Embed Size (px)

Citation preview

EUR Prev. 2010A Prev. 2011A Prev. 2012E Prev. 2013E

Rev. (MM) -- 4,507.9 -- 5,651.0 4,762.5 4,782.0 6,476.6 5,229.9

EV/Rev 4.2x 3.3x 4.0x 3.6x

EPS

Mar -- 0.25 -- 0.90 -- 0.68A -- 0.43

Jun -- 0.54 -- 1.00 -- 0.71A -- 0.65

Sep -- 0.61 -- 0.84 0.69 0.65 -- 0.98

Dec -- 0.93 -- 0.68 0.56 0.60 -- 1.12

FY Dec -- 2.33 -- 3.42 2.64 2.65 4.54 3.18

FY P/E 17.9x 12.2x 15.7x 13.1x

Price Performance

OCT-11 FEB-12 JUN-12 OCT-12

50

45

40

35

30

25

COMPANY NOTE

Target | Estimate Change

NLD | Technology | Semi. Cap. Equipment 11 October 2012

ASML Hldng (ASML NA)Slowing Down

EQU

ITY R

ESEARC

H EU

ROPE

HOLDPrice target €39.00

(from €45.00)Price €41.68

Financial SummaryNet Debt (MM): (€1,725.9)

Market Data52 Week Range: €48.34 - €26.19Total Entprs. Value (MM): €18,918.2Market Cap. (MM): €20,644.1Insider Ownership: 0.0%Institutional Ownership: 36.5%Shares Out. (MM): 495.3Float (MM): 420.6Avg. Daily Vol.: 2,229,440

Lee Simpson *Equity Analyst

44 (0) 207 029 8695 [email protected]

* Jefferies International Limited

Key Takeaway

As Moore's Law slows and capacity ordering appears absent (memory?) webelieve FY13 sales growth to be modest. Customer co-investment (~€1.4bn forR&D) and the associated buyback should support the SP near term but shouldEUV suffer further pushout (2015+) concerns may begin to swirl around pricingpower as key customer numbers dwindle. We retain our Hold for now given therecent indifferent trading but cut our PT to €39 (from €45).

Intel as anchor tenant can have its drawbacks (pricing?) but it seems alsothat the traditional model of funding semiconductor equipment is changing.In effect, the equipment industry is no longer set to make enough profits to fund theinvestment itself needed for the future. And it is unclear whether there are enough processgenerations still ahead to recover the cost of the investment in the likes of EUV and 450mmwafer manufacturing.

We expect ASML to confirm a further delay in EUV. EUV is late, throughput isexceptionally slow (10-12 wafers per hour vs. 200+ for immersion tools) and associatedecosystem issues abound. We believe that there is a high chance that ASML make public theirbelief that EUV will be further delayed by a further 1-2 years. We see volume productionat >100 w/hr as feasible sometime beyond 2015.

We fear a possible order book slowdown for 28nm logic in 2H12 may be temporaryas 20-22nm logic ordering could burst into view in 1Q13. That said, we think this couldreverse the supply constraint fears talked about previously in 28nm and see a slowing of the28nm capacity build out phase.

As our recent piece argues (see “Moore Stress”, Sep 27, 2012) Moore's Law is slowingand has been for some time. Indeed for the last decade or so, only a handful of largeIDMs and foundries have been able to afford Moore’s Law. As time passes even this groupdwindles as each in turn applies their fab technology to fewer and fewer high volume chips.

Valuation/Risks

Our emerging FY13e estimates point to sales of c. €5.2bn and an EPS of €3.18. It is temptingto mark "FY13" as a mid-cycle year for ASML and as such is likely to enjoy a ~12x multiple.As a result, we retain our Hold rating given the recent indifferent trading butcut our PT to €39 (from €45). Risks to our thesis include a resumption in heavy orderingfor 22/20nm in early FY13 allied with a stronger than expected macro recovery next year.

Jefferies does and seeks to do business with companies covered in its research reports. As a result, investors should be aware that Jefferies may have a conflictof interest that could affect the objectivity of this report. Investors should consider this report as only a single factor in making their investment decision.Please see analyst certifications, important disclosure information, and information regarding the status of non-US analysts on pages 17 to 21 of this report.

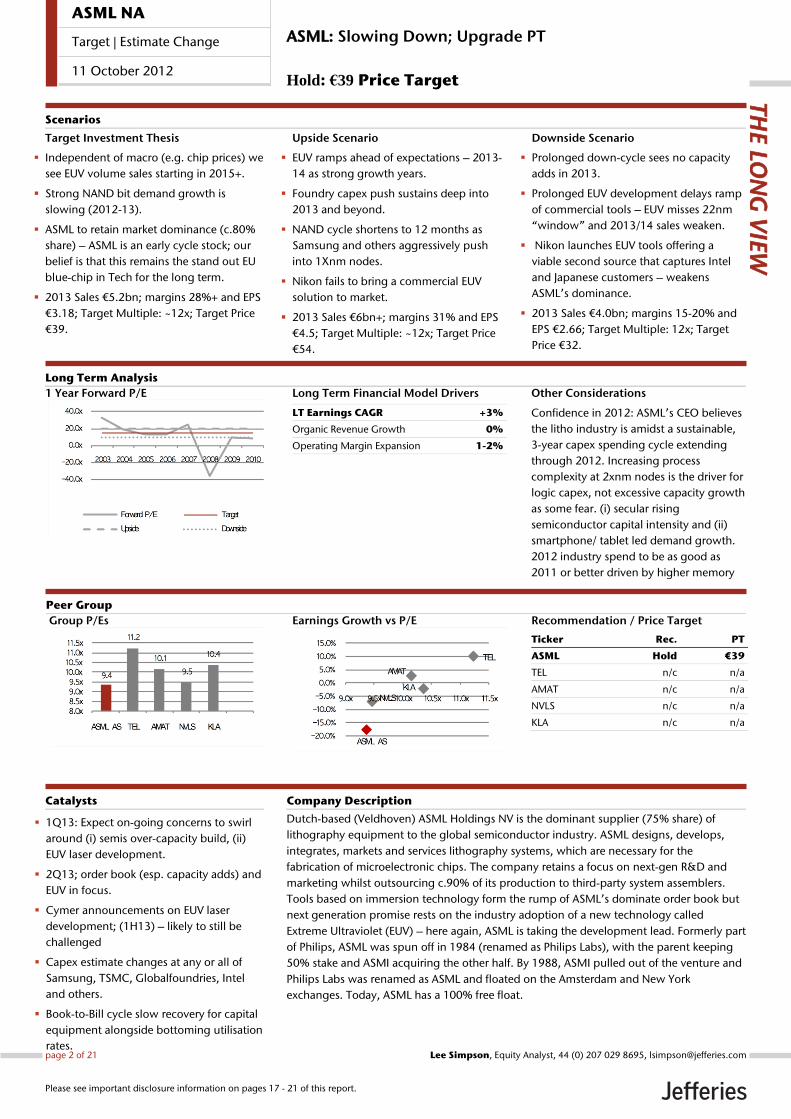

Long Term Financial Model Drivers

LT Earnings CAGR +3%

Organic Revenue Growth 0%

Operating Margin Expansion 1-2%

Other Considerations

Confidence in 2012: ASML’s CEO believes

the litho industry is amidst a sustainable,

3-year capex spending cycle extending

through 2012. Increasing process

complexity at 2xnm nodes is the driver for

logic capex, not excessive capacity growth

as some fear. (i) secular rising

semiconductor capital intensity and (ii)

smartphone/ tablet led demand growth.

2012 industry spend to be as good as

2011 or better driven by higher memory

spend and higher capital intensity at

1 Year Forward P/E

Dutch-based (Veldhoven) ASML Holdings NV is the dominant supplier (75% share) of

lithography equipment to the global semiconductor industry. ASML designs, develops,

integrates, markets and services lithography systems, which are necessary for the

fabrication of microelectronic chips. The company retains a focus on next-gen R&D and

marketing whilst outsourcing c.90% of its production to third-party system assemblers.

Tools based on immersion technology form the rump of ASML’s dominate order book but

next generation promise rests on the industry adoption of a new technology called

Extreme Ultraviolet (EUV) – here again, ASML is taking the development lead. Formerly part

of Philips, ASML was spun off in 1984 (renamed as Philips Labs), with the parent keeping

50% stake and ASMI acquiring the other half. By 1988, ASMI pulled out of the venture and

Philips Labs was renamed as ASML and floated on the Amsterdam and New York

exchanges. Today, ASML has a 100% free float.

1Q13: Expect on-going concerns to swirl

around (i) semis over-capacity build, (ii)

EUV laser development.

2Q13; order book (esp. capacity adds) and

EUV in focus.

Cymer announcements on EUV laser

development; (1H13) – likely to still be

challenged

Capex estimate changes at any or all of

Samsung, TSMC, Globalfoundries, Intel

and others.

Book-to-Bill cycle slow recovery for capital

equipment alongside bottoming utilisation

rates.

Catalysts

Target Investment Thesis

Independent of macro (e.g. chip prices) we

see EUV volume sales starting in 2015+.

Strong NAND bit demand growth is

slowing (2012-13).

ASML to retain market dominance (c.80%

share) – ASML is an early cycle stock; our

belief is that this remains the stand out EU

blue-chip in Tech for the long term.

2013 Sales €5.2bn; margins 28%+ and EPS

€3.18; Target Multiple: ~12x; Target Price

€39.

Upside Scenario

EUV ramps ahead of expectations – 2013-

14 as strong growth years.

Foundry capex push sustains deep into

2013 and beyond.

NAND cycle shortens to 12 months as

Samsung and others aggressively push

into 1Xnm nodes.

Nikon fails to bring a commercial EUV

solution to market.

2013 Sales €6bn+; margins 31% and EPS

€4.5; Target Multiple: ~12x; Target Price

€54.

Downside Scenario

Prolonged down-cycle sees no capacity

adds in 2013.

Prolonged EUV development delays ramp

of commercial tools – EUV misses 22nm

“window” and 2013/14 sales weaken.

Nikon launches EUV tools offering a

viable second source that captures Intel

and Japanese customers – weakens

ASML’s dominance.

2013 Sales €4.0bn; margins 15-20% and

EPS €2.66; Target Multiple: 12x; Target

Price €32.

Long Term Analysis

Scenarios

Group P/Es

Earnings Growth vs P/E

Recommendation / Price Target

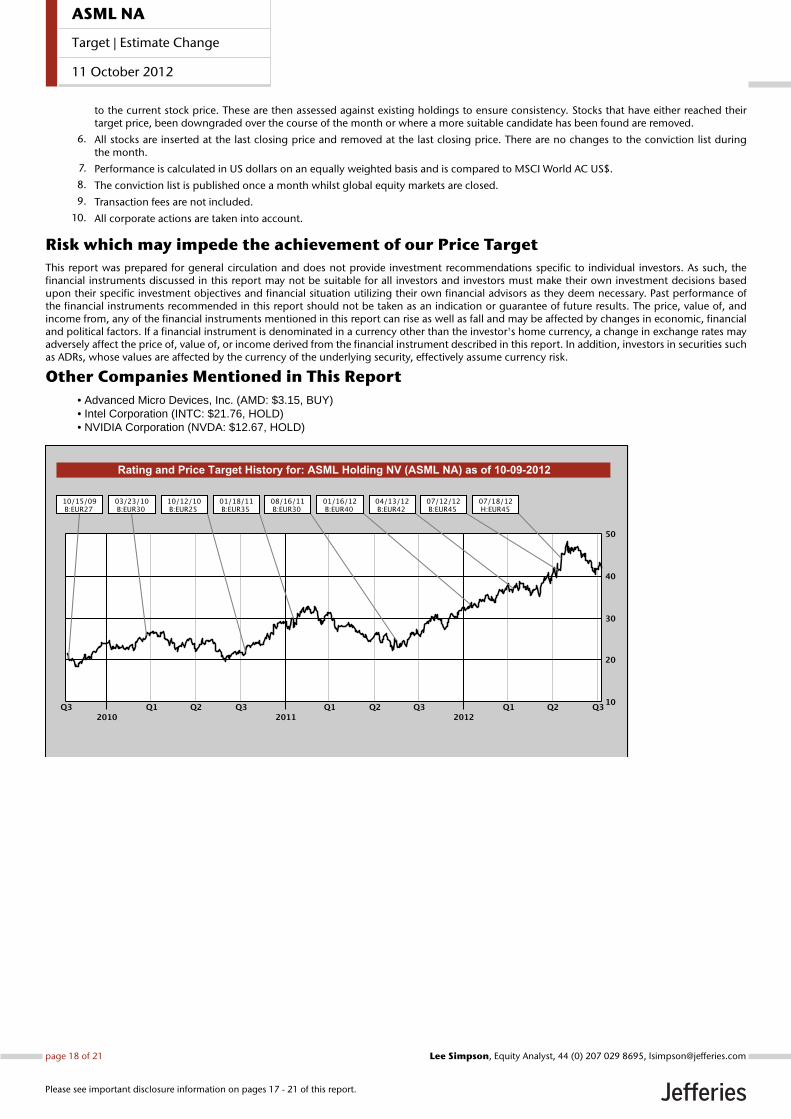

Ticker Rec. PT

ASML Hold €39

TEL n/c n/a

AMAT n/c n/a

NVLS n/c n/a

KLA n/c n/a

Company Description

THE LO

NG

VIE

W

Peer Group

ASML: Slowing Down; Upgrade PT

Hold: €39 Price Target

page 2 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Slowing Down As Moore's Law slows and capacity ordering appears absent (memory?) we

believe FY13 sales growth to be modest. Customer co-investment (~€1.4bn for

R&D) and the associated buyback should support the SP near term but should

EUV suffer further pushout (2015+) concerns may begin to swirl around

pricing power as key customer numbers dwindle. We retain our Hold for now

given the recent indeifferent trading but cut our PT to €39 (from €45) Our

emerging FY13e estimates point to sales of c. €5.2bn and an EPS of €3.18. It is

tempting to mark "FY13" as a mid-cycle year for ASML and as such is likely to

enjoy a ~12x multiple. As a result, ASML could trade to a range of €38-39 on

fears of a slowdown in Moore’s Law.

Intel as anchor tenant can have its drawbacks (pricing?) but it seems also that

the traditional model of funding semiconductor equipment is changing. In

effect, the equipment industry is no longer set to make enough

profits to fund the investment itself needed for the future. And it is

unclear whether there are enough process generations still ahead to recover the

cost of the investment in the likes of EUV and 450mm wafer manufacturing.

We expect ASML to confirm a further delay in EUV. EUV is late,

throughput is exceptionally slow (10-12 wafers per hour vs. 200+ for immersion

tools) and associated ecosystem issues abound. We believe that there is a high

chance that ASML make public their belief that EUV will be delayed by a further

1-2 years. We see volume production at >100 w/hr as feasible sometime beyond

2015.

We fear a possible order book slowdown for 28nm logic in 2H12: may

be temporary as 20-22nm logic ordering could burst into view in 1Q13. That

said, we think this could reverse the supply constraint fears talked about

previously in 28nm and see a slowing of the 28nm capacity build out phase.

As our recent piece argues (see ‚Moore Stress‛, Sep 27, 2012) Moore's Law is

slowing and has been for some time. Indeed for the last decade or so, only

a handful of large IDMs and foundries have been able to afford Moore’s Law. As

time passes even this group dwindles as each in turn applies their fab

technology to fewer and fewer high volume chips.

1. Co-investment with Customers

In a move to bring investment into its future development needs ASML has

made the strategic decision to allow lead customers (Intel, Samsung, TSMC)

to invest in its business. The customer investment program sees Intel (15%) ,

Samsung and TSMC (both ~4%) take a 23% stake in ASML and commit to

ploughing €1.38bn into ASML’s R&D budget over the next 5 years (current

run rate is ~€580m per annum). This will be funnelled into both EUV and

450mm wafer technology development. Intel as anchor tenant can have its

drawbacks (pricing?) but it seems that the traditional model of funding

semiconductor equipment is changing. In effect, the equipment industry

(and perhaps ASML) could be no longer set to make enough profits to fund

the investment needed for the future. And it is unclear whether there are

enough process generations still ahead to recover the cost of the investment

in the likes of EUV.

Comment ###

We believe FY13 sales growth to be

modest as Moore’s Law slows.

Comment ###

We believe there’s a strong chance

that ASML will push out volume

production on EUV to beyond 2015.

It seems that the traditional model of

funding semiconductor equipment is

changing.

page 3 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Near-term, shares supported by buybacks. ASML are issuing ~23% (of existing

stock) as new stock, as part of the synthetic buyback. This is to be a 100/77 reverse stock

split. The price of the share issue is fixed at €39.91 (20 day average prior to the initial Intel

deal announcement). These new shares (no voting rights) will be issued to the three

customers with all existing investors (at time of deal announce) getting the equivalent of

€9.81 per share in cash (all €1.7bn of net proceeds returned to existing investors). This has

been 98% approved at EGM and looks set to go ahead during Nov ’12. ASML issued

shares to Intel and Samsung during Sep ’12 and will issue shares to TSMC by the end of

this month (Oct ’12). ASML expects to execute the Synthetic Buyback sometime after 11th

Nov ’12 with the cash payment date expected in early Dec ’12. Note, of course that the

buyback will have zero effect on total number of shares outstanding before and after issue

– so should have no difference on EPS as a result.

Exhibit 1: Terms of co-investment with Intel

Source: Intel

Why did Intel do this deal?

There was a risk that 450mm wouldn’t happen. If ASML had passed on the development

and given it’s unlikely Nikon could support this (at least in time for 2016 HVM) then there

is a fair chance that 450mm development would not have happened. ASML’s terms were

to tie Intel closer to its EUV development plans with R&D investments and commitments

to tool orders. Intel, especially at 450mm, have to participate in the risk/financing on

development and have signed a guarantee to buy tools.

What does Intel get here? Both the EUV transition (2015+) and 450mm migration

(2016/17) are essentially back-half of the decade events. Historically, wafer transitions

have led to ~30-40% reductions in die cost for Intel. This time out, Intel believes its ROI on

the 450mm transition (from 300mm) could be >5x higher than that on its 300mm

transition (from 200mm) which it estimated at $2 bn.

… why did ASML do this deal?

Some investors are concerned that the deal sees Intel squeeze ASML for its

roadmap development. We think Intel not only spends the highest dollar amount on

its equipment/processes vs. all other foundries put together but looks to guarantee its

development needs and bring about its strategic relevance to suppliers as well. So, ASML

has to be careful with the needs of its other customers and showing too much favouritism

for Intel. Investors are asking:

Why if Intel gets a 15% stake at zero premium is that good for me as a

shareholder?

Does Intel and co. get favourable pricing on this deal?

ASML expects to execute the

Synthetic Buyback sometime after

11th Nov’12.

ASML has to be careful with the

needs of its other customers.

page 4 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Is it negative for TSMC and Samsung that Intel has a bigger stake?

We try and address this below. That all said, (i) ASML gets to squeeze out Nikon, (ii) has

product commitment from the one customer that could guarantee success for EUV, and

(iii) has a fair slug of its development costs paid for by customer base. Overall, investors

diluted but income streams accelerated. If Moore’s Law is ‚re-booted‛ (by EUV) ASML’s

multiple will likely expand again; it has dropped cycle-on-cycle for the last three we

believe on fear of a Moore’s Law slowdown.

No voting rights or board seat for Intel as part of this deal. ASML claim

that there are no price guarantees to Intel as part of this deal and state that in

fact machines will be made available to all customers not just through a specific

customer development. Intel also don’t get a board seat and have no voting

rights on their shares. How fully ASML can maintain its independence in light of

such a hefty investment should be something to be mindful of (e.g., look at how

SVG developed under a one customer agreement). So ASML must continue

to strike a balance across the needs of various sectors (e.g. ,for a

memory fab you need a different toolset configuration to that for logic say).

TSMC, Samsung did not match Intel size in EUV (Intel took 5% in EUV;

10% was 450mm). The offer was for a maximum equity stake of 25% for

customers (split 10% for 450mm migration and 15% for EUV transition). Intel

has secured up to 5% of the 15% available for EUV (and, unsurprisingly all of the

450mm). Yet when offered, TSMC and Samsung did not match Intel’s size in the

consortium even in EUV. We believe that Samsung and TSMC are cautious

investors in the scheme. Intel has, arguably, a 2-4 year lead on rivals with its

22nm FinFET process technology. Previous break-throughs such as High-K Metal

Gate (HKMG) delivered similar leads in the past. Moore's Law scaling, however,

remains key to Intel's lead meaning EUV commitment can't be seen as a

complete surprise. Why should TSMC and Samsung get involved? It may

be perceived that Intel is pressing these two to play their game and this could

create reactions for the likes of ASML. But without this investment ASML believe

they couldn’t have had an accelerated EUV tool program – higher ASPs and

faster throughputs at better resolutions – in time for 2015+. But for a zero

premium equity stake, Samsung and TSMC get an equity play (and a

dividend check) as ‚rebate‛ against the rising cost of EUV to them,

which could just be attractive enough.

What’s the upside for ASML’s EUV program? ASML tells us that Intel gets

(i) new tech and (ii) earlier; but so will other customers. Meantime, EUV

guidance is being increased given Intel commitments – development should

allow for new tools, for smaller EUV resolutions and with higher ASPs than

previously stated. There is no $-impact mentioned but the presentation deck

talks of a rough development roadmap where there will be 450mm tools in

2015 (for immersion and dry) and in 2016 for EUV (volume in 2018).

Why didn’t ASML finance this out of their own B/S? But put another

way, how would the market have reacted should ASML have financed this on

their own — would increasing R&D in EUV by up to €2bn over the next 5 years

been anything other than a disaster for ASML’s SP. Again, ASML claim that

without this deal there could not be an accelerated EUV development program

and thus limited revenue growth in the longer term. Intel as anchor tenant

can have its drawbacks (pricing?) but it seems also that the

traditional model of funding semiconductor equipment is changing.

In effect, the equipment industry (and perhaps ASML) is no longer set

to make enough profits to fund the investment needed for the future.

And it is unclear whether there are enough process generations still

ahead to recover the cost of the investment in the likes of EUV.

How about Nikon? It’s unlikely such a stake by Intel does not come with

guarantees beyond just commitment by ASML to 450mm migration

A Moore’s Law re-boot would see

multiples expand.

ASML sees the investment program

as crucial to EUV delivery.

page 5 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

development. Instead, Intel may have to seek assurances on price or perhaps

even some early embargo on new EUV toolsets in favour of "lead" partners. Both

of which ASML deny as being in the deal. Nonetheless, it’s tempting to think that

Nikon may be the net loser here anyway - often seen as Intel's weapon of

last resort in keeping ASML's pricing keen, Nikon may now be being

squeezed out of EUV. Recent discussions with ASML management alerted us

to the possibility that Nikon may even have to pay a royalty to ASML for any EUV

use.

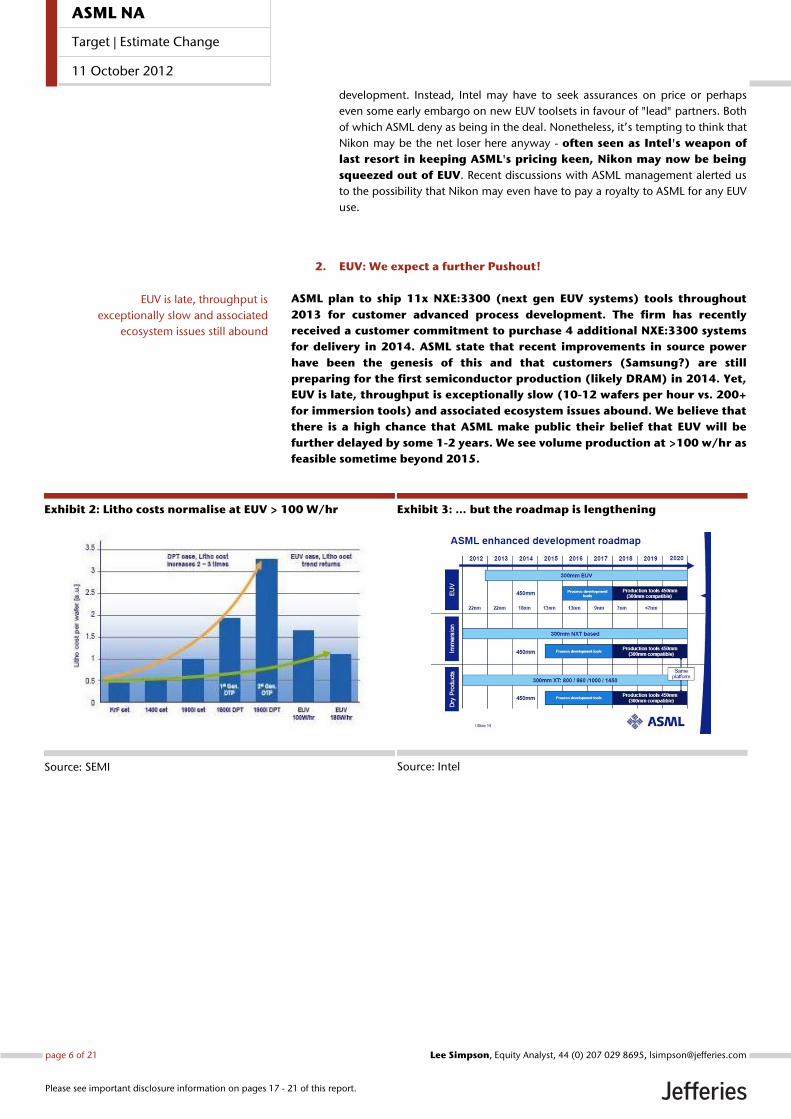

2. EUV: We expect a further Pushout!

ASML plan to ship 11x NXE:3300 (next gen EUV systems) tools throughout

2013 for customer advanced process development. The firm has recently

received a customer commitment to purchase 4 additional NXE:3300 systems

for delivery in 2014. ASML state that recent improvements in source power

have been the genesis of this and that customers (Samsung?) are still

preparing for the first semiconductor production (likely DRAM) in 2014. Yet,

EUV is late, throughput is exceptionally slow (10-12 wafers per hour vs. 200+

for immersion tools) and associated ecosystem issues abound. We believe that

there is a high chance that ASML make public their belief that EUV will be

further delayed by some 1-2 years. We see volume production at >100 w/hr as

feasible sometime beyond 2015.

Exhibit 2: Litho costs normalise at EUV > 100 W/hr

Source: SEMI

Exhibit 3: … but the roadmap is lengthening

Source: Intel

Comment ###

EUV is late, throughput is

exceptionally slow and associated

ecosystem issues still abound

page 6 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

ASML has already compromised on its target of 60 wafers/hr for EUV by YE’12 - that first

shipment of the 3rd gen EUV system (NXE:3300) is now expected in 1H13 although a total

of 11 systems have been ordered for 2013 shipment. Even the testing process can add

delay; laser power development is (i) tested at Cymer (San Diego) but then needs to be

put into final tool parts and then (ii) shipped to and tested again (approval) back at

ASML’s Veldhoven site before being (iii) shipped to the customer and validated there. All

this occurs before the customer can begin to run its own process on the tools and start to

determine volume production at 60 w/hr. We still expect this target to be a real challenge

for ASML and don’t see tools at customers’ sites running 60 wafers/hr unhindered by

YE’13.

The primary reason lies with the numerous issues that continue to hinder EUV production

development:

Resist chemicals have been developed (or at least the raw materials

determined) to give adequate resolutions at 22nm. But the solution is ‘thicker’

than is ideal meaning it has to be exposed to the light longer thus slowing the

throughput of the tool. There is also a paucity of EUV tools available to resist

developers and a question mark over whether photoresist makers can make a

return on investment, should they even arrive at the right solution, given the

high cost of EUV machinery they would need to test on.

Line width roughness (LWR) continues to be a problem and may need to be

solved with a non-lithographic clean-up.

Light sources are one or two orders of magnitude dimmer than they should be

and it can take 30kW to create the 30W of EUV light. That said, ASML have

shown a 50W power capability that can run for over 5 hours. Yet it is assumed

EUV: A Brief Summary

Why use EUV? It returns cost of ownership to the chipmakers - it is a single

patterning technology (and should remain so for the foreseeable future) with just

one mask and one photolithography process per chip layer.

How does it work? Creating EUV light is a difficult process. It involves zapping

droplets of molten tin with a high powered CO2 laser in order to release a small

amount of EUV light.

The inherent difficulties (‚Physics‛): At the 14nm light wavelengths of

extreme ultra violet, the photons (light particles) won't go through lenses … or even

air. So EUV needs a switch from refractive optics (use of lenses as in immersion

lithography) to reflective optics (i.e. mirrors) and put everything in a vacuum.

The main issues (‚Engineering‛): The industry needs to create a different

photoresist than currently used and of course, we need a light source that generates

stable EUV light for long periods of time.

We see Volume production at 60

w/hr sometime after 2013.

page 7 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

that ~100W is needed to deliver 60 wafers/hour with volume production

unlikely before 2014.

Defect-free Mask blanks are still hard to produce - any particle that gets on the

mask is in the focal plane of the mask and so will print on the wafer. This is

unlike refractive masks that have a pellicle to keep particles away from the plane

of the mask itself.

Debris in the system is a by-product of using metal plasma. Tin particles can

build up on the mirror surfaces which means optics have to be cleaned or

replaced every week or so. Indeed we have heard of simple problems with the

delivery nozzle where tin has built up at the nozzle head blocking or impeding

delivery of the tin and thus disturbing the light source sustainability.

Recently our Japanese analyst (Yoshihiro Azuma) has talked about problems the

glass makers have with the reflectivity needed on mirrors used in EUV systems

(see ‚Obstacles for EUVL‛, Oct 9, ’12). It seems even the decision on which

material is best suited to make the mirrors is in some dispute. Secondly, these

mirrors reflect light due to multi-layer interference and mean that even with

good mirrors, only ~70% of the EUV light is reflected. Since the optics need >8

mirrors to focus the light first on the mask and then on the wafer, very little of

the light you start with (~4%) ends up hitting the photoresist increasing the

pressures on the light source.

Triple patterning carries a hefty cost. Triple patterning is essentially the same

machine as used for double patterning only with a head change. Because EUV is late, we

are starting to see some triple patterning tools in development fabs already. Market

leaders such as Intel are not waiting for EUV to be mature enough to start using and so

continue to develop double patterning techniques alongside preparing EUV. But given

EUV development at customers is very early stage, big customers are betting on Triple

patterning too. ASML believe that one of its customers has a chip with 1 layer using triple

patterning – this, however, needs 5 exposures (for single layer) and yields are

horrible meaning customer cost of ownership is too high. These will be high ASP

machines and will ship with computational lithography (Brion) alongside. All in, we

believe that there are unlikely to be more than 2 or 3 triple patterning tools in the order

book for next year.

3. Moore Stress: This could be rough for pricing power…

ASML dominates (~80%) the lithography space with its Twinscan systems and

so has a vested interest in the cadence of Moore’s Law. Indeed it’s often

claimed that Moore’s Law is actually supported by the speed of lithographic

product cycles and innovation. But as our recent piece argues (see ‚Moore

Stress‛, Sep ’12) Moore's Law is slowing and has been for some time. Indeed

for the last decade or so, only a handful of large IDMs and foundries have

been able to afford Moore’s Law. As time passes even this group dwindles as

each in turn applies their fab technology to fewer and fewer high volume

chips. This means an ever diminishing pool of engineering talent is at the

‘coal-face’ of the leading edge process design. With EUV late (estimates range

from 4-6 years late) the cost/transistor has ticked up.

Over the next 3 to 5 years, we think exponential growth in leading edge factory costs will

undermine the cost per transistor declines the industry has come to rely on. We expect

this will translate to a structural shift that will benefit integrators on mature process nodes,

challenge fabless players on the leading edge, and drive unexpected share gains for Intel

and Samsung. For ASML this could drastically reduce its serviceable market of customers

Comment ###

Our cycle metrics are mixed but

shows at least that much of the value

of this cycle reflected.

page 8 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

and force reliance on capacity growth as tech shrink slows. This may finally see ASML

more exposed to slowing end markets (PCs) and changes in chip designs (e.g. 3D ICs).

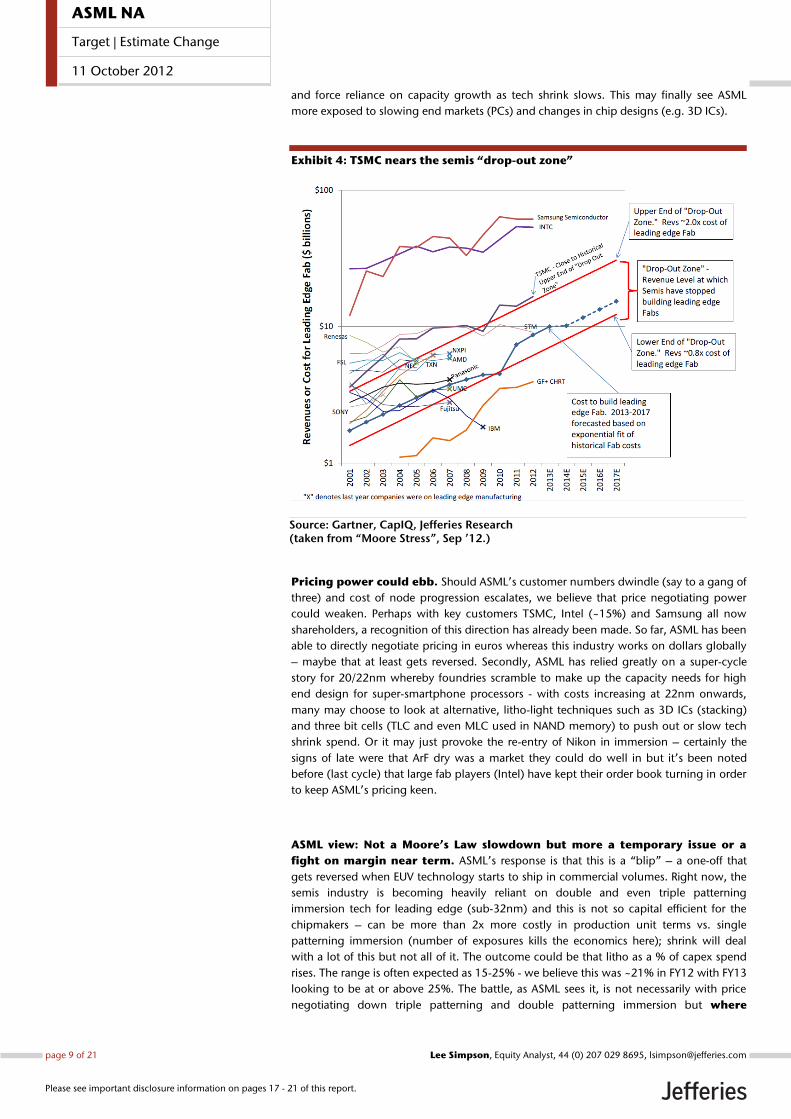

Exhibit 4: TSMC nears the semis ‚drop-out zone‛

Source: Gartner, CapIQ, Jefferies Research (taken from “Moore Stress”, Sep ’12.)

Pricing power could ebb. Should ASML’s customer numbers dwindle (say to a gang of

three) and cost of node progression escalates, we believe that price negotiating power

could weaken. Perhaps with key customers TSMC, Intel (~15%) and Samsung all now

shareholders, a recognition of this direction has already been made. So far, ASML has been

able to directly negotiate pricing in euros whereas this industry works on dollars globally

– maybe that at least gets reversed. Secondly, ASML has relied greatly on a super-cycle

story for 20/22nm whereby foundries scramble to make up the capacity needs for high

end design for super-smartphone processors - with costs increasing at 22nm onwards,

many may choose to look at alternative, litho-light techniques such as 3D ICs (stacking)

and three bit cells (TLC and even MLC used in NAND memory) to push out or slow tech

shrink spend. Or it may just provoke the re-entry of Nikon in immersion – certainly the

signs of late were that ArF dry was a market they could do well in but it’s been noted

before (last cycle) that large fab players (Intel) have kept their order book turning in order

to keep ASML’s pricing keen.

ASML view: Not a Moore’s Law slowdown but more a temporary issue or a

fight on margin near term. ASML’s response is that this is a ‚blip‛ – a one-off that

gets reversed when EUV technology starts to ship in commercial volumes. Right now, the

semis industry is becoming heavily reliant on double and even triple patterning

immersion tech for leading edge (sub-32nm) and this is not so capital efficient for the

chipmakers – can be more than 2x more costly in production unit terms vs. single

patterning immersion (number of exposures kills the economics here); shrink will deal

with a lot of this but not all of it. The outcome could be that litho as a % of capex spend

rises. The range is often expected as 15-25% - we believe this was ~21% in FY12 with FY13

looking to be at or above 25%. The battle, as ASML sees it, is not necessarily with price

negotiating down triple patterning and double patterning immersion but where

page 9 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

foundries will let their margins drift to vs. how much pain (cost) the fabless

chipmakers (e.g. NVidia) will just suck up this time.

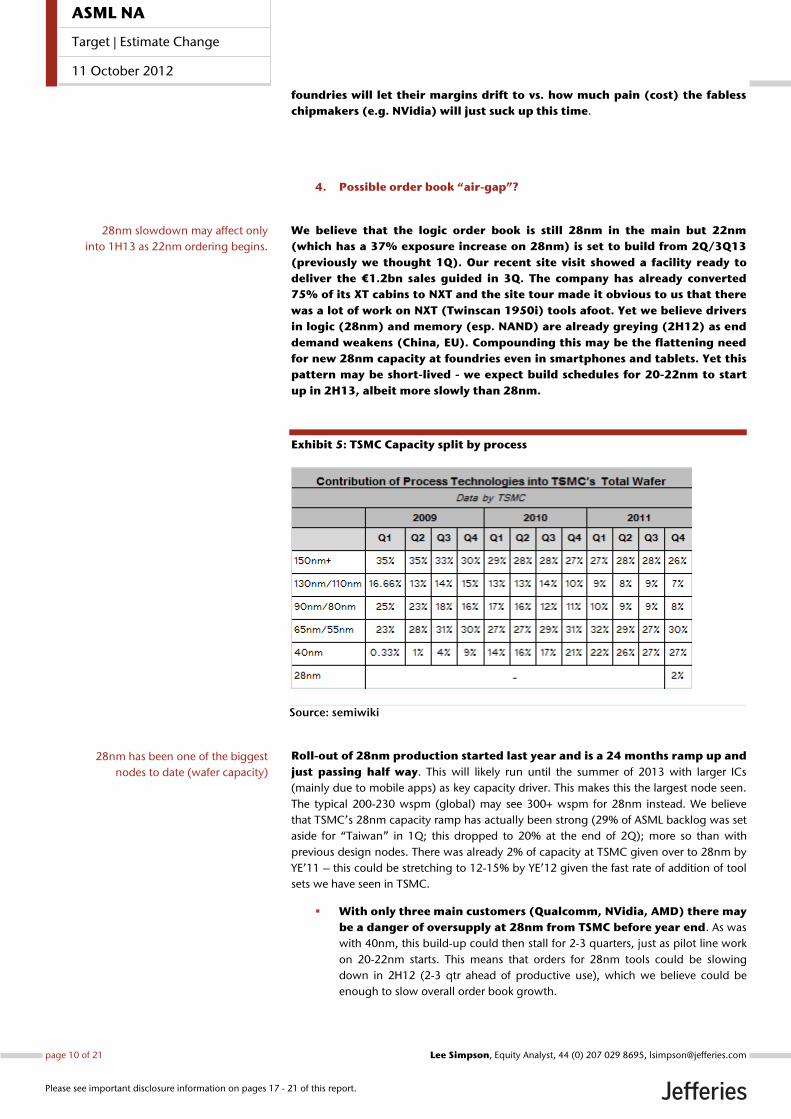

4. Possible order book ‚air-gap‛?

We believe that the logic order book is still 28nm in the main but 22nm

(which has a 37% exposure increase on 28nm) is set to build from 2Q/3Q13

(previously we thought 1Q). Our recent site visit showed a facility ready to

deliver the €1.2bn sales guided in 3Q. The company has already converted

75% of its XT cabins to NXT and the site tour made it obvious to us that there

was a lot of work on NXT (Twinscan 1950i) tools afoot. Yet we believe drivers

in logic (28nm) and memory (esp. NAND) are already greying (2H12) as end

demand weakens (China, EU). Compounding this may be the flattening need

for new 28nm capacity at foundries even in smartphones and tablets. Yet this

pattern may be short-lived - we expect build schedules for 20-22nm to start

up in 2H13, albeit more slowly than 28nm.

Exhibit 5: TSMC Capacity split by process

Source: semiwiki

Roll-out of 28nm production started last year and is a 24 months ramp up and

just passing half way. This will likely run until the summer of 2013 with larger ICs

(mainly due to mobile apps) as key capacity driver. This makes this the largest node seen.

The typical 200-230 wspm (global) may see 300+ wspm for 28nm instead. We believe

that TSMC’s 28nm capacity ramp has actually been strong (29% of ASML backlog was set

aside for ‚Taiwan‛ in 1Q; this dropped to 20% at the end of 2Q); more so than with

previous design nodes. There was already 2% of capacity at TSMC given over to 28nm by

YE’11 – this could be stretching to 12-15% by YE’12 given the fast rate of addition of tool

sets we have seen in TSMC.

With only three main customers (Qualcomm, NVidia, AMD) there may

be a danger of oversupply at 28nm from TSMC before year end. As was

with 40nm, this build-up could then stall for 2-3 quarters, just as pilot line work

on 20-22nm starts. This means that orders for 28nm tools could be slowing

down in 2H12 (2-3 qtr ahead of productive use), which we believe could be

enough to slow overall order book growth.

Comment ###

28nm slowdown may affect only

into 1H13 as 22nm ordering begins.

28nm has been one of the biggest

nodes to date (wafer capacity)

page 10 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

20-22nm logic as driver? Looking into 2H13e we see an order rebound

(Immersion, KrF) as the semis industry marks a cyclical upswing in spending in

response to: (i) end of pause in 28nm investment in 2H12, (ii) a new shrink and

return to spend in NAND and (iii) increasing critical layers in logic at 22nm. Both

65 and 40nm were cost reduction shrink – it’s possible that 20/22nm will be the

same but we think this will be more driven by competitive needs given Intel’s

lead.

2013: Are we really in a logic super-cycle? In the past, TSMC were masters at

balancing demand and capacity, often putting customers on ‚allocation‛ if new. Now

rivals Samsung and GlobalFoundries are spending heavily forcing TSMC’s hand and

changing their capex spending habits – now aim to have capacity to make 10-15% more

chips as buffer. This has hastened the changing capital efficiency at TSMC. The question is

will the trend stay like this? Intel may be key. We note Intel’s plans to have 14nm in

production using double patterning immersion during 2013. We also believe there are

plans to start up an EUV pilot line (initially using an NXE3100 machine) at some point next

year too. At 10nm, Intel will likely use complementary patterning – a mix of EUV and ArF

immersion techniques. With Intel moving to high-volume 14nm production (critical layers

double) in 2013/14 we should see continued spend by Intel on Fab equipment through

2013. But this can be satisfied to some degree by excess capacity at 22nm.

5. Memory Softness: More downside possible

NAND: We don’t expect ASML’s NAND sales to pick up again until 2Q/3Q13.

We are still seeing 70-80% bit growth this year but despite shortages (spot

price squeeze?) we believe this slows to ~50% next year as production cuts

(30% at Toshiba) impact. The recent over-capacity in 1H gave way to spot price

softness and recent moves to cut capacity. The advent of 3-bits per cell (or TLC) means

rather than shrinking the die to improve density/capacity, TLC just increases the number

of bits per cell. TLC is working better than expected due to controllers (software)

distinguishing the levels. Elsewhere, some customer DRAM capacity is being converted to

NAND capacity.

With NAND, most of the bit supply growth this year (~50%) should come through shrink

with the balance coming from moderate capacity adds. Yet we believe that NAND capacity

will remain stable or increase only slightly next year. NAND suppliers just went

through another period of hard learning in 1H12, and that is likely to

translate to capacity add moderation in FY13. The market for Flash cards (aka

memory cards), which has traditionally represented 50%+ of the NAND market, is

shrinking to ~30% or lower fraction of the NAND market in CY12. Solid state drives (SSDs)

are still too nascent in market size and smartphone NAND is unlikely to grow within the

device. But it is still macro uncertainty and a proclivity for chipmakers to under ship

consumption to maintain pricing that carries the greatest risk to order flow in memory.

DRAM: PC pain goes on

Some mid-year glimmers of hope for DRAM capex (pricing recovery) were

extinguished with poor PC traction. Bit demand hovers below 40% per annum. There’s no

more than 4GB DRAM in Win8 devices and Apple is picked up just 0.5GB in the new iPad.

Ultrabooks can be thought of as a mandatory project for Intel and MSFT (otherwise big

product cycle pressure there) but the relative size of the market means this is unlikely a

genuine driver for ASML vs. mobility drivers. We see DRAM bit growth capped below 40%

annually with a chance that DRAM capacity taken is actually transferred out. Bit demand

growth of c.40% can be satisfied on upgrades and new shrinks only. So there is no real

need for new fabs.

Early signs are that 2013 order book

should resume growth

Bit demand growth for both NAND

and DRAM is too narrow to support

order book.

Comment ###

page 11 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

6. The 450mm Migration

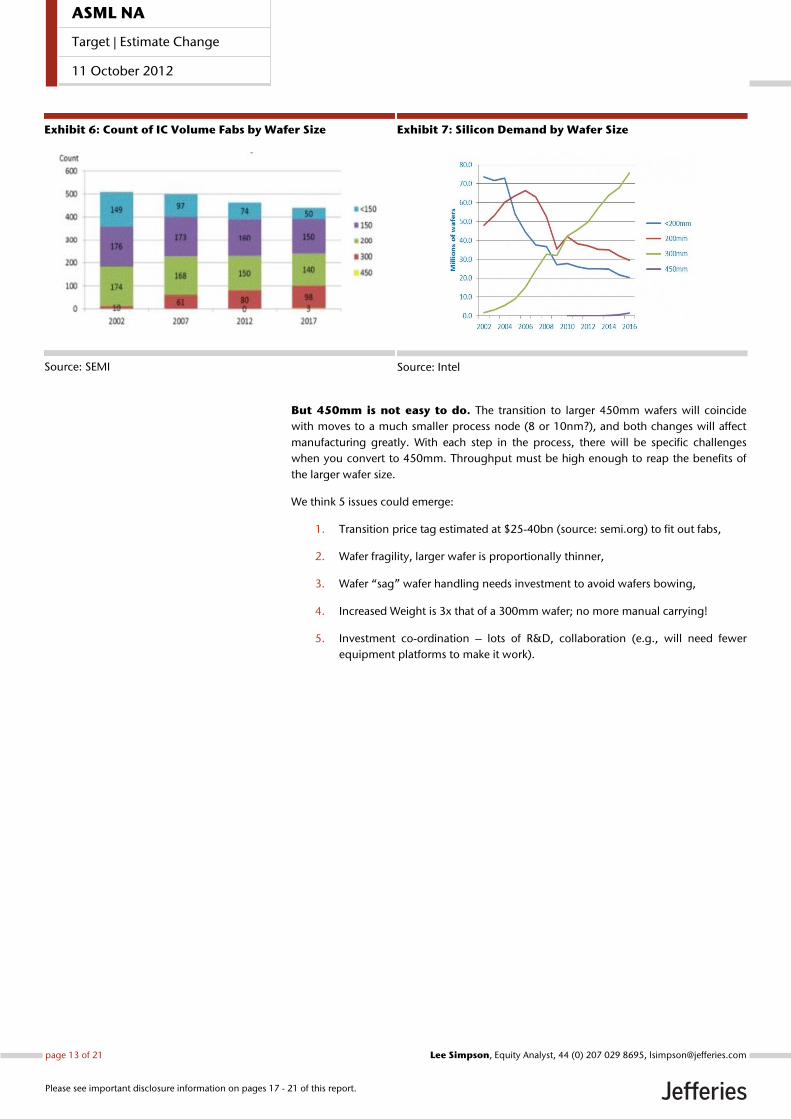

Many SPE players note that the size of the 450mm opportunity is smaller than

the opportunity at 300mm was, which was in turn smaller than the

opportunity at 200mm. Meaning, equipment suppliers will not see as many

orders for 450mm tools as they did in the previous wafer size transitions. A

small number of chip makers dominate the industry now, however, and if

those suppliers begin to really demand 450mm, equipment makers will need

to support the move. A tie up between Intel/ASML here is (i) skewed much

more to the needs of Intel, and (ii) puts inevitable pressure on other

equipment makers to follow course. This will likely see a lot more chip

fab/supply chain collaboration – recent consolidation in the chip

manufacturing sector could actually improve supply chain collaboration, as

tool suppliers and infrastructure support companies build R&D teams around

‚mega companies‛ making chips.

There has been a perceived issue for ASML in past that with 450mm, being

more than double the size of surface area than 300mm, demand for

individual machines would be crunched. Firstly, ASML would likely re-use as much

of the same modular design in their machines (laser, lens, supply, etc.) as they could. But

things like the wafer platform (stage) and also the chassis will have to size up to

accommodate bigger wafer size. There may also have to be a change to the motors for

stepping but likely a more trivial change.

So ASML may have something like a 1.3-1.5x component cost (just a total guess here) for

something that does a similar task to 300mm equivalent – it’s conjecture on my part but

likely that with Intel as the main customer they will be able to get say a 1.2x ASP

equivalent for 450mm vs. 300mm with perhaps a bit more elasticity in price with other

customers. This is crude but suggests we have a smaller margin. More worrying for me is

that demand needs are covered more by these bigger wafers. This is a 2015+ story but

something that might appear as a headwind for the story just as EUV goes into volume

production. I'm just playing with darker side of the story here.

The cost for the chipmaker What goes into making a cleanroom 450mm accessible?

Higher ceilings, increased weight-bearing specifications, and more room for tools like

extreme ultraviolet (EUV) lithography scanners. Litho equipment that needs new wafer

stages that move at high speeds through various environments (air, liquid, etc.) is just one

piece in the puzzle.

How is the ecosystem developing? The annual SPE conference, SEMICON West, is on

right now and there's lots of buzz around 450mm.

KLA-Tencor installed its first process control systems for handling and inspecting

unpatterned 450mm wafers (Surfscan SP3 450). KLA-Tencor says it has received

multiple orders for its 450mm-capable tool and shipped several systems (IMEC,

the research institute, is using one).

Elsewhere, CyberOptics came out with a 450mm version of its WaferSense Auto

Vibration System, AVS450. The product is a wireless wafer-life vibration

monitoring device that measures vibrations of wafer transfers in x, y and z

dimensions during semiconductor processes.

We also note that IMEC has a €100m grant from the Belgian government to

build 450mm wafer fab cleanrooms, which means they are working on process

challenges, throughput enhancement, etc., for the 10nm/14nm node.

So, you can see the ecosystem is starting to build.

Comment ###

page 12 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Exhibit 6: Count of IC Volume Fabs by Wafer Size

Source: SEMI

Exhibit 7: Silicon Demand by Wafer Size

Source: Intel

But 450mm is not easy to do. The transition to larger 450mm wafers will coincide

with moves to a much smaller process node (8 or 10nm?), and both changes will affect

manufacturing greatly. With each step in the process, there will be specific challenges

when you convert to 450mm. Throughput must be high enough to reap the benefits of

the larger wafer size.

We think 5 issues could emerge:

1. Transition price tag estimated at $25-40bn (source: semi.org) to fit out fabs,

2. Wafer fragility, larger wafer is proportionally thinner,

3. Wafer ‚sag‛ wafer handling needs investment to avoid wafers bowing,

4. Increased Weight is 3x that of a 300mm wafer; no more manual carrying!

5. Investment co-ordination – lots of R&D, collaboration (e.g., will need fewer

equipment platforms to make it work).

page 13 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Exhibit 8: Too Heavy to carry manually?

Source: Semicon

Exhibit 9: ALL production tools will need re-configuration

Source: Semicon

All in, we think this is a 2017+ story with investment needed across EUV as well as ArF and

KrF based tools. The industry's fundamental issues with 450mmm migration

have yet to be addressed but that work appears to have some momentum if

not even some kind of determination behind it.

For IMEC Initial 450mm assessment is taking place now, with R&D on processes slated to

occur in 2015 and 2016. Early manufacturing will begin in 2017. With this in mind, IMEC

recognized a need to open the new cleanroom by 2015. Initial tool assessments will be

done in the 450mm-compatible area of IMEC’s 300mm pilot line cleanroom. So, I'd say

that Intel could have 450mm-compatible pilot lines by 2014 with Intel only at the head of

development here. Transition for other industry leaders is over the subsequent 3-5 years

(reliant on work from places like IMEC). And, as with 200mm during the 300mm

transition, significant 300mm development will cease. Some observers saying that

‚450mm only‛ at 8nm process node (c.f. ‚300mm only‛ at 65nm), which suggests to me

sometime around c. 2020??

The benefits for Intel of using 450mm are clear - includes higher productivity

(including fewer defects), cost effective (volume) and may allow them to attack the future

fabless space as a result (competitive footprint). It’s arguably the case that only Intel will

be using this tech (has been an advocate of this for some time). More likely is that industry

will let Intel plough the new furrow and then come in (say 2 years behind) when the

marginal cost of plant migration is lower.

page 14 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

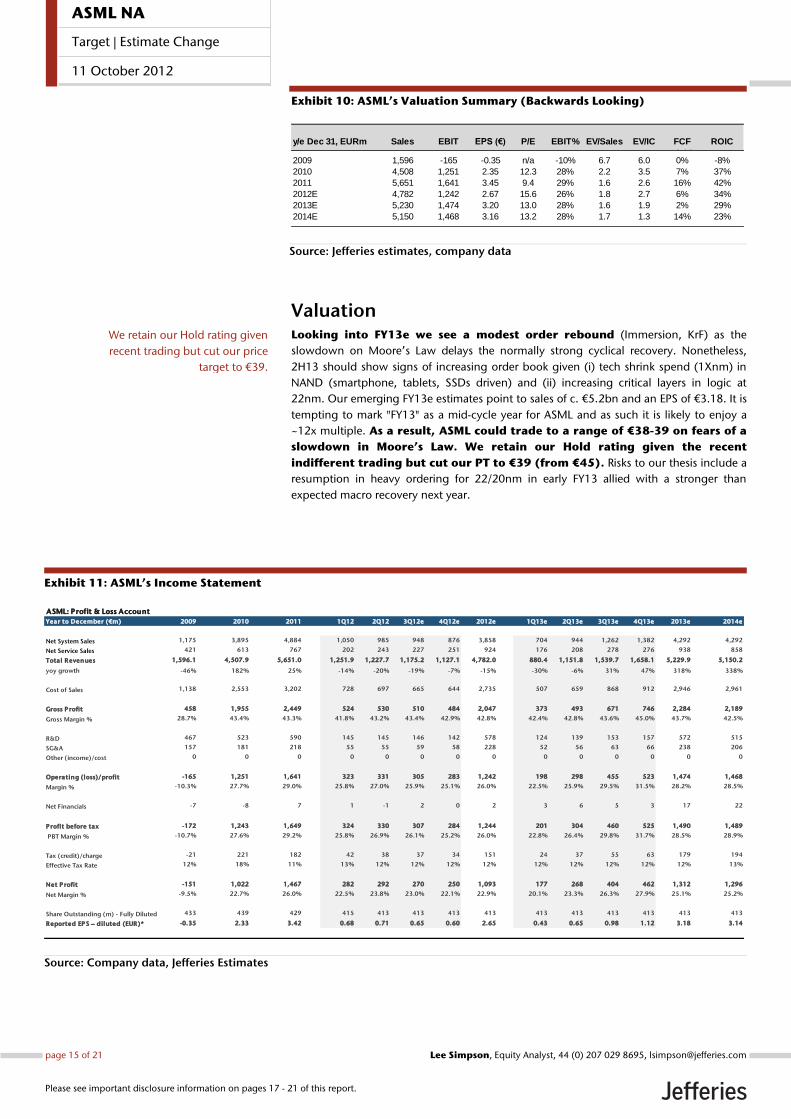

Exhibit 10: ASML’s Valuation Summary (Backwards Looking)

Source: Jefferies estimates, company data

Valuation Looking into FY13e we see a modest order rebound (Immersion, KrF) as the

slowdown on Moore’s Law delays the normally strong cyclical recovery. Nonetheless,

2H13 should show signs of increasing order book given (i) tech shrink spend (1Xnm) in

NAND (smartphone, tablets, SSDs driven) and (ii) increasing critical layers in logic at

22nm. Our emerging FY13e estimates point to sales of c. €5.2bn and an EPS of €3.18. It is

tempting to mark "FY13" as a mid-cycle year for ASML and as such it is likely to enjoy a

~12x multiple. As a result, ASML could trade to a range of €38-39 on fears of a

slowdown in Moore’s Law. We retain our Hold rating given the recent

indifferent trading but cut our PT to €39 (from €45). Risks to our thesis include a

resumption in heavy ordering for 22/20nm in early FY13 allied with a stronger than

expected macro recovery next year.

Exhibit 11: ASML’s Income Statement

Source: Company data, Jefferies Estimates

Sales EBIT EPS (€) P/E EBIT% EV/Sales EV/IC FCF

yield

ROIC

2009 1,596 -165 -0.35 n/a -10% 6.7 6.0 0% -8%

2010 4,508 1,251 2.35 12.3 28% 2.2 3.5 7% 37%

2011 5,651 1,641 3.45 9.4 29% 1.6 2.6 16% 42%

2012E 4,782 1,242 2.67 15.6 26% 1.8 2.7 6% 34%

2013E 5,230 1,474 3.20 13.0 28% 1.6 1.9 2% 29%

2014E 5,150 1,468 3.16 13.2 28% 1.7 1.3 14% 23%

y/e Dec 31, EURm

2009 2010 2011 1Q12 2Q12 3Q12e 4Q12e 2012e 1Q13e 2Q13e 3Q13e 4Q13e 2013e 2014e

Net System Sales 1,175 3,895 4,884 1,050 985 948 876 3,858 704 944 1,262 1,382 4,292 4,292

Net Service Sales 421 613 767 202 243 227 251 924 176 208 278 276 938 858

Total Revenues 1,596.1 4,507.9 5,651.0 1,251.9 1,227.7 1,175.2 1,127.1 4,782.0 880.4 1,151.8 1,539.7 1,658.1 5,229.9 5,150.2

yoy growth -46% 182% 25% -14% -20% -19% -7% -15% -30% -6% 31% 47% 318% 338%

Cost of Sales 1,138 2,553 3,202 728 697 665 644 2,735 507 659 868 912 2,946 2,961

Gross Profit 458 1,955 2,449 524 530 510 484 2,047 373 493 671 746 2,284 2,189

Gross Margin % 28.7% 43.4% 43.3% 41.8% 43.2% 43.4% 42.9% 42.8% 42.4% 42.8% 43.6% 45.0% 43.7% 42.5%

R&D 467 523 590 145 145 146 142 578 124 139 153 157 572 515

SG&A 157 181 218 55 55 59 58 228 52 56 63 66 238 206

Other (income)/cost 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Operating (loss)/profit -165 1,251 1,641 323 331 305 283 1,242 198 298 455 523 1,474 1,468

Margin % -10.3% 27.7% 29.0% 25.8% 27.0% 25.9% 25.1% 26.0% 22.5% 25.9% 29.5% 31.5% 28.2% 28.5%

Net Financials -7 -8 7 1 -1 2 0 2 3 6 5 3 17 22

Profit before tax -172 1,243 1,649 324 330 307 284 1,244 201 304 460 525 1,490 1,489

PBT Margin % -10.7% 27.6% 29.2% 25.8% 26.9% 26.1% 25.2% 26.0% 22.8% 26.4% 29.8% 31.7% 28.5% 28.9%

Tax (credit)/charge -21 221 182 42 38 37 34 151 24 37 55 63 179 194

Effective Tax Rate 12% 18% 11% 13% 12% 12% 12% 12% 12% 12% 12% 12% 12% 13%

Net Profit -151 1,022 1,467 282 292 270 250 1,093 177 268 404 462 1,312 1,296

Net Margin % -9.5% 22.7% 26.0% 22.5% 23.8% 23.0% 22.1% 22.9% 20.1% 23.3% 26.3% 27.9% 25.1% 25.2%

Share Outstanding (m) - Fully Diluted 433 439 429 415 413 413 413 413 413 413 413 413 413 413

Reported EPS – diluted (EUR)* -0.35 2.33 3.42 0.68 0.71 0.65 0.60 2.65 0.43 0.65 0.98 1.12 3.18 3.14

Year to December (€m)

ASML: Profit & Loss Account

We retain our Hold rating given

recent trading but cut our price

target to €39.

page 15 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

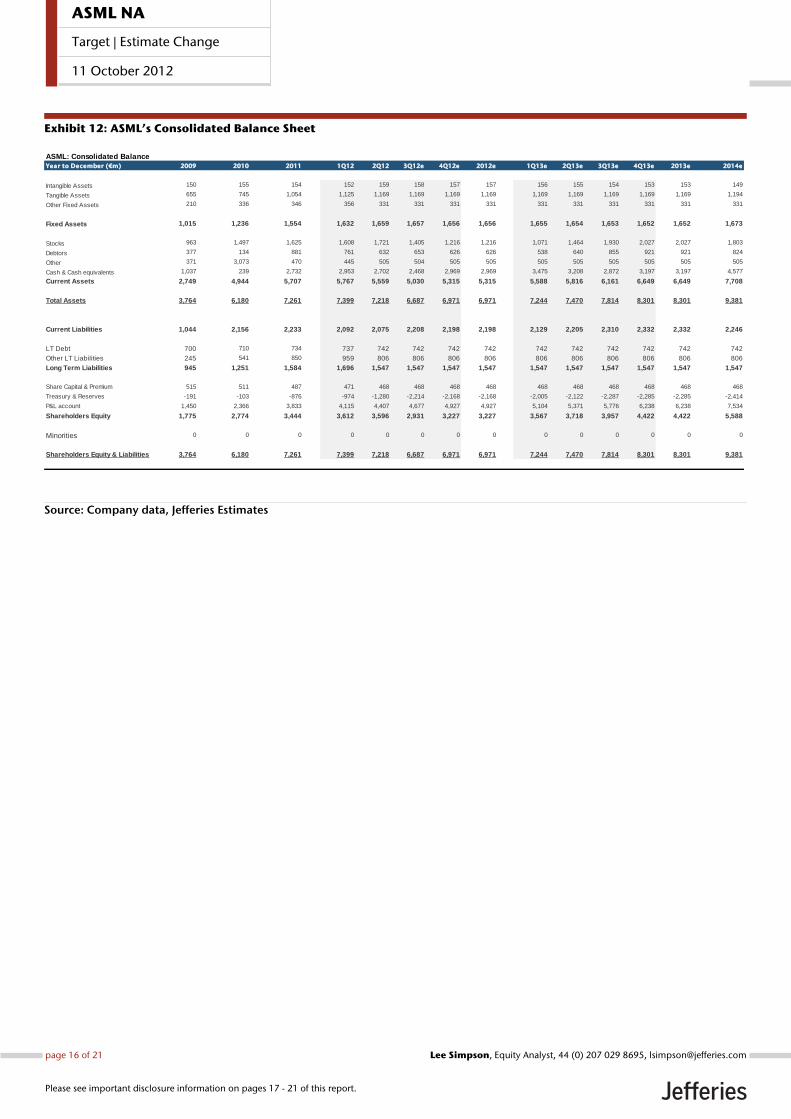

Exhibit 12: ASML’s Consolidated Balance Sheet

Source: Company data, Jefferies Estimates

2009 2010 2011 1Q12 2Q12 3Q12e 4Q12e 2012e 1Q13e 2Q13e 3Q13e 4Q13e 2013e 2014e

Intangible Assets 150 155 154 152 159 158 157 157 156 155 154 153 153 149

Tangible Assets 655 745 1,054 1,125 1,169 1,169 1,169 1,169 1,169 1,169 1,169 1,169 1,169 1,194

Other Fixed Assets 210 336 346 356 331 331 331 331 331 331 331 331 331 331

Fixed Assets 1,015 1,236 1,554 1,632 1,659 1,657 1,656 1,656 1,655 1,654 1,653 1,652 1,652 1,673

Stocks 963 1,497 1,625 1,608 1,721 1,405 1,216 1,216 1,071 1,464 1,930 2,027 2,027 1,803

Debtors 377 134 881 761 632 653 626 626 538 640 855 921 921 824

Other 371 3,073 470 445 505 504 505 505 505 505 505 505 505 505

Cash & Cash equivalents 1,037 239 2,732 2,953 2,702 2,468 2,969 2,969 3,475 3,208 2,872 3,197 3,197 4,577

Current Assets 2,749 4,944 5,707 5,767 5,559 5,030 5,315 5,315 5,588 5,816 6,161 6,649 6,649 7,708

Total Assets 3,764 6,180 7,261 7,399 7,218 6,687 6,971 6,971 7,244 7,470 7,814 8,301 8,301 9,381

Current Liabilities 1,044 2,156 2,233 2,092 2,075 2,208 2,198 2,198 2,129 2,205 2,310 2,332 2,332 2,246

LT Debt 700 710 734 737 742 742 742 742 742 742 742 742 742 742

Other LT Liabilities 245 541 850 959 806 806 806 806 806 806 806 806 806 806

Long Term Liabilities 945 1,251 1,584 1,696 1,547 1,547 1,547 1,547 1,547 1,547 1,547 1,547 1,547 1,547

Share Capital & Premium 515 511 487 471 468 468 468 468 468 468 468 468 468 468

Treasury & Reserves -191 -103 -876 -974 -1,280 -2,214 -2,168 -2,168 -2,005 -2,122 -2,287 -2,285 -2,285 -2,414

P&L account 1,450 2,366 3,833 4,115 4,407 4,677 4,927 4,927 5,104 5,371 5,776 6,238 6,238 7,534

Shareholders Equity 1,775 2,774 3,444 3,612 3,596 2,931 3,227 3,227 3,567 3,718 3,957 4,422 4,422 5,588

Minorities 0 0 0 0 0 0 0 0 0 0 0 0 0 0

Shareholders Equity & Liabilities 3,764 6,180 7,261 7,399 7,218 6,687 6,971 6,971 7,244 7,470 7,814 8,301 8,301 9,381

Year to December (€m)

ASML: Consolidated Balance

page 16 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Company DescriptionDutch-based (Veldhoven) ASML Holdings NV is the dominant supplier (75% share) of lithography equipment to the global semiconductorindustry. ASML designs, develops, integrates, markets and services lithography systems, which are necessary for the fabrication ofmicroelectronic chips. The company retains a focus on next-gen R&D and marketing whilst outsourcing c.90% of its production to third-party system assemblers. Formerly part of Philips, ASML was spun off in 1984 (renamed as Philips Labs). By 1988, Philips Labs was renamedas ASML and floated on the Amsterdam and New York exchanges. Today, ASML has a 100% free float.

Analyst CertificationI, Lee Simpson, certify that all of the views expressed in this research report accurately reflect my personal views about the subject security(ies) andsubject company(ies). I also certify that no part of my compensation was, is, or will be, directly or indirectly, related to the specific recommendationsor views expressed in this research report.Registration of non-US analysts: Lee Simpson is employed by Jefferies International Limited, a non-US affiliate of Jefferies & Company, Inc. andis not registered/qualified as a research analyst with FINRA. This analyst(s) may not be an associated person of Jefferies & Company, Inc., a FINRAmember firm, and therefore may not be subject to the NASD Rule 2711 and Incorporated NYSE Rule 472 restrictions on communications with a subjectcompany, public appearances and trading securities held by a research analyst.

As is the case with all Jefferies employees, the analyst(s) responsible for the coverage of the financial instruments discussed in this report receivescompensation based in part on the overall performance of the firm, including investment banking income. We seek to update our research asappropriate, but various regulations may prevent us from doing so. Aside from certain industry reports published on a periodic basis, the large majorityof reports are published at irregular intervals as appropriate in the analyst's judgement.

Rafi Hassan owns shares of Nividia Corporation common stock.Jefferies Group, Inc. makes a market in the securities or ADRs of ASML Holding NV.Jefferies Group, Inc. makes a market in the securities or ADRs of Intel Corporation.Jefferies Group, Inc. makes a market in the securities or ADRs of NVIDIA Corporation.Within the past twelve months, Jefferies & Company, Inc. and/or its affiliates received compensation for products and services other than investmentbanking services from non-investment banking, securities related compensation for client services it provided to Advanced Micro Devices, Inc..Within the past twelve months, Jefferies & Company, Inc. and/or its affiliates received compensation for products and services other than investmentbanking services from non-investment banking, securities related compensation for client services it provided to Intel Corporation.

Meanings of Jefferies RatingsBuy - Describes stocks that we expect to provide a total return (price appreciation plus yield) of 15% or more within a 12-month period.Hold - Describes stocks that we expect to provide a total return (price appreciation plus yield) of plus 15% or minus 10% within a 12-month period.Underperform - Describes stocks that we expect to provide a total negative return (price appreciation plus yield) of 10% or more within a 12-monthperiod.The expected total return (price appreciation plus yield) for Buy rated stocks with an average stock price consistently below $10 is 20% or more withina 12-month period as these companies are typically more volatile than the overall stock market. For Hold rated stocks with an average stock priceconsistently below $10, the expected total return (price appreciation plus yield) is plus or minus 20% within a 12-month period. For Underperformrated stocks with an average stock price consistently below $10, the expected total return (price appreciation plus yield) is minus 20% within a 12-month period.NR - The investment rating and price target have been temporarily suspended. Such suspensions are in compliance with applicable regulations and/or Jefferies policies.CS - Coverage Suspended. Jefferies has suspended coverage of this company.NC - Not covered. Jefferies does not cover this company.Restricted - Describes issuers where, in conjunction with Jefferies engagement in certain transactions, company policy or applicable securitiesregulations prohibit certain types of communications, including investment recommendations.Monitor - Describes stocks whose company fundamentals and financials are being monitored, and for which no financial projections or opinions onthe investment merits of the company are provided.

Valuation MethodologyJefferies' methodology for assigning ratings may include the following: market capitalization, maturity, growth/value, volatility and expected totalreturn over the next 12 months. The price targets are based on several methodologies, which may include, but are not restricted to, analyses of marketrisk, growth rate, revenue stream, discounted cash flow (DCF), EBITDA, EPS, cash flow (CF), free cash flow (FCF), EV/EBITDA, P/E, PE/growth, P/CF,P/FCF, premium (discount)/average group EV/EBITDA, premium (discount)/average group P/E, sum of the parts, net asset value, dividend returns,and return on equity (ROE) over the next 12 months.

Conviction List Methodology

1. The aim of the conviction list is to publicise the best individual stock ideas from Jefferies Global Research2. Only stocks with a Buy rating are allowed to be included in the recommended list.3. Stocks are screened for minimum market capitalisation and adequate daily turnover. Furthermore, a valuation, correlation and style screen

is used to ensure a well-diversified portfolio.4. Stocks are sorted to a maximum of 30 stocks with the maximum country exposure at around 50%. Limits are also imposed on a sector basis.5. Once a month, analysts are invited to recommend their best ideas. Analysts’ stock selection can be based on one or more of the following:

non-Consensus investment view, difference in earnings relative to Consensus, valuation methodology, target upside/downside % relative

page 17 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

to the current stock price. These are then assessed against existing holdings to ensure consistency. Stocks that have either reached theirtarget price, been downgraded over the course of the month or where a more suitable candidate has been found are removed.

6. All stocks are inserted at the last closing price and removed at the last closing price. There are no changes to the conviction list duringthe month.

7. Performance is calculated in US dollars on an equally weighted basis and is compared to MSCI World AC US$.8. The conviction list is published once a month whilst global equity markets are closed.9. Transaction fees are not included.

10. All corporate actions are taken into account.

Risk which may impede the achievement of our Price TargetThis report was prepared for general circulation and does not provide investment recommendations specific to individual investors. As such, thefinancial instruments discussed in this report may not be suitable for all investors and investors must make their own investment decisions basedupon their specific investment objectives and financial situation utilizing their own financial advisors as they deem necessary. Past performance ofthe financial instruments recommended in this report should not be taken as an indication or guarantee of future results. The price, value of, andincome from, any of the financial instruments mentioned in this report can rise as well as fall and may be affected by changes in economic, financialand political factors. If a financial instrument is denominated in a currency other than the investor's home currency, a change in exchange rates mayadversely affect the price of, value of, or income derived from the financial instrument described in this report. In addition, investors in securities suchas ADRs, whose values are affected by the currency of the underlying security, effectively assume currency risk.

Other Companies Mentioned in This Report• Advanced Micro Devices, Inc. (AMD: $3.15, BUY)• Intel Corporation (INTC: $21.76, HOLD)• NVIDIA Corporation (NVDA: $12.67, HOLD)

page 18 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

page 19 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

Distribution of RatingsIB Serv./Past 12 Mos.

Rating Count Percent Count Percent

BUY 743 47.32% 117 15.75%HOLD 708 45.10% 78 11.02%UNDERPERFORM 119 7.58% 0 0.00%

Other Important Disclosures

Jefferies Equity Research refers to research reports produced by analysts employed by one of the following Jefferies Group, Inc. (“Jefferies”) groupcompanies:

United States: Jefferies & Company, Inc., which is an SEC registered firm and a member of FINRA.

United Kingdom: Jefferies International Limited, which is authorized and regulated by the Financial Services Authority; registered in England andWales No. 1978621; registered office: Vintners Place, 68 Upper Thames Street, London EC4V 3BJ; telephone +44 (0)20 7029 8000; facsimile +44 (0)207029 8010.

Hong Kong: Jefferies Hong Kong Limited, which is licensed by the Securities and Futures Commission of Hong Kong with CE number ATS546; locatedat Suite 2201, 22nd Floor, Cheung Kong Center, 2 Queen’s Road Central, Hong Kong.

Singapore: Jefferies Singapore Limited, which is licensed by the Monetary Authority of Singapore; located at 80 Raffles Place #15-20, UOB Plaza 2,Singapore 048624, telephone: +65 6551 3950.

Japan: Jefferies (Japan) Limited, Tokyo Branch, which is a securities company registered by the Financial Services Agency of Japan and is a memberof the Japan Securities Dealers Association; located at Hibiya Marine Bldg, 3F, 1-5-1 Yuraku-cho, Chiyoda-ku, Tokyo 100-0006; telephone +813 52516100; facsimile +813 5251 6101.

India: Jefferies India Private Limited, which is licensed by the Securities and Exchange Board of India as a Merchant Banker (INM000011443) and a StockBroker with Bombay Stock Exchange Limited (INB011438539) and National Stock Exchange of India Limited (INB231438533) in the Capital MarketSegment; located at 42/43, 2 North Avenue, Maker Maxity, Bandra-Kurla Complex, Bandra (East) Mumbai 400 051, India; Tel +91 22 4356 6000.

This material has been prepared by Jefferies employing appropriate expertise, and in the belief that it is fair and not misleading. The information setforth herein was obtained from sources believed to be reliable, but has not been independently verified by Jefferies. Therefore, except for any obligationunder applicable rules we do not guarantee its accuracy. Additional and supporting information is available upon request. Unless prohibited by theprovisions of Regulation S of the U.S. Securities Act of 1933, this material is distributed in the United States ("US"), by Jefferies & Company, Inc.,a US-registered broker-dealer, which accepts responsibility for its contents in accordance with the provisions of Rule 15a-6, under the US SecuritiesExchange Act of 1934. Transactions by or on behalf of any US person may only be effected through Jefferies & Company, Inc. In the United Kingdomand European Economic Area this report is issued and/or approved for distribution by Jefferies International Limited and is intended for use onlyby persons who have, or have been assessed as having, suitable professional experience and expertise, or by persons to whom it can be otherwiselawfully distributed. Jefferies International Limited has adopted a conflicts management policy in connection with the preparation and publicationof research, the details of which are available upon request in writing to the Compliance Officer. Jefferies International Limited may allow its analyststo undertake private consultancy work. Jefferies International Limited’s conflicts management policy sets out the arrangements Jefferies InternationalLimited employs to manage any potential conflicts of interest that may arise as a result of such consultancy work. For Canadian investors, this materialis intended for use only by professional or institutional investors. None of the investments or investment services mentioned or described herein ispage 20 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012

available to other persons or to anyone in Canada who is not a "Designated Institution" as defined by the Securities Act (Ontario). For investors inthe Republic of Singapore, this material is provided by Jefferies Singapore Limited pursuant to Regulation 32C of the Financial Advisers Regulations.The material contained in this document is intended solely for accredited, expert or institutional investors, as defined under the Securities and FuturesAct (Cap. 289 of Singapore). If there are any matters arising from, or in connection with this material, please contact Jefferies Singapore Limited. InJapan this material is issued and distributed by Jefferies (Japan) Limited to institutional investors only. In Hong Kong, this report is issued and approvedby Jefferies Hong Kong Limited and is intended for use only by professional investors as defined in the Hong Kong Securities and Futures Ordinanceand its subsidiary legislation. In the Republic of China (Taiwan), this report should not be distributed. In India this report is made available by JefferiesIndia Private Limited. In Australia this information is issued solely by Jefferies International Limited and is directed solely at wholesale clients withinthe meaning of the Corporations Act 2001 of Australia (the "Act") in connection with their consideration of any investment or investment servicethat is the subject of this document. Any offer or issue that is the subject of this document does not require, and this document is not, a disclosuredocument or product disclosure statement within the meaning of the Act. Jefferies International Limited is authorised and regulated by the FinancialServices Authority under the laws of the United Kingdom, which differ from Australian laws. Jefferies International Limited has obtained relief underAustralian Securities and Investments Commission Class Order 03/1099, which conditionally exempts it from holding an Australian financial serviceslicence under the Act in respect of the provision of certain financial services to wholesale clients. Recipients of this document in any other jurisdictionsshould inform themselves about and observe any applicable legal requirements in relation to the receipt of this document.

This report is not an offer or solicitation of an offer to buy or sell any security or derivative instrument, or to make any investment. Any opinion orestimate constitutes the preparer's best judgment as of the date of preparation, and is subject to change without notice. Jefferies assumes no obligationto maintain or update this report based on subsequent information and events. Jefferies, its associates or affiliates, and its respective officers, directors,and employees may have long or short positions in, or may buy or sell any of the securities, derivative instruments or other investments mentioned ordescribed herein, either as agent or as principal for their own account. Upon request Jefferies may provide specialized research products or servicesto certain customers focusing on the prospects for individual covered stocks as compared to other covered stocks over varying time horizons orunder differing market conditions. While the views expressed in these situations may not always be directionally consistent with the long-term viewsexpressed in the analyst's published research, the analyst has a reasonable basis and any inconsistencies can be reasonably explained. This materialdoes not constitute a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individualclients. Clients should consider whether any advice or recommendation in this report is suitable for their particular circumstances and, if appropriate,seek professional advice, including tax advice. The price and value of the investments referred to herein and the income from them may fluctuate. Pastperformance is not a guide to future performance, future returns are not guaranteed, and a loss of original capital may occur. Fluctuations in exchangerates could have adverse effects on the value or price of, or income derived from, certain investments. This report has been prepared independently ofany issuer of securities mentioned herein and not in connection with any proposed offering of securities or as agent of any issuer of securities. Noneof Jefferies, any of its affiliates or its research analysts has any authority whatsoever to make any representations or warranty on behalf of the issuer(s).Jefferies policy prohibits research personnel from disclosing a recommendation, investment rating, or investment thesis for review by an issuer priorto the publication of a research report containing such rating, recommendation or investment thesis. Any comments or statements made herein arethose of the author(s) and may differ from the views of Jefferies.

This report may contain information obtained from third parties, including ratings from credit ratings agencies such as Standard & Poor’s. Reproductionand distribution of third party content in any form is prohibited except with the prior written permission of the related third party. Third party contentproviders do not guarantee the accuracy, completeness, timeliness or availability of any information, including ratings, and are not responsible forany errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such content. Third party contentproviders give no express or implied warranties, including, but not limited to, any warranties of merchantability or fitness for a particular purpose oruse. Third party content providers shall not be liable for any direct, indirect, incidental, exemplary, compensatory, punitive, special or consequentialdamages, costs, expenses, legal fees, or losses (including lost income or profits and opportunity costs) in connection with any use of their content,including ratings. Credit ratings are statements of opinions and are not statements of fact or recommendations to purchase, hold or sell securities. Theydo not address the suitability of securities or the suitability of securities for investment purposes, and should not be relied on as investment advice.

Jefferies research reports are disseminated and available primarily electronically, and, in some cases, in printed form. Electronic research issimultaneously available to all clients. This report or any portion hereof may not be reprinted, sold or redistributed without the written consent ofJefferies. Neither Jefferies nor any officer nor employee of Jefferies accepts any liability whatsoever for any direct, indirect or consequential damagesor losses arising from any use of this report or its contents.

For Important Disclosure information, please visit our website at https://javatar.bluematrix.com/sellside/Disclosures.action or call 1.888.JEFFERIES

© 2012 Jefferies Group, Inc.

page 21 of 21 , Equity Analyst, 44 (0) 207 029 8695, [email protected] Simpson

Please see important disclosure information on pages 17 - 21 of this report.

ASML NA

Target | Estimate Change

11 October 2012