Embed Size (px)

DESCRIPTION

Â

Citation preview

1

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Business Plan

2014 – 2018

Table of Contents

Page No.

1. Introduction 3.

2. Our Vision and Corporate Aims 5.

3. Our Priorities and Key Projects 6.

4. Our Risks 14.

5. Our People and Our Structures 16.

6. Appendices 18.

Appendix A Our Progress against Previous Objectives 19.

Appendix B How It All Fits Together 26.

Appendix C Financial Forecasts 1.

Base Assumptions 5.

Current Financial Projections 6 – 8

3

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Introduction

In 1900 George Cadbury founded the Bournville Village Trust

(BVT), a charitable organisation set up to ensure the planned

development and maintenance of the Estate and to preserve it

for future generations. The Deed of Foundation ensured that

surplus income was devoted to the improvement of the

Bournville Estate and the encouragement of better building

elsewhere. The founding of BVT signalled a change from

merely a building estate into a complete village community.

Shops, places of worship, open spaces, sports facilities,

community buildings and schools were included to form the

heart of the new model village.

Over one hundred years on, the Trust continues to allocate

homes to people in the greatest housing need to live in our

mixed communities. The estate now comprises 1,000 acres of land with almost 8,000

homes, ranging from one-bedroom flats to five-bedroom houses, split just about equally

between tenanted and owner-occupied. BVT remains at the forefront of housing provision

for architectural design, estate management and development. By keeping sustainability

(environmental, social and economic) at the forefront of our thinking, BVT has gained the

reputation of being a model estate whilst remaining committed to keeping faith with our

Founder’s aims.

Our responsibilities are diverse and whilst our core activities reflect our status as a housing

association, we embrace a wide range of roles that support the original aims of the Trust and

help make BVT the unique organisation it has always been:

The provision of housing management and repairs services to general needs rented

accommodation; shared ownership homes; and a leasehold scheme for older people.

The provision of sheltered, residential care and nursing accommodation for older

people and supported housing and care services for special needs groups – in

particular for young people leaving care and for people with learning difficulties.

The long-term maintenance of the overall amenities and appearance of the Bournville

Estate which comprises 1000 acres of land and almost 8,000 households in south

west Birmingham.

Bournville Almshouse Trust, which owns almost 100 almshouses, flats and houses,

run by the same 12 Trustees as BVT.

A subsidiary, Bournville Works Housing Society, which owns 314 homes on the

Bournville Estate. Management and maintenance of this stock is undertaken by the

Trust under the terms of an Intra Group Services Agreement.

In terms of developing new homes our main focus is on:

The creation of an urban village of over 1,000 new homes at Lightmoor in Telford,

Shropshire.

George Cadbury

At Lawley, in Telford, providing rented and shared ownership housing and taking lead

responsibility for estate management or stewardship services to a mixed-tenure new

village, growing to 3,000 properties by 2027, in partnership with Sanctuary Housing

Group.

A new care village for Bournville on the old Bournville College site (College Green).

The first phase will be a large Extra Care project to provide 212 apartments, including

some for rent through BVT, with a range of fantastic facilities. This project is in

partnership with Extracare Charitable Trust and Birmingham City Council.

The running of two major direct labour organisations:

Bournville Propertycare Services (BPS) providing a top quality repairs service to our

housing stock in Birmingham and Shropshire in addition to work undertaken for other

clients.

Bournville Village Landscapes (BVL) providing a top quality landscaping service to

the Bournville Estate on behalf of the Trust.

Outside of our core housing association activities:

Responsibility for overseeing the maintenance of the external fabric of Bournville

Infant and Junior Schools.

An in-house Architects Team (Bournville Architects) which undertakes a wide variety

of architectural work on behalf of the Trust and a range of external clients.

The running of Selly Manor Museum located in the heart of the Bournville Village

Conservation Area. Selly Manor itself dates back to at least 1327 whilst an adjacent

building, Minworth Greaves, is even older. The whole site is a very attractive visitor

destination, which gives people the opportunity to learn about the Tudor way of life.

The Bournville Experience – a hands-on visitor attraction, run jointly with Cadbury

World, offering a variety of exhibits about the development of Bournville Village. Entry

to the Bournville Experience is free of charge.

The running of an Agricultural Estate comprising over 2,500 acres on the south-

western edge of Birmingham.

The Trust owns a number of Community Halls and Shops which are let on

commercial leases. A Community Services Team is dedicated to ensuring that the

communities in which we work are well served with a range of facilities and that they

are flourishing places where people will choose to live.

Strong business support services covering the Business Improvement Unit, financial

and human resources administration plus information technology support.

5

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

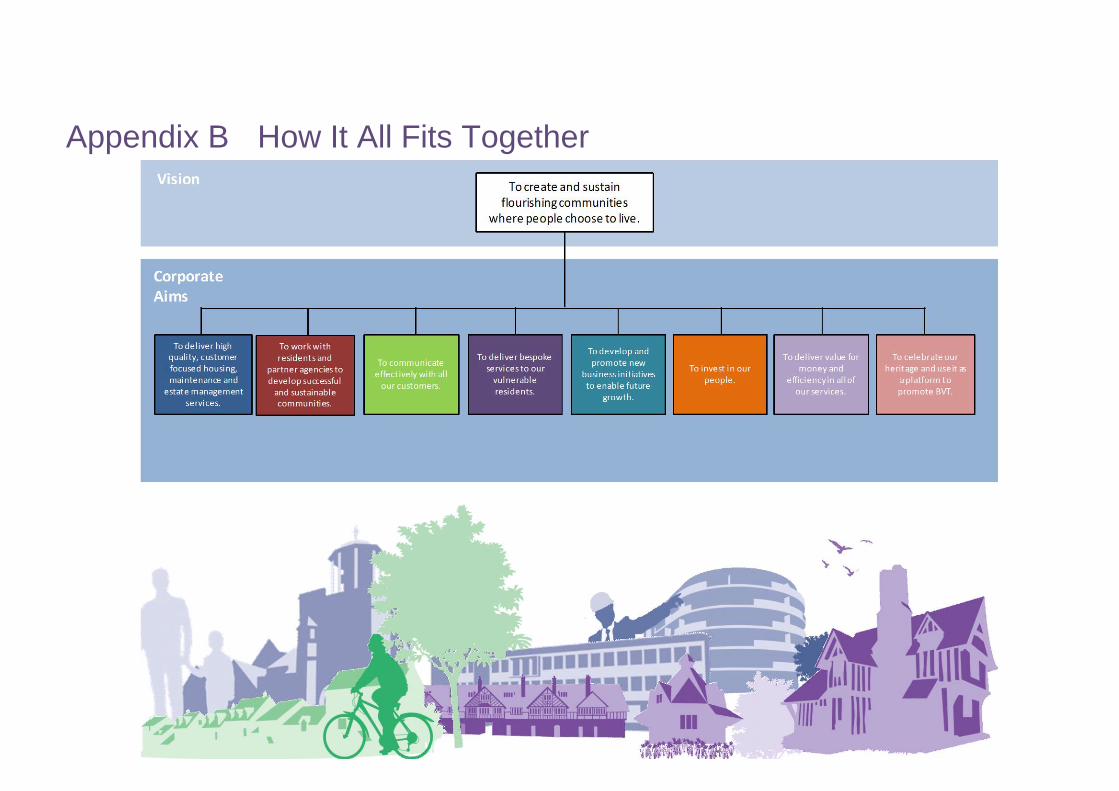

Our Vision & Corporate Aims

Our Vision

Bournville Village Trust has a very long history that is steeped in a reputation for high quality

housing and estate management services. Sustaining this level of quality is never easy and

the environment we work in is constantly changing. To continue to thrive as a housing

organisation over the next five years and beyond, we must continually look ahead,

understand the trends and respond to the external factors that will shape our organisation

and our customers’ needs and expectations in the future and move swiftly to prepare for

what is to come.

Our vision and corporate aims create a long-term destination for our organisation and

provides us with a framework for our “Journey to Excellence”, guiding every aspect of our

work by describing what it is we are trying to accomplish.

Our Corporate Aims

In order to achieve our vision, we have a clear set of corporate aims that support this ideal

and which the entire organisation continues to work towards with the development of new

and innovative projects.

To deliver high quality, customer focused housing, maintenance and estate

management services.

To work with residents and partner agencies to develop successful and sustainable

communities.

To communicate effectively with all our customers.

To deliver bespoke services to our vulnerable residents.

To develop and promote new business initiatives to enable future growth.

To invest in our people.

To deliver value for money and efficiency in all of our services.

To celebrate our heritage and use it as a platform to promote BVT.

To create and sustain flourishing communities where

people choose to live.

Our Priorities & Key Projects

To deliver high quality, customer focused housing, maintenance

and estate management services.

Our primary aim is to provide good

quality, affordable housing,

maintenance and estate

management services to people

both in housing need and to our

communities as a whole. This

involves a wide range of activities

from processing applications,

recovering rent arrears, managing

anti-social behaviour and repairs

programmes to resident

involvement and organising

important community events. As

part of this, we must ensure our

housing stock and estates are well maintained and in good condition. This means providing

our residents with a high quality, fast and efficient repairs service; delivering improvement

programmes to keep our properties up-to-date and warm and comfortable to live in; and

providing and maintaining an environment which is a safe and attractive place to live.

Our priorities and some key projects in delivering high quality, customer focused housing,

maintenance and estate management services for 2014 to 2018 are:

To continue to work towards mitigating the impact of the Welfare Benefit

Reforms through the delivery of our Anti-Poverty Strategy.

Now we are in our new offices we aim to complete the sale of the

former Estate Office on Oak Tree Lane and let the former

Bournville Area Office and Sycamore House on Sycamore Road.

Raise the profile of the Shenley shopping area in order to

ensure the area is sustainable for our local communities.

Carry out a Condition Survey of the estate infrastructure with a

view to planning future renewal programmes.

To continue to achieve the Decent Homes Standard and improve

our SAP rating by continuing our commitment to our 30 Year

Planned Maintenance plan for BVT and BWHS.

The new BPS van liveries

7

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

To work with residents and partner agencies to develop successful

and sustainable communities.

Building and sustaining successful communities is a collaborative effort and requires the

input of not only ourselves and our residents but several other partner agencies. This is a

fine balance and whilst we continue to develop our new homes and communities in

Shropshire, we continue to invest in our established communities in Birmingham and

elsewhere, by looking for opportunities to improve our working relationships with our

stakeholders.

Resident involvement is the name most housing organisations give to all the activities

undertaken that help them understand what their residents need and want, and that enable

residents to influence, challenge and scrutinise the services they receive. Over the past few

years, there has been increasing government emphasis on choice, accountability and

localism. These common themes have led to the development of a co-regulation approach

which BVT have adopted through the introduction of our cross tenure Scrutiny Panel made

up of tenants, freeholders and leaseholders. This is supported by a robust resident

involvement framework that provides residents with the opportunity to get involved with

specific service areas and to have a real input in the decisions that affect them and their

wider communities. Our priorities and some key projects in terms of working with residents

and partner agencies for 2014 to 2018 are:

Review our Resident

Involvement Framework in

order to ensure we are

engaging with our

residents in the most

effective way.

To progress the Shenley

Feasibility Study which will

help us support our local

communities by providing

appropriate services in

those areas.

To continue progressing

our green initiatives including exploring the possibility of an Eco-

demonstration Project at Lightmoor.

Residents attending our 2013 Better Living Exhibition

To communicate effectively with all our customers.

Effective communication is always a

challenge and we continue to work hard in

ensuring that good communication is at the

heart of providing the very best in customer

service. In practical terms, this could mean

the way in which we communicate with our

customers over the telephone, in our letters

and emails, during visits or it could mean

the contents of the publications in our

newsletters or on our website. To provide

good customer service we need to

understand what our customers want and

how they feel about the services provided

to them. This means we need to share

information with them and listen carefully to what they are saying. Equally, our customers

need to understand what we are telling them and what it is we are able to do for them.

Communicating effectively with our customers is essential to the successful delivery of all

our projects and services and remains a long term key priority for the organisation. Our

priorities and some key communication projects for 2014 to 2018 are:

To develop a Digital Inclusion Strategy that will help to support our

customers online.

Begin to use our customer satisfaction data that has been collected

using the operatives’ Personal Digital Assistant (PDA) system as a

way of improving our services.

Carry out a review of the current BVT website in

order to ensure it is customer focused and easy to

use.

To continue to work with the Customer Services

Team ensuring that as many queries as possible

are answered at the first point of contact.

Carry out a review of all current

communications, including our standard letters

in order to ensure the content is current and

appropriate to our customers’ needs.

Members of our Customer Services Team

9

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

To deliver bespoke services to our vulnerable residents.

Our services are delivered to a wide

range of people including those

who could be considered

vulnerable. We recognise that we

have a responsibility to ensure that

the vulnerable and socially

excluded are protected and are

able to access those services. We

make continuous efforts when

dealing with our more vulnerable

residents to ensure they can

access our services by putting

processes in place that are

sensitive to individual needs and

provide adequate opportunities

to access support networks when necessary.

Many of our current projects are looking to address the specific needs of our more

vulnerable residents and we are fully aware of our responsibilities in terms of the provision of

support and ensuring their ability to access not only our services but third party provision

also. Our priorities and some key projects for delivering bespoke services to our vulnerable

residents for 2014 to 2018 are:

To promote Selly Wood House.

To develop a Home Care Service that is available for all residents in order to

help residents to stay in their homes for as long as possible.

To implement BVT’s Dementia Action Plan in order to promote a dementia

friendly community in Birmingham and Telford.

To progress the College Green development towards its 2015 completion,

providing a brand new Care Village for Bournville.

Concept art-work for the gardens in the extra-care scheme at College Green

To develop and promote new business initiatives to enable future

growth.

Every sector is in a constant state of change and the Housing Sector is no different. In order

for our organisation to remain at the forefront in terms of delivering high quality housing and

a range of services, we must continually look ahead, understand the needs of our customers

and provide services that are value for money, all whilst safeguarding our history and our

excellent reputation in the sector. It is for this reason and the need to draw in external

income in a difficult economic climate, that a strategic decision was made to begin identifying

gaps in our service delivery and explore opportunities for new business initiatives within our

commercial arms, namely Bournville Propertycare Services (BPS) and Bournville Architects.

The unique work carried out by both teams has helped secure the organisation’s reputation

as a lead service provider and helps to underpin and deliver our commitment to good quality

distinctive design. Bournville Architects in particular makes an important contribution to our

work on environmental sustainability and has been doing so throughout most of the long

history of BVT. Our priorities and some key projects in the development of new business

initiatives for 2014 to 2018 are:

To explore the promotion and marketing of BVT’s stewardship services on a

consultancy basis to other large new developments.

To work towards possible

input into the

development of the Selly

Oak Hospital site.

To move day to day

electrical works in house.

To showcase Bournville

Propertycare Services as

a beacon DLO and

arrange site visits from

other housing

associations.

Employ a Professional

Fundraiser post within

BVT to help bring in funding to support our projects.

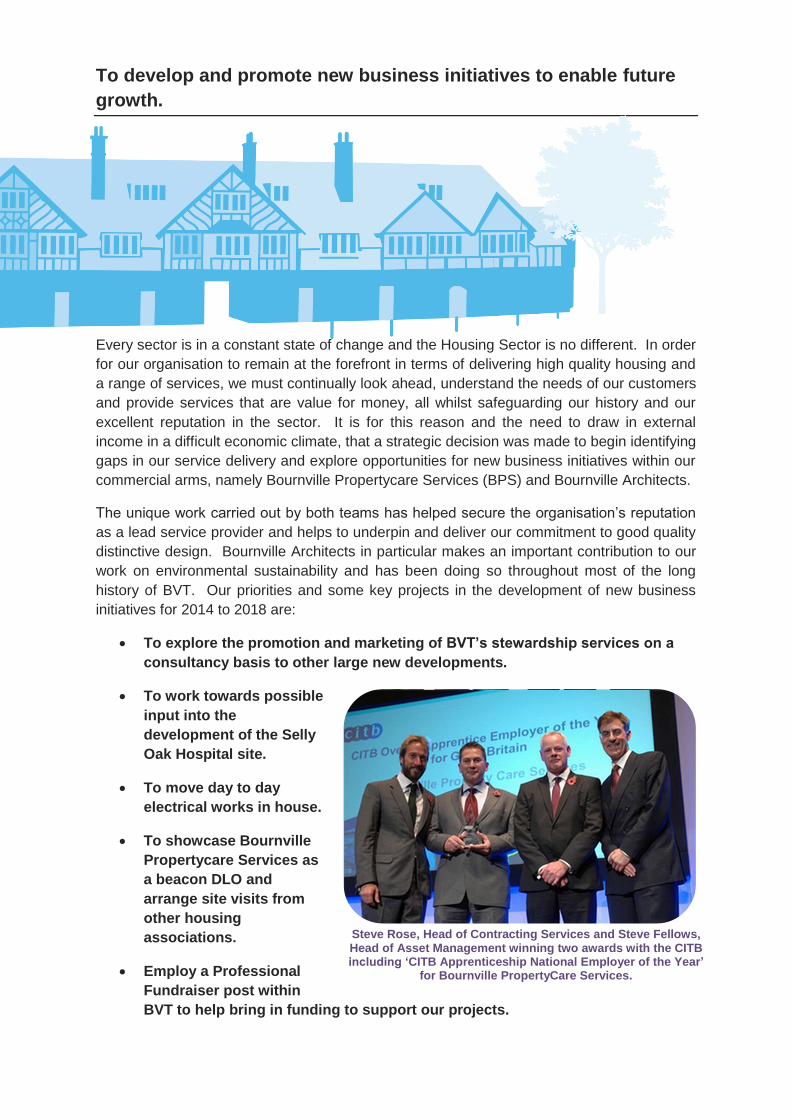

Steve Rose, Head of Contracting Services and Steve Fellows, Head of Asset Management winning two awards with the CITB including ‘CITB Apprenticeship National Employer of the Year’

for Bournville PropertyCare Services.

11

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

To invest in our people.

We believe that the continued

success of our organisation depends

on the continued commitment and

productivity of our staff. People are

our most important asset, an

investment that needs to be

cultivated and properly managed.

We recognise that investing in staff

has an impact in many different

ways. It reduces staff turnover and

sickness absence and investments

in employee engagement

programmes, training, mentoring,

support, communication, healthcare

incentives and technology all have a

positive effect on our workforce performance and productivity. In 2013, we were awarded

‘Apprenticeship National Employer of the Year’ by the Construction Industry Training Board.

An organisation as varied as ours also boasts a wide range of job types, from plumber,

carpenter, electrician and gas fitter to care workers, administration staff and architects, all of

whom work with different requirements and risks on a day to day basis.

We continue to invest in staff training, health and safety and staff support and a number of

key projects and priorities will be implemented for 2014 – 2018:

Carry out a twelve month review of the Customer Services Team which will

include updated training and personal development plans.

Implement auto-enrolment ensuring that all qualifying staff are included on a

pension scheme unless they opt out.

Carry out improvements and energy efficiency works

to the Five Gates Depot, Willow Road,

Provide additional office accommodation

and a staff room at Cherry Tree House,

Lightmoor Village.

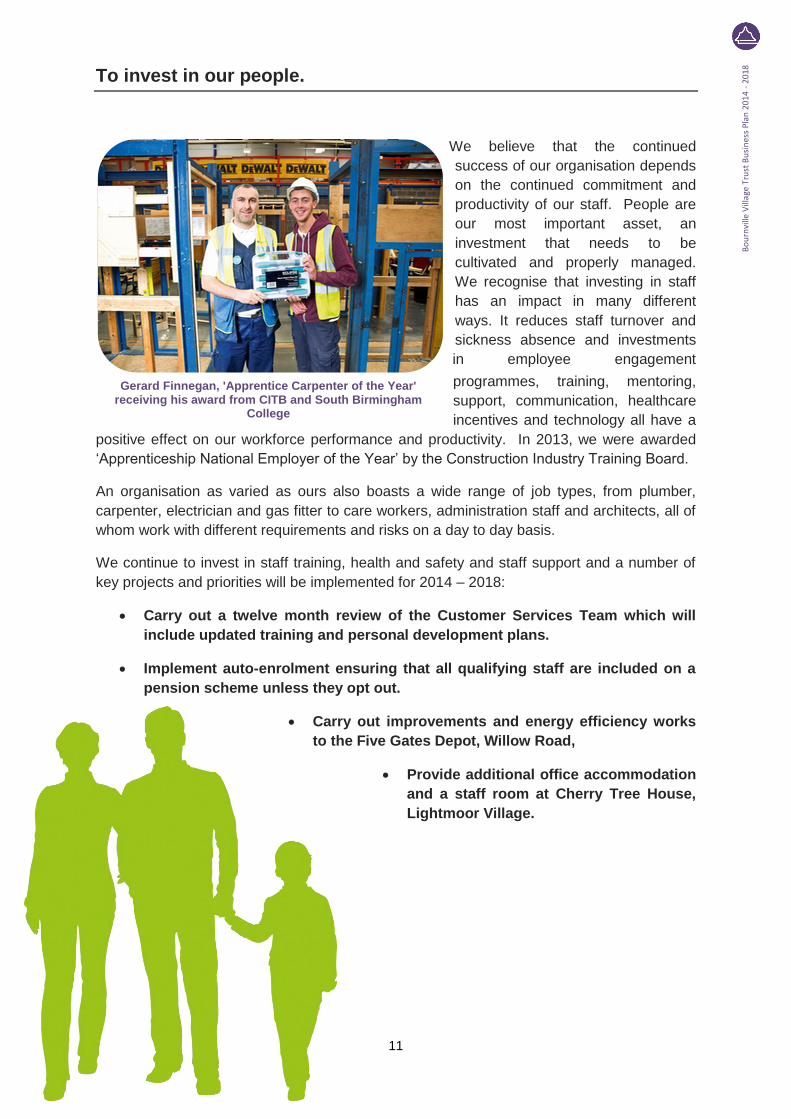

Gerard Finnegan, 'Apprentice Carpenter of the Year' receiving his award from CITB and South Birmingham

College

Dame Elizabeth Hall on Oak Tree Lane, Bournville

To deliver value for money and efficiency in all of our services.

These are difficult economic times for

everyone and constrained public spending

coupled with the general economic

downturn, means that organisations such

as ourselves and other service providers

are under pressure to deliver value for

money and efficiencies in all that we do.

We do have some advantages over other

housing organisations which mean we are

better placed than many others to

navigate our way through these more

difficult times but the challenge is clear.

Providing efficient services that are value

for money for our residents is a key priority

for our organisation and we work continuously to ensure we are as cost effective as

possible. Many of our current projects are looking to address the value for money and

efficiency agendas and some key projects for 2014 – 2018 are:

To develop a Social Value model for BVT to use and apply to all our key

projects.

To implement an Asset Management Plan for our Community Halls.

Introduce a new self-assessment model to identify efficiencies and areas for

improvement.

Work towards providing a more efficient IT Helpdesk service.

Roll out Microsoft Office 2010 for all staff

in order to ensure a consistent approach

across all our offices.

Modernise Bournville Village Landscapes

and develop a new Risk Assessment

model for that part of our Organisation.

13

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

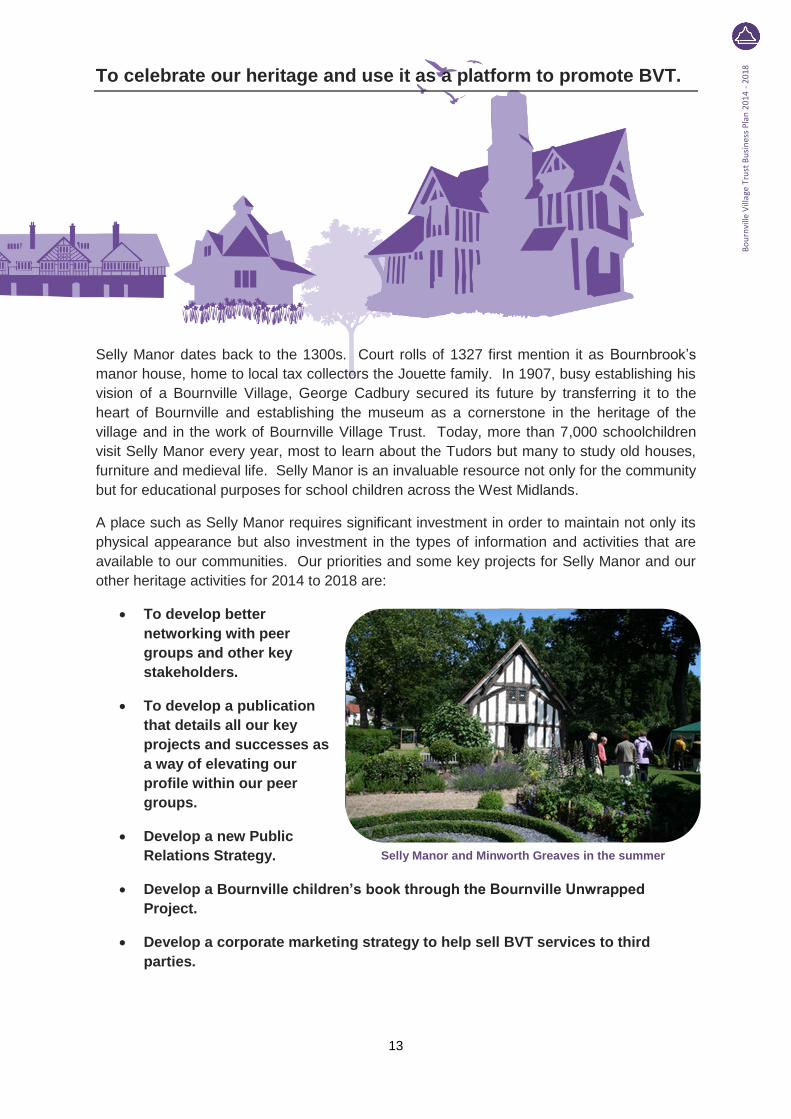

To celebrate our heritage and use it as a platform to promote BVT.

Selly Manor dates back to the 1300s. Court rolls of 1327 first mention it as Bournbrook’s

manor house, home to local tax collectors the Jouette family. In 1907, busy establishing his

vision of a Bournville Village, George Cadbury secured its future by transferring it to the

heart of Bournville and establishing the museum as a cornerstone in the heritage of the

village and in the work of Bournville Village Trust. Today, more than 7,000 schoolchildren

visit Selly Manor every year, most to learn about the Tudors but many to study old houses,

furniture and medieval life. Selly Manor is an invaluable resource not only for the community

but for educational purposes for school children across the West Midlands.

A place such as Selly Manor requires significant investment in order to maintain not only its

physical appearance but also investment in the types of information and activities that are

available to our communities. Our priorities and some key projects for Selly Manor and our

other heritage activities for 2014 to 2018 are:

To develop better

networking with peer

groups and other key

stakeholders.

To develop a publication

that details all our key

projects and successes as

a way of elevating our

profile within our peer

groups.

Develop a new Public

Relations Strategy.

Develop a Bournville children’s book through the Bournville Unwrapped

Project.

Develop a corporate marketing strategy to help sell BVT services to third

parties.

Selly Manor and Minworth Greaves in the summer

Our Risks

As with all successful housing organisations, we adapt and change what we do and how we

do things in response to unforeseen events and periods of difficulty, whatever the cause.

Recognising, controlling and managing risk has always been a critical consideration in our

approach to good governance. It is a central feature of our day-to-day and operational

management and is fundamental to Trustee and Executive Team initiatives, audit and

strategic planning.

The organisation has well developed internal controls and risk management processes. Our

corporate and departmental risk maps are reviewed regularly by the relevant Committees

who exercise robust and thorough oversight of governance and risk management systems.

This is further complemented and checked by Gateway Assure, our internal auditors. Even

so, to further strengthen our resilience we have worked with our Scrutiny Panel in 2012 who

chose to review with a critical eye our corporate approach to financial risk management.

They have looked at our processes and concluded that financial risk management at BVT is

handled effectively but that the following key issues merit some further attention due to the

longer term nature of their potential impact on the organisation and the environment:

Car parking across the estates.

The future viability of our shops.

Making use of our open spaces.

Actions have been attached to these risks and work will begin in terms of addressing these

issues during the lifecycle of this Business Plan period.

With regards to our shorter term risks, Trustees regularly review our risk map to ensure we

know what our major risks are and consider what we can do to minimise the probability of

the risks materialising and the potential impact, should they occur. The following are some

of our key risks over the next five years and should be viewed alongside the information

detailed in Appendix C, Financial Forecasts:

Breach of Loan Covenants

Like many housing associations, BVT has financed its development programmes over the

years through taking out loan funding. We have always sought to ensure that these loans

can be paid back over time from the income streams of the business and that continues to

be the case today. These loans do come with certain conditions (known as loan covenants).

It’s always been important to meet these loan covenants, but nowadays it is more important

than ever. That’s because the loans we have with some of the major banks were all taken

out before the credit crunch and are therefore on much more attractive terms than we would

find today. Banks are always looking for opportunities to re-negotiate older loans and breach

of loan covenants would give them the opportunity to do so. The impact of a breach of loan

covenant would see a big increase in the cost of servicing our loans – perhaps increasing

our interest costs by as much as 40% or around £1.9m a year.

To minimise this risk, Trustees monitor covenant compliance projections for the future to

identify potential issues as soon as possible and then to identify mitigation strategies should

15

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

that be necessary. Our latest projections indicate full compliance with loan covenants.

However, this is something that we are ever vigilant about and our efficiency agenda is partly

intended to give us further headroom against these loan covenants in the future (as well as

delivering better value for money for our customers).

Welfare Benefit Reforms

Over the next few years, we are going to see some major changes to the Welfare Benefit

System. The impact of the 'bedroom tax' in relation to under-occupation will reduce Housing

Benefit in the short term. Various benefits have already been reduced and tenants’ incomes

are or will be affected. Universal Credit is due to be phased in, in the near future, rolling

many welfare benefits into one and apart from vulnerable tenants, benefits will be paid direct

to the tenant rather than to the landlord as it is now. These changes will cause a

considerable challenge to residents juggling limited finances and it is inevitable that our rent

arrears will increase despite much support and advice being given to tenants.

BVT has therefore developed an Anti-Poverty Strategy to address these changes. The

strategy has a number of strands such as educating tenants about the changes and seeking

to re-locate tenants if they are going to be unable to meet their rent because of the reduction

in the benefit they receive.

Pensions

As a responsible employer, BVT have for many years provided a pension facility for its staff.

In the main, this has been through our membership of the Cadbury Pension Fund, although

since 2010, new employees have not been eligible to join the Cadbury scheme and therefore

BVT has set up its own pension scheme (BVT Pensionsaver).

The Cadbury Pension Fund, like many pension schemes, is currently in deficit and the

Trustees of the Pension Fund have put in place a series of measures to eliminate that deficit

in the medium term. Fundamentally, these measures involve the employers contributing

more towards the fund and BVT has therefore seen a significant increase in its pension

contributions over the past couple of years. Those increased contributions are likely to be

required throughout the business plan period and are therefore reflected in the financial

projections in this Business Plan.

The other key factor is the introduction of auto-enrolment. This will mean that BVT

employees who are not currently in a pension scheme will be automatically enrolled into the

BVT Pensionsaver scheme, unless they opt out. Currently we have 170 staff who are not in

a pension scheme, so there will be another sizeable increase in our pension costs as a

result. For BVT, auto enrolment comes into effect in 2014 and again, the financial impact has

been reflected in the business plan projections.

16

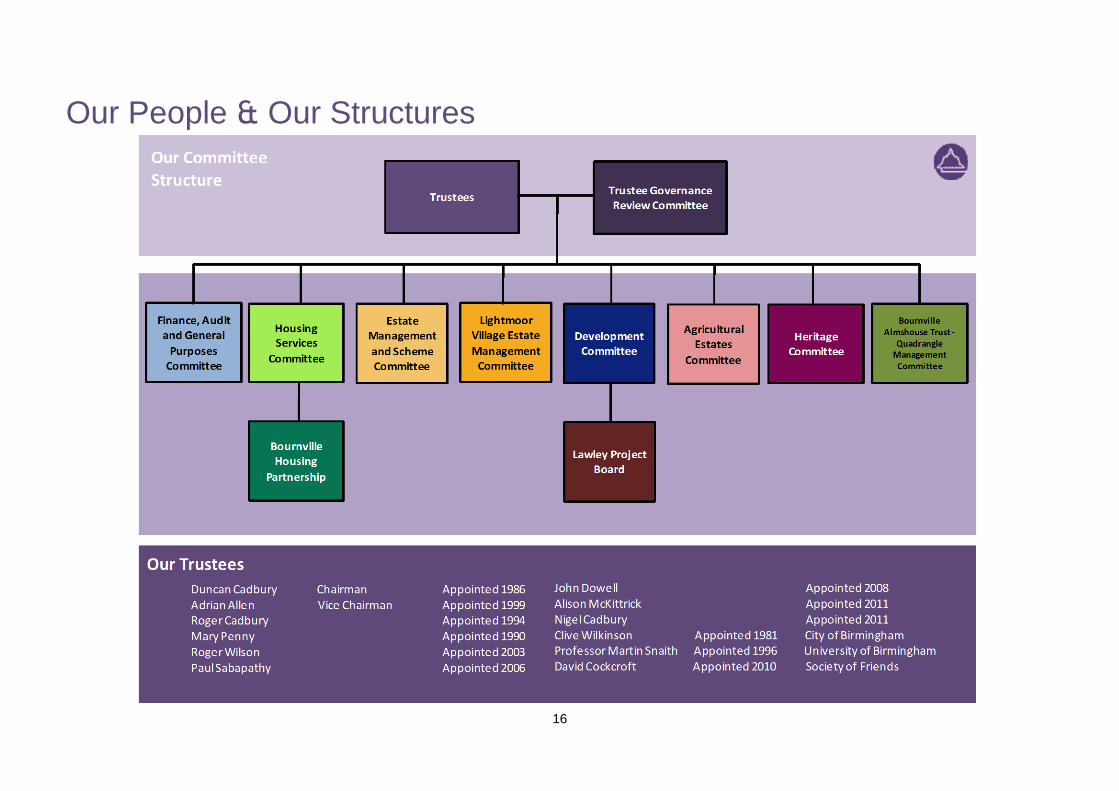

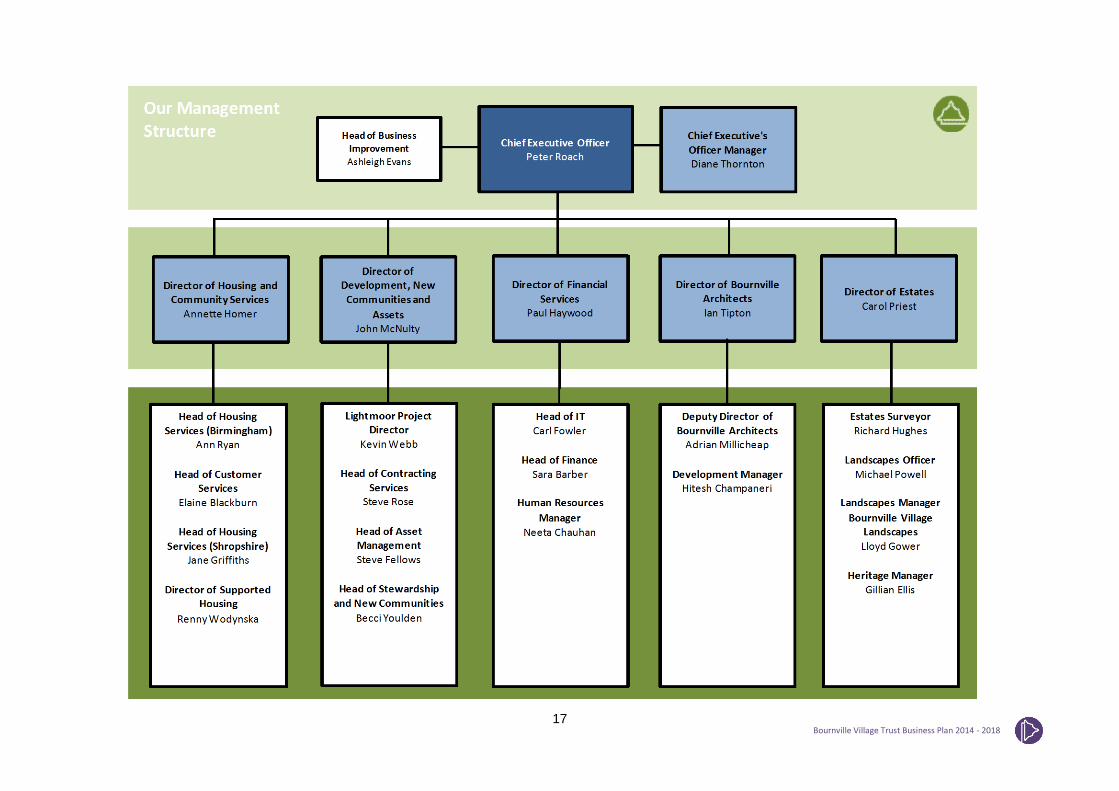

Our People & Our Structures

17

Bournville Village Trust Business Plan 2014 - 2018

18

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Appendices

19

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Bournville Village Trust Business Plan 2014 - 2018

Appendix A Progress Against Previous

Objectives

To deliver high quality, customer focused housing, maintenance and estate management services

Estate Management

Objective Progress

Gather views from a wide cross-section of residents into the future provision and use of open spaces on the Estate. We will then make proposals for a future strategy.

The three Village Councils/Residents Associations have been asked to carry out a consultation exercise with residents in their areas to ascertain aspirations for the BVT open space on the Estate.

In addition, opinion was canvassed at the 2013 Open View event. Very few comments were received but suggestions of more bins and benches were put forward, and some comments about the need for more facilities for youngsters.

We are awaiting feedback from Village Councils. In addition it may be appropriate to prompt a response through the Spring edition of InView magazine.

Look to draw up a strategy to re-vitalise our shopping areas, which would examine the most effective ways of sustaining the commercial viability of local shopping facilities.

External advisors have been briefed to review the commercial property portfolio and work is currently in hand.

Improvement programme for agricultural estate cottages and houses (via BVT Asset Management Team).

Asset Management have completed and issued a comprehensive survey and planned maintenance plan for all cottages and houses not directly connected to a farmstead to provide a programme of work for forthcoming years subject to budgetary provision. Some works identified are planned for 2013.

Review proposals from recent strategic review of agricultural estate by Smiths Gore.

Smiths Gore continue to progress the review of proposals raised in their strategic review of the Estate, and are continuing to report to the Agricultural Estates Committee at each of their meetings.

Corporate Services

Set up a new Customer Services Team at 350 Bournville Lane.

The new Customer Services Team was launched in May 2013 to coincide with the opening of our new office. The Team are working well together and much positive feedback has been received from residents and colleagues.

I.T

Review Disaster Recovery arrangements to cater for A fair amount has been completed on setting up a replication

transfer of services from Estate Office to 350 Bournville Lane.

system to operate from Cherry Tree House. The process has been a little more problematic than first envisaged, but this should be finalised early in 2014.

Planned Maintenance

Beyond Decent Homes - continue to invest and deliver our property investment and cyclical repair portfolio in compliance with our 30 year plans in Birmingham and Shropshire.

Planned and Cyclical repairs are near to completion and all contracts completed in line with our improvement programme and budgetary commitments.

Customer satisfaction with work carried out is shown at an all time high

2013 will see the end of the metal window replacements in Birmingham.

Empty property refurbishments (voids) continue to rise in number and expense with 2013 seeing a record year for property terminations

Bournville PropertyCare Services

Continue to develop mobile working, thus enabling BPS to establish its reputation as a leading DLO and improve the customer experience.

Mobile working is 90% operational. Customers have already noticed an improvement in the service and this technology has brought BPS right into the 21st Century. Gas will be the next stage of the project and will be introduced in Spring 2014.

Stewardship and New Communities

Take into management areas of public open space in Woodlands Park, Hollywell Meadow, Little Green Avenue, various smaller areas of Oakham Manor and the LEAP on phase 1b at Lawley.

Woodlands Park, Holywell Meadow and the wildflower meadow (Woodlands East Meadow, part of L2) – completed. Transferred to BVT and within management. Fields in Trust deed also completed.

Various land areas at Oakham Manor (Little Green Avenue and Stocking Park Road), are not yet complete.

Taylor Wimpey have yet to do works to rectify certain problems and bring the scheme to an acceptable standard before it can be recommended that BVT take the land areas into management.

Take courtyards into management at Lawley. The works to complete the courtyards and mews links at Lightmoor have been undertaken by Crest and snagged by the Trust. The final snagging works have commenced and this will then allow the courtyards to be transferred.

As referred to above, Taylor Wimpey courtyards require remedial work before they can be brought into management.

The Barratt and Persimmon courtyards on Lawley phases 1A and 1B have been completed and recommended to Trustee’s to be transferred into joint ownership between the Trust and Sanctuary.

Housing Services

Herefordshire Housing - monitor and review the out of hours service to embed new service provider.

Review carried out, no concerns raised. The service is working well. Next review meeting arranged for January

21

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Bournville Village Trust Business Plan 2014 - 2018

2014.

The Quadrangle - to replace the defective 'special' ridge tiles to all roofs.

Works completed. As the contract progressed, essential works to the chimney stacks were identified. These works have been included in the 2014 budget.

To support tenants through the Welfare Benefit Reforms to protect the Trust's income, and continue to work through the Anti-Poverty Strategy Action Plan.

Following Trustees’ support, we have taken on additional temporary staff to give Welfare Benefit Support to tenants. We have developed a more robust data base in terms of tenants experiencing difficulties and have been forming new partnerships with organisations to whom we can signpost tenants. Many positive outcomes have been achieved helping tenants apply for Discretionary Housing Payments. Support to tenants is time consuming and ongoing but very worthwhile and is essential work in protecting our rental income stream. Our income recovery team continues to take action in line with policy but courts are reluctant to grant even suspended orders if tenants are experiencing financial difficulty.

A successful internal audit was undertaken in October 2013 “Rental Income – Welfare Reform”, the objective being to ensure that the Trust has taken suitable steps to minimise the impact of the Government’s changes to the welfare benefits system on the collection of its rental income. A “substantial” rating was awarded in this respect.

To work with residents and partner agencies to develop successful and sustainable communities

Estate Management

Assist in planning for new investment at Rowheath Park and Pavilion.

Proposals for improvements to the Pavilion and a new changing facility were approved by Estate Management and Scheme Committee, and have also received planning consent.

Funding is currently being sought by Rowheath. BVT have pledged £105,000. Progress is expected in 2014.

Community Services

Promote and raise the profile of the Volunteer’s Bureau in order to support the aims of our Anti-Poverty Strategy.

Much work has gone into progressing the Volunteer Bureau over the past few months with updated processes and procedures. To date, over 5152 hours of voluntary work has been recorded so far this year. We recently commissioned an independent review of this service area, the report is due shortly.

Development

Lightmoor - progress the next phase of new high quality homes through the Joint Venture with Homes and Communities Agency, i.e. Lightmoor Green Phases 3 and 4.

Crest are on site and making good progress.

Progress the Croppings Phase 1 Public Land Initiative Good progress on site. Sales are progressing at a pace, with many off plan purchases. First houses handed over to

to deliver 150 houses through Keepmoat Homes. residents, and more in the pipeline.

Lawley - progress phases 3, 4 and 6 to provide quality homes through the Joint Venture with Sanctuary HA.

33 properties for rent and shared ownership secured at phases 3 and 4, expected to be completed 2015 and 29 properties to come over to BVT at phase 6 – completion expected summer 2016.

Possible conversion of Estate Office to flats in conjunction with the disposal programme of satellite offices.

Regular reports have been brought to Trustees and work is well in hand.

Stewardship and Communities

Devise a programme of community activities and events via an Events Planning Group to encourage community cohesion and promote the work of BVT and local community groups - Lightmoor and Lawley.

The event planning group in Lightmoor Village has been formed and have planned a variety of events for the rest of the year.

In Lawley, work continues with residents to foster a community spirit that will enable the formation of an events group. Events are planned in Lawley for the rest of this year to engage with residents.

Joint events with Lawley and Lightmoor are also planned to bring the two communities together. BVT use the events to promote the positive work that is done in each community.

Establishment (through the Resident Involvement Strategy) of Lawley Village Management Board. Aim to increase resident satisfaction with IMS and have more say in the running and development of the services provided by IMS.

Work is progressing on a new Resident Involvement Structure.

Hold elections for resident representation to the Lightmoor Village Estate Management Committee.

Elections were held and the resident reps. selected. The residents attended the LVEMC meeting in April as visitors, and will attend as reps. in August. Already, the relationship between the reps., LVRA, and BVT has become stronger due to the insight the reps. have of the work BVT do in Lightmoor to sustain and promote the community.

Community Services

Launch a recruitment campaign in order to attract more residents to our Points of View Panels and our Scrutiny Panel.

The Resident Involvement Structure is currently being revamped to ensure it meets both the Trust’s and our customers’ requirements. There will be greater emphasis on themed project groups and the use of social media in addition to the valuable contribution of our three Resident Associations.

OpenView 2013 attracted some 500 residents and we collected 54 expressions of interest in getting involved, which we have followed up. We have also developed much closer links with our Volunteer Bureau and directed people onto activities from this link. This is work in progress and will be further developed in 2014.

To communicate effectively with all our customers

23

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Bournville Village Trust Business Plan 2014 - 2018

Community Services

Embed the new OpenView customer forums and to continue to utilise the website as a way to gather views and provide insight into the priorities of our wider community.

The Forums have been developed to make them easier to use and they can now be accessed via social media. Vision 13 voting saw almost 2000 people visit our website to cast their votes, the highest number ever. A wide variety of website articles have been produced by the Community Team over the past few months publicising activities and ways to get involved with BVT.

The Team are also working with our Residents Associations to help them develop their own websites and train members in their upkeep.

Expand and develop the annual OpenView event as a way to capture feedback and raise the profile of BVT within the wider community.

This year’s OpenView event at Rowheath took place on 21st September. Some 500 residents attended and gave us their views on a wide range of topics. OpenView is our biggest corporate event aimed at raising our profile within the locality and we are currently exploring what OpenView 2014 will look like. However, there are numerous other initiatives in place (and being developed), to raise our profile including our significant partnership work and regular presence at Bournville Festival. This year we were joined by the Busy Parents Network, Selly Oak Live at Home Scheme and Street Associations.

Business Improvement Unit

Use the feedback and outcomes from the Annual Satisfaction Survey to identify areas for improvement and respond to them through the work of various teams across the organisation.

This work is ongoing and the Satisfaction Surveys provide us with valuable data, enabling us to focus on areas for improvement.

I.T.

Explore the possibility of implementing a new GIS Mapping System for use across the organisation once we have moved to 350 Bournville Lane.

New system (GeoSamba) has been implemented prior to office move.

To develop and promote new business initiatives to enable future growth

Bournville Architects

To outperform the 3 year support package agreed with Trustees in 2010.

Bournville Architects returned to surplus 12 months earlier than originally anticipated.

2011 2012 2013

Profit/ (loss) before Capital As approved by Trustees

(65,000) (15,000) 15,000

Profit/ (loss) before Capital Actual

(59,708) 19,720 16,000 (outturn forecast)

Heritage

To increase visitor figures to Selly Manor by 5%. Still expecting to achieve this target for 2013.

Community Services

Increase usage and sustainability of both Shenley Court Hall and Phoenix Hall to ensure that they continue to meet the needs of their local communities.

Both halls continue to meet local needs and diversify their activities. Footfall has increased and Shenley succeeded in exceeding the income target for 2012/13. Phoenix Hall is situated in one of the most deprived areas in the country and has different challenges.

The Annual Phoenix Fun Day on 8 June was attended by over 100 people and feedback was extremely positive.

Bournville Architects have undertaken a property condition survey for each of our halls and developed an Asset Management Plan for us. We are currently awaiting an independent report to consider activities at each hall. The feedback will be incorporated into our new Community Development and Resident Involvement Strategy.

To invest in our people

Corporate Services

Develop a new Corporate Health and Safety Policy. Completed.

Human Resources

Develop a series of action points that arise from our first ever staff survey.

Action plan has been prepared and a lot of work has been completed in accordance with the plan. There are some issues to be resolved and these will be completed in due course. We also plan to undertake another staff survey in 2015.

Auto-enrolment to pension scheme (from April 2013). Preparations are underway with progress reports presented through FAGP committee. Confirmation now received that auto-enrolment will begin for BVT in January 2014.

Reduce sickness absence - through individual case management assessments from 2012.

Individual cases have been managed through medical reports and specialists. Where possible long term sickness absence has not been prolonged and decisions on employment have been made quickly on medical evidence and consultation with the staff member concerned.

There have also been a number of changes made to the sickness absence policy now called the Well-being and Absence policy. The aim of the changes is to encourage staff to take responsibility for their own health and well-being. The policy focuses more on the Simply Health Scheme to encourage staff to utilise the facilities so that they can make a speedy recovery and reducing the length of time that they are off work e.g. counselling service, employee help line, other treatments such as physiotherapy etc. The policy also now allows the Trust to review a case and dismiss during a period

25

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Bournville Village Trust Business Plan 2014 - 2018

of absence before the employee’s sick pay comes to end.

The impact of these changes will be monitored periodically.

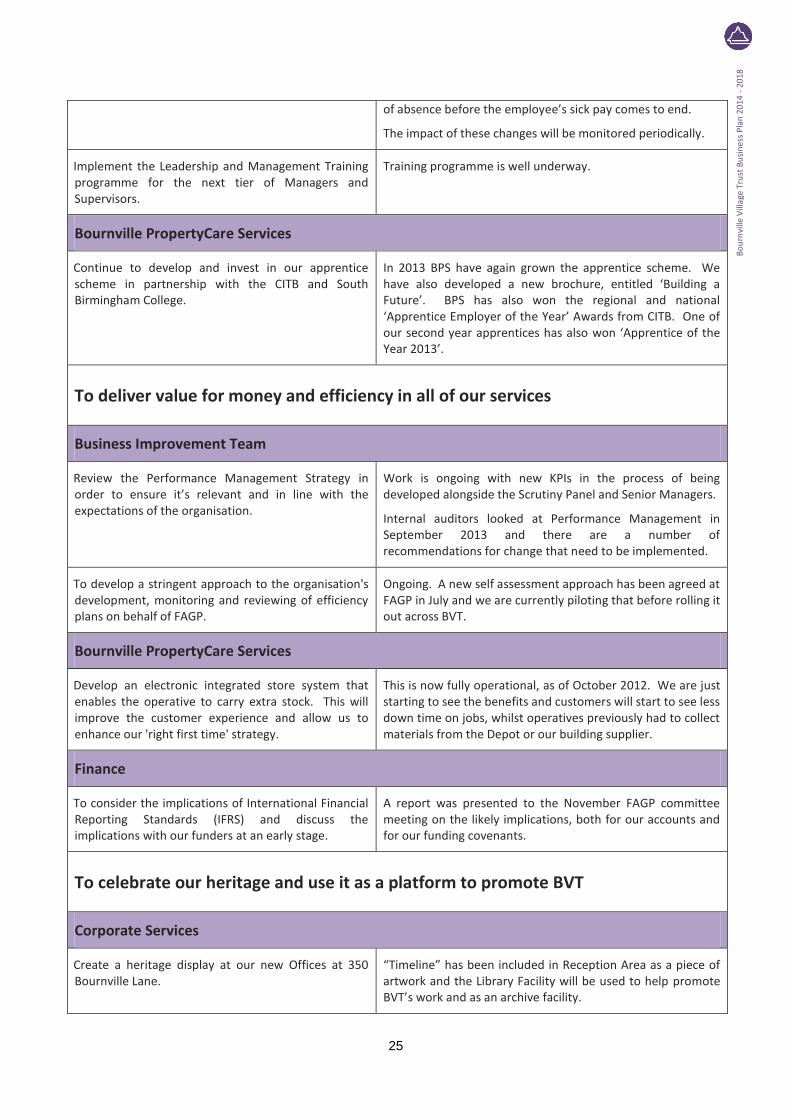

Implement the Leadership and Management Training programme for the next tier of Managers and Supervisors.

Training programme is well underway.

Bournville PropertyCare Services

Continue to develop and invest in our apprentice scheme in partnership with the CITB and South Birmingham College.

In 2013 BPS have again grown the apprentice scheme. We have also developed a new brochure, entitled ‘Building a Future’. BPS has also won the regional and national ‘Apprentice Employer of the Year’ Awards from CITB. One of our second year apprentices has also won ‘Apprentice of the Year 2013’.

To deliver value for money and efficiency in all of our services

Business Improvement Team

Review the Performance Management Strategy in order to ensure it’s relevant and in line with the expectations of the organisation.

Work is ongoing with new KPIs in the process of being developed alongside the Scrutiny Panel and Senior Managers.

Internal auditors looked at Performance Management in September 2013 and there are a number of recommendations for change that need to be implemented.

To develop a stringent approach to the organisation's development, monitoring and reviewing of efficiency plans on behalf of FAGP.

Ongoing. A new self assessment approach has been agreed at FAGP in July and we are currently piloting that before rolling it out across BVT.

Bournville PropertyCare Services

Develop an electronic integrated store system that enables the operative to carry extra stock. This will improve the customer experience and allow us to enhance our 'right first time' strategy.

This is now fully operational, as of October 2012. We are just starting to see the benefits and customers will start to see less down time on jobs, whilst operatives previously had to collect materials from the Depot or our building supplier.

Finance

To consider the implications of International Financial Reporting Standards (IFRS) and discuss the implications with our funders at an early stage.

A report was presented to the November FAGP committee meeting on the likely implications, both for our accounts and for our funding covenants.

To celebrate our heritage and use it as a platform to promote BVT

Corporate Services

Create a heritage display at our new Offices at 350 Bournville Lane.

“Timeline” has been included in Reception Area as a piece of artwork and the Library Facility will be used to help promote BVT’s work and as an archive facility.

26

Appendix B How It All Fits Together

1

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Appendix C Financial Forecasts

Introduction

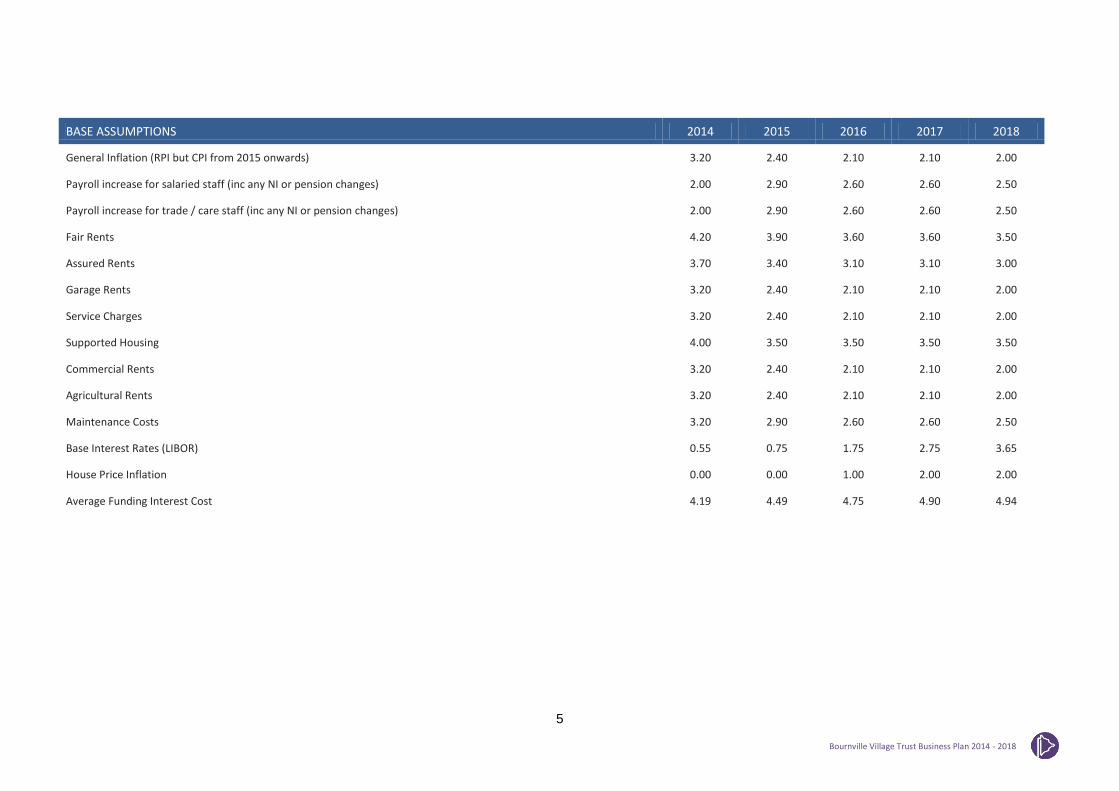

This appendix to the Business Plan shows the latest financial forecasts based upon the 2014

budget, the current development programme and the assumptions set out on page 5 of this

appendix.

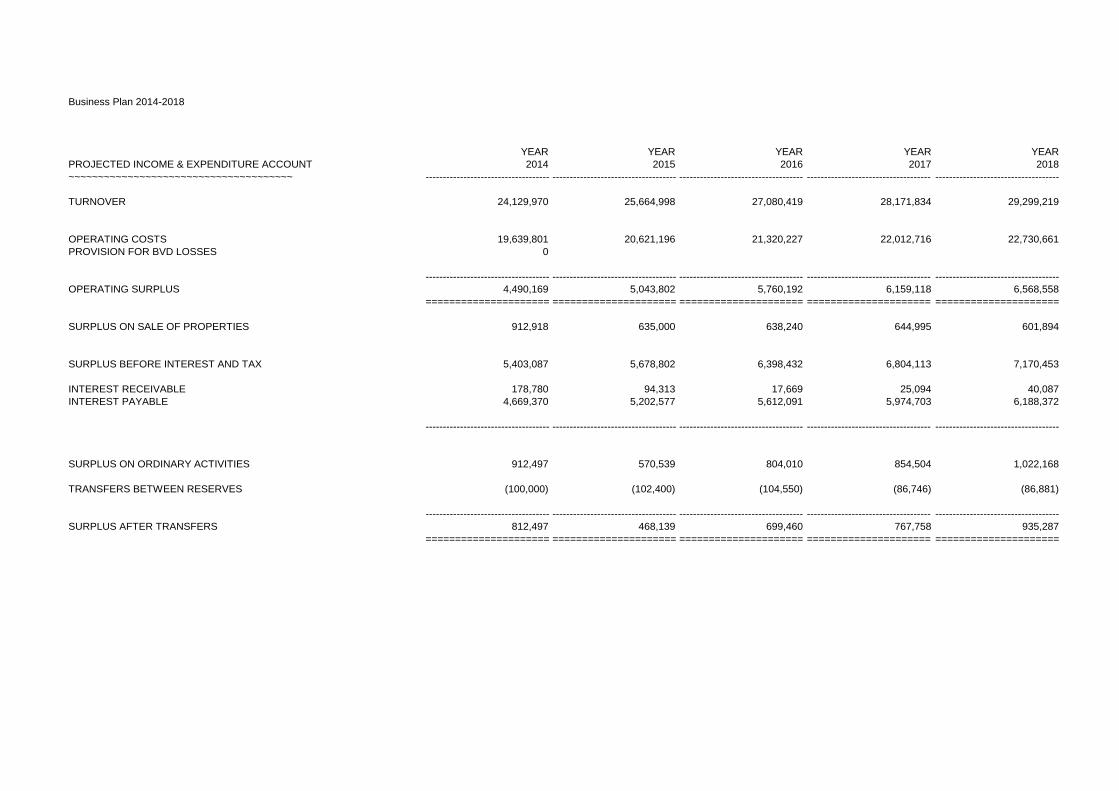

Summary

The forecasts on pages 6-8 of this appendix show a reasonable surplus is projected for each

year of the plan. The highest surplus is projected for 2014, when we are planning to sell off

our former head office, as well as a couple of properties on our agricultural estates which

Trustees no longer require. The surplus on these sales helps to boost the anticipated

surplus in 2014 by around £300,000. From 2015 onwards, surpluses are projected to grow,

despite interest rates increasing and despite allowances made for the impact of welfare

benefit reform. At this stage, it’s difficult to know what impact the various changes to welfare

benefits will have on our business, but I have factored in a 10% year on year increase in

arrears within these forecasts, in addition to a 50% increase in allowance for bad debts as

well as additional staffing costs.

BVT has a number of development aspirations during this business plan period. By 2015,

we hope to complete the development of our College Green Care Village, albeit some

elements of this will be delivered by other organisations. We shall also be pressing ahead

with our Lightmoor and Lawley development projects in Telford. In fact, over the 5 years of

the business plan period, we aim to acquire 270 new units of accommodation.

We also ensure that we continue to look after our current property portfolio. Indeed, we shall

be spending over £3m each year to ensure our properties continue to meet the Decent

Homes Standard as well as investing in our non-housing portfolio.

To help fund this development and investment programme, we aim to utilise the most cost

effective finance that we can. We have already registered our interest in taking funding from

Affordable Housing Finance, the company set up to administer the government’s loan

guarantee scheme. We shall always ensure that, as far as reasonably possible, we will work

within the funding covenants agreed with each of our funders. These forecasts indicate a

fairly healthy level of headroom on our covenants and Trustees will seek to ensure that this

level of headroom is maintained in the longer-term.

Sensitivity Analysis

Let’s have a look at the key risks BVT faces over the business plan period and what impact

these could have on these financial forecasts.

i) Breach of Loan Covenants

Whilst the latest projections indicate a reasonable amount of headroom over all of

our funding covenants, the prospect of a “technical” breach can never be truly

discounted. The real concern is that a breach of any loan covenant would result in all

our principal funders (except THFC) being able to re-price their loans. This would be

a matter for negotiation with each funder, but it could result in a significant increase in

our interest costs of around £1.9m a year. Clearly, that is not something we can

allow to happen, which is why Trustees pay very close attention to our covenant

compliance projections and would take remedial action before the level of headroom

became too small.

This is also why we are closely monitoring the introduction of International Financial

Reporting Standards in 2015. Some of the accounting changes currently being

proposed could have a real impact on our ability to meet our loan covenants. Our

funders really should allow us to eliminate the impact of any accounting changes

when calculating compliance with funding covenants. We will therefore be

discussing this with our funders over the coming weeks and months to ensure that

these accounting changes do not adversely impact on our ability to meet our

covenants.

ii) Welfare Benefit Reforms and Government Spending

We all know that the government has got to reduce the level of public expenditure to

bring our nation’s finances into better order. We know about some changes to

welfare benefits over the next few years, which will ultimately lead to Universal Credit

replacing a number of current benefits. The process is expected to lead to a

reduction in benefits and we have begun to implement our Anti-Poverty Strategy to

educate and assist our customers as much as we can. The issue is compounded by

the fact that, apart from vulnerable customers, benefits are going to be paid to the

customers, rather than to the landlord as is generally the case at present (at least as

far as housing benefit is concerned).

At this stage, no-one can be certain of the impact of these changes on housing

association finances. These financial projections allow for an annual increase in rent

arrears of around 10% year on year. It would require an annual increase in arrears in

excess of 80% to give us real cause for concern in terms of our finances. At this

stage, this seems to be extremely unlikely, but this is again something that Trustees

will be monitoring closely in the years ahead.

iii) Pensions

The financial forecasts currently allow for the potential impact of auto-enrolment in

2014. Auto-enrolment will require BVT to put all 170 staff not currently in a pension

scheme, into such a scheme. If these 170 staff are put into our BVT Pensionsaver

scheme, with BVT contributing 1% for each member of staff, this adds around

£36,000 to our annual pension costs. Staff may choose to increase their

contributions which would result in a further increase in employer contributions.

Whilst this has a detrimental impact on our future finances, as a responsible

employer, we welcome auto-enrolment as a means of encouraging people to think

about their pension needs.

3

Bo

urn

ville

Vill

age

Tru

st B

usi

nes

s P

lan

20

14

- 2

01

8

Bournville Village Trust Business Plan 2014 - 2018

More of an issue for us is meeting our share of the liabilities to the Cadbury Pension

Fund (CPF). BVT has just over 140 staff within the CPF. The financial forecasts

currently allow for a capital injection of £300,000 per year into the fund as well as the

ongoing employer contributions which range from 13.2% to 28.1% depending upon

which section of the CPF each employee is in. All of this has been in place since the

2010 actuarial valuation of the CPF was undertaken and which calculated a deficit of

£326m. Hopefully, at these contribution levels, the deficit will reduce, but with people

living longer and uncertainty about future investment returns, this is not guaranteed.

So, the 2013 actuarial valuation will be crucial in identifying whether we are on the

right track to eliminate the deficit in the medium term or whether contributions have to

be increased still further. We will know the outcome of the 2013 valuation early in

2014. If we assume no change in the rate of ongoing employer contributions, but

that our annual capital injections have to increase, when does this become a real

concern for us? The answer is that even if the level of capital injection trebled to

£900,000, we would still be able to meet all of our loan covenants.

v) Increase in Future Funding

Borrowing from banks has not only become more expensive in recent times, but no

bank these days is prepared to lend for longer than 10 years. BVT Trustees have

always preferred long-term funding, which is why we have recently drawn £20m from

bonds issued by THFC. Indeed more and more housing associations are looking for

funding from the bond markets. I don’t see this trend changing in the near future.

In recent months, a number of housing associations have launched bonds and have

been able to secure funds usually at a rate of between 4.5% and 5%. The current

business plan assumes all future funding will be secured at 5%. It could be argued

that this is pessimistic on the basis that as more housing associations come to the

bond market for funding, investors become more familiar with the sector and begin to

reduce their expectations, thus reducing funding rates. Equally, it could be argued

that as the Bank of England’s programme of quantitative easing (QE) is gradually

unwound, then bond pricing will start to increase – the argument being that QE has

had an artificial impact on keeping down the price of bond funding in recent years.

Time will tell which of these arguments will prevail, but at what level does future

funding become unviable for BVT? If funding rates increase beyond 8.5% in the

longer-term, then, without some other beneficial change, BVT would struggle to meet

its loan covenants towards the very end of the business plan period.

In reality, I think it’s most unlikely that rates would increase beyond 8.5% unless

there was a marked increase in inflation. If that were the case, then the rent formula

(which is linked to inflation), would offset at least some of the impact of the increase

in funding costs.

Mitigation Strategies

Whilst the sensitivity analysis above would appear to give a fair degree of reassurance about

BVT’s financial position, the real concern could be that two or more of these scenarios come

together to knock us off-course. So, what can be done if such an eventuality materialises?

i) Reduce Expenditure

Trustees would no doubt look at what options they have for reducing expenditure.

There is already a requirement on officers to deliver greater value for money, but if

further measures were necessary then Trustees would have to consider contracting

out services if they could be done more cost effectively by a third party. They could

also look to reduce pay increases for staff. They may even have to consider closing

down some functions / facilities that cost money to run, even though these may be an

important part of BVT’s commitment to the success of the communities we serve,

things that distinguish BVT from most other housing associations.

ii) Asset Management

Trustees may well look again at the Asset Management Strategy as a way of selling

off some assets, in order to generate additional financial capacity. This could be just

the selective sale of void properties or could mean that a block of assets are

identified for sale to another suitable organisation.

iii) Income Generation

To some degree, BVT already sells its services to third parties. This could be done

on a larger scale to generate additional income, although inevitably it would mean an

increase in expenditure too. The best example of this would be selling our

stewardship service to other organisations who are developing new communities

elsewhere or possibly selling our repairs service to customers who own their own

homes but are looking for a trustworthy, reliable contractor to undertake maintenance

on those homes. We may even be able to make more of our charitable status to

seek donations / grants from third parties to help us through more difficult times.

Indeed a combination of all three may be required if the going gets really tough.

Conclusion

These financial forecasts indicate that BVT is in good financial health and is likely to be able

to cope even if some key risks materialise over the business plan period.

Paul Haywood

Director of Financial Services

5

Bournville Village Trust Business Plan 2014 - 2018

BASE ASSUMPTIONS 2014 2015 2016 2017 2018

General Inflation (RPI but CPI from 2015 onwards) 3.20 2.40 2.10 2.10 2.00

Payroll increase for salaried staff (inc any NI or pension changes) 2.00 2.90 2.60 2.60 2.50

Payroll increase for trade / care staff (inc any NI or pension changes) 2.00 2.90 2.60 2.60 2.50

Fair Rents 4.20 3.90 3.60 3.60 3.50

Assured Rents 3.70 3.40 3.10 3.10 3.00

Garage Rents 3.20 2.40 2.10 2.10 2.00

Service Charges 3.20 2.40 2.10 2.10 2.00

Supported Housing 4.00 3.50 3.50 3.50 3.50

Commercial Rents 3.20 2.40 2.10 2.10 2.00

Agricultural Rents 3.20 2.40 2.10 2.10 2.00

Maintenance Costs 3.20 2.90 2.60 2.60 2.50

Base Interest Rates (LIBOR) 0.55 0.75 1.75 2.75 3.65

House Price Inflation 0.00 0.00 1.00 2.00 2.00

Average Funding Interest Cost 4.19 4.49 4.75 4.90 4.94

Business Plan 2014-2018

YEAR YEAR YEAR YEAR YEAR

PROJECTED INCOME & EXPENDITURE ACCOUNT 2014 2015 2016 2017 2018

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

TURNOVER 24,129,970 25,664,998 27,080,419 28,171,834 29,299,219

OPERATING COSTS 19,639,801 20,621,196 21,320,227 22,012,716 22,730,661

PROVISION FOR BVD LOSSES 0

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

OPERATING SURPLUS 4,490,169 5,043,802 5,760,192 6,159,118 6,568,558

===================== ===================== ===================== ===================== =====================

SURPLUS ON SALE OF PROPERTIES 912,918 635,000 638,240 644,995 601,894

SURPLUS BEFORE INTEREST AND TAX 5,403,087 5,678,802 6,398,432 6,804,113 7,170,453

INTEREST RECEIVABLE 178,780 94,313 17,669 25,094 40,087

INTEREST PAYABLE 4,669,370 5,202,577 5,612,091 5,974,703 6,188,372

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

SURPLUS ON ORDINARY ACTIVITIES 912,497 570,539 804,010 854,504 1,022,168

TRANSFERS BETWEEN RESERVES (100,000) (102,400) (104,550) (86,746) (86,881)

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

SURPLUS AFTER TRANSFERS 812,497 468,139 699,460 767,758 935,287

===================== ===================== ===================== ===================== =====================

7

Bournville Village Trust Business Plan 2014 - 2018

Business Plan 2014-2018

YEAR YEAR YEAR YEAR YEAR

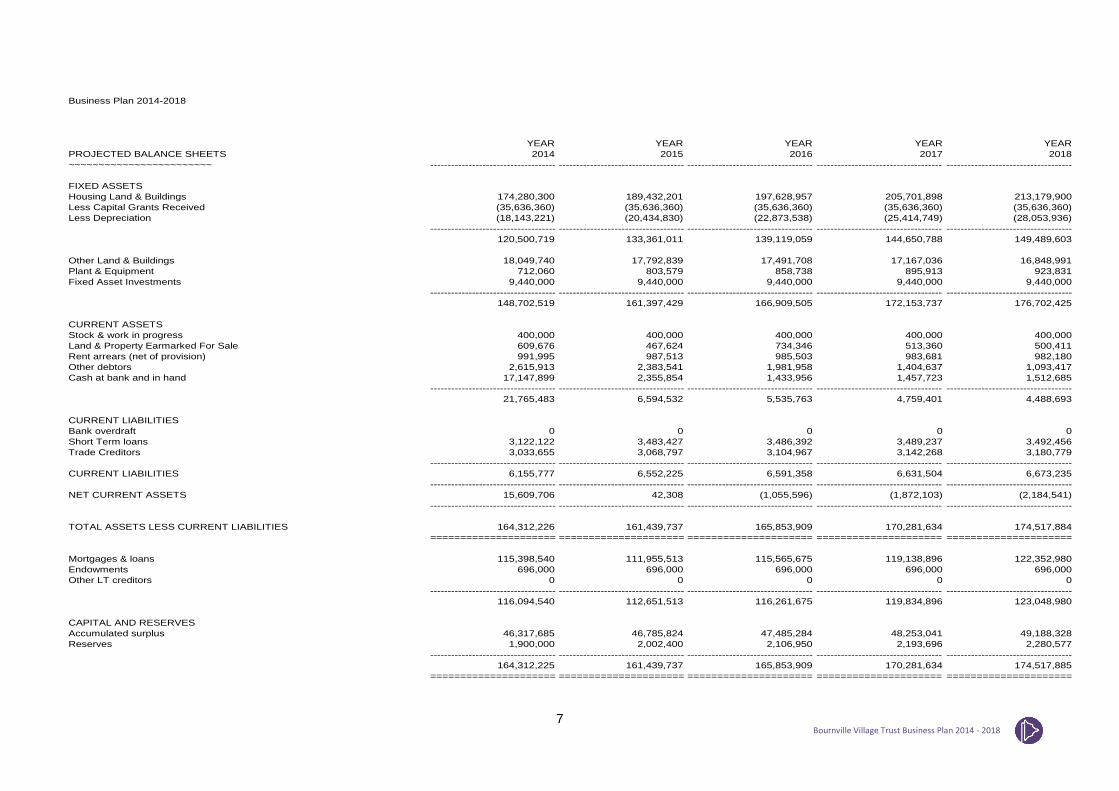

PROJECTED BALANCE SHEETS 2014 2015 2016 2017 2018

~~~~~~~~~~~~~~~~~~~~~~~~ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

FIXED ASSETS

Housing Land & Buildings 174,280,300 189,432,201 197,628,957 205,701,898 213,179,900

Less Capital Grants Received (35,636,360) (35,636,360) (35,636,360) (35,636,360) (35,636,360)

Less Depreciation (18,143,221) (20,434,830) (22,873,538) (25,414,749) (28,053,936)

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

120,500,719 133,361,011 139,119,059 144,650,788 149,489,603

Other Land & Buildings 18,049,740 17,792,839 17,491,708 17,167,036 16,848,991

Plant & Equipment 712,060 803,579 858,738 895,913 923,831

Fixed Asset Investments 9,440,000 9,440,000 9,440,000 9,440,000 9,440,000

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

148,702,519 161,397,429 166,909,505 172,153,737 176,702,425

CURRENT ASSETS

Stock & work in progress 400,000 400,000 400,000 400,000 400,000

Land & Property Earmarked For Sale 609,676 467,624 734,346 513,360 500,411

Rent arrears (net of provision) 991,995 987,513 985,503 983,681 982,180

Other debtors 2,615,913 2,383,541 1,981,958 1,404,637 1,093,417

Cash at bank and in hand 17,147,899 2,355,854 1,433,956 1,457,723 1,512,685

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

21,765,483 6,594,532 5,535,763 4,759,401 4,488,693

CURRENT LIABILITIES

Bank overdraft 0 0 0 0 0

Short Term loans 3,122,122 3,483,427 3,486,392 3,489,237 3,492,456

Trade Creditors 3,033,655 3,068,797 3,104,967 3,142,268 3,180,779

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

CURRENT LIABILITIES 6,155,777 6,552,225 6,591,358 6,631,504 6,673,235

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

NET CURRENT ASSETS 15,609,706 42,308 (1,055,596) (1,872,103) (2,184,541)

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

TOTAL ASSETS LESS CURRENT LIABILITIES 164,312,226 161,439,737 165,853,909 170,281,634 174,517,884

===================== ===================== ===================== ===================== =====================

Mortgages & loans 115,398,540 111,955,513 115,565,675 119,138,896 122,352,980

Endowments 696,000 696,000 696,000 696,000 696,000

Other LT creditors 0 0 0 0 0

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

116,094,540 112,651,513 116,261,675 119,834,896 123,048,980

CAPITAL AND RESERVES

Accumulated surplus 46,317,685 46,785,824 47,485,284 48,253,041 49,188,328

Reserves 1,900,000 2,002,400 2,106,950 2,193,696 2,280,577

------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------ ------------------------------------

164,312,225 161,439,737 165,853,909 170,281,634 174,517,885

===================== ===================== ===================== ===================== =====================

Business Plan 2014-2018

Base Model

Year 2014 2015 2016 2017 2018

Global Assumptions

Inflation 3.20% 2.40% 2.10% 2.10% 2.00%

Average Interest Rate 0.55% 0.75% 1.75% 2.75% 3.65%

Net Development Costs (£'000s) 4,537 11,279 4,155 3,764 3,304

Key Financial Data

Total Income (£'000s) 24,130 25,665 27,080 28,172 29,299

Interest Cost (£'000s) 4,669 5,203 5,612 5,975 6,188

Cash in hand (£'000s) 17,148 2,356 1,434 1,458 1,513

Total Debt (£'000s) 118,521 115,439 119,052 122,628 125,845

Total Net Worth At Historic Cost(£'000s) 199,949 197,076 201,490 205,918 210,154

Total Net Worth At Existing Use Value (£'000s) 200,421 202,628 218,584 232,570 246,689

Total Net Worth At Open Makret Value (£'000s) 527,255 533,062 575,037 611,833 648,974

Total Number of Rented Homes at Year End 3,541 3,580 3,678 3,727 3,765

Key Performance Indicators

Interest Cover 1.53 1.60 1.57 1.64 1.63

Gearing ratio based on historic cost 59.28% 58.58% 59.09% 59.55% 59.88%

EBITDA 98.54% 100.87% 106.95% 108.09% 111.76%

Gearing Based on Historic Cost

55%

57%

59%

61%

63%

65%

2014 2015 2016 2017 2018

Interest Cover

1.30

1.40

1.50

1.60

1.70

2014 2015 2016 2017 2018

Cash Balance

0

2,000

4,000

6,000

8,000

10,000

2014 2015 2016 2017 2018

9

Bournville Village Trust Business Plan 2014 - 2018

10

Bournville Village Trust Business Plan 2014 - 2018