Embed Size (px)

Citation preview

STAR ConferenceSTAR ConferenceOctober, 7 2009

Andrea CasaliniChi f E ti OffiChief Executive Officer

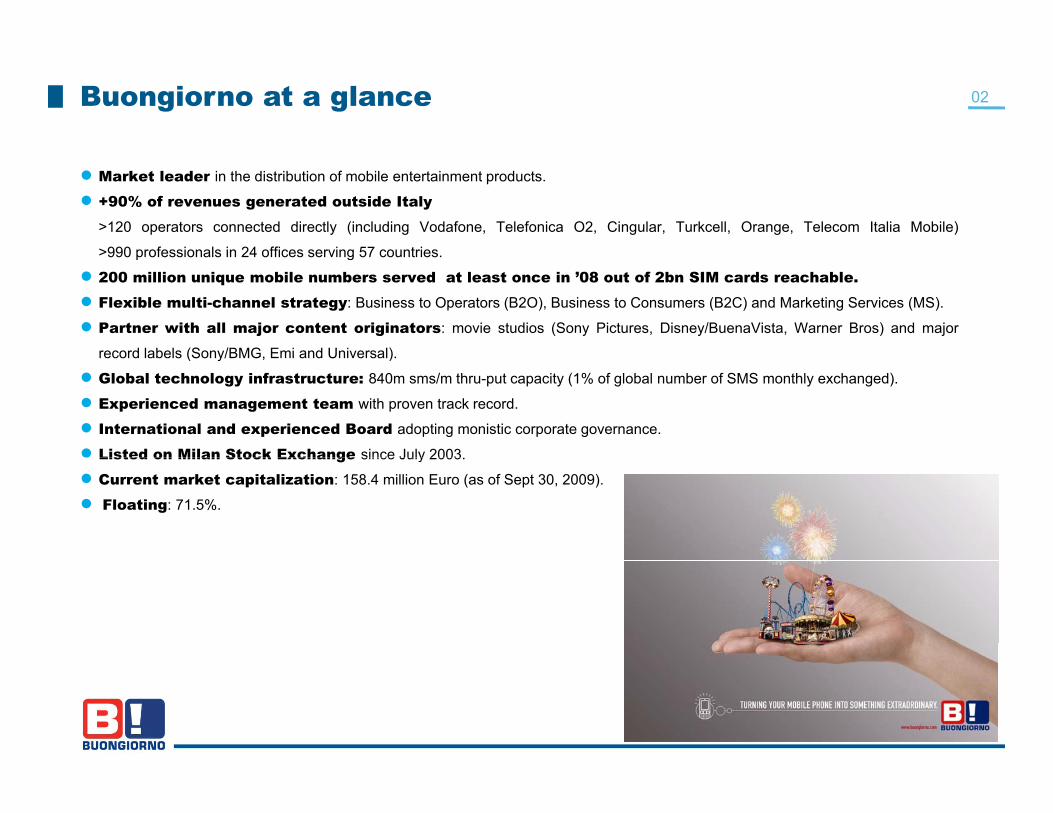

02Buongiorno at a glance

● Market leader in the distribution of mobile entertainment products.

● +90% of revenues generated outside Italy>120 operators connected directly (including Vodafone, Telefonica O2, Cingular, Turkcell, Orange, Telecom Italia Mobile)

>990 professionals in 24 offices serving 57 countries>990 professionals in 24 offices serving 57 countries.

● 200 million unique mobile numbers served at least once in ’08 out of 2bn SIM cards reachable.● Flexible multi-channel strategy: Business to Operators (B2O), Business to Consumers (B2C) and Marketing Services (MS).

● Partner with all major content originators: movie studios (Sony Pictures, Disney/BuenaVista, Warner Bros) and major

record labels (Sony/BMG Emi and Universal)record labels (Sony/BMG, Emi and Universal).

● Global technology infrastructure: 840m sms/m thru-put capacity (1% of global number of SMS monthly exchanged).

● Experienced management team with proven track record.

● International and experienced Board adopting monistic corporate governance.

● Listed on Milan Stock Exchange since July 2003.Listed on Milan Stock Exchange since July 2003.

● Current market capitalization: 158.4 million Euro (as of Sept 30, 2009).

● Floating: 71.5%.

2

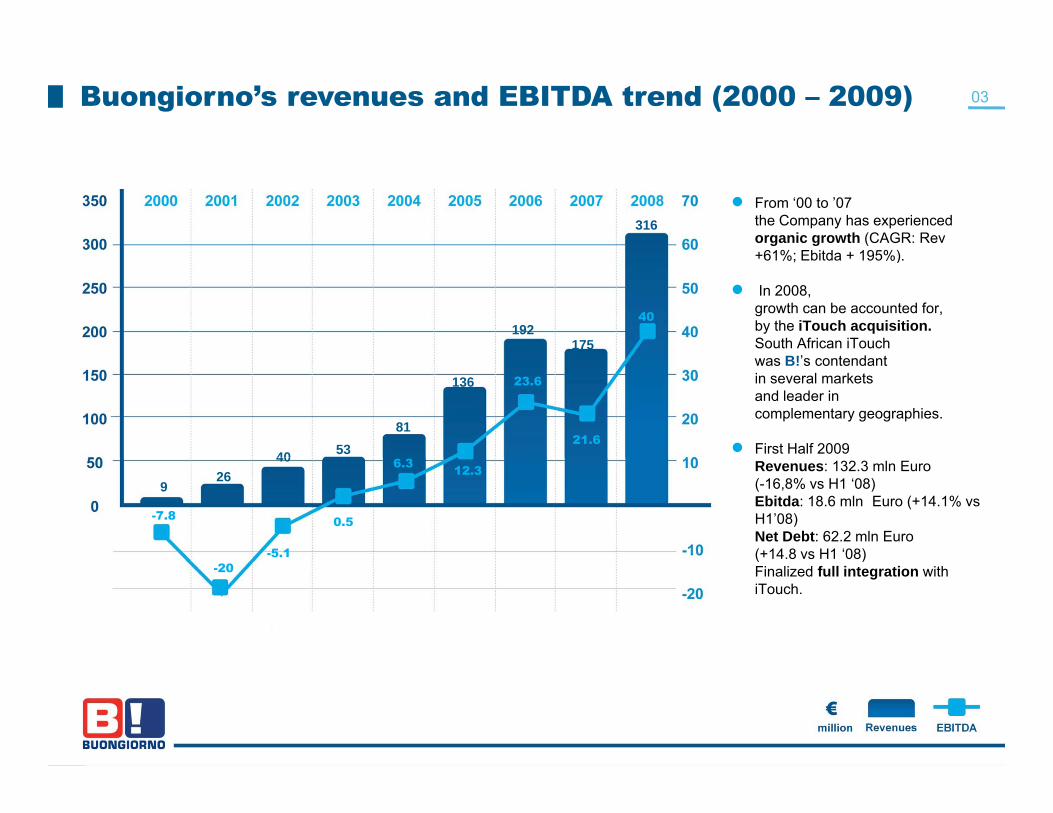

Buongiorno’s revenues and EBITDA trend (2000 – 2009) 03

316● From ‘00 to ’07

the Company has experienced organic growth (CAGR: Rev+61%; Ebitda + 195%)

192175

40

+61%; Ebitda + 195%).

● In 2008, growth can be accounted for, by the iTouch acquisition.South African iTouch

B!’ d

5340

136

8121.6

23.6was B!’s contendantin several markets and leader in complementary geographies.

● First Half 2009 40

926 12.36.3

0.5

-5.1

-7.8

Revenues: 132.3 mln Euro (-16,8% vs H1 ‘08) Ebitda: 18.6 mln Euro (+14.1% vsH1’08)Net Debt: 62.2 mln Euro(+14.8 vs H1 ‘08)

-20( )Finalized full integration withiTouch.

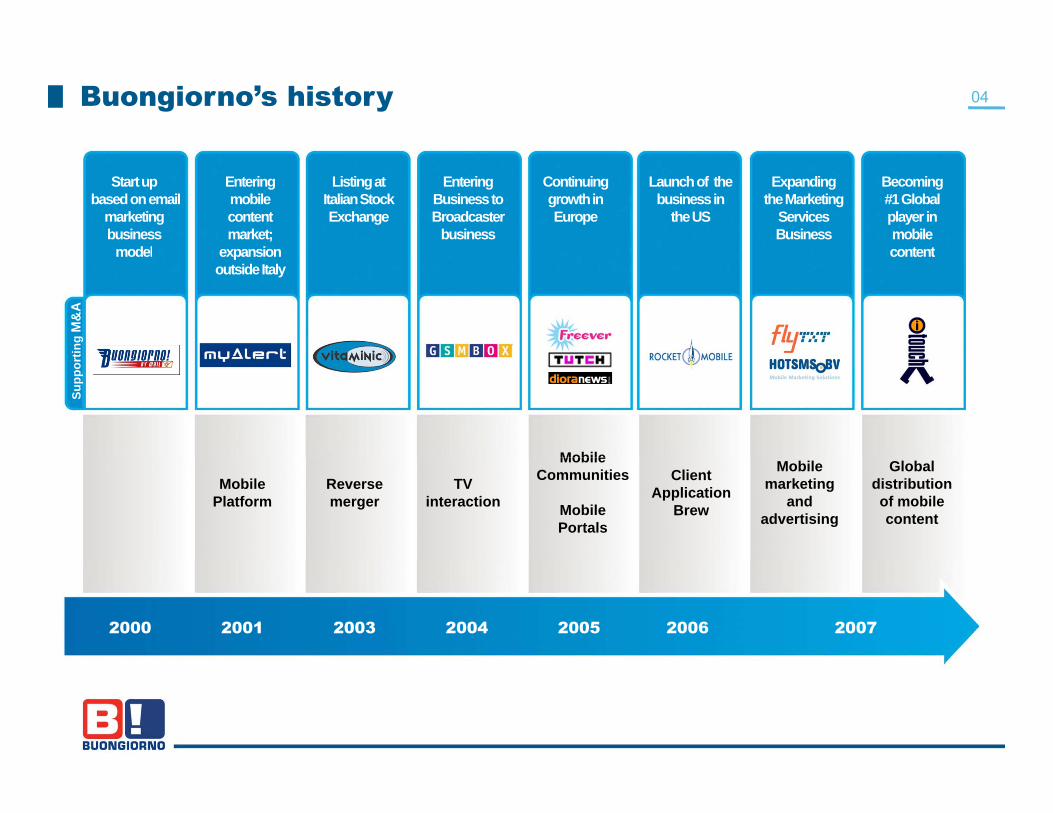

04Buongiorno’s history

Becoming#1 Global player in mobile content

Listingat ItalianStock Exchange

EnteringBusiness toBroadcaster

business

Continuinggrowthin Europe

Launchof the business in

the US

Enteringmobile contentmarket;

expansion

Expandingthe Marketing

ServicesBusiness

Start upbasedon email

marketing business

model contentexpansionoutsideItaly

model

ting

M&

A

Mobile

Supp

ort

Mobile Platform

Reverse merger

TV interaction

Mobile Communities

Mobile Portals

Mobile marketing

and advertising

Client Application

Brew

Global distributionof mobile content

2001 2003 2004 2005 2006 20072000

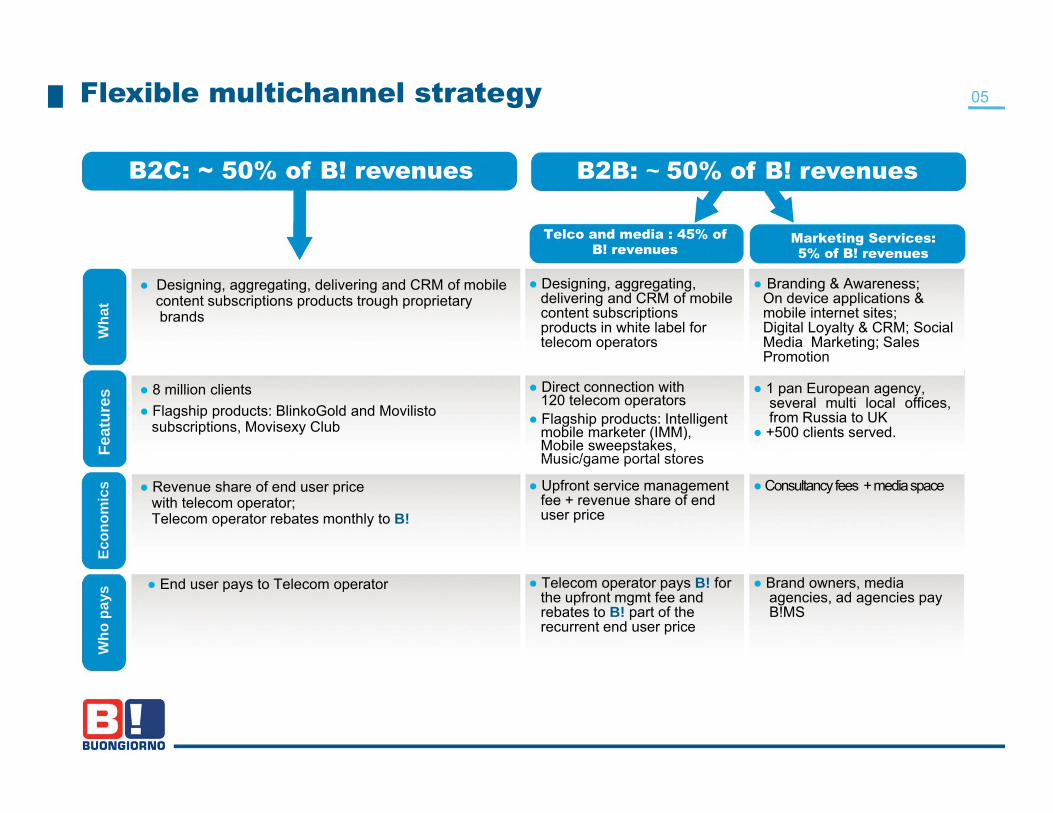

05Flexible multichannel strategy

Telco and media : 45% ofB! revenues

Marketing Services: 5% of B! revenues

B2B: ~ 50% of B! revenuesB2C: ~ 50% of B! revenues

B! revenues 5% of B! revenues

● Designing, aggregating, delivering and CRM of mobile content subscriptions products in white label for telecom operators

● Branding & Awareness; On device applications & mobile internet sites; Digital Loyalty & CRM; Social Media Marketing; Sales Promotion

Wha

t

● Designing, aggregating, delivering and CRM of mobile content subscriptions products trough proprietary brands

● Direct connection with 120 telecom operators

● Flagship products: Intelligent mobile marketer (IMM), Mobile sweepstakes, Music/game portal stores

Promotion

● 8 million clients● Flagship products: BlinkoGold and Movilisto

subscriptions, Movisexy Club

● 1 pan European agency,several multi local offices,from Russia to UK

● +500 clients served.

Feat

ures

● Revenue share of end user price with telecom operator; Telecom operator rebates monthly to B!

Music/game portal stores

● Upfront service management fee + revenue share of end user price

Econ

omic

s ●Consultancy fees + media space

● End user pays to Telecom operator ● Brand owners, media agencies, ad agencies pay B!MS

Who

pays

● Telecom operator pays B! for the upfront mgmt fee and rebates to B! part of the recurrent end user price

06Buongiorno’s global competitive position in the mobile content market

Competitors: End2End GermanyUK

Competitors: Motoricity, Amdocs, RealNetworks, FoxMobile/Jamba, Acotel/Flycell Dada

Competitors: Amdocs, Momac, RealNetworks, Materna, FoxMobile/Jamba, Dada, Zed, Cellcast

Competitors: Amdocs, Arvato Mobile, RealNetworks, FoxMobile/Jamba, Materna, Dada, Zed, Celldorado,BobMobile

Competitors: End2End, Amdocs, Arvato Mobile, Momac, RealNetworks, FoxMobile/Jamba, Materna, Zed, Celldorado

GermanyFrance

Usa

Acotel/Flycell, Dada, Thumbplay

Competitors: Acotel/Flycell, FoxMobile/Jamba, WixawinTimwe, C lld d

Competitors: Acotel/Flycel,Timwe, Neomobile

Competitors:Amdocs, Arvato Mobile,

RealNetworks, Dada, Materna, Acotel/Flycell, Zed, Timwe, N bil 1

ItalyTurkeyPortugal

Competitors: Amdocs, Arvato Mobile, RealNetworks, Zed,

Competitors: Amdocs, Arvato Mobile, RealNetworks, Acotel/Flycell C i

Competitors: Timwe, Celldorado, BobMobile

Celldorado Neomobile Neomobile1

India

Greece

SpainMexico

Acotel/Flycell, xMobile/Jamba, Dada, Wixawin, Timwe, Neomobile

Competitors: AmdocsCompetitors:

Acotel/Flycell Competitors: End2End, Amdocs, RealNetworks,+OnMobile

AfricaLatAmCompetitors: Amdocs, Arvato Mobile, RealNetworks, OnMobile, Zed, Timwe,Celldorado

Competitors: Amdocs, Arvato Mobile, RealNetworks, Zed, Acotel/Flycell, Dada, Timwe, Neomobile

Competitors: End2End, Amdocs, RealNetworks, OnMobile

A few truly global competitors, still many local opportunistic players

Australia

= Buongiorno among top 10 players in the country= Buongiorno among top 3 players in the country

A few truly global competitors, still many local opportunistic players

07Buongiorno’s governance and management team

● Buongiorno’s success has been generated

by a very strong, diverse, international management

team.

● The team is a combination of Buongiorno’s founders

Mauro Del Rio Chairman

Andrea Casalini Chief Executive Officer

Carlo FrigatoChief Financial Officer

and the integration of several managers

who have steered the development of other

successful industry players.

● The result is that no other company can rely on such

Pietro De NardisMarket Development & Sales

Lucia Predolin Marketing Communications & IR

Matteo MontanExecutive Programme Officer

a combined experience in the mobile media space.

● The management team’s interest is strongly aligned

with shareholders through a stock option plan

for a combined 5 million shares benefitingpgg

the key 22 top managers.

● Total granting is linked to minimum sales & Ebitda

margin and to staying in the Company

until the year 2014.

Fernando Gonzales MesonesMarketing Product & Supply

Florence KaminskaHR & Organization Development

Alessandro GatteschiTechnology & Delivery

08Mitsui and B! global strategic partnership

● The leading conglomerates in Japan● Established in 1947; 161 offices in 69 countries● Gross profit (March ‘09) 10.7 bn USD ● Trading company with strong capacity in rolling out business

2005 MarchMitsui became one of the most important B!’s shareholders(3.3% as of today)2005 October

History of the partnership with B!

● Trading company with strong capacity in rolling out business in new markets

● IT business and value creation chain: Electronic, mobile, ICT, Display and Media

● Experience in innovative Digital Media Solution & technology in Japan/USA

2005 OctoberMitsui and B! established B! Hong Kong2007 JuneMitsui made a significant equity investment inB! Marketing Services

Buongiorno Marketing Service

Buongiorno Hong Kong:

U i l b l i M bil C t t S t

B! 49% - Mitsui 51%Non consolidatedActivities in India,Philippines and Vietnam.Total reach of 400m users.

B! 59% - Mitsui 41% Consolidated

Unique global coverage in Mobile Content Segment

09Expected trends in Mobile Content market

● Market started in the late 1990s with the launch of the first mono-ringtone service…

● In 2008, generated revenues of nearly USD 24 billion worldwide.

● Growth drivers are expected to be related to: - overall growth in mobile subscribers base in emerging geographies;

- widespread adoption of 3G penetration and streamlining of competition.

1010Mobile content: what next?

M bil Ti k tiMobile Payments1

Mobile ConfigurationMobile social gamingContent

Catalogue& User

interfaceClients’

acquisitionGeographicalfootprint Mobile Ticketing

M bil h

Mobile CommunityMobile Tv broadcasting

yfootprint

Tech Mobile search

Mobile Blogging

Mobile skilled games

Mobile Video on Demand

Arpumaximization

TechDelivery &

BillingInfrastructure

● Rigoro s R&D process in place to alidate se eral options a ailable emerging from the combination of B!’s capabilit to r n the

Mobile Video on DemandLocation Based services

SuperiorChurn mgmtcapabilities

● Rigorous R&D process in place to validate several options available emerging from the combination of B!’s capability to run the mobile business and new market’s conditions.

●R&D process led by senior managers; task forces of internal resources with specific expertise in Asian markets, web marketing and mobile communities.

● Heavy involvement by Mitsui.● New portfolio under continuous scrutiny by Board with in-or-out approach.● C 2 & ( ) ( )● Currently already 2 initiatives are in the test phase by R&D: mobile social networking (peoplesound) and status aggregator (Hellotxt).

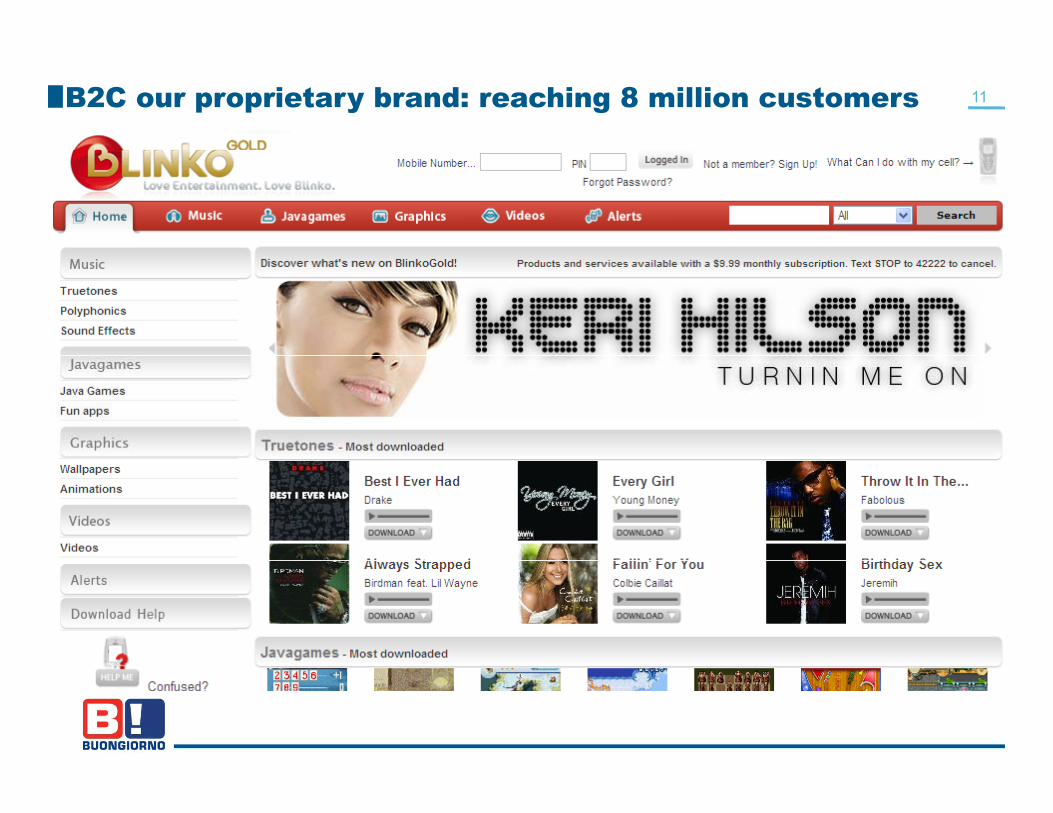

11B2C our proprietary brand: reaching 8 million customers

11

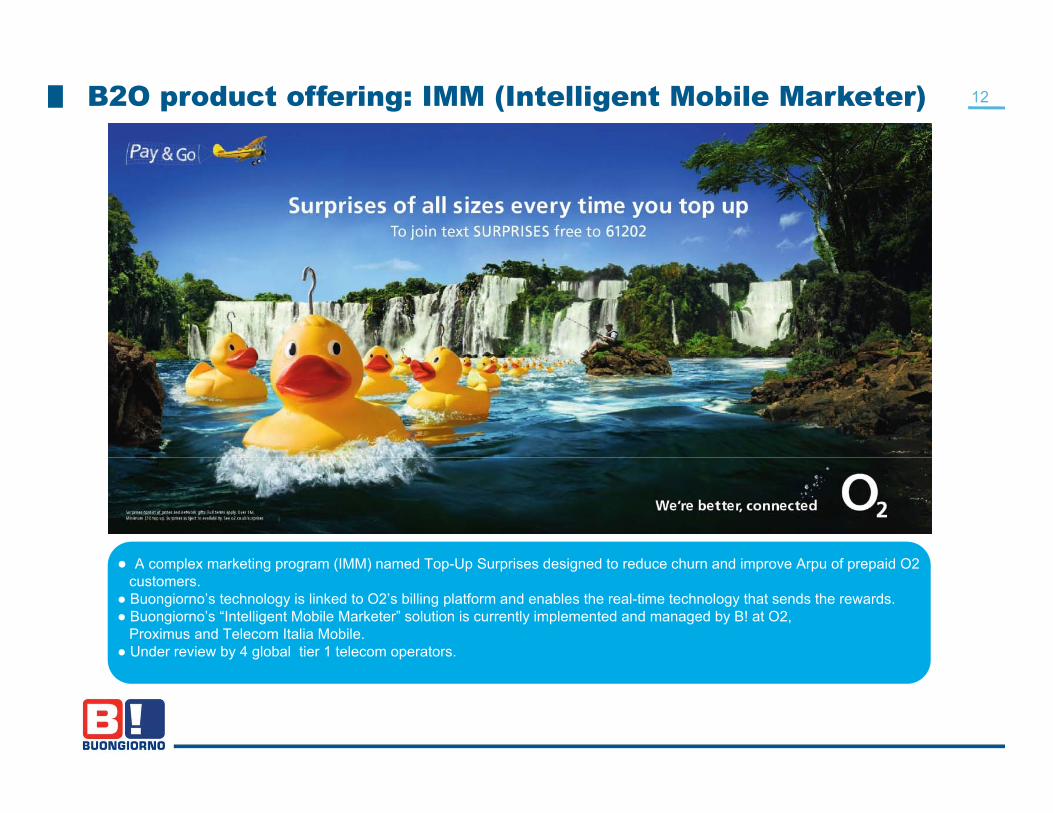

12B2O product offering: IMM (Intelligent Mobile Marketer)

A l k ti (IMM) d T U S i d i d t d h d i A f id O2● A complex marketing program (IMM) named Top-Up Surprises designed to reduce churn and improve Arpu of prepaid O2customers.

● Buongiorno’s technology is linked to O2’s billing platform and enables the real-time technology that sends the rewards.● Buongiorno’s “Intelligent Mobile Marketer” solution is currently implemented and managed by B! at O2,

Proximus and Telecom Italia Mobile.● Under review by 4 global tier 1 telecom operators.

12

13B!Marketing Services product offering: mobile centric marketing solutions

● Joint Venture:B! 59%, Mitsui 41%

● 30% d● 30% adv,70% business solutions.

● Tapping into: mobile adv, web adv and online adv markets.

● 1 pan European agency, several multi local offices, from Russia to UK.

● +500 clients served.

● Q4 ‘09 launch of the Mobile Internet enabling and affiliation platform.

● Mobile adv market expectedto reach 12 bn USD by 2011 (Gartner).

14Mobile content: what next? Mobile Social Networking

● peoplesound is the evolutionary link from computer centric to

mobile centric social networking.

● Over 500,000 users in 3 countries.

● Friends’ list limited to 20.

● Key features:

● Based on mobile phone number and real name.

● Messaging based on real time communication.

● P2P SMS & SMS Alerts.

● Content channels can be followed and commented

(for now for free).

14

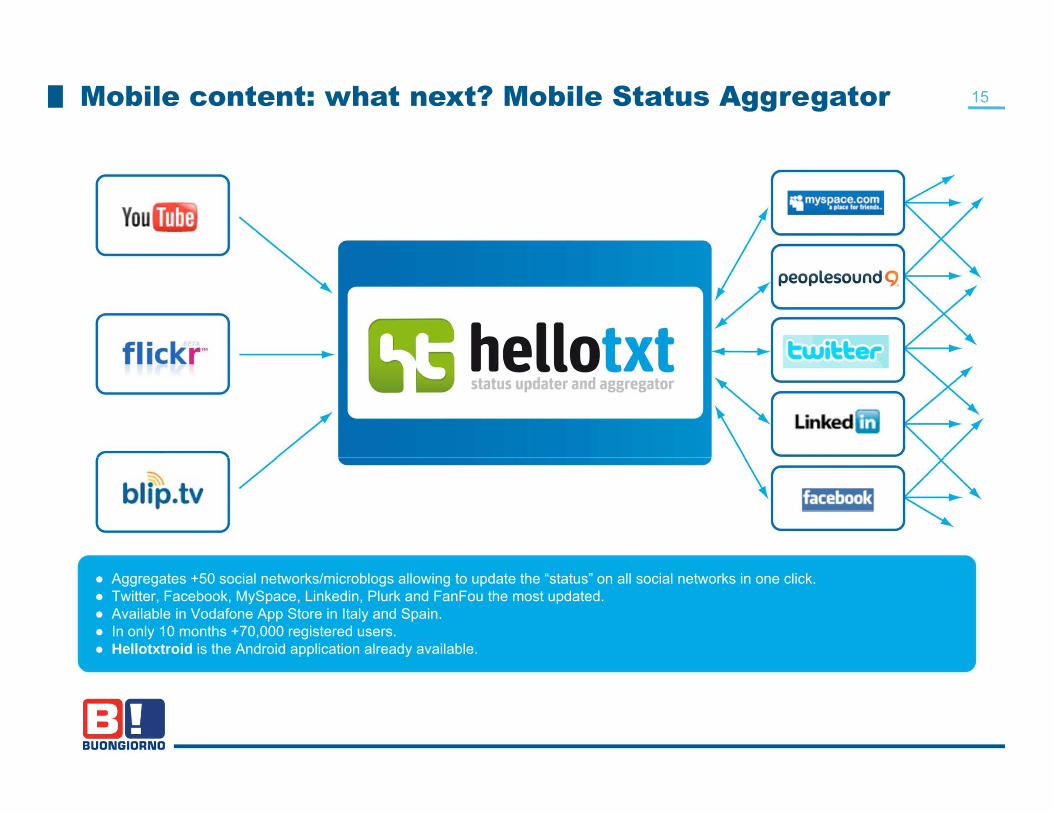

15Mobile content: what next? Mobile Status Aggregator

● Aggregates +50 social networks/microblogs allowing to update the “status” on all social networks in one click.● Twitter, Facebook, MySpace, Linkedin, Plurk and FanFou the most updated.● Available in Vodafone App Store in Italy and Spain.● In only 10 months +70,000 registered users.● Hellotxtroid is the Android application already available.

Fi i lFinancials

16

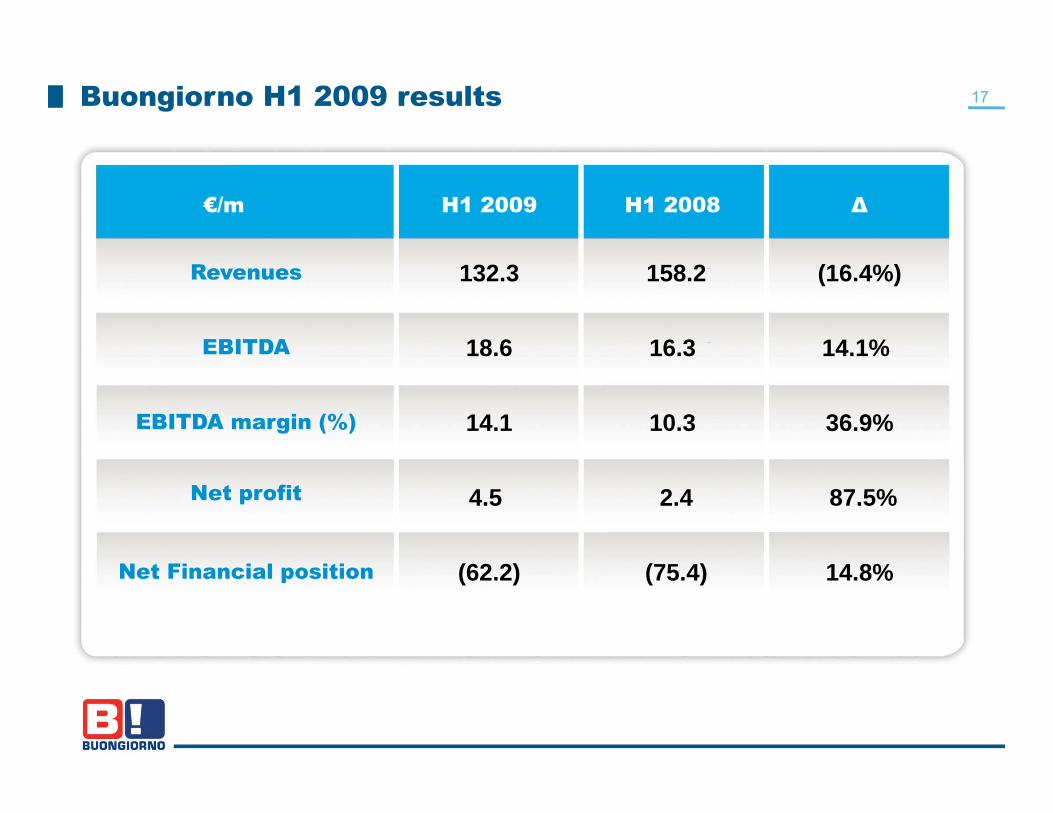

17Buongiorno H1 2009 results

H1 2009 H1 2008€/m Δ

EBITDA

Revenues 132.3 158.2

18.6 16.3

(16.4%)

14.1%

EBITDA margin (%)

18.6 16.3

14.1 10.3

14.1%

36.9%

Net profit 4.5 2.4 87.5%

Net Financial position (62.2) (75.4) 14.8%

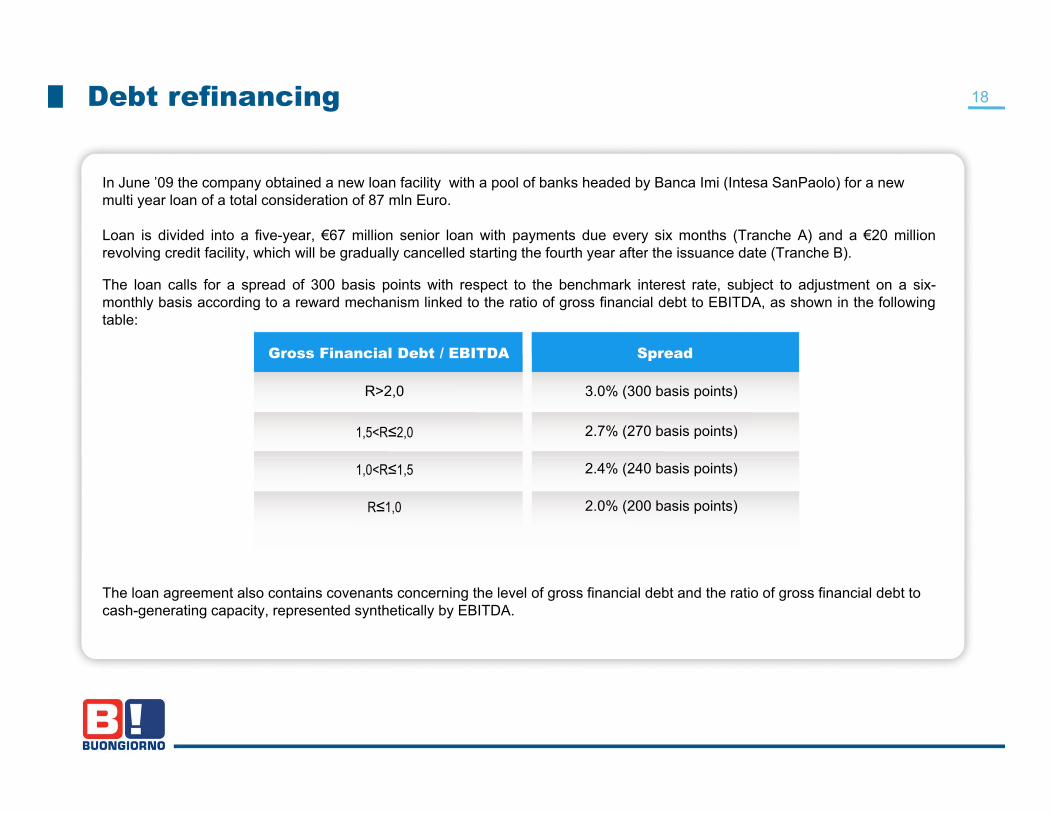

18Debt refinancing

In June ’09 the company obtained a new loan facility with a pool of banks headed by Banca Imi (Intesa SanPaolo) for a newmulti year loan of a total consideration of 87 mln Euro.

Loan is divided into a five-year, €67 million senior loan with payments due every six months (Tranche A) and a €20 millionrevolving credit facility which will be gradually cancelled starting the fourth year after the issuance date (Tranche B)revolving credit facility, which will be gradually cancelled starting the fourth year after the issuance date (Tranche B).

The loan calls for a spread of 300 basis points with respect to the benchmark interest rate, subject to adjustment on a six-monthly basis according to a reward mechanism linked to the ratio of gross financial debt to EBITDA, as shown in the followingtable:

Gross Financial Debt / EBITDA SpreadGross Financial Debt / EBITDA

R>2,0

1,5<R≤2,0

Spread

3.0% (300 basis points)

2.7% (270 basis points)

1,0<R≤1,5

R≤1,0

2.4% (240 basis points)

2.0% (200 basis points)

The loan agreement also contains covenants concerning the level of gross financial debt and the ratio of gross financial debt tocash-generating capacity, represented synthetically by EBITDA.

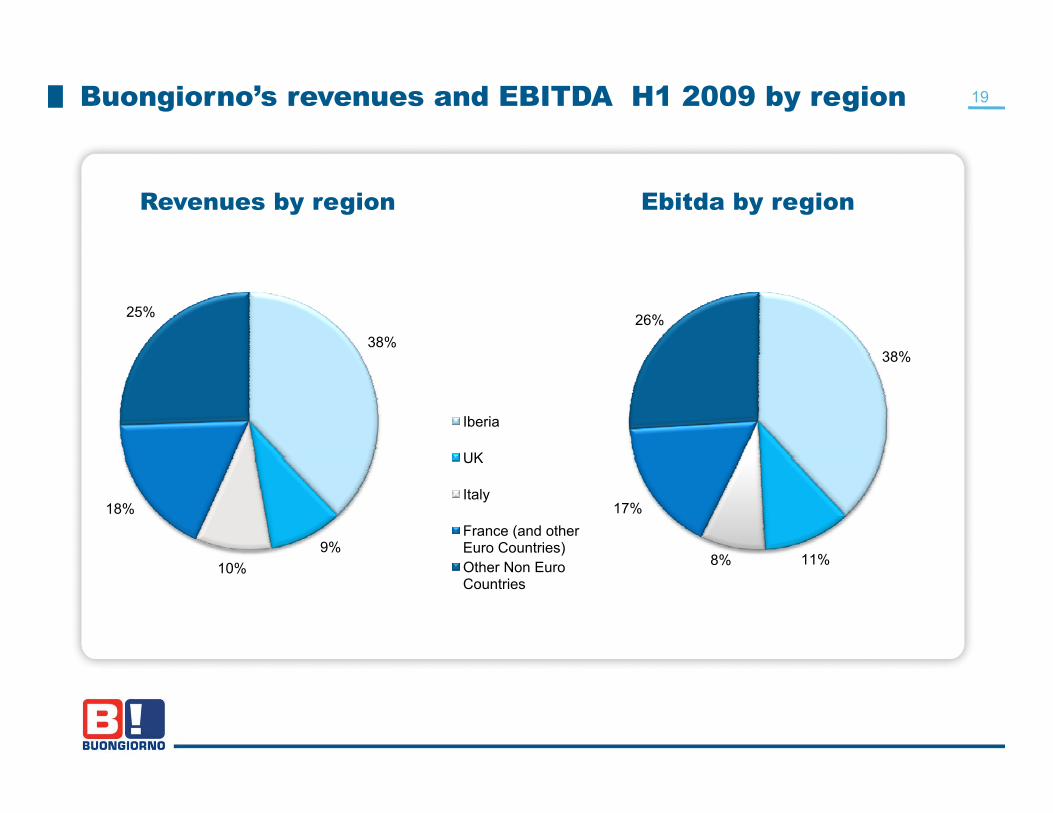

19Buongiorno’s revenues and EBITDA H1 2009 by region

Revenues by region Ebitda by region

38%

25%

38%

26%

Iberia

UK

38%

9%

18%

UK

Italy

France (and other Euro Countries)

11%8%

17%

10% Other Non Euro Countries

11%8%

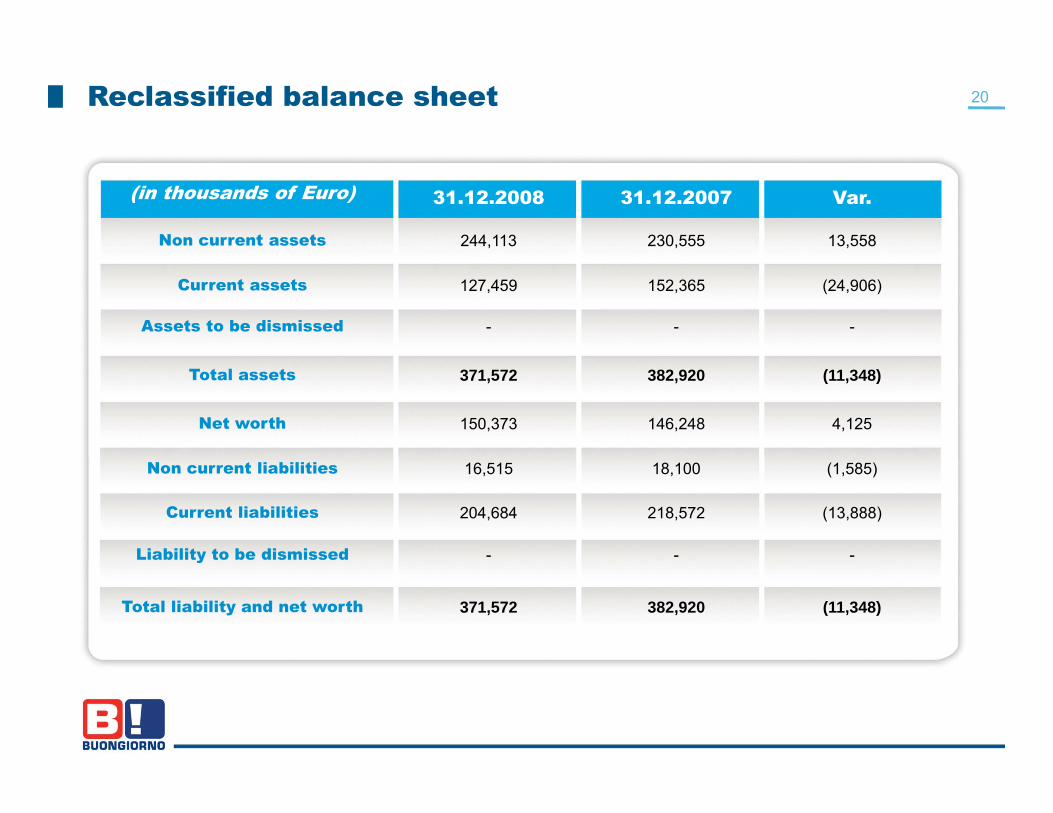

20Reclassified balance sheet

Non current assets 230,555244,113 13,558

(in thousands of Euro) 31.12.2007 Var.31.12.2008

Current assets

Assets to be dismissed

152,365

-

127,459

-

(24,906)

-

Total assets

Net worth

382,920371,572 (11,348)

146,248150,373 4,125

Non current liabilities

Current liabilities

Liability to be dismissed

18,100

218,572

-

16,515

204,684

-

(1,585)

(13,888)

-y

Total liability and net worth 382,920371,572 (11,348)

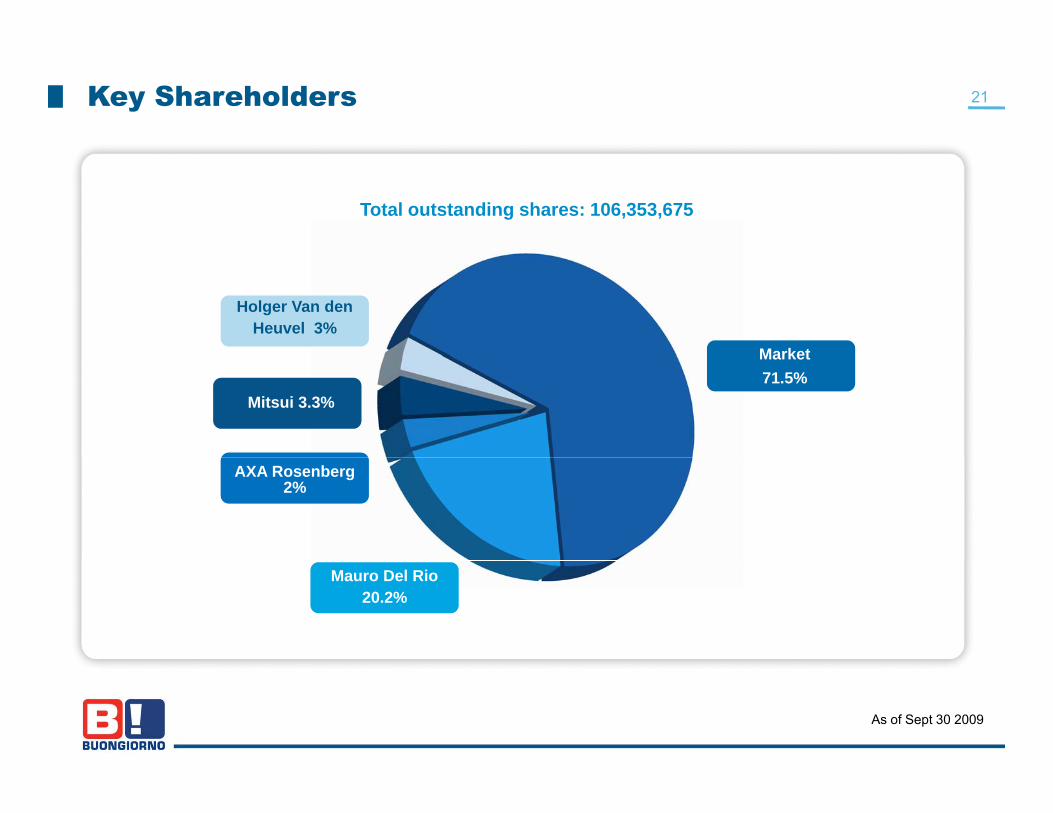

Key Shareholders 21

Total outstanding shares: 106,353,675

Market

Holger Van den Heuvel 3%

Market 71.5%

Mitsui 3.3%

AXA Rosenberg 2%

Mauro Del Rio20.2%

As of Sept 30 2009

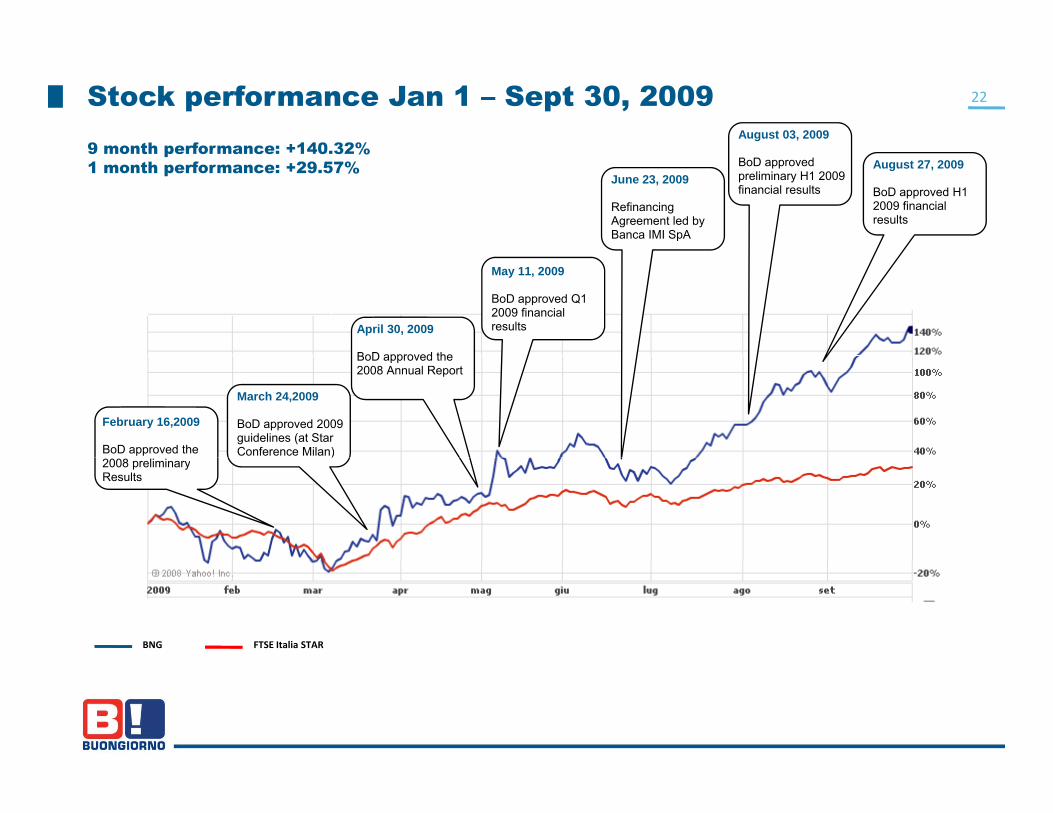

22Stock performance Jan 1 – Sept 30, 20099 month performance: +140 32%

August 03, 20099 month performance: +140.32%1 month performance: +29.57%

June 23, 2009

RefinancingAgreement led byBanca IMI SpA

BoD approvedpreliminary H1 2009 financial results

August 27, 2009

BoD approved H1 2009 financialresults

April 30, 2009

BoD approved the

May 11, 2009

BoD approved Q1 2009 financialresults

February 16,2009

BoD approved the

March 24,2009

BoD approved 2009 guidelines (at Star Conference Milan)

BoD approved the 2008 Annual Report

2008 preliminaryResults

)

FTSE Italia STARBNG

22

Th k Thank you

23

24Disclaimer

This presentation contains statements that are neither reported financial results nor other historical information. These

statements are forward-looking statements. These forward-looking statements rely on a number of assumptions and are subject

to a number of risks and uncertainties, many of which are outside the control of Buongiorno SpA, that could cause actual

results to differ materially from those expressed in or implied by such statements, such as future market conditions, currencyresults to differ materially from those expressed in or implied by such statements, such as future market conditions, currency

fluctuations, the behavior of other market participants and the actions of governmental and state regulators

24