Embed Size (px)

Citation preview

Annual World Refining Outlook 2017

Leading consultancy for the oil & gas marketswww.fgenergy.com

A Return to the Golden Age?

Leading consultancy for the oil & gas markets www.fgenergy.com

Despite the recent OPEC and non-OPEC production agreements, we continue to forecast a low price oil environment for the foreseeable future. Consequently, we expect products demand to be robust, especially for gasoline. At the same time CAPEX for investment in any part of the oil business will be limited, with refining investment continuing to be under pressure. While there are many projects announced in the Press, only a small percentage actually get built! Consequently, the pressure on existing capacity and that which is actually built is increasing and is being exacerbated by a refinery configuration more focused on distillate production whereas the largest demand growth is for gasoline. There is plenty of potential for the strong cracks and margins seen over the last 2 years or more to continue. In this study we look at this potential, what the main drivers are and how long it could last for.

Refiners are continuing to invest in sophisticated upgrading capacity, essentially converting fuel oil into gasoline and distillate. Recent and imminent new capacity has focused on distillate production in particular. But has the low crude price environment resulted in a shift towards gasoline and if so, how long will this last for?

Also, 2020 will see a seismic change to the demand barrel with the introduction of new specifications for bunker fuel oil (to 0.5%S max without flue gas mitigation) for the world’s marine fleet. We look at how refiners and the fleet will react to this, the implications for distillate and fuel oil demand and balances, product cracks and refinery margins. Will there be enough refining capacity? Will this be the solution for the distillate oversupply? What will happen to product prices, especially for fuel oil?

Our conclusions will continue to challenge the conventional wisdom of gasoline length and distillate shortage (at least to 2020!). It will also raise new concerns about how the refining/shipping industries will react to the 2020 IMO regulation changes; all set within an internally consistent framework of refinery capacity, estimated refinery margins and products prices. We review how surplus refining capacity may change, challenging the traditional call for further reductions in capacity. Indeed, we may well be experiencing the beginning of a new “Golden Age of Refining” which will see new capacity being required and added throughout the 2020s.

FGE’s Annual World Refining Outlook 2017

A detailed assessment of the mid/long-term operating environment for global refining and the implications for products trade. We forecast product demand and review refinery investment to identify the likely pressures on the refining sector and what this could mean for refining margins in the next 5 -10 years.

Overview

• How will products demand evolve in a long-lasting low crude oil price environment?

• How might refinery investments develop over the next 5-10 years?

• How will the 2020 bunker fuel spec changes impact products demand and refinery margins?

• How does refinery capacity match-up to products demand? Has the need for refinery capacity closure passed? Indeed, do we need to build more capacity?

• How will product trade flows develop?• What will happen to refinery margins over the next 5-10

years?

Key Areas Addressed in This Study

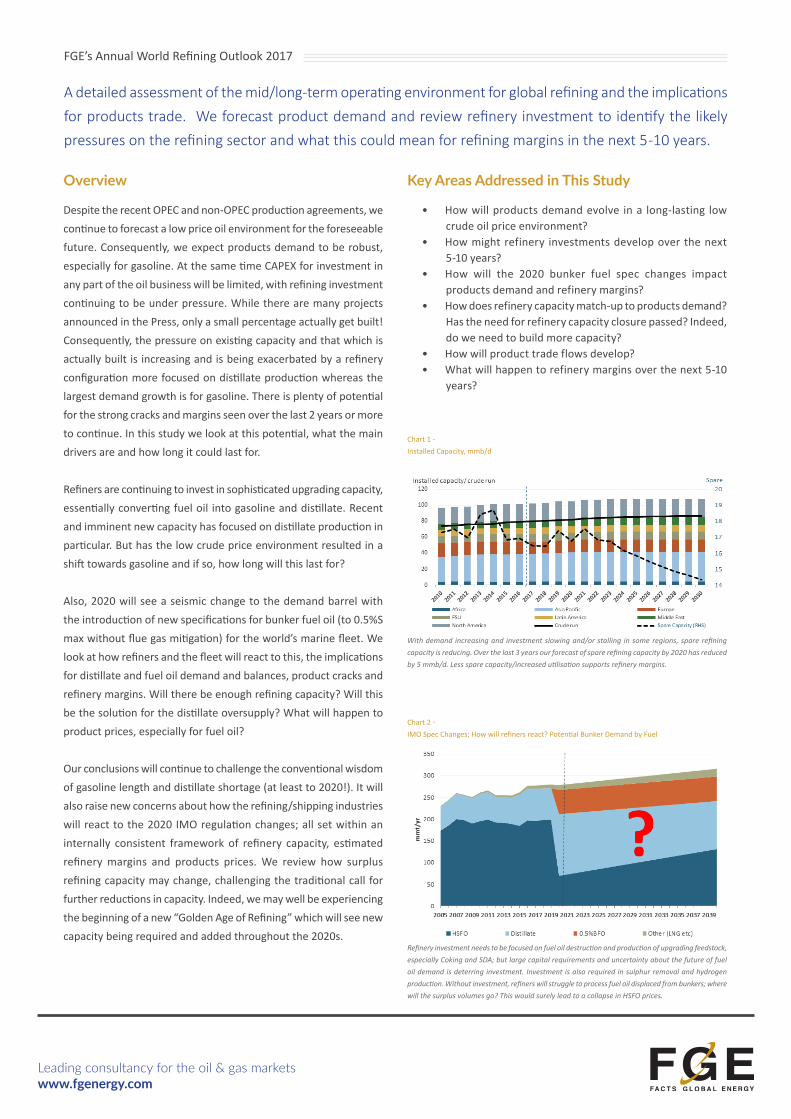

With demand increasing and investment slowing and/or stalling in some regions, spare refining capacity is reducing. Over the last 3 years our forecast of spare refining capacity by 2020 has reduced by 5 mmb/d. Less spare capacity/increased utilisation supports refinery margins.

Chart 1 - Installed Capacity, mmb/d

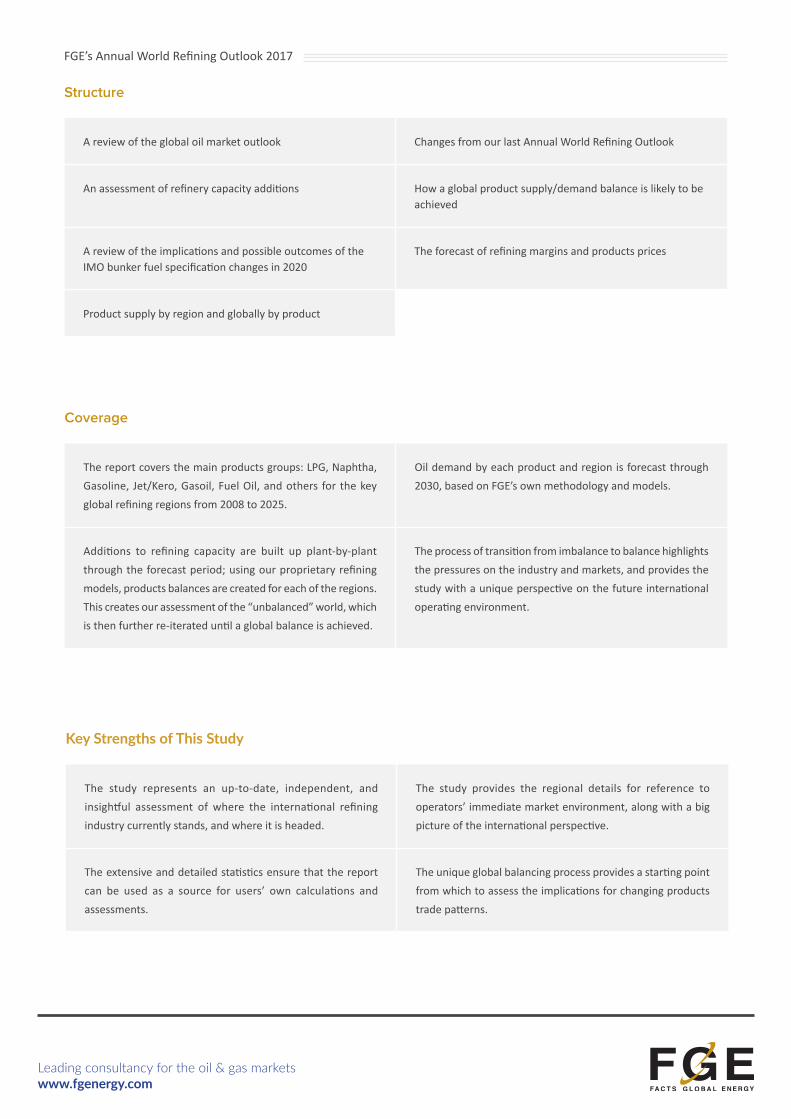

Refinery investment needs to be focused on fuel oil destruction and production of upgrading feedstock, especially Coking and SDA; but large capital requirements and uncertainty about the future of fuel oil demand is deterring investment. Investment is also required in sulphur removal and hydrogen production. Without investment, refiners will struggle to process fuel oil displaced from bunkers; where will the surplus volumes go? This would surely lead to a collapse in HSFO prices.

Chart 2 - IMO Spec Changes; How will refiners react? Potential Bunker Demand by Fuel

Leading consultancy for the oil & gas marketswww.fgenergy.com

FGE’s Annual World Refining Outlook 2017

Key Strengths of This Study

The study represents an up-to-date, independent, and insightful assessment of where the international refining industry currently stands, and where it is headed.

The study provides the regional details for reference to operators’ immediate market environment, along with a big picture of the international perspective.

The extensive and detailed statistics ensure that the report can be used as a source for users’ own calculations and assessments.

The unique global balancing process provides a starting point from which to assess the implications for changing products trade patterns.

Coverage

The report covers the main products groups: LPG, Naphtha, Gasoline, Jet/Kero, Gasoil, Fuel Oil, and others for the key global refining regions from 2008 to 2025.

Oil demand by each product and region is forecast through 2030, based on FGE’s own methodology and models.

Additions to refining capacity are built up plant-by-plant through the forecast period; using our proprietary refining models, products balances are created for each of the regions. This creates our assessment of the “unbalanced” world, which is then further re-iterated until a global balance is achieved.

The process of transition from imbalance to balance highlights the pressures on the industry and markets, and provides the study with a unique perspective on the future international operating environment.

Structure

A review of the global oil market outlook Changes from our last Annual World Refining Outlook

An assessment of refinery capacity additions How a global product supply/demand balance is likely to be achieved

A review of the implications and possible outcomes of the IMO bunker fuel specification changes in 2020

The forecast of refining margins and products prices

Product supply by region and globally by product

Further Information

If you are interested in obtaining further information on this study, or would like to order the Annual World Refining Outlook 2017, please contact FGE’s marketing department. Discounts available to FGE clients and previous purchasers of the study.

FGE LondonTel: +44 (0) 20 7726 9570 Email: [email protected]

Leading consultancy for the oil & gas marketswww.fgenergy.com

This Study Will Add Value To:

FGE’s Annual World Refining Outlook 2017

FGE SingaporeTel: +65 6222 0045

Downstream OperatorsNeeding a perspective on the extent to which the emerging pressures on their business emanate from local or international sources.

Integrated CompaniesSeeking an outside perspective on the likely future economic operating environment of the sector.

InvestorsLooking for input in assessing their portfolio strategies.

Products TradersTrying to identify emerging underlying shifts in trade flows.

Crude Oil ProducersLooking for changing trends in crude oil demand, prices, and quality considerations.

Shipping OperatorsConducting analysis of potential tanker demand, also reviewing the overall implications of the new IMO bunker regulations.

Deliverables:

PDF copy of the report (PowerPoint layout) All associated tables available in Excel (if required).

FGE will be available for a conference call, WebEx meeting, or a general meeting to present and discuss the key findings of the report.

A PowerPoint Executive Presentation Pack, providing a visual summary of the key coverage and conclusions, accompanied by bullet point explanations.

FGE’s regular Refinery Investment Quarterly Update is also included in the study fee for one year after purchase of this report.