Embed Size (px)

Citation preview

GENERAL MILLS Barc lays Global Consumer

Staples Conference

September 7, 2017

Don MulliganEVP, Chief Financial Officer

This presentation contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995that are based on management’s current expectations and assumptions. These forward-looking statements are subject to certainrisks and uncertainties that could cause actual results to differ materially from the potential results discussed in the forward-lookingstatements. In particular, our predictions about future net sales and earnings could be affected by a variety of factors, including:competitive dynamics in the consumer foods industry and the markets for our products, including new product introductions,advertising activities, pricing actions and promotional activities of our competitors; economic conditions, including changes ininflation rates, interest rates, tax rates, or the availability of capital; product development and innovation; consumer acceptance ofnew products and product improvements; consumer reaction to pricing actions and changes in promotion levels; acquisitions ordispositions of businesses or assets; changes in capital structure; changes in the legal and regulatory environment, includinglabeling and advertising regulations and litigation; impairments in the carrying value of goodwill, other intangible assets, or otherlong-lived assets, or changes in the useful lives of other intangible assets; changes in accounting standards and the impact ofsignificant accounting estimates; product quality and safety issues, including recalls and product liability; changes in consumerdemand for our products; effectiveness of advertising, marketing and promotional programs; changes in consumer behavior, trendsand preferences, including weight loss trends; consumer perception of health-related issues, including obesity; consolidation in theretail environment; changes in purchasing and inventory levels of significant customers; fluctuations in the cost and availability ofsupply chain resources, including raw materials, packaging and energy; disruptions or inefficiencies in the supply chain;effectiveness of restructuring and cost savings initiatives; volatility in the market value of derivatives used to manage price risk forcertain commodities; benefit plan expenses due to changes in plan asset values and discount rates used to determine planliabilities; failure or breach of our information technology systems; foreign economic conditions, including currency rate fluctuations;and political unrest in foreign markets and economic uncertainty due to terrorism or war. The company undertakes no obligation topublicly revise any forward-looking statements to reflect any future events or circumstances.

A Reminder on Forward-looking Statements

3

General Mills Overview

4

Purpose: We serve the world by making food

people love

Goal: Create market leading growth to

deliver top tier shareholder returns

Strategy: Consumer First

$15.6B Net Sales in F17

38,000 Employees

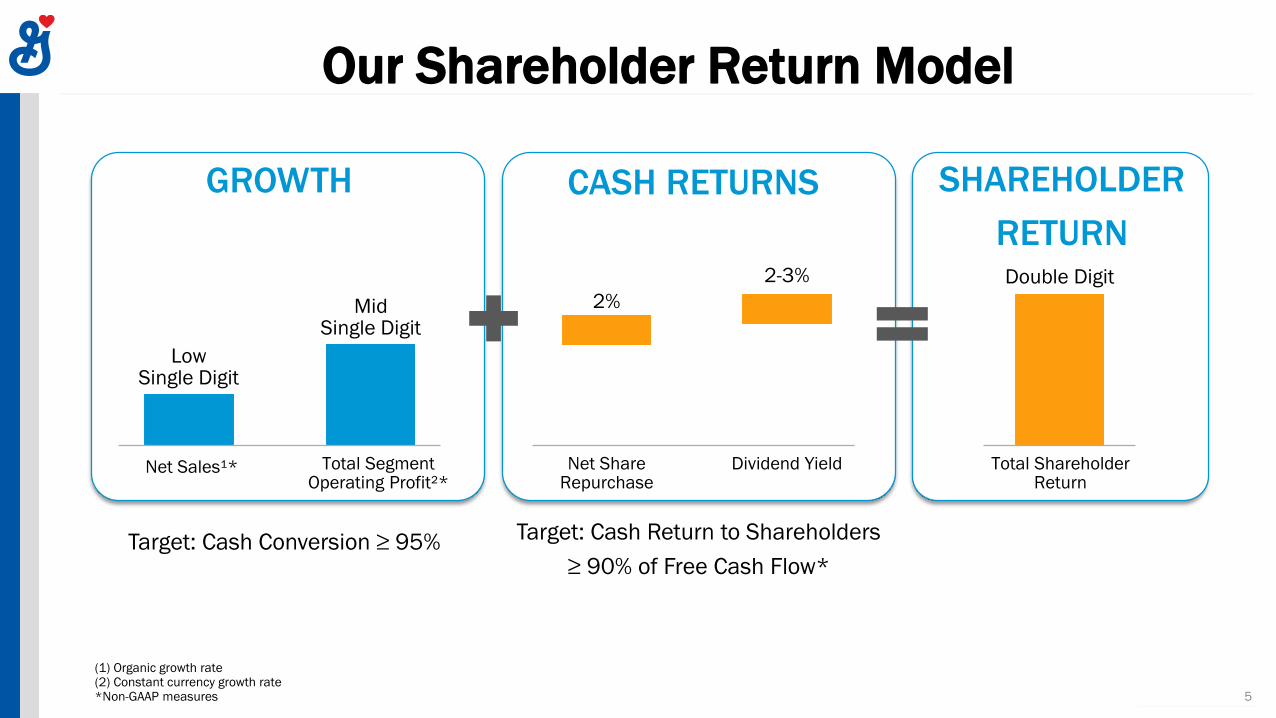

(1) Organic growth rate(2) Constant currency growth rate*Non-GAAP measures

Our Shareholder Return Model

Target: Cash Conversion ≥ 95% Target: Cash Return to Shareholders

≥ 90% of Free Cash Flow*

GROWTH

LowSingle Digit

Net Sales¹* Total Segment Operating Profit²*

MidSingle Digit

Total Shareholder Return

Double Digit

Dividend YieldNet Share Repurchase

CASH RETURNS SHAREHOLDER

RETURN

2%

2-3%

5

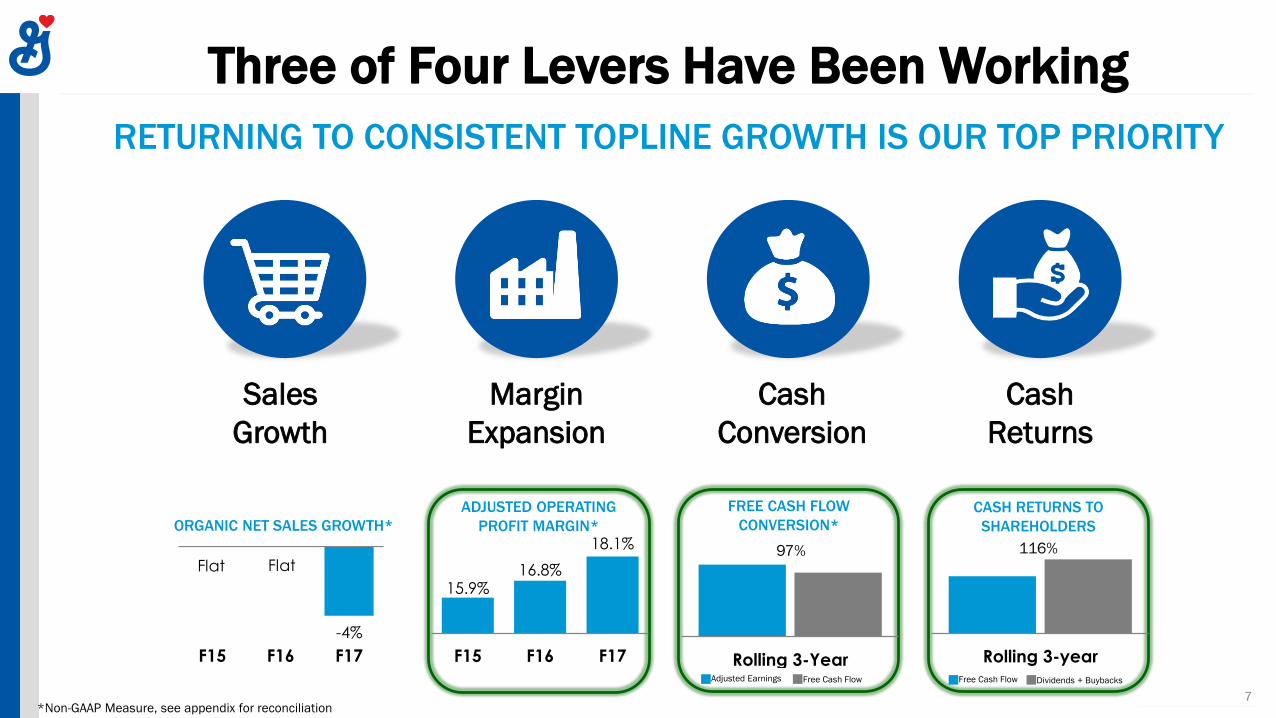

Four Levers to Drive Shareholder Returns

6

Sales

Growth

Margin

Expansion

Cash

Conversion

Cash

Returns

RETURNING TO CONSISTENT TOPLINE GROWTH IS OUR TOP PRIORITY

Three of Four Levers Have Been Working

7*Non-GAAP Measure, see appendix for reconciliation

Sales

Growth

Margin

Expansion

Cash

Conversion

Cash

Returns

ORGANIC NET SALES GROWTH*

ADJUSTED OPERATING

PROFIT MARGIN*

FREE CASH FLOW

CONVERSION*

CASH RETURNS TO

SHAREHOLDERS

-4%

F15 F16 F17

15.9%16.8%

18.1%

F15 F16 F17 Rolling 3-YearAdjusted Earnings Free Cash Flow

97%

Rolling 3-year

116%

Free Cash Flow Dividends + Buybacks

FlatFlat

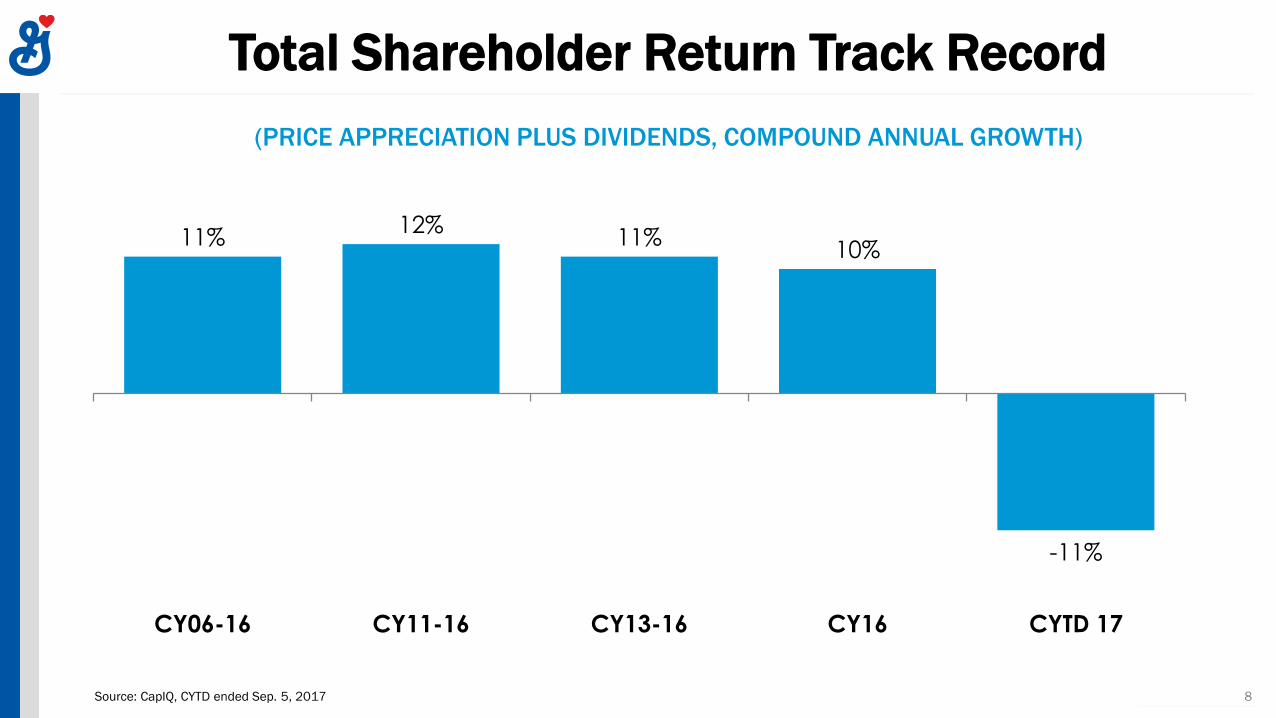

(PRICE APPRECIATION PLUS DIVIDENDS, COMPOUND ANNUAL GROWTH)

Total Shareholder Return Track Record

Source: CapIQ, CYTD ended Sep. 5, 2017

11%12%

11%10%

-11%

CY06-16 CY11-16 CY13-16 CY16 CYTD 17

8

• Grow Cereal Globally (Including CPW)

• Improve U.S. Yogurt Through Innovation

• Invest in Differential Growth Opportunities

− Häagen-Dazs

− Snack Bars

− Old El Paso

− Natural & Organic

• Manage Foundation Brands with Appropriate Investment

Fiscal 2018 Growth Priorities

9

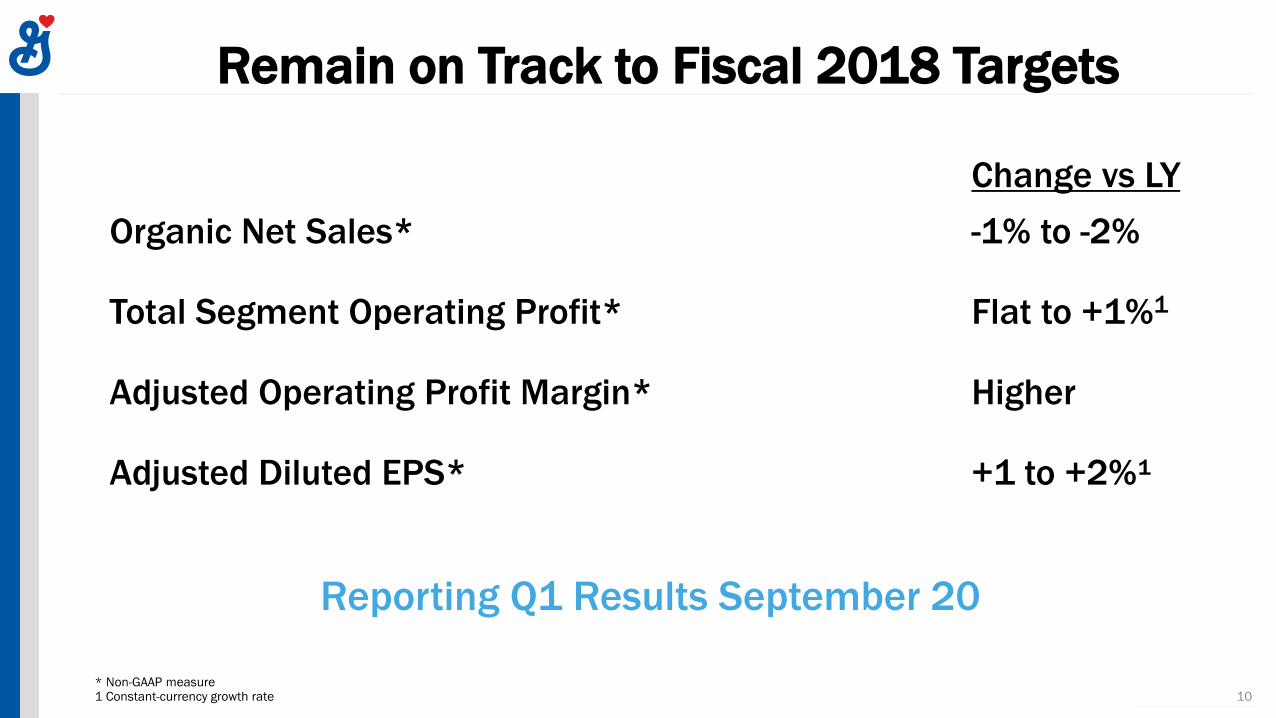

Change vs LY

Organic Net Sales* -1% to -2%

Total Segment Operating Profit* Flat to +1%1

Adjusted Operating Profit Margin* Higher

Adjusted Diluted EPS* +1 to +2%¹

Reporting Q1 Results September 20

Remain on Track to Fiscal 2018 Targets

* Non-GAAP measure1 Constant-currency growth rate 10

• As You Enter Fiscal 2018, What is Changing at General Mills?

• What are you Seeing in the Food Retail Environment in the U.S.?

• Can General Mills Return to Consistent Topline Growth?

ADDRESS INVESTORS’ TOP FAQS IN RECENT MONTHS

Today’s Agenda

11

• General Mills’ Purpose and Values

• Our Consumer First Strategy

• Our Focus on Five Key Global Platforms

• Our Shareholder Return Model

What’s Not Changing at General Mills

12

• Jeff Harmening Appointed CEO on June 1

• New Business Segments

• Flatter Organization & More Global Senior Leadership

• Strengthening Capabilities with External Talent

New Global Organization Structure

13

Realigned

Global

Segments

New Global

Capabilities

Global

Functions

Global Prioritization

14

Oui by Yoplait in the U.S. Häagen-Dazs Stick Bars in Asia and Europe Yoplait Expansion in China

Annie’s on TV for the First Time Old El Paso Brand Building Global Häagen-Dazs Campaign

Global Priorities & Structure Enable Better Idea Sharing

15

DAIRY STRATEGIC BUSINESS UNIT

GLOBAL SNACK BARS

GLOBAL OLD EL PASO

U.S. Retail

India

Optimizing Across GeographiesLeveraging Global Insights Transferring Local Best Practices

Finding the Right Balance in Fiscal 2018

16

INCREASED INNOVATION

“IN THE ZONE” ON PRICING

INCREASED MEDIA INVESTMENT

• As You Enter Fiscal 2018, What is Changing at General Mills?

• What are you Seeing in the Food Retail Environment in the U.S.?

• Can General Mills Return to Consistent Topline Growth?

ADDRESS INVESTORS’ TOP FAQS IN RECENT MONTHS

Today’s Agenda

17

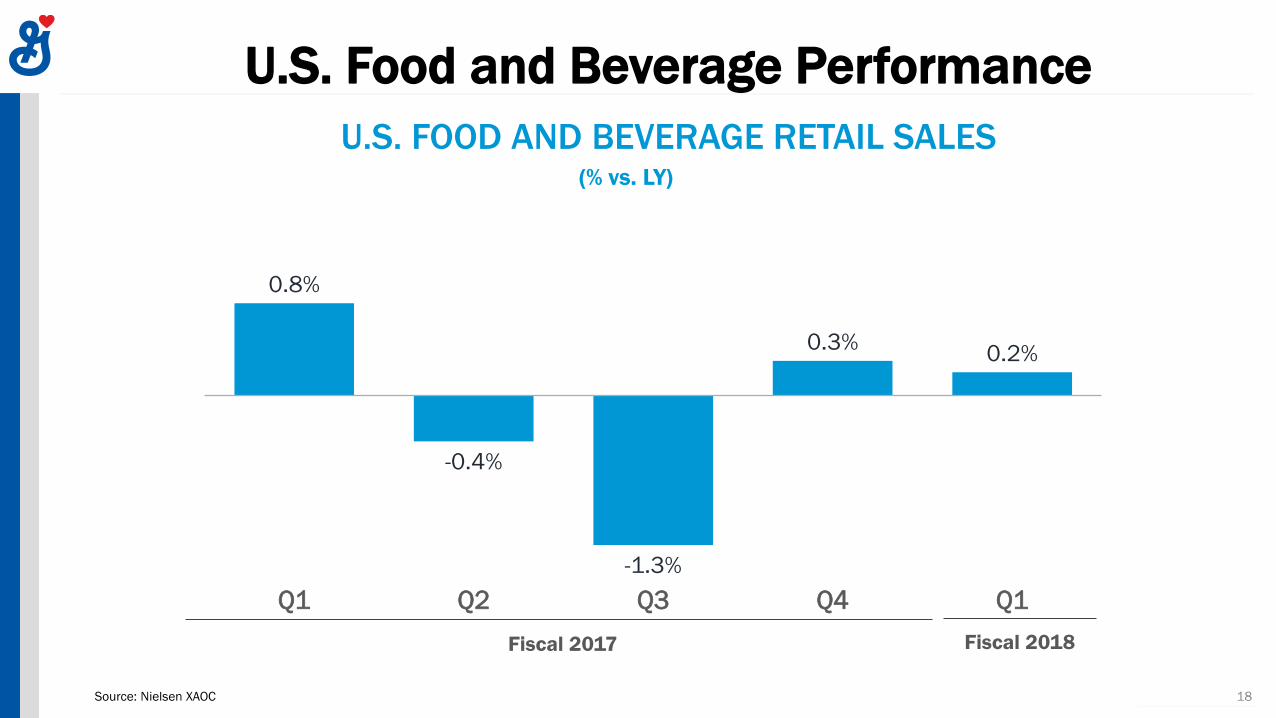

U.S. FOOD AND BEVERAGE RETAIL SALES

U.S. Food and Beverage Performance

18Source: Nielsen XAOC

0.8%

-0.4%

-1.3%

0.3%0.2%

Q1 Q2 Q3 Q4 Q1

(% vs. LY)

Fiscal 2017 Fiscal 2018

Private Label in the U.S.

19Source: Nielsen XAOC, 26-week data

18.5 18.4 18.0 18.4

10.3 10.1 9.7 10.0

U.S. PRIVATE LABEL

RETAIL DOLLAR SHARE (% OF SALES)

Total Food & Beverage General Mills Categories

• Private Label Share Low in General Mills’ Categories

• Share Relatively Flat Across Industry

• Innovation is Best Defense Against Private LabelJul ‘14 Jul ‘15 Jul ‘16 Jul ‘17

• Transition to Full Basket Shopping Will Drive U.S. Food Growth Online

• Winning the First Basket is Critical

• Online Will Represent At Least 5% of General Mills U.S. Retail Sales by 2020

Food E-commerce in the U.S.

20

E-COMMERCE PROJECTION

(Share of General Mills U.S. Food Net Sales)

1.5%

5%

F17 F20

Goal

U.K. RETAIL SALES DOLLAR SHARE INDEX

(E-COMMERCE / TRADITIONAL)

21

65

128

Private Label General Mills

Food E-commerce in Europe

Source: Nielsen/IRI, 52 weeks ended Jun 2017

• Private Label Share Under-indexes Online in Europe, Even in High P/L Markets Like the U.K.

• General Mills Brands are Advantaged Online

• Similar Dynamics Playing Out in the U.S.

• As You Enter Fiscal 2018, What is Changing at General Mills?

• What are you Seeing in the Food Retail Environment in the U.S.?

• Can General Mills Return to Consistent Topline Growth?

ADDRESS INVESTORS’ TOP FAQS IN RECENT MONTHS

Today’s Agenda

22

1) Win Where We Play

2) Expand Where We Play

3) Reshape Our Portfolio for Growth

The Keys to Consistent Topline Growth

23

Win Where We Play

Source: Euromonitor, Calendar 2016

GLOBAL CATEGORY2016

RETAIL SALESPROJECTED 5-YR. CGR

RTE Cereal $23 Billion +LSD

Ice Cream $64 Billion +MSD

Yogurt $84 Billion +HSD

Convenient Meals $89 Billion +MSD

Sweet & Savory Snacks $295 Billion +MSD

24

POSITIVE OUTLOOK IN OUR GLOBAL CATEGORIES

FISCAL 2018 PLAN HIGHLIGHTS

Win Where We Play

25

TASTE NEWS IN U.S. CEREAL FUNDAMENTAL INNOVATION IN U.S. YOGURT

INNOVATION AND MEDIA SUPPORT ON NATURE VALLEY HÄAGEN-DAZS INNOVATION IN EUROPE

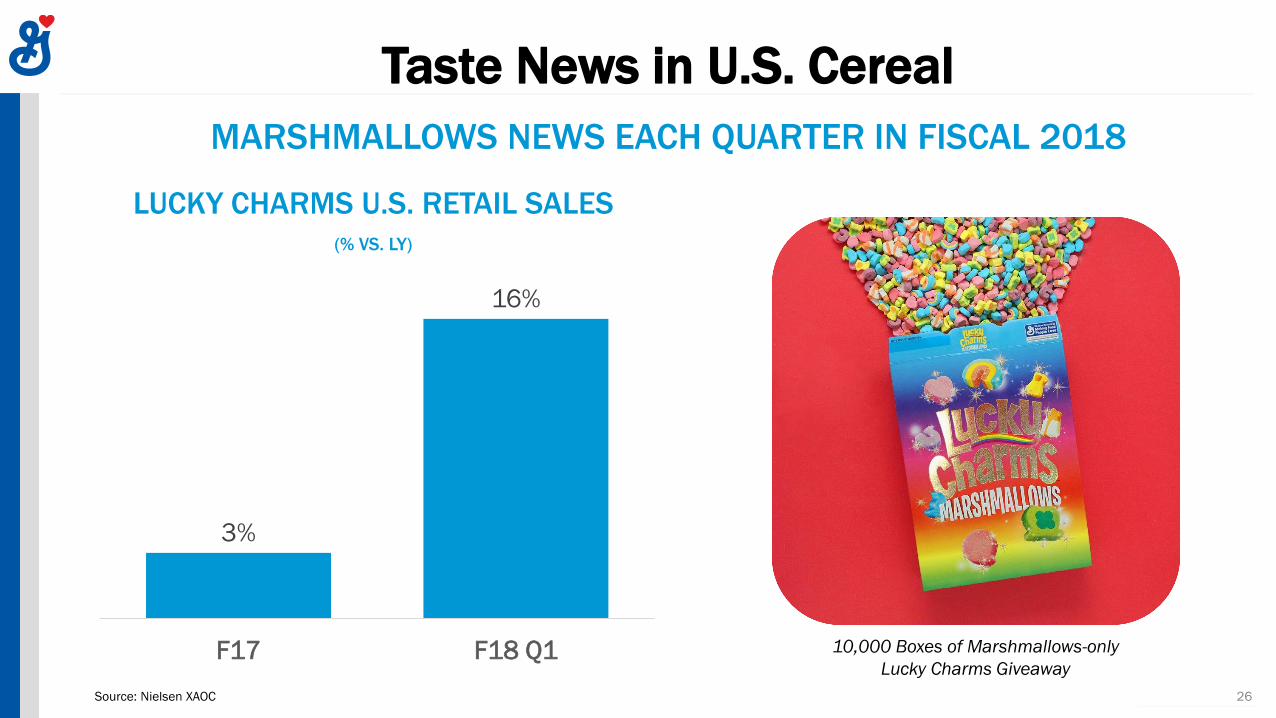

3%

16%

F17 F18 Q1

MARSHMALLOWS NEWS EACH QUARTER IN FISCAL 2018

Taste News in U.S. Cereal

26Source: Nielsen XAOC

LUCKY CHARMS U.S. RETAIL SALES

(% VS. LY)

10,000 Boxes of Marshmallows-only

Lucky Charms Giveaway

Taste News in U.S. Cereal

27Source: Nielsen XAOC

REESE’S PUFFS U.S. RETAIL SALES

(% VS. LY)

7%

8%

F17 F18 Q1

REACHING MORE CONSUMERS

• Outperforming Other Recent Category Innovations

• Distribution Still Building

• Media Support Just Beginning

Fundamental Innovation in U.S. Yogurt

28Source: Nielsen XAOC

LARGEST U.S. YOGURT LAUNCHES IN F13-F18RETAIL SALES INDEX

(FIRST SIX WEEKS RETAIL SALES, NEW PRODUCT VS. OUI)

100

78

54 51 46

Oui Launch

A

Launch

B

Launch

C

Launch

D

OUI BY YOPLAIT

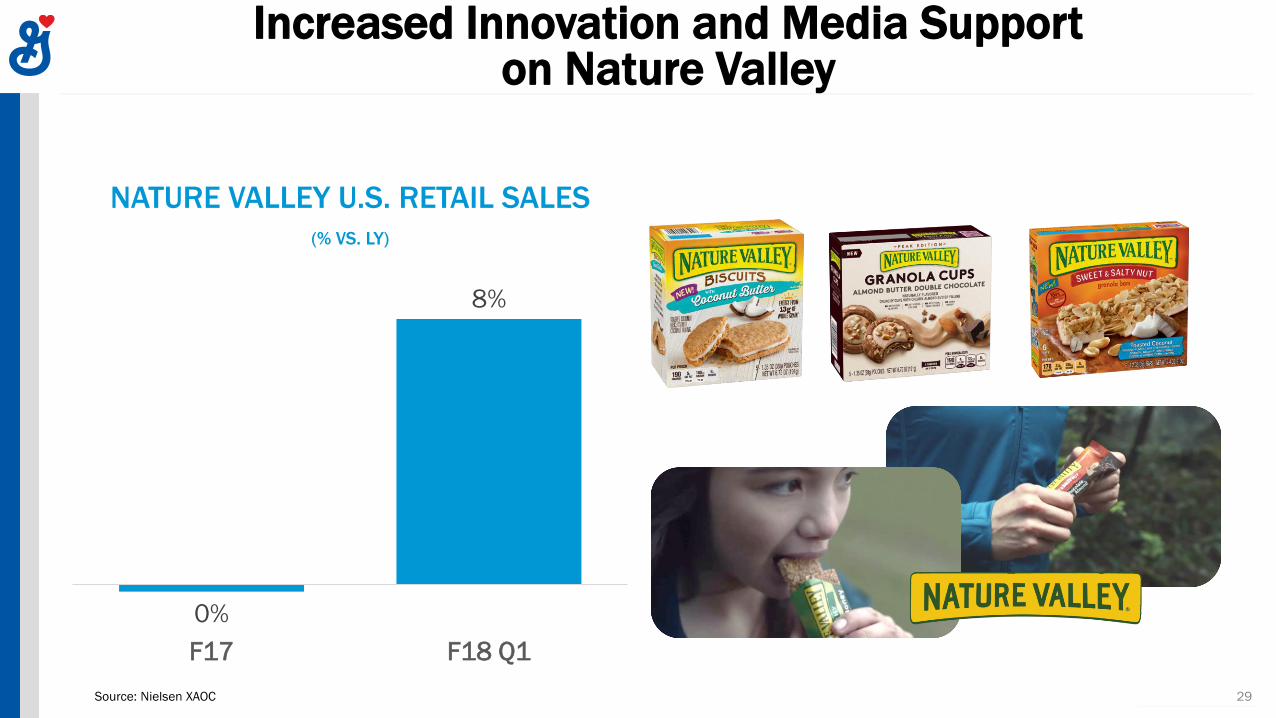

Increased Innovation and Media Support on Nature Valley

29Source: Nielsen XAOC

NATURE VALLEY U.S. RETAIL SALES

(% VS. LY)

0%

8%

F17 F18 Q1

Häagen-Dazs Flavor and Format Innovation in Europe

30Source: Nielsen/IRI, 12 weeks ended July 15, 2017

HÄAGEN-DAZS EUROPE & AUSTRALIA SEGMENT

RETAIL SALES(% VS. LY)

13%

28%

F17 Latest 12 Weeks

General Mills U.S. Retail Sales Trends Improving, As Expected

31Source: Nielsen XAOC

Fiscal 2017 Fiscal 2018

GENERAL MILLS U.S. RETAIL SALES(% vs. LY)

-6%

-7%

-8%

-7%

-4%

Q1 Q2 Q3 Q4 Q1

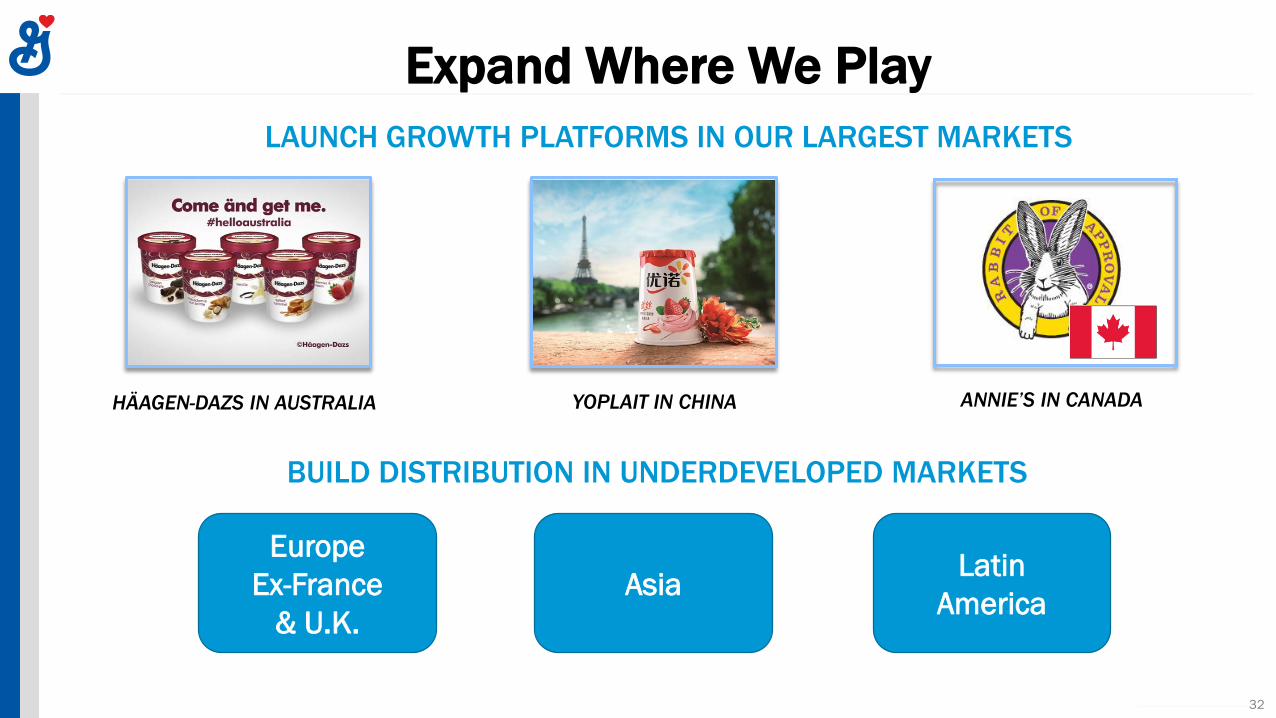

Expand Where We Play

32

HÄAGEN-DAZS IN AUSTRALIA YOPLAIT IN CHINA ANNIE’S IN CANADA

LAUNCH GROWTH PLATFORMS IN OUR LARGEST MARKETS

BUILD DISTRIBUTION IN UNDERDEVELOPED MARKETS

Europe

Ex-France

& U.K.

AsiaLatin

America

Reshape Our Portfolio for Growth

33

• M&A Has Enhanced Our Organic Growth Profile

• M&A Focus Areas:

• Bolt-on Acquisitions in North America and Europe

• Adding Scale in Emerging Markets

F15-F17 ACQUISITIONS

F16 DIVESTITURE

• We’ve Made a Number of Significant Changes to Drive Improved Performance at General Mills

• E-commerce Will be the Biggest Driver of Change in the U.S. Food Retail Environment and We See it as an Opportunity

• We Will Return to Consistent Topline Growth By Winning Where We Play, Expanding Where We Play, and Reshaping our Portfolio for Growth

Today’s Summary

34

GENERAL MILLS Barc lays Global Consumer

Staples Conference

September 7, 2017

Our fiscal 2018 outlook for organic net sales growth, constant-currency total segment operating profit and adjusted diluted EPS,

and adjusted operating profit margin are non-GAAP financial measures that exclude, or have otherwise been adjusted for, items

impacting comparability, including the effect of foreign currency exchange rate fluctuations, restructuring charges and project-

related costs, and commodity mark-to-market effects. Our fiscal 2018 outlook for organic net sales growth also excludes the

effect of acquisitions and divestitures. We are not able to reconcile these forward-looking non-GAAP financial measures to their

most directly comparable forward-looking GAAP financial measures without unreasonable efforts because we are unable to

predict with a reasonable degree of certainty the actual impact of changes in foreign currency exchange rates and commodity

prices or the timing of acquisitions, divestitures and restructuring actions throughout fiscal 2018. The unavailable information

could have a significant impact on our fiscal 2018 GAAP financial results.

For fiscal 2018, we currently expect: foreign currency exchange rates (based on blend of forward and forecasted rates and

hedge positions), acquisitions, and divestitures to have an immaterial impact on net sales growth; foreign currency exchange

rates to have an immaterial impact on total segment operating profit and adjusted diluted EPS growth; and total restructuring

charges and project-related costs related to actions previously announced to total approximately $45 million.

A Reminder on Non-GAAP Guidance

36

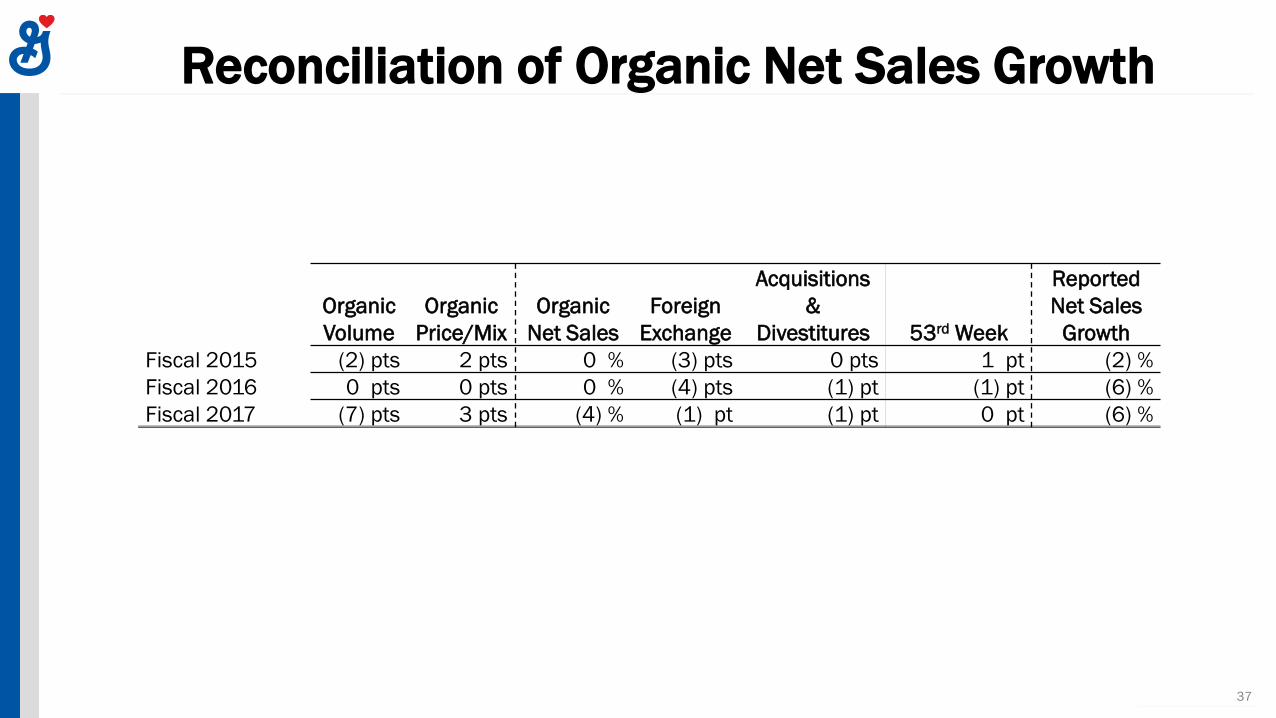

Reconciliation of Organic Net Sales Growth

37

Organic

Volume

Organic

Price/Mix

Organic

Net Sales

Foreign

Exchange

Acquisitions

&

Divestitures 53rd Week

Reported

Net Sales

Growth

Fiscal 2015 (2) pts 2 pts 0 % (3) pts 0 pts 1 pt (2) %

Fiscal 2016 0 pts 0 pts 0 % (4) pts (1) pt (1) pt (6) %

Fiscal 2017 (7) pts 3 pts (4) % (1) pt (1) pt 0 pt (6) %

Reconciliation of Adjusted Operating Profit Margin

Full Year

% of Net Sales

2017 2016 2015

Operating profit as reported 16.4 % 16.3 % 11.8 %

Mark-to-market effects (0.1) (0.4) 0.5

Divestitures (gain) loss, net 0.1 (0.9) -

Restructuring costs 1.4 1.4 1.9

Project-related costs 0.3 0.4 0.1

Acquisition integration costs - - 0.1

Intangible asset impairment - - 1.5

Adjusted operating profit margin 18.1 % 16.8 % 15.9 %

(Fiscal Years)

38

2017 2016 2015

Net earnings, including earnings attributable to redeemable and

noncontrolling interests $1,701 $1,737 $1,259

Mark-to-market effects* (9) (40) 57

Divestitures (gain) loss* 9 (66) -

Tax-related items* - - 79

Acquisition integration costs* - - 10

Venezuela currency devaluation* - - 8

Restructuring costs* 154 161 218

Project-related costs* 28 37 8

Intangible asset impairment* - - 177

Adjusted net earnings, including earnings attributable to redeemable

and noncontrolling interests $1,884 $1,829 $1,816

Net cash provided by operating activities, as reported $2,313 $2,630 $2,543

Purchases of land, buildings, and equipment (684) (729) (712)

Free cash flow $1,629 $1,901 $1,830

Free cash flow, rolling 3-year $5,360

Free cash flow conversion, rolling 3-years 97%

Reconciliation of Free Cash Flow and Free Cash Flow Conversion

(Fiscal Years, $ in Millions)

*See reconciliation of income taxes on adjusted items.

Table does not foot due to rounding.39

Cash Return to Shareholders(Fiscal Years, $ in Millions)

2017 2016 2015

Dividends paid $1,135 $1,072 $1,018

Purchases of common stock for treasury 1,652 607 1,162

Proceeds from common stock issued on

exercised options (113) (172) (164)

Total cash return to shareholders $2,674 $1,507 $2,016

Cash returns, rolling 3-year $6,197

Cash returns % of Free Cash Flow, rolling 3-year 116%

40

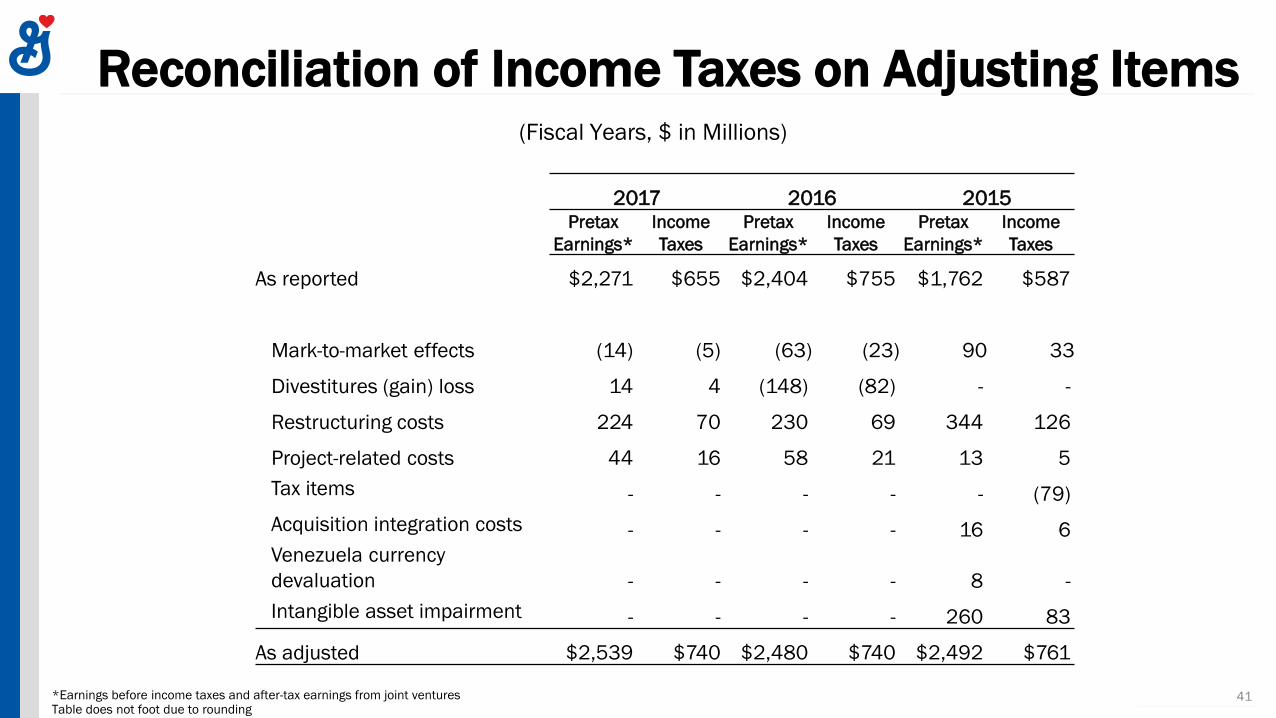

Reconciliation of Income Taxes on Adjusting Items

2017 2016 2015Pretax

Earnings*

Income

Taxes

Pretax

Earnings*

Income

Taxes

Pretax

Earnings*

Income

Taxes

As reported $2,271 $655 $2,404 $755 $1,762 $587

Mark-to-market effects (14) (5) (63) (23) 90 33

Divestitures (gain) loss 14 4 (148) (82) - -

Restructuring costs 224 70 230 69 344 126

Project-related costs 44 16 58 21 13 5

Tax items - - - - - (79)

Acquisition integration costs - - - - 16 6

Venezuela currency

devaluation - - - - 8 -

Intangible asset impairment - - - - 260 83

As adjusted $2,539 $740 $2,480 $740 $2,492 $761

(Fiscal Years, $ in Millions)

*Earnings before income taxes and after-tax earnings from joint venturesTable does not foot due to rounding

41