Embed Size (px)

Citation preview

Registration number 84

Automated Trading System for OnlineBetting Exchange Betfair

Supervised by Dr Graeme Richards

University of East Anglia

Faculty of Science

School of Computing Sciences

Abstract

In this work a study of Betfair’s betting exchange is carried out with extensive focus

on identifying factors that influence market direction. Based on research, two trading

strategies are proposed backed up by analysing ten data sets of Betfair historic data.

Four main factors are identified as market influences. These factors are used to develop

a multithreaded automated trading system that interacts with the Betfair API indepen-

dently making subsequent trades on predicting the market direction. An Android ap-

plication is also developed to act as a user interface for the system. The system is run

for a period of 20 days. An outstanding success rate is observed resulting in a 21%

cumulative profit on stake over the 20 day period.

Acknowledgements

I would like to thank my project supervisor Dr Graeme Richards for all his help and

feedback he has provided on my work throughout. I would also like to thank Dr Peirre

Chardaire and Dr Richard Harvey for the organisational support they have provided

throughout running the module.

CMPC3P2Y Contents

Contents

1. Introduction 1

1.1. Betfair Betting Exchange . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.2. Trading with Betfair . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1

1.3. Betfair Developer Program . . . . . . . . . . . . . . . . . . . . . . . . 2

1.4. Advantages of Automated Trading . . . . . . . . . . . . . . . . . . . . 3

1.4.1. Avoiding Human Error . . . . . . . . . . . . . . . . . . . . . . 3

1.4.2. Human Emotion . . . . . . . . . . . . . . . . . . . . . . . . . 4

1.4.3. No Time Limitations . . . . . . . . . . . . . . . . . . . . . . . 4

1.4.4. Multiple Market Analysis . . . . . . . . . . . . . . . . . . . . 4

1.4.5. Speed . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

2. Literature Review 5

2.1. Prediction Markets . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

2.2. Sports Betting Arbitrage . . . . . . . . . . . . . . . . . . . . . . . . . 6

2.3. Existing Trading Strategies . . . . . . . . . . . . . . . . . . . . . . . . 7

2.3.1. In Play Strategies . . . . . . . . . . . . . . . . . . . . . . . . . 7

2.3.2. Pre in play Strategies . . . . . . . . . . . . . . . . . . . . . . . 8

2.3.3. Swing Trading . . . . . . . . . . . . . . . . . . . . . . . . . . 9

2.3.4. Scalping . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

2.4. Time Series Data Analysis . . . . . . . . . . . . . . . . . . . . . . . . 11

2.4.1. Machine Learning . . . . . . . . . . . . . . . . . . . . . . . . 12

2.4.2. Case Based Reasoning . . . . . . . . . . . . . . . . . . . . . . 12

2.4.3. Other Machine Learning Algorithms . . . . . . . . . . . . . . . 12

3. Proposed Trading Strategies 13

3.1. Strategy A . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

3.2. Strategy B . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 14

4. Modelling Betfair Historical Data 15

4.1. Data Set . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 15

Reg: 84 iii

CMPC3P2Y Contents

5. Proposed Hypotheses 16

5.1. Weight of Money . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 16

5.2. Back and Lay Over-rounds . . . . . . . . . . . . . . . . . . . . . . . . 17

5.3. Lowering Risk . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

5.4. Volume Spikes . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

6. Data Analysis 18

6.1. Methods of Analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

6.2. Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 21

6.2.1. Weight of Money . . . . . . . . . . . . . . . . . . . . . . . . . 21

6.2.2. Back and Lay Over-rounds . . . . . . . . . . . . . . . . . . . . 23

6.2.3. Trading In Non Volatile Markets . . . . . . . . . . . . . . . . . 26

6.2.4. Volume Spikes . . . . . . . . . . . . . . . . . . . . . . . . . . 28

6.3. Conclusions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 29

7. Implementation 30

7.1. Automated Betfair Tool . . . . . . . . . . . . . . . . . . . . . . . . . . 31

7.1.1. Trading Thresholds and Rules . . . . . . . . . . . . . . . . . . 33

7.2. User Interface . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 36

8. Results 37

8.1. Strategy Success . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 39

9. Conclusion 39

References 41

A. Other Examples to Show Weight of Money Affect 44

B. Example Green Screens 45

Reg: 84 iv

CMPC3P2Y List of Figures

List of Figures

3.1. English Premier League - Relegation . . . . . . . . . . . . . . . . . . 14

4.1. Historic Data - Everton vs Norwich - Draw . . . . . . . . . . . . . . . 16

4.2. Data Set Overview . . . . . . . . . . . . . . . . . . . . . . . . . . . . 17

Reg: 84 v

CMPC3P2Y 1. Introduction

1. Introduction

1.1. Betfair Betting Exchange

Betfair was launched in June 2000 and has had a huge impact in the way in which

betting is perceived and has revolutionized sports betting. Betfair is an online betting

exchange which doesn’t directly set the odds of the selections users can place bets on.

Instead Betfair simply provides a market and allows users to essentially trade-off against

each other for the best available price. Instead of the traditional betting model where

the bookmaker will set fixed odds of the implied probabilities of a selection, a betting

exchange allows users to effectively become the bookmaker and offer their own implied

probabilities for other users to place bets on. Placing a bet on an outcome is known as

a "back" bet whereas offering a bet to be backed by another user is called a "lay" bet.

Betfair claims to process more than six million transactions every day which is more

than all European stock exchanges combined, Alberola and Garcia-Fornes (2013).

1.2. Trading with Betfair

The above concept of being able to both back and lay on the same outcome provides

the opportunity to make profits on market movements in a similar way to how stock

market traders do on the stock market. For example consider the scenario below: A

bet is placed for £10 on a selection with odds of 10/1 (Back Phase). A second bet is

then offered to the market to take a £10 bet on the same selection with odds of 9/1 (Lay

Phase).

Back Phase: Potential winnings = £100 Potential Loss = £10

Lay Phase: Potential winnings = £10 Potential Loss = £90

From these figures we can see that if the selection wins the back bet will win £100

but the lay bet will lose £90 resulting in a net profit of £10. On the other hand if the

selection loses the lay bet will win £10 and the back bet will lose £10 resulting in a

break even situation. To further eliminate relying on the selection winning in order to

Reg: 84 1

CMPC3P2Y 1. Introduction

make a profit, the profits can be hedged across all selections to lock in a guaranteed

profit, this is often known as "greening up" to represent a green profit figure displayed

over all selections on the screen. For example if the selection was "laid" for £11 instead

of £10 this would lock in a £1 profit if the selection was to win or lose.

This may appear a very easy way to gain profits on the exchange however in order

for the above scenario to play out successfully it is required that a lay bet is placed at

odds of lower than the odds of the placed back bet or the opposite (backing at a higher

price than the original lay bet). This would therefore involve correctly predicting the

market to move in a certain direction, in the above scenario this is represented as the

odds dropping from 10/1 to 9/1.

1.3. Betfair Developer Program

The Betfair developer program is designed to allow users to develop their own appli-

cations and software that can interact with the exchange. The program is dedicated to

assisting Betfair customers with integrating their applications into the Betfair exchange

platforms. Betfair (2013a)The API uses an XML-based interface description language

known as Web Services Description Language (WSDL) which can be loaded into an

IDE project. The API is pulled from an URL and the various built in functions and vari-

ables are then accessible from within the project. There are three options when signing

up to the program which include:

• Personal Free Access - This is the most basic of the developer spaces aimed for

personal use it offers limited API services with various caps on data requests, for

most of the API functions 60 requests per minute is the limit. A full list can be

found at Betfair (2013b)

• Software Vendor - This option is applicable for developers that wish to com-

mercialise their application. These applications are often trading software that

provide enhanced tooling and analysis of the markets, there are various software

vendor applications available including BetAngel, GeeksToy and FracSoft. This

service has an undisclosed fee which is expected to be quite large.

Reg: 84 2

CMPC3P2Y 1. Introduction

• Personal Full Access - This is similar to the personal free access service but

has no data limitations. However for this service a charge of £200 per month is

required.

The API itself contains a powerful set of features that allow advanced market navigation,

search, odds retrieval and bet placement. The API also provides Betfair account related

services via the Accounts API.Betfair (2013a) The API is available for various platforms

including Java, Python, and Visual Basic 5 and 6.

1.4. Advantages of Automated Trading

As Betfair is a prediction market it is very similar to modern day financial markets,

here some of the advantages of automated trading versus manual trading are considered

both lowering risk by excluding factors such as human error and emotion as well as

performance enhancing factors such as increased speed and efficiency and analysing

markets in parallel.

1.4.1. Avoiding Human Error

Human error and risk management are considered vitally important factors in financial

market trading. A study by (1Baddeley and Longman, 1973) shows that humans have

a tendency to incur error in even the simplest of tasks. Baddeley and Longman’s study

shows a 1% error rate for postal workers copying down the correct postal code on de-

liveries, a seemingly simple task however this shows that human error is inevitable in

almost everything. In relation to financial market trading these types of human errors

are often magnified because of the large amounts of money at stake. In October 2012

Google saw $22 Billion wiped off there market value caused by someone accidently

e-maling the wrong person. More recently in January 2014 a trader lost approximately

£400,000 in 30 seconds when he accidentally bought a large amount of shares of bank

HSBC Mason (2014). This type of error is often referred to as a "fat finger" trade, where

the trader buys the wrong, or wrong amount of shares by accident. Factors that lead to

human error can include tiredness, inexperience, complacency, distractions and fatigue.

Reg: 84 3

CMPC3P2Y 1. Introduction

1.4.2. Human Emotion

Trading in financial markets is one of the most emotionally connected occupations, this

is because traders are dealing with their own or other peoples money and feel a strong

connection to the outcomes of their trades. In a study by Lo (2005) the authors show a

direct link between fear and greed to trading performance. As well as greed and fear,

stress and pressure can play a major part in human performance. In a study by Guttman

(1983) a group of candidates are asked to perform the simple task of turning a control

in a particular direction. However the conditions of the experiment involved trying to

perform the task under extreme stress. The results show an error rate of 50% per turn of

the control. Overconfidence can also be an emotion experienced by traders that appear

to be doing very well, the overconfidence can lead to taking increased unnecessary

risks, often resulting in an overall decrease in performance. Odean (2001) show that

overconfidence in both men and women decreased trading performace by 2.65% and

1.72% respectively. Finally as this work aims to trade on a betting exchange using an

automated approach eliminates any gambling and addiction based emotional conflicts.

1.4.3. No Time Limitations

Betfair betting exchange runs seven days a week twenty four seven, using an automated

approach means that full exposure to the markets is possible. Analysis can be done con-

tinually unlike manual traders which may miss opportunities outside of normal trading

hours.

1.4.4. Multiple Market Analysis

Manual traders can only fully focus on one market at a time, whereas using an auto-

mated approach multi threading can be introduced to both analyse and trade on multiple

markets at the same time. This advantage therefore increases coverage and efficiency.

1.4.5. Speed

Using rule based algorithms the advantage of automation means that spotting patterns

and trends as well as simply placing bets is a lot faster. For some trading strategies

Reg: 84 4

CMPC3P2Y 2. Literature Review

speed is vitally important.

2. Literature Review

In this section a brief look into the background of betting exchanges and sports arbi-

trage is discussed followed by a look into different trading strategies and factors that

have been found to influence marlet direction. Finally looking into techniques used for

technical market analysis.

2.1. Prediction Markets

Wolfers and Zitzewitz (2004)state that Betfair can be categorized as a prediction market,

a form of financial market that is based on speculation of the outcome of an unknown

future event. S.J. Hardiman (2011) states Bets placed act as assets which have a value

related to the outcome of an event. Prediction markets have proved to be extremely

accurate at predicting the true probabilities of future events occurring. J.E. Berg (2008)

A recent study showed that the Iowa Political Stock Market has been shown to beat

opinion polls at forecasting the outcomes of presidential elections.

Prediction markets are fuelled by the views of a large contingency, battling for a prize in

the case of Betfair’s betting exchange, the stake multiplied by the estimated probability

that they are correct. Betfair being the largest betting exchange in the world abides by

this accuracy on high volume markets, often sports such as football, tennis and horse

racing. Betfair processes more than five million transactions every day which is more

than all European stock exchanges combined Goncalves (2013). The market fluctuates

due to the supply and demand of a particular price being offered. If lots of people be-

lieve that the implied probability is greater than the actual probability then the odds will

shorten. The same can be said if the implied probability is less than the actual probabil-

ity then the odds will rise. This is due to the competitiveness of the market, users are

fighting for the best available price for both backing and laying, which in turn balances

the market. For example if there is a high demand to back a particular selection then

Reg: 84 5

CMPC3P2Y 2. Literature Review

people that are trying to lay the selection will most likely lower there asking price as not

to offer over the odds of the true probability, thus balancing the market.

2.2. Sports Betting Arbitrage

Arbitrage is the concept of placing bets on all outcomes of an event where all outcomes

will result in a profit. Arbitrage focuses on creating a book percentage of less than 100%

which puts the better in a position where betting on all selection will guarantee profit.

The book percentage can be defined as the sum of 100 divided by the odds of each se-

lection. The book percentage will always be above 100% for the bookmaker to make a

profit. For example if the book percentage was 105% this represents that the bookmaker

will make £105 for every £100 they pay out.

Originally sports arbitrage would be done between 2 or more bookmakers that was of-

fering different odds on selections in the same event. This type of arbitrage is discussed

by D.C. Edelman (2004) Consider the following scenario:

In an event of 2 possible outcomes either player A winning or player B winning. If

one bookmaker was offering odds of 3.5 for player A and 1.37 for player B we can

work out the book percentage as the sum of 100/selection odds:

Book Percentage = 100/3.5 + 100/1.37 = 101.56%

As we can see the book percentage here shows the bookmaker will win £101.56 for

every £100 he pays out. However if another bookmaker was offering odds of 3.2 for

player A and 1.42 for player B we can again work out the book percentage as:

Book Percentage = 100/3.2 + 100/1.42 = 101.67%

Again these odds would result in a guaranteed profit for the bookmaker as the book

percentage is greater than 100%. However if someone was to take the odds for player A

from the first bookmaker of 3.5 and the odds for player B from the second bookmaker

Reg: 84 6

CMPC3P2Y 2. Literature Review

of 1.42 we can again work out the book percentage as:

Book Percentage = 100/3.5 + 100/1.42 = 98.99%

The punter is now in a successful arbitrage situation, for every £100 they win they

will lose only £98.99 resulting in a profit of 1.01%. Before the arrival of betting ex-

changes this would be very hard to come by as many bookmakers would set up book

percentages of between 105% - 120%, E. Franck (2009) found that the average book

percentage excluding exchanges was between 110.9% and 114.1%. With book percent-

ages this high it would be very hard to find arbitrage opportunities where the odds where

so far apart. As Betfair is a betting exchange and doesn’t set the odds of selections we

find that the average book percentage is a lot lower than other bookmakers at 102.6%

excluding commission O’Connor (2013), on higher profile events the book percentage

can drop to fluctuate between 100.1% - 101%.

Typically arbitrage is done over two or more bookmakers however trading on the Bet-

fair exchange can be considered a type of arbitrage betting as the market prices fluctuate

and can present the arbitrage opportunities of "backing" high and "laying" low. How-

ever this form of arbitrage is more risky as it involves predicting the market direction in

order to formulate the book percentage at less than 100%.

2.3. Existing Trading Strategies

Since the introduction of betting exchanges there has been many different trading strate-

gies developed and used by traders.

2.3.1. In Play Strategies

One of the most common trading strategies is trading the in play markets on Betfair.

A market that is in play means that the event has already started, this therefore means

there will be high volatility in the market as the odds rise and fall dependent on things

happening during the event. For example if a goal is scored in a football match the odds

Reg: 84 7

CMPC3P2Y 2. Literature Review

will change drastically. Football and Tennis markets are often traded in play, Wozniak

(2011) Investigates the in play markets of tennis, his work shows how volatile the mar-

ket can be often swinging up and down large amounts. In this paper Wozniak develops a

trading strategy to calculate probabilities of a player winning a game based on a Markov

Chain, "a stochastic model describing a sequence of possible events in which the prob-

ability of each event depends only on the state attained in the previous event." Lawler

(2006). The probabilities are then compared to the implied probabilities on Betfair and

trades are opened where the Markov Chain probabilities are higher than those on the

exchange. The trade is then closed when the swing in the market occurs.

Although in play market trading can be very lucrative offering large swings in mar-

ket prices it is also very risky, with big profits also comes big loses. The market can

swing in both directions as is pointed out by Ovregard (2008) the in play markets are

very volatile and effective contingency planning is highly required. To implement this

Ovregard, and Oyvind Norstein employ a stop loss technique for their in play trading

strategy.

A stop loss is a rule set by the trader to protect the open trades from going drastically in

the wrong direction and producing large losses.

2.3.2. Pre in play Strategies

Many traders prefer to trade before the market goes in play as this is less risky, the

markets are a lot less volatile and traders can rely on market trends and analytics to

predict market direction and not random events that occur in play. Horse Racing is a

very popular market for pre in play traders. One of the most famous and successful

Betfair traders Adam Heachcote heavily traded the horse racing markets between 5 - 15

minutes before the off. Heachcote wrote a blog in 2009 of how he started trading with

a bankroll of £6000 in which he accumulated £296,208.92 in just one year. Heathcote

(2012) Trading software BetAngel founder Peter Webb also claims to be very successful

using pre in play strategies. He claims a turnover of a quarter of a billion pounds a year

trading on betfair and is known as "The master of the markets" Blincoe (2010) Webb

Reg: 84 8

CMPC3P2Y 2. Literature Review

discusses various trading strategies in his blog Webb (2013), two of the main techniques

he refers to are swing trading and scalping.

2.3.3. Swing Trading

A swing trade is a large market movement in one direction. A large swing in the market

may be triggered by several factors. Goncalves (2013) paper explores the notion of the

"weight of money" concept. The weight of money encapsulates the supply and demand

of a particular selection by looking at how much money is waiting to be matched on

either side of the market. If there is a higher amount of money waiting to be matched

on one side of the market then this represents a high demand of people wanting to take

this price and an expected drop in price. Likewise if there is a low amount of money on

one side of the market this represents a weak demand for the price and an expected rise

in the price will occur.

This concept has been explored by Christiansen (2007). In Christiansen’s study a pre-

diction market is set up and a set of traders attempt to make a favoured selection appear

more likely to win by placing large amounts of money at certain positions in the market.

Although the money wasn’t real the results showed that the apparent high demand of

a selection represented by large sums of money could manipulate traders into believ-

ing that the selection was more likely to trend positively. Other factors discussed by

Nordsted (2009) that are believed to have effect on the direction of the market include:

• Large Volume Spikes - Large volume spikes can often be a sign of high demand

and are also not prone to market manipulation as the weight of money concept is.

• Competitor Movements - Markets will always remain balanced, if one selection

is trending positively then other selections must be trending negatively.

• News - News of influencing events such as injuries or non-runners will almost

definitely have an effect on the market.

• Graphical correlation and trends - Spotting trends and patterns from the graph

of the previously traded prices as well as statistical analysis such as last traded

Reg: 84 9

CMPC3P2Y 2. Literature Review

price and moving averages can provide vital information about future trends.

• External Price Movements - Movements in external bookmaker prices, espe-

cially if multiple bookmakers are trending this can represent false pricing or

a high demand. An arbitrage strategy highlighted in Constantinou and Fenton

(2012) uses the website Oddschecker (www.oddschecker.com) to compare the

odds across a range of bookmakers.

• The Book Percentage - Not so much a sign of a market swing, however if the

book percentage is tight (close to 100%) then the odds are less likely to drop

than if the book percentage was loose. This is because dropping below 100%

would mean it would be possible to back all selections at their current prices

and make a profit for this reason the book percentage will very rarely dip below

100%. Therefore the if the book percentage is close to 100% the odds are unable

to increase anymore as this will lower the book percenatage further

• Momentum - When a selection begins to move in a particular direction it can pick

up momentum as traders adopt a frenzy like attitude to all get in on the market

movement. Docherty and Eastion (2011) explore this concept with a trading strat-

egy for the 2008 Ryder cup sports market by trading over short term (1 minute)

momentum periods.

Nordsted explains no one factor is the key to predicting the market direction, appropriate

consideration of all factors is needed, however the main market mover is money.

2.3.4. Scalping

Scalping is the second of the two techniques referred to by Webb. Scalping involves a

very short term trade which is often only active a number of seconds before it is closed.

To scalp a market the trader is looking to take a very small market movement in each

direction. A trade is opened with the intention to sell at one point below the original

value, an ideal market to employ the scalping technique would be on a selection that has

no real trend correlation, a simple one point move is all that is required. Unlike swing

trading scalping does not require as much prediction of which way the market is going

Reg: 84 10

CMPC3P2Y 2. Literature Review

to move it simply just requires 2 bets (1 back and 1 lay to be matched next to each other.

Bets (2012) discusses various scalping techniques:

• Low volume scalping - This technique involves getting money down early on

odds that don’t have much liquidity, this therefore places the trader at the front of

the queue for money waiting to be matched. If the trader can manage to get fairly

near the front of the queue on each side of the market and the odds are sustained

then both bets will be matched and a profit is locked in.

• Range scalping - This technique involves finding the upper and lower thresholds

of a selections trading activity. This may not be apparent in all markets however

some selections will tend to trade between a set of virtual limits. Range scalping

involves identifying these thresholds placing marker trades at these positions and

then sell at one point below the threshold.

• Trend scalping - Similar to swing trading the trader looks to predict the direction

of the market, opening a position in the market and immediately exiting if the

market moves 1 point in the predicted direction. A 1 point stop loss is normally

used to suggest that the key to trend scalping is to get over a 50% success rate as

a successful scalp would result in +1 point and a negative scalp results in âAS1

point.

2.4. Time Series Data Analysis

Betfair data can be defined as a type of time series data. A time series is a sequence of

consecutive data points, measured at equally spaced time intervals. A trend is the way in

which a variable changes over these time periods. There are various techniques used to

analyse time series data. In order to effectively predict the future market direction and

other trading opportunities, consider the various approaches and techniques that can be

used to design and build an effective trading algorithm for market analysis and analysis

of historical data.

Reg: 84 11

CMPC3P2Y 2. Literature Review

2.4.1. Machine Learning

As the problem description is to classify the future market direction of a given mar-

ket based on a set of market conditions the variable we want to classify is discrete, as

the market direction will either go up or down. Therefore we will look at the various

machine learning classification algorithms which could be used. In Ovregard (2008)

market analysis and future price predictions are done using an artificial neural network

(ANN). A neural network can be defined as "a computing system made up of a num-

ber of simple, highly interconnected processing elements, which process information

by their dynamic state response to external inputs" Caudill (1987) ANN algorithms can

be trained using a set of training data. Ovregard and Oyviind Norstein use historical

data of the tennis in play markets to train their algorithm to classify a profitable or

non-profitable trade based on a set of condition variables or neurons. To develop and

train the algorithm The Fast Artificial Neural Network (FANN) open source software

was used. ANN algorithms have also been used in other financial markets, Pissarenko

(2002) explores the use of neural networks for financial time series prediction, a train-

ing algorithm is used to find the optimum weights between neurons that determine the

global minimum of the error function.

2.4.2. Case Based Reasoning

Another approach used by Alberola and Garcia-Fornes (2013) is to use a case based

reasoning classification algorithm to predict future odds by finding similarities with

past events. The algorithm will also find the best trading decision based on the current

conditions of the event. The algorithm was tested on the football over/under 2.5 goals

market against a set of 11 human traders with varied experience on betting exchanges,

the CBR algorithm scored the highest yield percentage of +8.5%.

2.4.3. Other Machine Learning Algorithms

There has been various work done on using machine learning algorithms to attempt to

correctly predict results of sports events. In M.B. Kim (2008) a rule-based reasoning

and Bayesian network model is used to predict football results. Historical data of pre-

Reg: 84 12

CMPC3P2Y 3. Proposed Trading Strategies

vious games is used as training data. The Bayesian network is a collection of nodes

representing variables that are interconnected by conditional dependencies. Each node

will have a related probability which is used to calculate the probability of an event

occurring. Another interesting algorithm is Support Vector Machine (SVM) seen by

many as the best off-the-shelf machine learning algorithm Liu and Lai (2010). SVM

is a binary linear classifier so it will classify an object as either one output or not the

output, which would suit the trading problem as there is only two market directions up

and down. SVM classifiers work by assigning objects a position in space which can be

clearly divided into two outputs.

3. Proposed Trading Strategies

Based on reasearch findings, two trading strategies are presented strategy A takes ad-

vantage mainly of the weight of money influence on the market whereas strategy B takes

advantage of trading in non volatile markets.

3.1. Strategy A

Unlike most trading strategies that are aimed at exploiting swings in volatile markets

such as horse racing this strategy is aimed at finding non volatile markets with a non

volatile selection. Upon finding a suitable market and selection a back bet is then placed

at the current lay price. This bet stays unmatched and joins the waiting money queue at

the lay price. As more money is traded on the selection the unmatched bet moves closer

to the front of the queue of waiting money until it is eventually matched to a layer. A

counter lay bet is then placed at the current back price which again stays unmatched

and waiting in the queue. This is now attempting to close the trade for a 1 point profit.

Providing that the market does not drastically move in the opposite direction as long

as the selection either comes down in price or remains the same price as more money

is traded on the selection the unmatched bet once again nears the front of the queue of

money waiting to be matched and becomes matched resulting in a one point profit. For

this reason it is very important to select a non volatile market and selection. As well as

being non volatile it is equally important that the amount of money being traded on the

Reg: 84 13

CMPC3P2Y 3. Proposed Trading Strategies

selection is reasonably high in order to flush the unmatched bets through the queue of

unmatched money. Most football match odds markets are fairly non volatile before the

match begins they also have a high volume throughput which makes them the perfect

target for this strategy. Also to enhance the non volatility factor the draw selection is the

only selection considered for trading as this is the least volatile selection in the market.

Finally this strategy also requires a strict exit strategy, for successful trades a 1 point

profit is the exit trade however as the entry trade will remain unmatched for a period of

time, it is important to keep monitoring the market and the selection to ensure that that

the conditions remain in the prime state. If the position deteriorates then the unmatched

bet can be cancelled with no profit or loss. Likewise if the entry trade does get taken and

then the position starts to deteriorate it is still possible to exit at the same price, this is

because the entry back trade was matched at the current lay price, therefore the current

lay price is still available to lay, simply issuing a lay bet at the current odds would result

in a scratch trade. In the unlikely event that the unmatched bet gets taken and the market

moves drastically in the wrong direction a stop loss of 1 point will be triggered to exit

with a 1 point loss.

3.2. Strategy B

Strategy B is aimed at exploiting holes in the market. With the same initial strategy as

strategy A a non volatile but high volume market and selection are required, so again

pre football match odds markets are selected and the draw is the selection of interest.

The market is then monitored for areas where there is a considerably low amount of

money waiting to be matched, supported by a large amount of money one place to the

right. This can be seen below in figure 3.1 with West Ham.

www.betfair.com/exchange

Figure 3.1: English Premier League - Relegation

Reg: 84 14

CMPC3P2Y 4. Modelling Betfair Historical Data

The hole is at the 3.45 odds as there is a small amount of money here, however it

is also backed up by a large amount of money to the right at 3.5. The hole should

be approximately 5 times less than money waiting at the current price with a support

amount of at least three times more than the money waiting at the current price. The

trade is then entered at the position of the hole, if the selection odds move in the correct

direction then the unmatched bet will be extremely close to the front of the queue with

a larger amount of unmatched money as this will now be the current available lay price.

The exit strategy is the same as in strategy A.

4. Modelling Betfair Historical Data

4.1. Data Set

To uncover the conditions that effect market movement and direction a data set of betfair

historical data is used. A data set of 10 previous football matches is used. The histor-

ical market data is obtained from Fracsoft a company that records and stores exchange

data from a variety of betfair markets. As this work focuses on developing a low risk

strategy, pre in play football match odds markets are the only markets considered as

data candidates. The ten markets where selected at random from a range of different

leagues and competitions to ensure that most market domains were represented. En-

glish Premier League, Italian Serie A, Spanish La Liga, German Bundasliga, European

Champions League and Internationals where all represented. The data obtained from

Fracsoft contains records of each selection in the market updated every second contain-

ing the following data fields:

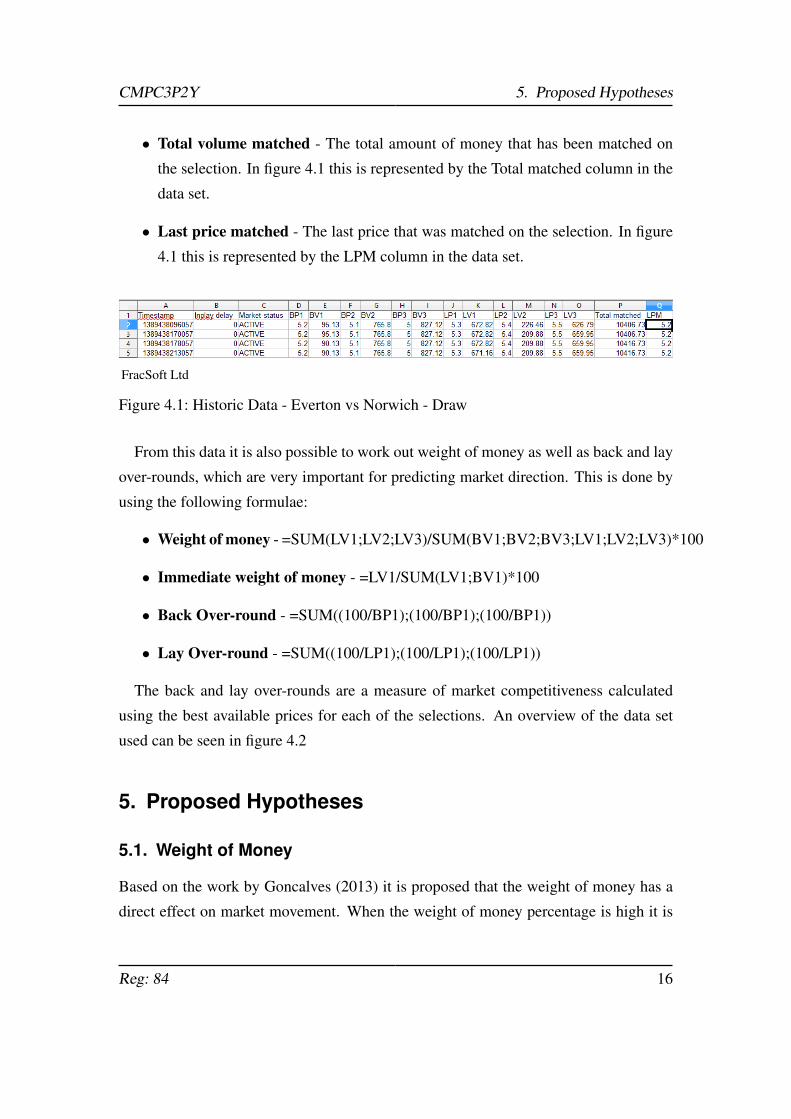

• Back and lay Odds - The best three available back and lay prices, in figure 4.1

these are represented by the columns BP1, BP2, BP3, LP1, LP2, LP3.

• Back and lay amounts waiting to be matched - The amount of unmatched

money waiting to be matched on each of the best three available back and lay

prices. In figure 4.1 these are represented by the columns BV1, BV2, BV3, LV1,

LV2, LV3.

Reg: 84 15

CMPC3P2Y 5. Proposed Hypotheses

• Total volume matched - The total amount of money that has been matched on

the selection. In figure 4.1 this is represented by the Total matched column in the

data set.

• Last price matched - The last price that was matched on the selection. In figure

4.1 this is represented by the LPM column in the data set.

FracSoft Ltd

Figure 4.1: Historic Data - Everton vs Norwich - Draw

From this data it is also possible to work out weight of money as well as back and lay

over-rounds, which are very important for predicting market direction. This is done by

using the following formulae:

• Weight of money - =SUM(LV1;LV2;LV3)/SUM(BV1;BV2;BV3;LV1;LV2;LV3)*100

• Immediate weight of money - =LV1/SUM(LV1;BV1)*100

• Back Over-round - =SUM((100/BP1);(100/BP1);(100/BP1))

• Lay Over-round - =SUM((100/LP1);(100/LP1);(100/LP1))

The back and lay over-rounds are a measure of market competitiveness calculated

using the best available prices for each of the selections. An overview of the data set

used can be seen in figure 4.2

5. Proposed Hypotheses

5.1. Weight of Money

Based on the work by Goncalves (2013) it is proposed that the weight of money has a

direct effect on market movement. When the weight of money percentage is high it is

Reg: 84 16

CMPC3P2Y 5. Proposed Hypotheses

Figure 4.2: Data Set Overview

proposed the price will decrease. Likewise when the weight of money percentage is low

it is proposed the price will increase.

5.2. Back and Lay Over-rounds

It is proposed that as each side of the market becomes more competitive the price is

affected. It is proposed that a low back over-round represents a highly competitive price

and therefore will result in a price decrease. Likewise it is proposed that a low lay

over-round represents a less competitive price for laying and therefore the price will

decrease.

5.3. Lowering Risk

The underlying concept of both trading strategies is to lower risk by trading on less

volatile markets and selections. This is achieved by choosing to trade on markets and

selections in which the odds do not move big amounts in any particular directions. Both

strategies are designed to only gain one point on the price a technique which is often

referred to as scalping Webb (2013).

Due to the design of these strategies it is proposed that it is possible to trade on

non volatile markets gaining a one point profit. Reverse buying and selling is also

introduced which shows that it is possible to trade gaining a one point profit without the

odds moving at all.

Reg: 84 17

CMPC3P2Y 6. Data Analysis

5.4. Volume Spikes

A volume spike is a large amount of money traded on a market selection in a short

amount of time, volume spikes are often one large trade. Although neither of the pro-

posed strategies directly rely or take advantage of volume spikes to make predictions,

it is proposed as a factor that affects market direction to bolster the weight of money

concept and show how large amounts of money affect market direction.

6. Data Analysis

This section shows analysis of how proposed factors such as weight of money and over-

rounds affect market direction and discusses whether they can be used to predict market

direction on live data. Also methods of lowering risk such as identifying and trading on

less volatile markets are explored as well as identifying risks such as volume spikes.

6.1. Methods of Analysis

In order to analyse the affect weight of money and over-rounds have on market direction

all points of price movement in the series are analysed. The mean of the ten closes points

to the movement are used obtain relevant values, this is shown in figure 6.1

Reg: 84 18

CMPC3P2Y 6. Data Analysis

Time series analysis methods

As can be seen in figure 6.1 the grey shaded areas are the areas of interest. In this

figure there are four price movements. For each of the movements the ten points of

interest before the movement occurs are analysed. When analysing the affects of weight

of money the mean weight of money percentage of these 10 points is calculated as a

representation of the value before the movement occurs. To fit hypothesis the weight of

money will be high when prices move down and low when prices move up. Therefore

to give a score of success when the movement is a price increase 100 is subtracted from

the weight of money so as to return a score of successful prediction. For example:

Mean weight of money before price increase = 30%

Score = 100 - 30 = 70

For downward movements the weight of money percentage is simply used. For ex-

ample:

Reg: 84 19

CMPC3P2Y 6. Data Analysis

Mean weight of money before price decrease = 70%

Score =70

This therefore shows that an equal score of correctly predicting movements in both di-

rections to fit the expected model. Similarly if the results do not fit the expected model

a low score will be awarded. For example:

Mean weight of money before price increase = 60%

Score = 100 - 60 = 40

After all movements scores have been calculated the mean score across the market is

calculated to give an overall measurement of fit to the expected model.

When analysing the affect back and lay over-rounds have on the market the same

method of selecting the ten points before every movement is used, with the mean value

used. As the expected model of this distribution follows the odds ie. When the odds

move down both the back and lay over-rounds move down, the mean over-rounds of

each market are calculated per up and down movement. This is shown per market as:

- Mean back over-round when the price decreases

- Mean back over-round when the price increases

- Mean lay over-round when the price decreases

- Mean lay over-round when the price increases

This allows the comparison between the values of the over-rounds when the prices

increase and decrease. The expected model shows that the mean back and lay over-

rounds when the price decrease should be lower than when the price increases.

As well as exploring factors that affect market direction, it is also necessary to explore

selecting and measuring volatility. Lowering risk is an important factor for both strate-

gies. To measure volatility the standard deviation of the series is calculated to measure

how much the price moves.

Reg: 84 20

CMPC3P2Y 6. Data Analysis

6.2. Results

6.2.1. Weight of Money

After running the analysis on all markets the following results can be observed.

As can be seen from the graph, all ten of the markets had a higher score than 50,

with the Arsenal vs Man Utd market achieving the highest score of 56.19264876633. If

the weight of money concept had no affect on the market direction then the distribution

would be centred more at around the 50 mark to suggest that there is an even probability

Reg: 84 21

CMPC3P2Y 6. Data Analysis

of market direction. In contrast we observe a distribution in favour of higher scores with

the mean score across all markets 52.922114579%. Overall it can be observed that all

markets fit the statistical model of inverse proportion reasonably well. However we do

notice throughout that in some cases movements are made in the unexpected direction.

For example in the Chelsea vs Man City market an upward price movement is made

when the weight of money percentage is as high as 67.7334382828% also a downward

movement is made when the weight of money percentage is just 46.1343916164%. Al-

though these are often rare throughout and this particular market achieved a reasonably

high score above the mean at 53.24720877% thanks to a lot of other movements fitting

the expected model, it is important to be aware that it is possible to move unexpectedly.

As is stated at the beginning the goal is not to find a sure fit way to make successful

trades every single time, it is simply to find an edge in order to make more successful

trades than unsuccessful.

Looking more in depth at the weight of money concept the above figure shows the

last price matched for the draw plotted against the weight of money percentage in the

Chelsea vs Galatasaray UEFA Champions league second round match. It can be ob-

Reg: 84 22

CMPC3P2Y 6. Data Analysis

served that the weight of money has a clear impact on market direction.

At the start of the series it can be seen that the weight of money initially starts rel-

atively high at 60% gradually dipping below the 50% mark down to 45%, this in turn

encourages a quick price increase by one point only to be struck back down again as the

weight of money rises back over 60%. The weight of money again drops below 50%

triggering the first solid price increase. After a period trading at the new higher odds

the odds begin to fall backed up by a high weight of money percentage peaking just

below the 70% mark. The odds drop and the weight of money continues to maintain

its high value, representing a high demand at the current price. As expected this pushes

the odds down yet again two more times until it finally bottoms out with the weight of

money dropping to just above 50%. The odds then move up one point which doesn’t

exactly fit the model because in order for the price to increase a value of less than 50%

is expected, however this could possibly be explained as a bounce back reaction to the

significantly big drop in the price in such a short period of time. Another rather long flat

stage proceeds with the weight of money continuing to stay high in the early stages an-

other dip in price is expected however the odds stay the same and the weight of money

drops slightly. Next another big price drop is observed with the weight of money in-

creasing dramatically back above 70% peaking at 80% at times. Similarly to the first

steep decrease when the movement ends the price bounces back up despite the weight

of money staying above 50%. This provides solid evidence that the odds and weight of

money are inversely proportional and contribute strongly to the market movements in

both directions.

6.2.2. Back and Lay Over-rounds

After running analysis on all of the markets the following results can be observed.

Reg: 84 23

CMPC3P2Y 6. Data Analysis

The above graph shows the results of analysis on the back and lay over-round. Each

market has a results set containing four results. This include the average back over-

round value when the price moves down. The average back over-round when the price

moves up, the average lay over-round when the price moves down and the average lay

over-round when the price moves up. In order to accept the alternative hypothesis that

both a lower back and lay over-round is more likely to lead to the market price moving

down the average back and lay over-rounds should reflect this in the results. As can

be seen in the results the overall mean back over-round is lower when the price moves

down and slightly higher for price increases. The same can be observed for the lay over-

round overall. However with mean results separated by only 0.0589309472% for the

back over-round and 0.0899720041% for the lay over-round the results remain slightly

in conclusive without a clear difference able to be seen. Also it can be seen on some

markets such as Tottenham vs Liverpool the complete opposite to the expected outcome

is observed, with a higher back and lay over-round leading to drops in the price. As

the over-round is a measure of the book percentage it is a measurement of the whole

Reg: 84 24

CMPC3P2Y 6. Data Analysis

market and not just a particular selection. Therefore this might explain some of the

unexpected results. For example movements on other selections will have an affect on

the over-round.

Looking more in depth at the affect book percentage has on market direction the above

graph shows the last price matched for the draw plotted against both back and lay over-

rounds in the AC Milan vs Roma match. It can be observed how both back and lay over-

rounds have an affect on market direction. This market is fairly non volatile throughout

with only three price movements the entire time. The first of which shows both back and

lay over-rounds reasonably low with the back over-round at approximately 100.6% and

the lay over-round at approximately 99.4%. The second movement is a price increase

in which it can be seen both over-rounds increase beforehand with the back over-round

exceeding 101% at times and the lay over-round exceeding 99.7%, however despite this

both over-rounds return to their original values just before the movement occurs. In the

final price movement towards the end the odds drop and yet again so do both the over-

rounds with the back over-round dropping below 100.2% as well as the lay over-round

dropping below 99%. The data shows clear evidence that in this market over-rounds

have an affect on market direction.

Reg: 84 25

CMPC3P2Y 6. Data Analysis

6.2.3. Trading In Non Volatile Markets

Both strategies that are proposed aim to reverse back and lay in non volatile markets,

meaning entering an unmatched back bet at the current lay price joining the queue of

money waiting to be traded at the higher price. If the price does not move in any direc-

tion then a reverse lay bet is fired meaning that an unmatched lay bet is entered at the

current back price again joining the queue of money waiting to be traded on the back

side of the market. Once both bets become matched this results in a one point profit

gain. This type of trading does not even require the market to move in any direction

therefore it has a very low risk association, which is exactly as planned per strategy.

The figure below shows how this is possible.

The figure shows the last price matched plotted against volume of money traded for

the AC Milan vs Roma match for the draw selection. As can be observed in the above

time period between 17:20 and 19:22 the odds stay the same with the back price at 3.45

and the lay price at 3.40. The columns along the bottom show amounts of money traded.

Throughout the series it can be seen large amounts of money being traded on both sides

of the market. In fact at the start of the series a total volume of £121,584.35 has been

traded on the selection, at the end of the series a total of £245,302.02 is traded showing

a total of £123,717.67 traded in the above time period whilst the market stays still. This

shows that there is enough traded volume throughout the series to queue on both sides

of the market, waiting for each bet to become matched. No movement is required.

In order to gauge how volatile a market is likely to be, working out the standard

deviation of the last price matched can be used. The standard deviation works out

Reg: 84 26

CMPC3P2Y 6. Data Analysis

how much the set of points deviate from the mean. Therefore if the market moves a

considerable amount the standard deviation value will be high, whereas if there is little

movement the standard deviation will be low. The formula used to work out standard

deviation is shown below.

Where n is the number of data points x bar is the mean of the data points and xi is

each individual point in the series. As the range between odds differ at different values

such as odds trading at 1.78 and 1.79 have an offset of just 0.01 whereas odds trading

at 4.2 and 4.3 have an offset of 0.1 the resulting standard deviation is divided by the

offset in each of the results. Applying this to all of the historic data set markets is shown

below:

The graph shows each markets standard deviation value after being divided by the

appropriate odds offset. It can be observed that non volatile markets such as the AC

Milan vs Roma match have a much lower value than more volatile markets such as

Reg: 84 27

CMPC3P2Y 6. Data Analysis

Everton vs Norwich and Man City vs Chelsea. AC Milan vs Roma shows a standard

deviation value of just 0.5799206691 whereas Everton vs Norwich and Man City vs

Chelsea show values of 1.48208257 and 1.932407519. The mean across all markets is

shown as 1.054980683. Working these values out during live analysis can be very useful

to provide a measure of volatility, limiting risk is very important for both strategies.

6.2.4. Volume Spikes

When large sums of money enter the market they represent a high demand, similar to on

a stock exchange if an organisation buys a large amount of shares in a particular stock,

this represents a demand at the current price and drives the share value higher. This can

also be seen on the betting exchange.

The above graph shows the last price matched plotted against the volume of money

traded on the Man City vs Chelsea match on the draw selection. The volume spikes are

shown by the tall grey columns. In this series there are three main price movements all

decreasing the price. Just before the first price drop a volume spike of just under £3000

is shown, resulting in the odds being forced down. Again just before the next price

drop another slightly smaller spike of just over £2000 forces the price down yet again.

Finally before the last dip yet another volume spike can be seen of just under £4000

forcing the price down even further. This shows that large amounts of money entering

the market can influence market direction. Volume spikes can be dangerous as they can

Reg: 84 28

CMPC3P2Y 6. Data Analysis

happen very suddenly shifting the market in either direction.

6.3. Conclusions

The historic data analyses has unearthed a variety of factors that influence market direc-

tion. The results of the analysis will be used in constructing rules in which to set when

analysing live data.

Firstly it is shown that the weight of money concept has an inverse relationship to

price, this means that when the weight of money increases the odds are likely to drop,

likewise if the weight of money decreases then it is likely that the odds will increase.

With all markets scoring higher than the 50 marker representing the even probability of

no relation and a mean score of 52.9221145 the hypothesis can be accepted.

The second factor identified as a market influence was the back and lay over-rounds,

although not as strong a relationship as the weight of money concept it is still observed in

the overall mean that a lower back and lay over-round lead to the odds decreasing while

a high back and lay over-round lead to an increase in price. However due to the over-

rounds being affected by other selections which in turn showed some markets showing

unexpected results where high back and lay over-rounds lead to price decreases and low

back and lay over-rounds lead to increases, the hypothesis can not be fully accepted as

a controllable factor.

It is confirmed and proven that trading in non volatile markets is possible even when

the odds do not change at all. A method of analysing the standard deviation on the last

price matched data points has been identified as a method to measure volatility. Trading

in less volatile markets means that the odds do not move much and therefore there is

less risk involved in trading on these markets.

Finally volume spikes were identified as another factor that influences market direc-

tion, the conclusions on this are some what of a warning moving ahead showing that

large amounts of money can move the market in either direction. Both strategies do not

use volume spikes as a method of predicting direction as volume spikes occur quickly

and have an immediate affect. Both the proposed strategies are grounded on long term

trading focusing on lowering risk which is not what volume spike trading provides.

Reg: 84 29

CMPC3P2Y 7. Implementation

7. Implementation

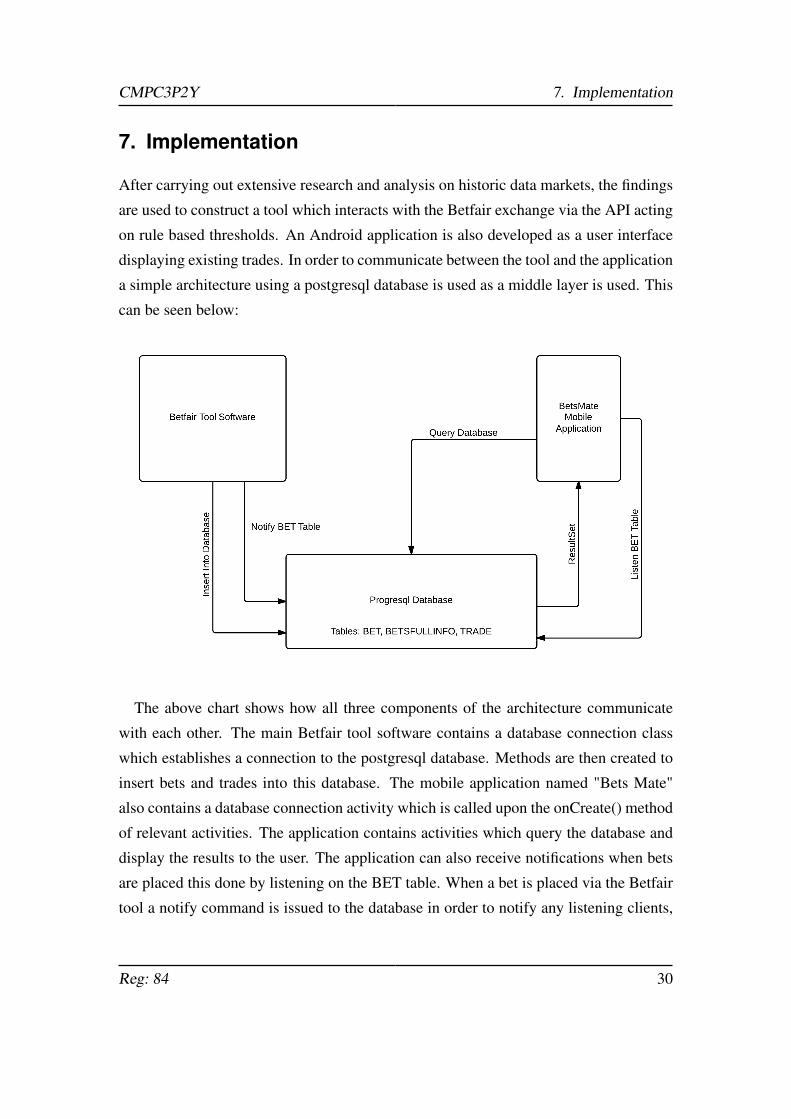

After carrying out extensive research and analysis on historic data markets, the findings

are used to construct a tool which interacts with the Betfair exchange via the API acting

on rule based thresholds. An Android application is also developed as a user interface

displaying existing trades. In order to communicate between the tool and the application

a simple architecture using a postgresql database is used as a middle layer is used. This

can be seen below:

The above chart shows how all three components of the architecture communicate

with each other. The main Betfair tool software contains a database connection class

which establishes a connection to the postgresql database. Methods are then created to

insert bets and trades into this database. The mobile application named "Bets Mate"

also contains a database connection activity which is called upon the onCreate() method

of relevant activities. The application contains activities which query the database and

display the results to the user. The application can also receive notifications when bets

are placed this done by listening on the BET table. When a bet is placed via the Betfair

tool a notify command is issued to the database in order to notify any listening clients,

Reg: 84 30

CMPC3P2Y 7. Implementation

in this case the application will acknowledge the notify and update via its notification

activity.

7.1. Automated Betfair Tool

For both strategies it was important to set up a framework to model both market and

selection data. To do so Java classes were set up to model a market and a second for

selection. This includes data such as current odds, amount of unmatched money, volume

statistics and other information. With this data key calculations such as working out the

weight of money and both back and lay over-rounds can be calculated. This data is also

stored in the Market and Selection classes as private fields. Market and Selection objects

can therefore be constructed to model the exchange data. The exchange framework is

modelled with 8 java classes which include:

• Market - Contains all information about a particular market such as market vol-

ume, back and lay over-rounds, market Id’s and names.

• Selection - Contains all information about a particular selection such as selection

volume, back and lay odds, available unmatched money, last price matched and

weight of money.

• MarketSelections - A MarketSelections Object contains a Market object and an

ArrayList of Selection objects that belong to the market.

• ExHeader - Sets up a connection to the exchange API by constructing an API

request header with a private session token.

• GlobHeader - Sets up a connection to the global API by constructing an global

API request header with a private session token.

• Bet - Stores information once a bet has been fired into the exchange, this contains

information such as the odds, volume, market and selection Id’s.

• Trade - Contains two Bet objects to model a trade. Trade objects are constructed

after a back and lay bet have been placed on the same selection.

Reg: 84 31

CMPC3P2Y 7. Implementation

• DatabaseConnect - Sets up a connection to the postgresql database.

In the main class targeted markets are selected to suit the proposed strategies, there-

fore they are required to have a reasonable market volume and be the match odds mar-

kets of football matches at least 3 hours before the kick-off. An ArrayList of Market

objects is used to store the relevant markets selected on the criteria. After the markets

have been selected the initial data is modelled into the Selection objects using various

API calls, finally when both market and selection data has been modelled a MarketS-

elections object can be constructed to represent a full model of the market. Once the

initial data has been modelled the market needs to be monitored for the purpose of

discovering the market volatility.

To do this a separate thread is launched which tracks the market prices and stores

them every 30 seconds. This thread is run for an hour in order to get a good idea of how

volatile the market and selections are. As was discovered in the data analysis in order

to work out a metric for volatility the standard deviation of the last price matched over

the hour is used. As well as the monitor thread another thread is launched to constantly

update the market and selection data, for both threads they are constructed with one

MarketSelections object, therefore multiple markets can be analysed at the same time to

increase ïnAnding optimum trading opportunities. The monitor and update threads are

run continuously, with the main thread set to sleep for 1 hour whilst the monitor thread

gathers market information.

The main thread is awoken when the monitor threads initial work is done, however

the monitor thread continues to record market prices and adjust the standard devia-

tion as appropriate. Meanwhile another thread is launched which is designed as an

entrance trigger. Again each MarketSelections object will construct an entrance trigger

thread called EntryTrigger, whose sole purpose is to wait until all the conditions of ei-

ther strategies are met, upon all conditions being met such as correct weight of money,

over-rounds, standard deviation and volume, a boolean variable is set to true and an

entrance bet is fired into the exchange at the current lay price as discussed in the strate-

gies. This is done using another call to the Betfair API. Once bets have been placed on

the exchange they are recorded and modelled by the Bet class. A row is also inserted

into the BET and BETSFULLINFO table in the database. Fiinally when a bet is placed

Reg: 84 32

CMPC3P2Y 7. Implementation

another thread is started called BetStatusUpdate whose sole purpose is to update the bet

status as unmatched or matched. This is very important as to switching between the two

exit triggers which are discussed below.

There are two exit triggers, the first of which is designed to either cancel unmatched

bets if conditions deteriorate to a point where the trade no longer looks appealing or to

fire a counter lay bet if the entry bet becomes matched. If the counter bet is fired then the

second exit trigger becomes active whose purpose is to either attempt to sell for a scratch

trade if available or cut losses at a 1 point loss if the open position deteriorates. This is

launched as soon as the entry bet becomes matched as a separate thread called StopLoss,

the StopLoss thread constantly checks the current lay price and if it slips by one point

in the wrong direction it will sell the bet immediately incurring a 1 point loss. This is to

ensure that no big losses are incurred. As soon as the counter lay bet becomes matched

the trade is complete, another row is inserted into the BET and BETSFULLINFO tables

as the lay bet. A Trade object is constructed and sent to the TRADE table in the database

containing information of both the back and lay bets. Finally as the trade is complete

the associated threads are killed.

7.1.1. Trading Thresholds and Rules

Using the findings from the data analysis a set of rules and thresholds can be set in order

to predict market direction. Focusing only on price decreases the following rules were

used.

Entering the exchange:

• Weight of Money - Due to discovering a strong relation between market direction

and weight of money this was set fairly high at 65% or higher.

• Immediate Weight of Money - The immediate weight of money is defined by

the weight of money just of the current back and lay prices. This threshold is set

to greater than 60% but no more than 90%. The reason for this is that because

when reverse backing at the lay price if the immediate weight of money is above

90% then it is unlikely that the unmatched bet will get matched in time before the

price moves. This is also a sign of a volatile market which is not the target.

Reg: 84 33

CMPC3P2Y 7. Implementation

• Back Over-round - A back over-round percentage of less than or equal to 100.6%

due to a slight correlation between low over-rounds and prices decreasing found

in the earlier analysis. As well as the slight correlation found during analysis,

due to the book percentage being capped at 100% due to arbitrage rules the closer

the over-round is to 100% the more this reflects that odds can not get any higher,

therefore one selection will have to move down.

• Lay Over-round - A lay over-round percentage of less than or equal to 99.5%.

Again due to a slight correlation between low over-rounds and prices decreasing

found during analysis, and book percentage rules.

• Standard Deviation - A standard deviation of less than or equal to 0.9. As has

been mentioned lowering the risk and trading on less volatile markets is key to

both strategies so a fairly stern threshold is used here, 0.154980683 below the

mean values found during analysis.

• Volume - It is important that the market and selection have enough liquidity to

trade on, this is to both push trades through and also stabilise the market. For this

reason the final rule is that there must be at least £200 on each side of the market

on the current back and lay prices.

Cancelling unmatched Bets:

Cancelling an unmatched bet was dependent on the position in the queue of money

waiting to be matched. For example if the money is right at the back of the queue and

the position deteriorates then it is more worthwhile cancelling the bet. Whereas if the

money is near the front of the queue then it is more likely to become matched sooner

inviting leniency in case the position materialises again. Also if the money is near the

front of the queue this means that there is money behind the current bet which means

even if the bet gets matched and the position deteriorates there is still money available

at the same price to scratch the trade immediately for no loss. In order to calculate the

position in queue the amounts of money traded and waiting are stored in the Bet class

when a bet is placed. This can then be checked against the current amounts matched

Reg: 84 34

CMPC3P2Y 7. Implementation

and waiting to work out position. For example:

difference = current total matched - bet total matched

If the current amount waiting is less than the amount available when the bet was made

take the difference from the amount waiting currently.

position = current amount waiting - difference

Else the current amount available must be more than the amount available when the

bet was made so take the difference from the amount waiting at the start of the bet as

more money has come on top, therefore the money is further down the queue.

position = amount waiting when bet was placed - difference

The percentage distance to the front can then be calculated as:

percentage distance to the front = 100 - ((position/current amount waiting)*100)

Therefore depending on the position in the queue cancelling an unmatched bet looks

at the immediate weight of money to asses whether the bet needs to be cancelled. If the

percentage distance in queue is less than 20% then if the immediate weight of money

drops below 30% it is cancelled. If the position in queue is between 20% and 50% a

threshold of 20% is used, and a position above 50% a threshold of 10% is used.

Scratch Trade:

In order to fulfil a scratch trade the same concept of queueing is used as for cancelling

an unmatched bet. However this time when the thresholds are exceeded a lay bet is

placed at the same odds as the matched back bet which therefore lays the bet for the

same as what it was backed at resulting in a scratch trade, no profit and no loss.

Stop Loss:

Reg: 84 35

CMPC3P2Y 7. Implementation

The stop loss is triggered if the price exceeds one point above the odds the back bet

was matched at. As soon as this occurs an immediate lay bet is fired into the exchange

cutting losses to one point.

7.2. User Interface

In addition to the software, a mobile application is also used as the main user interface.

The application is to be run on android devices. The application uses the Android 8

API. The purpose of the application is to display information to the user on any existing

or new trades that the tool is working on, as well as an overall profit/loss figure based

on previous trades. The app consists of 5 activities which include:

• MainActivity - The main activity is the main screen which is loaded upon open-

ing the application. This activity is fairly simple and contains two buttons, the first

of which takes the user to the ShowBetsActivity which displays current trades in

progress, the second of which takes the user to the ShowProfitLossActivity which

shows the user their current profit /loss figure on screen. The main activity also

establishes a connection to the postgresql database using a database connection

class called DBHelper. This in turn issues the LISTEN command on the BET

table in order to receive notifications on new bets.

• ShowBetsActivity - This activity is started by the main activity and shows the

user a list of current bets in progress on the exchange. The activity queries the

BET table to receive a results set of the bets stored in the table. Bets are displayed

on screen to the user showing which market the bet was placed on, whether it is

matched or unmatched, and the odds at which it was placed. If the bet is a back

bet it is displayed in light blue whereas if it is a lay bet it is displayed in light pink

as to fit with the Betfair colour scheme. Each bet is displayed in a table which

is click-able, clicking on an entry takes the user to the BetDetailsActivity which

shows more information about the bet.

• BetDetailsActivity - This activity is started by the ShowBetsActivity and shows

more information about the bet which was selected by the user. The id of the bet

Reg: 84 36

CMPC3P2Y 8. Results

is parsed to the activity via an Intent which can then be received to and used to

query the BETSFULLINFO table which returns more detailed information about

the bet including, weight of money, immediate weight of money, back and lay

over-rounds, standard deviation and links to both the market and selection on the

Betfair exchange.

• NotificationsActivity - This activity is started when the application receives a

NOTIFY command from the Betfair tool. The activity displays a pop up on screen

showing the new bet that has been placed.

• ShowProfitLossActivity - This activity is started by the main activity when the

user clicks the show profit/loss button. The activity simply shows the user their

current profit/loss figure on screen by querying the TRADE table in the database.

8. Results

Because of the API limits restricting access to the API by a maximum of 10 requests per

minute for a free access account in order to gather a good set of results the full personal

access account was purchased. This allows unlimited API calls therefore multiple mar-

ket analysis was possible. The tool was run for 20 days starting 19th April and ending

8th May. Trades where limited to £2 each meaning profits and losses were limited to a

few pence. A total of 39 trades where completed during this period. A table of results

are shown below:

Reg: 84 37

CMPC3P2Y 8. Results

The results show that over the 20 day period 39 trades were entered with an overall

cumulative profit of 42 pence. Only 4 of the 39 trades resulted in a loss the biggest of

which -7 pence in the Manchester United vs Sunderland match in which the stop loss

was triggered. The total of the four losses accumulates to 17 pence. 18 of the 40 trades

were successful the largest of which was in the Norwich vs Liverpool match for 6 pence.

The total of the profit accumulated by the 18 successful trades was 59 pence. 2 of the

trades were cancelled before they became matched due to the position deteriorating. It

is possible that more trades did this as an unmatched bet is not recorded in the database

observing this behaviour first hand was the only way in which they these types of trades

were recorded. 6 of the trades were cancelled at in play, this was most commonly

because the odds moved down before the entrance bet became matched. Finally 9 of the

trades resulted in a scratch trade where the bet was sold for the same odds as the back

price resulting in no profit and no loss.

Reg: 84 38

CMPC3P2Y 9. Conclusion

8.1. Strategy Success

Of the 39 trades the most commonly triggered strategy was strategy A with 32 trades

compared to only 7 which were triggered by strategy B. In comparison just 1 of strategy

B trades was unsuccessful, 4 were successful, 1 were cancelled and 1 was a scratch

trade. 3 of strategy A trades were unsuccessful 14 were successful 7 were cancelled

and 8 were scratch trades. Both strategies faired very well with strategy A profiting 37

pence and strategy B profiting 5 pence.

The overall results can be seen to steadily increase in profit shown in the graph below:

9. Conclusion

To conclude, based mainly on the work by Goncalves (2013) and Nordsted (2009) as

well as Webb (2013) and Heathcote (2012) four main factors of market influence have

successfully been identified and tested with extensive data analysis. Weight of money,

book percentage, market volatility and volume spikes were all shown to have an af-

fect on market direction. Integrating these factors a multithreaded automated peice of

software was developed. Live market data was able to be monitored and scouted for a

combination of the four influencing factors to predict market movements. The results

Reg: 84 39

CMPC3P2Y 9. Conclusion

show both strategies were very successful, such that only 12.5% of the trades resulted

in a loss in turn resulting in a 21% cummulative profit on stake over the 20 day period.

Reg: 84 40

CMPC3P2Y REFERENCES

References

Alberola, M. J. and Garcia-Fornes, A. (2013). Using a case-based reasoning approach

for trading in sports betting markets. Springer US.

Betfair (2013a). Betfair developers program. http:// bdp.betfair.com/ index.php?option=

com_frontpage&Itemid=1.

Betfair (2013b). Betfair developers program - compare access types. http:// bdp.betfair.

com/ index.php?option=com_content&task=view&id=36&Itemid=64.

Bets, . L. C. (2012). Betfair scalping trading techniques explained. http:// latest.

letscomparebets.com/ betfair-scalping-trading-techniques-explained/ .