and earnings for more than 5 years and the profit before zakat and taxation this year is at an all-time high.

net interest income was recorded at RM788.7 million compared to RM784.9 million in 2011. islamic banking income grew by 14.8% to RM216.8 million from RM188.8 million in the previous year.

The Bank’s growth was tempered with fiscal prudence in ensuring that asset quality was not compromised in the pursuit of loans growth. Asset quality remained resilient with a lower net impaired loan ratio of 1.1% in 2012 compared to 1.3% in 2011. Operational Highlights in line with growing the Bank’s presence in key population areas, AffinBAnk opened three new branches in Selangor – Bangi, klang and Cyberjaya. This brings our branch network strength to 100 nationwide.

The move to launch new branches is aimed to increase our brand visibility, improve our accessibility to customers and to establish a credible presence in key population areas that offer exciting growth potential. The goal is to provide AffinBAnk products and services in locations which are within easy reach and convenient in fast expanding towns and communities.

Affin BAnk BERHAD (25046-T)31Annual Report 2012

As customers’ financial needs evolve and grow in sophistication, they would require new and comprehensive offerings. By being closer to these target groups, AffinBAnk can offer its financial solutions to them and ultimately tap this market segment effectively.

The most significant of these new AffinBAnk branches is the Bandar Bukit Tinggi (klang) operation. This is the Bank’s fourth ‘all under one roof’ branch, offering a complete portfolio of financial services and solutions, targeting the business community from the busy Port klang area and a prominent shopping centre.

The Bandar Bukit Tinggi Branch offers financial services from both AffinBAnk and Affin investment Bank Berhad.

in addition to these new branches, three other branches were relocated to Ara Damansara, Puchong and Muar while 15 additional off-site ATMs were installed for easier accessibility and customer convenience.

Building on the success of the O.M.G. deposit campaigns from previous years (O.M.G and O.M.G It’s Back!), AffinBAnk launched O.M.G The Trilogy from July to December 2012.

The campaign targeted new and existing conventional and islamic Savings, Current and fixed Deposit Account holders while encouraging customers to save more with the Bank. With the O.M.G campaign and other marketing promotions, the Bank recorded a healthy growth in deposits in 2012.

The campaign also created plenty of excitement and brand awareness for the Bank. The attractive prizes offered proved to be a major enticement in attracting and retaining customers.

PERFORMANCE REVIEW

45.2%Cost To

income Ratio

13.65%Risk Weighted

Capital Ratio

14.1%Return On

Equity

in collaboration with Permodalan nasional Berhad (PnB), AffinBAnk also launched its 24-hour, online ASnB Top-Up facility on 31 May 2012. AffinBAnk is one of only four banks in Malaysia to offer online additional ASnB funds subscription and only the second bank to provide a 24-hour service facility.

This is in line with the Bank’s objective of leveraging on digital technology to take customer service to a new level, to make banking as easy as possible for customers, while offering new services and initiatives that provide them with better access to a wider spectrum of online transaction options. AffinBAnk is also empowering investors to manage their own investment portfolio.

Through the 24-hour top up service, the Bank is also fulfilling its mandate of encouraging Malaysians to participate in the corporate sectors and equities market.

As in previous years, the focus on iT has continued to yield results – enabling the Bank to work faster and more effectively with improved turnaround time and security, better customer service levels, facilitation of more strategic decision-making and other benefits. One of the two areas where this was evident in 2012 was the launch of a new Loan Origination System to enable faster turnaround time in processing of loans applications. The other was the enhancement to the Retail internet Banking and Corporate internet Banking systems to improve the functional capabilities for customers’ convenience during online transactions.

A robust risk management framework is in place to balance the expected competitive market environment with business growth strategies.

Affin BAnk BERHAD (25046-T) 32 Annual Report 2012

PERFORMANCE REVIEW

Besides stringent loan monitoring processes, a Special Early Alert Committee was formed to track the loan portfolio of the Bank. There are also credit clinics and other credit related talks to inculcate a risk awareness culture amongst the employees of the Bank.

Recognised for Excellence

2012 also saw AffinBAnk garnering several awards. These include the Top 30 Most Valuable Brands by the Association of Accredited Advertising Agents (4As) and the Best of Malaysia Service to Care Champion in the category of Conventional Bank with assets less than USD20 billion.

The latter was awarded by MarkPlus insight in conjunction with the Philip kotler and the Christopher Lovelock Centre for Services Marketing. This Award is given in recognition of best performers and companies with best practices in customer service and customer care in the ASEAn region.

During the inaugural Service to Care Award in 2011, AffinBAnk was also awarded the Malaysia Service To Care Champion for Customer Satisfaction (Category: Conventional Bank with assets below USD20 billion).

These recognitions in customer service excellence re-enforces the Bank’s commitment to continuously improve our service levels and our relationships with customers. We wish to thank all our customers for their endearing support.

HR and Talent Management

During the year, AffinBAnk continued to focus on the development of its human capital. This was achieved through a structured talent and leadership development program, which emphasises on succession planning and enhancing team performance via development of functional competencies.

The Leadership Development Program (LDP) is implemented at all levels from junior to senior management to inculcate new mindsets and behavioural capabilities in view of developing potential leaders to undertake greater roles and responsibilities within the Bank.

in nurturing young talent, the Affin Management Training Programme (AMP) continued to be an effective tool in developing our human capital pool and identifying the future leaders of the Bank.

Prospects & Outlook

Moving into 2013, the Bank’s robust financial position together with new emerging market opportunities present bright prospects going forward.

in growing its business, AffinBAnk will continue to emphasise key business drivers such as growing its loans and advances as well as customer deposits. The Bank waits in much anticipation for its 101st branch opening, which will be a major milestone. in addition, the success of the O.M.G campaigns will be built on further to grow AffinBAnk’s presence in the market. This will be supported by more innovative product offerings that appeal to the retail and commercial segments.

Affin BAnk BERHAD (25046-T)33Annual Report 2012

FINANCIAL HIgHLIgHTS

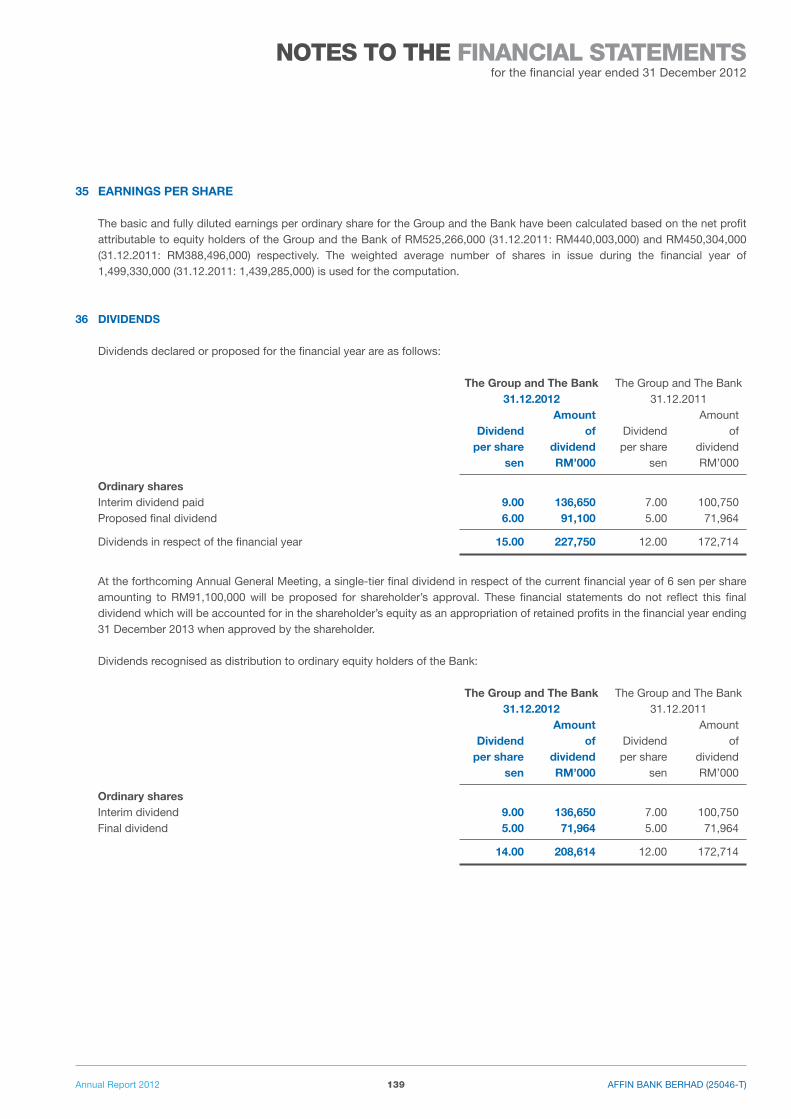

AffinBAnk’s EPS for the financial year ended 31 December 2012 stood at 35.0 sen compared to 30.6 sen the year before.

35.0

26.5

30.6

23.0

22.1

1210 1108 0970

3.2

521.

9

613.

1

454.

6

425.

1

1210 1108 09

52.1

42.1

49.2

33.0

35.6

1210 1108 09

33.5

26.0

29.7

19.5

22.0

1210 1108 09

41.3

31.0

36.5

25.2

26.4

1210 1108 09

4.1

3.3

3.6

2.7

3.0

1210 1108 09

Earnings Per Share (EPS)(Sen)

Profit Before Zakat And Taxation (RM’million)

Total Assets(RM’billion)

AffinBAnk’s net loans, advances and financing grew by 12.77% to RM33.5 billion compared with RM29.7 billion in 2011, as economic activities and demand for credit gathered momentum during the year under review.

Net Loans, Advances & Financing(RM’billion)

Deposits From Customers(RM’billion)

Shareholders’ Equity (RM’billion)

AffinBAnk achieved profit before zakat and taxation of RM703.2 million, a commendable 14.7% rise for the year ended 31 December 2012, compared to RM613.1 million in 2011. AffinBAnk’s profit after zakat and taxation also rose by 19.4% to RM525.3 million for the year ended 31 December 2012.

AffinBAnk’s financial position as at 31 December 2012 continued to remain strong with total assets of RM52.1 billion, an increase of 5.8% compared with RM49.2billion as at 31 December 2011.

Total deposits increased by 12.9% year-on-year to RM41.3 billion as at 31 December 2012, in correspondence to AffinBAnk’s loan growth.

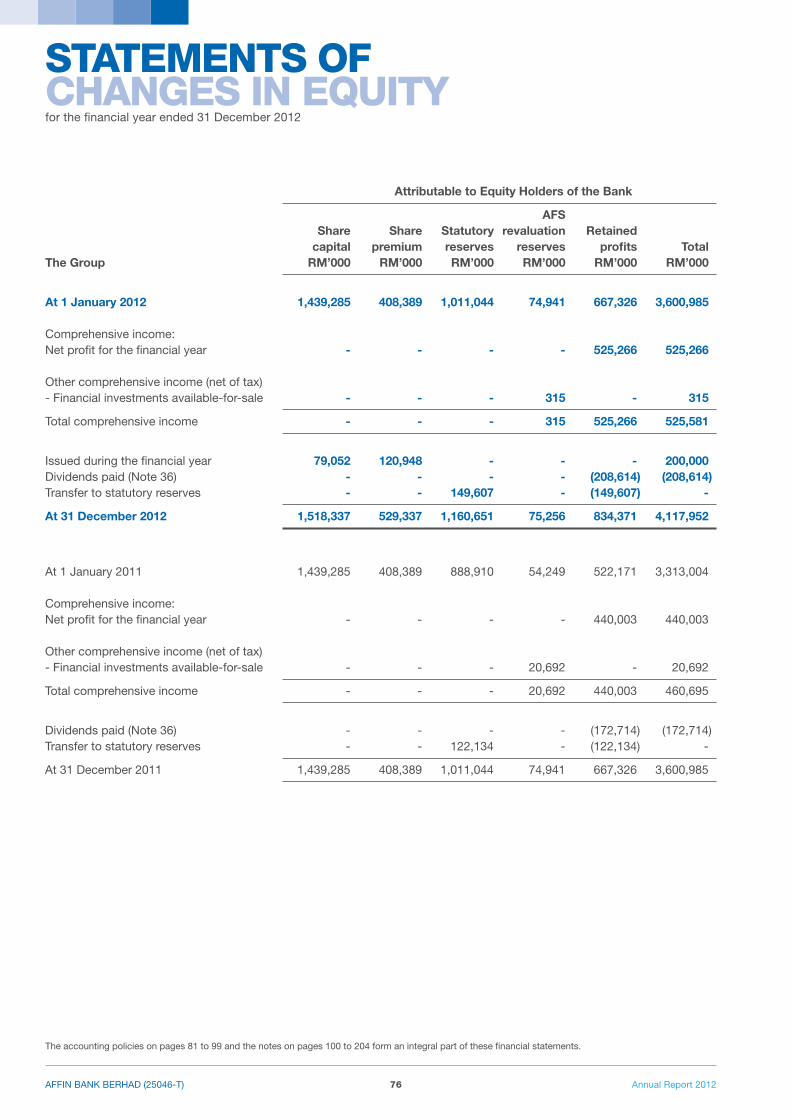

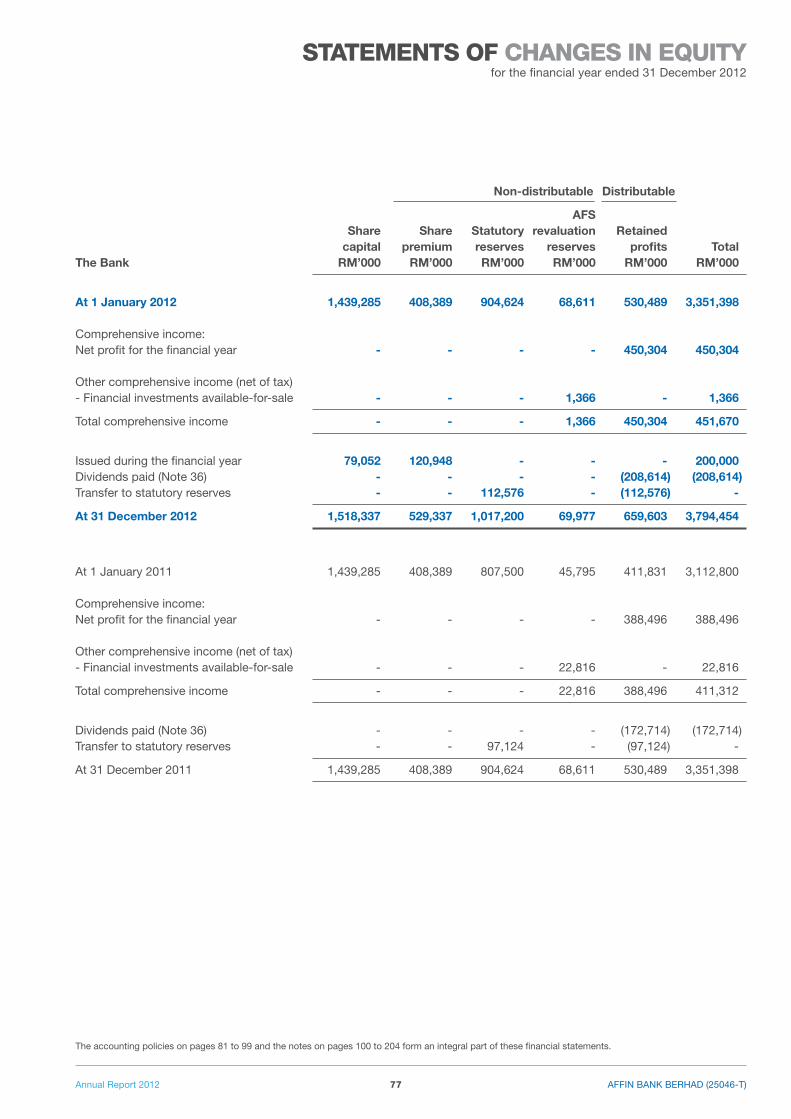

Total shareholders’ equity of AffinBAnk increased by 14.36% to RM4.1 billion from RM3.6 billion the year before.

Affin BAnk BERHAD (25046-T) 34 Annual Report 2012

CORPORATE DIARY

18 January 2012

AffinBAnk holds its OMG It’s Back! prize giving ceremony, where Suzi Zuliana Zalekan won a Volkswagen Golf GTi and RM300,000 cash deposit. Second prize winner, Mardziiah Mansor drove away a Toyota Prius and RM120,000 whereas third prize winner Liew Yen fui took home a Perodua Myvi and RM60,000.

20 March 2012

AffinBAnk hosts ‘An Evening of Splendour’ as a form of appreciation towards its top valued corporate and consumer clients.

16 March 2012

AffinBAnk sponsors RM70,000 for Lembaga Tabung Haji’s “Wirid Terpilih untuk Dhuyufurrahman”, a book to be distributed to pilgrims during their stay at the Holy land.

21 May 2012

AffinBAnk and Affin inVESTMEnT officially and jointly opens its doors, offering an ‘all under one roof’ branch of financial services and solutions to the growing 80,000 residents of Bandar Baru Bukit Tinggi.

16 April 2012

Partnering with the national Blood Centre, AffinBAnk holds a blood donation drive to encourage a joint effort between its staff and customers in meeting their roles as conscious citizens and humanitarians.

24 April 2012

AffinBAnk sponsors RM100,000 to Majlis Bekas Wakil Rakyat Malaysia (MUBARAk) to support the launch of the book, “100 Wira negara”. it is a form of recognition and appreciation for the heroes and icons in various fields and institutions that had great impact on national development.

Affin BAnk BERHAD (25046-T)35Annual Report 2012

CORPORATE DIARY

31 May 2012

in collaboration with Permodalan nasional

Berhad (PnB), AffinBAnk officially launches its new 24-hour online service – Amanah Saham nasional Berhad (ASnB) funds Additional Top Up via its website affinOnline.com, placing AffinBAnk amongst the four main banks in Malaysia to provide this service to the public.

June – November 2012

Rallying to the call to help protect the environment, over 500 students from 42 secondary schools come together to help reduce environmental problems at their schools. These students are all participants in “Young Voices for Conservation”, an environment programme by Treat Every Environment Special (TrEES) in partnership with AffinBAnk.

3 August 2012

160 orphans and 30 new Muslim converts from the klang Valley area enjoy a hearty ‘buka puasa’ feast at AffinBAnk’s headquarters, Menara Affin. The board of directors, management staff, AffinBAnk and Affin iSLAMiC employees get to know the orphans and newly converts on a more personal level.

3 November 2012

AffinBAnk holds a colourful come-one-and-come-all ‘Jom Karnival’ for its newly opened 100th branch in Cyberjaya.

4 June 2012

in a bid to support deserving youths in achieving their dreams, AffinBAnk rewards the Examination Excellence Award to a total of 70 PMR and SPM achievers, as well as award scholarships to deserving students to pursue their tertiary education.

10 July 2012

AffinBAnk sponsors The Star’s Step-Up niE, a pullout for primary schools, distributed to selected schools and caters specifically for students year four, five and Six. The objective of this program is to contribute to the community by helping students explore a more creative and innovative way of learning through the use of newspapers.

Affin BAnk BERHAD (25046-T) 36 Annual Report 2012

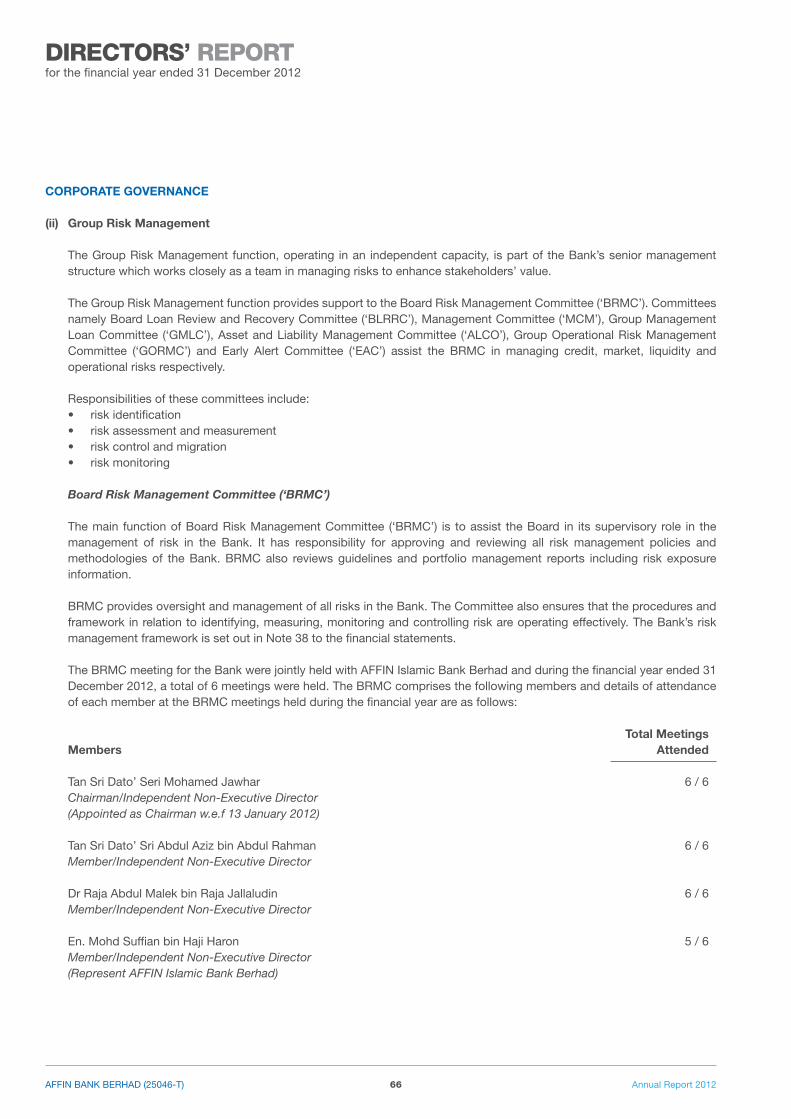

The Board of Directors of AffinBAnk (“Board”) and Management appreciate the importance of adopting high standards of Corporate Governance in all areas of its business towards enhancing business prosperity and corporate accountability with the ultimate objective of safeguarding the interest of shareholder’s value. The Board takes cognizance of the Malaysian Code on Corporate Governance 2012 (MCCG 2012) issued by the Securities Commission Malaysia. The Board and Management are fully committed and constantly strive to ensure that the MCCG 2012 and Bank negara Malaysia (BnM) Guidelines on Corporate Governance for Licensed institutions (Revised BnM/GP1) are adopted and practised throughout the group. This is important so as to ensure that AffinBAnk is managed safely and soundly; where risks and business prudence are appropriately balanced so as to maximize shareholder’s return and to protect the interests of all stakeholders. Throughout 2012 and to date, AffinBAnk continues to conduct its business with integrity and exercises a high level of transparency and objectivity.

The Board and Management are fully committed in ensuring employees adhere closely to BnM’s Guidelines (BnM/GP7) on Code of Ethics (“COE”), which aims at instilling the five values namely discipline, integrity, humility, caring and creativity in AffinBAnk and its employees. The Board and Management set high ethical business standards and practices for business conduct and the code of behaviour for employees to adhere to. in addition to the COE, all Directors are also required to observe the Directors’ COE. The responsibility for implementation of COE policies and guidelines rests primarily with Management, oversights by the Audit & Examination Committee. Good Corporate Governance is the foundation of the culture and business practices of AffinBAnk.

The following statements set out the commitment of AffinBAnk in applying good Corporate Governance principles and the extent of compliance with the recommended best practices.

1. BOARD OF DIRECTORS

The Board is committed in establishing and enhancing shareholder’s value in the long term. The Board is pleased to report that, to its best efforts and knowledge, has complied with the principles and the best practices of the Code throughout the financial year under review.

The Board of AffinBAnk has a balance composition with a strong independent element. it consists of representatives

from the private sector with suitable qualifications fulfilling the fit and proper criteria, a mixture of different skills, competencies, experience and personalities. Directors’ profiles which appear on pages 16 to 19 reflect clearly the depth and diversity in expertise and perspective to lead AffinBAnk as well as to allow for an independent and objective analysis of major issues.

Board’s Responsibilities

The Board acknowledges its roles and responsibilities for the overall performance of AffinBAnk.

The Board’s responsibilities remain within the framework of BnM Guidelines and AffinBAnk’s Board Policy Manual. The Board also exercises great care to ensure that high ethical standards are upheld, and that the interests of stakeholders are not compromised. These include responsibility for determining AffinBAnk’s general policies and strategies for the short, medium and long term, approving business plans, including targets and budgets, and approving major strategic decisions.

STATEMENT OFCORPORATE gOVERNANCE

Affin BAnk BERHAD (25046-T)37Annual Report 2012

in carrying out its functions, the Board has delegated specific responsibilities to other Board Committees, which operate under approved terms of reference, to assist the Board in discharging its duties. The Board Committees report on the outcome of their meetings to the Board and any further deliberation is made at Board level, if required. Reports and deliberations are incorporated into the Minutes of the Board meetings. The various Committees are listed below:-

Board Remuneration Committee (“BRC”)

The BRC is responsible for providing a formal and transparent procedure for developing the remuneration policy for Directors, Managing Director/Chief Executive Officer and key senior management personnel. BRC is to ensure that compensation is competitive and consistent with AffinBAnk’s culture, objectives and strategies. BRC obtains advice from experts in compensation and benefits, both internally and externally.

Board Nominating Committee (“BNC”)

The BnC is responsible for providing a formal and transparent procedure for the appointment of Directors and Managing Director/Chief Executive Officer and key senior management personnel. BnC assesses the effectiveness of individual Director, the Board as a whole and the performance of the Managing Director/Chief Executive Officer and key senior management personnel.

Board Risk Management Committee (“BRMC”)

The BRMC is responsible for overseeing management’s activities in managing credit, market, liquidity, operational, legal and other risks and to ensure that the risk management process is in place and functioning.

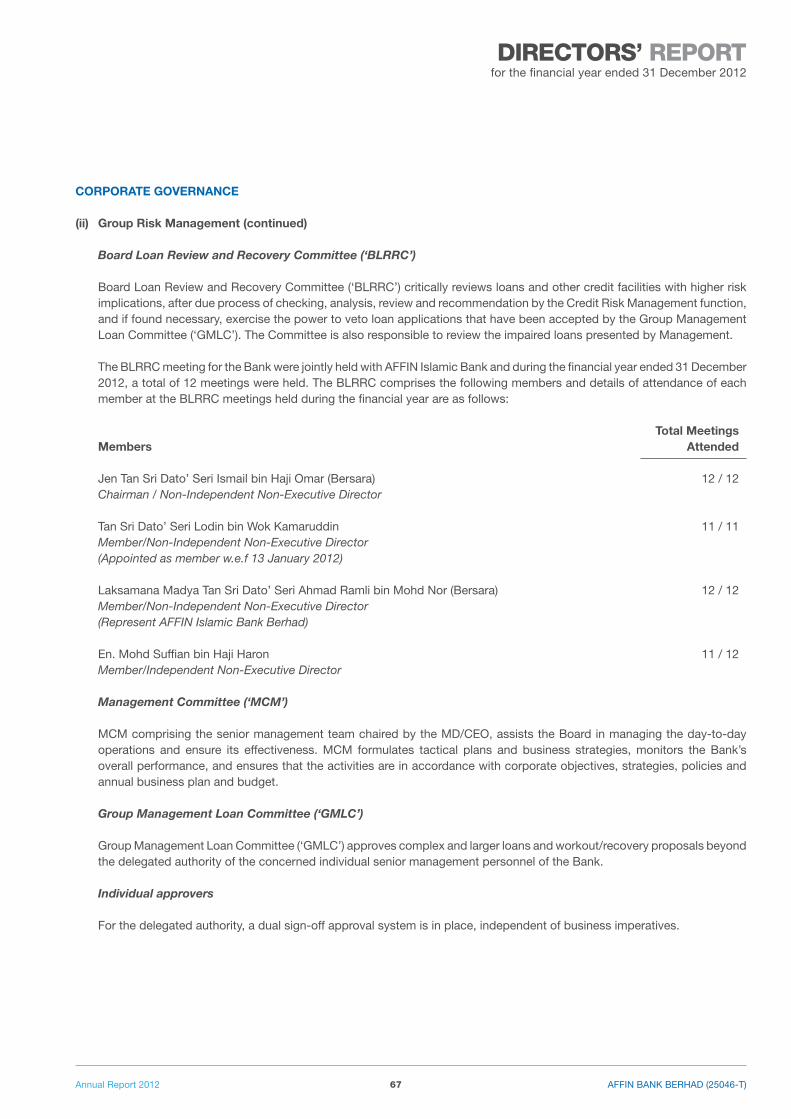

Board Loan Review and Recovery Committee (“BLRRC”)

The BLRRC is responsible in providing critical review of loans and other credit facilities with higher risk implications, after due process of checking, analysis, review and recommendation by the Credit Risk Management function, and if found necessary, exercise the power to veto loan applications that have been approved by the Group Management Loan Committee.

Audit & Examination Committee (“AEC”)

The AEC is responsible for providing oversight on reviewing the adequacy and integrity of the internal control systems and oversees the work of the internal and external auditors.

Board Composition and Balance

The Board consist of seven (7) non-Executive Directors with one (1) Alternate Director; four (4) are independent non-Executive Directors and three (3) are non-independent non-Executive Directors. All Directors met the criteria set by the BnM guidelines.

Board meetings are presided by a non-independent non-Executive Chairman whose role is clearly separated from the role of the Managing Director/Chief Executive Officer. The Chairman is responsible for ensuring the effectiveness and smooth functioning of the Board, the governance structure, independence and inculcate a positive culture in the Board.

The Board comprises Directors who, as a group, provides a mixture of core competencies such as finance, accounting, business, management, marketing, information technology and investment management, which are essential for the effective functioning and discharging of responsibilities by the Board.

The Managing Director/Chief Executive Officer is responsible for the overall day-to-day business affairs of AffinBAnk while providing strong leadership in the implementation of Board decisions.

STATEMENT OF CORPORATE gOVERNANCE

Affin BAnk BERHAD (25046-T) 38 Annual Report 2012

STATEMENT OF CORPORATE gOVERNANCE

AffinBAnk’s Board composition possesses a strong element of independence by having majority independent Directors. Although all the Directors have an equal responsibility for the Group’s business directions and operations, the role of these independent non-Executive Directors are particularly important in ensuring that the strategies proposed by the management are fully discussed and evaluated, having considered the long term interests of AffinBAnk’s objectives. no individual or small group of individuals dominates the Board’s decision making process.

Independence and Conflict of Interest

it is the Directors’ responsibility to declare whether they have a potential or actual interest in any transaction of AffinBAnk. Where issues involve conflict of interest, the interested Directors abstained from discussing or voting on the matter.

Appointments and Re-election to the Board in 2012, BnM approved the re-appointment of two (2) independent non-Executive Directors. in accordance with the

Company’s Memorandum and Articles of Association, one-third (1/3) of the Directors, or, if their number is not three (3) or a multiple of three (3), the number nearest to one-third (1/3), shall retire from office at each Annual General Meeting and they may offer themselves for re-election.

Directors’ Training

All newly appointed non-Executive Directors are furnished by AffinBAnk with copies of the BnM Guidelines, the Banking and financial institutions Act 1989 and other relevant legislation governing the banking industry to facilitate their understanding and requirements of banking business. All Directors have attended various training programmes organised internally as well as externally by the relevant authorities such as BnM, Securities Commission (“SC”) and Companies Commission of Malaysia (“CCM”). in addition, the members of the Board keep abreast with the relevant developments in business, banking and finance industry as well as new regulatory requirements on a continuous basis via various conferences, seminars and training programmes organised within the Group and by other external organisers. The development and training programmes attended by the Directors during the financial year ended 31 December 2012 are set out below.

Director Trainer/Organiser Course Title Date

Jen Tan Sri Dato’ Seri Ismail bin Haji Omar (Bersara)

1. inCEif/iQRA(MARA) Seminar Wakaf : Penjana Pembangunan

14 february 2012

2. Asian World Summit Sdn Bhd 4th Annual Corporate Governance Summit

5 March 2012 &6 March 2012

3. fleming Gulf india Ltd 2nd Annual World islamic finance Conference 2012, London Uk

27 March 2012 &28 March 2012

4. Malaysian institute of Defence & Security

Putrajaya forum 2012 – Enhancing Multilateralism for Regional Defence and Security

17 April 2012 to 19 April 2012

5. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

6. iCLif iCLif Leading Voices – Creating Cross-Border Champions Program by fons Trompenaars

10 May 2012

Affin BAnk BERHAD (25046-T)39Annual Report 2012

Director Trainer/Organiser Course Title Date

7. fiDE Official Launch of fiDE forum 2012 and Talk by Mr Youssef A nasr “Corporate Governance…. Should i Take it Seriously?”

12 June 2012

8. Affin investment Bank Berhad Politics & Business: The Malaysian Connection

28 June 2012

9. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

10. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

11. fiDE Breakfast Talk on Global Consumer Banking Survey 2012 – “The Customer Takes Control” by Ernst & Young

9 October 2012

Tan Sri Dato’ Seri Lodin bin Wok Kamaruddin

1. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

2. fiDE Official Launch of fiDE forum 2012 and Talk by Mr Youssef A nasr “Corporate Governance…. Should i Take it Seriously?”

12 June 2012

3. Affin investment Bank Berhad Politics & Business: The Malaysian Connection

28 June 2012

4. fiDE/iCLif fiDE forum – Breakfast Talk on “Human Capital Management in the Boardroom”

14 August 2012

5. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

6. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

7. fELCRA Berhad Delivered Corporate Talk on “Diversification for future Sustainability: Boustead Holdings Berhad Experience” Senior Management and Officers of fELCRA Berhad

19 December 2012

STATEMENT OF CORPORATE gOVERNANCE

Affin BAnk BERHAD (25046-T) 40 Annual Report 2012

Director Trainer/Organiser Course Title Date

Dr. Raja Abdul Malek bin Raja Jallaludin

1. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

2. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

3. fiDE The nomination/ Remuneration Committee Program

13 September 2012 &14 September 2012

4. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

Tan Sri Dato’ Sri Abdul Aziz bin Abdul Rahman

1. fleming Gulf india 2nd Annual World islamic finance Conference 2012, London Uk

27 March 2012 &28 March 2012

2. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

3. fiDE/iCLif iCLif Leading Voices – Creating Cross-Border Champions Program by fons Trompenaars

10 May 2012

4. fiDE/iCLif fiDE Elective Program: iCAAP Program

2 July 2012 &3 July 2012

5. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

6. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

Mr. Aubrey Li Kwok-Sing 1. Towers Watson

Latest Trends in Executive Compensation, Hong kong

3 february 2012

2. PricewaterhouseCoopers Board Effectiveness : What Works Best, Hong kong

8 february 2012

3. kPMG What’s around the corner in 2012, Hong kong

15 March 2012

4. PricewaterhouseCoopers Board Effectiveness: factors for the Long-term Strategy in the financial Services industry (also relevant to other industries),Hong kong

20 June 2012

5. kPMG 1. Corporate Governance• The draft revised UK CG Code• 10 CG Themes for 2012• Whistleblowing• Crisis Management

2. Regulatory Changes3. Audit Committee focus areas4. Anti-Money laundering and

fraud Hong kong

25 June 2012

STATEMENT OF CORPORATE gOVERNANCE

Affin BAnk BERHAD (25046-T)41Annual Report 2012

STATEMENT OF CORPORATE gOVERNANCE

Director Trainer/Organiser Course Title Date

6. Hk institute of Directors/ kowloon Development

Update on Hk Listing Rules and Corporate Governance Code, Hong kong

19 September 2012

7. Hk institute of Directors Bank Board effectiveness in light of the financial Crisis, Hong kong

22 September 2012

8. Hk institute of Directors internal Control, Hong kong 11 October 2012

9. Hk institute of Directors/ kowloon Development

Anti-Money Laundering, Hong kong

31 October 2012

10. Mr. Gavin nesbitt, Deacon/ BEA

new Statutory Regime for Disclosure of inside information, Hong kong

22 november 2012

11. Deloitte inED Workshop The regulator’s View of inEDs, Hong kong

29 november 2012

12. kPMG inED forum The Audit Committee agenda; information Governance; Taxation update; financial reporting preview; Legal Developments, Hong kong

10 December 2012

13. PricewaterhouseCoopers / Café de Coral Holdings

Corporate Governance, Hong kong 11 December 2012

14. Mayer JSM/CdC, Hong kong

Disclosure of inside information 11 December 2012

15. Hk institute of Directors/ kowloon Development

How to run effective meetings, Hong kong

12 December 2012

Mr. Gary Cheng Shui Hee(Alternate Director Mr. Aubrey Li Kwok-Sing)

1. fiDE/iCLif Leadership & Governance

fiDE Core Program 2012 Group 1 – Mr Gary Cheng Shui Hee

19 March 2012 (Module 1)18 June 2012 to 21 June 2012 (Module 2)

En. Mohd Suffian bin Haji Haron

1. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

2. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

3. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

Tan Sri Dato’ Seri Mohamed Jawhar bin Hassan

1. Affin Holdings Berhad Half Day Talk by Messrs PricewaterhouseCoopers (a) Basel iii (b) PWC Banking Banana Skin Survey (c) Accounting and Other Regulatory Updates (d) future Trend in Banking

2 May 2012

2. Affin Holdings Berhad Half Day forum on islamic Banking by Assoc. Prof Dr Asyraf Wajdi and Assoc. Prof Dr Said Bouhrouea

5 September 2012

3. Affin Holdings Berhad Half Day Talk on “Rebuilding Trust in the financial Sector” by John Zinkin

8 October 2012

Affin BAnk BERHAD (25046-T) 42 Annual Report 2012

STATEMENT OF CORPORATE gOVERNANCE

Meeting and Supply of Information to the Board

Board meetings for each financial year are scheduled in advance to enable the Directors to plan their schedules.

The Board meets on a scheduled basis at least eleven (11) times a year. Additional meetings are convened when necessary to review progress reports on AffinBAnk’s financial performance, approved strategies, business plans and significant policies as well as to consider business and other proposals which require the Board’s approval. for financial year ended 31 December 2012, thirteen (13) Board meetings were held. Meetings are usually held at the Bank’s Board Room at 19th floor, Menara Affin, 80, Jalan Raja Chulan, 50200 kuala Lumpur.

Board meetings are conducted in accordance to a planned agenda. Board Members are provided with the agenda together with relevant documents and information in a form and of an appropriate quality in advance of each Board meeting. This is to facilitate the Directors to peruse the Board papers and seek clarifications that may require from the Management or the Company Secretary well ahead of the meeting date. Urgent papers may be presented for tabling at the Board meetings under supplemental agenda.

The Board monitors AffinBAnk’s performance by reviewing the monthly Management Report, which provides a comprehensive review and analysis of AffinBAnk’s operational and financial issues. in addition, the Minutes of the various Board Committees and Management Committee meetings and other issues are also tabled and considered by the Board.

Procedures are in place for Directors to seek independent professional advice at AffinBAnk’s expense. AffinBAnk

also provides the Board full access to necessary materials and relevant information including the services of the Company Secretary in order for the Board to fulfill their duties and specific responsibilities.

2. DIRECTORS’ REMuNERATION

Composition

AffinBAnk acknowledges the importance of attracting and retaining the right calibre of Directors with the necessary skills, qualifications and experience for effective Board oversight of AffinBAnk’s business activities and affairs.

The make-up of the Managing Director/Chief Executive Officer’s remuneration remained unchanged consisting of salary, allowances, bonus and other customary benefits as appropriate. Any salary review, takes into account market rates and the performance of the individual and of AffinBAnk.

non-executive Directors’ emoluments consist of three components – an annual fee as a Board member, an allowance

for attendance of meetings and a committee fee. The Directors’ fees, allowances and committee fees are those recommended by the Board and in line with Affin Holdings group of companies.

Directors’ emoluments are disclosed in the relevant note to the financial statements as an aggregate sum, in conformance to the relevant legislation.

3. SHAREHOLDER

AffinBAnk is a wholly owned subsidiary of Affin Holdings Berhad, a company listed on Bursa Malaysia Securities Berhad.

4. ANNuAL gENERAL MEETINg (“AgM”) The Annual Report and financial statements for the year ended 31 December 2011 were tabled at the 36th AGM on 21

March 2012. Likewise the Annual Report and financial statements for the year ended 31 December 2012 will be tabled at the 37th AGM on Monday, 25 March 2013.

Affin BAnk BERHAD (25046-T)43Annual Report 2012

STATEMENT ONINTERNAL CONTROL

INTERNAL CONTROL

AffinBAnk has a well-established and fully operational risk management and internal control system. The Statement on internal Control, which is set out in the Annual Report provides an overview on the risk management process/framework as well as on how the internal control system has been designed to manage risks and avert failures. AffinBAnk continues to enhance its system of internal control and risk management, in order to better quantify its compliance with the Code.

The Board has overall responsibility for maintaining the proper management and protection of AffinBAnk’s interests by ensuring effective implementation of the risk management policy and process, as well as adherence to a sound system of internal control, and by seeking regular assurance on their effectiveness. The Board also recognizes that risks cannot be eliminated completely. As such, the inherent system of internal control is designed to provide a reasonable though not absolute assurance against the risk on material errors, fraud or losses occurring.

The Audit & Examination Committee has an oversight responsibility for the adequacy and integrity of the internal control system. Reliance is placed on the results of independent audits performed primarily by Group internal auditors, the outcome of statutory audits on financial statements conducted by external auditors and on representations by Management based on their control self-assessment on all areas of their responsibility.

Minutes of Audit & Examination Committee meetings, which provide a summary of the proceedings, are circulated to Board members for notation and discussion.

AffinBAnk has an established Group internal Audit Division which reports functionally to the Audit & Examination Committee and administratively to the Managing Director/ Chief Executive Officer. The division is responsible for conducting independent audits in accordance with the approved annual internal Audit Plan.

RELATIONSHIP WITH AuDITORS

A professional and transparent relationship continues to exist between the Board/Audit & Examination Committee and the external auditors. The Audit Committee is authorized to communicate directly with both the external and Group internal auditors. A full Audit Committee report outlining its role in relation to the Auditors is also set out in the Annual Report. in addition, the external auditors meet with the Board at least once a year when the annual audited financial statements are presented to the Board.

ASSuRANCE

The Board through the Audit & Examination Committee has satisfactorily performed its oversight role in ensuring there is a sound internal control system and regular review on the adequacy and integrity of the system. Assurance on the effectiveness of risk management, control and governance process is obtained from the Management and Auditors (internal and external).

BnM auditors, Group internal auditors and external auditors conduct independent audits on AffinBAnk’s business operations, support activities and financial records and statements respectively to derive an opinion on the adequacy and integrity of AffinBAnk’s overall internal control framework.

finally, with the benefit of the above assurances and the external auditor’s comments incorporated in their audit report to the financial statements for the financial year ended 31 December 2012, the Board is able to conclude that AffinBAnk conducts its business prudently and in line with good governance practices.

Affin BAnk BERHAD (25046-T) 44 Annual Report 2012

STATEMENT ON INTERNAL CONTROL

Responsibility

The Board acknowledges overall responsibility for AffinBAnk Group’s system of internal controls and its effectiveness. The system of internal controls encompasses controls relating to financial, operational, risk management and compliance with applicable laws, regulations, policies and guidelines.

However, the system of internal controls is designed to manage rather than eliminate the risks of failure to achieve the goals and objectives of the Group. Therefore, it can only provide a reasonable and not absolute assurance against material misstatement of management and financial information, or against financial losses or fraud.

The Board has an established process for identifying, evaluating, managing and reporting all significant risks that may impact the achievement of business goals and objectives of the Group. The system of internal controls is dynamic and updated from time to time to meet the changes in regulatory guidelines and business environment. This process is regularly reviewed by the Board through its Board Risk Management Committee (BRMC) and Audit and Examination Committee (AEC).

The Board is of the view that the system of internal controls in place for the year under review is sound and sufficient to safeguard the investment of the shareholders, the interest of the customers and regulators, and the assets of the Group.

The management assists the Board in implementing the policies approved by the Board, implementing risk and control procedures, and developing, operating and monitoring internal controls to mitigate and control identified risks.

key Internal Control Processes

The key processes put in place to assist the Board in reviewing the adequacy and integrity of the system of internal controls include the following:

• Relevant Board committees are established with specific responsibilities delegated by the Board to deliberate on matters within the respective scope of responsibility. The committees are guided by written terms of reference and their minutes of meetings are tabled to the Board.

• The BRMC assists the Board in its supervisory role concerning the overall management of risk in the Bank. It has responsibility for reviewing and approving all risk management policies and risk management methodologies. BRMC also reviews guidelines and portfolio management reports including risk exposure information.

• The Board Loan Review and Recovery Committee (BLRRC) critically reviews loans and other credit facilities with higher risk implications, after due process of checking, analysis, review and recommendation by Group Risk Management and if found necessary, exercise the power to veto loan applications that have been approved by the Group Management Loan Committee (GMLC). BLRRC also reviews the non performing loan reports presented by the Management.

• Group Management Committee (GMCM), comprising the senior management team, assists the Board in managing day-to-day operations and ensure its effectiveness. GMCM formulates tactical plans and business strategies, monitors the Bank’s overall performance and ensures that the activities are in accordance with corporate objectives, strategies, policies and annual business plan and budget.

• The Group Management Loan Committee (GMLC) is established within senior management to approve complex and larger loans and workout recovery proposals beyond the delegated authority of the concerned individual senior management personnel of the Bank. The other committees comprising senior management include Asset & Liability Management Committee (ALCO) which manages market and liquidity risks and Group Operational Risk Management Committee (GORMC) which manages operational risk.

Affin BAnk BERHAD (25046-T)45Annual Report 2012

• A detailed budgeting process is in place with annual business plans and budgets prepared by the business divisions, reviewed by the GMCM and approved by the Board. The actual business performances are monitored against the approved targets and budgets of each business division by GMCM on a monthly basis.

• The business plan is supported by an annual credit plan, prepared by Group Risk Management and approved by BRMC. The credit plan sets out the prevailing risk appetite and provides credit strategies and lending guidelines for the development and management of new and existing customer relationships.

• Policies and procedures for key processes are documented and regularly updated to ensure relevance and compliance with internal controls, directives, laws and regulations. To enhance risk culture and awareness, road shows are undertaken by Group Risk Management across the Bank.

• Proper guidelines for the hiring and termination of employees, staff training programs and performance appraisals are established and other relevant procedures in place to ensure staff are adequately trained and equipped to carry out their responsibilities competently.

• An integrated risk management framework is in place. The risk management function operates in an independent capacity and is a part of the Bank’s senior management structure which works closely as a team in managing risks to enhance stakeholders’ value. its responsibilities extend to cover market, liquidity, credit and operational risks. The risk management function reports to BRMC.

STATEMENT ON INTERNAL CONTROL

Affin BAnk BERHAD (25046-T) 46 Annual Report 2012

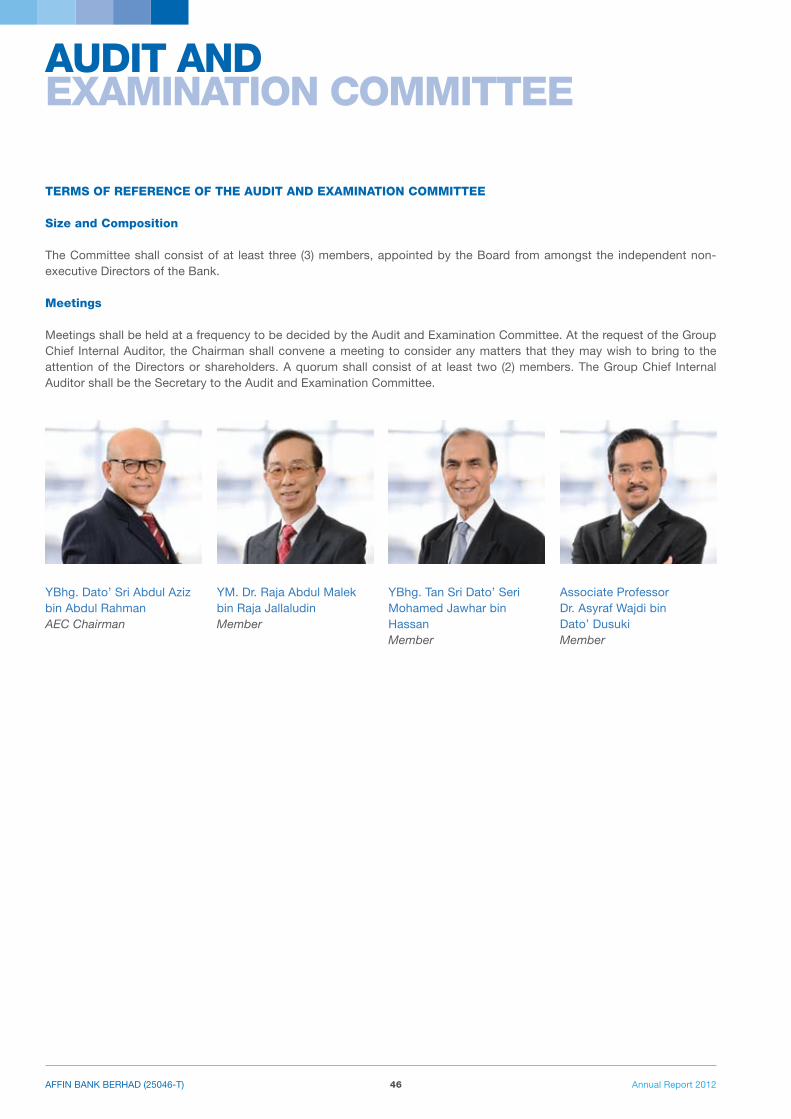

AuDIT ANDExAMINATION COMMITTEE

TERMS OF REFERENCE OF THE AuDIT AND ExAMINATION COMMITTEE

Size and Composition

The Committee shall consist of at least three (3) members, appointed by the Board from amongst the independent non-executive Directors of the Bank.

Meetings