Embed Size (px)

Citation preview

Page | 1 | PHILLIP SECURITIES INDONESIA MCI (P) 019/11/2014_0013 Ref. No.: INDO2014_0015

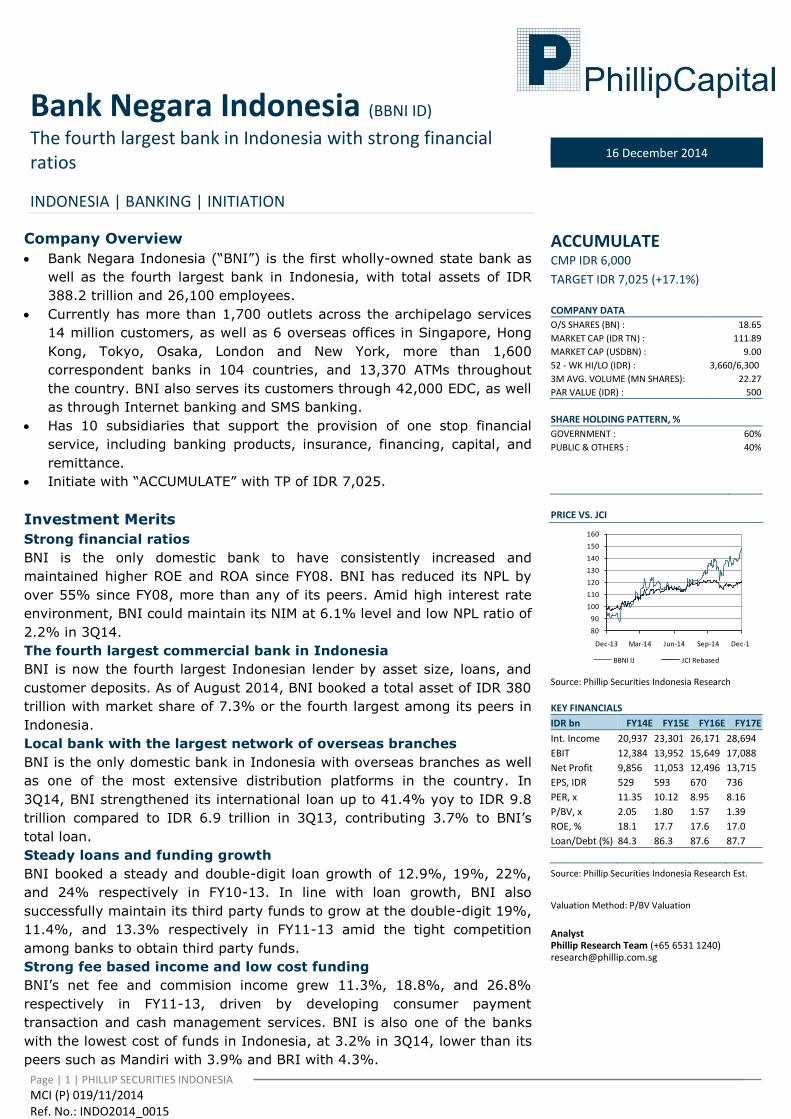

Bank Negara Indonesia (BBNI ID)

The fourth largest bank in Indonesia with strong financial ratios

INDONESIA | BANKING | INITIATION

16 December 2014

Company Overview

Bank Negara Indonesia (“BNI”) is the first wholly-owned state bank as

well as the fourth largest bank in Indonesia, with total assets of IDR

388.2 trillion and 26,100 employees.

Currently has more than 1,700 outlets across the archipelago services

14 million customers, as well as 6 overseas offices in Singapore, Hong

Kong, Tokyo, Osaka, London and New York, more than 1,600

correspondent banks in 104 countries, and 13,370 ATMs throughout

the country. BNI also serves its customers through 42,000 EDC, as well

as through Internet banking and SMS banking.

Has 10 subsidiaries that support the provision of one stop financial

service, including banking products, insurance, financing, capital, and

remittance.

Initiate with “ACCUMULATE” with TP of IDR 7,025.

Investment Merits

Strong financial ratios

BNI is the only domestic bank to have consistently increased and

maintained higher ROE and ROA since FY08. BNI has reduced its NPL by

over 55% since FY08, more than any of its peers. Amid high interest rate

environment, BNI could maintain its NIM at 6.1% level and low NPL ratio of

2.2% in 3Q14.

The fourth largest commercial bank in Indonesia

BNI is now the fourth largest Indonesian lender by asset size, loans, and

customer deposits. As of August 2014, BNI booked a total asset of IDR 380

trillion with market share of 7.3% or the fourth largest among its peers in

Indonesia.

Local bank with the largest network of overseas branches

BNI is the only domestic bank in Indonesia with overseas branches as well

as one of the most extensive distribution platforms in the country. In

3Q14, BNI strengthened its international loan up to 41.4% yoy to IDR 9.8

trillion compared to IDR 6.9 trillion in 3Q13, contributing 3.7% to BNI’s

total loan.

Steady loans and funding growth

BNI booked a steady and double-digit loan growth of 12.9%, 19%, 22%,

and 24% respectively in FY10-13. In line with loan growth, BNI also

successfully maintain its third party funds to grow at the double-digit 19%,

11.4%, and 13.3% respectively in FY11-13 amid the tight competition

among banks to obtain third party funds.

Strong fee based income and low cost funding

BNI’s net fee and commision income grew 11.3%, 18.8%, and 26.8%

respectively in FY11-13, driven by developing consumer payment

transaction and cash management services. BNI is also one of the banks

with the lowest cost of funds in Indonesia, at 3.2% in 3Q14, lower than its

peers such as Mandiri with 3.9% and BRI with 4.3%.

ACCUMULATE CMP IDR 6,000

TARGET IDR 7,025 (+17.1%) COMPANY DATA

O/S SHARES (BN) : 18.65

MARKET CAP (IDR TN) : 111.89

MARKET CAP (USDBN) : 9.00

52 - WK HI/LO (IDR) : 3,660/6,300

3M AVG. VOLUME (MN SHARES): 22.27

PAR VALUE (IDR) : 500

SHARE HOLDING PATTERN, %

GOVERNMENT : 60%

PUBLIC & OTHERS : 40%

PRICE VS. JCI

80

90

100

110

120

130

140

150

160

Dec-13 Mar-14 Jun-14 Sep-14 Dec-14

BBNI IJ JCI Rebased

Source: Phillip Securities Indonesia Research

KEY FINANCIALS

IDR bn FY14E FY15E FY16E FY17E

Int. Income 20,937 23,301 26,171 28,694

EBIT 12,384 13,952 15,649 17,088

Net Profit 9,856 11,053 12,496 13,715

EPS, IDR 529 593 670 736

PER, x 11.35 10.12 8.95 8.16

P/BV, x 2.05 1.80 1.57 1.39

ROE, % 18.1 17.7 17.6 17.0

Loan/Debt (%) 84.3 86.3 87.6 87.7

Source: Phillip Securities Indonesia Research Est.

Valuation Method: P/BV Valuation

Analyst Phillip Research Team (+65 6531 1240) [email protected]

Page | 2 | PHILLIP SECURITIES INDONESIA

Risk Factor

Coupled with global economic slowdown, especially in China and India,

some local factors such as rising inflation and gradual increase in electricity

tariffs will also potentially pressure Indonesia’s economic growth. A slower

demand from the export market could reduce revenue growth of real

sector, which in turn would cause slower loan growth in the banking sector.

The possibility of higher interest rate by the U.S. Federal Reserve will

potentially result in increased liquidity pressure.

Investment Action

We initiate coverage on BNI with “Accumulate” rating. We are positive on

1) Positive demand for syndicated loans from the infrastructure sector and

2) BNI’s target to reduce cost to income and increase its efficiency. Based

on our FY15 BVPS of IDR 3,342 and a P/B of 1.80x, we derive a target

price of IDR 7,025 with potential upside of 17.1% (not include a DPS of

IDR 178).

Key Financial Summary

FYE Dec FY12 FY13 FY14F FY15F FY16F

Net interest income (IDR mn) 15,458,991 19,149,281 20,936,989 23,301,162 26,170,696

Non interest income (IDR mn) 8,445,813 9,440,904 10,553,237 11,796,626 13,186,512

NPAT. Adj. (IDR mn) 6,789,823 9,089,579 9,860,361 11,056,983 12,500,489

EPS, adj. (IDR) 378 490 529 593 670

P/E (X), adj. 9.79 8.05 11.35 10.12 8.95

BVPS (IDR) 2,334 2,557 2,927 3,342 3,811

P/B (X) 1.59 1.54 2.05 1.80 1.57

DPS (IDR) 113 146 159 178 201

Div. Yield (%) 3.06% 3.69% 2.64% 2.96% 3.35%

Source: Bloomberg, PSI Research Est.*Forward multiples and yields are based on current price and historical multiples andyields are based on historical prices

PHILLIP SECURITIES INDONESIA | 3 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

PHILLIP SECURITIES INDONESIA | 4 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Banking Industry in Indonesia

Slower Economic Growth in Indonesia

Statistic Indonesia announced that economic growth in Indonesia

reached 5.01% yoy in 3Q14. This result was slightly below analysts’

forecast and implies that the slowing trend of economic expansion in

Southest Asia’s largest economy continues. Since FY11, GDP growth has

been declining amid global and domestic economy declines. The 5.01%

point GDP growth in 3Q14 was the slowest quarterly growth pace in 5

years.

Externally, economic expansion in Indonesia has been limited by

sluggish global economy. With China’s economy growing at a relatively

low pace, global demand for Indonesian commodities has declined

sharply. In 3Q14, exports declined by 0.7% yoy. Furthermore, the

slowdown in exports was also partly caused by the controversial ban on

mineral ore exports which was implemented by the Indonesian

government in January 2014.

Indonesia’s quarterly GDP growth FY09-14 (annual % change)

4.6

5.996.45 6.29 6.03

5.224.37

6.29 6.52 6.365.89

5.124.31

5.816.49 6.16

5.625.01

4.58

6.81 6.56.11 5.78

0

1

2

3

4

5

6

7

2009 2010 2011 2012 2013 2014

1Q 2Q 3Q 4Q

Source: Statistics Indonesia, PSI Research

According to the Bank Indonesia, inflation may reach around 7.5% yoy

by FY14 as a result of higher subsidized fuel prices. In 4Q14, subsidized

fuel prices (gasoline and diesel) were raised more than 30% in an

attempt to reallocate government funds to more productive sectors as

well as to curb the country’s wide current account deficit. However, the

Bank Indonesia projects the IDR 2,000/liter fuel price hike will add

another 2.5% of Indonesian inflation to 7.5-8% for FY14.

The Bank Indonesia immediately responded to the fuel price hike by

raising its key interest rate by 25 basis points to 7.75%, for the first

time in 12 months. The higher interest environment in Indonesia led to

slower credit growth of 14% in 3Q14 versus 2013’s 21.4% pace.

However, the liquidity condition in banking sector has relatively eased,

proved by a decrease in the loan to deposit (LDR) ratio of 89.13% in

3Q14, compared to above 92% level in the previous month.

Indonesian economy grew 5.01% yoy in 3Q14, the slowest quarterly growth pace in 5 years.

Subsidized fuel prices were raised by more than 30% in 4Q14. In response, BI raised its key interest rate to 7.75%.

PHILLIP SECURITIES INDONESIA | 5 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Indonesia’s Economic Growth Accelerates in 2015

According to the Asian Development Bank (ADB), Indonesian economy is

expected to pick up in FY15 as external demand improves and the new

government’s reform agenda takes hold. The ADB expects a growth

pace of 5.5% in FY15. Optimism over the new Joko Widodo (Jokowi)-led

administration brings new hope that can trigger investment growth.

Jokowi has been the market-favorite in the 2014 election.

Higher global economic growth forecast of 4% in FY15 compared to

3.4% in FY14 will encourage optimism over Indonesian economic growth

in FY15. Global trade, which is forecast to grow 5.3% in FY15 compared

to 4% in FY14, will encourage export performance to increase 4.4% in

FY15 compared to 1.4% in FY14. Due to enhanced certainty about

investment and employment programs of the new government,

investments in Indonesia are expected to grow by 5.5% or higher than

the 5.2% point growth projected in FY14.

Furthermore, the reallocation of fuel subsidies to finance infrastructure

development as well as various other productive activities (healthcare

and education) will improve the central government’s fiscal space in

term of nurturing stronger and more sustainable GDP growth. As such,

Bank Indonesia also estimates that Indonesia’s economic growth will

return to 5.5% yoy in FY15 and higher in the medium-long term.

Meanwhile, we have conservative view regarding the value of the Rupiah

(IDR). The average IDR rate is estimated to depreciate at IDR

12,600/USD range in FY15.

Despite positive impacts thanks to easing current account deficit, risks

poses by U.S. tappering off and possible increase in U.S. interest rates

will most likely lead to another round of capital outflows from the stock

and financial markets of emerging markets, including Indonesia. This is

because Indonesia’s 5.5% growth target will be highly dependent on

global economic growth, the acceleration of infrastructure development

in Indonesia, as well as government budget.

Banking Outlook in 2015

In line with economic growth forecast of 5.5% in FY15, the Bank

Indonesia sees loan growth between 15-17% next year, higher than

13-15% in FY14, while total deposits is expected to grow 11-13% in

FY15, or higher than 10-12% in FY14. We expect a slower loan growth

in the 1Q15 following the key interest rate hike at the end of FY14. The

Bank Indonesia increased key interest rate by 25 basis point to 7.75%

in 4Q14 to anticipate higher inflation after fuel price hike by Indonesian

government. We see a high chance of key interest rate hike in 2015 to

8.00% along with possible increase in U.S. Fed funds rates.

But we are positive that the 5.5% economic growth forecast will

encourage loan growth in the long term. Better use of government funds

from fuel consumption to infrastructure development will lead to lower

logistic costs. Moreover, along with improving economy in the US and

Japan, as well as signs of economic recoveries in Europe, China, and

We expect loans to grow 15-17% in FY15, in line with economic growth.

Infrastructure development will create more sustainable GDP growth of 5.5% in FY15.

PHILLIP SECURITIES INDONESIA | 6 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

India, it is expected that the global economy will improve in FY15 to

support future growth of Indonesian economy.

In addition, major lenders also expect positive demand for syndicated

loans from infrastructure sector next year, as President Jokowi envisions

more project developments to boost Indonesia’s economy. According to

Bloomberg’s Global Syndicated Loans League Tables, as many as 20

international banks and financial institutions acted as Indonesia’s

mandated arrangers as of September 2014 for 42 syndicated-loan deals

with a total volume of USD 14.56 billion, increased by 30.23% from USD

11.18 billion last year. However, the non-performing loan (NPL) level is

estimated to rise in the beginning of FY15, along with an increase of BI

rate. We expect higher loan risks in FY15, but it will likely to remain

below 3% or better than 3.8% NPL rate in FY08-09.

PHILLIP SECURITIES INDONESIA | 7 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Investment Thesis

The fourth largest commercial bank in Indonesia

BNI is now the fourth largest Indonesian lender by asset size, loans, and

customer deposits. As of August 2014, BNI booked a total asset of IDR

380 trillion with market share of 7.3%, making it the fourth largest

among peers in Indonesia. BNI also recorded total loans of IDR 157

trillion (7.1% market share) and total customer deposits of IDR 293

trillion (7.6% market share) in the same period, which is the fourth

largest after BRI, Mandiri, and BCA.

The top 10 largest bank in Indonesia in terms of assets, loans,

and customer deposits as of August 2014

Source: Bank Indonesia, PSI Research

Has a solid liquidity position and asset quality

BNI’s liquidity was well maintained within the range set by Bank

Indonesia, with LDR of 85.7% in 3Q14, an increase compared with

84.7% a year earlier as a result of higher loan growth compared to

growth in third party deposits. Despite high interest rate environment,

BNI could maintain its NIM at 6.1% level and low NPL ratio of 2.2% in

3Q14. This shows that BNI has no difficulty in liquidity position and its

asset quality.

Strong financial ratios

BNI is the only domestic bank to have consistently increased and

maintained higher ROE since FY08, and its emphasis on quality growth

has led to a 400% rise in ROA during the same seven year period.

Meanwhile, the bank has reduced its NPL by over 55% since FY08, more

than any of its peers, and has significantly improved its coverage ratio

as well. BNI also boasts one of the strongest and low LDR banks, with

ROA and ROE have been maintained at consistently improving trajectory

under the stewardship of a focused and commited management team.

In 3Q14, BNI booked LDR of 85.7%, lower than industry’s 90.6%.

Local bank with the largest network of overseas branches

BNI is the only domestic banks in Indonesia with overseas branches.

The bank has overseas offices in Singapore, Hong Kong, Tokyo, Osaka,

London and New York, and 6 overseas ATM (4 ATMs in HongKong and 2

ATMs in Singapore). BNI also has one of the most extensive distribution

platforms in the country. In 3Q14, BNI strengthened its international

BNI has overseas offices in Singapore, Hong Kong, Tokyo, Osaka, London, and New York.

BNI boasts one of the strongest, low-cost funding-based and low LDR banks, with ROA and ROE have been maintained at consistently improving trajectory.

PHILLIP SECURITIES INDONESIA | 8 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

loans to up to 41.4% yoy to IDR 9.8 trillion, compared to IDR 6.9 trillion

in 3Q13, contributin 3.7% of BNI’s total loan.

Steady loans and funding growth

BNI booked steady and double-digit loan growths of 12.9%, 19%, 22%,

and 24% respectively in FY10-13. Despite slowdown of global economy

in FY13, BNI managed to increase its loans to grow by more than 24%,

above banking sector average of 21.6%. In line with loan growth, BNI

also successfully maintained its third party funds to grow at double-digit

pace of 19%, 11.4%, and 13.3%, respectively in FY11-13 amid tight

competitions among banks to secure third party funds.

Strong fee-based income and low-cost funding

BNI’s net fee and commision income grew 11.3%, 18.8%, and 26.8%

respectively in FY11-13, driven by developing consumer payment

transactions and cash management services. These fee-based income

contribute 14% to BNI’s total income in FY13. BNI is also one of the

banks with the lowest cost of funds in Indonesia, with 3.2% CoF in

3Q14, up 31.3% compared to 2.3% in 3Q13. This is lower compared to

its peers such as Mandiri with 3.9% CoF and BRI with 4.3% CoF.

BNI is one of the banks with the lowest cost of funds in Indonesia.

PHILLIP SECURITIES INDONESIA | 9 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

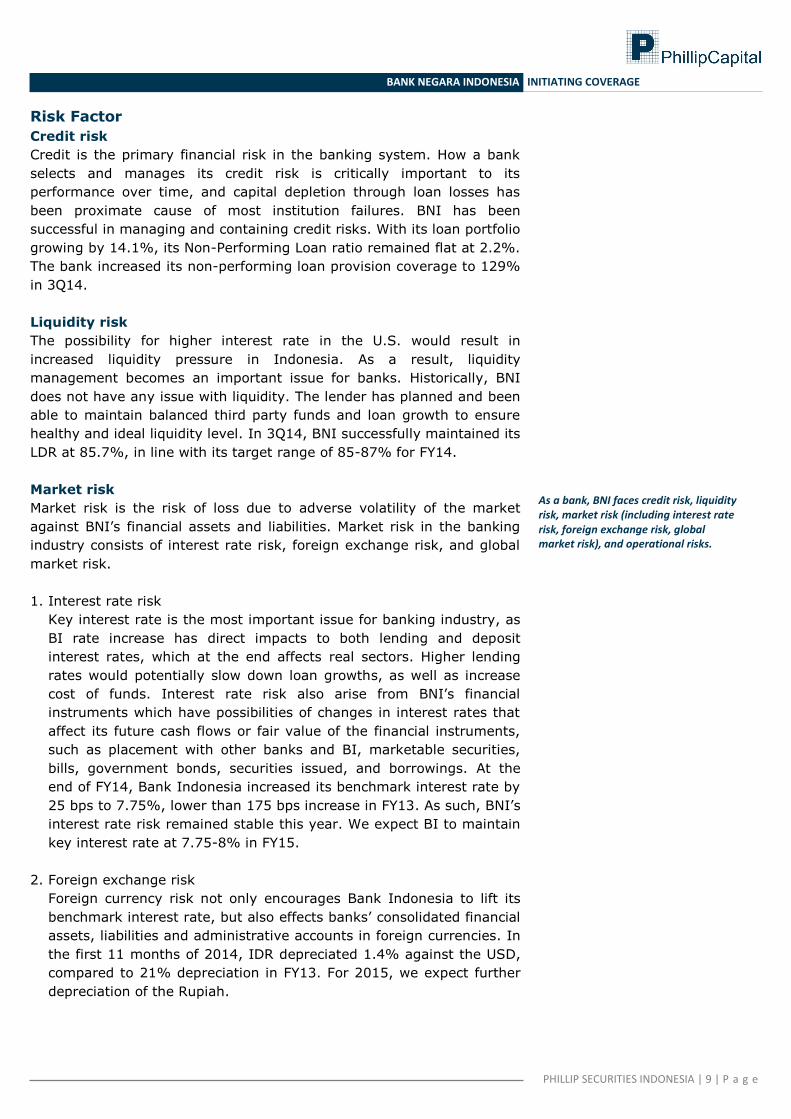

Risk Factor

Credit risk

Credit is the primary financial risk in the banking system. How a bank

selects and manages its credit risk is critically important to its

performance over time, and capital depletion through loan losses has

been proximate cause of most institution failures. BNI has been

successful in managing and containing credit risks. With its loan portfolio

growing by 14.1%, its Non-Performing Loan ratio remained flat at 2.2%.

The bank increased its non-performing loan provision coverage to 129%

in 3Q14.

Liquidity risk

The possibility for higher interest rate in the U.S. would result in

increased liquidity pressure in Indonesia. As a result, liquidity

management becomes an important issue for banks. Historically, BNI

does not have any issue with liquidity. The lender has planned and been

able to maintain balanced third party funds and loan growth to ensure

healthy and ideal liquidity level. In 3Q14, BNI successfully maintained its

LDR at 85.7%, in line with its target range of 85-87% for FY14.

Market risk

Market risk is the risk of loss due to adverse volatility of the market

against BNI’s financial assets and liabilities. Market risk in the banking

industry consists of interest rate risk, foreign exchange risk, and global

market risk.

1. Interest rate risk

Key interest rate is the most important issue for banking industry, as

BI rate increase has direct impacts to both lending and deposit

interest rates, which at the end affects real sectors. Higher lending

rates would potentially slow down loan growths, as well as increase

cost of funds. Interest rate risk also arise from BNI’s financial

instruments which have possibilities of changes in interest rates that

affect its future cash flows or fair value of the financial instruments,

such as placement with other banks and BI, marketable securities,

bills, government bonds, securities issued, and borrowings. At the

end of FY14, Bank Indonesia increased its benchmark interest rate by

25 bps to 7.75%, lower than 175 bps increase in FY13. As such, BNI’s

interest rate risk remained stable this year. We expect BI to maintain

key interest rate at 7.75-8% in FY15.

2. Foreign exchange risk

Foreign currency risk not only encourages Bank Indonesia to lift its

benchmark interest rate, but also effects banks’ consolidated financial

assets, liabilities and administrative accounts in foreign currencies. In

the first 11 months of 2014, IDR depreciated 1.4% against the USD,

compared to 21% depreciation in FY13. For 2015, we expect further

depreciation of the Rupiah.

As a bank, BNI faces credit risk, liquidity risk, market risk (including interest rate risk, foreign exchange risk, global market risk), and operational risks.

PHILLIP SECURITIES INDONESIA | 10 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

3. Global market risk

The economic slowdown in global markets, especially in China and

India as Indonesia’s top importers, could have negative impacts on

Indonesian banking industry. Slower demand from export markets

could reduce revenue growth in real sector, which in turn could slow

loan growth in the banking sector. Indonesia’s export value declined

by 2.21% yoy to USD 15.35 billion in October 2014, bringing current

account deficit to up to USD 270.3 million. Coupled with global

economic slowdown, several local factors such as rising inflation and

gradual increase in electricity tariffs will also weigh on Indonesia’s

economic growth.

Operational risk

Bank Indonesia (BI) said Indonesia needs to merge banks so that the

country’s lenders could compete in ASEAN region. Commission XI

overseeing financial affairs at the House of Representatives also

supports mergers between state-owned banks. This merger plan would

negatively effect BNI, since it would more likely be taken over by Bank

Mandiri. Banks that becomes unnaturally large would have more

complex financial and operational system. As a result, the system

becomes more fragile. If the two banks merged and became a larger

bank, the government will have to set aside a huge sum of money for

bailout funds if this huge lender were to collapse.

Investment Correlation

The correlation between BNI’s stock price and the Jakarta Composite

Index (JCI) has been 76.5% positive over the past 12 months. Among

Indonesian banks, BNI’s share price movement has higher correlation

with the JCI compared to the average banking sector correlation of

68.5%.

BNI’s share price movement among banking sector companies

and its correlation with the Jakarta Composite Index (JCI) over

the past 12 months

Source: Bloomberg, PSI Research

BNI’s share price movement has 76.5% positive correlation with the JCI over the past 12 months.

PHILLIP SECURITIES INDONESIA | 11 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Financial Review and Forecast

Loan Growth

Loans represent the largest component (65.67%) of BNI’s assets in

3Q14, growing by 14.1% from IDR 234.91 trillion in 3Q13 to IDR 267.94

trillion in 3Q14. We expect BNI to record a loan growth of 16% to IDR

277.59 trillion for FY14, in line with BNI’s loan growth target of 14-17%

this year, compared to IDR 250.64 trillion in FY13. BNI’s loans

performance until 3Q14 has represented 96.5% of our loans estimation,

hence we believe BNI will achieve our loan growth estimation this year.

In line with our expectation for a slower loan growth of 15.5% in the

banking industry in FY15, we assume BNI’s loans to grow at the similar

level. Considering the lender’s historical loan growth which stood above

industry average over the last 2 years, we surmise a 15.5% loan growth

as attainable in FY15. However, we are positive on growing demands for

syndicated loans from infrastructure sector next year, since BNI

participated in the government’s infrastructure fund pool with USD 234

million investment.

BNI’s total loan composition in 3Q14 and its 8 sector focus in

business banking

Source: Company

BNI loans were mainly disbursed to corporate segment, representing

44% of its total loans, followed by consumer segment which comprises

18.2% of total loans. With respect to loan growth during 3Q14, loan

declines in the small segment are attributed to the upgrading of some

small segment debtors to become middle segment customers. The

upgrade indicates that BNI has successfully helped business customers

to grow. The small business segment that now meets the criteria for

middle debtors amounts to IDR 38.3 trillion.

BNI has recorded loan of IDR 268 trillion until 3Q14 or 96.5% of our loan estimate of IDR 278 trillion in FY14.

PHILLIP SECURITIES INDONESIA | 12 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Deposit Growth

Customer deposits consisting of current accounts, savings, and time

deposits, represented the largest component (88.1%) of BNI’s liabilities

in 3Q14. Total customer deposits stood at IDR 308.33 trillion in 3Q14,

up by 11.9% from IDR 275.63 trillion in the same period in FY13. Based

on funding compositions, total funds from time deposits represented

38% of total customer deposits of IDR 117.12 trillion, while CASA

increased IDR 3 trillion or 1.6% yoy whereas CASA ratio decreased to

62% versus 68% in 3Q13.

We expect BNI to book customer deposit growth of 11.6% and 13% in

FY14 and FY15, respectively. With 3Q14 achievement of IDR 308.33

trillion, BNI has reached 94.7% of our customer deposit estimation for

FY14 of IDR 325.73 trillion. CASA only grew 1.6% yoy in 3Q14 or below

our estimation of 6.9% for FY14, while time deposits have grown

significantly by 32.8% or higher than our estimation of 21.8%.

However, these high-cost funds have increased BNI’s cost of funds to

3.2% in 3Q14, while we estimated 2.4% cost of funds in FY14.

BNI’s total customer deposits by type, by currencies, and by cost

Source: Company

Interest Rate Forecast

In line with our key interest rate assumption, we forecast average

interest rate for loans and deposits at 8.5% and 2.5% for FY14, flat

enough compared to FY13. We expect only small changes of 25 basis

points increase in our interest rate forecast for FY15. Based on

management’s guidance, BNI plans to maintain its interest rates to

avoid slower loan growth and higher cost of funds. After BI raised its

benchmark interest rate by 25 bps at the end of FY14, BNI does not

have any plan to adjust its interest rate.

BNI recorded customer deposits of IDR 308.33 trillion in 3Q14 or 94.7% of our estimation of IDR 325.73 trillion in FY14, with composition of 38% customer deposits and 62% CASA.

We forecast interest rates for loans and deposits to average at 8.5% and 2.5% in FY14, and expect only small changes of 25 bps for FY15.

PHILLIP SECURITIES INDONESIA | 13 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Earnings Forecast

We forecast BNI’s earnings by estimating banking industry’s loan size

compared to GDP growth and the key interest rate. We believe a 15.5%

loan growth is feasible in FY15 due to improving economic growth and

better strategies from BNI. Considering historical loan growth of 19%,

22%, and 24% respectively in FY11, FY12, and FY13, we surmise a

15.5% loan growth as attainable in FY15.

FY15 management guidance:

(1) Maintain NIM at the same level of 6%.

(2) Loan growth: 16.5-17.5% from FY14’s forecast of IDR 278

trillion.

(3) Maintain LDR at a comfortable level of 85-90%.

(4) Expanding its business by setting up a joint venture with

Sumitomo through BNI Life, building 76 new branch offices, and

adding new branches for BNI Syariah with a total investment of

IDR 500 billion.

(5) Branchless banking targets 3,000 agents to increase BNI’s

efficiency as well as to decrease its cost to income ratio.

(6) Focus on corporate loans and support the government’s program.

Based on our assumption, interest income is projected to grow 12.4%

CAGR in FY15-19F while net profit is forecast to rise by 14.9% CAGR

over the same period. We believe our key interest rate estimates to be

conservative and earnings forecast to be attainable with BNI’s continued

efforts to improve operational efficiency.

Interest income and net profit forecast for FY14-19F

3016434655

3769240318

4324147463

0

10000

20000

30000

40000

50000

FY09 FY10 FY11 FY12 FY13 FY14F FY15F FY16F FY17F FY18F FY19F

985611061

1250213723

1538416938

0

3000

6000

9000

12000

15000

18000

FY09 FY10 FY11 FY12 FY13 FY14F FY15F FY16F FY17F FY18F FY19F

Source: PSI Research Est.

Interest income is projected to grow 12.4% CAGR for FY15-19F while net profit is forecast to rise by 14.9% CAGR over the same period.

PHILLIP SECURITIES INDONESIA | 14 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Dividends: BNI’s dividend policy is determined every year through the

General Meeting of Shareholders (GMS). In FY13, BNI paid full-year

dividend of IDR 146, translating into payout ratio of 30%, or unchanged

compared to the previous year. We expect the same dividend payout

ratio of 30% for FY15-19.

BNI’s dividend and payout ratio over FY10-14F

0.0%

10.0%

20.0%

30.0%

40.0%

-

1,000,000

2,000,000

3,000,000

4,000,000

FY10 FY11 FY12 FY13 FY14F

Dividend (IDR mn) Dividend Payout

3016434655

3769240318

4324147463

0

10000

20000

30000

40000

50000

FY09 FY10 FY11 FY12 FY13 FY14F FY15F FY16F FY17F FY18F FY19F

985611061

1250213723

1538416938

0

3000

6000

9000

12000

15000

18000

FY09 FY10 FY11 FY12 FY13 FY14F FY15F FY16F FY17F FY18F FY19F

Source: PSI Research Est.

3Q14 Financial Performance

BNI, who reported higher net income, had seen its net profit increase by

16.4% yoy to IDR 7.61 trillion from January to September 2014, or

77.2% from our estimation of IDR 9.86 trillion for FY14. According to its

latest financial report, net interest income rose 18.6% to IDR 16.39

trillion, supported by higher lending, which grew 14.1% to IDR 308.33

trillion. This loan growth was in line with industry growth, which rose

14.0%.

Loan to Deposit Ratio (LDR) increased from 84.7% in 3Q13 to 85.7% in

3Q14, in line with BNI’s strategy in managing productive assets with

higher yields. On the other hand, its fee-based income remained flat by

2.0% to IDR 7.29 trillion. The majority of the fee-based income came

from provision and commissions (49.2%) which stood at IDR 3.59

trillion.

BNI managed to maintain its Net Interest Margin (NIM) at 6.1% amid

tightening liquidity issue faced by Indonesian banks. BNI also reduced

its Non Performing Loan (NPL) ratio to 2.2% in 3Q14 compared to 2.4%

in 3Q13, in line with its target of 1.8-2.2% in FY14. Loan to Deposit

Ratio (LDR) in 3Q14 reached 85.7%, thanks to its foreign currency loans

which grew 34.3% year-on-year. Capital Adequacy Ratio (CAR)

increased to 16.2% in 3Q14 from 15.7% in 3Q13. The CAR growth

showed the ability of BNI’s capital structure to anticipate credit risk,

operational risk, and market risk, as it was higher than the minimum

8% CAR set by Bank Indonesia.

In 3Q14, BNI reported net income of IDR 7.61 trillion, or 77.2% from our estimation of IDR 9.86 trillion.

PHILLIP SECURITIES INDONESIA | 15 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

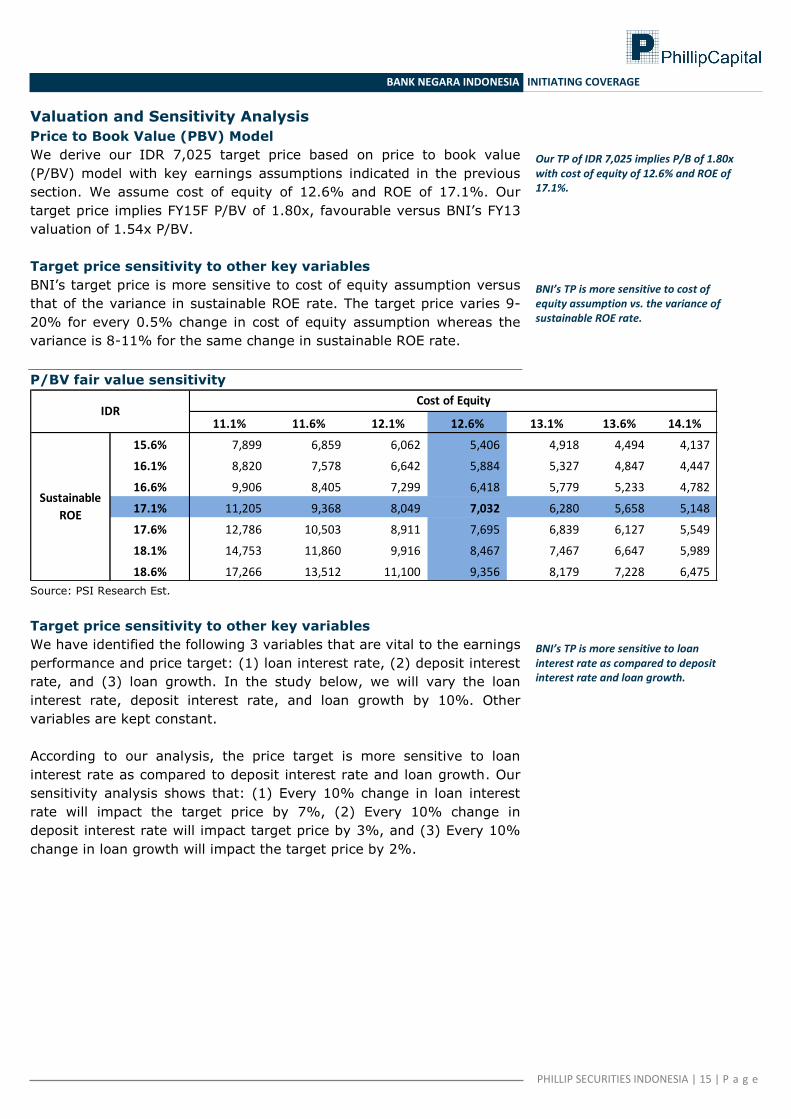

Valuation and Sensitivity Analysis

Price to Book Value (PBV) Model

We derive our IDR 7,025 target price based on price to book value

(P/BV) model with key earnings assumptions indicated in the previous

section. We assume cost of equity of 12.6% and ROE of 17.1%. Our

target price implies FY15F P/BV of 1.80x, favourable versus BNI’s FY13

valuation of 1.54x P/BV.

Target price sensitivity to other key variables

BNI’s target price is more sensitive to cost of equity assumption versus

that of the variance in sustainable ROE rate. The target price varies 9-

20% for every 0.5% change in cost of equity assumption whereas the

variance is 8-11% for the same change in sustainable ROE rate.

P/BV fair value sensitivity

11.1% 11.6% 12.1% 12.6% 13.1% 13.6% 14.1%

15.6% 7,899 6,859 6,062 5,406 4,918 4,494 4,137

16.1% 8,820 7,578 6,642 5,884 5,327 4,847 4,447

16.6% 9,906 8,405 7,299 6,418 5,779 5,233 4,782

17.1% 11,205 9,368 8,049 7,032 6,280 5,658 5,148

17.6% 12,786 10,503 8,911 7,695 6,839 6,127 5,549

18.1% 14,753 11,860 9,916 8,467 7,467 6,647 5,989

18.6% 17,266 13,512 11,100 9,356 8,179 7,228 6,475

IDRCost of Equity

Sustainable

ROE

IDR in M illion unless otherw ise stated

2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F

Loan Interest Rate (%) 7.65 7.92 7.65 8.50 8.80 8.50 9.35 9.68 9.35

Interest Income 27,902,407 32,061,105 34,708,228 30,164,024 34,603,622 37,635,765 32,425,640 37,452,466 40,563,302

EBIT 11,252,785 12,680,331 14,184,966 12,383,593 13,951,590 15,648,735 13,514,402 15,376,012 17,112,503

Net profit 8,915,210 9,994,452 11,277,147 9,856,460 11,052,609 12,495,543 10,797,711 12,238,255 13,713,940

BV (IDR) 2,892 3,267 3,690 2,927 3,342 3,811 2,962 3,422 3,936

Price target (IDR) 6,573 7,032 7,546

Deposit Interest Rate (%) 2.25 2.52 2.25 2.50 2.80 2.50 2.75 3.08 2.75

Interest Income 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765

EBIT 12,795,112 14,378,392 16,161,691 12,383,593 13,951,590 15,648,735 11,972,074 13,339,221 15,135,779

Net profit 10,267,817 11,479,242 13,008,296 9,856,460 11,052,609 12,495,543 9,445,104 10,440,483 11,982,790

BV (IDR) 2,942 3,373 3,862 2,927 3,342 3,811 2,911 3,303 3,753

Price target (IDR) 7,223 7,032 6,791

Loan Growth (%) 14.40 13.77 11.07 16.00 15.30 12.30 17.60 16.83 13.53

Interest Income 29,831,659 33,833,486 36,450,683 30,164,024 34,603,622 37,635,765 30,496,388 35,364,562 38,811,865

EBIT 12,241,777 13,642,002 15,189,157 12,383,593 13,951,590 15,648,735 12,525,410 14,257,205 16,105,055

Net profit 9,742,492 10,807,541 12,135,241 9,856,460 11,052,609 12,495,543 9,970,429 11,294,476 12,853,340

BV (IDR) 2,923 3,328 3,784 2,927 3,342 3,811 2,931 3,355 3,838

Price target (IDR) 6,914 7,032 7,150

Loan Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -7.50% -7.35% -7.78% 0.00% 0.00% 0.00% 7.50% 8.23% 7.78%

EBITDA -9.13% -9.11% -9.35% 0.00% 0.00% 0.00% 9.13% 10.21% 9.35%

Net profit -9.55% -9.57% -9.75% 0.00% 0.00% 0.00% 9.55% 10.73% 9.75%

BV (IDR) -1.21% -2.25% -3.17% 0.00% 0.00% 0.00% 1.21% 2.39% 3.30%

Price target (IDR) -6.54% 0.00% 7.30%

Deposit Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

EBITDA 3.32% 3.06% 3.28% 0.00% 0.00% 0.00% -3.32% -4.39% -3.28%

Net profit 4.17% 3.86% 4.10% 0.00% 0.00% 0.00% -4.17% -5.54% -4.10%

BV (IDR) 0.53% 0.94% 1.33% 0.00% 0.00% 0.00% -0.53% -1.15% -1.51%

Price target (IDR) 2.71% 0.00% -3.44%

Loan Growth (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -1.10% -2.23% -3.15% 0.00% 0.00% 0.00% 1.10% 2.20% 3.12%

EBITDA -1.15% -2.22% -2.94% 0.00% 0.00% 0.00% 1.15% 2.19% 2.92%

Net profit -1.16% -2.22% -2.88% 0.00% 0.00% 0.00% 1.16% 2.19% 2.86%

BV (IDR) -0.15% -0.40% -0.71% 0.00% 0.00% 0.00% 0.15% 0.40% 0.70%

Price target (IDR) -1.68% 0.00% 1.68%

% Changes

K e y F in a n cia l S u m m a r y

F Y E D e c F Y 1 2 F Y 1 3 F Y 1 4 F F Y 1 5 F F Y 1 6 F

N e t in te r e s t in c o m e ( ID R m n ) 1 5 ,4 5 8 ,9 9 1 1 9 ,1 4 9 ,2 8 1 2 0 ,9 3 6 ,9 8 9 2 3 ,3 0 1 ,1 6 2 2 6 ,1 7 0 ,6 9 6

N o n in te r e s t in c o m e ( ID R m n ) 8 ,4 4 5 ,8 1 3 9 ,4 4 0 ,9 0 4 1 0 ,5 5 3 ,2 3 7 1 1 ,7 9 6 ,6 2 6 1 3 ,1 8 6 ,5 1 2

N P A T . A d j. ( ID R m n ) 6 ,7 8 9 ,8 2 3 9 ,0 8 9 ,5 7 9 9 ,8 6 0 ,3 6 1 1 1 ,0 5 6 ,9 8 3 1 2 ,5 0 0 ,4 8 9

E P S , a d j. ( ID R ) 3 7 8 4 9 0 5 2 9 5 9 3 6 7 0

P / E (X ) , a d j. 9 .7 9 8 .0 5 1 1 .3 5 1 0 .1 2 8 .9 5

B V P S ( ID R ) 2 ,3 3 4 2 ,5 5 7 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1

P / B (X ) 1 .5 9 1 .5 4 2 .0 5 1 .8 0 1 .5 7

D P S ( ID R ) 1 1 3 1 4 6 1 5 9 1 7 8 2 0 1

D iv . Y ie ld (% ) 3 .0 6 % 3 .6 9 % 2 .6 4 % 2 .9 6 % 3 .3 5 %

S o u r c e : B lo o m b e r g , P S I R e s e a r c h E s t.

Source: PSI Research Est.

Target price sensitivity to other key variables

We have identified the following 3 variables that are vital to the earnings

performance and price target: (1) loan interest rate, (2) deposit interest

rate, and (3) loan growth. In the study below, we will vary the loan

interest rate, deposit interest rate, and loan growth by 10%. Other

variables are kept constant.

According to our analysis, the price target is more sensitive to loan

interest rate as compared to deposit interest rate and loan growth. Our

sensitivity analysis shows that: (1) Every 10% change in loan interest

rate will impact the target price by 7%, (2) Every 10% change in

deposit interest rate will impact target price by 3%, and (3) Every 10%

change in loan growth will impact the target price by 2%.

Our TP of IDR 7,025 implies P/B of 1.80x with cost of equity of 12.6% and ROE of 17.1%.

BNI’s TP is more sensitive to cost of equity assumption vs. the variance of sustainable ROE rate.

BNI’s TP is more sensitive to loan interest rate as compared to deposit interest rate and loan growth.

PHILLIP SECURITIES INDONESIA | 16 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

BNI’s earnings and price target analysis

IDR in Million unless otherwise stated

2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F

Loan Interest Rate (%) 7.65 7.92 7.65 8.50 8.80 8.50 9.35 9.68 9.35

Interest Income 27,902,407 32,061,105 34,708,228 30,164,024 34,603,622 37,635,765 32,425,640 37,452,466 40,563,302

EBIT 11,252,785 12,680,331 14,184,966 12,383,593 13,951,590 15,648,735 13,514,402 15,376,012 17,112,503

Net profit 8,915,210 9,994,452 11,277,147 9,856,460 11,052,609 12,495,543 10,797,711 12,238,255 13,713,940

BV (IDR) 2,892 3,267 3,690 2,927 3,342 3,811 2,962 3,422 3,936

Price target (IDR) 6,573 7,032 7,546

Deposit Interest Rate (%) 2.25 2.52 2.25 2.50 2.80 2.50 2.75 3.08 2.75

Interest Income 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765

EBIT 12,795,112 14,378,392 16,161,691 12,383,593 13,951,590 15,648,735 11,972,074 13,339,221 15,135,779

Net profit 10,267,817 11,479,242 13,008,296 9,856,460 11,052,609 12,495,543 9,445,104 10,440,483 11,982,790

BV (IDR) 2,942 3,373 3,862 2,927 3,342 3,811 2,911 3,303 3,753

Price target (IDR) 7,223 7,032 6,791

Loan Growth (%) 14.40 13.77 11.07 16.00 15.30 12.30 17.60 16.83 13.53

Interest Income 29,831,659 33,833,486 36,450,683 30,164,024 34,603,622 37,635,765 30,496,388 35,364,562 38,811,865

EBIT 12,241,777 13,642,002 15,189,157 12,383,593 13,951,590 15,648,735 12,525,410 14,257,205 16,105,055

Net profit 9,742,492 10,807,541 12,135,241 9,856,460 11,052,609 12,495,543 9,970,429 11,294,476 12,853,340

BV (IDR) 2,923 3,328 3,784 2,927 3,342 3,811 2,931 3,355 3,838

Price target (IDR) 6,914 7,032 7,150

Loan Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -7.50% -7.35% -7.78% 0.00% 0.00% 0.00% 7.50% 8.23% 7.78%

EBITDA -9.13% -9.11% -9.35% 0.00% 0.00% 0.00% 9.13% 10.21% 9.35%

Net profit -9.55% -9.57% -9.75% 0.00% 0.00% 0.00% 9.55% 10.73% 9.75%

BV (IDR) -1.21% -2.25% -3.17% 0.00% 0.00% 0.00% 1.21% 2.39% 3.30%

Price target (IDR) -6.54% 0.00% 7.30%

Deposit Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

EBITDA 3.32% 3.06% 3.28% 0.00% 0.00% 0.00% -3.32% -4.39% -3.28%

Net profit 4.17% 3.86% 4.10% 0.00% 0.00% 0.00% -4.17% -5.54% -4.10%

BV (IDR) 0.53% 0.94% 1.33% 0.00% 0.00% 0.00% -0.53% -1.15% -1.51%

Price target (IDR) 2.71% 0.00% -3.44%

Loan Growth (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -1.10% -2.23% -3.15% 0.00% 0.00% 0.00% 1.10% 2.20% 3.12%

EBITDA -1.15% -2.22% -2.94% 0.00% 0.00% 0.00% 1.15% 2.19% 2.92%

Net profit -1.16% -2.22% -2.88% 0.00% 0.00% 0.00% 1.16% 2.19% 2.86%

BV (IDR) -0.15% -0.40% -0.71% 0.00% 0.00% 0.00% 0.15% 0.40% 0.70%

Price target (IDR) -1.68% 0.00% 1.68%

% Changes

Base Estimates +10% vs. Base-10% vs. Base

Key Financial Summary

FYE Dec FY12 FY13 FY14F FY15F FY16F

Net interest incom e (IDR m n) 15,458,991 19,149,281 20,936,989 23,301,162 26,170,696

Non interest incom e (IDR m n) 8,445,813 9,440,904 10,553,237 11,796,626 13,186,512

NPAT. Adj. (IDR m n) 6,789,823 9,089,579 9,860,361 11,056,983 12,500,489

EPS, adj. (IDR) 378 490 529 593 670

P/E (X), adj. 9.79 8.05 11.35 10.12 8.95

BVPS (IDR) 2,334 2,557 2,927 3,342 3,811

P/B (X) 1.59 1.54 2.05 1.80 1.57

DPS (IDR) 113 146 159 178 201

Div. Yield (%) 3.06% 3.69% 2.64% 2.96% 3.35%

Source: Bloom berg, PSI Research Est.

Source: PSI Research Est.

PHILLIP SECURITIES INDONESIA | 17 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Peer group valuation comparison

P/B (x) ROE ROA Div. Yield

Company Ticker Market Cap 2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F

(USD Bn) 14y 15y 16y 14y 15y 16y 14y 15y 16y 14y 15y 16y

Bank Negara Indonesia BBNI IJ 8.95 2.05 1.80 1.58 17.96 17.69 17.52 2.26 2.26 2.30 2.46 2.79 3.17

Indonesia

Bank Mandiri BMRI IJ 19.88 2.42 2.09 1.81 20.94 20.73 20.5 2.65 2.68 2.71 2.33 2.60 2.93

Bank Rakyat Indonesia BBRI IJ 22.42 2.89 2.40 2.00 27.17 25.43 24.24 3.64 3.50 3.50 2.40 2.68 10.24

Bank Central Asia BBCA IJ 26.45 4.23 3.56 3.01 23.4 22.32 21.28 3.12 3.18 3.16 1.06 1.28 1.5

Bank Danamon BDMN IJ 3.43 1.27 1.18 1.09 9.55 10.31 11.26 1.66 1.74 1.86 2.45 2.49 2.89

Mean 2.57 2.21 1.90 19.80 19.30 18.96 2.67 2.67 2.71 2.14 2.37 4.15

Median 2.42 2.09 1.81 20.94 20.73 20.5 2.65 2.68 2.71 2.40 2.60 2.93

Malaysia

CIMB CIMB MK 13.09 1.24 1.16 1.08 12.04 12.09 12.52 1.05 1.12 1.15 3.83 4.34 4.90

Maybank MAY MK 23.75 1.59 1.49 1.40 13.48 13.38 13.48 1.13 1.14 1.17 5.92 6.23 6.43

Public Bank PBK MK 20.08 2.52 2.32 2.13 18.04 16.84 16.65 1.38 1.36 1.34 2.93 3.10 3.35

Mean 1.78 1.66 1.54 14.52 14.10 14.22 1.19 1.21 1.22 4.23 4.56 4.89

Median 1.59 1.49 1.40 13.48 13.38 13.48 1.13 1.14 1.17 3.83 4.34 4.90

Singapore

United Overseas Bank UOB SP 29.63 1.44 1.33 1.24 11.98 11.62 11.77 1.08 1.06 1.08 3.09 3.24 3.5

DBS Group DBS SP 37.27 1.33 1.24 1.15 11.38 11.35 11.86 0.96 0.98 1.04 3.02 3.21 3.52

OCBC OCBC SP 31.46 1.36 1.26 1.17 13.01 12.1 12.42 1.02 0.98 1.01 3.42 3.63 3.91

Mean 1.38 1.28 1.19 12.12 11.69 12.02 1.02 1.01 1.04 3.18 3.36 3.64

Median 1.36 1.26 1.17 11.98 11.62 11.86 1.02 0.98 1.04 3.09 3.24 3.52

Overall industry mean 2.03 1.80 1.61 16.27 15.81 15.77 1.81 1.82 1.85 2.99 3.24 4.21

Overall industry median 1.59 1.49 1.40 13.48 13.38 13.48 1.38 1.36 1.34 2.93 3.10 3.50

11.1% 11.6% 12.1% 12.6% 13.1% 13.6% 14.1%

15.6% 7,899 6,859 6,062 5,406 4,918 4,494 4,137

16.1% 8,820 7,578 6,642 5,884 5,327 4,847 4,447

16.6% 9,906 8,405 7,299 6,418 5,779 5,233 4,782

17.1% 11,205 9,368 8,049 7,032 6,280 5,658 5,148

17.6% 12,786 10,503 8,911 7,695 6,839 6,127 5,549

18.1% 14,753 11,860 9,916 8,467 7,467 6,647 5,989

18.6% 17,266 13,512 11,100 9,356 8,179 7,228 6,475

IDR

Sustainable

ROE

ID R in M illio n u n le s s o t h e r w is e s t a t e d

2 0 1 4 F 2 0 1 5 F 2 0 1 6 F 2 0 1 4 F 2 0 1 5 F 2 0 1 6 F 2 0 1 4 F 2 0 1 5 F 2 0 1 6 F

L o a n In te r e s t R a te (% ) 7 .6 5 7 .9 2 7 .6 5 8 .5 0 8 .8 0 8 .5 0 9 .3 5 9 .6 8 9 .3 5

In te r e s t In c o m e 2 7 ,9 0 2 ,4 0 7 3 2 ,0 6 1 ,1 0 5 3 4 ,7 0 8 ,2 2 8 3 0 ,1 6 4 ,0 2 4 3 4 ,6 0 3 ,6 2 2 3 7 ,6 3 5 ,7 6 5 3 2 ,4 2 5 ,6 4 0 3 7 ,4 5 2 ,4 6 6 4 0 ,5 6 3 ,3 0 2

E B IT 1 1 ,2 5 2 ,7 8 5 1 2 ,6 8 0 ,3 3 1 1 4 ,1 8 4 ,9 6 6 1 2 ,3 8 3 ,5 9 3 1 3 ,9 5 1 ,5 9 0 1 5 ,6 4 8 ,7 3 5 1 3 ,5 1 4 ,4 0 2 1 5 ,3 7 6 ,0 1 2 1 7 ,1 1 2 ,5 0 3

N e t p r o f it 8 ,9 1 5 ,2 1 0 9 ,9 9 4 ,4 5 2 1 1 ,2 7 7 ,1 4 7 9 ,8 5 6 ,4 6 0 1 1 ,0 5 2 ,6 0 9 1 2 ,4 9 5 ,5 4 3 1 0 ,7 9 7 ,7 1 1 1 2 ,2 3 8 ,2 5 5 1 3 ,7 1 3 ,9 4 0

B V ( ID R ) 2 ,8 9 2 3 ,2 6 7 3 ,6 9 0 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1 2 ,9 6 2 3 ,4 2 2 3 ,9 3 6

P r ic e ta r g e t ( ID R ) 6 ,5 7 3 7 ,0 3 2 7 ,5 4 6

D e p o s it In te r e s t R a te (% ) 2 .2 5 2 .5 2 2 .2 5 2 .5 0 2 .8 0 2 .5 0 2 .7 5 3 .0 8 2 .7 5

In te r e s t In c o m e 3 0 ,1 6 4 ,0 2 4 3 4 ,6 0 3 ,6 2 2 3 7 ,6 3 5 ,7 6 5 3 0 ,1 6 4 ,0 2 4 3 4 ,6 0 3 ,6 2 2 3 7 ,6 3 5 ,7 6 5 3 0 ,1 6 4 ,0 2 4 3 4 ,6 0 3 ,6 2 2 3 7 ,6 3 5 ,7 6 5

E B IT 1 2 ,7 9 5 ,1 1 2 1 4 ,3 7 8 ,3 9 2 1 6 ,1 6 1 ,6 9 1 1 2 ,3 8 3 ,5 9 3 1 3 ,9 5 1 ,5 9 0 1 5 ,6 4 8 ,7 3 5 1 1 ,9 7 2 ,0 7 4 1 3 ,3 3 9 ,2 2 1 1 5 ,1 3 5 ,7 7 9

N e t p r o f it 1 0 ,2 6 7 ,8 1 7 1 1 ,4 7 9 ,2 4 2 1 3 ,0 0 8 ,2 9 6 9 ,8 5 6 ,4 6 0 1 1 ,0 5 2 ,6 0 9 1 2 ,4 9 5 ,5 4 3 9 ,4 4 5 ,1 0 4 1 0 ,4 4 0 ,4 8 3 1 1 ,9 8 2 ,7 9 0

B V ( ID R ) 2 ,9 4 2 3 ,3 7 3 3 ,8 6 2 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1 2 ,9 1 1 3 ,3 0 3 3 ,7 5 3

P r ic e ta r g e t ( ID R ) 7 ,2 2 3 7 ,0 3 2 6 ,7 9 1

L o a n G r o w th (% ) 1 4 .4 0 1 3 .7 7 1 1 .0 7 1 6 .0 0 1 5 .3 0 1 2 .3 0 1 7 .6 0 1 6 .8 3 1 3 .5 3

In te r e s t In c o m e 2 9 ,8 3 1 ,6 5 9 3 3 ,8 3 3 ,4 8 6 3 6 ,4 5 0 ,6 8 3 3 0 ,1 6 4 ,0 2 4 3 4 ,6 0 3 ,6 2 2 3 7 ,6 3 5 ,7 6 5 3 0 ,4 9 6 ,3 8 8 3 5 ,3 6 4 ,5 6 2 3 8 ,8 1 1 ,8 6 5

E B IT 1 2 ,2 4 1 ,7 7 7 1 3 ,6 4 2 ,0 0 2 1 5 ,1 8 9 ,1 5 7 1 2 ,3 8 3 ,5 9 3 1 3 ,9 5 1 ,5 9 0 1 5 ,6 4 8 ,7 3 5 1 2 ,5 2 5 ,4 1 0 1 4 ,2 5 7 ,2 0 5 1 6 ,1 0 5 ,0 5 5

N e t p r o f it 9 ,7 4 2 ,4 9 2 1 0 ,8 0 7 ,5 4 1 1 2 ,1 3 5 ,2 4 1 9 ,8 5 6 ,4 6 0 1 1 ,0 5 2 ,6 0 9 1 2 ,4 9 5 ,5 4 3 9 ,9 7 0 ,4 2 9 1 1 ,2 9 4 ,4 7 6 1 2 ,8 5 3 ,3 4 0

B V ( ID R ) 2 ,9 2 3 3 ,3 2 8 3 ,7 8 4 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1 2 ,9 3 1 3 ,3 5 5 3 ,8 3 8

P r ic e ta r g e t ( ID R ) 6 ,9 1 4 7 ,0 3 2 7 ,1 5 0

L o a n In te r e s t R a te (% ) -1 0 .0 0 % -1 0 .0 0 % -1 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 %

S a le s -7 .5 0 % -7 .3 5 % -7 .7 8 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 7 .5 0 % 8 .2 3 % 7 .7 8 %

E B IT D A -9 .1 3 % -9 .1 1 % -9 .3 5 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 9 .1 3 % 1 0 .2 1 % 9 .3 5 %

N e t p r o f it -9 .5 5 % -9 .5 7 % -9 .7 5 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 9 .5 5 % 1 0 .7 3 % 9 .7 5 %

B V ( ID R ) -1 .2 1 % -2 .2 5 % -3 .1 7 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 .2 1 % 2 .3 9 % 3 .3 0 %

P r ic e ta r g e t ( ID R ) -6 .5 4 % 0 .0 0 % 7 .3 0 %

D e p o s it In te r e s t R a te (% ) -1 0 .0 0 % -1 0 .0 0 % -1 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 %

S a le s 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 %

E B IT D A 3 .3 2 % 3 .0 6 % 3 .2 8 % 0 .0 0 % 0 .0 0 % 0 .0 0 % -3 .3 2 % -4 .3 9 % -3 .2 8 %

N e t p r o f it 4 .1 7 % 3 .8 6 % 4 .1 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % -4 .1 7 % -5 .5 4 % -4 .1 0 %

B V ( ID R ) 0 .5 3 % 0 .9 4 % 1 .3 3 % 0 .0 0 % 0 .0 0 % 0 .0 0 % -0 .5 3 % -1 .1 5 % -1 .5 1 %

P r ic e ta r g e t ( ID R ) 2 .7 1 % 0 .0 0 % -3 .4 4 %

L o a n G r o w th (% ) -1 0 .0 0 % -1 0 .0 0 % -1 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 % 1 0 .0 0 %

S a le s -1 .1 0 % -2 .2 3 % -3 .1 5 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 .1 0 % 2 .2 0 % 3 .1 2 %

E B IT D A -1 .1 5 % -2 .2 2 % -2 .9 4 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 .1 5 % 2 .1 9 % 2 .9 2 %

N e t p r o f it -1 .1 6 % -2 .2 2 % -2 .8 8 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 1 .1 6 % 2 .1 9 % 2 .8 6 %

B V ( ID R ) -0 .1 5 % -0 .4 0 % -0 .7 1 % 0 .0 0 % 0 .0 0 % 0 .0 0 % 0 .1 5 % 0 .4 0 % 0 .7 0 %

P r ic e ta r g e t ( ID R ) -1 .6 8 % 0 .0 0 % 1 .6 8 %

% C h a n g e s

K e y F in a n c ia l S u m m a r y

F Y E D e c F Y 1 2 F Y 1 3 F Y 1 4 F F Y 1 5 F F Y 1 6 F

N e t i n t e r e s t i n c o m e ( ID R m n ) 1 5 ,4 5 8 ,9 9 1 1 9 ,1 4 9 ,2 8 1 2 0 ,9 3 6 ,9 8 9 2 3 ,3 0 1 ,1 6 2 2 6 ,1 7 0 ,6 9 6

N o n i n t e r e s t i n c o m e ( ID R m n ) 8 ,4 4 5 ,8 1 3 9 ,4 4 0 ,9 0 4 1 0 ,5 5 3 ,2 3 7 1 1 ,7 9 6 ,6 2 6 1 3 ,1 8 6 ,5 1 2

N P A T . A d j . ( ID R m n ) 6 ,7 8 9 ,8 2 3 9 ,0 8 9 ,5 7 9 9 ,8 6 0 ,3 6 1 1 1 ,0 5 6 ,9 8 3 1 2 ,5 0 0 ,4 8 9

E P S , a d j . ( ID R ) 3 7 8 4 9 0 5 2 9 5 9 3 6 7 0

P / E ( X ) , a d j . 9 .7 9 8 .0 5 1 1 .3 5 1 0 .1 2 8 .9 5

B V P S ( ID R ) 2 ,3 3 4 2 ,5 5 7 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1

P / B ( X ) 1 .5 9 1 .5 4 2 .0 5 1 .8 0 1 .5 7

D P S ( ID R ) 1 1 3 1 4 6 1 5 9 1 7 8 2 0 1

D i v . Y i e l d ( % ) 3 .0 6 % 3 .6 9 % 2 .6 4 % 2 .9 6 % 3 .3 5 %

S o u r c e : B l o o m b e r g , P S I R e s e a r c h E s t .

IDR in M illion unless otherw ise stated

2014F 2015F 2016F 2014F 2015F 2016F 2014F 2015F 2016F

Loan Interest Rate (%) 7.65 7.92 7.65 8.50 8.80 8.50 9.35 9.68 9.35

Interest Income 27,902,407 32,061,105 34,708,228 30,164,024 34,603,622 37,635,765 32,425,640 37,452,466 40,563,302

EBIT 11,252,785 12,680,331 14,184,966 12,383,593 13,951,590 15,648,735 13,514,402 15,376,012 17,112,503

Net profit 8,915,210 9,994,452 11,277,147 9,856,460 11,052,609 12,495,543 10,797,711 12,238,255 13,713,940

BV (IDR) 2,892 3,267 3,690 2,927 3,342 3,811 2,962 3,422 3,936

Price target (IDR) 6,573 7,032 7,546

Deposit Interest Rate (%) 2.25 2.52 2.25 2.50 2.80 2.50 2.75 3.08 2.75

Interest Income 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765 30,164,024 34,603,622 37,635,765

EBIT 12,795,112 14,378,392 16,161,691 12,383,593 13,951,590 15,648,735 11,972,074 13,339,221 15,135,779

Net profit 10,267,817 11,479,242 13,008,296 9,856,460 11,052,609 12,495,543 9,445,104 10,440,483 11,982,790

BV (IDR) 2,942 3,373 3,862 2,927 3,342 3,811 2,911 3,303 3,753

Price target (IDR) 7,223 7,032 6,791

Loan Growth (%) 14.40 13.77 11.07 16.00 15.30 12.30 17.60 16.83 13.53

Interest Income 29,831,659 33,833,486 36,450,683 30,164,024 34,603,622 37,635,765 30,496,388 35,364,562 38,811,865

EBIT 12,241,777 13,642,002 15,189,157 12,383,593 13,951,590 15,648,735 12,525,410 14,257,205 16,105,055

Net profit 9,742,492 10,807,541 12,135,241 9,856,460 11,052,609 12,495,543 9,970,429 11,294,476 12,853,340

BV (IDR) 2,923 3,328 3,784 2,927 3,342 3,811 2,931 3,355 3,838

Price target (IDR) 6,914 7,032 7,150

Loan Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -7.50% -7.35% -7.78% 0.00% 0.00% 0.00% 7.50% 8.23% 7.78%

EBITDA -9.13% -9.11% -9.35% 0.00% 0.00% 0.00% 9.13% 10.21% 9.35%

Net profit -9.55% -9.57% -9.75% 0.00% 0.00% 0.00% 9.55% 10.73% 9.75%

BV (IDR) -1.21% -2.25% -3.17% 0.00% 0.00% 0.00% 1.21% 2.39% 3.30%

Price target (IDR) -6.54% 0.00% 7.30%

Deposit Interest Rate (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00% 0.00%

EBITDA 3.32% 3.06% 3.28% 0.00% 0.00% 0.00% -3.32% -4.39% -3.28%

Net profit 4.17% 3.86% 4.10% 0.00% 0.00% 0.00% -4.17% -5.54% -4.10%

BV (IDR) 0.53% 0.94% 1.33% 0.00% 0.00% 0.00% -0.53% -1.15% -1.51%

Price target (IDR) 2.71% 0.00% -3.44%

Loan Growth (%) -10.00% -10.00% -10.00% 0.00% 0.00% 0.00% 10.00% 10.00% 10.00%

Sales -1.10% -2.23% -3.15% 0.00% 0.00% 0.00% 1.10% 2.20% 3.12%

EBITDA -1.15% -2.22% -2.94% 0.00% 0.00% 0.00% 1.15% 2.19% 2.92%

Net profit -1.16% -2.22% -2.88% 0.00% 0.00% 0.00% 1.16% 2.19% 2.86%

BV (IDR) -0.15% -0.40% -0.71% 0.00% 0.00% 0.00% 0.15% 0.40% 0.70%

Price target (IDR) -1.68% 0.00% 1.68%

-10% vs. Base

K e y F in a n cia l S u m m a r y

F Y E D e c F Y 1 2 F Y 1 3 F Y 1 4 F F Y 1 5 F F Y 1 6 F

N e t in te r e s t in c o m e ( ID R m n ) 1 5 ,4 5 8 ,9 9 1 1 9 ,1 4 9 ,2 8 1 2 0 ,9 3 6 ,9 8 9 2 3 ,3 0 1 ,1 6 2 2 6 ,1 7 0 ,6 9 6

N o n in te r e s t in c o m e ( ID R m n ) 8 ,4 4 5 ,8 1 3 9 ,4 4 0 ,9 0 4 1 0 ,5 5 3 ,2 3 7 1 1 ,7 9 6 ,6 2 6 1 3 ,1 8 6 ,5 1 2

N P A T . A d j. ( ID R m n ) 6 ,7 8 9 ,8 2 3 9 ,0 8 9 ,5 7 9 9 ,8 6 0 ,3 6 1 1 1 ,0 5 6 ,9 8 3 1 2 ,5 0 0 ,4 8 9

E P S , a d j. ( ID R ) 3 7 8 4 9 0 5 2 9 5 9 3 6 7 0

P / E ( X ) , a d j. 9 .7 9 8 .0 5 1 1 .3 5 1 0 .1 2 8 .9 5

B V P S ( ID R ) 2 ,3 3 4 2 ,5 5 7 2 ,9 2 7 3 ,3 4 2 3 ,8 1 1

P / B ( X ) 1 .5 9 1 .5 4 2 .0 5 1 .8 0 1 .5 7

D P S ( ID R ) 1 1 3 1 4 6 1 5 9 1 7 8 2 0 1

D iv . Y ie ld (% ) 3 .0 6 % 3 .6 9 % 2 .6 4 % 2 .9 6 % 3 .3 5 %

S o u r c e : B lo o m b e r g , P S I R e s e a r c h E s t.

Source: PSI Research Est.

PHILLIP SECURITIES INDONESIA | 18 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Company Profile

Company Background

Founded in 1946 as the first wholly-owned state bank, BNI began its

history by serving as the first central bank of Indonesia, before

assuming its status as a commercial bank back in 1955. BNI became the

first State-Owned Enterprise (SOE) bank to go public by listing its

shares on the Jakarta Stock Exchanges in 1996. To further strengthen

its financial structure and competitive edge in the national banking

industry, BNI conducted a series of corporate actions, such as

recapitalization by the Government in 1991, divestment of the

Government’s shares in 1997, and a rights issue in 2011. By the end of

2011, the Government of the Republic of Indonesia held 60% of stake

BNI, with the remaining 40% held by individuals and institutional

shareholders, domestic as well as overseas.

BNI Milestones

Source: Company

Company Overview

Offering various financial products and services, BNI currently is the

fourth largest bank in Indonesia in terms of total assets, lending and

third-party funds. In providing comprehensive financial services, BNI is

supported by its subsidiaries, namely Bank BNI Syariah, BNI Multi

Finance, BNI Securities, and BNI Life Insurance. By the end of 2013,

BNI had total assets of IDR 388.2 trillion and a total of 26,100

employees. BNI operates a wide ranging service network, comprising

1,693 domestic outlets and overseas branches in New York, London,

Tokyo, Hong Kong, Singapore, and Osaka. BNI is able to provide

complete trade finance services to its corporate clients, assisting

exports, imports and remittances, and also essential treasury services

such as foreign exchange transactions and hedging. BNI’s current ATM

network consists of 13,370 proprietary ATMs. BNI also serves its

customers through 42,000 EDC, as well as through Internet banking and

SMS banking.

BNI was the first wholly-owned state bank, founded in 1946. By FY11, the Government holds 60% stake in BNI.

PHILLIP SECURITIES INDONESIA | 19 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

BNI Network and Distribution

Source: Company

Business Model and Business Segment

Purposes: BNI strives to become a bank that ‘excels’ in terms of quality

human capital and internal business processes that provide value for

customers through improvements and innovation as well as quality

banking management with measured risks. ‘Prominent’ means to be the

bank of choice with superior service quality, which will lead BNI to be

the ‘advanced’ bank relative to its peers in terms of financial

performance, profitability and growth, and thus providing quality

investments for the satisfaction of stakeholders.

Process: To achieve its long-term objective, BNI implemented a multi-

prolonged approach to growth as follows: (1) Provide excellent services

and value added solutions to all customers as the banking partner of

choice, (2) Enhance investment value for investors, (3) Provide the best

environment for its employees, to be the source of pride to perform and

excel, (4) Improve social and environmental responsibility, and (5) To

be the benchmark for compliance and good corporate governance

practices.

BNI Business Concept

BNI had equity participation in 10 subsidiaries

Source: Company

PHILLIP SECURITIES INDONESIA | 20 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

BNI focuses on quality asset growth by targeting key sectors, supported

by 10 subsidiaries. BNI’s subsidiaries were established to support the

provision of one stop financial service, including banking products,

insurance, financing, capital, and remittance.

1. Bank BNI Syariah

PT Bank BNI Syariah is the result of a spin-off from BNI’s Sharia

Business Unit. Micro financing, productive retail and Griya Hasanah

products to become the champion products. By FY13, BNI Syariah

operated a total of 282 outlets, comprised 49 regular branches, 15

micro branches, 95 regular sub branches, 66 micro sub branches, 17

cash offices, 22 BNI Syariah mobile services and 20 payment points.

2. BNI Securities

The main business of BNI Securities is securities brokerage and

underwriting. BNI Securities also established a strategic alliance with

SBI Securities Co. Ltd., a securities company in Japan. In FY13, BNI

securities operated 66 branches throughout Indonesia with 15,741

active customers from a total of 22,210 customers. Indonesia’s

capital market is expected to continue growing, supported by stable

economic growth and strong investor growth.

3. BNI Multi Finance

BNI Multi Finance is a subsidiary of BNI operating in the consumer

financing sector, specifically in car ownership financing and capital

goods leasing business. BNI Multi Finance operates 9 branch offices in

Indonesia and also acquired BNI Oto’s financing business in FY13.

Going forward, BNI Multi Finance will also offer Multi Product

Financing solutions for consumer products, such as electronics and

household equipment.

4. BNI Life Insurance

BNI Life Insurance focuses on accelerating business growth, service

quality improvement and strategic alliance development. In FY13, BNI

announced a strategic partnership with Sumitomo Life that will be

implemented via a subscription of IDR 4.2 trillion worth of new shares

issued by BNI Life Insurance. Indonesia’s life insurance industry is

expected to continue growing, supported by the country’s strong

macro economy fundamentals, political stability and fast growing

middle class segment. Indonesia remains an attractive life insurance

market, given that the country has the largest population in South

East Asia with low insurance penetration relative to the GDP.

5. BNI Remittance Ltd

BNI Remittance Ltd. (BRL) is a subsidiary established by BNI Hong

Kong branch in FY96 as “High Motivation Company”, before becoming

BNI Remittance Limited in FY09. At present, BRL holds 5% market

share of total remittance transactions from Hong Kong to Indonesia,

which positions the Company as the third largest player in the

remittance transaction business from Hong Kong to Indonesia and the

largest player compared to other Indonesian banks that provide

BNI has 10 subsidiaries, including banking, insurance, financing, capital, and remittance.

PHILLIP SECURITIES INDONESIA | 21 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

remittance services in Hong Kong. Going forward, BRL will focus on

increasing its market share in Hong Kong and entering new market in

Taiwan.

Management

Board of Directors

Board of Commissioners

PHILLIP SECURITIES INDONESIA | 22 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

SWOT Analysis

Strength

1. Top fourth largest bank in Indonesia in

terms of asset, loan, and customer deposit.

2. Has strong brand name with 68 years

history in Indonesia as the first wholly-

owned state bank.

3. The only bank that is connected directly to

the integrated state revenue service

system for forex.

4. A leader bank in providing international

services in Indonesia.

5. Has wide customer base with 14,000

customers and wide ranging service

network, comprising 1,745 domestic outlets

and overseas branches.

6. The only bank to have strong ROA and ROE

improvement trajectory.

Weakness

1. Over diversification in it business portfolio

and does not have specific focus for its loan

target.

2. Has quite high efficiency ratio of 47.3%

compared to its peers.

Opportunity

1. Rapid grow in the domestic population.

2. Strong demand for syndicated loans from

the infrastructure sector.

3. Overseas market potentials can be

explored further.

Threats

1. Economic slowdown in the global markets

may reduce demand for bank loans.

2. Tight competitions among banks will make it

difficult to obtain cheap funding.

3. Presence of foreign banks in Indonesia.

4. The uncertainty in regulation and market

environment.

5. Government’s plan to merge state-owned

banks in Indonesia.

6. Tighter liquidity condition to continue in

Indonesia.

PHILLIP SECURITIES INDONESIA | 23 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

FYE Dec FY12 FY13 FY14F FY15F FY16F FYE Dec FY12 FY13 FY14F FY15F FY16F

Income Statement (IDR bn) Valuation Ratios

Net interest income 15,459 19,149 20,937 23,301 26,171 P/E (X), adj. 9.79 8.05 11.35 10.12 8.95

Non interest income 8,446 9,441 10,553 11,797 13,187 P/B (X) 1.59 1.54 2.05 1.80 1.57

Total operating income 23,905 28,590 31,490 35,098 39,357 Dividend Yield (%) 3.1% 3.7% 2.6% 3.0% 3.4%

Operating expenses (12,739) (14,573) (15,745) (17,549) (19,679) Growth & Margins (%)

Provisions (2,525) (2,708) (3,362) (3,597) (4,030) Growth

Operating profit 8,641 11,310 12,384 13,952 15,649 Assets 11.5% 16.0% 11.6% 12.5% 10.8%

Taxation (1,851) (2,220) (2,523) (2,895) (3,148) Loan 23.9% 25.8% 13.9% 15.3% 12.3%

Profit after tax 6,790 9,090 9,860 11,057 12,500 Deposit 11.4% 13.3% 11.6% 12.8% 10.6%

Non-controlling interest 2 4 4 4 5 Equity 15.0% 9.6% 14.5% 14.2% 14.0%

Net income 6,788 9,086 9,856 11,053 12,496 Net interest income 17.2% 23.9% 9.3% 11.3% 12.3%

Non interest income 11.1% 11.8% 11.8% 11.8% 11.8%

FYE Dec FY12 FY13 FY14F FY15F FY16F Operating income 19.3% 30.9% 9.5% 12.7% 12.2%

Balance Sheet (IDR bn) Net income 21.1% 33.9% 8.5% 12.1% 13.1%

Cash 7,969 10,090 8,593 5,115 3,967 Margins

Current account with BI & other banks 28,263 27,232 31,483 36,338 39,426 Net interest margin 5.9% 6.1% 6.0% 6.0% 6.0%

Placement with other banks and BI 32,617 23,473 23,190 22,911 22,636 Key Ratios (%)

Marketable securities 9,801 11,966 12,579 13,208 13,869 ROE 16.2% 19.2% 18.1% 17.7% 17.6%

Acceptance receivables 10,077 11,479 12,938 14,922 16,763 ROA 2.1% 2.4% 2.3% 2.3% 2.3%

Loans 193,835 243,758 277,593 320,175 359,657 Non-interest/total income ratio 35.3% 33.0% 33.5% 33.6% 33.5%

Government bonds 38,561 41,432 44,559 47,922 51,539 Cost/income ratio 53.3% 51.0% 50.0% 50.0% 50.0%

Fixed assets 4,592 5,514 5,582 5,545 5,410 Loan/deposit ratio 74.3% 82.6% 84.3% 86.3% 87.6%

Others 7,589 11,712 15,019 19,260 24,697 Capital Adequacy Ratio 17.9% 16.4% 16.5% 16.3% 16.4%

Total Assets 333,304 386,655 431,536 485,397 537,962

Obligations due to immediately 2,726 1,760 1,936 2,129 2,342 FYE Dec FY12 FY13 FY14F FY15F FY16F

Deposits from customers & other banks 260,906 295,075 329,215 371,132 410,365 Per share data (IDR)

Acceptances payable 4,625 6,199 6,819 7,501 8,251 EPS, adj. 378 490 529 593 670

Borrowings 8,750 18,951 20,846 22,930 25,223 DPS 113 146 159 178 201

Securities issued 4,769 6,037 6,640 7,304 8,035 BVPS 2,334 2,557 2,927 3,342 3,811

Others 8,003 10,950 11,498 12,073 12,676

Total liabilities 289,778 338,971 376,953 423,070 466,892

Shareholder's equity 43,473 47,600 54,500 62,237 70,983

Non-controlling interest 52 83 83 83 83

Total equity 43,525 47,684 54,583 62,320 71,067 Source: Company, PSI Research Est.

PHILLIP SECURITIES INDONESIA | 24 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Contact Information (Singapore Research Team) Management Chan Wai Chee (CEO, Research - Special Opportunities)

+65 6531 1231 Research Operations Officer Jaelyn Chin +65 6531 1240

Joshua Tan (Head, Research - Equities & Macro)

+65 6531 1249

Macro | Equities Market Analyst | Equities US Equities Soh Lin Sin +65 6531 1516 Kenneth Koh +65 6531 1791 Wong Yong Kai +65 6531 1685 Bakhteyar Osama +65 6531 1793 Finance | Offshore Marine Real Estate Benjamin Ong +65 6531 1535 Caroline Tay +65 6531 1792 Telecoms | Technology Transport & Logistics Colin Tan +65 6531 1221 Richard Leow, CFTe +65 6531 1735

Contact Information (Regional Member Companies) SINGAPORE

Phillip Securities Pte Ltd Raffles City Tower

250, North Bridge Road #06-00 Singapore 179101 Tel +65 6533 6001 Fax +65 6535 6631

Website: www.poems.com.sg

MALAYSIA Phillip Capital Management Sdn Bhd

B-3-6 Block B Level 3 Megan Avenue II, No. 12, Jalan Yap Kwan Seng, 50450

Kuala Lumpur Tel +603 2162 8841 Fax +603 2166 5099

Website: www.poems.com.my

HONG KONG Phillip Securities (HK) Ltd

11/F United Centre 95 Queensway Hong Kong

Tel +852 2277 6600 Fax +852 2868 5307

Websites: www.phillip.com.hk

JAPAN

Phillip Securities Japan, Ltd. 4-2 Nihonbashi Kabuto-cho Chuo-ku,

Tokyo 103-0026 Tel +81-3 3666 2101 Fax +81-3 3666 6090

Website: www.phillip.co.jp

INDONESIA PT Phillip Securities Indonesia

ANZ Tower Level 23B, Jl Jend Sudirman Kav 33A Jakarta 10220 – Indonesia

Tel +62-21 5790 0800 Fax +62-21 5790 0809

Website: www.phillip.co.id

CHINA Phillip Financial Advisory (Shanghai) Co Ltd

No 550 Yan An East Road, Ocean Tower Unit 2318,

Postal code 200001 Tel +86-21 5169 9200 Fax +86-21 6351 2940

Website: www.phillip.com.cn

THAILAND Phillip Securities (Thailand) Public Co. Ltd

15th Floor, Vorawat Building, 849 Silom Road, Silom, Bangrak,

Bangkok 10500 Thailand Tel +66-2 6351700 / 22680999

Fax +66-2 22680921 Website www.phillip.co.th

FRANCE King & Shaxson Capital Limited

3rd Floor, 35 Rue de la Bienfaisance 75008 Paris France

Tel +33-1 45633100 Fax +33-1 45636017

Website: www.kingandshaxson.com

UNITED KINGDOM King & Shaxson Capital Limited

6th Floor, Candlewick House, 120 Cannon Street, London, EC4N 6AS

Tel +44-20 7426 5950 Fax +44-20 7626 1757

Website: www.kingandshaxson.com

UNITED STATES Phillip Futures Inc

141 W Jackson Blvd Ste 3050 The Chicago Board of Trade Building

Chicago, IL 60604 USA Tel +1-312 356 9000 Fax +1-312 356 9005

Website: www.phillipusa.com

AUSTRALIA Phillip Capital Limited

Level 12, 15 William Street, Melbourne, Victoria 3000, Australia

Tel +61-03 9629 8288 Fax +61-03 9629 8882

Website: www.phillipcapital.com.au

SRI LANKA Asha Phillip Securities Limited

No-10 Prince Alfred Tower, Alfred House Gardens, Colombo 03, Sri Lanka Tel: (94) 11 2429 100 Fax: (94) 11 2429 199

Website: www.ashaphillip.net

INDIA PhillipCapital (India) Private Limited

No.1, 18th Floor Urmi Estate

95, Ganpatrao Kadam Marg Lower Parel West, Mumbai 400-013

Maharashtra, India Tel: +91-22-2300 2999 / Fax: +91-22-2300 2969

Website: www.phillipcapital.in

TURKEY PhillipCapital Menkul Degerler

Dr. Cemil Bengü Cad. Hak Is Merkezi No. 2 Kat. 6A Caglayan 34403 Istanbul, Turkey

Tel: 0212 296 84 84 Fax: 0212 233 69 29

Website: www.phillipcapital.com.tr

DUBAI Phillip Futures DMCC

Member of the Dubai Gold and Commodities Exchange (DGCX)

Unit No 601, Plot No 58, White Crown Bldg, Sheikh Zayed Road, P.O.Box 212291

Dubai-UAE Tel: +971-4-3325052 / Fax: + 971-4-3328895

Website: www.phillipcapital.in

PHILLIP SECURITIES INDONESIA | 25 | P a g e

BANK NEGARA INDONESIA INITIATING COVERAGE

Important Information

This publication is prepared by Phillip Securities Research Pte Ltd., 250 North Bridge Road, #06-00, Raffles City Tower, Singapore 179101 (Registration Number: 198803136N), which is regulated by the Monetary Authority of Singapore (“Phillip Securities Research”). By receiving or reading this publication, you agree to be bound by the terms and limitations set out below. This publication has been provided to you for personal use only and shall not be reproduced, distributed or published by you in whole or in part, for any purpose. If you have received this document by mistake, please delete or destroy it, and notify the sender immediately. Phillip Securities Research shall not be liable for any direct or consequential loss arising from any use of material contained in this publication.

The information contained in this publication has been obtained from public sources, which Phillip Securities Research has no reason to believe are unreliable and any analysis, forecasts, projections, expectations and opinions (collectively, the “Research”) contained in this publication are based on such information and are expressions of belief of the individual author or the indicated source (as applicable) only. Phillip Securities Research has not verified this information and no representation or warranty, express or implied, is made that such information or Research is accurate, complete, appropriate or verified or should be relied upon as such. Any such information or Research contained in this publication is subject to change, and Phillip Securities Research shall not have any responsibility to maintain or update the information or Research made available or to supply any corrections, updates or releases in connection therewith. In no event will Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, (i) be liable in any manner whatsoever for any consequences (including but not limited to any special, direct, indirect, incidental or consequential losses, loss of profits and damages) of any reliance or usage of this publication or (ii) accept any legal responsibility from any person who receives this publication, even if it has been advised of the possibility of such damages. You must make the final investment decision and accept all responsibility for your investment decision, including, but not limited to your reliance on the information, data and/or other materials presented in this publication.

Any opinions, forecasts, assumptions, estimates, valuations and prices contained in this material are as of the date indicated and are subject to change at any time without prior notice. Past performance of any product referred to in this publication is not indicative of future results.

This report does not constitute, and should not be used as a substitute for, tax, legal or investment advice. This publication should not be relied upon exclusively or as authoritative, without further being subject to the recipient’s own independent verification and exercise of judgment. The fact that this publication has been made available constitutes neither a recommendation to enter into a particular transaction, nor a representation that any product described in this material is suitable or appropriate for the recipient. Recipients should be aware that many of the products, which may be described in this publication involve significant risks and may not be suitable for all investors, and that any decision to enter into transactions involving such products should not be made, unless all such risks are understood and an independent determination has been made that such transactions would be appropriate. Any discussion of the risks contained herein with respect to any product should not be considered to be a disclosure of all risks or a complete discussion of such risks. Nothing in this report shall be construed to be an offer or solicitation for the purchase or sale of any product. Any decision to purchase any product mentioned in this research should take into account existing public information, including any registered prospectus in respect of such product.

Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may provide an array of financial services to a large number of corporations in Singapore and worldwide, including but not limited to commercial / investment banking activities (including sponsorship, financial advisory or underwriting activities), brokerage or securities trading activities. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have participated in or invested in transactions with the issuer(s) of the securities mentioned in this publication, and may have performed services for or solicited business from such issuers. Additionally, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may have provided advice or investment services to such companies and investments or related investments, as may be mentioned in this publication.

Phillip Securities Research or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report may, from time to time maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation in respect of the foregoing. Investments will be denominated in various currencies including US dollars and Euro and thus will be subject to any fluctuation in exchange rates between US dollars and Euro or foreign currencies and the currency of your own jurisdiction. Such fluctuations may have an adverse effect on the value, price or income return of the investment.

To the extent permitted by law, Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may at any time engage in any of the above activities as set out above or otherwise hold a interest, whether material or not, in respect of companies and investments or related investments, which may be mentioned in this publication. Accordingly, information may be available to Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, which is not reflected in this material, and Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited to its officers, directors, employees or persons involved in the preparation or issuance of this report, may, to the extent permitted by law, have acted upon or used the information prior to or immediately following its publication. Phillip Securities Research, or persons associated with or connected to Phillip Securities Research, including but not limited its officers, directors, employees or persons involved in the preparation or issuance of this report, may have issued other material that is inconsistent with, or reach different conclusions from, the contents of this material.

The information, tools and material presented herein are not directed, intended for distribution to or use by, any person or entity in any jurisdiction or country where such distribution, publication, availability or use would be contrary to the applicable law or regulation or which would subject Phillip Securities Research to any registration or licensing or other requirement, or penalty for contravention of such requirements within such jurisdiction. Section 27 of the Financial Advisers Act (Cap. 110) of Singapore and the MAS Notice on Recommendations on Investment Products (FAA-N01) do not apply in respect of this publication.

This material is intended for general circulation only and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. The products mentioned in this material may not be suitable for all investors and a person receiving or reading this material should seek advice from a professional and financial adviser regarding the legal, business, financial, tax and other aspects including the suitability of such products, taking into account the specific investment objectives, financial situation or particular needs of that person, before making a commitment to invest in any of such products.

Please contact Phillip Securities Research at [65 65311240] in respect of any matters arising from, or in connection with, this document. This report is only for the purpose of distribution in Singapore.