Embed Size (px)

Citation preview

Deloitte Center for Health Solutions

April 8, 2013

Monday memo

Health reform update

This week’s headlines: My take

Implementation update - Key ACA provisions impacting the medical device and biopharma industries - Rule on small business plan options on HIXs delayed - Report: number of self-insured plans decreased but participant enrollment increased - OIG report: information about health insurance plans for consumers on

Healthcare.gov website inadequate - HHS proposes new guidelines for HIX Navigator Program, does not allow insurance

companies to provide Navigator services

Legislative update - President to release budget Wednesday - SGR fix proposed in House committee - Senate Finance Committee schedules hearing on Tavenner - Meaningful use update: bill to exempt solo practices and physicians nearing

retirement; request for safe harbor guidance - District court rules in favor of emergency contraception coverage without age

restriction

State update - State HIX update

- Medicaid expansion update - State round-up

Industry news - Cuts to Medicare Advantage plans set aside; Part D rates announced - Medical testing labs see growth but margin erosion; Medicare cost-sharing

accelerates sector pressure - Small business survey: ACA the major concern - Generic drug makers challenge abuse deterrent requirements as anti-competitive - IOM analysis: Medicare spending variation influenced largely by long-term care

utilization - India Supreme Court strikes down cancer drug patent - Study: dementia costs $215 billion

Research snapshots

Quotable

Fact file

Subscribe to the Health Care Reform Memo

Deloitte Center for Health Solutions research

Read the blog

Upcoming life sciences and health care Dbriefs webcasts and events

Deloitte contacts

My take

From Paul Keckley, Executive Director, Deloitte Center for Health Solutions

I embarrassed myself Monday night. After a jog on the beach and round of golf in

Naples, Florida, I passed out at a reception from dehydration. All I remember is a cold

sweat and next hearing my Deloitte colleague Mitch Morris who is a physician, ask “what

medications are you taking” as he attended to my recovery.

I’ve re-lived that moment frequently since—my right elbow bore the brunt of my fall so

it’s quite sensitive a week later. But I also find myself, once again, thinking through that

ordeal as a consumer in the health care system.

Like good doctors do, Mitch instinctively knew he needed information about my

prescriptions. It’s the first question I recall as I came to my senses. I remember saying

“statin” but little more. After a while, I was feeling better, though no less embarrassed.

Like the advertisement says, life comes at you fast. I was drinking ice water one minute

and on the floor the next. My recollection is falling and next Mitch’s inquiry asking about

my prescription drug regimen.

For health care industry folks, the drug manufacturing industry is a prominent player—at

$320 billion in U.S. sales, it’s 12% of the U.S. health care spend and almost half of the

total global market.1 It’s a big industry: $49 billion research and development (R&D)

investment exploring 2,900 new therapies currently in development.2

For policymakers and public health officials it’s often a perplexing industry with promise

and peril: prescription drug abuse could be viewed as an epidemic, especially addictions

to pain medications dispensed fairly freely through pill mills. Protection of intellectual

property owned by its companies is often problematic in emerging markets where

copycats are likely to flourish with government approval. Patent expirations could cut

$142 billion from the industry’s revenues through 2015 resulting in a decrease in drug

spending for the first time in 20 years.3 And medication non-adherence is costly:

estimated to cause up to 10% of hospital admissions and 23% of nursing home

admissions as a direct result.4 Yet, appropriate use of medications—prescribed and

dosed accurately—combined with patient adherence is a promising way to reducing

costs and improving health.

But for the average Joe, prescription drugs are a way of life, and for some a lifeline.

Pharmacies are on every corner—56,000 of them and counting. The industry spends

almost $20 billion promoting its products—$5 billion on TV ads that encourage would-be

users to “consult your doctor.”5 And online and newsstand tools to assist in smart

purchasing are readily accessible like the “Consumer Reports Best Buy Drugs” and

others. Perhaps unlike any other industry, in health care, the biopharmaceutical industry

is on the frontline of consumerism.

As a student of the health care industry, I can’t imagine a more complicated sector: its

market is global; its regulatory framework unique in each; its risks are high; its visibility

even higher and demand is soaring. An Internal Revenue Service (IRS) report released

last week said it well:

“Many foreign companies have been entering the United States market because of its

uncontrolled pricing structure, rapid approval processes, private and public insurance

reimbursement policies and government support for basic research. Additionally, the

industry enjoys many tax benefits not available in other countries, although the benefits

are narrowing.

The tax benefits include Research & Experiment Credit for research conducted in the

United States, the IRC 936 Puerto Rican Tax Credit for possession companies, and

Orphan Drug Credit for illnesses afflicting two hundred thousand or less patients.

Benefits of relocation to the United States include the ability to advertise to both the

medical community and direct to consumers in an effort to increase awareness and

consumption.”6

The U.S. biopharmaceutical industry is at a tipping point: increased consumerism,

increased scrutiny of business relationships and conflicts with investigators, increased

rigor in scientific efficacy and effectiveness (including comparative effectiveness

research), increased regulation, increased margin pressure, increased costs of

development, and increased competition from non-regulated products and marketing

channels that require new thinking and bold transformation.

For me, Monday’s embarrassing event reminded me to think afresh about the vital role

this industry plays…and to drink more water.

1CMS Office of the Actuary; IMS Institute for Healthcare Informatics, "The Use of Medicines in the

United States: Review of 2011," April 2012

2Pharmaceutical Research and Manufacturers Association, http://www.phrma.org/

3The Impending Patent Cliff: Implications for Pharmacists, Pharmacy Time. February 2012.

http://www.pharmacytimes.com/publications/issue/2012/February2012/The-Impending-Patent-

Cliff-Implications-for-Pharmacists

4Assessing Medication Adherence in the Elderly, Drugs Aging. 2005

http://www.dhcs.ca.gov/services/ltc/Documents/Medication%20Noncompliance%20Research%20-

%20Highlighted%20Studies%20B.pdf

5The Need to Develop Responsible Marketing Practice in the Pharmaceutical Sector, Problems

and Perspectives in Management, April 2004.

http://businessperspectives.org/journals_free/ppm/2004/PPM_EN_2004_04_Buckley.pdf;

http://www.ncbi.nlm.nih.gov/pmc/articles/PMC3278148/

6Internal Revenue Service, “Pharmaceutical Industry Overview – Trends,” LMSB-04-0207-010,

April 2013

return to top

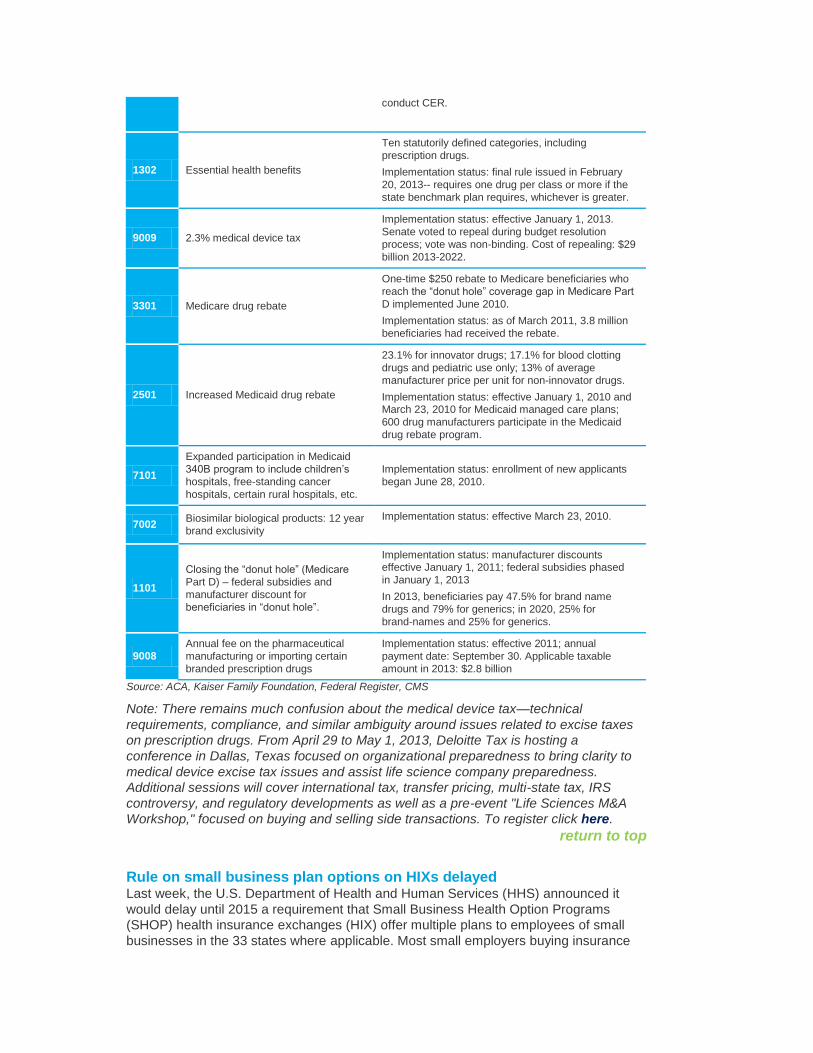

Implementation update

Key ACA provisions impacting the medical device and biopharma

industries In recent weeks, trade groups representing the pharmaceutical and device industries

have sought relief from the Affordable Care Act (ACA) mandated excise taxes including

the 2.3% device excise tax that started January 1, 2013. In the ACA, these “supply

chain” sectors are a central focus:

Section Provision Implementation update

6301 Patient Centered Outcomes Research

Institute (PCORI)

Established to conduct comparative effectiveness

research (CER).

Goal: to help consumers, physicians, and

policymakers make informed decisions surrounding

medical treatment. Implementation status: 25 awards

amounting to $40.7 million have been awarded to

conduct CER.

1302 Essential health benefits

Ten statutorily defined categories, including

prescription drugs.

Implementation status: final rule issued in February

20, 2013-- requires one drug per class or more if the

state benchmark plan requires, whichever is greater.

9009 2.3% medical device tax

Implementation status: effective January 1, 2013.

Senate voted to repeal during budget resolution

process; vote was non-binding. Cost of repealing: $29

billion 2013-2022.

3301 Medicare drug rebate

One-time $250 rebate to Medicare beneficiaries who

reach the “donut hole” coverage gap in Medicare Part

D implemented June 2010.

Implementation status: as of March 2011, 3.8 million

beneficiaries had received the rebate.

2501 Increased Medicaid drug rebate

23.1% for innovator drugs; 17.1% for blood clotting

drugs and pediatric use only; 13% of average

manufacturer price per unit for non-innovator drugs.

Implementation status: effective January 1, 2010 and March 23, 2010 for Medicaid managed care plans;

600 drug manufacturers participate in the Medicaid

drug rebate program.

7101

Expanded participation in Medicaid

340B program to include children’s

hospitals, free-standing cancer

hospitals, certain rural hospitals, etc.

Implementation status: enrollment of new applicants

began June 28, 2010.

7002 Biosimilar biological products: 12 year

brand exclusivity

Implementation status: effective March 23, 2010.

1101

Closing the “donut hole” (Medicare

Part D) – federal subsidies and

manufacturer discount for

beneficiaries in “donut hole”.

Implementation status: manufacturer discounts effective January 1, 2011; federal subsidies phased

in January 1, 2013

In 2013, beneficiaries pay 47.5% for brand name

drugs and 79% for generics; in 2020, 25% for

brand-names and 25% for generics.

9008 Annual fee on the pharmaceutical

manufacturing or importing certain

branded prescription drugs

Implementation status: effective 2011; annual

payment date: September 30. Applicable taxable

amount in 2013: $2.8 billion

Source: ACA, Kaiser Family Foundation, Federal Register, CMS

Note: There remains much confusion about the medical device tax—technical

requirements, compliance, and similar ambiguity around issues related to excise taxes

on prescription drugs. From April 29 to May 1, 2013, Deloitte Tax is hosting a

conference in Dallas, Texas focused on organizational preparedness to bring clarity to

medical device excise tax issues and assist life science company preparedness.

Additional sessions will cover international tax, transfer pricing, multi-state tax, IRS

controversy, and regulatory developments as well as a pre-event "Life Sciences M&A

Workshop," focused on buying and selling side transactions. To register click here.

return to top

Rule on small business plan options on HIXs delayed Last week, the U.S. Department of Health and Human Services (HHS) announced it

would delay until 2015 a requirement that Small Business Health Option Programs

(SHOP) health insurance exchanges (HIX) offer multiple plans to employees of small

businesses in the 33 states where applicable. Most small employers buying insurance

through a HIX will offer a single health plan to their workers next year.

return to top

Report: number of self-insured plans decreased but participant enrollment

increased Per the ACA, the Secretary of Labor must prepare aggregate annual reports – due on

March 23 each year – on self-insured group health plans based on Form 5500 Annual

Return/Report of Employee Benefit Plan (“Form 5500”) filings and financial filings of self-

insured employers. Deloitte Financial Advisory Services LLP assisted the U.S.

Department of Labor (DOL) by preparing the report Self-Insured Health Benefit Plans

2013.

Key findings:

From 2001 to 2010, the percentage of plans with a self-insured component (self-insured or mixed-funded) decreased from 56% to 48%.

In the same time period, the percentage of participants in a plan with a self-insured component increased from 75% to 83%. This paradox appears to be explained by a trend toward less self-insurance among relatively small plans and more self-insurance among relatively large plans.

The prevalence of self-insurance generally increased with plan size. For example, 30% of plans with 100-199 participants had a self-insured component in 2010, compared with 90% of plans with 5,000 or more participants.

Note: for additional information, see Deloitte’s report incorporated in the appendix of the

Secretary of Labor’s Report to Congress here. Also available: other Deloitte reports

on employer health and pension plans published at the U.S. Department of Labor (DOL)

website here or contact. Michael Brien, Director, Deloitte Financial Advisory Services

LLP ([email protected]) or Caroline Lee, Senior Manager, Deloitte Financial

Advisory Services LLP ([email protected]).

My take: in the last decade, 10% of businesses dropped insurance coverage due to

costs. In the next decade, with or without the ACA, 9% more, representing 3% of the

civilian workforce is likely to cease providing coverage (Deloitte Center for Health

Solutions’ 2012 Employer Survey).

Our data is consistent with the DOL report—that small- and mid-size companies,

including many that are self-insured, are more likely to drop coverage. Notably, in our

surveys, these employers are inclined to think that HIXs might be an alternative channel

for employees that lose coverage.

return to top

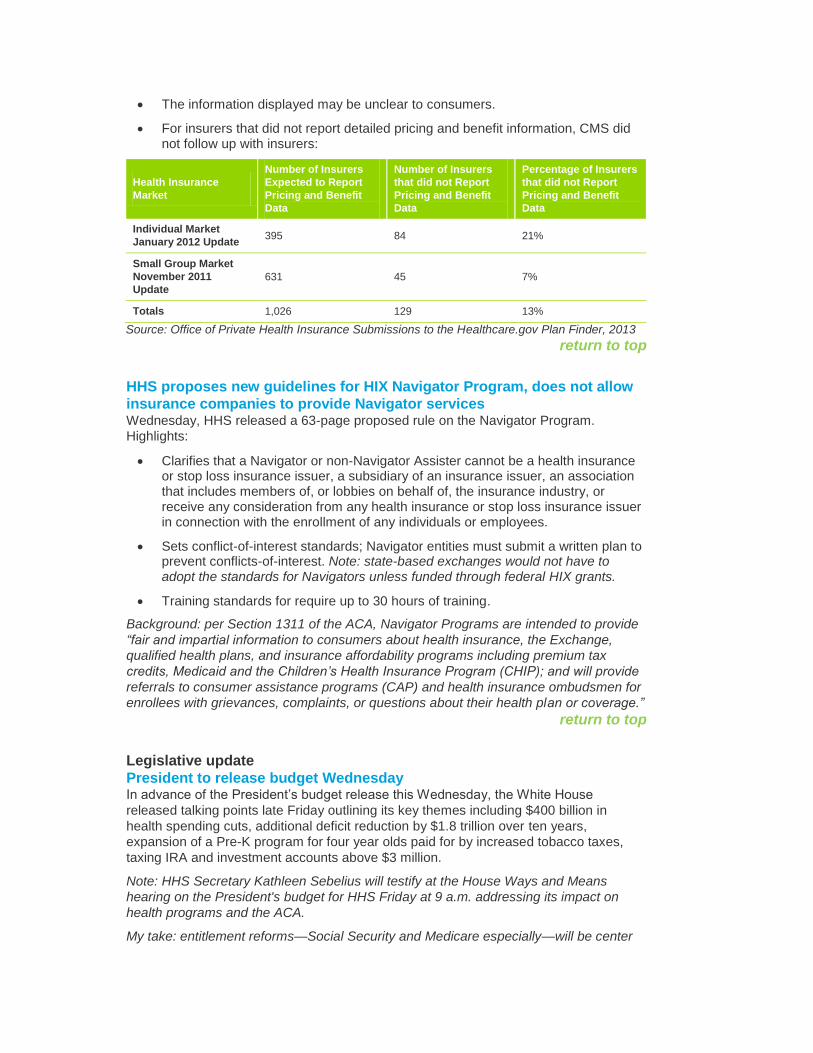

OIG report: information about health insurance plans for consumers on

Healthcare.gov website inadequate Findings from an HHS Office of the Inspector General (OIG) report released last week

showed that data displayed on the Centers for Medicare and Medicaid Services (CMS)

Healthcare.gov Plan Finder – the online tool available to consumers to compare health

insurance plans required by Section 1103 of the ACA – is inadequate.

Key findings:

“Products and plans displayed on Healthcare.gov Plan Finder were not always available or recognized by private insurers’ representatives.”

Of plans and products that were available and recognized, “81% of data matched the information provided by private insurers’ representatives.”

The information displayed may be unclear to consumers.

For insurers that did not report detailed pricing and benefit information, CMS did not follow up with insurers:

Health Insurance

Market

Number of Insurers

Expected to Report

Pricing and Benefit

Data

Number of Insurers

that did not Report

Pricing and Benefit

Data

Percentage of Insurers

that did not Report

Pricing and Benefit

Data

Individual Market

January 2012 Update 395 84 21%

Small Group Market

November 2011

Update

631 45 7%

Totals 1,026 129 13%

Source: Office of Private Health Insurance Submissions to the Healthcare.gov Plan Finder, 2013

return to top

HHS proposes new guidelines for HIX Navigator Program, does not allow

insurance companies to provide Navigator services Wednesday, HHS released a 63-page proposed rule on the Navigator Program.

Highlights:

Clarifies that a Navigator or non-Navigator Assister cannot be a health insurance or stop loss insurance issuer, a subsidiary of an insurance issuer, an association that includes members of, or lobbies on behalf of, the insurance industry, or receive any consideration from any health insurance or stop loss insurance issuer in connection with the enrollment of any individuals or employees.

Sets conflict-of-interest standards; Navigator entities must submit a written plan to prevent conflicts-of-interest. Note: state-based exchanges would not have to adopt the standards for Navigators unless funded through federal HIX grants.

Training standards for require up to 30 hours of training.

Background: per Section 1311 of the ACA, Navigator Programs are intended to provide

“fair and impartial information to consumers about health insurance, the Exchange,

qualified health plans, and insurance affordability programs including premium tax

credits, Medicaid and the Children’s Health Insurance Program (CHIP); and will provide

referrals to consumer assistance programs (CAP) and health insurance ombudsmen for

enrollees with grievances, complaints, or questions about their health plan or coverage.”

return to top

Legislative update

President to release budget Wednesday In advance of the President’s budget release this Wednesday, the White House

released talking points late Friday outlining its key themes including $400 billion in

health spending cuts, additional deficit reduction by $1.8 trillion over ten years,

expansion of a Pre-K program for four year olds paid for by increased tobacco taxes,

taxing IRA and investment accounts above $3 million.

Note: HHS Secretary Kathleen Sebelius will testify at the House Ways and Means

hearing on the President's budget for HHS Friday at 9 a.m. addressing its impact on

health programs and the ACA.

My take: entitlement reforms—Social Security and Medicare especially—will be center

stage in coming budget deliberations. Among the major topics: changing the cost-of-

living calculation used to set Social Security payments to a “chained CPI formula

(savings $390 billion/10 years), raising the age of Medicare eligibility gradually from 65-

67 (savings $120 billion/10 years), changing subsidies and adjusting premiums that

wealthier seniors pay ($58 billion), and combining premiums for Parts A and B (savings

$110 billion/10 years); and fixing the sustainable growth rate (SGR) (one time cost of

$138 billion) as part of the deal. Reductions in funding required in the ACA will no doubt

be discussed, but there’s no way to know the result at this point—more to come.

return to top

SGR fix proposed in House Committee Last Wednesday, Chairmen of the House Energy and Commerce Fred Upton, (R-MI)

and Ways and Means Dave Camp, (R-MI) committees along with their respective health

subcommittee chairs, Joe Pitts (R-PA) and Kevin Brady (R-TX) issued a revised

proposal to replace the SGR model used to determine Medicare payments to

physicians.

Their proposal links physician pay to performance in three categories: quality measure

scores endorsed by consensus-based organizations like the National Quality Forum,

quality improvement from the previous year's score, and “executing clinical improvement

activities.” It also mandates that physicians get timely feedback on their performance

and the development of an appeals process for reconsideration of a quality score.

Quality scores would include four categories: clinical care; safety; care coordination; and

patient and caregiver experience.

Background: instituted as part of the 1997 Balanced Budget Act, the SGR links

physician fees to U.S. gross domestic product, and includes a “clawback” provision

whereby Medicare fees to physicians are cut if spending exceeded a targeted amount in

the previous year. In 2002, the formula resulted in a 4.8% pay cut, but Congress set

aside the model accruing a liability to the Medicare fund. And on 14 occasions since, the

SGR cuts were suspended by Congress accruing a $245 billion liability. Recent interest

in replacing the SGR has gained momentum as a result of the CBO revised estimate on

February 5, 2013 that lowered the ten year cost of its repeal for ten years to $138

billion—40% lower than the $245 billion projection released in August, 2012. Per the

SGR, a 24.4% Medicare pay cut is scheduled to go in effect on January 1, 2014, unless

Congress repeals the SGR or approves another temporary patch.

Note: For more information about the SGR, download the report Understanding the

SGR: Analyzing the “Doc Fix” from the Deloitte Center for Health Solutions.

My take: as part of the upcoming budget process, it appears replacement of the SGR is

increasingly likely. And the proposal to link physician pay to valid and reliable measures

by which physician performance is gauged sensible. There are, however, two elements

of physician performance that should also be included: measures of cost

effectiveness/efficiency whereby physicians encourage use of lower cost treatments

where clinical evidence support their use, and an alternative methodology for scoring for

team-based medical care delivery (in lieu of individual physician performance scoring)

since patient outcomes are the result of care teams and many physicians are already

employed in team-based models.

return to top

Senate Finance Committee schedules hearing on Tavenner Tomorrow, the U.S. Senate Finance Committee will hold a confirmation hearing for CMS

Acting Administrator Marilyn Tavenner. CMS Has not had a confirmed Administrator

since Mark McClellan left the agency in 2006. Prior to Tavenner holding the position, Dr.

Don Berwick served as Interim Administrator of CMS as a result of a Recess

Appointment by President Obama in July 2010. Dr. Berwick stepped down in December

2011.

Background: CMS operates the Medicaid and Medicare programs in addition to CHIP

and the Center for Consumer Information and Insurance Oversight (CCIIO) to

implement insurance related provisions of ACA; with an operating budget of $3,820,112

and employs 4,477 individuals nationwide. Before coming to CMS, Tavenner was

served for four years as the Commonwealth of Virginia’s Secretary of Health and

Human Resources in the administration of former Governor Tim Kaine, and served as

President of Outpatient Services for the Hospital Corporation of American Group prior to

working for the state of Virginia.

return to top

Meaningful use update: bill to exempt solo practices and physicians

nearing retirement; request for safe harbor guidance Prior to Congress breaking for March recess, Representative Diane Black (R-TN)

introduced the Electronic Health Records Improvement Act (H.R. 1331) to exempt solo

practitioners and physicians within three years of retirement from meaningful use

requirements. If passed, the bill would exempt penalties (i.e. 1% reduction in Medicare

reimbursements) for failing to meet meaningful use requirements by 2015. The

Electronic Health Record (EHR) Incentive Program has paid 234,065 participating

organizations to-date, amounting to $12.7 billion since 2011. Program participants:

264,292 eligible Medicare eligible professionals, 120,002 Medicaid eligible professionals

and 4,299 eligible hospitals.

Also, Representative Jim McDermott (D-WA) asked HHS Chief Counsel to the Inspector

General Greg Demske to renew safe harbors that protect EHR equipment and software

donations under the federal Anti-Kickback Statute and Physician Self-Referral laws.

When these exceptions expire, hospital systems can no longer provide a subsidy to a

physician for EHRs if it has a direct or indirect financial relationship with that entity. For

hospitals that are already in subsidy agreements, all donations of items and services

must occur on or before December 31, 2013.

Background: in 1972, the Anti-Kickback Statute makes it illegal for providers to

“knowingly and willfully” accept remuneration or bribes in order to generate revenue

from federal health programs (i.e. Medicare and Medicaid). The Physician Self-Referral

law (i.e. Stark law) is a civil statute enacted in 1989 outlawing physician referrals of a

patient covered in a federal health program (Medicare, Medicaid, CHIP, et al) to an

entity (laboratories, testing centers, etc.) in which the physician has a vested interest,

such as ownership or a compensation arrangement. To help promote the use of health

information technology, safe harbors within the Anti-Kickback and Physician Self-

Referral laws were enacted.

return to top

District court rules in favor of emergency contraception coverage without

age restriction Friday, District Judge Edward R. Korman (Eastern District of NY) ruled that the U.S.

Food and Drug Administration (FDA) must make emergency contraception available

over-the-counter with no age restrictions concluding HHS had “failed to offer a coherent

justification for denying the over-the-counter sale of levonorgestrel-based emergency

contraceptives to the overwhelming majority of women of all ages who may have need

for those drugs and who are capable of understanding their correct use.” The White

House and HHS had advocated for restrictions requiring women under 17 to have a

prescription for contraception. The Department of Justice said it would review the

District Judge’s ruling after the announcement.

return to top

State update

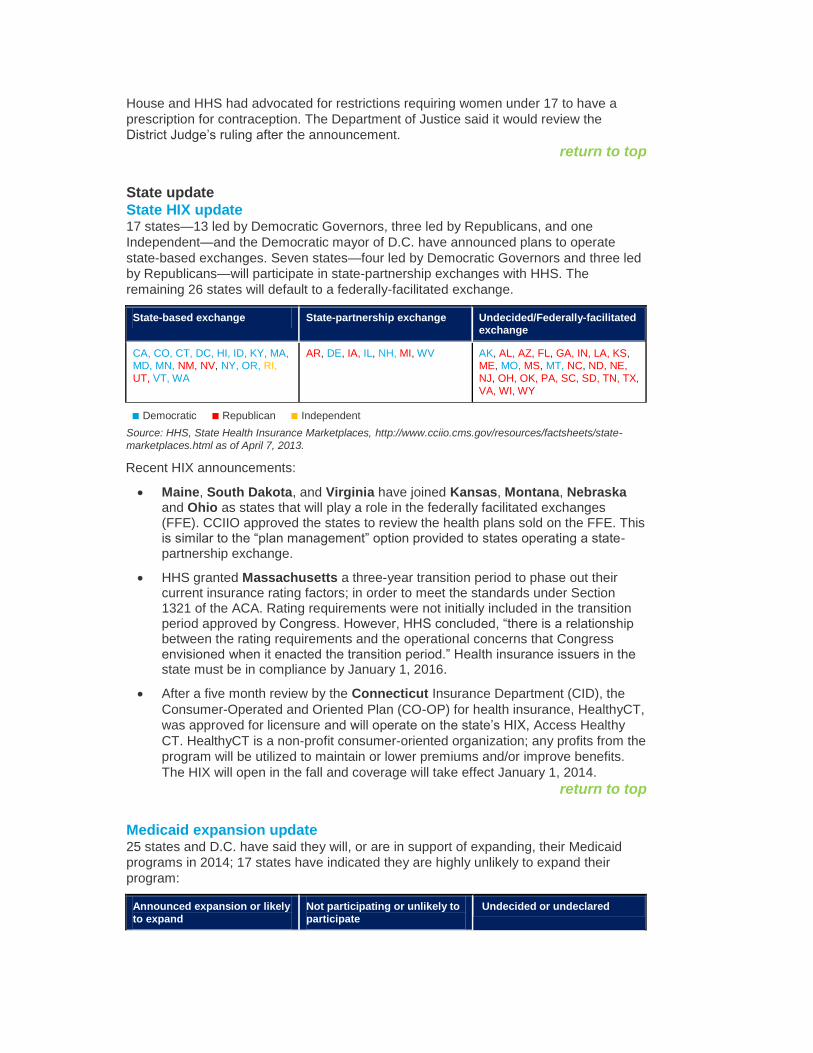

State HIX update 17 states—13 led by Democratic Governors, three led by Republicans, and one

Independent—and the Democratic mayor of D.C. have announced plans to operate

state-based exchanges. Seven states—four led by Democratic Governors and three led

by Republicans—will participate in state-partnership exchanges with HHS. The

remaining 26 states will default to a federally-facilitated exchange.

State-based exchange State-partnership exchange Undecided/Federally-facilitated exchange

CA, CO, CT, DC, HI, ID, KY, MA, MD, MN, NM, NV, NY, OR, RI,

UT, VT, WA

AR, DE, IA, IL, NH, MI, WV AK, AL, AZ, FL, GA, IN, LA, KS, ME, MO, MS, MT, NC, ND, NE,

NJ, OH, OK, PA, SC, SD, TN, TX,

VA, WI, WY

■ Democratic ■ Republican ■ Independent

Source: HHS, State Health Insurance Marketplaces, http://www.cciio.cms.gov/resources/factsheets/state-

marketplaces.html as of April 7, 2013.

Recent HIX announcements:

Maine, South Dakota, and Virginia have joined Kansas, Montana, Nebraska and Ohio as states that will play a role in the federally facilitated exchanges (FFE). CCIIO approved the states to review the health plans sold on the FFE. This is similar to the “plan management” option provided to states operating a state-partnership exchange.

HHS granted Massachusetts a three-year transition period to phase out their current insurance rating factors; in order to meet the standards under Section 1321 of the ACA. Rating requirements were not initially included in the transition period approved by Congress. However, HHS concluded, “there is a relationship between the rating requirements and the operational concerns that Congress envisioned when it enacted the transition period.” Health insurance issuers in the state must be in compliance by January 1, 2016.

After a five month review by the Connecticut Insurance Department (CID), the

Consumer-Operated and Oriented Plan (CO-OP) for health insurance, HealthyCT,

was approved for licensure and will operate on the state’s HIX, Access Healthy

CT. HealthyCT is a non-profit consumer-oriented organization; any profits from the

program will be utilized to maintain or lower premiums and/or improve benefits.

The HIX will open in the fall and coverage will take effect January 1, 2014.

return to top

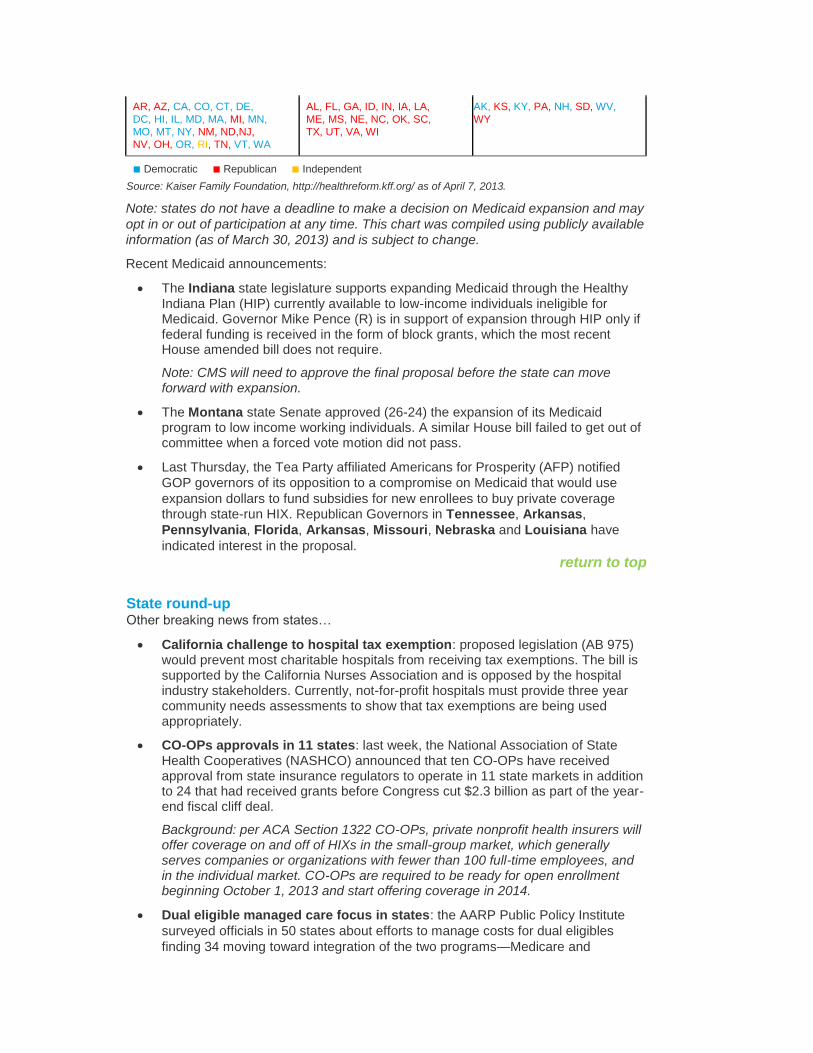

Medicaid expansion update 25 states and D.C. have said they will, or are in support of expanding, their Medicaid

programs in 2014; 17 states have indicated they are highly unlikely to expand their

program:

Announced expansion or likely

to expand

Not participating or unlikely to

participate

Undecided or undeclared

AR, AZ, CA, CO, CT, DE,

DC, HI, IL, MD, MA, MI, MN,

MO, MT, NY, NM, ND,NJ,

NV, OH, OR, RI, TN, VT, WA

AL, FL, GA, ID, IN, IA, LA,

ME, MS, NE, NC, OK, SC,

TX, UT, VA, WI

AK, KS, KY, PA, NH, SD, WV,

WY

■ Democratic ■ Republican ■ Independent

Source: Kaiser Family Foundation, http://healthreform.kff.org/ as of April 7, 2013.

Note: states do not have a deadline to make a decision on Medicaid expansion and may

opt in or out of participation at any time. This chart was compiled using publicly available

information (as of March 30, 2013) and is subject to change.

Recent Medicaid announcements:

The Indiana state legislature supports expanding Medicaid through the Healthy Indiana Plan (HIP) currently available to low-income individuals ineligible for Medicaid. Governor Mike Pence (R) is in support of expansion through HIP only if federal funding is received in the form of block grants, which the most recent House amended bill does not require.

Note: CMS will need to approve the final proposal before the state can move forward with expansion.

The Montana state Senate approved (26-24) the expansion of its Medicaid program to low income working individuals. A similar House bill failed to get out of committee when a forced vote motion did not pass.

Last Thursday, the Tea Party affiliated Americans for Prosperity (AFP) notified

GOP governors of its opposition to a compromise on Medicaid that would use

expansion dollars to fund subsidies for new enrollees to buy private coverage through state-run HIX. Republican Governors in Tennessee, Arkansas,

Pennsylvania, Florida, Arkansas, Missouri, Nebraska and Louisiana have

indicated interest in the proposal.

return to top

State round-up Other breaking news from states…

California challenge to hospital tax exemption: proposed legislation (AB 975) would prevent most charitable hospitals from receiving tax exemptions. The bill is supported by the California Nurses Association and is opposed by the hospital industry stakeholders. Currently, not-for-profit hospitals must provide three year community needs assessments to show that tax exemptions are being used appropriately.

CO-OPs approvals in 11 states: last week, the National Association of State Health Cooperatives (NASHCO) announced that ten CO-OPs have received approval from state insurance regulators to operate in 11 state markets in addition to 24 that had received grants before Congress cut $2.3 billion as part of the year-end fiscal cliff deal.

Background: per ACA Section 1322 CO-OPs, private nonprofit health insurers will offer coverage on and off of HIXs in the small-group market, which generally serves companies or organizations with fewer than 100 full-time employees, and in the individual market. CO-OPs are required to be ready for open enrollment beginning October 1, 2013 and start offering coverage in 2014.

Dual eligible managed care focus in states: the AARP Public Policy Institute

surveyed officials in 50 states about efforts to manage costs for dual eligibles

finding 34 moving toward integration of the two programs—Medicare and

Medicaid and implementation of managed care models as a vehicle for cost

containment and medical management. The “duals” are older, lower income

adults eligible for both Medicare and Medicaid—10.4 million eligible for both

programs and 7.4 million for full eligibility. (Source: AARP Public Policy Institute,

“Two-Thirds of States Integrating Medicare and Medicaid Services for Dual

Eligibles”, April 2013)

return to top

Industry news

Cuts to Medicare advantage plans set aside; Part D rates announced Monday, CMS announced Medicare Advantage (MA) plans will receive a +3.3%

payment adjustment in fiscal year (FY) 2014 based on the assumption that Congress

will override the SGR, resulting in a zero percent change for the 2014 physician fee

schedule. Note: in 2012, 27% of Medicare beneficiaries were enrolled in MA plans.

CMS also modified the Part D (prescription drug benefit) parameters, finalizing the

following for FY 2014:

2012 2013

Standard Benefit

Deductible $320 $325

Initial Coverage Limit $2,930 $2,970

Out-of-Pocket Threshold $4,700 $4,750

Total Covered Part D Spending at Out-of-Pocket Threshold for Non-Applicable Beneficiaries

$6,657.50 $6,733.75

Estimated Total Covered Part D Spending at Out-of-Pocket Threshold for

Applicable Beneficiaries

$6,730.39 $6,954.52

Minimum Cost-Sharing in Catastrophic Coverage Portion of the Benefit

Generic/Preferred Multi-Source Drug $2.60 $2.62

Other $6.50 $6.60

Full Subsidy-Full Benefit Dual Eligible (FBDE) Individuals

Deductible $0.00 $0.00

Copayments for Institutionalized Beneficiaries $0.00 $0.00

Copayments for Beneficiaries Receiving Home and Community-Based Services $0.00 $0.00

Maximum Copayments for Non-Institutionalized Beneficiaries

Up to or at 100% FPL

Up to Out-of-Pocket Threshold $1.10 $1.15

Generic/Preferred Multi-Source Drug $3.30 $3.50

Other $0.00 $0.00

Over 100% FPL

Up to Out-of-Pocket Threshold

Generic/Preferred Multi-Source Drug $2.60 $2.65

Other $6.50 $6.60

Above Out-of-Pocket Threshold $0.00 $0.00

Full Subsidy-Non-FBDE Individuals

Eligible for QMB/SLMB/QI, SS1 or applied and income at or below 135% FPL and resources ≤

$6,940 (individuals) or ≤ $10,410 (couples)

Deductible $0.00 $0.00

Maximum Copayments up to Out-of-Pocket Threshold

Generic/Preferred Multi-Source Drug $2.60 $2.65

Other $6.50 $6.60

Maximum copayments above Out-of-Pocket Threshold $0.00 $0.00

Partial Subsidy

Applied and income below 150% FPL and resources below $11,570 (individuals) or $23,120 (couple)

Deductible $65.00 $66.00

Coinsurance up to Out-of-Pocket Threshold 15% 15%

Maximum Copayments above Out-of-Pocket Threshold

Generic/Preferred Multi-Source Drug $2.60 $2.65

Other $6.50 $6.60

Retiree Drug Subsidy Amounts

Cost Threshold $320 $325

Cost Limit $6,500 $6,600

Sources: http://online.wsj.com/article/Medicare+advantage

http://www.medpac.gov/documents/Mar13_entirereport.pdf;

http://www.cms.gov/Medicare/HealthPlans/MedicareAdvtgSpecRateStats.pdf

return to top

Medical testing labs see growth but margin erosion; Medicare cost-

sharing accelerates sector pressure The U.S. medical testing industry is growing: it’s a $48 billion sector and growing rapidly.

But it faces a challenge similar to the acute and long term care sectors: increased

demand, but declining margins resulting from lower Medicare and Medicaid

reimbursement. Compounding the issue, competition from newer channels—point of

care testing that allow in-office testing, mail order genetic tests and routine lab work, and

new cost sharing requirements for Medicare enrollees likely to increase bad debt and

cause operational challenges.

My take: What’s ahead for labs? The possibilities include: 1) innovation in the scope of

services offered; 2) alternative channels through which they’re commercialized and 3)

continued consolidation as the industry sees thinner margins. As a key element in the

supply chain sector, the sector will be exposed to market forces like transparency,

consumerism, value-based design, etc. that require changes in the operating model,

while also facing competition from new entrants with deep pockets from their non-

traditional sponsors. Having been a frequent user of labs the past year, it’s also

incumbent that operators seek a differentiated strategy by delivering a unique value

proposition to customers—consumers, employers, hospitals and clinicians—lest they

become commodities.

return to top

Small business survey: ACA the major concern The U.S. Chamber of Commerce survey of 1,332 c-suite executives in companies with

fewer than 500 employees conducted last month found:

“Requirements of the health care law are now the biggest concern for small businesses, having bumped economic uncertainty from the top spot which it has

held for the last two years.”

77% say the health care law will make coverage for their employees more expensive, and 71% say the law makes it harder for them to hire more employees.

32% of small businesses plan to reduce hiring as a result of the employer

mandate and 31% will cut back hours to reduce the number of full time

employees.

(Source: Q1 U.S. Chamber of Commerce Small Business Outlook Survey conducted

online March 14 – 26 by Harris Interactive. 1,332 Small Business Executives–defined as

executive level position in a company with fewer than 500 employees and annual

revenue less than $25 million–were surveyed)

return to top

Generic drug makers challenge abuse deterrent requirements as anti-

competitive According to the Generic Pharmaceutical Association (GPhA), requiring generic drug

makers to adopt abuse deterrent properties of their branded counterparts "would

effectively shield branded opioids from generic competition." GPhA cited lack of

scientific evidence that abuse deterrent formulations prevent drug abuse.

(Source: InsideHealthPolicy, “Generic Drugmakers: Abuse Deterrent Requirements Are

Anti-Competitive)

return to top

IOM analysis: Medicare spending variation influenced largely by long-term

care utilization Geographic variation in Medicare spending is strongly influenced by the utilization of

post-acute care, especially home health and skilled nursing per the Institute of Medicine

(IOM) report released last week. The March 28, 2013 report concluded that as much as

40% of Medicare spending variation is due to over-use/misuse of home care, skilled

nursing and related long-term care services. This spending variation is higher than acute

and physician services.

Note: for more information on geographic variation see April 1, 2013 Health Reform

Monday Memo.

(Source: IOM, “Interim Report of the Committee on Geographic Variation in Health Care

Spending and Promotion of High-Value Health Care: Preliminary Committee

Observations,” March 2013)

return to top

India Supreme Court strikes down cancer drug patent Last Monday, India's Supreme Court denied Novartis patent protection for Glivec, a

major cancer drug. Public health advocates were in support of the court’s decision citing

concerns of the ability for developing countries to produce affordable generic drugs. The

pharmaceutical industry opposed the ruling, arguing that it discourages future

investment in innovative drug developments and recognition of intellectual property

rights. Indian pharmaceutical company Cipia manufactures a generic version of the

cancer drug for 10% of branded drugs original price according to reports.

Industry reaction: “PhRMA is very disappointed with the Indian Supreme Court’s

decision to deny a patent on Glivec. This decision marks yet another example of the

deteriorating innovation environment in India. Innovation is critical in meeting unmet

needs of patients and is particularly relevant in the context of changing healthcare

systems. In order to solve the real health challenges of India’s patients, it is critically

important that India promote a policy environment that supports continued research and

development of new medicines for the health of patients in India and worldwide.

Protecting intellectual property is fundamental to the discovery of new medicines. The

research-based pharmaceutical industry is committed to working closely with the Indian

Government and other stakeholders to find appropriate solutions to this challenge.”—

Pharmaceutical Research and Manufacturers of America (PhRMA), “PhRMA Statement

on India Supreme Court Decision on Glivec,” April 1, 2013

return to top

Study: dementia costs $215 billion RAND researchers concluded that 15% of the population older than 71, or 3.8 million

people, have dementia, and estimate it will increase to 9.1 million by 2040. Direct costs

were $109 billion for facility and professional services in 2010 vs. $102 billion for heart

disease and $77 billion for cancer per the report. Indirect costs for caregiving services

provided by family members or friends added $50-106 billion dependent on the method

used to calculate the value of these services. Each case of dementia costs $41,000 to

$56,000 per year.

(Source: M.D. Hurd, P. Martorell, A. Delavande, K.J. Mullen, and K.M. Langa “Monetary

Costs of Dementia in the United States” New England Journal of Medicine April 4, 2013

Vol. 368 No. 14)

return to top

Research snapshots New industry and peer-reviewed studies of note to health system transformers…

Mortality rates for Medicare beneficiaries in critical access hospitals

higher than in non CAH settings Citation: Karen Joynt, “Mortality Rates for Medicare Beneficiaries Admitted to Critical Access and Non–Critical Access Hospitals, 2002-2010”, Journal of American Medical Association, April 2013

Objective: “to evaluate trends in mortality for patients receiving care at critical access hospitals (CAHs) providing inpatient care to individuals living in rural communities, and compare these trends with those for patients receiving care at non-CAHs.”

Methods: “researcher conducted a retrospective observational study using Medicare fee-for-service (FFS) data for 1,902,586 patients with acute myocardial infarctions, 4,488,269 with congestive heart failure, and 3,891,074 patients with pneumonia admitted to acute care hospitals with between 2002 and 2010.”

Results: “accounting for differences in patient, hospital, and community characteristics, CAHs had mortality rates comparable with those of non-CAHs in 2002; 12.8% vs. 13.0%. Between 2002 and 2010, mortality rates increased 0.1% per year in CAHs but decreased 0.2% per year in non-CAHs, for an annual difference in change of 0.3%. Thus, by 2010, CAHs had higher mortality rates compared with non-CAHs (13.3% vs. 11.4%). The patterns were similar when each individual condition was examined separately. Comparing CAHs with other small, rural hospitals, similar patterns were found.”

Key Findings: “among Medicare beneficiaries with acute myocardial infarction, congestive heart failure, or pneumonia, 30-day mortality rates increased for those admitted to CAHs, compared with those admitted to other acute care hospitals.”

My take: given changes in the technologies necessary to promote the safest and most

effective care, clinical innovations that require expensive infrastructure, massive investments in team-based care coordination, and declining reimbursements from Medicare, one might ask what the role of CAHs are in the acute system of care. No doubt, CAH is an important sector, especially in rural communities where jobs are important, but transformational change in the delivery system seems to suggest a re-thinking of the appropriate role of CAH.

return to top

Coverage expansion for children and impact on pediatrician workload Citation: He, Fang, White, Chapin, “The Effect of the Children’s Health Insurance Program on Pediatricians’ Work Hours” Medicare & Medicaid Research Review 2013.

Objective: “study examines changes in physicians’ work hours in response to a coverage expansion.”

Methodology/data: “We use as a natural experiment the Children’s Health Insurance Program (CHIP)… The magnitude of the CHIP expansion varied across states and over time, allowing its effects to be identified using a state-year fixed effects model. We focus on pediatricians, and we measure their self-reported work hours using multiple waves (pre- and post-CHIP) of the physician survey component of the Community Tracking Study. To address endogeneity concerns, we instrument for CHIP enrollment using key program features (income eligibility cutoffs and waiting times).”

Key Finding: “We find a large negative relationship between the magnitude of a state's CHIP expansion and trends in pediatricians' work hours. This relationship could be due to key supply-side features of CHIP, including relatively low provider reimbursements and heavy use of managed care tools.”

My take: physicians adapt, especially pediatricians who are among the most skillful of the medical professions. They’ve been on the front line of adaptation because their clientele—parents, kids, public health programs, etc. necessitated it. They were first to propose the now-popular medical home model, first to encourage the use of electronic medical records (along with family medicine) and first to leverage nurses and health coaches in their practices—necessary to taking care of patients and parents after hours and in-between scheduled visits. The findings underscore the adaptive behavior of the profession. No surprise.

return to top

Quotable “When you feel pressure to follow that path, use our research to make the case that by

and large, companies don’t become truly great by reducing costs or assets; they earn

their way to greatness. Exceptional companies often, even typically, accept higher costs

as the price of excellence. In fact, many of them have developed quite a taste for

spending and investment. These organizations put significant resources, over long

periods of time, into creating nonprice value and generating higher revenue. Point out

that when successful companies are led astray by the seeming certainties of short-run

cost cutting or disinvestment, they are more likely to destroy what they most want to

enhance.” —Michael Raynor and Mumtaz Ahmed “Three Simple Rules for Making a

Company Great” Harvard Business Review, April 2013.

“Fees in the private health care sector have been jealously guarded trade secrets

among insurers and providers of health care. True, some health insurers now provide

their insured members with “cost estimates,” by provider and by major procedure, of

what the procedures rendered by a particular providers might cost patients out of

pocket, but not full prices. I have found the site for that purpose on my insurance policy

very difficult and cumbersome to navigate... It is truly remarkable that few state

governments have made any effort to provide their residents with greater price

transparency in health care, as well they could and should. A report on March 18,

“Report Card on State Price Transparency Laws” by the Catalyst for Payment Reform

and the Health Care Incentives Improvement Institute gives 29 states the failing grade of

F on this score, including New York and New Jersey. Another 6 earned a D, barely

passing. Only Massachusetts and New Hampshire earned an A. With so much carefully

guarded and government-shielded opacity on health care prices, it should be no

surprise that prices for health care vary as much as they do in the United States, even

within small regions and for the same health insurer. It will not change until citizens

make it an issue in political campaigns.” —Uwe E. Reinhardt, “U.S. Health Care Prices Are the Elephant in the Room” New York Times Blog , March 29, 2013

return to top

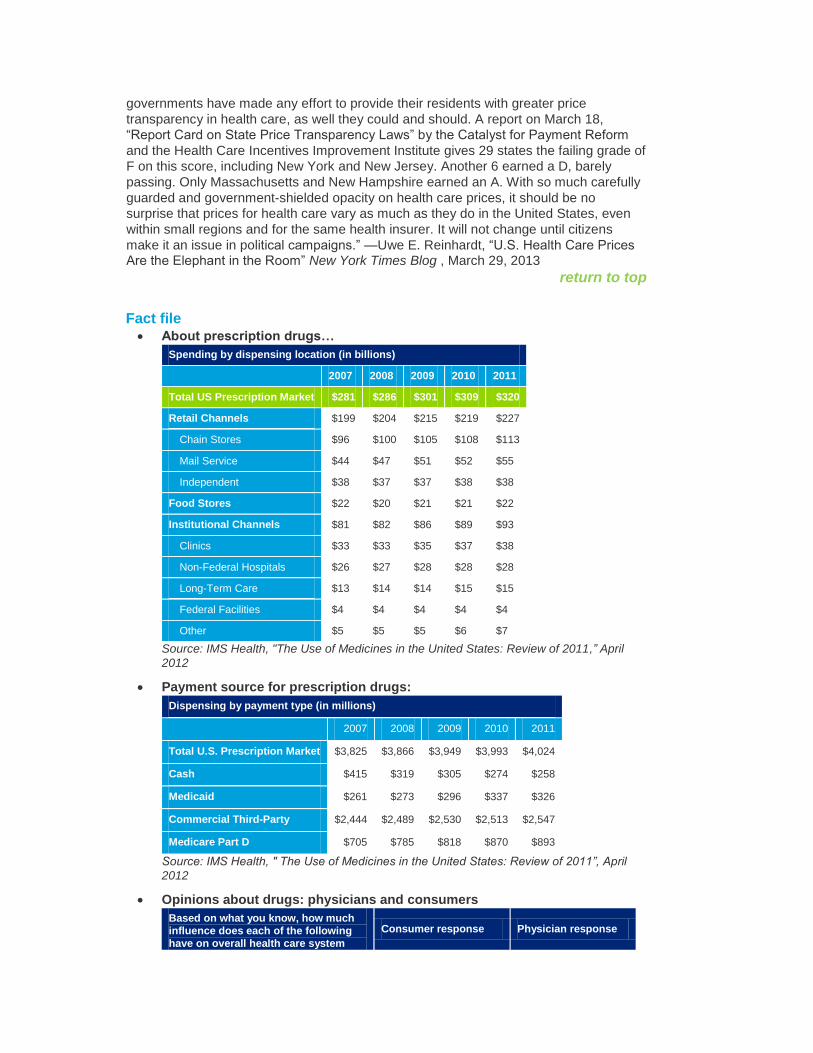

Fact file About prescription drugs…

Spending by dispensing location (in billions)

2007 2008 2009 2010 2011

Total US Prescription Market $281 $286 $301 $309 $320

Retail Channels $199 $204 $215 $219 $227

Chain Stores $96 $100 $105 $108 $113

Mail Service $44 $47 $51 $52 $55

Independent $38 $37 $37 $38 $38

Food Stores $22 $20 $21 $21 $22

Institutional Channels $81 $82 $86 $89 $93

Clinics $33 $33 $35 $37 $38

Non-Federal Hospitals $26 $27 $28 $28 $28

Long-Term Care $13 $14 $14 $15 $15

Federal Facilities $4 $4 $4 $4 $4

Other $5 $5 $5 $6 $7

Source: IMS Health, "The Use of Medicines in the United States: Review of 2011,” April

2012

Payment source for prescription drugs:

Dispensing by payment type (in millions)

2007 2008 2009 2010 2011

Total U.S. Prescription Market $3,825 $3,866 $3,949 $3,993 $4,024

Cash $415 $319 $305 $274 $258

Medicaid $261 $273 $296 $337 $326

Commercial Third-Party $2,444 $2,489 $2,530 $2,513 $2,547

Medicare Part D $705 $785 $818 $870 $893

Source: IMS Health, " The Use of Medicines in the United States: Review of 2011”, April

2012

Opinions about drugs: physicians and consumers

Based on what you know, how much

influence does each of the following

have on overall health care system

Consumer response Physician response

costs?

Prescription drugs

Major Influence 48% 57%

Minor Influence 30% 37%

No Influence 9% 4%

Not Sure 13% 1%

New Technologies and equipment (e.g. medical technologies and electronic health record systems)

Major Influence 36% 49%

Minor Influence 36% 43%

No Influence 11% 7%

Not Sure 17% 1%

Source: Deloitte Center for Health Solutions 2013 Survey of Physicians; 2012 Survey of

Consumers

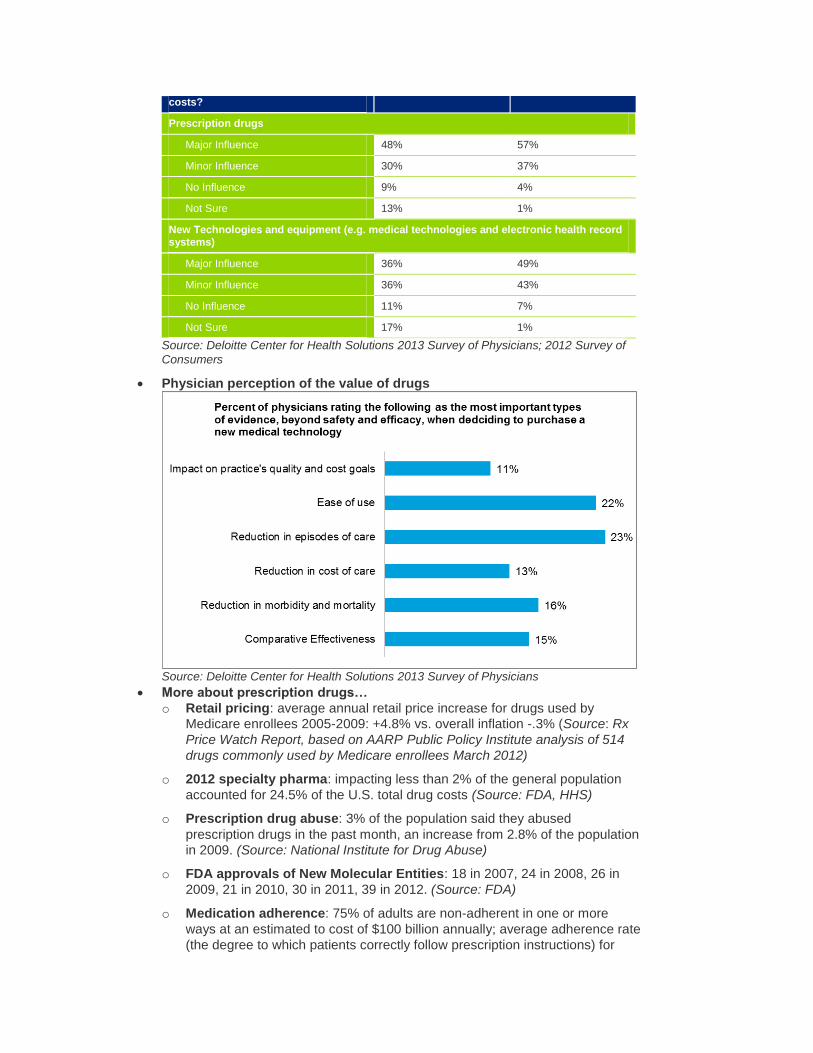

Physician perception of the value of drugs

Source: Deloitte Center for Health Solutions 2013 Survey of Physicians

More about prescription drugs…

o Retail pricing: average annual retail price increase for drugs used by

Medicare enrollees 2005-2009: +4.8% vs. overall inflation -.3% (Source: Rx

Price Watch Report, based on AARP Public Policy Institute analysis of 514

drugs commonly used by Medicare enrollees March 2012)

o 2012 specialty pharma: impacting less than 2% of the general population

accounted for 24.5% of the U.S. total drug costs (Source: FDA, HHS)

o Prescription drug abuse: 3% of the population said they abused

prescription drugs in the past month, an increase from 2.8% of the population

in 2009. (Source: National Institute for Drug Abuse)

o FDA approvals of New Molecular Entities: 18 in 2007, 24 in 2008, 26 in

2009, 21 in 2010, 30 in 2011, 39 in 2012. (Source: FDA)

o Medication adherence: 75% of adults are non-adherent in one or more

ways at an estimated to cost of $100 billion annually; average adherence rate

(the degree to which patients correctly follow prescription instructions) for

medicines taken only once daily is nearly 80% compared to about 50% for

treatments taken 4 times a day. 50% of chronically ill patients) fail to adhere

to, or comply with physician prescribed treatment regimens. (PhRMA) Non

adherence is responsible for 23% of nursing home admissions (Cost $31.3

billion / 380,000 patients) and.10% of hospital admissions (Cost $15.2 billion

/ 3.5 million patients). (Source: Schering Report IX the Forgetful Patient: The

High Cost of Improper Patient Compliance and the National Council for

Patient Information and Education)

Employment report: overall job growth for March was 88,000 vs. 236,000 in

February; health care job growth was 23,000 vs. 24,300 in February (ambulatory

services 15,000; 8,000 hospitals); unemployment remained at 7.6% (Source: US

Bureau of Labor Statistics Monthly Jobs Report released April 5, 2013)

Medical resident match day: 99.4% of the 29,171 medical residency slots were

filled this year vs. 98.5% in 2012. Note: the NRMP's Main Residency Match is a

two-part process: the NRMP aligns the rank order lists of applicants and

residency program directors using an algorithm. “This year, only 1,041 positions

were unfilled, and 939 were placed in the Match Week Supplemental Offer and

Acceptance Program for unfilled residency positions.” (Source: National

Residency Matching Program April 5, 2013)

Consumer spending on vitamins: $23 billion spent on vitamins, minerals and

supplements in the past year; growing at an annual rate of 5-7%. (Sources:

Consumer Health Products Association; Wall Street Journal, “With Top Lines

Drooping, Firms Reach for Vitamins,” March 31, 2013)

Medicaid enrollee health status: 36% say they smoke (17% points above adult

average); 26% say they had trouble paying for health care services within the

past year; 34% are obese and 22% are being treated for depression and 24% for

high blood pressure (Source: Gallup poll of 28,000 interviews between Jan. 3 and

March 1, come with a 4 percent margin of error and Gallup Wellbeing,

“Preventable Chronic Conditions Plague Medicaid Population,” April 4, 2013)

Public health funding: 29 states decreased their public health budgets from

FY2011 to FY2012; per capita state spending on public health decreased from

$33.71 to $27.40 between 2008- 2012 fiscal years—a $1.9 billion cut when

inflation adjusted. (Source: Trust for America’s Health, “Investing in America’s

Health: A State-by-State Look at Public Health Funding and Key Health Facts,”

April 2013)

Medical technologies and physicians: seven in 10 physicians believe that

physician-led, peer review of new medical technologies (covering both efficacy

and value) followed by use of evidence-based guidelines (six in 10 physicians)

are the leading best practices in the selection and purchase of medical

technologies; six in 10 physicians rank doctors as being the personnel with the

greatest influence on medical technology purchasing decisions currently and in the next three to five years. (Source: DCHS 2013 Survey of Physicians)

return to top

Subscribe to the Health Care Reform Memo

Health Care Reform Memo — The weekly Health Care Reform Memo is available for

subscription. Please visit www.deloitte.com/us/healthmemos/subscribe. First,

confirm your sector(s) of interest. Then, select the Health Care Reform Memo as one of

your Email Newsletters (under Health Sciences). return to top

Deloitte Center for Health Solutions research To learn more about recent Deloitte thought leadership, please visit Deloitte University

Press at www.DUPress.com.

Coming soon: Physician Survey 2013: HIT Report

Hospital consolidation: What happens, what’s ahead?

Currently available: Breaking Constraints: Can incentives change consumer health choices?—March 2013. Available online at http://dupress.com/articles/breaking-constraints/?coll=3024

2013 Survey of U.S. Physicians: Physician perspectives about health care reform

and the future of the medical profession—March 2013. Available online at

www.deloitte.com/us/2013physiciansurvey

Health System Chief Information Officers: Juggling responsibilities, managing expectations, building the future—February 2013. Available online at www.deloitte.com/us/2013CIOstudy

Unlocking value in health plan M&A: Sometimes the deals don’t deliver—January 2013. Available online at www.deloitte.com/us/2013planconsolidation

Deloitte 2012 Survey of U.S. Health Care Consumers—December 2012. Access a

library of resources including an INFOBrief series, an infographic, and a Five-Year Look

Back report. Available online at www.deloitte.com/us/consumerstudies return to top

Read the blog

To stay up-to-date, check out the Center for Health Solutions’ blog: A view from the Center—where policy, innovation, and industry meet

http://blogs.deloitte.com/centerforhealthsolutions/

return to top

Upcoming life sciences and health care Dbrief webcasts and events Anticipating tomorrow's complex issues and new strategies is a challenge. Stay fresh with Dbriefs – live webcasts that give you valuable insights on important developments

affecting your business.

Join us on April 9: Managing Security and Privacy for Health Care. To register click here.

2013 Deloitte Life Sciences Tax Conference: April 29 to May 1, 2013

Deloitte Tax is hosting a conference in Dallas, Texas focused on organizational

preparedness to bring clarity to medical device excise tax issues and assist life science

company preparedness. Additional sessions will cover international tax, transfer pricing,

multi-state tax, IRS controversy, and regulatory developments as well as a pre-event

"Life Sciences M&A Workshop," focused on buying and selling side transactions. To register click here.

return to top

Deloitte contacts

Paul H. Keckley, Ph.D., Executive Director, Deloitte Center for Health Solutions

Jessica Blume, U.S. Public Sector National Industry Leader, Deloitte LLP

Bill Copeland, U.S. Life Sciences and Health Care National Industry Leader, Deloitte

LLP ([email protected])

Jason Girzadas, National Managing Director, Life Sciences & Health Care, Deloitte

Consulting LLP ([email protected])

Harry Greenspun, M.D., Senior Advisor, Health Care Transformation and Technology,

Deloitte Center for Health Solutions ([email protected])

Mitch Morris, M.D., National Leader, Health Information Technology, Deloitte

Consulting LLP ([email protected])

George Serafin, Managing Director, Health Sciences Governance Regulatory & Risk

Strategies, Deloitte & Touche LLP ([email protected])

Rick Wald, Director, Human Capital, Deloitte Consulting LLP ([email protected])

To receive email alerts when new research is published by the Deloitte Center for Health

Solutions, please register at www.deloitte.com/centerforhealthsolutions/subscribe.

To access Center research online, please visit

www.deloitte.com/centerforhealthsolutions.

To arrange a briefing for your team, contact Jennifer Bohn ([email protected]).

return to top

Deloitte.com | Security | Legal | Privacy

30 Rockefeller Plaza New York, NY 10112-0015 United States

About Deloitte Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee, and its network of member firms, each of which is a legally separate and independent entity. Please see www.deloitte.com/about for a detailed description of the legal structure of Deloitte Touche Tohmatsu Limited and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Disclaimer This publication contains general information only and Deloitte is not, by means of this publication, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor.

Deloitte shall not be responsible for any loss sustained by any person who relies on this publication.

Copyright © 2013 Deloitte Development LLC. All rights reserved. Member of Deloitte Touche Tohmatsu Limited

To unsubscribe, reply to this message and add “Unsubscribe” in the subject line.