Embed Size (px)

Citation preview

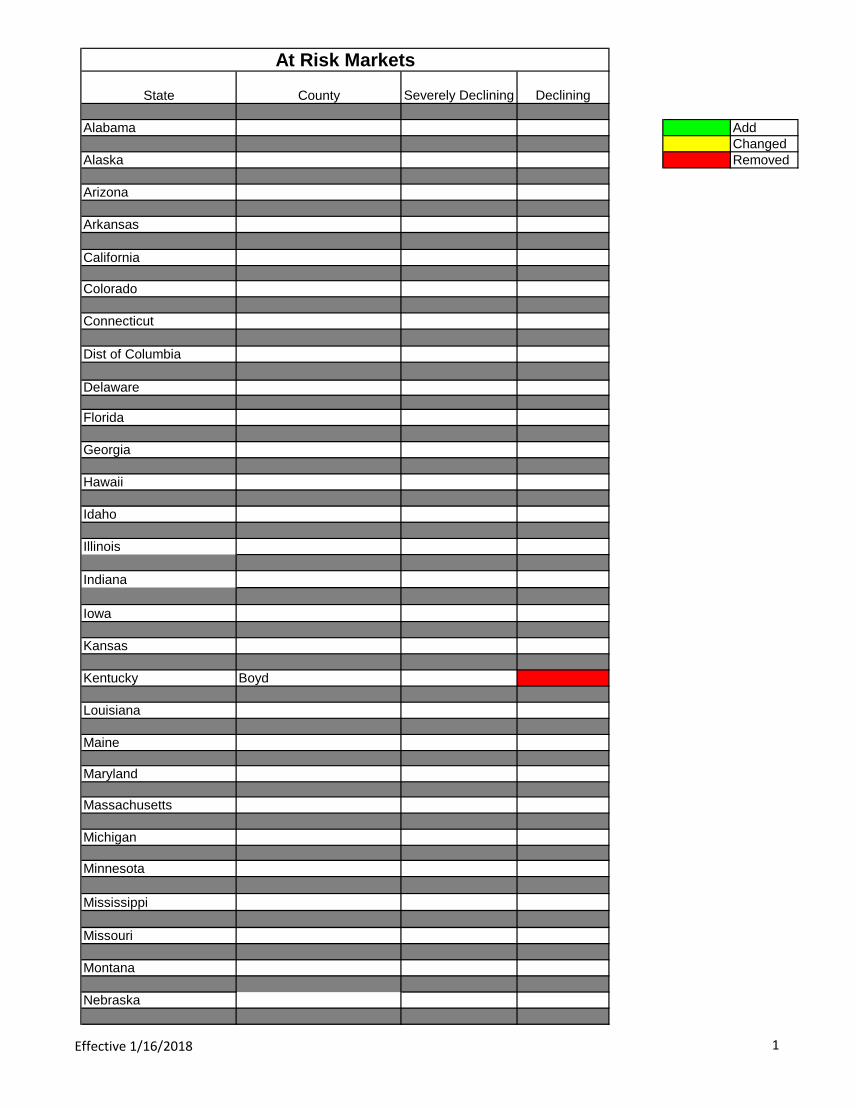

Effective 1/16/2018 1

State County Severely Declining Declining

Alabama AddChanged

Alaska Removed

Arizona

Arkansas

California

Colorado

Connecticut

Dist of Columbia

Delaware

Florida

Georgia

Hawaii

Idaho

Illinois

Indiana

Iowa

Kansas

Kentucky Boyd

Louisiana

Maine

Maryland

Massachusetts

Michigan

Minnesota

Mississippi

Missouri

Montana

Nebraska

At Risk Markets

Effective 1/16/2018 2

State County Severely Declining Declining

At Risk Markets

Nevada

New Hampshire

New Jersey

New Mexico

New York

North Carolina

North Dakota

Ohio

Oklahoma

Oregon

Pennsylvania

Rhode Island

South Carolina

South Dakota

Tennessee

Texas

Utah

Vermont

Virginia

Washington

West Virginia

Wisconsin

Wyoming

BB&T Internal The information in this document is the property of BB&T and is intended for the use of

BB&T associates and authorized representatives. 4/30/2018

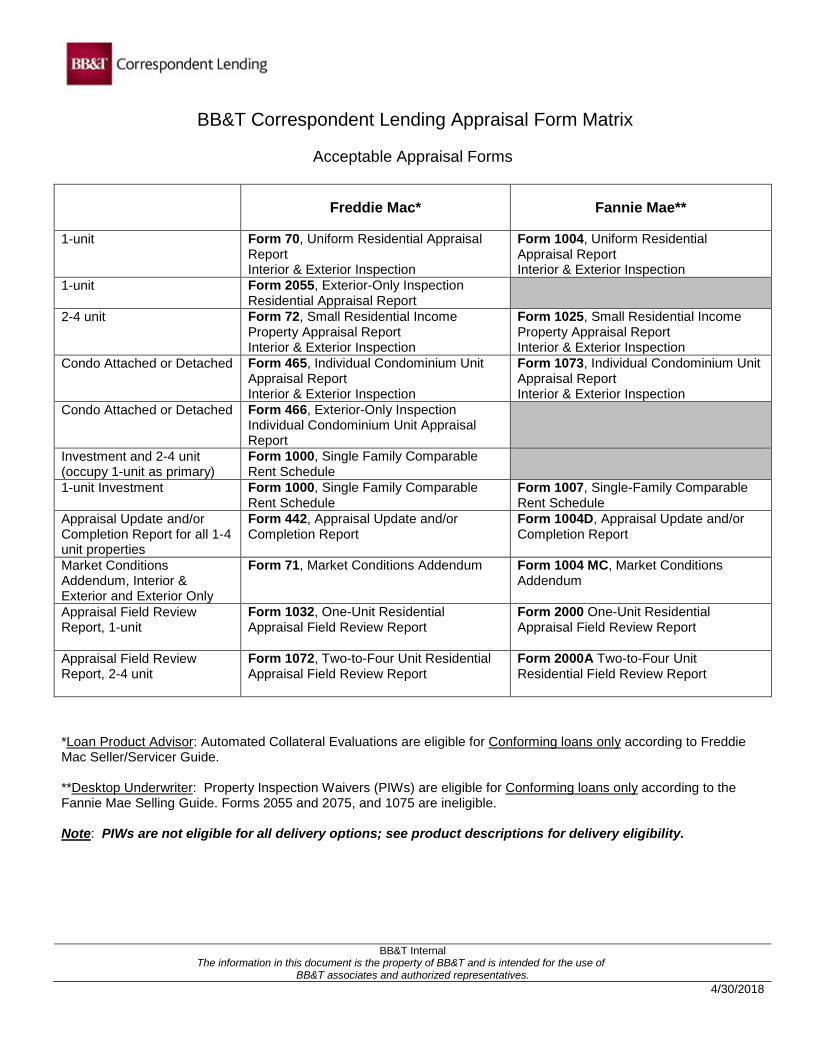

BB&T Correspondent Lending Appraisal Form Matrix

Acceptable Appraisal Forms

Freddie Mac*

Fannie Mae**

1-unit Form 70, Uniform Residential Appraisal Report Interior & Exterior Inspection

Form 1004, Uniform Residential Appraisal Report Interior & Exterior Inspection

1-unit Form 2055, Exterior-Only Inspection Residential Appraisal Report

2-4 unit Form 72, Small Residential Income Property Appraisal Report Interior & Exterior Inspection

Form 1025, Small Residential Income Property Appraisal Report Interior & Exterior Inspection

Condo Attached or Detached Form 465, Individual Condominium Unit Appraisal Report Interior & Exterior Inspection

Form 1073, Individual Condominium Unit Appraisal Report Interior & Exterior Inspection

Condo Attached or Detached Form 466, Exterior-Only Inspection Individual Condominium Unit Appraisal Report

Investment and 2-4 unit (occupy 1-unit as primary)

Form 1000, Single Family Comparable Rent Schedule

1-unit Investment Form 1000, Single Family Comparable Rent Schedule

Form 1007, Single-Family Comparable Rent Schedule

Appraisal Update and/or Completion Report for all 1-4 unit properties

Form 442, Appraisal Update and/or Completion Report

Form 1004D, Appraisal Update and/or Completion Report

Market Conditions Addendum, Interior & Exterior and Exterior Only

Form 71, Market Conditions Addendum Form 1004 MC, Market Conditions Addendum

Appraisal Field Review Report, 1-unit

Form 1032, One-Unit Residential Appraisal Field Review Report

Form 2000 One-Unit Residential Appraisal Field Review Report

Appraisal Field Review Report, 2-4 unit

Form 1072, Two-to-Four Unit Residential Appraisal Field Review Report

Form 2000A Two-to-Four Unit Residential Field Review Report

*Loan Product Advisor: Automated Collateral Evaluations are eligible for Conforming loans only according to Freddie Mac Seller/Servicer Guide. **Desktop Underwriter: Property Inspection Waivers (PIWs) are eligible for Conforming loans only according to the Fannie Mae Selling Guide. Forms 2055 and 2075, and 1075 are ineligible. Note: PIWs are not eligible for all delivery options; see product descriptions for delivery eligibility.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

Any disclosure, copying, distribution, or use by others of the information contained herein is strictly prohibited. 2-06-18

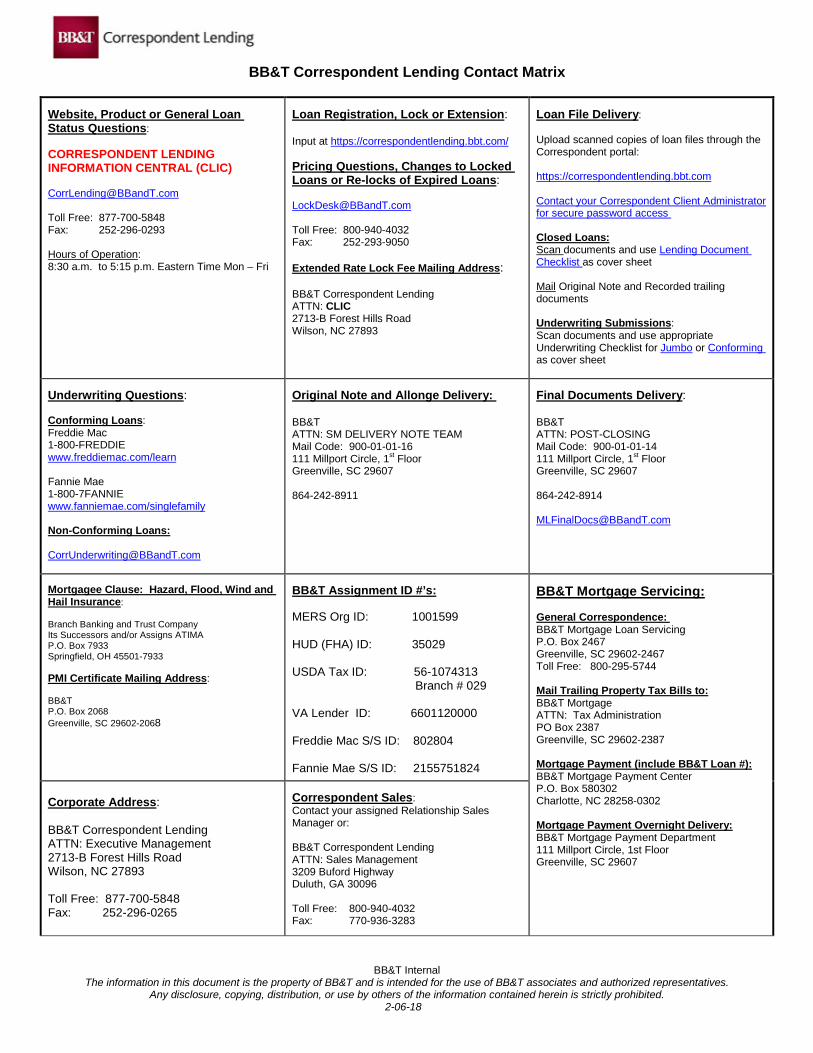

BB&T Correspondent Lending Contact Matrix

Website, Product or General Loan Status Questions: CORRESPONDENT LENDING INFORMATION CENTRAL (CLIC) [email protected] Toll Free: 877-700-5848 Fax: 252-296-0293 Hours of Operation: 8:30 a.m. to 5:15 p.m. Eastern Time Mon – Fri

Loan Registration, Lock or Extension: Input at https://correspondentlending.bbt.com/ Pricing Questions, Changes to Locked Loans or Re-locks of Expired Loans: [email protected] Toll Free: 800-940-4032 Fax: 252-293-9050 Extended Rate Lock Fee Mailing Address: BB&T Correspondent Lending ATTN: CLIC 2713-B Forest Hills Road Wilson, NC 27893

Loan File Delivery: Upload scanned copies of loan files through the Correspondent portal: https://correspondentlending.bbt.com Contact your Correspondent Client Administrator for secure password access Closed Loans: Scan documents and use Lending Document Checklist as cover sheet Mail Original Note and Recorded trailing documents Underwriting Submissions: Scan documents and use appropriate Underwriting Checklist for Jumbo or Conforming as cover sheet

Underwriting Questions: Conforming Loans: Freddie Mac 1-800-FREDDIE www.freddiemac.com/learn Fannie Mae 1-800-7FANNIE www.fanniemae.com/singlefamily Non-Conforming Loans: [email protected]

Original Note and Allonge Delivery: BB&T ATTN: SM DELIVERY NOTE TEAM Mail Code: 900-01-01-16 111 Millport Circle, 1st Floor Greenville, SC 29607 864-242-8911

Final Documents Delivery: BB&T ATTN: POST-CLOSING Mail Code: 900-01-01-14 111 Millport Circle, 1st Floor Greenville, SC 29607 864-242-8914 [email protected]

Mortgagee Clause: Hazard, Flood, Wind and Hail Insurance: Branch Banking and Trust Company Its Successors and/or Assigns ATIMA P.O. Box 7933 Springfield, OH 45501-7933 PMI Certificate Mailing Address: BB&T P.O. Box 2068 Greenville, SC 29602-2068

BB&T Assignment ID #’s: MERS Org ID: 1001599 HUD (FHA) ID: 35029 USDA Tax ID: 56-1074313 Branch # 029 VA Lender ID: 6601120000 Freddie Mac S/S ID: 802804 Fannie Mae S/S ID: 2155751824

BB&T Mortgage Servicing: General Correspondence: BB&T Mortgage Loan Servicing P.O. Box 2467 Greenville, SC 29602-2467 Toll Free: 800-295-5744 Mail Trailing Property Tax Bills to: BB&T Mortgage ATTN: Tax Administration PO Box 2387 Greenville, SC 29602-2387 Mortgage Payment (include BB&T Loan #): BB&T Mortgage Payment Center P.O. Box 580302 Charlotte, NC 28258-0302 Mortgage Payment Overnight Delivery: BB&T Mortgage Payment Department 111 Millport Circle, 1st Floor Greenville, SC 29607

Corporate Address: BB&T Correspondent Lending ATTN: Executive Management 2713-B Forest Hills Road Wilson, NC 27893 Toll Free: 877-700-5848 Fax: 252-296-0265

Correspondent Sales: Contact your assigned Relationship Sales Manager or: BB&T Correspondent Lending ATTN: Sales Management 3209 Buford Highway Duluth, GA 30096 Toll Free: 800-940-4032 Fax: 770-936-3283

DECLINING MARKET POLICY DECLINING MARKET POLICY Overview Conditions in the real estate industry have resulted in declining values in many markets. BB&T is implementing the following policy in order to mitigate some of the collateral risk associated with declining markets. A list of declining/at risk markets will be updated periodically and posted on the BB&T Correspondent Lending website. BB&T has identified two market conditions which are defined below: Declining markets are experiencing depreciation of value which is expected to continue trending downward. Severely Declining markets are experiencing significant depreciation of value which is expected to continue into the future. If the property is located in an area that is on the BB&T Declining/At Risk list or the appraiser indicates on the appraisal report that the property is located in a declining market, the property may not be eligible for maximum financing. The loan to value ratio for properties designated as being in a declining/at risk market must be reduced as indicated below. Conforming Loan Products (includes Fixed Rate and ARMs) Super Conforming Loan Products (includes Fixed Rate and 5/1 ARMs) • Eligible loan products must be underwritten in accordance with Freddie Mac and Fannie Mae

guidelines. Loans underwritten to satisfy these guidelines will not require a reduction in the LTV/TLTV.

• Correspondents are responsible for obtaining required mortgage insurance on all loans sold

to BB&T which require mortgage insurance and for being knowledgeable of guideline changes and restrictions implemented by the mortgage insurance companies.

Non-Conforming Loans (includes Fixed Rate and ARMs) • Property located in a Declining market requires a 5% LTV/TLTV reduction from maximum allowed

financing for the property and transaction type. The LTV/TLTV may not exceed 80%. For example, if the maximum LTV for the application is 80% LTV and 80% TLTV, the maximum allowed in a Declining market is 75% LTV and 75% TLTV. If the maximum LTV for the application is 70% LTV and 70% TLTV, the maximum allowed in a Declining market is 65% LTV and 65% TLTV.

• Property located in a Severely Declining market requires a 10% LTV/TLTV reduction from maximum

allowed financing for the property and transaction type. The LTV/TLTV may not exceed 75%. For example, if the maximum LTV for the application is 80% LTV and 80% TLTV, the maximum allowed in a Severely Declining market is 70% LTV and 70% TLTV. If the maximum LTV/TLTV for the application is 70% LTV and 70% TLTV, the maximum allowed in a Severely Declining market is 60% LTV and 60% TLTV.

• If property is not on the list and the appraiser indicates a declining market, the LTV/TLTV must be

reduced by 5%. The LTV/TLTV may not exceed 80%. • If the appraiser indicates that the Marketing Time is “over 6 months” on a non-conforming appraisal,

Management in its discretion will consider acceptable loan risk tolerance. This may result in a reduction in allowable loan amount for LTV maximums.

Page 1 7/18/2016

DECLINING MARKET POLICY Construction Conversion and Renovation Mortgages – Non-Conforming If the property is not on the BB&T Correspondent Lending At Risk Markets list and the appraiser indicates declining property values, the market condition will be considered declining. Refer to the LTV Charts for Non-Conforming, Declining and Severely Declining market requirements. Exceptions to this policy will be entertained if the appraisal supports that values and marketability are stable. The requirements listed below in the Exceptions Policy section must be met.

Exceptions Policy Exceptions to this policy will be entertained if the appraisal supports that values and marketability are stable. All of the following must be provided. • The application is not for a Non-Conforming loan that involves a cash-out refinance or condo. • The appraiser provides days on the market for each comparable sale, including expired listings of

the property and this data is consistent with marketing time reflected on the first page of the appraiser’s report.

• The three closed comparable sales must have closed no more than six months from the date of the

appraisal report.

• At least two of the comparable sales must have closed no more than three months from the date of the appraisal report.

• At least one pending sale is provided, as an additional comparable evidencing the market is stable.

• Adjustments to comparables must be in the standard 15% net and 25% gross adjustment range.

• Comparable sales should be located within one mile of the subject for urban and suburban areas

and within 10 miles of the subject for rural areas. Additional Information • This revision to the BB&T Correspondent Lending Declining Market Policy is effective with

loans registered, locked or relocked with BB&T on or after July 18, 2016. Loans registered or locked prior to July 18, 2016 may be delivered provided they meet all previous declining market requirements.

• The current BB&T At Risk Markets list is available on the website.

• The registration confirmation will notify Correspondents that the property may be located in a

Declining Market. Loans received for funding will be audited for compliance with BB&T Correspondent Lending’s LTV/TLTV guidelines for Declining Markets. Any loan which exceeds our LTV/TLTV guidelines will not be funded.

• FHA, VA and USDA/Rural Housing loans are not affected by this policy. The applicable FHA, VA or

USDA guidelines should be followed.

Page 2 7/18/2016

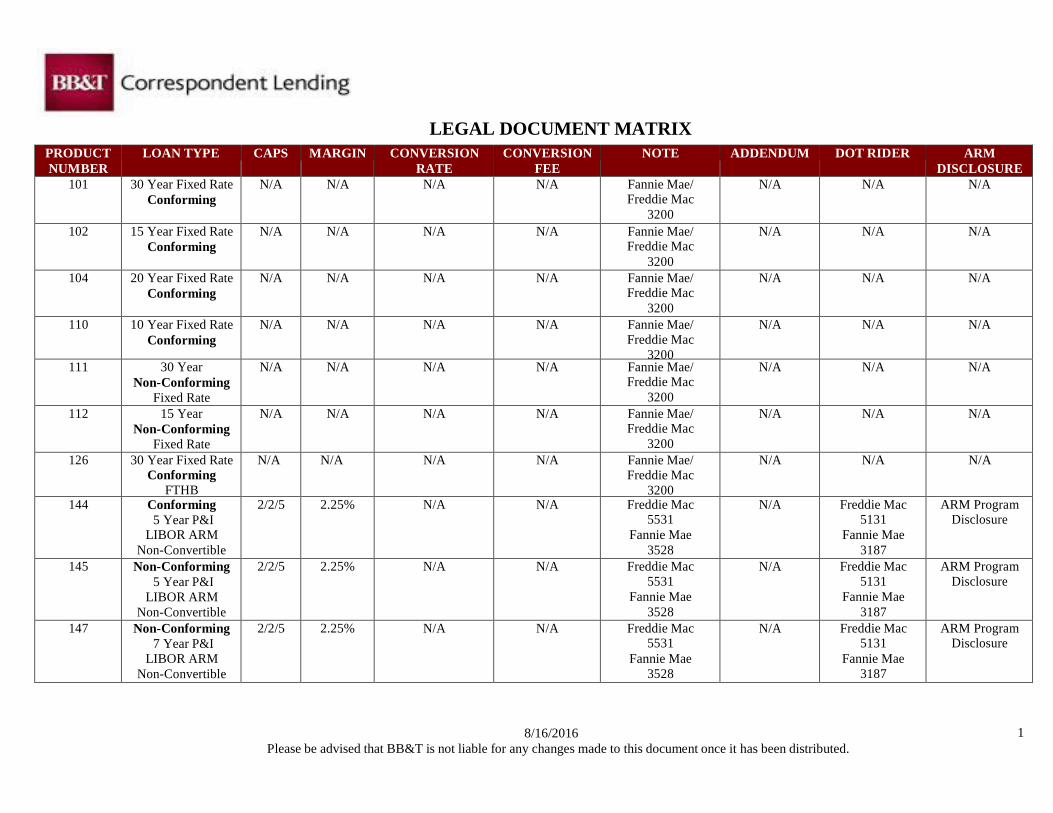

LEGAL DOCUMENT MATRIX

PRODUCT NUMBER

LOAN TYPE CAPS MARGIN CONVERSION RATE

CONVERSION FEE

NOTE ADDENDUM DOT RIDER ARM DISCLOSURE

101 30 Year Fixed Rate Conforming

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

102 15 Year Fixed Rate Conforming

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

104 20 Year Fixed Rate Conforming

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

110 10 Year Fixed Rate Conforming

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

111 30 Year Non-Conforming

Fixed Rate

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

112 15 Year Non-Conforming

Fixed Rate

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

126 30 Year Fixed Rate Conforming

FTHB

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

144 Conforming 5 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

145 Non-Conforming 5 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

147 Non-Conforming 7 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

8/16/2016 1 Please be advised that BB&T is not liable for any changes made to this document once it has been distributed.

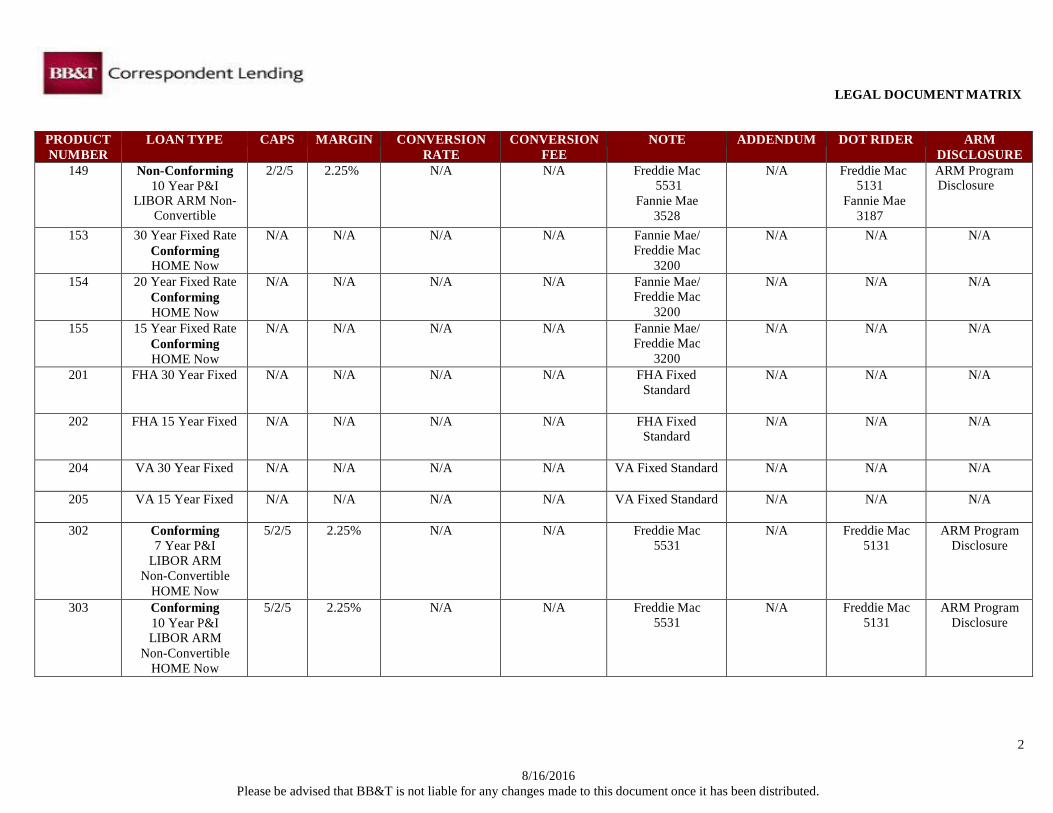

LEGAL DOCUMENT MATRIX

2

8/16/2016 Please be advised that BB&T is not liable for any changes made to this document once it has been distributed.

PRODUCT NUMBER

LOAN TYPE CAPS MARGIN CONVERSION RATE

CONVERSION FEE

NOTE ADDENDUM DOT RIDER ARM DISCLOSURE

149 Non-Conforming 10 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

153 30 Year Fixed Rate Conforming HOME Now

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

154 20 Year Fixed Rate Conforming HOME Now

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

155 15 Year Fixed Rate Conforming HOME Now

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

201 FHA 30 Year Fixed N/A N/A N/A N/A FHA Fixed Standard

N/A N/A N/A

202 FHA 15 Year Fixed N/A N/A N/A N/A FHA Fixed Standard

N/A N/A N/A

204 VA 30 Year Fixed N/A N/A N/A N/A VA Fixed Standard N/A N/A N/A

205 VA 15 Year Fixed N/A N/A N/A N/A VA Fixed Standard N/A N/A N/A

302 Conforming 7 Year P&I

LIBOR ARM Non-Convertible

HOME Now

5/2/5 2.25% N/A N/A Freddie Mac 5531

N/A Freddie Mac 5131

ARM Program Disclosure

303 Conforming 10 Year P&I LIBOR ARM

Non-Convertible HOME Now

5/2/5 2.25% N/A N/A Freddie Mac 5531

N/A Freddie Mac 5131

ARM Program Disclosure

LEGAL DOCUMENT MATRIX

3

8/16/2016 Please be advised that BB&T is not liable for any changes made to this document once it has been distributed.

PRODUCT NUMBER

LOAN TYPE CAPS MARGIN CONVERSION RATE

CONVERSION FEE

NOTE ADDENDUM DOT RIDER ARM DISCLOSURE

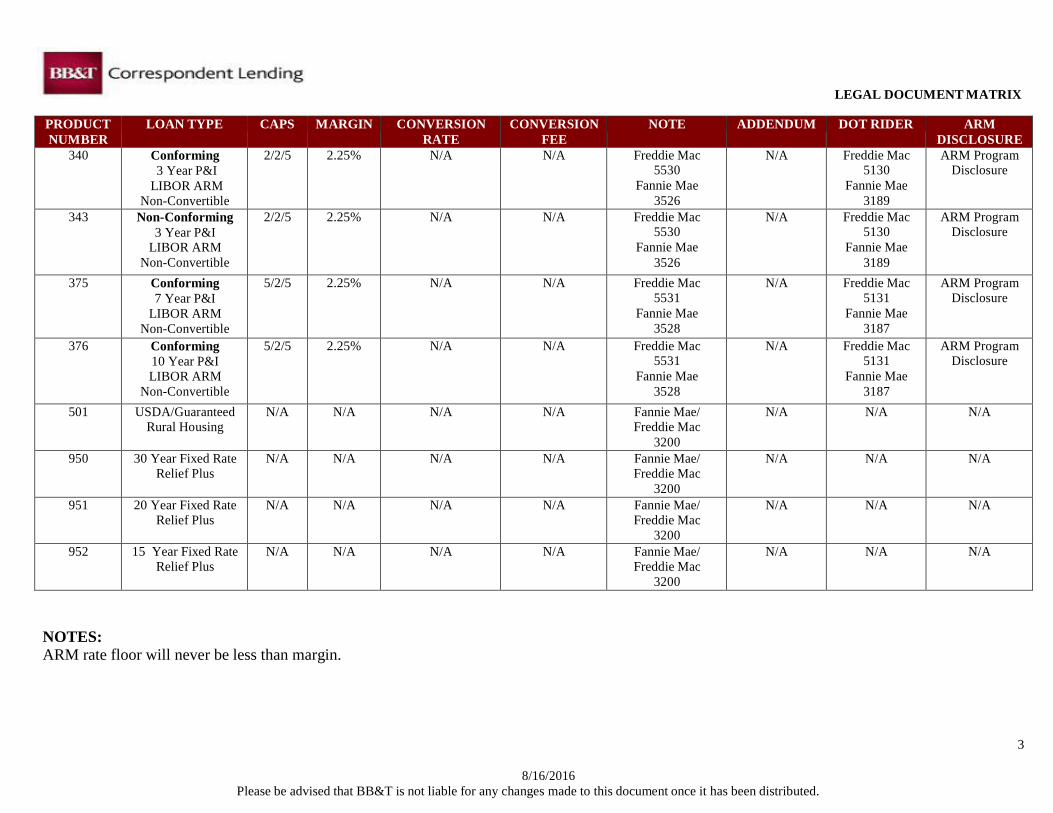

340 Conforming 3 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5530

Fannie Mae 3526

N/A Freddie Mac 5130

Fannie Mae 3189

ARM Program Disclosure

343 Non-Conforming 3 Year P&I

LIBOR ARM Non-Convertible

2/2/5 2.25% N/A N/A Freddie Mac 5530

Fannie Mae 3526

N/A Freddie Mac 5130

Fannie Mae 3189

ARM Program Disclosure

375 Conforming 7 Year P&I

LIBOR ARM Non-Convertible

5/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

376 Conforming 10 Year P&I LIBOR ARM

Non-Convertible

5/2/5 2.25% N/A N/A Freddie Mac 5531

Fannie Mae 3528

N/A Freddie Mac 5131

Fannie Mae 3187

ARM Program Disclosure

501 USDA/Guaranteed Rural Housing

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

950 30 Year Fixed Rate Relief Plus

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

951 20 Year Fixed Rate Relief Plus

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

952 15 Year Fixed Rate Relief Plus

N/A N/A N/A N/A Fannie Mae/ Freddie Mac

3200

N/A N/A N/A

NOTES: ARM rate floor will never be less than margin.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

1

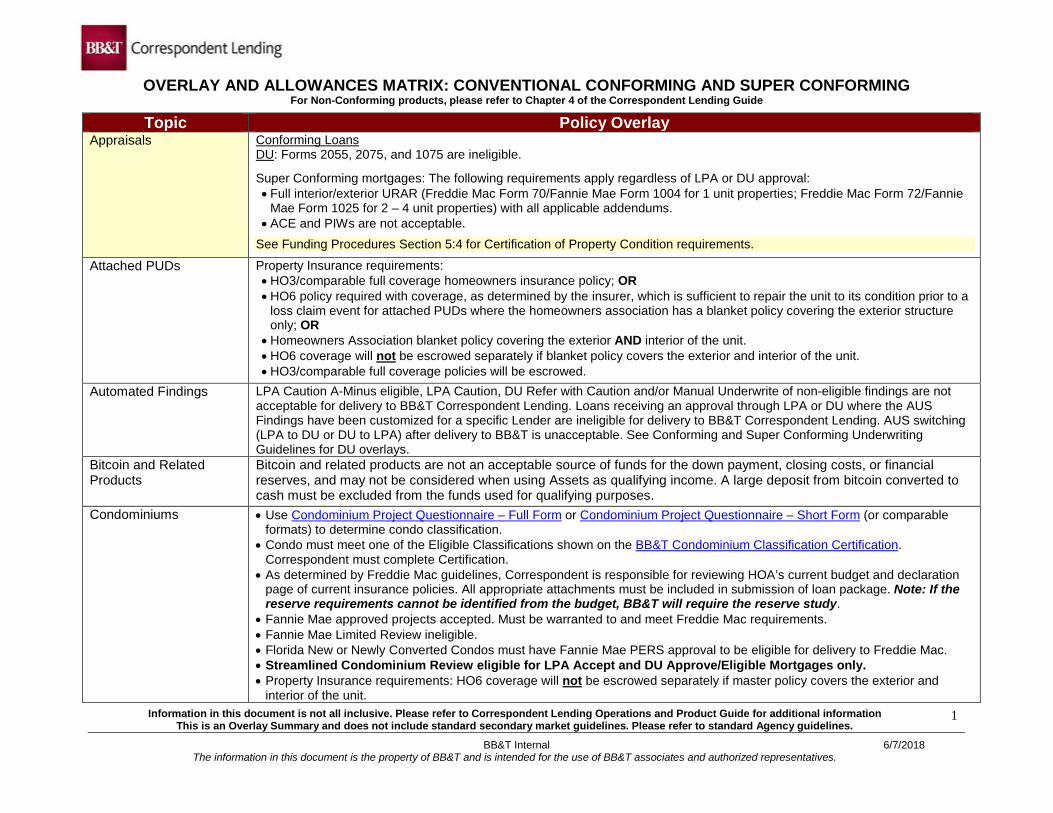

OVERLAY AND ALLOWANCES MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

Topic Policy Overlay Appraisals Conforming Loans

DU: Forms 2055, 2075, and 1075 are ineligible.

Super Conforming mortgages: The following requirements apply regardless of LPA or DU approval: • Full interior/exterior URAR (Freddie Mac Form 70/Fannie Mae Form 1004 for 1 unit properties; Freddie Mac Form 72/Fannie

Mae Form 1025 for 2 – 4 unit properties) with all applicable addendums. • ACE and PIWs are not acceptable.

See Funding Procedures Section 5:4 for Certification of Property Condition requirements.

Attached PUDs Property Insurance requirements: • HO3/comparable full coverage homeowners insurance policy; OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a

loss claim event for attached PUDs where the homeowners association has a blanket policy covering the exterior structure only; OR

• Homeowners Association blanket policy covering the exterior AND interior of the unit. • HO6 coverage will not be escrowed separately if blanket policy covers the exterior and interior of the unit. • HO3/comparable full coverage policies will be escrowed.

Automated Findings LPA Caution A-Minus eligible, LPA Caution, DU Refer with Caution and/or Manual Underwrite of non-eligible findings are not acceptable for delivery to BB&T Correspondent Lending. Loans receiving an approval through LPA or DU where the AUS Findings have been customized for a specific Lender are ineligible for delivery to BB&T Correspondent Lending. AUS switching (LPA to DU or DU to LPA) after delivery to BB&T is unacceptable. See Conforming and Super Conforming Underwriting Guidelines for DU overlays.

Bitcoin and Related Products

Bitcoin and related products are not an acceptable source of funds for the down payment, closing costs, or financial reserves, and may not be considered when using Assets as qualifying income. A large deposit from bitcoin converted to cash must be excluded from the funds used for qualifying purposes.

Condominiums • Use Condominium Project Questionnaire – Full Form or Condominium Project Questionnaire – Short Form (or comparable formats) to determine condo classification.

• Condo must meet one of the Eligible Classifications shown on the BB&T Condominium Classification Certification. Correspondent must complete Certification.

• As determined by Freddie Mac guidelines, Correspondent is responsible for reviewing HOA’s current budget and declaration page of current insurance policies. All appropriate attachments must be included in submission of loan package. Note: If the reserve requirements cannot be identified from the budget, BB&T will require the reserve study.

• Fannie Mae approved projects accepted. Must be warranted to and meet Freddie Mac requirements. • Fannie Mae Limited Review ineligible. • Florida New or Newly Converted Condos must have Fannie Mae PERS approval to be eligible for delivery to Freddie Mac. • Streamlined Condominium Review eligible for LPA Accept and DU Approve/Eligible Mortgages only. • Property Insurance requirements: HO6 coverage will not be escrowed separately if master policy covers the exterior and

interior of the unit.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

2

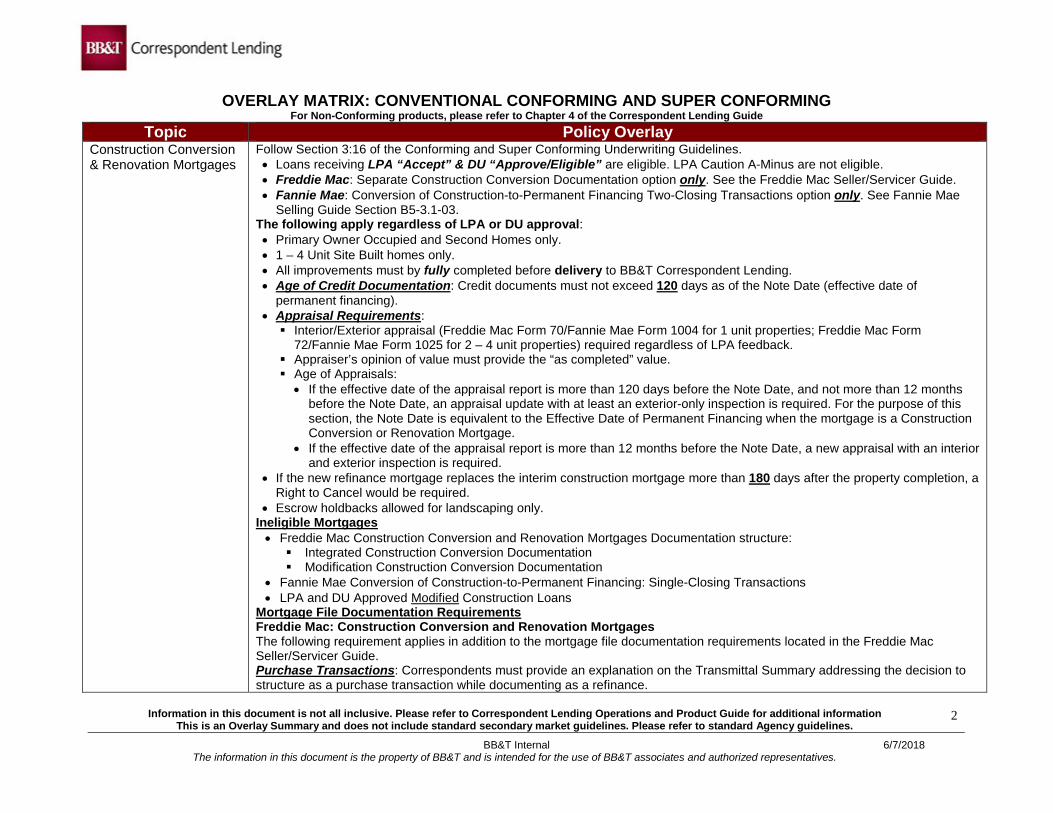

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING

For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide Topic Policy Overlay

Construction Conversion & Renovation Mortgages

Follow Section 3:16 of the Conforming and Super Conforming Underwriting Guidelines. • Loans receiving LPA “Accept” & DU “Approve/Eligible” are eligible. LPA Caution A-Minus are not eligible. • Freddie Mac: Separate Construction Conversion Documentation option only. See the Freddie Mac Seller/Servicer Guide. • Fannie Mae: Conversion of Construction-to-Permanent Financing Two-Closing Transactions option only. See Fannie Mae

Selling Guide Section B5-3.1-03. The following apply regardless of LPA or DU approval: • Primary Owner Occupied and Second Homes only. • 1 – 4 Unit Site Built homes only. • All improvements must by fully completed before delivery to BB&T Correspondent Lending. • Age of Credit Documentation: Credit documents must not exceed 120 days as of the Note Date (effective date of

permanent financing). • Appraisal Requirements: Interior/Exterior appraisal (Freddie Mac Form 70/Fannie Mae Form 1004 for 1 unit properties; Freddie Mac Form

72/Fannie Mae Form 1025 for 2 – 4 unit properties) required regardless of LPA feedback. Appraiser’s opinion of value must provide the “as completed” value. Age of Appraisals:

• If the effective date of the appraisal report is more than 120 days before the Note Date, and not more than 12 months before the Note Date, an appraisal update with at least an exterior-only inspection is required. For the purpose of this section, the Note Date is equivalent to the Effective Date of Permanent Financing when the mortgage is a Construction Conversion or Renovation Mortgage.

• If the effective date of the appraisal report is more than 12 months before the Note Date, a new appraisal with an interior and exterior inspection is required.

• If the new refinance mortgage replaces the interim construction mortgage more than 180 days after the property completion, a Right to Cancel would be required.

• Escrow holdbacks allowed for landscaping only. Ineligible Mortgages • Freddie Mac Construction Conversion and Renovation Mortgages Documentation structure: Integrated Construction Conversion Documentation Modification Construction Conversion Documentation

• Fannie Mae Conversion of Construction-to-Permanent Financing: Single-Closing Transactions • LPA and DU Approved Modified Construction Loans

Mortgage File Documentation Requirements Freddie Mac: Construction Conversion and Renovation Mortgages The following requirement applies in addition to the mortgage file documentation requirements located in the Freddie Mac Seller/Servicer Guide. Purchase Transactions: Correspondents must provide an explanation on the Transmittal Summary addressing the decision to structure as a purchase transaction while documenting as a refinance.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

3

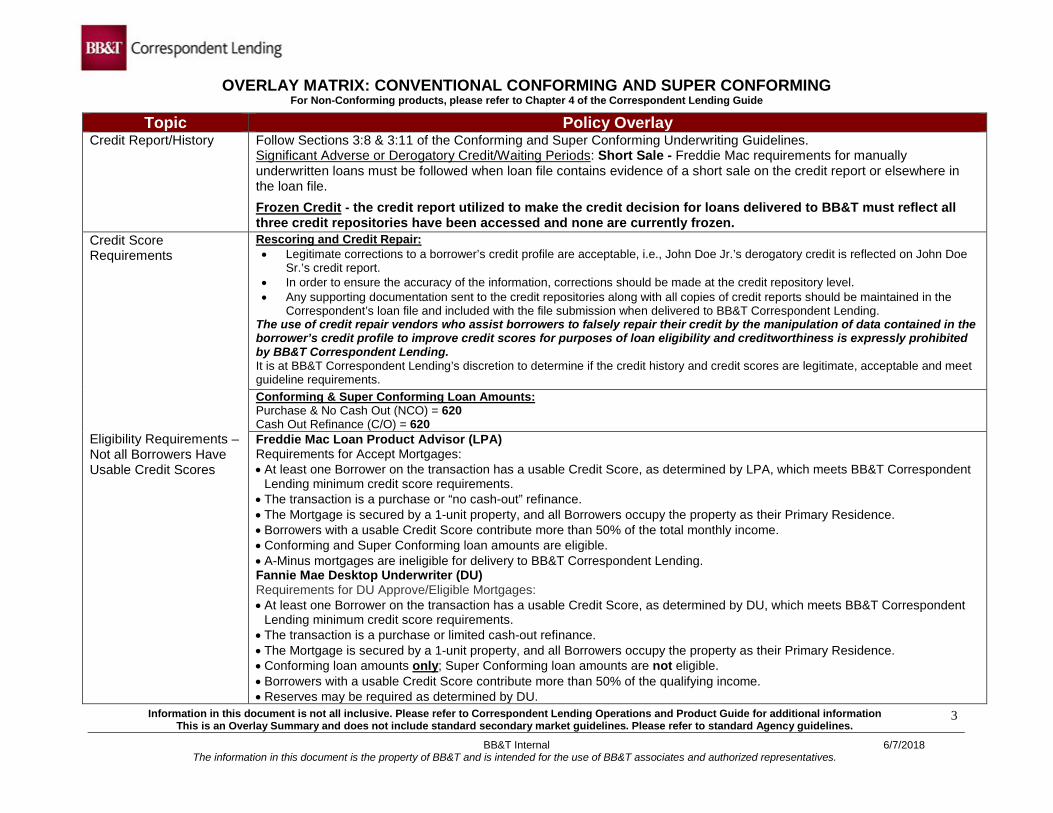

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

Topic Policy Overlay Credit Report/History Follow Sections 3:8 & 3:11 of the Conforming and Super Conforming Underwriting Guidelines.

Significant Adverse or Derogatory Credit/Waiting Periods: Short Sale - Freddie Mac requirements for manually underwritten loans must be followed when loan file contains evidence of a short sale on the credit report or elsewhere in the loan file.

Frozen Credit - the credit report utilized to make the credit decision for loans delivered to BB&T must reflect all three credit repositories have been accessed and none are currently frozen.

Credit Score Requirements Eligibility Requirements – Not all Borrowers Have Usable Credit Scores

Rescoring and Credit Repair: • Legitimate corrections to a borrower’s credit profile are acceptable, i.e., John Doe Jr.’s derogatory credit is reflected on John Doe

Sr.’s credit report. • In order to ensure the accuracy of the information, corrections should be made at the credit repository level. • Any supporting documentation sent to the credit repositories along with all copies of credit reports should be maintained in the

Correspondent’s loan file and included with the file submission when delivered to BB&T Correspondent Lending. The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower’s credit profile to improve credit scores for purposes of loan eligibility and creditworthiness is expressly prohibited by BB&T Correspondent Lending. It is at BB&T Correspondent Lending’s discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements.

Conforming & Super Conforming Loan Amounts: Purchase & No Cash Out (NCO) = 620 Cash Out Refinance (C/O) = 620 Freddie Mac Loan Product Advisor (LPA) Requirements for Accept Mortgages: • At least one Borrower on the transaction has a usable Credit Score, as determined by LPA, which meets BB&T Correspondent

Lending minimum credit score requirements. • The transaction is a purchase or “no cash-out” refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary Residence. • Borrowers with a usable Credit Score contribute more than 50% of the total monthly income. • Conforming and Super Conforming loan amounts are eligible. • A-Minus mortgages are ineligible for delivery to BB&T Correspondent Lending. Fannie Mae Desktop Underwriter (DU) Requirements for DU Approve/Eligible Mortgages: • At least one Borrower on the transaction has a usable Credit Score, as determined by DU, which meets BB&T Correspondent

Lending minimum credit score requirements. • The transaction is a purchase or limited cash-out refinance. • The Mortgage is secured by a 1-unit property, and all Borrowers occupy the property as their Primary Residence. • Conforming loan amounts only; Super Conforming loan amounts are not eligible. • Borrowers with a usable Credit Score contribute more than 50% of the qualifying income. • Reserves may be required as determined by DU.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

4

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

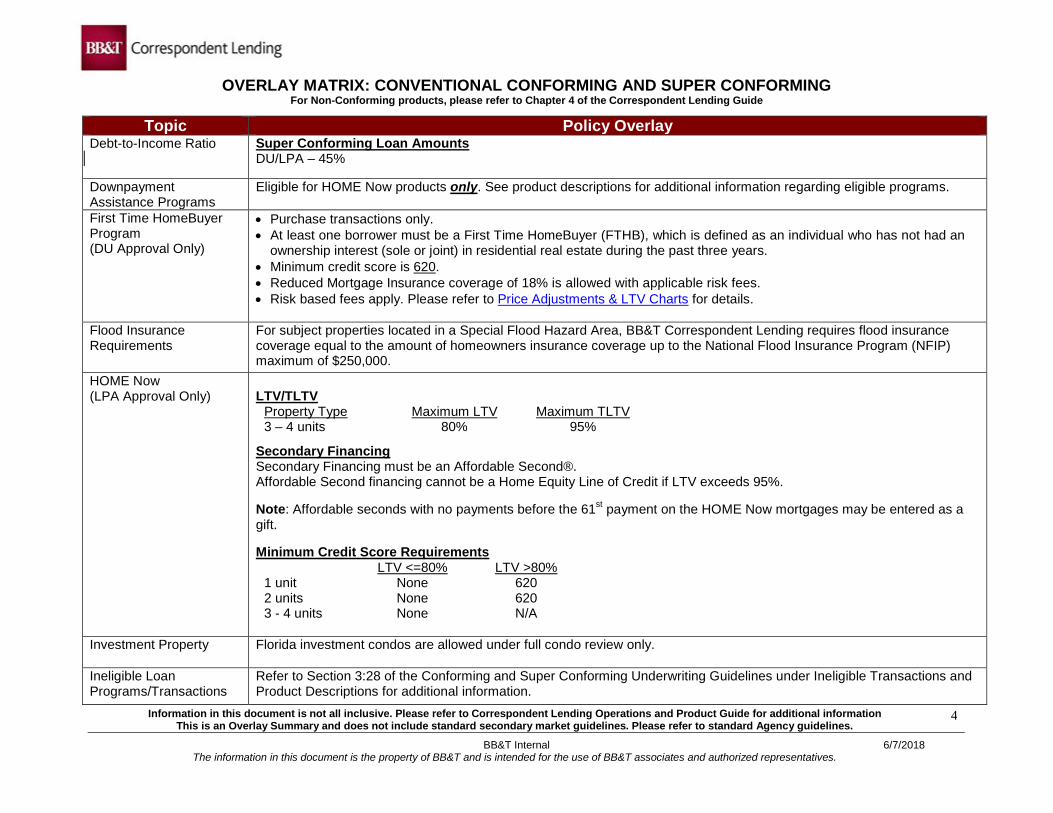

Topic Policy Overlay Debt-to-Income Ratio Super Conforming Loan Amounts

DU/LPA – 45%

Downpayment Assistance Programs

Eligible for HOME Now products only. See product descriptions for additional information regarding eligible programs.

First Time HomeBuyer Program (DU Approval Only)

• Purchase transactions only. • At least one borrower must be a First Time HomeBuyer (FTHB), which is defined as an individual who has not had an

ownership interest (sole or joint) in residential real estate during the past three years. • Minimum credit score is 620. • Reduced Mortgage Insurance coverage of 18% is allowed with applicable risk fees. • Risk based fees apply. Please refer to Price Adjustments & LTV Charts for details.

Flood Insurance Requirements

For subject properties located in a Special Flood Hazard Area, BB&T Correspondent Lending requires flood insurance coverage equal to the amount of homeowners insurance coverage up to the National Flood Insurance Program (NFIP) maximum of $250,000.

HOME Now (LPA Approval Only)

LTV/TLTV

Property Type Maximum LTV Maximum TLTV 3 – 4 units 80% 95%

Secondary Financing Secondary Financing must be an Affordable Second®. Affordable Second financing cannot be a Home Equity Line of Credit if LTV exceeds 95%. Note: Affordable seconds with no payments before the 61st payment on the HOME Now mortgages may be entered as a gift. Minimum Credit Score Requirements

LTV <=80% LTV >80% 1 unit None 620 2 units None 620 3 - 4 units None N/A

Investment Property Florida investment condos are allowed under full condo review only.

Ineligible Loan Programs/Transactions

Refer to Section 3:28 of the Conforming and Super Conforming Underwriting Guidelines under Ineligible Transactions and Product Descriptions for additional information.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

5

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

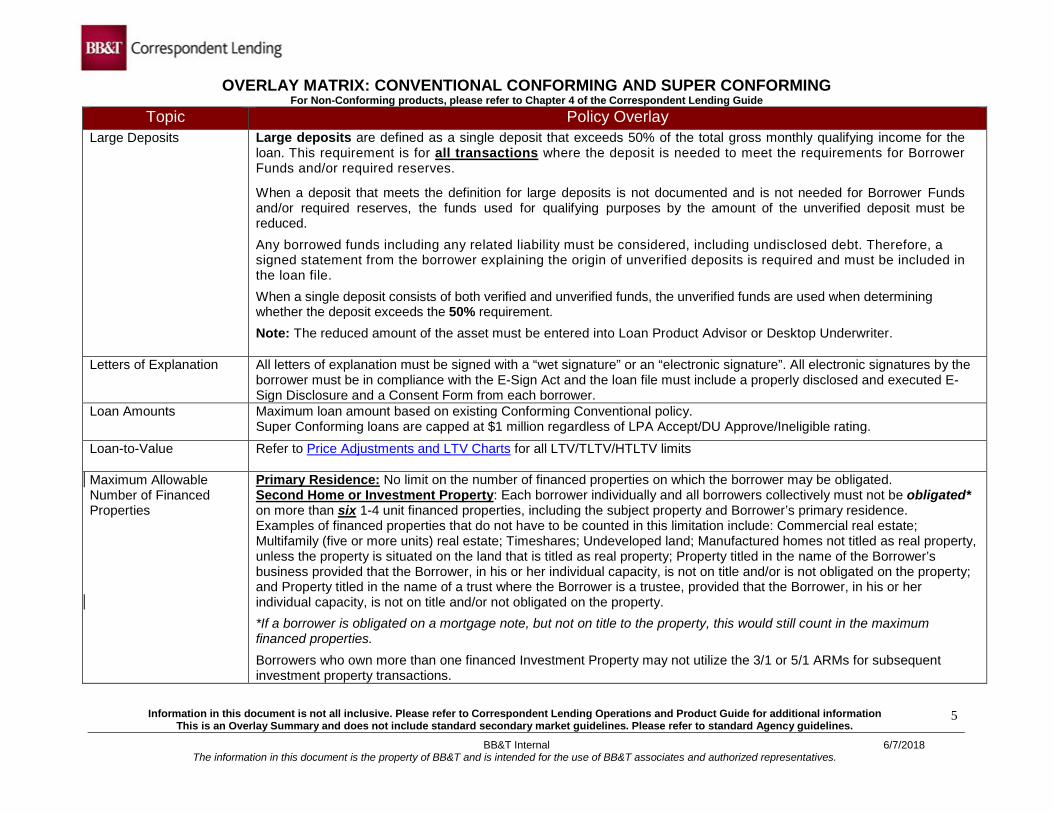

Topic Policy Overlay Large Deposits Large deposits are defined as a single deposit that exceeds 50% of the total gross monthly qualifying income for the

loan. This requirement is for all transactions where the deposit is needed to meet the requirements for Borrower Funds and/or required reserves.

When a deposit that meets the definition for large deposits is not documented and is not needed for Borrower Funds and/or required reserves, the funds used for qualifying purposes by the amount of the unverified deposit must be reduced.

Any borrowed funds including any related liability must be considered, including undisclosed debt. Therefore, a signed statement from the borrower explaining the origin of unverified deposits is required and must be included in the loan file.

When a single deposit consists of both verified and unverified funds, the unverified funds are used when determining whether the deposit exceeds the 50% requirement.

Note: The reduced amount of the asset must be entered into Loan Product Advisor or Desktop Underwriter.

Letters of Explanation All letters of explanation must be signed with a “wet signature” or an “electronic signature”. All electronic signatures by the borrower must be in compliance with the E-Sign Act and the loan file must include a properly disclosed and executed E-Sign Disclosure and a Consent Form from each borrower.

Loan Amounts Maximum loan amount based on existing Conforming Conventional policy. Super Conforming loans are capped at $1 million regardless of LPA Accept/DU Approve/Ineligible rating.

Loan-to-Value Refer to Price Adjustments and LTV Charts for all LTV/TLTV/HTLTV limits

Maximum Allowable Number of Financed Properties

Primary Residence: No limit on the number of financed properties on which the borrower may be obligated. Second Home or Investment Property: Each borrower individually and all borrowers collectively must not be obligated* on more than six 1-4 unit financed properties, including the subject property and Borrower’s primary residence. Examples of financed properties that do not have to be counted in this limitation include: Commercial real estate; Multifamily (five or more units) real estate; Timeshares; Undeveloped land; Manufactured homes not titled as real property, unless the property is situated on the land that is titled as real property; Property titled in the name of the Borrower’s business provided that the Borrower, in his or her individual capacity, is not on title and/or is not obligated on the property; and Property titled in the name of a trust where the Borrower is a trustee, provided that the Borrower, in his or her individual capacity, is not on title and/or not obligated on the property.

*If a borrower is obligated on a mortgage note, but not on title to the property, this would still count in the maximum financed properties.

Borrowers who own more than one financed Investment Property may not utilize the 3/1 or 5/1 ARMs for subsequent investment property transactions.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

6

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

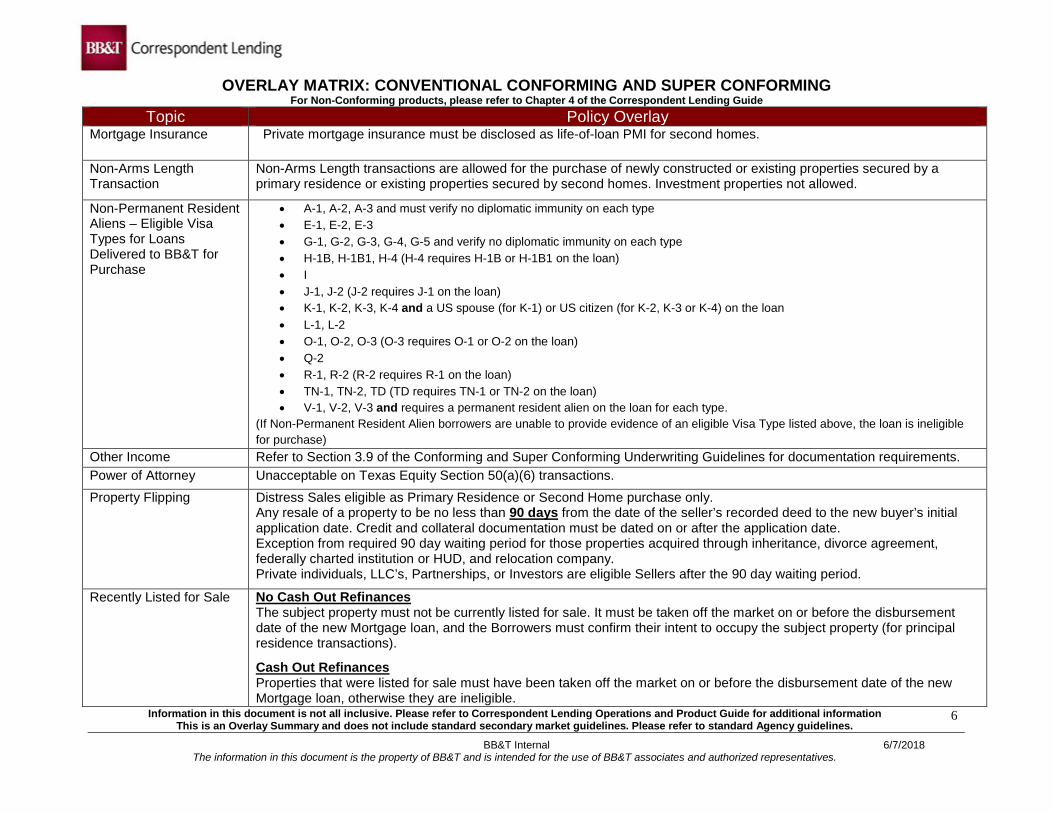

Topic Policy Overlay Mortgage Insurance Private mortgage insurance must be disclosed as life-of-loan PMI for second homes.

Non-Arms Length Transaction

Non-Arms Length transactions are allowed for the purchase of newly constructed or existing properties secured by a primary residence or existing properties secured by second homes. Investment properties not allowed.

Non-Permanent Resident Aliens – Eligible Visa Types for Loans Delivered to BB&T for Purchase

• A-1, A-2, A-3 and must verify no diplomatic immunity on each type • E-1, E-2, E-3 • G-1, G-2, G-3, G-4, G-5 and verify no diplomatic immunity on each type • H-1B, H-1B1, H-4 (H-4 requires H-1B or H-1B1 on the loan) • I • J-1, J-2 (J-2 requires J-1 on the loan) • K-1, K-2, K-3, K-4 and a US spouse (for K-1) or US citizen (for K-2, K-3 or K-4) on the loan • L-1, L-2 • O-1, O-2, O-3 (O-3 requires O-1 or O-2 on the loan) • Q-2 • R-1, R-2 (R-2 requires R-1 on the loan) • TN-1, TN-2, TD (TD requires TN-1 or TN-2 on the loan) • V-1, V-2, V-3 and requires a permanent resident alien on the loan for each type.

(If Non-Permanent Resident Alien borrowers are unable to provide evidence of an eligible Visa Type listed above, the loan is ineligible for purchase)

Other Income Refer to Section 3.9 of the Conforming and Super Conforming Underwriting Guidelines for documentation requirements. Power of Attorney

Unacceptable on Texas Equity Section 50(a)(6) transactions. Property Flipping Distress Sales eligible as Primary Residence or Second Home purchase only.

Any resale of a property to be no less than 90 days from the date of the seller’s recorded deed to the new buyer’s initial application date. Credit and collateral documentation must be dated on or after the application date. Exception from required 90 day waiting period for those properties acquired through inheritance, divorce agreement, federally charted institution or HUD, and relocation company. Private individuals, LLC’s, Partnerships, or Investors are eligible Sellers after the 90 day waiting period.

Recently Listed for Sale No Cash Out Refinances The subject property must not be currently listed for sale. It must be taken off the market on or before the disbursement date of the new Mortgage loan, and the Borrowers must confirm their intent to occupy the subject property (for principal residence transactions).

Cash Out Refinances Properties that were listed for sale must have been taken off the market on or before the disbursement date of the new Mortgage loan, otherwise they are ineligible.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

7

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

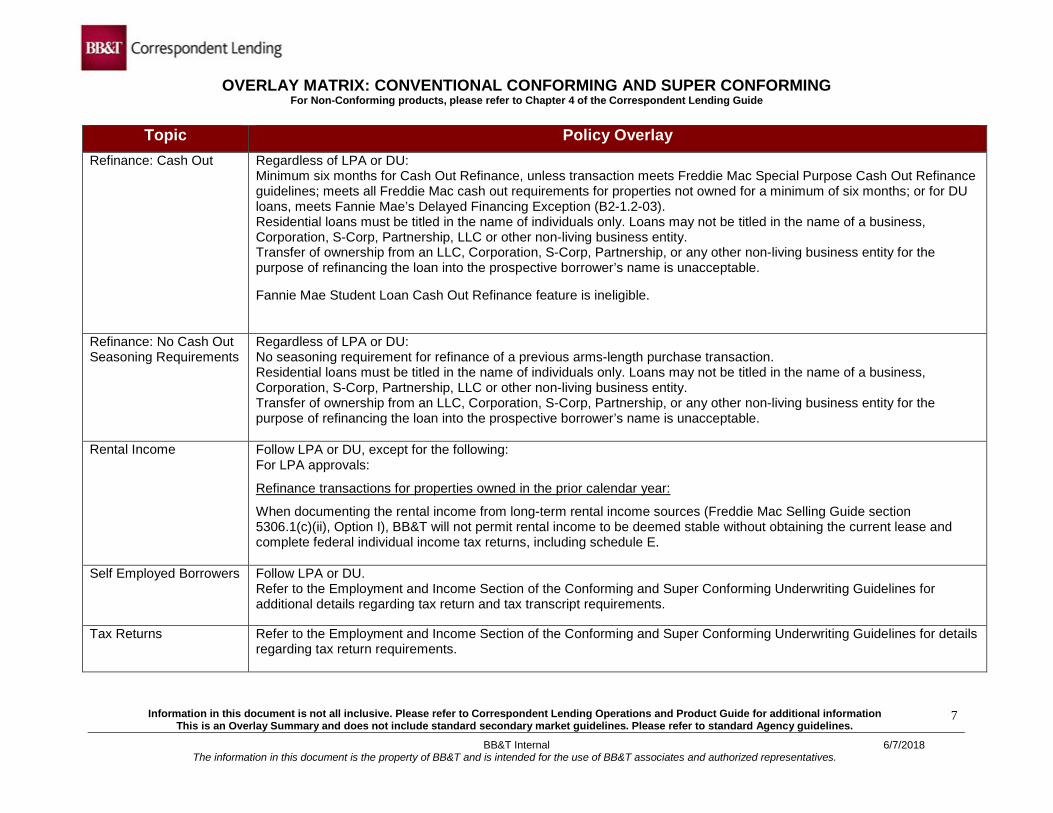

Topic Policy Overlay Refinance: Cash Out Regardless of LPA or DU:

Minimum six months for Cash Out Refinance, unless transaction meets Freddie Mac Special Purpose Cash Out Refinance guidelines; meets all Freddie Mac cash out requirements for properties not owned for a minimum of six months; or for DU loans, meets Fannie Mae’s Delayed Financing Exception (B2-1.2-03). Residential loans must be titled in the name of individuals only. Loans may not be titled in the name of a business, Corporation, S-Corp, Partnership, LLC or other non-living business entity. Transfer of ownership from an LLC, Corporation, S-Corp, Partnership, or any other non-living business entity for the purpose of refinancing the loan into the prospective borrower’s name is unacceptable. Fannie Mae Student Loan Cash Out Refinance feature is ineligible.

Refinance: No Cash Out Seasoning Requirements

Regardless of LPA or DU: No seasoning requirement for refinance of a previous arms-length purchase transaction. Residential loans must be titled in the name of individuals only. Loans may not be titled in the name of a business, Corporation, S-Corp, Partnership, LLC or other non-living business entity. Transfer of ownership from an LLC, Corporation, S-Corp, Partnership, or any other non-living business entity for the purpose of refinancing the loan into the prospective borrower’s name is unacceptable.

Rental Income

Follow LPA or DU, except for the following: For LPA approvals:

Refinance transactions for properties owned in the prior calendar year:

When documenting the rental income from long-term rental income sources (Freddie Mac Selling Guide section 5306.1(c)(ii), Option I), BB&T will not permit rental income to be deemed stable without obtaining the current lease and complete federal individual income tax returns, including schedule E.

Self Employed Borrowers Follow LPA or DU. Refer to the Employment and Income Section of the Conforming and Super Conforming Underwriting Guidelines for additional details regarding tax return and tax transcript requirements.

Tax Returns Refer to the Employment and Income Section of the Conforming and Super Conforming Underwriting Guidelines for details regarding tax return requirements.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

8

OVERLAY MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING For Non-Conforming products, please refer to Chapter 4 of the Correspondent Lending Guide

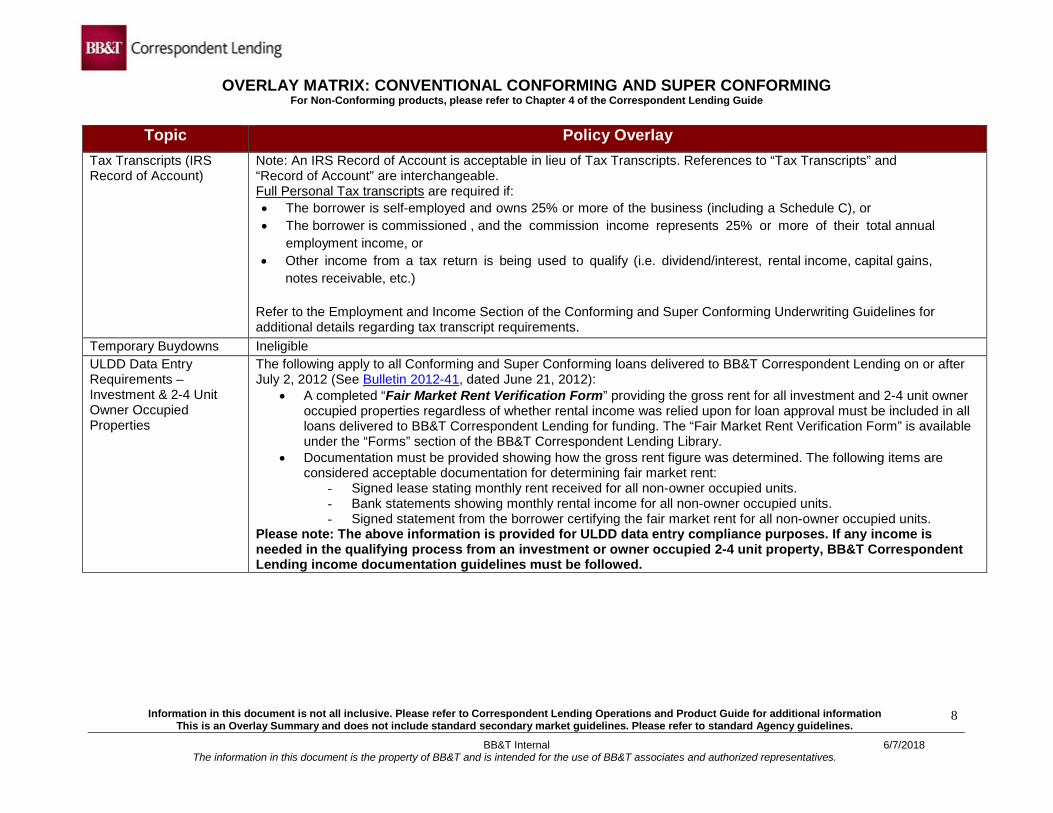

Topic Policy Overlay Tax Transcripts (IRS Record of Account)

Note: An IRS Record of Account is acceptable in lieu of Tax Transcripts. References to “Tax Transcripts” and “Record of Account” are interchangeable. Full Personal Tax transcripts are required if: • The borrower is self-employed and owns 25% or more of the business (including a Schedule C), or • The borrower is commissioned , and the commission income represents 25% or more of their total annual

employment income, or • Other income from a tax return is being used to qualify (i.e. dividend/interest, rental income, capital gains,

notes receivable, etc.)

Refer to the Employment and Income Section of the Conforming and Super Conforming Underwriting Guidelines for additional details regarding tax transcript requirements.

Temporary Buydowns Ineligible ULDD Data Entry Requirements – Investment & 2-4 Unit Owner Occupied Properties

The following apply to all Conforming and Super Conforming loans delivered to BB&T Correspondent Lending on or after July 2, 2012 (See Bulletin 2012-41, dated June 21, 2012):

• A completed “Fair Market Rent Verification Form” providing the gross rent for all investment and 2-4 unit owner occupied properties regardless of whether rental income was relied upon for loan approval must be included in all loans delivered to BB&T Correspondent Lending for funding. The “Fair Market Rent Verification Form” is available under the “Forms” section of the BB&T Correspondent Lending Library.

• Documentation must be provided showing how the gross rent figure was determined. The following items are considered acceptable documentation for determining fair market rent:

- Signed lease stating monthly rent received for all non-owner occupied units. - Bank statements showing monthly rental income for all non-owner occupied units. - Signed statement from the borrower certifying the fair market rent for all non-owner occupied units.

Please note: The above information is provided for ULDD data entry compliance purposes. If any income is needed in the qualifying process from an investment or owner occupied 2-4 unit property, BB&T Correspondent Lending income documentation guidelines must be followed.

Information in this document is not all inclusive. Please refer to Correspondent Lending Operations and Product Guide for additional information This is an Overlay Summary and does not include standard secondary market guidelines. Please refer to standard Agency guidelines.

BB&T Internal 6/7/2018 The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives.

9

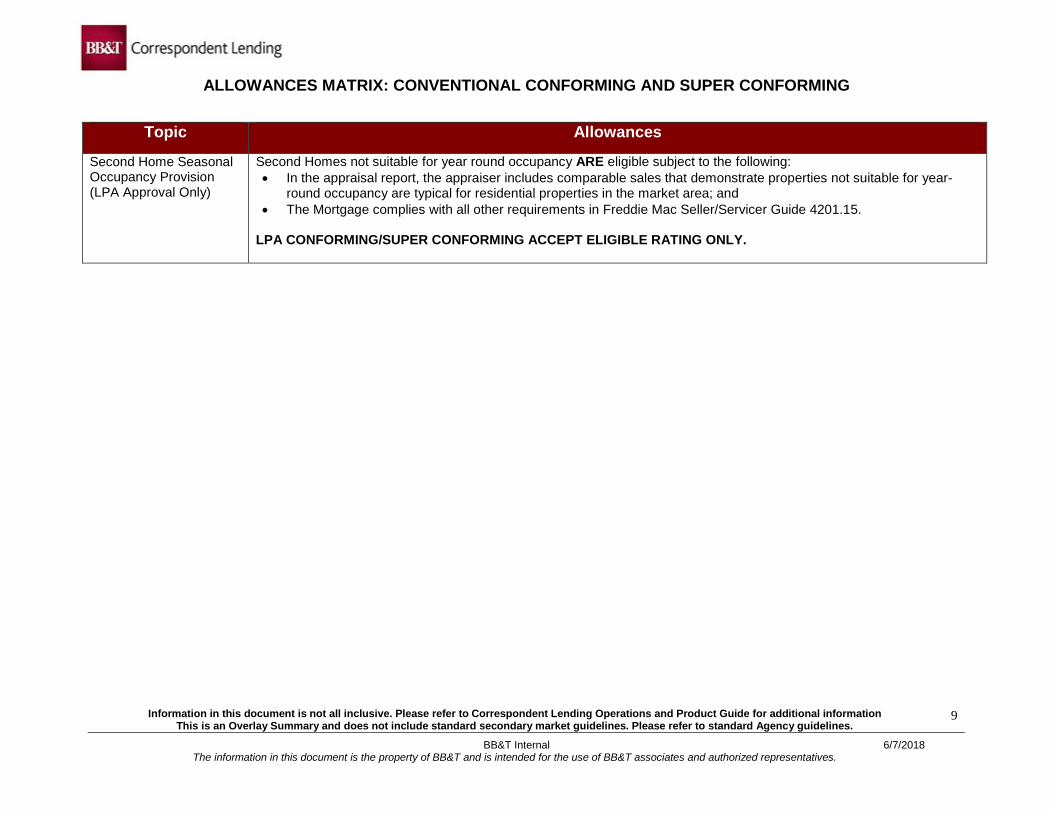

ALLOWANCES MATRIX: CONVENTIONAL CONFORMING AND SUPER CONFORMING

Topic Allowances

Second Home Seasonal Occupancy Provision (LPA Approval Only)

Second Homes not suitable for year round occupancy ARE eligible subject to the following: • In the appraisal report, the appraiser includes comparable sales that demonstrate properties not suitable for year-

round occupancy are typical for residential properties in the market area; and • The Mortgage complies with all other requirements in Freddie Mac Seller/Servicer Guide 4201.15.

LPA CONFORMING/SUPER CONFORMING ACCEPT ELIGIBLE RATING ONLY.

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives. Page 1 of 3

Topic Policy Overlay FHA

VA USD

A

• HO3/comparable full coverage homeowners policy (escrow required); OR • HO6 policy required with coverage, as determined by the insurer, which is sufficient to repair the unit to its condition prior to a loss claim event for attached PUDs where the HOA has a blanket policy covering the exterior structure only (will not be escrowed separately if blanket policy covers exterior and interior); OR • HOA blanket policy covering the exterior AND interior of unit (5:4 Funding Procedures)

x x x

FHA Approved: DELRAP and HRAP are acceptable. EXCEPTION: Streamline Refinances currently serviced by BB&T are acceptable for delivery to BB&T where the condominium project is no longer insurable under FHA guidelines or the project was DE approved and not FHA approved. (11:2)

x

LPA Accept or DU Approve/Eligible findings required on Purchases, No Cash Out Refinances, and Cash-Out Refinances. TOTAL Scorecard run through an approved FHA vendor is acceptable. See FHA Connection for approved list of vendors. Manual Underwriting required for Streamlined Refinances. Simple Refinance Transactions are not eligible for delivery at this time. (11:2)

x

LPA Accept or DU Approve/Eligible findings required on Purchase and Cash-Out Refinances. Manual Underwriting required on VA IRRRLs. (11:3)

x

Manual Underwriting or GUS Accept Eligible accepted. Loans submitted to GUS receiving a "Refer" or "Refer with Caution" and switched to manual underwriting are not eligible. (11:1)

x

Bitcoin & Related ProductsNot acceptable source of funds for down payment, closing costs, or reserves. A large deposit from bitcoin converted to cash must be excluded from funds used for qualifying. (11:1, 11:2, 11:3)

x x x

Credit Inquiries & New Debt

Written explanation is required fom Borrower for all credit inquiries made within the last 90 days. New debts must be included in debt ratios. (11:1, 11:2, 11:3)

x x

Purchases, No Cash-Out, Cash-Out & BB&T serviced Owner Occupied Streamline Refinances/HUD REO properties: ≤ $453,100 = 660 $453,101 - $750,000 = 680BB&T Serviced Non-Owner Occupied Streamline Refinances: All loan amounts = 720FHA Owner Occupied and Non-Owner Occupied Streamlines that are not BB&T serviced are ineligible. (11:2)

x

Purchases & Cash-Out Refinances: ≤ $453,100 = 620 $453,101 - $750,000 = 660IRRRLs: An In-file or Tri-Merge Credit Report is required to determine compliance with BB&T minimum credit score requirements. O/O BB&T serviced all loan amounts: 620 O/O Non-BB&T serviced ≤ $453,100 = 640 O/O Non-BB&T serviced $453,101 - $750,000 = 660 Non-Owner Occupied BB&T serviced only IRRRL = 700 (11:3)

x

The primary source (Seller Guide section number) is provided for easy reference; however, Sellers should be aware that the references are not all inclusive. Please refer to the Correspondent Lending Operations and Product Guide for additional information.

This is an Overlay Summary and does not include standard secondary market guidelines.

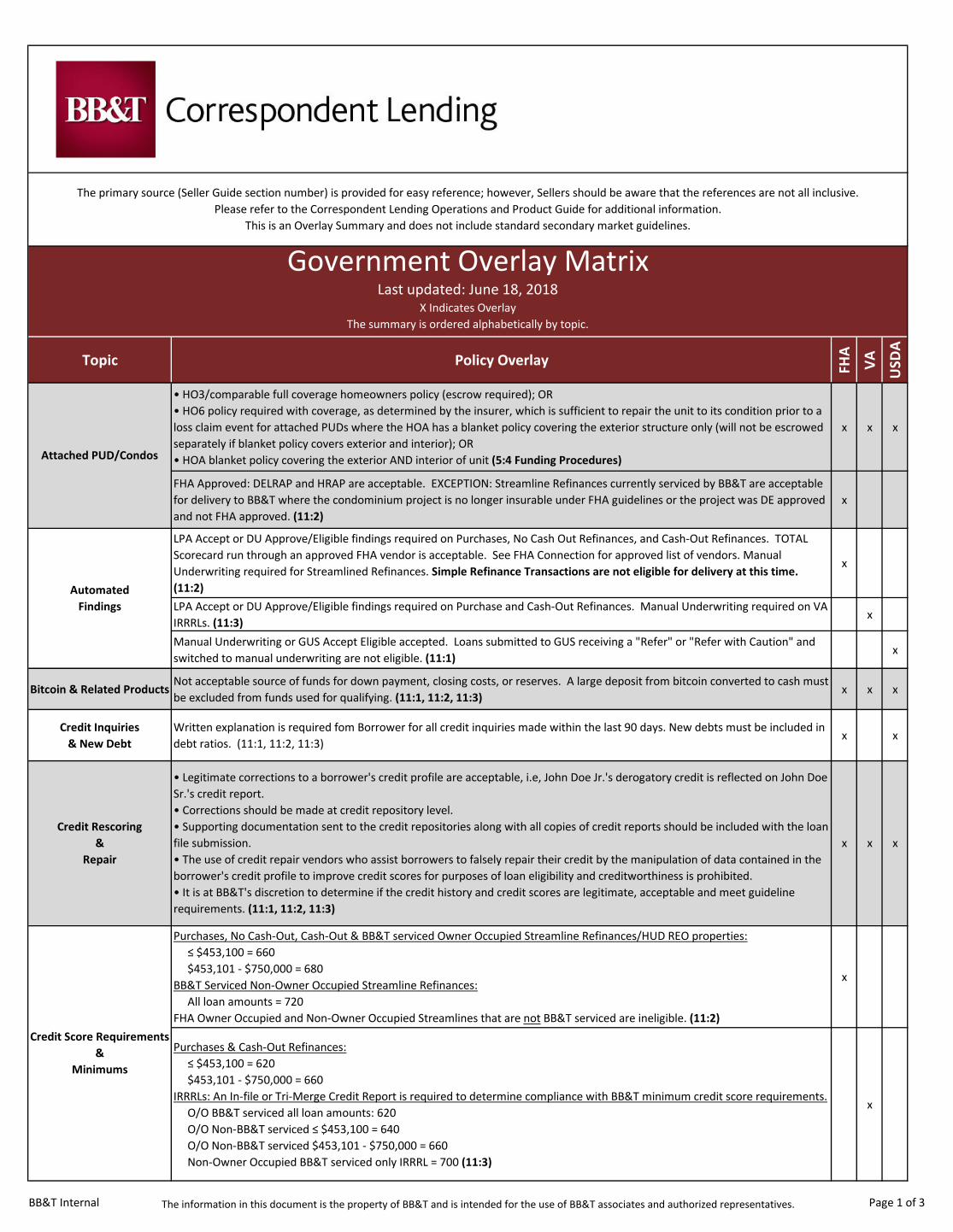

Government Overlay MatrixLast updated: June 18, 2018

X Indicates OverlayThe summary is ordered alphabetically by topic.

Automated Findings

• Legitimate corrections to a borrower's credit profile are acceptable, i.e, John Doe Jr.'s derogatory credit is reflected on John Doe Sr.'s credit report. • Corrections should be made at credit repository level.• Supporting documentation sent to the credit repositories along with all copies of credit reports should be included with the loan file submission.• The use of credit repair vendors who assist borrowers to falsely repair their credit by the manipulation of data contained in the borrower's credit profile to improve credit scores for purposes of loan eligibility and creditworthiness is prohibited. • It is at BB&T's discretion to determine if the credit history and credit scores are legitimate, acceptable and meet guideline requirements. (11:1, 11:2, 11:3)

x x x

Attached PUD/Condos

Credit Score Requirements&

Minimums

Credit Rescoring&

Repair

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives. Page 2 of 3

Topic Policy Overlay FHA

VA USD

A

Credit Score Requirements&

Minimums (Continued)

Minimum credit score for each borrower on transaction is 640 for program eligibility and credit underwriting. For borrowers with one credit score reported on the traditional credit report, non-traditional credit scores are required. See USDA Product Description for more details. A non-traditional mortgage credit report score is not eligible for consideration to meet credit score requirement. No minimum credit score requirement for USDA Streamlined Assist Refinance transactions, however a merged credit report must be included with the loan submission package. (11:1)

x

Debt-to-Income RatioMaximum DTI is 50% on Purchases and Refinances, regardless of DU or LPA Approval. FHA Jumbo loans are limited to 45% regardless of DU or LPA Approval. DTI is calculated on non-credit qualifying Streamline Refinances. (11:2)

x

Downpayment Assistance Programs

FHLB eligible for all government programs. See product descriptions for information regarding additional eligible programs. (11:1, 11:2, 11:3)

x x x

Flood Insurance

For subject properties located in a Special Flood Hazard Area, flood insurance coverage equal to the amount of homeowner's insurance coverage up to the National Flood Insurance Program (NFIP) maximum of $250,000 will be required. (5:4 Funding Procedures)

x x x

Frozen CreditThe credit report utilized to make the credit decision must reflect all three credit repositories have been accessed and none are currently frozen. (11:1, 11:2, 11:3)

x x x

Income

Projected Income - Borrower's employment offer must be non-contingent, and the non-contingent offer letter must be retained in the file. In the event the borrower provides an offer letter with contingencies, the file must contain an additional letter from the employer stating that all contingencies have been cleared for employment. Borrower's written acceptance of the employment offer must also be retained in the file. (11:2)

x

Construction Modification loans; Energy Efficient Mortgages (EEMs); Texas Equity Refinance Section 50(a)(6); Adjustable Rate Mortgages; Temporary Buydowns; Lending on Native American Tribal Lands (11:1, 11:2, 11:3)

x x x

Disaster Victims Mortgages 203(h); Good Neighbor Next Door (GNND); Home Equity Conversion Mortgages (HECMS); Non-BB&T serviced Streamline Refinances; Simple Refinances as defined in the FHA Single Family Housing Policy Handbook (4000.1: II.A.8.d.vi.B); Refinances of Borrowers in negative equity position; 203(k) loans that are not fully disbursed with a final inspection in the file at time of delivery. (11:2)

x

VA Vendee Financing Program; Investment Property IRRRLs not serviced by BB&T (11:3) xLoans with an assumability feature; Streamline Refinances. (11:1) xSingle or Double-wide Manufactured housing, Properties subject to a Property Assessed Clean Energy (PACE) Obligation, Condotels, Geodomes, Earth Homes, Quonset Huts, Co-ops. (11:1,11:2, 11:3)

x x x

Loans secured by properties with individual water purification systems. (5:4 Funding Procedures) xProperties located in a mudslide zone (11:1) x

Letters of ExplanationAll letters of explanation must be signed with a "wet signature" or an "electronic signature". All electronic signatures by the borrower must be in compliance with the E-Sign Act and the loan file must include a properly disclosed and executed E-Sign Disclosure and a Consent Form from each borrower. (11:1, 11:2, 11:3)

x x x

Maximum base loan cannot exceed $750,000 in high cost areas. Upfront MIP/VA Funding Fee can be added to maximum base. (11:2, 11:3)

x x

Maximum base loan cannot exceed current conforming conventional limit. Guarantee Fee can be added to maximum base. (11:1)

x

Non-Permanent Resident Aliens - Eligible Visa Types

• A-1, A-2, A-3 and must verify no diplomatic immunity on each type• E-1, E-2, E-3• G-1, G-2, G-3, G-4, G-5 and verify no diplomatic immunity on each type• H-1B, H-1B1, H-4 (H-4 requires H-1B or H-1B1 on the loan)• I• J-1, J-2 (J-2 requires J-1 on the loan)• K-1, K-2, K-3, K-4 and a US spouse (for K-1) or US citizen (for K-2, K-3, or K-4) on the loan• L-1, L-2• O-1, O-2, O-3 (O-3 requires O-1 or O-2 on the loan)• Q-2• R-1, R-2 (R-2 requires R-1 on the loan)• TN-1, TN-2, TD (TD requires TN-1 or TN-2 on the loan)• V-1, V-2, V-3 and requires a permanent resident alien on the loan for each type. (11:1, 11:2, 11:3)(If Non-Permanent Resident Alien Visa Type is not listed in this chart, loan is ineligible for purchase)

x x x

Non-Permanent Resident Aliens - Employment

Authorization Documentation Cards

(EAD)

• A03• A05• A08• A12 - If the country of birth is El Salvador, Honduras or Nicaragua• A17 - Requires spouse with E-1 or E-2 Visa on the loan• A18 - Requires spouse with L-1 Visa on the loan• C02 - Requires spouse with E-1 Visa on the loan• C08• C12 - Requires spouse with E-2 Visa on the loan• C36 - Requires spouse with E-3, H-1B, H-1B1, L-1, or O-1 Visa on the loan (11:1, 11:2, 11:3)(If Non-Permanent Resident Alien EAD Card is not listed in this chart, loan is ineligible for purchase)

x x x

Loan Amounts

Ineligible Property Types

Ineligible Programs / Features

BB&T Internal The information in this document is the property of BB&T and is intended for the use of BB&T associates and authorized representatives. Page 3 of 3

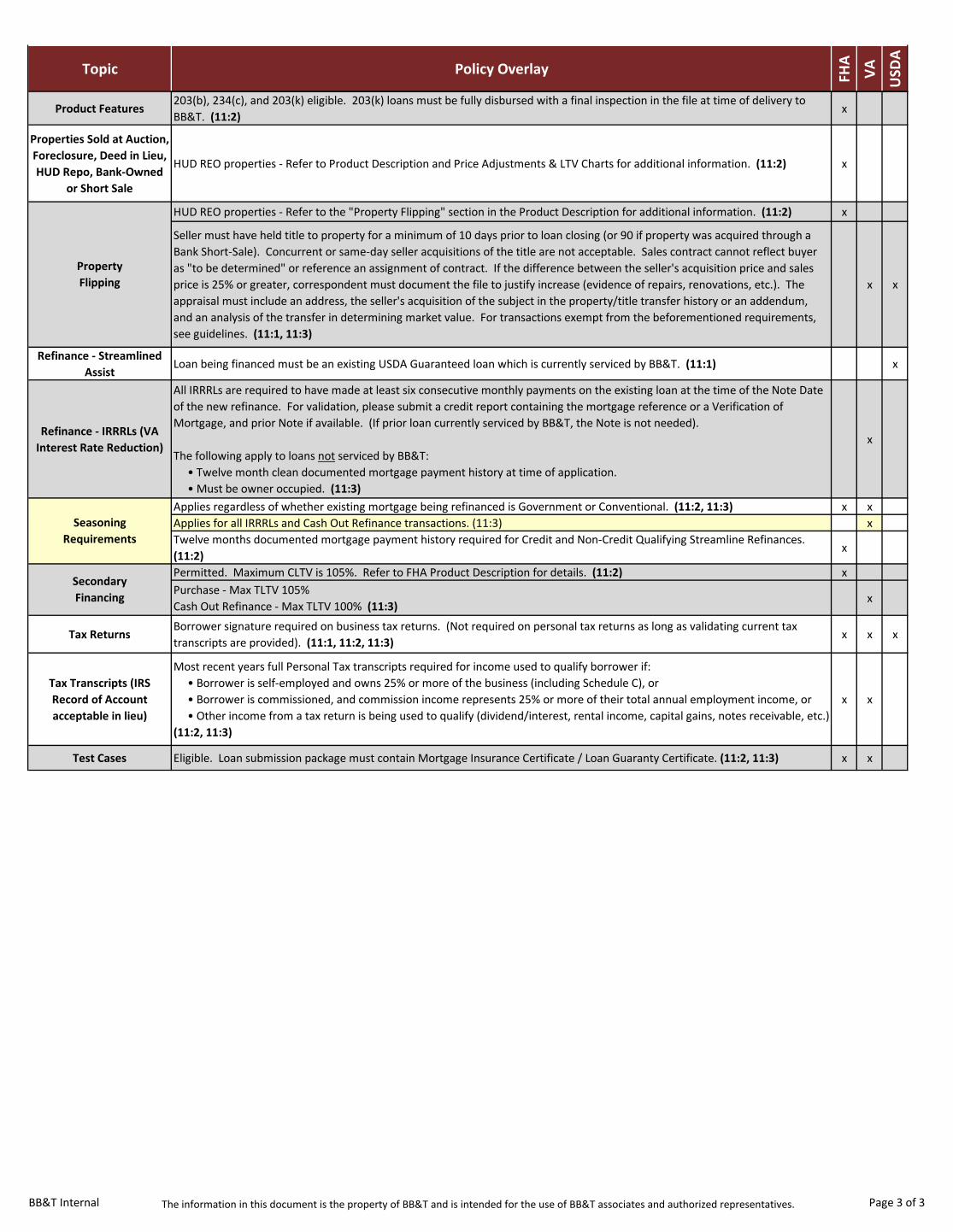

Topic Policy Overlay FHA

VA USD

A

Product Features203(b), 234(c), and 203(k) eligible. 203(k) loans must be fully disbursed with a final inspection in the file at time of delivery to BB&T. (11:2)

x

Properties Sold at Auction, Foreclosure, Deed in Lieu, HUD Repo, Bank-Owned

or Short Sale

HUD REO properties - Refer to Product Description and Price Adjustments & LTV Charts for additional information. (11:2) x

HUD REO properties - Refer to the "Property Flipping" section in the Product Description for additional information. (11:2) x

Seller must have held title to property for a minimum of 10 days prior to loan closing (or 90 if property was acquired through a Bank Short-Sale). Concurrent or same-day seller acquisitions of the title are not acceptable. Sales contract cannot reflect buyer as "to be determined" or reference an assignment of contract. If the difference between the seller's acquisition price and sales price is 25% or greater, correspondent must document the file to justify increase (evidence of repairs, renovations, etc.). The appraisal must include an address, the seller's acquisition of the subject in the property/title transfer history or an addendum, and an analysis of the transfer in determining market value. For transactions exempt from the beforementioned requirements, see guidelines. (11:1, 11:3)

x x

Refinance - Streamlined Assist

Loan being financed must be an existing USDA Guaranteed loan which is currently serviced by BB&T. (11:1) x

Refinance - IRRRLs (VA Interest Rate Reduction)

All IRRRLs are required to have made at least six consecutive monthly payments on the existing loan at the time of the Note Date of the new refinance. For validation, please submit a credit report containing the mortgage reference or a Verification of Mortgage, and prior Note if available. (If prior loan currently serviced by BB&T, the Note is not needed).

The following apply to loans not serviced by BB&T: • Twelve month clean documented mortgage payment history at time of application. • Must be owner occupied. (11:3)

x

Applies regardless of whether existing mortgage being refinanced is Government or Conventional. (11:2, 11:3) x xApplies for all IRRRLs and Cash Out Refinance transactions. (11:3) xTwelve months documented mortgage payment history required for Credit and Non-Credit Qualifying Streamline Refinances. (11:2)

x

Permitted. Maximum CLTV is 105%. Refer to FHA Product Description for details. (11:2) xPurchase - Max TLTV 105%Cash Out Refinance - Max TLTV 100% (11:3)

x

Tax ReturnsBorrower signature required on business tax returns. (Not required on personal tax returns as long as validating current tax transcripts are provided). (11:1, 11:2, 11:3)

x x x

Tax Transcripts (IRS Record of Account acceptable in lieu)

Most recent years full Personal Tax transcripts required for income used to qualify borrower if: • Borrower is self-employed and owns 25% or more of the business (including Schedule C), or • Borrower is commissioned, and commission income represents 25% or more of their total annual employment income, or • Other income from a tax return is being used to qualify (dividend/interest, rental income, capital gains, notes receivable, etc.) (11:2, 11:3)

x x

Test Cases Eligible. Loan submission package must contain Mortgage Insurance Certificate / Loan Guaranty Certificate. (11:2, 11:3) x x

Seasoning Requirements

Secondary Financing

Property Flipping