Embed Size (px)

Citation preview

Workshop on FINANCIAL EDUCATION Subject: Consumer Protection and Financial Literacy in the Provision of Payment Services

Speaker: Ramos da Cruz Lisbon, Centro Cultural de Belém, 23 to 25 October 2012

BANCO NACIONAL DE ANGOLA

National Bank of Angola

1

2

CONTENTS: 1. REGULATORS IN THE ANGOLAN FINANCIAL SYSTEM 2. TASKS OF THE BNA (National Bank of Angola) 3. MAIN OBJECTIVES OF THE DEPARTMENT OF

CONDUCT (DSC) 4. IMPORTANCE OF FINANCIAL EDUCATION

001

3

Law on Financial Institutions (LIF) no. 13/05 of 30 September

Banking Financial Institutions Non-banking Financial

Institutions

National Bank of Angola

(BNA)

Art. 5, no. 1, Banking and non-banking financial institutions, except insurance companies, social welfare and capitals market

Art. 5, no. 2, Insurance companies and social welfare

Art. 5, no. 3, Companies linked to the capitals and investments markets

REGULATORS OF THE FINANCIAL SYSTEM

003

Insurance Supervision

Institute (ISS)

Capital Market Commission

(CMC)

4

TASKS OF THE BNA

BNA Law - Law no. 16/10 of 15 July

Issue, ensure and preserve the value of the national currency

Contribute towards the definition of monetary, financial and exchange policies

Execute, follow up and monitor the monetary, exchange and credit policies

Manage the payments system and money supply within the framework of Angola’s economic policies

Art. 3, nos. 1 and 2: Chapter VI, Rules of Conduct, sections I to IV, arts. 55 to 69. Art. 57, no. 1 – Information obligations

Provisions on technical competences, relations with clients, information obligations, codes of conduct, professional secrecy, cooperation with other bodies, conflicts of interests, competition and advertising

Inform the clients clearly and transparently on remuneration, interest rates, requirements for credit, the price of services, etc.

002

General Objectives

5

1. Bridge the gap between clients and institutions

2. Identify risks and calculate the level of vulnerability of the financial system

3. Ensure the stability of the financial system and prevent financial crises

4. Introduce the supervision of financial institutions as a legal concept within the framework of the BNA’s duties

5. Ensure the protection of consumers of financial products and services

6. Set up effective methods to ensure compliance with the Code of Conduct, through:

1. regulation and sanctions

2. the analysis of clients’ complaints

004

7. Monitor the operations and internal control methods of financial institutions

005

Micro and macro prudential supervision

Issuing of prudential rules and conduct rules

Supervision of conduct

• Types of action:

• Protection of the interests of consumers of financial products and services

• Time frame for transfer processing • Timeframe for the availability of payment

operations • Issuing, accepting and using payment cards

Regulatory matters within the framework of the BNA’s supervisory role

006

Protection of the Consumers of Financial Products and Services (Notice no. 02/11 of 01 June)

8

PROTECTION OF THE CONSUMERS OF FINANCIAL PRODUCTS AND SERVICES

Notice no. 02/11 of 01 June establishes the rules and procedures financial institutions must respect when providing financial products and services, ensuring:

the non-discriminatory treatment of consumers of financial products and services

priority attendance

personal safety and property protection for individuals accessing financial institutions

information protection

the right to file complaints

007

Transferências e Disponibilização de Fundos (Aviso n.º 02/12, de 09 de Março)

9

TIME FRAME FOR TRANSFER PROCESSING

Intrabank transfers (national or foreign currency) – must be made on the day on which the orders are validated (validation must take place on the same day)

Interbank transfer orders received before 15:00 on a working day – Credit Transfer Subsystem (STC) clearing of the same day

Interbank transfer orders received after 15:00 – Credit Transfer Subsystem (STC) clearing of the next working day

Multicaixa system orders made before 15:00 – clearing on the same day

Multicaixa orders made after 15:00 – clearing on the following working day

Urgent real time gross settlement system transfers (SPTR) – on the same day or on the following working day

008

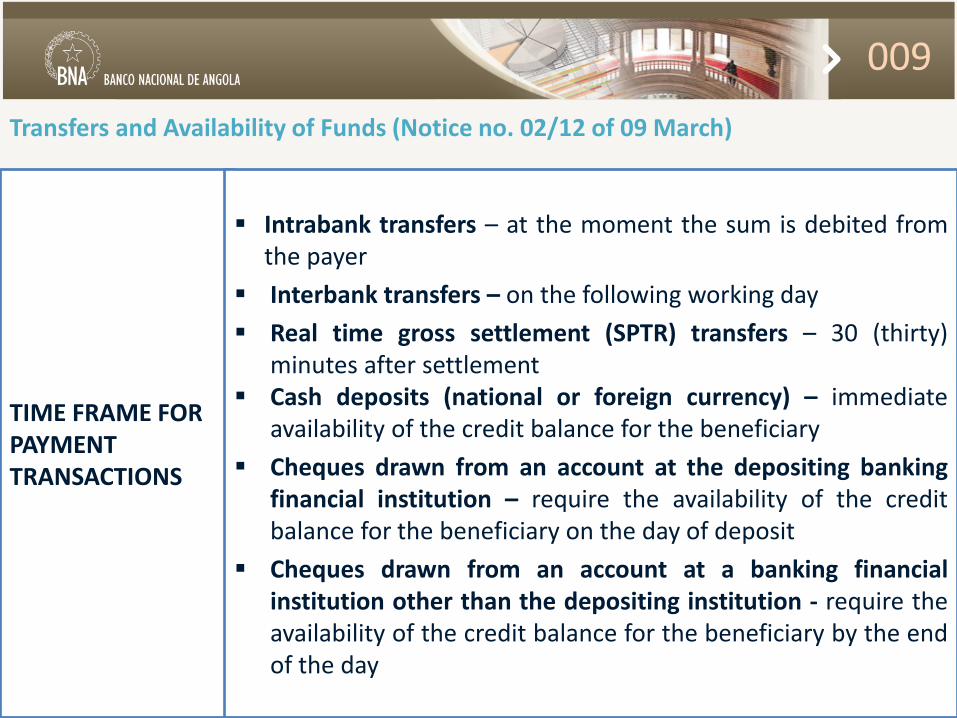

Transfers and Availability of Funds (Notice no. 02/12 of 09 March)

10

TIME FRAME FOR PAYMENT TRANSACTIONS

Intrabank transfers – at the moment the sum is debited from the payer

Interbank transfers – on the following working day

Real time gross settlement (SPTR) transfers – 30 (thirty) minutes after settlement

Cash deposits (national or foreign currency) – immediate availability of the credit balance for the beneficiary

Cheques drawn from an account at the depositing banking financial institution – require the availability of the credit balance for the beneficiary on the day of deposit

Cheques drawn from an account at a banking financial institution other than the depositing institution - require the availability of the credit balance for the beneficiary by the end of the day

009

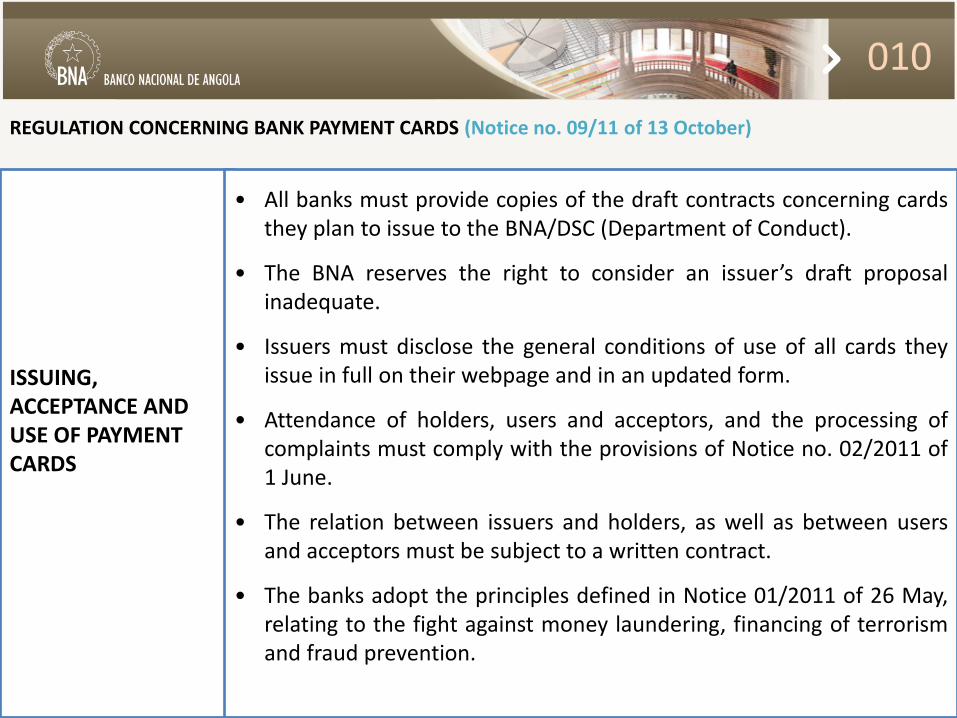

REGULATION CONCERNING BANK PAYMENT CARDS (Notice no. 09/11 of 13 October)

11

ISSUING, ACCEPTANCE AND USE OF PAYMENT CARDS

• All banks must provide copies of the draft contracts concerning cards they plan to issue to the BNA/DSC (Department of Conduct).

• The BNA reserves the right to consider an issuer’s draft proposal inadequate.

• Issuers must disclose the general conditions of use of all cards they issue in full on their webpage and in an updated form.

• Attendance of holders, users and acceptors, and the processing of complaints must comply with the provisions of Notice no. 02/2011 of 1 June.

• The relation between issuers and holders, as well as between users and acceptors must be subject to a written contract.

• The banks adopt the principles defined in Notice 01/2011 of 26 May, relating to the fight against money laundering, financing of terrorism and fraud prevention.

010

PRUDENTIAL RULES Money Laundering

12

MONEY LAUNDERING AND FINANCING TERRORISM

Law no. 34/11 of 12 September establishes preventive and repressive measures and sanctions to fight money laundering and the financing of terrorism.

Law no. 1/12 of 12 January establishes the authority of States, persons, groups or bodies and specific measures to fight terrorism, to respect international commitments to maintain peace and security, as well as protect national and external security.

Notice no. 21/12 of 25 April regulates the conditions ruling the obligations linked to identification and diligence, as well as the establishment of a system to prevent money laundering and the financing of terrorism (Compliance Officer) in the organisational structure of non-banking financial institutions under the supervision of the BNA.

Notice no. 22/12 of 25 April regulates the conditions ruling the obligations in terms of identification and diligence, as well as the establishment of a system to prevent money laundering and the financing of terrorism (Compliance Officer) in the organisational structure of banking financial institutions under the supervision of the BNA.

011

The BNA’s Conduct Supervision Strategy

Financial product offer Financial markets

(property, consumption, savings, banking services)

Financial product demand

Financial literacy, training and education

012

NEW REGULATORY PACKAGE:

14

The BNA will issue draft standards on the matters below, in accordance with

developments in the Angolan Financial System (SFA) and with the new international

supervisory agreements. They will be reflected in internationally recognised

practices.

Notices, instructions, circular letters, directives: •Advertising •Information for the public •Contracts (transparency of the information) •Rules and Code of Conduct •Reporting

REGULATORY POWER

013

Instructions

for

reporting to

the BNA

The importance of financial training and education

014

Financial training and education • Financial information is very important, but:

– it does not necessarily mean that the characteristics, risks and return of financial products is well understood

– it does not promote changes in financial behaviour • Financial training:

– is a process that allows consumers to understand financial products and services – represents added value, in addition to consumer protection measures – highlights the value of transparency and regulation instruments of financial

institutions, as well as the fulfillment of their information duties • Financial education:

– is the level of knowledge and behavioural patterns developed by means of financial training

– allows the more efficient and adequate application of financial knowledge

015

The Portal for Consumers of Financial Products and Services

The set-up of the portal:

Operational system

Complaints management

Management of pre-contractual and contractual conditions:

• Indicators

• Document archives

OBJECTIVE:

Train and inform the consumers of financial products and services

016

017

The Complaints Management System

The system permits: the simple and efficient recording and filing of

complaints, by: • allowing consumers to file complaints • opening and classifying the file • managing the file • establishing indicators

020

026

Demonstration of the Operational System

Extranet: www.gestaodereclamacoes.bna.ao

027

The Portal for Consumers of Financial Products and Services

Portal: www.consumidorbancario.bna.ao

22

Upcoming stages:

In the medium-term, the National Bank of Angola aims to:

• publish the regulatory package regarding the conduct of financial institutions in the sale of financial products and services

• increase the surveillance and monitoring of financial institutions

• organise seminars and workshops about the protection of consumers of financial products and services for the banking financial sector and non-banking financial sector

• proceed with the Financial Education Programme on a national level

028

Thank you