Embed Size (px)

Citation preview

BMO Capital Markets Economics | A Weekly Financial Digest

BMO Capital Markets Economics economics.bmo.com • 416-359-6372

Please refer to the last page for important disclosures

Focus

Too Negative Rates Don’t Make a Positive The Talented Mr. Loonie

Let’s Make a (Trade) Deal

Will Super Saturday be Truly Super?

Complacency Setting In?

Eye on Earnings

October 18, 2019

Feature Article

Our Thoughts

Our Thoughts

The Talented Mr. Loonie

.

In a week filled with tentative deals, markets rolled higher amid a rising appetitefor risk. A big winner from that trend was the Canadian dollar, which pushed above76 cents (US), close to its high for the year and up almost 2% in the past two weeks.The currency is hardly alone in the upswing, as the biggest driver of the recent movehas been a broader sag in the U.S. dollar. Still, the loonie now stands as the strongestmajor currency in the world in 2019, rising 3.8% YTD, with its NAFTA partner next inline; the Mexican peso is up 2.5% this year.

It’s not hard to find reasons why markets were in a mildly upbeat mood this week,as a wide variety of thorns were close to being removed. In the past seven daysalone, we have seen a preliminary agreement on “Phase 1” of a deal on U.S./Chinatrade; a tentative deal on the GM strike in the U.S.; an agreement between the EUand the U.K. on Brexit; and, even a five-day standstill by Turkey in Northern Syria.However, investors contained their enthusiasm: in each and every case, the outcomestill very much hangs in the balance. By Friday, global equities were aiming for a 1%gain (roughly), long-term yields were slightly higher, and the greenback had nudgedlower—the pound was the single-biggest mover, currently up more than 5% since themiddle of last week.

Amid this wave of potentially key global developments, the Canadian dollar’s ascentis notable as it comes at a time of rising uncertainty ahead of Monday’s federalelection. Polls overwhelmingly point to a close-fought minority government, with thetwo leading parties running neck-and-neck and also a close race for third place on theseat count. Some forecasts even suggest that it may require three parties to get overthe 170-seat majority threshold. And, given how close the pollsters expect the resultsto be, it’s quite possible that it will take an extended period of time to sort out a) whoactually won; and, b) how and with whom they are going to govern.

Many market commentators are downplaying concerns about the outcome, suggestingthat minorities are far from rare in Canada, and that there isn’t that much daylightbetween the economic policies of the major parties. However, while Canada doeshave plenty of experience with minority governments (including three differentversions from 2004 through 2011), a three-party dynamic is new. As well, whilethere isn’t a huge gap in the overall proposed thrust of fiscal policy, details differwidely, especially when considering some of the proposals of other parties—withpotentially big implications for the energy sector at the very least. Suffice it to say, thepreternatural calm of the Canadian dollar during the campaign is a surprise.

Of course, one key factor holding the currency aloft has been a sturdy underlyingeconomic backdrop. The flashy employment results in recent months have grabbedthe biggest headlines, with unemployment falling to just 5.5%, average hourly wagesbouncing up by more than 4%, and jobs up by a cycle-high of 2.5% y/y. As well,the housing market has made a spirited comeback from last year’s tough results,with sales rebounding 15.5% y/y last month and average prices rising 5.3% y/y. Thehousing revival has been spread across most of the country, with double-digit salesgains and price increases in seven provinces. True, neither the jobs bonanza nor thehousing rebound has translated into much in the way of overall GDP growth—we’re

October 18, 2019 | Page 2 of 19

Our Thoughts

just expecting a 1.5% advance this year. But the outlook hasn’t deteriorated amid theturbulent global backdrop of recent months, which counts as a big win.

In turn, the firm backdrop for jobs and housing has put the Bank of Canada backon ice. We have long believed that the hurdle for any rate cut by the Bank wouldbe very high. Initially, it appeared that a series of Fed rate cuts and intense globaluncertainty would be enough to convince the Bank to trim rates. However, withCanadian core inflation grinding up to a cycle high (of 2.1% y/y last month), householdborrowing beginning to stir again, and the loonie reasonably well-behaved, the casefor a BoC rate cut has vanished, at least for now. Even looking all the way through2020, markets are now priced for less than half a rate cut. That compares with roughly60 bps of additional Fed trims, including still-high odds of a move on October 30.

As we have long pointed out, a Fed cut in two weeks’ time, along with an on-holdBoC that same day, will leave Canada with the highest overnight rate in the advancedworld. Accordingly, Canadian two-year yields at 1.65% are also the highest among 22countries surveyed. In the past six months, Canadian short-term yields have barelybudged, even as others were plunging all around them. This factor alone helps explainthe primary talent of Mr. Loonie—to keep its calm amid a turbulent global backdrop aswell as a complete election toss-up.

Appearing on a panel of Chief Economists earlier this week, I was assigned a varietyof puff-ball questions, ranging from: 1) thoughts on negative interest rates (“anabomination”, see the Focus Feature); 2) implications of an inverted yield curve (“it’sdifferent this time, and it’s no longer inverted”); and 3) thoughts on the U.S. budgetdeficit (“how I learned to stop worrying and love the debt bomb”). But the finalone was a bit trickier, and it’s an issue many have been grappling with for much ofthis year—how can you explain the solid gains in equities amid massive geopoliticaluncertainty, trade wars, and a slowing global economy? To wit, the all-world MSCI is upalmost 16% this year, battling for the second best year of the decade (it’s going to betough to top 2013’s 22% rise).

The answer is two-fold: 1) we have to remember where we started the year—comingoff a horrendous Q4, markets are now basically just back to where they were inSeptember 2018. And, 2) the sudden pivot by central banks—most notably the Fed,of course—has helped slash bond yields and largely countered concerns on the tradefront. But that raises a new question: What do we do for an encore with the Fed likelyto stop easing after this next expected move? That question becomes much morepressing if some of the tentative deals fall through in the days ahead.

Let’s Make a (Trade) Deal

.

Prior to the tentative deals to avoid a hard Brexit and a prolonged GM strike, late lastFriday the U.S. and China struck a deal that could mark the first step toward endingthe 15-month trade war between the two nations. According to the White House, Chinapledges to buy $40- to $50-billion of American farm products each year, more thandoubling its purchases, and will improve intellectual property protections and removerestrictions on foreign financial services firms. In return, the U.S cancelled a planned5-ppt tariff hike to 30% on $250 billion of China’s goods this week. The deal marksa truce and de-escalation in tensions that have been building all year, culminating

October 18, 2019 | Page 3 of 19

Our Thoughts

in the U.S. imposing new and larger tariffs on all of China’s goods by year-end. Theceasefire should bolster business confidence, a welcome development given moreevidence that slowing U.S. job growth is undercutting consumers. The IMF estimatesthat current and announced tariffs will reduce U.S. GDP by about 0.6% by 2020 andChina’s GDP by 2%, in the ballpark of our tallies (0.5% and 1.5%). Though not enoughto trigger a U.S. downturn, the tariffs have only aggravated the impact of fading fiscalstimulus.

However, there are good reasons why the agreement is called a “mini-deal”. First,it still needs to be signed by the two presidents, presumably at the APEC meeting inChile in mid-November. Given how provisional it is (i.e., lacking in details), and howquickly an earlier deal fell apart, this ceasefire could end in a tweet of an eye if Chinafails to comply with U.S. demands. Second, there’s no guarantee that signing the dealwill forestall a planned 15% tariff on about $160 billion of China’s goods on December15, or lead to the rolling back of other tariffs. Third, this is just “phase one” of possiblyseveral deals that will need to be made before the trade dispute is fully resolved. Andthose deals will need to address the U.S.’s core grievances about industrial subsidies,forced technology transfers, and regulation of foreign firms operating in the country,demands that have bipartisan support in Congress.

Given ongoing uncertainty about the trade war—and not just with China; next monthwe will know whether automobiles made outside North America are slapped witha tariff—the mini-deal doesn’t mean much for the Fed. The week brought morenews of economic casualties from the front lines, with the malaise in exportsand manufacturing now seeping into the broader economy via slower job growth.Following disappointing reports on employment and retail sales, a decline in industrialproduction may have been the last straw tipping the FOMC toward trimming ratesfor a third time in as many months on October 30. Policymakers will take special noteof a sharp drop in output of business equipment and slowing production of consumergoods. Beyond this month, the need for additional easing will be influenced by thedirection of trade talks. Should further progress ensue—and that’s our assumption,though we aren’t holding our breath for a speedy resolution—and the economysteadies around potential growth, the Fed will likely shift into neutral gear for a while.But until there is peace, the downside risks won’t cease.

Will Super Saturday be Truly Super?

.

The BoE has “Super Thursday” and now the U.K. Parliament has “Super Saturday”.

They’re “super” in the sense that there is so much to cover off. And Super Saturday,October 19th, will have every member of the British Parliament on hand to debatethe deal made between the EU and PM Boris Johnson. The deal was unanimouslyapproved by the EU leaders and is considered to be final by some officials, thoughnot all. European Commissioner Jean-Claude Juncker’s view that “If we have a deal,we have a deal and there is no need for prolongation” is an opinion shared by FrenchPresident Macron, but is not the last word. In fact, another EU official kept the dooropen to the “possibility of an extension, to be discussed at a later stage—if required”.

But as far as PM Johnson is concerned, if Parliament rejects the deal, which is verypossible, he will not ask for a delay. The Benn Act stipulates that by October 19th, hemust have a deal with the EU (check), and have it approved by Parliament (work in

October 18, 2019 | Page 4 of 19

Our Thoughts

progress). The other parts of the Act say that if there is no deal, then ask for moretime. Well, voilà, le deal. Time to vote, so everyone can move on. Ah, if it were onlythat easy.

Some key points of the proposed agreement:

• Transition period from November 1, 2019 to December 31, 2020 (i.e., 14 months)

• Northern Ireland will be aligned to the EU for four years (starting January 1, 2021).Then, right before the end, Stormont will vote if it wants to stay in that setup. Ifthere’s cross-community support (weighted majority of 60%), then it’ll stay for eightmore years. Otherwise, it is just another four years. This is the part that the DUPdoes not like, as pro-EU parties are the majority in Stormont.

• Specifically, Northern Ireland will be in the EU customs union (so goods can flowfreely… no checks); but, it will be aligned with the U.K. customs territory and willpartake in new free trade deals that Britain signs.

• If Northern Ireland votes to leave the EU customs union, there will be a 2-yeartimeframe to figure out how it will happen; ensuring no hard border, etc. Is it me ordoes it sound like it could potentially be Brexit Part Deux?

Will PM Johnson get enough support? Who knows? No matter which way thevote goes, it will be a slim margin (for or against). And it doesn’t help that theConservatives do not have a majority. Parliament has 650 seats, so he needs aminimum of 318 votes (not 326 due to some exclusions). The seat count breakdownis as follows (roughly): 288 Conservative Party members (there were 309 by 21 wereexpelled), 244 Labour Party, 35 SNP, 15 Independent, 19 Liberal Democrats, 10 DUP, andthe rest are under 10. Assume most, but not all, of his Conservatives will vote for thedeal; assume most, but not all, of Labour will vote against the deal (Jeremy Corbyn is“unhappy” with it but the BBC says 10 will support it), and the DUP has stated that itdoes not have its support because it will weaken the bonds between Northern Irelandand the rest of the U.K. Actually, in the words of Nigel Dodds, the DUP’s deputy leader,the deal “drives a coach and horses through the Good Friday Agreement” and BorisJohnson was “too eager” in his efforts to land this deal. There are hard-core Brexiteerswho may vote for the deal because it will finally allow the country to leave the EU,and there are some who feel that it is not good enough. In other words, it will bechallenging and will require lots of convincing and likely some promises to get to318. And many in the Opposition may want to hold a referendum on the deal, and anelection. “Put it to the people!”

This is a very difficult one to call. So if the deal is voted down, is that it? The DUPfeels it is not. But the EU is clearly ready to move on… it has been ready for a longtime. Once again, let us be reminded that it takes two to tango… you can ask for anextension, but you may be told no. You can make a deal, but it needs to be supported.You get the drill.

October 18, 2019 | Page 5 of 19

Our Thoughts

Complacency Setting In?

.

The Bank of Canada’s policy announcement is two weeks away, and there’s little doubtpolicy rates will be on hold. Indeed, we dropped our call for a rate cut earlier thisweek, acknowledging that the facts have changed since initially calling for the Bankto ease. Over the past couple of weeks, we’ve seen the makings of a U.S./China tradedeal and a possible Brexit deal, easing two significant sources of downside risk. Weremain skeptical that the trade deal will quickly end the war (see Sal’s Thought), butfriendly talk is better than the alternative and lessens near-term downside risks.

Despite the good news, we have yet to see the impact of the September tariffs on theglobal economy, as those figures are just starting to roll in. China’s Q3 GDP deceleratedto the slowest pace since at least 1993, global PMIs suggest growth continues todecelerate broadly, and the drop in U.S. September retail sales is worrying. Meantime,Canada continues to skate by with seemingly no impact from the global turmoil. It’shard to believe that a country where exports account for over 30% of GDP will remainunscathed by a much weaker global backdrop. And, domestically, Canada is hardlyrobust with domestic demand barely expanding in the year to Q2.

There are some positives though, and the labour market is the most obvious one.Employment is growing at the best pace in the decade, though hours worked areexpanding at about half the pace, suggesting conditions aren’t as strong as theyappear. The Canadian data have been resilient generally, and core CPI is right ontarget, making the BoC one of the only central banks that can make that claim.

Those factors and the positive global developments have slashed BoC rate cut odds,with less than 20 bps in easing priced by the end of 2020. This compares with 60 bpspriced for the Fed over the same period. That’s pushed Canada 2-year and 5-year bondyields above comparable U.S. Treasury yields for the first time since 2017. Marketsappear to be pricing in an extremely benign outcome for Canada. Are markets beingtoo complacent?

Eye on Earnings

.

The Q3 earnings season got off to a solid start this week, with a few big names toppingexpectations. This comes as the S&P 500 is flirting with a record high. Expectationsare currently for a 3% y/y dip in S&P 500 earnings, according to Thomson Reuters’tally, weighed down by deep declines in energy and materials—ex-energy earningsare only expected to be about flat, as there’s not much growth elsewhere. While theexpectations profile has flattened out in recent months, growth is expected to pick upto +3.5% y/y in 2019Q4, and then spring back to double digits for calendar 2020. Is thattoo optimistic? Not necessarily, but a few things will have to go right. Here are somekey macro drivers of U.S. profit growth and how they fare right now:

Factory activity: In a nutshell, not good. The trade war has taken its hardest tollhere, and M&E investment has stalled. While we think this sector will turn aroundsomewhat in the year ahead, we are only calling for low single-digit growth in realM&E investment through 2020. Meantime, the factory ISM is a very good indicatorof earnings growth, and that picture doesn’t look good. We’ll need a meaningfulbounceback on this front to drive a pickup in earnings.

October 18, 2019 | Page 6 of 19

Our Thoughts

Yield curve: Generally, a steepening yield curve supports stronger earnings growth,especially for financials. It’s also an indication of broader economic strength. Of course,recent activity has inverted the U.S. yield curve, which is not positive for the earningsoutlook. If there’s a saving grace here, it’s that two (maybe three) Fed rate cuts havehelped turn the curve positive again, which could be an indication that the cycle canrun on a bit longer still.

The big dollar: A stronger dollar correlates well with weaker USD-reported revenuesand earnings. Currently, the currency is acting as a drag on earnings growth, with thetrade-weighted dollar rising steadily since early-2018 and only this week showing signsof letting up. This is magnified by the fact that an increasing share of S&P 500 profitscomes from overseas, but potentially dampened by any hedging activity.

Oil prices: The emergence of the U.S. energy sector has made oil prices an importantdriver of S&P 500 earnings growth. In fact, there’s been a near-90% correlation overthe past eight years, versus a negligible relationship through the 1990s and about 25%through the 2000s. Looking ahead, we see WTI as remaining rangebound, and actuallydown slightly in calendar 2020.

The mighty consumer: Consumer spending slowed sharply early in the year, whichhas been a drag on earnings growth. Momentum has firmed recently, which is goodnews, but durable goods spending is the best driver of earnings growth, and we’re notoverly bullish going forward. Credit growth has firmed alongside the drop in interestrates, as has housing, but auto sales have long since peaked.

All told, the macro backdrop will probably have to improve from here in order to hitcurrent earnings expectations. That’s not out of the realm of possibility if Fed rate cutscontinue to do their work, and a trade deal becomes reality.

October 18, 2019 | Page 7 of 19

Recap

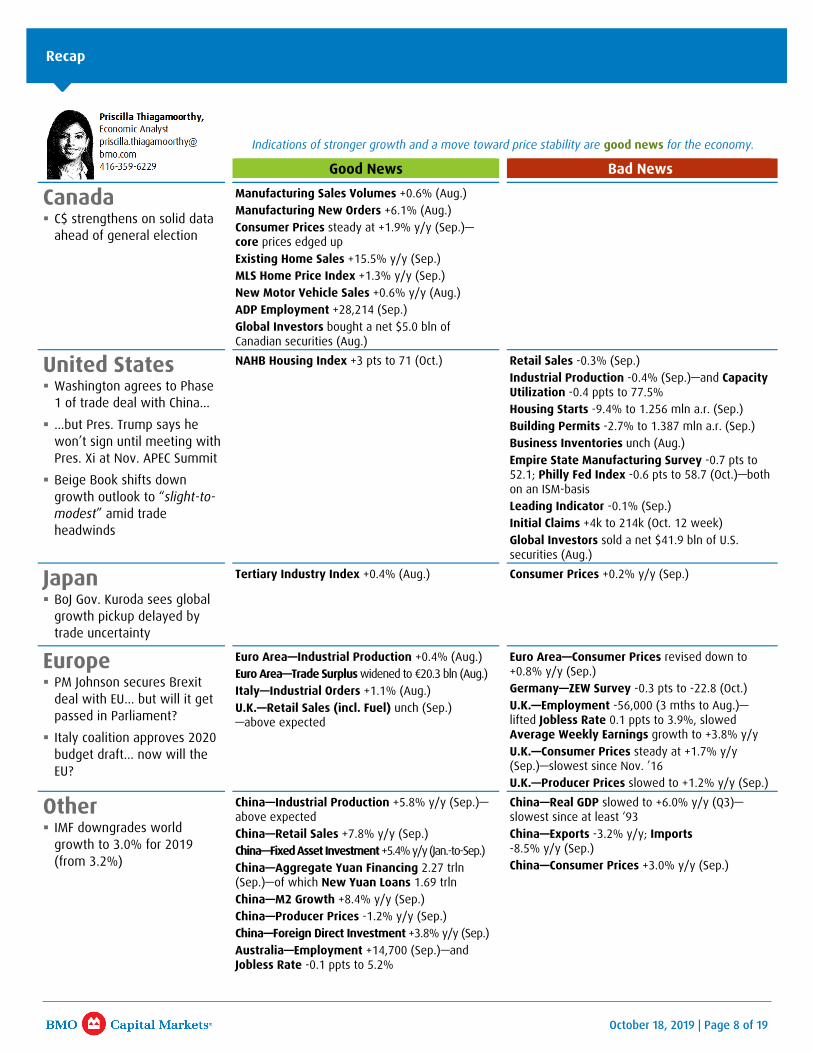

Indications of stronger growth and a move toward price stability are good news for the economy.

Good News Bad News

Canada C$ strengthens on solid data

ahead of general election

Manufacturing Sales Volumes +0.6% (Aug.) Manufacturing New Orders +6.1% (Aug.) Consumer Prices steady at +1.9% y/y (Sep.)—core prices edged up Existing Home Sales +15.5% y/y (Sep.) MLS Home Price Index +1.3% y/y (Sep.) New Motor Vehicle Sales +0.6% y/y (Aug.) ADP Employment +28,214 (Sep.) Global Investors bought a net $5.0 bln of Canadian securities (Aug.)

United States Washington agrees to Phase

1 of trade deal with China…

…but Pres. Trump says he won’t sign until meeting with Pres. Xi at Nov. APEC Summit

Beige Book shifts down growth outlook to “slight-to-modest” amid trade headwinds

NAHB Housing Index +3 pts to 71 (Oct.)

Retail Sales -0.3% (Sep.) Industrial Production -0.4% (Sep.)—and Capacity Utilization -0.4 ppts to 77.5% Housing Starts -9.4% to 1.256 mln a.r. (Sep.) Building Permits -2.7% to 1.387 mln a.r. (Sep.) Business Inventories unch (Aug.) Empire State Manufacturing Survey -0.7 pts to 52.1; Philly Fed Index -0.6 pts to 58.7 (Oct.)—both on an ISM-basis Leading Indicator -0.1% (Sep.) Initial Claims +4k to 214k (Oct. 12 week) Global Investors sold a net $41.9 bln of U.S. securities (Aug.)

Japan BoJ Gov. Kuroda sees global

growth pickup delayed by trade uncertainty

Tertiary Industry Index +0.4% (Aug.)

Consumer Prices +0.2% y/y (Sep.)

Europe PM Johnson secures Brexit

deal with EU… but will it get passed in Parliament?

Italy coalition approves 2020 budget draft... now will the EU?

Euro Area—Industrial Production +0.4% (Aug.) Euro Area—Trade Surplus widened to €20.3 bln (Aug.) Italy—Industrial Orders +1.1% (Aug.) U.K.—Retail Sales (incl. Fuel) unch (Sep.) —above expected

Euro Area—Consumer Prices revised down to +0.8% y/y (Sep.) Germany—ZEW Survey -0.3 pts to -22.8 (Oct.) U.K.—Employment -56,000 (3 mths to Aug.)—lifted Jobless Rate 0.1 ppts to 3.9%, slowed Average Weekly Earnings growth to +3.8% y/y U.K.—Consumer Prices steady at +1.7% y/y (Sep.)—slowest since Nov. ’16 U.K.—Producer Prices slowed to +1.2% y/y (Sep.)

Other IMF downgrades world

growth to 3.0% for 2019 (from 3.2%)

China—Industrial Production +5.8% y/y (Sep.)—above expected China—Retail Sales +7.8% y/y (Sep.) China—Fixed Asset Investment +5.4% y/y (Jan.-to-Sep.) China—Aggregate Yuan Financing 2.27 trln (Sep.)—of which New Yuan Loans 1.69 trln China—M2 Growth +8.4% y/y (Sep.) China—Producer Prices -1.2% y/y (Sep.) China—Foreign Direct Investment +3.8% y/y (Sep.) Australia—Employment +14,700 (Sep.)—and Jobless Rate -0.1 ppts to 5.2%

China—Real GDP slowed to +6.0% y/y (Q3)—slowest since at least ‘93 China—Exports -3.2% y/y; Imports -8.5% y/y (Sep.) China—Consumer Prices +3.0% y/y (Sep.)

October 18, 2019 | Page 8 of 19

Feature

Too Negative Rates Don’t Make a Positive

.

“Negative interest rates may be an effective monetary policy tool to help easefinancial conditions” — SF Fed Economist Jens Christensen.

“I don’t think it would be one of the first things we would do” — Neel Kashkari

“Negative rates are “unattractive” for the U.S.” — Lael Brainard

“I do not think we would be looking at using negative rates.” — Jay Powell

“The Federal Reserve should get our rates down to ZERO, or less” — President Trump.

With the Fed poised to ease policy again late thismonth and recession chatter in the air, the possibilityof negative interest rates is suddenly back on the radarscreen. The Wall Street Journal pointed out this weekthat options trading in Eurodollars suggest that “negativerates are not just possible, but reasonably probable”,while a paper from the San Francisco Fed added anapproving nod for such a policy. And, as far back as2015, BoC Governor Stephen Poloz suggested in a speechthat the Bank now views the low-end threshold forits overnight rate as -0.50%, rather than the previouslow of +0.25%. The debate, of course, is not whethernegative rates are possible—they are already a prominentfeature for many advanced country central banksand government bond markets (Chart 1). The debateis whether they are an appropriate monetary policyresponse, especially in North America.

.

How did we get here?The depth of the 2008/09 downturn, combined withthe lengthy workout period and near-absent inflationpressures, prompted new and aggressive actions by avariety of central banks. From explicit forward guidance,to quantitative easing, to negative policy rates, centralbanks were pushed into many new avenues in recentyears. But overlaying the intense cyclical pressures of thepast decade were monumental secular factors at play aswell. Interest rates broadly have been declining steadilysince their peak in the Fall of 1981 (to paraphrase theTragically Hip, “38 years old, never kissed a bond bear”).While nominal GDP growth doesn’t have a precise anddirect bearing on borrowing costs, it has tended to act asa very strong anchor on equilibrium interest rates overlong stretches of history (Chart 2). It’s no coincidence

.

October 18, 2019 | Page 9 of 19

Feature

that the sustained decline in long-term rates has beenaccompanied by the downward grind in nominal GDPgrowth over that period, reflecting a cooldown in bothinflation and real growth. In turn, the slowdown in thelatter reflects trends in both labour force population andproductivity growth.

If the descent in nominal GDP continues, then it is reasonable to assume that the entirespectrum of interest rates will reset lower as well. Note that the underlying trendin U.S. nominal GDP since 2007 of 3.3% annualized is actually near the high end ofthe developed world. Over that same stretch, Canada posted 3.2% growth, the U.K.3.1%, the Euro Area 2.0%, Switzerland 1.7% and Japan just 0.3%. (We have chosena 12-year time period to deliberately include the past recession, to get a full-cycleview.) The much slower pace in Europe and Japan reflects milder inflation, but alsooutright declines in labour force populations, and thus much lower potential growth.Fundamentally, this helps explain why long-term yields are so much lower in thoseregions than in North America.

Looking forward, we don’t anticipate a huge downshift in U.S. or Canadian nominalGDP growth rates from the average pace since 2007. While demographic trends willlikely weigh on labour force population growth rates somewhat, they're not expectedto slow nearly to the same extent as in Europe or Japan. And, there is a case to bemade that productivity could hold up or even improve in the coming decade as AI androbotics are more widely adopted in the service sector. In other words, we suspectthe secular forces at play just won’t become as conducive for negative rates in NorthAmerica as they are in other regions.

October 18, 2019 | Page 10 of 19

Feature

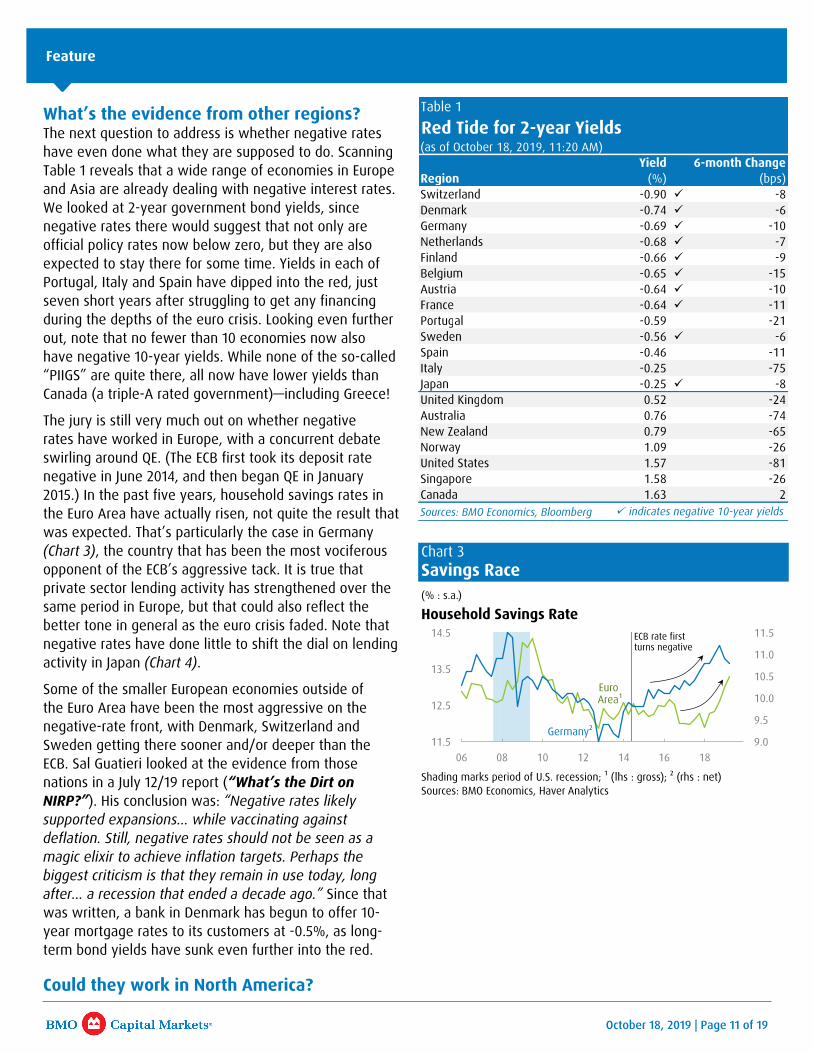

What’s the evidence from other regions?The next question to address is whether negative rateshave even done what they are supposed to do. ScanningTable 1 reveals that a wide range of economies in Europeand Asia are already dealing with negative interest rates.We looked at 2-year government bond yields, sincenegative rates there would suggest that not only areofficial policy rates now below zero, but they are alsoexpected to stay there for some time. Yields in each ofPortugal, Italy and Spain have dipped into the red, justseven short years after struggling to get any financingduring the depths of the euro crisis. Looking even furtherout, note that no fewer than 10 economies now alsohave negative 10-year yields. While none of the so-called“PIIGS” are quite there, all now have lower yields thanCanada (a triple-A rated government)—including Greece!

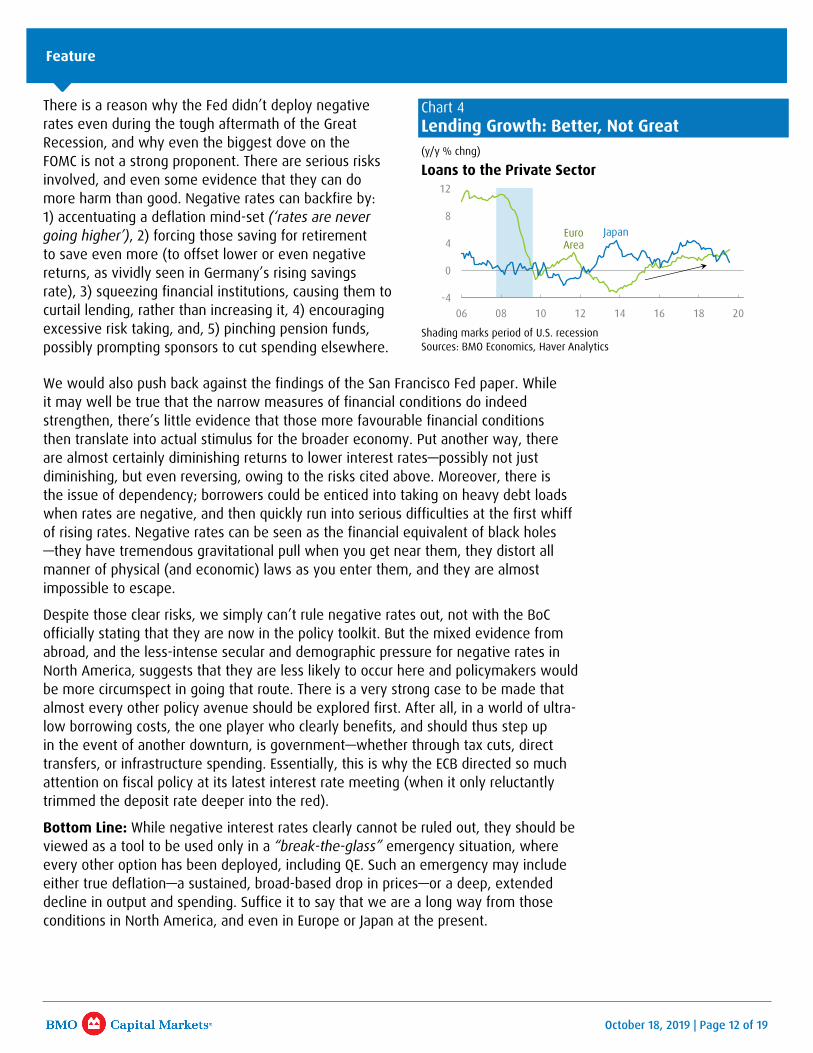

The jury is still very much out on whether negativerates have worked in Europe, with a concurrent debateswirling around QE. (The ECB first took its deposit ratenegative in June 2014, and then began QE in January2015.) In the past five years, household savings rates inthe Euro Area have actually risen, not quite the result thatwas expected. That’s particularly the case in Germany(Chart 3), the country that has been the most vociferousopponent of the ECB’s aggressive tack. It is true thatprivate sector lending activity has strengthened over thesame period in Europe, but that could also reflect thebetter tone in general as the euro crisis faded. Note thatnegative rates have done little to shift the dial on lendingactivity in Japan (Chart 4).

Some of the smaller European economies outside ofthe Euro Area have been the most aggressive on thenegative-rate front, with Denmark, Switzerland andSweden getting there sooner and/or deeper than theECB. Sal Guatieri looked at the evidence from thosenations in a July 12/19 report (“What’s the Dirt onNIRP?”). His conclusion was: “Negative rates likelysupported expansions… while vaccinating againstdeflation. Still, negative rates should not be seen as amagic elixir to achieve inflation targets. Perhaps thebiggest criticism is that they remain in use today, longafter… a recession that ended a decade ago.” Since thatwas written, a bank in Denmark has begun to offer 10-year mortgage rates to its customers at -0.5%, as long-term bond yields have sunk even further into the red.

Could they work in North America?

.

.

October 18, 2019 | Page 11 of 19

Feature

There is a reason why the Fed didn’t deploy negativerates even during the tough aftermath of the GreatRecession, and why even the biggest dove on theFOMC is not a strong proponent. There are serious risksinvolved, and even some evidence that they can domore harm than good. Negative rates can backfire by:1) accentuating a deflation mind-set (‘rates are nevergoing higher’), 2) forcing those saving for retirementto save even more (to offset lower or even negativereturns, as vividly seen in Germany’s rising savingsrate), 3) squeezing financial institutions, causing them tocurtail lending, rather than increasing it, 4) encouragingexcessive risk taking, and, 5) pinching pension funds,possibly prompting sponsors to cut spending elsewhere. .

We would also push back against the findings of the San Francisco Fed paper. Whileit may well be true that the narrow measures of financial conditions do indeedstrengthen, there’s little evidence that those more favourable financial conditionsthen translate into actual stimulus for the broader economy. Put another way, thereare almost certainly diminishing returns to lower interest rates—possibly not justdiminishing, but even reversing, owing to the risks cited above. Moreover, there isthe issue of dependency; borrowers could be enticed into taking on heavy debt loadswhen rates are negative, and then quickly run into serious difficulties at the first whiffof rising rates. Negative rates can be seen as the financial equivalent of black holes—they have tremendous gravitational pull when you get near them, they distort allmanner of physical (and economic) laws as you enter them, and they are almostimpossible to escape.

Despite those clear risks, we simply can’t rule negative rates out, not with the BoCofficially stating that they are now in the policy toolkit. But the mixed evidence fromabroad, and the less-intense secular and demographic pressure for negative rates inNorth America, suggests that they are less likely to occur here and policymakers wouldbe more circumspect in going that route. There is a very strong case to be made thatalmost every other policy avenue should be explored first. After all, in a world of ultra-low borrowing costs, the one player who clearly benefits, and should thus step upin the event of another downturn, is government—whether through tax cuts, directtransfers, or infrastructure spending. Essentially, this is why the ECB directed so muchattention on fiscal policy at its latest interest rate meeting (when it only reluctantlytrimmed the deposit rate deeper into the red).

Bottom Line: While negative interest rates clearly cannot be ruled out, they should beviewed as a tool to be used only in a “break-the-glass” emergency situation, whereevery other option has been deployed, including QE. Such an emergency may includeeither true deflation—a sustained, broad-based drop in prices—or a deep, extendeddecline in output and spending. Suffice it to say that we are a long way from thoseconditions in North America, and even in Europe or Japan at the present.

October 18, 2019 | Page 12 of 19

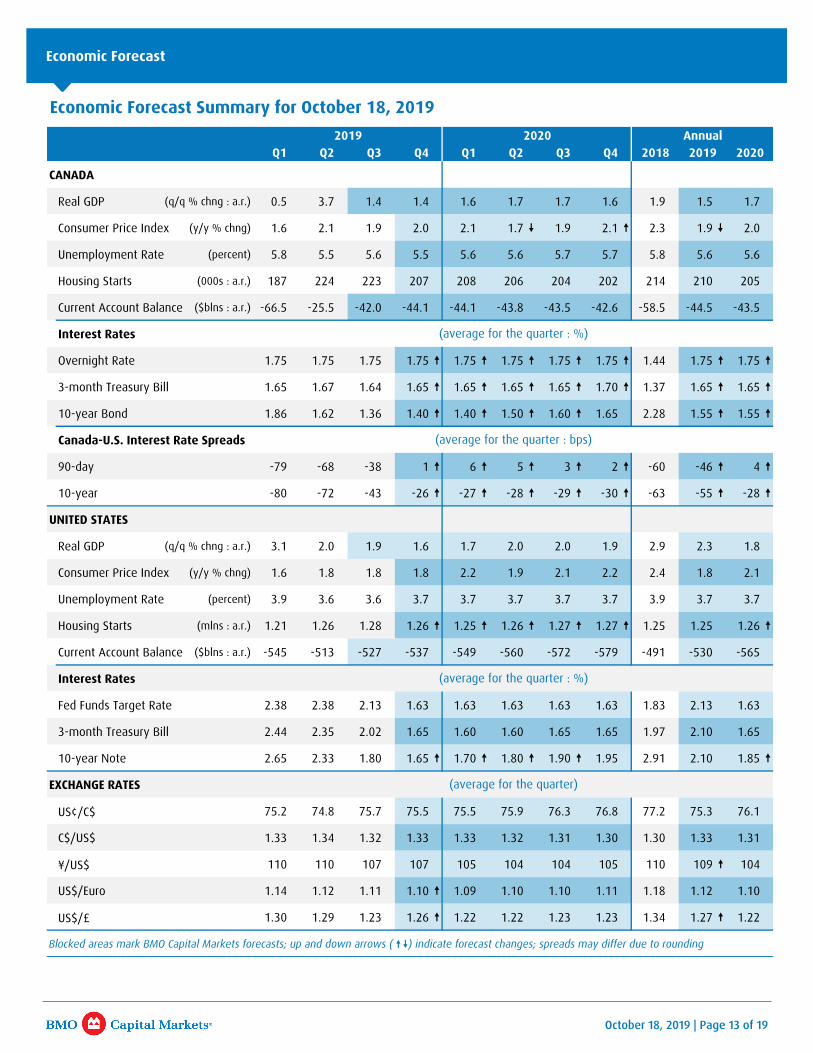

Economic Forecast

.

October 18, 2019 | Page 13 of 19

Key for Next Week

Canada

.

.Canadians head to the polls on October 21st to elect the 43rd Parliament. The polls showit’s a two-way race between the Liberals and Conservatives for who wins the mostseats. That’s been the case consistently since the writ was dropped. However, theNDP have surged over the past couple of weeks, potentially changing the dynamic forwhoever wins the most seats. Indeed, CBC’s Polltracker puts low odds on a majority ofany kind. That could leave the balance of power with the NDP or Bloc Quebecois, butthe polls aren’t always right as we’ve seen in recent years. Any minority result wouldlikely mean uncertainty around the stability of government and a decent probabilitythat Canadians could be headed back to the polls within a year or two. Polls closein most of Canada at 9:30 pm EDT, with the final polls (in B.C.) closing half an hourlater. Given how tight the overall race appears, we may not know until the nextmorning who has officially won; and it could take longer pending recounts. Even then,in the event of a minority government, it could take weeks before parties reach anagreement on who will lead and how.

.

Retail sales look to rise modestly in August, driven largely by a solid gain in autosales. A sharp drop in interest rates has provided a nice boost to autos and home sales.Some calendar quirkiness might have lifted auto sales somewhat, as September sawa sharp pullback in activity. A steep decline in seasonally-adjusted gasoline prices isexpected to provide some offset to the big-ticket items. We’re looking for a modestgain in sales excluding autos and gas, consistent with a debt-constrained consumer.With goods prices lower (thanks largely to gasoline), volumes will likely see a decentgain, perhaps the best since March.

.

The Bank of Canada’s Fall Business Outlook Survey (BOS), likely compiled fromlate August into September, is expected to show continued apprehension about theoutlook. Recall that the summer survey saw the BOS indicator rebound from the largestdeterioration since the crisis. Following a string of solid economic data and a blowoutQ2 GDP report, the Canadian economy has slowed. That suggests sales expectationswill soften from the prior survey’s two-year high. There was extreme market volatilitythrough that period, with markets very pessimistic in August, then starting a completereversal post-Labour Day.

Employment has been a strong spot for Canada, with gains running at the fastest pacein over a decade facilitated by strong population growth. While there’s no denying thelabour market is solid, hours worked suggests conditions aren’t quite as firm as thejobs data would lead you to believe. Look for hiring expectations to hold about steadyfrom the summer. Meantime, business investment intentions face some downside riskafter holding above the long-run average for the past few years. Global uncertaintyand sluggish domestic demand could make Canadian businesses a bit more reluctantto invest. And, credit conditions in the BOS and Senior Loan Officer Survey should staypretty loose amid easing financial conditions.

October 18, 2019 | Page 14 of 19

Key for Next Week

United States

. .

.

The housing market has caught a second wind on the back of plunging mortgagerates, but slowing job growth could be taking a toll. After sprinting higher, newmortgage applications have cooled since the summer. In September, the GM strikeand hurricanes likely depressed sales. So, after hitting 1½-year highs, existing homesales look to retreat 0.7% to 5.45 million units annualized. The earlier sprint soaked upsupply, leaving a lean 4.1 months of listings (at the current sales pace) compared witha more typical six. Similarly, new home sales are expected to retrace 2% to 699,000units after spiking 7.1% in August. (But they could rebound in October according to theNAHB homebuilders' survey which is nearing cycle highs.) Demand appears firmer fornew rather than used homes. Supply is somewhat more plentiful in the new market(5.5 months), and builders are trying to hold down prices. While the median price of asingle-family new home has steadied this year, growth in resale prices remains above4% y/y. Buyers likely see better value in new homes as the spread between the twomarkets has narrowed to $45,000 (on average) this year from $71,000 in the priorseven years. This bodes well for residential construction, which likely broke a string ofsix quarterly declines in Q3.

.

The GM strike, which began mid-September and continued through the remainder ofthe month, will drive total durable goods orders down 1.4%. The rebound in Boeingorders, to 25 aircraft from 6 in August, will provide only a partial offset as this was stillthe weakest September tally in a decade. Excluding the transportation sector, durablegoods orders should be flat, reflecting capex caution owing to the escalating U.S./Chinatrade war. September began with a new 15% tariff on about $112 billion of Chinesegoods and China retaliated. However this caution is being partly countered by outlayson durable items related to oil production (which averaged a record high 12.6 mln bpdin the month), along with equipment purchases designed to address labour shortages.Core capital goods orders should dip 0.1%, failing to advance for a third straight month.

Central Banks

.

.

The ECB is meeting on Thursday. Given what happened at the last meeting (bigpackage!), no changes to policy are expected this time around. It is only noteworthyas this will be Mario Draghi's final meeting as ECB President. He will pass thereins over to Christine Lagarde (the EU leaders officially gave her the green light). Shecertainly has her work cut out for her, given that there is plenty of unrest within theranks. She has promised to review the central bank's policy framework and some areurging a review on current policy, and possibly a change to the inflation target.

October 18, 2019 | Page 15 of 19

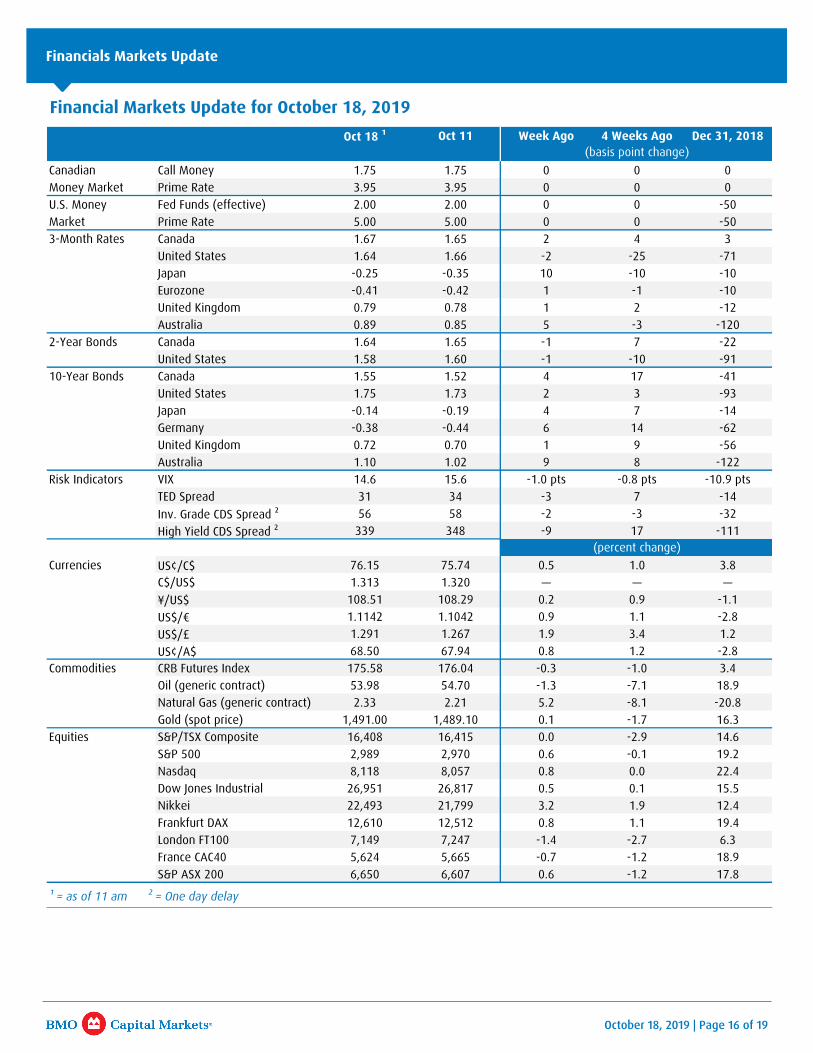

Financials Markets Update

.

October 18, 2019 | Page 16 of 19

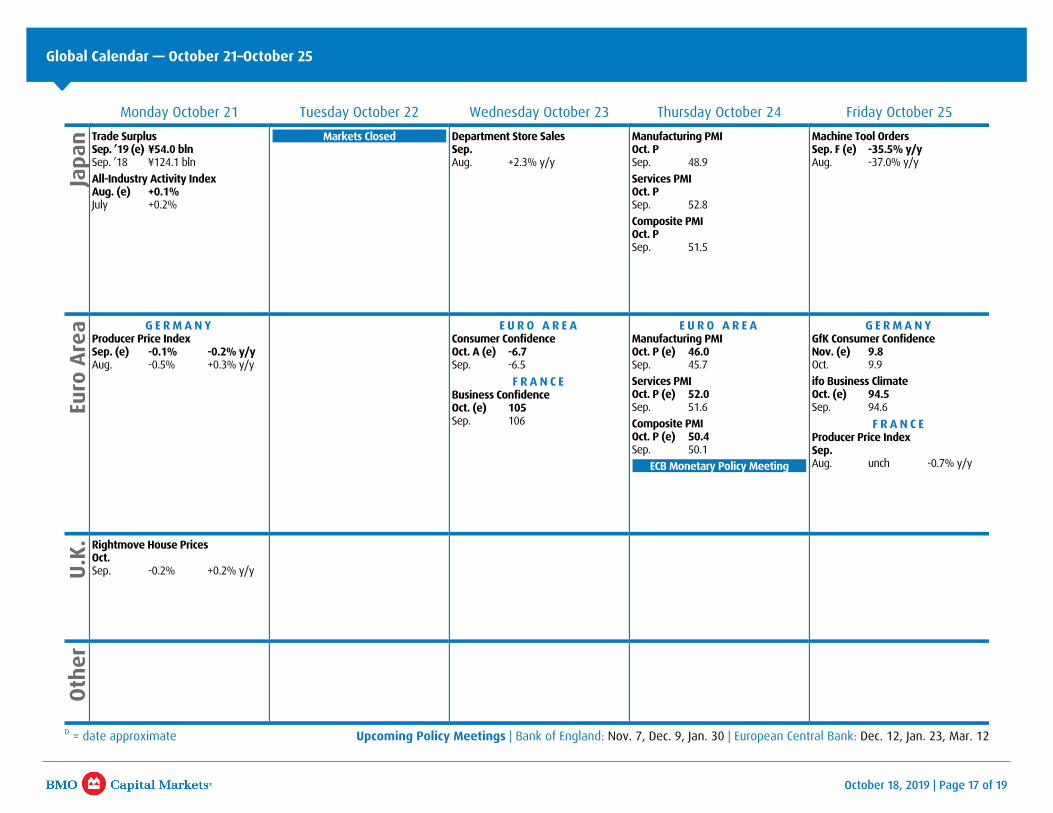

Global Calendar — October 21–October 25

Monday October 21 Tuesday October 22 Wednesday October 23 Thursday October 24 Friday October 25

Japa

n Trade Surplus Sep. ’19 (e) ¥54.0 bln Sep. ’18 ¥124.1 bln All-Industry Activity Index Aug. (e) +0.1% July +0.2%

Markets Closed Department Store Sales Sep. Aug. +2.3% y/y

Manufacturing PMI Oct. P Sep. 48.9 Services PMI Oct. P Sep. 52.8 Composite PMI Oct. P Sep. 51.5

Machine Tool Orders Sep. F (e) -35.5% y/y Aug. -37.0% y/y

Euro

Are

a G E R M A N Y Producer Price Index Sep. (e) -0.1% -0.2% y/y Aug. -0.5% +0.3% y/y

E U R O A R E A Consumer Confidence Oct. A (e) -6.7 Sep. -6.5

F R A N C E Business Confidence Oct. (e) 105 Sep. 106

E U R O A R E A Manufacturing PMI Oct. P (e) 46.0 Sep. 45.7 Services PMI Oct. P (e) 52.0 Sep. 51.6 Composite PMI Oct. P (e) 50.4 Sep. 50.1

ECB Monetary Policy Meeting

G E R M A N Y GfK Consumer Confidence Nov. (e) 9.8 Oct. 9.9 ifo Business Climate Oct. (e) 94.5 Sep. 94.6

F R A N C E Producer Price Index Sep. Aug. unch -0.7% y/y

U.K.

Rightmove House Prices Oct. Sep. -0.2% +0.2% y/y

Othe

r

D = date approximate Upcoming Policy Meetings | Bank of England: | European Central Bank: Dec. 12, Jan. 23, Mar. 12Nov. 7, Dec. 9, Jan. 30

October 18, 2019 | Page 17 of 19

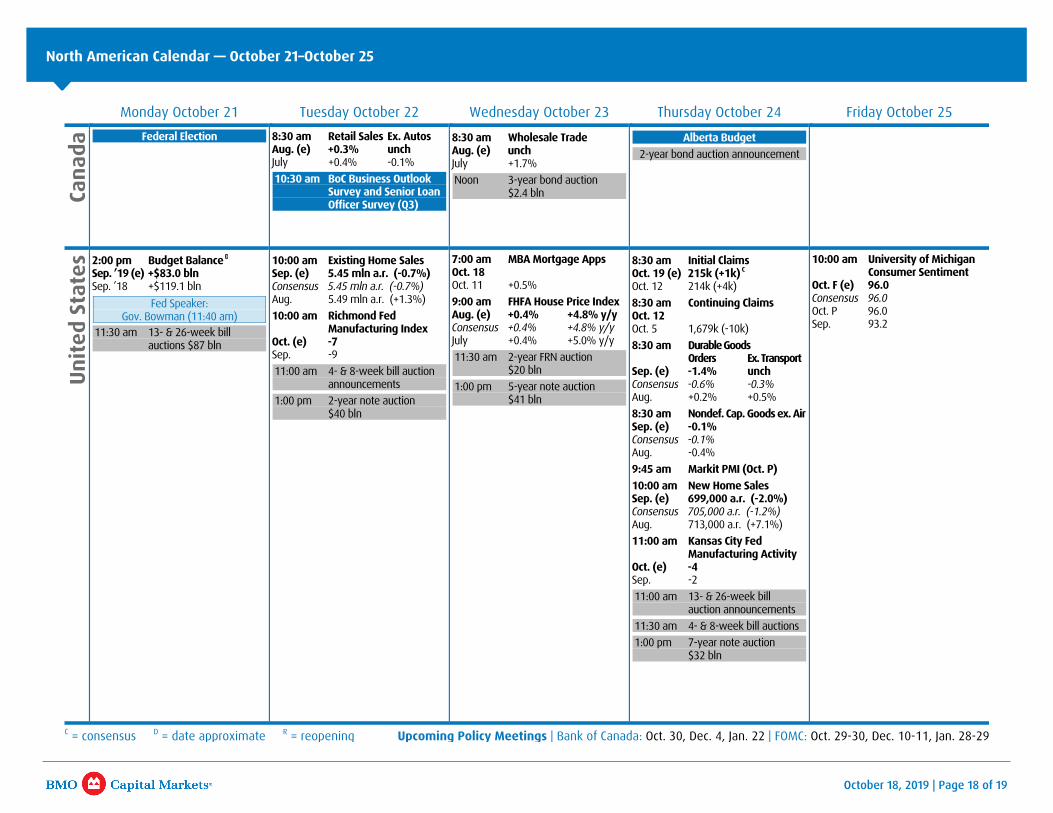

North American Calendar — October 21–October 25

Monday October 21 Tuesday October 22 Wednesday October 23 Thursday October 24 Friday October 25

Cana

da

Federal Election 8:30 am Retail Sales Ex. Autos Aug. (e) +0.3% unch July +0.4% -0.1% 10:30 am BoC Business Outlook

Survey and Senior Loan Officer Survey (Q3)

8:30 am Wholesale Trade Aug. (e) unch July +1.7% Noon 3-year bond auction

$2.4 bln

Alberta Budget

2-year bond auction announcement

Unite

d St

ates

2:00 pm Budget Balance D Sep. ’19 (e) +$83.0 bln Sep. ’18 +$119.1 bln

Fed Speaker: Gov. Bowman (11:40 am)

11:30 am 13- & 26-week bill auctions $87 bln

10:00 am Existing Home Sales Sep. (e) 5.45 mln a.r. (-0.7%) Consensus 5.45 mln a.r. (-0.7%) Aug. 5.49 mln a.r. (+1.3%) 10:00 am Richmond Fed

Manufacturing Index Oct. (e) -7 Sep. -9 11:00 am 4- & 8-week bill auction

announcements

1:00 pm 2-year note auction $40 bln

7:00 am MBA Mortgage Apps Oct. 18 Oct. 11 +0.5% 9:00 am FHFA House Price Index Aug. (e) +0.4% +4.8% y/y Consensus +0.4% +4.8% y/y July +0.4% +5.0% y/y 11:30 am 2-year FRN auction

$20 bln

1:00 pm 5-year note auction $41 bln

8:30 am Initial Claims Oct. 19 (e) 215k (+1k) C Oct. 12 214k (+4k) 8:30 am Continuing Claims Oct. 12 Oct. 5 1,679k (-10k) 8:30 am Durable Goods

Orders Ex. Transport Sep. (e) -1.4% unch Consensus -0.6% -0.3% Aug. +0.2% +0.5% 8:30 am Nondef. Cap. Goods ex. Air Sep. (e) -0.1% Consensus -0.1% Aug. -0.4% 9:45 am Markit PMI (Oct. P)

10:00 am New Home Sales Sep. (e) 699,000 a.r. (-2.0%) Consensus 705,000 a.r. (-1.2%) Aug. 713,000 a.r. (+7.1%) 11:00 am Kansas City Fed

Manufacturing Activity Oct. (e) -4 Sep. -2 11:00 am 13- & 26-week bill

auction announcements

11:30 am 4- & 8-week bill auctions

1:00 pm 7-year note auction $32 bln

10:00 am University of Michigan Consumer Sentiment

Oct. F (e) 96.0 Consensus 96.0 Oct. P 96.0 Sep. 93.2

C = consensus D = date approximate R = reopening Upcoming Policy Meetings | Bank of Canada: | FOMC: Oct. 29-30, Dec. 10-11, Jan. 28-29Oct. 30, Dec. 4, Jan. 22

October 18, 2019 | Page 18 of 19

General Disclosures"BMO Capital Markets" is a trade name used by the BMO Investment Banking Group, which includes the wholesale arm of Bank of Montreal and its subsidiaries BMO Nesbitt Burns Inc., BMO Capital Markets Limited inthe U.K., Bank of Montreal Europe Plc in Ireland and BMO Capital Markets Corp. in the U.S. BMO Nesbitt Burns Inc., BMO Capital Markets Limited, Bank of Montreal Europe Plc and BMO Capital Markets Corp are affiliates.BMO does not represent that this document may be lawfully distributed, or that any financial products may be lawfully offered or dealt with, in compliance with any regulatory requirements in other jurisdictions, orpursuant to an exemption available thereunder. This document is directed only at entities or persons in jurisdictions or countries where access to and use of the information is not contrary to local laws or regulations.Their contents have not been reviewed by any regulatory authority. Bank of Montreal or its subsidiaries (“BMO Financial Group”) has lending arrangements with, or provide other remunerated services to, many issuerscovered by BMO Capital Markets. The opinions, estimates and projections contained in this report are those of BMO Capital Markets as of the date of this report and are subject to change without notice. BMO CapitalMarkets endeavours to ensure that the contents have been compiled or derived from sources that we believe are reliable and contain information and opinions that are accurate and complete. However, BMO CapitalMarkets makes no representation or warranty, express or implied, in respect thereof, takes no responsibility for any errors and omissions contained herein and accepts no liability whatsoever for any loss arising fromany use of, or reliance on, this report or its contents. Information may be available to BMO Capital Markets or its affiliates that is not reflected in this report. The information in this report is not intended to be usedas the primary basis of investment decisions, and because of individual client objectives, should not be construed as advice designed to meet the particular investment needs of any investor. This document is notto be construed as an offer to sell, a solicitation for or an offer to buy, any products or services referenced herein (including, without limitation, any commodities, securities or other financial instruments), nor shallsuch Information be considered as investment advice or as a recommendation to enter into any transaction. Each investor should consider obtaining independent advice before making any financial decisions. Thisdocument is provided for general information only and does not take into account any investor’s particular needs, financial status or investment objectives. BMO Capital Markets or its affiliates will buy from or sell tocustomers the securities of issuers mentioned in this report on a principal basis. BMO Capital Markets or its affiliates, officers, directors or employees have a long or short position in many of the securities discussedherein, related securities or in options, futures or other derivative instruments based thereon. The reader should assume that BMO Capital Markets or its affiliates may have a conflict of interest and should not relysolely on this report in evaluating whether or not to buy or sell securities of issuers discussed herein.

Dissemination of Economic Publications

Our publications are disseminated via email and may also be available via our web site https://economics.bmo.com. Please contact your BMO Financial Group Representative for more information.

Additional Matters

This report is directed only at entities or persons in jurisdictions or countries where access to and use of the information is not contrary to local laws or regulations. Its contents have not been reviewed by anyregulatory authority. BMO Capital Markets does not represent that this report may be lawfully distributed or that any financial products may be lawfully offered or dealt with, in compliance with regulatoryrequirements in other jurisdictions, or pursuant to an exemption available thereunder.

To Australian residents: BMO Capital Markets Limited is exempt from the requirement to hold an Australian financial services licence under the Corporations Act and is regulated by the UK Financial Conduct Authorityunder UK laws, which differ from Australian laws. This document is only intended for wholesale clients (as defined in the Corporations Act 2001) and Eligible Counterparties or Professional Clients (as defined in AnnexII to MiFID II).

To Canadian Residents: BMO Nesbitt Burns Inc. furnishes this report to Canadian residents and accepts responsibility for the contents herein subject to the terms set out above. Any Canadian person wishing to effecttransactions in any of the securities included in this report should do so through BMO Nesbitt Burns Inc.

To U.K./E.U. Residents: In the UK, Bank of Montreal London Branch is authorised and regulated by the Prudential Regulation Authority and the Financial Conduct Authority (“FCA”) and BMO Capital Markets Limitedis authorised and regulated by the FCA. The contents hereof are intended solely for clients which satisfy the criteria for classification as either a “professional client” or an “eligible counterparty”, each as defined inDirective 2014/65/EU (“MiFID II”). Any U.K. person wishing to effect transactions in any security discussed herein should do so through Bank of Montreal, London Branch or BMO Capital Markets Limited; any personin the E.U. wishing to effect transactions in any security discussed herein should do so through BMO Capital Markets Limited. In the UK this document is published by BMO Capital Markets Limited which is authorisedand regulated by the Financial Conduct Authority. The contents hereof are intended solely for the use of, and may only be issued or passed on to, (I) persons who have professional experience in matters relating toinvestments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Order") or (II) high net worth entities falling within Article 49(2)(a) to (d) of the Order (allsuch persons together referred to as "relevant persons"). The contents hereof are not intended for the use of and may not be issued or passed on to retail clients.In an E.U. Member State this document is issued anddistributed by Bank of Montreal Europe plc which is authorised and regulated in Ireland and operates in the E.U. on a passported basis. This document is only intended for Eligible Counterparties or Professional Clients,as defined in Annex II to “Markets in Financial Instruments Directive” 2014/65/EU (“MiFID II”).

To Hong Kong Residents: This document is issued and distributed in Hong Kong by Bank of Montreal (“BMO”). BMO is an authorized institution under the Banking Ordinance (Chapter 155 of the Laws of Hong Kong)and a registered institution with the Securities and Futures Commission (CE No. AAK809) under the Securities and Futures Ordinance (Chapter 571 of the Laws of Hong Kong). This material has not been reviewed orapproved by any regulatory authority in Hong Kong. Accordingly the material must not be issued, circulated or distributed in Hong Kong other than (1) except for "structured products" as defined in the Securities andFutures Ordinance, in circumstances which do not constitute it as a “Prospectus” as defined in the Companies Ordinance or which do not constitute an offer to the public within the meaning of that Ordinance, or (2) toProfessional investors as defined in the Securities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules made thereunder. Unless permitted by the securities laws of Hong Kong, no personmay issue in Hong Kong, or have in its possession for issue in Hong Kong this material or any other advertisement, invitation or document relating to the products other than to a professional investor as defined theSecurities and Futures Ordinance and the Securities and Futures (Professional Investor) Rules.

To Korean Residents: This material is not provided to make a recommendation for specific Korean residents to enter into a contract for trading financial investment instruments, for investment advising, fordiscretionary investment, or for a trust, nor does it constitute advertisement of any financial business or financial investment instruments towards Korean residents. The material is not provided as advice on the valueof financial investment instruments or any investment decision for specific Korean residents. The provision of the material does not constitute engaging in the foreign exchange business or foreign exchange brokeragebusiness regulated under the Foreign Exchange Transactions Act of Korea.

To PRC Residents: This material does not constitute an offer to sell or the solicitation of an offer to buy any financial products in the People’s Republic of China (excluding Hong Kong, Macau and Taiwan, the “PRC”).BMO and its affiliates do not represent that this material may be lawfully distributed, or that any financial products may be lawfully offered, in compliance with any applicable registration or other requirements inthe PRC, or pursuant to an exemption available thereunder, or assume any responsibility for facilitating any such distribution or offering. This material may not be distributed or published in the PRC, except undercircumstances that will result in compliance with any applicable laws and regulations.

Singapore Residents: This document has not been registered as a prospectus with the Monetary Authority of Singapore and the material does not constitute an offer or sale, solicitation or invitation for subscription orpurchase of any shares or financial products in Singapore. Accordingly, BMO and its affiliates do not represent that this document and any other materials produced in connection therewith may lawfully be circulatedor distributed, whether directly or indirectly, to persons in Singapore. This document and the material do not and are not intended to constitute the provision of financial advisory services, whether directly or indirectly,to persons in Singapore. This document and any information contained in this report shall not be disclosed to any other person. If you are not an accredited investor, please disregard this report. BMO Singapore Branchdoes not accept legal responsibility for the contents of the report. In Asia, Bank of Montreal is licensed to conduct banking and financial services in Hong Kong and Singapore. Certain products and services referred toin this document are designed specifically for certain categories of investors in a number of different countries and regions. Such products and services would only be offered to these investors in those countries andregions in accordance with applicable laws and regulations. The Information is directed only at persons in jurisdictions where access to and use of such information is lawful.

To Thai Residents: The contents hereof are intended solely for the use of persons qualified as Institutional Investors according to Notification of the Securities and Exchange Commission No. GorKor. 11/2547 Re:Characteristics of Advice which are not deemed as Conducting Derivatives Advisory Services dated 23 January 2004 (as amended). BMO and its affiliates do not represent that the material may be lawfully distributed,or that any financial products may be lawfully offered, in compliance with any regulatory requirements in Thailand, or pursuant to an exemption available under any applicable laws and regulations.

To U.S. Residents: BMO Capital Markets Corp. furnishes this report to U.S. residents and accepts responsibility for the contents herein, except to the extent that it refers to securities of Bank of Montreal.

These documents are provided to you on the express understanding that they must be held in complete confidence and not republished, retransmitted, distributed, disclosed, or otherwise made available, in whole orin part, directly or indirectly, in hard or soft copy, through any means, to any person, except with the prior written consent of BMO Capital Markets.

ADDITIONAL INFORMATION IS AVAILABLE UPON REQUEST

BMO Financial Group (NYSE, TSX: BMO) is an integrated financial services provider offering a range of retail banking, wealth management, and investment and corporate banking products. BMO serves Canadian retailclients through BMO Bank of Montreal and BMO Nesbitt Burns. In the United States, personal and commercial banking clients are served by BMO Harris Bank N.A., (Member FDIC). Investment and corporate bankingservices are provided in Canada and the US through BMO Capital Markets.

BMO Capital Markets is a trade name used by BMO Financial Group for the wholesale banking businesses of Bank of Montreal, BMO Harris Bank N.A, (Member FDIC), Bank of Montreal Europe Plc, and Bank of Montreal(China) Co. Ltd. and the institutional broker dealer businesses of BMO Capital Markets Corp. (Member FINRA and SIPC) in the U.S., BMO Nesbitt Burns Inc. (Member Canadian Investor Protection Fund) in Canada, Europeand Asia, Bank of Montreal Europe Plc in Europe, BMO Capital Markets Limited in the U.K. and Australia and BMO Advisors Private Limited in India.

® Registered trademark of Bank of Montreal in the United States, Canada and elsewhere.

™ Trademark Bank of Montreal in the United States and Canada.

© COPYRIGHT 2020 BMO CAPITAL MARKETS CORP.

A member of BMO Financial Group

October 18, 2019 | Page 19 of 19