Embed Size (px)

Citation preview

Asian agricultural markets: export potential for inland

N e w South Wales

Asian agricultural markets: .

export potential for inland N e w South Wales

Report by ABARE and AUSTRADE

May 1997

0 AUS? T R A D E ABARE

Asian agricultural markets: export potential for inland New South Wales, Report by ABARE and AUSTRADE, Canberra.

Australian Bureau of Agricultural and Resource Economics GPO Box 1563 Canberra 2601

Telephone (06) 272 2000 Facsimile (06) 272 2001 Internet http://www.abare.gov.au

ABARE is a professionally independent government economic research agency.

ASIAN AGRICULTURAL MARKETS

Summary

Over the past three decades the importance of the Asian markets have grown and they are

now the most important destination for many of the agricultural products grown in the

inland region of New South Wales. The importance of the Asian markets for farmers in this

region has been recognised by Senator the Hon David Brownhill, Parliamentary Secretary

to the Ministers for Trade and Primary Industries and Energy, and as a result ABARE and

Austrade collaborated on compiling this report.

The rapidly growing Asian markets offer considerable potential for expanding agricultural

trade. Indeed, many examples of growth in Asian imports of Australian agricultural

products were identified by Austrade officers in reviewing Asian import trends.

While there are indications of considerable oppo~tunities for exports of agricultural

products that are or could be produced in inland New South Wales, there are nevertheless

considerable hurdles to overcome in establishing and maintaining an export market in Asia.

Of particular importance are the trade barriers (tariffs and other trade measures) used in

various countries and the cultural differences between Asian countries and Australia. In

addition, the Asian market has become the focus of attention of many agricultural exporters

and prospective Australian exporters will need to compete with these exporters as well as

domestic Asian producers on quality, consistency of supply and price.

ASIAN AGRICULTURAL MARKETS

1 Introduction

The aim in this report is to provide to growers and marketers in inland New South Wales

an indication of the potential for growth in agricultural exports to markets in Asia. The

nature of agricultural production in inland New South Wales is outlined in the next section.

In section 3 the trends in Asian agricultural imports are discussed and detailed in an

extensive table compiled from information provided by Austrade officers based in various

Asian countries and from statistical and tariff data provided by the Department of Foreign

Affairs and Trade. As well as discussing the opportunities for Australian exports, in section

3 recognition is given to the need for market development by exporters and the potential

problems and trade baniers exporters may face. Finally, to assist those interested in

seeking further information or assistance in pinpointing export opportunities or developing

an export potential a list of contacts is given.

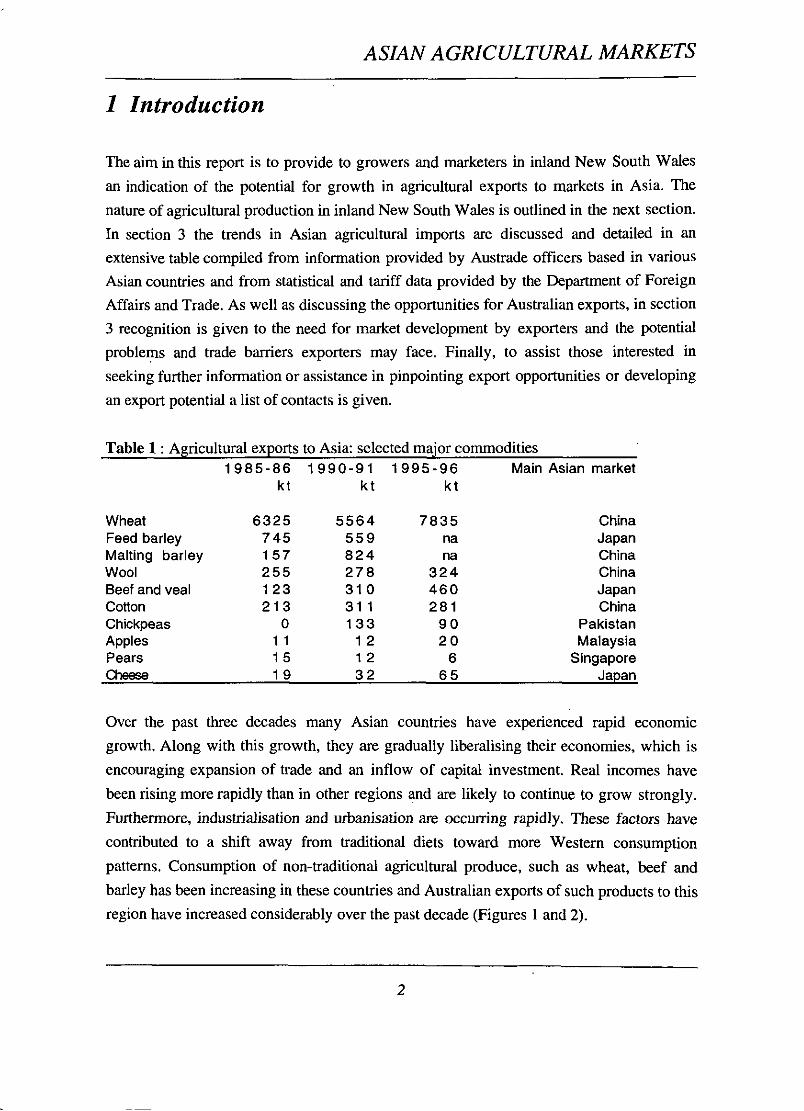

Table 1 : Agricultural exports to Asia: selected major commodities 1985-86 1990-91 1995-96 Main Asian market

kt k t k t

Wheat 6325 5564 7835 China Feed barley 745 559 na Japan Malting barley 157 824 na China Wool 255 278 324 China Beef and veal 123 31 0 460 Japan cotton 213 31 1 281 China Chickpeas 0 133 9 0 Pakistan Apples 1 1 12 2 0 Malaysia Pears 15 12 6 Singapore Cheese 19 3 2 6 5 Japan

Over the past three decades many Asian countries have experienced rapid economic

growth. Along with this growth, they are gradually liberalising their economies, which is

encouraging expansion of trade and an inflow of capital investment. Real incomes have

been rising more rapidly than in other regions and are likely to continue to grow strongly.

Furthermore, industrialisation and urbanisation are occurring rapidly. These factors have

contributed to a shift away from traditional diets toward more Western consumption

patterns. Consumption of non-traditional agricultural produce, such as wheat, beef and

barley has been increasing in these countries and Australian exports of such products to this

region have increased considerably over the past decade (Figures 1 and 2).

ASIAN AGRICULTURAL MARKETS

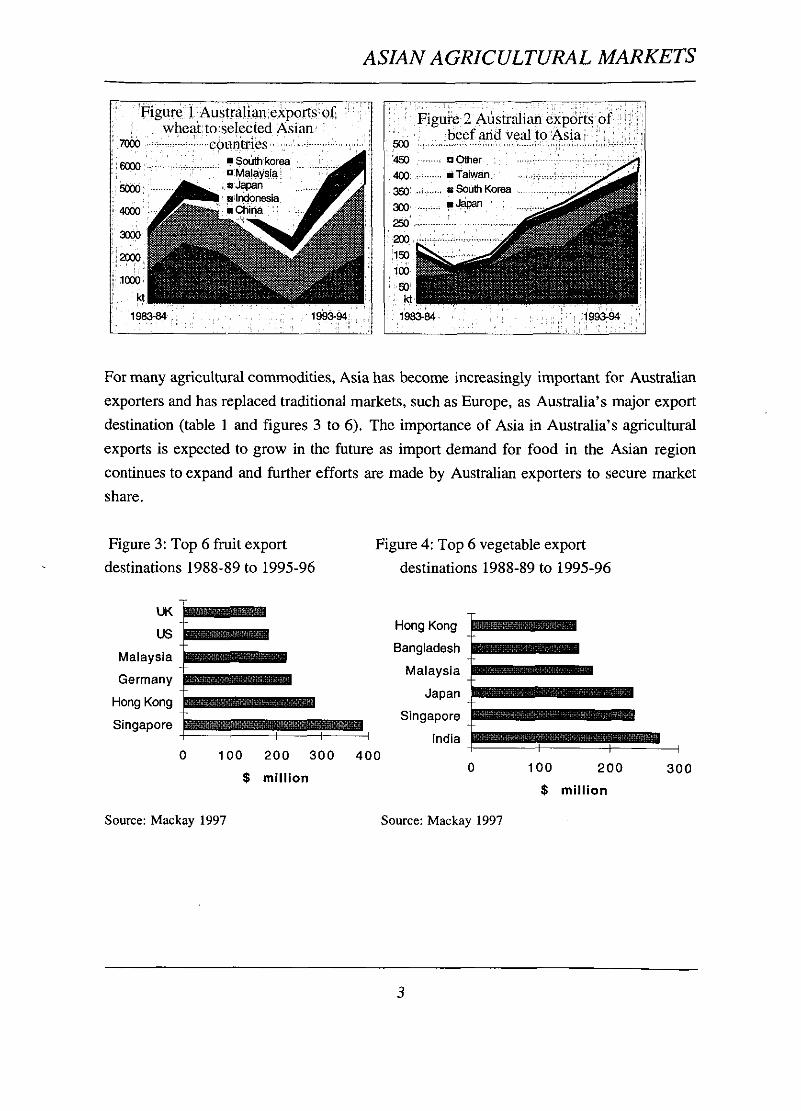

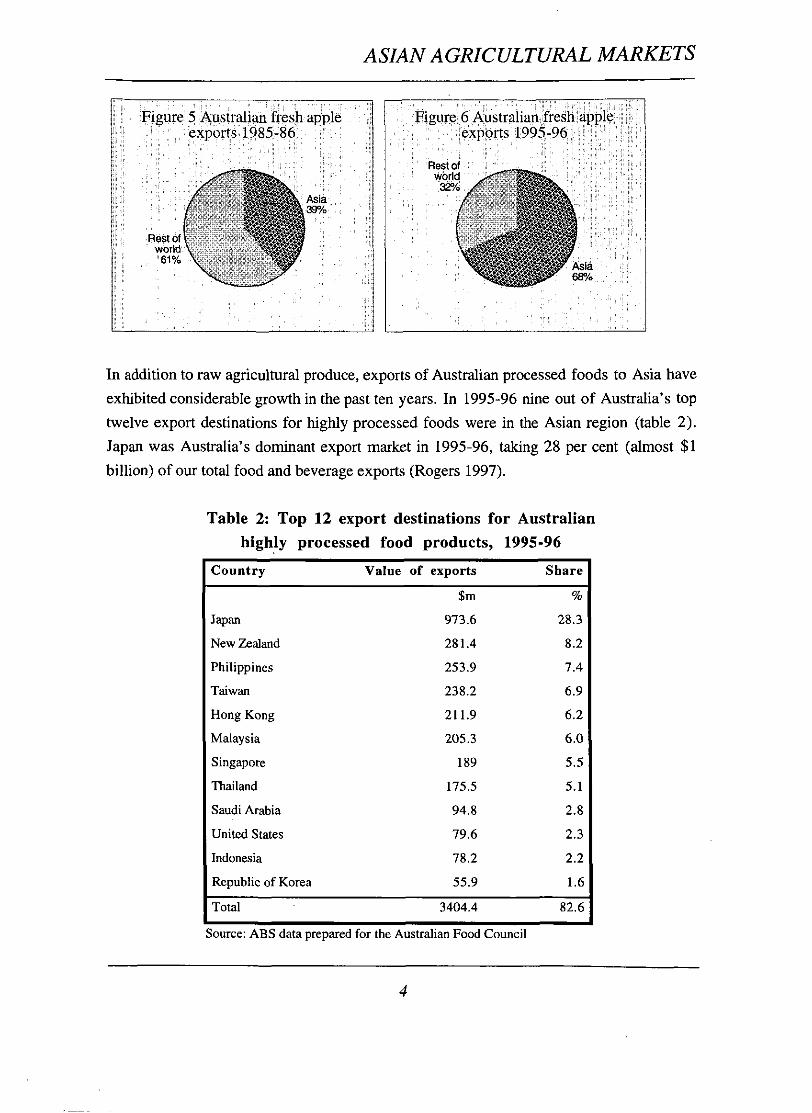

For many agricultural commodities, Asia has become increasingly important for Australian

exporters and has replaced traditional markets, such as Europe, as Australia's major export

destination (table 1 and figures 3 to 6). The importance of Asia in Australia's agricultural

exports is expected to grow in the future as import demand for food in the Asian region

continues to expand and further efforts are made by Australian exporters to secure market

share.

Figure 3: Top 6 fruit export Figure 4: Top 6 vegetable export

destinations 1988-89 to 1995-96 destinations 1988-89 to 1995-96

UK

US Hong Kong

Bangladesh Malaysia

Malaysia Germany

Japan Hong Kong

Singapore Singapore

India 0 100 200 300 400

0 100 200 $ million

$ million

Source: Mackay 1997 Source: Mackay 1997

ASIAN AGRICULTURAL MARKETS

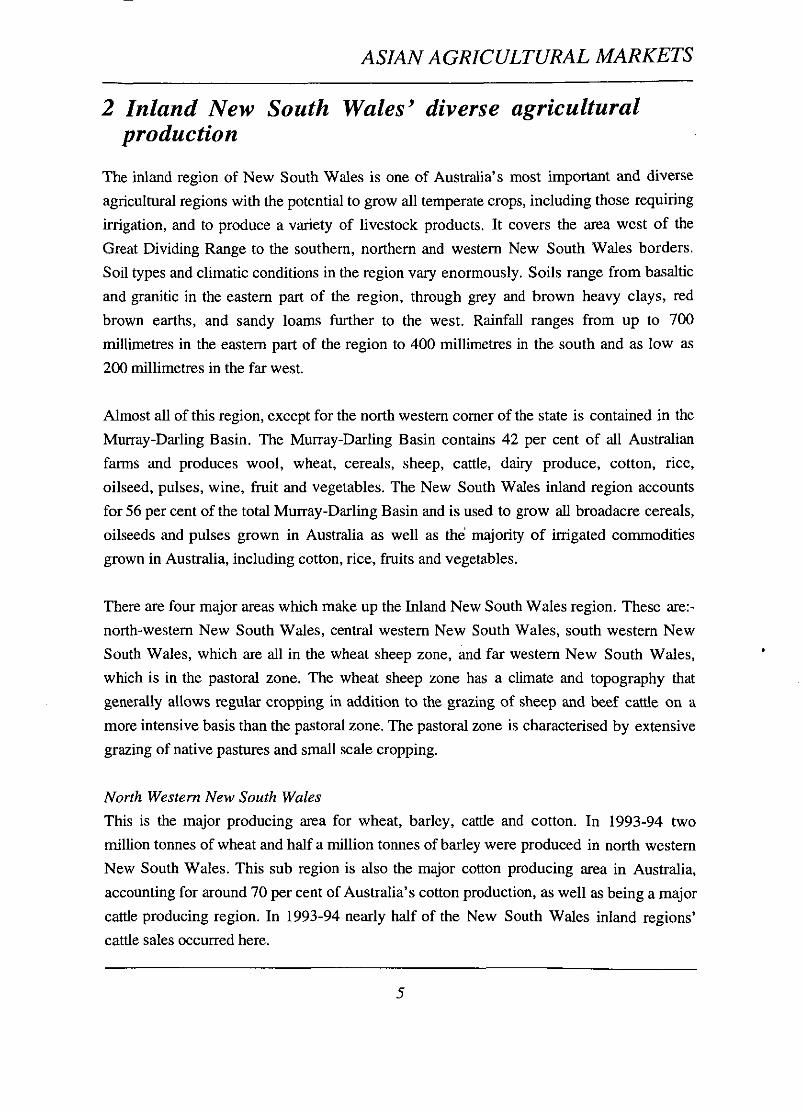

In addition to raw agricultural produce, exports of Australian processed foods to Asia have

exhibited considerable growth in the past ten years. In 1995-96 nine out of Australia's top

twelve export destinations for highly processed foods were in the Asian region (table 2).

Japan was Australia's dominant export market in 1995-96, taking 28 per cent (almost $1

billion) of our total food and beverage exports (Rogers 1997).

Table 2: Top 12 export destinations for Australian

highly processed food products, 1995-96

1 Country Value of exports Share I

New Zealand

Philippines

1 Taiwan 238.2 6.9 1 I Hong Kong 21 1.9 6.2 1 ( Malaysia 205.3 6.0 1 1 Singapore 189 5.5 1 I Thailand 175.5 5.1 1 I Saudi Arabia 94.8 2.8 1 I United States 79.6 2.3 1 ( Indonesia 78.2 2.2 (

Republic of Korea 55.9 1.6

Total 3404.4 82.6

Source: ABS data prepared for the Australian Food Council

ASIAN AGRICULTURAL MARKETS

2 Inland New South Wales' diverse agricultural production

The inland region of New South Wales is one of Australia's most important and diverse

agricultural regions with the potential to grow all temperate crops, including those requiring

irrigation, and to produce a variety of livestock products. It covers the area west of the

Great Dividing Range to the southern, northern and western New South Wales borders.

Soil types and climatic conditions in the region vary enormously. Soils range from basaltic

and granitic in the eastern part of the region, through grey and brown heavy clays, red

brown earths, and sandy loarns further to the west. Rainfall ranges from up to 700

millimetres in the eastern part of the region to 400 millimetres in the south and as low as

200 millimetres in the far west.

Almost all of this region, except for the north western comer of the state is contained in the

Murray-Darling Basin. The Murray-Darling Basin contains 42 per cent of all Australian

farms and produces wool, wheat, cereals, sheep, cattle, dairy produce, cotton, rice,

oilseed, pulses, wine, fruit and vegetables. The New South Wales inland region accounts

for 56 per cent of the total Murray-Darling Basin and is used to grow all broadacre cereals,

oilseeds and pulses grown in Australia as well as the majority of irrigated commodities

grown in Australia, including cotton, rice, fruits and vegetables.

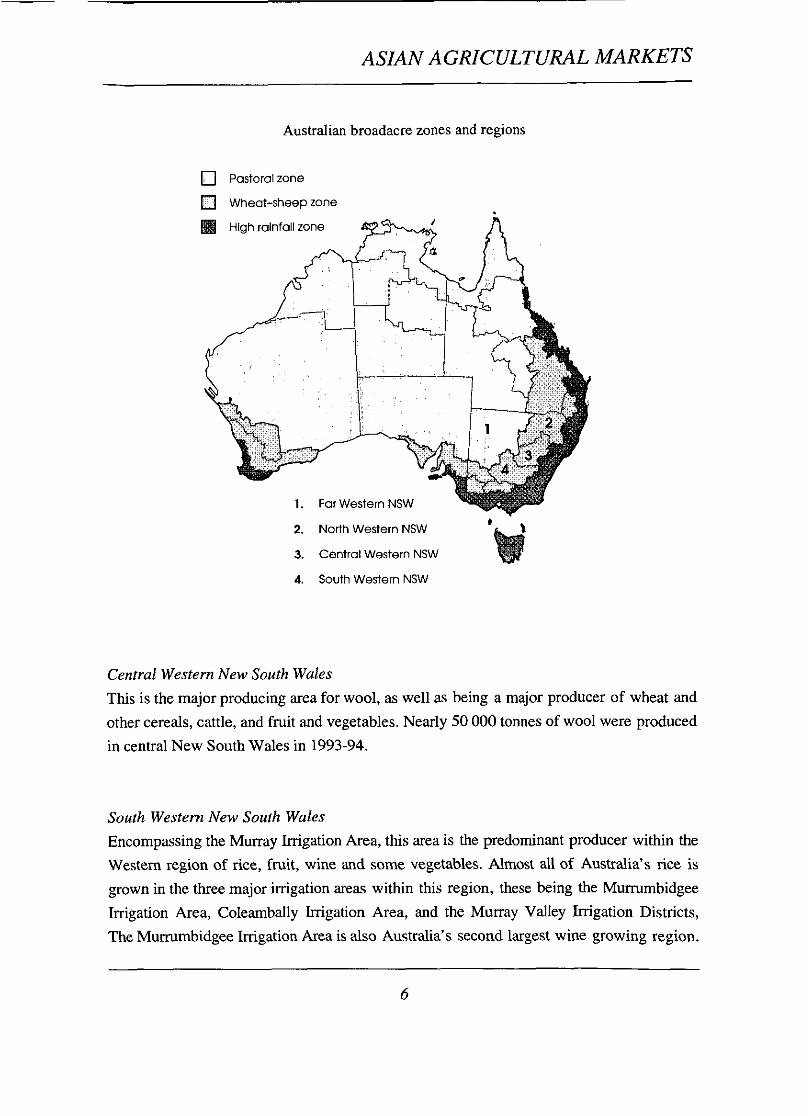

There are four major areas which make up the Inland New South Wales region. These are:-

north-western New South Wales, central western New South Wales, south western New

South Wales, which are all in the wheat sheep zone, and far western New South Wales,

which is in the pastoral zone. The wheat sheep zone has a climate and topography that

generally allows regular cropping in addition to the grazing of sheep and beef cattle on a

more intensive basis than the pastoral zone. The pastoral zone is characterised by extensive

grazing of native pastures and small scale cropping.

North Western New South Wales

This is the major producing area for wheat, barley, cattle and cotton. In 1993-94 two

million tonnes of wheat and half a million tonnes of barley were produced in north western

New South Wales. This sub region is also the major cotton producing area in Australia,

accounting for around 70 per cent of Australia's cotton production, as well as being a major

cattle producing region. In 1993-94 nearly half of the New South Wales inland regions'

cattle sales occurred here.

5

ASIAN AGRICULTURAL MARKETS

Australian broadacre zones and regions

2. North Western NSW

3. Central Western NSW

4. South Western NSW

Central Western New South Wales

This is the major producing area for wool, as well as being a major producer of wheat and

other cereals, cattle, and fruit and vegetables. Nearly 50 000 tonnes of wool were produced

in central New South Wales in 1993-94.

South Western New South Wales

Encompassing the Murray Irrigation Area, this area is the predominant producer within the

Western region of rice, fruit, wine and some vegetables. Almost all of Australia's rice is

grown in the three major irrigation areas within this region, these being the Munumbidgee

Irrigation Area, Colearnbally Irrigation Area, and the Murray Valley Irrigation Districts,

The Murrumbidgee Inigation Area is also Australia's second largest wine growing region.

ASIAN AGRICULTURAL MARKETS - - -

In addition 35 per cent of Australia's citrus production comes from south western New

South Wales, mainly in the form of Valencia oranges.

Far Western New South Wales

This area is situated entirely within the pastoral zone and is the least productive of the four

western areas due to the semi arid and arid nature of much of the land. The major

agricultural commodities within this region are lambs, wool, cattle, and wheat.

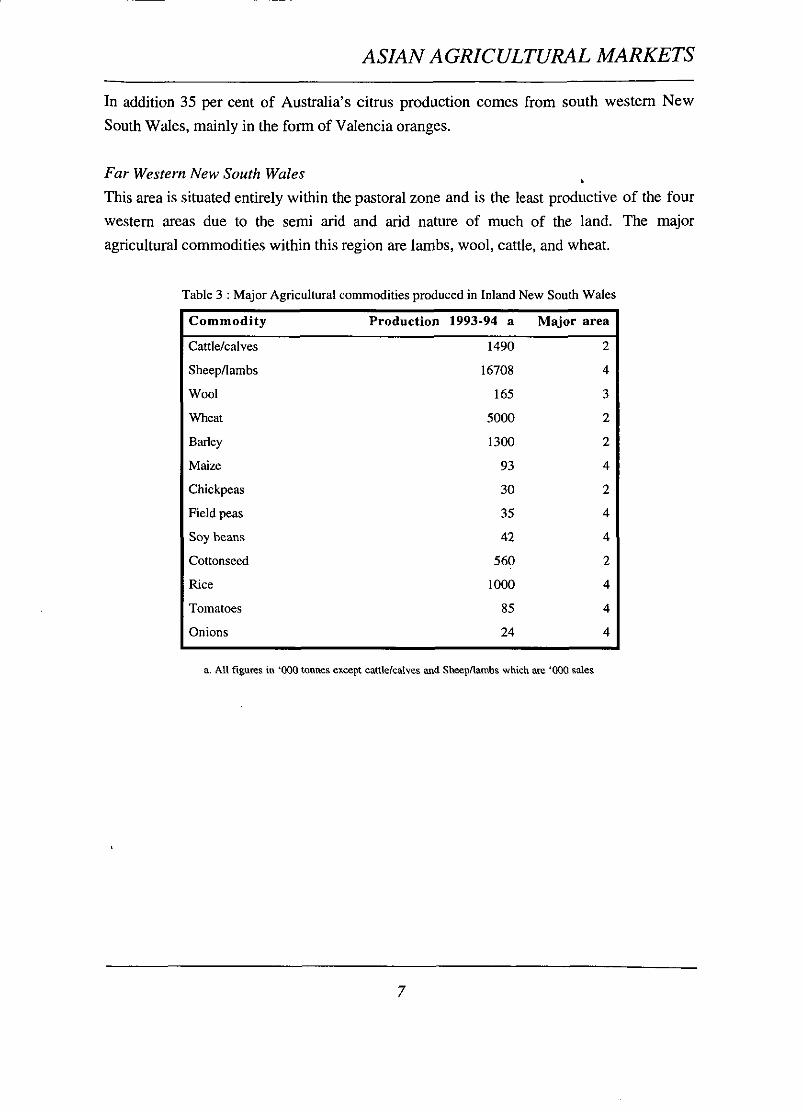

Table 3 : Major Agricultural commodities produced in Inland New South Wales

Commodity Production 1993-94 a Major area

Cattle/calves 1490 2

SheepAambs 16708 4

Wool 165 3

Wheat 5000 2

Barley 1300 2

Maize 93 4

Chickpeas 30 2

Field peas 35 4

Soy beans 42 4

Cottonseed 560 2

Rice 1000 4

Tomatoes 85 4

Onions 24 4

a. All tigum in '000 tonnes except cattlelcalves and Sheepnambs which are 'WO sales

ASIAN AGRICULTURAL MARKETS

3 Growth in Asian imports ,of agricultural products

Many of the agricultural commodities and processed food products for which Asian import

demand has been increasing are grown in the Inland New South Wales region. Table 4

illustrates the growth over the five years to 1995 in imports of a range of agricultural

products for individual Asian countries, both in total and for imports sourced from

Australia. The table was compiled by Austrade through their officers, based in countries

throughout Asia, who pinpointed which Australian commodities they believed to have the

greatest future import potential. This was based on import trends over the previous five

years and through market analysis and direct contact with importers.

For each of the commodities examined it is possible by using the table to examine the

overall change in agricultural imports by countries within the Asian region, and the change

in imports to these countries sourced from Australia. This illustrates which markets we

have lost or gained import market share, and those where Australia's import market share

has remained stagnant. For example, while Philippine cotton imports sourced from

Australia have increased by over 28 per cent in the five years to 1995, overall cotton

imports to the Philippines have increased by just 10 per cent during the same period.

Although imports have grown considerably for some products Australia has lost market

share to other agricultural exporters such as the US, Canada, New Zealand, South Africa

and South American countries. For example, while pear imports to Singapore have

increased by over 13 per cent in the 5 years to 1995, those sourced from Australia have

actually declined by nearly 18 per cent during this period.

It should be noted that this table only illustrates past trends and is not intended to be used as

a forecasting tool. Instead the table provides an indication of future potential for trade

between Australia and the Asian region for a broad range of agricultural commodities.

Also, for several of the major commodities grown in the New South Wales inland region,

including wheat, barley, and rice, single desk sellers such as the Australian Wheat Board

are used to market and export Australian produce and due to confidentiality Australian

export figures are unable to be presented.

ASIAN AGRICULTURAL MARKETS

Impediments to trade

From the table it can be seen that potential export markets exist for growers in the New

South Wales inland region for many agricultural products. However, it is also clear that

there are impediments and limitations to such trade. The onus is on the exporter to

undertake considerable research on identifying opportunities plus the impediments to trade

and to be aware that considerable market development is also necessary to establish and

maintain profitable trade with Asia. A brief overview of some of the impediments faced by

exporters to the Asian region is given below.

One of the major impediments for exports of Australian produce into the Asian market is

the high level of tariff protection which currently exists in many of the major Asian

importing countries. The effect of the tariff is to raise the price of the imported good in the

imported country. However, the level of tariff, or import duty, varies between commodities

and countries as illustrated in table 4. Several of Australia's major export markets

throughout Asia, including Indonesia, Thailand, The Philippines, and Taiwan have

maintained high levels of import duty for most commodities while others, such as Hong

Kong and Singapore have removed almost all tariff barriers for agricultural imports.

Tariff and non-tariff measures are used by the aforementioned countries as a means of

supporting domestic industries and minimising dependence on imported produce. In

general, the highest rates of import duty exist for fruits, vegetables, wine, bovine meat, and

processed juices and jams. However, as a result of the Uruguay round of negotiations

under the General Agreement on Tariffs and Trade import duties in all developing countries

in the Asian region are to be reduced by an average of 24 per cent by 2004, with minimum

cuts of 10 per cent for any specific agricultural commodity (Vanzetti et al. 1994). In

addition, further pressure for reductions in impediments to trade in the Asian region may

occur as a result of the World Trade Organisation round of negotiations due to commence

in 1999 and through regional groupings such as the Asia Pacific Economic Cooperation

(APEC). Any resulting reductions in tariffs or non-tariff barriers would assist in improving

export opportunities for Australia into the Asian region (see Implications of APEC for

Australian agriculture 1996).

When developing export markets within the Asian region, Australian exporters of

agricultural produce also need to consider the different import measures which exist in the

various Asian countries. These measures differ markedly between countries and products

ASIAN AGRICULTURAL MARKETS

and include:- health, food safety and technical standards, import and customs laws, import

licensing, exchange controls and voluntary restraint arrangements. In some instances these

are used to limit the quantity of imports which may enter a country or to increase the price

of imports in that country (Tarchalski et al. 1996). Many of these impediments are indicated

in table 4, however, this is not a comprehensive list and up to date complete information

should be obtained prior to commencing export market development (see the contact list at

the end of this report).

Market development

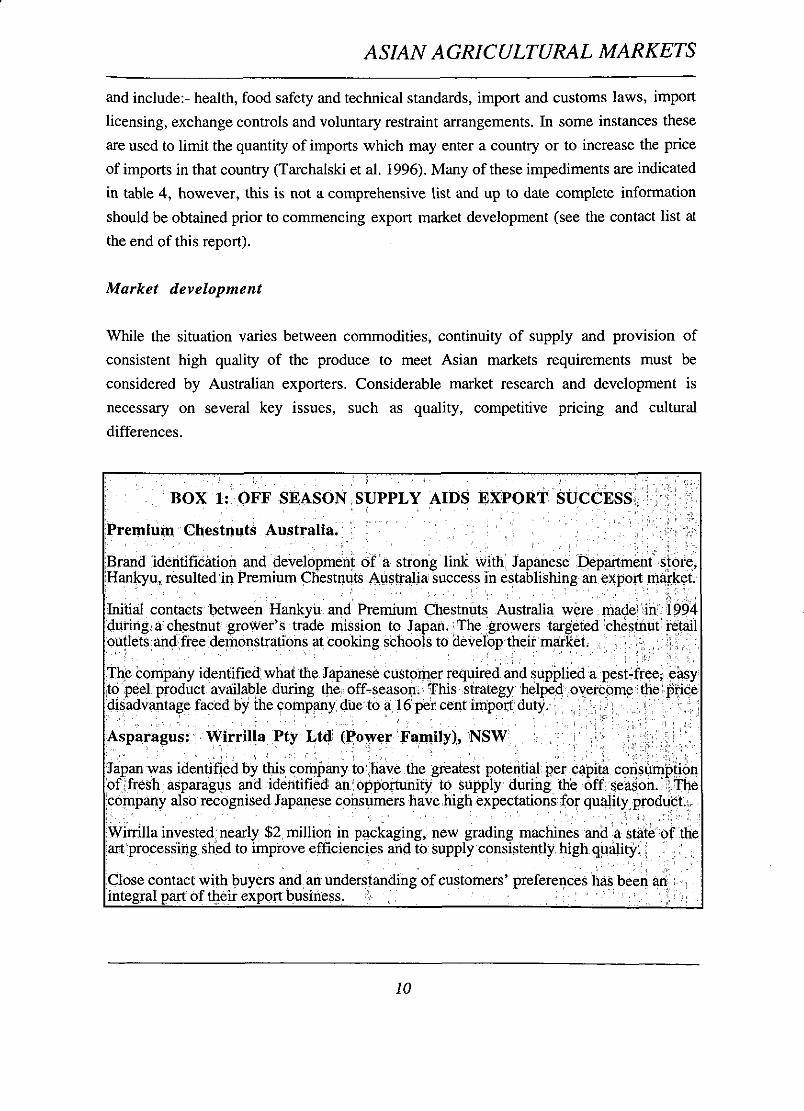

While the situation varies between commodities, continuity of supply and provision of

consistent high quality of the produce to meet Asian markets requirements must be

considered by Australian exporters. Considerable market research and development is

necessary on several key issues, such as quality, competitive pricing and cultural

differences.

ASIAN AGRICULTURAL MARKETS

Australian exporters to the Asian region need to be able to meet the volumes and continuity

of supply that is demanded by the Asian market. This may be achieved through cooperative

marketing schemes such as Riversun or focussing on meeting demand during the Asian off

season as illustrated by the case studies in box I.

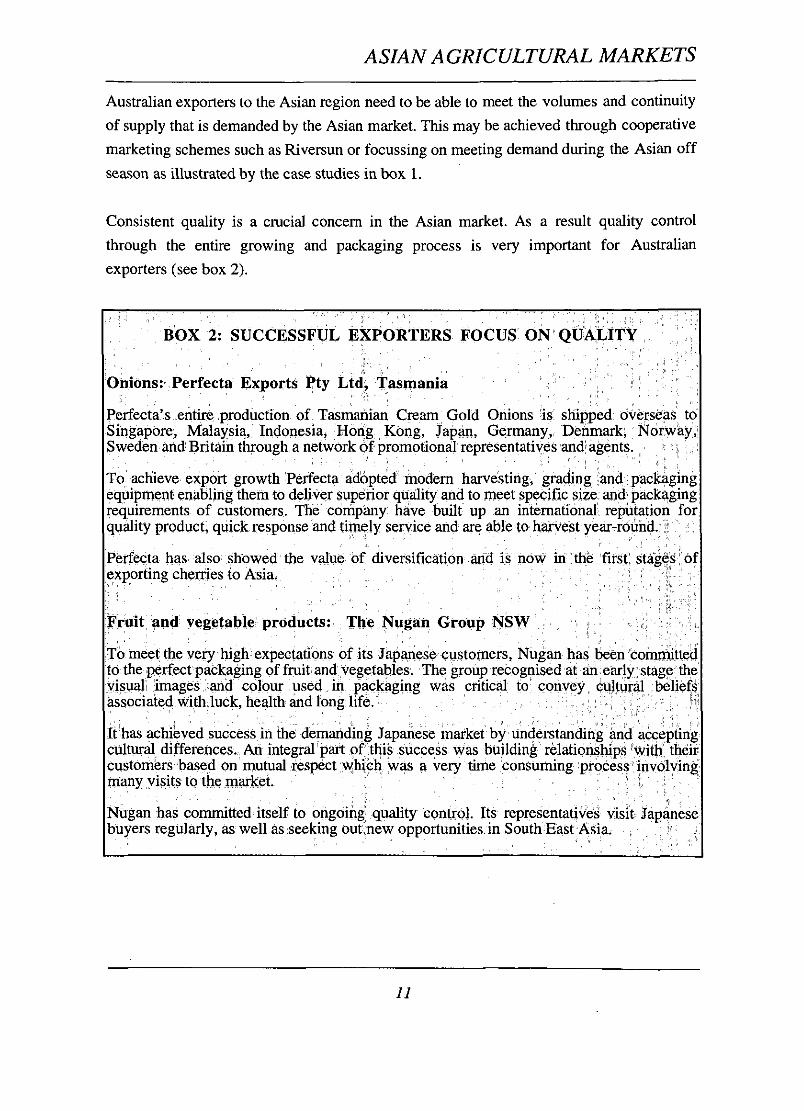

Consistent quality is a crucial concern in the Asian market. As a result quality control

through the entire growing and packaging process is very important for Australian

exporters (see box 2).

C r e q Gold Onions 'is'

ASIAN AGRICULTURAL MARKETS

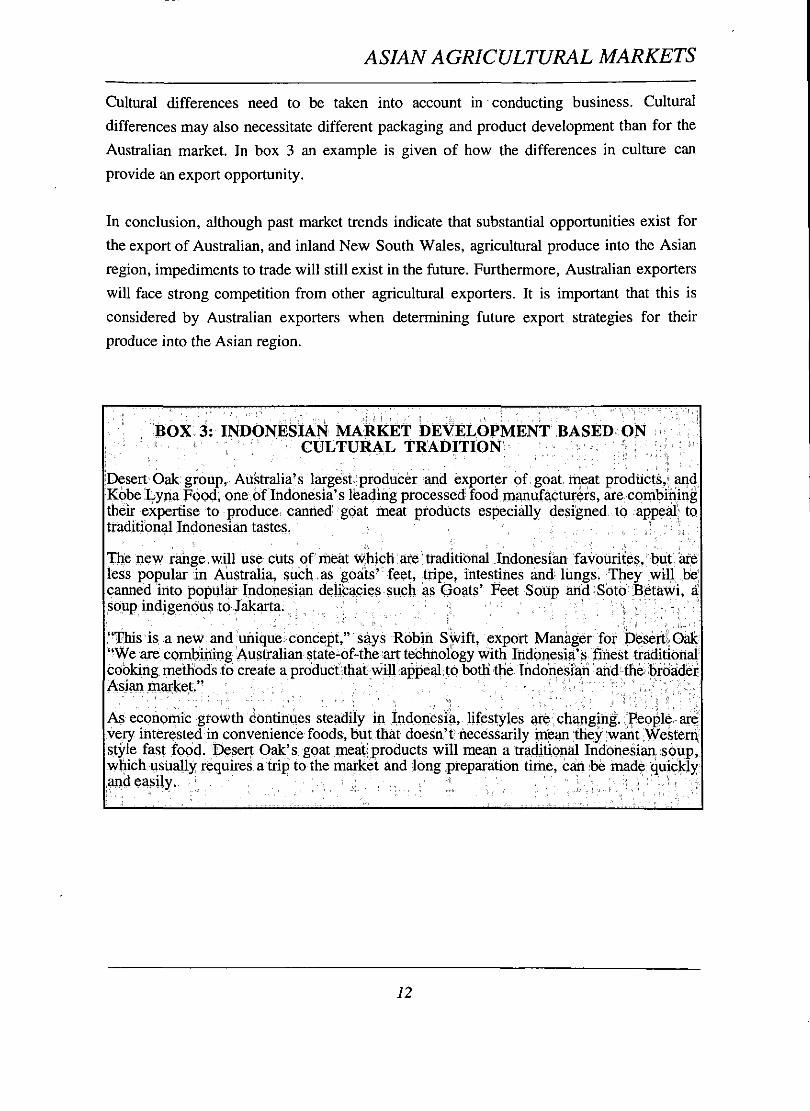

Cultural differences need to be taken into account in conducting business. Cultural

differences may also necessitate different packaging and product development than for the

Australian market. In box 3 an example is given of how the differences in culture can

provide an export opportunity.

In conclusion, although past market trends indicate that substantial opportunities exist for

the export of Australian, and inland New South Wales, agricultural produce into the Asian

region, impediments to trade will still exist in the future. Furthermore, Australian exporters

will face strong competition from other agricultural exporters. It is important that this is

considered by Australian exporters when determining future export strategies for their

produce into the Asian region.

ASIAN AGRICULTURAL MARKETS

References

Mackay, A., Moody, J. and Petrushevski, N. 1997, 'The changing face of horticulture in

Australia-a statistical perspective', in Proceedings of MARE'S National Agricultural and

Resources Outlook Conference, Canberra, 4-6 February, Outlook 97, vol. 1, Agriculture,

pp 305-315.

Podbury, T., Ladlow, S., Mai, Y,. Atisuthaphot, A. and Rose, R. 1996, 'Implications of

APEC for Australian agriculture', in Proceedings of ABARE's National Agricultural and

Resources Outlook Conference, Canberra, 6-8 February, Outlook 96, vol. 1, Agriculture,

pp 29-46.

Rogers, M. 1997, 'Food markets-capturing emerging opportunities', in Proceedings of

MARE'S National Agricultural and Resources Outlook Conference, Canberra,

4-6 February, Outlook 97, vol. 1 , Agriculture, pp 27-37.

Tarchalski, T., Rees, R., Roberts, I., Cockinos, A. and Whish-Wilson, P. 1996,

'ASEAN wheat markets: prospects for their liberalisation', Australian Commodities,

vol. 3, no. 1, p. 63.

Vanzetti, D., Melanie, J. and Barry, G. 1994, 'South East Asia: agriculture post Uruguay

Round', Australian Commodities, vol. 1, no. 2, p 256.

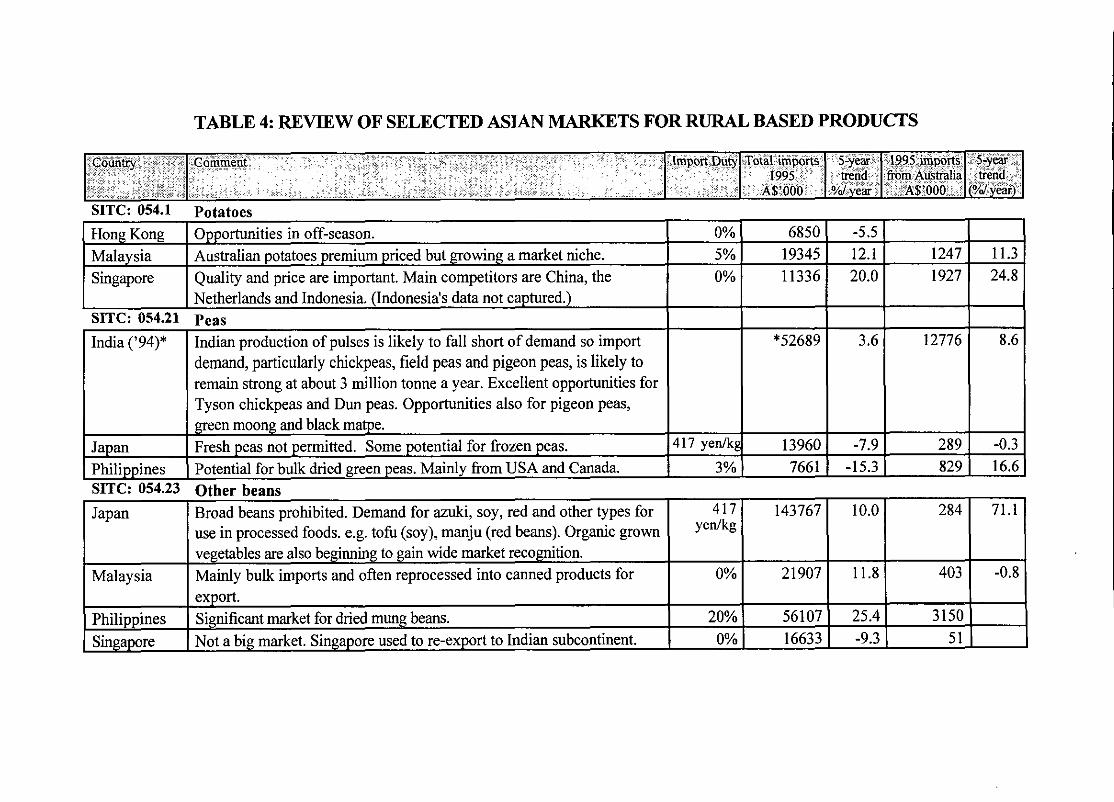

TABLE 4: REVIEW OF SELECTED ASIAN MARKETS FOR RURAL BASED PRODUCTS

5-year vend

(Yd year)

SITC: 054.1 potatoes

Japan Philippines SITC: 054.23

Japan

Malaysia

5-year trend

?'d year

Country

11.3 24.8

8.6

Philippines Singapore

1995 imports from Australia

AS'000

Import Duty Comment

demand, particularly chickpeas, field peas and pigeon peas, is likely to remain strong at about 3 million tonne a year. Excellent opportunities for Tyson chickpeas and Dun peas. Opportunities also for pigeon peas, green moong and black matpe. Fresh peas not permitted. Some potential for frozen peas. Potential for bulk dried green peas. Mainly from USA and Canada.

Total impons 1995

AS'000

-5.5 12.1 20.0

3.6

Hong Kong Malaysia Singapore

export. Significant market for dried mung beans. Not a big market. Singapore used to re-export to Indian subcontinent.

0% 5% 0%

1247 1927

12776

Opportunities in off-season. Australian potatoes premium priced but growing a market niche. Quality and price are important. Main competitors are China, the Netherlands and Indonesia. (Indonesia's data not captured.)

4 17 yenlkg

3%

6850 19345 11336

*52689 SITC: 054.21 Peas

I India ('94)* 1 Indian production of pulses is likely to fall short of demand so import

Other beans

20% 0%

13960 7661

71.1

-0.8

56107 16633

-7.9 -15.3

Broad beans prohibited. Demand for azuki, soy, red and other types for use in processed foods. e.g. tofu (soy), manju (red beans). Organic grown vegetables are also beginniig to gain wide market recognition. Mainly bulk imports and often reprocessed into canned products for

10.0

11.8

25.4 -9.3

289 829

417 yenlkg

0%

284

403

3150 51

-0.3 16.6

143767

21907

SITC: 054.4 Tomatoes

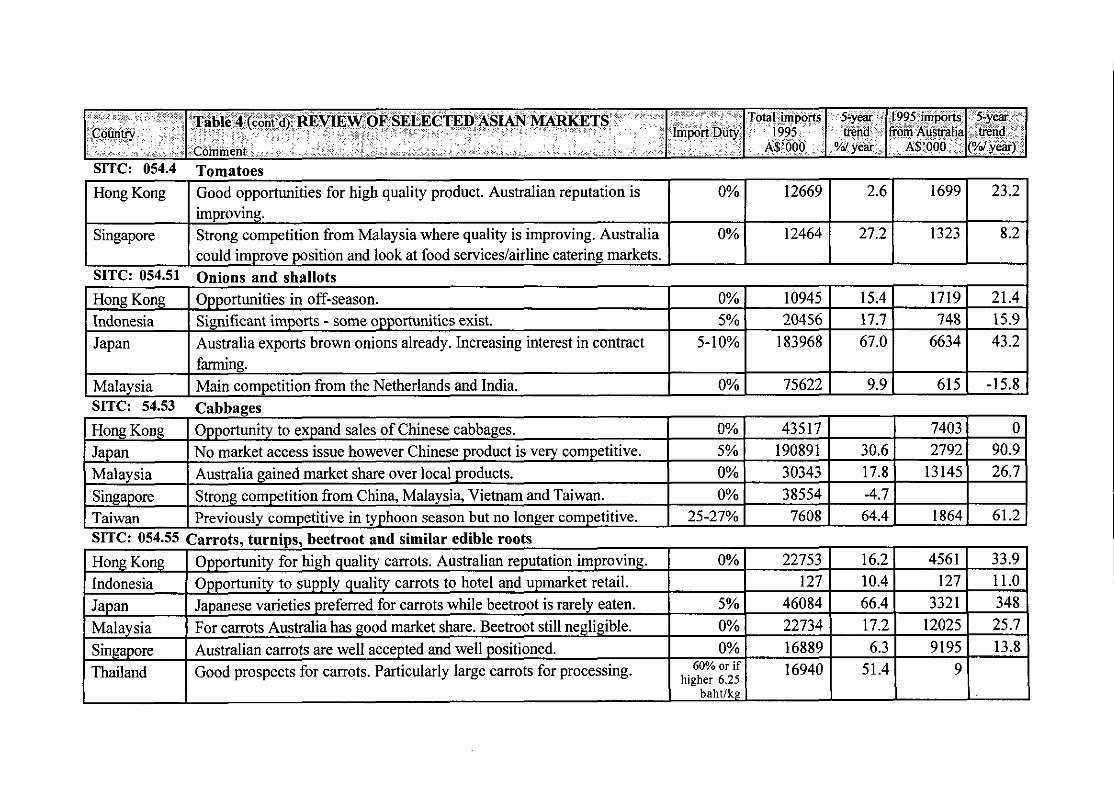

I Hong Kong I Good opportunities for high quality product. Australian reputation is I 0% I 12669 ( 2.6 1 1699 1 23.2 1

( farming. Malaysia ( Main competition from the Netherlands and India. S I X : 54.53 Cahhsoes

Singapore

SITC: 054.51

Hong Kong Indonesia Japan

Hong Kong I Opportunity to expand sales of Chinese cabbages. Japan I No market access issue however Chinese product is very competitive.

improving. Strong competition from Malaysia where quality is improving. Australia could improve position and look at food serviceslairline catering markets. Onions and shallots Opportunities in off-season. Significant imports - some opportunities exist. Australia exports brown onions already. Increasing interest in contract

Malaysia 1 Australia gained market share over local products. Singapon: 1 Strong competition from China, Malaysia, Vietnam and 'l'aiwan.

I Taiwan ( Previously competitive in typhoon season but no longer competitive. SITC: 054.55 Carrots, turnips, beetroot and similar edible roots Hong Kong I Opportunity for high quality carrots. Australian reputation improving. Indonesia ( Opportunity to supply quality carrots to hotel and upmarket retail. Japan I Japanese varieties preferred for carrots while beetroot is rarely eaten. Malaysia 1 For carrots Australia has good market share. Beetroot still negligible. Singapore I Australian carrots are well accepted and well positioned. Thailand I Good prospects for carrots. Particularly large carrots for processing.

>year trend

(Yd year)

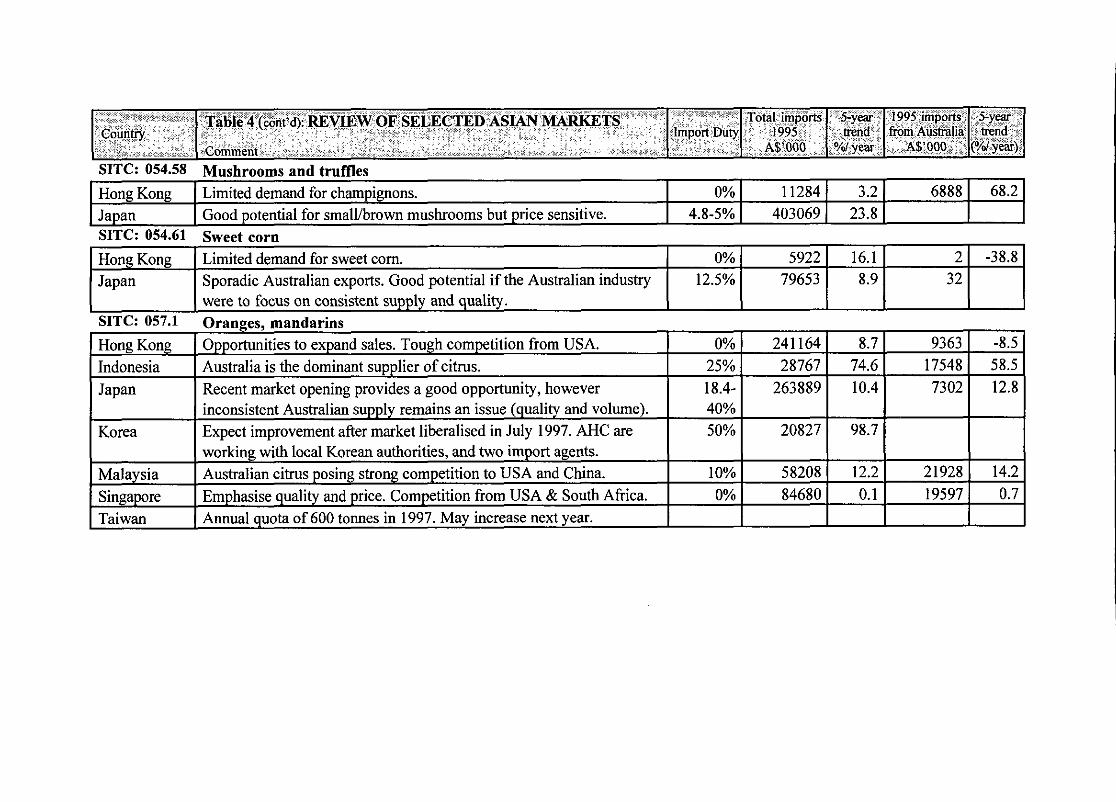

SITC: 054.58 Mushrooms and truffles

Taiwan 1 Annual quota of 600 tonnes in 1997. May increase next year.

Counny

Malaysia Singapore

lmpon Duty Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

0% I 11284 1 3.2 Hong Kong 6888 1 68.2

working with local Korean authorities, and two import agents. Australian citrus posing strong competition to USA and China. Emphasise quality and price. Competition from USA & South Africa.

Total imports 1995

AVO00

Limited demand for champignons.

2 32

9363 17548 7302

Japan SITC: 054.61

Hong Kong Japan

SITC: 057.1

Hong Kong Indonesia Japan

Korea

-38.8

-8.5 58.5 12.8

10% 0%

5-year trend

O/d year

1995 imports from Australia

A6'000

Good potential for small/brown mushrooms but price sensitive. 1 4.8-5% 1 403069 1 23.8 Sweet corn

58208 84680

16.1 8.9

8.7 74.6 10.4

98.7

Limited demand for sweet corn. Sporadic Australian exports. Good potential if the Australian industry were to focus on consistent supply and quality.

12.2 0.1

0% 12.5%

21928 19597

5922 79653

14.2 0.7

241 164 28767

263889

20827

Oranges, mandarins Opportunities to expand sales. Tough competition from USA. Australia is the dominant supplier of citrus. Recent market opening provides a good opportunity, however inconsistent Australian supply remains an issue (quality and volume). Expect improvement after market liberalised in July 1997. AHC are

0% 25% 18.4- 40% 50%

I I negotiated one-desk trading with Itochu who will purchase all 1 1 I I 1 I

Hong Kong Indonesia Japan

I I production for two years once quarantine restrictions are lifted in June I I I I I I

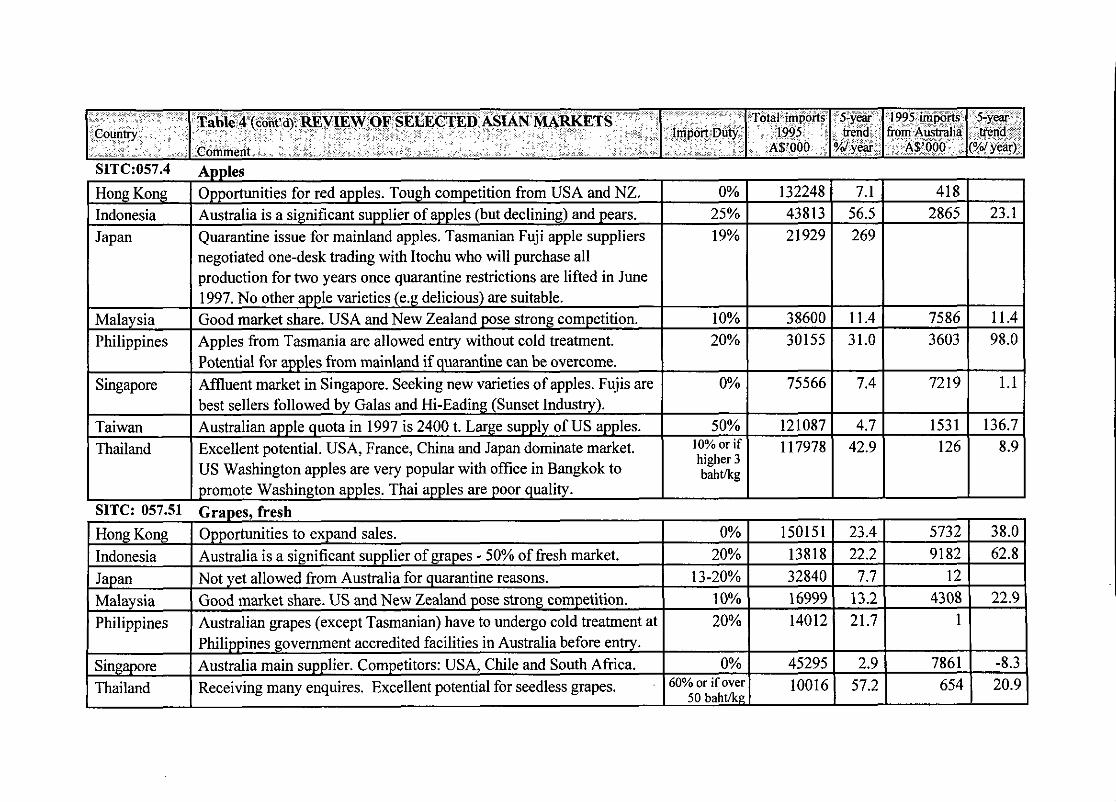

Opportunities foired apples. Tough competition from USA and NZ. Australia is a significant supplier of apples (but declining) and pears. Quarantine issue for mainland apples. Tasmanian Fuji apple suppliers

Malaysia Philippines

0% 25% 19%

Singapore

Taiwan Thailand

1997. No other apple varieties (e.g delicious) are suitable. Good market share. USA and New Zealand pose strong competition. Apples from Tasmania are allowed entry without cold treatment.

Singapore Thailand

132248 43813 21929

Potential for apples from mainland if quarantine can be overcome. Affluent market in Singapore. Seeking new varieties of apples. Fujis are best sellers followed by Galas and Hi-Eading (Sunset Industry). Australian apple quota in 1997 is 2400 t. Large supply of US apples. Excellent potential. USA, France, China and Japan dominate market. US Washington apples are very popular with ofice in Bangkok to promote Washington apples. Thai apples are poor quality.

10% 20%

- - Philippines government accredited facilities in Australia before entry. Australia main supplier. Competitors: USA, Chile and South Africa. Receiving many enquires. Excellent potential for seedless grapes.

7.1 56.5 269

38600 30155

0%

50% 10% or if higher 3 bahtlkg

SITC: 057.51 Grapes, fresh

75566

121087 11 7978

0% 20%

13-20% 1 OYO 20%

Hong Kong Indonesia Japan Malaysia Philippines

0% 60% or if over

50 bahtkg

418 2865

150151 13818 32840 16999 14012

Opportunities to expand sales. Australia is a significant supplier of grapes - 50% of fresh market. Not yet allowed from Australia for quarantine reasons. Good market share. US and New Zealand pose strong competition. Australian grapes (except Tasmanian) have to undergo cold treatment at

45295 10016

23.1

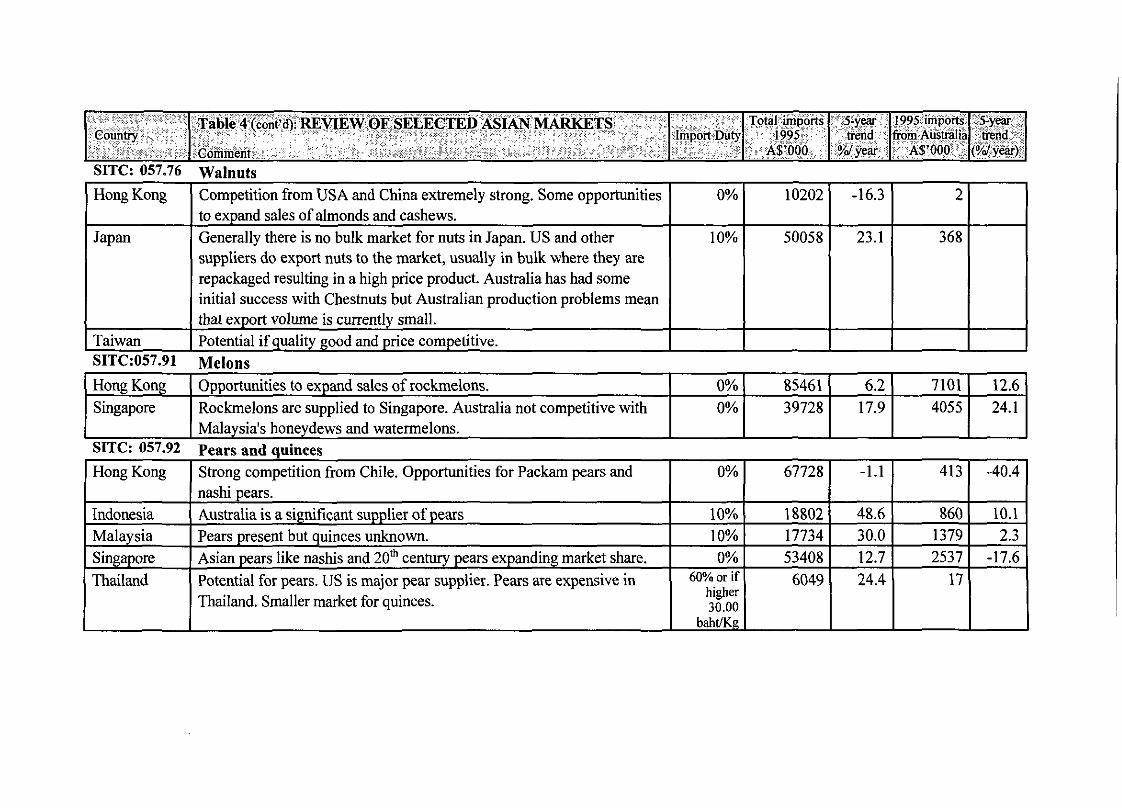

SITC: 057.76 Walnuts

( Hong Kong 1 Competition from USA and Chiia extremely strong. Some opportunities 1 OYO 1 102021 -16.3) 2 1

Counby

I repackaged resulting in a high price product. Australia has had some initial success with Chestnuts but Australian production problems mean I

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

Japan

I that export volume is currently small. I I I I I Taiwan I Potential if quality good and price competitive. SITC:057.91 Mplnns

..----mm"

Hon Kon -1 85461 6.2 7101 ( 12.6

Import Duty

to expand sales of almonds and cashews. Generally there is no bulk market for nuts in Japan. US and other suppliers do export nuts to the market, usually in bulk where they are

10%

Singapore

Total imports 1995

A$'000

1995 imports h m Australia

A$'000

5-year trend

'Yd year

50058

S I X : 057.92 Pears and quinces I Hong Kong I Strong competition from Chile. Opportunities for Packam pears and I 67728 1 -1.1 1 413 1 -40.4 1

Rockmelons are supplied to Singapore. Australia not competitive with Malaysia's honeydews and watermelons.

5-year m n d

('Yd year)

23.1

0%

368

39728 17.9 4055 24.1

. .

packaging. Opportunity if pursued especially 100% pure juice. Thailand Opportunity especially orange and apple juices. Thai companies now 30% or if

higher 10- 5119

manufacture with US oranges, hence market is more price sensitive. 25 b a h t k ~

- --

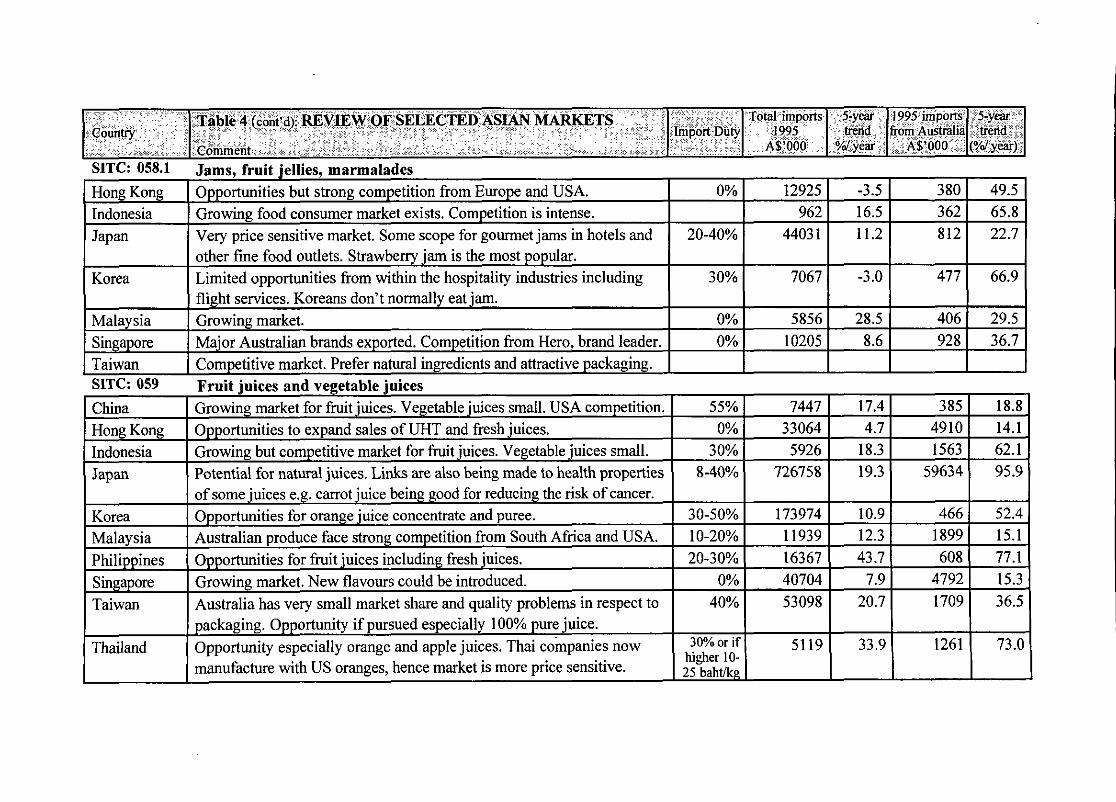

SITC: 058.1 Jams, fruit jellies, marmalades

1995 imports h m Australia

A6'000 Country

5-year bend

(Yd year)

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

Hong Kong Indonesia Japan

Korea

Malaysia Singapore Taiwan

5-year bend

Yd year Import Duty

0%

20-40%

30%

0% 0%

Opportunities but strong competition from Europe and USA. Growing food consumer market exists. Competition is intense. Very price sensitive market. Some scope for gourmet jams in hotels and other fine food outlets. Strawberry jam is the most popular. Limited opportunities from within the hospitality industries including flight services. Koreans don't normally eat jam. Growing market. Major Australian brands exported. Competition from Hero, brand leader. Competitive market. Prefer natural ingredients and attractive packaging.

'Total imports 1995

A6'000

12925 962

4403 1

7067

5856 10205

SITC: 059 Fruit juices and vegetable juices China Growing market for fruit juices. Vegetable juices small. USA competition. 55% 7447 Hong Kong Opportunities to expand sales of UHT and fresh juices. 0% 33064 Indonesia Growing but competitive market for fruit juices. Vegetable juices small. 30% 5926 J a ~ a n Potential for natural juices. Links are also being made to health properties 8-40% 726758

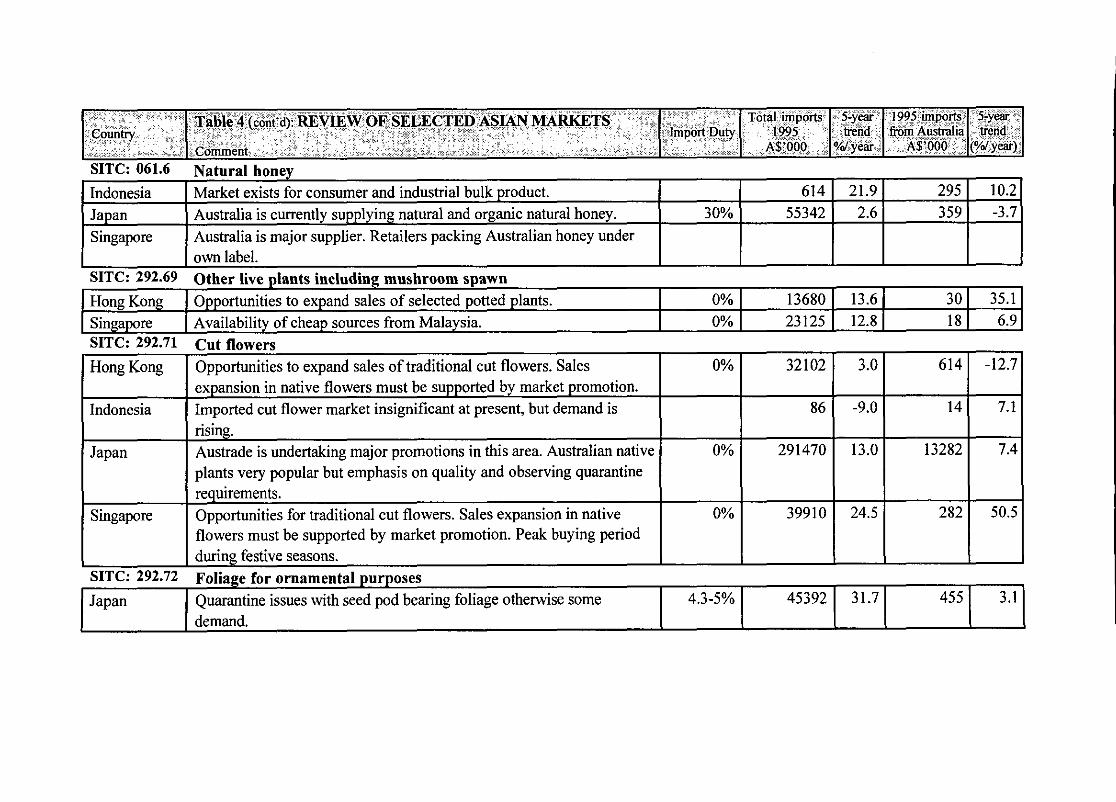

I I own label. I J SITC: 292.69 Other live plants including mushroom spawn Hong Kong I Opportunities to expand sales of selected potted plants. I 0% I 13680 1 13.6 1 30 1 35.1 Singapore I Availability of cheap sources from Malaysia. 0% I 23125 1 12.8 1 18 1 6.9

5-year trend

(Yd year)

SITC: 061.6 Natural honey

Japan

5-year trend

O/d year Counhy

10.2 -3.7

SITC: 292.71 Cut flowers

Singapore

1995 imports from Australia

A$'000 Import Duty

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

Japan

Total imports 1995

AS'000

21.9 2.6

Indonesia Japan Singapore

rising. Austrade is undertaking major promotions in this area. Australian native plants very popular but emphasis on quality and observing quarantine requirements. Opportunities for traditional cut flowers. Sales expansion in native flowers must be supported by market promotion. Peak buying period

, during festive seasons. Foliage for ornamental purposes Quarantine issues with seed pod bearing foliage otherwise some

295 359 30%

Market exists for consumer and industrial bulk product. Australia is currently supplying natural and organic natural honey. Australia is major supplier. Retailers packing Australian honey under

614

14

Hong Kong

Indonesia

614 55342

-12.7

7.1

0% Opportunities to expand sales of traditional cut flowers. Sales expansion in native flowers must be supported by market promotion. Imported cut flower market insignificant at present, but demand is

32102

86

3.0

-9.0

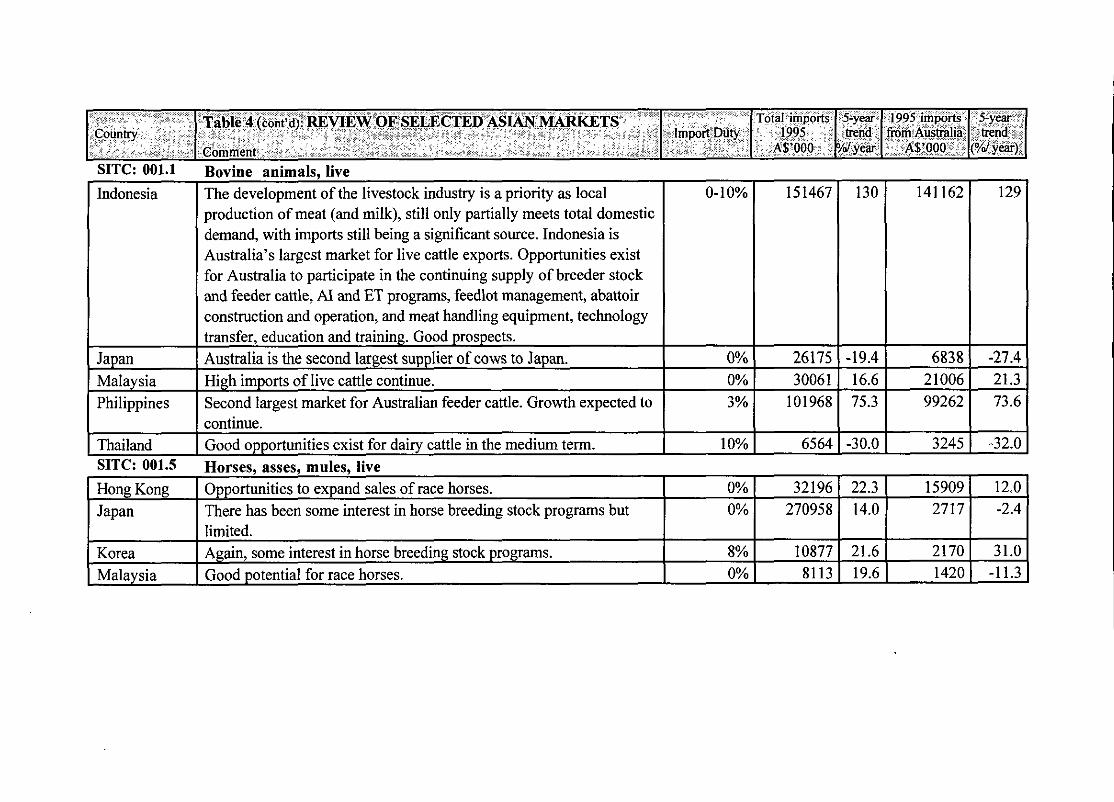

SITC: 001.1 Bovine animals, live r Indonesia I The development of the livestock industry is a priority as local 0-10% 1 1514671 130 1 141162 1 129 1

I production of meat (and milk), still only partially meets total domestic demand, with imports still being a significant source. Indonesia is I Australia's largest market for live cattle exports. Opportunities exist for Australia to participate in the continuing supply of breeder stock and feeder cattle, A1 and ET programs, feedlot management, abattoir

ear trend

year lmpoli Duty Country

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

1995 imports from Australia

A6'000

Japan

5-year trend

(O'dyear)

-

Malaysia I High imports of live cattle continue.

Korea I Again, some interest in horse breeding stock programs. 8% 1 108771 21.6 1 21701 31.0 Malaysia 1 Good potential for race horses. I 0% 1 8113 1 19.6 1 1420 1 -11.3

construction and operation, and meat handling equipment, technology transfer, education and training. Good prospects. Australia is the second largest supplier of cows to Japan.

0% I 30061 1 16.6 1 210061 21.3

I continue. I I I I I Philippines I Second largest market for Australian feeder cattle. Growth expected to I 3% 1 101968 1 75.3 1 99262 1 73.6

Thailand I Good opportunities exist for dairy cattle in the medium term.

0%

10% 1 6564 1 -30.0 1 3245 1 -32.0 SITC: 001.5 Horses, asses, mules, live Hong Kong I Opportunities to expand sales of race horses. I 0% I 32196 1 22.3 1 15909 1 12.0 Japan I There has been some interest in horse breeding stock programs but 270958 1 14.0 1 2717 1 -2.4

26175 -19.4 6838 -27.4 .

5-year trend

(Yd year)

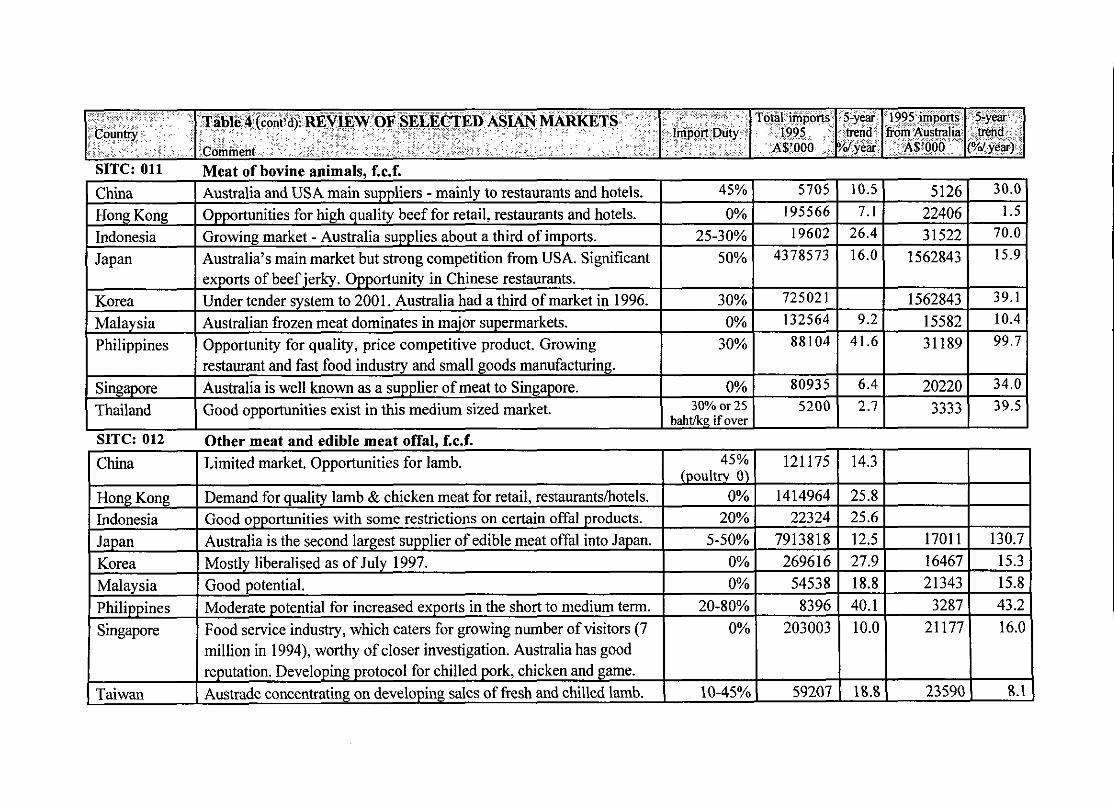

SITC: 011 Meat of bovine animals, f.c.f.

1995 imports from Australia

A%'000

Korea Malaysia Philippines

SITC: 012 Other meat and edible meat offal f.c.f.

Counhy

Singapore Thailand

Import Duty Table 4 (cont'd): REVlEW OF SELECTED ASLAN MARKETS

Comment

10.5 7.1

26.4 16.0

China Hong Kong Indonesia Japan -

exports of beef jerky. Opportunity in Chinese restaurants. Under tender system to 2001. Australia had a third of market in 1996. Australian fkozen meat dominates in major supermarkets. Opportunity for quality, price competitive product. Growing

5-year trend

year

45%

0% 25-30%

50%

Australia and USA main suppliers - mainly to restaurants and hotels. Opportunities for high quality beef for retail, restaurants and hotels. Growing market - Australia supplies about a third of imports. Australia's main market but strong competition from USA. Significant

restaurant and fast food industry and small goods manufacturing. Australia is well known as a supplier of meat to Singapore. 0% 80935

Good o~~or tuni t ies exist in this medium sized market. 30% or 25 5200

5126 22406 31522

1562843

5705 195566

19602 4378573

30% 0%

30%

30.0 1.5

70.0 15.9

6.4 2.7

725021 132564 88104

20220 3333

9.2 41.6

34.0 39.5

1562843 15582 31189

39.1 10.4 99.7

sources. I I I I I Niche market but demand for delicacies and smallgoods growing. 0% I 6401 ( 8.1 1 51 1 -0.9

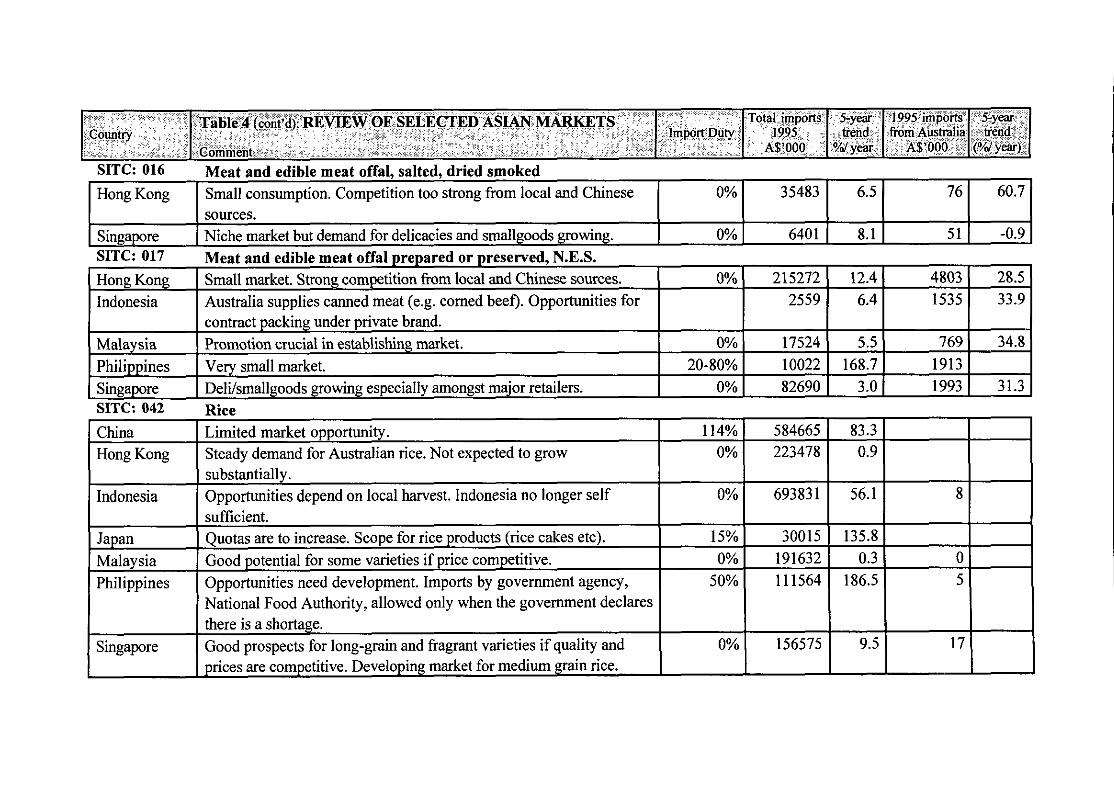

SITC: 016 Meat and edible meat offal, salted, dried smoked

SITC: 042

China Hong Kong

Indonesia

I Hong Kong I Small consumption. Competition too strong fiom local and Chinese ( 0%

Japan Malaysia Philippines

76 35483 1 6.5

Singapore

60.7

Rice Limited market opportunity. 114% Steady demand for Australian rice. Not expected to grow 0% substantially. Opportunities depend on local harvest. Indonesia no longer self 0%

Quotas are to increase. Scope for rice products (rice cakes etc). 15%

Good potential for some varieties if price competitive. 0%

Opportunities need development. Imports by government agency, 50% National Food Authority, allowed only when the government declares there is a shortage. Good prospects for long-grain and fragrant varieties if quality and 0% prices are competitive. Developing market for medium grain rice.

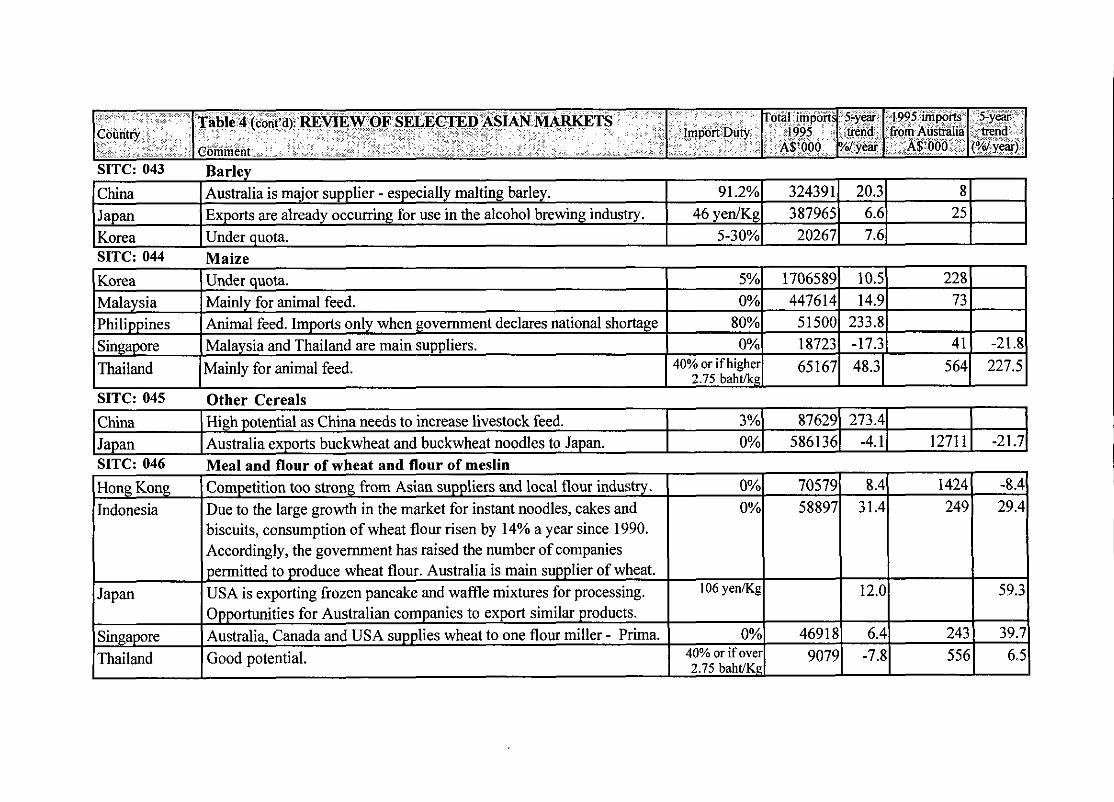

SITC: 043 Barley

1995 imports from Ausnalia

A$'000

5-year Import Duty trend

year Country

SITC: 045 Other cereals

5-year trend

(O/d year)

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

SITC: 044 Maize

20.3 6.6 7.6

China Japan Korea

8 25

91.2% 46 yen/Kg

5-30%

Australia is major supplier - especially malting barley. Exports are already occurring for use in the alcohol brewing industry. Under quota.

3% 0%

0% 0%

106 yeniKg

0% 40% or if over 2.75 baht1Kg

876291 273.4) I 5861361 -4.11 127111 -21.7

China ( High potential as China needs to increase livestock feed. Japan I Australia exports buckwheat and buckwheat noodles to Japan. SITC: 046 Meal and flour of wheat and flour of meslin

324391 387965 20267

70579 58897

46918 9079

Hong Kong Indonesia

Japan

Singapore Thailand

Competition too strong from Asian suppliers and local flour industry. Due to the large growth in the market for instant noodles, cakes and biscuits, consumption of wheat flour risen by 14% a year since 1990. Accordingly, the government has raised the number of companies permitted to produce wheat flour. Australia is main supplier of wheat. USA is exporting frozen pancake and waffle mixtures for processing. Opportunities for Australian companies to export similar products. Australia, Canada and USA supplies wheat to one flour miller - Prima.

Good potential.

8.4 31.4

12.0

6.4 -7.8

1424 249

243 556

-8.4 29.4

59.3

39.7 6.5

I suppliers. Indonesia I Malt - For brewing - opportunities exist

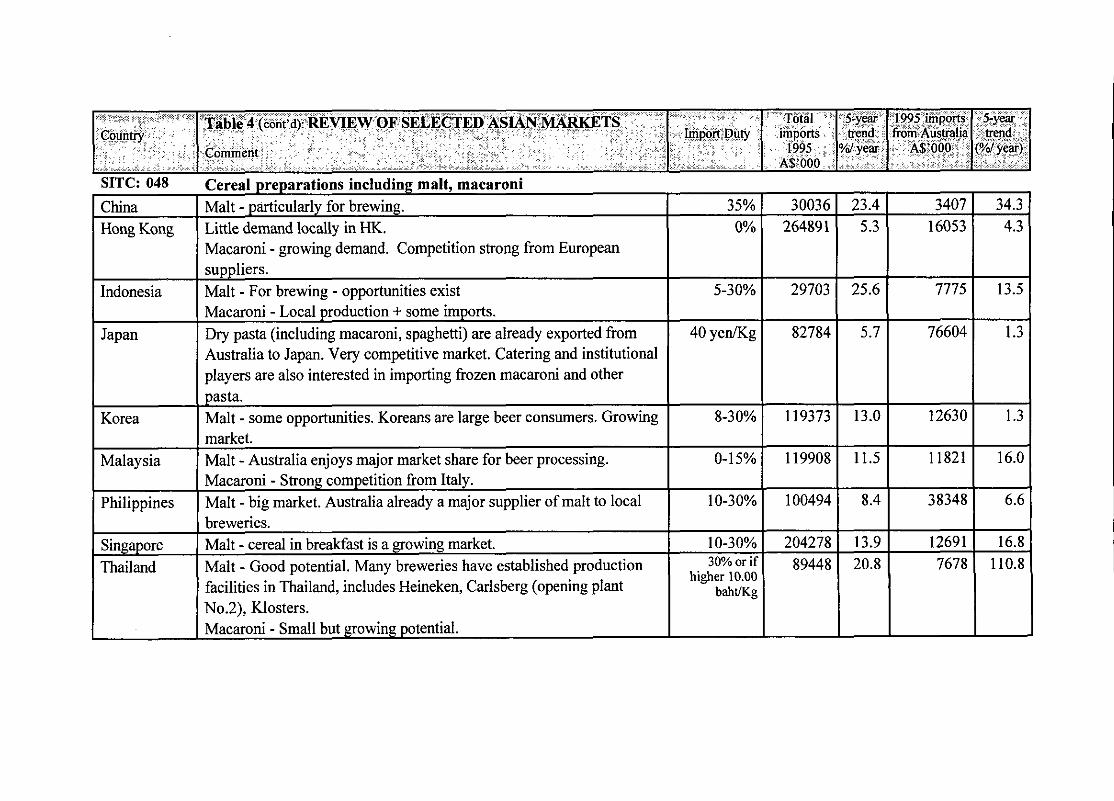

SITC: 048 Cereal preparations including malt, macaroni

( Macaroni - Local production + some imports. Japan I Dry pasta (including macaroni, spaghetti) are already exported from

China Hong Kong

Australia to Japan. Very competitive market. Catering and institutional players are also interested in importing frozen macaroni and other

Malt - particularly for brewing. Little demand locally in HK. Macaroni - growing demand. Competition strong from European

I pasta. Korea I Malt - some opportunities. Koreans are large beer consumers. Growing

Malaysia

Philippines

market. Malt - Australia enjoys major market share for beer processing. Macaroni - Strong competition from Italy. Malt - big market. Australia already a major supplier of malt to local

Singapore Thailand 8944481 20.8 ( 7678 ( 110.8 1

higher 10.00

breweries. Malt - cereal in breakfast is a growing market. Malt - Good potential. Many breweries have established production facilities in Thailand, includes Heineken, Carlsberg (opening plant NO.^), Klosters. Macaroni - Small but growing potential.

Import Duly 1995 imports

from Australia A$'000

5-year trend

(W year)

Total imports

1995 A$'000

5-year trend

Yd year

I orders. Taiwan 1 Australian product higher priced than other imports, due to cost of I 0%) 50770) 41.11 531 1 162.1

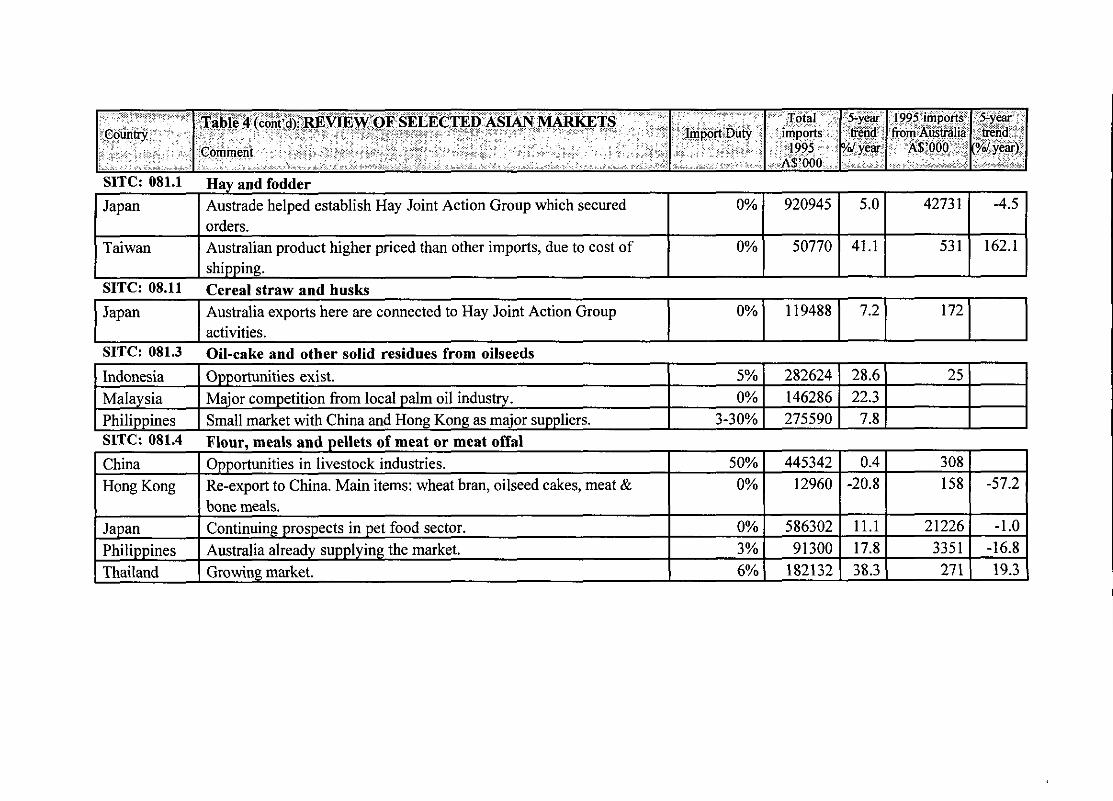

S I X : 081.1 Hay and fodder

I I shipping. I SITC: 08.11 Cereal straw and husks

) Japan 1 Australia exports here are connected to Hay Joint Action Group I 0%1 119488) 7.2) 172 1 I

1995 impons from Ausbalia

A6'000 Country

5-year trend

(?/d year) Import Duty

Table 4 (cont'd): REVIEW OF SELECTED ASIAN MARKETS

Comment

Japan I Austrade helped establish Hay Joint Action Group which secured 5.0 0% ( 920945

SITC: 081.3 Oil-cake and other solid residues from oilseeds

Total imports

1995 AS'OOO

5-yew trend

Yd year

42731

25

-4.5

Indonesia Malaysia Philippines

5% 0%

3-30%

Opportunities exist. Major competition from local palm oil industry. Small market with China and Hong Kong as major suppliers.

282624 146286 275590

28.6 22.3

7.8

t. a"<~S~* ,$ , , , ."," ..*<" .,,,: >,..>

'Country ?':.,

,~ " . , . . . ,. . ,. , . , , - ~

. . " n: _"). .-

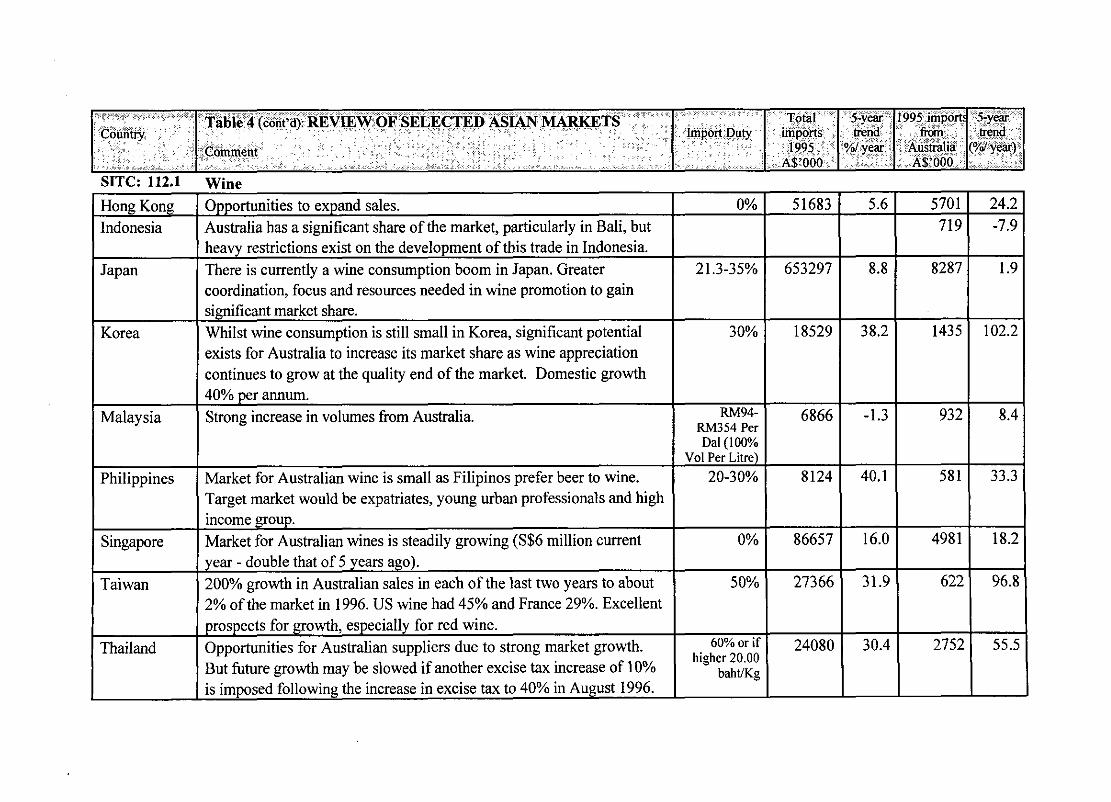

SITC: 112.1

Indonesia

Japan

Korea

Malaysia I-- Philippines t- Singapore

1 Thailand

Wine Opportunities to expand sales. Australia has a significant share of the market, particularly in Bali, but heavy restrictions exist on the development of this trade in Indonesia. There is currently a wine consumption boom in Japan. Greater coordination, focus and resources needed in wine promotion to gain significant market share. Whilst wine consumption is still small in Korea, significant potential exists for Australia to increase its market share as wine appreciation continues to grow at the quality end of the market. Domestic growth 40% per annum. Strong increase in volumes from Australia.

Market for Australian wine is small as Filipinos prefer beer to wine. Target market would be expatriates, young urban professionals and high income group. Market for Australian wines is steadily growing (S$6 million current year - double that of 5 years ago). 200% growth in Australian sales in each of the last two years to about 2% of the market in 1996. US wine had 45% and France 29%. Excellent prospects for growth, especially for red wine. Opportunities for Australian suppliers due to strong market growth. But future growth may be slowed if another excise tax increase of 10% is imposed following the increase in excise tax to 40% in August 1996.

RM354 Per Da1(100%

Vol Per Lihe

higher 20.00

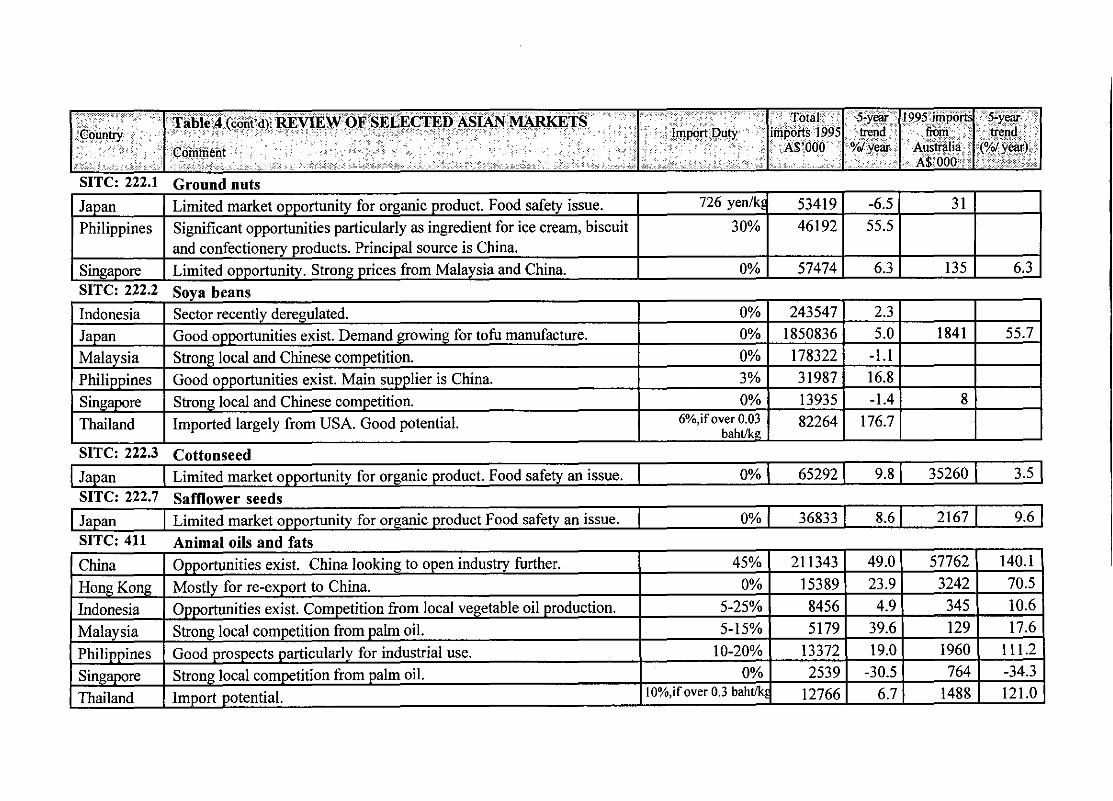

SITC: 222.1 Ground nuts Japan I Limited market opportunity for organic product. Food safety issue. 726 yenlkd 53419 1 -6.5 ( 31 1 Philippines I Significant opportunities particularly as ingredient for ice cream, biscuit I 30% 1 46192 1 55.5 1 - - - . . I and confectionery products. Principal source is China. Singapore 1 Limited opportunity. Strong prices from Malaysia and China. 0% I 57474 1 6.3 1 135 1 6.3

SITC: 222.7 Safflower seeds Japan I Limited market opportunity for organic product Food safety an issue. I OYo 1 36833 1 8.6 1 2167 1 9.6 1