Embed Size (px)

Citation preview

EUV – Supporting Moore’s Law

Jefferies 2014 Global TMT Conference

Miami, Florida

May 06, 2014

Craig De Young

Vice President of Investor Relations

Forward looking statements

“Safe Harbor” Statement under the US Private Securities Litigation Reform Act of 1995: the matters discussed in this document may include forward-looking statements, including statements made about our outlook, expected sales levels, IC unit demand, forecasted industry developments, including expected bit growth in 2014, expected semiconductor sales and expected smartphone, tablet and PC use in future years, expectations on development of the shrink roadmap across all of our systems, expected number of EUV systems to be recognized in 2014, expectations on timing for volume production for EUV systems and other statements about the expected development of EUV technology and its adoption by our customers.

These forward looking statements are subject to risks and uncertainties including: economic conditions, product demand and semiconductor equipment industry capacity, worldwide demand and manufacturing capacity utilization for semiconductors (the principal product of our customer base), including the impact of general economic conditions on consumer confidence and demand for our customers' products, competitive products and pricing, the impact of manufacturing efficiencies and capacity constraints, the continuing success of technology advances and the related pace of new product development and customer acceptance of new products, our ability to enforce patents and protect intellectual property rights, the risk of intellectual property litigation, availability of raw materials and critical manufacturing equipment, trade environment, changes in exchange rates, available cash, our ability to successfully integrate Cymer, and other risks indicated in the risk factors included in ASML's Annual Report on Form 20-F and other filings with the US Securities and Exchange Commission.

May 6 2014

Public

Slide 2

Content

May 6 2014

Slide 3

• Semiconductor environment

• Challenges of shrink

• Our response: the lithography roadmap

Public

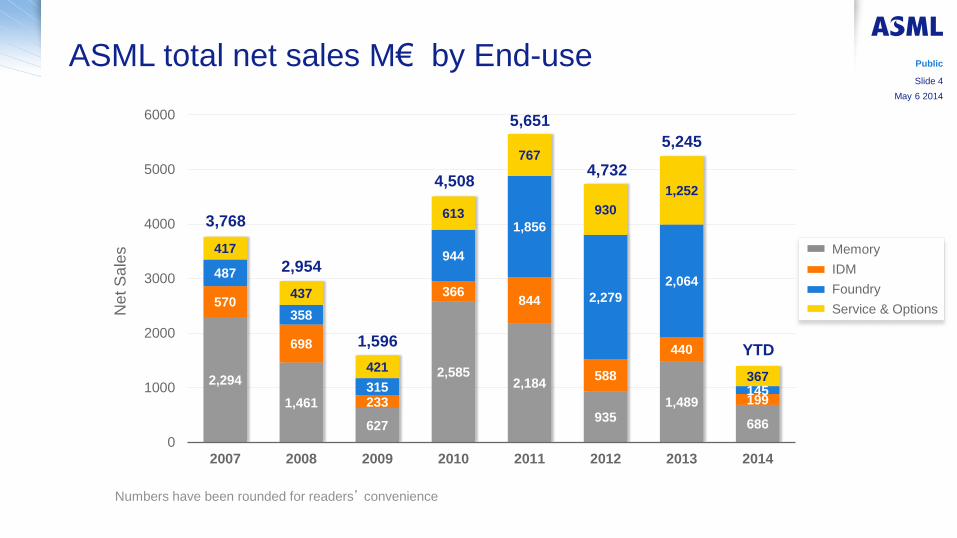

2,294

1,461

627

2,585 2,184

935 1,489

686

570

698

233

366 844

588

440

199

487

358

315

944

1,856

2,279

2,064

145

417

437

421

613

767

930

1,252

367

0

1000

2000

3000

4000

5000

6000

2007 2008 2009 2010 2011 2012 2013 2014

Net S

ale

s

ASML total net sales M€ by End-use May 6 2014

Public

Slide 4

3,768

Numbers have been rounded for readers’ convenience

2,954

1,596

4,508

5,651

Memory

IDM

Foundry

Service & Options

4,732

5,245

YTD

Business environment for 2014

• Bit growth forecast mid 40s% driven by SSD drives and smartphones

• Demand being met through shrink and capacity expansion

• Challenges in qualification of vertical NAND and future node planar

technologies, creating litho demand timing uncertainty

• Bit growth forecast of 20 - 30%

• Bits supplied by planned technology transitions meet bit demand forecast

• Litho process intensity increases due to node transition and mobile DRAM

process complexity

May 6 2014

Public

Slide 5

• Customers are installing capacity for their 20/16/14 nm nodes

• Timing uncertainty in next generation device designs and production ramps

Longer term Logic growth is in Mobile Creating Logic market share battles

May 6 2014

Slide 6

Public

Source: Bob Johnson,Gartner, ISS, Jan 2014

Mobile

Market growth

2011-2017

Premium Smartphone

Basic Smartphone

Traditional Mobile Phone

Premium tablet

Basic Tablet

PC. Ultra Mobile

PC. Notebook

PC. Desktop

2011 2013 2015 2017 2012 2014 2016

140

120

100

80

60

40

20

0

160

Semiconductor Sales

$B

+60%

Semi Mobile/PC

+400% Traditional

-20%

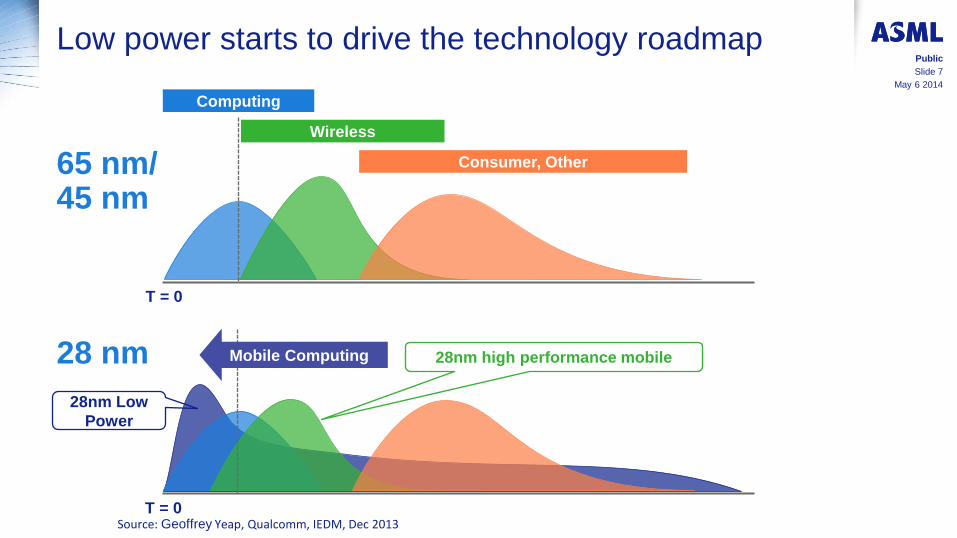

Low power starts to drive the technology roadmap

Source: Geoffrey Yeap, Qualcomm, IEDM, Dec 2013

65 nm/ 45 nm

28 nm

Computing

Wireless

Consumer, Other

T = 0

T = 0

Mobile Computing

28nm Low

Power

28nm high performance mobile

May 6 2014

Public

Slide 7

Source: IHS Electronics & Media, January 2014

The Smartphone boom Foundries and fabless drive the logic market

May 6 2014

Public

Slide 8

Content

May 6 2014

Slide 9

• Semiconductor environment

• Challenges of shrink

• Our response: the lithography roadmap

Public

No end in sight for logic scaling

N20 N20 / N14 N1x / N7 N7 / N5 N5 / N3.5

SOI: Silicon on Insulator

Bulk FinFet : Fin field effect

transistor

SOI FinFet : Silicon on insulator

fin field effect

transistor, III-V

Gate-all-around

transistor

Bulk CMOS: Complementary

Metal Oxide

Semiconductor

May 6 2014

Public

Slide 10

Bulk CMOS:100nm gate length

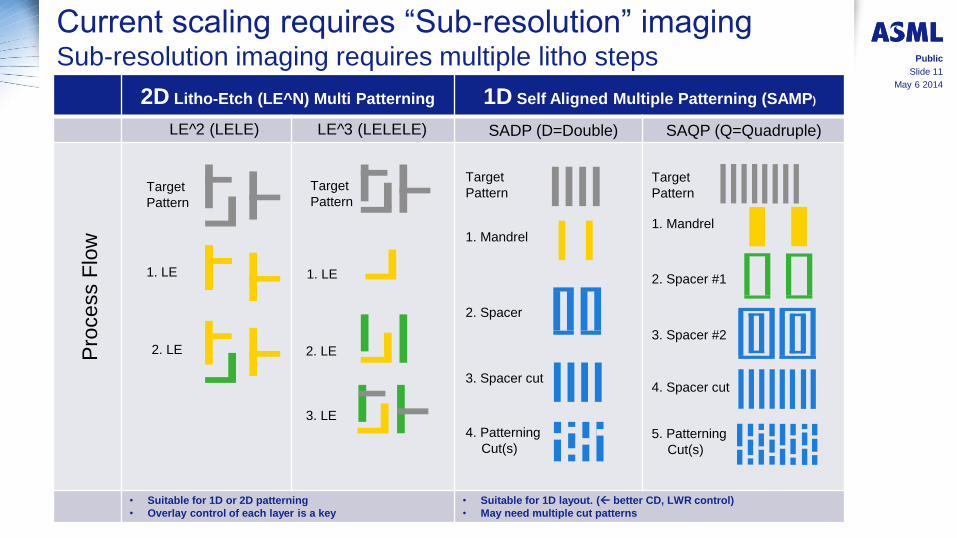

Current scaling requires “Sub-resolution” imaging Sub-resolution imaging requires multiple litho steps

2D Litho-Etch (LE^N) Multi Patterning 1D Self Aligned Multiple Patterning (SAMP)

• Suitable for 1D or 2D patterning

• Overlay control of each layer is a key

• Suitable for 1D layout. ( better CD, LWR control)

• May need multiple cut patterns

LE^2 (LELE) LE^3 (LELELE) SADP (D=Double) SAQP (Q=Quadruple)

1. Mandrel

2. Spacer

3. Spacer cut

Pro

cess F

low

1. LE

2. LE

Target

Pattern

Target

Pattern Target

Pattern

Target

Pattern

2. LE

1. LE

3. LE

1. Mandrel

2. Spacer #1

3. Spacer #2

4. Spacer cut

5. Patterning

Cut(s)

4. Patterning

Cut(s)

May 6 2014

Public

Slide 11

Content Slide 12

• Semiconductor environment

• Challenges of shrink

• Our response: the litho roadmap

Public

May 6 2014

Our Challenge: enable affordable scaling Slide 13

• Scaling needs to create lower cost and

improved performance – ie., support Moore’s Law

• Affordable scaling in lithography can be achieved:

• In the near term - Immersion: drive productivity and yield

(overlay and focus control) with multiple patterning using

advanced litho equipment extended with application

products - Holistic Lithography/Yieldstar

• In the mid/long term - EUV: drive productivity/availability

and improve operational cost

Public

May 6 2014

NXE:3300B, NXE:3350C, …

NXT:1950i, NXT:1960Bi, NXT:1970Ci

Affordable shrink roadmap

May 6 2014

Slide 14

2012 2013 2014 2015 2016 2017

ArF

Dry

KrF

2018 2019 2020

EU

V

Imm

ers

ion

DCO 2.5 nm <1.0 nm

CDU 2.0 nm 0.6 nm

Throughput 230 wafers per hour (wph) >250 wph

Resolution 27 nm 7 nm

EUV to immersion overlay 7.0 nm 1.7 nm

Throughput 50 wph >125 wph

XT:1460,1060,860

Overlay main driver in logic/foundry (ArF with 1460K system

and KrF with 1060K system)

Extend the productivity on the non critical KrF (XT:860L/800-

3D): memory applications

Supported by a Holistic

Lithography approach using

computational litho, overlay

and CD metrology, feedback

loops for wider process

window creation and process

control

Public

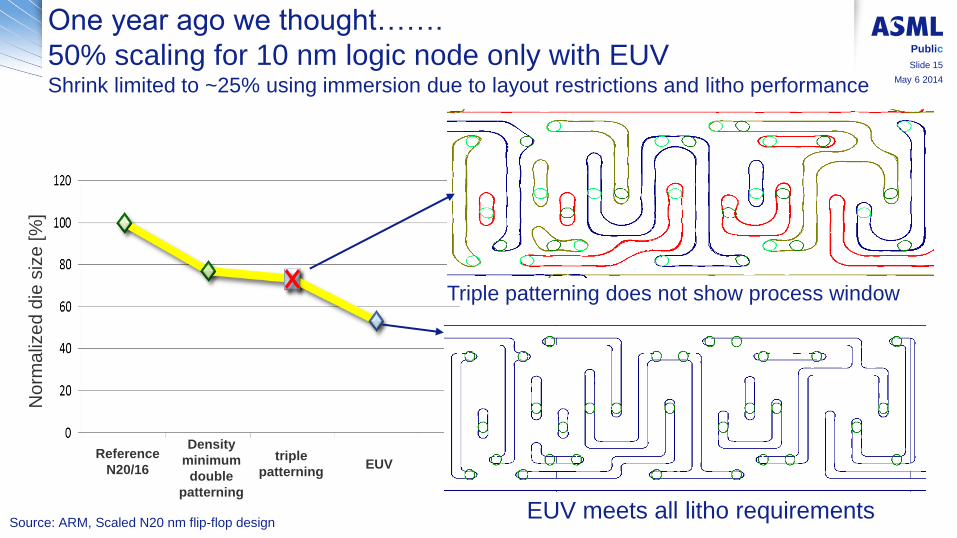

One year ago we thought…….

50% scaling for 10 nm logic node only with EUV Shrink limited to ~25% using immersion due to layout restrictions and litho performance

Reference

N20/16

Density

minimum

double

patterning

triple

patterning EUV

No

rma

lize

d d

ie s

ize

[%

]

Source: ARM, Scaled N20 nm flip-flop design EUV meets all litho requirements

Triple patterning does not show process window

Slide 15

Public

May 6 2014

One year ago we thought…….

50% scaling for 10 nm logic node only with EUV Shrink limited to ~25% using immersion due to layout restrictions and litho performance

EUV 2D metal structure

Single layer solution

ArFi 2D metal structure

3-4 exposures, single layer

insufficient patterning fidelity

Slide 16

Public

May 6 2014

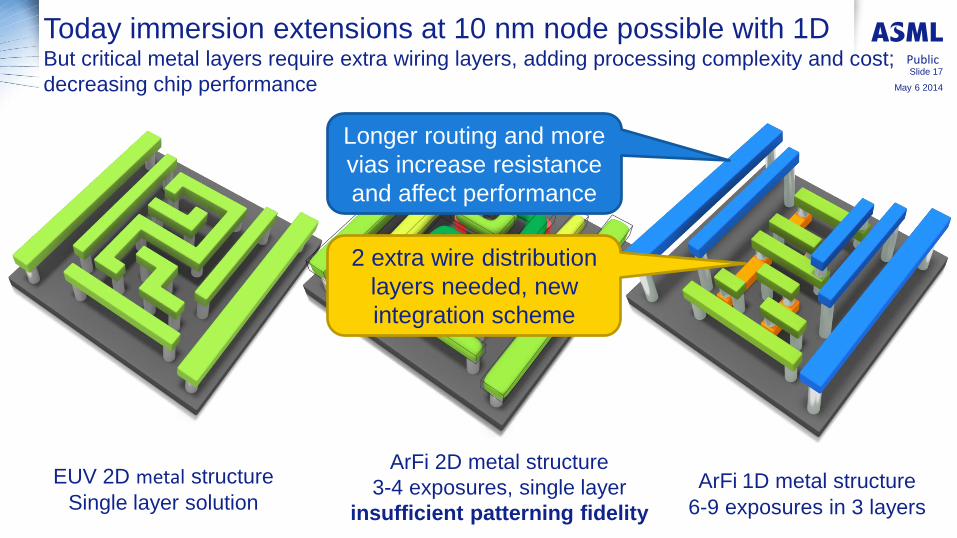

Today immersion extensions at 10 nm node possible with 1D But critical metal layers require extra wiring layers, adding processing complexity and cost;

decreasing chip performance

EUV 2D metal structure

Single layer solution ArFi 1D metal structure

6-9 exposures in 3 layers

ArFi 2D metal structure

3-4 exposures, single layer

insufficient patterning fidelity

Longer routing and more

vias increase resistance

and affect performance

2 extra wire distribution

layers needed, new

integration scheme

Slide 17

Public

May 6 2014

10nm logic design can be done in 1D design w/ immersion

But at the cost of 15% larger dies at comparable design rules May 6 2014

Public

Slide 18

2D

Die Size: 100%

1D

Die Size: 115%

EUV Immersion multi-pass

patterning

0.1

1

40 nm 28 nm 20/16 nm 10 nm 7 nm 5 nm

Critical metal cost/immersion

Patterning cost per flop/immersion

Moore's law

Patte

rnin

g c

ost

norm

aliz

ed to N

20/N

16

Cost: 1D/immersion vs 2D/EUV

Critical metal 1D density

requires extra layers, results in

steep cost increase

Shrink is possible with 1D

designs using immersion, but

cost reduction slows

May 6 2014

Slide 19

Public

The flip flop is a basic

building block of

sequential logic

circuits.

0.1

1

40 nm 28 nm 20/16 nm 10 nm 7 nm 5 nm

Critical metal cost/immersion

Critical metal cost/EUV

Patterning cost per flop/immersion

Patterning cost per flop/EUV

Moore's law

Cost: 1D/immersion vs 2D/EUV

Staying with 2D designs using EUV at N10

is more cost-effective, but risk mitigation

may force 1D design with multiple patterning

Patte

rnin

g c

ost

norm

aliz

ed to N

20/N

16

2D EUV: critical

metal cost

dramatically

reduced

May 6 2014

Slide 20

Public

The flip flop is a basic

building block of

sequential logic

circuits.

EUV: Evaluations for 10nm process insertion underway May 6 2014

Public

Slide 21

Large vacuum

chamber

Mirror optics

New light

source

EUV – progress toward production insertion

• Customers are qualifying EUV for insertion at the 10 nm logic node

• For process development, customers typically require 100 wafers per day,

increasing to 500 wafers per day on average for production qualification

• We have provided customers with process development capability

• In 2016 we will provide our customers with the productivity needed for

volume production, 1500wpd -> 2000wpd

• Our target is to recognize a total of 8 EUV systems in revenue this year

May 6 2014

Public

Slide 22

NXE:3100 in use for cycles of learning at customers 6 systems operational at customers for multiple years

Ac

cu

mu

late

d w

afe

rs e

xp

os

ed

on

NX

E:3

10

0

0

10000

20000

30000

40000

50000

60000

70000

80000

20

10

26

20

10

32

20

10

38

20

10

44

20

10

50

20

11

04

20

11

10

20

11

16

20

11

22

20

11

28

20

11

34

20

11

40

20

11

46

20

11

52

20

12

06

20

12

12

20

12

18

20

12

24

20

12

30

20

12

36

20

12

42

20

12

48

20

13

02

20

13

08

20

13

14

20

13

20

20

13

26

20

13

32

20

13

38

20

13

44

20

13

50

20

14

04

Slide 23

Public

May 6 2014

NXE:3100 shows stable performance and is used for

device development at customer sites

Data courtesy of TSMC and imec – EUVL Toyama 2013

Slide 24

Public

May 6 2014

Full wafer CDU = 1.5nm

22nm HP

BE = 15.9 mJ/cm2

EL = 13% DoF = 160 nm

13 nm HP (Inpria) 9 nm HP

EUV Spacer

NXE:3300B Excellent single exposure imaging performance

16 nm HP (CAR)

22nm 31nm 17nm

2D Contact

10nm Metal 1

Tip-Line, Tip-Tip

1D line spaces

Slide 25

Public

May 6 2014

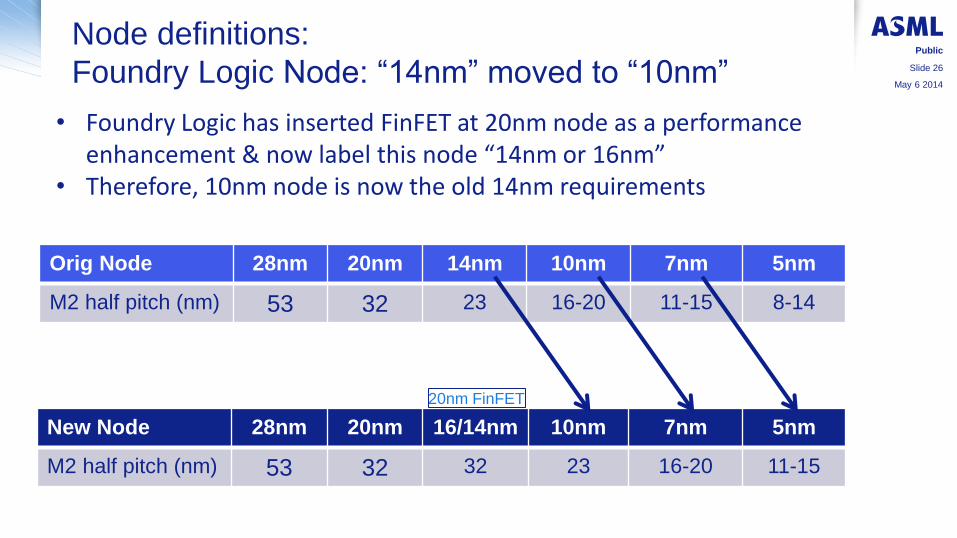

Node definitions:

Foundry Logic Node: “14nm” moved to “10nm” Public

Slide 26

• Foundry Logic has inserted FinFET at 20nm node as a performance enhancement & now label this node “14nm or 16nm”

• Therefore, 10nm node is now the old 14nm requirements

New Node 28nm 20nm 16/14nm 10nm 7nm 5nm

M2 half pitch (nm) 53 32 32 23 16-20 11-15

Orig Node 28nm 20nm 14nm 10nm 7nm 5nm

M2 half pitch (nm) 53 32 23 16-20 11-15 8-14

20nm FinFET

May 6 2014

NXE:3300B showing excellent matched machine overlay

performance on multiple systems to immersion

Systems

Mat

ched

Mac

hin

e

Ove

rlay

[n

m]

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

1 2 3 4

Overlay X Overlay Y

Slide 27

Public

May 6 2014

EUV meets aggressive 2D logic imaging requirements

0

10

20

30

40

50

60

70

80

20 nm 16 nm 10 nm 7 nm

CD

[n

m]

CD requirements by node

Tip-to-tip Tip-to-line Lines and spaces

31nm

22nm

16nm

* using high dose resist @ ~50mJ

EUV (SE)* Slide 28

Public

May 6 2014

• Multiple NXE:3300B systems fully qualified

• 2 systems exposing wafers at the customer sites

• 3 systems under install

EUV (NXE:33x0B) system status overview

• 6 more NXE:3300B systems being integrated

• First NXE:3350B system has been started

• EUV cleanroom extension is under construction

Slide 29

Public

May 6 2014

Under study

Resolution [nm] 32 27 22 16 13 10 7 <7

layo

ut NA 0.25 0.33

13.5

Lens flare 8% 6% 4%

Illumination Flex-OAI s=0.8 Extended Flex-OAI

reduced pupil fill ratio

0.33NA DPT

s=0.5 s=0.2-0.9 coherence

Wavelength [nm]

4.0 7 3.0 DCO [nm]

MMO [nm] 7.0 - 5.0

1.2 1.5 1.0

2.0 2.5 1.7

pupil fill ratio defined as the

bright fraction of the pupil

Overlay

10 5 15 Dose [mJ/cm2]

Power [W] 10 - 105 3 80 - 250

20 20

250 250 TPT (300mm)

Throughphut [w/hr] 6 - 60 - 50 - 125 125 125

20

500

165

NXE technology roadmap - extendibility to <7nm (half pitch)

>0.5NA

Slide 30

Public

Half pitch

May 6 2014

EUV results summary and status Slide 31 Summary

• NXE:3300B operational and exposing wafers at customer sites

• Performance fit for customer development 10nm Logic (and sub-20nm DRAM) and beyond

Status

1. EUV lithography technology is proven and is entering the industrialization phase

2. The EUV qualification requires 100 wafer per day output, which is determined by:

a) Power: Supporting 30 wafers per hour

b) Availability: Of greater than 50%

3. For pre-production customers have asked us to deliver 500 wafers per day by the end of 2014.

4. The full market potential of EUV will be realized at 125 wafers per hour and system availability >

90%. This will happen as a result of series of stepped through-put and reliability/availability

upgrades.

5. The value of EUV is undisputed as the lithographic shrink technology of choice for multiple nodes

starting in 2016/2017.

6. Our customers and peers continue to support and drive development of EUV systems and

infrastructure for introduction of EUV into volume production in the stated timeframe.

Public

May 6 2014