Embed Size (px)

Citation preview

1

September 2016

ASIA PACIFIC DIGITAL LIMITED

FY16 Results Presentation

For

per

sona

l use

onl

y

2ASIA PACIFIC DIGITAL

DISCLAIMER

FY16 FULL YEAR RESULTS PRESENTATION

Not an offer

This Presentation is not a prospectus, product

disclosure statement or other offering document under

Australian law or any other law. This Presentation is for

information purposes only and is not an invitation or

offer of securities for subscription, purchase or sale in

any jurisdiction (and will not be lodged with the U.S

Securities Exchange Commission).

No Advice

This Presentation does not constitute investment or

financial product advice (nor tax, accounting or legal

advice) or any recommendation to acquire entitlements

or shares in the Company and does not and will not

form any part of any contract for the acquisition of

shares in the Company. Each recipient of this

Presentation should make its own enquiries and

investigations regarding all information in this

Presentation including but not limited to the

assumptions, uncertainties and contingencies which

may affect future operations of the Company and the

impact that different future outcomes may have on the

Company. Before making an investment decision,

prospective investors should consider the

appropriateness of the information having regard to

their own investment objectives, financial situation and

needs and seek legal, accounting and taxation advice

appropriate to their jurisdiction.

Foreign Jurisdictions

This Presentation may not be released or distributed in

the United States. This Presentation does not

constitute an offer to sell, or the solicitation of an offer

to buy, any securities in the United States.

Future performance

This Presentation contains certain ‘forward looking

statements’. Forward looking statements can generally

be identified by the use of forward looking words such

as, ‘expect’, ‘anticipate’, ‘likely’, ‘intend’, ‘should’,

‘could’, ‘may’, ‘predict’, ‘plan’, ‘propose’, ‘will’, ‘believe’,

‘forecast’, ‘estimate’, ‘target’ ‘outlook’, ‘guidance’ and

other similar expressions within the meaning of

securities laws of applicable jurisdictions. You are

cautioned not to place undue reliance on forward

looking statements. The statements, opinions and

estimates in this Presentation are based on

assumptions and contingencies subject to change

without notice, as are statements about market and

industry trends, projections, guidance and

estimates. The forward looking statements contained

in this Presentation are not guarantees or predictions of

future performance and involve known and unknown

risks and uncertainties and other factors, many of

which are beyond the control of the Company, and may

involve significant elements of subjective judgement

and assumptions as to future events which may or may

not be correct. There can be no assurance that actual

outcomes will not differ materially from these forward-

looking statements. A number of important factors

could cause actual results, achievements or

performance to differ materially from the forward

looking statements, including the risk factors set out in

this Presentation. The forward looking statements are

based on information available to the Company as at

the date of this Presentation.

Past performance

Investors should note that past performance is given

for illustrative purposes only and cannot be relied upon

as an indicator of (and provides no guidance as to)

future the Company’s performance. The pro forma

historical information is not represented as being

indicative of the Company’s views on its future financial

condition and/or performance.

Disclaimer

Neither the Company or its advisers or any of their

respective affiliates, related bodies corporate, directors,

officers, partners, employees and agents, have

authorised, permitted or caused the issue, submission,

dispatch or provision of this Presentation and, except to

the extent referred to in this Presentation, none of them

makes or purports to make any statement in this

Presentation and there is no statement in this

Presentation which is based on any statement by any

of them. To the maximum extent permitted by law, the

Company and its advisers, affiliates, related bodies

corporate, directors, officers, partners, employees and

agents make no representation or warranty, express or

implied, as to the currency, accuracy, reliability or

completeness of information in this Presentation.

Statements made in this Presentation are made only as

the date of this Presentation. The information in this

Presentation remains subject to change without notice.

For

per

sona

l use

onl

y

3VALUATION & INVESTMENT HIGHLIGHTSVALUATION & INVESTMENT HIGHLIGHTS

FY16 FULL YEAR RESULTS PRESENTATION

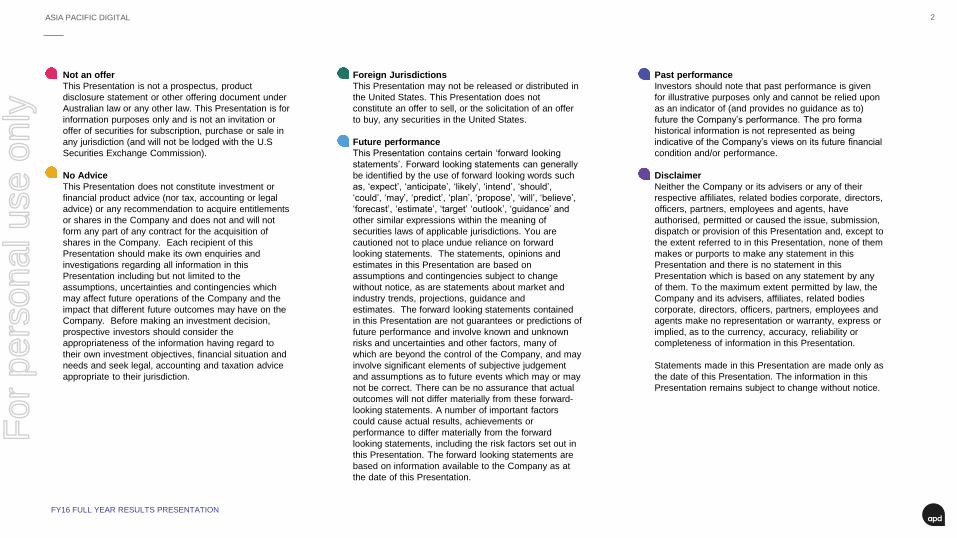

INVESTMENT HIGHLIGHTS

After platform

build, on track to

move to sustained

profitability in

FY17

p.24

South East Asia

is the world’s

highest growth

digital market

p.19

APD is uniquely

positioned to

participate in this

growth

p.20

Largely de-risked

with regional

platform

established

p.11-12

Expert team

with deep

industry

experience and

tech track

record

p.7-8

Valuation

undemanding

relative to market

peers and

transaction

metrics

p.29

1 2 3

4 5 6For

per

sona

l use

onl

y

4

OVERVIEW OF APD

For

per

sona

l use

onl

y

5

OVERVIEW OF APD

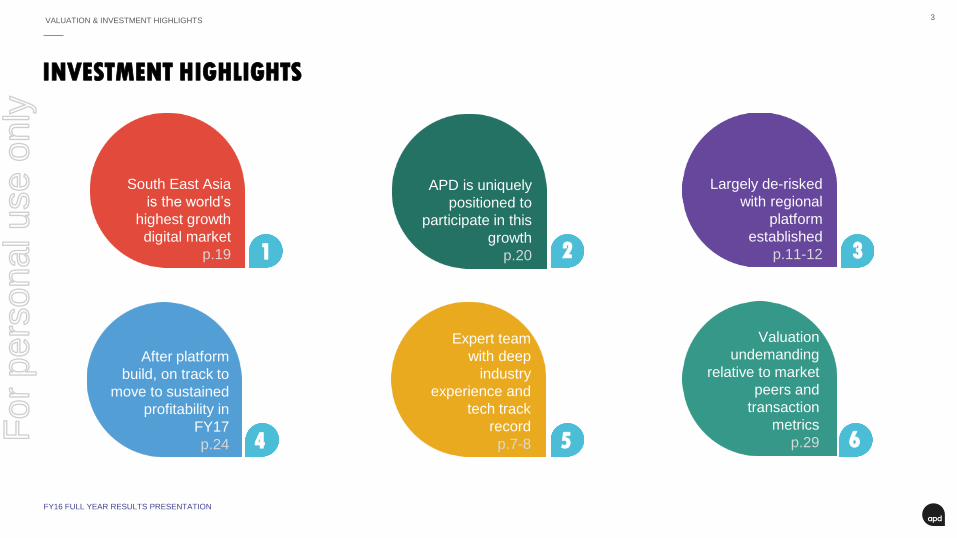

OVERVIEW OF APD

APAC’s largest

independent digital

services company

ASX: DIG ~400-strong team in

nine countries

$55m FY16 revenues

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

6OVERVIEW OF APD

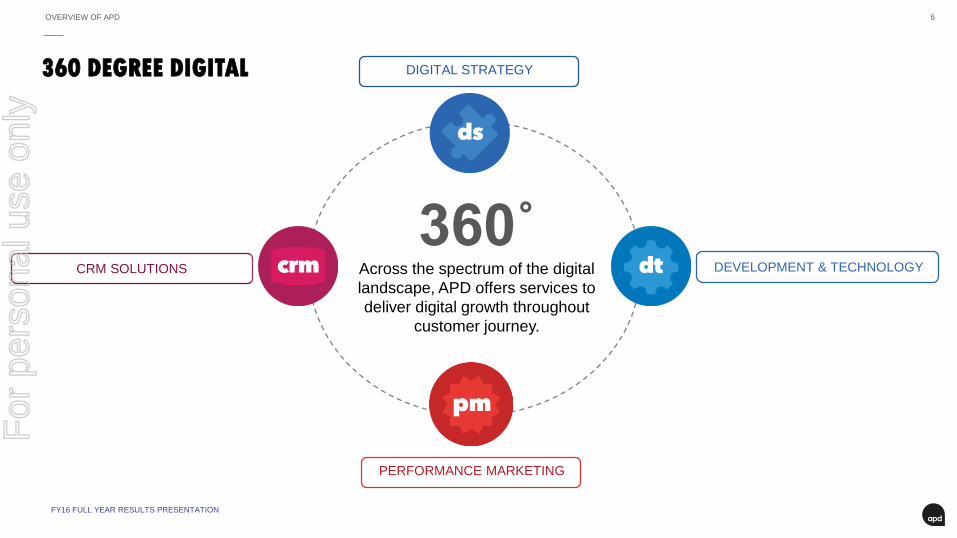

DIGITAL STRATEGY

DEVELOPMENT & TECHNOLOGY

PERFORMANCE MARKETING

CRM SOLUTIONS

360˚Across the spectrum of the digital

landscape, APD offers services to

deliver digital growth throughout

customer journey.

360 DEGREE DIGITAL

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

7

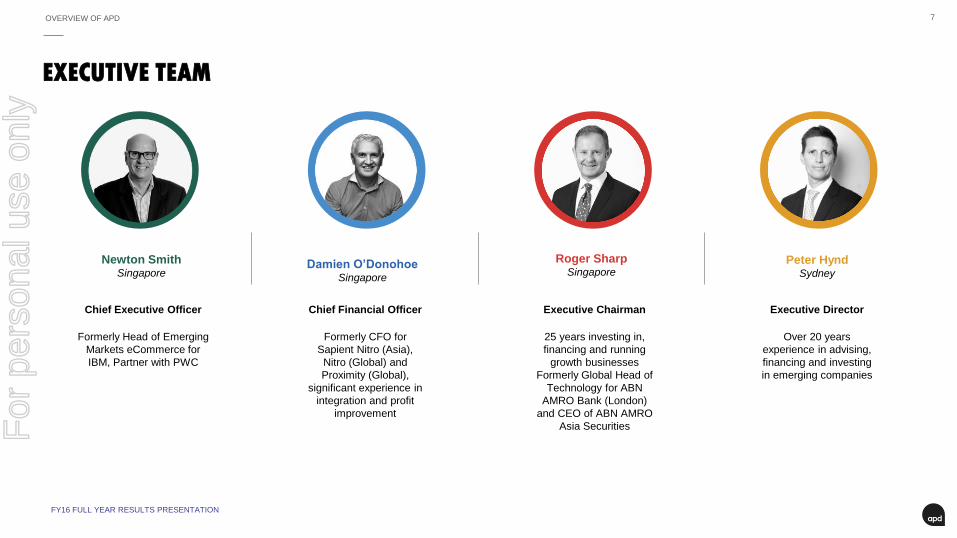

EXECUTIVE TEAM

Newton SmithSingapore

Chief Executive Officer

Formerly Head of Emerging

Markets eCommerce for

IBM, Partner with PWC

Damien O’DonohoeSingapore

Chief Financial Officer

Formerly CFO for

Sapient Nitro (Asia),

Nitro (Global) and

Proximity (Global),

significant experience in

integration and profit

improvement

Roger SharpSingapore

Peter HyndSydney

Executive Director

Over 20 years

experience in advising,

financing and investing

in emerging companies

Executive Chairman

25 years investing in,

financing and running

growth businesses

Formerly Global Head of

Technology for ABN

AMRO Bank (London)

and CEO of ABN AMRO

Asia Securities

OVERVIEW OF APD

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

8

MAJOR SHAREHOLDER

OVERVIEW OF APD

FY16 FULL YEAR RESULTS PRESENTATION

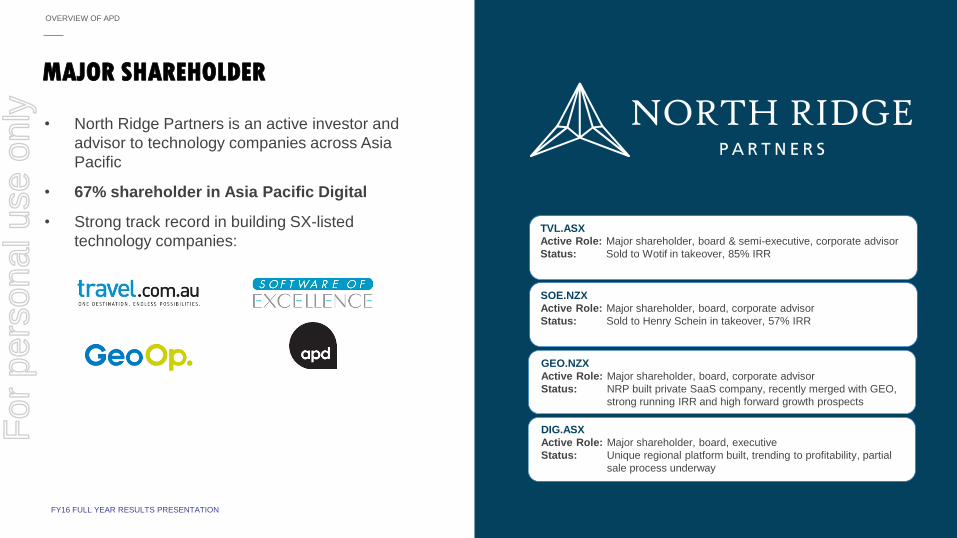

• North Ridge Partners is an active investor and

advisor to technology companies across Asia

Pacific

• 67% shareholder in Asia Pacific Digital

• Strong track record in building SX-listed

technology companies:TVL.ASX

Active Role: Major shareholder, board & semi-executive, corporate advisor

Status: Sold to Wotif in takeover, 85% IRR

SOE.NZX

Active Role: Major shareholder, board, corporate advisor

Status: Sold to Henry Schein in takeover, 57% IRR

GEO.NZX

Active Role: Major shareholder, board, corporate advisor

Status: NRP built private SaaS company, recently merged with GEO,

strong running IRR and high forward growth prospects

DIG.ASX

Active Role: Major shareholder, board, executive

Status: Unique regional platform built, trending to profitability, partial

sale process underway

For

per

sona

l use

onl

y

9OVERVIEW OF APD

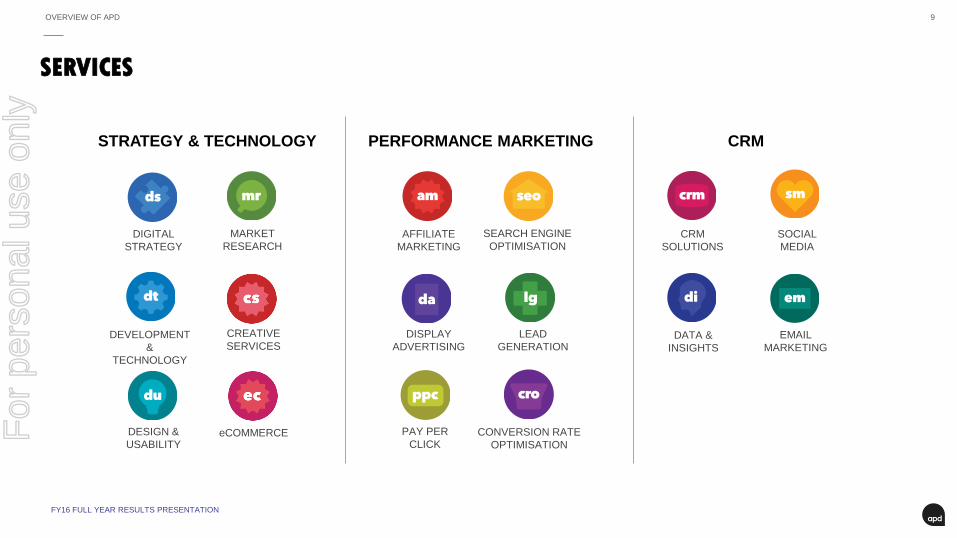

SERVICES

STRATEGY & TECHNOLOGY

DIGITAL

STRATEGY

DEVELOPMENT

&

TECHNOLOGY

DESIGN &

USABILITY

MARKET

RESEARCH

CREATIVE

SERVICES

eCOMMERCE

PERFORMANCE MARKETING

AFFILIATE

MARKETING

DISPLAY

ADVERTISING

PAY PER

CLICKCONVERSION RATE

OPTIMISATION

LEAD

GENERATION

SEARCH ENGINE

OPTIMISATION

CRM

CRM

SOLUTIONS

DATA &

INSIGHTS

MARKETING

SOCIAL

MEDIA

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

10OVERVIEW OF APD

FY16 FULL YEAR RESULTS PRESENTATION

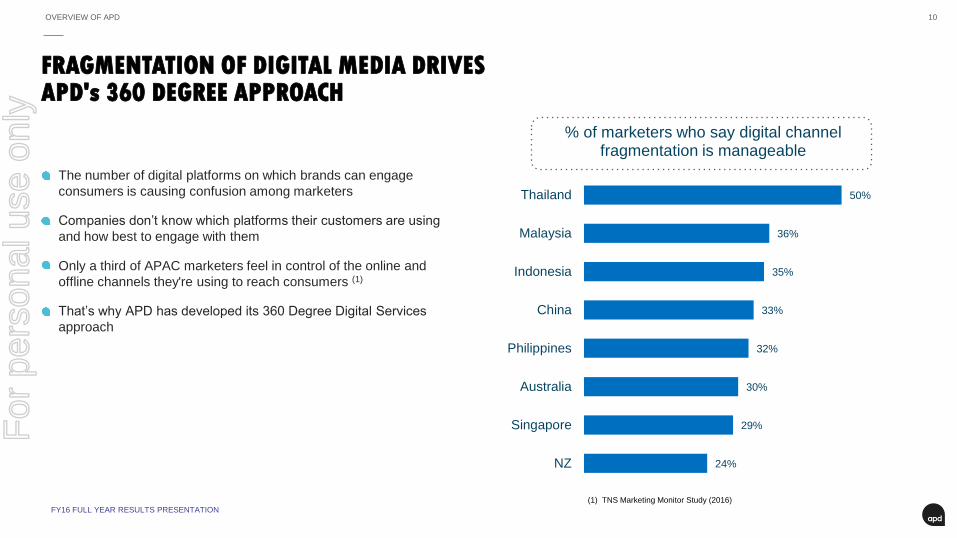

(1) TNS Marketing Monitor Study (2016)

The number of digital platforms on which brands can engage

consumers is causing confusion among marketers

Companies don’t know which platforms their customers are using

and how best to engage with them

Only a third of APAC marketers feel in control of the online and

offline channels they're using to reach consumers (1)

That’s why APD has developed its 360 Degree Digital Services

approach

24%

29%

30%

32%

33%

35%

36%

50%

NZ

Singapore

Australia

Philippines

China

Indonesia

Malaysia

Thailand

% of marketers who say digital channel fragmentation is manageable

FRAGMENTATION OF DIGITAL MEDIA DRIVES APD's 360 DEGREE APPROACH

For

per

sona

l use

onl

y

11

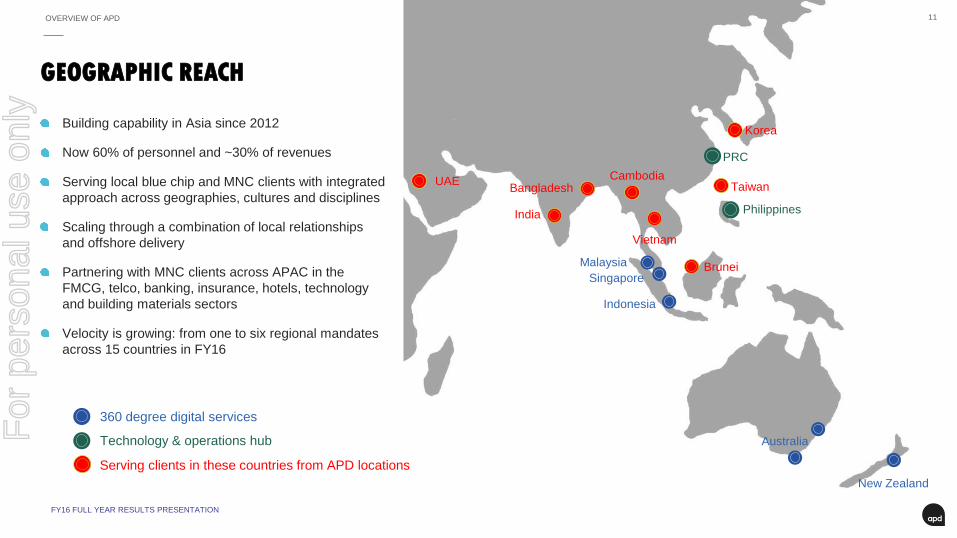

Building capability in Asia since 2012

Now 60% of personnel and ~30% of revenues

Serving local blue chip and MNC clients with integrated

approach across geographies, cultures and disciplines

Scaling through a combination of local relationships

and offshore delivery

Partnering with MNC clients across APAC in the

FMCG, telco, banking, insurance, hotels, technology

and building materials sectors

Velocity is growing: from one to six regional mandates

across 15 countries in FY16

PRC

Malaysia

Singapore

Australia

New Zealand

Indonesia

GEOGRAPHIC REACH

Serving clients in these countries from APD locations

Korea

Taiwan

Philippines

Vietnam

Brunei

CambodiaBangladesh

India

UAE

Technology & operations hub

360 degree digital services

OVERVIEW OF APD

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

12

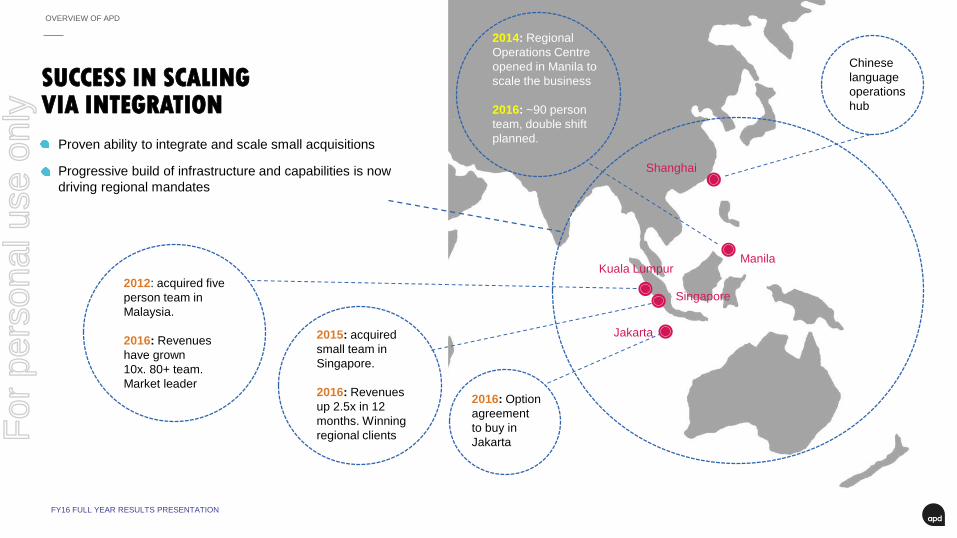

Proven ability to integrate and scale small acquisitions

Progressive build of infrastructure and capabilities is now

driving regional mandates

SUCCESS IN SCALING VIA INTEGRATION

OVERVIEW OF APD

FY16 FULL YEAR RESULTS PRESENTATION

Kuala Lumpur

Singapore

Manila

2012: acquired five

person team in

Malaysia.

2016: Revenues

have grown

10x. 80+ team.

Market leader

2014: Regional

Operations Centre

opened in Manila to

scale the business

2016: ~90 person

team, double shift

planned.

2015: acquired

small team in

Singapore.

2016: Revenues

up 2.5x in 12

months. Winning

regional clients

2016: Option

agreement

to buy in

Jakarta

Jakarta

Shanghai

Chinese

language

operations

hub

For

per

sona

l use

onl

y

13OVERVIEW OF APD

20 YEARS OF CLIENT SUCCESS STORIES

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

14OVERVIEW OF APD

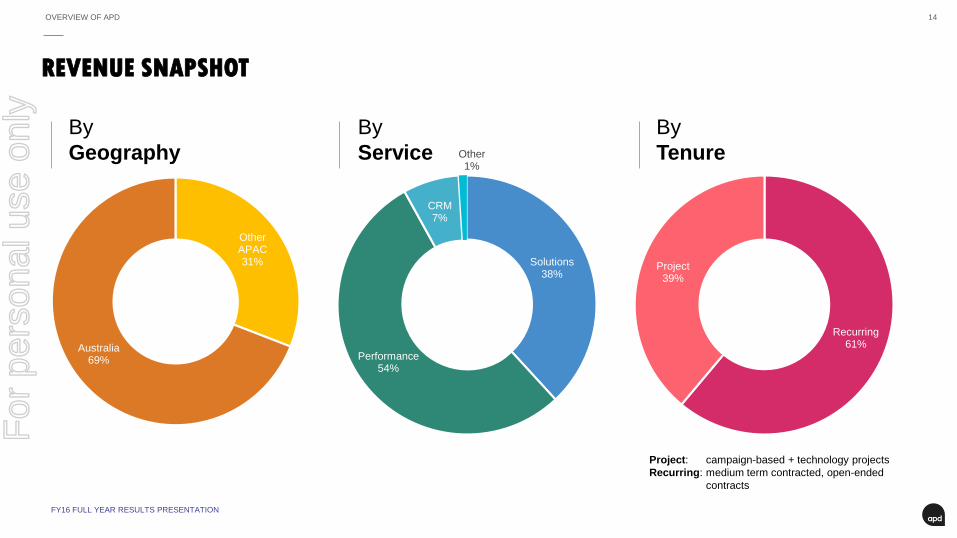

REVENUE SNAPSHOT

Other APAC31%

Australia69%

Solutions38%

Performance54%

CRM7%

Other1%

Recurring61%

Project39%

By

Geography

By

Service

By

Tenure

FY16 FULL YEAR RESULTS PRESENTATION

Project: campaign-based + technology projects

Recurring: medium term contracted, open-ended

contracts

For

per

sona

l use

onl

y

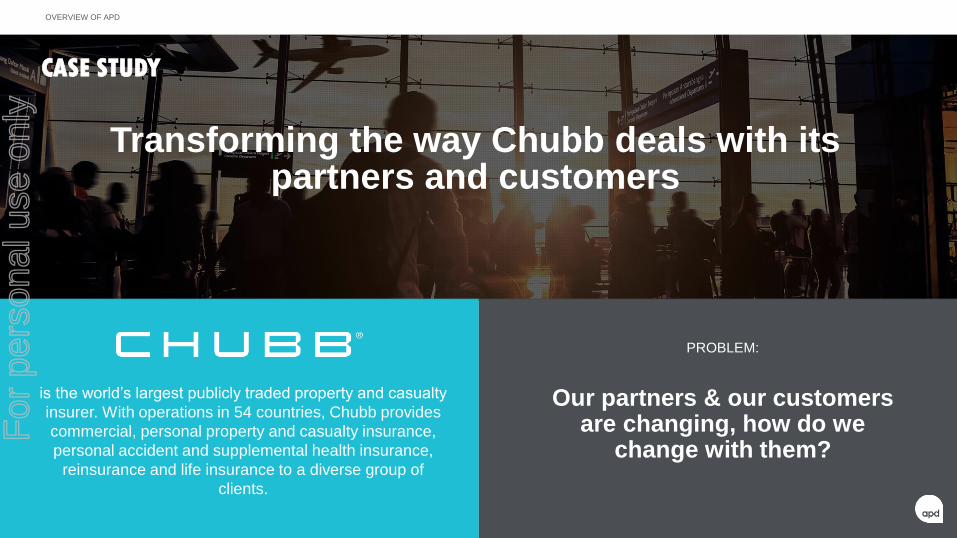

is the world’s largest publicly traded property and casualty

insurer. With operations in 54 countries, Chubb provides

commercial, personal property and casualty insurance,

personal accident and supplemental health insurance,

reinsurance and life insurance to a diverse group of

clients.

Transforming the way Chubb deals with its partners and customers

Our partners & our customers are changing, how do we

change with them?

PROBLEM:

CASE STUDY

OVERVIEW OF APDF

or p

erso

nal u

se o

nly

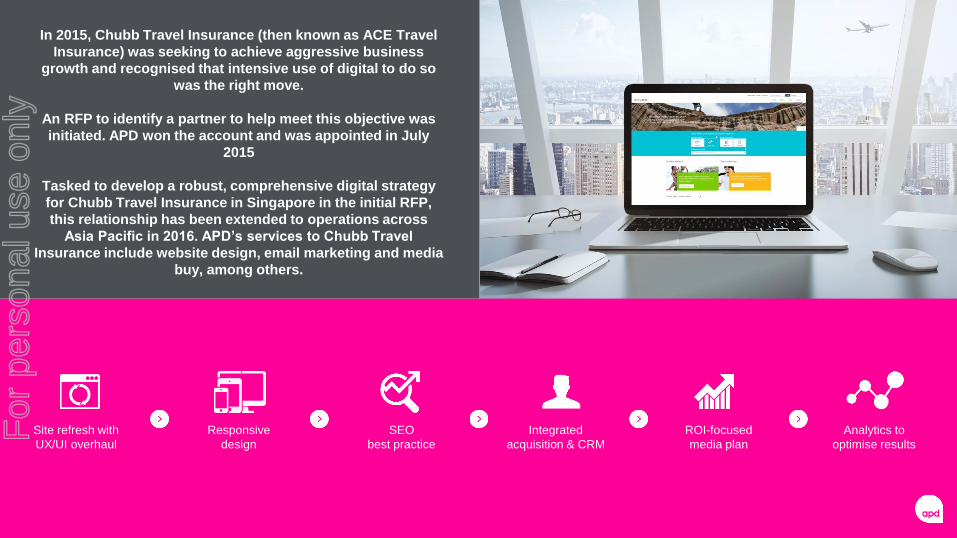

In 2015, Chubb Travel Insurance (then known as ACE Travel

Insurance) was seeking to achieve aggressive business

growth and recognised that intensive use of digital to do so

was the right move.

An RFP to identify a partner to help meet this objective was

initiated. APD won the account and was appointed in July

2015

Tasked to develop a robust, comprehensive digital strategy

for Chubb Travel Insurance in Singapore in the initial RFP,

this relationship has been extended to operations across

Asia Pacific in 2016. APD’s services to Chubb Travel

Insurance include website design, email marketing and media

buy, among others.

Site refresh with

UX/UI overhaul

Responsive

design

SEO

best practice

Integrated

acquisition & CRM

ROI-focused

media plan

Analytics to

optimise results

For

per

sona

l use

onl

y

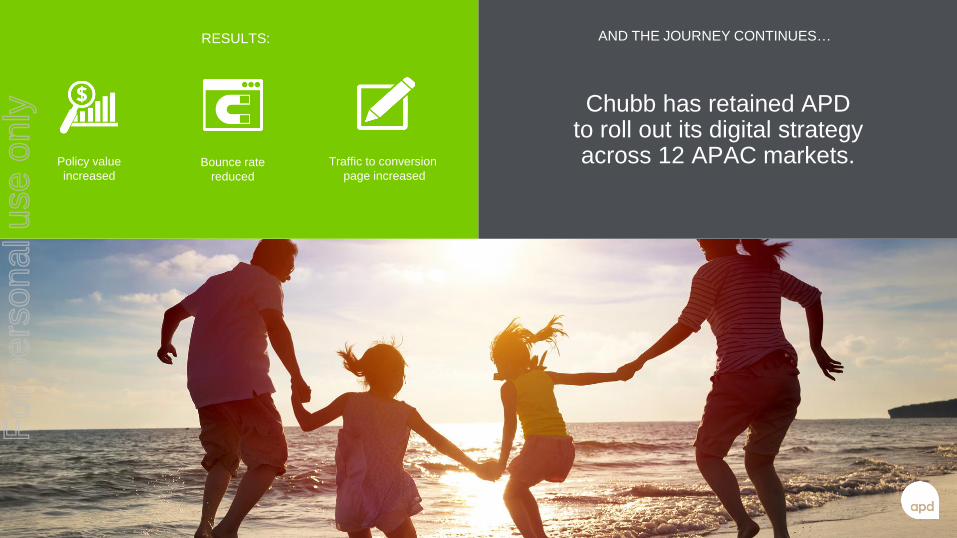

Traffic to conversion

page increased

RESULTS:

Bounce rate

reduced

Chubb has retained APD to roll out its digital strategy across 12 APAC markets. Policy value

increased

AND THE JOURNEY CONTINUES…F

or p

erso

nal u

se o

nly

18

MARKET & OPPORTUNITY

For

per

sona

l use

onl

y

19MARKET & OPPORTUNITY

FY16 FULL YEAR RESULTS PRESENTATION

MARKET OPPORTUNITY

World’s Fastest Growing Internet Region

SEA is adding 3.8m new internet users

per month

14 14

4

1 1

ASEAN India China US EU

2015-20 CAGR in Internet Users (%)

0.8

6.4

2015 2025

eComm as % of Total Retail Spend

SEA eCommerce Spend Rapidly Expanding

eCommerce spend will grow 16x from 2015-

20

Online Advertising Increasing as a Result

SEA online advertising will grow 5x by 2025

0.2

0.7

0.1

0.30.4

0.3

0.91

1.51.6

2.3

2.7

MY SG PH VN TH ID

Online Ad Market ($b)

2015 2025(f)

Source: Google | Temasek: e-conomy SEA Report (2016)

For

per

sona

l use

onl

y

20MARKET & OPPORTUNITY

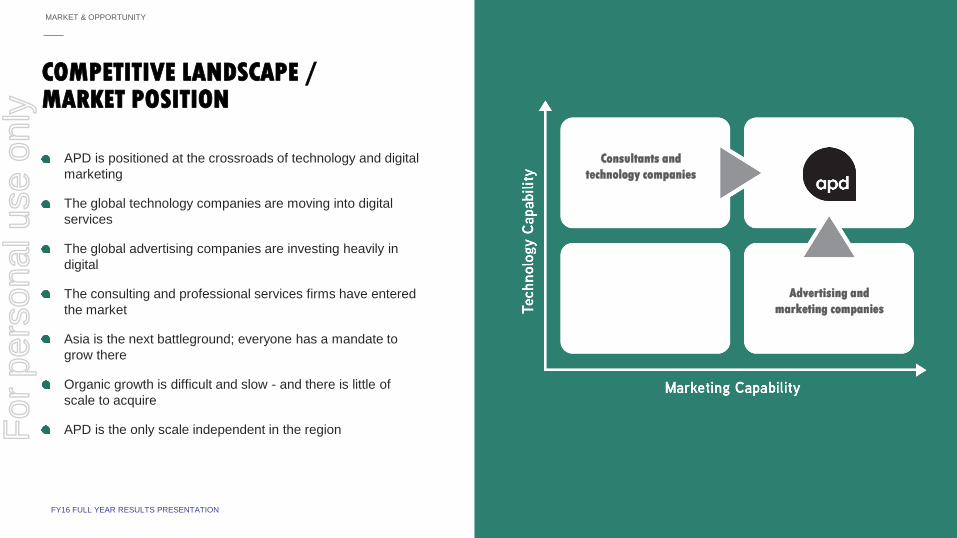

APD is positioned at the crossroads of technology and digital

marketing

The global technology companies are moving into digital

services

The global advertising companies are investing heavily in

digital

The consulting and professional services firms have entered

the market

Asia is the next battleground; everyone has a mandate to

grow there

Organic growth is difficult and slow - and there is little of

scale to acquire

APD is the only scale independent in the region

COMPETITIVE LANDSCAPE / MARKET POSITION

FY16 FULL YEAR RESULTS PRESENTATION

Advertising and

marketing companies

Consultants and

technology companies

For

per

sona

l use

onl

y

21

FY16 RESULTS OVERVIEW

For

per

sona

l use

onl

y

22

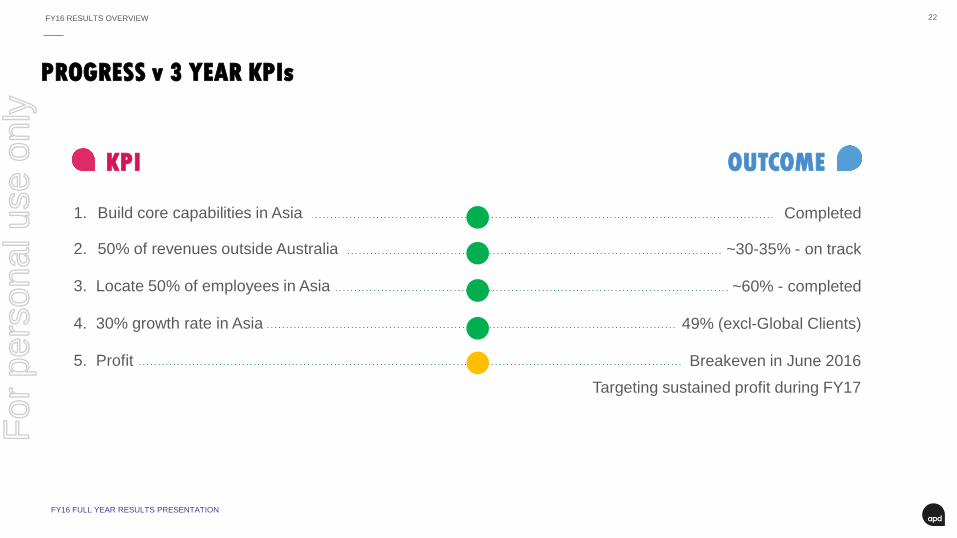

PROGRESS v 3 YEAR KPIs

FY16 RESULTS OVERVIEW

Completed

~30-35% - on track

~60% - completed

49% (excl-Global Clients)

Breakeven in June 2016

Targeting sustained profit during FY17

1. Build core capabilities in Asia

2. 50% of revenues outside Australia

3. Locate 50% of employees in Asia

4. 30% growth rate in Asia

5. Profit

KPI OUTCOME

FY16 RESULTS OVERVIEW

FY16 FULL YEAR RESULTS PRESENTATION

For

per

sona

l use

onl

y

23

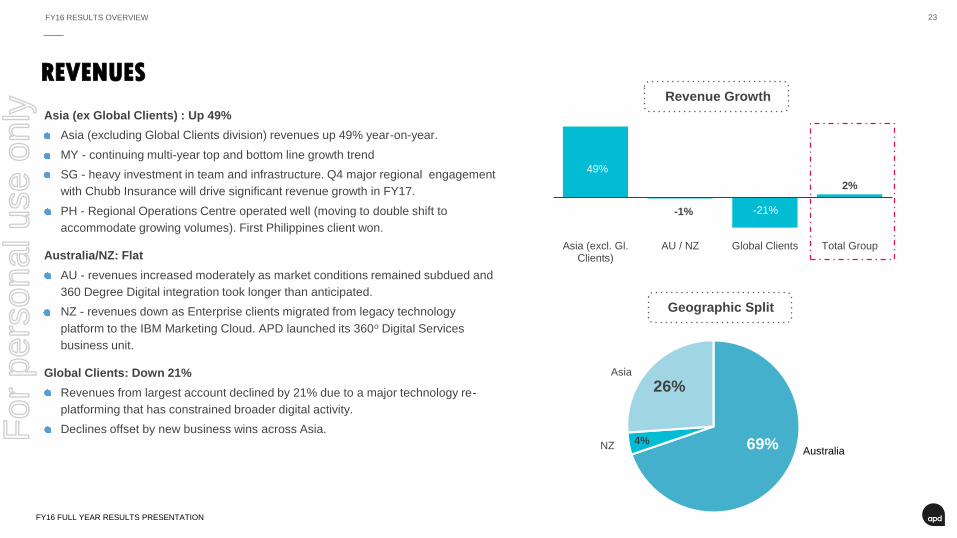

49%

-1% -21%

2%

Asia (excl. Gl.Clients)

AU / NZ Global Clients Total Group

Revenue Growth

REVENUES

FY16 RESULTS OVERVIEW

FY16 FULL YEAR RESULTS PRESENTATION

Asia (ex Global Clients) : Up 49%

Asia (excluding Global Clients division) revenues up 49% year-on-year.

MY - continuing multi-year top and bottom line growth trend

SG - heavy investment in team and infrastructure. Q4 major regional engagement

with Chubb Insurance will drive significant revenue growth in FY17.

PH - Regional Operations Centre operated well (moving to double shift to

accommodate growing volumes). First Philippines client won.

Australia/NZ: Flat

AU - revenues increased moderately as market conditions remained subdued and

360 Degree Digital integration took longer than anticipated.

NZ - revenues down as Enterprise clients migrated from legacy technology

platform to the IBM Marketing Cloud. APD launched its 360o Digital Services

business unit.

Global Clients: Down 21%

Revenues from largest account declined by 21% due to a major technology re-

platforming that has constrained broader digital activity.

Declines offset by new business wins across Asia.

69%4%

26%

Geographic Split

Australia

Asia

NZ

For

per

sona

l use

onl

y

24

PROFITABILITY

FY16 RESULTS OVERVIEW

FY16 FULL YEAR RESULTS PRESENTATION

$2m

$3m

$4m

J F M A M J

H2Y16 Financial Progression

Revenue, net of direct variable costs

Other Expenses

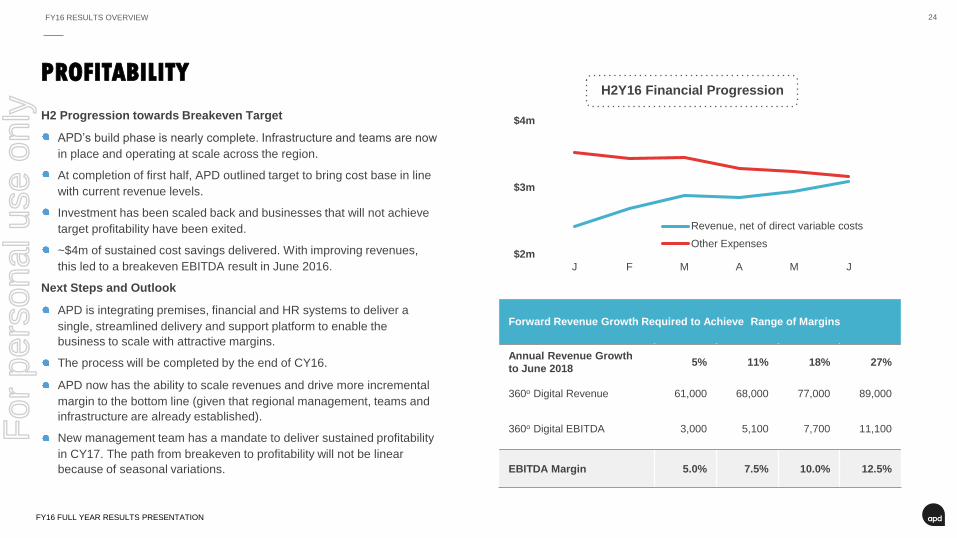

H2 Progression towards Breakeven Target

APD’s build phase is nearly complete. Infrastructure and teams are now

in place and operating at scale across the region.

At completion of first half, APD outlined target to bring cost base in line

with current revenue levels.

Investment has been scaled back and businesses that will not achieve

target profitability have been exited.

~$4m of sustained cost savings delivered. With improving revenues,

this led to a breakeven EBITDA result in June 2016.

Next Steps and Outlook

APD is integrating premises, financial and HR systems to deliver a

single, streamlined delivery and support platform to enable the

business to scale with attractive margins.

The process will be completed by the end of CY16.

APD now has the ability to scale revenues and drive more incremental

margin to the bottom line (given that regional management, teams and

infrastructure are already established).

New management team has a mandate to deliver sustained profitability

in CY17. The path from breakeven to profitability will not be linear

because of seasonal variations.

Forward Revenue Growth Required to Achieve Range of Margins

Annual Revenue Growth

to June 20185% 11% 18% 27%

360o Digital Revenue 61,000 68,000 77,000 89,000

360o Digital EBITDA 3,000 5,100 7,700 11,100

EBITDA Margin 5.0% 7.5% 10.0% 12.5%

For

per

sona

l use

onl

y

25

FY16 FULL YEAR RESULTS PRESENTATION

FY16 RESULTS OVERVIEW

FINANCIAL RESULTS

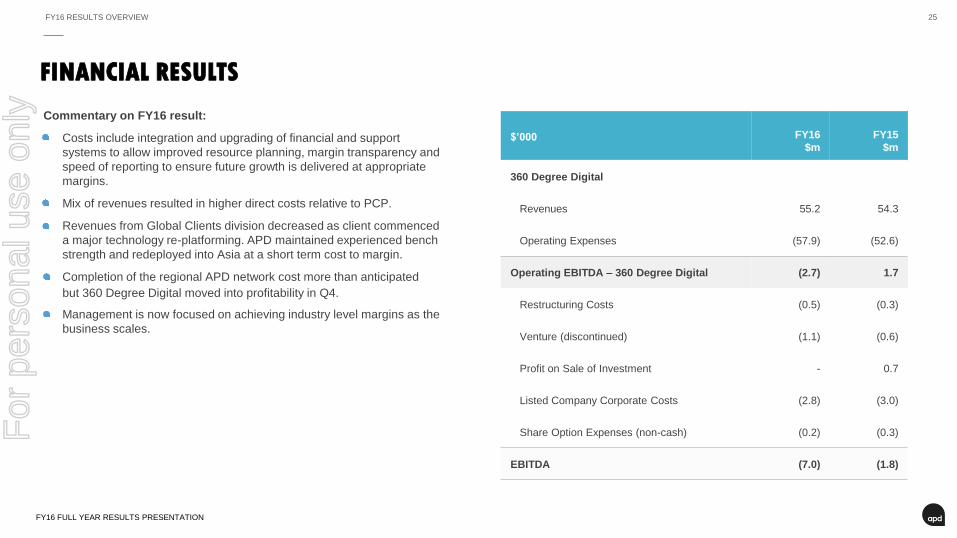

Commentary on FY16 result:

Costs include integration and upgrading of financial and support

systems to allow improved resource planning, margin transparency and

speed of reporting to ensure future growth is delivered at appropriate

margins.

Mix of revenues resulted in higher direct costs relative to PCP.

Revenues from Global Clients division decreased as client commenced

a major technology re-platforming. APD maintained experienced bench

strength and redeployed into Asia at a short term cost to margin.

Completion of the regional APD network cost more than anticipated

but 360 Degree Digital moved into profitability in Q4.

Management is now focused on achieving industry level margins as the

business scales.

$’000 FY16

$m

FY15

$m

360 Degree Digital

Revenues 55.2 54.3

Operating Expenses (57.9) (52.6)

Operating EBITDA – 360 Degree Digital (2.7) 1.7

Restructuring Costs (0.5) (0.3)

Venture (discontinued) (1.1) (0.6)

Profit on Sale of Investment - 0.7

Listed Company Corporate Costs (2.8) (3.0)

Share Option Expenses (non-cash) (0.2) (0.3)

EBITDA (7.0) (1.8)

For

per

sona

l use

onl

y

26FY16 RESULTS OVERVIEW

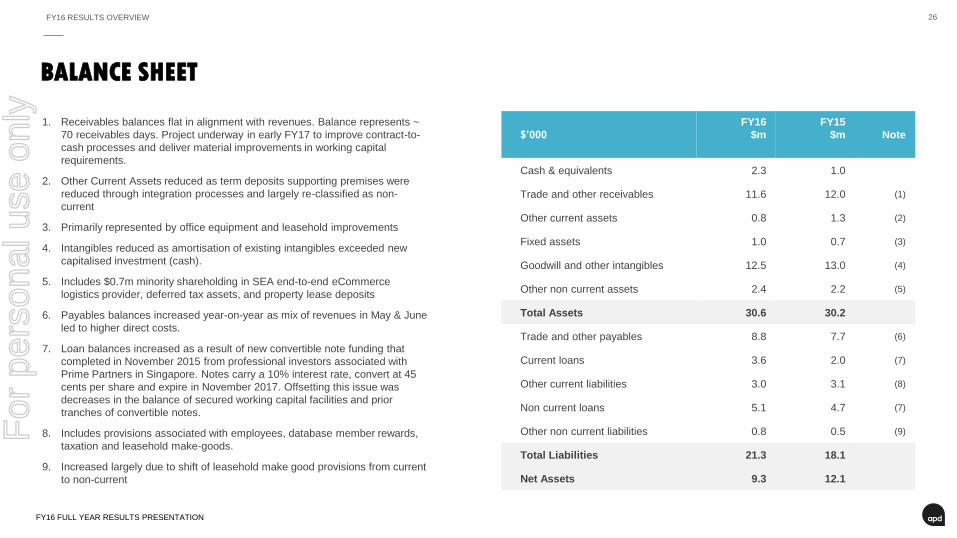

BALANCE SHEET

$’000

FY16

$m

FY15

$m Note

Cash & equivalents 2.3 1.0

Trade and other receivables 11.6 12.0 (1)

Other current assets 0.8 1.3 (2)

Fixed assets 1.0 0.7 (3)

Goodwill and other intangibles 12.5 13.0 (4)

Other non current assets 2.4 2.2 (5)

Total Assets 30.6 30.2

Trade and other payables 8.8 7.7 (6)

Current loans 3.6 2.0 (7)

Other current liabilities 3.0 3.1 (8)

Non current loans 5.1 4.7 (7)

Other non current liabilities 0.8 0.5 (9)

Total Liabilities 21.3 18.1

Net Assets 9.3 12.1

• [x]

FY16 FULL YEAR RESULTS PRESENTATION

1. Receivables balances flat in alignment with revenues. Balance represents ~

70 receivables days. Project underway in early FY17 to improve contract-to-

cash processes and deliver material improvements in working capital

requirements.

2. Other Current Assets reduced as term deposits supporting premises were

reduced through integration processes and largely re-classified as non-

current

3. Primarily represented by office equipment and leasehold improvements

4. Intangibles reduced as amortisation of existing intangibles exceeded new

capitalised investment (cash).

5. Includes $0.7m minority shareholding in SEA end-to-end eCommerce

logistics provider, deferred tax assets, and property lease deposits

6. Payables balances increased year-on-year as mix of revenues in May & June

led to higher direct costs.

7. Loan balances increased as a result of new convertible note funding that

completed in November 2015 from professional investors associated with

Prime Partners in Singapore. Notes carry a 10% interest rate, convert at 45

cents per share and expire in November 2017. Offsetting this issue was

decreases in the balance of secured working capital facilities and prior

tranches of convertible notes.

8. Includes provisions associated with employees, database member rewards,

taxation and leasehold make-goods.

9. Increased largely due to shift of leasehold make good provisions from current

to non-current

For

per

sona

l use

onl

y

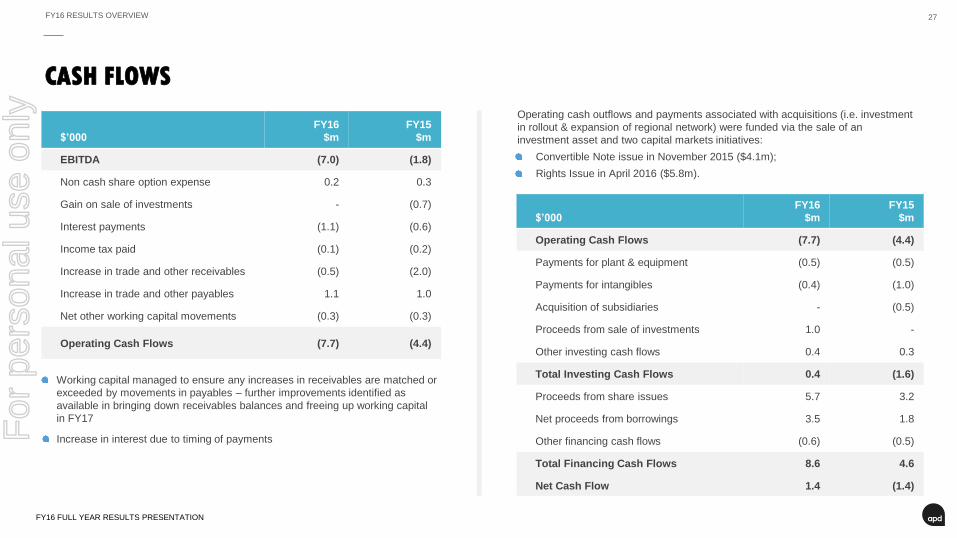

27FY16 RESULTS OVERVIEW

2

7

$’000

FY16

$m

FY15

$m

EBITDA (7.0) (1.8)

Non cash share option expense 0.2 0.3

Gain on sale of investments - (0.7)

Interest payments (1.1) (0.6)

Income tax paid (0.1) (0.2)

Increase in trade and other receivables (0.5) (2.0)

Increase in trade and other payables 1.1 1.0

Net other working capital movements (0.3) (0.3)

Operating Cash Flows (7.7) (4.4)

FY16 FULL YEAR RESULTS PRESENTATION

CASH FLOWS

Working capital managed to ensure any increases in receivables are matched or

exceeded by movements in payables – further improvements identified as

available in bringing down receivables balances and freeing up working capital

in FY17

Increase in interest due to timing of payments

$’000

FY16

$m

FY15

$m

Operating Cash Flows (7.7) (4.4)

Payments for plant & equipment (0.5) (0.5)

Payments for intangibles (0.4) (1.0)

Acquisition of subsidiaries - (0.5)

Proceeds from sale of investments 1.0 -

Other investing cash flows 0.4 0.3

Total Investing Cash Flows 0.4 (1.6)

Proceeds from share issues 5.7 3.2

Net proceeds from borrowings 3.5 1.8

Other financing cash flows (0.6) (0.5)

Total Financing Cash Flows 8.6 4.6

Net Cash Flow 1.4 (1.4)

Operating cash outflows and payments associated with acquisitions (i.e. investment

in rollout & expansion of regional network) were funded via the sale of an

investment asset and two capital markets initiatives:

• Convertible Note issue in November 2015 ($4.1m);

• Rights Issue in April 2016 ($5.8m).

For

per

sona

l use

onl

y

28

VALUATION & INVESTMENT

HIGHLIGHTS

For

per

sona

l use

onl

y

29VALUATION & INVESTMENT HIGHLIGHTS

2

9

• [x]

FY16 FULL YEAR RESULTS PRESENTATION

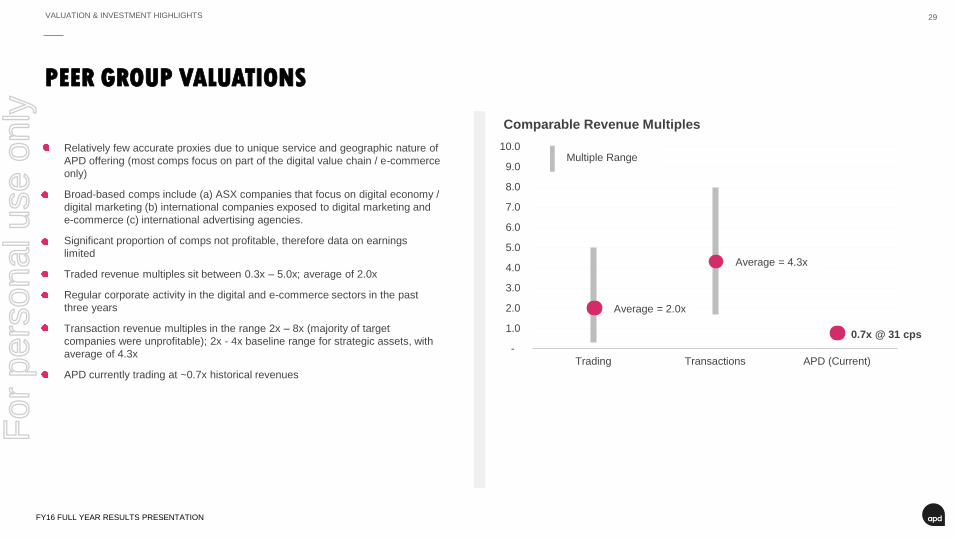

PEER GROUP VALUATIONS

-

1.0

2.0

3.0

4.0

5.0

6.0

7.0

8.0

9.0

10.0

Trading Transactions APD (Current)

Relatively few accurate proxies due to unique service and geographic nature of

APD offering (most comps focus on part of the digital value chain / e-commerce

only)

Broad-based comps include (a) ASX companies that focus on digital economy /

digital marketing (b) international companies exposed to digital marketing and

e-commerce (c) international advertising agencies.

Significant proportion of comps not profitable, therefore data on earnings

limited

Traded revenue multiples sit between 0.3x – 5.0x; average of 2.0x

Regular corporate activity in the digital and e-commerce sectors in the past

three years

Transaction revenue multiples in the range 2x – 8x (majority of target

companies were unprofitable); 2x - 4x baseline range for strategic assets, with

average of 4.3x

APD currently trading at ~0.7x historical revenues

Comparable Revenue Multiples

Multiple Range

Average = 2.0x

Average = 4.3x

0.7x @ 31 cps

For

per

sona

l use

onl

y

30VALUATION & INVESTMENT HIGHLIGHTSVALUATION & INVESTMENT HIGHLIGHTS

FY16 FULL YEAR RESULTS PRESENTATION

INVESTMENT HIGHLIGHTS

After platform

build, on track to

move to

sustained

profitability in

FY17

South East Asia

is the world’s

highest growth

digital market

APD is

uniquely

positioned to

participate in

this growth

Largely de-

risked with

regional

platform

established

Expert team

with deep

industry

experience and

tech track

record

Valuation

undemanding

relative to market

peers and

transaction

metricsFor

per

sona

l use

onl

y

31

APPENDIX

For

per

sona

l use

onl

y

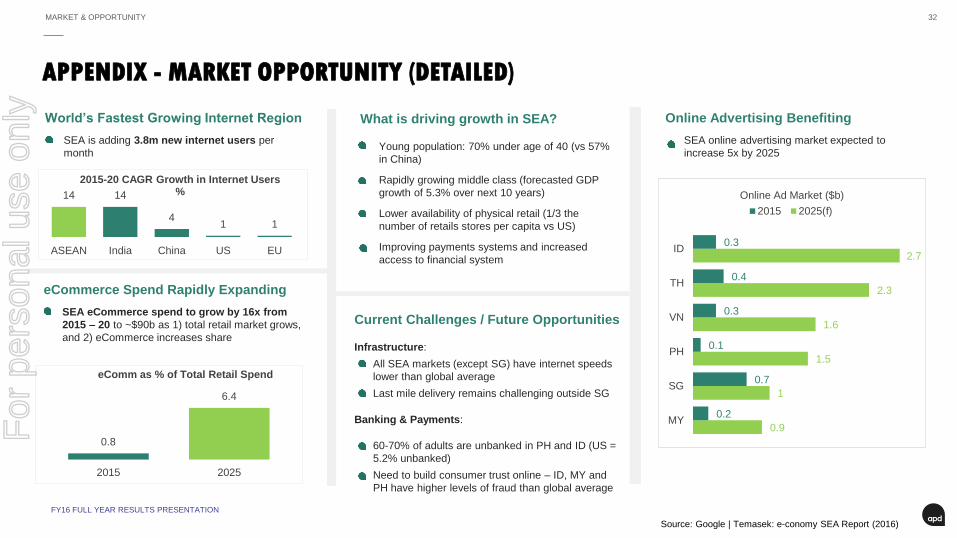

32MARKET & OPPORTUNITY

FY16 FULL YEAR RESULTS PRESENTATION

APPENDIX - MARKET OPPORTUNITY (DETAILED)

World’s Fastest Growing Internet Region

SEA is adding 3.8m new internet users per

month

What is driving growth in SEA?

Young population: 70% under age of 40 (vs 57%

in China)

Rapidly growing middle class (forecasted GDP

growth of 5.3% over next 10 years)

Lower availability of physical retail (1/3 the

number of retails stores per capita vs US)

Improving payments systems and increased

access to financial system

14 14

41 1

ASEAN India China US EU

2015-20 CAGR Growth in Internet Users %

0.8

6.4

2015 2025

eComm as % of Total Retail Spend

eCommerce Spend Rapidly Expanding

SEA eCommerce spend to grow by 16x from

2015 – 20 to ~$90b as 1) total retail market grows,

and 2) eCommerce increases share

Current Challenges / Future Opportunities

Infrastructure:

All SEA markets (except SG) have internet speeds

lower than global average

Last mile delivery remains challenging outside SG

Banking & Payments:

60-70% of adults are unbanked in PH and ID (US =

5.2% unbanked)

Need to build consumer trust online – ID, MY and

PH have higher levels of fraud than global average

Online Advertising Benefiting

SEA online advertising market expected to

increase 5x by 2025

0.9

1

1.5

1.6

2.3

2.7

0.2

0.7

0.1

0.3

0.4

0.3

MY

SG

PH

VN

TH

ID

Online Ad Market ($b)

2015 2025(f)

Source: Google | Temasek: e-conomy SEA Report (2016)

For

per

sona

l use

onl

y

33

THANK YOU

For

per

sona

l use

onl

y