Embed Size (px)

Citation preview

© 2013, CMG Financial. All Rights Reserved. CMG Financial is a registered trade name of CMG Mortgage, Inc., NMLS #1820, 3160 Crow Canyon Rd, Ste 400, San Ramon, CA 94583. Intended for mortgage professionals only. Not for consumer distribution. Not a commitment to lend. Pricing and terms are subject to change without notice. To verify our state licenses, please visit: www.nmlsconsumeraccess.com. For information about our company, please visit us at www.cmg!.com.

THIS SELLER GUIDE IS CURRENTLY

UNDER CONSTRUCTION

Please check back again later. Thank you!

C o r r e s p o n d e n t L e n d i n g

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

A Division of CMG Mortgage, Inc., NMLS #1820

CMG Financial Correspondent Lending Guide

Welcome to CMG Financial CMG Financial, a division of CMG Mortgage, Inc. (“CMG”) is an established, privately held Mortgage Bank, headquartered in San Ramon, California. Providers of the patented All In One™ home loan, CMG Financial is widely known for responsible lending practices, industry and consumer advocacy, market innovation and operational superiority. The following are the requirements to be able to become an approved Correspondent with CMG. DISCLAIMERS: CMG is authorized to purchase closed residential mortgage loans in all states except for Louisiana and West Virginia. “CMG Financial” is a registered trade name in all states except for Connecticut, Maryland, Nevada, Ohio and South Carolina.

CMG Financial Correspondent Lending Guide Page 2

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

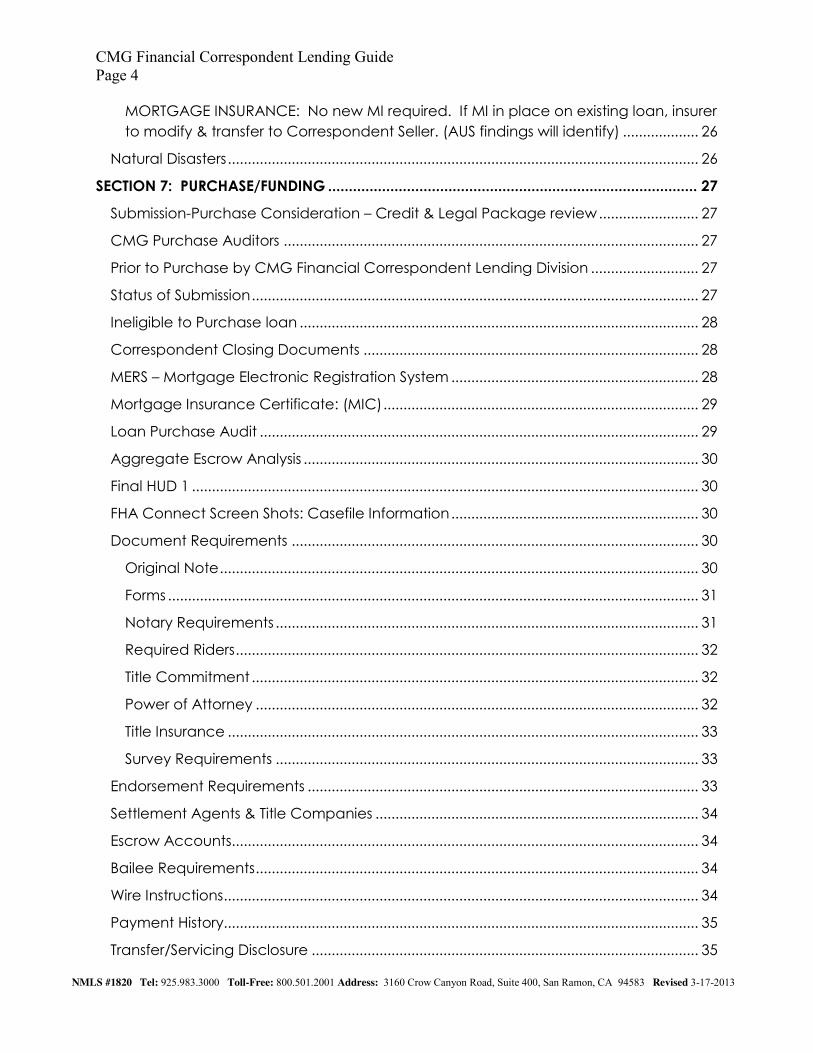

TABLE OF CONTENTS: .................................................................................................................... Page

SECTION 1: OVERVIEW ............................................................................................................ 6

Definitions ................................................................................................................................... 6

Contacts .................................................................................................................................... 6

Operating Hours ........................................................................................................................ 7

Holiday Schedule ...................................................................................................................... 7

SECTION 2: ELIGIBLE PRODUCTS .............................................................................................. 7

The CMG Correspondent Lender: .......................................................................................... 7

SECTION 3: SELLER REQUIREMENTS .......................................................................................... 8

Qualities of the CMG Financial Correspondent Seller: ........................................................ 8

Third Party Originations ............................................................................................................. 9

Regulatory Compliance .......................................................................................................... 9

Compliance by Correspondent Seller ................................................................................... 9

QC Requirements ................................................................................................................... 10

Social Security Validation ...................................................................................................... 10

Expectations ............................................................................................................................ 10

Required Notification ............................................................................................................. 11

SECTION 4: UNDERWRITING AUTHORITY AND SUBMISSION ................................................. 12

Correspondent Lender Delegation Authority ..................................................................... 12

SECTION 5: REGISTRATION AND LOCKING ........................................................................... 12

Registration .............................................................................................................................. 12

Underwriting Submission ......................................................................................................... 12

Rate Sheets .............................................................................................................................. 13

Locking ..................................................................................................................................... 13

Relocking/Expired locks ......................................................................................................... 13

Extensions on undelivered loans ........................................................................................... 13

Extensions on delivered loans ............................................................................................... 13

Cancellations .......................................................................................................................... 14

SECTION 6: LOAN ELIGIBILITY ................................................................................................ 14

FHA Programs .......................................................................................................................... 14

CMG Financial FHA Product .............................................................................................. 14

Enhancements: CMG Financial will consider for purchase ........................................ 14

CMG Financial Correspondent Lending Guide Page 3

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

FHA Streamline Refinance Transactions ........................................................................... 15

Escrow Holdbacks ............................................................................................................... 15

CMG Property/Program Restrictions – FHA Program ..................................................... 15

AVM/Electronic Value Review .......................................................................................... 16

VA Programs ............................................................................................................................ 16

CMG Financial VA Product ............................................................................................... 16

Enhancements: CMG Financial will consider for purchase ........................................ 16

VA IRRRL Refinance Transactions: ..................................................................................... 17

CMG Property/Program Restrictions – VA Program ....................................................... 17

VA Interest Rate Reduction Refinance Loan Transactions ........................................... 17

Conventional ........................................................................................................................... 18

HARP 2.0 DU Refi Plus and LP Open Access ................................................................... 18

Documentation: .................................................................................................................. 18

CORE Conventional Transactions ......................................................................................... 19

HOME Path Purchase Program ............................................................................................. 19

Multiple Financed Properties ................................................................................................. 19

Underwriting Requirements for Multiple Financed Properties ....................................... 20

Delayed Financing Exception ............................................................................................... 21

CMG Property/Program Restrictions – Conventional Program ........................................ 21

Minimum Loan Amount.......................................................................................................... 21

Geographic Restrictions ........................................................................................................ 22

Exclusionary Lists ...................................................................................................................... 22

Allowable Vesting ................................................................................................................... 22

Ownership Type ....................................................................................................................... 22

Prepayment Penalties ............................................................................................................ 22

Real Estate Taxes ..................................................................................................................... 22

Hazard Insurance: Section A ................................................................................................. 23

Hazard Insurance: Section B ................................................................................................. 24

Condominiums Hazard .......................................................................................................... 25

Mortgage Insurance ............................................................................................................... 25

Standard Mortgage Insurance (Borrower Paid – BPMI) .................................................... 26

Lender-Paid Mortgage Insurance (LPMI) ............................................................................ 26

CMG Financial Correspondent Lending Guide Page 4

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

MORTGAGE INSURANCE: No new MI required. If MI in place on existing loan, insurer to modify & transfer to Correspondent Seller. (AUS findings will identify) ................... 26

Natural Disasters ...................................................................................................................... 26

SECTION 7: PURCHASE/FUNDING ......................................................................................... 27

Submission-Purchase Consideration – Credit & Legal Package review ......................... 27

CMG Purchase Auditors ........................................................................................................ 27

Prior to Purchase by CMG Financial Correspondent Lending Division ........................... 27

Status of Submission ................................................................................................................ 27

Ineligible to Purchase loan .................................................................................................... 28

Correspondent Closing Documents .................................................................................... 28

MERS – Mortgage Electronic Registration System .............................................................. 28

Mortgage Insurance Certificate: (MIC) ............................................................................... 29

Loan Purchase Audit .............................................................................................................. 29

Aggregate Escrow Analysis ................................................................................................... 30

Final HUD 1 ............................................................................................................................... 30

FHA Connect Screen Shots: Casefile Information .............................................................. 30

Document Requirements ...................................................................................................... 30

Original Note ........................................................................................................................ 30

Forms ..................................................................................................................................... 31

Notary Requirements .......................................................................................................... 31

Required Riders .................................................................................................................... 32

Title Commitment ................................................................................................................ 32

Power of Attorney ............................................................................................................... 32

Title Insurance ...................................................................................................................... 33

Survey Requirements .......................................................................................................... 33

Endorsement Requirements .................................................................................................. 33

Settlement Agents & Title Companies ................................................................................. 34

Escrow Accounts..................................................................................................................... 34

Bailee Requirements ............................................................................................................... 34

Wire Instructions ....................................................................................................................... 34

Payment History....................................................................................................................... 35

Transfer/Servicing Disclosure ................................................................................................. 35

CMG Financial Correspondent Lending Guide Page 5

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

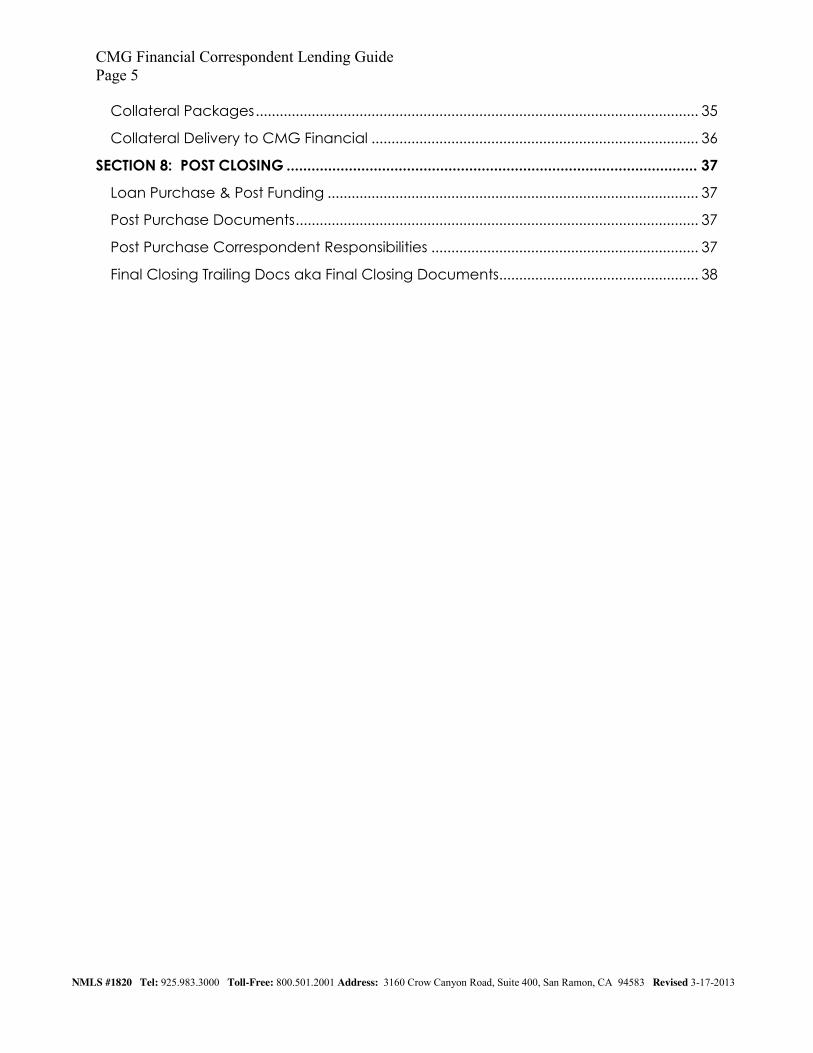

Collateral Packages ............................................................................................................... 35

Collateral Delivery to CMG Financial .................................................................................. 36

SECTION 8: POST CLOSING ................................................................................................... 37

Loan Purchase & Post Funding ............................................................................................. 37

Post Purchase Documents ..................................................................................................... 37

Post Purchase Correspondent Responsibilities ................................................................... 37

Final Closing Trailing Docs aka Final Closing Documents.................................................. 38

CMG Financial Correspondent Lending Guide Page 6

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

SECTION 1: OVERVIEW

Definitions As they appear in this document, the terms “CMG Financial” and “CMG Financial Correspondent Lending Division” refer to CMG Mortgage, Inc., dba CMG Financial (“CMG”). “Correspondent”, “Seller,” or “Correspondent Seller” is defined as the seller of a closed mortgage loan to CMG. “Correspondent Loan” is defined as mortgage loan that is made to a natural person for primarily consumer, family or household purposes, that is secured by a one- to four-family residential dwelling. Correspondent loan also contains the feature where closing documents are drawn in the name of the Correspondent, closed in the name of the Correspondent, using the Correspondent’s dedicated commercial warehouse line(s), and the closed loan is submitted for purchase consideration to CMG Financial Correspondent Lending Division by the Correspondent. The Correspondent performs of all of the following functions:

Originates mortgage loans directly through its own retail/wholesale operations;

Closes the loan in its name utilizing their warehouse line(s); and

Ships the loan to CMG for data, legal documents, compliance review, and purchase.

Contacts Corporate Headquarters: CMG Mortgage, Inc., NMLS #1820 Attn: Correspondent Lending Division 3160 Crow Canyon Road, Suite 400 San Ramon, CA 94583 Telephone: 800.501.2001 Please contact your assigned Regional Correspondent Manager for program questions. Ronald M. Harrison Director, Correspondent Lending Direct: 925.983.3206 Cell: 714.904.3500 cell Email: [email protected] Sam A. Gomaa National Correspondent Operations Manager 925.498.6680 direct Email: [email protected]

CMG Financial Correspondent Lending Guide Page 7

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

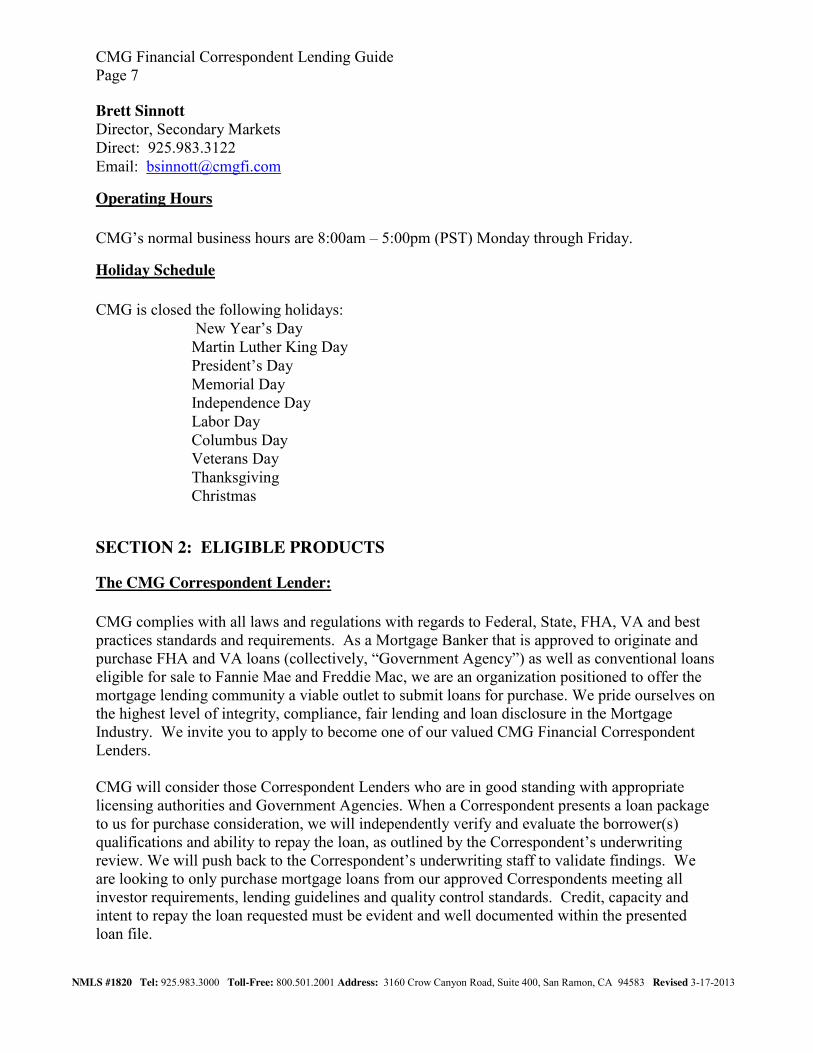

Brett Sinnott Director, Secondary Markets Direct: 925.983.3122 Email: [email protected]

Operating Hours CMG’s normal business hours are 8:00am – 5:00pm (PST) Monday through Friday.

Holiday Schedule CMG is closed the following holidays:

New Year’s Day Martin Luther King Day President’s Day Memorial Day Independence Day Labor Day Columbus Day Veterans Day Thanksgiving Christmas

SECTION 2: ELIGIBLE PRODUCTS

The CMG Correspondent Lender: CMG complies with all laws and regulations with regards to Federal, State, FHA, VA and best practices standards and requirements. As a Mortgage Banker that is approved to originate and purchase FHA and VA loans (collectively, “Government Agency”) as well as conventional loans eligible for sale to Fannie Mae and Freddie Mac, we are an organization positioned to offer the mortgage lending community a viable outlet to submit loans for purchase. We pride ourselves on the highest level of integrity, compliance, fair lending and loan disclosure in the Mortgage Industry. We invite you to apply to become one of our valued CMG Financial Correspondent Lenders. CMG will consider those Correspondent Lenders who are in good standing with appropriate licensing authorities and Government Agencies. When a Correspondent presents a loan package to us for purchase consideration, we will independently verify and evaluate the borrower(s) qualifications and ability to repay the loan, as outlined by the Correspondent’s underwriting review. We will push back to the Correspondent’s underwriting staff to validate findings. We are looking to only purchase mortgage loans from our approved Correspondents meeting all investor requirements, lending guidelines and quality control standards. Credit, capacity and intent to repay the loan requested must be evident and well documented within the presented loan file.

CMG Financial Correspondent Lending Guide Page 8

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

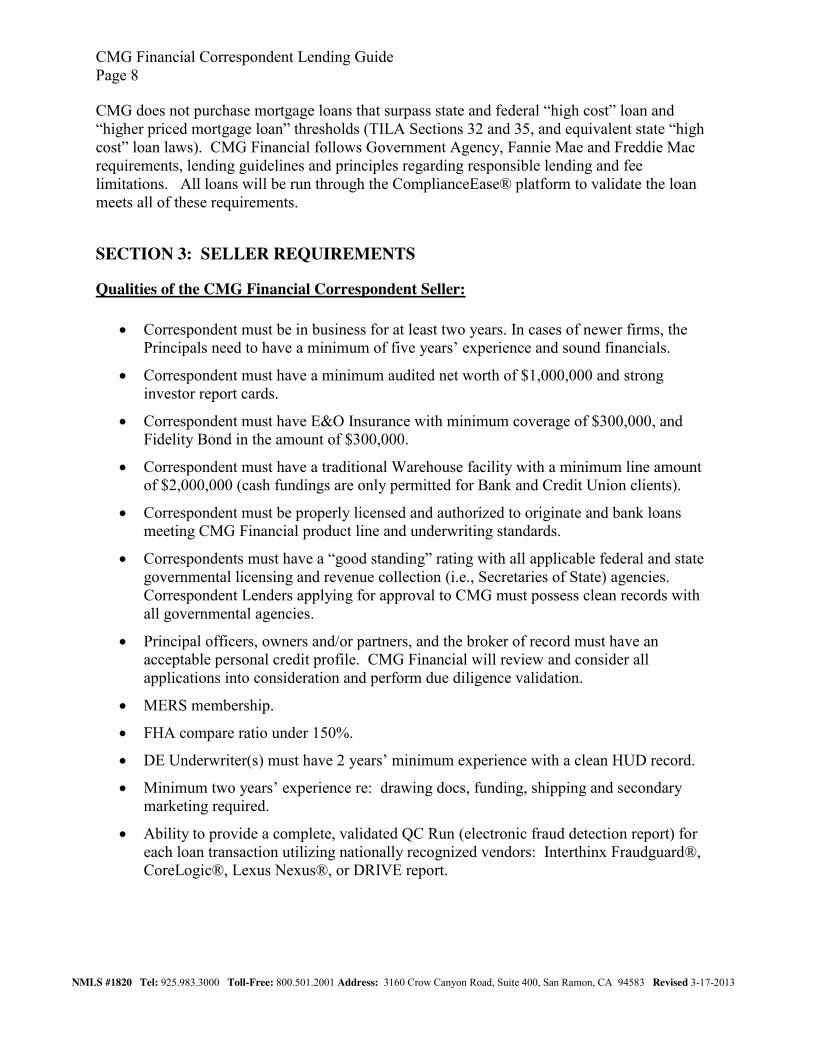

CMG does not purchase mortgage loans that surpass state and federal “high cost” loan and “higher priced mortgage loan” thresholds (TILA Sections 32 and 35, and equivalent state “high cost” loan laws). CMG Financial follows Government Agency, Fannie Mae and Freddie Mac requirements, lending guidelines and principles regarding responsible lending and fee limitations. All loans will be run through the ComplianceEase® platform to validate the loan meets all of these requirements.

SECTION 3: SELLER REQUIREMENTS

Qualities of the CMG Financial Correspondent Seller:

Correspondent must be in business for at least two years. In cases of newer firms, the Principals need to have a minimum of five years’ experience and sound financials.

Correspondent must have a minimum audited net worth of $1,000,000 and strong investor report cards.

Correspondent must have E&O Insurance with minimum coverage of $300,000, and Fidelity Bond in the amount of $300,000.

Correspondent must have a traditional Warehouse facility with a minimum line amount of $2,000,000 (cash fundings are only permitted for Bank and Credit Union clients).

Correspondent must be properly licensed and authorized to originate and bank loans meeting CMG Financial product line and underwriting standards.

Correspondents must have a “good standing” rating with all applicable federal and state governmental licensing and revenue collection (i.e., Secretaries of State) agencies. Correspondent Lenders applying for approval to CMG must possess clean records with all governmental agencies.

Principal officers, owners and/or partners, and the broker of record must have an acceptable personal credit profile. CMG Financial will review and consider all applications into consideration and perform due diligence validation.

MERS membership.

FHA compare ratio under 150%.

DE Underwriter(s) must have 2 years’ minimum experience with a clean HUD record.

Minimum two years’ experience re: drawing docs, funding, shipping and secondary marketing required.

Ability to provide a complete, validated QC Run (electronic fraud detection report) for each loan transaction utilizing nationally recognized vendors: Interthinx Fraudguard®, CoreLogic®, Lexus Nexus®, or DRIVE report.

CMG Financial Correspondent Lending Guide Page 9

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Third Party Originations

CMG does not purchase third-party originations (TPOs) without prior approval and special screening process for Correspondents and their brokers.

Regulatory Compliance You must operate your business in compliance with all federal, state and local laws and regulations. This manual is provided as information only and is not to be interpreted as legal advice. While it is our intent to always have this manual reflect the most current information, there may be times when it does not. It is your responsibility to comply with legal and regulatory requirements promulgated by all federal, state and other government entities and to be and remain current with regard to those standards.

Compliance by Correspondent Seller Any information and guidance contained in this document regarding policies and procedures to utilize while doing business with CMG Financial should in no way be construed as CMG providing the Correspondent with legal advice. For legal determination, the Correspondent should seek out independent legal opinions from qualified sources. Our Correspondent Lending Division provides helpful tools, policies, procedures and requirements that the Correspondent should follow when seeking the purchase of a closed loan.

Correspondent must report HMDA LAR data as required by federal HMDA/Regulation C.

For loans to be considered eligible for purchase: Correspondent must abide by RESPA/Regulation X which includes, but is not limited to: properly disclosed Good Faith Estimate, re-disclosure (when necessary and applicable), and correct association of GFE to COC and final HUD-I Settlement Statement.

Correspondent must adhere to their own current requirements as detailed in the Correspondent’s Quality Control Policy provided to CMG within the application process.

Correspondent is required to close loans in compliance with their own specific licensing regulations.

Correspondent must adhere to current requirements as mandated by all Federal, State, Municipal Agencies, as well as appropriate transaction requirements of Fannie Mae, Freddie Mac, FHA, and/or VA.

Correspondent must keep CMG abreast of any company licensing changes that may affect the purchase of a particular closed loan prior to CMG purchasing.

CMG Financial Correspondent Lending Guide Page 10

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

QC Requirements IRS 4506T Tax Transcripts Validation document. Validation of tax years per AUS requirements of income verification required.

Signed 4506t is required with credit package and as a required document with closing documents.

Acceptable results are required on all borrower income with the exception of FHA Streamline Refinance for loan purchase eligibility.

Regarding non self-employed borrowers, in which correspondent provides required paystubs and W-2’s, 4506t results for W-2 earnings is acceptable.

Correspondent must adhere to AUS findings for number of years verification required however all borrower income must be verified by the results of the 4506T.

Correspondent may wish to order a “Record of Account” from the IRS if the borrower has filed amended returns. It takes the IRS approximately 6-8 weeks to update their system with any recent account activity and have a transcript available regarding amended return detail.

Social Security Validation A Direct SSN validation is often used in conjunction with the credit report and borrower documentation. May also show on the electronic QC run provided by Correspondent.

Expectations Our goal is to establish and maintain a productive and profitable long-term relationship with you. We have a strong commitment to customer service and would like to hear from you if your expectations are not met. Concerns or suggestions can be communicated to [email protected]. We value certain things in a relationship and will be tracking your performance in the following areas:

Volume;

Conversion or pull-through ratio;

Adherence to CMG’s Delivery and Purchase procedures;

Quality of underwriting submissions;

Loan performance (EPO and EPD).

CMG Financial Correspondent Lending Guide Page 11

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Required Notification You must notify us in writing within 30 days of any change in:

Ownership (or percentage of ownership);

Financial condition;

Warehouse bank or warehouse line;

Company ownership, Board of Directors composition, and Executive/Senior Management;

Opening/closing of licensed locations doing business with CMG;

Contact information (Address, phone numbers, fax numbers and email addresses). You must immediately notify us in writing if your company or any owner, employee, agent or officer in your company:

Fails to maintain any applicable license or registration in each jurisdiction governs your company’s activities;

Becomes subject to any enforcement and/or investigative proceeding by any licensing or regulatory authority or agency;

Is named as a party or becomes involved in any material litigation;

Is placed on Fannie Mae’s or Freddie Mac’s exclusionary list, HUD’s limited denial of participation or any other agency, or any private investor’s exclusionary list.

You must also immediately notify us in writing if:

Your company and/or any of its principal directors or owners becomes the subject of any bankruptcy or has incurred or is likely to incur a material, adverse change in its/their financial condition.

There are any investigative actions, proceedings or lawsuits that relate to or concern your agreement with us or any mortgage loans subject to that agreement.

There is an investigation, proceeding, litigation or other event which, if resolved adversely, could have a material adverse effect on your ability to originate loans or perform your obligations under your agreement with us.

If there is a change in authorized signatures, you should submit a revised Certificate of Signatures form as soon as possible in order to avoid purchase delays.

You may submit documentation regarding changes by email to the following: Email: [email protected]

CMG Financial Correspondent Lending Guide Page 12

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

SECTION 4: UNDERWRITING AUTHORITY AND SUBMISSION

Correspondent Lender Delegation Authority FHA-approved Full Eagle DE Lenders who meet CMG requirements are fully delegated to underwrite loans to CMG credit and eligibility standards. The Correspondent’s DE or approved staff (i.e., for ZFHA transactions) will be held solely responsible for the file diligence and integrity, as per HUD Requirements. The CMG FHA pre-purchase review is to assist those Correspondents in which their respective warehouse lines require a pre-review. CMG is not issuing out a credit or property approval, but rather a set of Purchase conditions we will require prior to the purchase of the FHA loan. For occasion in which the transaction is not an acceptable FHA transaction, CMG will release a notification: “Unable to Purchase.” Communication will be transmitted directly to the Correspondent.

If Correspondent chooses to submit a “credit only” review prior to drawing loan documents, an underwriting fee of $150.00 will be assessed for the FHA product.

SECTION 5: REGISTRATION AND LOCKING

Registration Lender uploads 3.2 file online to register loan with CMG Correspondent Lending.

https://wt.cmgmortgage.com/DataTracWeb/Logon

Underwriting Submission All Correspondent loans must be electronically submitted through www.CMGfi.com/correspondent website access. Please adhere to these CMG Submission guidelines:

Submission to include complete 3.2 uploaded Fannie Mae file with all appropriate application information completed and insure all borrowers part of the transaction are included.

Submission to include DU Approve/Eligible or Freddie Mac “Accept” findings. Provide complete required findings documentation included within the file. Submissions to be stacked in proper order. CMG will not pre-review “TBD purchase files”. Provide documentation to clear all AUS “Red Flag Alerts”. “Piecemeal” conditions submissions are strongly discouraged.

CMG Financial Correspondent Lending Guide Page 13

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Rate Sheets Rate sheets are distributed daily by 8:00 a.m. Pacific Time. Contact your Regional Correspondent Manager to be added to the daily distribution list. Rates are subject to change without advance notice.

Locking

Approved Correspondent may lock a loan transaction with CMG via Webtrac® at any time.

Forward Locks are allowed.

Relocking/Expired locks

Relock at worse case price. Original and Relock term must match. Relock > 30 days from expiration date: use current market price.

Extensions on undelivered loans

If the current market improves a free 15 day extension can be requested to allow for loan delivery.

Anything past 15 days will be relocked at worse case pricing for the original lock term requested plus a fee of .250.

If the current market is worse, 15 days will cost .250. Any delivery requiring more than 15 days will be relocked at worse case pricing plus a fee of 0.250

Extensions on delivered loans

Delivery loans are defined as loans in which the entire credit and legal package received by CMG.

Legal package must be delivered to CMG for review, no later than 12 pm (PST) on the day prior to the lock expiration date.

Credit and Legal Package received prior to lock expiration date: 10 day grace period will be granted.

If conditions are not cleared within the 10 day grace period, the loan will be extended automatically at a cost of .250 for 10 days until the loan is purchased.

Maximum number of extensions is two (2). Contact information: For relocks or extensions: [email protected] For general questions: [email protected]

CMG Financial Correspondent Lending Guide Page 14

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Cancellations You must notify us immediately if a loan/lock is cancelled.

To cancel a loan/lock email: [email protected]

SECTION 6: LOAN ELIGIBILITY

FHA Programs CMG follows the standards, requirements, and guidelines released and updated periodically by HUD. We look to the expertise and diligence by our Correspondent Lenders to keep informed of all changes to the guidelines, requirements, standards. Any changes to our current list of restrictions will be announced by CMG.

CMG Financial FHA Product The following outlines the general product credit and eligibility guidelines. Sellers are again reminded they must follow the applicable underwriting and collateral guidelines set forth by HUD.

FHA Forward Purchase Programs.

FHA Forward Refinance Programs.

FHA Streamline without an appraisal – as defined within the HUD Handbook 4155.1 and ML2011-11/ subsequent HUD releases.

FHA Streamlines without an appraisal- Non-Owner occupied transactions.

Enhancements: CMG Financial will consider for purchase 600 minimum mid Credit Score – full credit qualifying transactions

High Balance transactions: 620 minimum mid credit score

< 91 Day Flip as defined: 24 CFR 203.37 (a) (b) 2- follow HUD waiver requirements

Non-occupant co-borrower transaction allowable

DU scorecard or LP accept – Follow AUS findings

Case by case manual underwrites with extenuating circumstances allowable: Must meet minimum HUD standards/guidelines/ requirements

HUD Reo transactions $100 down with repair escrows (Seller provides HUD 92300)

Modifications/short equity/short sales allowable per HUD guidelines/requirements

HUD EEM : Energy Efficient Program acceptable

DAP programs acceptable per HUD standards/ guidelines/ requirements

Good Neighbor Next Door program accommodated

CMG Financial Correspondent Lending Guide Page 15

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

FHA Streamline Refinance Transactions

If the Correspondent is involved in a promised future refinance transaction with the Borrower, Correspondent may not submit a loan for purchase by CMG.

FHA Streamlines allowable - pay off any Seller Servicer

600 minimum mid Credit Score – utilizing full credit report

Mortgage Credit only acceptable: 620 minimum mid credit score:

Non Owner occupied (Investment) streamlines - 620 minimum mid credit score

Verbal VOE required

Allows the addition of a Borrowing spouse with no score. Price as 600 credit score transaction

Removal of an original obligor to the FHA note requires full documentation and evidence of min 12 months payments made by applicant party

High Balance streamline refinance transaction requires minimum 620 mid credit score full tri merge

Condo streamline does not require current condo approval. Per HUD – provide evidence project has not been rejected nor withdrawn

Escrow Holdbacks HUD REO property forward transactions, which include an Escrow Holdback, are eligible for purchase by CMG Financial including Escrow holdbacks. Transaction must meet HUD requirements and standards. Correspondent must be familiar with accommodating said transactions. Purchase file must contain a copy of the fully completed HUD forms 92300. The CIR 92051 must be provided within 45 days of Correspondent closing transaction. Completion of the transaction is the responsibility of the Correspondent. CMG Financial will monitor the Correspondent to insure the documentation is provided, or CMG Financial may remove the Correspondent’s capability to accommodate the transactions in the future without all pieces completed prior to CMG Financial purchase.

CMG Property/Program Restrictions – FHA Program The following property types/programs are not permitted:

Cooperatives Manufactured / Mobile Homes Any property type excluded by HUD requirements 203K Adjustable Cooperatives Texas Cash Out Reverse Mortgages (HECM) Title 1 loans

CMG Financial Correspondent Lending Guide Page 16

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

AVM/Electronic Value Review The responsibility of supporting value is placed by HUD upon the Seller’s Direct Endorsement Underwriter reviewing the appraisal. The executed HUD 92800.5b conditional Commitment must be provided for every loan in which an appraisal is required. Just as HUD looks to the DE Underwriter to support value, as will CMG. While neither an AVM, nor an additional third party independent validation of the appraisal is required for a HUD loan purchase by CMG, we do reserve the right to request additional support on any transaction. If required, Sellers may provide an AVM, desk review or field review from any vendor.

VA Programs CMG follows the standards, requirements, and guidelines released and updated periodically by the Veterans Administration. We look to the expertise and diligence by our Correspondent Lenders to keep informed of all changes to the guidelines, requirements, standards. Any changes to our current list of restrictions will be announced by CMG.

CMG Financial VA Product The following outlines the general product credit and eligibility guidelines. Sellers are again reminded they must follow the applicable underwriting and collateral guidelines set forth by VA.

VA Forward Purchase Programs.

VA Refinance Programs.

VA IRRRL Streamlines

VA IRREL Streamlines Non/Owner

Enhancements: CMG Financial will consider for purchase

Minimum mid credit score 600

Loan Balance > $417,000: Minimum mid credit score 620

AUS Approve/Eligible or LP Accept -Follow AUS findings

Case by case manual underwrites with extenuating circumstances allowable:

Must meet minimum VA standards/ guidelines/ requirements

Modifications/ short equity/short sales allowable per VA guidelines/ requirements

CMG Financial Correspondent Lending Guide Page 17

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

VA IRRRL Refinance Transactions:

Pay off any Seller Servicer

600 minimum mid/low Credit Score

Mortgage Credit Only acceptable: 620 minimum mid credit score

High Balance transactions > $417,000: 620 minimum mid credit score

Non Owner occupied (investment) IRRRL- 620 minimum mid credit score

Verbal VOE required on all non-credit qualifying IRRRL transactions

AVM or Conventional FNMA 2055 with comps to validate value

VA does not require Condo approval

Any IRRRL submission not qualifying under VA IRRRL requirements will be considered under VA Refinance fully qualifying transaction.

VA Credit Qualify Refinance Programs – as defined within the VA Lenders Handbook and subsequent VA releases.

CMG Property/Program Restrictions – VA Program The following property types are not permitted:

Cooperatives

Manufactured / Mobile Homes

Any property type excluded by VA requirements

Leasehold Properties

Texas Cash Out

VA Interest Rate Reduction Refinance Loan Transactions

If the Correspondent is involved in a promised future refinance transaction with the Borrower, Correspondent may not submit a loan for purchase by CMG.

CMG Financial Correspondent Lending Guide Page 18

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Conventional Conventional loans submitted for purchase consideration must comply with the Fannie Mae Seller Guide and any applicable subsequent FNMA directives/ updates. CMG will consider for purchase the following:

HARP 2.0 DU Refi Plus and LP Open Access

Documentation: DU AUS: Approve/Eligible, EAI/eligible, EA2/Eligible, or EA3/ Eligible LP AUS: Accept findings required.

Provide documentation to meet all findings

Loan Amount: Conforming and High Balance Conforming LTV/CLTV/HCLTV: UNLIMITED Credit: NO MINIMUM CREDIT SCORE Mortgage History: - MUST BE CURRENT. Additionally for LP: 0 x 30 days late past 6

months, 1 x 30 past 7-12 months BK or Foreclosure : Standard Fannie Mae/Freddie Mac guidelines apply Occupancy: ALL including primary residence, 2nd homes, investment, 1-4 units Property Types: All including Condos & PUDs

RE: Freddie Mac CA Condos: For California condos and open access loans, provided project earthquake insurance or complete form 465S to determine FHLMC earthquake insurance waiver eligibility. (CMG WILL REQUEST ) Note: price Exception required if FHLMC does not grant waiver request. Excludes: Co-ops, condotels and manufactured homes. Properties recently/currently listed OK with cancelled listing

APPRAISAL: NOT required with DU PIW (property inspection waiver) OR o LP HVE (HOME VALUATION EXPLORER) waiver o Note: $75 (PIW) Appraisal Waiver Fee WAIVED unless seller charged as per

HUD1 o *DU EA1, EA2, and EA3 requires DU Appraisal Waiver

PROPERTIES FINANCED: DU: No Limit

o FHLMC: No Limit o SUBORDINATE LIENS: MUST re-subordinate; CAN NOT be paid off through

loan proceeds. o NO new subordinate financing o Provide Copy of Note o Provide copy of executed/certified Note Subordination o Follow AUS findings

CMG Financial Correspondent Lending Guide Page 19

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

CASH OUT: LIMITED TO $250 back to borrower; loan proceeds can cover recurring

and non-recurring closing costs BORROWER BENEFIT: MUST include one or more of the following:

Provide certification: o Lower rate and/or P&I payment o Move from ARM to Fixed Rate (more stable product) o Move from Interest Only to Fully Amortized o Shorten term, i.e.: 30 yr. to 25 yr., 20 yr. or 15 yr.

NET TANGIBLE BENEFIT Form required

AUS Requirement: Provide AUS reflecting Lending Institution :

o Seller or CMG

Prior to CMG Purchase, all information reflected as per final submitted AUS must match submitted final 1008 Transmittal and final 1003 Application.

Ineligible Property Types:

o Condotels o Leasehold properties o Manufactured Homes

CORE Conventional Transactions Standard Fannie Mae/Freddie Mac guideline adherence applies. CMG will accommodate Non-Owner Occupied purchase consideration for the highly qualified investor who owns 5-10 properties including subject transaction.

HOME Path Purchase Program Home Path renovation transactions not available for purchase by CMG

Multiple Financed Properties 5 to 10 Financed Properties Non Owner or 2nd HM Transaction Type Number of

Units Maximum LTV/CLTV/HCLTV Ratio

Minimum Credit Score

Second Home or Investment Property

Purchase Limited Cash-Out

1 unit Loans subject to general loan limits

720

CMG Financial Correspondent Lending Guide Page 20

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

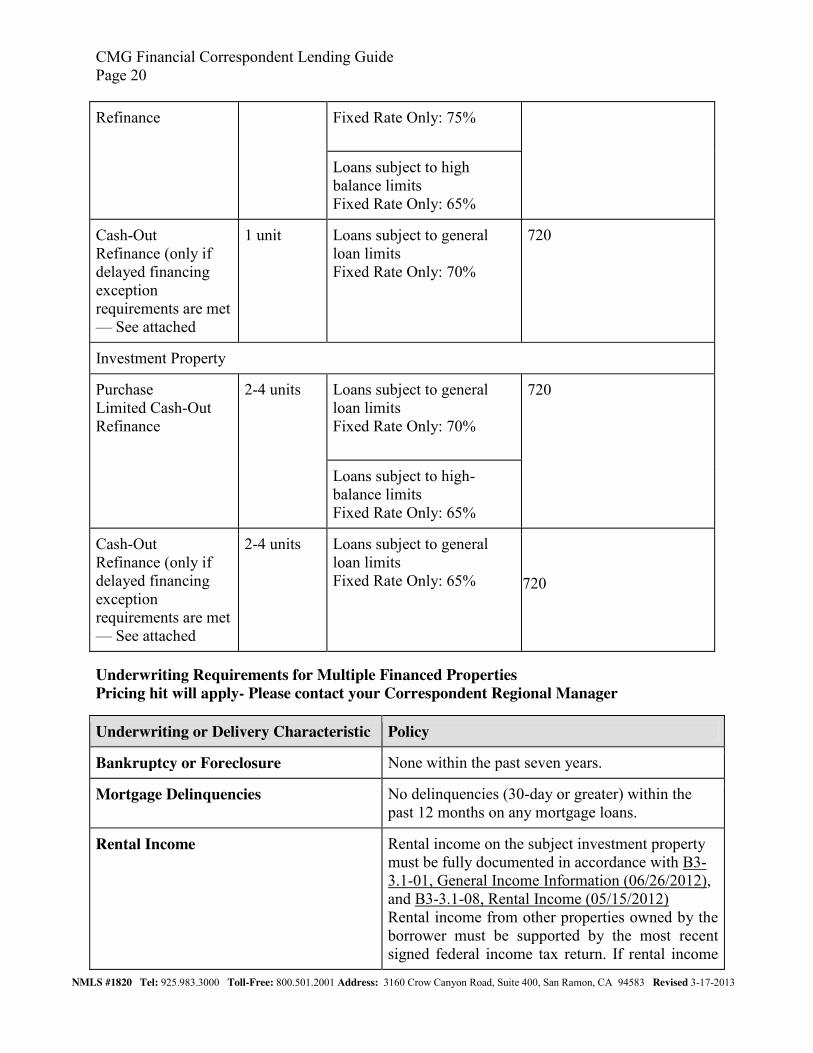

Refinance Fixed Rate Only: 75%

Loans subject to high balance limits Fixed Rate Only: 65%

Cash-Out Refinance (only if delayed financing exception requirements are met — See attached

1 unit Loans subject to general loan limits Fixed Rate Only: 70%

720

Investment Property

Purchase Limited Cash-Out Refinance

2-4 units Loans subject to general loan limits Fixed Rate Only: 70%

720

Loans subject to high- balance limits Fixed Rate Only: 65%

Cash-Out Refinance (only if delayed financing exception requirements are met — See attached

2-4 units Loans subject to general loan limits Fixed Rate Only: 65% 720

Underwriting Requirements for Multiple Financed Properties Pricing hit will apply- Please contact your Correspondent Regional Manager

Underwriting or Delivery Characteristic Policy

Bankruptcy or Foreclosure None within the past seven years.

Mortgage Delinquencies No delinquencies (30-day or greater) within the past 12 months on any mortgage loans.

Rental Income Rental income on the subject investment property must be fully documented in accordance with B3-3.1-01, General Income Information (06/26/2012), and B3-3.1-08, Rental Income (05/15/2012) Rental income from other properties owned by the borrower must be supported by the most recent signed federal income tax return. If rental income

CMG Financial Correspondent Lending Guide Page 21

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

has not yet been reported on tax returns because the properties were acquired subsequent to the last tax filing, leases may be used to document rental income.

Minimum Reserve Requirements

6 months PITI for each second home or investment property

Delayed Financing Exception

Borrowers who purchased the subject property within the past six months are eligible for a cash-out refinance if all of the following requirements are met:

The new loan amount can be no more than the actual documented amount of the borrower's initial investment in purchasing the property plus the financing of closing costs, prepaid fees, and points (subject to the maximum LTV/CLTV/HCLTV ratios for the transaction).

The purchase transaction was an arms-length transaction.

The transaction is documented by the HUD-1, which confirms that no mortgage financing was used to obtain the subject property. A recorded trustee’s deed (or similar alternative) confirming the amount paid by the grantee to trustee may be substituted for a HUD-1 if a HUD-1 was not provided to the purchaser at time of sale.

The sources of funds for the purchase transaction are documented (ie: bank statements, personal loan documents, HELOC on another property).

All other cash-out refinance eligibility requirements are met and cash-out pricing is applied.

Note: The preliminary title search or report must not reflect any existing liens on the subject property.

CMG Property/Program Restrictions – Conventional Program The following property types are not permitted:

Manufactured Homes/Mobile Homes

Cooperative properties

Texas Cash out 50(a)(6)

Leasehold properties

Minimum Loan Amount $50,000 minimum loan amount on all products.

CMG Financial Correspondent Lending Guide Page 22

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Geographic Restrictions CMG will not accommodate the purchase of loans located in the following states:

Louisiana West Virginia

Any other geographic restrictions as outlined within this Manual continue to apply.

Exclusionary Lists CMG Financial does not publish a list of excluded parties. Check LDP, GSA lists regularly. CMG Financial reserves the right to exclude a closing agent at any time during a transaction.

Allowable Vesting Borrowers may hold title individually, as joint tenants, as tenants in common or as an Inter Vivos Trust. (Meeting HUD Requirements) Title may not be held in any of the following: Corporation, Partnership, or Real Estate syndication

Ownership Type

Fee Simple

Prepayment Penalties Not allowed, except as defined as acceptable by HUD.

Real Estate Taxes Delinquent taxes must be paid before or at closing. If taxes are due within 60 days of the loan closing, the tax installment must be paid at closing (with evidence of payment included in the purchase package). Any special lump sum assessments that are part of the tax bill must be paid in full.

In the property is located in an area where homeowners are required to complete a homestead exemption form for reduced taxes, the borrower must be informed of this at closing.

CMG Financial Correspondent Lending Guide Page 23

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Hazard Insurance: Section A Each borrower has the right to select his or her own insurance carrier to provide hazard insurance for the secured property, provided that the insurance policy and coverage meet CMG’s requirements. The Correspondent must ensure that the insurance carrier, policy, and coverage meet CMG’s requirements. In some cases, CMG may require additional coverage or consider coverage that differs from these requirements.

Unless CMG has approved alternative arrangements in advance, the hazard insurance policy for a property securing any first mortgage – including blanket policies for condos, co-ops, and PUDs – must be written by a carrier that meets the following rating requirements. The carrier only needs to meet only one of the following rating categories, even if it is rated by more than one agency:

Carriers rated by the A.M. Best Company, Inc. must have either: o a “B” or better Financial Strength Rating in Best’s Insurance Reports or o an “A” or better Financial Strength Rating and a Financial Size Category of “VIII” or

greater in Best’s Insurance Reports Non-US Edition.

Carriers providing coverage for co-op projects must have a general policyholder’s rating of “A” and a Financial Size Category of “V” in Best’s Insurance Reports.

Carriers rated by Demotech, Inc. must have an “A” or better rating in Demotech’s Hazard Insurance Financial Stability Ratings.

Carriers rated by Standard and Poor’s must have a “BBB” or better Insurer Financial Strength Rating in Standard and Poor’s Ratings Direct Insurance Service.

Policies underwritten by a state’s Fair Access to Insurance Requirements (FAIR) plan, if it is the only coverage that can be obtained;

Policies obtained through state insurance plans – such as the Hawaii Property Insurance Association (HPIA), Florida’s Citizens Property Insurance Corporation, or other state-mandated windstorm and beach erosion insurance pools – if that is the only coverage that is available; and

A separate hurricane insurance policy issued by the Hawaiian Hurricane Relief Fund (for properties in Hawaii), as long as the companion non-catastrophic fire and extended coverage (or homeowner’s) policy is obtained from a hazard insurer that satisfies CMG’s rating criteria.

The Mortgagee Clause on Hazard Insurance Transfer Letter must read:

CMG Mortgage, Inc., dba CMG Financial, ISAOA 3160 Crow Canyon Road, Suite 400 San Ramon, CA 94583

CMG Financial Correspondent Lending Guide Page 24

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Hazard Insurance: Section B The Insurance Company issuing the policy must meet Fannie Mae guidelines. The insurance company must be authorized by law or licensed by the jurisdiction to transact business within the state where the subject property is located. The mortgaged property and all improvements thereon are insured against loss by fire and other such hazards as are customary in the area where the mortgaged property is located. Such coverage shall contain fire and hazard insurance policy with extended coverage. The following is a review of some of the requirements. The coverage under such policy shall be at least equal to the greater of the outstanding principal balance of the mortgage loan, 80% of the insurable value of the improvements as long as that value equals the replacement cost of the improvements with a replacement cost guarantee endorsement, or an amount sufficient to prevent the borrower or loss payee from becoming a coinsurer (however, under no circumstances shall the amount of insurance required exceed that amount allowed by law). Hazard insurance policies that include optional coverage that is not required by CMG are acceptable, provided that CMG is not obligated to renew any part of the coverage that they do not require. At the time of Closing Package submission, the Seller must provide either a hazard insurance binder with a paid receipt for one full year’s premium paying in advance, or the final hazard insurance policy evidencing coverage is paid in full or no payment is due. Refinance transactions do not need to be paid for one full year but the next premium due date may not occur for at least 90 days from the date of closing. Upon purchase the Correspondent is required to send a change of loss payee to the insurance company. The Correspondent must be prepared to provide evidence the request was sent to insurance company if required. An updated Hazard Insurance policy listing CMG Mortgage, Inc., dba CMG Financial, its successors and or assigns must be received within 90 days of purchase. The Mortgagee Clause must read:

CMG Mortgage, Inc., dba CMG Financial ISAOA 3160 Crow Canyon Rd, Suite 400 San Ramon, CA 94583

CMG Financial Correspondent Lending Guide Page 25

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Loans purchased by CMG located in the following states:

Connecticut Maryland Nevada Ohio South Carolina

Require the loss payee change to reflect:

CMG Mortgage, Inc. ISAOA 3160 Crow Canyon Rd, Suite 400 San Ramon, CA 94583

Condominiums and attached PUDs require a master or blanket policy covering the project, and a certificate of insurance for each individual unit secured by the loan sold to CMG Financial. Contents only HO-‐6 policies for at least 20% of the value of the property must be obtained by borrower or evidenced in master hazard policy for project and be paid through escrow or collected with impounds if required. PUD units covered under the project’s blanket policy must be allowed in the homeowner’s association documents and under the blanket insurance policy. The HOA Hazard Insurance policy must contain the borrowers name and unit. In addition, the homeowner association must maintain a policy that covers the common areas, fixtures, equipment, personal property, and supplies of the project. Premiums with respect to such policies should be considered a common expense of the related project.

Condominiums Hazard

The Certificate of Insurance policy must contain the borrower name and unit. An individual hazard insurance policy is not required for a condominium unit. Seller must verify that coverage of $1,000,000 is in force for the entire project before the mortgage loan is delivered to CMG Financial.

For attached PUDs and condominiums, the amount of hazard insurance coverage must be

at least equal to 100% of the insurable replacement costs of the project improvements, including individual units. A hazard insurance policy that includes a guaranteed replacement cost endorsement or a replacement cost endorsement satisfies.

Mortgage Insurance Mortgage Insurance (MI) is required for all conventional loans with loan-to-value ratios exceeding 80%. Seller may use MI companies, which are listed below as approved MI companies. Coverage must meet current CMG Financial Program Guidelines in addition to Fannie Mae/Freddie Mac requirements.

CMG Financial Correspondent Lending Guide Page 26

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Standard Mortgage Insurance (Borrower Paid – BPMI)

Only MI companies allowed are MGIC, Radian, PMI, and Genworth. Triad allowable for DU refi plus only.

Mortgage Insurance guidelines can change at any time;; it is therefore the underwriter’s responsibility to check the applicable Mortgage Insurance Underwriting Guidelines online and order the MI Cert at the time of underwriting and prior to sending out an approval.

MI cert must be transferred to Correspondent Seller and must document close of escrow date.

Lender-Paid Mortgage Insurance (LPMI)

Requires single premium or transfer to borrower paid MI. Any outstanding balance must be paid in full.(Cannot be rolled into the loan amount)

MORTGAGE INSURANCE: No new MI required. If MI in place on existing loan, insurer to modify & transfer to Correspondent Seller. (AUS findings will identify)

HARP loans with MI Dropped: If the AUS approval shows MI required you must provide

BOTH letters listed below for review: o Letter from MI Company stating MI no longer required and why the MI was

dropped o Letter from current servicing Company stating MI is no longer required and why

the MI was dropped o Requires Senior Management review

Natural Disasters When natural disasters occur (i.e., hurricanes, tropical storms, tornadoes, wildfires) steps must be taken to assure that the “security” on each loan is protected. A re-inspection or inspection will be required on all properties located in the Federally Declared Disaster Areas if the value of the property was determined prior to the date of the natural disaster. These requirements apply to all loans regardless of processing style or appraisal requirements.

CMG Financial Correspondent Lending Guide Page 27

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

SECTION 7: PURCHASE/FUNDING

Submission-Purchase Consideration – Credit & Legal Package review

Correspondent Loans must be fully processed and closed prior to submission to CMG for purchase consideration.

Correspondent registers and locks loan via CMGfi website.

Correspondent submits loan for purchase consideration via CMGfi website.

CMG Correspondent Lending Division Audit review.

Correspondent submits evidence of active collateral at Texas Capital Bank, along with validation of collateral pieces, OR submits the endorsed original Note (or note and executed Allonge), along with the appropriate Bailee letter.

CMG Purchase Auditors Review Legal Documents

Perform HUD –GFE/TIL Review

Run Compliance Ease

Set up loan for purchase

Prior to Purchase by CMG Financial Correspondent Lending Division

MERS transfer to Seller must be provided..

Evidence MIP has been paid to HUD must be provided by Seller.

Collateral pieces must be complete and correct.

Any requirements regarding Principal Reduction requirements, Servicing History, etc. must be complete and acceptable to CMG.

Status of Submission CMG will not suspend a Correspondent Loan submitted for purchase. The status reflected to the Correspondent will appear as U/W Approved or Denied. If the loan is denied, CMG will allow a maximum of 30 days to provide additional documentation for a re-look analysis. If there is no activity on a file declined for purchase, the process must begin again if the Correspondent wishes to resubmit for purchase consideration. If CMG is in receipt of the original collateral (Note), the note endorsement will be cancelled, and the Note returned to the Correspondent’s Warehouse Bank (or it’s Document Custodian).

CMG Financial Correspondent Lending Guide Page 28

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Ineligible to Purchase loan

If at any time after a Correspondent Loan has been submitted for CMG purchase review, the status is changed to “ineligible for purchase or declined for purchase” the Correspondent will be provided a notification regarding the change.

If a loan is denied based on information derived from the consumer credit report, the Correspondent is required to send the Credit Denial Disclosure and it must contain the contact information of the agency that provided such information used in the decision

ECOA/Regulation B Credit Denial Disclosures are required to be delivered to the applicant(s) in a timely manner – within thirty (30 calendar days from the date the loan application is declared to be “complete” by the Correspondent.

The term “complete application” is defined as a loan application inclusive of all documentation required in making the credit decision.

NOTE: The Correspondent Lending Division will conduct periodic audits to ensure Correspondent’s compliance with these procedures.

Correspondent Closing Documents Correspondent will deliver complete executed instruments necessary to convey all rights, title interests in and to each loan, and all documents evidencing and insuring each loan as is required. All taxes and governmental assessments that became due and owing prior to the closing date with respect to the mortgage property must be evidenced previously paid- including, but not limited to: Property taxes, hazard insurance premiums, flood insurance premiums, etc.

All correspondent closing documents must meet requirements as set forth in this guide and our program guidelines.

Per Diem interest to be based on 365 days per year for FHA.

FHA late charge of 4.00% as per FHA.

Loan documents must reflect Correspondent loan number.

Loan documents must reflect MERS registered MIN number.

MERS – Mortgage Electronic Registration System The correspondent will maintain an active account with MERS and execute all closing documents with a valid MIN number. The Mortgage Instrument must contain MIN (mortgage Identification number) by registering the loan in the MERS System.

CMG will purchase the loan once the Correspondent has registered the loan in the MERS System.

The beneficial and servicing rights to the loan must be transferred within the MERS

system to CMG within one days of purchase:

CMG Financial Correspondent Lending Guide Page 29

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

CMG Financial Originator ID #1000724. The website evidence of the transfer is to be uploaded to the CMGfi.com/correspondent website for the appropriate loan.

Mortgage Insurance Certificate: (MIC) Correspondent Responsibility. MIC certificates are part of post-closing requirements. Maximum 60 days after purchase by CMG. Mortgage Insurance Transfer letter is required prior to purchase. The certificate must reflect the close of escrow date and the sellers name as the servicing company. **Correspondent must register Mortgagee Record Change with HUD within 15 days of CMG’s purchase of loan. CMG Financial HUD # 78442.

Loan Purchase Audit CMG will complete a review of the closing document to ensure Federal and State specific documents are compliant. Review includes, but not limited to:

TILA

APR accuracy

Section 32, prepays and other Federal and State specific Laws

CMG will run compliance Ease prior to purchase of all loans

Truth-‐In-‐Lending (Reg. Z)

The closing document review will include:

Final Truth-‐In-‐Lending Disclosure (“TIL review for proper and accurate disclosure of the finance charge and annual percentage rate.”)

Correspondent must ensure Tolerance levels are met.

Acceptable = no more than $100 understated tolerance.

The Finance charge is understated by no more than $100 OR the APR is understated by .125% or less. Note: Both can overstate.

The warehouse lender information at loan closing must match the data most recently supplied by Correspondent. CMG validates wire authorization with the warehouse bank for each loan purchased.

A Purchase Advice is prepared detailing the principal balance, commitment price, interest rate, per diem and CMG fees.

CMG Financial Correspondent Lending Guide Page 30

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Aggregate Escrow Analysis CMG requires aggregate escrow analysis and all initial escrow account disclosure statements to be calculated and prepared in full compliance with the requirements of RESPA and all relevant state law.

Final HUD 1 Provide the Final HUD 1 appropriately executed by closing agent and borrower(s) or Estimated HUD 1 executed by closing agent and borrowers, along with certified Final HUD I. (depending on wet or dry state) Any and all appropriate HUD, Federal, State, lender documents must be appropriately executed with conforming signatures to the parties involved in the transaction. All borrowers on the note and documents must be part of the FHA Connection Casefile.

FHA Connect Screen Shots: Casefile Information It is the Correspondent’s responsibility to provide CMG Financial the FHAC screen shots.

Validated borrower(s) information,

Casefile assignment screen shot

Current case query for the file.

CAIVRS clearance

Evidence MIP paid Any required conditions to purchase will be generated and posted to the www.CMGfi.com/correspondent website. .

Document Requirements Failure to comply with delivery and documentation requirements could result in a delay in the purchase of your loan or a purchase denial.

Original Note An original, properly Endorsed Note (or Original Note with appropriately executed Allonge) must be executed by each borrower and delivered to:

CMG Financial Attn: Correspondent Lending Division 3160 Crow Canyon Road, Suite 400 San Ramon, CA 94583

CMG Financial Correspondent Lending Guide Page 31

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

The original Note must include the following:

Date on the Note that matches the date of Deed of Trust/Mortgage.

Property address that matches the address of the Deed of Trust/Mortgage, Appraisal, and Preliminary Title Report.

Correct loan amount and interest rate, both written and numeric.

Correct lender name and maturity date.

Correct payment amount, using Fannie Mae/Freddie Mac factors to calculate the principal and interest payment.

Accurate first payment information that does not exceed 62 days from the funding disbursement date.

A grace period that does not exceed 15 days, except where prohibited by state law.

Late charge that does not exceed 5% (Conventional Loans) or 4% (Government Loans) of the payment amount, or the maximum allowable in that state, whichever is less.

Borrower’s names typed exactly as listed on the Preliminary Title Report or Purchase Contract.

Signature of all borrowers, exactly as typed on the Note; the borrowers may over sign but never under sign.

All applicable Note Riders/Addendum.

Forms The most current HUD, Fannie Mae and Freddie Mac forms that are correct for the jurisdiction, loan program and mortgage and property type must be used.

Notary Requirements The security instrument and all applicable riders must be executed by the borrowers before a notary. The notary must sign the notary acknowledgement and the notary seal/stamp and expiration date must be affixed to each document.

CMG Financial Correspondent Lending Guide Page 32

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Required Riders If Riders are required, they must also be recorded with the Mortgage/Deed of Trust, with a certified copy included in the purchase package. In order for a Rider to be made a part of the Mortgage/Deed of Trust, the applicable Rider Box must be checked on the Mortgage/Deed of Trust.

The following Riders are required, as noted:

Condo Rider (required for properties located in a condominium project).

PUD Rider (required for properties either located in a planned unit development or subject to assessments from a homeowners association).

Second Home Rider (required for properties that will be occupied by the borrower as a second or vacation home).

Title Commitment The Title Commitment must contain the following:

The proposed dollar amount of the loan referenced in the Deed of Trust/Mortgage.

A legal description of the property that agrees with the Deed of Trust/Mortgage and appraisal.

A copy of the survey or plat map, if required by the title company.

An Attorney’s Opinion Letter, if applicable in the state where the property is located.

An Environmental Protection Lien and endorsement for all loans.

The latest ALTA form of title insurance policy (required).

NOTE: In states where ALTA forms are not used, similar coverage is required.

24 months of property ownership (chain of title).

Power of Attorney

If a power of attorney form is used, it must meet the following requirements:

The Assigner must be the borrower and at least one borrower must be present at closing/signing; exceptions may be made on a case-by-case basis.

The POA must be specific to the transaction (noting the property address or legal description). It must comply with state law, allow for the Note and related Mortgage/Deed of Trust to be legally enforced, and be acceptable to the title insurer and closing agent.

The POA must be fully executed, notarized, dated prior to the closing date and recorded prior to the Mortgage/Deed of Trust, with a certified copy retained in the purchase package.

CMG Financial Correspondent Lending Guide Page 33

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Title Insurance Each title insurer is qualified to do business in the jurisdiction where the subject is located. Each such policy shall insure Seller, its successors and assigns to the first (or, if indicated by Seller, second) priority of the mortgage, and shall be in the amount of the original principal of the mortgage loan. Seller warrants that they are the named insured and sole insured of such title policy and that the assignment to CMG Financial of Seller’s interest in such title insurance does not require the consent of or notification to the insurer, and that such insurance policy is and will remain in full force and effect and will insure to the benefit of CMG Financial and if CMG Financial assigns upon the consummation of the transaction contemplated by the Agreement and any subsequent assignments by CMG Financial Seller warrants that no claims have been made under such title insurance policy and neither Seller nor any prior holder of the mortgage has done anything which would impair the coverage of such title insurance policy and that nothing contemplated in the Agreement, or any transfer to CMG Financial, will impair the coverage of such title insurance policy. In the event that a married borrower wishes to take title to the mortgaged property without his or her spouse, the lien created by the mortgage must be superior to any interest in the mortgaged property the spouse may have under the law or otherwise. Only the borrower(s) applying for a mortgage loan are allowed to be on the note and security instrument. Title can only be in the name of the borrower(s) applying for a mortgage loan. A spouse is allowed to sign the security instrument (Mortgage, Deed of Trust) to be added to title without applying for a mortgage loan.

Survey Requirements Unless it is covered by a master title insurance policy which insures against loss due to survey-‐related matters, a plat or improvement survey must be provided. The survey must indicate the location of the subject plot, any easements, encroachments, building lines, street lines, boundary lines, structures and/or improvements.

Endorsement Requirements The following endorsements are required as applicable:

All loans: 8.1 Environmental Protection

Condominiums: 115.1

PUD: 115.2

Comprehensive Endorsement 100 or its equivalent

116 Location Endorsement or its equivalent

CMG Financial Correspondent Lending Guide Page 34

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Settlement Agents & Title Companies Sellers are required to provide settlement agent/title companies with complete and accurate instructions. Settlement agent/title companies are required to adhere fully to all written closing instructions. Non-compliance to the above requirements will render loans ineligible for purchase by CMG.

Escrow Accounts CMG purchases loans with and without taxes and homeowners insurance escrowed/impounded. For loans purchased with escrows/impounds, the correspondent must provide the borrower with an escrow disclosure statement indicating all terms to be escrowed. The escrow account and appropriate reserves must be established at the time of closing, as evidenced by the HUD-1.

Impound/Escrow account is required over 80% LTV on all loan products.

Bailee Requirements A Bailee Letter prepared by your Warehouse Bank will be required when funds from your warehouse line are used to secure interest in the Original Note.

The Bailee Letter should contain the following information:

Name, address, and fax number of the Warehouse Bank

Name and address of the correspondent lender

Complete wiring instructions for payment

Name of borrower(s)

Loan amount

CMG loan number, if available

Acknowledgement that the Warehouse Bank’s security interest will be terminated upon receipt of the payment

The Bailee Letter/Agreement should be addressed as follows: CMG Financial, without recourse

Wire Instructions Funds will be wired per the wire instructions provided by you. Wire instructions must be submitted in each purchase package. We cannot accept wire Instructions over the phone.

CMG will only wire to approved Warehouse lines and not to company operating accounts

Note: Banks, S&Ls, Credit Unions and their wholly owned subsidiaries are exempt from this rule, providing that the wholly owned subsidiaries use the parent company’s operating account.

CMG Financial Correspondent Lending Guide Page 35

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Payment History If any scheduled payments were due prior to the purchase date, a Mortgage Payment history must be submitted. Payments on the loan must be current as of the date of purchase.

Transfer/Servicing Disclosure A Notice of Servicing Transfer that meets all regulatory requirements must be given to the borrower at least 15 days before the effective date of the servicing transfer (the date the first payment is due to the new servicer). The following is the information to use for the new servicer:

CMG Mortgage, Inc., DBA CMG Financial 3160 Crow Canyon Road, Suite 400 San Ramon, CA 94583 866-659-8989 Hours 8:30 am – 5 pm Monday – Friday

Collateral Packages The Collateral Package will contain exhibits as required by the Correspondent’s Warehouse Bank and may include all or some of the following:

Original Endorsed Note, Bailee Letter, Original Allonge

Certified copy of Original Note – with endorsement (may be endorsed in blank). An allonge may be used as long as the form and content comply with all applicable state, local, or federal law governing the use of an allonge and result in an enforceable and proper endorsement to the note.

Certified copy of Deed of Trust, Mortgage including all pages and riders

Copy of Closing Protection Letter

Copy of Specific Power of Attorney (if applicable)

Copy of AKA Statements (if applicable)

Copy of Signature Affidavit

Copy Bailee letter or wire instructions (if correspondent is a Bank utilizing funds from own Bank )

Reverse Bailee letter accompanied by certified copy of endorsed note to CMG Mortgage INC., dba CMG Financial or Reverse Bailee letter accompanied by applicable Allonge meeting standard enforceable and proper endorsement to the note . All Warehouse Banks provide Reverse Bailee Letters must be approved by CMG CFO department

CMG Financial Correspondent Lending Guide Page 36

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013

Collateral Delivery to CMG Financial Delivery address:

CMG Financial Correspondent Lending Division 3160 Crow Canyon Rd, Suite 400 San Ramon, CA 94583

The following documents must be delivered to CMG Financial by the Correspondent’s Warehouse Bank for review and approval prior to Purchase by CMG Financial The Original Note and Bailee Letter (from the Warehouse Bank) including proper endorsement as follows: (Except Specific States referenced below)

Pay to the order of: CMG Mortgage, Inc., dba CMG Financial Without Recourse Correspondent Name _______________________________ By: Its:

Collateral Assignment/Allonge Endorsement Requirements regarding Specific States:

Collateral located in the States listed below:

Maryland, Nevada, Ohio, South Carolina, and Connecticut: Pay to the order of: CMG Mortgage, Inc. Without Recourse Correspondent name ___________________________________________ By: Its: Collateral must be assigned to CMG Mortgage, Inc. Without Recourse

Note: Without the proper endorsement on the Original Note, Correspondent may provide a properly executed Allonge. The mortgage seller may not delegate to an attorney-in-fact its authority to execute an endorsement. The endorsement may not be executed by a party using a power of attorney.

CMG Financial Correspondent Lending Guide Page 37

NMLS #1820 Tel: 925.983.3000 Toll-Free: 800.501.2001 Address: 3160 Crow Canyon Road, Suite 400, San Ramon, CA 94583 Revised 3-17-2013