Embed Size (px)

Citation preview

February 5, 2015

BMO 12th Annual Infrastructure & Utilities ConferenceInvestor Presentation

Pierre Despars

Executive Vice President, Corporate Affairs

and Chief Financial Officer

Cautionary note

Certain statements contained in this presentation may be forward-looking pursuant to applicable securities laws. Such forward-looking

statements reflect the intentions, plans, expectations and opinions of the management of Gaz Métro inc., acting in its capacity as General

Partner of Gaz Métro Limited Partnership (“Gaz Métro”), (the “Management”) and are based on information currently available to

Management and assumptions about future events. Forward-looking statements involve known and unknown risks and uncertainties and

other factors outside Gaz Métro’s control. A number of factors could cause actual results of Gaz Métro to differ materially from the current

expectations as expressed in the forward-looking statements.

Although these forward-looking statements are based upon what Management believes to be reasonable assumptions, Gaz Métro cannot

assure investors that actual results will be consistent with these forward-looking statements. These forward-looking statements are made as

of the date of this presentation, and Gaz Métro assumes no obligation to update or revise them to reflect new events or circumstances, except

as required pursuant to applicable securities laws. You are cautioned not to place undue reliance on these forward-looking statements. The

complete version of the cautionary note regarding forward-looking statements as well as a description of the relevant assumptions and risk

factors likely to affect Gaz Métro’s actual results are included in the Management’s Discussion and Analysis for the fiscal year ended

September 30, 2014 of Gaz Métro inc., which is available on SEDAR under Gaz Métro inc.’s profile at www.sedar.com.

Non-GAAP Financial Measures

In the opinion of Management, certain indicators, such as net income attributable to the Partners of Gaz Métro, excluding non-recurring items

(“recurring net income”), provide readers with information considered useful for analyzing the financial results of Gaz Métro. However, these

indicators are not standardized in accordance with Canadian generally accepted accounting principles (“GAAP”) and should not be

considered in isolation or as substitutes for other performance measures that are in accordance with GAAP. The results obtained might not be

comparable with similar indicators used by other issuers and should therefore be considered only as complementary information.

1

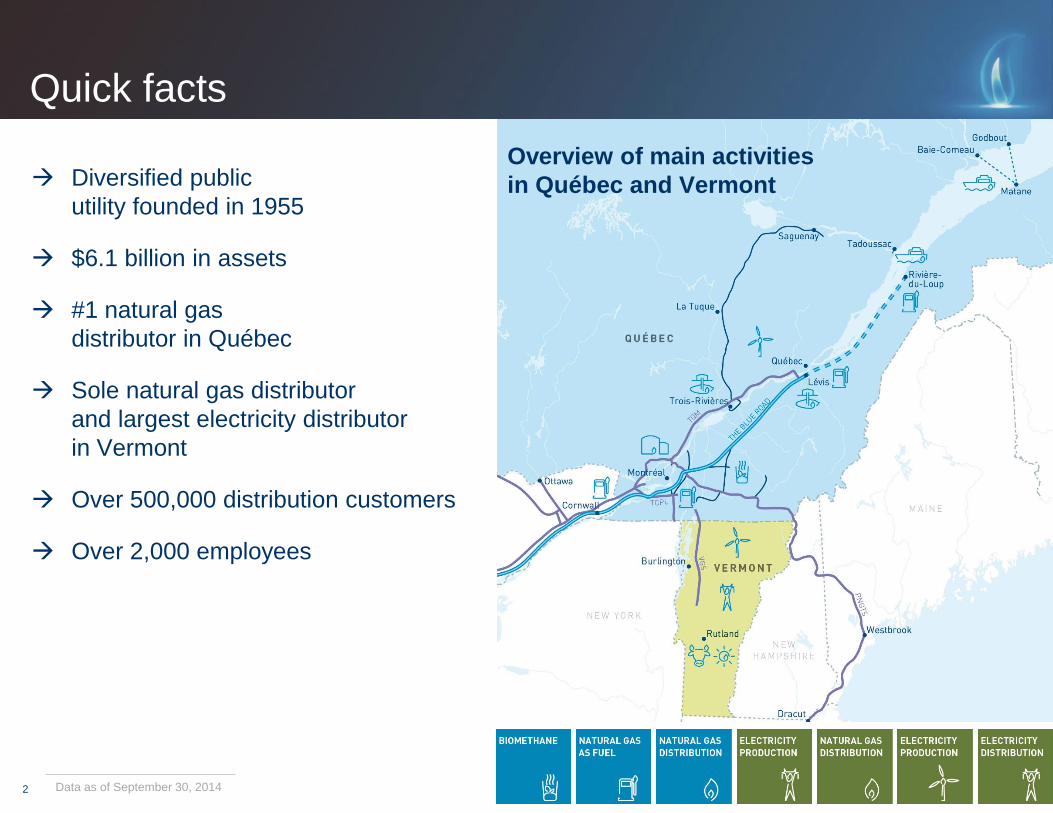

Quick facts

Diversified public

utility founded in 1955

$6.1 billion in assets

#1 natural gas

distributor in Québec

Sole natural gas distributor

and largest electricity distributor

in Vermont

Over 500,000 distribution customers

Over 2,000 employees

2 Data as of September 30, 2014

Overview of main activities

in Québec and Vermont

Highlights

Regulated asset base with predictable returns

Nearly all recurring net income generated by regulated activities

Increasingly diversified public utility through a prudent

and targeted diversification strategy

Total assets have more than doubled since 2006

Strong sponsorship from key interest owners

Strong and predictable financial performance

Strong credit ratings from internationally

recognized rating agencies

3

Business segments

Energy

Distribution

Transportation of

Natural Gas

Energy Services,

Storage and OtherEnergy Production

% of net income

F201491.3% 8.7% n.m. n.m.

4

Storage: Regulated

Others: Non-regulated

Non-regulatedRegulated

Natural gas distribution in Québec

1 Projected rate base in the 2015 rate case filed with the Régie de l’énergie.

Approved ROE for fiscal 2015.

Distributes ≈ 97%of natural gas in Québec

Over 10,000 kmof pipeline

300municipalities served

≈ 195,000 customers

Regulated assets:

≈ $1.9 billion1

Authorized ROE:

8.90%1

Natural gas distribution in Québec: our customers1

61 Fiscal year 2014

RESIDENTIAL COMMERCIAL INDUSTRIAL

Customers 139,445 71.3% Customers 48,600 24.8% Customers 7,572 3.9%

Volume 20.1 Bcf 10.0% Volume 62.3 Bcf 30.9% Volume 119.1 Bcf 59.1%

% of distribution revenues ≈ 21% % of distribution revenues ≈ 45% % of distribution revenues ≈ 34%

7

Natural gas distribution in Vermont

Wholly-owned since

1986

Sole gas distributor in Vermont

≈ 47,000 customers

1 Based on 2015 rate case as approved by Vermont Public Service Board (VPSB). Regulated assets include US$89M related to investments for Phase I. 2 Phase II subject to VPSB’s approval (Phase I approved in December 2013)

Projects to extend

distribution network2

Phase I to service Vergennes

and Middlebury

Phase II to service International

Paper Mill (NY State)

Investments: US$154M

for Phase I

Commissioning of Phase I

expected in 2016

Regulated assets:

≈ US$215M1

Authorized ROE:

10.20%1

8

Electricity distribution in Vermont

Acquisition of Green Mountain

Power (GMP) in

2007

Acquisition of Central Vermont

Public Service (CVPS) in

2012

1 Based on 2015 rate case as approved by Vermont Public Service Board (VPSB)

≈ 70%of electricity distribution market

in Vermont

≈ 260,000customers

Regulated assets:

≈ US$1.2B1

Authorized ROE:

9.60%1

Asset base diversification since 2006

In 2005, adoption of development and diversification strategy to reduce exposure

to the Québec natural gas distribution activity and become a diversified energy provider Entry in Vermont electricity distribution market

Participation in the Seigneurie de Beaupré Wind Farms (340 MW)

As a result of the successful execution of this strategy, Gaz Métro reduced its asset

exposure to Québec natural gas distribution from 72.5% in 2006 to 38.3% in 2014

9

2006$2.8 billion in assets≈ 200,000 customers

2014$6.1 billion in assets

≈ 500,000 customers

Natural gas distribution in Québec

Natural gas distribution in Vermont

Natural gas transportation

Energy services, Storage and Other

Natural gas distribution in Québec

Natural gas and electricity

distribution in Vermont

Natural gas transportation

Energy production

Energy services, Storage and Other

Data for fiscal years ended September 30, 2006 and 2014

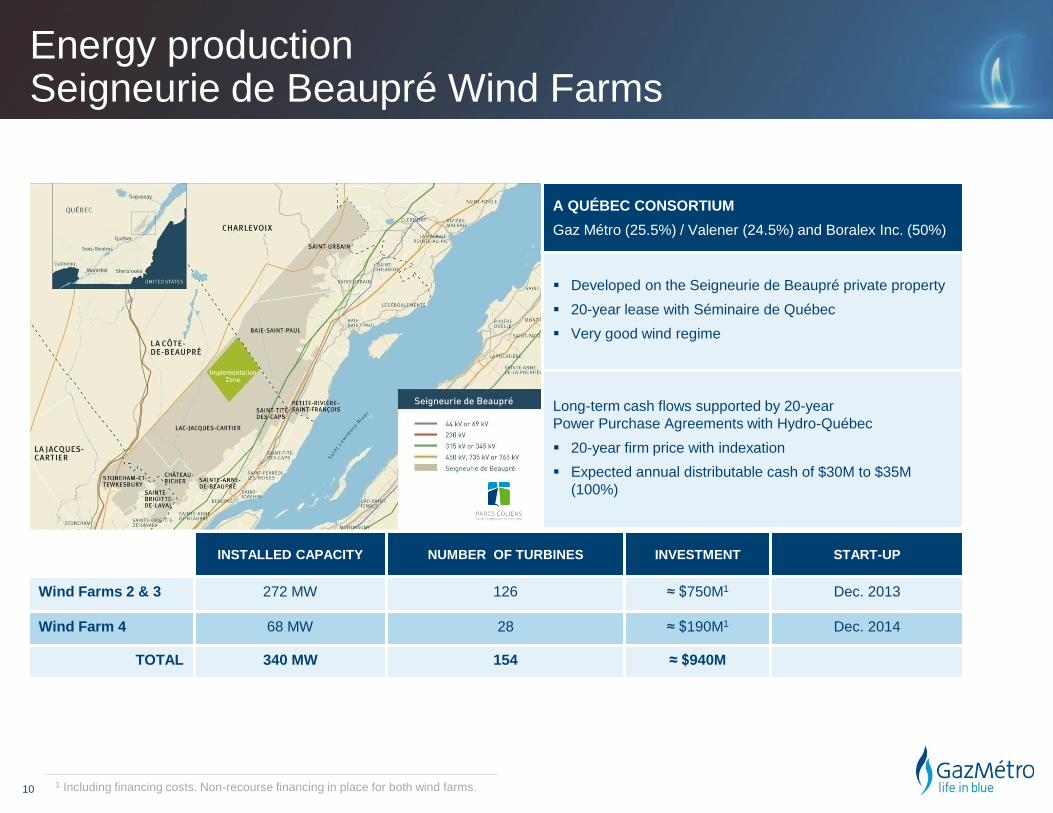

Energy productionSeigneurie de Beaupré Wind Farms

101 Including financing costs. Non-recourse financing in place for both wind farms.

A QUÉBEC CONSORTIUM

Gaz Métro (25.5%) / Valener (24.5%) and Boralex Inc. (50%)

Developed on the Seigneurie de Beaupré private property

20-year lease with Séminaire de Québec

Very good wind regime

Long-term cash flows supported by 20-year

Power Purchase Agreements with Hydro-Québec

20-year firm price with indexation

Expected annual distributable cash of $30M to $35M

(100%)

INSTALLED CAPACITY NUMBER OF TURBINES INVESTMENT START-UP

Wind Farms 2 & 3 272 MW 126 ≈ $750M1 Dec. 2013

Wind Farm 4 68 MW 28 ≈ $190M1 Dec. 2014

TOTAL 340 MW 154 ≈ $940M

Energy productionSeigneurie de Beaupré Wind Farms

11

A significant environmental advantage

-32% GHGs compared to FUEL OIL

Up to -25% GHGs compared to DIESEL

12

Electricity

Heavy fuel oil, gasoline and diesel

Natural gas

Increase

natural gas

presence

Quebec energy consumption

39.7% 38.1% 13.8%

Source: Ministère de l’énergie et des Ressources naturelles (2011 data)

Liquefied natural gas

Partnership with Government of Quebec

through Investissement Québec (IQ)

$118M investment in which IQ

will contribute up to $50M

Project to triple the liquefaction

capacity of Gaz Métro’s LSR1

plant located in Eastern Montreal Provide LNG to industries located outside main

distribution network such as Nord-du-Québec

and Côte-Nord regions

Target road and maritime transportation sectors

Capacity expected to be available

by end of 2016

13 1 Gaz Métro’s natural gas liquefaction, storage and re-gasification plant

Ownership structure

Caisse de dépôt et placement

du Québec (“CDPQ”) 25.9% indirect ownership in Gaz Métro

Enbridge Inc. 27.6% indirect ownership in Gaz Métro

Valener (TSX: VNR) Publicly-traded company whose main

asset consists of a 29.0% direct interest

in Gaz Métro

Provides Gaz Métro with potential access

to public equity market as required

Also owns 24.5% of the Seigneurie de

Beaupré Wind farms (340 MW contracted)

14 * CDPQ is Trencap’s controlling shareholder (59.64%)

Principal Interest Owners Corporate Structure

100%

100%

61.11%

100%

38.89%

71%

29%

25.5%

24.5%

TRENCAP

NOVERCO

GAZ MÉTRO INC. (the Issuer)

PUBLIC

SEIGNEURIE DE BEAUPRÉ WIND

FARMS (ENERGY PRODUCTION)

ENERGY

DISTRIBUTION

TRANSPORTATION OF

NATURAL GAS

ENERGY SERVICES,

STORAGE & OTHER

*

(THE GUARANTOR)

Key features of trust indenture

Gaz Métro inc. (GMi) (the “Issuer”)

Single purpose entity

General Partner of Gaz Métro

Financing vehicle for Gaz Métro

First mortgage bonds secured by the assets of GMi and Gaz Métro

(including Gaz Métro’s network)

Debt issuance test (Gaz Métro level)

No additional debt unless:

Funded Debt / Aggregate Capitalization ≤ 65%

Interest Coverage (EBIT) ≥ 1.5x

Distribution test (Gaz Métro level)

No distributions unless Funded Debt / Aggregate Capitalization ≤ 75%

Maintenance of regulated activities

Interest in non-regulated energy activities not to exceed 10%

of Gaz Métro’s assets (sub-level of 5% for non-energy activities)

15

Financial strength

16

S&P DBRS

Corporate / Issuer rating A (stable) A (stable)

Senior debt rating A+ (stable) A (stable)

Strong credit ratings

Strong financial preformance

151,3

147,5

151,6

165,7

174,7

130

135

140

145

150

155

160

165

170

175

180

2010 2011 2012 2013 2014

17

3.7% compound annual

growth rate (CAGR)

Recurring net income ($ millions)

Fiscal year

Strong key ratios

Regulated businesses provide Gaz Métro with significant stability and

predictability in its cash flows

Total debt / total capitalization ratio of 68.1% as of September 30, 2014

(consolidated basis)

18

Total Debt is defined as the sum of long-term debt, current portion of long-term debt and bank loans, and Total Capitalization is

defined as Total Debt plus total shareholders’ equity plus minority interests. Interest Coverage is defined as EBIT (Earnings Before

Interest and Taxes, including share in earnings of entities subject to significant influence) / Interest Expense.

Funds from Operations is defined as cash flows related to operating activities (before change in non-cash working capital items).

0,0%

10,0%

20,0%

30,0%

40,0%

50,0%

60,0%

70,0%

80,0%

0,0

0,5

1,0

1,5

2,0

2,5

3,0

3,5

4,0

4,5

5,0

2010 2011 2012 2013 2014

Interest Coverage Total Debt / Total Capitalization Funds from Operations / Average Total Debt

Fiscal year

Debt maturity profile

Staggered debt maturity profile

No significant short term refinancing risk

19

0

50

100

150

200

250

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

20

31

20

32

20

33

20

34

20

35

20

36

20

37

20

38

20

39

20

40

20

41

20

42

20

43

20

44

20

45

20

46

20

47

20

48

20

49

20

50

20

51

20

52

C$ First Mortgage Bonds US$ Senior Secured Notes$ millions

Fiscal year

Cash flows from operations

& credit facilities of ≈ $226M

Long-term debt of ≈ $93M1

Contribution from Investissement

Québec of ≈ $21M

Equity injection from GMi of ≈ $85M2

Equity injection from Valener

of ≈ $35M2

CAPEX of ≈ $390M for

extensions and improvements

to energy distribution systems Gaz Métro-QDA: ≈ $130M

VGS & GMP: ≈ $240M

Other: ≈ $20M

CAPEX of ≈ $50M

for LSR plant expansion

CAPEX of ≈ $20M

to complete wind farm 4

Expected cash requirements for fiscal 2015

20

≈ $460M

1 $20M project financing non-recourse to Gaz Métro and Valener. Already funded (included in restricted cash).

Remaining portion in US$ converted at C$1.122 Additional equity could be required depending on impact of CATS regulation

Note: amounts presented on consolidated basis

Requirements Sources

Questions?21