Embed Size (px)

Citation preview

• TIME TO ACT - GOVERNMENT ON THE MOVE

• SELL THE INTANGIBLE - MARKETING• 2018 SURVEY – BIGGEST BOOKKEEPER CHALLENGE

….and much more!

2018EDITION 1

Bookies BULLETIN

2 | Australian Bookkeepers Network | BOOKIES BULLETIN

contents02 DIRECTOR'S CORNER

03 WHAT HAVE YOU DONE FOR ME LATELY?

05 SELL THE INTANGIBLE

06 TIME TO ACT - GOVERNMENT ON THE MOVE

08 NUTS AND BOLTS

12 FIVE MINUTES WITH

Edition 1 2018Bookies Bulletin produced bi-monthly by the Australian Bookkeepers Network3rd Floor—Plaza Chambers, 15 Dennis RoadSpringwood QLD 4127E-mail: [email protected] Address: PO Box 1140, Springwood QLD 4127Telephone: (07) 3290 4914

Company Information:Legal Title: Australian Bookkeepers Network Pty. Ltd.Australian Company Number: 096 035 648Australian Business Number: 49 096 035 648

Disclaimer: The information contained in this edition is current as at time of writing (March 2018). Information contained herein is general in nature and is intended to provide guidance to bookkeepers in providing bookkeeping services for their clients. It is not intended to be taken as a substitute for you or your clients seeking professional advice in relation to their own specific circumstances.

Copyright: Except for use with other staff members or contractors of your bookkeeping firm, no part of this publication may be reproduced.

Director's CORNER

In a recent Bookkeeper Radio interview, I was asked what my thoughts were on what makes a great conference? Great question and one that gets you pondering. My answer was something like the following.

Content is king!!! For me if I am going to make an investment in a conference I want to make sure that I have something tangible I can take away and implement in my business immediately. I use the word investment because it is. There is the cost to attend, travel, accommodation, time away from your clients and your business – all of those things can add up. I want a return on my investment, so content is important to me but that is not the only thing.

Next comes speakers. I don’t want to hear chest beating, sales flogs or fluff! I want to hear from speakers that are experts in their field and that can share something new that I have not heard before. Importantly part of their role is to inspire and motivate me and to help me embrace change .

Last but no means least is what I call “time for sharing”. Some may call it networking but for me, whether you are meeting new connections, or catching up with old friends, the time to share and chat about your business, systems, software, clients, current problem or current success is paramount. We are lucky enough to be part of a great community that loves to share, so time dedicated to that is vital.

Of course there is a lot more I can add like awesome exhibitors, lots of fun times, amazing locations and lasting memories …. however, the editor tells me I only have so much room on this page!

The Bookkeeper Event is ABN’s very own Bi-annual conference. Why every 2 years – because it is big and it is special! Our ABN mantra when putting together The Bookkeeper Event is to deliver BIG on my traits of a great conference! The conference is being held on 12th and 13th of October on the glorious Gold Coast at Seaworld Conference Centre. You can get lots of details by checking out the website here www.bkevent.com.au.

I would love to see you there!

Kellie Powell ABN Director

BOOKIES BULLETIN | Australian Bookkeepers Network | 3

WHAT HAVE YOU DONE

FOR ME lately?

ABN has been working away for members on a number of fronts of late.

Industry Insight and Business ToolsIn early January, we released our Bookkeeping Benchmark Report 2017

The report continues to set the standard for any bookkeeper wanting to know and understand some of the key drivers of the bookkeeping industry.

This industry-leading report, surveys and collects core data, both operational and financial, from bookkeeping businesses operating in Australia and then studies and analyses that data to identify operational and financial performance trends for the bookkeeping community and stakeholders. It then assists bookkeepers to understand and use this information in order to build a successful bookkeeping business. Australian Bookkeepers Network (ABN) is committed to the continual improvement and profitability of business owners in the bookkeeping industry and this report makes a contribution to that process.

The report is available for purchase in the ABN Shop.

Industry News and Views - Bookkeeper Radio Bookkeeper Radio is back for on air for 2018!

In one of this year’s first episodes, we provided an overview of the current state of the bookkeeping industry by revealing some of the key findings from our Bookkeeping Benchmark Report. If you missed this or previous episodes, you can download them for free from our website.

Hosted on the 1st and 3rd Wednesdays of every month by our very own DJs, Peter Thorp and Kelvin Deer! ABN’s Bookkeeper Radio offers a unique and insightful look at your industry. For each broadcast, see and hear your hosts interview a prominent industry figure and then give you the opportunity to ask your own questions. It's a fun, free and interactive way to keep up with industry news and views.

4 | Australian Bookkeepers Network | BOOKIES BULLETIN

Industry EventsIn February we proudly launched another new product for bookkeepers – our Bookkeeper Events Calendar!

The all-in-one event calendar that allows you to view upcoming:

• Webinars

• Conferences

• Industry events

• Coffee Clubs

What’s even better is you can now register for each event directly from the calendar! You’ll never have to worry about scrolling through every webpage to book your events again. Keep an eye on the calendar as we continue to update it with upcoming events.

You can now view and access this great tool through the ABN Website.

Technical KnowledgeGetting Technical

In January and February, we sent you the latest editions of our monthly publication Getting Technical. Although ABN already provides a wealth of in-depth technical material for members, we appreciate that from time to time very specific technical issues arise that you may need guidance on. Getting Technical fills that space. These latest editions dealt with various bookkeeping issues around capital expenditure, and also the business versus hobby distinction.

Delivering you the best technical resources, that’s your ABN.

NetworkingOur Coffee Clubs are back for 2018. Our wonderful Network Leaders have been out in their local area hosting Coffee Clubs throughout January and February.

Coffee Clubs are a community where bookkeepers can connect in what can be an otherwise isolating industry. Meet other like-minded people, share your knowledge, learn from others, and keep up to date with industry developments. You are only a Coffee Club meeting away from building your own professional network of friends and creating long-lasting relationships with your industry peers. To find out when the next Coffee Club is being held near you, subscribe to our Notification List.

Bookkeepers Knowledge BaseWe’re happy to report that our entire library of BKBs is now fully up-to-date! The ABN Team has combed through every page of the 87 BKBs and made edits where necessary to ensure that the publications are current as at January 2018. This mammoth task was completed with the expert assistance of ABN member Vija Platacis who we thank very much.

Our Bookkeepers Knowledge Base library represents an unmatched technical resource for our members – providing in-depth accounting, tax, BAS and ethical guidance on the topics that matter most to bookkeepers.

12-13 OCTOBER SEA WORLD CONFERENCE CENTRE, GOLD COASTwww.bkevent.com.au

BOOKNOW!

WHAT HAVE YOU DONE FOR ME lately cont...

In Edition 5 of this publication last year, Martin Grunstein (a previous ABN Conference Keynote Speaker) gave us a wonderful article about a trend that is increasingly obvious to many of us. Margins for many of the goods and services we buy are being eroded; caused by the commoditisation of those selling them. You can buy a computer, a car or a holiday on-line and, with suppliers voluntarily commoditising their offerings, all that is left to differentiate the offerings is price. The outcome? - Margin erosion.

Martin looked at what retailers and suppliers could do in this environment; citing a number of examples such as Crimsafe where the supplier changed the focus of the sales proposition from a commodity to an intangible. With a sales line that went something like …“imagine what it would be like if someone broke into your house and hurt the people you love the most”……….. “Crimsafe makers of the best security doors in Australia”. His point being that Crimsafe had moved the focus of the sale equation from selling security doors to fear. All of a sudden saving a few dollars on a security door became a secondary issue. He cited some other wonderful examples of how other suppliers had made an intangible (an emotion) the primary sale driver and not price.

Perhaps there is something bookkeepers could take from this when marketing or promoting their services. Selling “bookkeeping” for $x per hour frames the sales argument around price. Firstly, it commoditises the service of “bookkeeping” by allocating a generic term. In doing so, it puts the vendor in the same market as everyone else selling “bookkeeping” which allows the potential customer to presume that the commodity is homogeneous. The only differentiator then is price, which is readily comparable. It might be that your “bookkeeping” is of superior quality with less hours charged or with superior results delivered but that does not come through when you frame the argument around a generic term and a price for one hour of it.

The truth is there is so much that differentiates your service from others and delivers value to your client and that is what

needs to come through in your promotion; not the cost of one

hour’s bookkeeping. Remember you are not selling a Big Mac

hamburger or a brand X computer, rather you are selling a service

so you get to tell your customer what YOUR service is all about.

More often than not the impetus to buy is an emotional one, so

consider the range of intangibles and emotions at play for your

potential clients:

• Fear: I can keep you out of the poo with the authorities

• Greed: I can produce timely and quality reports that will let

you see how your business is going so you can make better

decisions and be more profitable

• Peace of mind: You can rest easy because I have got your

back; your taxes are squared away, so the ATO are happy.

OR Your employees are paid properly so there is nothing to

worry about from Fair Work or other payroll regulators

• The gift of time: I can take tasks off you that give you back

the most precious commodity of all – time. With time you can

do great things in your business and personal life

• Fear of Missing Out (FOMO): The rest of the business

world is adopting new and better technology; let me show

you how.

Think about the intangibles you deliver your clients and make sure

they come through loud and clear in all your promotional material

including website, brochure-ware, business cards, emails and

even the way you describe your business when networking.

SELL THE Intangible

BOOKIES BULLETIN | Australian Bookkeepers Network | 5

By Peter ThorpABN Director

BOOKIES BULLETIN | Australian Bookkeepers Network | 6

This article examines a number of recent key developments that may impact you and your clients.

Superannuation CrackdownThe Government’s flagged Superannuation Guarantee (SG) “crackdown” is now here. In January, the Government released for public consultation, exposure draft legislation in the form of the Superannuation Guarantee Integrity Measures Bill (2018). The consultation period has now closed. The draft Bill when passed will:

1. Allow the ATO to issue directions to pay unpaid SG and undertake SG education courses in cases where employers fail to comply with their SG obligations

2. Introduce criminal penalties for failure to comply with a direction to pay SG (including prison terms of up to 12 months)

3. Allow the ATO to disclose more information about SG non-compliance to affected employees

4. Facilitate more regular reporting to the ATO by superannuation funds (at least once per month).

Employers should particularly take note of the third item. Under the proposed legislation, if an employee made a complaint to the ATO about their employer failing to make the required superannuation contributions, the ATO could under the new law communicate its concerns to other employees who might be similarly affected. The Bill also makes clear that employers will not be required to report actual superannuation contributions through Single Touch Payroll – this obligation will fall on the receiving superannuation fund.

The new Bill is a compelling reason for clients to thoroughly review their SG processes and practices with a view towards ensuring compliance.

Data Breach LawsThe new national data breach notification laws are now in operation!

From 22 February, businesses are required to notify affected individuals (e.g. clients, employees etc.) and also the Office of the Australian Information Commissioner of a data breach. Failure to do so can result in fines of up to $1.8 million. As TFN recipients, bookkeepers are caught by this new regime to the extent that TFN information is involved in a breach (“TFN information” is information that connects a TFN with the identity of a particular individual). For more details on this regime, see our various articles in this publication last year. See also our Bookkeeper Radio session of 7 March 2018.

Although the Tax Practitioners Board does not administer this new regime, on 14 February the Board said in a statement that “if tax practitioners fail to comply with the new scheme there may be implications in relation to the Tax Agent Services Act 2009 (TASA). Such a failure may be considered by the TPB in determining whether you have breached the TASA, including the Code of Professional Conduct (Code)”. This recently-issued Board statement contains a range of useful information on the new regime including how to comply, support available in the event of a breach, and links to some practical tips on bolstering your own cyber security.

Separate to this new regime, bookkeepers should check their PI insurance to ensure they are covered in the event of a cyber breach. Bookkeeping firms, because of the nature of the information they hold, are particularly attractive targets for hackers. To this end, both of ABN’s PI insurance providers offer cyber security coverage.

TIME TO ACT -

GOVERNMENT

ON THE

MOVE

7 | Australian Bookkeepers Network | BOOKIES BULLETIN

Black EconomyTax practitioners are very likely to face increased scrutiny in relation to client cash transactions in the coming year.

By way of background, the Black Economy Taskforce was formed in late 2016 to develop a holistic approach to combat the black economy (also known as the cash or hidden economy) which is worth an estimated $30 billion in lost revenue. While its final report is not due until early 2018, it’s clear that tax practitioners will face increased scrutiny in respect of clients who operate partially or substantially in the black economy, especially in light of a paper released by the taskforce late last year titled Additional Policy Ideas where the following recommendation was made:

Greater attention needs to be paid to sanctioning unethical agents and the role that the Tax Practitioners Board should be playing with this. The message to the professional bodies is that it is no longer acceptable for agents to cast a blind eye on their client’s tax affairs and help them break the law.

These were followed up by equally strong comments in the Financial Review later in the year by the head of the taskforce who was quoted as saying: “we need to get a lot tougher (as) agents are either assisting their clients to make fraudulent claims, or are blind to techniques and systems used in the black economy”.

For their part, the ATO has published what it considers ‘best practice examples' (see page 14 and 15) for practitioner conduct for clients who have cash transactions (this document is an interesting read).

Irrespective of the taskforce’s final recommendations or what the ATO considers ‘best practice’, the Tax Practitioners Board do not require you to audit a client’s affairs or report non-complying clients to the ATO. Rather you are only required to:

• Take reasonable steps to ascertain a client’s state of affairs, but only as far as it concerns work you are undertaking

• Take reasonable care to ensure that the taxation laws are applied correctly when advising a client or undertaking work for them

• Advise clients of their rights and obligations under the law in respect of the services you provide to them

• Not knowingly obstruct the proper administration of the law.

By way of example, if you are completing a BAS on the basis of an accounting file provided to you by a client, while there is no requirement to sight all client tax invoices, if you were to come across transactions that you had concerns about you would be expected to sight source documents in relation to those transactions before proceeding in respect of those transactions.

With an increased focus coming onto agents, to evidence that you have covered off on these Board requirements, it’s recommended that you document any actions you take to that end. Returning to the above example, you may wish to email the client (thus documenting your actions) that you will need to check the tax invoice in relation to this particular transaction.

Tax Debt AlertIn the previous edition of this publication (page 7) we previewed a new measure that will allow the ATO to report certain overdue, undisputed tax debts of $10 000 (not covered by a formal arrangement) to Credit Reporting Bureaus (CRBs). As we noted, the effect of this on a business could be quite devastating as CRBs may include the tax debt information in their credit reports which are available for purchase by parties who wish to use this information to make an informed decision on the credit worthiness of a business. This could have profound effects on the reported business such as support from financiers being withdrawn, and supplier credit stopped.

The Government has since released Exposure Draft legislation for publication consultation (the consultation period closed on 9 February). In that Exposure Draft legistlation, an extra condtion has been added before the ATO is able to report the debt. Namely, the debt must be overdue by 90 days or more. With public consultation now concluded, legislation will in the coming weeks or months be introduced into Parliament. The new law commences immediately when passed by Parliament. Therefore, as a matter of some urgency businesses with debts that meet the above conditions need to take corrective action such as by:

• Paying the ATO the debt in full

• Entering into a payment arrangement with the ATO

• Abiding by the terms of any existing repayment arrangement with the ATO

• Formally disputing that there is actually a debt owed.

TIME TO ACT - GOVERNMENT ON THE MOVE cont...

21 MarchFebruary monthly Activity Statements - due for lodgement and payment

31 MarchEnd of 2017/2018 FBT year

1 AprilSingle Touch Payroll: employee headcount (see page 10)

21 AprilMarch monthly Activity Statements - due for lodgement and payment

28 April Superannuation Guarantee contributions (Jan-March) due for payment

30 AprilTFN Report (Oct-Dec) for closely held trusts for TFNs quoted to a trustee by beneficiaries - due for lodgement

NUTS & bolts

key DATES

FBT Time!With the end of the 2017/2018 FBT year looming, as a BAS Agent there are a number of ways to assist your clients’ Accountant. Although the Tax Agent Services Act restricts your role to services that relate to the “collection and recovery” of FBT, services that come within this parameter that you can undertake include:

• Advising on the due date for FBT returns, including any penalties that may apply for late lodgement

• Helping gather information to determine whether a fringe benefit has been provided (e.g. an Accountant may ask you to detail/collate all the instances where a private expense has been paid by an employer for an employee)

• Assisting with record keeping requirements, including employee declarations and the recording of odometer readings at the start and end of the FBT year

• Appropriate coding of transactions (e.g. coding personal expenses paid by an employer to an ‘employee benefits (FBT)’ account in the management accounts)

• From 1 July, you can also prepare payment summaries (including the reportable fringe benefits amount).

Electronic RecordsWith many clients now keeping records electronically – either on their internal hard drive or ‘in the cloud”, in mid-February the ATO released Taxation Ruling TR 2018/2 – Record keeping and access – electronic records. Whether you as a BAS Agent are responsible for keeping/maintaining/storing records for a client is a matter that will be resolved by the terms of your engagement (which should be documented in your Engagement Letter with the client).

The new ruling contains a number of principles that the ATO says can apply to new and emerging methods of electronic record-keeping as follows:

• electronic records are recognised as documents for tax law purposes

• business taxpayers must keep records that record and explain all transactions and other acts they engage in which are relevant for any purpose of the income tax law

• records must be kept of electronic business transactions. As a minimum, the date, amount and character of the transaction needs to be recorded

• a hard copy of the information does not need to be kept (unless a particular rule requires it)

• electronic records must be in a form that the ATO can access and understand in order to ascertain the taxpayer’s tax liability (if required)

• true and clear electronic reproductions of original paper records can be kept

• the taxpayer must ensure that electronic records are secure, accurate and maintained in accordance with the record-keeping requirements

BOOKIES BULLETIN | Australian Bookkeepers Network | 8

9 | Australian Bookkeepers Network | BOOKIES BULLETIN

• if the ATO requires access to the document, the person may provide it in either electronic or hard copy form, unless directed otherwise

• the occupier of land, premises or a place being accessed must give the ATO reasonable use of facilities and assistance to extract electronically stored information, including login codes, encryption keys and passwords and

• the ATO’s access powers can be used to obtain records stored in the cloud, even if the service provider is offshore.

The full ruling is available on the ATO website.

Superannuation Clearing House AccessThere’s been some confusion around access to the ATO’s Superannuation Clearing House since it joined the ATO’s online services in late February (previously the service was accessible on its own standalone site via www.sbsch.gov.au )

Tax professionals (including BAS Agents) will be able to continue using the Clearing House on behalf of their clients – it’s just that the facility is now accessed from the Tax Agent and BAS Agent portals since Monday 26 February 2018. The Clearing House is located in the 'Manage Employees' menu.

If clients manage their own Superannuation Guarantee contributions, then they will need to use the ATO’s Business Portal to access the Clearing House. This may require them to obtain an AUSkey or alternative ATO authentication credential.

CPE RequirementsIn this first of a series of pieces on Continuing Professional Education (CPE), we look at the different requirements imposed by professional associations and the Tax Practitioners Board.

Many Bookkeepers and Accountants are members of professional associations (such as Australian Bookkeepers Association!). In order to be eligible to renew their membership, some of these associations impose their own CPE requirements. This typically involves the completion of a certain number of hours over a set peroid, with a minimum number of hours required each year. Which education/learning activities are relevant and count towards these hours is often couched loosely, for example that the education “increases your ability to do your job”. It then falls to the Bookkeeper to assess which education/learning fits this criterion.

The Tax Practitioners Board also impose their own CPE requirements which must be met by Tax Agents and BAS Agents as a condition of their registration as Agents. The Board’s requirements are totally separate to those of professional associations and for BAS Agents involve the completion of a minimum 45 hours over a three-year period with a minimum of five hours each year. Some of the key differences with professional association CPE requirements are:

• Board CPE must relate to a BAS Agent service that you provide (not just be CPE that increases your ability to do your job or run your business). For example, if you offer payroll tax services, then whilst CPE in this area will increase your ability to do your job, as it is not a BAS service it will not count towards your Tax Practitioner Board CPE requirements

• No more than 25 per cent of Board CPE should be undertaken through relevant technical or professional reading

(thus the balance must be filled by other forms of CPE such as webinars, seminars, workshops, conferences etc.)

• Interestingly, cyber security awareness training has been deemed by the Board to be relevant CPE as it can assist you in preventing a cyber attack.

Therefore, the Board’s requirements should be considered separately to the those of professional associations. While some of your CPE hours may count for both Board and professional association purposes, some of the hours may not.

Wine TimeIn the previous edition of this publication, we examined the income tax and GST treatment of a simple cup of coffee. This time we examine the treatment of wine in typical business expense situations:

GST Creditable and Income Tax Deductible

• Travelling overnight on business – wine and other meal expenses you incur in the form of sustenance

• Wine is given as a gift to a 3rd party (such as a client, supplier or contractor) or an employee or their spouse

• Where wine is part of entertainment that is subject to FBT under the Actual Method or 50/50 Method (if in doubt, ask the client’s accountant about these FBT Methods).

Non-GST Creditable and Not Tax Deductible

• Friday night drinks

• Christmas parties

• Client lunches.

For further guidance, see our Bookkeepers Knowledge Base publication (edition 20) in the Member Centre of our website.

NUTS & bolts

NUTS & bolts

BOOKIES BULLETIN | Australian Bookkeepers Network | 10

Client InformationWe trust that you are enjoying ABN’s 2017 Bookkeeping Benchmark Report released in January. In the report, bookkeepers identified that the biggest challenge they face in their work is obtaining timely and accurate data from their clients. To assist with this we recommend where possible developing and distributing to clients checklists of the information that you require from them, as well as the dates that this should be supplied. This may vary from client to client. While these checklists may take some time to develop, they will doubtless be worth it in terms of the future time and frustration that can saved.

ABN’s Bookkeeping Benchmark Report continues to set the standard for any bookkeeper wanting to know and understand some of the key drivers of the bookkeeping industry. The Report is the result of a nation-wide survey of bookkeepers undertaken every year. This is not just another charge rate report—the Bookkeeping Business Benchmark Report cuts to the very heart of the financial benchmarks and performance of a bookkeeping business. It specifically focuses on identifying a number of key performance indicators (KPI) that influence a bookkeeping business and its profits—KPIs that all owners and principals of a bookkeeping business should be striving to achieve. To purchase your copy if you have not already done so, visit the ABN website.

Single Touch PayrollSingle Touch Payroll head-counts need to be undertaken in less than one month!

On 1 April 2018, if a client has 20 or more employees (part-time, full-time, or casual) they will be required to be STP-compliant by 1 July 2018. Where this 20 employee threshold is met, even if the number of employees at a later date drops below this number, an employer will still be required to report via STP (however they may be able to apply to the ATO for an exemption if going forward employee numbers are expected to be permanently below 20).

‘Employee’ for STP head-count purposes is the common law definition of employee (which is narrower than the definition for Superannuation Guarantee purposes). Thus, workers for whom an employer does not withhold PAYG from will generally not count towards the 20 employee threshold. Also not included in the count are staff provided by third-party labour-hire, office-holders and directors of companies, casual employees who did not work in March 2018, independent contractors, or religious practitioners. On the other hand, employees based overseas, employees absent on leave, and seasonal employees are included. Although in most cases it will be clear cut as to whether a worker is an employee, if you are uncertain, you should seek advice from the Accountant. Note that it appears that connected or related businesses are not required to include employees from those other businesses in their head count. Only wholly-owned groups are required to do so. Where a company owns 100% of any other company they would generally form a wholly-owned group and if the employee headcount across all entities of the wholly owned group was 20 or more, then all entities in the wholly owned group would be larger employers and thus required to be STP-compliant by 1 July 2018.

Note that although the ATO is currently working closely with software providers, some providers may not be ready by the 1 July start date. Where this is the case, the ATO will grant a deferral for affected employers. The ATO may also grant exemptions for employers in rural areas with no reliable internet connection, and also employers who only have 20 or more employees for a short period of the income year (e.g. due to harvesting activities).

Still on Single Touch Payroll, the Government has released draft legislation to make this new regime mandatory for smaller employers (those with less than 20 employees) from 1 July 2019.

Upcoming CPE OpportuntiesATO Open Forums

• In-person

• Various locations around Australia

• Topics covered include Single Touch Payroll, Small Business Superannuation Clearing House changes, identity authentication and authorisation including details on the replacement for AUSkey and more.

• Free

ATO Monthly Webcast

• Practitioner Lodgement Service – special edition

- 27 March at 2pm AEDT

- Online

- Free

ATO Single Touch Payroll Webinars

Find out how Single Touch Payroll will affect you and your clients at the ATO's Single Touch Payroll webinars:

• Why and what is Single Touch Payroll? on 13 March at 2.00pm EDT

• Headcount on14 March at 2.00pm EDT

Places are limited so register now to secure your place.

Australian Payroll Association

• Classroom payroll training (Masterclass and Fundamentals)

- Various dates, locations, and topics

- Fees apply

Tax Practitioners Board Webinars

• Confidentiality and Conflicts – What to do!, Tuesday 20 March 2018, 11am – 12pm (AEDT)

• Emerging Issues Affecting Your Practice, Tuesday 20 March 2018, 1pm – 2pm (AEDT)

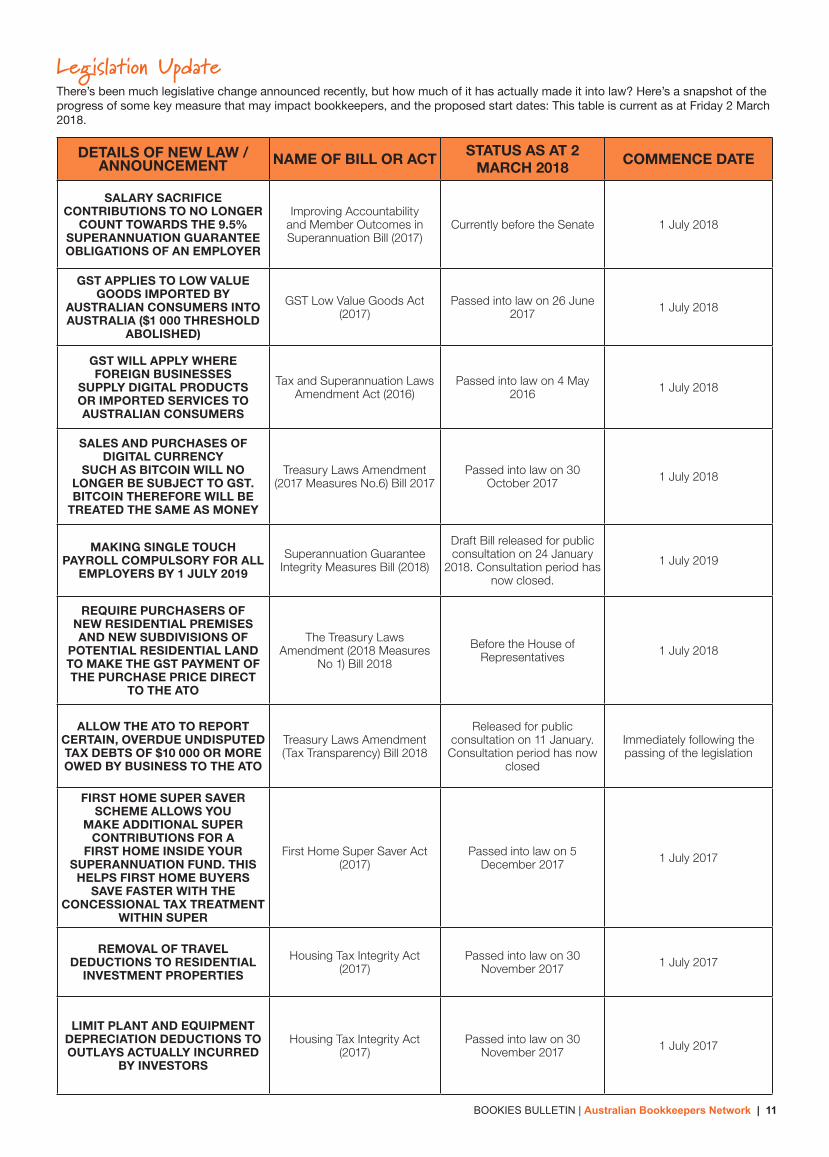

Legislation UpdateThere’s been much legislative change announced recently, but how much of it has actually made it into law? Here’s a snapshot of the progress of some key measure that may impact bookkeepers, and the proposed start dates: This table is current as at Friday 2 March 2018.

DETAILS OF NEW LAW / ANNOUNCEMENT NAME OF BILL OR ACT STATUS AS AT 2

MARCH 2018 COMMENCE DATE

SALARY SACRIFICE CONTRIBUTIONS TO NO LONGER

COUNT TOWARDS THE 9.5% SUPERANNUATION GUARANTEE OBLIGATIONS OF AN EMPLOYER

Improving Accountability and Member Outcomes in Superannuation Bill (2017)

Currently before the Senate 1 July 2018

GST APPLIES TO LOW VALUE GOODS IMPORTED BY

AUSTRALIAN CONSUMERS INTO AUSTRALIA ($1 000 THRESHOLD

ABOLISHED)

GST Low Value Goods Act (2017)

Passed into law on 26 June 2017 1 July 2018

GST WILL APPLY WHERE FOREIGN BUSINESSES

SUPPLY DIGITAL PRODUCTS OR IMPORTED SERVICES TO AUSTRALIAN CONSUMERS

Tax and Superannuation Laws Amendment Act (2016)

Passed into law on 4 May 2016 1 July 2018

SALES AND PURCHASES OF DIGITAL CURRENCY

SUCH AS BITCOIN WILL NO LONGER BE SUBJECT TO GST. BITCOIN THEREFORE WILL BE

TREATED THE SAME AS MONEY

Treasury Laws Amendment (2017 Measures No.6) Bill 2017

Passed into law on 30 October 2017 1 July 2018

MAKING SINGLE TOUCH PAYROLL COMPULSORY FOR ALL

EMPLOYERS BY 1 JULY 2019

Superannuation Guarantee Integrity Measures Bill (2018)

Draft Bill released for public consultation on 24 January

2018. Consultation period has now closed.

1 July 2019

REQUIRE PURCHASERS OF NEW RESIDENTIAL PREMISES AND NEW SUBDIVISIONS OF

POTENTIAL RESIDENTIAL LAND TO MAKE THE GST PAYMENT OF THE PURCHASE PRICE DIRECT

TO THE ATO

The Treasury Laws Amendment (2018 Measures

No 1) Bill 2018

Before the House of Representatives 1 July 2018

ALLOW THE ATO TO REPORT CERTAIN, OVERDUE UNDISPUTED TAX DEBTS OF $10 000 OR MORE OWED BY BUSINESS TO THE ATO

Treasury Laws Amendment (Tax Transparency) Bill 2018

Released for public consultation on 11 January. Consultation period has now

closed

Immediately following the passing of the legislation

FIRST HOME SUPER SAVER SCHEME ALLOWS YOU

MAKE ADDITIONAL SUPER CONTRIBUTIONS FOR A

FIRST HOME INSIDE YOUR SUPERANNUATION FUND. THIS

HELPS FIRST HOME BUYERS SAVE FASTER WITH THE

CONCESSIONAL TAX TREATMENT WITHIN SUPER

First Home Super Saver Act (2017)

Passed into law on 5 December 2017 1 July 2017

REMOVAL OF TRAVEL DEDUCTIONS TO RESIDENTIAL

INVESTMENT PROPERTIES

Housing Tax Integrity Act (2017)

Passed into law on 30 November 2017 1 July 2017

LIMIT PLANT AND EQUIPMENT DEPRECIATION DEDUCTIONS TO OUTLAYS ACTUALLY INCURRED

BY INVESTORS

Housing Tax Integrity Act (2017)

Passed into law on 30 November 2017 1 July 2017

BOOKIES BULLETIN | Australian Bookkeepers Network | 11

12 | Australian Bookkeepers Network | BOOKIES BULLETIN

FIVE MINUTES WITH...Elizabeth McFarlane

Let’s start with a personal introduction—tell us a bit about yourself.Originally from Melbourne, I moved to Perth for work and a lifestyle change. I stayed in Perth for five years, started my business, met my husband and had a baby. We have just moved to Townsville for my husbands work.

How did you get started in the bookkeeping industry?I started my career working in accounts for private companies. After a few commercial Accounting roles, a friend suggested I register for an ABN and run my own business. I didn’t really know what to do with it but had a strong Accounting background so decided to do bookkeeping and it went from there.

Tell us about your bookkeeping practice. What services do you offer, what is the industry like in your area, etc? My bookkeeping business is based on small to medium enterprises. We offer general bookkeeping, payroll and BAS services. My clients are based in Melbourne and Perth. I am not sure of the local area as we have only been living in Townsville for a few months. Through our coffee club I hope to gage more local industry knowledge.

What is your opinion on the growth of the bookkeeping profession? How has it changed since you first started bookkeeping? I started in the industry when it was desktop software programs and everyone used MYOB. Through online computing and the cloud, bookkeeping functionality has been streamlined significantly. We are constantly keeping up to date with technology on top of industry knowledge and compliance.

What makes you passionate about bookkeeping? I am passionate about seeing businesses grow. I feel that I can add value to a business by providing bookkeeping services.

Do have any marketing tips or tricks you would like to share? Be natural. I am not very good at marketing but find if I believe in and know what I am talking about it goes a long way in gaining a new client.

What have you gained from your ABN membership? ABN guided me with getting started in my business. I wasn’t a BAS Agent when I first started out so utilized ABN BAS to lodge clients BAS’. Since I have grown professionally, I have gained a network of like minded people, resources to assist running my business and general knowledge of the industry.

What essential advice do you have for other bookkeepers? Have a good mentor and ensure you keep up to date on industry knowledge. Don’t be afraid to ask for advice when you need it.

Tell us what Coffee Clubs are about for you. And, as a network leader, how do you prepare for your meetings?Coffee Clubs for me are about networking with and meeting new people. It is good to chat about our industry over a coffee. My preparation involves setting the agenda items and completing research to provide as much information as possible for our discussion.

PROFESSIONAL TITLE Director

BUSINESS NAME EightySeven Business Services Pty Ltd

LOCATIONTownsville QLD

PROUD ABN MEMBER SINCE 2013

FAVOURITE ABN SERVICE & WHY Coffee Clubs are a great way to meet like minded people and chat about common interests and network.