Embed Size (px)

DESCRIPTION

Official Newsletter for IIANM

Citation preview

August 2009

La

Voz"The Voice" of Independent Agents since 1934

FREEADMISSION

IAN

M

ve

nt

ion

!

IIANM’s AnnualConvention is RightAround the Corner!

page 18

Page 2 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

IIABA and IIANM are ideally positioned to create an electronic bridge between product providers and independent agencies. IIABA has the technological expertise, systems and industry contacts; IIANM has local marketing and educational ability, as well as close relationships with agents. Together IIABA and IIANM can bring product providers to agents' desktops and make agents aware of what products are there and how to take advantage of them.

The Big “I” ADVANTAGE

You will need to log-in in order to view more information.

Please contact Rachel for your log-in information.

Products & Services

www.bigimarkets.com

New member service aims to help lower agency exposure to E&O claims.

IIABA recently introduced a new web-based agency resource called the Big “I” Virtual Risk Consultant (VRC) powered by Rough Notes to help members better serve their customers, generate increased sales and lower their exposure to E&O claims.

“One in five claims that we see with the Big ‘I’ Professional Liability Program are a direct result of recommendation or risk assessment errors alleged against the agent,” says David Hulcher, Big “I” director of agency E&O risk management. “The VRC will go a long way to help agents avoid these types of claims and will increase the professionalism of agency staff.”

The VRC offers a comprehensive suite of tools to help agency staff better understand customer operations and to identify risk exposure with business specific questionnaires and checklists that also provide solid customer file documentation should a claim arise. This powerful product allows members to create more professional customer proposals and effectively explain complex insurance coverage. The VRC also provides invalu-able content to assist the agency in successfully promoting its services in the way of pre-written business letters and hundreds of articles for use in customer communications and marketing.

“The VRC was created at the direction of the volunteer member agents who realized we had not only found a great E&O risk management and file documentation tool but also a tremendous enhancement to agency productivity, profes-sionalism and profit,” says Jack Sherrill, chairman of the Big “I” loss control working group and founder and senior partner of

Sherrill & Company in Savannah, Ga.

“The VRC is a culmination of a diligent search of the market-place for an affordable and easy to use risk analysis tools that will help agencies grow their business. It is thorough, afford-able, and easy to use. The product is supported by a strong partner in Rough Notes and their 130 years of experience pro-viding technical insurance content to agents. I strongly believe that member agents will see a positive return on investment, whether it is in growing their business or avoiding the cost of their E&O deductible, by subscribing to the VRC,” Sherrill adds.

“Helping in the development of VRC has been a great op-portunity for me to participate in creating the most dynamic sales tool and technical resource available to the independent agent,” says Peggy Ogren, Rough Notes vice president of sales. “Knowing that every agent in the nation will benefit from having it on their desktop has made this the most worthwhile experience I’ve had in the insurance business. Rough Notes and I are especially honored to be partnered with the Big ‘I’ and VRC.”

Members can learn more and purchase the VRC directly at www.iiaba.net/VRC. An annual subscription for an agency with 15 or fewer users is $250 per year, per state. The fee for agencies with over 15 users is $500. A four year subscription for the price of three at $750 and $1500 depending on agency user count is also available. This compares very favorably to similar products in the marketplace.

IIABA INTRODUCES BIG “I” VIRTUAL RISK CONSULTANT

Page 2 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

IIANM Staff

2008-2009 Officers

“La Voz” is the official monthly publication of the

Independent Insurance Agents of NM 1511 University Blvd. NE Albuquerque, NM 87102.

(505) 843-7231. Fax (505) 243-3367.

President/CEOThom Turbett, CIC

VP Of Membership ServicesLorri Gaffney

Director Of CommunicationsRachel Sheffield

Director Of Insurance ProgramsCarmen Reese Porter, ACSR, CISR

Director Of Education Jeff Straight, CIC, LUTCF

Receptionist / Member Services Associate

Renee Trujillo

ChairAngela VasquezVice-ChairAlma Franzoy-CapronSecretary/TreasurerKathy YeagerNational DirectorPatty Padon, AAI, CIC, LUTCFImmediate Past ChairSam Conlee

Big I Advantage 02

Tech Talk 08

IIANM's Annual Convention Incentive - 5% off in August! 18

Partners Program Company Listings 24

Last Chance Seminar Registration 26

Win an iPod Shuffle! 28

Education Edge 29

August's Clickable Calendar 30

Odds n Ends 31

FeaturesThis publication is intended to provide accurate and authoritative information on the subject mat-ter covered, but is distributed with the under-standing that neither IIANM, nor any contributing author, publisher, contributor or advertiser is rendering legal, accounting or any other profes-sional service and assume no liability whatsoever in connection with its use. Further, the electronic links to our advertisers and/or contributors found in this publication are provided as a courtesy to our readers and do not necessarily indicate an endorsement by IIANM.

News items from members of Independent Insurance Agents of New Mexico and the general insurance industry are encouraged. The advertis-ing deadline is the fifteenth day of the month, pre-ceding publication.

Advertising rates are available upon request.

Please contact Rachel Sheffield at [email protected] for details

New Mexico Mutual Adds 3 New Companies for NM Businesses 05

The Importance of Customer Retention 06

Joint Fly-In 11

Big "I" Eagle Agency Expanded 13

L&H Trends - The Perfect Time to Give a Gift 15

OSHA Rule: Big Fines for Employers Whose Workers Drink at.... 16

A Retention Clause is All You Need, Right? 20

Fewer Customers Shopping for Auto Insurance 23

9 Steps to Better Delegating 25

American Mining 09

Burns & Wilcox 10

Colonial General Insurance Agency, Inc. 22

Market Finders, Inc. 07

NCMIC 21

New Mexico Mutual 04

RPS - Risk Placement Services 14

La Voz"The Voice" of Independent Agents since 1934

In Every Issue

Advertiser Index

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 5

The five road show events will take place on the following dates and locations:

Las Cruces August 18th

Roswell August 19th

Albuquerque August 20th

Santa Fe August 26th

Farmington August 27th

“The expansion will offer a local rate structure competitive with out-of-state insurers” said Becker. “We were created as a New Mexico business for New Mexico businesses and inde-pendent agents.”

As part of the roll-out and consistent with our vision, two exist-ing companies will undergo name changes. Southwest Casu-alty Company will become New Mexico Southwest Casualty Company and Foundation Reserve Insurance Company will be renamed New Mexico Foundation Insurance Company.

Independent agents and customer service representatives can RSVP for the meeting in their nearest area by clicking here or by contacting New Mexico Mutual Marketing Assistant Mike Baldwin at 505-343-2831 or [email protected].

Las Cruces August 18thRoswell August 19thAlbuquerque August 20thSanta Fe August 26thFarmington August 27th

New Mexico Mutual is adding three new companies to its umbrella of workers’ compensation insurance companies

and will be traveling throughout New Mexico this month to introduce them to independent agencies.

By September 1, 2009, New Mexico Mutual anticipates binding business in New Mexico Premier Insurance Company, New Mexico Assurance Company and New Mexico Employers As-surance Company.

Norm Becker, President and CEO of New Mexico Mutual said, “The addition of these three new companies will allow New Mexico Mutual to continue to fulfill our mission of ensuring that all New Mexico companies have access to affordable workers’ compensation insurance.”

The new companies will provide independent agents and their clients a total of six coverage options with the New Mexico Mutual Group. These six options will provide competitive rates aligned to particular risk exposure, class of business, safety experience and sophistication.

With the new companies, New Mexico Mutual can continue to meet the needs of New Mexico businesses by providing sound underwriting and quality in-state services, all at competitive rates.

To formally introduce the new companies to independent agent partners, New Mexico Mutual will host five road shows throughout New Mexico. Becker and other members of New Mexico Mutual’s senior management, marketing and under-writing team will provide an overview of the new companies and answer questions.

Adds Three New Companies for New Mexico Businesses

by Mike Zambrano

Page 6 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

The Importance of Customer RetentionCustomer service is critical to agency profitability and growth.

Outstanding customer service leads to customer satisfaction.

Customer satisfaction leads to customer loyalty.

Customer loyalty leads to retention and referrals...

Retention is the key to profitability and referrals are the key to cost-effective growth.

We all know that, don't we?

Of course, we all know that. But how many of us know, from the standpoint of customer satisfaction, loyalty and reten-

tion, how well we actually focus on customer service? Without the usual pontificating, below are some customer service facts and statistics that should demonstrate how valuable your CSR's are to your success. At the end of this article, there are a couple of downloadable tests you can give your staff to see how you measure up.

The Importance of Customer Retention

Depending on the nature of the account, it takes 2-7 years for a new insured to be profitable for the agency, according to a composite of several agency management studies. And, an agency must spend, on average, $2.60 for each $1.00 of com-mission to place the account on the books.

For each 5% increase in your retention rate, you will increase your agency profits by at least 10%. The U.S. Consumer Af-fairs Department estimates the profitability increase to be 25-85% and, according to a Harvard Business Review article, this figure could be as high as 100%.

According to the International Customer Service Association and the U.S. Consumer Affairs Department, it costs FIVE times as much to acquire a new client as is does to retain and service an existing one. Service guru Tom Peters estimates that it takes $10 in new business to replace $1 of exist-ing business, given normal attrition rates in the retail/service sector.According to Technical Assistance Re-search Programs, Inc., if a customer has a bad service experience, they will tell at least 8-10 people...20% of them will tell as many as 20 people. One estimate is that it

takes 12 positive experiences to make up for 1 negative expe-rience. The average satisfied customer will tell 5 people about their experience.

According to Audits & Surveys, Inc., only 4% of people with real or perceived problems or complaints will bring them to the attention of the business. Therefore, for every complaint you

receive, you probably have 26 customers who have also had a bad experience but never told you.

In an often cited study by the American Productivity & Quality Center, 68% of custom-ers that take their business elsewhere do so because they perceive the business to be indifferent to them. If a customer leaves be-cause of an unresolved problem, 91% of them will never come back. However, if a problem is resolved, 54-70% of these customers will come back...if the problem is resolved on the spot, 95% will come back.

According to the Strategic Planning Insti-tute of Cambridge, PA:

• Businesses with low service quality average 1% return on sales.

• Businesses with low service quality lose 2% of their market share annually.

• Businesses with high service quality aver-age 12% return on sales.

• Businesses with high service quality gain 6% market share annually.

How do you measure up? Take the following two tests to find out:

Customer Service Self-Test

Customer Retention Awareness Test

by Bill Wilson

Page 6 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009Page 20 Independent Insurance Agents of New Mexico - www.iianm.org - * September 2008

www.marketfindersnm.com

Since 1977New Mexico’s Locally Owned Managing General Agency

Representing some of the most financially strong and innovative insurance companies in the specialty marketplace!

Top-Tier Markets For:

Commercial / Public AutoGeneral LiabilityProperty / VacantsGarage / DealersLiquor LiabilitySpecial EventsInland MarineDirectors & Officers LiabilityProfessional Liability / E&OCommercial UmbrellaWatercraft / Motorcycles / ATVsPersonal UmbrellasHomeownersMobile HomesDwelling Fire / Vacants

At Market Finders, Inc., our mission is to professionally provide quality specialty markets and service to the Agents of New Mexico.

Market Finders, Inc.4910 Alameda Blvd NE - P.O. Box 90280Albuquerque, NM 87199

Phone: (505) 822-8711Fax: (505) 822-1165Toll Free: (800) 530-8711

ww

w.m

arke

tfin

ders

nm.c

om

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

1.

It's always handy to be able to do a screen capture, creat-ing an image of part or all of your screen. Some versions of Windows, and all versions of Mac, have this capability in the basic operating interface, but it's usually very limited. Jing is a free, full-featured screen capture utility that is available in both Windows and Mac versions.

What makes Jing stand out from the limited built-in screen capture capability is its annotation features. Once you capture the part of the screen you want, you can draw arrows, create boxes, add text, and more. So, for example, if you're capturing a screen from your Web site to point out a change you want made, you can annotate the image right in Jing. You can save it as an image file (which means you have to delete it later, of course) or you can just capture it straight to your clipboard and paste it into an e-mail or document.

Jing will also make screen videos-with sound-if you want to show something in more depth than a screenshot will display. If you use the video capability, I recommend purchasing their pro upgrade, which is a nominal $15 per year and has im-proved video features.

2.

Music might seem to be a personal, non-business pursuit. For many of us slaving away over a hot keyboard, background music drowns out ambient noise and allows us to buckle down and work. Pandora is a terrific free (advertising supported) service. It is a clever implementation of Internet radio. Instead of searching for existing Internet radio stations-many of which are going out of business due to new music company licensing fees-Pandora lets you create up to 100 custom virtual radio stations. Using their "Music Genome" technology, you enter either a favorite artist or a favorite song. Pandora takes a few moments, and then creates a stream of music that has all the same characteristics.

As I'm writing this, my radio station called "Leon Redbone" is playing. Redbone is an old-style singer (who sounds like

he has a mouthful of stones) who sings old favorites. Other stations I have created include "Ricky Nelson" and "Fats Domino," which are mostly 50s and 60s songs. I also have a "George Jones" station (country western).

For those with iPhones, there is a free Pandora application in the App Store. Once you sign in, all your radio stations will ap-pear. Even with all my music in iTunes, Pandora has far more and will play for hours without any interruption.

The pro version, called Pandora One, is $36 per year and gives you faster download streaming, a mini desktop player (instead of using the browser), and supports the company.

3.

Everyone needs to keep follow-ups, to-do lists, and other re-minders somewhere. When my previous task manager, Sandy, suddenly went out of business, I switched to Remember the Milk. Remember the Milk is a free, Web-based task manager. There are multiple ways to tag and identify tasks and remind-ers. You can set up notifications to remind you by e-mail and/or text messages.

You can set due dates with plain English, such as "Tuesday" or "Aug 5" and it will automatically convert it to the correct for-mat. Nagware is built in, if you want it. It also plays nicely with all the usual technology suspects: Twitter, Jott, Google Gears, and more.

As with any Web-based service, you have to be online to use it. Remember the Milk has an iPhone application that actually downloads all your data to the iPhone, so you can use it even if you're not online.

The pro account is only $25 per year (required for the iPhone application) and includes priority support.

4.

eBay is well-known, of course, for its enormous auction site. It seems you can buy or sell almost anything. In fact, I sold my 20-year-old Jeep on eBay. You can easily play for hours on eBay, but I use it regularly for business.

Five Favorites:This month you'll get to learn about five of my favorite sites and services. You'll certainly know some, but you might find something useful (or something you didn't know).

i n t e rne t r ad io

Page 8 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

G. Barry Klein is a former insurance agent who maintains UltimateInsuranceLinks.com as an industry service. He can be reached at [email protected].

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 9

There are an amazing number of discount retail merchants selling brand new goods through their online stores. If you have an eBay account, and preferably also a PayPal account (their online payment system), you can buy supplies in min-utes, instead of taking a long trip to the store.

For example, we use an HP multi-function printer that has six different cartridges. They're available in sets, of course, but we tend not to use them evenly. Since we're mostly printing docu-ments, for example, we use far more black refills than colored ones.

To buy a new refill or two, I just search eBay for "HP02 black" and get countless dealers, almost all with free shipping. Pick-ing one, buying it with "Buy It Now" and paying with PayPal takes a total of two or three minutes, far less than a trip to Staples. It will show up in the mail in a few days.

5.

Like eBay, Amazon is really a large marketplace. As a mer-chant, Amazon itself is one of the world's largest stores. Note

that that was an unqualified statement- Amazon is not just one of the largest online stores; it is one of the largest stores-peri-od-outpacing most brick-and-mortar stores. You can buy most retail products from Amazon, usually at less than retail prices. If you have an account established, their 1-Click ordering is even faster than buying on eBay. For larger items, I usually buy from Amazon. Like Costco, their customer support is leg-endary (compared to dealing with a large number of unknown dealers on eBay).

"Prime" is their shipping program, for regular purchasers. For a flat $79 per year, you get unlimited, free two-day shipping on any item marked "Eligible for Prime," which is most of their stock. To put it in perspective, the fee comes out to less than $7 per month, which is less than the shipping charge for just one item. Between our home and office, UPS usually delivers five to 10 boxes per week. We're not only saving significant time running around from store to store, but we're also usually getting the best price.

Who has the ability to handle all your specialty insurance needs?

Albuquerque, New Mexico(866) 643-8538 / (505) 822-0018 / fax (505) 822-0092

scottsdale.burnsandwilcox.com

Global Resources. Local Relationships.

Professional Liability

Umbrella & Excess

Employment Practices

Commercial Property

Products Liability

General Liability

Commercial Auto

Personal Lines

is

The

is

TheAnswer

Your Specialty Insurance Professionals

20688 Burns_LaVoz_6.75x9.25.indd 1 1/15/08 3:54:25 PM

w w w . s c o t t s d a l e . b u r n s a n d w i l c o x . c o m

ww

w.s

cott

sdal

e.bu

rnsa

ndw

ilco

x.co

m

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 11

Who has the ability to handle all your specialty insurance needs?

Albuquerque, New Mexico(866) 643-8538 / (505) 822-0018 / fax (505) 822-0092

scottsdale.burnsandwilcox.com

Global Resources. Local Relationships.

Professional Liability

Umbrella & Excess

Employment Practices

Commercial Property

Products Liability

General Liability

Commercial Auto

Personal Lines

is

The

is

TheAnswer

Your Specialty Insurance Professionals

20688 Burns_LaVoz_6.75x9.25.indd 1 1/15/08 3:54:25 PM

I n July more than 1,000 professional health insurance ad-visors, agents, brokers, consultants and employee benefit

specialists met with more than 400 Senate and House offices as part of the Health Insurance Agent & Broker Alliance health care reform fly-in on Capitol Hill.

The Big “I” worked with other health producer associations to form the Health Insurance Agent & Broker Alliance, which consists of: the Big “I,” AHIA-NAIFA Health and Employee Benefits (AHIA), The Council of Insurance Agents & Bro-kers (CIAB), the National Association of Health Underwrit-ers (NAHU) and the National Association of Insurance and Financial Advisors (NAIFA).

Big “I” members came to the Hill representing two viewpoints in the health care debate: as health care advisors to con-sumers and as small business owners. Fly-in participants had meetings with their representatives in Congress on the critical role professional health insurance agents and brokers play in providing health care to millions of Americans. They emphasized the need to maintain and expand both choice and access, reduce health care costs and improve health care quality.

When the idea of the joint fly-in was conceived, the Alliance hoped to get 400 participants total from the five associations, but expectations were exceeded more than twofold when more than 1,000 agents and brokers from 49 states attended.

Brian Baker, vice president of Bouchard Insurance in Clear-water, Fla., said he thought the fly-in was “great” and “en-joyed meeting so many colleagues.” The enthusiasm and energy at the breakfast hosted by the alliance prior to the pilgrimage to Capitol Hill reflected Baker’s sentiment. Baker said he thought “the members of Congress were impressed with how many people showed up. There was good atten-dance, and I think that helped.”

Steve Spiro, president of Spiro Risk Management, Inc. in

Valley Stream, N.Y. and a member of the Big “I” government affairs committee, met with several offices and emphasized that “there are too many uninsured people, and yes, reforms are needed, but we should not be throwing the baby out with the bathwater.” Spiro stressed the importance of not rushing the process but instead to ensure it’s done correctly.

As the House and Senate debate comprehensive health care reform legislation, the joint grassroots fly-in provided an opportunity for the health insurance agent and broker community to send a strong message to Congress to pre-serve the private delivery of health insurance and to oppose the creation of a government-run public plan.

The House unveiled its version of reform while the Senate continues to move forward on a dual track with bills in both the Committee on Health, Education, Labor and Pensions (HELP) and the Committee on Finance.

In addition to the “Alliance,” whose collective memberships represent more than 500,000 professional health insur-ance advisors, agents, brokers, consultants and employee benefit specialists, many in the health care and business communities are concerned that a public plan will lead to diminishing quality in health care that leaves taxpayers holding the bag.

Spencer Houldin, principal of Ericson Insurance in Wash-ington Depot, Conn. and chairman of the Big “I” government affairs committee, said taxpayers will end up paying for a government-run program. “This country is built on capital-ism and choice, but a government-run program would end up being subsidized,” says Houldin. He is concerned that the current language in the bill would “force people to go to the government plan.” The grassroots fly-in could not come at a better time with health care reform front and center in both the House and the Senate.

On the Hill

Agents Storm Capitol Hill for Health Care Fly-In

by Margarita Tapia

More than 1,000 agents voice support for reform but object to government-run plan.

Page 12 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

What is Eagle Agency?Eagle Agency is a general agency created exclusively for IIABA members.

Easy access to top-rated carriers

Low volume commitments

No fees

Opportunity to receive direct contracts with the partner carriers

Competitive commissions (66% of the commissions we receive)

Gross commissions vary, depending on the line of coverage and the state.

Eagle agents retain ownership of all the business placed through the Eagle Agency

�

�

�

�

�

�

�

Who are the carriers?

MetLife Auto & Home

Travelers Personal

Travelers Commercial

Availability varies by state, visit

www.independentagent.com/Eagle

to view an availability chart.

How do I apply for MetLife?

To be considered for Eagle Agency, log onto Big “I” Markets at

www.bigimarkets.com and select Eagle Met from the offline products menu. You

will be instructed on how to proceed from there.

If you have not yet registered for Big “I” Markets you can do so by going to the Big

“I” Markets home page and clicking on the “register here” button.

How do I apply for Travelers?

To be considered for Travelers, log onto Big “I” Markets at

www.bigimarkets.com and select Eagle Travelers from the offline products menu.

You will be instructed on how to proceed from there.

If you have not yet registered for Big “I” Markets you can do so by going to the Big

“I” Markets home page and clicking on the “register here” button.

Contact us.If you have any questions

about Eagle, please

contact [email protected] or

call (800) 221-7917.

Which company can I apply for?

In states where both

carriers are available,

agents may work with

either or both!

What about volume requirements?

Each company requires

two new policies a

month in personal lines

and Travelers

Commercial requires

two submissions a

month.

Minimum Qualifications To be considered for Eagle

Agency an agent must

have three years of

experience as a licensed

producer or have extensive

industry experience (i.e.

former underwriter, CPCU

etc). If the agent is brand

new to the business

consideration will be given

to agents who can quantify

that they have licensed

support staff with at least

three years of agency

experience.

Page 12 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

F or over eight years the Eagle Agency has been a successful part of the Big I Advantage portfolio of markets.

Eagle Agency was created primarily to assist newer and/or small agencies get their feet on the ground.

Eagle Agency is a general agency created exclusively forIIABA members. It gives Big “I” member agencies easy access to top-rated carriers for personal lines with low volume commit-ments and no fees. After achieving a predeterminedlevel of written premium with Eagle Agency, if the book of busi-ness is profitable, Eagle agents will have the opportunity toreceive direct contracts with the partner carriers.

Eagle Agency offers competitive commissions on new and renewal business. (Commission is 66% of the commissions we receive.) Gross commissions vary, depending on the line of coverage and the state. Eagle agents retain ownership of all the business placed through the Eagle Agency.

Eagle agents have placed more then $9 million of premiumwith the program and many agents have gone on to receive di-rect appointments. At no charge, member agents receive ac-cess to online underwriting information including motor vehiclereports, CLUE reports and insurance scoring.

Comparative rating software also is provided so risks may be underwritten and bound in an Eagle agent’s office. Until recently, Travelers has been the sole company Eagle has worked with in only a dozen states. That has changed.Eagle has procured an agreement with MetLife Auto& Home® to expand into every state EXCEPTCalifornia, Delaware, District of Columbia, Michigan andNew Jersey. Expansion into California and New Jersey is planned for MetLife Auto & Home® in 2009.

Travelers also continues its support of the Eagle Agency and is now available in every state EXCEPT Alaska, Hawaii,Louisiana, Massachusetts, Michigan, North Dakota, South Dakota, Texas, West Virginia, and Wyoming. In addition to personal lines, agents can now access the Travelers Select Accounts for small and middle market commercial business. Travelers is now managing the Eagle program through its national distribution channel, rather than through the former regional structure. This change will give the Eagle Agency and its members access to uniform appointment processes, centralized training, service and support, and will also allow expansion into most states. Florida will be available for auto-only appointments. Auto ONLY appointments will also be avail-able in specific counties within coastal states that are currently under CAT management guidelines.

Which Company Can You Apply For?In states where both carriers are available, agents have the choice of which company to work with or they can chooseBOTH. Each company requires two new policies a month in

personal lines and Travelers Commercial requires twoSUBMISSIONS a month. Minimum Qualifications To be considered for Eagle Agency an agent must have three years of experience as a licensed producer or have exten-sive industry experience (i.e. former underwriter, CPCU etc). If the agent is brand new to the business consideration will be given to agents who can quantify that they have licensed support staff with at least three years of agency experience.

How to ApplyTo be considered for MetLife Auto & Home® log onto Big “I” Markets at www.bigimarkets.com and select Eagle Met Personal Lines from the Offline

Products menu. To be considered for Travelers please log onto www.bigimarkets.com and select Eagle Travelers Personal Lines from the Offline Products menu. For the commercial mar-kets select Eagle Travelers Commercial. There you will be instructed on how to proceed. If you have not yet registered for Big “I” Markets you can do so by going to the Big “I” Mar-kets home page and clicking on the “register here” button.

What Happens Next?Once on Big “I” Markets you will be instructed on how submit a quote request. An Eagle Agency team member will review the information in your request.

Upon approval of your initial submission you will receive an email directing you to either a MetLife Auto & Home® mar-keting representative or the Travelers Netappoint applica-tion. You will also receive a cover letter explaining how the Netappoint process works.

The expansion of Eagle Agency provides a great opportunity for members in most of the country to expand their inven-tory of markets and to increase the size of their agencies. At the same time more states will now have the opportunity to benefit from the revenue sharing arrangement Eagle Agency has with participating States.

So if you meet the minimum requirements and you need access to more personal lines markets, sign up for Eagle Agency today!If you need more information about Eagle Agency to help you decide if it is right for you, send an email to [email protected] and a representative will contact you.

Big “I” Eagle Agency Expanded New carrier, more states added to the program.

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 13

www.

RPSi

ns.c

om/s

cotts

dale

8700 East Northsight Blvd., Suite 100, Scottsdale, AZ 85260-3671

Please visit us at www.RPSins.com/scottsdale

WA

OR

MT

ID WY

NVUT

CO

NM

AZ

For information about becoming an RPS broker call our Marketing Directors at

Underwriting and Brokering from our five locations (Casper, Boise, Denver, Scottsdale and Seattle)

Accounting and Claims handled from our Scottsdale location

Proud Members of AAMGA, NAPLSO, PLUS and Various State Independent Agency Associations

Excellence in Service

Relationship Driven

AND MORE!

Property Professional LiabilityPrograms General Liability

Excess & Umbrella Transportation Inland MarineGarage Liability & Physical DamagePersonal Lines

L&H Trends

by Dave Evans

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 15

The Perfect Time to Give a Gift

O ne consequence of the faltering economy has been the breathtaking increase in the national debt. In the near

term there doesn’t seem to be an immediate impact on infla-tion. However, many economists are voicing concern about the long-term prospects for a return to the inflationary period of the mid-1970s. In order to reduce the size of the deficit – which President Barack Obama has pledged to do once the economy is back on track – there will have to be an increase in revenue to the federal government. There has been a lot of discussion regarding raising income taxes on Americans who have incomes in excess of $250,000 annually. But, federal income taxes are not the only avenue for more revenue. The opportunity to raise the estate tax is another tempting target because it directly impacts a much smaller number of people. The estate tax situation has been murky since the 2001 tax law, which increased the estate exemption and eliminated the federal estate tax for one year with a return to the 2001 levels in 2011.

While the ultimate size of the estate tax exemption, or the amount of a person’s includable estate that is subject to income taxes, is not yet known, there is no doubt that people with larger estates should be refocusing on estate planning reduction strategies to lower their potential estate tax liability. To that end, one of the most basic estate planning techniques is making lifetime gifts. The annual gift tax exclusion, or the amount that someone can give to any individual each year without it being considered a taxable gift (which is indexed for inflation), is $13,000. Thus, a married couple will be able to give up to $26,000 each to multiple recipients without incurring any federal gift tax.

Gifts of the annual exclusion amount to children, grandchildren and other beneficiaries are often recommended as an excellent way to reduce one’s taxable estate at no transfer tax cost.

Outright gifts to grandchildren of the annual exclusion amount will also be exempt from the generation-skipping transfer tax (the GST). Gifts in trust for grandchildren who qualify for the gift tax annual exclusion can also qualify for exclusion from the GST if the trust is properly structured. Payments of tuition, if paid directly to the educational institution, and payments of medical expenses, if paid directly to the provider of the servic-es, are also transfers that are not considered taxable gifts and are not subject to GST.

Gifts may be “split,” meaning that even if one spouse makes the entire gift, he or she may use the other spouse’s annual exclu-sion amount if that spouse consents. To illustrate, a wife can give the entire $26,000 to a child with no gift tax cost, as long as the husband consents to having his annual exemption applied to the gift. For this reason, many clients make the annual gifts in January, to be assured that both spouses are alive at the time of the gift. Estate planning professionals face the trade-off that when lifetime gifts are made, the recipient’s basis for calculating any future gain for tax purposes is the donor’s basis, which is usually lower than the market value. When beneficiaries receive an inheritance consisting of property, they receive a “step-up” in basis valued at the date of death (or six months later if elected). So from a beneficiary’s viewpoint, they typically would prefer receiving an asset with a step-up in basis through an inheritance

rather than a gift. However, with the significant reductions in the value of stocks and real estate, now may be a per-

fect time to consider making lifetime gifts, rather than waiting until death to transfer assets.

Independent insurance agents should be having a conversation with their

higher net worth clients to discuss the most advanta-

geous approach for their situation.

Advise your high net worth clients on the advantages of the gift tax exclusion.

Page 16 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

The Environmental Improvement Board (EIB) held apublic hearing to approve new Occupational Health &

Safety Bureau (OHSB) regulations to prohibit unlawfuldrug use and alcoholic beverage use at the workplace.The new regulations become effective soon,and apply to all industries in the state. This means every business – from banks, accountants, and title companies to contractors, plumbers, electricians and suppliers – will have to comply or face the possibility of fines.

The regulations were developed following the highlypublicized death of a road construction worker lastyear who had been drinking beer with co-workers afterwork hours on the highway bridge his employer wasconstructing.

The regulations require employers to develop andimplement a written policy prohibiting unlawful drug useand alcoholic beverage use by employees at their place ofemployment. This is the first time the OHSB has directlyrequired employers to write and implement a particularpersonnel policy. Of particular note for constructionsites, the regulation also makes no distinction betweenwork site drinking during working hours and drinkingafter working hours (although those in food servicesand agriculture who must test alcoholic beverages forquality control are exempt as long as they do not becomeintoxicated).

Employers who develop a new policy to comply with thisnew rule would be wise to review it with employees andhave the employee sign a form that states the employeehas received a copy of the policy and understands itscontents. A sample policy and signature form will soonbe available on our website at www.nmhba.org.OHSB fine costs for violations of these regulations are

not covered by workers’ compensation insurance and arethe sole responsibility of the employer. Injury or death isnot required to trigger for the fines; it is drinking and druguse on the job site.

Large Fines and Possible Jail Time

The new rule does not contain its own fines. Regularfining policy of OHSB will apply. Fines for violationof OHSB regulations have varied widely based uponeach circumstance, but one trend has been clearly seen:the larger the company committing the violation, thelarger the fine. Under NM Statutes any employer who"willfully or repeatedly" violates OHSB regulations mayreceive a civil penalty between $5,000 and $7,000. If theemployer has received a citation for a violation (whetherserious or not) the civil penalty is not to exceed $7,000per violation. If the violation seems especially willfuland serious, (an example from other OHSA enforcementwould be for the use of unsafe equipment) the employermay receive a fine of up to $7,000 per day until theunsafe situation is remedied.

If an employee dies as a result of the violation the penaltybecomes criminal, and the fine may go up to $10,000or result in imprisonment of the employer for up to sixmonths. If the conviction is for a second conviction,the fine and imprisonment may double to $20,000 or 1year in jail. Recent OHSB threats of jail for repeatedviolations have been reported by NMHBA contractormembers.

General Contractor Fines for Subcontractor Violations Possible

For a general contractor on a project, fines may be leviedfor violations by either a direct employee or the employeeof a subcontractor. If a general contractor has had two or

Rule: Big Fines for Employers Whose Workers Drink at theWorkplace

Page 16 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 17

more subcontractors receive violations within two years,the general contractor is labeled a “repeat offender” andupon the third violation fines may double and jail timecould be involved.

What Causes an OHSB Investigation?

There are five general reasons that a business or publicentity may be inspected:

1. A complaint filed by an employee or theirrepresentative

2. A referral from another governmental agency ormember of the public

3. A general schedule inspection

4. A fatality investigation

5. An accident where three or more individuals arehospitalized

Upon receipt of a complaint or referral, the ComplianceProgram Manager decides whether or not to initiate aninvestigation. If an investigation is decided upon, it iseither in the form of an official letter of inquiry into thesituation and the nature of the complaint, a telephone call, by a fax inquiry, or in an on-site inspection.

An inspection may be performed on any complaintor referral. OHSB’s staff have stated they sometimesstop to check a job site next door to one on which theyhave received a complaint just because they are in theneighborhood. Homeowners next door to a commercialconstruction project in downtown Albuquerque (whoobjected to the noise from the construction project) notonly complained to OHSB about workers drinking beeron the job site after hours, but took a video of the eventand sent it to television stations where it was aired. Atthat time the incident was merely an embarrassment forthe contractors involved. Under the new rules, fineswould be the probable result. (At that particular incident,no one could really tell if the pictures showed cans ofalcoholic beverages or soda, so no action could be taken.)Here is the text of the new regulation for the constructionindustry (the regulations for general industry andagriculture contain the same new language):

Rule: Big Fines for Employers Whose Workers Drink at theWorkplace

11.5.3.10 PROHIBITION AGAINSTUNLAWFUL DRUG USE AND ALCOHOLICBEVERAGE USE IN THE PLACE OFEMPLOYMENT

A. Employers shall provide a place of employmentthat is free of unlawful drug use by employeesand free of alcoholic beverage use by employees.To determine whether an employer has violatedthis subsection, the department shall considerwhether the employer knew, or with the exerciseof reasonable diligence could have known, of thepresence of the prohibited unlawful drug or alcoholuse.

B. Employers shall develop and implement a writtenpolicy prohibiting unlawful drug use and alcoholicbeverage use by employees in the place ofemployment.

C. For purposes of this section, “place ofemployment” does not include a location whereemployees of an employer are present to participatein an event, the primary purpose of which is notwork-related.

$209

$181

$143

$181

5% Off!in August

Attention All Agency Members:

5% Off Registrat ions Received in the month of August!

“I have enjoyed my time at all of the IIANM conventions I have attended. The meetings with other agents and carriers are really helpful in getting your arms around what’s going on in the industry. The golf tournament is always 1st class. There is never a shortage of food, libations or good times. If you want a couple of days to relax, reload and see old friends then join me at the convention.”

~Bruce V FosterCress Insurance Consultants, Inc.

Sponsors & Exhibitors: Click HERE

Page 20 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

A n agency owner told me the other day that agency acquisitions were not that hard. Very little analysis was

really required and most due diligence was unnecessary. He advised that not much risk was involved if the buyer just based the deal on retention or as some call it, an earn out. Let's test his hypothesis.

Most deals require a 20% down payment even if the deal is retention based. Consider a worst case scenario where nothing renews. The 20% down payment, which is usually a substantial sum, is wasted. So how did the retention clause protect the buyer? Sure, if they had not purchased the agency on a retention basis, they would have lost more, but good due

diligence would likely have provided greater protection against the total loss.

That may be an ex-treme example but disasters like this do happen when buyers do not complete adequate due diligence. A more common example is buying accounts the seller does not own. This may be due to a cluster situation, a brokerage situation where the agency is writing business for other agencies, or the producers own all or part of their books. Sure, the buyer is only paying for what renews, but even if 100% renews, the buyer has paid a lot of money for accounts it does not really own. These may seem like ridiculous examples, but they are real. Retention-based clauses do not replace good due diligence.

Let's consider some other situations. Let's say the buyer man-ages to not make any down payment and the entire deal is 100% retention based. The buyer moves the staff, the data, the files, the entire office to their location, or at the very least converts the seller's data to their system, adds the employees to their payrolls, and so forth. Then the producers walk away with most of the business because they don't have non-compete agreements. How much did the buyer spend and what did they get in return? I have seen producers walk away with millions in commissions. This is not far-fetched. Acquisitions cost a lot of money even if the actual book is free.

Even if the producers have non-

competes and abide by them for two years, rarely, if ever will an acquisition generate an adequate return on investment in two or three years. Most often, the minimum payback period is five years, regardless of whether a retention clause exists. A retention-based deal does not shorten the investment horizon. Additionally, unless the seller is a bad negotiator, they are not going to agree to a retention clause lasting five years without the buyer paying them a big premium for the extra insurance. Most often the retention clause is three years or less. So if the business rolls off the books in years four and five rather than year one, the retention clause has made no difference.

A retention clause also does not eliminate operational risk. I have lost count of the carriers and agencies that did retention-based acquisitions without good due diligence whose opera-tions still have not adequately merged five years later. Good due diligence would have alerted the buyers to develop a proper merger execution plan. Instead, the buyers lose a mini-mum of 10% - 20% of productivity for the next five years. The productivity loss does not just apply to the acquired book, but the buyer's book too. How profitable is the acquisition now? Sure, the retention clause offered some protection, but did it make the deal profitable?

Buyers that rely solely on a retention clause to remove risk have a tendency to pay higher prices--usually at least 20% more than for a fixed price deal. The problem is the price should never be based on risk alone. The price should be based on a combination of three factors: Future profits, future growth, and the risk that something will go wrong. Higher pric-es are only justified if future profits and future growth are also higher, all else being equal. When future profits and growth are ignored, retention-based deals will often fail to return an adequate return on investment because only one part of price is being addressed.

I have found that if the buyer conducts detailed and thorough due diligence and acquisition analysis, most of the risk can be identified allowing the buyer to not pay the premium and not incur any extra risk. It is the best of both worlds. I am not sug-gesting retention clauses should be eliminated. I am stating that retention-based clauses should

A retention clause is all you need, right?

The problem is the price should never be based on risk alone.

by Chris Burand

Page 20 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 21

never replace good due diligence.

Another dangerous mistake is to ignore the balance sheet in an acquisition. This potentially fatal mistake can happen with any kind of deal, but it seems more common with heavily focused retention-based deals. When doing an acquisition, the buyer should not just be getting the book of business. They should also be getting cash adequate to cover the trust ratio and to provide thirty days of working capital. If a buyer makes a large enough acquisition or serial acquisitions without obtain-ing adequate working capital, their agency will ultimately fail unless it can find substantial cash somewhere else.

The problem is twofold. First, the market value of agencies anticipates working capital will come with the deal. So if it does not, the buyer has likely significantly overpaid. Second, bills al-ways come first and revenues follow. When buying an agency, even on a retention basis, the bills still arrive earlier than the revenue. If one adds enough business fast enough, the bills will far outpace the revenues and the payroll will be tough to meet. This mistake has caused more than one agency owner

Retention-based clauses should never replace good due diligence.

to lie awake at night wondering how they will make the payroll.

Acquisitions done right are about oppor-tunity. Excess reliance on a retention clause is about defense, protecting oneself against loss rather than focusing on making the most of an opportunity. In every single instance when I've had an opportunity to look at a buyers' financials after they've done deals based solely on retention without adequate due diligence, their return on investment was miserable. Of course, most could claim they had not lost a ton of money because the retention clause had saved them. But that is not the point. They could have made a lot of money if they had done adequate due diligence and thoroughly analyzed the acquisition.

ww

w.c

olon

ialg

ener

al.c

om

Founded in 1985, Colonial General Insurance Agency, Inc. is a wholesale General Agency providing quality insurance products to the Independent Insurance Agent.

Colonial General specializes in both standard and non-standard business. Our Property and Casualty business includes:

♦ Commercial Auto

♦ Commercial Contract

♦ Personal Lines

♦ Professional Liability

With 2,500 active producers under contract, Colonial General operates in eight states throughout the South-West. Our offices are located in Murray, Utah and Scottsdale, Arizona.

Most of all, we pride ourselves in our friendly customer service and our ability to help our producing agents with their many insurance needs.

♦ Preferred BOP ♦ Property ♦ Inland Marine ♦ Professional Liability ♦ Commercial Liability ♦ Workers Compensation

♦ Truckers ♦ Physical Damage ♦ NB Mexican Truckers ♦ Local Radius ♦ Garage ♦ Intermediate Radius

♦ Masterpiece Company ♦ Standard Company ♦ Umbrellas ♦ Stand-alone Liability ♦ Vacant ♦ Seasonal ♦ Dwelling Fire ♦ Homeowners

Commercial Lines/Brokerage Department

Transportation Department

Personal Lines Department

Preferred Commercial Lines Division

Avoid monthly or annual membership fees, use Colonial General for your Preferred Business Owners Policies. We have several markets available to give you the best quote possible. For additional information contact your underwriter.

Please contact our Utah office for all your Transportation needs!

P.O. Box 571770, Murray, Utah 84157 Phone: (801) 562-1188 Wats: (800) 594-8900

Fax: (801) 562-2218 Toll Free Fax: (800) 332-9285

You will never pay a fee to access our companies. No volume or binding contracts.

P.O. Box 14770 Scottsdale, AZ 85267 8475 E. Hartford Drive, Suite #100 Scottsdale, AZ 85255

Phone: (480) 991-7889 Wats: (800) 848-8860 Fax: (480) 948-1394 www.colonialgeneral.com

Colonial General Insurance Agency Colonial General Insurance Agency

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 23

Founded in 1985, Colonial General Insurance Agency, Inc. is a wholesale General Agency providing quality insurance products to the Independent Insurance Agent.

Colonial General specializes in both standard and non-standard business. Our Property and Casualty business includes:

♦ Commercial Auto

♦ Commercial Contract

♦ Personal Lines

♦ Professional Liability

With 2,500 active producers under contract, Colonial General operates in eight states throughout the South-West. Our offices are located in Murray, Utah and Scottsdale, Arizona.

Most of all, we pride ourselves in our friendly customer service and our ability to help our producing agents with their many insurance needs.

♦ Preferred BOP ♦ Property ♦ Inland Marine ♦ Professional Liability ♦ Commercial Liability ♦ Workers Compensation

♦ Truckers ♦ Physical Damage ♦ NB Mexican Truckers ♦ Local Radius ♦ Garage ♦ Intermediate Radius

♦ Masterpiece Company ♦ Standard Company ♦ Umbrellas ♦ Stand-alone Liability ♦ Vacant ♦ Seasonal ♦ Dwelling Fire ♦ Homeowners

Commercial Lines/Brokerage Department

Transportation Department

Personal Lines Department

Preferred Commercial Lines Division

Avoid monthly or annual membership fees, use Colonial General for your Preferred Business Owners Policies. We have several markets available to give you the best quote possible. For additional information contact your underwriter.

Please contact our Utah office for all your Transportation needs!

P.O. Box 571770, Murray, Utah 84157 Phone: (801) 562-1188 Wats: (800) 594-8900

Fax: (801) 562-2218 Toll Free Fax: (800) 332-9285

You will never pay a fee to access our companies. No volume or binding contracts.

P.O. Box 14770 Scottsdale, AZ 85267 8475 E. Hartford Drive, Suite #100 Scottsdale, AZ 85255

Phone: (480) 991-7889 Wats: (800) 848-8860 Fax: (480) 948-1394 www.colonialgeneral.com

Colonial General Insurance Agency Colonial General Insurance Agency

F ewer people are shopping for auto insurance, according to a recent study by J.D. Power & Associates, and customers

who are shopping are not basing their decisions exclusively on price, as might be expected in a difficult economy.

Instead, J.D. Power & Associates’ 2009 Auto Insurance Shop-ping Study reveals that while price does play a significant role in customers’ purchasing decisions, 10% of customers did not ultimately choose the carrier offering the lowest quote.

Erie Insurance is leading the pack in new buyer satisfaction with auto insureds, according to J.D. Power, which based its rankings on three factors: the distribution channel, price and policy offerings. Interestingly, the top performers in the study were divided among the primary sales channels of indepen-dent agents, captive agents, Web sales and call centers. American Family Insurance, which sells through captive agents, The Hartford, which is known for its call center model and Web sales giant GEICO ranked third, fourth and fifth in new customer satisfaction, respectively.

While the variation among distribution channels in the study shows that customers shop for auto insurance in a variety of ways, Jeremy Bowler, director of insurance practice at J.D. Power & Associates, says the fact that not all customers are shopping based exclusively on price indicates that customer service and the agent’s role as a trusted advisor are still impor-tant to shoppers.

“The importance of price has not swamped everything else out,” says Bowler. “Nine out of 10 decisions are still based on price, but if they really like their agent and are close on price, one in 10 customers will pass up the lowest bid for the whole package that they prefer.”

Darlene McGehee, an agent at Iroquois Insurance in Watseka, Ill., says her clients rarely feel the need to shop because she does it for them. “We will usually shop for people proactively because no one likes to feel as if they need to come in and complain to get results,” says McGehee. “It’s not always based on price, because maybe another company or product is bet-ter. But, if I know someone will be concerned (about price), I will call them proactively before they get the policy on renewal. We have gotten good results with that because customers know we’re looking out for them.”

While the study revealed that 90% of U.S. auto insurance customers are retained by their provider and 8% fewer are shopping compared to last year, Bowler says more than 55% of companies do not make dedicated attempts to retain cus-tomers when they do shop elsewhere. Bowler adds that when it comes to a last-ditch effort to keep a customer, price does usually play a major role.

“(Trying) to explain the benefits of remaining with (the com-pany) had a modest impact on customers, as did discussing their current coverage and options. What had the most impact was when a carrier offered discounts and could come up with the price the customer wanted.”

Brewa Kennedy, director of marketing and operations at Today’s Insurance Solutions in Orlando, Fla., says his agency never negotiates on price because they prefer to retain cus-tomers who will be with them long-term.

“We take an education approach to our business so that we are able to ‘graduate’ lower-tiered clients into better programs,” says Kennedy. “Gradually increasing limits, in our experience, has helped many of our insureds to realize greater cost sav-ings, and better coverage, over the long run.”

Bowler says he has seen agents working harder than ever to retain their books of business in an increasingly competitive environment

“Everything is expensive,” says Bowler. “(Agents are) lowering premium to retain business, which results in fewer commission dollars. If they’re not working to right-size the policy, the cus-tomer is at risk. (But), agents are being shrewd and are looking down the road by making sure they can keep customers (and) continue to harvest the benefits of tenured customers in future years.”

Fewer Customers Shopping for Auto InsuranceDespite difficult economy, customers’ decisions are based on more than price.

by Veronica DeVore

Page 24 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

Page 24 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

9 Steps to Better DelegatingBe sure you’ve defined the task and why it’s important.

Thoroughly explain what the task will involve and be clear about how the job fits into the overall goal of what you’re trying to accomplish. Don’t assume someone knows what you want and why you’re asking for it. The clearer the goal, the more invested the individual will be.

Understand the strengths & weaknesses of the individuals you are delegating to & assign work accordingly.

Too difficult an assignment will undermine confidence and assigning work that is substantially beneath some-one’s skill level is a surefire way to turn him or her off to the assignment.

Take responsibility for your part in the progression of the assignment.

Depending on the scope of the task and the ability level of the of the individual it’s been assigned to, you will need to make yourself available as an authority, a resource, a peer or a mentor.

Clearly define the expected results.

Discuss what successful completion of the project means to you. Elicit feedback from the other person to ensure he or she is clear about the goal and your expectations. Also be sure you provide any additional resources necessary for the individual to complete the assignment successfully.

Establish and agree on deadlines

Specify the date the assignment needs to be finished. Determine if your expec-tations are realistic based on the individual’s other responsibilities and the avail-ability of any additional resources necessary to complete the job. You may need to work together on establishing priorities. Everything can’t be due at the same time and all tasks cannot be top priority. Encourage open discussions about how to manage multiple projects.

Put a system in place for tracking progress

Know what you’ve delegated, who is responsible and when each project is due. Keep a mas-ter project list that includes priorities, review dates and expected completion dates. This way you can be sure the project is progressing without feeling the need to micro-manage it.

Don’t “take over.”

When things aren’t progressing exactly your way, don’t jump to the conclusion that the method is wrong. If you’re concerned ask to hear the whole plan and determine if the approach will ultimately lead to the desired results. With an open mind, you may actually discover ideas and options to help you with future projects. If the plan does seem doomed to fail, explain why and work together to come up with an appropriate alternative.

Give feedback and recognition.

Discuss any concerns you have about how the assignment was handled so future problems can be avoided. Explore the thought-process behind how the person approached the job and agree on what to do differently next time. If you are pleased with the outcome, or even with certain stages of the project, say so. Point any specific aspects of the assignment that you were particularly impressed with. Give credit for successes. A little praise goes a long way.

1

2

3Use delegation as a way to develop employees.

Employees who are given new opportunities to grow and develop their abilities, tend to be happier and more productive than those who are not challenged. And you gain a more capable individual who can take on more difficult jobs in the future.

4

5

6

7

8

9

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 25

Name:

Organization:

Address:

City, State & Zip:

Phone: Fax:

E-mail:

Please see other side for class descriptions

Wednesday, September 2nd

Thursday, September 3rd

AM

PM

ethics

AM

PM

ethics

For more information, please contact Jeff Straight at (505) 999-5802 or (800) 621-3978 or [email protected].

Fax Registration To:(505) 243-3367

Registration Form

Class Choices

Location Information

Hilton Albuquerque1901 University Blvd. NEAlbuquerque, NM 87107

(505) 884-2500 / 800-374-6835

Reservations may be made at the rate of $100 per night until August 30th, 2009. Please be sure to state you are with the

Independent Insurance Agents of New Mexico to receive this special rate.

Ethics Only(1 Hour of CE)

$45 (Regular Cost) $35 (Member Cost)

Mail Registration to:

IIANM1511 University Blvd. NEAlbuquerque, NM 87102

(800) 621-3978

Prices

One Half DayOne half day of instruction

(4 Hours of CE for AM class or 3 Hours of CE + Ethics for PM class)

$75 (Regular Cost) $65 (Member Cost)

Entire SeminarTwo full days of instruction + Ethics (15 Hours of CE)

$240 (Regular Cost) $195 (Member Cost)

One Full DayOne full day of instruction + Ethics (8 Hours of CE)

$140 (Regular Cost) $100 (Member Cost)

Bill Agency (Members Only)

Check made payable to IIANM

Charge my card:

Number:

Exp. Date:

Signature:

Method of Payment

Your Time is Running Out! September 2nd & 3rd, 2009

15 Hours of Continuing Education for the Insurance Professional IIANM’s 20th Annual Last Chance SeminarFrom the Wild, Wild West to the Best of the Best

Celebrating 75 Years of Independents in New Mexico

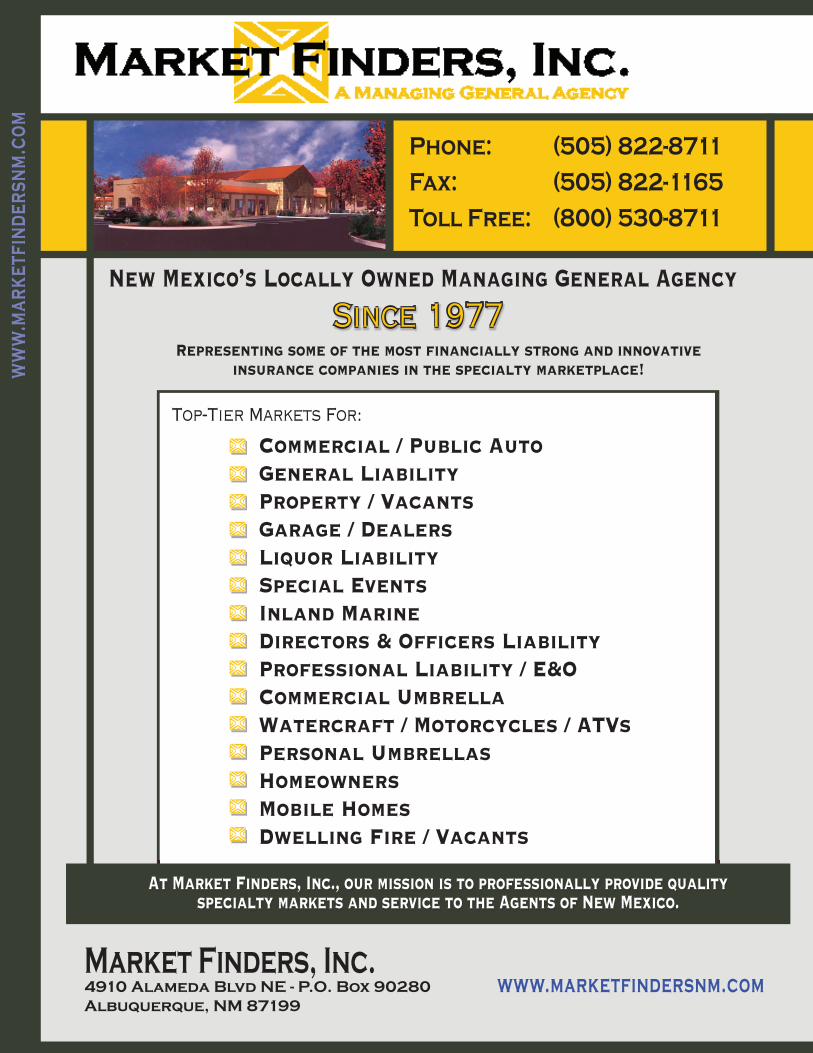

Class Details:Wednesday, September 2nd : Thursday, September 3rd :

“Commercial Crime in the 21st Century”

Dan Myers with Professional Insurance Educators of Indiana

8 to 12 noon / 4 CE hrs

ISO has totally restructured the Crime Program. This seminar will cover all details of the New Crime Program. This will be an excellent opportunity to learn the new program because every class code, form, endorsement, rule, and rating procedure is new.

“Inland Marine Coverages”

Dan Myers with Professional Insurance Educators of Indiana1 to 4 / 3 CE hrs

This seminar will take a look at the development of Inland Marine coverages and its purpose and uses. The discussion will include Builder’s Risk, Installation Float-ers, Contractor’s Equipment, and Surface Carriers.

“Group Health Insurance”

Carole Henry with Lovelace Health Plans8 to 12 noon / 4 CE hrs

The purpose of this class is to take an in depth look at Group Health Insurance including the basic concepts. The discussion will include the features and benefits of the various Health plans and how they are underwritten and priced. Additionally, it will investigate the impact of New Mexico regulations have on pricing and underwrit-ing for small employer groups. The case studies will look at underwriting submissions and common mistakes which are made.

“Health Care Legislation and NM”

Anne Sperling, CSA, LPRT with Daniels Insurance, Inc.1 to 4pm / 3 CE hrs

Anne will be discussing the 2009 Legislative requests made by the Legislative Health and Human Services Subcommittee. She will discuss the comprehensive health care reform strategy. Anne will also be discussing how the requests turned into statute and how the state will move forward based on the legislative outcome. She will also weave the national health care discussion into the NM discussion.

“A Renewed Look at the CGL”

Jack Cleary, CPCU, ARM with Cleary & Associates8 to 12 noon / 4 CE hrs

Has it been a while since you took a close look at the CGL? Perhaps it is time to dig into it again. Jack will discuss the basics plus cover some of the “finer” points of the CGL. Come and spend some time with our old friend – CGL.

“Certficates of Insurance & Additional Insureds”

Jack Cleary, CPCU, ARM with Cleary & Associates1 to 4 / 3 CE hrs

This class will discuss types of insureds such as Named Insured, Additional and Miscellaneous Insureds under the CGL, Commercial Auto, Umbrella, and Workers Com-pensation policies. Other topics include: Intercompany Products Suits, Separation of Insureds, Subrogation among Insureds, Cross Liability, Additional Insured En-dorsements, Application of Exclusions to Insureds, Forms of Business Organizations, Ownership and Insurance Problems, and Discontinued Operations Problems.

“COBRA Updates”

Sue Bisbee with Infinisource 8 to 12 noon / 4 CE hrs

Sue will bring us to date on COBRA. The penalties and Enforcement, TAMARA, Who Must Comply, Qualified Beneficiaries, Qualifying Events, COBRA Extensions, COBRA Coverage, COBRA Notifications, Election and Time Frames, Terminating Events, COBRA Premiums and lots more.

“The Impact of Wellness Programs on Premium Rates”

Jim Campbell with Wellness Improvement Experts1 to 4pm / 3 CE hrs

The objectives of this class are to educate the mem-bers regarding resources and their use to maintain and expand their client base in the face of continually increas-ing health insurance premium rate increases. Drivers of those increases that are within the control of clients will be identified. The class will provide members with information to communicate proven ways for clients to mitigate future rate increases by addressing those drivers to maintain or expand current client coverages. Specifi-cally, attendees will learn how to create added value for their clients by reducing needs for employee health care utilization. Attendees will learn the critical components of effective wellness programs for client’s employees that will produce high returns on investment to offset signifi-cant portions of future health insurance rate increases for clients. The result will be greater client good will, loyalty and retention.

Ethics

4:00 – 5:00 pm / Both Days, September 2nd & 3rd

We would like to invite everyone in the Association to celebrate our collective success in this endeavor, so throughout 2009, we will be announcing a number of fun and informative initiatives to

commemorate this milestone year.Every month La Voz will feature a trivia question where the answers can be located on

our web site and Membership Directory.

This month's trivia question is:

"In What Year Did the Association Change It’s Name to ‘Independent Insurance Agents of NM’ (IIANM)?"

Email your answers to [email protected] by August 17, 2009. On August 18, there will be a drawing for the winner

from the correct entries.

Look out for next month issue of La Voz for your next chance to win!

From the Wild, Wild West to the Best of the Best!IIANM Celebrates our

75th Anniversary in 2009!

Last month's WINNER!!Andrea Cordova HUB International Insurance, Albuquerque, NM

HINT: If you do not have access to a hard copy of our Membership Directory, you can find it online on our site. Look for “Member Resources”, then “Member Directory”.

Page 28 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

Win an iPod Shuffle!!

Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 29

Full Name:

First Name for Badge:

Agency / Company:

Address:

City, State, Zip:

Telephone:

Fax:

The pre-licensing classes are designed to be a review for the state licensing examination. We recommend that students be familiar with the study material prior to attending class.

Study materials are NOT included in class prices.

Pre-Licensing Classes

E-Mail:

Method of Payment:

Bill Agency (Members Only)

Check Enclosed (Payable to IIANM)

M/C Visa Disc Amex

Amount: (all prices include tax)

Card No:

Exp. Date:

Signature:

( )

Send in your registration:

Fax in:(505) 243-3367

Mail in:1511 University Blvd. NEAlbuquerque, NM 87102

Give us a call:(505) 843-7231 (800) 621-3978

Go on-line:www.iianm.org or E-mail:

The FINE PRINT: IIANM reserves the right to cancel/reschedule classes. Please call ahead to verify when classes will run. Decisions will be made three days prior to class. Cancellations received after 5 business days, will be assessed a $50.00 cancellation fee. Cancellations received on or after deadline and ‘no shows‘ will forfeit the registration fee altogether. A substitute is always welcome, with no extra fee, but prior notification would be appreciated.

Class Name/Date:

( )

Instructor: Kitty Leslie - August 11 - 12 8am - 5pm Instructor: Jack Cleary - September 15 - 16 8am - 5pm

Property & Casualty Review Class (2 days)

Regular Price: $150 Member Price: $120

Click here for a full listing of our education program.

Life & Health Review Class (1 day)

Regular Price: $115 Member Price: $90

Instructor: Bob Ouellette - August 13 8am - 5pm Instructor: Manny Mansour - September 17 8am - 5pm

Insurance Education Programs in New Mexico are critical to a successful and profitable career in the insurance industry. Every year, we offer exciting opportunities to expand your professional horizons. All of these education programs are designed to help insurance agents thrive in the most competitive of marketplaces.

EducationEDGEIIANM’s

Pre-Licensing Study MaterialsTo see a list of what is available and to purchase your study materials online, click here.

Page 28 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009

Page 30 Independent Insurance Agents of New Mexico - www.iianm.org - * August 200

Cla

ssifieds

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

3 8

9 10 12 13 14 15

16 17 18 19 20 21 2223

P&CPre-licensing

Class

P&CPre-licensing

Class

L&HPre-licensing

Class

Looking to fill a position within your agency? Trying to find a job but don’t know where to look?

Whether you are looking for somewhere new to share your special skills or an employer looking for quality, professional employees, we are there to lend a helping hand.

The staff at IIANM knows that “Teamwork Makes Us Stronger” and we want to help all interested individuals find that perfect fit.

Click here to take advantage of IIANM’s Job Bank.

Where Will You Find Your Next Great Hire?

- Click on a class to register online - CE ‘ continuing education hours

6 7

1

2

24

27 2825 26 2930

August's Clickable Calendar

AAI 83/CAgnecy

FinancialManagement

8 CE

31

CL Update(ACSR Update)

8 CE

Comm Property(ACSR #6)

8 CE

ROSWELL

CL Related Coverages(ACSR #9)

8 CEComm Liability

(ACSR #7)8 CE

ROSWELL

Life Insurance(ACSR #10)

8 CE

ROSWELL

Odds n E

nds

Page 30 Independent Insurance Agents of New Mexico - www.iianm.org - * August 200 Independent Insurance Agents of New Mexico - www.iianm.org - * August 2009 Page 31 Page 33

The Blue Hope45.52 Carats, the ironically named Hope diamond (named for its purchaser, Henry Thomas Hope) may have had a long and illustrious history before it became associated with a run of bad luck for its owners. The Blue was purchased by King Louis XIV who had it cut to 67.50 carats from 112 carats to bring out its bril-liance. The diamond was stolen during the French Revolution, and a smaller diamond of similar color was sold in 1830 to Hope, an English banker. After inheriting the diamond, Hope's son lost his fortune. It was eventually acquired by an American widow, Mrs. Edward McLean, whose family then suffered a series of catastrophes: her only child was accidentally killed, the family broke up, Mrs. McLean lost her money, and then committed suicide. When Harry Winston, the New York diamond merchant, bought the stone in 1949, many clients refused to touch the stone. It is now on display at the Smithosonian Institute in Washington.

the 18th century: trade, slave labour cotton plantations increased, workers wore jean cloth because the material was very strong and it did not wear out easily.--the 19th century: the california gold rushthe gold miners wanted clothes that were strong and did not tear easily. in 1853, leob strauss started a wholesale busi-ness, supplying clothes. strauss later changed his name from leob to levi.--the 1930's: westernscowboys - who often wore jeans in the movies-became very popular.--the 1940's: warfewer jeans were made during the time of world war 2, but they were introduced to the world by american soldiers, who sometimes wore them when they were off duty. after the war, rival companies, like wrangler and lee, began to compete with levi for a share of the international market.--the 1950's: rebelsìn the 1950's, denim became popular with young people. it was the symbol of the teenage rebel in TV shows and movies (james dean in the 1955 movie rebel without a cause). some schools in the USA banned students from wearing denim.--the 1960-70's: hippies & the cold wardifferent styles of jeans were made, to match the 60's fash-ions: embroidered jeans, painted jeans, psychedelic jeans...in many non-western countries, jeans became a symbol of'western decadence' and were very hard to get.--the 1980's: designer jeansin the 1980's jeans became high fashion clothing, when fa-mous designers started making their own styles of jeans, with their own labels on them. sales of jeans went up and up.--the 1990's: recessionin these years the youth market wasn't particularly interested in 501s and other traditional jeans styles, mainly because their parents: the' generation born in blue' were still busy