Embed Size (px)

Citation preview

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 1/9

LATVIA

Tax facts 2012

Corporate income tax • Withholding taxes

• Value added tax • Customs and excise duties

• Capital gains • Natural resources tax

• Property taxes and property transfer taxes

• Tax on lotteries and games of chance

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 2/9

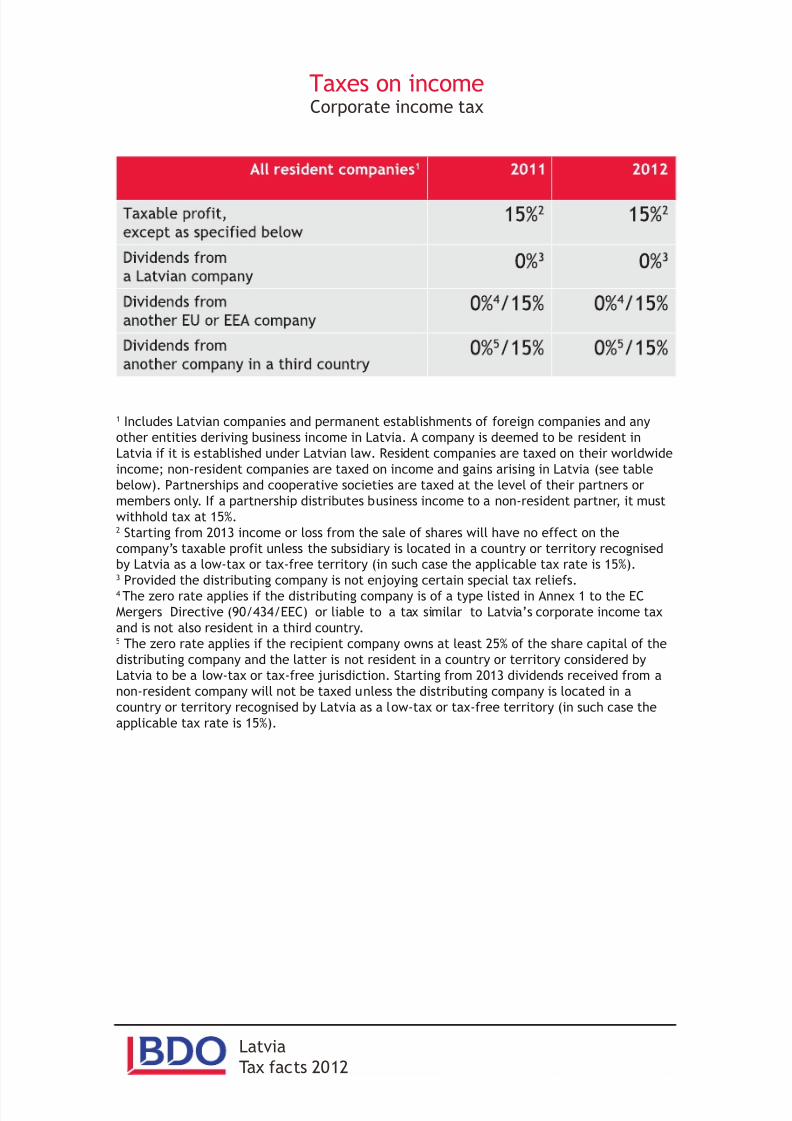

Taxes on incomeCorporate income tax

Latvia

Tax facts 2012

1 Includes Latvian companies and permanent establishments of foreign companies and any

other entities deriving business income in Latvia. A company is deemed to be resident in

Latvia if it is established under Latvian law. Resident companies are taxed on their worldwide

income; non-resident companies are taxed on income and gains arising in Latvia (see table

below). Partnerships and cooperative societies are taxed at the level of their partners or

members only. If a partnership distributes business income to a non-resident partner, it must

withhold tax at 15%.2 Starting from 2013 income or loss from the sale of shares will have no effect on the

company’s taxable profit unless the subsidiary is located in a country or territory recognised

by Latvia as a low-tax or tax-free territory (in such case the applicable tax rate is 15%).3 Provided the distributing company is not enjoying certain special tax reliefs.4 The zero rate applies if the distributing company is of a type listed in Annex 1 to the EC

Mergers Directive (90/434/EEC) or liable to a tax similar to Latvia’s corporate income tax

and is not also resident in a third country.5 The zero rate applies if the recipient company owns at least 25% of the share capital of the

distributing company and the latter is not resident in a country or territory considered by

Latvia to be a low-tax or tax-free jurisdiction. Starting from 2013 dividends received from a

non-resident company will not be taxed unless the distributing company is located in a

country or territory recognised by Latvia as a low-tax or tax-free territory (in such case the

applicable tax rate is 15%).

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 3/9

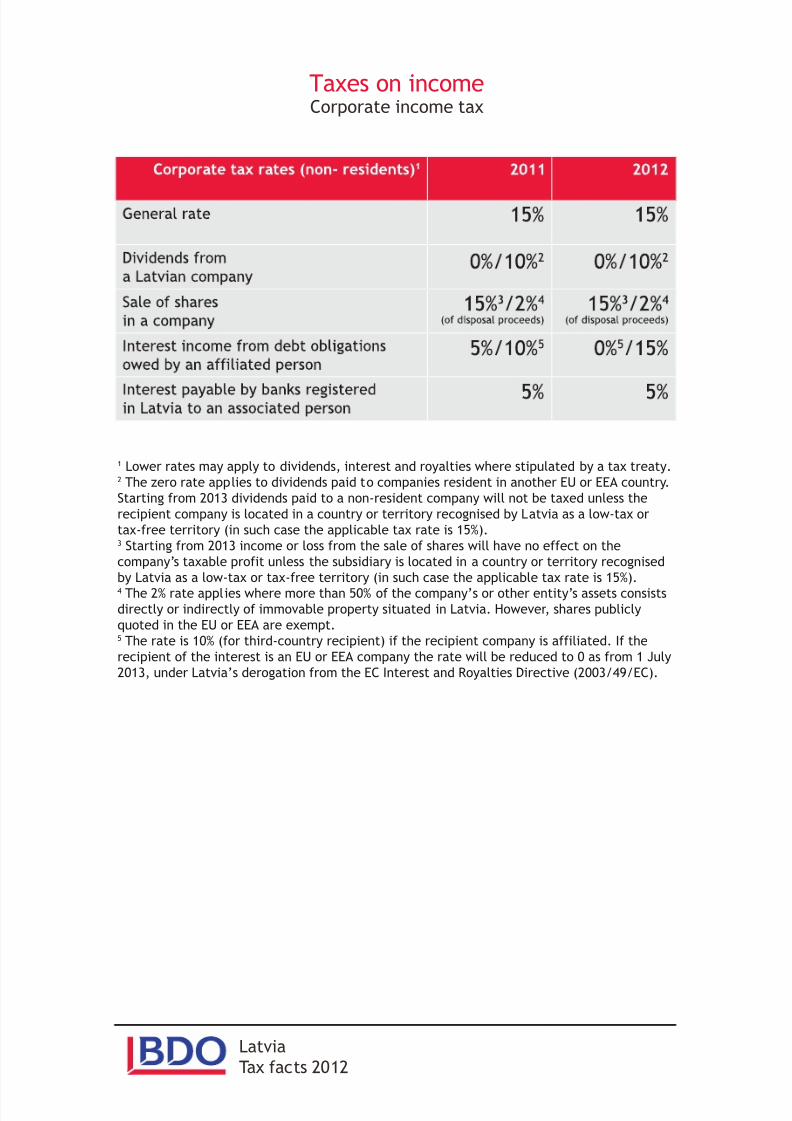

1 Lower rates may apply to dividends, interest and royalties where stipulated by a tax treaty.2 The zero rate applies to dividends paid to companies resident in another EU or EEA country.

Starting from 2013 dividends paid to a non-resident company will not be taxed unless the

recipient company is located in a country or territory recognised by Latvia as a low-tax or

tax-free territory (in such case the applicable tax rate is 15%).3 Starting from 2013 income or loss from the sale of shares will have no effect on the

company’s taxable profit unless the subsidiary is located in a country or territory recognised

by Latvia as a low-tax or tax-free territory (in such case the applicable tax rate is 15%).4 The 2% rate applies where more than 50% of the company’s or other entity’s assets consistsdirectly or indirectly of immovable property situated in Latvia. However, shares publicly

quoted in the EU or EEA are exempt.5 The rate is 10% (for third-country recipient) if the recipient company is affiliated. If the

recipient of the interest is an EU or EEA company the rate will be reduced to 0 as from 1 July

2013, under Latvia’s derogation from the EC Interest and Royalties Directive (2003/49/EC).

Taxes on incomeCorporate income tax

Latvia

Tax facts 2012

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 4/9

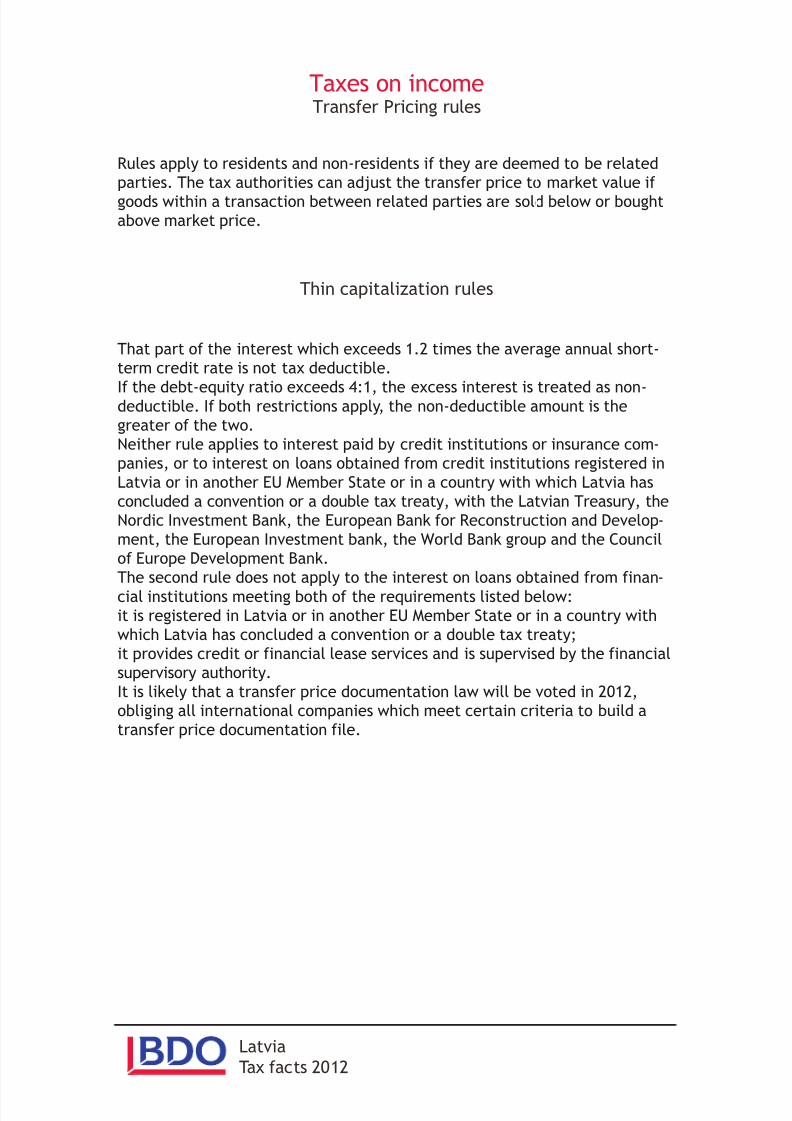

Rules apply to residents and non-residents if they are deemed to be related

parties. The tax authorities can adjust the transfer price to market value if

goods within a transaction between related parties are sold below or boughtabove market price.

Thin capitalization rules

That part of the interest which exceeds 1.2 times the average annual short-

term credit rate is not tax deductible.

If the debt-equity ratio exceeds 4:1, the excess interest is treated as non-deductible. If both restrictions apply, the non-deductible amount is the

greater of the two.

Neither rule applies to interest paid by credit institutions or insurance com-

panies, or to interest on loans obtained from credit institutions registered in

Latvia or in another EU Member State or in a country with which Latvia has

concluded a convention or a double tax treaty, with the Latvian Treasury, the

Nordic Investment Bank, the European Bank for Reconstruction and Develop-

ment, the European Investment bank, the World Bank group and the Council

of Europe Development Bank.

The second rule does not apply to the interest on loans obtained from finan-

cial institutions meeting both of the requirements listed below:

it is registered in Latvia or in another EU Member State or in a country with

which Latvia has concluded a convention or a double tax treaty;

it provides credit or financial lease services and is supervised by the financial

supervisory authority.

It is likely that a transfer price documentation law will be voted in 2012,

obliging all international companies which meet certain criteria to build a

transfer price documentation file.

Taxes on incomeTransfer Pricing rules

Latvia

Tax facts 2012

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 5/9

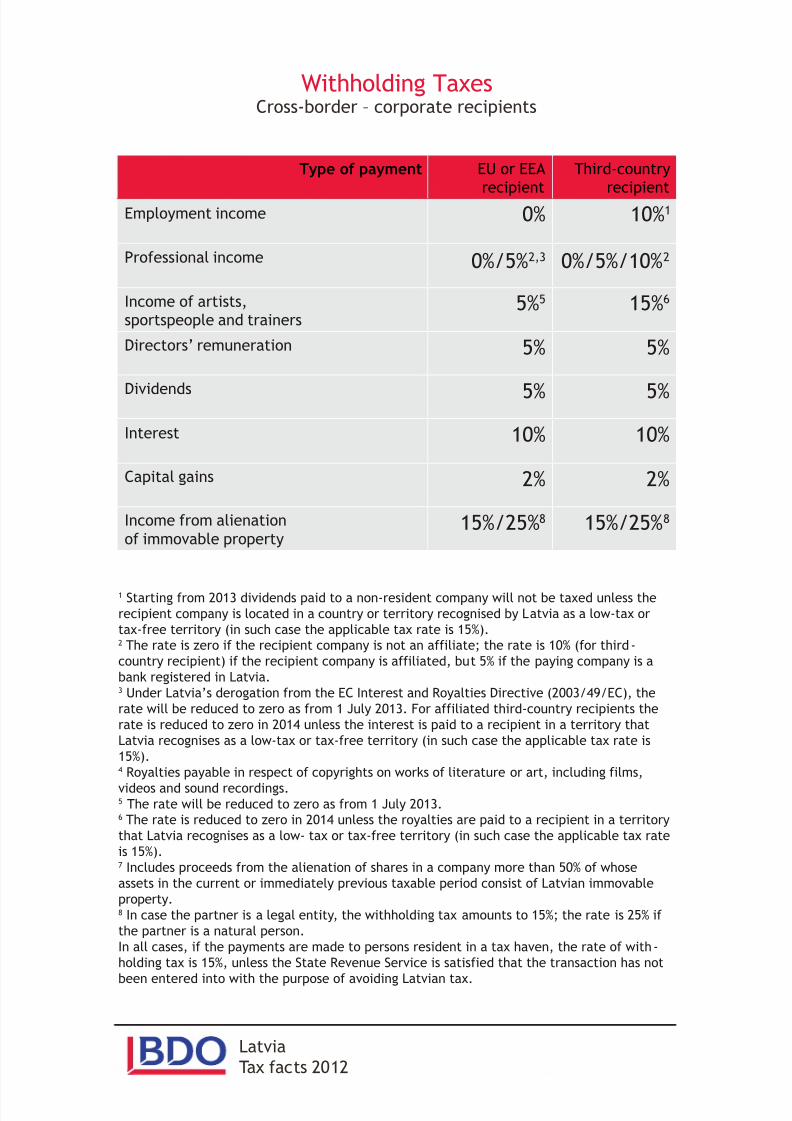

1 Starting from 2013 dividends paid to a non-resident company will not be taxed unless the

recipient company is located in a country or territory recognised by Latvia as a low-tax or

tax-free territory (in such case the applicable tax rate is 15%).2 The rate is zero if the recipient company is not an affiliate; the rate is 10% (for third-

country recipient) if the recipient company is affiliated, but 5% if the paying company is a

bank registered in Latvia.3 Under Latvia’s derogation from the EC Interest and Royalties Directive (2003/49/EC), the

rate will be reduced to zero as from 1 July 2013. For affiliated third-country recipients the

rate is reduced to zero in 2014 unless the interest is paid to a recipient in a territory that

Latvia recognises as a low-tax or tax-free territory (in such case the applicable tax rate is

15%).4 Royalties payable in respect of copyrights on works of literature or art, including films,

videos and sound recordings.5 The rate will be reduced to zero as from 1 July 2013.6 The rate is reduced to zero in 2014 unless the royalties are paid to a recipient in a territory

that Latvia recognises as a low- tax or tax-free territory (in such case the applicable tax rate

is 15%).7 Includes proceeds from the alienation of shares in a company more than 50% of whose

assets in the current or immediately previous taxable period consist of Latvian immovable

property.8 In case the partner is a legal entity, the withholding tax amounts to 15%; the rate is 25% if

the partner is a natural person.

In all cases, if the payments are made to persons resident in a tax haven, the rate of with-

holding tax is 15%, unless the State Revenue Service is satisfied that the transaction has not

been entered into with the purpose of avoiding Latvian tax.

Withholding TaxesCross-border – corporate recipients

Latvia

Tax facts 2012

Employment income

Professional income

Income of artists,sportspeople and trainers

Directors’ remuneration

10%10%

0%/5%/10%20%/5%2,3

15%65%5

5%5%

Dividends 5%5%

Type of payment

Interest

Capital gains

10%10%

2%2%

Income from alienation

of immovable property15%/25%815%/25%8

EU or EEArecipient

Third-countryrecipient

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 6/9

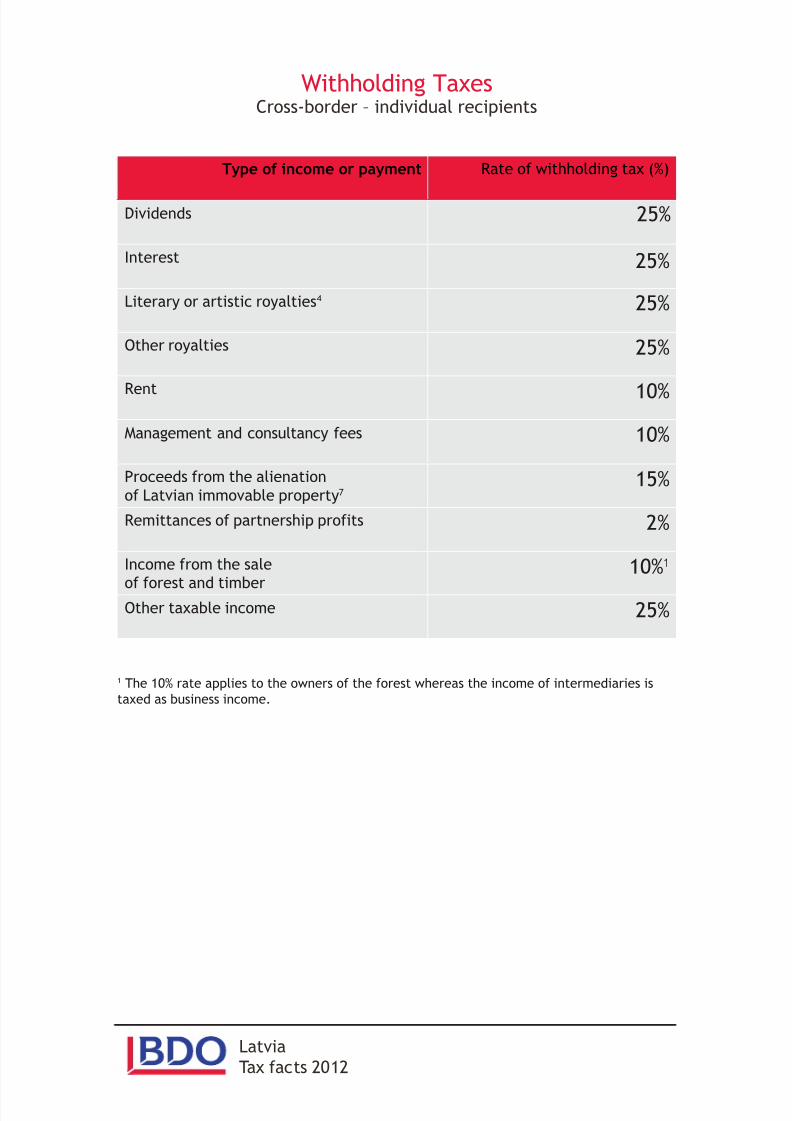

1 The 10% rate applies to the owners of the forest whereas the income of intermediaries is

taxed as business income.

Withholding TaxesCross-border – individual recipients

Latvia

Tax facts 2012

Dividends

Interest

Literary or artistic royalties4

Other royalties

25%

25%

25%

25%

Rent 10%

Type of income or payment

Management and consultancy fees

Proceeds from the alienation

of Latvian immovable property7

10%

15%

Remittances of partnership profits 2%

Income from the sale

of forest and timber

10%1

Other taxable income 25%

Rate of withholding tax (%)

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 7/9

Latvia has no separate capital gains tax; where capital gains are taxable, they

are subject to the corporate or individual income tax at the standard rates.

Gains derived from the sale of shares listed on the securities markets of anEU or EEA member state (including Latvia) are exempt from taxation. Starting

from 2013 income or loss from the sale of shares will have no effect on the

company’s taxable income unless the subsidiary is located in a country or

territory recognised by Latvia as a low-tax or tax-free territory (in such case

the applicable tax rate is 15%).

Taxable capital gains are calculated as the difference between the acquisition

and the sales price. The same principle applies to real property: the gain is

the difference between the acquisition value or the value at the time the

property was developed and the sales price.In the case of individuals, gains from the alienation of real property are not

taxable provided he owned the property for more than 60 months (from the

day when the relevant immovable property was registered in the Land Regis-

try) and has been his declared his only place of residence for at least 12

months until the day of entering into the alienation contract.

For non-residents, income from the alienation of Latvian real estate is tax-

able at a 2% on the alienation proceeds.

Taxes on capitalGift and inheritance taxes

Latvia has no gift or inheritance taxes.

Wealth tax

There is no wealth tax in Latvia.

Calculating the taxable baseCapital gains

Latvia

Tax facts 2012

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 8/9

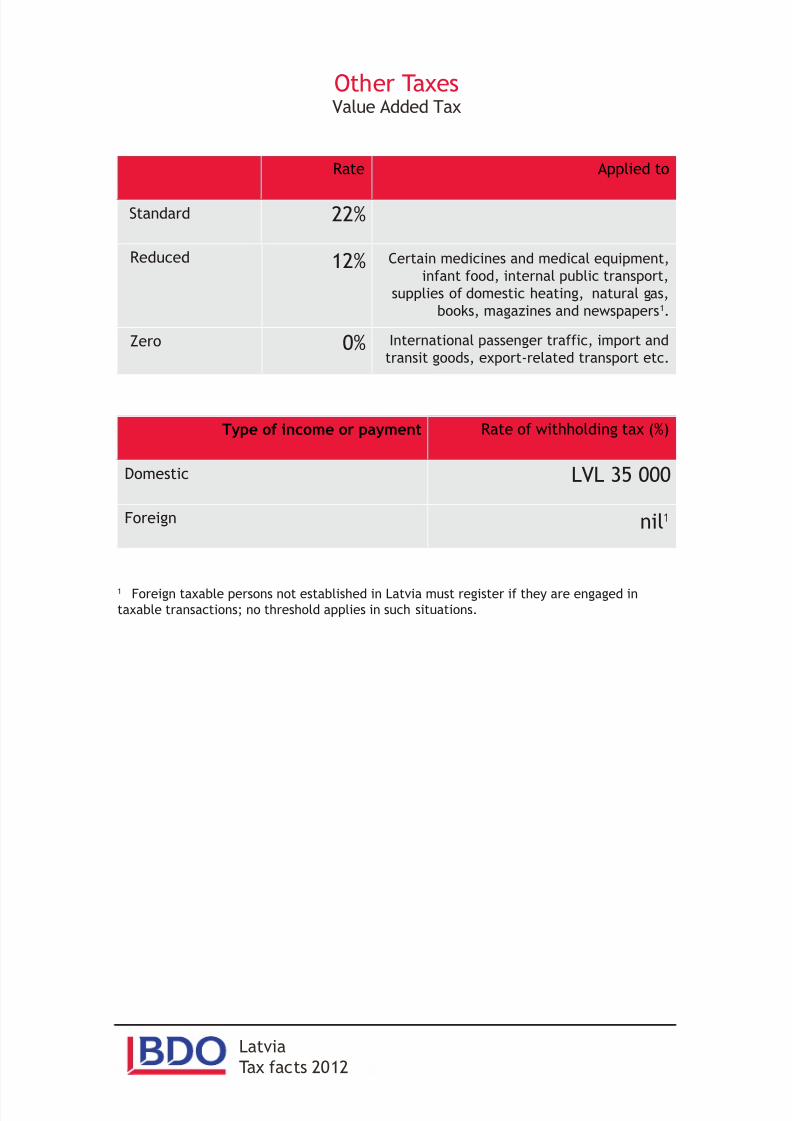

1 Foreign taxable persons not established in Latvia must register if they are engaged intaxable transactions; no threshold applies in such situations.

Other TaxesValue Added Tax

Latvia

Tax facts 2012

Standard

Reduced

Zero

22%

Certain medicines and medical equipment,

infant food, internal public transport,

supplies of domestic heating, natural gas,

books, magazines and newspapers1.

12%

International passenger traffic, import and

transit goods, export-related transport etc.0%

Rate Applied to

Domestic

Foreign

LVL 35 000

nil1

Type of income or payment Rate of withholding tax (%)

8/2/2019 BDO Zelmenis&Liberte publication Latvia Tax Facts 2012

http://slidepdf.com/reader/full/bdo-zelmenisliberte-publication-latvia-tax-facts-2012 9/9

Goods imported from non EU countries are subject to customs duties; excise

duties apply to certain products (alcoholic and non-alcoholic beverages,

tobacco and oil products). The rates vary with the type of goods.

Property Taxes & Property Transfer Taxes

The tax is 1,5% of the cadastral value of the immovable property for land and

buildings used in a commercial activity.

Taxable objects are residential apartments and buildings, auxiliary buildings

with area exceeding 25 m², garages (rate varies), land, commercial buildings,

technical buildings, toll parking lots (rate 1,5%) uncultivated agricultural

land, slums (rate 3%). The minimum tax is LVL 5 (EUR 7,1) per object.

The rate applied to apartments and buildings depends on the cadastral value

of the object:

less than 40’000 LVL – 0,2%

40’001 – 75’000 LVL – 0,4%

more than 75’001 LVL – 0,6%

The property transfer duty is 2% of the higher of the purchase price, the

cadastral value or the valuation for mortgage purposes. The maximum duty is

LVL 30 000.

Natural Resources Tax

Companies engaged in extractive business or which sell resources harmful to

the environment (including plastic packaging etc.) are subject to the natural

resources tax.

Tax on lotteries and games of chance

The tax is imposed on enterprises that have a license to organize and run

lotteries and games of chance.

Other TaxesCustoms and Excise Duties

Latvia

Tax facts 2012